default prediction around the world: international ...default prediction around the world:...

TRANSCRIPT

Default Prediction Around the World: International Evidence on the Role of Corporate Transparency and Market Frictions

Mark Maffett* University of Chicago Booth School of Business

Edward Owens

Simon School of Business, University of Rochester

Anand Srinivasan National University of Singapore

October, 2012

Abstract We document significant heterogeneity across countries in the ability to assess a firm’s likelihood of default using market- and accounting-based sources of default risk information. Surprisingly, for some countries, we find that a default prediction model based solely on public financial reporting information outperforms a model based solely on market variables. Our evidence suggests that variation in the predictive ability of market-based variables across countries is primarily attributable to the existence of capital market frictions, such as short sale constraints, which prevent the incorporation of information into prices, rather than the availability of information. Finally, we document that direct incorporation of accounting information into the default prediction model largely offsets the loss in overall predictive accuracy created by market frictions, especially in countries with high corporate transparency.

_______________________________

Financial support from the University of Chicago Booth School of Business and the University of Rochester Simon School of Business is gratefully acknowledged. We are grateful for comments received from Bill Beaver, Mike Minnis, Shiva Rajgopal, and workshop participants at Emory University. * Corresponding author. Tel.: +17737029656; [email protected].

1

1. Introduction

Over the last fifteen years, numerous episodes of global financial turmoil have created

periods of extreme economic contraction and waves of financial distress. In the wake of these

episodes, the incidence of corporate default around the world has been on the rise. The ability of

market participants, from institutions to individual investors, to assess a company’s likelihood of

default is of first order importance in an economy. Yet, while the factors that affect default

prediction have been studied extensively in U.S. capital markets (e.g., Altman 1968; Beaver

1966; Ohlson 1980; Shumway 2001; Chava and Jarrow 2004; Beaver et al. 2005), little is known

about how market and accounting-based predictors of financial distress perform across countries

and in particular how differences in countries’ information environments affect market

participants’ abilities to assess a company’s likelihood of default. In this paper, we investigate

these issues directly using a broad sample of global defaults to examine cross-country

differences in the predictive accuracy of a commonly used class of default prediction models.

Conceptually, there are compelling reasons to believe that the ability of market

participants to accurately assess default likelihood may vary across countries. For example, prior

U.S.-based research has found that the quality of the accounting inputs is critically important in

determining default model predictive accuracy (e.g. Beaver et al. 2005; Beaver et al. 2012). An

extensive literature has shown that, internationally, the availability of high quality accounting

information varies dramatically (e.g., Leuz et al. 2003; Lang et al. 2012). Further, other country-

level factors, such as the intensity of the information acquisition activities of intermediaries, may

affect the availability of non-accounting-based information (Bushman et al. 2004). A lack of

useful information clearly hampers the ability of market participants’ to predict default.

2

However, in equilibrium, the overall supply of information in a particular economy arises

endogenously in response to market participants’ demand for such information. Given the central

importance of default prediction, even in settings where the supply of information available

through some channels is lacking, it is possible that market demands encourage the acquisition of

information through alternative channels to offset these deficiencies. For example, a lack of high

quality public financial reporting information can be offset through greater private information

acquisition by intermediaries such as institutional investors (Maffett 2012). If such information is

efficiently incorporated into equity prices, similar amounts of default prediction-relevant

information may be available even in settings where some information channels are relatively

weak. Ex ante, it is not obvious how these disparate information channels interact to determine

the equilibrium level of information in a particular economy and how this interplay affects the

ability of market participants to assess default using accounting- and market-based sources of

default risk information.

We begin by examining how market- and accounting-based predictors of default

commonly employed in a U.S.-context perform internationally. To address this question, we

employ a dynamic multiperiod logit default prediction model that includes both market (relative

size, prior return and return volatility) and accounting (return-on-assets, leverage and cash flow-

to-total liabilities) inputs following the procedure suggested in Shumway (2001). While there is

no explicit theory identifying the optimal combination or weighting of market-based and

financial statement-based predictors of financial distress, it has become common practice to

employ a model that combines both classes of predictors (hereafter referred to as a "combined"

model) and allows the relative weightings to be determined empirically (e.g., Shumway 2001;

Chava and Jarrow 2004; Campbell et al. 2008).

3

In our first analysis, we estimate default prediction models both for our pooled global

sample and separately for each of the countries in our sample. Although we find that our set of

market and accounting-based predictors generally behave as expected (in terms of sign and

significance) for the vast majority of our sample, we document significant differences across

countries in model predictive accuracy.1 Specifically, although combined and accounting-only

models demonstrate significant variation, we find that the predictive accuracy of market-only

models differs most across countries. Surprisingly, our results show that for half of the countries

in our sample, a model that uses only accounting information outperforms a model that uses only

market-based variables. This result stands in stark contrast to prior research which has

overwhelmingly found that market-based default predictors are superior to accounting predictors,

as one would expect in an efficient capital market where accounting information is merely a

subset of the total information set reflected in stock price.

In our next set of analyses, we examine the drivers of the observed variation in model

predictive accuracy. Conceptually, two fundamental economic forces could be responsible for

the observed heterogeneity in default prediction: the availability of information about firms’

financial condition (i.e., corporate transparency) and market frictions that restrict the

incorporation of information about firms’ financial condition into prices.2 Bushman et al. (2004)

develop a framework that defines corporate transparency as a function of the numerous facets

within a country that collectively produce, gather, validate and disseminate firm-specific

1 Following prior research, we define predictive accuracy as the cumulative percentage of default observations that fall in the top three estimated default probability deciles, where deciles are constructed based on the estimated default probabilities of both default and non-default sample observations (e.g., Beaver et al. 2012). In robustness analyses we consider an alternate measure based on receiver operating characteristic curves. 2 Although there are also likely differences across countries in the formal legal institutions that surround the resolution of the default process (e.g., bankruptcy laws), in this study we focus on the occurrence of default, rather than on legal bankruptcy filing. We assume that the conditions that signal financial distress and entrance into a default state (i.e., the inability to pay outstanding debt claimants when due) are more general and likely to be determined by similar economic forces across countries. Nonetheless, we also explore a variety of means for controlling differences across countries in the legal origins and resolution mechanisms of the bankruptcy code.

4

information. An extensive prior literature documents how corporate transparency, determined at

both the country- and firm-level, can affect the extent to which a country’s capital markets reflect

information about firm fundamentals (e.g., La Porta et al. 1997; Leuz and Verrecchia 2000; Leuz

et al. 2003; Daske et al. 2008; Lang et al. 2012). Prior default research in a U.S. context supports

this notion by demonstrating that the quality of a firm’s financial reporting information is an

important determinant of the ability to assess a firm’s likelihood of default using market- and

accounting based predictors of financial distress (Beaver et al. 2012).

However, even if relevant and reliable data about firm fundamentals are available, this

information may not be fully reflected in prices if significant capital market frictions exist. An

extensive prior literature demonstrates how frictions can limit the informativeness of equity

prices (e.g., Miller 1977; Diamond and Verrecchia 1987). While numerous sources of capital

market friction exist, we focus on country-level constraints on short selling. Saffi and Sigurdsson

(2011) find that, internationally, stocks with greater short-sale constraints have less informative

prices. Moreover, short-sale constraints explicitly limit the ability of market participants to

incorporate negative information into stock prices, which is likely to be particularly relevant for

default prediction.3

We begin our investigation of the relative importance of these two potential sources of

variation by focusing on cross-country differences in the predictive accuracy of the market-only

model. This initial focus allows for a parsimonious investigation of the relative importance of

both information availability and market frictions, as the informativeness of market-based

sources of default risk information can, in principle, be affected by both forces. Empirically, we

measure country-level information availability following the institutional cluster categorizations

3 While good news may also be useful in predicting defaults, for firms on the verge of financial distress, bad news is likely to be more relevant for assessing the likelihood of an eventual default (Beaver et al. 2012).

5

in Leuz (2010), and constraints on short selling following the details in Bris et al. (2007). In a

country-level multivariate analysis, controlling for differences in the legal origin and resolution

mechanisms of the bankruptcy law, we find evidence that cross-country variation in the ability of

market variables to predict default is primarily attributable to market frictions, rather than the

availability of relevant information. This finding provides some insight into the seemingly

anomalous superior performance of accounting- over market-based sources of default risk

information we observe in some countries. In contrast to the market-only model, we find that

both market frictions and corporate transparency explain a significant portion of the variation in

the predictive accuracy of the combined model. Intuitively, this result is reassuring because the

combined prediction model directly includes financial reporting information, the informativeness

of which should be affected by the strength of the institutional infrastructure.

Given that we have relatively few country-level observations in our regression analysis,

we next seek to corroborate our initial findings through a series of non-parametric tests. In these

analyses, we estimate each prediction model separately across partitions based on country-level

short sale constraints and again across partitions based on country-level corporate transparency.

Overall, the results of these tests further support the conclusion that market frictions are the

primary driver of variation in the performance of the market-only model. These results also shed

some light on the economic importance of our main findings. Specifically, our non-parametric

analyses suggest that market-only model predictive accuracy is twenty-five percentage points

lower in countries with short-sales constraints than in those without short-sales constraints, and

ten percentage points lower in countries with low corporate transparency relative to those with

high corporate transparency.

6

Our non-parametric analysis also reveals that an accounting-only model exhibits little

variation across partitions based on market frictions. The fact that the accounting-only model

performs equally well in the presence of market frictions, leading to a larger relative contribution

of accounting information to combined model predictive accuracy, suggests that the direct

inclusion of accounting information into a combined default prediction model may help to

overcome the loss in predictive ability created by market frictions. To corroborate this inference,

we examine model performance across corporate transparency partitions within the market

friction subsample (i.e., those countries with short sale constraints). If accounting information

indeed helps to offset the loss in market-only model predictive accuracy created by market

frictions, we would expect to see that this ability of financial statement variables to overcome

market frictions is enhanced in settings with high corporate transparency. Consistent with this

prediction, in the presence of short sale constraints we find that the incremental predictive

accuracy gained from the addition of accounting variables to the model is larger when corporate

transparency is relatively high.

Our paper makes several contributions to the existing literature. Foremost, ours is the first

paper (of which we are aware) to document significant heterogeneity in the predictive accuracy

of default models across countries. Prior research on default prediction across countries is

virtually non-existent. We document that, while market- and accounting based sources of default

risk information behave as predicted in the vast majority of countries in our sample, there is

significant heterogeneity in the predictive accuracy of these commonly used default models

across countries, particularly with respect to the market-based predictors. Further, we identify

market frictions, such as short sale constraints, as the primary driver of these differences.

7

Second, we find that the direct inclusion of accounting information improves default

model predictive accuracy in the presence of market frictions, particularly where a strong

institutional infrastructure supports greater corporate transparency. Prior default prediction

literature does not clearly articulate why, other than model misspecification, public financial

reporting information should have any effect on default prediction incremental to market

information. We shed light on this issue by identifying market frictions as an explanation for the

incremental explanatory power of accounting-based sources of default risk information relative

to market-based sources. Moreover, our findings highlight that an important capital market

benefit of greater corporate transparency is improved default prediction ability in the presence of

significant market frictions.

Finally, our results shed light on the implications of short sale constraints. Consistent

with the theoretical arguments of Miller (1977) and Diamond and Verrecchia (1987), an

extensive empirical literature demonstrates that short sale constraints can inhibit the

incorporation negative information into prices. Our findings highlight a significant decrease in

default prediction accuracy as a novel consequence of the loss in informativeness created by

short sale constraints.

The remainder of the paper proceeds as follows: in Section 2, we discuss the related prior

literature and motivation for our study; in Section 3 we describe our research design; in Section 4

we provide a description of our data source and sample selection criteria; in Sections 5 and 6 we

present our empirical results; in Section 7 we conclude.

2. Background and motivation

Although there is an extensive literature examining default prediction in a U.S. context,

there is virtually no evidence on how the ability to assess default, or the relative importance of

8

market versus accounting-based sources of default risk information, varies across countries. Yet,

internationally, there are dramatic differences in the development and efficiency of capital

markets, the extent of corporate transparency and the legal procedures surrounding default, all of

which likely affect both the overall predictive accuracy of default models and the relative

importance of market- versus accounting-based predictive inputs. The goal of our paper is to

understand whether and how this institutional heterogeneity affects default prediction.

The vast majority of prior literature on default prediction has focused on model predictive

accuracy. Shumway (2001) demonstrates that a default prediction model that explicitly accounts

for time-varying covariates and allows a firm’s changing financial data to reveal its changing

health is superior to the single period static approach employed in prior research (e.g., Altman

1968; Ohlson 1980; Zmijewski 1984). Examining an extensive list of potential explanatory

variables, Shumway (2001) finds that a default model that includes a combination of market-

based variables (size, prior returns, and return volatility) and accounting ratios (return-on-assets

and leverage) has the best out of sample classification ability. Following Shumway (2001), it has

become common practice to assess a company’s likelihood of default using a multi-period logit

model including a combination of both market- and accounting based default risk measures. For

example, Campbell et al. (2008) follows the Shumway (2001) approach and estimates a dynamic

logit model using market and accounting information to examine the determinants of corporate

failure and the pricing of financially distressed stocks.

Prior U.S. based literature has also given some consideration to the relative importance of

accounting- and market-based sources of default risk information. This literature has generally

confirmed the presumption that, because stock prices draw information from a variety of sources

of which accounting is a subset, market-based predictors of default should outperform

9

accounting-based predictors. For example, Shumway (2001) shows that, using a hazard model

approach, approximately fifty percent of accounting ratios used in prior research are not

statistically related to bankruptcy. He also notes that a model that uses only market variables also

performs quite well, implicitly suggesting that accounting variables add relatively little

predictive ability over and above market-based variables. Chava and Jarrow (2004) use an

expanded bankruptcy sample within the U.S. to validate the superiority of hazard models over

static models and similarly show that accounting variables add little predictive power over and

above market-based variables in out-of-sample tests. 4 Further, Beaver et al. (2012) document

that the predictive ability of financial statement ratios has declined over time.

An important caveat is that the vast majority of the prior literature on default prediction

has been conducted on firms domiciled in the United States. Inferences from these studies may

have limited generalizability to an international setting given that the U.S. is, arguably, the

world’s most developed and efficient capital market. For example, relative to other countries,

U.S. capital markets have an extensive network of information intermediaries (e.g., analysts,

institutions and the news media), relatively few market frictions (e.g., high liquidity, broad

options markets, few short sale constraints) and high quality corporate financial reporting. It is

not necessarily clear from this line of prior research how accurately market participants would be

able to assess default in the absence of some (or all) of these attributes prevalent in U.S. capital

markets. For example, Beaver et al. (2012), allude to the importance of the underlying

4 Despite the relative dominance of market-based default prediction models over accounting-based models documented in prior literature, it is important to note that these findings do not imply that accounting variables are unimportant in default prediction. Specifically, as pointed out in Beaver et al. (2012), in an efficient market, market-based variables (i.e., prices) likely already incorporate accounting information, such that part of the predictive ability of market-based variables comes from their incorporation of accounting information.

10

information environment to accurate default prediction by demonstrating that the quality of a

firm’s financial reporting has a significant effect on default model predictive accuracy.

Given that deficiencies in one information channel increase the incentives of market

participants to acquire information from other sources, the development of a country’s

information environment is likely to affect not only the overall ability to assess firms’ default

likelihood, but also the relative importance of market- versus accounting-based sources of

default risk information. Given its U.S. focus, prior research has been unable to address these

issues, which are the focus of our study.

3. Research Design

3.1. Primary empirical specification

We follow current literature and estimate a dynamic default prediction model using a

hazard model framework. To implement this approach, Shumway (2001) recommends using a

multiperiod logit model, where each year a firm survives is included as a non-failure observation,

and default observations are included as a failure observation only in the year of failure. We

follow the multiperiod logit approach using six candidate explanatory variables (three accounting

variables plus three market variables) that are used in both Beaver et al. (2005) and Beaver et al.

(2012).5 Specifically, we estimate the following logistic regression with standard errors clustered

at the firm level to account for lack of independence between firm-year observations:

,

1Pr( 1) ,

1i t zDEFAULT

e

(1)

0 1 , 2 , 3 , 4 , 5 , 6 , .i t i t i t i t i t i tz LRET LSIGMA LRSIZE ROA LTA ETL

5 Our objective is not to identify the “best” empirical default prediction model, but rather to explore cross-sectional variation in the performance of default prediction models in general across countries. To this end, we employ what we believe is a widely accepted empirical default prediction model in the academic literature.

11

DEFAULT is an indicator variable that equals one if the firm-year predictive variables are

measured in the most recently available year immediately preceding a firm's default, and equals

zero otherwise. Note that under this dynamic methodology DEFAULT = 0 includes all firm-year

data for firms that never default, as well as all firm-year data for defaulted firms in years prior to

the year immediately preceding their default. We delete all firm-years of data for defaulted firms

after their default year.

ROA, LTA, and ETL are the accounting-based predictive variables, where ROA is a

measure of profitability (return-on-assets), LTA is a measure of leverage (total liabilities divided

by total assets), and ETL is a cash flow-to-total liabilities ratio (e.g., Beaver, 1966). LRET,

LSIGMA, and LRSIZE are the market-based predictive variables, where LRET is lagged

cumulative stock return, LSIGMA is lagged return volatility, and LRSIZE is the logarithm of a

firm's market capitalization relative to the aggregate sample market capitalization. We use

market data as of the end of the month following the month of financial statement data

availability. For example, if financial statement data are available 04/17/2004, we use market

data as of 05/31/2004. This allows the market time to incorporate the financial statement data, so

that the accounting data do not have an unfair advantage in the default prediction models. We

estimate three versions of Eq. (1) - a specification that omits ROA, LTA, and ETL (i.e., the

market-only model), a specification that omits LRET, LSIGMA, and LRSIZE (i.e., the accounting-

only model), and the full Eq. (1) specification (i.e., the combined model). All variables are

further defined in the Appendix.

3.2. Assessing predictive ability

In order to compare the market-only, accounting-only, and combined models with each

other as well as across countries, we must select an approach for assessing predictive ability.

12

Several methods are offered in extant literature. We adopt the approach followed in Beaver et. al

(2005) and Beaver et al. (2012) and measure a model's predictive ability as the fraction of sample

defaults with a predicted probability of default falling in the top three predicted probability of

default deciles for all sample firm-years.6 That is, after using a given model to estimate predicted

default probabilities for all sample firm-years, we rank the predicted default probabilities into

deciles and note the decile into which each sample observation falls. We then construct the

variable ACCURm (i.e, predictive accuracy of model m) as the cumulative percentage of sample

default observations that fall in the top three deciles when default probabilities are estimated

using model m. In particular, we refer to the predictive accuracy of a market-only model,

accounting-only model, and combined model as ACCURMO, ACCURAO, and ACCURC,

respectively. We examine differences both in ACCURm across sample partitions and in ACCUR

across different models within the same partition, and the statistical significance of these

differences using a Monte Carlo randomization methodology. In robustness tests we consider an

alternative measure of predictive accuracy based on receiver operating characteristic curves,

which we discuss in Section 6.

4. Data and sample selection

4.1. NUS Credit Research Initiative

The principle data source we use in this study is from the National University of

Singapore Risk Management Institute (RMI). In July 2009, RMI launched the Credit Research

Initiative (CRI) to promote research in the credit risk arena.7 The foundation of the CRI is a

database of over 53,000 listed firms in 46 countries across the Asian-Pacific, North American,

Western European and Latin American regions. The principle output of the CRI is daily firm-

6 Although we discuss in the text results only for the first three deciles, we present results for all ten deciles. 7 For more information on this initiative, refer to http://rmicri.org/home/.

13

level default probabilities. The proprietary database that underlies this output, compiled by a

RMI team of nearly thirty people, includes extensive panel data on firm stock price, financial

statement data, and events of defaults from 1990 to the present, categorized by default class. It is

this underlying proprietary database from which we draw our sample data.

The CRI research team collects default events from numerous sources, including

Bloomberg, Compustat, CRSP, Moody's, exchange web sites and media outlets. Because

definitions of credit default can vary across national jurisdictions and between data sources, CRI

continuously attempts to normalize to a common set of default definitions. In the version of the

dataset we use, default events recognized by CRI include "1) bankruptcy filing, receivership,

administration, liquidation, or any other legal impasse to the timely settlement of interest and/or

principal payments; 2) a missed or delayed payment of interest and/or principal, excluding

delayed payments made within a grace period; 3) debt restructuring/distressed exchange."

Delistings or "other exits" are not considered as defaults initially, but are reclassified as defaults

if a firm experiences a default within one year of the delisting. Technical defaults (i.e., covenant

violations) are not included in the definition of default. In addition to these general categories,

CRI separately examines cases that require special attention to determine whether a default event

has actually occurred.

4.2. Sample selection and descriptive statistics

We begin with all default observations in the CRI database, which gives us an initial

default sample of 12,771 default observations. However, the CRI default dataset provides a

separate observation for each instrument that is defaulted upon by a given occurrence of firm

default (e.g., if a firm has two loans outstanding at the time of bankruptcy filing, the bankruptcy

filing would generate two observations in the default dataset). Accordingly, we delete all such

14

"duplicate" observations, leaving 8,258 distinct firm-default observations. Because of the

structure of our empirical tests, in the case where a given firm has multiple defaults in the

database we retain only the first default occurrence for a given firm, which reduces our default

sample to 5,562 firm-level observations. We next delete banks and utilities, leaving 5,416

defaults.

Our analyses require both accounting data and market data. Our primary source for

accounting data is the CRI 'financial statements' dataset. Specifically, we require measures of

return on assets (ROA), cash flow to total liabilities (ETL), and leverage (LTA). The CRI

financial statement dataset initially contains 572,589 firm-year observations after deletion of

banks and utilities, with 84,082, 72,489, and 31,430 missing observations for ROA, ETL, and

LTA, respectively. We attempt to supplement the missing CRI financial statement data with

Worldscope data, where we merge the CRI data with Worldscope based on ISIN. After merging

in Worldscope-based ROA, ETL and LTA, there remain 83,482, 71,640, and 30,691 missing

observations, respectively. 8 After merging the financial statement data into the default sample,

the 5,416 defaults yield 31,703 firm-year observations (i.e., 5,416 default-year observations and

26,287 non-default-year observations). The remaining 533,422 firm-year observations in the

financial statements data set provide the pool of additional non-default-year observations (i.e., all

firm-year observations for firms that never defaulted), yielding a total sample of 565,125 firm-

year observations.

As discussed in section 3, we utilize three market-based measures in our prediction

models. For return (LRET) and return volatility (LSIGMA), our primary data source is the CRI

'pd' dataset, which contains data on closing monthly stock price. When missing (207,428 and

8 The fact that supplementation with data from Worldscope/Datastream adds very few additional observations to the sample suggests that the CRI data are fairly comprehensive.

15

208,975 missing observations out of our 565,125 observation sample for LRET and LSIGMA,

respectively), we supplement the data using Datastream. After merging in Datastream-based

LRET and LSIGMA, there remain 201,018 and 202,355 missing observations, respectively. For

the third market variable, LRSIZE, our primary data source is Datastream, because the use of

Datastream allows us to directly obtain market capitalization in a common currency (i.e., U.S.

dollars) across all sample observations, which obviates the need to engage in currency

conversion on the CRI price data.

We next delete all observations with missing values for any of our three financial

statement variables (ROA, ETL and LTA) or any of our three market variables (LRET, LSIGMA,

and LRSIZE), which leaves a sample of 323,858 firm-year observations. We likewise delete

observations where LSIGMA equals zero (i.e., firms with no price change over the prior twelve

months), as well as all observations from countries with no defaults in the dataset. These

deletions result in a final analysis sample of 321,947 firm-year observations comprised of 2,871

default-year observations and 319,076 non-default-year observations from fiscal years 1989

through 2012. The defaults that underlie the default-year observations span the years 1991

through 2012. Finally, we Winsorize the financial statement variables at the upper and lower

2.5%, and Winsorize LRET and LSIGMA at the upper 2.5% only, because these variables have

natural lower bounds.

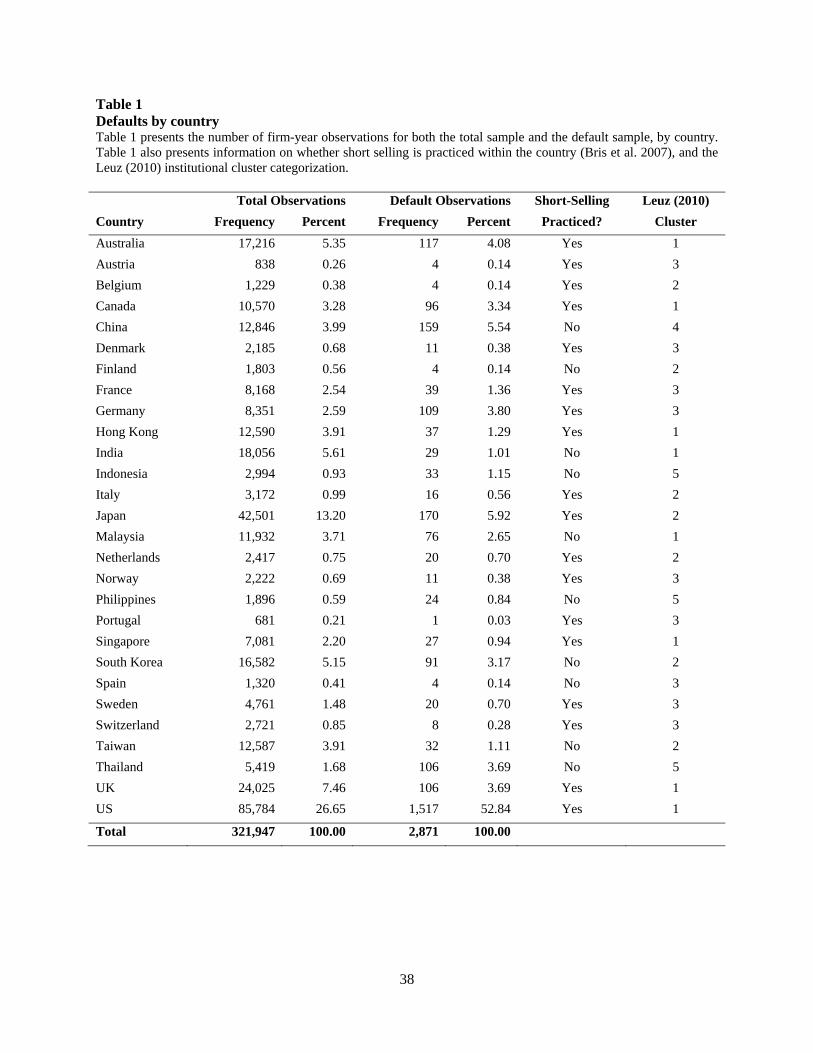

Table 1 presents the total number of sample observations and number of sample default

observations by country. Clearly, the United States is dominant in the overall CRI database, both

in total number of observations (26.65%) and in default observations (52.84%).9 With a few

exceptions, the United States is joined in the high informativeness group primarily by Eurozone

9 In untabulated robustness tests, we find that our key inferences are robust to exclusion of the United States from the analysis.

16

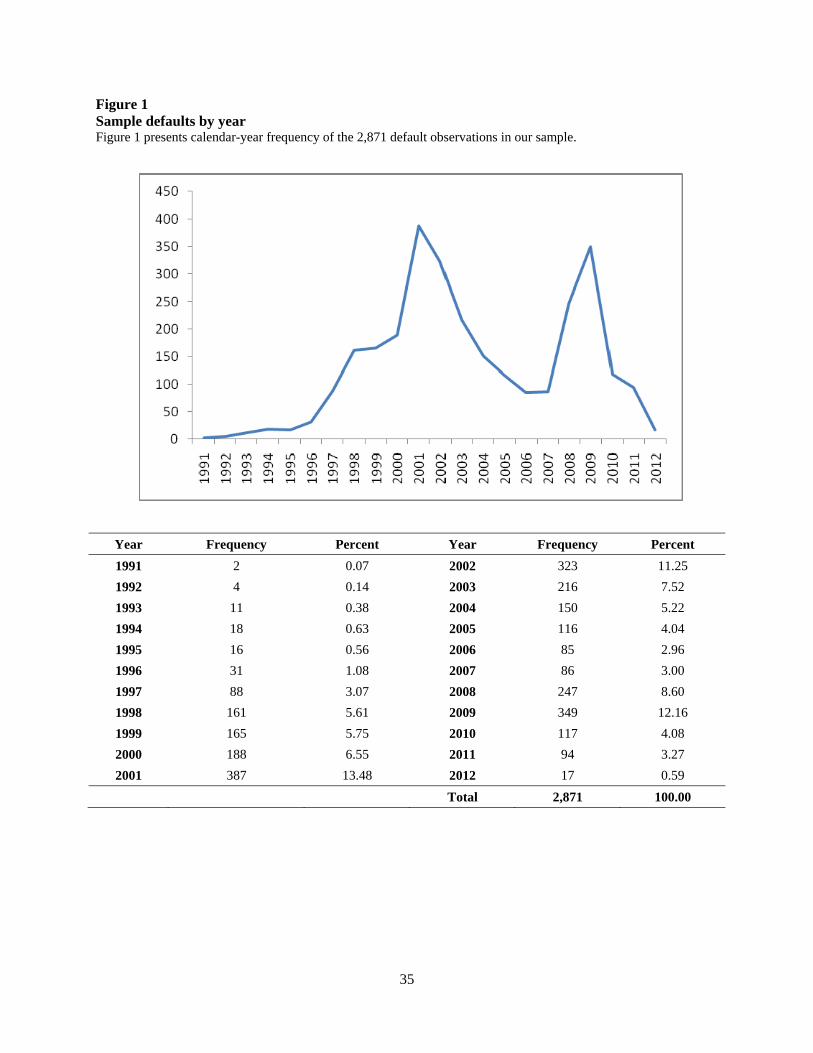

countries. Asia-Pacific nations are also well represented in the sample. Figure 1 presents our

sample default frequency by year. As expected, our sample exhibits a pronounced spike in

default frequency in the years surrounding 2000 and 2008, which roughly coincide with the

aftermath of the Asian financial crisis, the 2001 recession and the 2008 financial crisis.

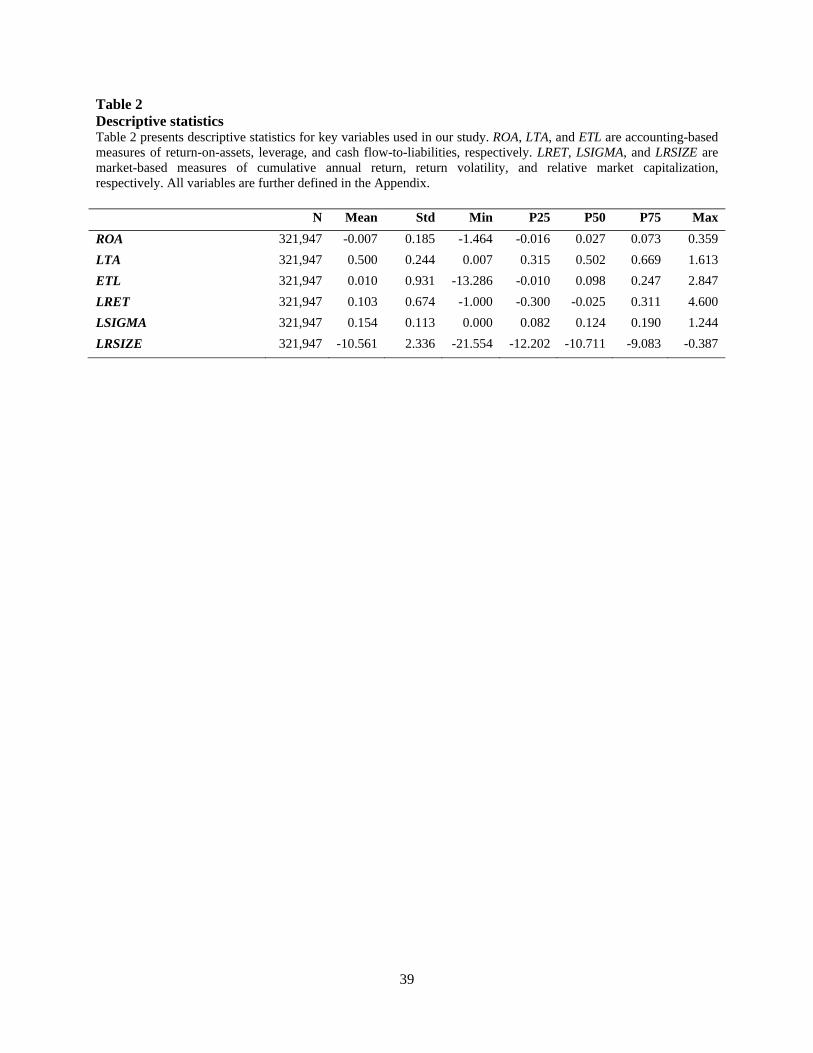

Table 2 presents aggregate sample descriptive statistics for the variables we use in our

default prediction models. Although we use a distinctly different sample and time period, the

overall distributional characteristics of our accounting and market-based predictor variables

appears to be generally similar to those reported in prior studies (e.g., Beaver et al. 2012).

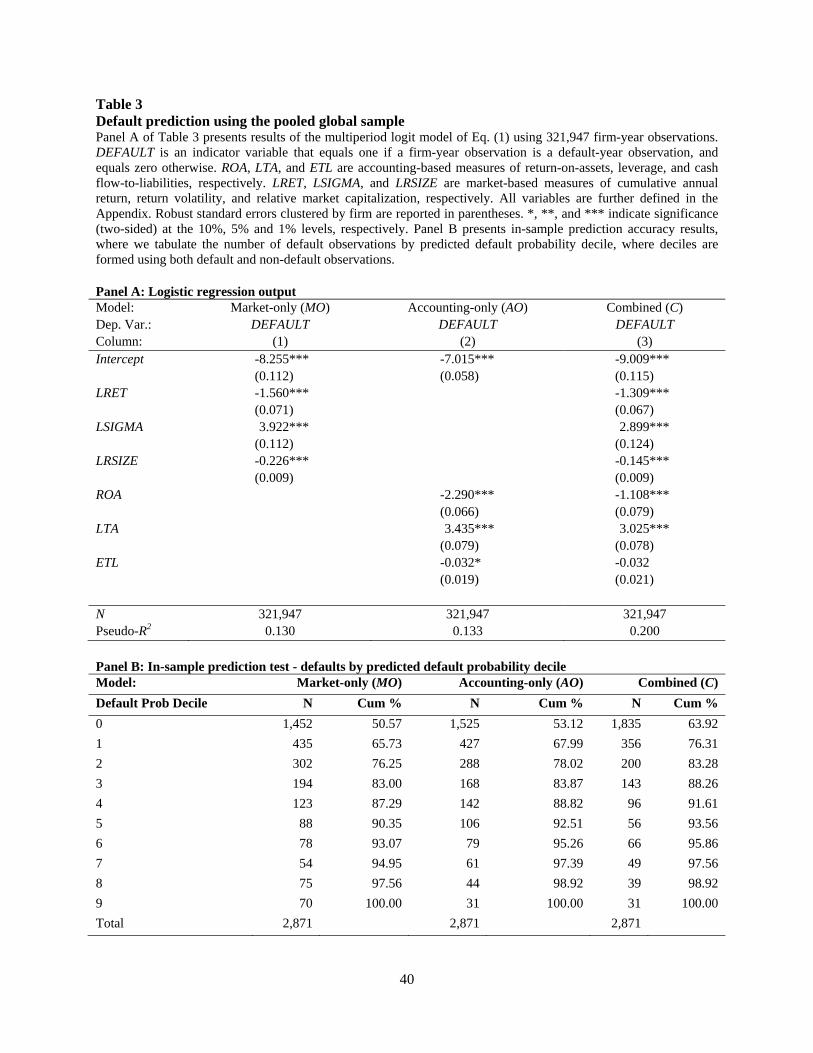

5. International default model estimation

We begin our analysis by estimating default prediction models (i.e., Eq. 1) using our

global pooled sample, with results presented in Table 3. Basic relations revealed by the pooled

estimation reported in Panel A are generally consistent with prior literature that has estimated

similar models using U.S.-only data (e.g., Beaver et. al 2005; Beaver et. al 2012). Specifically,

firms that have higher lagged stock returns (LRET), a larger relative size (LRSIZE), a greater

return-on-assets (ROA) and a higher cash flow to liabilities ratio (ETL) (marginal significance)

are less likely to default, whereas firms with higher return volatility (LSIGMA) and greater

leverage (LTA) are more likely to default. The relatively weak statistical significance of ETL is

consistent with similar findings in Shumway (2001) and Beaver et al. (2005).

Panel B of Table 3 presents the number of default observations falling in each decile of

predicted default probability, where each decile is computed from the combined default and non-

default firm-year observations, and is ranked in descending order (i.e., decile 0 has the highest

predicted default probability). For example, in the combined model, 63.92% of the default-year

observations fall in the highest predicted default probability decile, whereas only 1.08% (i.e.,

17

100%-98.92%) of default firms appear in the lowest predicted default probability decile. As

described earlier, our key focus in terms of model predictive accuracy (ACCUR) is the

cumulative percentage of default firms in the highest three deciles (e.g., Beaver et al. 2005).

Looking at this statistic in Panel B reveals that the combined model predictive accuracy

(ACCURC) is 83.28%, which is similar in magnitude to the comparable statistic in Beaver et al.

(2005). The market-only model predictive accuracy (ACCURMO) is 76.25%, and the accounting-

only model predictive accuracy (ACCURAO) is 78.02%. The observation that ACCURMOis

slightly lower than ACCURAO is noteworthy, as prior studies conducted using U.S.-only data

have exclusively found that the market-only model outperforms the accounting-only model. This

initial finding provides an indication that default prediction models may perform differently in an

international setting.

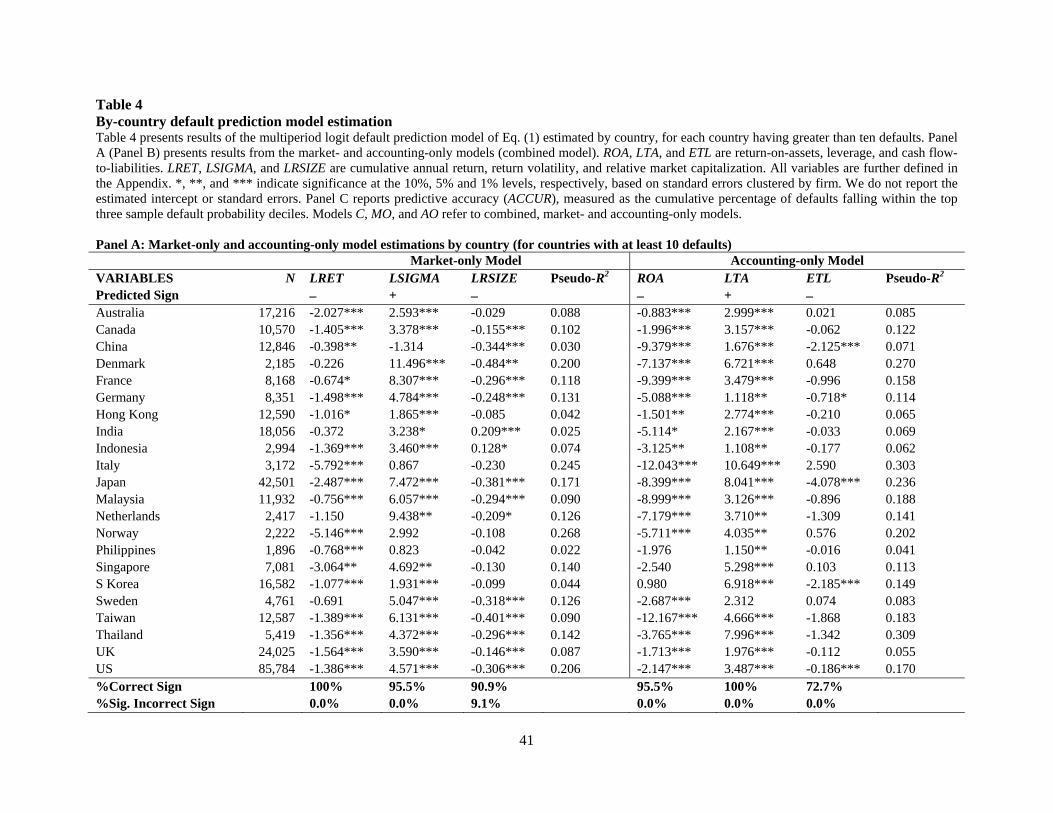

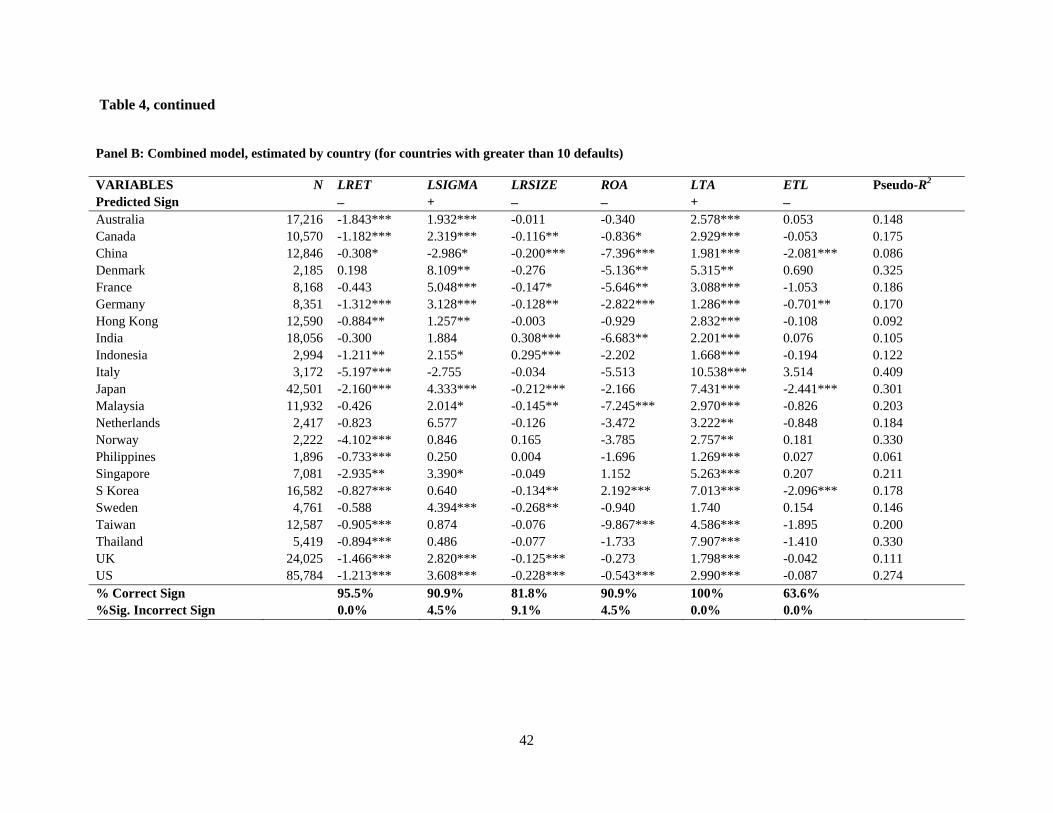

Table 4 presents results from estimation of the three forms of Eq. (1) (i.e., MO, AO, and

C) by country, for each sample country with greater than ten default observations. Panel A

presents regression statistics by country for the market-only and accounting-only models, and

Panel B presents regression statistics for the combined model. Generally speaking, the relations

between the six predictor variables and default incidence are consistent in sign and significance

across the country-level estimations. For example, in the market-only model, two of the three

predictive variables never enter a country-level regression with a statistically significant sign that

is opposite to the predicted sign. The exception is LRSIZE, which has a statistically significant

negative coefficient in 9.1% of the sample countries. In the accounting-only model, not one of

the three predictive variables enters a country-level regression with a statistically significant sign

that is opposite to the predicted sign.

18

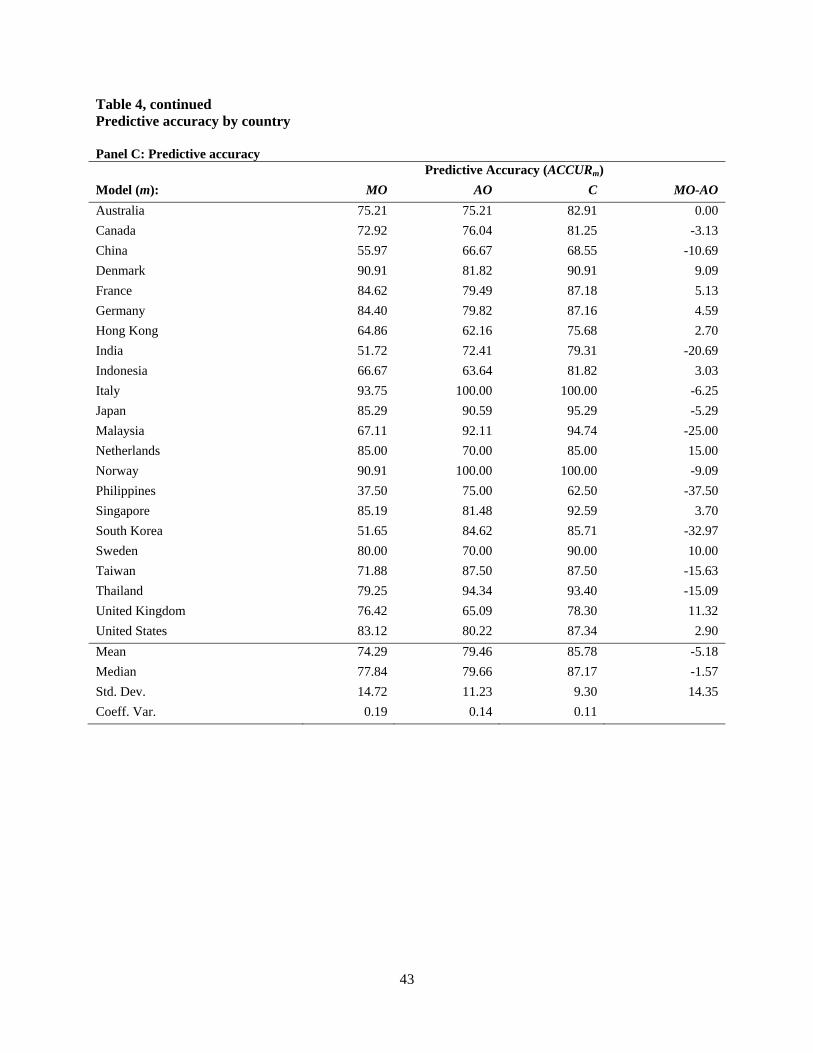

In Panel C of Table 4 we tabulate the predictive accuracy statistics from the estimations

of the default prediction models by country. In general, the mean accuracy statistics across

countries is generally consistent with results from our pooled estimation from Table 3. For

example, the mean predictive accuracy of the combined model across countries is in the mid

80% range (85.8%). Further, once again we find that, on average the accounting-only model

outperforms the market-only model (i.e., mean ACCURMOACCURAO of 5.18). We note wide

variation in the predictive accuracy of the market-only model across countries, ranging from

37.50% in the Philippines to 93.75% in Italy. Interestingly, the variation in combined model

accuracy is less pronounced, ranging from 62.50% in the Philippines to 100% in Norway and

Italy.10 This differential variation also is evident in looking at the respective coefficients of

variation, 0.19 and 0.11, respectively. Another noteworthy observation is that in eleven of the

twenty-two countries examined in Table 4, ACCURMOACCURAO is negative, i.e., accounting

variables outperform market variables in their ability to predict default. In the next section, we

examine potential drivers of the wide variation both in the market-only model predictive

accuracy and in the relative importance of accounting- versus market-based predictors.

6. Determinants of variation in model predictive accuracy

As shown in Panel C of Table 4, there is substantial variation in the predictive accuracy

of the market-only model across countries. Conceptually, two fundamental economic forces

could be responsible for this variation: corporate transparency and market frictions. We next

discuss these two forces and the empirical proxies we use to capture them in forthcoming

analyses. Then, we outline the empirical analyses we employ to examine the relative importance

10 We note that countries at the upper end of these ranges (i.e., Italy, Norway) have relatively few sample defaults, which could explain their high predictive accuracy. We conduct several procedures to ensure that our inferences are not attributable to the number of defaults in a particular country, which we discuss in subsequent sections along with the associated results.

19

of these forces in explaining variation in default model predictive accuracy around the world,

and present associated results.

6.1. Corporate transparency and market frictions

The first force that may explain variation in predictive accuracy of market-based

variables is the existence of differences across countries in the availability of information about

firms' economic condition, i.e., corporate transparency. In reality, corporate transparency reflects

the collective output of numerous components of a system that produces, gathers, and

disseminates information to market participants that are external to a firm (Bushman et al. 2004).

Although it is naturally challenging to come up with a single empirical proxy that captures all

such transparency dimensions, in our forthcoming analyses we rely on the institutional cluster

categorizations in Leuz (2010). Leuz (2010) (p. 246) categorizes countries into five institutional

clusters based on a broad set of institutional features that are fundamentally related to a country's

information environment (e.g., securities regulation, investor protection, enforcement

mechanisms), and shows that these clusters are correlated with the transparency of financial

reporting practices. We note that, although much of the discussion of Leuz (2010) is focused on

corporate reporting regulation, he points out that reporting regulation is a part of a country's

broader institutional framework, and is designed to fit with and reinforce other elements of the

institutional infrastructure. Accordingly, we believe that these clusters serve as a valid proxy not

only for financial reporting transparency, but also for a more general notion of country-level

corporate transparency.

The second potential explanatory force is the existence of differences across countries in

the extent of market frictions which prevent default risk information from being impounded into

market variables. The observation in Panel C of Table 4 that the accounting-only model often

20

outperforms the market-only model suggests that a lack of information about firm economics is

not the sole explanation for the observed heterogeneity in predictive accuracy, indicating that

market frictions may play an important role. We focus on short-sale constraints as our primary

measure of market frictions. Given that short-sale constraints are likely to specifically impede the

incorporation of bad news into prices, they represent a market friction that is particularly likely

to decrease the informativeness of prices with respect to assessing default risk. Using a sample of

firms from 26 countries, Saffi and Sigurdsson (2011) show that stocks with greater short-sale

constraints have less informative prices. Moreover, because short-sale constraints function as a

friction on the incorporation of information into prices, rather than serving as a proxy for the

availability of information in a particular setting, they are unlikely to directly affect firm

fundamental value or the extent to which financial reporting information reflects this underlying

value. We utilize the details in Bris et al. (2007) to categorize each of our sample countries as

allowing or prohibiting short selling.

6.2. Multivariate tests

As an initial test of the relative importance of corporate transparency and market frictions

in explaining variation in default model predictive accuracy, we estimate a country-level

multivariate analysis of the following form using OLS with twenty-two country-level

observations (i.e., the twenty-two countries for which we estimate country-level default

prediction models):

, 0 1 2

1

K

MO c c c k c ck

ACCUR TRANSP SHORT Control

(2)

where ACCUR is as previously defined. We also estimate Eq. (2) with ACCURC as the dependent

variable.

21

SHORTc is an indicator variable that equals one if there are short sale constraints in

country c and equals zero otherwise, following details in Bris et al. (2007). Again, SHORT serves

as our proxy for the existence of market frictions that may prevent market variables from fully

incorporating default risk information. TRANSPc is an indicator that equals one (zero) if country

c is has relatively strong corporate transparency (Leuz [2010] clusters 1 and 2), and equals zero

if country c has relatively weak corporate transparency (Leuz [2010] clusters 3, 4 or 5).11

In this study, we focus on occurrence of default, rather than specifically on legal

bankruptcy filing. We believe that, although there are differences across countries in the

institutions that surround the resolution of the default process, the conditions that signal the

entrance to the default state, i.e., inability to pay debts when due, are more general and are likely

to be determined by similar factors across countries.12 Nonetheless, Eq. (2) also includes a vector

of country-level institutional control variables related to the insolvency regime and legal origin

to ensure that our results are not affected by these institutional differences. Extant literature

provides evidence that bankruptcy use is affected by creditor rights, which are in turn largely

influenced by a country's insolvency regime (Claessens and Klapper 2005). Moreover, the law

and finance literature finds that insolvency practices are strongly correlated with legal origin

(Djankov et al. 2008). Accordingly, for one set of controls we define the following indicator

variables that equal one if foreclosure, liquidation, or reorganization, respectively, is the likely

outcome of a potential insolvency in country c and equal zero otherwise (Djankov et al. 2008):

FCLOSE, LIQUID, and REORG. The second set of controls relates to the legal origin of a

11 In the analyses that follow, inferences are not sensitive to the choice of including Leuz (2010) cluster 3 countries in the TRANSP = 0 versus TRANSP = 1 category. 12 Stated differently, whereas bankruptcy is a legal process that resolves default, the occurrence of default itself is an economic state that arises when a company cannot meet its payments when due. In other words, our dependent variable is more likely determined by firm economics than by country-level legal mechanisms.

22

country’s bankruptcy code, where we define the following indicator variables accordingly:

ENGLISH, FRENCH, GERMAN and NORDIC (Djankov et al. 2008).

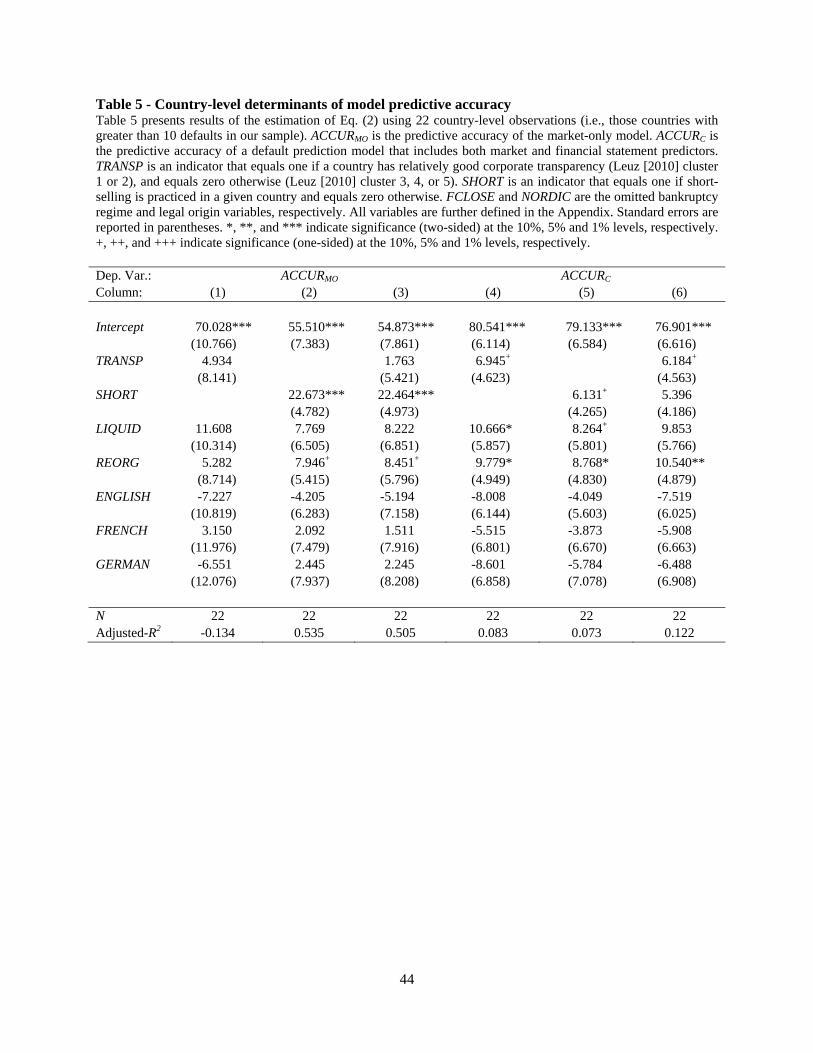

Table 5 presents results from estimation of Eq. (2), where columns (1) through (3) use the

predictive accuracy of the market-only model as the dependent variable. Although the analysis

only includes twenty-two observations, we find strong evidence that variation in market-only

model predictive accuracy is driven by market frictions. Specifically, focusing on the full

specification in column (3), the coefficient on SHORT of 22.46 (t-statistic of 4.52) provides

evidence that the market-only model is more (less) accurate in countries where short-selling is

practiced (prohibited). The coefficient on TRANSP, while positive, is statistically insignificant,

suggesting that a country's corporate transparency is not a primary determinant of variation in the

ability of market variables to predict default, i.e., market frictions are the dominant force that

drives cross-country variation in the performance of market-based default prediction models.

Columns (4) through (6) present estimation of Eq. (2) where the dependent variable is the

predictive accuracy of the combined model, i.e., the model that includes both market-based and

accounting-based predictors. Here, we find evidence that predictive accuracy of the combined

model is associated with both market frictions and corporate transparency, although statistical

significance is marginal. Focusing on column (6) for discussion, the coefficient on TRANSP of

6.18 (t-statistic of 1.36) weakly suggests that the predictive accuracy of the combined model is

positively associated with corporate transparency. The coefficient of 5.40 on SHORT (t-statistic

of 1.29), although only marginally significant, has a similar economic magnitude as TRANSP.

Taken together, these results suggest that corporate transparency is more important in the

combined model, and that both forces contribute to predictive accuracy. This result is intuitive,

23

as the combined model includes not only market-based predictors, but also includes predictive

variables that are direct outputs of the corporate reporting system, i.e., financial statement ratios.

Across all specifications, the country-level institutional control variables related to legal

origin are insignificant. The control variables related to bankruptcy resolution mechanisms enter

with some significance depending on the specification, with REORG appearing to be particularly

relevant in the combined model. The interpretation of the positive coefficient on REORG is that

the predictive accuracy of combined default prediction models is greater in countries where

reorganization is the likely resolution of bankruptcy, relative to countries where foreclosure is

the likely resolution.

6.3. Non-parametric analyses

The multivariate analysis outlined above provides an initial indication that market

frictions (as proxied by short-selling constraints) are the dominant force in explaining variation

in the predictive ability of market-based variables. However, we hesitate to draw strong

conclusions based solely on a regression analysis with so few observations. In this section we

seek to corroborate our inferences by utilizing an alternative research design, where we estimate

default prediction models separately across market friction and corporate transparency partitions

using the full sample, and test the differences in model predictive accuracy across partitions

using non-parametric techniques (i.e., Monte Carlo permutation tests).

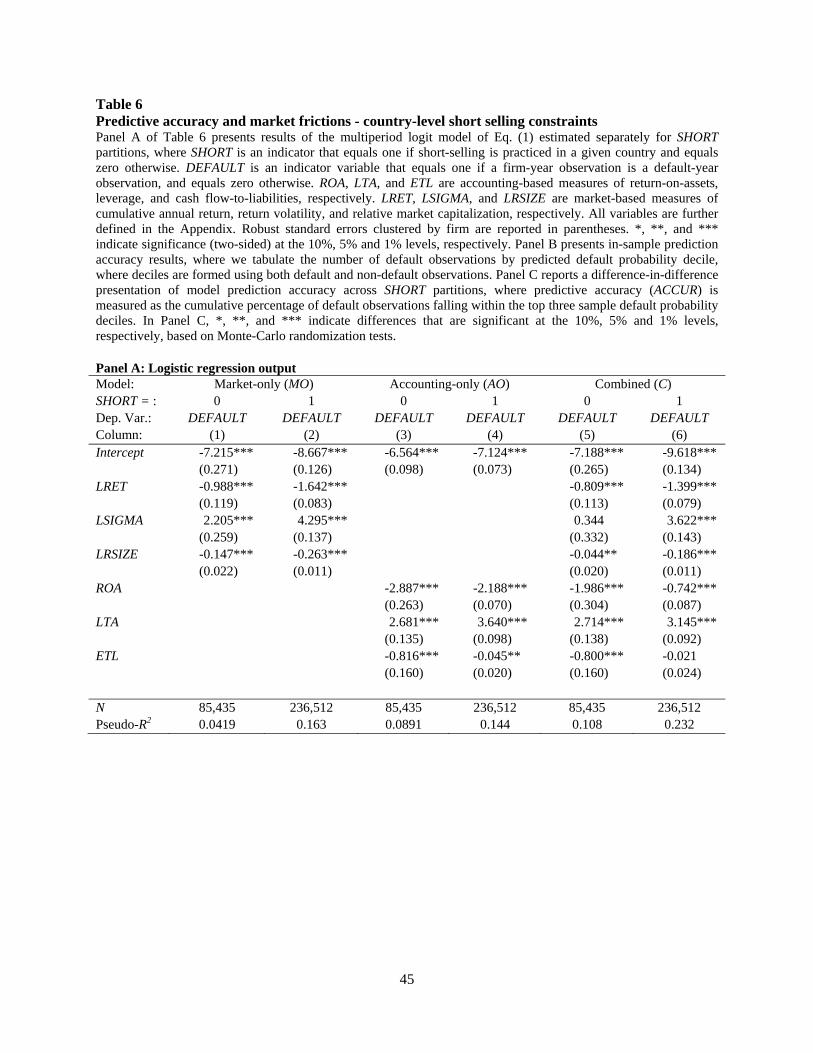

6.3.1. Market friction partitions

We begin by estimating the default prediction models separately for the SHORT = 0 and

SHORT = 1 sample partitions. Panel A of Table 6 presents associated coefficient estimates and

standard errors. In both market friction regimes, the basic relations between the predictive

variables and incidence of default are generally consistent with prior literature and our pooled

24

results in Table 3. Again, lagged stock return (LRET), relative size (LRSIZE), return-on-assets

(ROA) and the cash flow to liabilities ratio (ETL) are negatively associated with estimated default

probability, whereas return volatility (LSIGMA) and leverage (LTA) are positively associated

with estimated default probability. The R2 values suggest that the default prediction models have

a better fit in SHORT=1 regimes, which is consistent with our expectations. Panel B of Table 6

presents the number of default observations falling in each decile of predicted default probability

within each SHORT regime, where each decile is computed from the combined default and non-

default firm-year observations, and is ranked in descending order (i.e., decile 0 has the highest

predicted default probability).

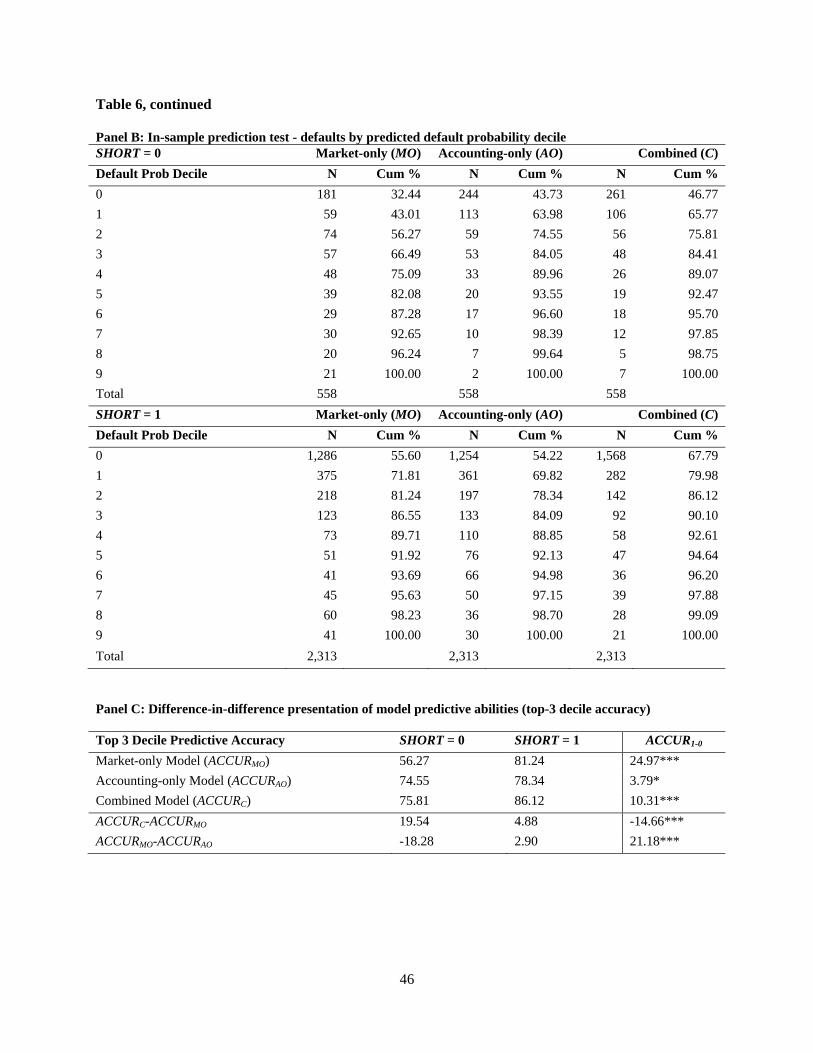

Panel C of Table 6 summarizes the predictive accuracy metrics from each model in each

market friction regime, and reports significance tests of the difference in accuracy across regimes

based on Monte Carlo randomization testing. Consistent with our multivariate analysis in Table

5, we see that there is a large and highly significant differential in the predictive accuracy of the

market-only model across SHORT partitions, again providing evidence that market frictions are

an important determinant of the ability of market variables to predict default. Specifically, the

predictive accuracy of the market-only model is nearly twenty-five percentage points higher

where short-selling is practiced (81.24 versus 56.27). In contrast, the predictive accuracy of the

accounting-only model shows little difference across market friction regimes, consistent with the

notion that market frictions do not generally inhibit the direct informativeness of financial

statement information. Based on this finding, it is not surprising that the difference in combined

model predictive accuracy across market friction regimes is less severe than that for the market-

only model (i.e., 10.31 versus 24.97).

25

An alternative way of making this latter point can be seen through a cross-regime

comparison of the incremental predictive accuracy of the combined model over the market-only

model, i.e., ACCURCACCURMO, where this difference captures the increase in predictive

accuracy that comes from the addition of financial statement information to the market-based

predictors. Where short-selling is not practiced, the addition of accounting variables improves

predictive accuracy nearly twenty percentage points, compared to only five percentage points

where short-selling is practiced (the difference of 14.66 is highly statistically significant). These

observations suggest the additional inference that the direct use of accounting information in

default prediction helps overcome the effects of market frictions.

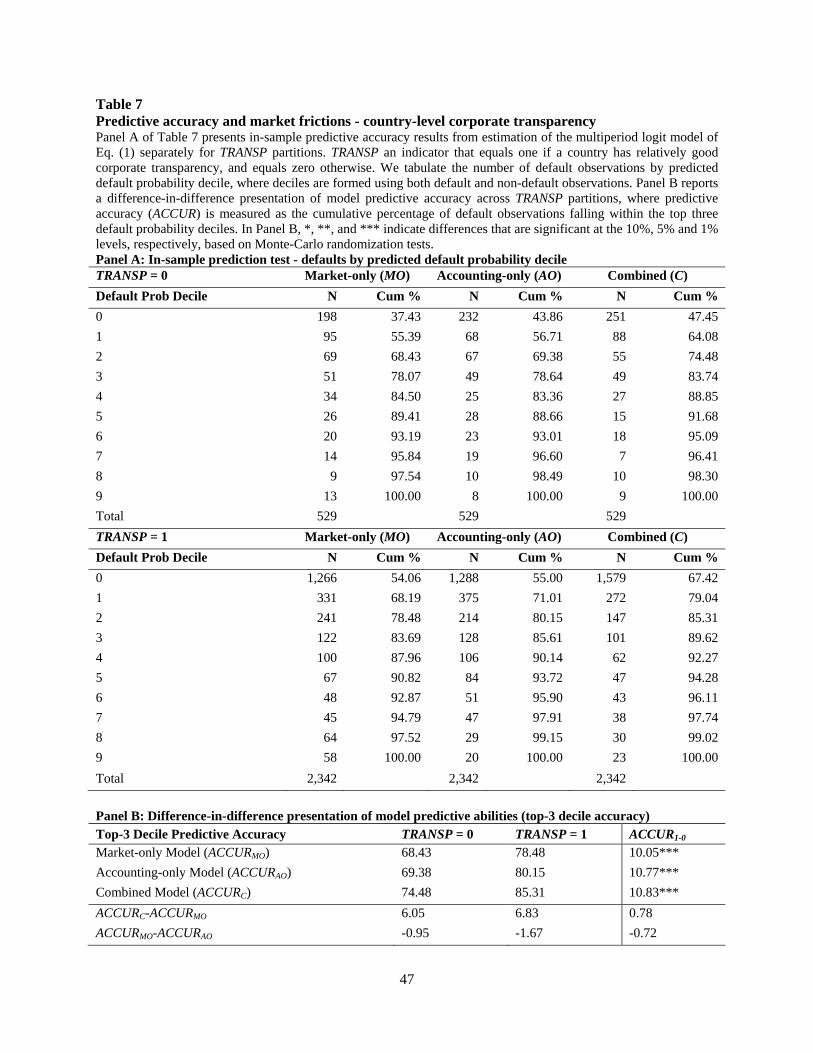

6.3.2. Corporate transparency partitions

We next estimate the default prediction models separately for the TRANSP = 0 and

TRANSP = 1 sample partitions. Panel A of Table 7 presents the number of default observations

falling in each decile of predicted default probability within each TRANSP regime (analogous to

the Table 6 Panel B presentation for SHORT regimes). Panel B of Table 7 summarizes the

predictive accuracy metrics from each model in each corporate transparency regime (analogous

to the Table 6 Panel C presentation for SHORT regimes). Here, we refocus on our attempt to

corroborate the Table 5 inference that market frictions are the primary determinant of variation in

market-only model predictive accuracy. Panel B of Table 7 reveals that there is a ten percentage

point difference in predictive accuracy of the market-only model across TRANSP regimes, which

seems to suggest that corporate transparency improves the predictive accuracy of the market-

only model. However, this ten percentage point difference is less than half the magnitude of the

twenty-five percentage point difference in the predictive accuracy of the market-only model

across market friction regimes, as observed in Table 6. Taken together, these results corroborate

26

the inference that market frictions are a more important determinant of market-only predictive

accuracy than is corporate transparency.

Interestingly, the difference in combined model predictive accuracy across transparency

regimes (10.83 percentage points) is almost identical to the difference in combined model

predictive accuracy across market friction regimes (10.31 percentage points, from Table 6). This

observation is likewise consistent with the general nature of the results from the Table 5

multivariate analysis. That is, in the combined model, the separate influences of market frictions

and corporate transparency on predictive accuracy seem to be of roughly equivalent magnitude.

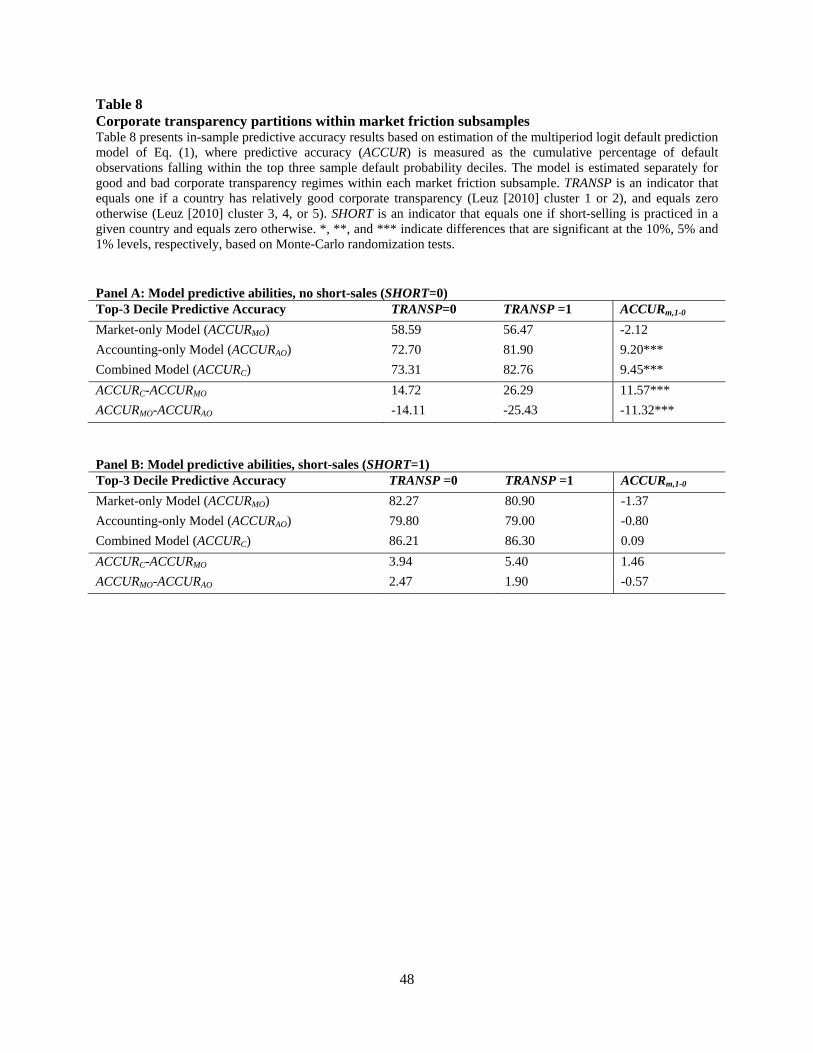

6.3.3. Corporate transparency partitions within market friction subsamples

Recall from our Table 6 analysis that the addition of financial statement-based default

predictors to the market-only model increases predictive accuracy to a greater extent where

short-selling is prohibited, which suggests that the direct inclusion of accounting information in

default prediction can help to overcome the detrimental effects of market frictions. If this

inference is correct, we would then expect to see that, in the presence of frictions, the addition of

accounting information increases predictive accuracy to a greater extent when corporate

transparency (and therefore the quality of reported accounting information) is high. Stated

differently, we expect that the ability of financial statement variables to overcome market

frictions will be mitigated in settings with poor corporate transparency.

To test this dynamic, we estimate the default prediction models across a two-by-two

sample partition sort. That is, we estimate the models separately for the TRANSP = 0 and

TRANSP = 1 partitions within each of the SHORT = 0 and SHORT = 1 subsamples. If the direct

use of accounting information in default prediction indeed helps overcome market frictions, in

the presence of market frictions (i.e., in the SHORT = 0 subsample) we expect to see a larger

27

effect from the addition of accounting information when transparency is high (i.e., in the

TRANSP = 1 partition). Panel A of Table 8 presents the results of this test. The incremental

contribution of accounting information over-and-above market variables is 14.72 percentage

points where transparency is low, which reveals that the direct inclusion of accounting

information contributes to predictive accuracy even when corporate transparency is relatively

low. Notably, this incremental contribution increases to 26.29 percentage points where

transparency is high. As reported, this difference-in-differences of 11.57 is highly statistically

significant, and corroborates our inference that the direct inclusion of accounting information in

default prediction helps overcome the detrimental effects of market frictions on the ability of

market-variables to predict default.

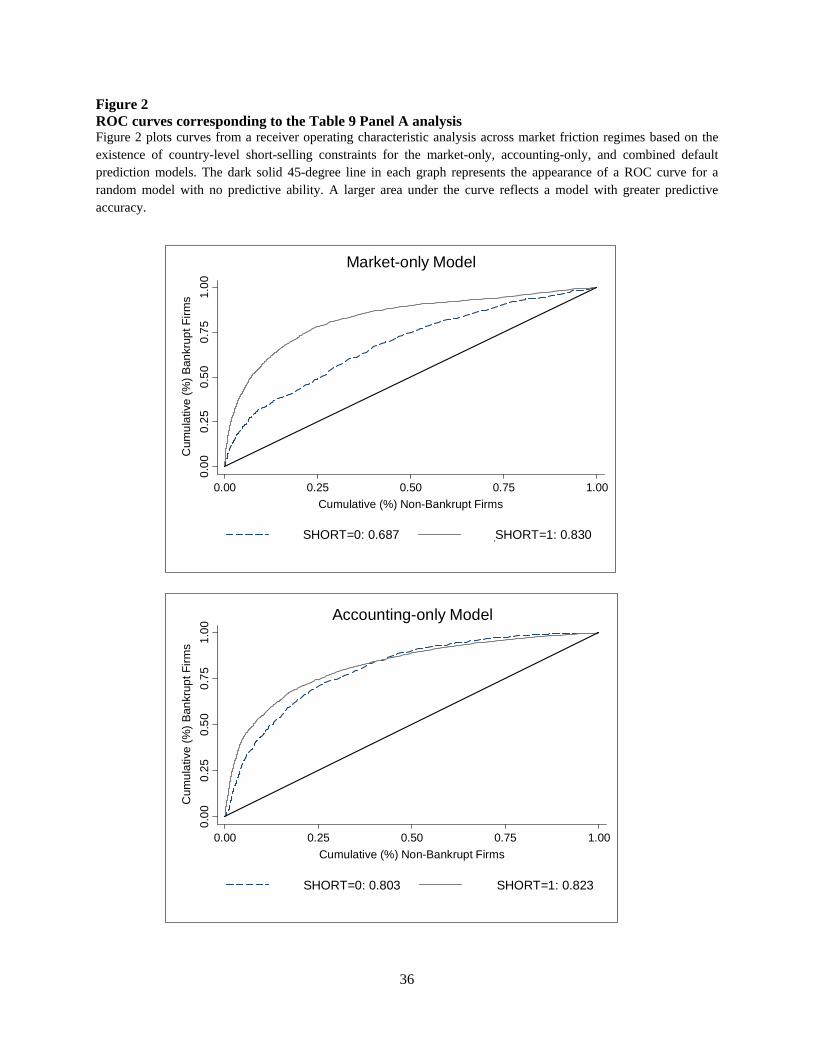

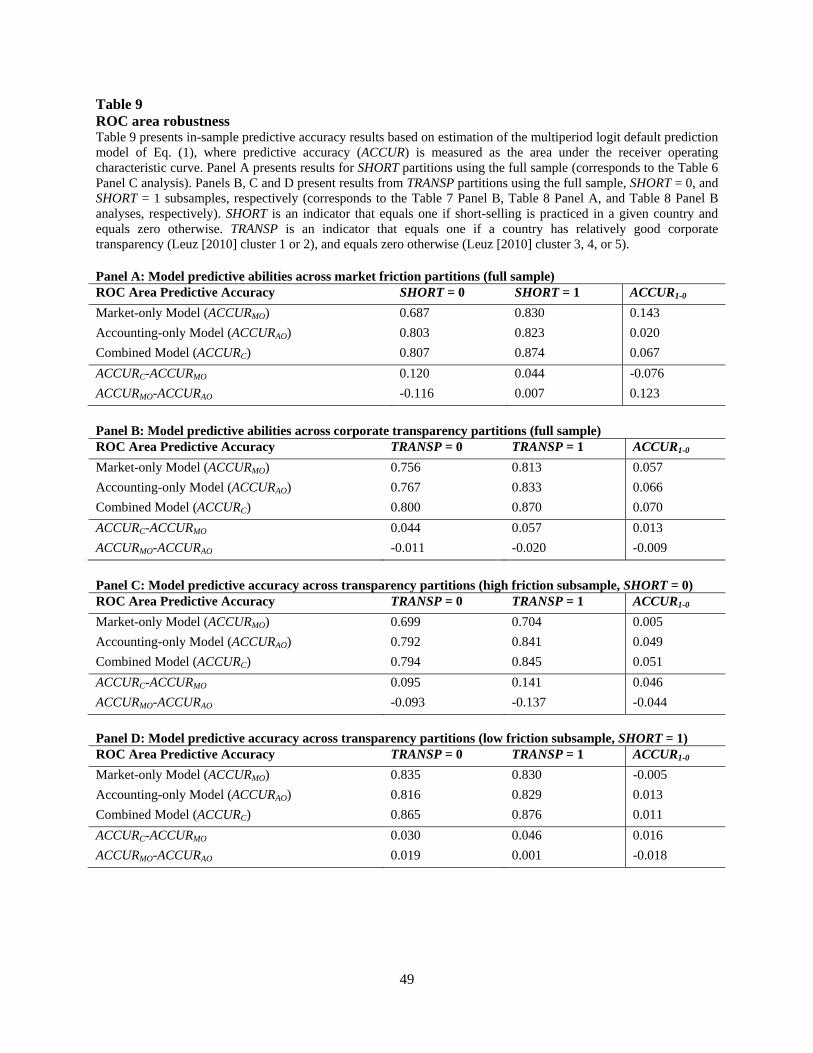

6.3.4. Robustness using receiver operating characteristic curves

To this point, we have measured the predictive accuracy of the default models we analyze

as the cumulative percentage of default observations in the top three estimated default

probability deciles across all sample observations (e.g., Beaver et al. 2012). In this section, we

consider whether our results are robust to an alternate measure of model predictive accuracy, the

area under the receiver operating characteristic (ROC) curve (e.g., Chava and Jarrow 2004).13 To

summarize, ROC curves are cumulative probability curves across the entire sample population

(ordered by estimated default probability) that simultaneously consider how a model performs in

terms of both Type I and Type II errors (i.e., how accurately the model classifies both default and

non-default observations), where the area under the curve is increasing in model accuracy. The

area under a ROC curve is generally expressed relative to the unit square area, where a value of

13 Moody's uses a similar tool called Cumulative Accuracy Profiles to assess model performance (Sobehart et al. 2001).

28

0.5 reflects a random model with no predictive ability, and a value of 1.0 indicates perfect

predictive ability.

Figure 2 plots the ROC curves that correspond to the market-only, accounting-only, and

combined models for both market friction regimes. The solid 45-degree line represents the no-

predictive-ability benchmark model, and the solid (dashed) curve represents the ROC curve for

the low (high) market friction partition. To aid interpretation, consider the curve for the

combined model in the low friction partition. The underlying full sample has been ranked by

estimated default probability, where estimated default probability decreases as the graph moves

away from the origin (note that estimated default probability is not reflected on either axis). One

of the points on that curve is approximately [0.15, 0.75]. The interpretation of this point is that, at

the particular estimated default probability underlying this point, 75% of the default observations

have a higher estimated default probability while only 15% of the non-default observations have

a higher estimated default probability.

Table 9 presents results from the ROC curve robustness analyses. Specifically, Panel A

repeats the market friction partition analysis from Table 6, Panel B repeats the corporate

transparency partition analysis from Table 7, and Panels C and D repeat the two-by-two partition

analysis from Table 8. To summarize, the pattern of results found across the panels in Table 9

are consistent with results and inferences made using our primary measure of predictive

accuracy. For example, a comparison of the differences in the ROC curve areas in the market-

only models in Panels A and B shows that the difference in predictive accuracy is more

pronounced across market friction partitions than across corporate transparency partitions (0.143

versus 0.057), and Panel A again shows that the addition of direct accounting information

29

improves predictive accuracy to a larger extent where significant frictions exist (0.120 versus

0.044).

6. Conclusion

While the factors that affect default prediction have been studied extensively in U.S.

capital markets, little is known from prior literature about how market and accounting-based

predictors of financial distress perform across countries and in particular how differences in

countries’ information environments affect market participants’ abilities to assess a company’s

likelihood of default. In this paper, we investigate these issues directly using a broad sample of

global defaults to examine cross-country differences in the predictive accuracy of a commonly

used class of default prediction models.

Although we find that our set of market and accounting-based predictors of default

generally behave as expected (in terms of sign and significance) for the vast majority of our

sample countries, we document significant differences across countries in the predictive accuracy

of these models, where the predictive ability of market-based variables differs most across

countries. Surprisingly, our results show that for half of the countries in our sample, a model that

uses only accounting information outperforms a model that uses only market-based variables.

This result stands in stark contrast to prior research which has overwhelmingly found that

market-based default predictors are superior to accounting predictors.

We also find evidence that cross-country variation in the ability of market variables to

predict default is primarily attributable to market frictions, rather than the availability of relevant

information. This finding provides some insight into the seemingly anomalous superior

performance of accounting- over market-based sources of default risk information that we

observe in some sample countries. In contrast to the market-only model, we find that both market

30

frictions and corporate transparency explain a significant portion of the variation in the

predictive accuracy of the combined model. Intuitively, this result is reassuring because the

combined prediction model directly includes financial reporting information, the informativeness

of which should be affected by the strength of the institutional infrastructure.

We find evidence that the direct inclusion of accounting information in default prediction

models helps to overcome the effects of market frictions, particularly in countries with relatively

high corporate transparency. Prior default prediction literature does not clearly articulate why,

other than model misspecification, public financial reporting information should have any effect

on default prediction incremental to market information. We shed light on this issue by

identifying market frictions as an explanation for the incremental explanatory power of

accounting-based sources of default risk information relative to market-based sources. Moreover,

our findings highlight improved default prediction accuracy in the presence of significant market

frictions as an additional capital market benefit of greater corporate transparency.

Consistent with extant literature, we do not attempt to quantify and incorporate variables

into the prediction models that capture publicly available information from non-accounting

sources, such as analyst outputs or media reports. It is unclear why extant literature has ignored

these sources of information in default prediction, other than the apparent assumption that

market-based variables likely incorporate default risk-relevant information from these alternate

information providers. One implication of our study is that, in the presence of market frictions,

this omission is not innocuous because information contained in these alternate sources may not

be imbedded in market-based variables. Therefore, including such variables may further improve

default prediction accuracy where significant market frictions exist. This issue remains an

interesting avenue for further study.

31

Appendix Variable definitions Subscripts i and t refer to a particular firm and fiscal year, respectively. Subscript c refers to a country, and subscript m refers to a particular default prediction model (market-only, accounting-only, or combined). ACCURm The predictive accuracy of default prediction model m, measured as the

cumulative percentage of default firm observations in the highest three predicted default probability deciles, where deciles are computed from combined default and non-default firm-year observations.

DEFAULTi,t An indicator variable that equals one if firm i has a default event in year t, and equals zero otherwise, where default events are identified from the RMI data from National University of Singapore.

ENGLISHc An indicator variable that equals one if the bankruptcy code in country c has an English legal origin, and equals zero otherwise.

ETLi,t Cash-flow-to-total liabilities ratio for firm i in year t; calculated from the RMI data as cash flow from operations divided by total liabilities.

FCLOSEc A variable that equals one if the hypothetical firm in Djankov et al. (2008) is most likely to undergo a foreclosure given the hypothetical circumstances presented, and equals zero otherwise.

FRENCHc An indicator variable that equals one if the bankruptcy code in country c has a French legal origin, and equals zero otherwise.

GERMANc An indicator variable that equals one if the bankruptcy code in country c has a German legal origin, and equals zero otherwise.

LIQUIDc A variable that equals one if the hypothetical firm in Djankov et al. (2008) is most likely to undergo a liquidation given the hypothetical circumstances presented, and equals zero otherwise.

LRETi,t Twelve month cumulative stock return for firm i ending in the month following firm i's financial statement availability for fiscal year t; calculated from the NUS RMI price data file.

LRSIZEi,t The natural logarithm of firm i's relative size, computed at the end of the month following firm i's fiscal year t financial statement data availability; relative size is computed as firm i's stock market capitalization (in U.S. dollars) divided by the aggregate sample market capitalization (in U.S. dollars), where stock market capitalization is obtained from Datastream.

LSIGMAi,t Standard deviation of firm i's monthly stock return for the twelve months ending in the month following firm i's financial statement availability for fiscal year t; calculated from the NUS RMI price data file.

LTAi,t Leverage ratio for firm i in year t; calculated from the RMI data as total liabilities divided by total assets.

32

NORDICc An indicator variable that equals one if the bankruptcy code in country c has a Nordic legal origin, and equals zero otherwise.

REORGc A variable that equals one if the hypothetical firm in Djankov et al. (2008) is most likely to undergo a reorganization given the hypothetical circumstances presented, and equals zero otherwise.

ROAi,t Return on assets for firm i in year t; calculated from the RMI data as net income divided by lagged total assets.

SHORTc A country-level price informativeness measure based on short-sales ability in country c; an indicator variable that equals one if short-selling is allowed/practiced in country c (i.e., "high" price informativeness) and equals zero otherwise (i.e., "low" price informativeness), where the coding is done based on the analysis in Bris et al. (2007).

TRANSPc An indicator variable that equals one if country c has a relatively strong corporate transparency (Leuz [2010] cluster 1 or 2), and equals zero otherwise (Leuz [2010] cluster 3, 4, or 5).

33

REFERENCES

Altman, E., 1968. Financial ratios, discriminant analysis and the prediction of corporate bankruptcy. Journal of Finance 23, 589-609.

Beaver, W., 1966. Financial ratios as predictors of failure. Journal of Accounting Research 4, 71-

111. Beaver, W., Correia, M., McNichols, M., 2012. Do differences in financial reporting attributes

impair the predictive ability of financial ratios for bankruptcy? Forthcoming, Review of Accounting Studies.

Beaver, W., McNichols, M., Rhie, J., 2005. Have financial statements become less informative?

Evidence from the ability of financial ratios to predict bankruptcy. Review of Accounting Studies 10, 93-122.

Bris, A., Goetzmann, W., Zhu, N., 2007. Efficiency and the bear: Short sales and markets around

the world. Journal of Finance 62 (3), 1029-1079. Bushman, R., Piotroski, J., Smith, A., 2004. What determines corporate transparency? Journal of

Accounting Research 42 (2), 207-252. Campbell, J., Hilscher, J., Szilagyi, J., 2008. In search of distress risk. Journal of Finance 63 (6),

2899-2939. Chava, S., Jarrow, R., 2004. Bankruptcy prediction with industry effects. Review of Finance 8,

537-569. Claessens, S., Klapper, L., 2005. Bankruptcy around the world: explanations of its relative use.

American Law and Economics Review 7 (1), 253-283. Djankov, S., Hart, O., McLiesh, C., Shleifer, A., 2008a. Debt enforcement around the world.

Journal of Political Economy 116 (6), 1105-1149. Durnev, A., Morck, R., Yeung, B., Zarowin, P., 2003. Does greater firm-specific return variation

mean more or less informed stock pricing? Journal of Accounting Research 41 (5), 797-836. Fernandes, N., Ferreira, M., 2009. Insider trading laws and stock price informativeness. Review

of Financial Studies 22, 1845-1887. Hillegeist, S., Keating, E., Cram, D., Lundstedt, K., 2004. Assessing the probability of

bankruptcy. Review of Accounting Studies 9, 5-34. Lang, M., Lins, K., Maffett, M., 2012. Transparency, liquidity and valuation: International

evidence on when transparency matters most. Journal of Accounting Research 50 (3), 729-774.

34

Leuz, C., 2010. Different approaches to corporate reporting regulation: how jurisdictions differ

and why. Accounting and Business Research 40 (3), 229-256. Leuz, C., Nanda, D., Wysocki, P., 2003. Earnings management and investor protection: An

international comparison. Journal of Financial Economics 69, 505-527. Maffett, M., 2012. Financial reporting opacity and informed trading by international institutional

investors. Journal of Accounting and Economics, forthcoming. Morck, R., Yeung, B., Yu, W., 2000. The information content of stock markets: why do

emerging markets have synchronous stock price movements? Journal of Financial Economics 58, 215-260.

Ohlson, J., 1980. Financial ratios and the probabilistic prediction of bankruptcy. Journal of

Accounting Research 18, 109-131. Saffi, P., Sigurdsson, K., 2011. Price efficiency and short selling. Review of Financial Studies 24

(3), 821-852. Shumway, T., 2001. Forecasting bankruptcy more accurately: A simple hazard model. Journal of

Business 74, 101-124. Sobehart, J., Keenan, S., Stein, R., 2001. Benchmarking quantitative default risk models: a

validation methodology. ALGO Research Quarterly 4, 57-72. Vassalou, M., Xing, Y., 2004. Default risk in equity returns. Journal of Finance 59, 831-868. Zmijewski, M.,1984. Methodological issues related to the estimation of financial distress

prediction models. Journal of Accounting Research 22, 59-82.

35

Figure 1 Sample defaults by year Figure 1 presents calendar-year frequency of the 2,871 default observations in our sample.

Year Frequency Percent Year Frequency Percent

1991 2 0.07 2002 323 11.25

1992 4 0.14 2003 216 7.52

1993 11 0.38 2004 150 5.22

1994 18 0.63 2005 116 4.04

1995 16 0.56 2006 85 2.96

1996 31 1.08 2007 86 3.00

1997 88 3.07 2008 247 8.60

1998 161 5.61 2009 349 12.16

1999 165 5.75 2010 117 4.08

2000 188 6.55 2011 94 3.27

2001 387 13.48 2012 17 0.59

Total 2,871 100.00

36

0.0

00

.25

0.5

00

.75

1.0

0

Cum

ula

tive

(%)

Ban

krup

t Fir

ms

0.00 0.25 0.50 0.75 1.00

Cumulative (%) Non-Bankrupt Firms

HPI_SHORT=0: 0.687 HPI_SHORT=1: 0.830

Market-only Model

0.0

00

.25

0.5

00

.75

1.0

0

Cum

ula

tive

(%)

Ban

krup

t Fir

ms

0.00 0.25 0.50 0.75 1.00

Cumulative (%) Non-Bankrupt Firms

HPI_SHORT=0: 0.803 HPI_SHORT=1: 0.823

Accounting-only Model

Figure 2 ROC curves corresponding to the Table 9 Panel A analysis Figure 2 plots curves from a receiver operating characteristic analysis across market friction regimes based on the existence of country-level short-selling constraints for the market-only, accounting-only, and combined default prediction models. The dark solid 45-degree line in each graph represents the appearance of a ROC curve for a random model with no predictive ability. A larger area under the curve reflects a model with greater predictive accuracy.

37

0.0

00

.25

0.5

00

.75

1.0

0

Cum

ula

tive

(%)

Ban

krup

t Fir

ms

0.00 0.25 0.50 0.75 1.00

Cumulative (%) Non-Bankrupt Firms

HPI_SHORT=0: 0.807 HPI_SHORT=1: 0.874

Combined Model

Figure 2, continued ROC curves corresponding to the Table 9 Panel A analysis

38

Table 1 Defaults by country Table 1 presents the number of firm-year observations for both the total sample and the default sample, by country. Table 1 also presents information on whether short selling is practiced within the country (Bris et al. 2007), and the Leuz (2010) institutional cluster categorization. Total Observations Default Observations Short-Selling Leuz (2010)

Country Frequency Percent Frequency Percent Practiced? Cluster

Australia 17,216 5.35 117 4.08 Yes 1

Austria 838 0.26 4 0.14 Yes 3

Belgium 1,229 0.38 4 0.14 Yes 2

Canada 10,570 3.28 96 3.34 Yes 1

China 12,846 3.99 159 5.54 No 4

Denmark 2,185 0.68 11 0.38 Yes 3

Finland 1,803 0.56 4 0.14 No 2

France 8,168 2.54 39 1.36 Yes 3

Germany 8,351 2.59 109 3.80 Yes 3

Hong Kong 12,590 3.91 37 1.29 Yes 1

India 18,056 5.61 29 1.01 No 1

Indonesia 2,994 0.93 33 1.15 No 5

Italy 3,172 0.99 16 0.56 Yes 2

Japan 42,501 13.20 170 5.92 Yes 2

Malaysia 11,932 3.71 76 2.65 No 1

Netherlands 2,417 0.75 20 0.70 Yes 2

Norway 2,222 0.69 11 0.38 Yes 3

Philippines 1,896 0.59 24 0.84 No 5

Portugal 681 0.21 1 0.03 Yes 3

Singapore 7,081 2.20 27 0.94 Yes 1

South Korea 16,582 5.15 91 3.17 No 2

Spain 1,320 0.41 4 0.14 No 3

Sweden 4,761 1.48 20 0.70 Yes 3

Switzerland 2,721 0.85 8 0.28 Yes 3

Taiwan 12,587 3.91 32 1.11 No 2

Thailand 5,419 1.68 106 3.69 No 5

UK 24,025 7.46 106 3.69 Yes 1

US 85,784 26.65 1,517 52.84 Yes 1

Total 321,947 100.00 2,871 100.00

39

Table 2 Descriptive statistics Table 2 presents descriptive statistics for key variables used in our study. ROA, LTA, and ETL are accounting-based measures of return-on-assets, leverage, and cash flow-to-liabilities, respectively. LRET, LSIGMA, and LRSIZE are market-based measures of cumulative annual return, return volatility, and relative market capitalization, respectively. All variables are further defined in the Appendix. N Mean Std Min P25 P50 P75 Max

ROA 321,947 -0.007 0.185 -1.464 -0.016 0.027 0.073 0.359

LTA 321,947 0.500 0.244 0.007 0.315 0.502 0.669 1.613

ETL 321,947 0.010 0.931 -13.286 -0.010 0.098 0.247 2.847

LRET 321,947 0.103 0.674 -1.000 -0.300 -0.025 0.311 4.600