defined benefit plans – legislative update, trends and opportunities - vince spina - maryann geary

TRANSCRIPT

B P A S P A R T N E R C O N F E R E N C E 2 0 1 6

Defined Benefit Plans – Legislative Update,

Trends and OpportunitiesVincent F. Spina

CPC, ERPA, Executive Vice President, BPAS Plan Administration

B P A S P A R T N E R C O N F E R E N C E 2 0 1 6

Maryann GearyASA, EA, MAAA, President, BPAS Actuarial & Pension Services, and & Recordkeeping Services

Agenda

2016 BPAS Partner Conference

• Legislative Update for Defined Benefit Plan Sponsors

• “Borrow, Fund & Immunize” Strategy

• Long-term Trends

2016 BPAS Partner Conference

On November 2, 2015, the President signed into law a two-year bipartisan budget deal that contains provisions relevant to sponsors of defined benefit pension plans. These provisions include:

• PBGC Premium Increases

• Segment Rate Stabilization Extension

Legislative UpdateBipartisan Budget Act of 2015 (“BBA”)

2016 BPAS Partner Conference

PBGC Premium Increases: The BBA calls for increases to both the flat-rate and variable-rate premium starting in 2017.

Plan Year Flat-Rate Premium Variable-Rate Premium(1)

2015 $57 2.4%

2016 $64 3.0%

2017 $69 3.3% + inflation

2018 $74 3.7% + inflation

2019 $80 + inflation 4.1% + inflation

(1) If using the alternative method, cannot utilize the interest rate stabilization provisions to determine the unfunded vested benefits.

Flat-Rate Premium = Per participant charge. Variable-Rate Premium = Percentage charge for unfunded vested benefits.

Legislative UpdateBipartisan Budget Act of 2015 (“BBA”)

2016 BPAS Partner Conference

Segment Rate Stabilization Extension

• Under the Moving Ahead for Progress in the 21st Century Act (MAP-21), interest rates used to determine the Funding Target Liability must be within a certain range of the 25-year average of interest rates.

• The Highway and Transportation Funding Act of 2014 (HATFA) extended the 10% corridor established by MAP-21 in 2012 through 2017. The BBA further extended the 10% corridor through 2020. The corridor will phase-out to 30% between 2021 and 2024.

Legislative UpdateBipartisan Budget Act of 2015 (“BBA”)

2016 BPAS Partner Conference

Segment Rate Stabilization Extension

It is important to note that the segment rate stabilization only impacts the calculation of the Plan’s minimum required contribution and the Adjusted Funding Target Attainment Percentage (AFTAP).

– Does not impact the calculation of:

• Financial accounting results under ASC 715-30

• PBGC variable rate premium

• Termination cost

• Lump sum calculations

Legislative UpdateBipartisan Budget Act of 2015 (“BBA”)

This chart assumes interest rates remain level from May 31, 2016 into the future.

2016 BPAS Partner Conference 7

4.46%

4.29%4.38% 4.37% 4.37% 4.37% 4.37% 4.37% 4.37% 4.37%

6.37%

6.18%

6.00%

5.49%

5.03%

4.61%

4.37%

5.81%

5.65%5.52%

5.09%

4.67%

4.41%

3.50%

4.00%

4.50%

5.00%

5.50%

6.00%

6.50%

7.00%

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024Plan Year Beginning January 1,

Projected Effective Interest Rate

Without MAP-21/HATFA With MAP-21/HATFA With BBA

Legislative UpdateBipartisan Budget Act of 2015 (“BBA”)

2016 BPAS Partner Conference

• PBGC variable rate premium is 3% of Plan’s underfunded in 2016, increasing to 4.1% by 2019

– Sponsor only receives “coverage” for this premium

– PBGC is making the statement: “we don’t want to be your bank”

One Approach to Underfunded Issues:Borrow, Fund & Immunize

2016 BPAS Partner Conference

Many sponsors with good credit are considering a strategy of borrow, fund & immunize. • A Sponsor borrows from a bank the amount of PBGC

underfunding and contributes it to the plan.– Borrowing rates may be very similar to that of PBGC variable rate premium, so

interest costs may be offset completely by reduction in PBGC premiums.– Any amount that the contribution earns on the deposit while in the plan’s trust is in

essence “arbitrage.”– If a client is a tax-paying entity, they receive the value of the deduction in the year

deposited: in essence the government “subsidizes the loan.”– Immunization of the portfolio at the time of deposit is a de-risking strategy.

One Approach to Underfunded Issues:Borrow, Fund & Immunize

2016 BPAS Partner Conference

UnderRelief

w/oRelief

Effective Interest Rate 6.32% 4.10%

Plan Assets $ 20,558,936 $ 20,558,936

Target Liability $ 18,990,676 $ 25,027,411

Over/(Under) Funding $ 1,568,260 $ (4,468,475)

Funded Percentage 108.3% 82.1%

One Plan’s Impact of Funding Relief

2016 BPAS Partner Conference

• Immunization Strategy– Looking at projected annual benefit payments from a plan and constructing a

portfolio of high-quality corporate bonds whose dividends and maturity values “match-up” to the payment stream.

– Immunization is meant to eliminate interest rate risk.– Some portfolio managers use derivatives to provide duration. Buyer beware!– How much lower can 30-year Treasury rates go?

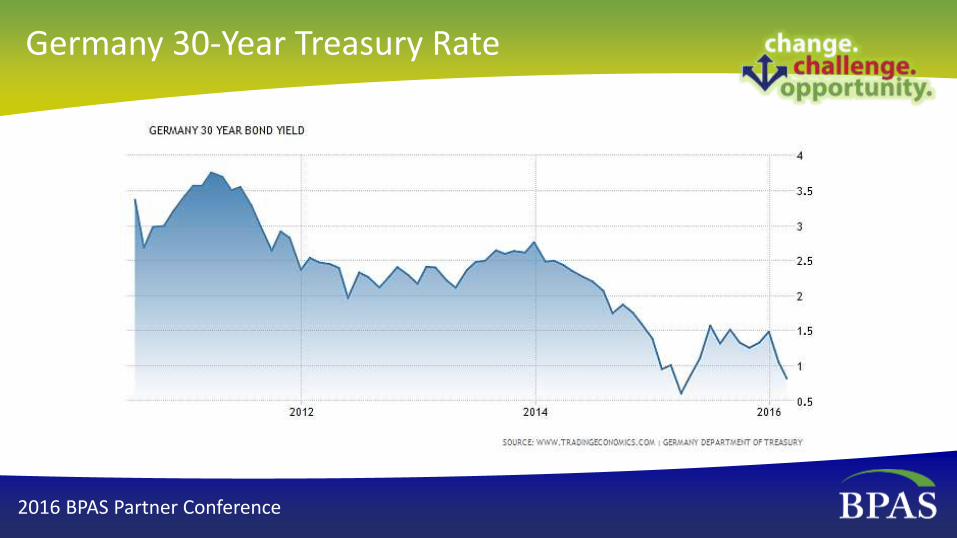

• United State 30-Year Treasury yields are currently around 2.6%.• German (i.e. 0.90%) and Japanese (i.e. 0.35%) rates are significantly lower!

• Our clients who have done this have replaced volatile pension expense with predictable loan payments.

One Approach to Underfunded Issues:Borrow, Fund & Immunize

2016 BPAS Partner Conference

From 2015 Trustees Report (Social Security and Medicare): https://www.ssa.gov/oact/trsum/

Social Security and Medicare: The Projected Cost “Blow-up”

2016 BPAS Partner Conference

Longer-term fixes will require one or combination of:

• Benefit cuts (increase retirement age, adjust COLA or actual cut in benefit itself)– Whose benefits get cut?

• Tax increase– Who do we tax more?

• Cut the Defense Budget– Whose jobs get cut?

• Run larger deficits– What we’ve been doing!

Social Security and Medicare Funding Issues

2016 BPAS Partner Conference

Median Household Income

2016 BPAS Partner Conference

Reduction in number of children…and…

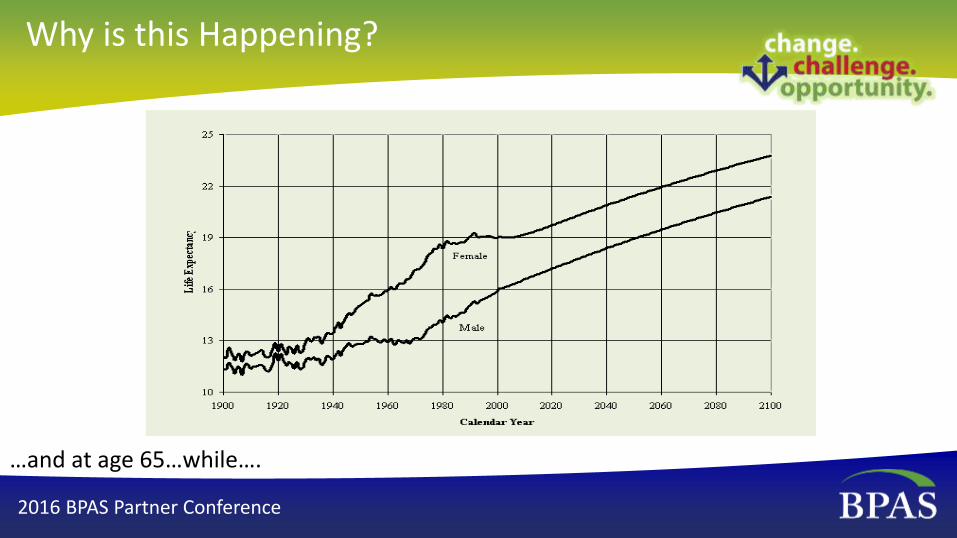

Social Security was “Fixed” in 1983… So Why is this Happening?

2016 BPAS Partner Conference

…dramatic improvements in life expectancy…at birth…

Why is this Happening?

2016 BPAS Partner Conference

…and at age 65…while….

Why is this Happening?

2016 BPAS Partner Conference

…% of those age 16 to 65 working has declined leading to…

Why is this Happening?

2016 BPAS Partner Conference

…reduction in Worker to Retiree ratio…projected to decrease to 2.0 in 2030.

Why is this Happening?

2016 BPAS Partner Conference

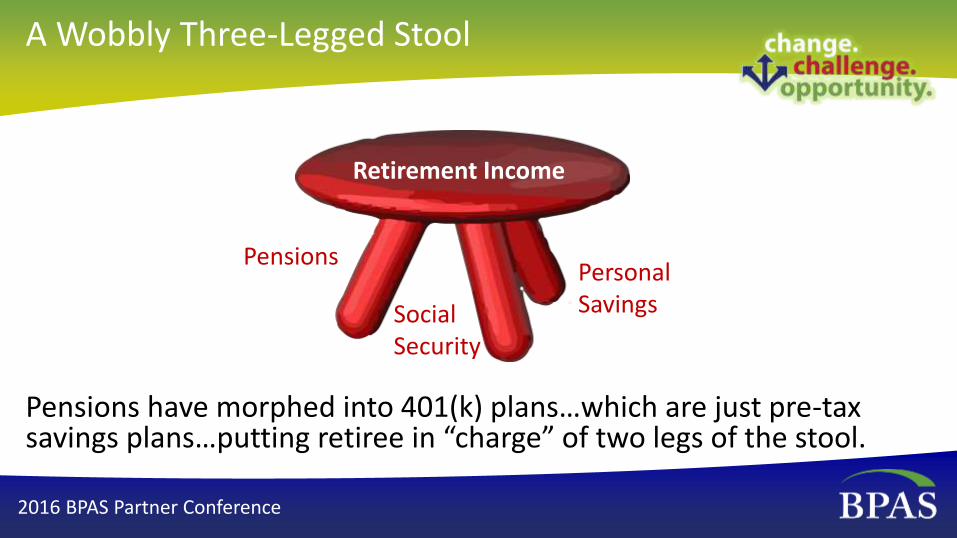

Pensions have morphed into 401(k) plans…which are just pre-tax savings plans…putting retiree in “charge” of two legs of the stool.

Retirement Income

Pensions

Social Security

Personal Savings

A Wobbly Three-Legged Stool

2016 BPAS Partner Conference

Decline in 30-Year Treasury Yields have led to...

2016 BPAS Partner Conference

$420,000

$760,000

$-

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

$900,000

Cost of Annuity Providing $50,000 a Year for Life to 65Year Old Male

1985

2016

Significant Increase in Cost of Guaranteed Income

2016 BPAS Partner Conference

• Employees are going to want to work longer.– For a married couple who are both age 65 and in good health, it’s 50-50

that one or both live until age 92!!

• If they want to retire comfortably, they almost certainly are going to have to save more than they have been.– Leading to explosive growth in Cash Balance Plans

• They are going to need a lot of help planning for retirement…whenever that is.

• How do employers navigate their fiduciary responsibilities in this environment?

Implications for Employers

2016 BPAS Partner Conference

Germany 30-Year Treasury Rate

2016 BPAS Partner Conference

Japan 30-Year Treasury Rate

2016 BPAS Partner Conference

Q&A

2016 BPAS Partner Conference

Vincent F. Spina, ASA, EA

President

BPAS Actuarial & Pension Services

(315) 703-8999

Contact Information

B P A S P A R T N E R C O N F E R E N C E 2 0 1 6

BPAS PARTNER CONFERENCE 2016

#BPASPC