definitions-m & as

TRANSCRIPT

Mergers and Acquisitions-An overview

AcquisitionAn acquisition, also known as a takeover, is the buying of one company (the ‘target’) by another. An acquisition may be friendly or hostile. In the former case, the companies cooperate in negotiations; in the latter case, the takeover target is unwilling to be bought or the target's board has no prior knowledge of the offer. Acquisition usually refers to a purchase of a smaller firm by a larger one. Sometimes, however, a smaller firm will acquire management control of a larger or longer established company and keep its name for the combined entity. This is known as a reverse takeover.

Another type of acquisition is reverse merger, deal that enables a private company to get publicly listed Co. A reverse merger occurs when a private company that has strong prospects and is eager to raise financing buys a publicly listed company, usually one with no business and limited assets. Achieving acquisition success has proven to be very difficult, while various studies have showed that 50% of acquisitions were unsuccessful. The acquisition process is very complex, with many dimensions influencing its outcome.

This model provides a good overview of all dimensions of the acquisition process.

The buyer buys the shares, and control of the target company being purchased. Ownership control in turn conveys effective control over the assets of the company, but since the company is acquired intact as a going business, this form of transaction carries with it all of the liabilities accrued by that business over its past and all of the risks that company faces in its commercial environment.

The buyer buys the assets of the target company. The cash the target receives from the sell-off is paid back to its shareholders by dividend or through liquidation. This type of transaction leaves the target company as an empty shell, if the buyer buys out the entire assets. This can be particularly important where foreseeable liabilities may include future, unquantified damage awards such as those that could arise from litigation over defective products, employee benefits or terminations, or environmental damage.

MergerIn business or economics a merger is a combination of two companies into one larger company. Such actions are commonly voluntary and involve stock swap or cash payment to the target. A merger can resemble a takeover but result in a new company name (often combining the names of the original companies) and in new branding; in some cases, terming the combination a "merger" rather than an acquisition is done for marketing reasons.

Classifications of mergers

Horizontal mergers take place where the two merging companies produce similar product in the same industry.

1

Mergers and Acquisitions-An overview

Vertical mergers occur when two firms, each working at different stages in the production of the same good, combine.

Congeneric merger/concentric mergers occur where two merging firms are in the same general industry, but they have no mutual buyer/customer or supplier relationship, such as a merger between a bank and a leasing company.

Conglomerate mergers take place when the two firms operate in different industries.

Merger raises concerns in antitrust circles. Regulatory bodies such as the European Commission, the United States Department of Justice and the U.S. Federal Trade Commission, Competition Commission of Pakistan may investigate anti-trust cases for monopolies dangers, and have the power to block mergers.

Accretive mergers are those in which an acquiring company's earnings per share (EPS) increase. An alternative way of calculating this is if a company with a high price to earnings ratio (P/E) acquires one with a low P/E.

Dilutive mergers are the opposite of above, whereby a company's EPS decreases. The company will be one with a low P/E acquiring one with a high P/E.

The completion of a merger does not ensure the success of the resulting organization; indeed, many mergers (in some industries, the majority) result in a net loss of value due to problems. Correcting problems caused by incompatibility—whether of technology, equipment, or corporate culture— diverts resources away from new investment, and these problems may be exacerbated by inadequate research or by concealment of losses or liabilities by one of the partners. Overlapping subsidiaries or redundant staff may be allowed to continue, creating inefficiency, and conversely the new management may cut too many operations or personnel, losing expertise and disrupting employee culture. These problems are similar to those encountered in takeovers. For the merger not to be considered a failure, it must increase shareholder value faster than if the companies were separate, or prevent the deterioration of shareholder value more than if the companies were separate.

Distinction between Mergers and Acquisitions

Although they are often uttered in the same breath and used as though they were synonymous, the terms merger and acquisition mean slightly different things.

When one company takes over another and clearly established itself as the new owner, the purchase is called an acquisition. From a legal point of view, the target company ceases to exist, the buyer "swallows" the business and the buyer's stock continues to be traded.

In pure sense of the term, merger happens when two firms, often of about the same size, agree to go forward as a single new company rather than remain separately owned and operated. This kind of action is more precisely referred to as a "merger of equals". Both

2

Mergers and Acquisitions-An overview

companies' stocks are surrendered and new company stock is issued in its place. For example, both Daimler-Benz and Chrysler ceased to exist when the two firms merged, and a new company, DaimlerChrysler, was created.

In practice, however, mergers of equals don't happen very often. Usually, one company will buy another and, as part of the deal's terms, simply allow the acquired firm to proclaim that the action is a merger of equals, even if it is technically an acquisition. Being bought out often carries negative connotations, therefore, by describing the deal euphemistically as a merger, deal makers and top managers try to make the takeover more palatable.

A purchase deal will also be called a merger when both managements agree that joining together is in the best interest of both of their companies. But when the deal is unfriendly - that is, when the target company does not want to be purchased - it is always regarded as an acquisition.

Whether a purchase is considered, a merger or an acquisition depends on whether the purchase is friendly or hostile and how it is announced. In other words, the real difference lies in how the purchase is communicated to and received by the target company's board of directors, employees and shareholders. It is quite normal though for M&A deal communications to take place in a so called 'confidentiality bubble' whereby information flows are restricted due to confidentiality agreements (Harwood, 2005).

Business valuationThe five most common ways to valuate a business are

asset valuation , historical earnings valuation, future maintainable earnings valuation, relative valuation (comparable company & comparable transactions), discounted cash flow (DCF) valuation

Professionals who valuate businesses generally do not use just one of these methods but a combination of some of them, as well as possibly others that are not mentioned above, in order to obtain a more accurate value. These values are determined for the most part by looking at a company's balance sheet and/or income statement.

Accurate business valuation is one of the most important aspects of M&A as valuations like these will have a major impact on the price that a business will be sold for. Most often this information is expressed in a Letter of Opinion of Value (LOV) when the business is being valuated for interest's sake. There are other, more detailed ways of expressing the value of a business. These reports generally get more detailed and expensive as the size of a company increases, however, this is not always the case as there are many complicated industries which require more attention to detail, regardless of size.

3

Mergers and Acquisitions-An overview

Financing M&AMergers are generally differentiated from acquisitions partly by the way in which they are financed and partly by the relative size of the companies. Various methods of financing an M&A deal exist:

(1) Cash

Payment by cash. Such transactions are usually termed acquisitions rather than mergers because the shareholders of the target company are removed from the picture and the target comes under the (indirect) control of the bidder's shareholders alone.

A cash deal would make more sense during a downward trend in the interest rates. Another advantage of using cash for an acquisition is that there tends to lesser chances of EPS dilution for the acquiring company. Cash places constraints on the cash flow of the company.

(2) Financing

Financing capital may be borrowed from a bank, or raised by an issue of bonds (Term Finance Certificates in Pakistan). Alternatively, acquirer's stock may be offered as consideration. Acquisitions financed through debt are known as leveraged buyouts if they take the target private, and the debt will often be moved down onto the balance sheet of the acquired company.

(3) Hybrids

An acquisition can involve a combination of cash and debt or of cash and stock of the purchasing entity.

Specialist M&A advisory firmsThough, at present majority of M&A advice is provided by full-service investment banks, recent years have seen a rise in the prominence of specialist M&A advisers, who only provide M&A advice (and not financing). In Pakistan, this job is also done by commercial banks. These specialized companies are sometimes referred to as Transition Companies, assisting businesses often referred to as "companies in transition." To perform these services in the US, an advisor must be a licensed broker dealer, and subject to SECP.

4

Mergers and Acquisitions-An overview

Key motives behind M&AThe dominant rationale to explain M&A activity is that acquiring firms seek improved financial performance and market capture in terms of sales, new product line or extension in the existing product line. The following motives are considered to improve financial performance:

Synergy : This refers to the fact that the combined company can often reduce its fixed costs by removing duplicate departments or operations, lowering the costs of the company relative to the same revenue stream, thus increasing profit margins.

Increased revenue or market share: This assumes that the buyer will be absorbing a major competitor and thus increase its market power (by capturing increased market share) to set prices.

Cross-selling : For example, a bank buying a stock broker could then sell its banking products to the stock broker's customers, while the broker can sign up the bank's customers for brokerage accounts. Or, a manufacturer can acquire and sell complementary products.

Economy of scale : For example, managerial economies such as the increased opportunity of managerial specialization. Another example are purchasing economies due to increased order size and associated bulk-buying discounts.

Taxation : A profitable company can buy a loss maker to use the target's loss as their advantage by reducing their tax liability. In the United States and many other countries, rules are in place to limit the ability of profitable companies to "shop" for loss making companies, limiting the tax motive of an acquiring company.

Geographical or other diversification: This is designed to smooth the earnings results of a company, which over the long term smoothens the stock price of a company, giving conservative investors more confidence in investing in the company. However, this does not always deliver value to shareholders (see below).

Resource transfer: resources are unevenly distributed across firms (Barney, 1991) and the interaction of target and acquiring firm resources can create value through either overcoming information asymmetry or by combining scarce resources.[1]

Vertical integration : Vertical integration occurs when an upstream and downstream firm merge (or one acquires the other). There are several reasons for this to occur. One reason is to internalise an externality problem. A common example is of such an externality is double marginalization. Double marginalization occurs when both the upstream and downstream firms have monopoly power, each firm reduces output from the competitive level to the monopoly level, creating two deadweight losses. By merging the vertically integrated firm can collect one deadweight loss by setting the upstream firm's output to the competitive level. This increases profits and consumer surplus. A merger that creates a vertically integrated firm can be profitable.[2]

However, on average and across the most commonly studied variables, acquiring firms' financial performance does not positively change as a function of their acquisition

5

Mergers and Acquisitions-An overview

activity. Therefore, additional motives for merger and acquisiiton that may not add shareholder value include:

Diversification: While this may hedge a company against a downturn in an individual industry it fails to deliver value, since it is possible for individual shareholders to achieve the same hedge by diversifying their portfolios at a much lower cost than those associated with a merger.

Manager's hubris: manager's overconfidence about expected synergies from M&A which results in overpayment for the target company.

Empire-building : Managers have larger companies to manage and hence more power.

Manager's compensation: In the past, certain executive management teams had their payout based on the total amount of profit of the company, instead of the profit per share, which would give the team a perverse incentive to buy companies to increase the total profit while decreasing the profit per share (which hurts the owners of the company, the shareholders); although some empirical studies show that compensation is linked to profitability rather than mere profits of the company.

Effects on managementA study published in the July/August 2008 issue of the Journal of Business Strategy suggests that mergers and acquisitions destroy leadership continuity in target companies’ top management teams for at least a decade following a deal. The study found that target companies lose 21 percent of their executives each year for at least 10 years following an acquisition – more than double the turnover experienced in non-merged firms.

M&A marketplace difficultiesIn many countries, no marketplace currently exists for the mergers and acquisitions of privately owned SMEs (see the definition from SBP/SMEDA web sites). Market participants often wish to maintain a level of secrecy about their efforts to buy or sell such companies. Their concern for secrecy usually arises from the possible negative reactions a company's employees, bankers, suppliers, customers and others might have if the effort or interest to seek a transaction were to become known. This need for secrecy has thus far thwarted the emergence of a public forum or marketplace to serve as a clearinghouse for this large volume of business.

At present, the process by which a company is bought or sold can prove difficult, slow and expensive. A transaction typically requires six to nine months and involves many steps. Locating parties with whom to conduct a transaction forms one step in the overall process and perhaps the most difficult one. Qualified and interested buyers of multimillion dollar corporations are hard to find. Even more difficulties attend bringing a number of potential buyers forward simultaneously during negotiations. Potential acquirers in an industry simply cannot effectively "monitor" the economy at large for

6

Mergers and Acquisitions-An overview

acquisition opportunities even though some may fit well within their company's operations or plans.

An industry of professional "middlemen" (known variously as intermediaries, business brokers, and investment bankers) exists to facilitate M&A transactions. These professionals do not provide their services cheaply and generally resort to previously-established personal contacts, direct-calling campaigns, and placing advertisements in various media. In servicing their clients they attempt to create a one-time market for a one-time transaction. Stock purchase or merger transactions involve securities and require that these "middlemen" be licensed broker dealers SECP regulations in order to be compensated as a % of the deal. Generally speaking, an unlicensed middleman may be compensated on an asset purchase without being licensed. Many, but not all, transactions use intermediaries on one or both sides. Despite best intentions, intermediaries can operate inefficiently because of the slow and limiting nature of having to rely heavily on telephone communications. Many phone calls fail to contact with the intended party. Busy executives tend to be impatient when dealing with sales calls concerning opportunities in which they have no interest. These marketing problems typify any private negotiated markets. Due to these problems and other problems like these, brokers who deal with small to mid-sized companies often deal with much more strenuous conditions than other business brokers. Mid-sized business brokers have an average life-span of only 12-18 months and usually never grow beyond 1 or 2 employees.

The market inefficiencies can prove detrimental for this important sector of the economy. Beyond the intermediaries' high fees, the current process for mergers and acquisitions has the effect of causing private companies to initially sell their shares at a significant discount relative to what the same company might sell for were it already publicly traded. An important and large sector of the entire economy is held back by the difficulty in conducting corporate M&A (and also in raising equity or debt capital). Furthermore, it is likely that since privately held companies are so difficult to sell they are not sold as often as they might or should be.

Previous attempts to streamline the M&A process through computers have failed to One part of the M&A process which can be improved significantly using networked computers is the improved access to "data rooms" during the due diligence process however only for larger transactions. For the purposes of small-medium sized business, these datarooms serve no purpose and are generally not used. Reasons for frequent failure of M&A was analyzed by Thomas Straub in "Reasons for frequent failure in mergers and acquisitions - a comprehensive analysis", DUV Gabler Edition, 2007.

The Great Merger MovementThe Great Merger Movement was a predominantly U.S. business phenomenon that happened from 1895 to 1905. During this time, small firms with little market share consolidated with similar firms to form large, powerful institutions that dominated their markets. It is estimated that more than 1,800 of these firms disappeared into consolidations, many of which acquired substantial shares of the markets in which they

7

Mergers and Acquisitions-An overview

operated. The vehicle used were so-called trusts. To truly understand how large this movement was—in 1900 the value of firms acquired in mergers was 20% of GDP. In 1990 the value was only 3% and from 1998–2000 is was around 10–11% of GDP. Organizations that commanded the greatest share of the market in 1905 saw that command disintegrate by 1929 as smaller competitors joined forces with each other. However, there were companies that merged during this time such as DuPont, Nabisco, US Steel, and General Electric that have been able to keep their dominance in their respected sectors today due to growing technological advances of their products, patents, and brand recognition by their customers. These companies that merged were consistently mass producers of homogeneous goods that could exploit the efficiencies of large volume production. Companies which had specific fine products, like fine writing paper, earned their profits on high margin rather than volume and took no part in Great Merger Movement.

Short-run factors

One of the major short run factors that sparked in The Great Merger Movement was the desire to keep prices high. That is, with many firms in a market, supply of the product remains high. During the panic of 1893, the demand declined. When demand for the good falls, as illustrated by the classic supply and demand model, prices are driven down. To avoid this decline in prices, firms found it profitable to collude and manipulate supply to counter any changes in demand for the good. This type of cooperation led to widespread horizontal integration amongst firms of the era. Focusing on mass production allowed firms to reduce unit costs to a much lower rate. These firms usually were capital-intensive and had high fixed costs. Because new machines were mostly financed through bonds, interest payments on bonds were high followed by the panic of 1893, yet no firm was willing to accept quantity reduction during this period.

Long-run factors

In the long run, due to the desire to keep costs low, it was advantageous for firms to merge and reduce their transportation costs thus producing and transporting from one location rather than various sites of different companies as in the past. This resulted in shipment directly to market from this one location. In addition, technological changes prior to the merger movement within companies increased the efficient size of plants with capital intensive assembly lines allowing for economies of scale. Thus improved technology and transportation were forerunners to the Great Merger Movement. In part due to competitors as mentioned above, and in part due to the government, however, many of these initially successful mergers were eventually dismantled. The U.S. government passed the Sherman Act in 1890, setting rules against price fixing and monopolies. Starting in the 1890s with such cases as U.S. versus Addyston Pipe and Steel Co., the courts attacked large companies for strategizing with others or within their own companies to maximize profits. Price fixing with competitors created a greater incentive for companies to unite and merge under one name so that they were not competitors anymore and technically not price fixing.

8

Mergers and Acquisitions-An overview

Cross-border M&AIn a study conducted in 2000 by Lehman Brothers, it was found that, on average, large M&A deals cause the domestic currency of the target corporation to appreciate by 1% relative to the acquirer's. For every $1-billion deal, the currency of the target corporation increased in value by 0.5%. More specifically, the report found that in the period immediately after the deal is announced, there is generally a strong upward movement in the target corporation's domestic currency (relative to the acquirer's currency). Fifty days after the announcement, the target currency is then, on average, 1% stronger.[5]

The rise of globalization has exponentially increased the market for cross border M&A. In 1996 alone there were over 2000 cross border transactions worth a total of approximately $256 billion. This rapid increase has taken many M&A firms by surprise because the majority of them never had to consider acquiring the capabilities or skills required to effectively handle this kind of transaction. In the past, the market's lack of significance and a more strictly national mindset prevented the vast majority of small and mid-sized companies from considering cross border intermediation as an option which left M&A firms inexperienced in this field. This same reason also prevented the development of any extensive academic works on the subject.

Due to the complicated nature of cross border M&A, the vast majority of cross border actions have unsuccessful results. Cross border intermediation has many more levels of complexity to it then regular intermediation seeing as corporate governance, the power of the average employee, company regulations, political factors customer expectations, and countries' culture are all crucial factors that could spoil the transaction.[6][7] However, with the weak dollar in the U.S. and soft economies in a number of countries around the world, we are seeing more cross-border bargain hunting as top companies seek to expand their global footprint and become more agile at creating high-performing businesses and cultures across national boundaries.

Even mergers of companies with headquarters in the same country are very much of this type (cross-border Mergers). After all,when Boeing acquires McDonnell Douglas, the two American companies must integrate operations in dozens of countries around the world. This is just as true for other supposedly "single country" mergers, such as the $27 billion dollar merger of Swiss drug makers Sandoz and Ciba-Geigy (now Novartis).

9

Mergers and Acquisitions-An overview

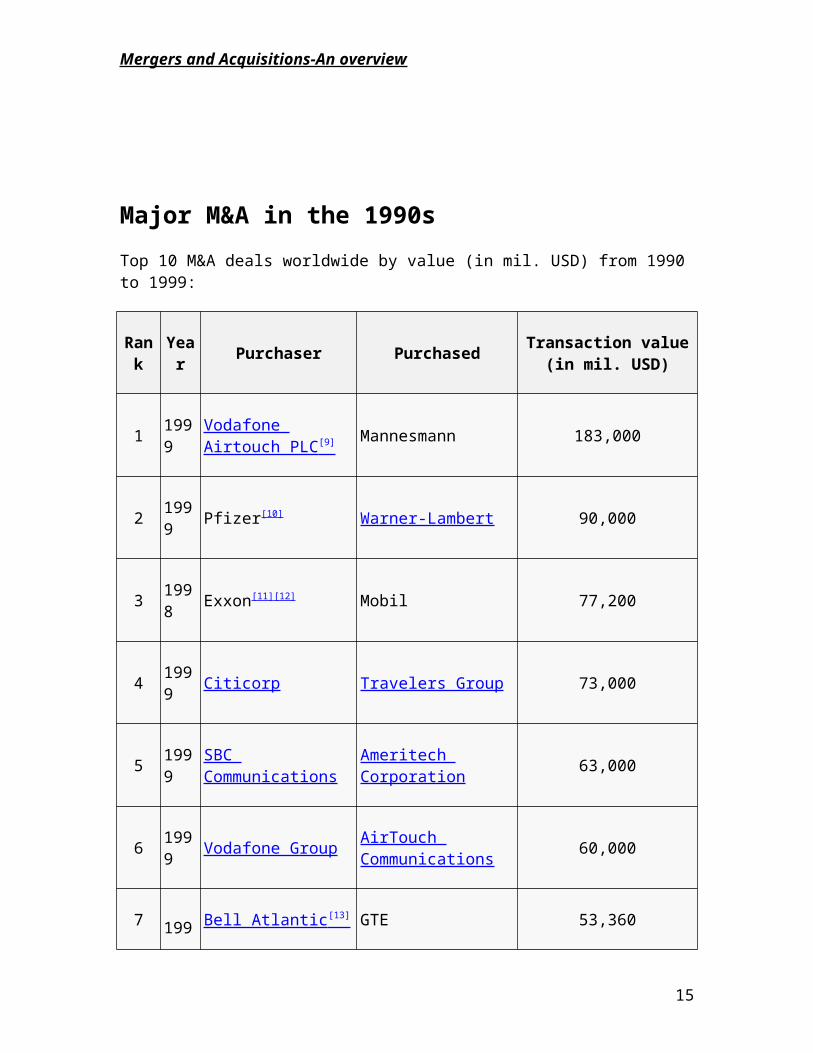

Major M&A in the 1990sTop 10 M&A deals worldwide by value (in mil. USD) from 1990 to 1999:

Rank Year Purchaser Purchased Transaction value (in mil. USD)

1 1999 Vodafone Airtouch PLC [9] Mannesmann 183,000

2 1999 Pfizer[10] Warner-Lambert 90,000

3 1998 Exxon[11][12] Mobil 77,200

4 1999 Citicorp Travelers Group 73,000

5 1999 SBC Communications Ameritech Corporation 63,000

6 1999 Vodafone Group AirTouch Communications 60,000

7 1998 Bell Atlantic [13] GTE 53,360

8 1998 BP[14] Amoco 53,000

9 1999 Qwest Communications US WEST 48,000

10 1997 Worldcom MCI Communications 42,000

10

Mergers and Acquisitions-An overview

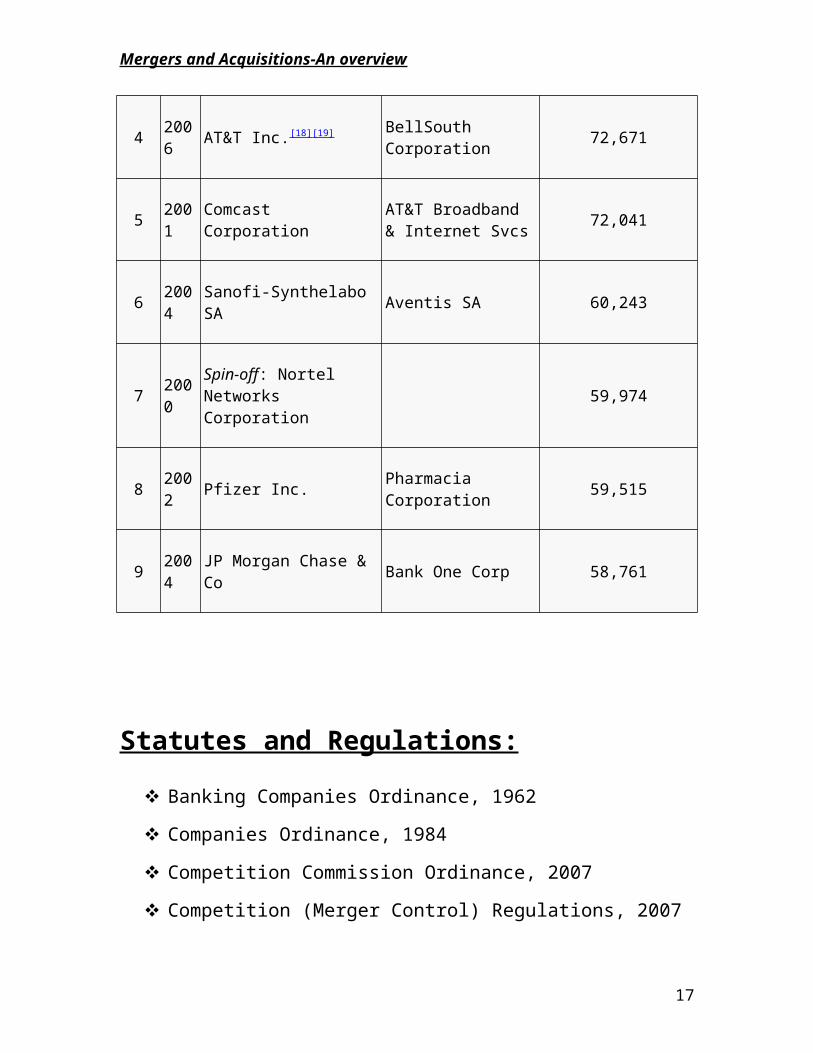

Major M&A from 2000 to presentTop 9 M&A deals worldwide by value (in mil. USD) since 2000

Rank Year Purchaser Purchased Transaction value (in mil. USD)

1 2000 Fusion: America Online Inc. (AOL)[16][17] Time Warner 164,747

2 2000 Glaxo Wellcome Plc. SmithKline Beecham Plc. 75,961

3 2004 Royal Dutch Petroleum Co.

Shell Transport & Trading Co 74,559

4 2006 AT&T Inc.[18][19] BellSouth Corporation 72,671

5 2001 Comcast Corporation AT&T Broadband & Internet Svcs 72,041

6 2004 Sanofi-Synthelabo SA Aventis SA 60,243

7 2000 Spin-off: Nortel Networks Corporation 59,974

8 2002 Pfizer Inc. Pharmacia Corporation 59,515

9 2004 JP Morgan Chase & Co Bank One Corp 58,761

11

Mergers and Acquisitions-An overview

Statutes and Regulations:

Banking Companies Ordinance, 1962

Companies Ordinance, 1984

Competition Commission Ordinance, 2007

Competition (Merger Control) Regulations, 2007

Contract Act, 1872

Foreign Exchange Regulation Act, 1947

Foreign Exchange Manual of State Bank of Pakistan

Income Tax Ordinance, 2001

Listed Companies (Substantial Acquisition of Voting Shares)

Ordinance, 2002

Registration Act, 1872

Sale of Goods Act, 1930

Stamp Act, 1899

State Bank of Pakistan Act, 1956

Transfer of Property Act, 1882

12

Mergers and Acquisitions-An overview

S hares and Mergers Acquisition Of Shares And Mergers Cleared By The CCP Under Section 11 Of The Competition Ordinance.

Brief of Transaction. Date of NOC.

1. ACQUISITION OF SHARES .

1 Acquisition of shares of M/s. IBL Modaraba Management Private Limited by Dr. Hasan Sohaib Murad

04-12-2007

2 Acquisition of shares of M/s. Wazeer Ali Industries Limited by M/s. Dalda Foods (Pvt) Limited.

13-12-2007

3 Acquisition of shares of M/s. Global Securities Pakistan Limited by M/s. NIB Bank Limited 31-12-2007

4 Acquisition of shares of M/s. Saudi Pak Bank Limited by a Consortium led by Mr. Shaukat Tarin.

11-01-2008

5 Acquisition of shares of M/s. Bosicor Oil Pakistan Limited by M/s Byco Industries Incorporated

07-02-2008

6 Acquisition of shares of M/s. DHL Pakistan (Pvt) Limited by M/s. Deutsche Post International BV

15-02-2008

7 Acquisition of shares of M/s Bosicor Pakistan Limited by M/s. Byco Industries Incorporated 20-02-2008

8 Acquisition of shares of M/s Bosicor Chemicals Pakistan Limited by M/s. Byco Industries Incorporated

20-02-2008

9 Acquisition of shares of M/s Worldcall Pakistan Limited by M/s. Oman Telecom. 25-02-2008

10 Acquisition of shares of M/s Makro Habib Pakistan Limited by M/s Thal Limited. 10-03-2008

11 Acquisition of shares of M/s. Tenaga Generasi Limited by M/s. Dawood Lawrencepur Limited.

27-03-2008

12 Acquisition of shares of Shirazi Group Companies by M/s. Shirazi Capital (Pvt) Limited. 28-03-2008

13

Mergers and Acquisitions-An overview

13 Acquisition of shares of M/s Indus Motor Company Limited by M/s. Toyota Corporation Japan .

29-04-2008

14 Acquisition of shares of M/s EFU General Insurance Company by M/s. EFU Life Assurance Company.

02-05-2008

15 Possible Acquisition of shares of M/s. Heavy Electrical Complex (Pvt) Limited by M/s. Siemens ( Pakistan ) Engg. Company Limited.

15-05-2008

16 Acquisition of shares of M/s. MCB Bank Limited by M/s. Malayan Banking Berhad 20-05-2008

17 Acquisition of shares of Agro General Insurance Company by M/s. The Direct Insurance Company.

21-05-2008

18 Acquisition of shares of M/s. ABN Amro Bank ( Pakistan ) Limited by a consortium led by The Royal Bank of Scotland Group PLC.

22-05-2008

19. Acquisition of shares of M/s. Pakistan Cement Company Limited by M/s. Lafarge S .A. 23-05-2008

20 Acquisition of shares of shares of M/s. Nalco Pakistan (Pvt) Limited by M/s. Nalco Asia Holding Pte. Ltd.

30-05-2008

21Acquisition of shares of shares of M/s. Millat Industrial Products Limited by M/s. Millat Tractors Limited.

05-06-2008

22Acquisition of shares of M/s ICI Pakistan Limited by M/s. Akzo Nobel N.V. 05-06-

2008

23Acquisition of shares of M/s Pakistan PTA Limited by M/s. Akzo Nobel N.V. 05-06-

2008

24Proposed acquisition of M/s. Hazara Phosphates Fertilizer Limited by M/s. Pak-American Fertilizer Company Limited .

11-06-2008

25Acquisition of shares of M/s. First Capital Investment Limited by M/s. First Capital Securities Corporation Limited.

19-06-2008

26 Acquisition of shares of M/s. Shaheen Insurance Company Limited by M/s. First Capital Securities Corporation Limited.

19-06-2008

27 Acquisition of shares of M/s. Media Times Limited by M/s. First Capital Securities Corporation Limited.

19-06-2008

28 Acquisition of shares of M/s. Pace Barka Properties Limited by M/s. First Capital Securities Corporation Limited.

19-06-2008

29 Acquisition of shares of M/s. Unilever Pakistan Limited by M/s. Unilever Overseas Holding Limited, UK .

25-06-2008

30 Acquisition of shares of M/s. Shakarganj Food Products Limited by M/s. KASB Capital Limited.

25-06-2008

31 Acquisition of Representative Offices of American Express Bank Limited in Pakistan by M/s. Standard Chartered Bank Limited.

25-06-2008

32 Acquisition of shares of M/s. Coca-Cola Beverages Pakistan Limited by M/s. Coca-Cola Icecek Anonim Sirketi

03-07-2008

14

Mergers and Acquisitions-An overview

33 Acquisition of shares of M/s. Sweetwater Dairies Pakistan (Pvt) Ltd 04-07-2008

34 Acquisition of 75% shares of M/s. Laraib Energy Limited by M/s. Hub Power Company Limited

03-07-2008

35 Acquisition of shares of M/s. DHA Cogen Limited by M/s. AEI Asia Limited 17-07-2008

36 Acquisition of shares of M/s. Capital Asset Leasing Corporation by Optimus Limited. 01-08-2008

37 Acquisition of M/s. Rafhan Maize Products Company Limited by M/s. Bunge Limited. 01-08-2008

38Proposed acquisition of 90 to 100 percent shares of M/s. Heavy Electrical Complex (Pvt) Limited by M/s. Iljin Electric Company Limited. 11-08-

2008 39

Acquisition of 62.50% shares of M/s. Al-Asif Sugar Mills Limited by M/s. Haq Bahu Sugar Mills (Pvt) Limited.

21-08-2008

40 Acquisition of 27.40% shares of M/s. Vision Network Television Limited by M/s. Eastgate GEMs SPV3

21-08-2008

41 Proposed acquisition of M/s. Hazara Phosphate Fertilizers Limited by a Consortium comprising of M/s. Kissan Chemicals & Fertilizers (Pvt) Limited and M/s. Chaudhry Steel Re-Rolling Mills (Pvt) Limited

05-09-2008

42 Acquisition of 10% shares of M/s.Saif Power Limited by M/s. Habib Bank Limited. 15-09-2008

43 Proposed acquisition of M/s. Hazara Phosphates Fertilizer Limited by M/s. Warble (Pvt) Limited

18-09-2008

44 Acquisition of shares of Meezan Bank Limited by M/s Noor Financial Investment Company. 22-09-2008

45 Acquisition of 05.63% shares of M/s. MCB Bank Limited by M/s. Adamjee Insurance Company Limited.

25-09-2008

46 Acquisition of shares of M/s. Karachi Electric Supply Company by M/s. IGCF SP 21 Limited (Abraaj).

23-10-2008

47 Acquisition of shares of M/s. BankIslami Pakistan Limited by M/s. Dubai Banking Group LLC.

28-10-2008

48 Acquisition of 29% shares of M.s. Sweetwater Dairies Pakistan (Pvt) Limited by M/s. Unicornn Investment Bank.

31-10-2008

49 Acquisition of 51% shares of Tameer Microfinace Bank Limited by Telenor Pakistan (Pvt.) Limited.

27-11-2008

50 Acquisition of 100% shares of Mobiserve Pakistan (Pvt) Limited by Mobiserve Holding 05-12-2008

51 Acquisition of 18.14% shares of Uch Power Limited by Creative Energy Resources Corporation .

05-12-2008

52Acquisition of 3.90% shares of Meezan Bank Limited by Noor Financial Investment Company .

05-12-2008

53Acquisition of 1.00 million Non Voting Ordinary Shares of Tetra Pak Pakistan Limited by Packages Limited .

26-12-2008

54 Acquisition of total paid up shares and associated assets of Bristol-Myers Pakistan (Pvt) Limited by S.R. One International B.V, Netherlands .

31-12-2008

15

Mergers and Acquisitions-An overview

55 Acquisition of 09.25% shares of Dawood Islamic Bank Limited by Unicorn Investment Bank, B.S.C, Bahrain .

29-01-2009

56 Acquisition of 20% shares of Sandal Bar Rolling Mills (Pvt) Limited by Dr. Tariq Mahmood Chaudhry

20-02-2009

57 Acquisition of 8.83% shares of M/s. Allied Bank Limited by M/s. Ibrahim Fibres Limited 03-03-2009

2. MERGERS.

1 Merger of M/s. Anwar Cotton Mills (Pvt) Limited and M/s. Aslam Industries Limited with and into M/s. ACRO Textile Mills Limited

06-12-2007

2 Merger of M/s. Pakistan Credit and Investment Corporation with and into M/s. NIB Bank Limited.

31-12-2007

3 Merger of M/s. PICIC Commercial Bank Limited with and into M/s. NIB Bank Limited.. 31-12-2007

4 Merger of M/s. Total Media Limited with and into M/s. Media Times Limited. 15-02-2008

5 Merger of M/s. Crescent Bahuman Energy and M/s. Crescent Bahuman Textile Limited with and into M/s. Crescent Bahuman Limited.

16-04-2008

6Merger of M/s. Yousaf Sugar Mills Limited with M/s. Abdullah Sugar Mills Limited

24-06-2008

7Merger of M/s. Haseeb Waqas Engineering Limited with Abdullah Sugar Mills Limited.

24-06-2008

8Amalgamation of Al Abbas Industries Limited with and into Al Abbas Sugar Mills Ltd

27-06-2008

9Merger of M/s. Al-Abbas Holding (Pvt) Limited and M/s. Ghani Holding (Pvt) Limited with and into M/s. Javedan Cement Limited 11-08-

2008

10Merger of M/s. International Multi Leasing Corporation with and into M/s. Al Zamin Leasinng Modaraba 11-08-

2008

11Merger of M/s. Pirkoh Gas Company (Private) Limited with and into M/s. Oil & Gas Development Company Limited 04-09-

2008

12Mergers of M/s. Automotive Battery Company Limited with and into M/s. Exide Pakistan Limited. 09-09-

2008

13Merger of M/s. Pfizer Laboratories Limited and Parke Davis & Company Limited.

12-09-2008

16

Mergers and Acquisitions-An overview

14Merger of M/s. Merck Sharpe and Dohme of Pakistan Limited with and into M/s. OBS Pakistan (Pvt) Limited. 25-09-

2008 15 Merger of KASB Bank Limited, KASB Capital and Atlas Bank Limited 07-11-

2008

16Merger of M/s. Nishat Apparel Limited with and into M/s Nishat Mills Limited.

11-11-2008

17 Merger of M/s. Jubilee Energy Limited with and into M/s. Jubilee Spinning and Weaving Mills Limited.

18-11-2008

18 Merger of Network Leasing Corporation Limited with and into KASB Bank Limited . 05-12-2008

19Amalgamation of the Hong Kong and Shanghai Banking Corporation (all branches in Pakistan ) with and into HSBC Bank Middle East Limited.

30-01-2009

Joint Venture:

1 Formation of a Joint Venture Company M/S. Adamjee Life Assurance Company Ltd by M/s. Adamjee Insurance Company Ltd, Hollard Life Assurance Company Ltd & IVM Intersurer B.V.

For reference:

http://www.mca.gov.pk/Downloads/ccp-Rules/Merger-Control-

Regulation.pdf

17

Mergers and Acquisitions-An overview

Standard Chartered acquires Union BankStandard Chartered PLC announced on Tuesday that its subsidiary company, Standard Chartered Bank (Pakistan) Limited, has completed the acquisition of 95.37 per cent interest in Union Bank Ltd.

The bank said it had paid an amount of $487 million for the purchase of Union Bank.

Standard Chartered Bank submitted a scheme of amalgamation to the State Bank of Pakistan. On approval, Union Bank and Standard Chartered Bank would amalgamate into Standard Chartered Bank (Pakistan) Ltd, said a press release issued by the bank.

The release said Union Bank provided Standard Chartered with a significant opportunity for growth in both consumer and wholesale banking through product innovation, wider distribution reach and leveraging Standard Chartered’s international network.

”Our overriding priority will be to ensure that we maintain the highest standards of service for our customers. For customers of both banks, it will be business as usual until further notice,” said the release.

Badar Kazmi, chief executive officer, Standard Chartered Pakistan, said in a statement: “I am delighted with the completion of the acquisition of Union Bank Limited. The merger with Union Bank demonstrates Standard Chartered’s commitment to Pakistan and presents tremendous opportunities. This acquisition is transformational for Standard Chartered in Pakistan. It will be beneficial for the customers in terms of our ability to provide value-added sophisticated products and services that match our customers’ needs.”

“It will also provide a strong platform for personal and professional development and growth to all staff across the bank,” he added.

18