deltek insight 2012: accounting for unallowable costs

TRANSCRIPT

Accounting for Unallowable Costs

Stephanie Widzinski, Sr. Manager, Watkins MeeganKiran Pinto, Manager, Watkins MeeganGC-175

2 ©2012 Deltek, Inc. All Rights Reserved

The Regulations

The “Unallowable” Concept

Basic Cost Principles and Unallowable Costs

How to properly account for Unallowable Cost in GCS Premier

Agenda

3 ©2012 Deltek, Inc. All Rights Reserved

Proper segregation of unallowable cost

Proper treatment in your indirect rate structure

Compliance with regulations

Key Take Aways

Basic Cost Principles – The Regulations

5 ©2012 Deltek, Inc. All Rights Reserved

FAR 31.201-6, Accounting for Unallowable Costs Certain costs may be allocable, but not allowable Introduces the concept of statistical sampling for quantification of

unallowables Introduces the concept of directly associated unallowable costs

FAR 31.2 – Contracts with Commercial Organizations

6 ©2012 Deltek, Inc. All Rights Reserved

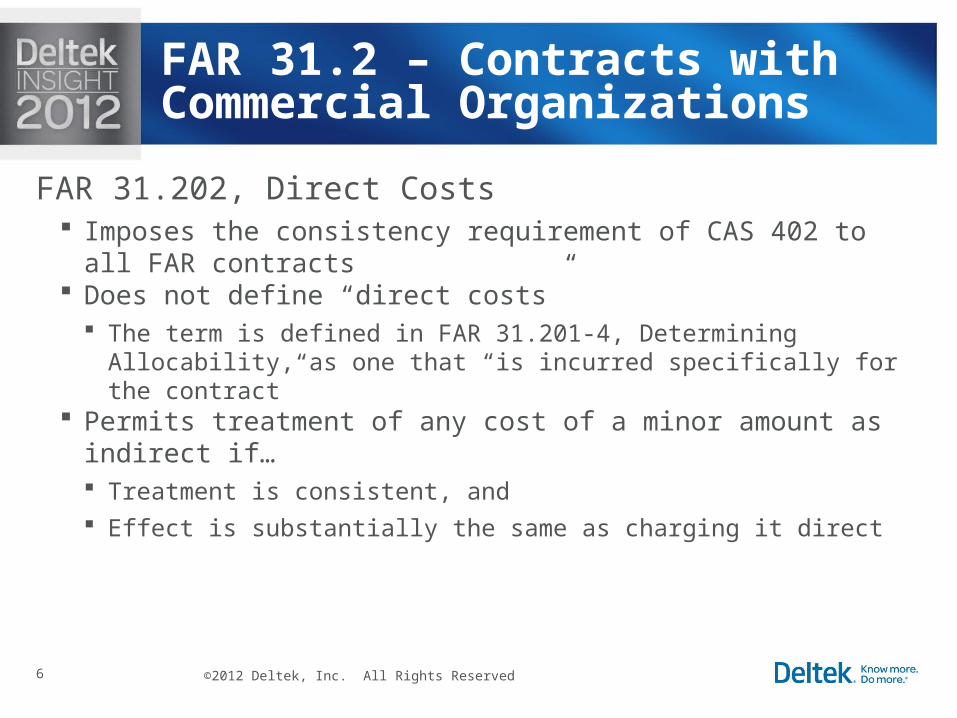

FAR 31.202, Direct Costs Imposes the consistency requirement of CAS 402 to all FAR contracts Does not define “direct costs”

The term is defined in FAR 31.201-4, Determining Allocability, as one that “is incurred specifically for the contract”

Permits treatment of any cost of a minor amount as indirect if… Treatment is consistent, and Effect is substantially the same as charging it direct

FAR 31.2 – Contracts with Commercial Organizations

7 ©2012 Deltek, Inc. All Rights Reserved

FAR 31.203, Indirect Costs Defers to CAS for covered contracts For all other contracts

Defines indirect as everything not direct (even unallowables) Mandates pool formation in logical, homogeneous cost groupings Established requirement for causal/beneficial relationship Prohibits fragmentation of pool bases Acknowledges need for “offsite” pools for some contractors Requires pools to be allocated over contractor’s fiscal year (with some

exceptions) Encourages use of “special allocations” (exception to G&A base) for GOCOs Establishes “excessive pass-through charges” as unallowable

FAR 31.2 – Contracts with Commercial Organizations

8 ©2012 Deltek, Inc. All Rights Reserved

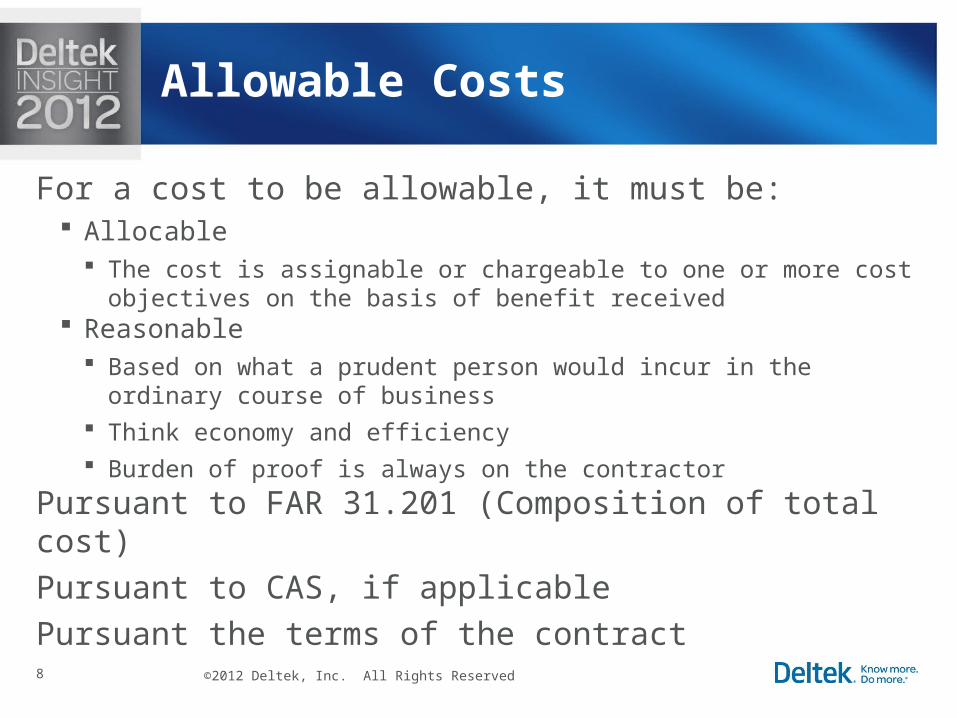

For a cost to be allowable, it must be: Allocable

The cost is assignable or chargeable to one or more cost objectives on the basis of benefit received

Reasonable Based on what a prudent person would incur in the ordinary course of

business Think economy and efficiency Burden of proof is always on the contractor

Pursuant to FAR 31.201 (Composition of total cost)

Pursuant to CAS, if applicable

Pursuant the terms of the contract

Allowable Costs

9 ©2012 Deltek, Inc. All Rights Reserved

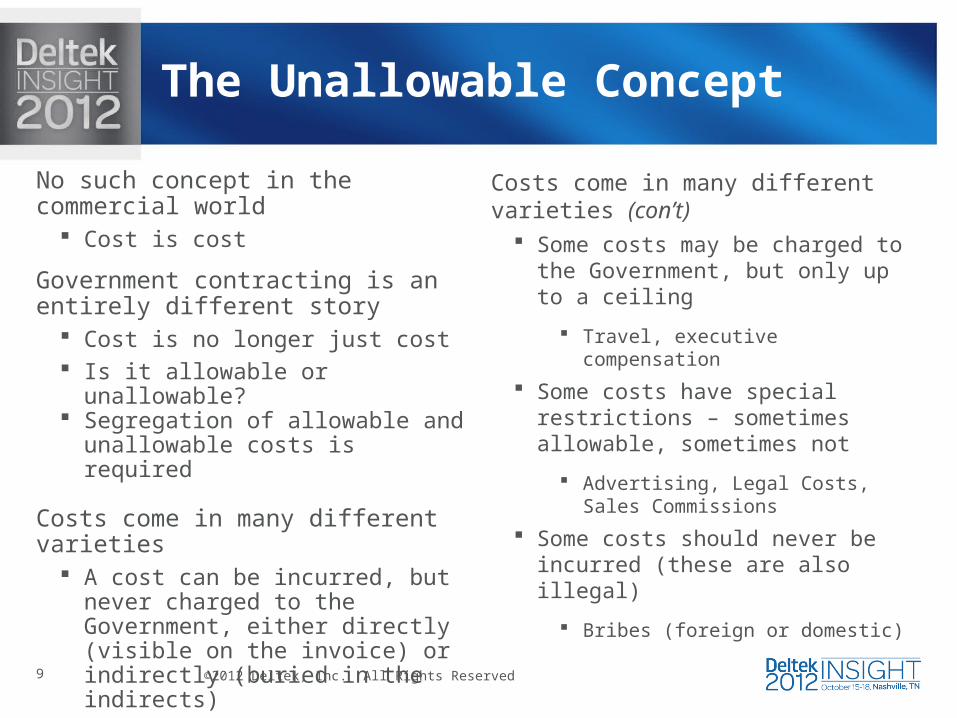

No such concept in the commercial world

Cost is cost

Government contracting is an entirely different story

Cost is no longer just cost Is it allowable or unallowable? Segregation of allowable and

unallowable costs is required

Costs come in many different varieties A cost can be incurred, but never

charged to the Government, either directly (visible on the invoice) or indirectly (buried in the indirects)

Interest, Alcohol, Entertainment, etc.

Costs come in many different varieties (con’t)

Some costs may be charged to the Government, but only up to a ceiling

Travel, executive compensation

Some costs have special restrictions – sometimes allowable, sometimes not

Advertising, Legal Costs, Sales Commissions

Some costs should never be incurred (these are also illegal)

Bribes (foreign or domestic)

The Unallowable Concept

10 ©2012 Deltek, Inc. All Rights Reserved

Unallowable costs are a cost of doing business, you just can’t charge the government for them

Some costs are unallowable by their nature (by law or regulation)

Bribes, gifts, and donations Alcoholic beverages, entertainment Interest Federal income taxes Allowance for bad debt

Some costs are intended to regulate or control costs Excess travel costs Excess executive compensation Business combination costs

The Legal Basis for Unallowable Cost

11 ©2012 Deltek, Inc. All Rights Reserved

Everyone in your organization should care

There are penalties for not caring

Unallowable cost might not be on your radar, but it is on the radar of DCAA

Who Really Cares about Unallowable Cost?

12 ©2012 Deltek, Inc. All Rights Reserved

Top Audit Issues for 2011

13 ©2012 Deltek, Inc. All Rights Reserved

Some unallowable costs are unavoidable

Visibility and proper treatment is key Unallowable direct costs stay with the job, receive all appropriate

allocations, but are not billed Unallowable indirect costs (fringe or overhead) must be removed from

their respective pool, but remain in the G&A base Unallowable G&A (and all statutory unallowable costs) are removed

from the G&A pool

Important to remember…one dollar of “directly associated” unallowable costs can become two dollars or more dollars of total unallowable costs to your company

If not for cost “A,” cost “B” would not have been incurred

Treatment of Unallowable Cost

14 ©2012 Deltek, Inc. All Rights Reserved

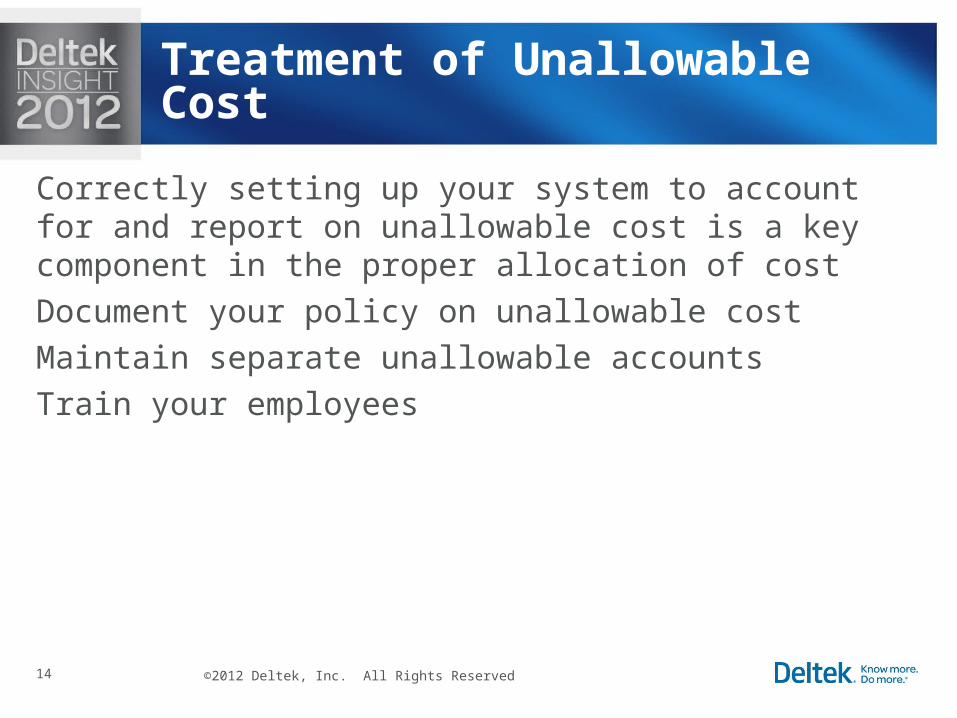

Correctly setting up your system to account for and report on unallowable cost is a key component in the proper allocation of cost

Document your policy on unallowable cost

Maintain separate unallowable accounts

Train your employees

Treatment of Unallowable Cost

GCS Premier and Unallowable Cost

Setup and Treatment

16 ©2012 Deltek, Inc. All Rights Reserved

Unallowable cost can come in all shapes and sizes Direct Labor, ODC’s, Overhead & G&A

Each is treated differently in government contracting

And each requires a different setup in your system

It is important to understand how your unallowable cost should be recorded

Unallowable Cost and GCS

17 ©2012 Deltek, Inc. All Rights Reserved

What to consider when setting up and capturing unallowable cost:

A separate and distinct numbering scheme for unallowable accounts Do I have both direct and indirect unallowable cost? What types of unallowable cost will be incurred?

Labor and non-labor Will you have unallowable G&A cost?

Should the unallowable cost be in the base of the G&A pool?

Unallowable Cost and GCS

Direct Cost

Unallowable/Non billable

19 ©2012 Deltek, Inc. All Rights Reserved

Two basic options to consider for the recording of direct unallowable (non billable) cost

If you only have unallowable/non billable ODC’s, a separate SFX will segregate those costs

If you have unallowable/non billable labor (less likely), you will need to set up a separate task under your contract

Direct Unallowable Cost

20 ©2012 Deltek, Inc. All Rights Reserved

Unallowable and non-billable mean the same thing for our discussion

These are costs that belong to the job but cannot be billed or included in revenue

Think excess per diem….

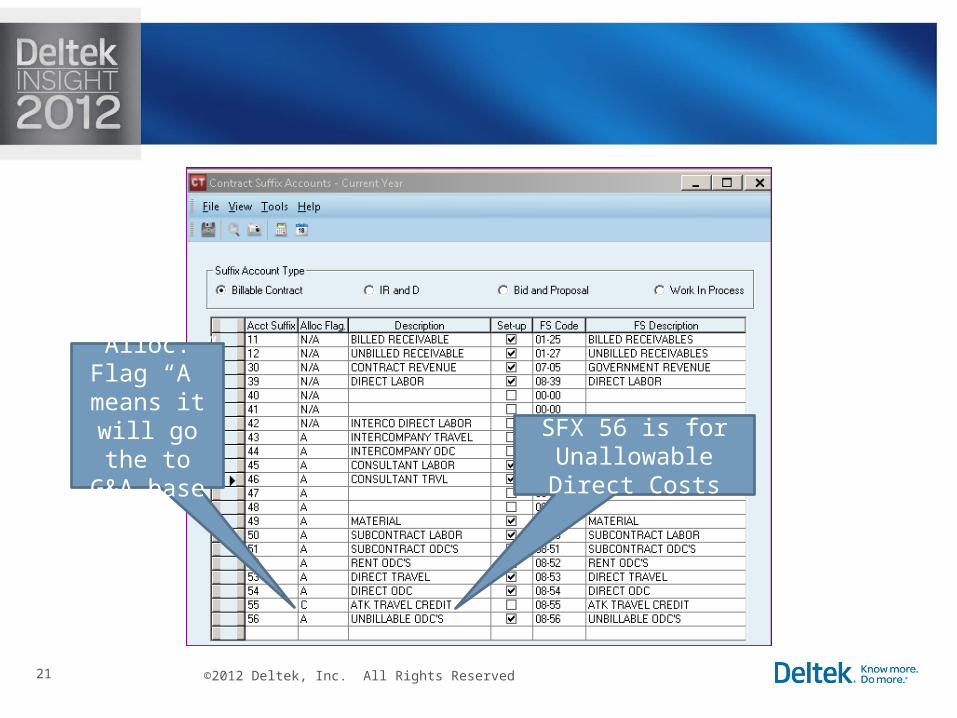

Set up a separate suffix to capture the cost For example, SFX 56 Non Billable Expense

Unallowable ODC

21 ©2012 Deltek, Inc. All Rights Reserved

Alloc. Flag “A” means it will go the to G&A base

SFX 56 is for Unallowable Direct

Costs

22 ©2012 Deltek, Inc. All Rights Reserved

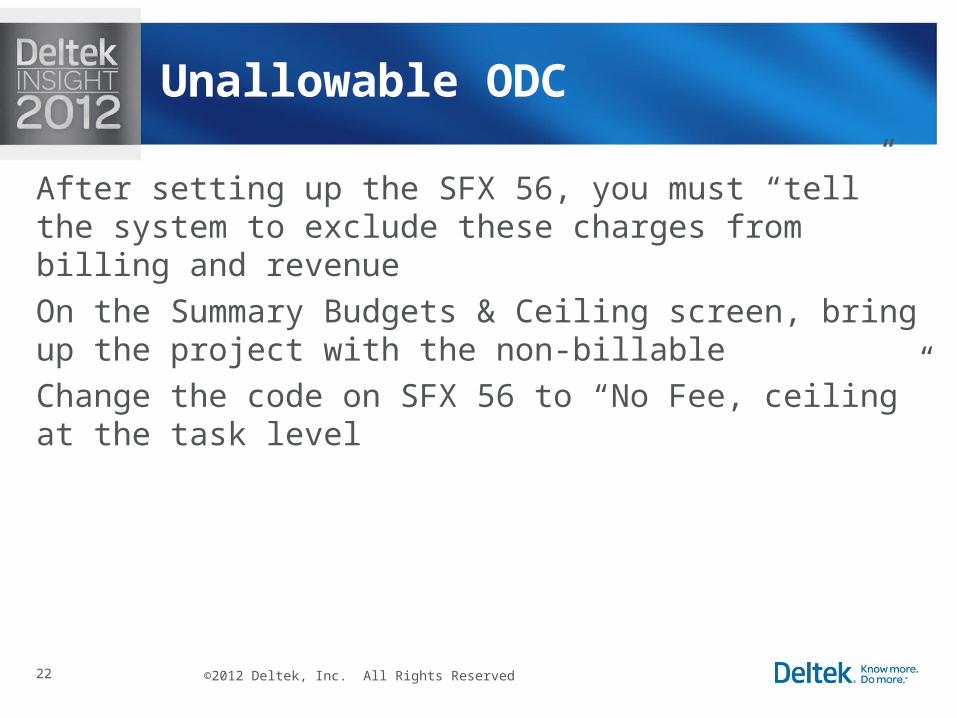

After setting up the SFX 56, you must “tell” the system to exclude these charges from billing and revenue

On the Summary Budgets & Ceiling screen, bring up the project with the non-billable

Change the code on SFX 56 to “No Fee, ceiling” at the task level

Unallowable ODC

23 ©2012 Deltek, Inc. All Rights Reserved

24 ©2012 Deltek, Inc. All Rights Reserved

This screen is automatically set up. This is where you can

manage ceilings. Change default code

25 ©2012 Deltek, Inc. All Rights Reserved

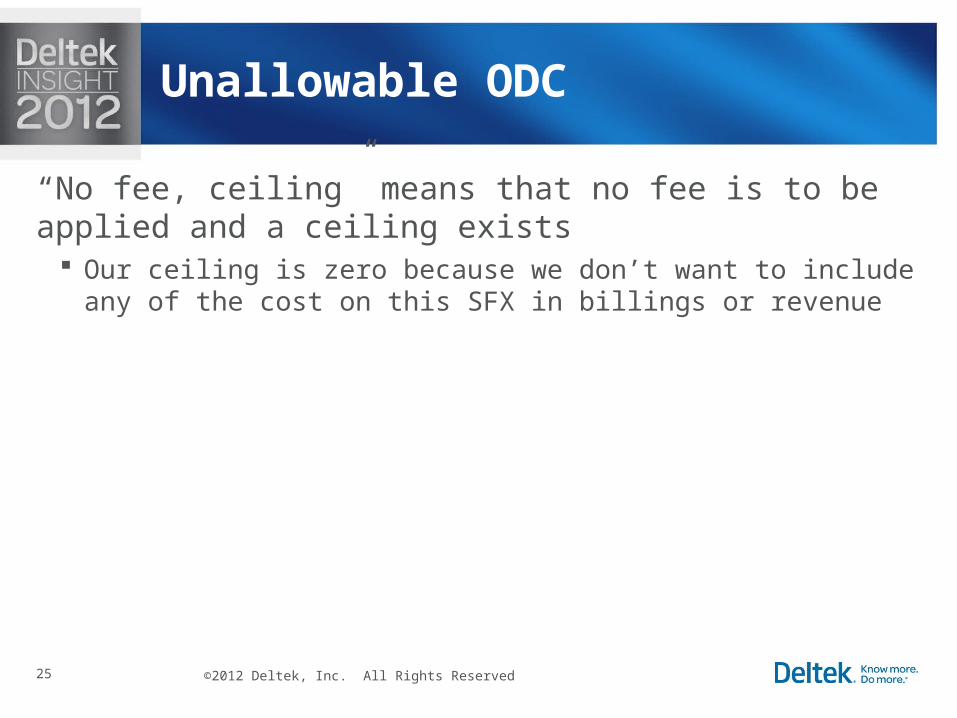

“No fee, ceiling” means that no fee is to be applied and a ceiling exists

Our ceiling is zero because we don’t want to include any of the cost on this SFX in billings or revenue

Unallowable ODC

26 ©2012 Deltek, Inc. All Rights Reserved

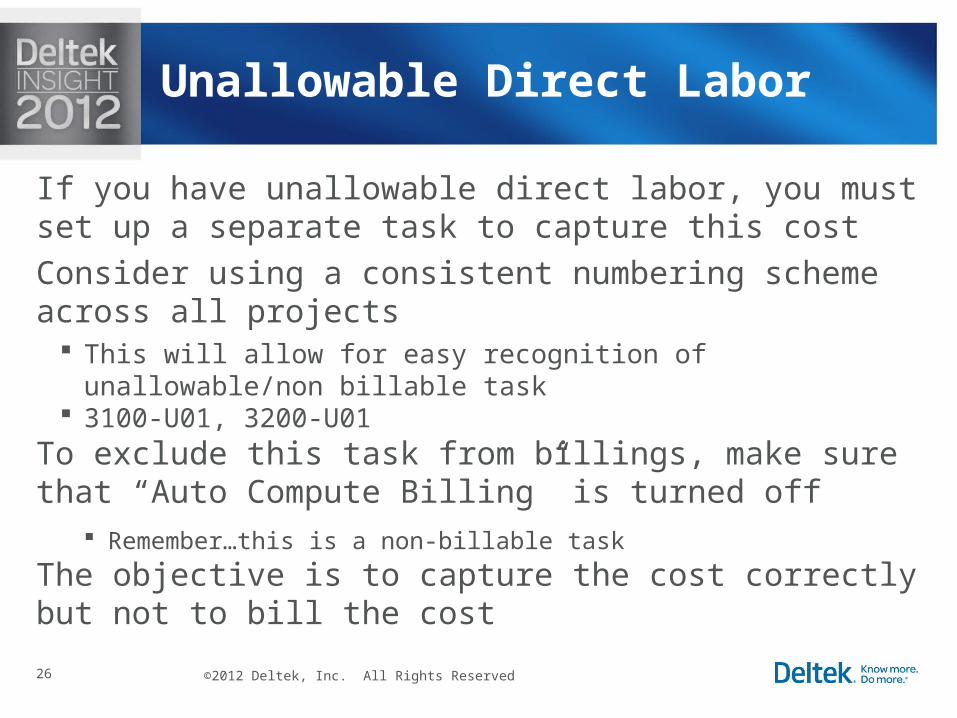

If you have unallowable direct labor, you must set up a separate task to capture this cost

Consider using a consistent numbering scheme across all projects

This will allow for easy recognition of unallowable/non billable task 3100-U01, 3200-U01

To exclude this task from billings, make sure that “Auto Compute Billing” is turned off

Remember…this is a non-billable task

The objective is to capture the cost correctly but not to bill the cost

Unallowable Direct Labor

27 ©2012 Deltek, Inc. All Rights Reserved

This would also be a non-revenue generating task Leave the Automatically compute this contract’s revenue checkbox

blank

Remember, you need to capture/segregate the cost so that is it not billed and does not generates revenue

It is, however, a cost to the project Remember non-billable (unallowable) cost on a project dilutes your

profit

Unallowable Direct Labor

28 ©2012 Deltek, Inc. All Rights Reserved

In the Contract Master File, uncheck the “auto

compute” box

29 ©2012 Deltek, Inc. All Rights Reserved

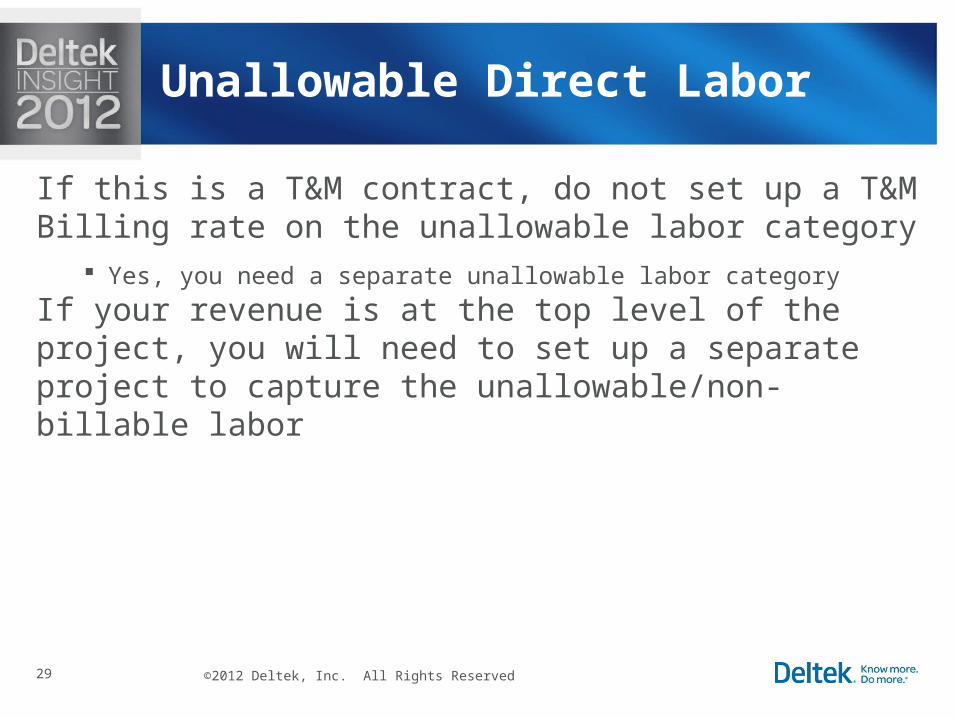

If this is a T&M contract, do not set up a T&M Billing rate on the unallowable labor category

Yes, you need a separate unallowable labor category

If your revenue is at the top level of the project, you will need to set up a separate project to capture the unallowable/non-billable labor

Unallowable Direct Labor

Indirect Cost

Unallowable Set Up

31 ©2012 Deltek, Inc. All Rights Reserved

Unallowable indirect cost can be either labor or non-labor

Unallowable expense can result from an Overhead activity or from a G&A activity

The origin of the expense will determine how it should be handled in the system

The goal is to properly treat your unallowable cost so that the government is not being allocated any unallowable cost

Unallowable Indirect Cost

32 ©2012 Deltek, Inc. All Rights Reserved

Recording unallowable cost to separately identified unallowable accounts will result in the most visible and accurate portrayal of the cost

To properly set up your system for unallowable cost, you must understand the flow of the cost and all related burdens

If you incur unallowable labor incurred, you will incur unallowable fringe

Who incurred the unallowable expense? This will determine if the expense belongs in the G&A base

Was it part of the Overhead pool? Was it a G&A type expense?

Unallowable Indirect Cost

33 ©2012 Deltek, Inc. All Rights Reserved

Costs that would be normally included in overhead, but by their nature are unallowable, should be excluded from the Overhead pool(s)

Excess per diem on indirect travel Alcohol at a business meeting

The unallowable “Overhead” cost should be included in the G&A base

The result is a lower overhead rate

Contracts cannot be burdened with unallowable overhead cost

Unallowable G&A costs must also be removed from the G&A pool

These costs should also be excluded from the G&A base

Unallowable Indirect Cost

34 ©2012 Deltek, Inc. All Rights Reserved

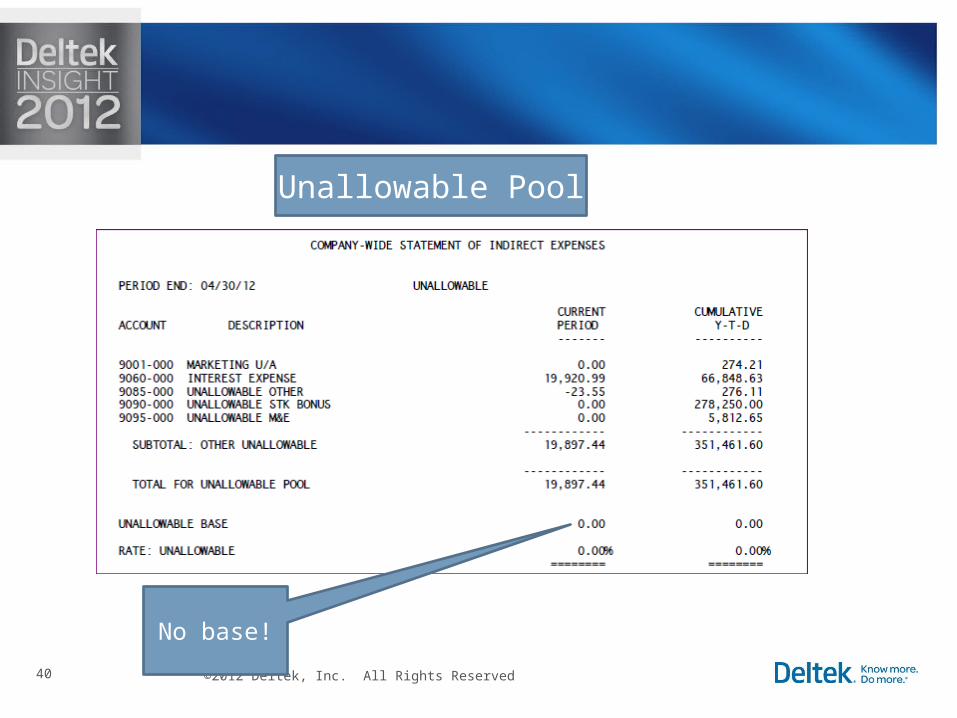

To properly account for unallowable cost, your indirect pool structure should include a separate pool for unallowable costs

This pool will not have a base

This pool will not allocate to projects

The purpose of the pool is accumulate unallowable cost so that cost can be properly included in your G&A base and properly excluded from other pools

How to Capture Unallowable Cost in GCS

35 ©2012 Deltek, Inc. All Rights Reserved

The pool will contain all labor and non-labor expense related unallowable cost, including the allocation of fringe on the unallowable labor

Unallowable labor needs to be included in the base of your fringe pool

How to Capture Unallowable Cost in GCS

36 ©2012 Deltek, Inc. All Rights Reserved

All unallowable accounts must be assigned to the unallowable pool

The unallowable labor account must have an account type of “L” so that it will properly be included in the base of the fringe pool

Allocation accounts must be set up

A base assigned

After the pool is set up, go to the chart of accounts file to modify each record to assign to the pool

Setting Up the Pool

37 ©2012 Deltek, Inc. All Rights Reserved

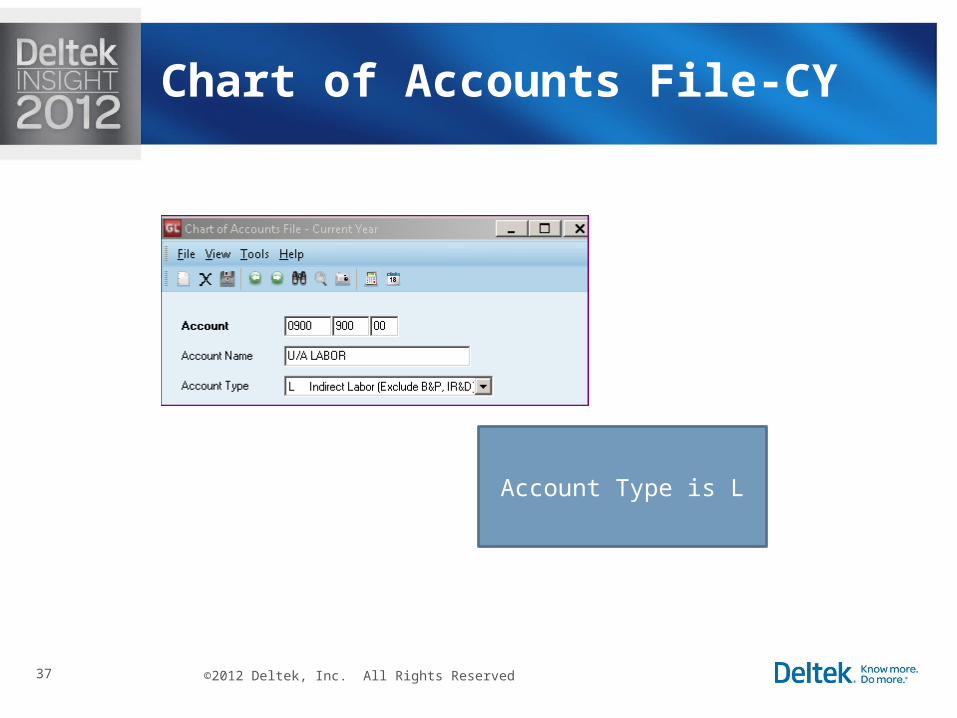

Chart of Accounts File-CY

Account Type is L

38 ©2012 Deltek, Inc. All Rights Reserved

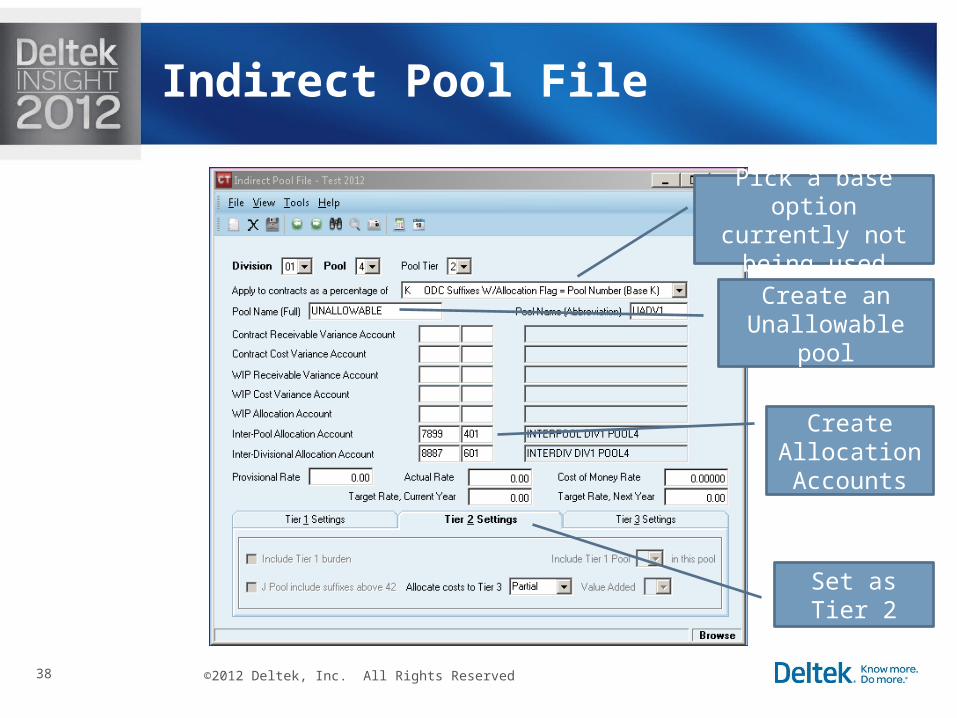

Indirect Pool File

Pick a base option currently not being

used

Create an Unallowable pool

Create Allocation Accounts

Set as Tier 2

39 ©2012 Deltek, Inc. All Rights Reserved

Chart of Accounts

40 ©2012 Deltek, Inc. All Rights Reserved

Unallowable Pool

No base!

41 ©2012 Deltek, Inc. All Rights Reserved

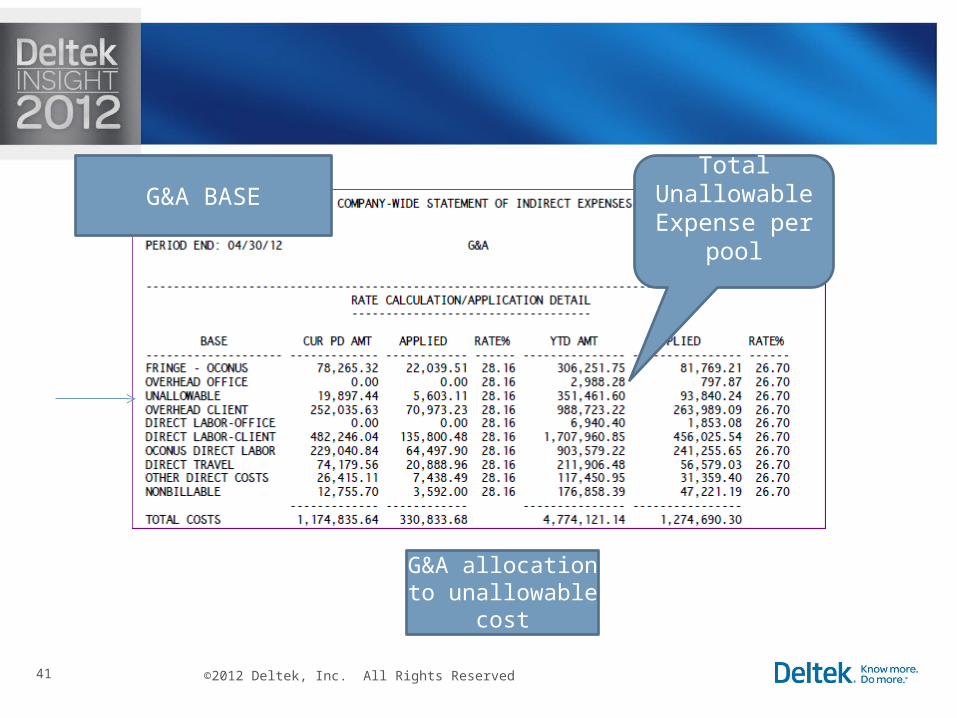

Total Unallowable Expense per

pool

G&A allocation to unallowable cost

G&A BASE

42 ©2012 Deltek, Inc. All Rights Reserved

Knowingly including unallowable direct costs in a public voucher submitted to the Government for payment is a violation of the False Claims Act (31 USC §§ 3729 – 3733)

The act states, in part, “those who knowingly submit, or cause another person or entity to submit, false claims for payment of government funds are liable for three times the government’s damages plus civil penalties of $5,500 to $11,000 per false claim”

Each invoice is considered a separate claim

Knowingly including unallowable costs in an Incurred Cost Submission (a “claim” for final settlement of indirect rates for a year) is also a violation of the False Claims Act

The Consequences of Ignoring Unallowable Cost

43 ©2012 Deltek, Inc. All Rights Reserved

Unallowable costs in an indirect claim are also subject to a penalty pursuant to FAR

Penalty amount is equal to “two times the disallowed costs, plus interest”

Penalty is in addition to False Claims Act provisions and disallowed costs

Can be waived upon a showing that the inclusion was inadvertent Absent such showing, the ACO is required to assess the penalty

Each voucher or payment is considered a separate violation

The Consequences of Ignoring Unallowable Cost – continued

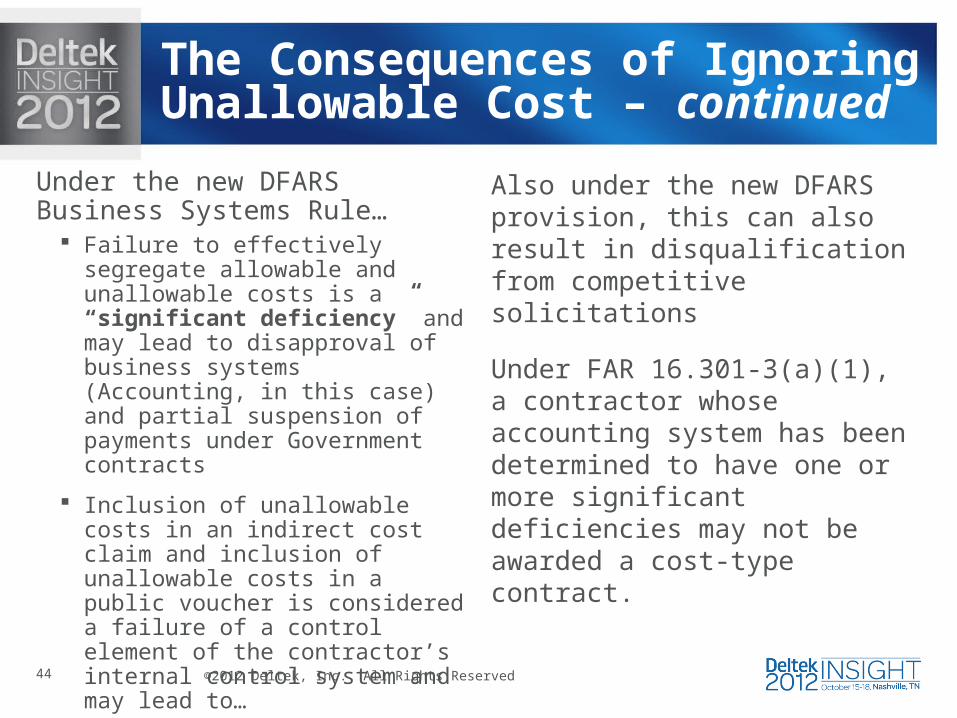

44 ©2012 Deltek, Inc. All Rights Reserved

Under the new DFARS Business Systems Rule…

Failure to effectively segregate allowable and unallowable costs is a “significant deficiency” and may lead to disapproval of business systems (Accounting, in this case) and partial suspension of payments under Government contracts

Inclusion of unallowable costs in an indirect cost claim and inclusion of unallowable costs in a public voucher is considered a failure of a control element of the contractor’s internal control system and may lead to…

Disapproval of one or more business systems

Also under the new DFARS provision, this can also result in disqualification from competitive solicitations

Under FAR 16.301-3(a)(1), a contractor whose accounting system has been determined to have one or more significant deficiencies may not be awarded a cost-type contract.

The Consequences of Ignoring Unallowable Cost – continued

45 ©2012 Deltek, Inc. All Rights Reserved

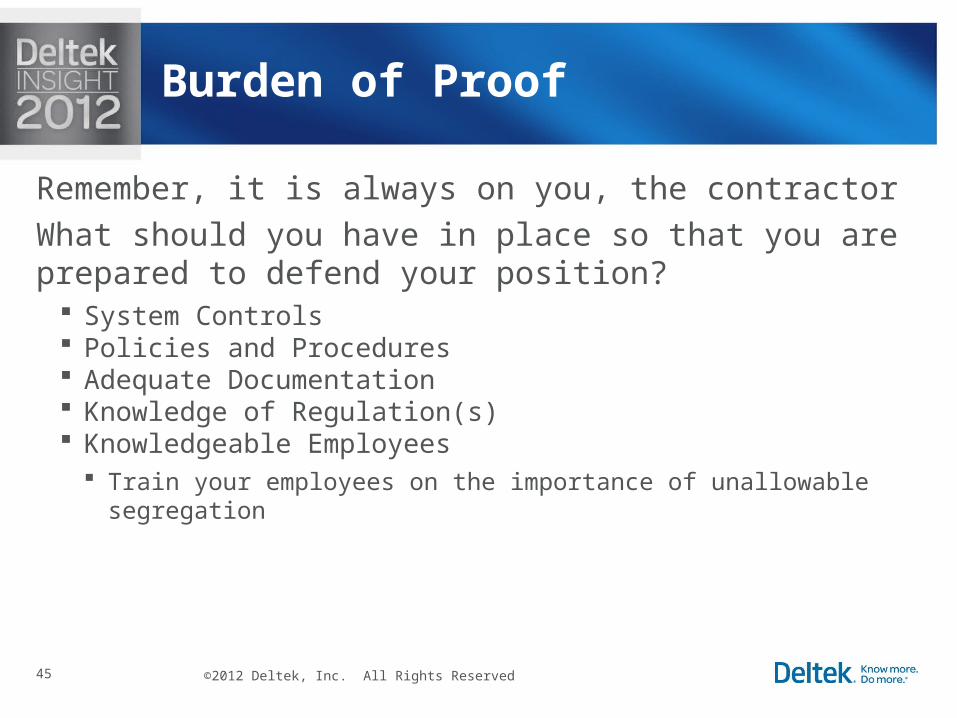

Remember, it is always on you, the contractor

What should you have in place so that you are prepared to defend your position?

System Controls Policies and Procedures Adequate Documentation Knowledge of Regulation(s) Knowledgeable Employees

Train your employees on the importance of unallowable segregation

Burden of Proof

46 ©2012 Deltek, Inc. All Rights Reserved

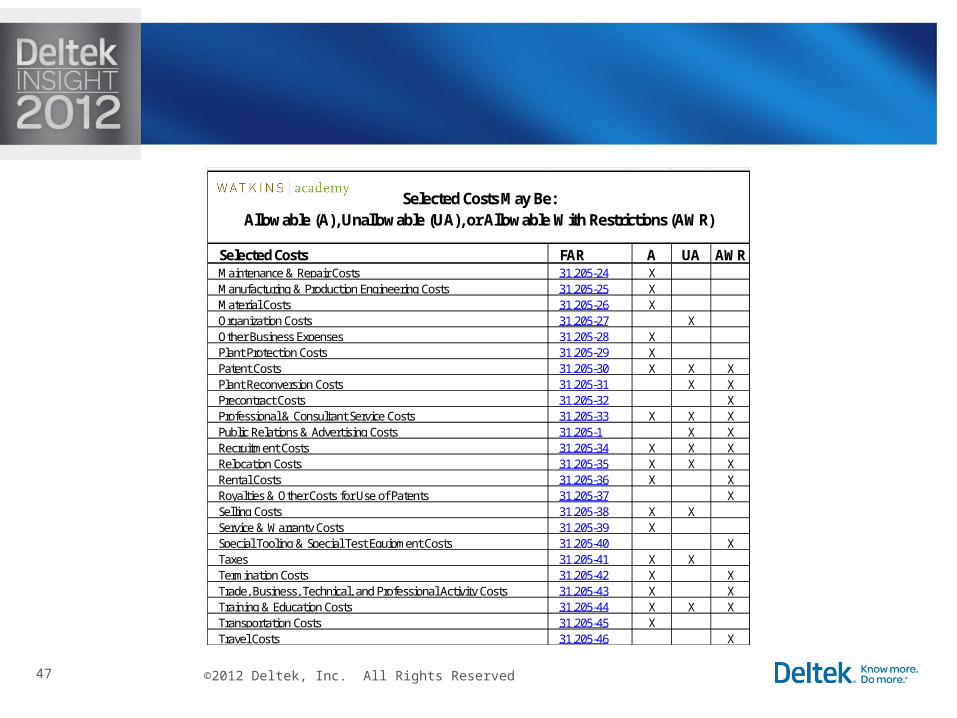

Selected Costs FAR A UA AWRAlcoholic Beverages 31.205-51 XAsset Valuations Resulting from Business Combinations 31.205-52 XBad Debts 31.205-3 XBonding Costs 31.205-4 XCompensation for Personal Services 31.205-6 X X XContingencies 31.205-7 X XContributions or Donations 31.205-8 XCost of Money 31.205-10 XDeferred Research & Development Costs 31.205-48 X XDepreciation 31.205-11 XEconomic Planning Costs 31.205-12 X XEmployee Morale, Health, Welfare, Food Service, & Dorm Costs 31.205-13 X XEntertainment Costs 31.205-14 XFines, Penalties, & Mischarging Costs 31.205-15 X XGains & Losses on Disposition of Assets 31.205-16 XGoodwill 31.205-49 XIdle Facilities & Idle Capacity Costs 31.205-17 X XIndependent Research & Development/ Bid & Proposal Costs 31.205-18 X XInsurance & Indemnification 31.205-19 X X XInterest & Other Financial Costs 31.205-20 X XLabor Relations Costs 31.205-21 XLegal & Other Proceedings Costs 31.205-47 X XLobbying and Political Activity Costs 31.205-22 XLosses on Other Contracts 31.205-23 X

Selected Costs May Be:Allowable (A), Unallowable (UA), or Allowable With Restrictions (AWR)

47 ©2012 Deltek, Inc. All Rights Reserved

Selected Costs FAR A UA AWRMaintenance & Repair Costs 31.205-24 XManufacturing & Production Engineering Costs 31.205-25 XMaterial Costs 31.205-26 XOrganization Costs 31.205-27 XOther Business Expenses 31.205-28 XPlant Protection Costs 31.205-29 XPatent Costs 31.205-30 X X XPlant Reconversion Costs 31.205-31 X XPrecontract Costs 31.205-32 XProfessional & Consultant Service Costs 31.205-33 X X XPublic Relations & Advertising Costs 31.205-1 X XRecruitment Costs 31.205-34 X X XRelocation Costs 31.205-35 X X XRental Costs 31.205-36 X XRoyalties & Other Costs for Use of Patents 31.205-37 XSelling Costs 31.205-38 X XService & Warranty Costs 31.205-39 XSpecial Tooling & Special Test Equipment Costs 31.205-40 XTaxes 31.205-41 X XTermination Costs 31.205-42 X XTrade, Business, Technical, and Professional Activity Costs 31.205-43 X XTraining & Education Costs 31.205-44 X X XTransportation Costs 31.205-45 XTravel Costs 31.205-46 X

Selected Costs May Be:Allowable (A), Unallowable (UA), or Allowable With Restrictions (AWR)

48 ©2012 Deltek, Inc. All Rights Reserved

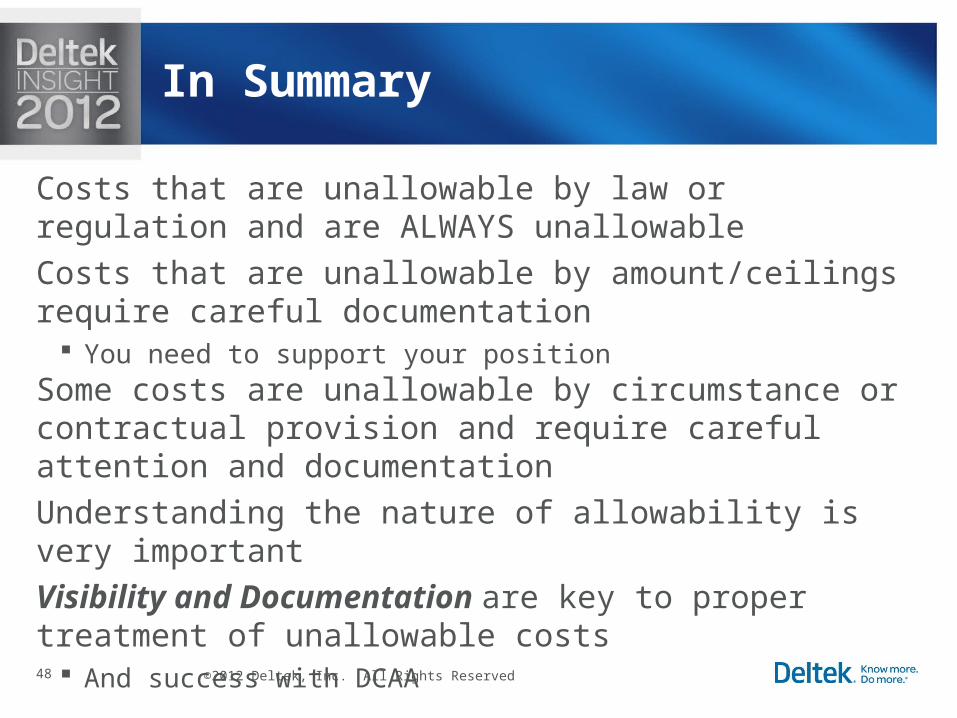

Costs that are unallowable by law or regulation and are ALWAYS unallowable

Costs that are unallowable by amount/ceilings require careful documentation

You need to support your position

Some costs are unallowable by circumstance or contractual provision and require careful attention and documentation

Understanding the nature of allowability is very important

Visibility and Documentation are key to proper treatment of unallowable costs

And success with DCAA

In Summary

49 ©2012 Deltek, Inc. All Rights Reserved

Learn more…

Stephanie Widzinski, CPASenior Manager, Government Contracting [email protected](703) 342-5951

Kiran Pinto, CPA Manager, Government Contracting Group

[email protected](703) 847-4458

Basic Cost Principles – The Regulations

51 ©2012 Deltek, Inc. All Rights Reserved

FAR 31.201-6, Accounting for Unallowable Costs Certain costs may be allocable, but not allowable Introduces the concept of statistical sampling for quantification of

unallowables Introduces the concept of directly associated unallowable costs

FAR 31.2 – Contracts with Commercial Organizations

52 ©2012 Deltek, Inc. All Rights Reserved

FAR 31.202, Direct Costs Imposes the consistency requirement of CAS 402 to all FAR contracts Does not define “direct costs”

The term is defined in FAR 31.201-4, Determining Allocability, as one that “is incurred specifically for the contract”

Permits treatment of any cost of a minor amount as indirect if… Treatment is consistent, and Effect is substantially the same as charging it direct

FAR 31.2 – Contracts with Commercial Organizations

53 ©2012 Deltek, Inc. All Rights Reserved

FAR 31.203, Indirect Costs Defers to CAS for covered contracts For all other contracts

Defines indirect as everything not direct (even unallowables) Mandates pool formation in logical, homogeneous cost groupings Established requirement for causal/beneficial relationship Prohibits fragmentation of pool bases Acknowledges need for “offsite” pools for some contractors Requires pools to be allocated over contractor’s fiscal year (with some

exceptions) Encourages use of “special allocations” (exception to G&A base) for GOCOs Establishes “excessive pass-through charges” as unallowable

FAR 31.2 – Contracts with Commercial Organizations

Thank You!

Overview of Selected Cost Principles

56 ©2012 Deltek, Inc. All Rights Reserved

Allowable costs are limited to: (1) Memberships in trade, business, technical and professional orgs.

(subject to limitations); (2) Subscriptions to trade, business, professional, or other technical

periodicals; (3) When the principal purpose of a meeting, conference or seminar is

the dissemination of trade, business, technical or professional information or the stimulation of production or improved productivity.

Careful documentation of the purpose of the event is key to establishing allowability

FAR 31.205-43, Trade, Business, Technical & Professional Activity Costs

57 ©2012 Deltek, Inc. All Rights Reserved

Trade, Business, Technical and Professional Activity Costs (FAR 31.205-43) states that the cost of technical or professional meetings and conferences are allowable when the primary purpose of the meeting is the dissemination of trade, business, technical, or professional information, or the stimulation of production or improved productivity, provided the costs meet the other requirements controlling allowability (FAR 31.201-2).

The cost principle makes the following type of professional and technical activity costs expressly allowable:

Organizing, setting up, and sponsoring the technical and professional meetings, symposia, seminars, etc., including rental of meeting facilities, transportation, subsistence, and incidental costs.

Attending the meetings by contractor employees, including travel costs (see FAR 31.205-46)

Attending the meetings by individuals who are not contractor employees, provided the costs are not reimbursed to them by their own employer and their attendance is essential to achieve the purpose of the meetings.

More on Conferences and Seminars… General

58 ©2012 Deltek, Inc. All Rights Reserved

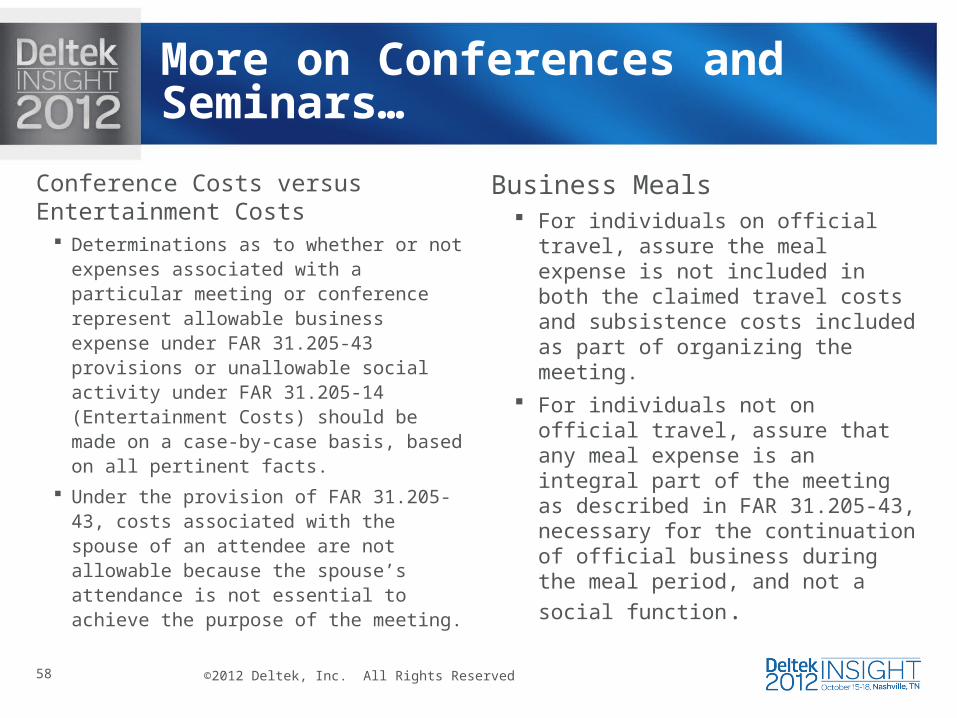

Conference Costs versus Entertainment Costs

Determinations as to whether or not expenses associated with a particular meeting or conference represent allowable business expense under FAR 31.205-43 provisions or unallowable social activity under FAR 31.205-14 (Entertainment Costs) should be made on a case-by-case basis, based on all pertinent facts.

Under the provision of FAR 31.205-43, costs associated with the spouse of an attendee are not allowable because the spouse’s attendance is not essential to achieve the purpose of the meeting.

Business Meals For individuals on official travel, assure

the meal expense is not included in both the claimed travel costs and subsistence costs included as part of organizing the meeting.

For individuals not on official travel, assure that any meal expense is an integral part of the meeting as described in FAR 31.205-43, necessary for the continuation of official business during the meal period, and not a social

function.

More on Conferences and Seminars…

59 ©2012 Deltek, Inc. All Rights Reserved

Documentation Determination of allowability requires knowledge concerning the purpose and

nature of activity at the meeting or conference. The contractor should maintain adequate records supplying the following information on properly prepared travel vouchers or expense records supported by copies of paid invoices, receipts, charge slips, etc. Date and location of meeting, including the name of the establishment. Names of employees and guests in attendance. Purpose of meeting or Agenda. Cost of the meeting, by item.

The above guidelines closely parallel the current record-keeping requirements in Section 274 of the Internal Revenue Code for entertainment costs as a tax deductible expense. Where satisfactory support assuring the claimed costs are allowable conference expenses is not furnished, the claimed conference/meal costs and directly associated costs should be questioned.

More on Conferences and Seminars…

60 ©2012 Deltek, Inc. All Rights Reserved

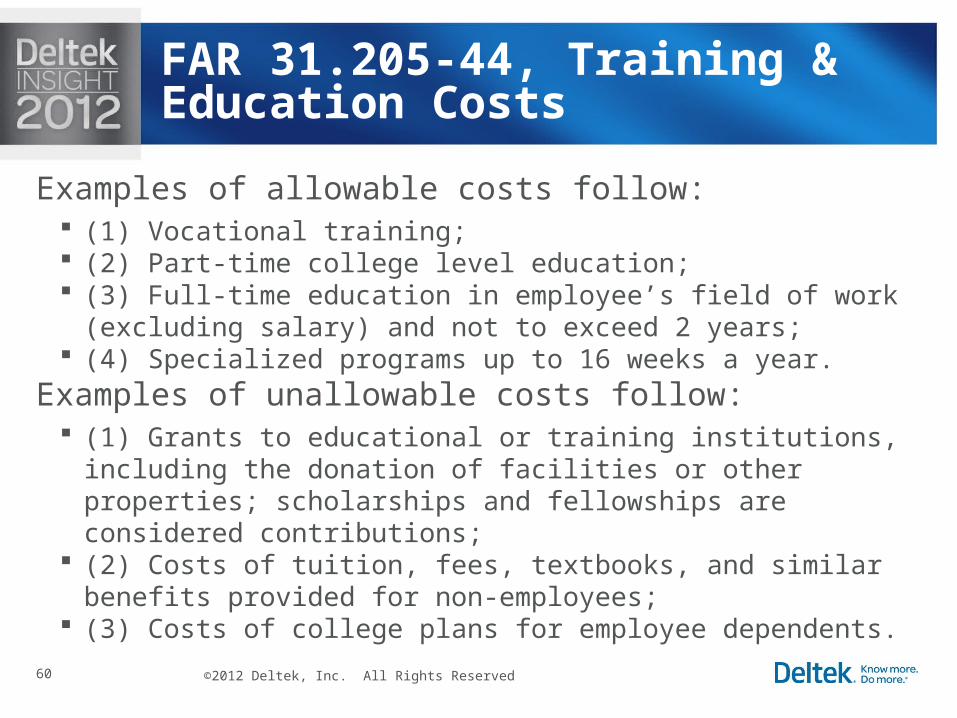

Examples of allowable costs follow: (1) Vocational training; (2) Part-time college level education; (3) Full-time education in employee’s field of work (excluding salary)

and not to exceed 2 years; (4) Specialized programs up to 16 weeks a year.

Examples of unallowable costs follow: (1) Grants to educational or training institutions, including the donation

of facilities or other properties; scholarships and fellowships are considered contributions;

(2) Costs of tuition, fees, textbooks, and similar benefits provided for non-employees;

(3) Costs of college plans for employee dependents.

FAR 31.205-44, Training & Education Costs

61 ©2012 Deltek, Inc. All Rights Reserved

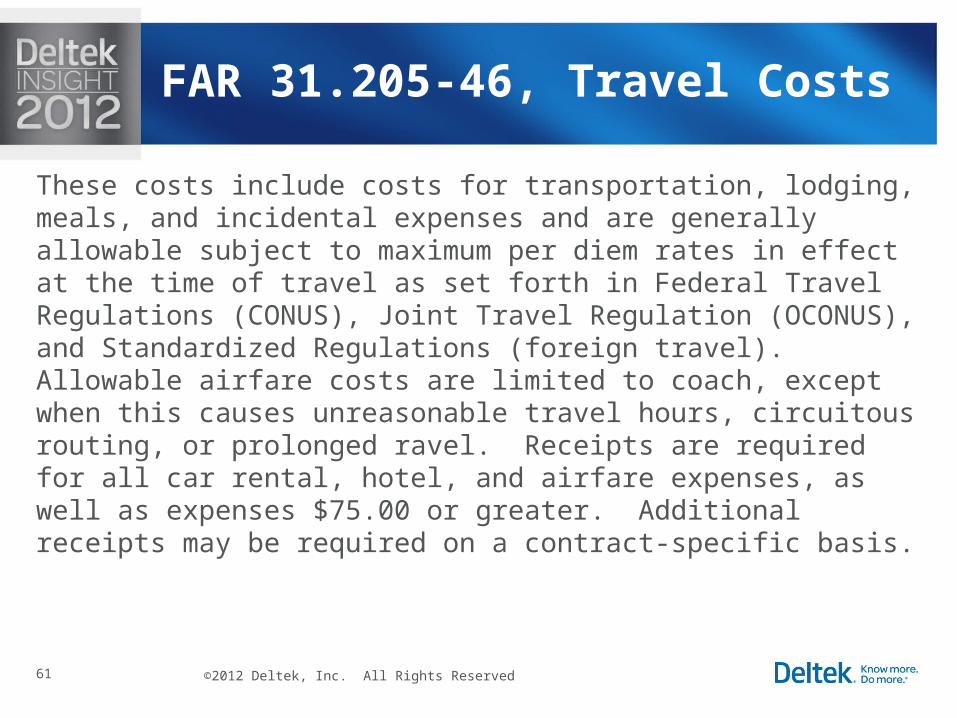

These costs include costs for transportation, lodging, meals, and incidental expenses and are generally allowable subject to maximum per diem rates in effect at the time of travel as set forth in Federal Travel Regulations (CONUS), Joint Travel Regulation (OCONUS), and Standardized Regulations (foreign travel). Allowable airfare costs are limited to coach, except when this causes unreasonable travel hours, circuitous routing, or prolonged ravel. Receipts are required for all car rental, hotel, and airfare expenses, as well as expenses $75.00 or greater. Additional receipts may be required on a contract-specific basis.

FAR 31.205-46, Travel Costs

62 ©2012 Deltek, Inc. All Rights Reserved

Substantiating documentation must be maintained if you are taking one of the exceptions in FAR 31.205-46(b).

Substantiating documentation should take the form of quotations from competing airlines or travel service providers.

Instances where only one flight is available may be substantiated by only one quote. Multiple instances of single quotes should be questioned by the auditor to determine if policies and procedures result in possible unreasonable airfare costs.

31.205-46, Lowest Cost Airfare

63 ©2012 Deltek, Inc. All Rights Reserved

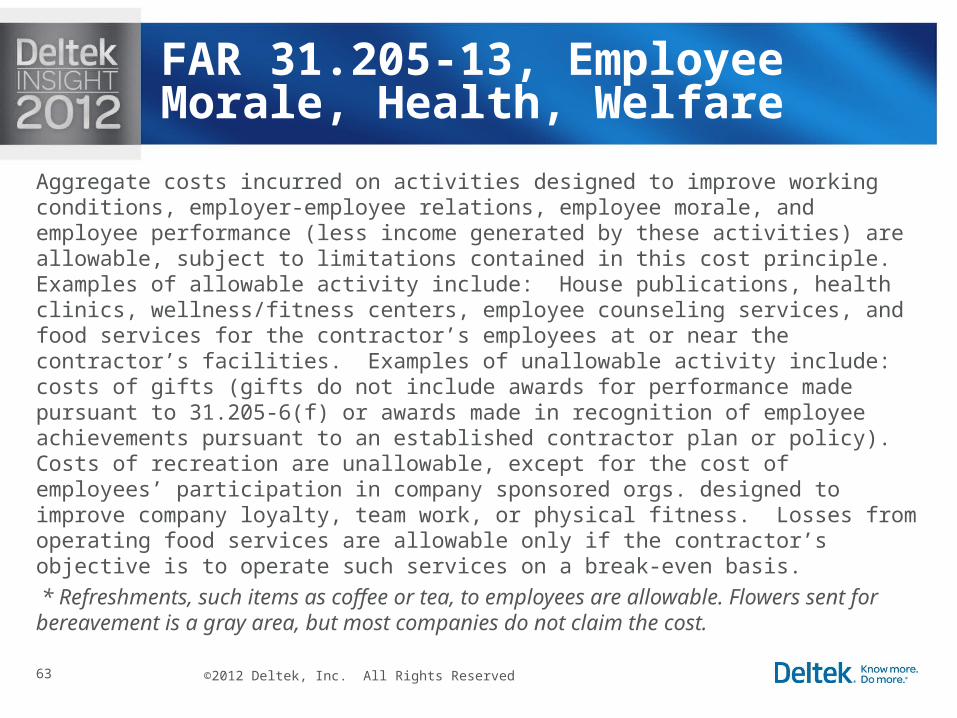

Aggregate costs incurred on activities designed to improve working conditions, employer-employee relations, employee morale, and employee performance (less income generated by these activities) are allowable, subject to limitations contained in this cost principle. Examples of allowable activity include: House publications, health clinics, wellness/fitness centers, employee counseling services, and food services for the contractor’s employees at or near the contractor’s facilities. Examples of unallowable activity include: costs of gifts (gifts do not include awards for performance made pursuant to 31.205-6(f) or awards made in recognition of employee achievements pursuant to an established contractor plan or policy). Costs of recreation are unallowable, except for the cost of employees’ participation in company sponsored orgs. designed to improve company loyalty, team work, or physical fitness. Losses from operating food services are allowable only if the contractor’s objective is to operate such services on a break-even basis.

* Refreshments, such items as coffee or tea, to employees are allowable. Flowers sent for bereavement is a gray area, but most companies do not claim the cost.

FAR 31.205-13, Employee Morale, Health, Welfare

64 ©2012 Deltek, Inc. All Rights Reserved

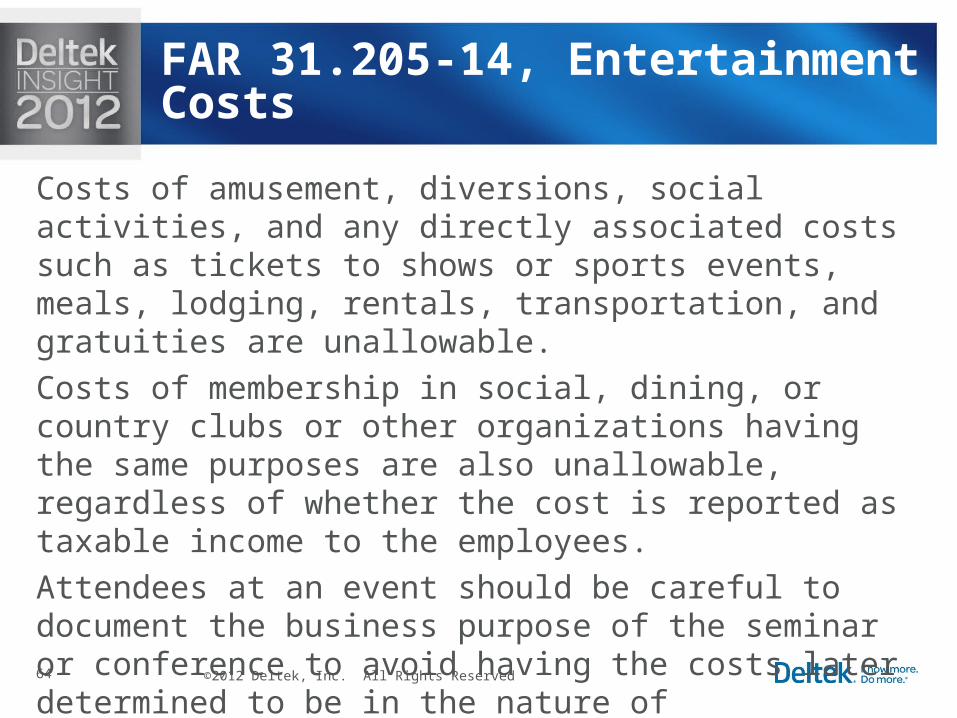

Costs of amusement, diversions, social activities, and any directly associated costs such as tickets to shows or sports events, meals, lodging, rentals, transportation, and gratuities are unallowable.

Costs of membership in social, dining, or country clubs or other organizations having the same purposes are also unallowable, regardless of whether the cost is reported as taxable income to the employees.

Attendees at an event should be careful to document the business purpose of the seminar or conference to avoid having the costs later determined to be in the nature of entertainment.

FAR 31.205-14, Entertainment Costs

65 ©2012 Deltek, Inc. All Rights Reserved

Costs of alcoholic beverages are unallowable

FAR 31.205-51, Costs of Alcoholic Beverages

66 ©2012 Deltek, Inc. All Rights Reserved

Expenditures in connection with: (1) Planning or executing the organization or reorganization of the corporate structure of a business, including mergers and acquisitions; (2) Resisting or planning to resist the reorganization of the corporate structure of a business or a change in the controlling interest in the ownership of a business; and (3) Raising capital (net worth plus long-term liabilities) are unallowable.

*Note: The cost of activities primarily intended to provide compensation will not be considered organizational costs subject to this subsection, but will be governed by 31.205-6. These activities include acquiring stock for (i) Executive bonuses (ii) Employee savings plans, and (iii) Employee stock ownership plans.

FAR 31.205-27, Organization Costs

67 ©2012 Deltek, Inc. All Rights Reserved

The following types of recurring costs are allowable: (a) Registry and transfer charges resulting from changes in ownership

of securities issued by the contractor; (b) Cost of shareholders’ meetings; (c) Normal proxy solicitations; (d) Preparing and publishing reports to shareholders; (e) Preparing and submitting required reports and forms to taxing and

other regulatory bodies; (f) Incidental costs of directors’ and committee meetings; and (g) Other similar costs.

FAR 31.205-28, Other Business Expenses

68 ©2012 Deltek, Inc. All Rights Reserved

Costs of fines and penalties resulting from violations of, or failure of the contractor to comply with federal, state, local, or foreign laws and regulations, are unallowable except when incurred as a result of compliance with specific terms and conditions of the contract or written instructions from the contracting officer.

Costs incurred in connection with, or related to, the mischarging of costs on Gov’t. contracts are unallowable when the costs are caused by, or result from, alteration or destruction of records, or other false or improper charging or recording of costs.

FAR 31.205-15, Fines, Penalties & Mischarging Costs

69 ©2012 Deltek, Inc. All Rights Reserved

Contributions or donations, including cash, property, and services, regardless of recipient, are unallowable, except as previously discussed in the community services portion of cost principle 31.205-1.

FAR 31.205-8, Contributions or Donations

70 ©2012 Deltek, Inc. All Rights Reserved

Public Relations (P.R.) includes activities associated with advertising and customer relations

Allowable P.R. costs include the following: (1) Costs specifically required by contract (Direct) (2) Costs of: (i) Responding to inquiries on company policies and

activities; (ii) Communicating with the public, press, stockholders, creditors and customers; (iii) Conducting general liaison with news media and Gov’t P.R. officers, to the extent that such activities are limited to communication necessary to keep the public informed on matters of public concern such as contract awards, plant closings and openings, employee layoffs, financial information, etc.

(3) Costs of participating in community service activities (e.g., blood bank drives, charity drives, savings bond drives, disaster assistance, etc.)

(4) Costs of plant tours and open houses

FAR 31.205-1, PR and Advertising Costs

71 ©2012 Deltek, Inc. All Rights Reserved

Advertising means the use of media to promote the sale of products/services

The only allowable advertising costs are those that are: Specifically required by contract or that arise from requirements of gov’t

contracts, and that are exclusively for: (i) acquiring scarce items for contract performance; or (ii) disposing of scrap or surplus materials acquired for contract performance.

Costs of activities to promote sales of products normally sold to the U.S. Government, including trade shows, which contain a significant effort to promote exports from the U.S. Note: Such costs do not include the costs of memorabilia (e.g., models, gifts,

and souvenirs), alcoholic beverages, entertainment, and facilities used primarily for entertainment rather than product promotion – unallowable.

And, those costs allowable in accordance with 31.205.34 (Recruitment costs).

FAR 31.205-1, PR and Advertising Costs – (cont.)

72 ©2012 Deltek, Inc. All Rights Reserved

Unallowable P.R. and advertising costs include the following: (1) All P.R. and advertising whose primary purpose is to promote the sale of products or

services by stimulating interest in a product line (except allowable directly selling costs later discussed in 31.205-38) or by disseminating messages calling favorable attention to the contractor for purposes of enhancing the company image to sell the company’s product or services.

(2) All costs of trade shows and other special events which do not contain a significant effort to promote the export sales of products normally sold to the U.S. Gov’t (can be allowable or unallowable).

(3) Costs of sponsoring meetings, conventions, symposia, seminars, and other special events when the principal purpose of the event is other than dissemination of technical information or stimulation of production.

(4) Costs of ceremonies such as: (i) Corporate celebrations; (ii) New product announcements.

(5) Costs of promotional material, motion pictures, videos, brochures, handouts, and other media that are designed to call favorable attention to the contractor.

(6) Costs of souvenirs and other mementos provided to the public or customers. (7) Costs of memberships in civic and community organizations (certain types of

membership fees are allowable, e.g., American Payroll Association).

FAR 31.205-1, PR and Advertising Costs – (cont.)

73 ©2012 Deltek, Inc. All Rights Reserved

In most cases, these cost are unallowable. An example of an allowable cost in this area would be providing technical or factual presentations of information on matters related to contract performance.

Attendees at seminars and conferences should be cautioned to be certain the event is not considered “lobbying.”

FAR 31.205-22, Lobbying and Political Activity Costs