demystifying the fbar

TRANSCRIPT

Demystifying The FBAR

Michael DeBlis III, Esq., LLMPartner

DeBlis Law

Modules• Module I: Deconstructing the FBAR rule (Part I)• Module II: Deconstructing the FBAR rule (Part II)• Module III: Most Commonly Asked Questions About the FBAR• Module IV: IRS Procedures for Ensuring Consistency and

Effectiveness in Administering Civil FBAR Penalties• Module V: Willfulness • Module VI: Beyond the FBAR – Everything You Never Wanted

to Know About All of the Other International Reporting Forms But Must

• Module VII: Challenging the IRS’s Assertion of the Non-willful FBAR Penalty: A New Hope

A Story

• Let me take you back to 1997, the year that Dustin Hoffman won the “Lifetime Achievement Award” at the Golden Globes Award Ceremony.

• After thanking everyone who helped him during his career, he told a story that has a great deal of relevance to this topic.

A Story• The story went something like this:

– “When I was doing a promotional tour for ‘The Graduate,’ I found myself flipping the dials in my hotel room one night. I came upon an interview of the great Russian-American composer, Igor Stravinsky. It caught my eye and after listening to it for a few minutes, I became spell-bounded. The interviewer asked Stravinsky:

– ‘Sir, what is the best moment for you as a composer? Is it when you have finished a newly completed work?

– Stravinsky pondered the question and answered: “ No-no-no, it’s not then.”

– ‘Then, is it when your agent informs you that the piece will be performed at one of the concert halls of the world?’

– ‘No, no, no it is not then either.’

– ‘Then is it on opening night at Carnegie Hall or The Kennedy Center, when the last note has been played and the audience erupts into a standing ovation, is that the best moment?’

– ‘No-no-no. Not then either.’

A Story– ‘Well, sir,’ the interviewer asked: ‘What IS the greatest

moment for you?’

– ‘Vell, I vill tell you. Ven I’m working on my piano in a composition, looking for the melodic phrase that vill carry the movement forward. I vill be sitting at the piano, going: bee-bum; bee-bum; bee-bum.’

– ‘This goes on for hours, days, sometimes even veeks: bee-bum; bee-bum; bee-bum. Then miraculously, it happens: I find the note! That, for me is the moment.’

The Moral of The Story

• Hoffman: “My fellow actors, for me ‘the moment’ is not when I get cast in a major role in a blockbuster movie. The moment is not when I stand before you accepting a lifetime achievement award or even an Oscar. But when I am doing my ‘bee-bums’ to find the inner sole of the person I am portraying. Whether it be Benjamin in ‘The Graduate’ or Ratzo Rizzo in ‘Midnight Cowboy’ or ‘Papillion’, when I come upon the ‘Bee-Bum’ that makes that character work, that for me, ‘is the moment.’”

How It Relates to Tax

• Well, my fellow tax practitioners, the ‘Bee-Bums’ in our profession are not found when we find the answer to a mind-numbing question in the U.S. Tax Code, but instead when we discover a way to translate and simplify it so that it can be understood by a layperson.

• This is the challenge that we face as tax practitioners: taking complicated principles and communicating them clearly and effectively to our clients.

• That is what I am going to attempt to do for you today with the FBAR.

Learning Objectives• Learn the purpose of the FBAR regulations

• Determine who must file the FBAR

• Determine the FBAR filing requirements

• Determine who is exempt from the FBAR filing requirements

• Understand the civil and criminal penalties that may be applicable for not complying with the FBAR filing requirements

The CulpritU.S. Worldwide Taxation

• The U.S. taxes its citizens and residents on their worldwide income, regardless of where it is earned.

• The U.S. is one of the only countries left in the world that still taxes its citizens and residents on their worldwide income. Own a business in Sri Lanka? You must report the profits on a U.S. tax return. Work for a French company in Costa Rica? You must report the earnings on your U.S. tax return. Very simply, U.S. taxpayers must report all of their income, even income earned outside of the United States.

The Culprit

How does U.S. international “double taxation” rear its ugly head?

– When a U.S. citizen or resident derives income or holds assets in another country. Both the U.S. and the foreign country tax the same item of income as their own. And both countries have jurisdiction to tax the same item.

– The main cause of international double taxation is inconsistent sourcing rules in different countries imposing overlapping taxes.

The Culprit

• If it were the norm, double taxation of this sort would stop international economic activity dead in its tracks.

The Culprit

• Recognizing this, the U.S. attempts to mitigate the harsh effects of worldwide taxation in three ways:

– Foreign tax credit (lies at the heart of the system of outbound U.S. taxation);

– Foreign earned income exclusion;– Section 911 exclusion for the personal service income

of nonresident citizens and for nonresident citizens’ housing costs.

The Culprit

• Of these three, the foreign tax credit can unilaterally blunt this quagmire in one fell swoop. It is for this reason that I refer to it as “the equalizer.”

• When foreign tax rates are roughly the same as U.S. tax rates, the combination of worldwide taxation and the foreign tax credit virtually eliminates double taxation entirely.

The Culprit

• What gives the United States the right to tax its citizens on a worldwide basis in the first place? – Not the Internal Revenue Code. – Not legislation passed by Congress.

• Nonetheless, it has long been established that the U.S. Constitution permits the federal government’s worldwide taxation of nonresident U.S. citizens

The Culprit

• Who do we have to thank for that? None other than the U.S. Supreme Court, in a little-known case by the name of, Cook v. Tait, 265 U.S. 47 (1924).

The Culprit

• What is the traditional justification for U.S. worldwide taxation? The “public benefits” stemming from U.S. citizenship

• These include:– Civil rights, – Political rights, and – Social rights.

Two Primary Tax Systems

• There are two primary ways by which a country can exercise jurisdiction to tax:– Worldwide Taxation &– Territorial Tax System

Territorial Tax System

• Under a territorial tax system, taxation is limited to taxation of income or assets located within a country’s borders, no matter who derives it – a citizen, resident, or anyone else.

• It is sometimes referred to as “source-based” taxation.

• Territorial tax systems accommodate other tax systems in the simplest way possible – by not extending their own.

Worldwide Taxation

• Worldwide taxation is based on “political allegiance.” • This system of taxation is premised not on the source

of income or assets but upon the “political allegiance” of the taxpayer who owns the income or assets.

• How a country defines the phrase, “political allegiance” leads to two different types of worldwide taxation: – Citizenship-based (U.S.), and– Residence-based (Canada)

Worldwide Taxation

• Citizenship-based: Taking a unique position, the U.S. defines “political allegiance” as an individual’s citizenship, regardless of his residence.

• Residence-based: Other nations define “political allegiance” for tax purposes on the “basis of residence.” In so doing, they tax an individual’s global income and holdings only if the individual resides in that nation.

Worldwide Taxation

• As the poster-child of residence-based taxation, Canada imposes worldwide taxation on all of its residents without regard to Canadian citizenship.

• “Is the distinction between citizenship-based taxation and residence-based taxation one without a difference?” Or, to use a Shakespearian reference, “Is it much ado about nothing?” No.

Worldwide Taxation

• What is the chief difference between the U.S. system of citizenship-based taxation and the Canadian system of residence-based taxation? – A non-resident Canadian citizen – one who lives

outside of Canada – does not pay Canadian income tax on the income that he earns in the foreign country in which he now resides.

– Instead, he only pays Canadian income tax on the income that is generated in Canada, if any.

Worldwide Taxation

– A non-resident U.S. citizen, on the other hand, must pay U.S. taxes not only on the income that is generated in the United States but also on the income that is generated in the foreign country in which he now resides.

FBAR History

• FBAR stands for “Foreign Bank Account Report.”

• The FBAR is a tool used by the U.S. government to identify persons who may be using foreign financial accounts to break U.S. law.

• Information contained in FBARs can be used to identify or trace funds used for illegal purposes or to identify unreported income maintained or generated abroad.

FBAR History• Contrary to popular belief, the FBAR is not technically

required by the tax code. Instead, it is a creature of the Bank Secrecy Act.

• A once obscure Bank Secrecy Act form, the FBAR was first instituted as a reporting requirement for U.S. persons with overseas accounts.

• Today, the IRS has breathed new life into the FBAR as a tax enforcement and revenue-raising tool. The IRS has administered and enforced the FBAR since 2003.

FBAR Rule

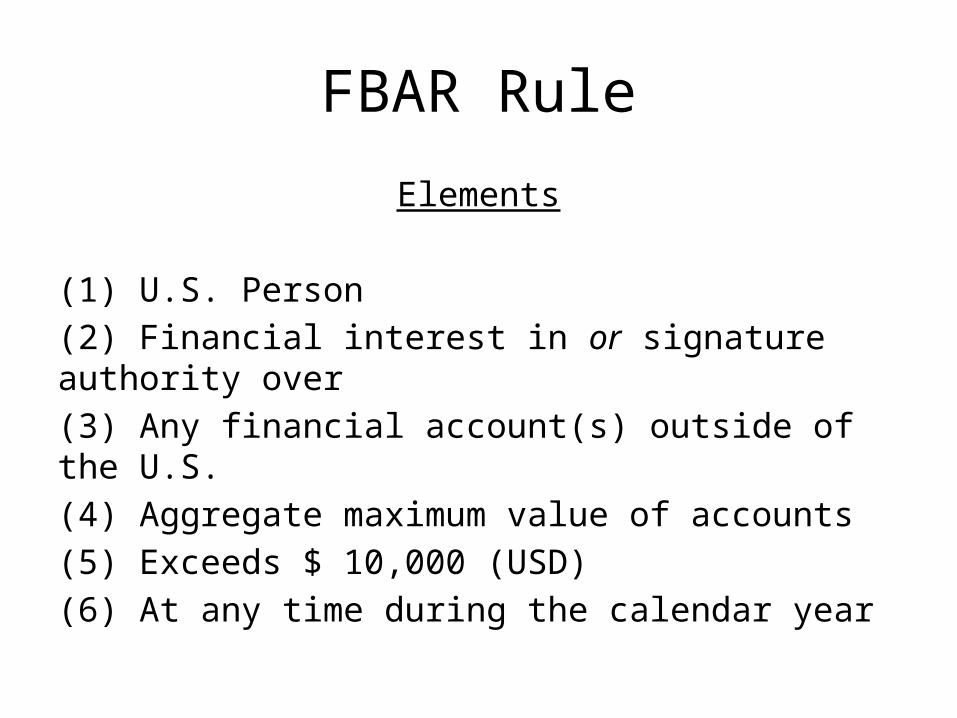

A U.S. person must file an FBAR if that person has a financial interest in or signature authority

over any financial account(s) outside of the United States and the aggregate maximum

value of the account(s) exceeds $ 10,000 (USD) at any time during the calendar year.

FBAR Rule

Elements

(1) U.S. Person(2) Financial interest in or signature authority over(3) Any financial account(s) outside of the U.S.(4) Aggregate maximum value of accounts(5) Exceeds $ 10,000 (USD)(6) At any time during the calendar year

Note Well

These are legal terms of art with precise meanings. They cannot be interpreted

according to the everyday meanings that we give to them, no matter how familiar they might

sound.

Deconstructing The Rule

Deconstructing The Rule

(1) Who is a U.S. Person?

– A citizen or resident of the U.S.– An entity created or organized in the U.S. or under

the laws of the U.S. • Entity includes, but is not limited to corporations,

partnerships, and limited liability companies.– A trust formed under the laws of the U.S.– An estate formed under the laws of the U.S.

Deconstructing The Rule

– U.S. Resident: To determine if the filer is a resident of the U.S., apply the residency tests in 26 U.S.C. § 7701(b).• Example # 1: Matt is a citizen of Argentina. He has lived in

the U.S. every day for the last three years. Because Matt is considered a resident by application of the rules under § 7701(b), he must file an FBAR.• Example # 2: Kyle is a permanent resident of the U.S. He is a

citizen of the UK. Under a tax treaty, Kyle is a tax resident of the UK and elects to be taxed as a resident of the UK. Kyle must file an FBAR. Tax treaties with the U.S. do not affect FBAR filing obligations.

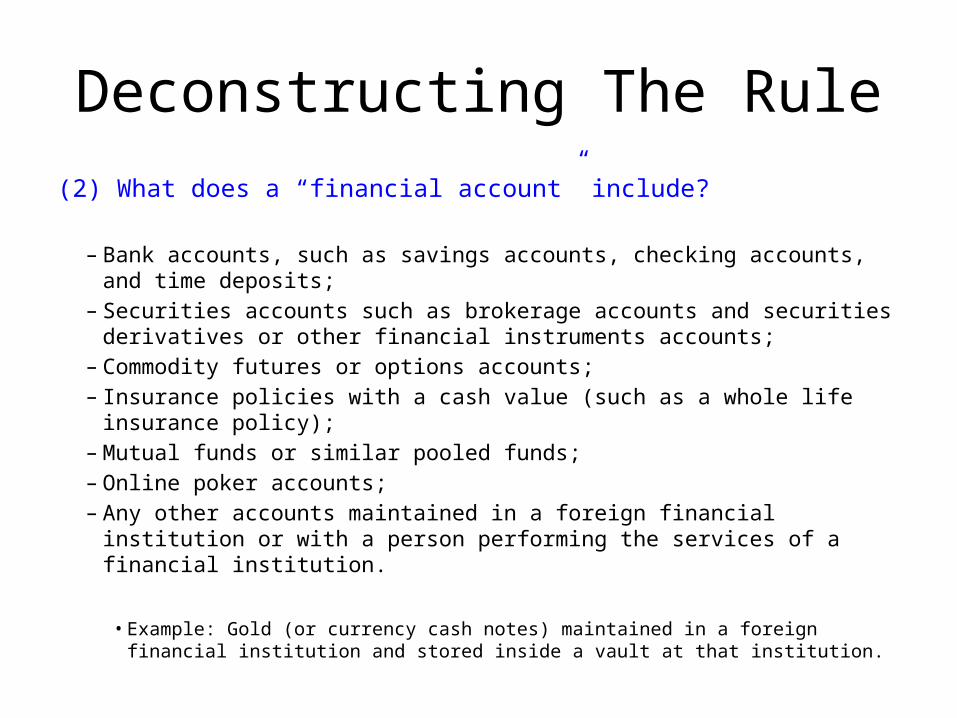

Deconstructing The Rule(2) What does a “financial account” include?

– Bank accounts, such as savings accounts, checking accounts, and time deposits;

– Securities accounts such as brokerage accounts and securities derivatives or other financial instruments accounts;

– Commodity futures or options accounts;– Insurance policies with a cash value (such as a whole life insurance policy);– Mutual funds or similar pooled funds;– Online poker accounts;– Any other accounts maintained in a foreign financial institution or with a

person performing the services of a financial institution.

• Example: Gold (or currency cash notes) maintained in a foreign financial institution and stored inside a vault at that institution.

Deconstructing The Rule• Contrary to popular belief, not all foreign asset owned by U.S. taxpayers must be reported. According to the FinCEN FBAR

reference guide, a financial account does not include: :

– IRA Owners & Beneficiaries: Owners or beneficiaries of IRAs are not required to report a foreign financial account held in the IRA.

– Participants In and beneficiaries of Tax-Qualified Retirement Plans: A participant in or beneficiary of a retirement plan described in Internal Revenue Code section 401(a), 403(a), or 403(b) is not required to report a foreign financial account held by or on behalf of the retirement plan.

– Consolidated FBAR: A U.S. person that is an entity and is named in a consolidated FBAR filed by a greater than 50% owner is not required to file a separate FBAR.

– Trust Beneficiaries: A trust beneficiary with a direct or indirect financial interest in more than 50% of the trust assets or income is not required to report the trust’s foreign financial accounts on an FBAR if the trust, trustee of the trust, or agent of the trust:

• Is a U.S. person, and• Files an FBAR disclosing the trust’s foreign financial accounts.

– Signature Authority: Individuals who have signature authority over, but no financial interest in, a foreign financial account are not required to report the account in certain situations.

Deconstructing The Rule

• Gray Area: Does gold (or cash notes) stored inside a vault in a foreign financial institution – but leased to a private company – trigger an FBAR-reporting requirement?

Deconstructing The Rule

(3) When is a financial account a “foreign financial account?”

– When it is located outside of the U.S.

– The U.S. includes:

• All 50 states and the District of Columbia

• All U.S. territories and possessions

Demystifying The FBAR

Module II: Deconstructing the rule (Part II)

Deconstructing The Rule(4) What does it mean for the taxpayer to have a “financial interest” in a financial account?

• A U.S. person has a financial interest in the following situations:

– The U.S. person is the owner of record or holder of legal title, regardless of whether the account is maintained for the benefit of the U.S. person or for the benefit of another person, including non-U.S. persons;

– The owner of record or holder of legal title is a person acting as an agent, nominee, attorney, or a person acting on behalf of the U.S. person with respect to the account;

• Example: John is a U.S. citizen. His brother, Paul, maintains bank accounts in Mexico on John’s behalf. The accounts are held in Paul’s name but Paul only accesses the accounts pursuant to John’s instructions.

• Does John have a financial interest in the Mexican bank accounts for FBAR-reporting purposes? Yes.

• Note well: If Paul is a U.S. citizen or resident, he also has an FBAR-reporting requirement with respect to the accounts.

Deconstructing The Rule– The owner of record or holder of legal title is a corporation in which a U.S. person owns

directly or indirectly:

• More than 50% of the total value of stock, or

• More than 50% of the voting power of all shares of stock.

• Example One: A Minnesota corporation owns 100% of a Spanish company. The Spanish company maintains several foreign bank accounts. Must the Minnesota corporation file an FBAR? Yes. Why? Because the Minnesota corporation is a U.S. person and it directly owns more than 50% of the total value of the shares of a Spanish company that, in turn, has legal title of several foreign financial accounts.

• Example Two: Assume that Jack, a U.S. person, owns 75% of the Minnesota corporation in the previous example. Must Jack also file an FBAR? Yes. Why? Because he indirectly owns more than 50% of the total value of shares of stock of the Spanish company and the Spanish company is the owner of record of the foreign financial accounts.

Deconstructing The Rule– The owner of record or holder of legal title is a partnership in which

the U.S. person owns directly or indirectly:

• An interest in more than 50% of the partnership’s profits, or

• An interest in more than 50% of the partnership capital.

Deconstructing The Rule– The owner of record or holder of legal title is a trust of which the U.S. person:

• Is the trust grantor; and

• Has an ownership interest in the trust for U.S. federal tax purposes.

• Example: Diana is a U.S. citizen. She is a grantor of a Foreign Asset Protection Trust but does not control trust assets. Nor does she receive distributions from the trust. Must Diana report the trust’s foreign financial accounts on an FBAR? Yes. Why? Because as the grantor, Diana is deemed to be the owner of the trust assets for federal tax purposes.

– The owner of record or holder of legal title is a trust in which the U.S. person has a greater than 50% present beneficial interest in the assets or income of the trust for the calendar year

• Example: Amy is a U.S. citizen. She has a remainder interest in a trust that has a foreign financial account. Must Amy report the trust’s foreign financial account on an FBAR? No. Why? Because a remainder interest is not considered a present beneficial interest for FBAR purposes.

Deconstructing the Rule

– The owner of record or holder of legal title is any other entity in which the U.S. person owns directly or indirectly more than 50% of the voting power, total value of equity interests or assets, or interest in profits.

Deconstructing The Rule

Reporting Jointly Held Accounts

• If two persons jointly maintain a foreign financial account, or if several persons each own a partial interest in an account, then each U.S. person has a financial interest in that account. Therefore, each person must report the entire value of the account on an FBAR.

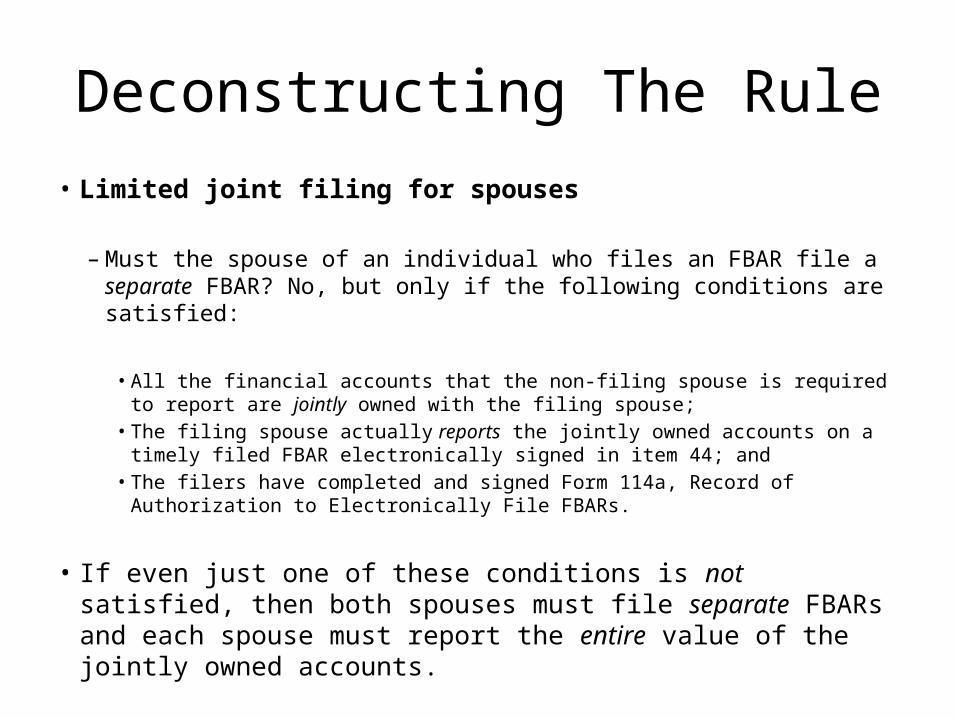

Deconstructing The Rule• Limited joint filing for spouses

– Must the spouse of an individual who files an FBAR file a separate FBAR? No, but only if the following conditions are satisfied:

• All the financial accounts that the non-filing spouse is required to report are jointly owned with the filing spouse;

• The filing spouse actually reports the jointly owned accounts on a timely filed FBAR electronically signed in item 44; and

• The filers have completed and signed Form 114a, Record of Authorization to Electronically File FBARs.

• If even just one of these conditions is not satisfied, then both spouses must file separate FBARs and each spouse must report the entire value of the jointly owned accounts.

Deconstructing The Rule

(5) What does it mean to have “signature authority” over a financial account?

– Signature authority is the authority of an individual to control the disposition of assets held in a foreign financial account by direct communication (whether in writing or otherwise) to the bank or other financial institution that maintains the financial account.

Deconstructing The Rule– A person has a “financial interest” in a foreign account not only if

he is the owner of record or holder of legal title, but also if he has signatory authority of the account or maintains it jointly with another person.

– There are additional ways in which a person can have a “financial interest” in a foreign account but this section only covers joint ownership of an account.

– Very simply, to the extent that two people jointly own a foreign financial account, each must file an FBAR reporting the entire value of the account because each has a financial interest in that account.

– Exception: The spouse of an individual who files an FBAR if certain conditions are satisfied.

Deconstructing the Rule

• Example: Megan is a U.S. resident. She has a power of attorney on her elderly parents’ accounts in Canada, but she has never exercised that power. Must Megan file an FBAR reporting her parents’ Canadian accounts? Yes, but only if the power of attorney gives Megan signature authority over the financial accounts. Whether or not Megan ever exercises that authority is meaningless for purposes of the FBAR filing requirement.

Deconstructing The Rule

(6) What is the maximum account value?

• It is defined as “a reasonable approximation of the greatest value of currency or nonmonetary assets in the account during the calendar year.”

Deconstructing The Rule

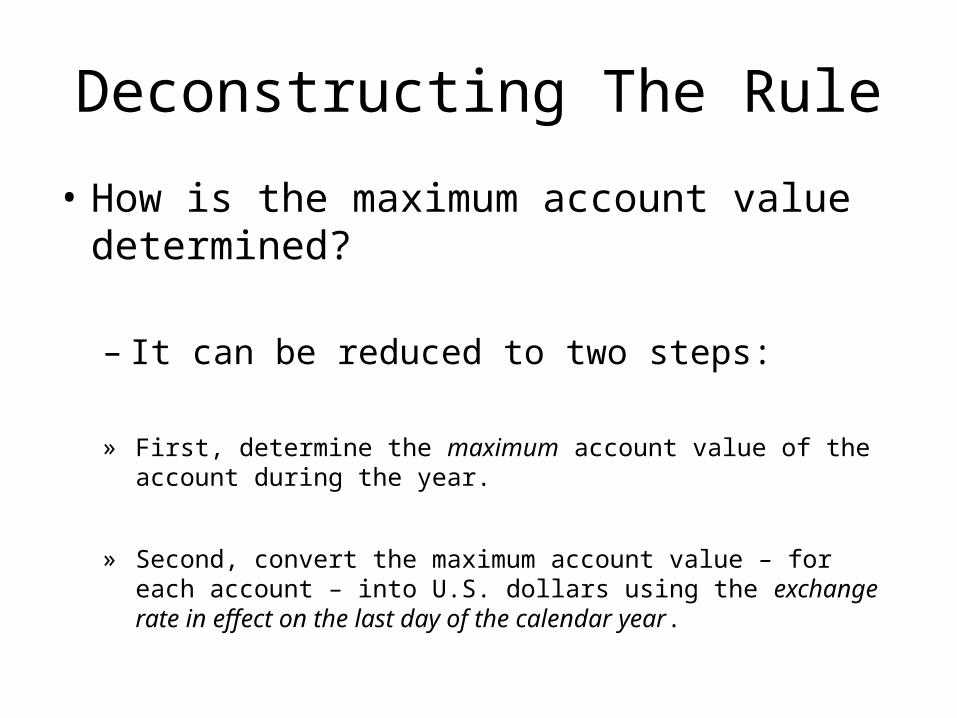

• How is the maximum account value determined?

– It can be reduced to two steps:

» First, determine the maximum account value of the account during the year.

» Second, convert the maximum account value – for each account – into U.S. dollars using the exchange rate in effect on the last day of the calendar year.

Deconstructing The Rule

• Example: In 2014, Todd had a foreign account with a Japanese bank. First, Todd would determine the maximum value of the account in Yen. Second, he would convert the maximum value of the account into U.S. dollars using the exchange rate in effect on December 31, 2014.

Deconstructing The Rule

• What type of documentation might Todd rely upon to determine the maximum balance of his foreign account?

– Periodic account statements, so long as they fairly reflect the maximum account balance of his account in 2014.

Deconstructing the Rule

(7) What is the “maximum aggregate value” rule?

Two Examples

Example # 1

Maximum Aggregate Balance: $ 25,000$ 35,000+ $ 40,000$ 100,000

Account Highest Balance for 2010 (USD)

Account A $ 25,000

Account B $ 35,000

Account C $ 40,000

Example # 2

Assume that John has three foreign accounts, the highest balances of which never exceed $ 10,000 (USD). The highest balance in each account is $ 9,000 (USD).

Account Highest Balance (USD)

A $ 9,000

B $ 9,000

C $ 9,000

Example # 2

Although none of the accounts by themselves trigger an FBAR reporting requirement because no single account exceeds the $ 10,000 reporting threshold, together they do. Indeed, the highest aggregate balance of the three accounts is $ 27,000. Therefore, all three accounts must be reported on an FBAR, even though none of them alone triggers an FBAR reporting requirement.

Demystifying The FBAR

Module III: Most Commonly Asked Questions About the FBAR

Most Commonly Asked Questions About the FBAR

Below are some of the most commonly asked questions when it comes to FBAR-reporting:

(1) How does an FBAR violation occur?

» An FBAR violation can occur in one of two ways:

• (1) first, by failing to disclose a foreign account on an FBAR altogether or

• (2) second, by disclosing a foreign account on an FBAR but underreporting the correct amount (i.e., the maximum value during the calendar year).

Most Commonly Asked Questions About the FBAR

It is the latter violation that many overlook. Many taxpayers think that as long as the account has been disclosed, there can be no violation, even though the amount was underreported. That is nothing more than a myth. Example: If Jason reports $ 50,000 (USD) as the maximum value of his offshore account but the maximum value is actually $ 150,000 (USD), he has committed an FBAR violation, notwithstanding the fact that he properly disclosed the account on an FBAR.

Most Commonly Asked Questions About the FBAR

(2) What is the date of an FBAR violation?

– Contrary to popular belief, it is not the last day of the calendar year.– An FBAR is due on June 30 of the year following the calendar year for

which the account is being reported. This is the last possible day for filing the FBAR.

– Therefore, the close of the day with no filed FBAR represents the first time that a violation has occurred.

– Example: If John opened up a Swiss bank account on October 1, 2014, then he would have until June 30, 2015 to report that account on an FBAR.

Most Commonly Asked Questions About the FBAR

(3) How far back in time can the IRS go to assert an FBAR penalty?

– The statute of limitations for asserting an FBAR penalty is six years from the date of the violation. If today is June 1, 2015, then the farthest back in time that the IRS can go to assert an FBAR penalty would be 2008.

– Why? Because the due date for a 2008 FBAR was June 30, 2009 and six years later is June 30, 2015. Thus, the statute of limitations for assessing a 2008 FBAR penalty is still open, albeit for just another 29 days. Of course, all of the later tax years are also fair game, namely 2009, 2010, 2011, 2012, and 2013. At the extreme, this means that FBAR penalties can potentially be asserted for the last six tax years, assuming of course that the taxpayer committed an FBAR violation in each one of these years.

Most Commonly Asked Questions About the FBAR

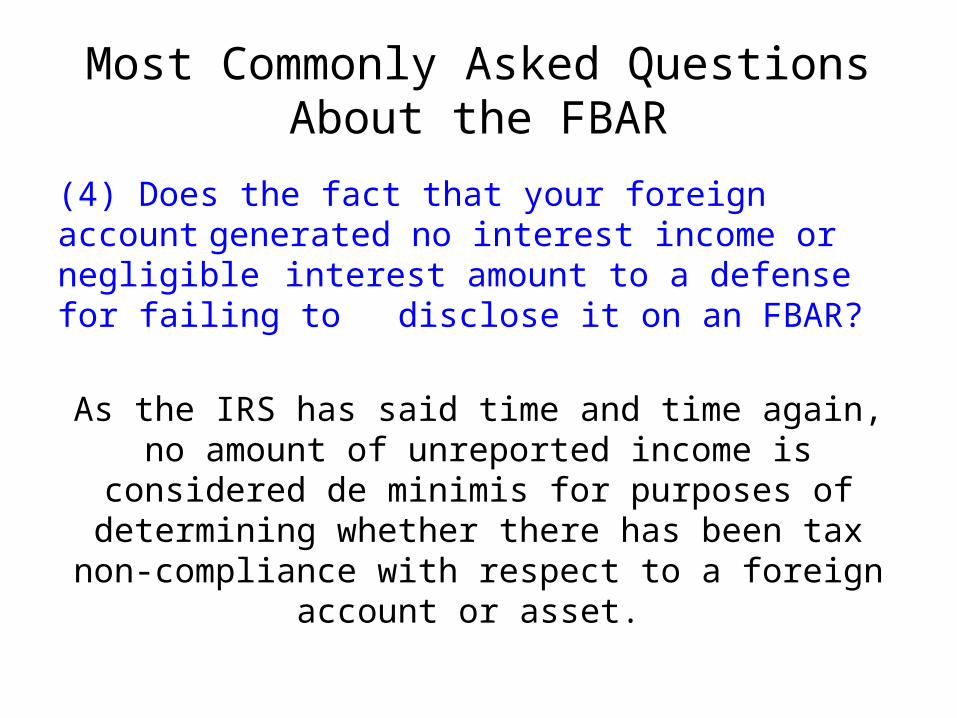

(4) Does the fact that your foreign account generated no interest income or negligible interest amount to a defense for failing to disclose it on an FBAR?

As the IRS has said time and time again, no amount of unreported income is considered de minimis for

purposes of determining whether there has been tax non-compliance with respect to a foreign account or

asset.

Most Commonly Asked Questions About the FBAR

(5) What are the penalties for failing to file an FBAR?

• First, contrary to popular belief, an FBAR violation doesn’t automatically mean that a penalty will be asserted.

– Examiners are expected to exercise their discretion when determining whether to assert a penalty. In doing so, they must consider the facts and circumstances of each case.

– For example, the examiner may decide that the facts do not justify asserting a penalty. In that case, the examiner would issue an FBAR warning letter (Letter 3800).

Most Commonly Asked Questions About the FBAR

• To the extent that the examiner determines that an FBAR penalty is warranted, there are two types:

–Non-willful, and

–Willful.

Most Commonly Asked Questions About the FBAR

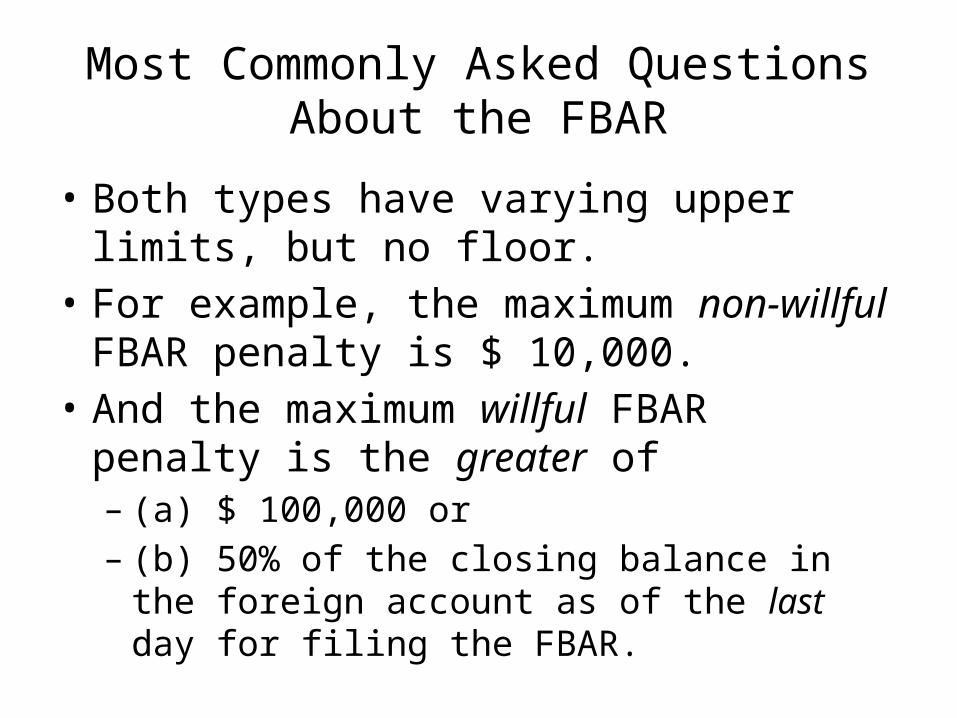

• Both types have varying upper limits, but no floor.

• For example, the maximum non-willful FBAR penalty is $ 10,000.

• And the maximum willful FBAR penalty is the greater of – (a) $ 100,000 or – (b) 50% of the closing balance in the foreign

account as of the last day for filing the FBAR.

Most Commonly Asked Questions About the FBAR

(6) Is the FBAR penalty the same as the miscellaneous offshore penalty under the streamlined procedures and OVDP?– No. – The FBAR penalty only exists outside of the OVDP

and streamlined framework. There is no such thing as an FBAR penalty within OVDP or the streamlined procedures. Instead, penalties under the OVDP or streamlined procedures are referred to as the “miscellaneous penalty.”

Most Commonly Asked Questions About the FBAR

(7) I’ve heard of something called the “penalty mitigation guidelines.” What are they?

• Because FBAR penalties have no set amount, the IRS has developed penalty mitigation guidelines to assist examiners in exercising their discretion in applying these penalties.

• The mitigation guidelines apply to both nonwillful and willful penalty amounts.

• Under the guidelines, the penalty amount is tied to a fixed, predetermined “maximum aggregate balance” for all accounts to which the violations relate.

Most Commonly Asked Questions About the FBAR

• For example, under the nonwillful penalty guidelines, if the maximum aggregate balance for all accounts to which the violations relate did not exceed $ 50,000 (USD) at any time during the year, a Level I nonwillful penalty applies.

• The corresponding penalty is $ 500 for each violation, not to exceed a total of $ 5,000 in penalties.

Most Commonly Asked Questions About the FBAR

(8) How do I know if I qualify for the penalty mitigation guidelines?

A taxpayer qualifies for the penalty mitigation guidelines if he satisfies the following conditions:

– The person has no history of criminal tax or Bank Secrecy Act convictions for the preceding ten years and has no history of prior FBAR penalty assessments;

– No money passing through any of the foreign accounts associated with the person can be from

an illegal source or used to further a criminal purpose;

– The person cooperated during the examination; and

– The IRS did not assert a fraud penalty against the person for an underpayment of income tax for the year in question due to the failure to report income related to any amount in a foreign account.

Most Commonly Asked Questions About the FBAR

(9) Are FBAR penalties determined per account, or per unfiled FBAR?

– First, FBAR penalties are determined per account, not per unfiled FBAR.

– Second, penalties apply for each year of each violation.

– Even though all of a taxpayer’s foreign accounts are itemized on a single FBAR, that does not necessarily mean that a taxpayer who has multiple unreported accounts in a single tax year is subject to only one FBAR penalty. On the contrary, because FBAR penalties are determined per account, a taxpayer with multiple unreported accounts in a single tax year could be subject to multiple FBAR penalties.

– For example, if John fails to report five foreign accounts in 2013, then he is subject to five separate FBAR penalties in that year alone.

Most Commonly Asked Questions About the FBAR

(10) The combination of the six-year statute of limitations and the fact that FBAR penalties are determined per account packs a “one-two” punch. Very simply, it can catapult a taxpayer’s FBAR liability into the penalty stratosphere.

Demystifying The FBAR

Module IV: IRS Procedures for Ensuring Consistency and Effectiveness in Administering

Civil FBAR Penalties

Procedures Applicable to all FBAR Cases

• On May 13, 2015, the IRS issued interim guidance to implement procedures to improve the administration of the IRS’s FBAR compliance program.

Procedures Applicable to all FBAR Cases

• The following procedures apply to all FBAR cases. Examiners must:

• Determine a recommended penalty based on the guidance in IRM 4.26.16 and (2), (3), and (4) below.

• Consult with an Operating Division FBAR Coordinator.

• Seek approval of the FBAR penalty from the group manager after consultation with an Operating Division FBAR Coordinator.

• Coordinate with Counsel if a penalty for a willful FBAR violation is being recommended.

• Coordinate with a Fraud Technical Advisor if there is reason to

believe a criminal referral may be warranted.

Penalty Amount for Willful Violations

• For cases involving willful violations over multiple years, examiners will recommend a penalty for each year for which the FBAR violation was willful.

• In most cases, the total penalty amount for all years under examination will be limited to 50 percent of the highest aggregate balance of all unreported foreign financial accounts during the years under examination.

Penalty Amount for Willful Violations

• Then the penalty for each year will be determined by allocating the total penalty amount to all years for which the FBAR violations were willful based upon the ratio of the highest aggregate balance for each year to the total of the highest aggregate balances for all years combined, subject to the maximum penalty limitation in 31 U.S.C. Section 5321(a)(5)(C) for each year.

• Under no circumstances will the total willful FBAR penalty amount exceed 50 percent of the highest aggregate balance of all unreported foreign financial accounts during the years under examination.

Penalty Amount for Willful Violations

Example:

• Assume highest aggregate balances of $ 50,000, $ 100,000, and $ 200,000 for 2010, 2011, and 2012, respectively. The total penalty amount is $ 100,000 (50 percent of the $ 200,000 highest aggregate balance during the years under examination).

• The total of the highest aggregate balances for all years combined is $ 350,000. The penalty for 2010 is $ 14,286 ($ 50,000/$ 350,000 x $ 100,000). The penalty for 2011 is $ 28,571 ($ 100,000/$ 350,000 x $ 100,000). The penalty for 2012 is $ 57,143 ($ 200,000/$ 350,000 x $ 100,000). The penalty amounts for each year are subject to the maximum penalty limitation under 31 U.S.C. Section 5321(a)(5)(C).

Penalty Amount for Nonwillful Violations

• For most cases involving multiple nonwillful violations, examiners will recommend one penalty for each open year, regardless of the number of unreported foreign financial accounts. In those cases, the penalty for each year will be determined based on the aggregate balance of all unreported foreign financial accounts, and the penalty for each year will be limited to $ 10,000.

• For some cases, the facts may indicate that asserting nonwillful penalties for each year is unwarranted. In those cases, examiners – with the approval of the group manager – may assert a single penalty, not to exceed $ 10,000, for one year only.

Penalty Amount for Nonwillful Violations

• For other cases, the facts (considering the conduct of the person required to file and the aggregate balance of the unreported foreign financial accounts) may indicate that asserting a separate nonwillful penalty for each unreported foreign financial account, and for each year, is warranted. In those cases, examiners – with the approval of the group manager – may assert a separate penalty for each account and for each year.

• Under no circumstances will the total amount of penalties for nonwillful violations exceed 50 percent of the highest aggregate balance of all unreported foreign financial accounts for the years under examination.

Penalty Amount for Nonwillful Violations

• A nonwillful penalty will not be recommended if the examiner determines that the FBAR violations were due to reasonable cause and if the taxpayer who failed to timely file correct and complete FBARs later files correct and complete FBARs.

Penalty Amount for Nonwillful Violations

• The rules for determining the penalty amount for a nonwillful FBAR violation can be reduced to three steps:

– First, the examiner must determine whether the mitigation threshold conditions found in IRM 4.26.16.4.6.1 are met.

Penalty Amount for Nonwillful Violations

– Second, if the mitigation threshold conditions are met, examiners should make a preliminary penalty calculation based upon the mitigation guidelines in IRM 4.26.16.4.6.2, except that the penalty for each year will be limited to $ 10,000. Unless the facts and circumstances of a case warrant a different penalty amount, this is the penalty amount to be asserted.

Penalty Amount for Nonwillful Violations

– Third, if the IRM mitigation threshold conditions are not met, the mitigation guidelines do not apply and examiners should not make a preliminary penalty calculation based upon the guidelines. Examiners, with the group manager’s approval, should assert a separate penalty for each account and for each year. However, under no circumstances will the total amount of the nonwillful penalties exceed 50 percent of the highest aggregate balance of all unreported foreign financial accounts for the years under examination.

Demystifying The FBAR

Module V: Willfulness

WillfulnessA Primer on Willfulness

• One small word is all that distinguishes a civil tax matter from a criminal tax matter. That word is called “willfulness.” It is the cornerstone of any criminal tax matter.

• The most common crime that the government charges in connection with the willful failure to report an offshore account is “willful failure to file an FBAR.”

• It is a felony punishable by a prison term of up to ten years and criminal penalties of up to $ 500,000.

Willfulness

• Willfulness is a necessary element not only of tax crimes but also of willful civil FBAR penalties.

• In the criminal setting, the government carries the heavy burden of proving – beyond a reasonable doubt – that the taxpayer acted willfully.

• How is willfulness defined? As an “intentional violation of a known legal duty.”

Willfulness

• How do courts interpret willfulness?

– The only thing that a person need know is that he has a reporting requirement. And if a person has that requisite knowledge, the only intent needed to constitute a willful violation of the requirement is a conscious choice not to file the FBAR.

– The latter is referred to in legal circles as the theory of “willful blindness.”

Willfulness• What does it mean for a defendant to be willfully blind?

– Under the theory of willful blindness, a jury may infer willfulness whenever a taxpayer intentionally fails to inquire and learn about his or her filing obligations.

– In other words, instead of proving that the defendant intentionally violated a known legal duty, the government need only show that “the defendant consciously avoided any opportunity to learn what the tax consequences were.” United States v. Bussey, 942 F.2d 1241, 1428 (8th Cir. 1992).

Willfulness - Criminal

• How does the government prove willfulness in the prosecution of a taxpayer for failing to file an FBAR?

– Seldomly are there any witnesses and only in a rare case would a defendant admit the required state of mind.

– So what does the government rely on? Indirect evidence. Specifically, conduct or acts from which a person’s state of mind can be inferred. These acts are commonly referred to as “badges of fraud.”

Badges of Fraud• Examples of some common “badges of fraud” that are sure to

attract the IRS’s attention:

– A taxpayer who checks the box off “no” on Schedule B in response to the question, “Do you have an interest in or signature authority over a financial account in a foreign country?” when, in fact, he has just such an account.

– Whether the failure to report the account occurred continuously over a period of years or whether it was merely an isolated incident. In other words, did the taxpayer’s failure to file an FBAR occur over the course of time or just one year?

Badges of Fraud– Whether the taxpayer failed to report a foreign account in a

later year despite having checked the box off “yes” on Schedule B of his tax return in an earlier year (and/or filing an FBAR in an earlier year). This reveals that the taxpayer knew that he had an FBAR-reporting obligation in the later year.

– The high watermark balance of the account: The amount of money at stake is crucial. Unreported accounts with maximum aggregate balances that are half-a-million or greater are heavily scrutinized. As one prominent tax attorney has been quoted as saying, “If a person has a $10 million account, I don’t want to hear he was nonwillful, and neither does the government.”

Badges of Fraud– Whether the taxpayer told his tax preparer about the account(s).

– Whether the account was held in such a way as to conceal ownership.

• For example, was it in the name of a “foreign shell corporation or foreign trust,” or some other entity that would make it difficult for the IRS to learn the true identity of the owner?

• Was the account a numbered account?

• Was the taxpayer issued a credit or debit card without his or her name visible on the card itself?

Badges of Fraud

–Did the bank help the taxpayer repatriate cash to the U.S. using covert means?

• Did bank managers and their U.S. clients use code words in emails to gain access to funds?

• Did U.S. clients ever use coded language, such as asking their private bankers, “can you download some tunes for us?” or note that their “gas tank [was] running empty” when they required additional cash to be loaded to their cards.

Badges of Fraud– Whether the taxpayer closed the foreign account and transferred the

assets to another bank in the wake of a DOJ press release or media coverage reporting that the taxpayer’s bank had become the target of an IRS summons demanding U.S. accountholder information or that it had agreed to participate in FATCA. Example: Headlines splashed across the front page of major newspapers.

– Whether a taxpayer who has a duty to file an FBAR checks the box off “yes” to the question, “Do you have an interest in or signature authority over a financial account in a foreign country?” but “no” to the follow-up question, “If ‘Yes,’ are you required to file Form TD F 90-22.1 [FBAR] to report that financial interest or signature authority?” This question gets to the heart of the matter: “Must an FBAR be filed?”

Badges of Fraud– The amount of interest generated by the foreign account and

whether that interest – no matter how negligible – was reported on the taxpayer’s U.S. tax return. If the interest was reported on a U.S. tax return, the IRS generally views the filing of an FBAR as a mere formality. In that case, the taxpayer can usually come into compliance with his U.S. tax obligations by filing a delinquent FBAR.

– Whether the taxpayer instructed bank personnel to hold back his bank statements and not mail them to him in the U.S. (if the U.S. residence was listed as the accountholder’s primary residence).

Badges of Fraud– Whether the taxpayer had been subject to a previous audit

involving unreported offshore assets or bank accounts.

– The number of foreign accounts held (i.e., one versus six).

Badges of Fraud

No single factor is dispositive. It is a totality of the circumstances test.

Badges of Fraud

• Ultimately, the jury must “look into the mind of the defendant-taxpayer to determine whether he intentionally violated the statute.”

• To the extent that the government can show the jury enough “badges of fraud” to prove willfulness beyond a reasonable doubt, the government will have satisfied its burden of proving criminal intent through circumstantial evidence.

Willfulness – Civil Penalties• To the extent that the examiner attempts to assert a willful FBAR penalty,

the burden is on the IRS to show that the violation was, in fact, willful.

• The IRS has adopted the same definition of willfulness here, in the civil context, as the one that applies in criminal tax cases: “an intentional violation of a known legal duty.”

• Not surprisingly, willfulness is often the battleground whenever the IRS attempts to assert a willful FBAR civil penalty.

• While the burden of establishing willfulness for purposes of asserting an FBAR civil penalty is on the IRS, the standard of proof is less than what it is for willfulness in the criminal context. It’s “clear and convincing evidence.”

Willfulness – Civil Penalties • How easy (or difficult) is it for the IRS to prove willfulness for

purposes of asserting a willful FBAR penalty?

– Lowering the bar for willfulness for FBAR Penalties

• Thanks to a recent fourth circuit court of appeals case, the quantum of evidence needed to show that the failure to file an FBAR was intentional has been substantially diluted.

• For this reason, J. Bryan Williams is a name that U.S. persons with unreported foreign bank accounts have come to dread.

Willfulness – Civil Penalties • Background: Every 1040 contains a “jurat,” just above the

signature line. It states the following: “Under penalties of perjury, I declare that I have examined this return and accompanying schedules and statements, and to the best of my knowledge and belief, they are true, correct, and complete.”

• What does this mean? There is a presumption in the law that a taxpayer who signed his 1040 did, in fact, examine the return and that it is “true, correct, and complete” – even if the taxpayer did not actually review it. Ouch!

Willfulness – Civil Penalties • The Fourth Circuit Court of Appeals reasoned that Mr. Williams

made a “conscious effort to avoid learning about reporting requirements.”

• While the majority could have rested there and concluded that the record established willful blindness and reversed on that basis alone, they decided to go one step further. That one step created a firestorm of opposition among critics.

• The majority held that Williams’ signature on his tax return was “prima facie evidence that he knew the contents of the return,” even though Williams denied ever reviewing it.

Willfulness – Civil Penalties – Analysis

• Because Mr. Williams was presumed to have known the contents of his return (by virtue of having signed the 1040), the court reasoned that he was cognizant of the FBAR-filing requirements. Why? Because Section III of Schedule B specifically refers the taxpayer to FinCEN Form 114 (FBAR) and its accompanying instructions, which contain the FBAR-filing requirements.

• That question asks: “If ‘Yes,’ are you required to file Form TD F 90-22.1 [FBAR] to report that financial interest or signature authority? See Form TD F 90-22.1 and its instructions for filing requirements and exceptions to those requirements.”

Willfulness – Civil Penalties • Thus, Schedule B’s reference to FinCEN Form 114

(FBAR) and its accompanying instructions were deemed to have put Williams on “inquiry notice” of the FBAR-filing requirements, even though he never reviewed the return, much less the filing instructions on the FBAR.

Willfulness

•What does this case mean for the average taxpayer with an unreported foreign bank account? Such taxpayers are presumed to be cognizant of the FBAR-filing requirements merely by signing the tax return (so long as it contains “Schedule B”).

Willfulness• The practical effect of this opinion is nothing short of

mind blowing.

– First, instead of having to prove a specific intent to “violate a known legal duty,” which other tax cases have upheld as the standard for proving willfulness, Williams makes a taxpayer liable for willful FBAR penalties based on nothing more than his or her presumed understanding of the FBAR requirement.

– As some tax professionals have artfully put it, Williams has given the IRS carte blanche to assert a willful FBAR penalty for something as arbitrary as a distaste for the color of a taxpayer’s shoes.

Willfulness

–Second, it gives a major boost to the IRS’s current intensive pursuit of overseas tax evasion. How? By making it easier for the IRS to prove willfulness in the context of a willful FBAR penalty.

The Empire Strikes Back

• Keep in mind that just because the IRS thinks that a willful FBAR penalty is warranted does not make it “official.”

• For example, a taxpayer can challenge the assertion. In doing so, he’d be putting the IRS’s feet to the fire, by holding them up to their burden of proving “willfulness” in court.

The Empire Strikes Back• To the extent that the IRS has asserted a willful FBAR

penalty, the IRS must prove willfulness to the satisfaction of a jury. While willfulness need only be proven by “clear and convincing evidence” in the civil context, the fact remains that proving the existence of a mental state is easier said than done.

• Stated otherwise, it is often easier for the taxpayer to prove the absence of a mental state (such as willfulness) than it is for the IRS to affirmatively show that it existed. But the taxpayer does not carry the burden of proving the absence of willfulness at trial.

Willfulness

• While Williams gave a major boost to the IRS’s efforts to root out offshore tax evasion by making it easier for the IRS to prove willfulness, taxpayers can take comfort in the following:

– First, the case was a gross example of offshore tax evasion

– Second, it is an unpublished opinion. Therefore, it is not binding precedent on federal courts in the fourth circuit, much less any of its sister circuits.

Willfulness

– Third, if the IRM is any indication, it appears that the official position of the IRS is to require a higher quantum of proof to establish willfulness than what the court in Williams required. In other words, the IRS will not indulge in the fiction that a taxpayer knows and understands his FBAR-reporting requirements merely by having signed his return.

Willfulness

• According to the IRM, the IRS uses the following standard when determining whether willfulness exists in a civil context:

– The taxpayer must know that he has a reporting requirement; and

– To the extent that the taxpayer has this requisite knowledge, the only intent needed to constitute a willful violation of the requirement is a conscious choice not to file the FBAR (i.e., willful blindness)

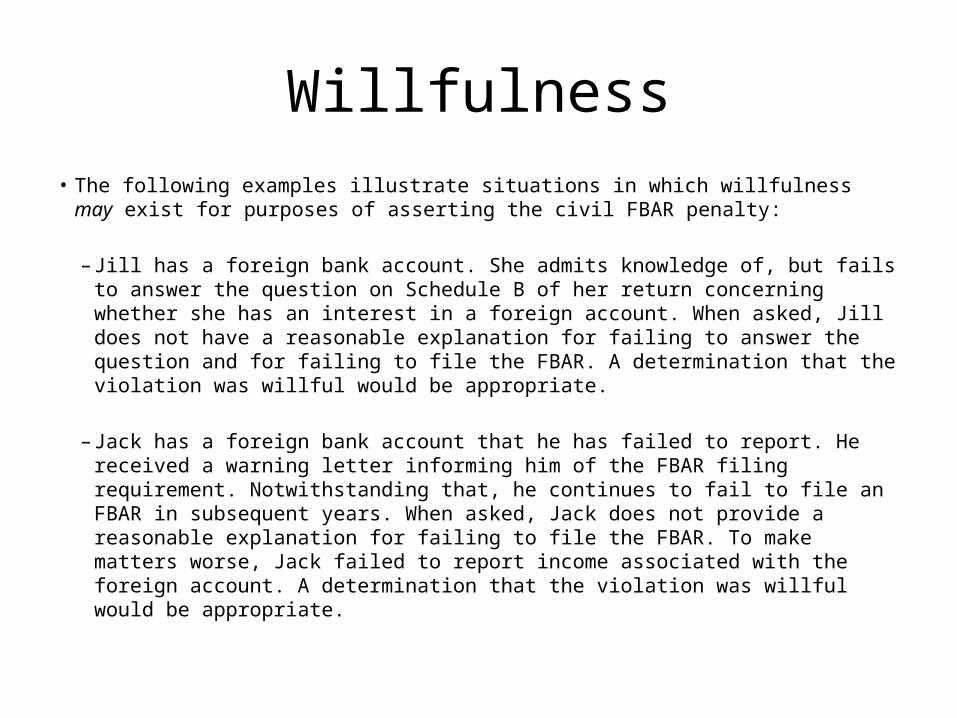

Willfulness• The following examples illustrate situations in which willfulness may exist for

purposes of asserting the civil FBAR penalty:

– Jill has a foreign bank account. She admits knowledge of, but fails to answer the question on Schedule B of her return concerning whether she has an interest in a foreign account. When asked, Jill does not have a reasonable explanation for failing to answer the question and for failing to file the FBAR. A determination that the violation was willful would be appropriate.

– Jack has a foreign bank account that he has failed to report. He received a warning letter informing him of the FBAR filing requirement. Notwithstanding that, he continues to fail to file an FBAR in subsequent years. When asked, Jack does not provide a reasonable explanation for failing to file the FBAR. To make matters worse, Jack failed to report income associated with the foreign account. A determination that the violation was willful would be appropriate.

Demystifying The FBAR

Module VI: Beyond the FBAR – Everything You Never Wanted to Know About All of the Other

International Reporting Forms (But Must)

Form 3520

(1) Form 3520, Annual Return to Report Transactions With Foreign Trusts and Receipt of Certain Foreign Gifts

– Under IRC § 6048, taxpayers must report various transactions involving foreign trusts, including creation of a foreign trust by a United States person, transfers of property from a United States person to a foreign trust, and receipt of distributions from foreign trusts.

– This return also reports the receipt of gifts from foreign entities under IRC § 6039F.

– The penalty for returns reporting gifts is five percent of the gift per month, up to a maximum penalty of 25 percent of the gift.

Form 926

(2) Form 926, Return by a U.S. Transferor of Property to a Foreign Corporation

– Under IRC § 6038B, taxpayers must report transfers of property to foreign corporations and other information.

– The penalty for failing to file each one of these information returns is ten percent of the value of the property transferred, up to a maximum of $100,000 per return, with no limit if the failure to report the transfer was intentional.

Form 3520-A

(3) Form 3520-A, Information Return of Foreign Trust With a U.S. Owner

– Under IRC § 6048(b), taxpayers must report their interests in foreign trusts, by United States persons with various interests in and powers over those trusts.

– The penalty for failing to file each one of these information returns or for filing an incomplete return, is the greater of $10,000 or 5 percent of the gross value of trust assets determined to be owned by the United States person.

Form 5471

(4) Form 5471, Information Return of U.S. Persons with Respect to Certain Foreign Corporations

– Under IRC §§ 6035, 6038 and 6046, certain United States persons who are officers, directors or shareholders in certain foreign corporations (including International Business Corporations) must report information.

– The penalty for failing to file each one of these information returns is $10,000, with an additional $10,000 added for each month the failure continues beginning 90 days after the taxpayer is notified of the delinquency, up to a maximum of $50,000 per return.

Form 5472(5) Form 5472, Information Return of a 25% Foreign-

Owned U.S. Corporation or a Foreign Corporation Engaged in a U.S. Trade or Business

– Under IRC §§ 6038A and 6038C, taxpayers may be required to report transactions between a 25 percent foreign-owned domestic corporation or a foreign corporation engaged in a trade or business in the United States and a related party.

– The penalty for failing to file each one of these information returns, or to keep certain records regarding reportable transactions, is $10,000, with an additional $10,000 added for each month the failure continues beginning 90 days after the taxpayer is notified of the delinquency.

Form 8865

(6) Form 8865, Return of U.S. Persons With Respect to Certain Foreign Partnerships

– Under IRC §§ 6038, 6038B, and 6046A, United States persons with certain interests in foreign partnerships must report interests in and transactions of these foreign partnerships, transfers of property to these foreign partnerships, and acquisitions, dispositions and changes in foreign partnership interests.

– Penalties include $10,000 for failure to file each return, with an additional $10,000 added for each month the failure continues beginning 90 days after the taxpayer is notified of the delinquency.

– The penalty is capped at $50,000 per return, and ten percent of the value of any transferred property that is not reported, subject to a $100,000 limit.

Demystifying The FBAR

Module VII: Challenging the IRS’s Assertion of the Non-willful FBAR Penalty: A New Hope

Some Background InformationThe current economic and political climate is very hostile

towards foreign account holders. Many people have a vision of wealthy expats who throw Great Gatsby-esque parties, during

which the attendees burn their delinquent tax notices with fondue candles as they cackle over bad jokes and gossip about people who aren’t in the room. Many politicians are only too

happy to promote this image.

A New Hope

Only a handful of court cases have considered the procedures and substance relating to FBAR

penalties – until now. As a result, the procedures associated with imposing civil penalties are not

well-established.

A New Hope

In the case of Moore v. United States, the district court for the western district of Washington examined the procedures and standards that

apply to penalties for non-willfully failing to file an FBAR. Its holdings were both good and bad

for taxpayers.

The Good

The judge issued a preliminary ruling stating that the IRS cannot spin the “Wheel of Misfortune” and

arbitrarily determine the amount of a civil penalty in a Report of Foreign Banks and Financial Accounts (FBAR)

failure to file case.

The Bad

Moore violated the law by not filing FBARs and did not have reasonable cause for not filing. However, the record before the court was

insufficient for it to determine whether the amount of the penalties was appropriate.

Summary

The Good The Bad

The judge issued a preliminary ruling stating that the IRS cannot spin the Wheel of Misfortune and arbitrarily determine the amount of a civil penalty in a Report of Foreign Banks and Financial Accounts (FBAR) failure to file case.

Moore violated the law by not filing FBARs and did not have reasonable cause for not filing. However, the record before it was insufficient for it to determine whether the amount of the penalties was appropriate.

A New Hope

Why the Moore Case is Important For Taxpayers Challenging Non-willful FBAR

Penalties

1. First, it discusses the constitutional challenges raised by Moore in opposing the IRS’s imposition of non-willful FBAR penalties.

2. Second, it explains the merits of Moore’s reasonable cause defense – a defense that has spawned a significant amount of case law in the context of civil tax penalties, but little more than a “mole hill” of law in the context of FBAR penalties.

A New Hope

What follows is a recitation of the facts from the case, the procedural background, and more

about the court’s holdings.

Moore v. United States• Facts:

– James Moore probably does not even own a dinner jacket or an ascot tie, but he did own a bank account in Switzerland that originated in the Bahamas, where Mr. Moore relocated in 1989. And that was more than enough to put him on the IRS’s radar screen.

– Mr. Moore did not file a FBAR for 20 years, even though the account balance never dipped below $300,000 and no exemptions applied. Around 2009, he approached the IRS through counsel as part of the Offshore Voluntary Disclosure Program. Both sides agreed that he owed about $18,000 in back taxes.

Facts

– With that unpleasantness out of the way, the IRS started calculating the penalty. In October 2011, an agent interviewed Mr. Moore via telephone for about five minutes. The agent never specifically said anything about penalties. Yet based on that conversation, and prior research, the agent prepared a detailed, eight-page Summary Memorandum that recommended a $40,000 penalty, or $10,000 per year for 2005-2008.

Moore v. United States– At some point, someone also produced an “Appeals Memo.” The

Service refused to produce this second memo during discovery, and the Court agreed that it was confidential.

– Two months later, the Service sent Mr. Moore a bill for $40,000, but provided no explanation of the charges. Mr. Moore never saw the Summary Memorandum until it was produced during discovery. Although the December 2011 letter said he could appeal and the IRS would hold off for another six weeks, the IRS reneged on its own promise (is anyone really surprised at that?) and almost immediately assessed a $10,000 penalty for 2005.

Moore v. United States• Procedural Posture:

– Mr. Moore appealed the assessment, and the Service responded with a three-sentence letter that began with the dreaded words “Dear Taxpayer” and ended with “Your case is now closed in Appeals.”

– In addition to a payment coupon, the letter included an invitation to participate in an “appeals customer satisfaction survey.”

– The Service said nothing about the remaining $30,000 in penalties, which were apparently hanging over his head like the sword of Damocles.

– Mr. Moore eventually filed suit in 2013, alleging a host of Constitutional and Administrative Procedures Act (APA) violations. We’ll get to those in a minute. He asked for a refund of the penalty he paid, and for the court to set aside the unassessed $30,000.

Moore v. United States

• Holdings: – First, the Court held that Mr. Moore committed

non-willful violations of the Bank Secrecy Act by failing to file FBARs. However, that was not much of a shock considering that he admitted that he owed taxes and penalties right from the start. Remember, he was the one who came forward in the first place.

– Second, the Court made rulings regarding Mr. Moore’s due process and APA claims, which are more relevant to our inquiry.

Moore v. United StatesRulings Regarding Mr. Moore’s Due Process & APA Claims

• Some background information about Mr. Moore’s APA claims is necessary: The APA says that an agency – including the IRS – cannot act in a way that is “arbitrary, capricious, an abuse of discretion, or otherwise not in accordance with the law.” These claims are difficult to win, because the government gets the benefit of the doubt.

• Now, we get to the heart of the matter. The Court explicitly ruled that it “Cannot, On the Record Before It, Determine if the IRS Acted Arbitrarily, Capriciously or Abused Its Discretion in Assessing the Penalties.” That finding was the equivalent of a “one-two punch” to the IRS.

Moore v. United States• Even though a court presumes that an agency acted fairly in

these situations, there must be some evidence in the record to support that presumption. Lawyers call this level of proof a scintilla.

• If there is a bread crumb anywhere on the kitchen floor, the Court can presume that someone ate a pepperoni pizza with extra mushrooms from Dominos for lunch at 12:02 that day.

Moore v. United States

• Judge Jones used a magnifying glass to look for a “crumb,” and the only thing he found was the aforementioned three sentence “pay-or-else” letter. Although the Summary Memorandum was in the record, Mr. Moore didn’t see it until he filed a lawsuit, so it doesn’t count.

• Judge Jones looked at the case and bluntly concluded that he would not “rubber-stamp a decision that lacks any explanation in the administrative record.”

Moore v. United States

What this decision means for the IRS

• The IRS must demonstrate that it had a rational basis for the $ 40,000 penalty and that Mr. Moore was at least somewhat in the loop.

• To do this, the IRS may simply supplement the record, and to the extent that the evidence it submits provides a rational basis for the $ 40,000 penalty, then Judge Jones’ next order will be “roll on two.”

• However, there is a very good chance that this evidence does not exist. And in this alternative ending, an emotional Paul Edgcomb will quietly escort Mr. Moore out of the death house.

Moore v. United States

My Musings

• From a practical point of view, the IRS may be in trouble. Unless there is something that we do not know, it does not appear as though the IRS can show that it had a rational basis for asserting the $ 40,000 penalty. On the contrary, it looks like the Service just gave Moore an account statement and informed him of his “right” to an appeal.

Moore v. United States

• What about the phantom “Appeals Memorandum?” That probably won’t help, because it is unlikely that Mr. Moore saw it, or even knew of its existence, before he got the bill.

• On the other hand, the government’s burden is very low. They only have to produce a scintilla. – There may be a transcript of that October 2011 interview that

gives some indication of the Service’s thought process in the matter.

– Or, there may be a stray letter or email between the IRS and Mr. Moore’s counsel. In other words, there may be something the parties missed. Remember: Any crumb will do.