depb procedures

TRANSCRIPT

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 120

Advance Authorisation Scheme(Erstwhile Advance Licence Scheme)

Schemes

The Duty Exemption Scheme enables duty free import of inputs required for export productionAn Advance Authorisation is issued under Duty Exemption Scheme Duty Exemption Schemeconsists of (a) Advance Authorisation Scheme and (b) Duty Free Import Authorisation Scheme(DFIA)

A Duty Remission Scheme enables post export replenishment remission of duty on inputsused in the export product Duty Remission scheme consist of (a) DFRC (Duty FreeReplenishment Certificate) and (b) DEPB (Duty Entitlement Pass Book Scheme) and (c) DBK(Duty Drawback Scheme)

Advance Authorisation Scheme

Advance Authorisation An Advance Authorisation is issued to allow duty free import of inputs

which are physically incorporated in the export product (making normal allowance for wastage) In addition fuel oil energy catalysts etc which are consumedutilised in the courseof their use to obtain the export product may also be allowed under the scheme

Duty free import of mandatory spares upto 10 of the CIF value of the Authorisation which arerequired to be exported supplied with the resultant product may also be allowed under Advance Authorisation

Advance Authorisations are issued on the basis of the inputs and export items given under SION However they can also be issued on the basis of Adhoc norms or self declared normsAdvance Authorisation can be issued either to a manufacturer exporter or merchant exporter tied to supporting manufacturer(s)

i) for Physical exports (including exports to SEZ) and or

ii) for Intermediate supplies and or

iii) to the main contractor for supply of goods to the categories mentioned in paragraph 82 (b)(c) (d) (e) (f) (g) (i) and

(iv) of the Foreign Trade Policy

for import of inputs required in the manufacture of goods In addition in respect of supply of goods to specified projects mentioned in paragraph 82 (d) (e) (f) (g) and (j) of the Policy anAdvance Authorisation can also be availed by the sub-contractor of the main contractor to

such project provided the name of the sub contractor(s) appears in the main contract

Such Authorisation can also be issued for supplies made to United Nations Organisations or under the Aid Programme of the United Nations or other multilateral agencies and paid for infree foreign exchange

Advance Authorisation is issued for duty free import of inputs subject to actual user conditionSuch Authorisations are exempted from payment of basic customs duty additional customsduty education cess anti dumping duty and safeguard duty if any However the imports for

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 220

supplies covered under sub-paragraph (h) amp (i) of paragraph Categories of Supply of SectionDeemed Exports of this site will not be exempted from the payment of applicable anti-dumping and safeguard duty if any

Advance Authorisation andor materials imported thereunder shall not be transferable evenafter completion of export obligation However the Authorisatione will have the option to

dispose off the product manufactured out of the duty free inputs once the export obligation iscompleted

Advance Authorisations shall be issued with a positive value addition

However for physical exports for which payments are not received in freely convertiblecurrency the same shall be subject to value addition as specified in Appendix-11 of Handbook(Vol1) In case of supplies to SEZ Units irrespective of the currency of realisation AdvanceAuthorisation shall be issued with a positive value addition

In case of Tea the minimum value addition under advance Authorisation shall be 100

In case of spices (covered by Chapter 9 of the ITC(HS) Classification of Export amp Import

Items 2004-09) the minimum value addition under advance Authorisation shall be 15

Advance Authorisation shall be issued in accordance with the Policy and procedure in force onthe date of issue of Authorisation

The validity period of advance Authorisation for import shall be as prescribed in the Handbook(Vol1)

The facility of Advance Authorisation shall also be available where some or all of the inputsare supplied free of cost to the exporter

In such cases for calculation of value addition the notional value of free of cost inputs along

with value of other duty-free inputs shall be taken into consideration

Export Obligation

The period for fulfilment of the export obligation under Advance Authorisation shall be asprescribed in the Handbook (Vol1)

Provision for BIFR units

Any firmcompany registered with BIFR or any firm company acquiring a unit which is under BIFR shall be allowed EOP extension as per the rehabilitation package prepared by theoperating agency subject to subsequent approval of BIFR

However in cases where the rehabilitation package does not specify the EOP extensionperiod a time period upto 5 years reckoned from the date of issue of Authorisation would bepermitted on merits of the case for fulfillment of export obligation

Similarly SSI units shall also be entitled for similar facility as per the rehabilitation scheme of the concerned State government However in cases where the State rehabilitation schemedoes not specify the export obligation extension period a time period upto 5 years reckonedfrom the date of issue of Authorisation would be permitted on merits of the case for fulfillmentof export obligation

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 320

Export Obligation Period Extension as mentioned above shall be without the payment of composition fee for cases where rehabilitation package has been announcedapproved

Advance Authorisation for annual requirement

Advance Authorisation can also be issued on the basis of annual requirement for physical

exports intermediate supplies and or deemed exports

One to Five Star Export House shall be entitled for the Advance Authorisation for annualrequirement All other categories of exporters having past export performance (in thepreceding two years) shall also be entitled for the Advance Authorisation for annualrequirement

In addition a merchant exporter shall also be issued the Advance Authorisation for AnnualRequirement provided they agree to the endorsement of the name(s) of the supportingmanufacturer(s) on the relevant Authorisation

The entitlement in terms of CIF value of imports under this scheme shall be upto 300 of theFOB value of physical export and or FOR value of deemed export in the preceding licensing

year or Rs 1 crore whichever is higher Such Authorisation shall have value addition

Advance Release Orders

An Advance Authorisation holder holder of advance Authorisation for annual requirementholder of Diamond Imprest Authorisation holder of DFIA and holder of DFRC intending tosource the inputs from indigenous sourcesState Trading Enterprises EOUSEZEHTPSTPBTP units in lieu of direct import has the option to source them against AdvanceRelease Orders denominated in free foreign exchange Indian rupees

The transferee of a DFRC shall also be eligible for ARO facility However supplies may beobtained against the Authorisation from EOU EHTPBTPSTPSEZ units without conversion

into ARO

The validity period of ARO shall be as prescribed in the Handbook (Vol1)

Back-to-Back Inland Letter of Credit

An Advance Authorisation holder holder of advanceAuthorisation for annual requirementholder of DFIA holder of Diamond Imprest Authorisation and holder of DFRC may instead of applying for an Advance Release Order avail of the facility of Back-to-Back Inland Letter of Credit in accordance with the procedure specified in Handbook of Procedures (Vol1)

Prohibited Items

Prohibited items of imports mentioned in ITC(HS) shall not be imported under the AdvanceAuthorisationDFIADFRC Further the items reserved for imports by State Trading Enterprisescannot be imported against advance Authorisation DFIADFRC However those items can beprocured from State Trading Enterprises against ARO or Invalidation letter issued to the holder of advance AuthorisationDFIADFRC The State Trading Enterprises are also allowed to sellthe goods on High Sea Sale basis to the holders of Advance AuthorisationDFIADFRC

In addition the State Trading Enterprises are permitted to issue No Objection Certificate(NOC)rsquo if they so desire for import by holder of advance Authorisation DFIA holders would

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 420

also be eligible to import such items based on No Objection Certificate (NOC) from the STEsfor only such products as notified by DGFT However the Authorisation Holder would berequired to file Quarterly Returns of the imports effected against such lsquoNo ObjectionCertificatersquo to the concerned State Trading Enterprises (STEs) and the STEs in turn wouldsubmit Half-yearly import figures of such imports to the concerned administrative Departmentfor monitoring with a copy endorsed to the Department of Commerce

Similarly prohibited items of exports mentioned in the ITC(HS) shall not be exported under theAuthorisation issued under the Advance AuthorisationDFIADFRC scheme Further export of restricted items shall be subject to all conditionalities or requirements of export Authorisationor permission as may be required under Schedule II of ITC (HS)

Admissibility of Drawback

In the case of an Advance Authorisation the drawback shall be available in respect of any of the duty paid materials whether imported or indigenous used in the goods exported as per the drawback rate fixed by Ministry of Finance (Directorate of Drawback) The Drawback shallhowever be restricted to the duty paid materials as mentioned in the application

Duty Free Replenishment Certificate (DFRC)

DFRC is issued to a merchant exporter or manufacturer exporter for the import of inputs usedin the manufacture of goods without payment of basic customs duty

However such inputs shall be subject to the payment of additional customs duty equal to theexcise duty at the time of import

DFRC shall be issued on minimum value addition of 25 except for items in gems and jewellery sector for which value addition as given in paragraph 4A21 of the Handbook of Procedures (Vol1) and items for which higher value addition is prescribed under AdvanceAuthorisation Scheme shall be applicable

DFRC may be issued for physical exports against freely convertible currency physicalexports to SEZ whether against freely convertible currency or non-convertible currencysupplies effected under paragraph 82 of the Policy (except for supplies made to DFRCholder)

DFRC may also be issued in respect of physical exports (other than supplies to SEZ) for whichpayments are received in non-convertible currency Such exports shall however be subject tovalue addition and conditions as specified in Appendix-11 of Handbook of Procedures (Vol1)

DFRC shall be issued only in respect of products covered under the Standard Input OutputNorms as notified by DGFT

However in respect of Standard Input Output Norms which are subject to actual usercondition or where the export proceeds have not been realised at the time of filing applicationor for import of fuel under the general norms DFRC shall be issued with actual user conditionfor these inputs

However for fuel the import entitlement may be transferred only to the companies which havebeen granted authorisation to market fuel by the Ministry of Petroleum amp Natural Gas

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 520

In cases where Standard Input Output Norms allow import of Acetic Anhydride Ephedrine andPseudo Ephedrine DFRC shall be issued provided these items are specifically deleted fromthe list of import items

DFRC will not be issued against SION which prescribe a prior import condition for inputs

DFRC shall be issued for import of inputs as per SION as indicated in the shipping bills Thevalidity of such Authorisations will be governed by the provision stipulated in the handbook(Vol I) DFRC and or the material(s) imported against it shall be freely transferable HoweverDFRC with actual user condition or the material(s) imported against it shall not be transferable

The export products which are eligible for modified VAT shall be eligible for CENVAT creditservice tax credit

However non excisable non dutiable or non CENVAT products shall be eligible for drawbackat the time of exports in lieu of additional customs duty to be paid at the time of imports under the scheme

The exporter shall be entitled for drawback benefits in respect of any of the duty paid

materials whether imported or indigenous used in the export product as per the drawbackrate fixed by Directorate of Drawback (Ministry of Finance)

The drawback shall however be restricted to the duty paid materials not covered under SION

Jobbing repairing etc for re-export

Import of goods including those mentioned as restricted in ITC(HS) but excluding prohibiteditems supplied free of cost may be permitted for the purpose of jobbing without aAuthorisationcertificate permission as per the terms of notification issued by Department of Revenue from time to time

Similarly import of goods for carrying out repairs re-conditioning re-engineering testing etcshall be allowed as per the terms and conditions of the Customs notification even though thegoods may be restricted for imports under the Foreign TradeITC(HS) Classification of Importsand Exports Book

Termination of the Scheme

DFRC Scheme shall be available for exports effected upto 3042006

The procedural aspects of Advance Authorisation Scheme (Erstwhile Advance LicenceScheme) are given in the Handbook of Procedures

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 620

Duty Entitlement Pass Book DEPB Secheme

Duty Entitlement Pass Book Scheme in short DEPB is an export incentive scheme Notified on141997 the DEPB Scheme consisted of (a) Post-export DEPB and (b) Pre-export DEPB The pre-export DEPB scheme was abolished wef 142000 Under the post-export DEPB which isissued after exports the exporter is given aduty entitlement Pass Book Scheme at a pre-determined credit on the FOB value The DEPBrates is allows import of any items except the items which are otherwise restricted for importsItems such as Gold Nibs Gold Pen Gold watches etc though covered under the genericdescription of writing instruments components of writing instruments and watches are thus noteligible for benefit under the DEPB scheme

The DEPB Rates are applied on the basis of FOB value or value cap whichever is lower For

example if the FOB value is Rs700- per piece and the value cap is Rs500- per piece theDEPB rate shall be applied on Rs500- The DEPB rate and the value cap shall be applicable asexisting on the date of exports as defined in paragraph 1515 of Handbook (Vol1)

DEPB Scheme is issued only on post-export basis and preexport DEPB Scheme has beendiscontinued The provisions of DEPB Scheme are mentioned in Para 43 and 431 to 435 of the Foreign Trade Policy or Exim Policy One significant change in the new DEPB Scheme isthat in terms of Para 435 of the Exim Policy even excise duty paid in cash on inputs used inthe manufacture of export product shall be eligible for brand rate of duty drawback as per rulesframed by Department of Revenue which was not mentioned in the earlier DEPB Scheme

Benefits of DEPB Rates

The benefit of DEPB schemes is available on the export products having extraneous material upto 5 by weight In such cases extraneous material up to 5 shall be ignored and the DEPB

rate as notified for that export product is be allowed

Review of DEPB Rates

The Government of India review the DEPB rates after getting the appropriate a export import

data on FOB value of exports and CIF value of inputs used in the export product as per SION Such data and information is usually obtained from the concerned Export Promotion Councils

Implementation of the DEPB Rates

Some additional facilities as listed below have been provided for better implementation of theDEPB Rates

bull DEPB rates rationalized to account for the changes in Customs duties

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 720

bull Caps fixed on certain items but there would be no verification of Present Market Value(PMV) on such items

bull A number of ports have been added for availing facilities under the Duty Exemption Scheme including DEPB

bull The threshold limit of Rs 200 million for fixing new DEPB rates removed

Provisional DEPB Rate

The main objective behind the provisional DEPB rates is to encourage diversification and to promote export of new products However provisional DEPB rates would be valid for a limited period of time during which exporter would furnish data on export and import for regular fixation of rates

Maintenance of Record

It is necessary for Custom House at ports to maintain a separate record of details of exports

made under DEPB Schemes

Port of Registration

The exportsimports made from the specified ports given shall be entitled for DEPB

Sea Ports Mumbai Kolkata Cochin Dahej Kakinada Kandla Mangalore MarmagoaMundra Chennai Nhavasheva Paradeep Pipavav Sikka Tuticorin Vishakhapatnam Surat(Magdalla) Nagapattinam Okha Dharamtar and Jamnagar

Airports Ahmedabad Bangalore Bhubaneshwar Mumbai Kolkata Coimbatore Air Cargo

Complex Cochin Delhi Hyderabad Jaipur Srinagar Trivandrum Varanasi Nagpur andChennai

ICDs Agra Ahmedabad Bangalore Bhiwadi Coimbatore Daulatabad (Wanjarwadi andMaliwada) Delhi Dighi (Pune) Faridabad Guntur Hyderabad Jaipur Jallandhar JodhpurKanpur Kota Ludhiana Madurai and the land Customs station at Ranaghat MallanpurMoradabad Meerut Nagpur Nasik Gauhati (Amingaon) Pimpri (Pune) Pitampur (Indore)Rudrapur (Nainital) Salem Singanalur Surat Tirupur Udaipur Vadodara Varanasi WalujBhilwara Pondicherry Garhi-Harsaru Bhatinda Dappar Chheharata (Amritsar) Karur Mirajand Rewari

LCSRanaghat Singhabad Raxaul Jogbani Nautanva ( Sonauli) Petrapole and Mahadipur

The exports made to the following Special Economic Zones (SEZ) are also entitled to DEPB

SEZ Santacruz Kandla Kochi Vishakhapatnam Chennai FALTA Surat NOIDA

Credit under DEPB and Present Market Value

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 820

In respect of products where rate of credit entitlement under DEPB Scheme comes to 10 or more amount of credit against each such export product shall not exceed 50 of Present MarketValue (PMV) of export product During export exporter shall declare on shipping bill that benefit under DEPB Scheme would not exceed 50 of PMV of export product

However PMV declaration shall not be applicable for products for which value cap existsirrespective of DEPB rate of product

Utilization of DEPB credit

Credit given under DEPB Schemes is utilized for payment of indian customs duty includingcapital goods which are free to import

Re-export of goods imported under DEPB Scheme

In case of return of any exported goods which has been found defective or unfit for use may be

again exported according to the exim guidelines as mentioned by the Department of Revenue

In such cases 98 of the credit amount debited against DEPB for the export of such goods isgenerated by the concerned Commissioner of Customs in the form of a Certificate containing the amount generated and the details of the original DEPB On the basis of certificate a freshDEPB is issued by the concerned DGFT Regional Authority It is important to note that theissued DEPB have the same port of registration and shall be valid for a period equivalent to the balance period available on the date of import of such defectiveunfit goods

DEPB Application Eligibility

Component of Special Additional Duty and indian customs duty on fuel shall also be allowedunder DEPB Scheme Rates (as a brand rate) in case of non-a ailment of CENVAT Credit

Neutralization shall be provided by way of grant of duty credit against export product

An exporter may apply for credit at specified percentage of FOB value of exports made infreely convertible currency or payment made from foreign currency account of SEZ unit SEZ

Developer in case of supply by DTA

Credit shall be available against such export products and at such rates as may be specified byDGFT by way of public notice Credit may be utilized for payment of a Customs Duty on freelyimportable items

DEPB holder shall have option to pay additional customs duty in cash as well

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 920

DEPB Application Pocedure for Application

An application for grant of credit under DEPB Rates may be made to RA concerned in Ayaat

Niryaat form ANF 4G along with prescribed documents Agency commission shall be allowed

for DEPB entitlement up to 125 of FOB value only FOB value in free foreign exchange shall be converted into Indian rupees as per exchange rate for exports notified by Ministry of Finance as applicable on the date of order of Let Export by Customs

In respect of consignment exports wherein exporter has declared FOB value on a provisional basis exporter shall be eligible for final assessment of such shipping bill based on actual FOBrealized upon sale of such goods in freely convertible currency

An application for grant of credit for supplies from DTA to SEZ can be made by DTA unit or SEZ unit DTA unit may claim benefits either fromRA or Development Commissioner concerned In case claim have been filed with RA RA while

allowing benefits to the DTA unit will simultaneously endorse a copy of communication toconcerned Development Commissioner along with details of export documents In case DTAsupplier prefers claim with Development Commissioner the Development Commissioner willverify Denied Entity List (DEL) status of supplier from DGFT website before allowing DEPB benefits SEZ unit will file application with Development Commissioner concerned in Ayaat

Niryaat Form ANF 4G along with prescribed documents

DEPB Rates shall be issued with transferable endorsement after payment confirmation In other cases DEPB Scheme shall be initially issued with non-transferable endorsement and uponrealization can be endorsed as transferable

DEPB Policy and Procedure for Application

and Benifits

Policy relating to Duty Entitlement Passbook (DEPB) Scheme is given in Chapter-4 of theIndian Foreign Trade Policy Duty credit under the DEPB scheme shall be calculated by takinginto account deemed import content of said export product as per Standard

Input Output Norms SION

Fixation of DEPB Rate

EPC is the governing body for receiving all applications for the fixation of DEPB rates Oncethe applications are submitted EPC verify the FOB value of exports as well as international priceof inputs covered under Standard Input Output Norms SION

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 1020

Exports in anticipation of DEPB Rate

No exports shall be allowed under DEPB scheme unless DEPB rate of concerned export productis notified

Port of Registration

Exports imports made from specified Sea Ports Airports ICD amp LCSs given in paragraph 419above of the Foreign Trade Policy DEPB shall be issued with single port of registration whichwill be port from where exports have been effected

Time Period

Wherever provisional shipment has been allowed by customs authorities DEPB against suchexports shall be issued only after release of shipping bill by Customs In such cases applicationfor DEPB shall be filed within six months from date of release of such shipping bill or six

months from date of realization whichever is later

Frequency of Application

All shipping bills in any one application must relate to exports made from one Custom Houseonly There is no limit on number of shipping bills which can be filed through EDI mode in asingle aplication

Verification by Customs

Before allowing imports against DEPB Customs shall verify that details of exports as given on

DEPB are as per their records However in case of EDI shipping bills issued on or after 1-10-2005 from EDI ports which are being transmitted electronically by Customs to DGFT DEPBsissued shall be sent to Customs at port of registration through an electronic message exchangesystem and DEPB shall be registered at port of registration electronically No verification of shipping bills against which such DEPBs have been issued will be required before allowingimports against these DEPBs

Re-export of goods imported under DEPB Scheme

Goods imported under DEPB scheme which are found defective or unfit for use may be re-exported as per guidelines given in paragraph 3236 of HBP v1

Issuance of DEPB and other duty credit certificates against lost EP copy of the Shipping

Bills

In case where EP copy of Shipping Bill has been lost DEPB and other duty credit certificatesclaim can be considered subject to submission of following documents-

bull A duplicate certified copy of Shipping Bill issued by Customs authority in lieu original

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 1120

bull An application fee equivalent to 2 of the DEPB or other duty credit entitlement inrespect of lost Shipping Bills However no fee shall be charged when Shipping Bill islost by Government agencies and a documentary proof to this effect is submitted

bull An affidavit by exporter about loss of Shipping Bills and an undertaking to surrender itimmediately to concerned RA if found subsequently and

bull

An indemnity bond by exporter to the effect that he would indemnify Government for financial loss if any on account of DEPB or other duty credit certificate issued againstlost Shipping Bills

Customs authority before allowing clearance shall ensure that no DEPB benefit has beenavailed against same shipping bill

Claim against lost Shipping Bill shall be preferred within a period of six months from date of release of duplicate copy of shipping bill and any application received thereafter will be rejectedHowever if a provisionally assessed DEPB shipping bill is lost time period for filing anapplication for DEPB would be six months from the date of release of the finally assessed

shipping bill

Loss of Original Bank Certificate

In such cases where original Bank Realization Certificate (BRC) has been lost the DEPB claimcan be considered subject to submission of following documents

bull A duplicate copy of BRC issued by bank authority in lieu of original loss b) Anapplication fee equivalent to 2 of the DEPB entitlement in respect of lost BRC

bull An affidavit by exporter about loss of BRC and an undertaking to surrender itimmediately to RA if found subsequently

bull

An indemnity bond by exporter to the effect that he would indemnify Government for financial loss if any on account of DEPB issued against lost BRC

Claim against lost BRC shall be preferred within a period of six months from date of realizationand application received thereafter will be rejected

In such cases where both documents have been lost exporter shall follow procedure laid downin paragraph 452 and 453 Time period for such application shall be as per paragraph 452 and453 whichever is later

DEPB General Instructions

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 1220

The DEPB Rates specified in book shall not be applicable to export of a commodity or productif such commodity or product is-

1 Manufactured partly or wholly in a warehouse under Section 65 of the Customs Act 1962 (52 of 1962)

2Manufactured andor exported in discharge of export obligation against an Advance License including Advance License for Annual Requirement or exported under DFRCScheme of the relevant EXIM Policy

3 Manufactured andor exported by a unit licensed as hundred percent export oriented unitinterms of the provisions of the relevantImport Policy and Export Policy

4 Manufactured andor exported by any of the units situated in free trade zones ExportProcessing Zone Special Economic zones EHTP Scheme

5 Exports of goods of foreign origin unless the goods have been manufactured or reprocessed or on which similar operations have been carried out in India

DEPB Rates Product Groups and DEPB Items

The DEPB rates are applicable on the following product categories

bull 61 Engineering Products

bull 62 Chemicals

bull 63 Plastics

bull 64 Leather and Leather Products

bull

65 Sports Goodsbull 66 Fish and Fish Products

bull 67 Food Products

bull 68 Handicrafts

bull 83 Electronics

bull 89 Textiles

bull 90 Miscellaneous Products

DGFT DEPB Rates Notification in India

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 1320

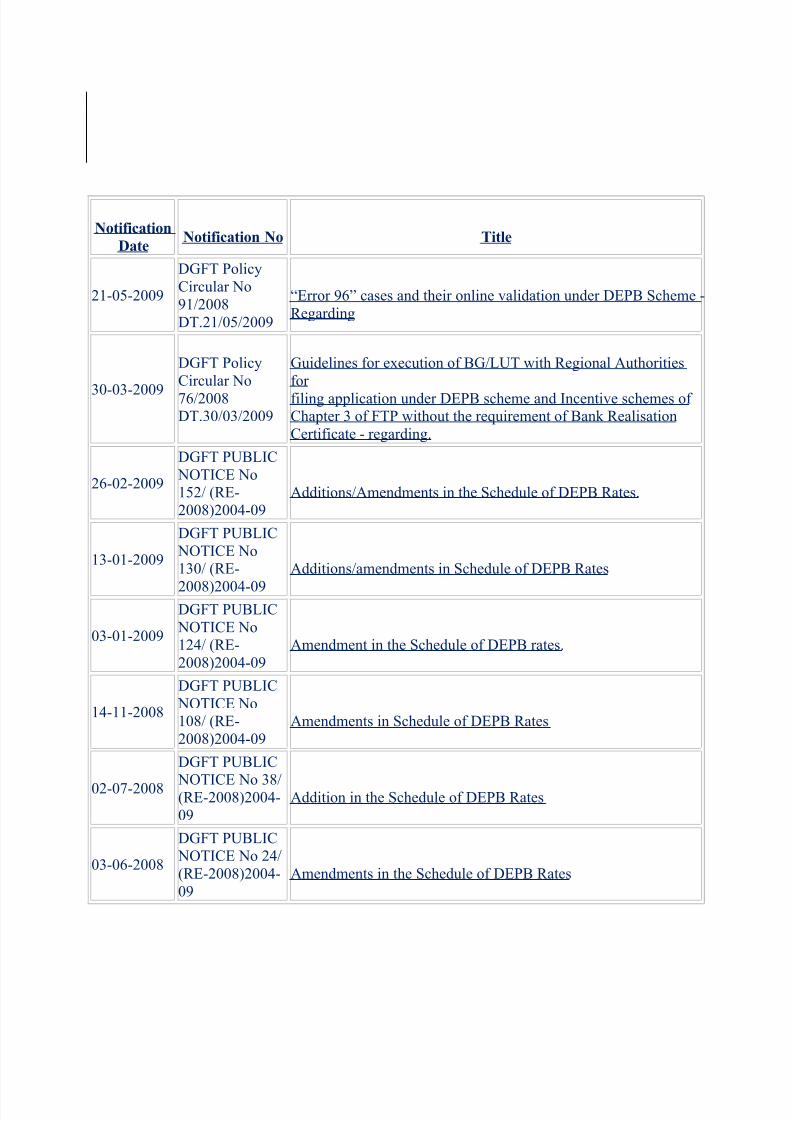

Notification

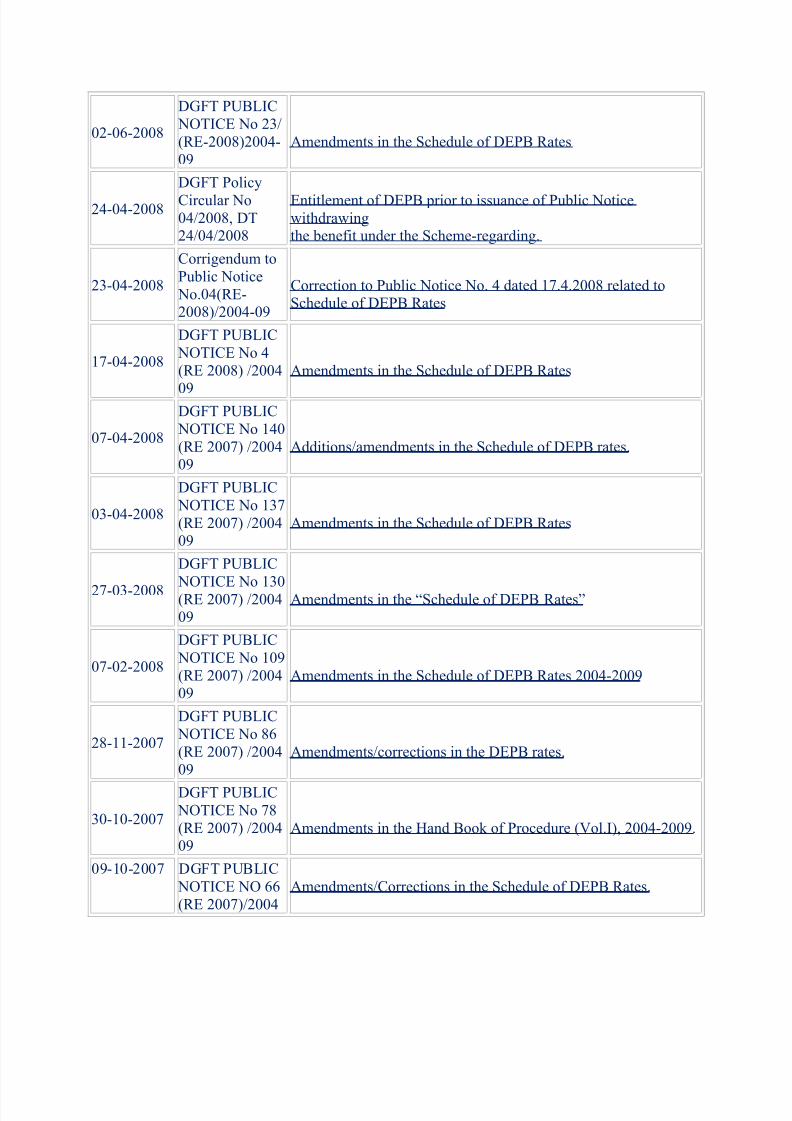

DateNotification No Title

21-05-2009

DGFT PolicyCircular No912008DT21052009

ldquoError 96rdquo cases and their online validation under DEPB Scheme -Regarding

30-03-2009

DGFT PolicyCircular No

762008DT30032009

Guidelines for execution of BGLUT with Regional Authoritiesfor

filing application under DEPB scheme and Incentive schemes of Chapter 3 of FTP without the requirement of Bank RealisationCertificate - regarding

26-02-2009

DGFT PUBLIC NOTICE No152 (RE-2008)2004-09

AdditionsAmendments in the Schedule of DEPB Rates

13-01-2009

DGFT PUBLIC NOTICE No130 (RE-

2008)2004-09

Additionsamendments in Schedule of DEPB Rates

03-01-2009

DGFT PUBLIC NOTICE No124 (RE-2008)2004-09

Amendment in the Schedule of DEPB rates

14-11-2008

DGFT PUBLIC NOTICE No108 (RE-2008)2004-09

Amendments in Schedule of DEPB Rates

02-07-2008

DGFT PUBLIC

NOTICE No 38(RE-2008)2004-09

Addition in the Schedule of DEPB Rates

03-06-2008

DGFT PUBLIC NOTICE No 24(RE-2008)2004-09

Amendments in the Schedule of DEPB Rates

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 1420

02-06-2008

DGFT PUBLIC NOTICE No 23(RE-2008)2004-09

Amendments in the Schedule of DEPB Rates

24-04-2008

DGFT Policy

Circular No042008 DT24042008

Entitlement of DEPB prior to issuance of Public Noticewithdrawingthe benefit under the Scheme-regarding

23-04-2008

Corrigendum toPublic Notice No04(RE-2008)2004-09

Correction to Public Notice No 4 dated 1742008 related toSchedule of DEPB Rates

17-04-2008

DGFT PUBLIC NOTICE No 4(RE 2008) 2004

09

Amendments in the Schedule of DEPB Rates

07-04-2008

DGFT PUBLIC NOTICE No 140(RE 2007) 200409

Additionsamendments in the Schedule of DEPB rates

03-04-2008

DGFT PUBLIC NOTICE No 137(RE 2007) 200409

Amendments in the Schedule of DEPB Rates

27-03-2008

DGFT PUBLIC

NOTICE No 130(RE 2007) 200409

Amendments in the ldquoSchedule of DEPB Ratesrdquo

07-02-2008

DGFT PUBLIC NOTICE No 109(RE 2007) 200409

Amendments in the Schedule of DEPB Rates 2004-2009

28-11-2007

DGFT PUBLIC NOTICE No 86(RE 2007) 200409

Amendmentscorrections in the DEPB rates

30-10-2007

DGFT PUBLIC NOTICE No 78(RE 2007) 200409

Amendments in the Hand Book of Procedure (VolI) 2004-2009

09-10-2007 DGFT PUBLIC NOTICE NO 66(RE 2007)2004

AmendmentsCorrections in the Schedule of DEPB Rates

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 1520

2009

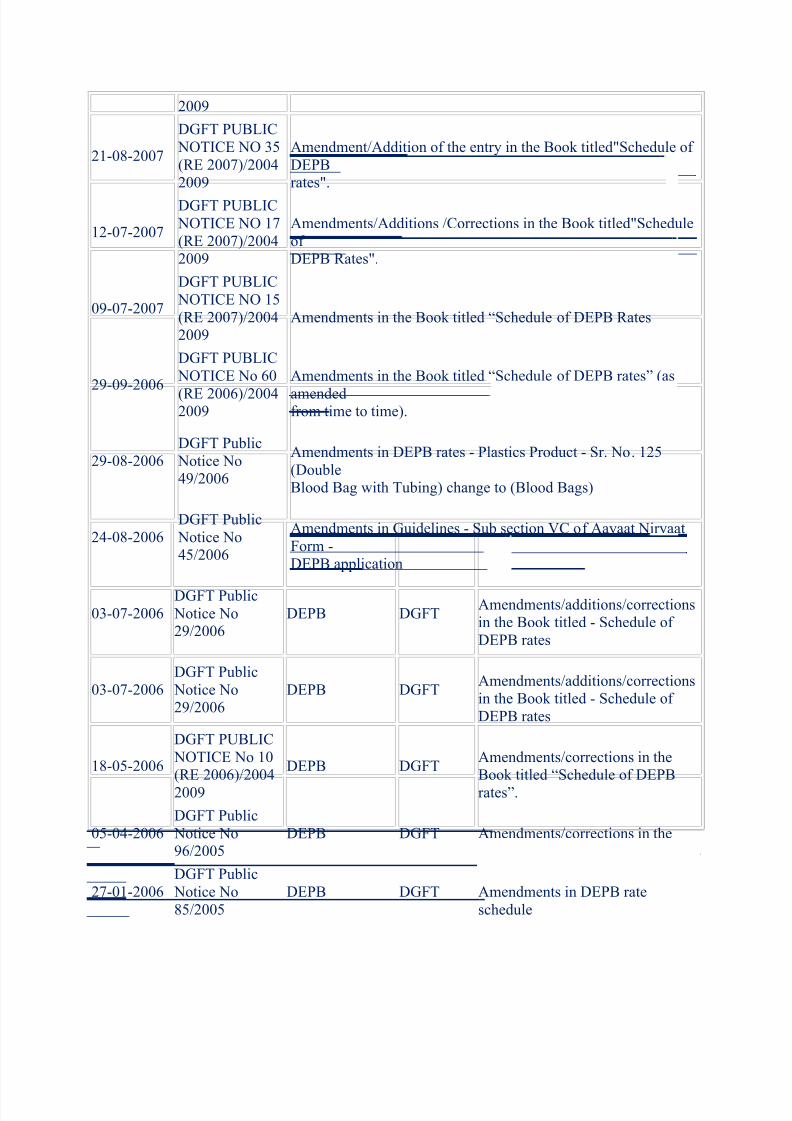

21-08-2007

DGFT PUBLIC NOTICE NO 35(RE 2007)20042009

AmendmentAddition of the entry in the Book titledSchedule of DEPBrates

12-07-2007

DGFT PUBLIC NOTICE NO 17(RE 2007)20042009

AmendmentsAdditions Corrections in the Book titledScheduleof DEPB Rates

09-07-2007

DGFT PUBLIC NOTICE NO 15(RE 2007)20042009

Amendments in the Book titled ldquoSchedule of DEPB Rates

29-09-2006

DGFT PUBLIC NOTICE No 60

(RE 2006)20042009

Amendments in the Book titled ldquoSchedule of DEPB ratesrdquo (as

amendedfrom time to time)

29-08-2006DGFT Public Notice No492006

Amendments in DEPB rates - Plastics Product - Sr No 125(DoubleBlood Bag with Tubing) change to (Blood Bags)

24-08-2006DGFT Public Notice No452006

Amendments in Guidelines - Sub section VC of Aayaat NiryaatForm -DEPB application

03-07-2006DGFT Public Notice No292006

DEPB DGFTAmendmentsadditionscorrectionsin the Book titled - Schedule of DEPB rates

03-07-2006DGFT Public Notice No292006

DEPB DGFTAmendmentsadditionscorrectionsin the Book titled - Schedule of DEPB rates

18-05-2006

DGFT PUBLIC NOTICE No 10(RE 2006)20042009

DEPB DGFTAmendmentscorrections in theBook titled ldquoSchedule of DEPBratesrdquo

05-04-2006DGFT Public Notice No962005

DEPB DGFT Amendmentscorrections in theBook titled Schedule of DEPB rates

27-01-2006DGFT Public Notice No852005

DEPB DGFT Amendments in DEPB rateschedule

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 1620

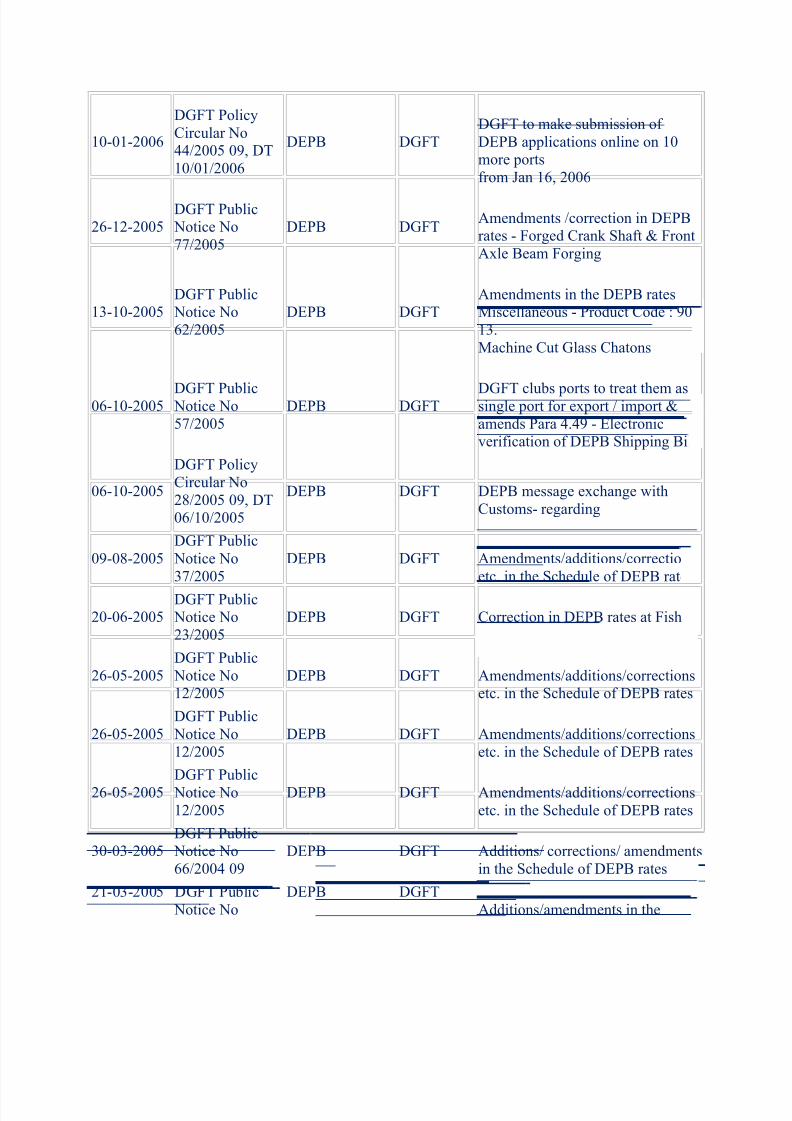

10-01-2006

DGFT PolicyCircular No442005 09 DT10012006

DEPB DGFTDGFT to make submission of DEPB applications online on 10more portsfrom Jan 16 2006

26-12-2005DGFT Public Notice No772005

DEPB DGFTAmendments correction in DEPBrates - Forged Crank Shaft amp FrontAxle Beam Forging

13-10-2005DGFT Public Notice No622005

DEPB DGFTAmendments in the DEPB ratesMiscellaneous - Product Code 90 -13Machine Cut Glass Chatons

06-10-2005 DGFT Public Notice No572005

DEPB DGFT DGFT clubs ports to treat them assingle port for export import ampamends Para 449 - Electronicverification of DEPB Shipping Bills

06-10-2005

DGFT PolicyCircular No282005 09 DT06102005

DEPB DGFT DEPB message exchange withCustoms- regarding

09-08-2005DGFT Public Notice No372005

DEPB DGFT Amendmentsadditionscorrectionsetc in the Schedule of DEPB rates

20-06-2005DGFT Public Notice No232005

DEPB DGFT Correction in DEPB rates at Fishand Fish Products - Sl NO 2

26-05-2005DGFT Public Notice No122005

DEPB DGFT Amendmentsadditionscorrectionsetc in the Schedule of DEPB rates

26-05-2005DGFT Public Notice No122005

DEPB DGFT Amendmentsadditionscorrectionsetc in the Schedule of DEPB rates

26-05-2005DGFT Public Notice No122005

DEPB DGFT Amendmentsadditionscorrectionsetc in the Schedule of DEPB rates

30-03-2005DGFT Public Notice No662004 09

DEPB DGFT Additions corrections amendmentsin the Schedule of DEPB rates

21-03-2005 DGFT Public Notice No

DEPB DGFTAdditionsamendments in the

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 1720

622004 09 DEPB rates

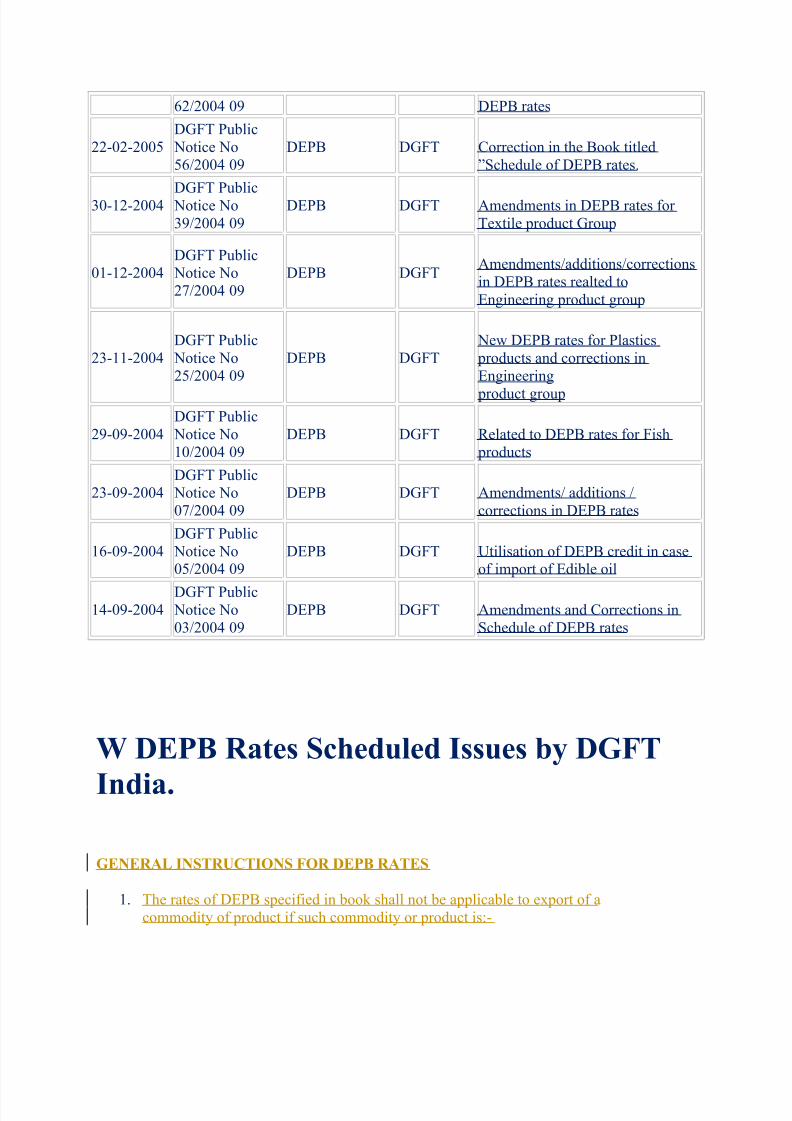

22-02-2005DGFT Public Notice No562004 09

DEPB DGFT Correction in the Book titledrdquoSchedule of DEPB rates

30-12-2004DGFT Public Notice No392004 09

DEPB DGFT Amendments in DEPB rates for Textile product Group

01-12-2004DGFT Public Notice No272004 09

DEPB DGFTAmendmentsadditionscorrectionsin DEPB rates realted toEngineering product group

23-11-2004DGFT Public Notice No252004 09

DEPB DGFT New DEPB rates for Plastics products and corrections inEngineering

product group

29-09-2004DGFT Public Notice No102004 09

DEPB DGFT Related to DEPB rates for Fish products

23-09-2004DGFT Public Notice No072004 09

DEPB DGFT Amendments additions corrections in DEPB rates

16-09-2004DGFT Public Notice No052004 09

DEPB DGFT Utilisation of DEPB credit in caseof import of Edible oil

14-09-2004DGFT Public Notice No032004 09

DEPB DGFT Amendments and Corrections inSchedule of DEPB rates

W DEPB Rates Scheduled Issues by DGFT

India

GENERAL INSTRUCTIONS FOR DEPB RATES

1 The rates of DEPB specified in book shall not be applicable to export of acommodity of product if such commodity or product is-

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 1820

a Manufactured partly or wholly in a warehouse under Section 65 of the CustomsAct 1962 (52 of 1962) b Manufacture andor exported in discharge of export obligation against anAdvance Autorisation including Advance Authorisation for Annual Requirement or exported under DFIA Scheme of the relevant Foreign Trade Policy

c Manufacture andor exported by a unit licenced as 100 Export Oriented Unitin terms of the provisions of the relevant Foreign Trade Policyd Manufactured and or exported by any of the units situated in Free TradeZonesExport Processing ZoneSpecial Economic ZonesEHTP Schemee Exports of goods of foreign origin unless the goods have been manufacturedor processed or on which similar operations have been carried out in Indiaf Exports made under paragraph 235 and 236 of the Foreign Trade Policy

2 The DEPB rate and the value cap shall be applicable as existing on the dateof order of ldquolet exportrdquo by the Customs

3 The value cap wherever existing shall be with reference to the FOB value of

exports The DEPB rates shall be applied on the FOB value or value cap whichever is lower For example if the FOB value is Rs500- per piece and the value capis Rs300- per piece the DEPB rate shall be applied on Rs300-

4 Wherever any specific rate exists for a particular item under DEPB rate listas given in this book the items shall not be covered under any genericdescription of the DEPB rate list

5 The DEPB rate aims to neutralize the incidence of duty on the inputs used inthe export product Therefore the DEPB rates as given in this book refer tonormally tradableexportable product Items such as Gold Nibs Gold Pen Goldwatches etc though covered under the generic description of writinginstructions components of writing instruments and watches are thus not

eligible for benefit under the DEPB scheme6 The DEPB rates given for various galvanized Engineering product shall cover non galvanised products and vice-a-versa

7 The DEPB rate given for various types of garments do not cover Silk as wellas Woolen garments unless specifically mentioned in the DEPB description

8 Portable product at SNo239 240241242243 and 286 of Product GroupEngineering (Product Code 61) exported in the form of incomplete CKDSKD Kit but consisting of (i) Engine (ii) Chassis (iii) Gear Box (iv) TransmissionAssembly system (v) Axle (Front amp Rear) and (vi) Suspension System or BodyCabor both shall be treated at par with complete CKDSKD Kit for the purpose of relevant DEPB benefits

9 The DEPB rate for formulation consisting of more than one bulk drug would becalculated as per provisions of Policy Circular No20 dated 31st July 2000

10 Wherever the export of resultant product in completely built form is allowedunder DEPB the CKDSKD export of such product shall also be allowed under DEPB

11 DEPB benefit would also be admissible on the export of composite productincluding assembled product having more than one constituent items for whichDEPB rates are individually fixed In such cases the DEPB entitlement would berestricted to the lowest of the rate applicable to the constituent items

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 1920

ignoring the rate of the constituent item(s) having weight less than 5 of thetotal net weight of such product However no DEPB benefit would be admissibleon the exportof such product if constituent item(s) is weighing more than 5 of the total net weight (of the product) and does not have any DEPB rate fixed

The exporters shall declare in the shipping bill the following details also for claiming DEPB benefit on the export of such product

i Description of the composite product including the assembled productalongwith its total net weightii Description of all the constitute item(s) of such products which attract aDEPB rate with their respective DEPB Nos and their credit rate alongwith totalweight of such constituent (s)iii Description and combined total weight of those constituent item(s) whichhave no DEPB rate in the schedule

(Explanatory Note)

In case (iii) above is more than 5 of total weight given in (i) no DEPB on thecomposite product would be admissible

12 DEPB benefit would be available on the export of products having extraneousmaterial upto 5 by weight In such cases extraneous material upto 5 shall beignored and the DEPB rate as notified for that export product shall be allowed

13 14 year old Duty Entitlement Pass Book ( DEPB ) is abolsihed from 1st October 2011and those items on which DEPB was allowed are shifted to Duty Drawback Scheme Thus Centre has now enhanced numbers of items under Duty Drawback to 4000 items

14 The move to scrap the DEPB is considered non-compatibility with Indiarsquos obligations atthe World Trade Organisation (WTO) DEPB scheme was on ventilation since 2005finally scrapped it from October 1 Presently there are 2130 items under DEPB that areallowed refunds on import duty paid on those items manufacture for export purposes

15 Under duty drawback scheme an equal amount is spent as tax refunds Central Board of Excise and Customs chairman Sumit Dutt Majumder said adding the revenue foregonewith the withdrawal of DEPB would be less The notification of the new rates will beissued in the next few days

16 Of the 1100 items being shifted to DDS there would be a ceiling of 55 per cent taxrefund rate on 660 items However the ceiling would not apply to 340 items includingworsted woolen yarn blanket nylon twine cut polished chat stones polyester metallisedfilm

17 Though exports have shown a remarkable performance growing by 542 per cent between April-August 2011 to $1345 billion there are concerns that the momentum maynot be sustained in the wake of economic crisis in US and Europe

18 A top Finance Ministry Official said ldquowhile there would be a minor reduction in dutydrawback rates for most items due care has been taken to ensure that the reduction iscapped at 10 per cent of the existing duty drawback ratesrdquo

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 2020

19 He also said government has decided to provide a smooth transition for the 1100 DEPBitems while incorporating these in the drawback schedule ldquoAs a transitory arrangementthese items will suffer a modest reduction in the existing DEPB rates to the extent of 1-3 per cent

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 220

supplies covered under sub-paragraph (h) amp (i) of paragraph Categories of Supply of SectionDeemed Exports of this site will not be exempted from the payment of applicable anti-dumping and safeguard duty if any

Advance Authorisation andor materials imported thereunder shall not be transferable evenafter completion of export obligation However the Authorisatione will have the option to

dispose off the product manufactured out of the duty free inputs once the export obligation iscompleted

Advance Authorisations shall be issued with a positive value addition

However for physical exports for which payments are not received in freely convertiblecurrency the same shall be subject to value addition as specified in Appendix-11 of Handbook(Vol1) In case of supplies to SEZ Units irrespective of the currency of realisation AdvanceAuthorisation shall be issued with a positive value addition

In case of Tea the minimum value addition under advance Authorisation shall be 100

In case of spices (covered by Chapter 9 of the ITC(HS) Classification of Export amp Import

Items 2004-09) the minimum value addition under advance Authorisation shall be 15

Advance Authorisation shall be issued in accordance with the Policy and procedure in force onthe date of issue of Authorisation

The validity period of advance Authorisation for import shall be as prescribed in the Handbook(Vol1)

The facility of Advance Authorisation shall also be available where some or all of the inputsare supplied free of cost to the exporter

In such cases for calculation of value addition the notional value of free of cost inputs along

with value of other duty-free inputs shall be taken into consideration

Export Obligation

The period for fulfilment of the export obligation under Advance Authorisation shall be asprescribed in the Handbook (Vol1)

Provision for BIFR units

Any firmcompany registered with BIFR or any firm company acquiring a unit which is under BIFR shall be allowed EOP extension as per the rehabilitation package prepared by theoperating agency subject to subsequent approval of BIFR

However in cases where the rehabilitation package does not specify the EOP extensionperiod a time period upto 5 years reckoned from the date of issue of Authorisation would bepermitted on merits of the case for fulfillment of export obligation

Similarly SSI units shall also be entitled for similar facility as per the rehabilitation scheme of the concerned State government However in cases where the State rehabilitation schemedoes not specify the export obligation extension period a time period upto 5 years reckonedfrom the date of issue of Authorisation would be permitted on merits of the case for fulfillmentof export obligation

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 320

Export Obligation Period Extension as mentioned above shall be without the payment of composition fee for cases where rehabilitation package has been announcedapproved

Advance Authorisation for annual requirement

Advance Authorisation can also be issued on the basis of annual requirement for physical

exports intermediate supplies and or deemed exports

One to Five Star Export House shall be entitled for the Advance Authorisation for annualrequirement All other categories of exporters having past export performance (in thepreceding two years) shall also be entitled for the Advance Authorisation for annualrequirement

In addition a merchant exporter shall also be issued the Advance Authorisation for AnnualRequirement provided they agree to the endorsement of the name(s) of the supportingmanufacturer(s) on the relevant Authorisation

The entitlement in terms of CIF value of imports under this scheme shall be upto 300 of theFOB value of physical export and or FOR value of deemed export in the preceding licensing

year or Rs 1 crore whichever is higher Such Authorisation shall have value addition

Advance Release Orders

An Advance Authorisation holder holder of advance Authorisation for annual requirementholder of Diamond Imprest Authorisation holder of DFIA and holder of DFRC intending tosource the inputs from indigenous sourcesState Trading Enterprises EOUSEZEHTPSTPBTP units in lieu of direct import has the option to source them against AdvanceRelease Orders denominated in free foreign exchange Indian rupees

The transferee of a DFRC shall also be eligible for ARO facility However supplies may beobtained against the Authorisation from EOU EHTPBTPSTPSEZ units without conversion

into ARO

The validity period of ARO shall be as prescribed in the Handbook (Vol1)

Back-to-Back Inland Letter of Credit

An Advance Authorisation holder holder of advanceAuthorisation for annual requirementholder of DFIA holder of Diamond Imprest Authorisation and holder of DFRC may instead of applying for an Advance Release Order avail of the facility of Back-to-Back Inland Letter of Credit in accordance with the procedure specified in Handbook of Procedures (Vol1)

Prohibited Items

Prohibited items of imports mentioned in ITC(HS) shall not be imported under the AdvanceAuthorisationDFIADFRC Further the items reserved for imports by State Trading Enterprisescannot be imported against advance Authorisation DFIADFRC However those items can beprocured from State Trading Enterprises against ARO or Invalidation letter issued to the holder of advance AuthorisationDFIADFRC The State Trading Enterprises are also allowed to sellthe goods on High Sea Sale basis to the holders of Advance AuthorisationDFIADFRC

In addition the State Trading Enterprises are permitted to issue No Objection Certificate(NOC)rsquo if they so desire for import by holder of advance Authorisation DFIA holders would

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 420

also be eligible to import such items based on No Objection Certificate (NOC) from the STEsfor only such products as notified by DGFT However the Authorisation Holder would berequired to file Quarterly Returns of the imports effected against such lsquoNo ObjectionCertificatersquo to the concerned State Trading Enterprises (STEs) and the STEs in turn wouldsubmit Half-yearly import figures of such imports to the concerned administrative Departmentfor monitoring with a copy endorsed to the Department of Commerce

Similarly prohibited items of exports mentioned in the ITC(HS) shall not be exported under theAuthorisation issued under the Advance AuthorisationDFIADFRC scheme Further export of restricted items shall be subject to all conditionalities or requirements of export Authorisationor permission as may be required under Schedule II of ITC (HS)

Admissibility of Drawback

In the case of an Advance Authorisation the drawback shall be available in respect of any of the duty paid materials whether imported or indigenous used in the goods exported as per the drawback rate fixed by Ministry of Finance (Directorate of Drawback) The Drawback shallhowever be restricted to the duty paid materials as mentioned in the application

Duty Free Replenishment Certificate (DFRC)

DFRC is issued to a merchant exporter or manufacturer exporter for the import of inputs usedin the manufacture of goods without payment of basic customs duty

However such inputs shall be subject to the payment of additional customs duty equal to theexcise duty at the time of import

DFRC shall be issued on minimum value addition of 25 except for items in gems and jewellery sector for which value addition as given in paragraph 4A21 of the Handbook of Procedures (Vol1) and items for which higher value addition is prescribed under AdvanceAuthorisation Scheme shall be applicable

DFRC may be issued for physical exports against freely convertible currency physicalexports to SEZ whether against freely convertible currency or non-convertible currencysupplies effected under paragraph 82 of the Policy (except for supplies made to DFRCholder)

DFRC may also be issued in respect of physical exports (other than supplies to SEZ) for whichpayments are received in non-convertible currency Such exports shall however be subject tovalue addition and conditions as specified in Appendix-11 of Handbook of Procedures (Vol1)

DFRC shall be issued only in respect of products covered under the Standard Input OutputNorms as notified by DGFT

However in respect of Standard Input Output Norms which are subject to actual usercondition or where the export proceeds have not been realised at the time of filing applicationor for import of fuel under the general norms DFRC shall be issued with actual user conditionfor these inputs

However for fuel the import entitlement may be transferred only to the companies which havebeen granted authorisation to market fuel by the Ministry of Petroleum amp Natural Gas

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 520

In cases where Standard Input Output Norms allow import of Acetic Anhydride Ephedrine andPseudo Ephedrine DFRC shall be issued provided these items are specifically deleted fromthe list of import items

DFRC will not be issued against SION which prescribe a prior import condition for inputs

DFRC shall be issued for import of inputs as per SION as indicated in the shipping bills Thevalidity of such Authorisations will be governed by the provision stipulated in the handbook(Vol I) DFRC and or the material(s) imported against it shall be freely transferable HoweverDFRC with actual user condition or the material(s) imported against it shall not be transferable

The export products which are eligible for modified VAT shall be eligible for CENVAT creditservice tax credit

However non excisable non dutiable or non CENVAT products shall be eligible for drawbackat the time of exports in lieu of additional customs duty to be paid at the time of imports under the scheme

The exporter shall be entitled for drawback benefits in respect of any of the duty paid

materials whether imported or indigenous used in the export product as per the drawbackrate fixed by Directorate of Drawback (Ministry of Finance)

The drawback shall however be restricted to the duty paid materials not covered under SION

Jobbing repairing etc for re-export

Import of goods including those mentioned as restricted in ITC(HS) but excluding prohibiteditems supplied free of cost may be permitted for the purpose of jobbing without aAuthorisationcertificate permission as per the terms of notification issued by Department of Revenue from time to time

Similarly import of goods for carrying out repairs re-conditioning re-engineering testing etcshall be allowed as per the terms and conditions of the Customs notification even though thegoods may be restricted for imports under the Foreign TradeITC(HS) Classification of Importsand Exports Book

Termination of the Scheme

DFRC Scheme shall be available for exports effected upto 3042006

The procedural aspects of Advance Authorisation Scheme (Erstwhile Advance LicenceScheme) are given in the Handbook of Procedures

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 620

Duty Entitlement Pass Book DEPB Secheme

Duty Entitlement Pass Book Scheme in short DEPB is an export incentive scheme Notified on141997 the DEPB Scheme consisted of (a) Post-export DEPB and (b) Pre-export DEPB The pre-export DEPB scheme was abolished wef 142000 Under the post-export DEPB which isissued after exports the exporter is given aduty entitlement Pass Book Scheme at a pre-determined credit on the FOB value The DEPBrates is allows import of any items except the items which are otherwise restricted for importsItems such as Gold Nibs Gold Pen Gold watches etc though covered under the genericdescription of writing instruments components of writing instruments and watches are thus noteligible for benefit under the DEPB scheme

The DEPB Rates are applied on the basis of FOB value or value cap whichever is lower For

example if the FOB value is Rs700- per piece and the value cap is Rs500- per piece theDEPB rate shall be applied on Rs500- The DEPB rate and the value cap shall be applicable asexisting on the date of exports as defined in paragraph 1515 of Handbook (Vol1)

DEPB Scheme is issued only on post-export basis and preexport DEPB Scheme has beendiscontinued The provisions of DEPB Scheme are mentioned in Para 43 and 431 to 435 of the Foreign Trade Policy or Exim Policy One significant change in the new DEPB Scheme isthat in terms of Para 435 of the Exim Policy even excise duty paid in cash on inputs used inthe manufacture of export product shall be eligible for brand rate of duty drawback as per rulesframed by Department of Revenue which was not mentioned in the earlier DEPB Scheme

Benefits of DEPB Rates

The benefit of DEPB schemes is available on the export products having extraneous material upto 5 by weight In such cases extraneous material up to 5 shall be ignored and the DEPB

rate as notified for that export product is be allowed

Review of DEPB Rates

The Government of India review the DEPB rates after getting the appropriate a export import

data on FOB value of exports and CIF value of inputs used in the export product as per SION Such data and information is usually obtained from the concerned Export Promotion Councils

Implementation of the DEPB Rates

Some additional facilities as listed below have been provided for better implementation of theDEPB Rates

bull DEPB rates rationalized to account for the changes in Customs duties

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 720

bull Caps fixed on certain items but there would be no verification of Present Market Value(PMV) on such items

bull A number of ports have been added for availing facilities under the Duty Exemption Scheme including DEPB

bull The threshold limit of Rs 200 million for fixing new DEPB rates removed

Provisional DEPB Rate

The main objective behind the provisional DEPB rates is to encourage diversification and to promote export of new products However provisional DEPB rates would be valid for a limited period of time during which exporter would furnish data on export and import for regular fixation of rates

Maintenance of Record

It is necessary for Custom House at ports to maintain a separate record of details of exports

made under DEPB Schemes

Port of Registration

The exportsimports made from the specified ports given shall be entitled for DEPB

Sea Ports Mumbai Kolkata Cochin Dahej Kakinada Kandla Mangalore MarmagoaMundra Chennai Nhavasheva Paradeep Pipavav Sikka Tuticorin Vishakhapatnam Surat(Magdalla) Nagapattinam Okha Dharamtar and Jamnagar

Airports Ahmedabad Bangalore Bhubaneshwar Mumbai Kolkata Coimbatore Air Cargo

Complex Cochin Delhi Hyderabad Jaipur Srinagar Trivandrum Varanasi Nagpur andChennai

ICDs Agra Ahmedabad Bangalore Bhiwadi Coimbatore Daulatabad (Wanjarwadi andMaliwada) Delhi Dighi (Pune) Faridabad Guntur Hyderabad Jaipur Jallandhar JodhpurKanpur Kota Ludhiana Madurai and the land Customs station at Ranaghat MallanpurMoradabad Meerut Nagpur Nasik Gauhati (Amingaon) Pimpri (Pune) Pitampur (Indore)Rudrapur (Nainital) Salem Singanalur Surat Tirupur Udaipur Vadodara Varanasi WalujBhilwara Pondicherry Garhi-Harsaru Bhatinda Dappar Chheharata (Amritsar) Karur Mirajand Rewari

LCSRanaghat Singhabad Raxaul Jogbani Nautanva ( Sonauli) Petrapole and Mahadipur

The exports made to the following Special Economic Zones (SEZ) are also entitled to DEPB

SEZ Santacruz Kandla Kochi Vishakhapatnam Chennai FALTA Surat NOIDA

Credit under DEPB and Present Market Value

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 820

In respect of products where rate of credit entitlement under DEPB Scheme comes to 10 or more amount of credit against each such export product shall not exceed 50 of Present MarketValue (PMV) of export product During export exporter shall declare on shipping bill that benefit under DEPB Scheme would not exceed 50 of PMV of export product

However PMV declaration shall not be applicable for products for which value cap existsirrespective of DEPB rate of product

Utilization of DEPB credit

Credit given under DEPB Schemes is utilized for payment of indian customs duty includingcapital goods which are free to import

Re-export of goods imported under DEPB Scheme

In case of return of any exported goods which has been found defective or unfit for use may be

again exported according to the exim guidelines as mentioned by the Department of Revenue

In such cases 98 of the credit amount debited against DEPB for the export of such goods isgenerated by the concerned Commissioner of Customs in the form of a Certificate containing the amount generated and the details of the original DEPB On the basis of certificate a freshDEPB is issued by the concerned DGFT Regional Authority It is important to note that theissued DEPB have the same port of registration and shall be valid for a period equivalent to the balance period available on the date of import of such defectiveunfit goods

DEPB Application Eligibility

Component of Special Additional Duty and indian customs duty on fuel shall also be allowedunder DEPB Scheme Rates (as a brand rate) in case of non-a ailment of CENVAT Credit

Neutralization shall be provided by way of grant of duty credit against export product

An exporter may apply for credit at specified percentage of FOB value of exports made infreely convertible currency or payment made from foreign currency account of SEZ unit SEZ

Developer in case of supply by DTA

Credit shall be available against such export products and at such rates as may be specified byDGFT by way of public notice Credit may be utilized for payment of a Customs Duty on freelyimportable items

DEPB holder shall have option to pay additional customs duty in cash as well

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 920

DEPB Application Pocedure for Application

An application for grant of credit under DEPB Rates may be made to RA concerned in Ayaat

Niryaat form ANF 4G along with prescribed documents Agency commission shall be allowed

for DEPB entitlement up to 125 of FOB value only FOB value in free foreign exchange shall be converted into Indian rupees as per exchange rate for exports notified by Ministry of Finance as applicable on the date of order of Let Export by Customs

In respect of consignment exports wherein exporter has declared FOB value on a provisional basis exporter shall be eligible for final assessment of such shipping bill based on actual FOBrealized upon sale of such goods in freely convertible currency

An application for grant of credit for supplies from DTA to SEZ can be made by DTA unit or SEZ unit DTA unit may claim benefits either fromRA or Development Commissioner concerned In case claim have been filed with RA RA while

allowing benefits to the DTA unit will simultaneously endorse a copy of communication toconcerned Development Commissioner along with details of export documents In case DTAsupplier prefers claim with Development Commissioner the Development Commissioner willverify Denied Entity List (DEL) status of supplier from DGFT website before allowing DEPB benefits SEZ unit will file application with Development Commissioner concerned in Ayaat

Niryaat Form ANF 4G along with prescribed documents

DEPB Rates shall be issued with transferable endorsement after payment confirmation In other cases DEPB Scheme shall be initially issued with non-transferable endorsement and uponrealization can be endorsed as transferable

DEPB Policy and Procedure for Application

and Benifits

Policy relating to Duty Entitlement Passbook (DEPB) Scheme is given in Chapter-4 of theIndian Foreign Trade Policy Duty credit under the DEPB scheme shall be calculated by takinginto account deemed import content of said export product as per Standard

Input Output Norms SION

Fixation of DEPB Rate

EPC is the governing body for receiving all applications for the fixation of DEPB rates Oncethe applications are submitted EPC verify the FOB value of exports as well as international priceof inputs covered under Standard Input Output Norms SION

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 1020

Exports in anticipation of DEPB Rate

No exports shall be allowed under DEPB scheme unless DEPB rate of concerned export productis notified

Port of Registration

Exports imports made from specified Sea Ports Airports ICD amp LCSs given in paragraph 419above of the Foreign Trade Policy DEPB shall be issued with single port of registration whichwill be port from where exports have been effected

Time Period

Wherever provisional shipment has been allowed by customs authorities DEPB against suchexports shall be issued only after release of shipping bill by Customs In such cases applicationfor DEPB shall be filed within six months from date of release of such shipping bill or six

months from date of realization whichever is later

Frequency of Application

All shipping bills in any one application must relate to exports made from one Custom Houseonly There is no limit on number of shipping bills which can be filed through EDI mode in asingle aplication

Verification by Customs

Before allowing imports against DEPB Customs shall verify that details of exports as given on

DEPB are as per their records However in case of EDI shipping bills issued on or after 1-10-2005 from EDI ports which are being transmitted electronically by Customs to DGFT DEPBsissued shall be sent to Customs at port of registration through an electronic message exchangesystem and DEPB shall be registered at port of registration electronically No verification of shipping bills against which such DEPBs have been issued will be required before allowingimports against these DEPBs

Re-export of goods imported under DEPB Scheme

Goods imported under DEPB scheme which are found defective or unfit for use may be re-exported as per guidelines given in paragraph 3236 of HBP v1

Issuance of DEPB and other duty credit certificates against lost EP copy of the Shipping

Bills

In case where EP copy of Shipping Bill has been lost DEPB and other duty credit certificatesclaim can be considered subject to submission of following documents-

bull A duplicate certified copy of Shipping Bill issued by Customs authority in lieu original

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 1120

bull An application fee equivalent to 2 of the DEPB or other duty credit entitlement inrespect of lost Shipping Bills However no fee shall be charged when Shipping Bill islost by Government agencies and a documentary proof to this effect is submitted

bull An affidavit by exporter about loss of Shipping Bills and an undertaking to surrender itimmediately to concerned RA if found subsequently and

bull

An indemnity bond by exporter to the effect that he would indemnify Government for financial loss if any on account of DEPB or other duty credit certificate issued againstlost Shipping Bills

Customs authority before allowing clearance shall ensure that no DEPB benefit has beenavailed against same shipping bill

Claim against lost Shipping Bill shall be preferred within a period of six months from date of release of duplicate copy of shipping bill and any application received thereafter will be rejectedHowever if a provisionally assessed DEPB shipping bill is lost time period for filing anapplication for DEPB would be six months from the date of release of the finally assessed

shipping bill

Loss of Original Bank Certificate

In such cases where original Bank Realization Certificate (BRC) has been lost the DEPB claimcan be considered subject to submission of following documents

bull A duplicate copy of BRC issued by bank authority in lieu of original loss b) Anapplication fee equivalent to 2 of the DEPB entitlement in respect of lost BRC

bull An affidavit by exporter about loss of BRC and an undertaking to surrender itimmediately to RA if found subsequently

bull

An indemnity bond by exporter to the effect that he would indemnify Government for financial loss if any on account of DEPB issued against lost BRC

Claim against lost BRC shall be preferred within a period of six months from date of realizationand application received thereafter will be rejected

In such cases where both documents have been lost exporter shall follow procedure laid downin paragraph 452 and 453 Time period for such application shall be as per paragraph 452 and453 whichever is later

DEPB General Instructions

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 1220

The DEPB Rates specified in book shall not be applicable to export of a commodity or productif such commodity or product is-

1 Manufactured partly or wholly in a warehouse under Section 65 of the Customs Act 1962 (52 of 1962)

2Manufactured andor exported in discharge of export obligation against an Advance License including Advance License for Annual Requirement or exported under DFRCScheme of the relevant EXIM Policy

3 Manufactured andor exported by a unit licensed as hundred percent export oriented unitinterms of the provisions of the relevantImport Policy and Export Policy

4 Manufactured andor exported by any of the units situated in free trade zones ExportProcessing Zone Special Economic zones EHTP Scheme

5 Exports of goods of foreign origin unless the goods have been manufactured or reprocessed or on which similar operations have been carried out in India

DEPB Rates Product Groups and DEPB Items

The DEPB rates are applicable on the following product categories

bull 61 Engineering Products

bull 62 Chemicals

bull 63 Plastics

bull 64 Leather and Leather Products

bull

65 Sports Goodsbull 66 Fish and Fish Products

bull 67 Food Products

bull 68 Handicrafts

bull 83 Electronics

bull 89 Textiles

bull 90 Miscellaneous Products

DGFT DEPB Rates Notification in India

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 1320

Notification

DateNotification No Title

21-05-2009

DGFT PolicyCircular No912008DT21052009

ldquoError 96rdquo cases and their online validation under DEPB Scheme -Regarding

30-03-2009

DGFT PolicyCircular No

762008DT30032009

Guidelines for execution of BGLUT with Regional Authoritiesfor

filing application under DEPB scheme and Incentive schemes of Chapter 3 of FTP without the requirement of Bank RealisationCertificate - regarding

26-02-2009

DGFT PUBLIC NOTICE No152 (RE-2008)2004-09

AdditionsAmendments in the Schedule of DEPB Rates

13-01-2009

DGFT PUBLIC NOTICE No130 (RE-

2008)2004-09

Additionsamendments in Schedule of DEPB Rates

03-01-2009

DGFT PUBLIC NOTICE No124 (RE-2008)2004-09

Amendment in the Schedule of DEPB rates

14-11-2008

DGFT PUBLIC NOTICE No108 (RE-2008)2004-09

Amendments in Schedule of DEPB Rates

02-07-2008

DGFT PUBLIC

NOTICE No 38(RE-2008)2004-09

Addition in the Schedule of DEPB Rates

03-06-2008

DGFT PUBLIC NOTICE No 24(RE-2008)2004-09

Amendments in the Schedule of DEPB Rates

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 1420

02-06-2008

DGFT PUBLIC NOTICE No 23(RE-2008)2004-09

Amendments in the Schedule of DEPB Rates

24-04-2008

DGFT Policy

Circular No042008 DT24042008

Entitlement of DEPB prior to issuance of Public Noticewithdrawingthe benefit under the Scheme-regarding

23-04-2008

Corrigendum toPublic Notice No04(RE-2008)2004-09

Correction to Public Notice No 4 dated 1742008 related toSchedule of DEPB Rates

17-04-2008

DGFT PUBLIC NOTICE No 4(RE 2008) 2004

09

Amendments in the Schedule of DEPB Rates

07-04-2008

DGFT PUBLIC NOTICE No 140(RE 2007) 200409

Additionsamendments in the Schedule of DEPB rates

03-04-2008

DGFT PUBLIC NOTICE No 137(RE 2007) 200409

Amendments in the Schedule of DEPB Rates

27-03-2008

DGFT PUBLIC

NOTICE No 130(RE 2007) 200409

Amendments in the ldquoSchedule of DEPB Ratesrdquo

07-02-2008

DGFT PUBLIC NOTICE No 109(RE 2007) 200409

Amendments in the Schedule of DEPB Rates 2004-2009

28-11-2007

DGFT PUBLIC NOTICE No 86(RE 2007) 200409

Amendmentscorrections in the DEPB rates

30-10-2007

DGFT PUBLIC NOTICE No 78(RE 2007) 200409

Amendments in the Hand Book of Procedure (VolI) 2004-2009

09-10-2007 DGFT PUBLIC NOTICE NO 66(RE 2007)2004

AmendmentsCorrections in the Schedule of DEPB Rates

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 1520

2009

21-08-2007

DGFT PUBLIC NOTICE NO 35(RE 2007)20042009

AmendmentAddition of the entry in the Book titledSchedule of DEPBrates

12-07-2007

DGFT PUBLIC NOTICE NO 17(RE 2007)20042009

AmendmentsAdditions Corrections in the Book titledScheduleof DEPB Rates

09-07-2007

DGFT PUBLIC NOTICE NO 15(RE 2007)20042009

Amendments in the Book titled ldquoSchedule of DEPB Rates

29-09-2006

DGFT PUBLIC NOTICE No 60

(RE 2006)20042009

Amendments in the Book titled ldquoSchedule of DEPB ratesrdquo (as

amendedfrom time to time)

29-08-2006DGFT Public Notice No492006

Amendments in DEPB rates - Plastics Product - Sr No 125(DoubleBlood Bag with Tubing) change to (Blood Bags)

24-08-2006DGFT Public Notice No452006

Amendments in Guidelines - Sub section VC of Aayaat NiryaatForm -DEPB application

03-07-2006DGFT Public Notice No292006

DEPB DGFTAmendmentsadditionscorrectionsin the Book titled - Schedule of DEPB rates

03-07-2006DGFT Public Notice No292006

DEPB DGFTAmendmentsadditionscorrectionsin the Book titled - Schedule of DEPB rates

18-05-2006

DGFT PUBLIC NOTICE No 10(RE 2006)20042009

DEPB DGFTAmendmentscorrections in theBook titled ldquoSchedule of DEPBratesrdquo

05-04-2006DGFT Public Notice No962005

DEPB DGFT Amendmentscorrections in theBook titled Schedule of DEPB rates

27-01-2006DGFT Public Notice No852005

DEPB DGFT Amendments in DEPB rateschedule

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 1620

10-01-2006

DGFT PolicyCircular No442005 09 DT10012006

DEPB DGFTDGFT to make submission of DEPB applications online on 10more portsfrom Jan 16 2006

26-12-2005DGFT Public Notice No772005

DEPB DGFTAmendments correction in DEPBrates - Forged Crank Shaft amp FrontAxle Beam Forging

13-10-2005DGFT Public Notice No622005

DEPB DGFTAmendments in the DEPB ratesMiscellaneous - Product Code 90 -13Machine Cut Glass Chatons

06-10-2005 DGFT Public Notice No572005

DEPB DGFT DGFT clubs ports to treat them assingle port for export import ampamends Para 449 - Electronicverification of DEPB Shipping Bills

06-10-2005

DGFT PolicyCircular No282005 09 DT06102005

DEPB DGFT DEPB message exchange withCustoms- regarding

09-08-2005DGFT Public Notice No372005

DEPB DGFT Amendmentsadditionscorrectionsetc in the Schedule of DEPB rates

20-06-2005DGFT Public Notice No232005

DEPB DGFT Correction in DEPB rates at Fishand Fish Products - Sl NO 2

26-05-2005DGFT Public Notice No122005

DEPB DGFT Amendmentsadditionscorrectionsetc in the Schedule of DEPB rates

26-05-2005DGFT Public Notice No122005

DEPB DGFT Amendmentsadditionscorrectionsetc in the Schedule of DEPB rates

26-05-2005DGFT Public Notice No122005

DEPB DGFT Amendmentsadditionscorrectionsetc in the Schedule of DEPB rates

30-03-2005DGFT Public Notice No662004 09

DEPB DGFT Additions corrections amendmentsin the Schedule of DEPB rates

21-03-2005 DGFT Public Notice No

DEPB DGFTAdditionsamendments in the

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 1720

622004 09 DEPB rates

22-02-2005DGFT Public Notice No562004 09

DEPB DGFT Correction in the Book titledrdquoSchedule of DEPB rates

30-12-2004DGFT Public Notice No392004 09

DEPB DGFT Amendments in DEPB rates for Textile product Group

01-12-2004DGFT Public Notice No272004 09

DEPB DGFTAmendmentsadditionscorrectionsin DEPB rates realted toEngineering product group

23-11-2004DGFT Public Notice No252004 09

DEPB DGFT New DEPB rates for Plastics products and corrections inEngineering

product group

29-09-2004DGFT Public Notice No102004 09

DEPB DGFT Related to DEPB rates for Fish products

23-09-2004DGFT Public Notice No072004 09

DEPB DGFT Amendments additions corrections in DEPB rates

16-09-2004DGFT Public Notice No052004 09

DEPB DGFT Utilisation of DEPB credit in caseof import of Edible oil

14-09-2004DGFT Public Notice No032004 09

DEPB DGFT Amendments and Corrections inSchedule of DEPB rates

W DEPB Rates Scheduled Issues by DGFT

India

GENERAL INSTRUCTIONS FOR DEPB RATES

1 The rates of DEPB specified in book shall not be applicable to export of acommodity of product if such commodity or product is-

832019 DEPB Procedures

httpslidepdfcomreaderfulldepb-procedures 1820

a Manufactured partly or wholly in a warehouse under Section 65 of the CustomsAct 1962 (52 of 1962) b Manufacture andor exported in discharge of export obligation against anAdvance Autorisation including Advance Authorisation for Annual Requirement or exported under DFIA Scheme of the relevant Foreign Trade Policy

c Manufacture andor exported by a unit licenced as 100 Export Oriented Unitin terms of the provisions of the relevant Foreign Trade Policyd Manufactured and or exported by any of the units situated in Free TradeZonesExport Processing ZoneSpecial Economic ZonesEHTP Schemee Exports of goods of foreign origin unless the goods have been manufacturedor processed or on which similar operations have been carried out in Indiaf Exports made under paragraph 235 and 236 of the Foreign Trade Policy

2 The DEPB rate and the value cap shall be applicable as existing on the dateof order of ldquolet exportrdquo by the Customs

3 The value cap wherever existing shall be with reference to the FOB value of

exports The DEPB rates shall be applied on the FOB value or value cap whichever is lower For example if the FOB value is Rs500- per piece and the value capis Rs300- per piece the DEPB rate shall be applied on Rs300-

4 Wherever any specific rate exists for a particular item under DEPB rate listas given in this book the items shall not be covered under any genericdescription of the DEPB rate list

5 The DEPB rate aims to neutralize the incidence of duty on the inputs used inthe export product Therefore the DEPB rates as given in this book refer tonormally tradableexportable product Items such as Gold Nibs Gold Pen Goldwatches etc though covered under the generic description of writinginstructions components of writing instruments and watches are thus not

eligible for benefit under the DEPB scheme6 The DEPB rates given for various galvanized Engineering product shall cover non galvanised products and vice-a-versa