depreciation and block of assets - wirc and block of assets... · • explanatory notes to finance...

TRANSCRIPT

Depreciation and block

of assets

Samir S Shah

WIRC 27 August 2011

Contents

• Qualifying assets

Tangible assets

Intangible assets

• Ownership

• Used for business

• Proviso and explanations to section 32

• Additional depreciation

• Unabsorbed depreciation

• Block of assets

• Written down value

2

Qualifying assets

• Tangible assets

Buildings

Machinery

Plant

Furniture

• Intangible assets acquired on or after 1 April 1998

Know-how, Patents, Copyrights, Trademarks, Licences, Franchises or any

other business or commercial rights of similar nature

3

Tangible assets

Building

‒Not defined in the Act. To be construed in its ordinary sense

‒“Building” include roads, bridges, culverts, wells and tube-wells • Note no.1 to New Appendix I of Rule 5

‒“Building used mainly for residential purpose where built up area used for residential purpose is not less than 66.67%.

‒Driveways and compound walls in petrol pumps are building • Indo Burmah Petroleum Co Ltd(1978)112 ITR 755 (Cal)

4

Tangible assets

Building

‒Whether roads are buildings eligible for depreciation? • Roads laid within factory premises as links or providing approach road to

buildings are "buildings". Similarly, drainage are buildings ‒ Gwalior Rayon Silk Mfg.Co. Ltd (1992) 196 ITR 149 (SC)

• As there was no other constructions excepts roads, roads cannot be treated as building ‒ Indore Municipal Corporation (2001) 247 ITR 803 (SC)

‒Land cost on which structure is built not eligible for depreciation

• Alps Theatre (1967) 65 ITR 377 (SC)

‒Cost of building is required to be increased by land development

expenses • Herdillia Chemicals Ltd. (1995) 216 ITR 742 (Bom.)

5

Tangible assets

Plant • Section 43(3)

‒“plant” includes ships, vehicles, books, scientific apparatus and surgical

equipment used for the purposes of the business or profession [but

does not include tea bushes or livestock] [or buildings or furniture and

fittings];

‒ Inclusive definition

‒Computers including computer software eligible for depreciation @ 60%

‒Depreciation on printer and scanner • Although the I-T Act has not defined Computer but it talks about computer

system in the Explanation to Sec 36(1). The printer and scanner are an integral part of the computer system and they are to be treated as computer ‒ ACIT V. Continental Carriers Pvt. Ltd.(2009) (ITA 2137/Del/2008) (Del)

6

Tangible assets

‒Depreciation on routers and switches • When "Computer Hardware", is used as a component of the computer, it

becomes part and parcel of the computer, as in the case of operating software in the computer. In such a situation, hardware in question can be considered as a part of a computer

• Router and switches can be classified as a computer Hardware when they are used along with a computer and when their functions are integrated with a `computer'

- DCIT v. Datacraft India Ltd., 6 Taxman 85 (2010) (Mumbai ITAT) (SB)

7

Tangible assets

Furniture and Fittings ‒ Partition works & False Ceilings – Building or Fittings?

• Partition works and false ceilings are fittings ‒ CIT v. Indian Metal & Metallurgical Corporation (1983) 141 ITR 40 (Mad)

• False ceilings and other accessories in cinema theatre are fittings ‒ CIT v. N. L. Mehta Cinema Enterprise (P) Ltd.(1993) 71 Taxman 443(Bom)

8

Intangible assets

know how ‒Meaning - Explanation 4 to Section 32(1) - know-how means any

industrial information or technique likely to assist in the manufacture or

processing of goods or in the working of a mine, oil-well or other

sources of mineral deposits (including searching for discovery or testing

of deposits for the winning of access thereto).

Patents, copyrights, trade marks, licenses, franchises or any

other business or commercial rights of similar nature not

defined

9

Intangible assets

‒Premium paid to tenants – whether could be termed as License

• Section 32 allows depreciation on know-how, patents, copyrights, trademarks, licenses, franchises and are followed by the general words “or any other business or commercial rights of similar nature”

• All the above expressions are placed at similar level with similar nature relating to business or commercial rights.

• Expression license cannot be singled out from business or commercial rights.

• Principle of Ejusdem Generis rule is that where general words follow specific words of the same nature, the general words must be confined to the things of same kind of those specific.

• Tenancy right cannot be equated with the license provided in section 32 to qualify as intangible asset eligible for depreciation.

‒ M. M. Nissim & Co. (2007) 18 SOT 274 (Mum)

10

11

Intangible assets

‒Customer contracts • The accounting treatment is not determinative for claiming depreciation • In section 32(1)(ii), certain intangible assets are followed by the expression

“any other business of commercial rights of similar nature” • The specific words in the section reveal the similarity that all the intangible

asset specified are tools of the trade which facilitate the assesse carrying on the business.

• Business or commercial rights would include such rights which can be used as a tool to carry on the business.

• As such assesse eligible to claim depreciation. ‒ Skyline Caterers (P) Ltd (2008) 20 SOT 266 (Mum)

12

Intangible assets

‒Brand • The definition of trade mark under Trade Mark Act 1999 includes mark and

mark includes brand. • Brand name is an intellectual property right similar to know how, patents and

trademarks, etc. • Explanatory notes to Finance Act 2001 explaining provision of Section 55

have used brand name or trade mark alternatively • Hence, Trade Mark includes brand and is eligible for depreciation. ‒ KEC International Ltd. (2010) (ITA No.4420/Mum/2009)(Mum)

Intangible assets

‒Non-compete fees • Observed that „capability to have market value, assignability, transferability,

diminution in value, are no more the „touch stones‟ on which admissibility for depreciation under section 32 of the Act has to be tested‟.

• Each of the terms knowhow, patents, trademark, etc represents a „business/commercial right‟

• Principle of Ejusdem Generis rule is the rule of generic words following more specific one.

• Right acquired by payment of non-compete fee was in the nature of a business or commercial right similar to know-how, patents, copyrights, trademarks, licenses and franchises

• Assessee eligible to claim depreciation on such non compete rights. ‒ Medicorp Technologies India Ltd. 2009-TIOL-203 (Chennai)

• “any other business or commercial rights of similar nature” should belong to same genus to which know-how, patents, copyrights, trademarks, licenses/franchises belong.

• Non-compete fee cannot be considered to belong to the same genus to which know-how, patents, copyrights, trademarks, licenses/franchises belong

• Non-compete fee covenant does not result into an intangible assets which can be transferred/assigned/leased.

‒ Sharp Business Systems (India) Ltd. (2011) ITA No.4564/Del/200 (Delhi)

13

14

Intangible assets

‒Geographical Report • The GR contains general description of mining area and the know how of

mine. • Know how is defined by Explanation 4 to section 32(1) so as to mean “any

industrial information or technique likely to assist in the manufacture or processing of goods or in the working of mine, oil well or other sources of minerals deposits (including searching for discovery or testing of deposits for the winning of access thereto)”.

• Accordingly, GR is an intangible asset falling u/s 32(1) (ii) of the Act eligible for depreciation.

• Not eligible for additional depreciation ‒ Integrated Coal Mining Ltd. (2010) (ITA 788/Kol/2010) (Kol)

Intangible assets

‒Goodwill • Depreciation is not allowed under section 32 ‒ R.G. Keswani v. ACIT, (2009) 308 ITR 271 (Mum) ‒ Bharatbhai J. Vyas, (2005) 97 ITD 248 (Ahmedabad) • Depreciation is allowed under section 32, if falls under the specified assets

mentioned under section 32 ‒ Hindustan Coca Cola Beverages Pvt. Ltd. (2009) 34 SOT 171 (Delhi) ‒ Kotak Forex Brokerage Ltd (2009) 33 SOT 237 (Mum) ‒ Piem Hotels Ltd. (2011) 128 ITD 275 (Mum)

‒Stock exchange membership card • Right of membership conferred upon a member under BSE membership

card in terms of rules and bye-laws of BSE, is a licence or akin to a licence and therefore eligible for depreciation

‒ Techno Shares & Stocks Ltd. [2010] 327 ITR 323(SC)

15

Ownership

‒Owned wholly or partly and used for the purpose of business or profession

• Anyone in possession of property in his own title exercising such dominion

over the property as would exclude others and having right to use and occupy the property and/or enjoy its usufruct in his own right would be the owner

• Formal deed of title may not have been executed and registered ‒ Mysore Minerals Ltd v. CIT (1999) 239 ITR 775(SC)

‒Hire purchase transaction • Ownership of asset transfer immediately then transaction should be

regarded as purchase by instalments. • No deduction in respect of hire. • Depreciation to buyer • Ownership of asset eventually transfer to buyer or option to purchase asset

at end then transaction should be as one of hire purchase • Consideration for hire should be allowed as deduction • Payment on account of capital outlay eligible for depreciation ‒ Circular no.9 of 23 March 1943

16

Ownership

‒Assets purchased on instalment basis

• Depreciation allowable ‒ CIT v. Nagpur Golden Transport Co. (1998) 233 ITR 389 (Delhi)

• Depreciation not allowable ‒ Atlas Cycle Industries Limited (2005) 270 ITR 108 (P & H)

17

Ownership ‒acquired under lease agreements

• Finance lease v. operating lease

• Operating lease – Lessor should be eligible

• Finance lease – Lessor or Lessee?

• Depreciation should not be disallowed to both lessor and lessee

‒ Instruction no. 1978 dated 31st December, 1999 [F. No.225/190/98/IT(A-II)]

‒Sale and lease back

• Sale and lease back transaction cannot be considered as a colorable device to evade tax liability merely because tax liability reduced

• Affairs to reduce tax liability without violating law still valid

• If transaction is genuine, deduction allowable

‒ Cosmo Films Ltd. (2011) ITA 1404/2008 (Delhi High Court)

‒ Punjab State Electricity Board, Patiala (2009) 30 DTR 153 (P & H)

• Explanation 4A to section 43 regarding actual cost to lessor introduced by Finance (No.2) Act, 1996 with effect from 1 October 1996

18

19

Used for business

‒Kept ready for use

• Allowance for normal depreciation allowance does not depend upon the actual working of the machinery. If the machinery is employed in the particular business and kept ready for use it is to be deemed to have been used within meaning of section 32

‒ Premier Industries (India) Ltd. (2008) 170 Taxman 407 (MP)

‒ Insilco (2009) 320 ITR 322 (Delhi)

‒ Chennai Petroleum Corporation (2010) 125 ITD 396 (Chennai)(TM)

• The word „used” denotes actually used and not merely ready for use.

‒ Dineshkumar Gulabchand Agrawal (2004) 267 ITR 768 (Bom)

‒ Yellamma Dasappa Hospital (2007) 159 Taxman 58 (Karn)

20

Used for business

‒Trial run production

• As the statute does not prescribe a minimum time-limit for „use‟ of the machinery, the benefit of depreciation cannot be denied on the ground that the machinery was used for a very short duration for trial run

‒ Ashima Syntex Ltd (2000) 251 ITR 133 (Guj.)

‒ Piccadily Agro Industries Ltd.(2007)164 Taxman 567 (P& H)

‒Commissioning of windmills

• Depreciation available on wind-mills commissioned on 31 March even though actual supply of electricity commenced in April

‒ Hindustan Platinum Pvt. Ltd (2011) (ITA 3352/M/2010) (Mum)

21

Used for business

‒Asset under repairs throughout the year

• Depreciation is allowed even if trucks were under repairs throughout relevant accounting years but were used for the purpose of business in earlier and later years

‒ G.N. Agrawal (1993) 75 Taxman 30 (Bom.)

‒Machinery installed but found defective

• Where machinery is installed but found defective it will amount to use of machinery.

‒ Chamundeshwari Sugar Ltd. (2009) 309 ITR 326 (Karn.)

22

Used for business

‒Factory under lock-out

• Where factory remained under lock-out throughout the previous year, depreciation on machinery was not allowable

‒ CIT v. Oriental Coal Co. Ltd. (1994) 206 ITR 682 (Cal)

• Despite non-user of assets due to closure of Bhopal unit for six years, depreciation is allowable if it is part of “Block of assets”

‒ Oswal Agro Mills Ltd. (2011) 238 CTR 113 (Delhi)

‒Adverse law and order

• An assessee should not be deprived of benefit of depreciation u/s 32 for not running its factory due to adverse law and order situation

‒ Norplex Oak India (2011) 10 taxmann.com 163 (Cal.)

23

Others

‒Personal use

• For company, no disallowance of depreciation can be made for the personal use of motor car by director

‒ Sayaji Iron and Engg. Co. v. CIT 253 ITR 749 (Guj.)

‒Custom duty paid under protest

• Custom duty on imported machinery though paid under protest is required to added to cost of machinery for the purpose of depreciation

‒ Orient Ceramics & Industries Ltd - [2011] 11 taxmann.com 417 (Delhi)

‒Website development expenses

• In view of the amendment of Appendix I allowing depreciation @ 60 percent on software, depreciation is allowable on expenditure for development of website @ 60 percent

‒ C. M. Y. K. Printech Ltd. (2011) 53 DTR 59 (Delhi)(Trib.)

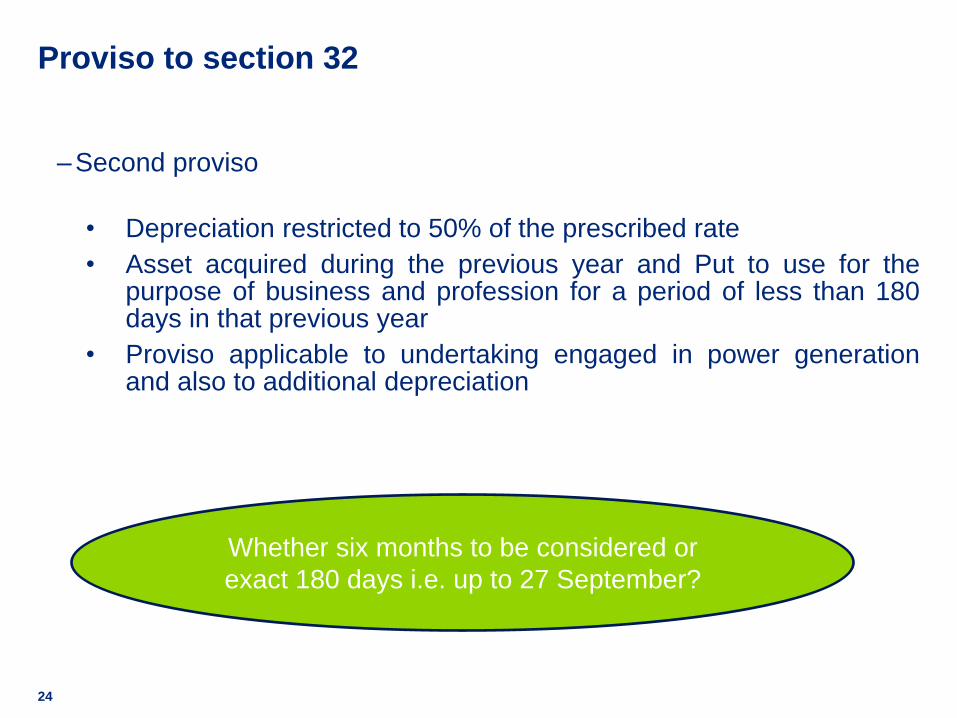

Proviso to section 32

‒Second proviso

• Depreciation restricted to 50% of the prescribed rate

• Asset acquired during the previous year and Put to use for the purpose of business and profession for a period of less than 180 days in that previous year

• Proviso applicable to undertaking engaged in power generation and also to additional depreciation

24

Whether six months to be considered or

exact 180 days i.e. up to 27 September?

Proviso to section 32

‒Third proviso

• Enhanced depreciation for:

‒ Commercial vehicles acquired on or after the 1 October, 1998 but before 1 April, 1999 and put to use before the 1 April, 1999 for the purposes of business or profession (40%)

‒ New commercial vehicles acquired on or after the 1 October, 1998, but before the 1 April, 1999 in replacement of condemned vehicle of over 15 years of age and is put to use for any period before the 1 April, 1999 for the purposes of business or profession (60%)

‒New Appendix I of the Income-tax Rules

‒ New commercial vehicle acquired on or after the 1 April, 1999 but before the 1 April, 2000 in replacement of condemned vehicle of over 15 years of age and is put to use before the 1 April, 2000 for the purposes of business or profession (60%)

‒ New commercial vehicle acquired on or after the 1 April, 2001 but before the 1 April, 2002 and is put to use before the 1 April, 2002 for the purposes of business or profession (50%)

25

Proviso to section 32

‒New commercial vehicle acquired on or after the 1 January,

2009 but before the 1 April, 2009 and is put to use before

the 1 April, 2009 for the purposes of business or profession

(50%)

• Commercial vehicles include „light motor vehicle‟ and „light motor

vehicle‟ as per motor vehicle act means transport vehicle or omnibus the gross vehicle weight of either of which or a motor car or tractor or road-roller the unladen weight of any of which, does not exceed 7,500 kilograms

• Separate entry in Rules for vehicle running on hire

• Maruti Zen purchased and used in business of civil construction would be eligible.

‒ Daleep S. Chandnani [2007] 14 SOT 233 (Mum.)

26

Proviso to section 32

‒Fifth proviso • Apportionment of depreciation between the predecessor and the

successor based on the number of days assets used provided that aggregate deduction allowable in the following cases of succession, amalgamation or demerger should not exceed the depreciation allowable had the succession, amalgamation or demerger has not taken place:

• Transfer of assets by:

‒ Firm to a company u/s 47(xiii)

‒ Private Limited company or unlisted company to LLP u/s 47(xiiib)

‒ Sole proprietor to a company u/s 47(xiv)

‒ amalgamating company to amalgamated company

‒ De-merged company to resulting company

‒ Succession of a business referred to in section 170

27

Explanations to section 32

‒Explanation 1 • Business or profession is carried on in a building not owned by him

but in respect of which assessee holds a lease or other right of occupancy and any capital expenditure is incurred by the assessee for the purposes of the business or profession on the construction of any structure or doing of any work in or in relation to, and by way of renovation or extension of, or improvement to, the building, then, the provisions of this clause shall apply as if the said structure or work is a building owned by the assessee

• Expenditure incurred on leased premises in order to make it fit for business, if any extra facility was created by way of brick works and connected expenditure, the same would be a capital expenditure eligible for depreciation under explanation 1 to s. 32(1) and if not, the expenditure would be revenue in nature covered by s. 30(a)(ii).

‒ EDS Electronic Data Systems (India) (P) Ltd. (2009) 23 DTR 10 (Del)(Trib).

28

Explanations to section 32

‒Explanation 5

• For the removal of doubts, it is hereby declared that the provisions of this sub-section shall apply whether or not the assessee has claimed the deduction in respect of depreciation in computing his total income

• Whether additional depreciation is mandatory?

• Depreciation mandatory for claiming deduction under Chapter VI-A

‒ Scoop Industries (P.) Limited (2007) 161 Taxman 366 (Bom.)

29

Additional depreciation is mandatory

Additional Depreciation

‒Section 32(1)(iia) • Assessee engaged in business of manufacture of article or thing

• Additional depreciation allowed @20% of actual cost when new asset (other than ships and aircraft) is acquired/installed after 31 March 2005

• Second proviso to Section 32(1)(ii) of the Act – asset put to use for less than 180 days – depreciation @50% of the additional depreciation

• Not allowed for:

‒ any machinery or plant which, before its installation by assessee, was used either within or outside India by any other person; or

‒ any machinery/ plant installed in any office premises or residential

accommodation including guest house or

‒ any office appliances or road transport vehicles or

‒ Any machinery or plant, the whole of the actual cost is allowed as

depreciation.

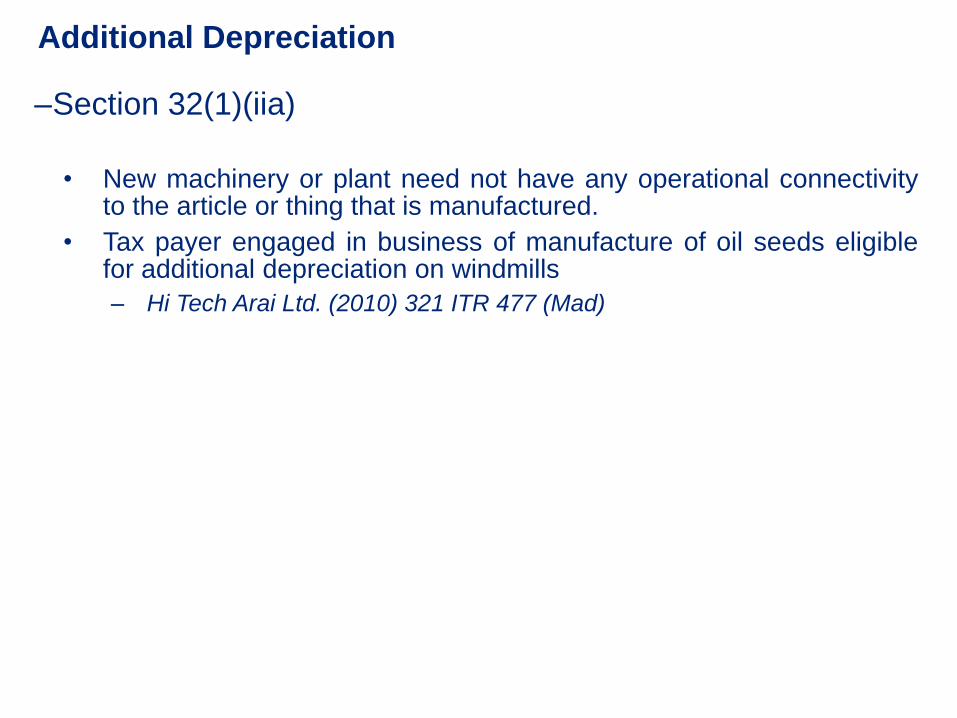

Additional Depreciation

‒Section 32(1)(iia)

• New machinery or plant need not have any operational connectivity to the article or thing that is manufactured.

• Tax payer engaged in business of manufacture of oil seeds eligible for additional depreciation on windmills

‒ Hi Tech Arai Ltd. (2010) 321 ITR 477 (Mad)

Additional Depreciation

‒Section 32(1)(iia)

• Whether tax payer can claim the balance 10% of additional depreciation in the subsequent year?

‒ Section does not specifically state that the additional depreciation has to be claimed in the year of acquisition or installation

‒ The restriction in the proviso to section 32(1)(iia) of the Act is only for the machinery or plant used by any other person before installation by the assessee.

‒ The proviso to section 32(1)(ii) does not mention that the balance depreciation under section 32(1)(iia) shall not be available in the subsequent financial year.

‒ SC in the case of Bajaj Tempo Ltd vs. CIT (196 ITR 188) has held that a provision in taxing statute granting incentives for promoting growth and development should be construed liberally.

32

Block of the

period for which

the unabsorbed

depreciation

pertains

Permissible

period to

carry

forward

Eligibility to set

off against the

other income of

the same year

Eligibility to set

off against the

other income of

the following

years

Up to F.Y. 1995-96

Indefinite

Yes

Yes

From F.Y. 1996-97

to 2000-01

Following

eight years

Yes

No

F.Y. 2001-02

onwards

Indefinite

Yes

Yes

Unabsorbed Depreciation

33

Unabsorbed depreciation

‒Treatment of unabsorbed depreciation from AY 1997-98 to 2001-02

‒Whether law existing in the year of loss incurred or year of sett off is to be applied ?

• ITAT-SB held that the unabsorbed depreciation relating to F.Y.1996-97 to 1998-99 is to be dealt with in accordance with the provisions of section 32(2) of the ITA as applicable for F.Y.1996-97 to 1998-99 and not in accordance to the provisions applicable in year of set off.

• Unabsorbed depreciation of AYs 1997-98 to 2001-02 not eligible for relief granted by amended s. 32(2) in AY 2002-03

‒ DCIT v. Times Guaranty (2010) 4 ITR 210 (Mum.)(SB)

34

Unabsorbed depreciation

‒Section 72A

• In the case of amalgamation, subject to fulfillment of certain conditions, the accumulated loss and unabsorbed depreciation of the amalgamating company shall be deemed to be loss or unabsorbed depreciation of the amalgamated company for the year in which the amalgamation was effected

• Section 72A would be applicable only when „amalgamating company‟ and not „amalgamated company‟ has accumulated losses or depreciation

‒ Wrigley India Private Limited ITA No.5224/Del/2011 dated 5 August 2011

35

Block of assets

‒Law prior to Assessment year 1988-89 • No block concept – Depreciation calculated for each asset

• Three types of depreciation, Normal depreciation, Extra shift depreciation and Initial depreciation

‒Law from the Assessment year 1988-89 • Block of asset concept come into existence

• Written down value to be computed with reference to each block of asset

‒Section 2(11) • means a group of assets falling within a class of assets comprising

‒ Tangible assets - Buildings, machinery, plant or furniture

‒ Intangible assets being know how, patents, copyrights, trademarks, licenses, franchises or any other business or commercial rights of similar nature,

in respect of which same percentage of depreciation is prescribed

36

37

Depreciation - Block of assets

‒Block of Assets- Individual assets loose its identity • In case of block of assets, in order to allow assessee‟s claim under

section 32(1), use of individual asset for purpose of its business can be examined only in first year when asset is purchased

• In subsequent years use of block of assets is to be examined. Existence of an individual asset in block of assets itself amounts to use for purpose of business

• Specific items in the said block as individual assets have lost their identity after becoming inseparable part of the block of assets.

• Therefore, depreciation is allowable on it, even though said asset is not actually used in course of business during relevant assessment year

‒ Swati Synthetics Ltd. Vs. ITO (2010) 38 SOT 208 (Mum.)

‒ CIT vs. Sonal Gum Industries (2010) 322 ITR 542 (Guj.)

• Even under concept of block of assets, it is very essential that assets included in block of assets otherwise entitled to depreciation. Non qualified asset cannot be granted depreciation only for reason that said asset qualified for depreciation in earlier assessment year and formed part of block of assets.

‒ Jagdish C. Sheth (2006) 101 ITD 360 (Mum.)

Written down value

‒Section 43(6) • WDV of the block of assets in immediately previous year

Less: depreciation actually allowed in immediately previous year

WDV at the beginning of the year

Add: actual cost of asses acquired during the year

Less: Money payable in respect of assets sold, discarded or demolished or destroyed together with scrap value

WDV on which depreciation available

• “Actually allowed” mean depreciation actually taken into account or granted and given effect to in computing taxable income

• In case of tea manufacturer, according to Rule 8 only 40% of composite income is brought to tax and consequently proportionate depreciation is required to be taken into account

‒ Doom Dooma India Ltd. (2009) 310 ITR 392 (SC)

38

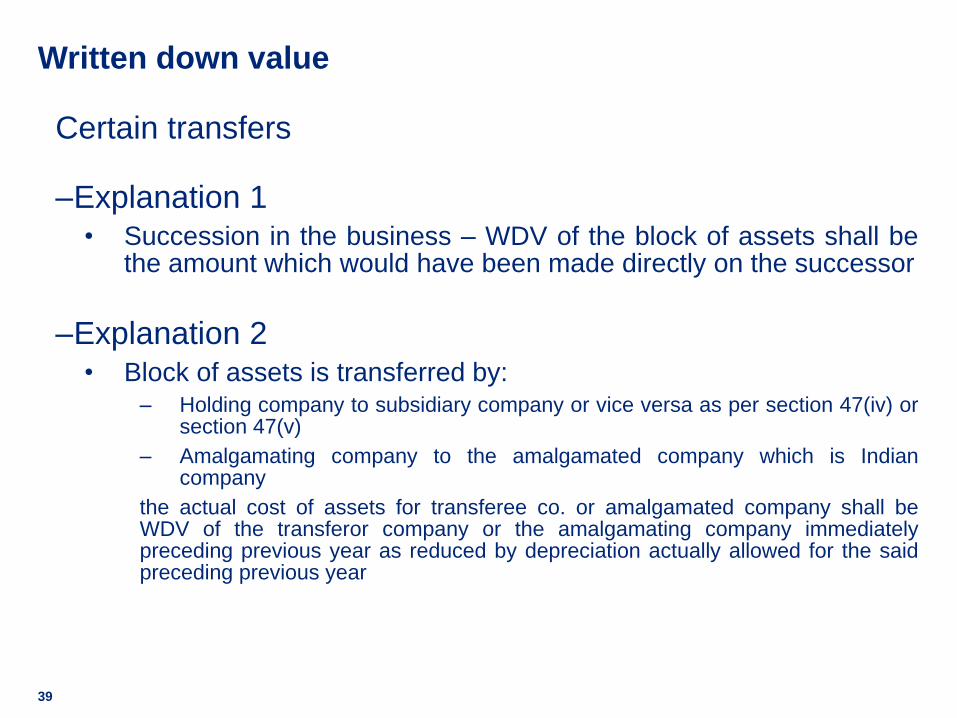

Written down value

Certain transfers ‒Explanation 1

• Succession in the business – WDV of the block of assets shall be the amount which would have been made directly on the successor

‒Explanation 2

• Block of assets is transferred by: ‒ Holding company to subsidiary company or vice versa as per section 47(iv) or

section 47(v)

‒ Amalgamating company to the amalgamated company which is Indian company

the actual cost of assets for transferee co. or amalgamated company shall be WDV of the transferor company or the amalgamating company immediately preceding previous year as reduced by depreciation actually allowed for the said preceding previous year

39

Written down value

‒Explanations 2A & 2B • Demerger

‒ WDV of block of assets of the de-merged company for the immediately preceding previous year shall be reduced by WDV of assets transferred to the resulting company

‒ WDV of the block of block of assets of the resulting company shall be WDV of the transferred assets of the de-merged company immediately before the de-merger

‒Explanations 2C

• Conversion from Private or Unlisted public company to LLP ‒ WDV of block of assets of LLP shall be WDV of block of assets of the private

or unlisted public company on the date of conversion

40

41

Thank

You