derivatives overview

TRANSCRIPT

Derivatives Overview

Introduction to Derivatives

Forwards

Futures Contracts

Options Contracts

(OTC) Over-The-Counter Derivatives

2

1

3

4

5

Derivatives overview

Forward Rate Agreements

Swaps

Credit Derivatives

Commodities & Exotics

Technology Impact of Dodd-Frank Act

6

7

8

9

10

Introduction to Derivatives Definition Classification by Market mechanism Exchange Traded Vs. OTC Traded Participants in Derivatives Market Usage of Derivatives Stock Market Regulatory Bodies

Derivative definition

‘Derivative’ is a ‘contract’ whose price is derived from or dependent upon underlying asset.

Underlying asset could be: Currency,

Stock, Market Index, an Interest bearing

security, Physical Commodity and

it could be even on Electricity,

Temperature and Volatility.

Derivatives Classification

.

TYPES OF DERIVATIVES

Over-The-Counter (OTC) Derivatives:

· Forwards

· Swaps

· Swaptions

· Credit Derivatives

· Forward Rate Agreements (FRA)

· Exotic options

Exchange Traded Derivatives:

· Futures

· Options

· Options on futures

· Some exchange-traded Swaps

Index CommoditiesPropertyInterest Rates

CurrencyStocks Energy, Weather, etc.

Classification by Market Mechanism

Exchange-Traded Vs. OTC-Traded

Exchange Traded: Derivatives can be entered in via, standardized contracts provided on derivatives exchanges (NSE, NYSE Liffe, CME Group) and these are called Exchange Traded.

OTC (Over-the-Counter): Derivatives can be negotiated and entered into away from any exchange, directly between the two counterparties referred as ‘Over-the-counter’ or OTC products (London Metal Exchange).

Exchange-Traded OTC-Traded

Contract Terms

Standardized, Qlty. & Qty. defined in product specification

Customized, Bilateral, Totally confidential

Delivery Standardized under exchange’s product specification and Fixed dates.

Negotiable

Trading & Liquidity

Contracts are easily traded and liquidity is excellent on major contracts, fast order execution.

Not standardized and not easily traded. Varies dramatically on underlying, slower execution.

Exchange Traded Vs. OTC Traded contd.

.

Exchange-Traded OTC-Traded

Financial Integrity

Central Counterparty (CME, ICE,LCH, EUREX)

Daily Mark to Market

Counterparty default exists, hence credit rating important

Margin Margin is normally required. (Initial and Variation margin)

Agreed on case-by-case basis to secure trade

Documentation Standard and Concise One-off and complex. (Though std.document provd by ISDA)

Regulation Subject to significant regulation (SEBI, FSA,SEC)

Less actively regulated

Price Quotes Highly Transparent Limited. Need to ‘Shop around’

Transaction cost Standardized, lower Individually priced, expensive

Fungibility Individual contracts (same expiry) totally fungible

Contracts are customized and are not as fungible

Hedging Precisely may not possible Negotiation can result in hedging

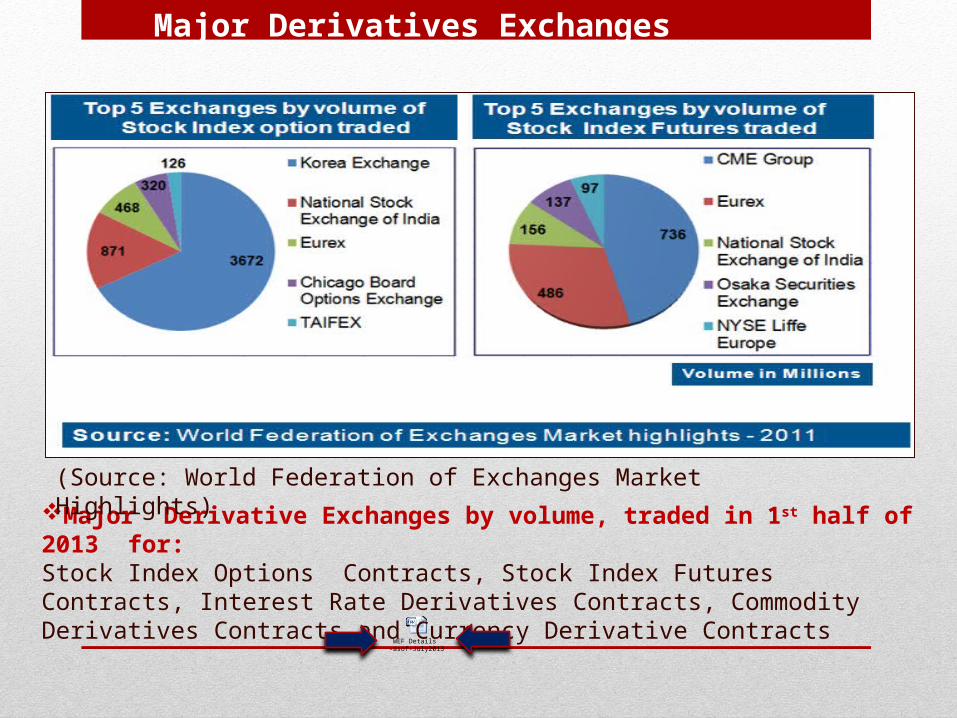

Major Derivatives Exchanges

.

WEF Details -asof-July2013

Major Derivative Exchanges by volume, traded in 1st half of 2013 for: Stock Index Options Contracts, Stock Index Futures Contracts, Interest Rate Derivatives Contracts, Commodity Derivatives Contracts and Currency Derivative Contracts

(Source: World Federation of Exchanges Market Highlights)

Participants in Derivative Market

.

Hedgers, Speculators and Arbitragers

Hedgers are investors with a present or anticipated exposure to the underlying asset which is subject to price risk.

Hedgers use derivatives markets primarily for price risk management of assets and portfolios.

Speculators take a view whether prices would rise or fall in future and accordingly buy or sell F&O to try and make out profit from future price movement of underlying

Arbitrage refers to a trader's attempt to profit by exploring price between identical or similar, financial instruments that are trading on different markets.

Arbitragers usually earn profit by trading in two different markets simultaneously or two instruments related to each other.

Derivatives are used increasingly by entities ranging from Corporates, Mutual Funds, Pension Funds, Banks, Insurance companies, Brokers, Individuals and Farmers.

Usage of Derivatives

USER Major Motivation

Corporates Hedging, Asset/Liability Management, Securitization

Commercial Banks Hedging, Risk Management, Asset/Liability Management.

Investment Managers Hedging, Alpha Gain, Speculation

Insurance Firms Risk Management

Hedge Funds Speculation, Risk Arbitrage

Brokerage Firms Market Making, Trading, Structuring New Products

Individual Investors Speculation

Banks use Derivatives to hedge against risks that may affect their operations.Farmers use Derivatives to lock their price of their crop in order to protect their harvest.Derivatives help in discovery of future as well as current prices.Users of Derivatives can hedge against fluctuations in exchange and interest rates, Equity and commodity Prices as well as Credit worthiness

Stock Markets Regulatory Bodies

Regulatory Bodies for Exchange Traded Derivatives

Forward

Contracts Common Terminologies Forward Contract

Common Terminologies

Buyer/Long Position: Buying of a security such as a Stock, Commodity or Currency with expectation that asset will rise in value.

Seller/Short Position: The Sale of a Security, Commodity or Currency with the expectation that the asset will fall in future.

Spot/Market price: The price at which an underlying asset traded in the spot/cash market.

Futures Price: The price at which the futures contract trades in the futures market.

Contract cycle: Period over which a Derivatives contract trades.

Ex: Index/Stock contracts on NSE have One/Two/Three-month expiry cycles, which expires on last Thursday of the month.

Expiry Date: The date when the contract is settled by delivery of underlying asset or cash.

Contract/Lot Size: The Quantity of underlying asset in one contract

Basis: Futures price minus the spot price.

Cost of carry: (Storage cost + Interest) - (Income) on an Asset

Index Futures: Futures contracts where the underlying is the ‘Stock Index’(Exp: Nifty, Sensex, FTSE, NYSE) and helps a trader to take a view on the market as whole.

Stock Futures: Futures contracts where the underlying is the stock Exp: Stocks of Reliance Ind, Wipro, HLL etc.

Open Interest: (Open Contracts/Open Commitments) Refers to the total number of Derivative Contracts like Futures and Options that have not been settled in for specific derivative contract.

Large open interest indicates more activity and liquidity for the contract.

Forward contracts

It is an agreement to buy or sell an asset on a specified date for a specified price.

Traded, off-exchange commonly known as OTC (Over-the-Counter)

Contract details (Delivery date, Price and quantity) are negotiated bilateral by parties and contracts are flexible/customized.

Bilateral contracts exposed to Counterparty risk.

On expiration date, contract has to be settled by delivery of asset.

Forwards are highly popular on Currencies and Interest rates.

To reverse the contract, it has to compulsorily go the same counter-party

In UK markets, to enter into a Contracts for Difference (cash settled) is to place a bet with a spread betting firm.

Forward Contracts Examples:Example 1:

Example 2: An OTC-like steel forward would allow a construction company to lock-in

today the price of steel, which is major input cost when submitting bid. It allows contract’s buyer to lock-in today the price of steel that will delivered

at future date

Forward Transactions Index Forwards/Futures are always cash settled. Settlement at expiry for Equity Forwards/Futures can be cash settled or by

delivery of assets.

Futures Contracts Stock Market’s Regulatory Bodies Hedging using Stock futures

(Example) Futures Contracts – Margin

requirement

Futures contract

• .

Microsoft Excel Worksheet

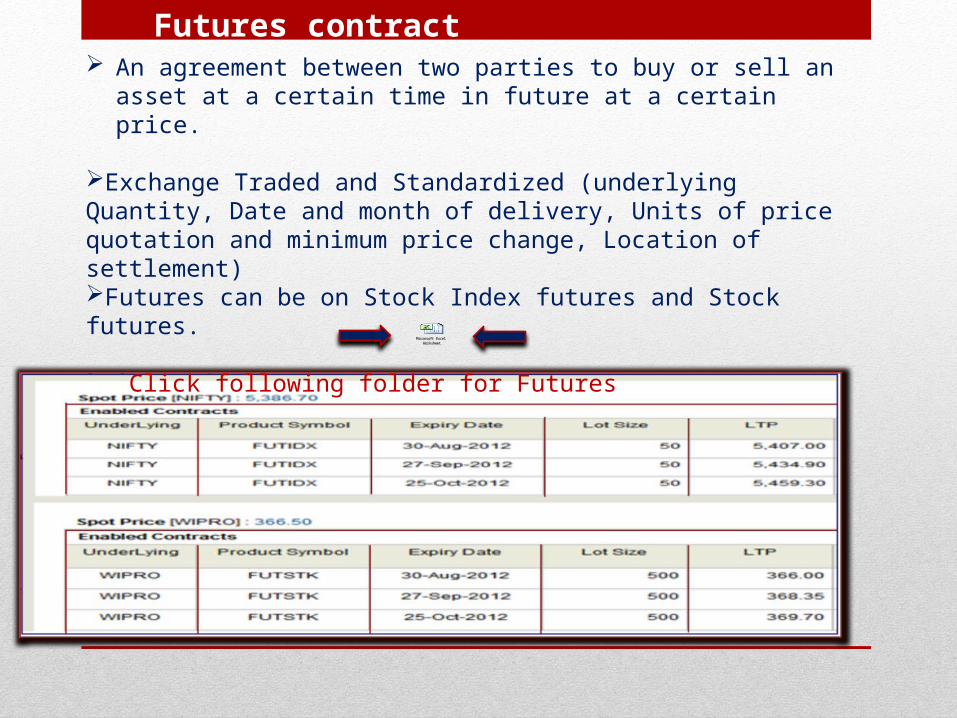

An agreement between two parties to buy or sell an asset at a certain time in future at a certain price.

Exchange Traded and Standardized (underlying Quantity, Date and month of delivery, Units of price quotation and minimum price change, Location of settlement)Futures can be on Stock Index futures and Stock futures.

Click following folder for Futures

Futures Transactions Index Forwards/Futures are always cash settled.

Settlement at expiry for Equity Forwards/Futures can be cash settled or by delivery of assets.

Delivery of Assets:

- The Buyer has to buy the assets at the future price

- The Seller has to sell the assets at the future price Cash Settled:

- The Buyer will get the value = Market Price – Future price

- The Seller has to pay the value = Market Price -Future Price

Default risk for Futures is lower because:

- Clearing House of the exchange guarantees the payment

- An initial margin is required to enter into Future contract

Distinction between Futures and Forwards

.

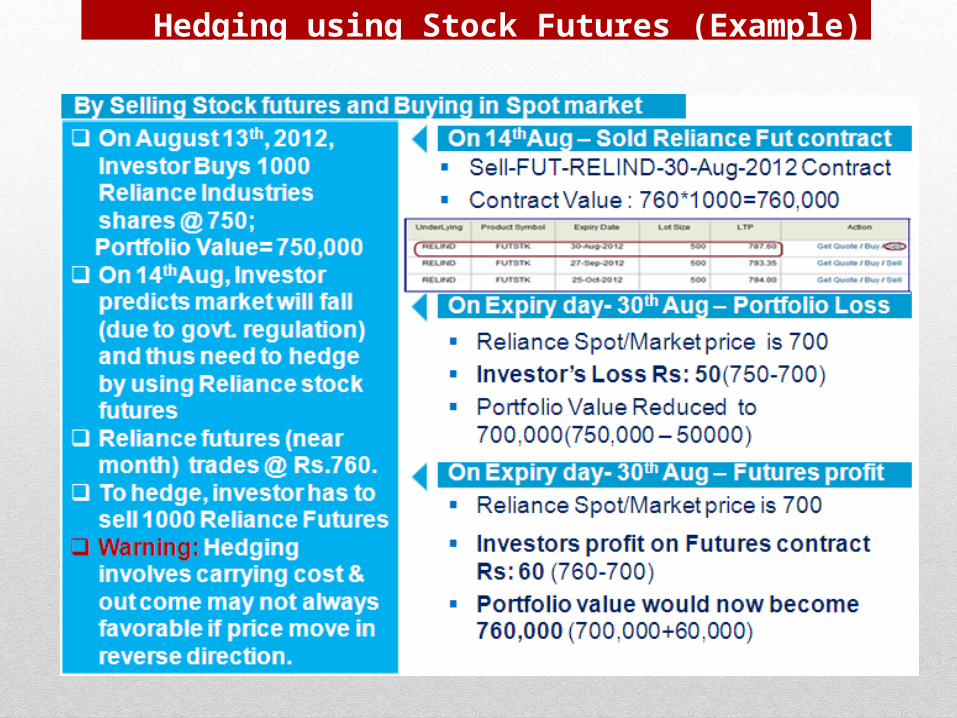

Hedging using Stock Futures (Example)

.

Future Contracts- Margins

Initial Margin: The amount must be deposited in margin account at future account to enter into contract.(Initial Margin on Futures is computed using VaR)

VaR (Value at Risk): A risk management methodology, which attempts to measure the maximum lose possible on a particular position, with a specified level of certainty or confidence.

Maintenance Margin: Minimum margin required by investors in margin account throughout the contract. (Lesser than initial margin)

Mark-to-Market: It is the process of adjusting the value of investments to reflect their current market price. Margin account adjusted to reflect investor’s gain/loss depending on futures closing price.

Futures Margin Example

.

Options Contracts

Introduction to Options Options Terminology Call Vs. Puts Options Payoff Options Pricing Call Option – Example on

Speculation

Options Contracts

An ‘Option’ is a contract that gives the buyer the right, but not the obligation, to sell or buy a particular asset at a particular price, on or before a specified date.

‘Option’ as a word suggests, is a choice given to buyer to either honor the contract; or if he chooses not, to walk away from the contract.

Options Contracts traded on exchanges as well as OTC.

Options can be traded on Commodities, Stocks, Sock Indexes, Interest Rates, Bonds, Currencies etc.,

Strike Price / Exercise Price: Denotes the price at which the buyer of the option has a right to purchase or sell underlying.

Based on the liquidity, Exchange will determine the interval & strike prices:

Options terminology

Buyer/Holder of an Option: Buyer is the one who by paying the option premium buys the right but not obligation. (Said to be long)

Seller/Writer of an Option: Writer of a call/put option, is the one who receives option premium and obliged to sell/buy the asset if buyer exercises. (Said to be short)

Premium: Cost of the Option to the buyer, for buying the rights. Non-returnable and paid by Option holder to Writer.

Index Options: Have the Index as the underlying. (Nifty, FTSE, NYSE) They are also cash settled.

Stock Options: They are options on Individual stocks. (Reliance, Wipro, HLL) They are also cash settled.

Lot size: The quantity of underlying asset in one contract. Options can be on Stock Index futures and Stock futures.

Click following folder for Options Stock list (NSE) for Lot size

Expiry Date: The last date up to which the o

Microsoft Excel Worksheet

Two Basic types of Options: Call and Put Options

Call Option: It gives the holder the right but not the obligation to buy an asset by certain date by certain price.

The Buyer of an option contract is said to be long or the holder or owner of the contract.

The Seller of an options contract is said to be short or the writer of the contract.

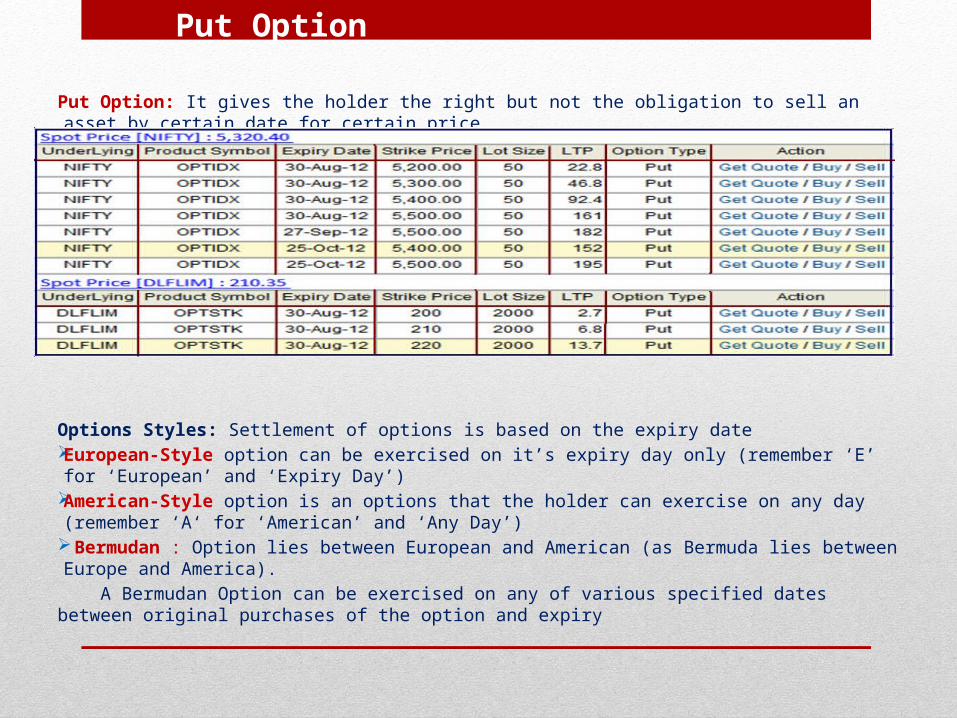

Put Option

Put Option: It gives the holder the right but not the obligation to sell an asset by certain date for certain price.

Options Styles: Settlement of options is based on the expiry date European-Style option can be exercised on it’s expiry day only (remember ‘E’ for ‘European’ and ‘Expiry

Day’) American-Style option is an options that the holder can exercise on any day (remember ‘A‘ for

‘American’ and ‘Any Day’) Bermudan : Option lies between European and American (as Bermuda lies between Europe and

America).

A Bermudan Option can be exercised on any of various specified dates between original purchases of the option and expiry

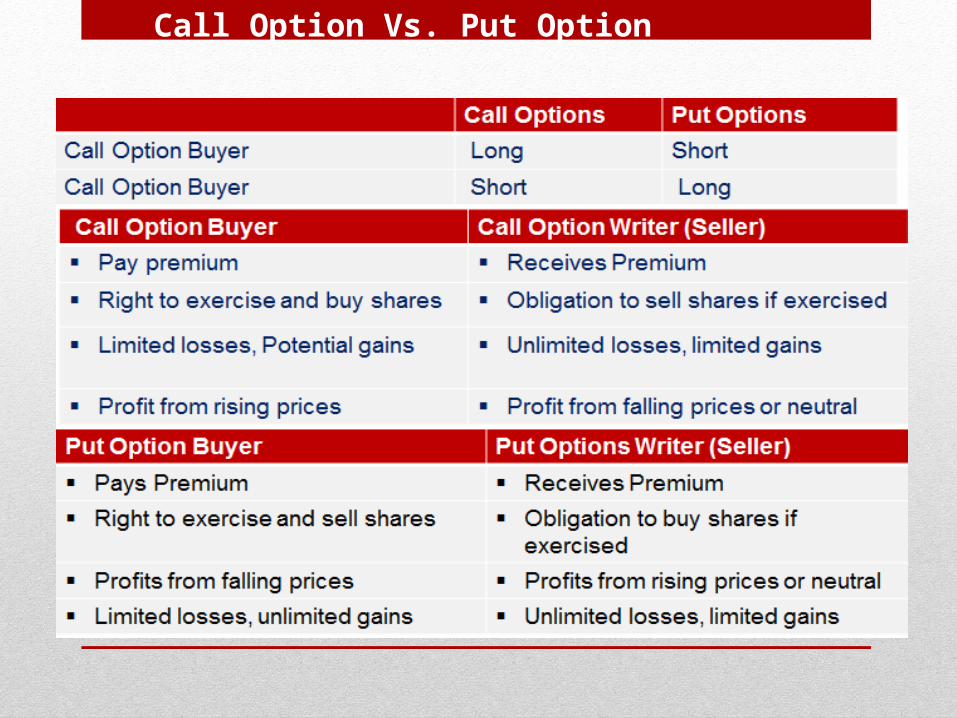

Call Option Vs. Put Option

.

Strike Price & Pay offs

Pricing of Option: Factors affecting the Option Premium:

Price of Underlying Time to Expiry Exercise Price Time to Maturity Volatility of the Underlying Interest Rates (Opportunity cost)

Option Premium = Intrinsic Value(IV) + Time Value (TV) Intrinsic Value (IV) is the difference between the strike price and the underlying

asset’s price..

For a Call Option = Spot Price – Strike Price For a Put Option = Strike Price – Spot Price

Call Option – Pay off profile (Exp.Buyer’s perspective)

.

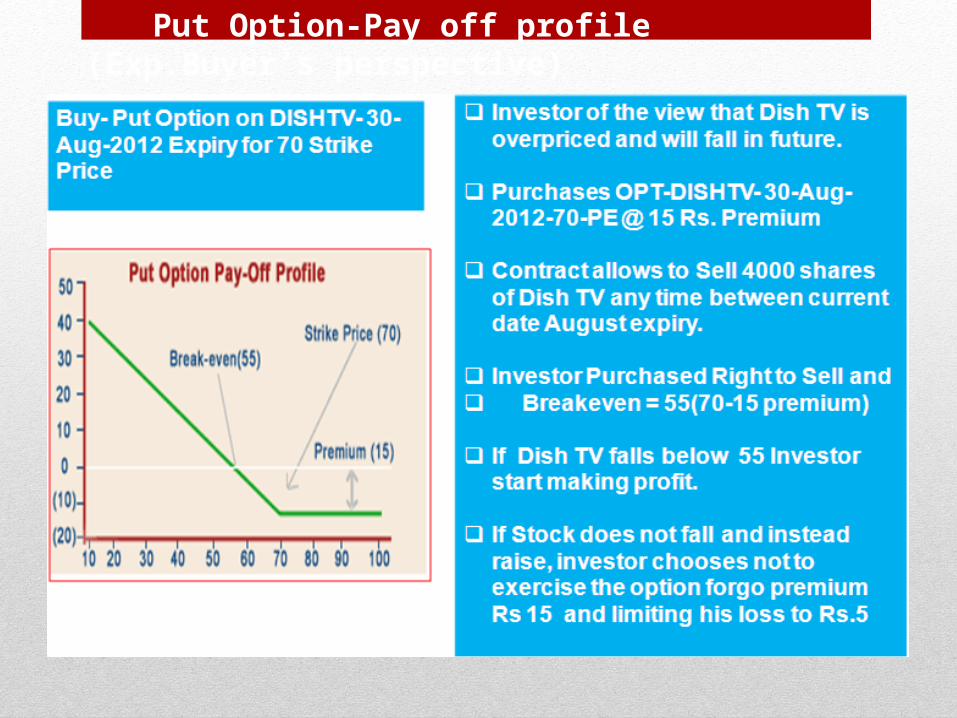

Put Option-Pay off profile (Exp.Buyer’s perspective)

.

Option Pricing

.Option Pricing Model:

Black & Scholes Model is one of the popular option pricing model to arrive right

value of option.

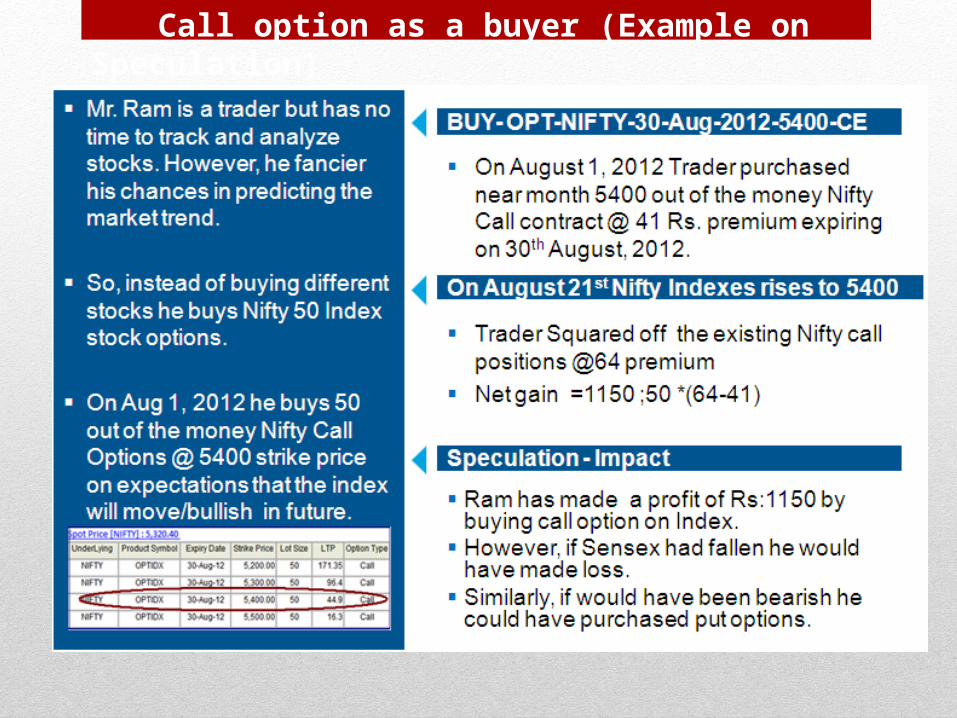

Call option as a buyer (Example on Speculation)

.

(OTC) Over-The-Counter Derivatives

OTC InstrumentsCurrent OTC

Environment

Global OTC Derivatives Market

The notional amount of OTC Derivatives outstanding stood

more than $633 Trillion at the end of December,2012. (source:BIS -Bank for International Settlements)

OTC Derivative Environment

• Forward Rate Agreements Introduction to FRA Forward Rate agreement & Calculation

Forward Rate Agreements (FRAs)

FRA is an agreement to buy or sell an interest rate, which is fixed today and which will be revalued against prevailing market rates, using benchmark rate (LIBOR) :

- Starting on an Agreed future date- For an agreed future period- Based on an agreed principal amount (a notional amount, i.e., used for

calculation but not actually transferred)

No Principal amount actually borrowed or lent, but a cash flow arises from the differences between the interest rate fixed (the fixed-rate) at the outset and the level benchmark rate (LIBOR) at a point of time in the future (the floating-rate)

The benchmark rate e.g.. LIBOR (i.e. the floating-rate) value is determined the first day of the FRA period and will then apply through to agreed maturity.

(LIBOR –FRA Rate) X Days in FRA period

NotionalPrincipal Amount X Days in Year

----------------------------------------

( 1+ (LIBOR X Days in FRA period ))

Days in Year

Net Settlement amount calculated as follows:

Example on Forward Rate Agreement &

Calculation

Suppose in the example, interest rates have fallen and the LIBOR fixing was 5.25%. The company will have to pay the seller .15% on 15 million Euro.

If Interest Rates change in adverse

(0.055 – 0.540) x 182/360

15,000,000 EURO X ______________________ = 11,064.06 EUR

( 1 + (0.0555 X 182/360))

The net settlement amount is

A company knows that, in one month’s time it will

need to borrow 15 million Euro for a period of six months

The company ‘s treasurer is concerned that interest

rates might rise in the next month, there by making its borrowing more expensive. He wants to fix the future borrowing rate today even though the money is not needed for a month. He enterers into a forward rate

agreement where by he ‘buys’ an FRA on 15 million EURO to start in one month’s time to run for a period of six months at a rate of 5.4 %.

Foreign Exchange (FX) Forwards

FX spot market involves the exchange of two currencies very soon after the date of transaction. Most currency transactions in the wholesale market is T+2.

( Trading day + 2 days) The market is used by customers with a need to exchange one currency for another.

Exp: Importer or Export of goods and services

Purchase or Sale of Investments For interbank deals, the GBP/USD spot rate might quoted as 1.5975/80 One Foreign currency is quoted of another; The first currency quoted (GBP) is

called the ‘Base currency’ In above example: $ 1.5975 is bid price and Ask price/offer price is ($1.5980)

Outright Forwards: Any FX contracts that matures one day beyond the normal spot date (T+2) is considered a forward deal.

1 Month is 1.2845/1.2820; 3 Month is 1.2775/1.2795

SWAPS

Introduction to Swaps Swaptions Interest Rate Swaps Currency Swaps

Swaps

A contract between two parties to exchange future cash flows on the basis of a pre arranged formula. Most of them are traded Over The Counter (OTC)

Interest Rate Swaps

Equity Swaps

Currency Swaps

Credit Default Swaps etc.

Swaptions:

Agreement where a buyer pays an upfront sum for the right to enter into a swap agreement, by a pre-agreed date in the future. (Buyer of a Swaption has the option to enter into a Swap).

Applicability: Large corporations and institutions use these Interest Rate Swaps and Swaptions for the following:

- Manage risk

- Potentially take advantage of cheaper and more appropriate funding.

Interest Rate Swaps

An IR Swap is an agreement to exchange a series of cash flows on a fixed Interest Rate for a series of cash flows based on a periodically adjusting (floating) deposit market interest rate (LIBOR).

LIBOR (London Interbank Offered Rate): It is known at the beginning of each period and paid at the end of the period.

IR Swap Buyer: will make the fixed payments. Aim is to transform the variable rate nature of its liabilities into fixed rate liabilities to better match the fixed returns earned on its assets.

IR Swap Seller: will make the float payments. Aim is to transform the fixed nature of its liabilities to variable rate liabilities to better match the variable return on its assets.

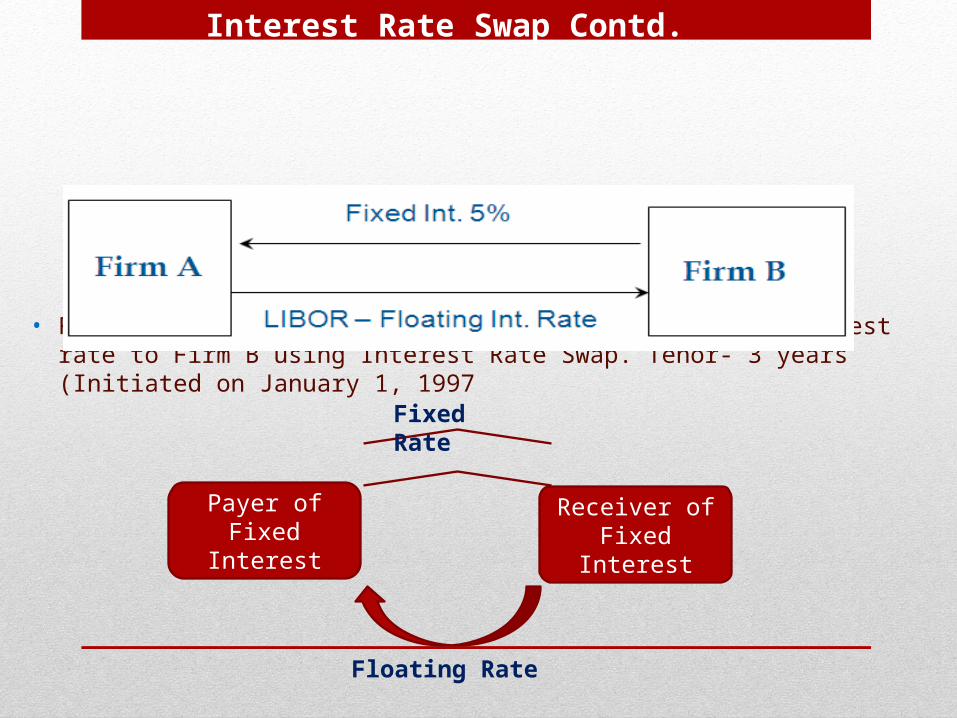

Interest Rate Swap Contd.

• Firm A receives 5% fixed Interest and pays LIBOR interest rate to Firm B using Interest Rate Swap. Tenor- 3 years (Initiated on January 1, 1997

Payer of Fixed Interest

Receiver of Fixed Interest

Fixed Rate

Floating Rate

Interest Rate Swap Contd.. Firm A’s view

The Sale of an Interest rate swap will enable Firm A to RECEIVE Fixed Interest Payments over the pre-determined period.

As the Seller (Firm B) will PAY Fixed Interest payments for the pre-determined period.

Firm A ‘s

Perspective

Millions of Dollars ($100 million notional principal)

Date LIBOR Floating Cash Flow

Fixed Cash Flow

Net Cash Flow

1/ 1/ 97 4.20

7/ 1/ 97 4.80 -2.10 2.50 0.40

1/ 1/ 98 5.30 -2.4 2.50 0.10

7/ 1/ 98 5.40 -2.65 2.50 -0.15

1/ 1/ 99 5.50 -2.70 2.50 -0.20

7/ 1/ 99 5.6 -2.75 2.50 -0.25

1/ 1/ 00 5.9 -2.80 2.50 -0.3

Interest Rate Swap Contd.. Firm B’s View

The Sale of an Interest rate swap will enable Firm A to PAY Floating Interest Payments over the pre-determined period.

As the Seller (Firm B) will RECEIVE Floating Interest payments for the pre-determined period.

Firm B’s

Perspective

Millions of Dollars ($100 million notional principal)

Date LIBOR Floating Cash Flow

Fixed Cash Flow

Net Cash Flow

1/ 1/ 97 4.20

7/ 1/ 97 4.80 2.10 -2.50 -0.40

1/ 1/ 98 5.30 2.4 -2.50 -0.10

7/ 1/ 98 5.40 2.65 -2.50 +0.15

1/ 1/ 99 5.50 2.70 -2.50 +0.20

7/ 1/ 99 5.6 2.75 -2.50 +0.25

1/ 1/ 00 5.9 2.80 -2.50 +0.3

Currency Swap

A Swap that involves the exchange of ‘Principal’ and ‘Interest’ in one currency for the same in another currency. It is considered to be a foreign exchange transaction and is not required by law to be shown on the balance sheet.

For example, suppose a U.S.-based company needs to acquire Swiss francs and a Swiss-based company needs to acquire U.S. dollars. These two companies could arrange to swap currencies by establishing an interest rate, an agreed upon amount and a common maturity date for the exchange.

Currency swaps were originally done to get around exchange controls.

Credit Derivatives

Classification of Credit Derivatives Credit Default Swaps

Overview on Credit Derivatives

Credit Derivatives are instruments that allow one party (beneficiary) to transfer credit risk of a reference asset to another party (guarantor) without actually selling the asset.

Derivative instruments whose value depends on agreed CREDIT EVENTS relating to a 3rd party company.• Default or Bankruptcy• A Credit rating downgrading of that company• Increase in that company’s cost of funds in the market

Credit Risk: Risk that borrower will default on any type of debt by failing to make payments.

Credit Events: If following credit events occur the seller makes a predetermined payment to the buyer; then Swap then terminates:

1. Default

2. Significant Fall in Asset price/value

3. Bankruptcy

4. Debt Restricting

5. Merger or Demerger

Classification of Credit Derivatives

1. Credit Default Swaps (CDS) CDS are more important type of Credit Derivative instruments which constitutes of 80% of total volume of Credit Derivatives

2. Total Return Swaps ( TRS)

3. Credit Linked Notes (CLN)

4. Collateral Debt Obligation (CDO)

5. Credit Options

Credit Derivatives – Benefits: Allow Banks and other institutions to hedge positions for the bear credit risk. (Default

Risk) Induce Banks to increase and diversify their lending activity by enabling them to hedge

their credit risk. Protect against unwanted credit exposure by passing that exposure to some one else. Increase credit exposure in return for income.

Credit Default Swap - Definition

A Credit default swap is similar to a Credit insurance contract whereby the protection Buyer transfers the risk that the reference entity will default

In return for the protection, the buyer pays a protection coupon to the seller, quarterly in arrears.

If a Credit Event occurs; the buyer delivers a portfolio of obligations of the reference entity, and receives par (or settles a net cash amount)

Credit Risk

Protection Buyer

Protection Seller

Risk Fee / Premium

Contingent Payment on default (losses)

Protection buyer Protection Seller

Credit Default Swaps contd..

When entering into a Credit Default Swap, the parties agree on the following - Credit Events that can trigger the settlement Notional Amount Rate for the premium (usually expressed in basis points per annum) Settlement Method (Physical or Cash) Maturity date of the transaction.

At maturity, the Buyer stops paying the premium and the protection expires.

Credit Default Swaps- Types

Single-name Credit Default Swap: A credit derivative where the reference asset is from a single entity.Multi-name Credit Default Swap: A contract where the reference entity is more than one name as in a portfolio or basket credit default swaps or credit default swap indices.Basket Credit Default Swap: is a Credit Default Swap referenced to a bunch of reference obligations.

Credit Default Swaps – Generic Trade Process Flow

Pretrade

Bilateral documentation and internal approvals - Overall parameters of trading activities are established through a bilateral master agreement. Counterparty credit reviews are conducted to establish credit lines and trading limits. E.g. International Swaps and Derivatives Association (ISDA) Master Agreement

Trade execution - Parties agree on terms via phone, fax, and/or electronic means.

Trade capture - Trade details are captured for processing and risk management. This may be manual (via trade tickets) or electronic.

Trade verification - Counterparties may opt to verify key economic details of the trade.

Trade affirmation or matching - Trade details may be provided by one party and affirmed by the other, or each party may exchange records for matching.

Confirmation - Final confirmation of the trade details are secured and exchanged. Confirmations may be paper-based or electronic-based.

Settlement - Cash or other assets are exchanged per the terms of the contract.

Trade Post-Trade

Credit Default Swaps – Transaction Legs

• Premium Leg – These are the periodic payments made the protection buyer to the protection seller till occurrence of credit event or maturity.

• Protection Leg – This is a one-time payment made by protection seller to the protection buyer on occurrence of a credit event. This payment equals the difference between par value and the price of the assets of the reference entity on the face value of the protection, and compensates the protection buyer for the loss.

Credit Default Swaps – Post Trade

Trade Confirmation

Submits the trade to Deriv/SERV

Deriv/SERV checks whether the trade is DTCC eligible

Submits the trade to Deriv/SERV

Send the trade back to Party A

Deriv/SERV compares both sides of the transactions

Do both sides match perfectly?

Transaction reported as “Confirmed” match

Reports the “Best Possible” match along with unmatched fields

Is the trade DTCC eligible?

Send the trade back to Party B

NO

NO

YES

Party A Party B

• OTC Trade Processing Services

DTCC: The Depository Trust & Clearing Corporation Largest Global Securities processing service Provides a matching service (‘Deriv/SERV’) for OTC derivatives (used in

post trade processing) Service requires mainframe-to-mainframe connections between the DTCC

and each firm. Deriv/SERV is a global service offering focused on automating the entire life

cycle of OTC Derivatives This includes front-office trade affirmation, automated confirmation and

matching, payment processing and a trade warehouse.Following electronic services are currently available in the Derivatives

Market: Markit SERV Markit Wire Swap Clear SWIFT FpML TriOptima ICE Link

Commodities & Exotics

Global commodity Derivatives MarketsBase and Precious MetalsSofts and AgriculturalEnergy ProductsExotics & Emissions

Global commodity Derivatives MarketsCommodity is a raw or primary product ; Commodity derivatives are based on commodities as distinct from financial derivatives.

Agricultural products (Live stock, Grain and Fruit) Energy Products (such as Oil and Gas) Metals (Copper, Aluminum)

Softs and Agricultural

Softs is a label for set of commodities that includes cocoa, sugar and Coffee.

Agricultural commodities would be the grains such as wheat and soya beans as well as livestock and seeds oils.

The price influence on soft commodities (Coffee, Sugar, Cocoa) and agricultural products (Wheat, Soya beans etc.) can be summarized as supply and demand factors.

Energy Products Energy Markets includes market for refined oil products and natural gas products.

Supply is finite, and countries with surplus oil and gas reserves are able to export to those countries with insufficient oil and gas to meet requirements.

Demand for oil and gas is ultimately driven by levels of consumptions which in turn is driven by energy needs (manufacturing industry and transport).

Exotics

Recent developments seen the expansion of derivatives trading into a wide range of exotics contracts.

A Weather derivative is contract that obligates the buyer to purchase the value of the underlying weather index – measured in heating degree days (HDD) or cooling degree days (CDD) at a future date.

Weather futures can enable business to protect themselves against losses caused by unexpected shifts in weather conditions.

Contract prices are also subject to 'shock' when unexpected weather events happen such as Hurricanes and Snowstorms.

Freight Derivatives It include forward freight agreements (FFA)s, container freight swap agreements and options,

are financial contracts that are based on the future levels of freight rates for dry bulk carriers tankers and containerships.

Primarily used by ship-owners and operators, oil companies trading companies and grain houses as tools for managing freight rate risk.

EFAs are often traded over-the-counter(through broker members of the Forward Freight Agreements Brokers' Association –FFAB).

Emissions

Growing environmental concerns have prompted several exchanges to start trading several different types of emissions contracts.

Exchanges in Europe, Asia and North America have listed several types of futures contracts for carbon dioxide, Sulpher Dioxide, Methane and Nitrogen Dioxide Emissions.

Those entities that are heavy polluters buy these to offset what they produce.

As regulations get stricter and pollution targets are reduced, prices as expected to rise.

The contracts set price for set amount of emissions allotments, with the goal of getting emissions to a predetermined level such as those set by the Kyoto Accord.

Derivatives can be high-risk.

It was mainly trading in Derivatives that brought about the collapse of 'Lehman Brothers', 'Bearings' and massive monetary losses at other organizations, with the 2008 credit crunch

With Disciplinary and self regulatory approach we can trade Derivatives.

Conclusion

Dodd-Frank Act & Technical Implications

Background of Dodd-Frank Act Proposed Central Counter Parties (CCP) Technology Implications of CCP

Background of Dodd-Frank Act

The Dodd-Frank Act signifies the biggest US Regulatory change and President Obama signed the Dodd-Frank Wall Street Reforms Consumer protection act (the Reforms Act) on July 21, 2010.

The intent of Dodd-Frank is to instill confidence in the financial markets by boosting transparency and liquidity, and mitigating counterparty exposure concentration.

Certain provisions of the reforms Act are immediately effective, and certain provisions will become effective on later dates.

More specifically, the reforms looks to mitigate the risk posed by activity that falls outside direct regulatory supervision, specifically the bilateral trading and clearing of over-the-counter (OTC) Derivatives.

Under the Dodd-Frank, clearing for all standardized OTC Derivative contract is to be carried out via Central Counterparties (CCP) by end of 2012.

Technology Implications of CCP

It is imperative, however that CCPs continue to make the necessary investments in technology to ensure and maintain best practices (Automatic, Electronic confirmations and Portfolio Reconciliation ) to operational risk.

As per market estimates the largest 15 dealers will spend approximately $1.8 billion to implement the Dodd-Frank rules for Derivatives.

From Business perspective Clearing and Execution are the key investment areas.

Investment Manager will incur higher technology and operations cost, as they need to reengineer process and technology to meet new requirements.

Futures Commission Merchants are likely to pass along the costs incurred in the setting up the systems and technology need to provide connectivity with multiple CCPs (CME, ICE, LCH, IDCG, EURES), SEFs(Trade Web, Market Access, Bloomberg, DFI, ICAP etc.) and SDs.