desert oaks plaza - constant...

TRANSCRIPT

DESERT OAKS PLAZANorth Las Vegas, Nevada

Offering Memorandum

N O N - E N D O R S E M E N T A N D D I S C L A I M E R N O T I C E

Confidentiality and DisclaimerThe information contained in the following Marketing Brochure is proprietary and strictly confidential. It is intended to

be reviewed only by the party receiving it from Marcus & Millichap and should not be made available to any other

person or entity without the written consent of Marcus & Millichap. This Marketing Brochure has been prepared to

provide summary, unverified information to prospective purchasers, and to establish only a preliminary level of

interest in the subject property. The information contained herein is not a substitute for a thorough due diligence

investigation. Marcus & Millichap has not made any investigation, and makes no warranty or representation, with

respect to the income or expenses for the subject property, the future projected financial performance of the

property, the size and square footage of the property and improvements, the presence or absence of contaminating

substances, PCB's or asbestos, the compliance with State and Federal regulations, the physical condition of the

improvements thereon, or the financial condition or business prospects of any tenant, or any tenant's plans or

intentions to continue its occupancy of the subject property. The information contained in this Marketing Brochure

has been obtained from sources we believe to be reliable; however, Marcus & Millichap has not verified, and will not

verify, any of the information contained herein, nor has Marcus & Millichap conducted any investigation regarding

these matters and makes no warranty or representation whatsoever regarding the accuracy or completeness of the

information provided. All potential buyers must take appropriate measures to verify all of the information set forth

herein. Marcus & Millichap is a service mark of Marcus & Millichap Real Estate Investment Services, Inc. © 2016

Marcus & Millichap. All rights reserved.

Non-Endorsement NoticeMarcus & Millichap is not affiliated with, sponsored by, or endorsed by any commercial tenant or lessee identified in

this marketing package. The presence of any corporation's logo or name is not intended to indicate or imply

affiliation with, or sponsorship or endorsement by, said corporation of Marcus & Millichap, its affiliates or

subsidiaries, or any agent, product, service, or commercial listing of Marcus & Millichap, and is solely included for

the purpose of providing tenant lessee information about this listing to prospective customers.

ALL PROPERTY SHOWINGS ARE BY APPOINTMENT ONLY.PLEASE CONSULT YOUR MARCUS & MILLICHAP AGENT FOR MORE DETAILS.

DESERT OAKS PLAZA

North Las Vegas, NV

ACT ID Y0220036

TABLE OF CONTENTS

SECTION

INVESTMENT OVERVIEW 01Offering Summary

Regional Map

Local Map

Aerial Photo

FINANCIAL ANALYSIS 02Tenant Summary

Lease Expiration Chart

Operating Statement

Notes

Pricing Detail

Acquisition Financing

MARKET COMPARABLES 03Comparables

MARKET OVERVIEW 04

Market Analysis

Demographic Analysis

DESERT OAKS PLAZA

DESERT OAKS PLAZA

4

INVESTMENT

OVERVIEW

DESERT OAKS PLAZA

#

EXECUTIVE SUMMARY

OFFERING SUMMARY

MAJOR EMPLOYERS

EMPLOYER # OF EMPLOYEES

Walmart 1,846

Epic Resorts - Scottsdale 1,798

Santa Fe Station Ht & Casino 1,500

Cox Nevada Telcom LLC 1,320

San Lorenzo Italian Restaurant 1,300

Texas Gambling Hall & Ht Inc 1,300

Station Casinos Inc 1,000

Station Casinos LLC 1,000

Clark County School District 940

Nstec 806

ISS Facility Services Inc 803

Yucaipa Companies LLC 760

DEMOGRAPHICS

1-Miles 3-Miles 5-Miles

2015 Estimate Pop 15,663 157,122 409,007

2010 Census Pop 14,686 145,625 382,533

2015 Estimate HH 5,457 52,444 135,966

2010 Census HH 5,106 48,884 127,989

Median HH Income $61,005 $60,207 $53,153

Per Capita Income $24,591 $23,861 $22,837

Average HH Income $70,511 $71,235 $68,019

VITAL DATA

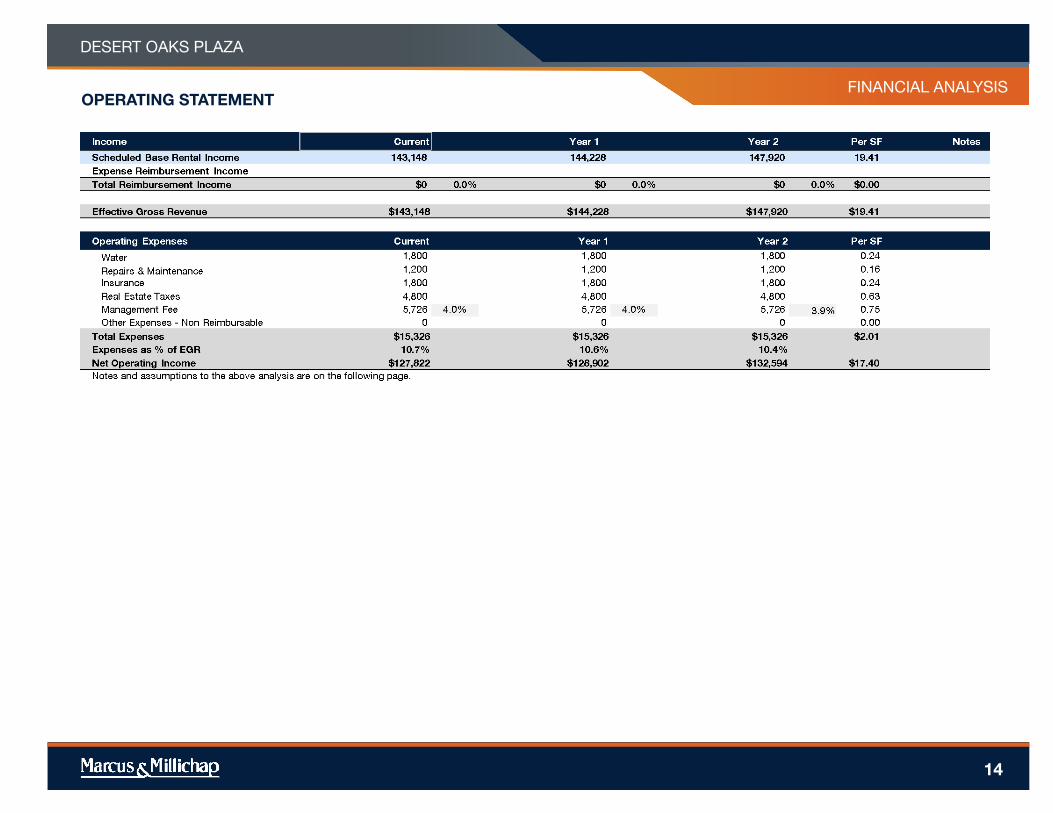

CURRENT PRO FORMA

Price $1,705,000 CAP Rate 7.56% 7.78%

Down Payment 40.6% / $692,230Net Operating Income

$128,902 $132,594

Loan Amount $1,023,000Net Cash Flow After Debt Service

8.76% / $60,668 9.3% / $64,360

Loan Type Proposed New Total Return 12.04% / $83,331 12.72% / $88,064

Interest Rate / Amortization 4.50% / 25 Years

Gross Leasable Area (GLA) 7,620 SF

Price/SF $224.00

Current Occupancy 81.63%

Year Built / Renovated 2008

Lot Size 0.57 acre(s)

5

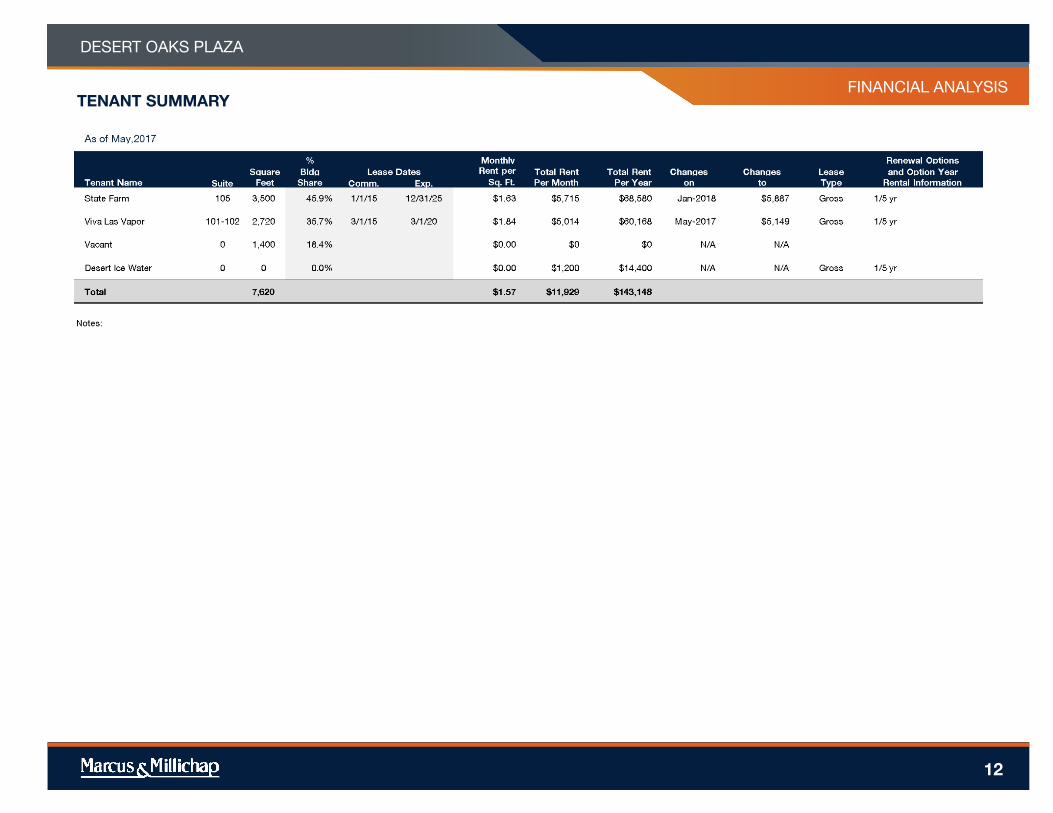

MAJOR TENANTS

TENANT GLA LEASE EXPIRATION LEASE TYPE

State Farm 3,500 12/31/2025 Gross

Viva Las Vapor 2,720 3/1/2020 Gross

DESERT OAKS PLAZA

#

OFFERING SUMMARY

High Traffic Counts

Newer Construction

Upside in Lease Once the Vacant Unit is Occupied

Pride of Ownership

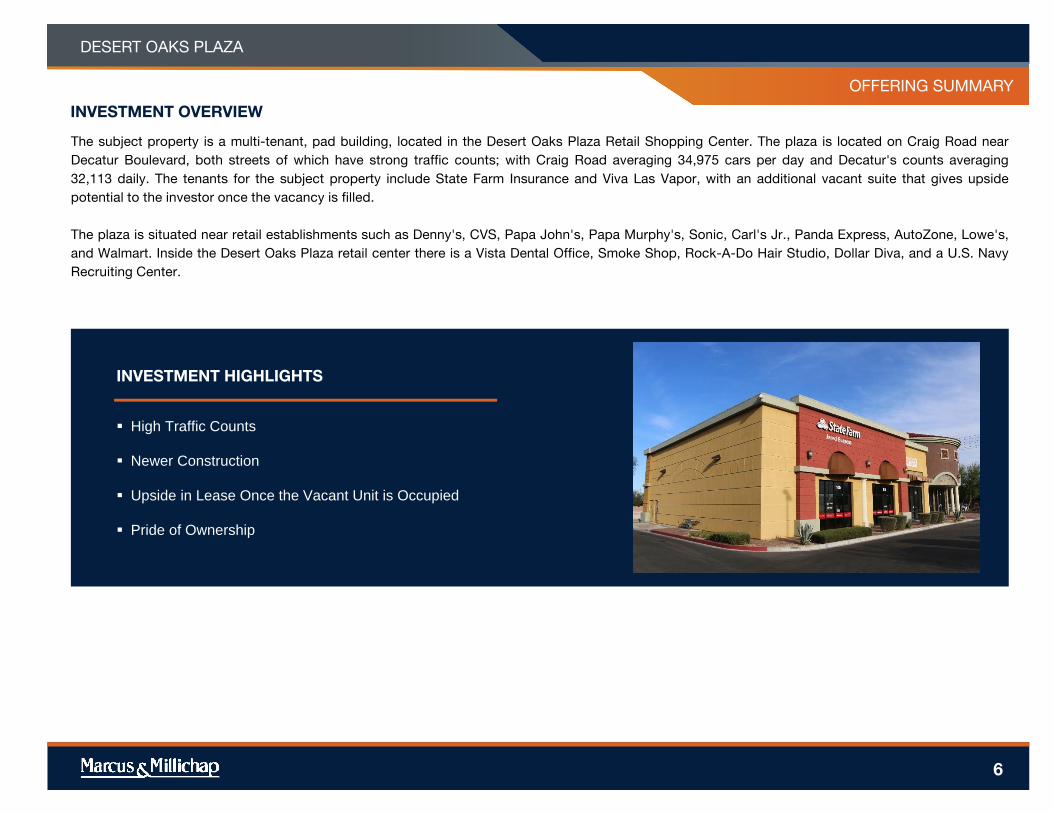

INVESTMENT HIGHLIGHTS

The subject property is a multi-tenant, pad building, located in the Desert Oaks Plaza Retail Shopping Center. The plaza is located on Craig Road near

Decatur Boulevard, both streets of which have strong traffic counts; with Craig Road averaging 34,975 cars per day and Decatur's counts averaging

32,113 daily. The tenants for the subject property include State Farm Insurance and Viva Las Vapor, with an additional vacant suite that gives upside

potential to the investor once the vacancy is filled.

The plaza is situated near retail establishments such as Denny's, CVS, Papa John's, Papa Murphy's, Sonic, Carl's Jr., Panda Express, AutoZone, Lowe's,

and Walmart. Inside the Desert Oaks Plaza retail center there is a Vista Dental Office, Smoke Shop, Rock-A-Do Hair Studio, Dollar Diva, and a U.S. Navy

Recruiting Center.

INVESTMENT OVERVIEW

6

DESERT OAKS PLAZA

#

PROPERTY SUMMARY

OFFERING SUMMARY

PROPOSED FINANCING

First Trust Deed

Loan Amount $1,023,000

Loan Type Proposed New

Interest Rate 4.50%

Amortization 25 Years

Loan Term 5 Years

Loan to Value 60%

Debt Coverage Ratio 1.89

THE OFFERING

Property Desert Oaks Plaza

Price $1,705,000

Property Address 3930 West Craig Road,North Las Vegas,NV

SITE DESCRIPTION

Year Built/Renovated 2008

Gross Leasable Area 7620

Ownership Fee Simple

Lot Size 0.57 acre(s)

7

Loan rates are subject to change at any time. Please consult your MMCC representative for more information.

Nick GrayMarcus & Millichap Capital Corporation

3800 Howard Hughes ParkwaySuite 1550

Las Vegas, NV 89169(702) 215‐7100 ext. 7144

(702) 215‐7110 [email protected]

NMLS: 1152363NV: 4096

CA: 01910898

REGIONAL MAP

DESERT OAKS PLAZA

8

LOCAL MAP

DESERT OAKS PLAZA

9

AERIAL PHOTO

DESERT OAKS PLAZA

10

DESERT OAKS PLAZA

11

FINANCIAL

ANALYSIS

FINANCIAL ANALYSIS

DESERT OAKS PLAZA

12

TENANT SUMMARY

12

TENANT SUMMARYFINANCIAL ANALYSIS

DESERT OAKS PLAZA

13

FINANCIAL ANALYSIS

DESERT OAKS PLAZA

OPERATING STATEMENT

14

FINANCIAL ANALYSIS

DESERT OAKS PLAZA

PRICING DETAIL

15

DESERT OAKS PLAZA

16

MARKET

COMPARABLES

8

DESERT OAKS PLAZA

SALES COMPARABLES MAP

17

DESERT OAKS PLAZA

(SUBJECT)

Pecos Patrick Retail Center

Siegel Plaza

Sahara & Nellis Retail

Center

Sahara Pointe

351 E Silverado Ranch Blvd

Torrey Pines Shopping

Center

Craig Plaza

Southfork Pointe

SALES COMPARABLES

1

2

3

4

5

7

8

6

18

Avg. 7.27%

0

1

2

3

4

5

5

6

7

8

9

Desert

Oaks Plaza

Pecos

Patrick

Retail

Center

Siegel

Plaza

Sahara &

Nellis

Retail

Center

Sahara

Pointe

351 E

Silverado

Ranch Blvd

Torrey

Pines

Shopping

Center

Craig Plaza Southfork

Pointe

Average Cap Rate

PROPERTY NAMEDESERT OAKS PLAZA

COMPARABLES

Avg. $269

$0

$60

$120

$180

$240

$300

$360

$420

$480

$540

$600

Desert

Oaks Plaza

Pecos

Patrick

Retail

Center

Siegel

Plaza

Sahara &

Nellis

Retail

Center

Sahara

Pointe

351 E

Silverado

Ranch Blvd

Torrey

Pines

Shopping

Center

Craig Plaza Southfork

Pointe

Average Price Per Square Foot

SALES COMPARABLES SALES COMPS AVG

PROPERTY NAME

MARKETING TEAM

DESERT OAKS PLAZA

COMPARABLES

rentpropertyname1

rentpropertyaddress1

rentpropertyname1

rentpropertyaddress1

rentpropertyname1

rentpropertyaddress1

19

SALES COMPARABLES

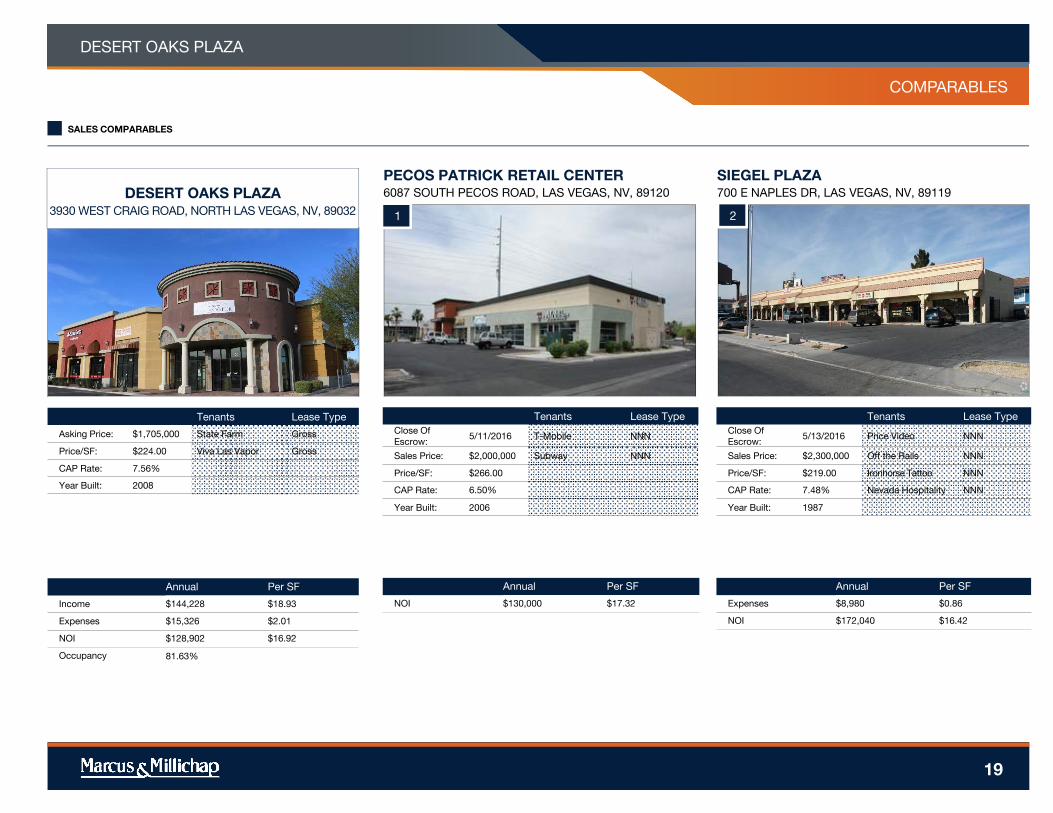

Annual Per SF

Income $144,228 $18.93

Expenses $15,326 $2.01

NOI $128,902 $16.92

Occupancy 81.63%

DESERT OAKS PLAZA

3930 WEST CRAIG ROAD, NORTH LAS VEGAS, NV, 89032

Tenants Lease Type

Asking Price: $1,705,000 State Farm Gross

Price/SF: $224.00 Viva Las Vapor Gross

CAP Rate: 7.56%

Year Built: 2008

1

PECOS PATRICK RETAIL CENTER

6087 SOUTH PECOS ROAD, LAS VEGAS, NV, 89120

Annual Per SF

NOI $130,000 $17.32

Tenants Lease Type

Close Of

Escrow:5/11/2016 T-Mobile NNN

Sales Price: $2,000,000 Subway NNN

Price/SF: $266.00

CAP Rate: 6.50%

Year Built: 2006

2

SIEGEL PLAZA

700 E NAPLES DR, LAS VEGAS, NV, 89119

Annual Per SF

Expenses $8,980 $0.86

NOI $172,040 $16.42

Tenants Lease Type

Close Of

Escrow:5/13/2016 Price Video NNN

Sales Price: $2,300,000 Off the Rails NNN

Price/SF: $219.00 Ironhorse Tattoo NNN

CAP Rate: 7.48% Nevada Hospitality NNN

Year Built: 1987

PROPERTY NAME

MARKETING TEAM

DESERT OAKS PLAZA

COMPARABLES

rentpropertyname1

rentpropertyaddress1

rentpropertyname1

rentpropertyaddress1

rentpropertyname1

rentpropertyaddress1

20

SALES COMPARABLES

3

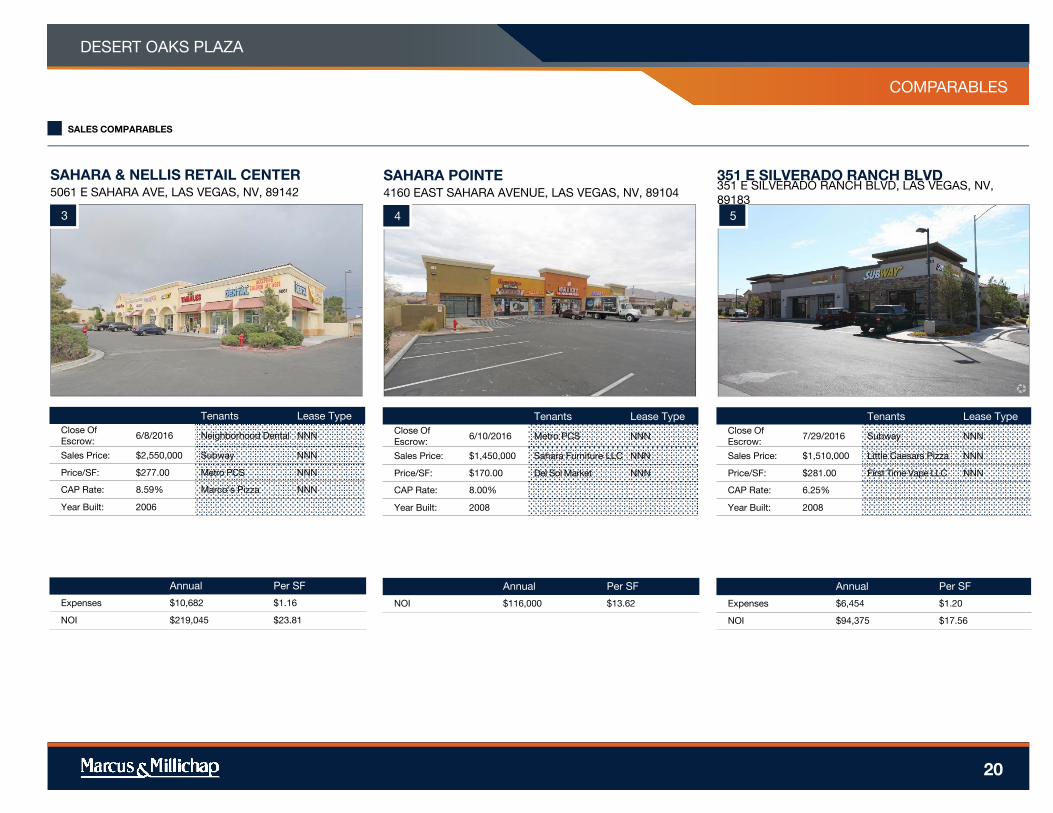

SAHARA & NELLIS RETAIL CENTER

5061 E SAHARA AVE, LAS VEGAS, NV, 89142

Annual Per SF

Expenses $10,682 $1.16

NOI $219,045 $23.81

Tenants Lease Type

Close Of

Escrow:6/8/2016 Neighborhood Dental NNN

Sales Price: $2,550,000 Subway NNN

Price/SF: $277.00 Metro PCS NNN

CAP Rate: 8.59% Marco's Pizza NNN

Year Built: 2006

4

SAHARA POINTE

4160 EAST SAHARA AVENUE, LAS VEGAS, NV, 89104

Annual Per SF

NOI $116,000 $13.62

Tenants Lease Type

Close Of

Escrow:6/10/2016 Metro PCS NNN

Sales Price: $1,450,000 Sahara Furniture LLC NNN

Price/SF: $170.00 Del Sol Market NNN

CAP Rate: 8.00%

Year Built: 2008

5

351 E SILVERADO RANCH BLVD351 E SILVERADO RANCH BLVD, LAS VEGAS, NV,

89183

Annual Per SF

Expenses $6,454 $1.20

NOI $94,375 $17.56

Tenants Lease Type

Close Of

Escrow:7/29/2016 Subway NNN

Sales Price: $1,510,000 Little Caesars Pizza NNN

Price/SF: $281.00 First Time Vape LLC NNN

CAP Rate: 6.25%

Year Built: 2008

PROPERTY NAME

MARKETING TEAM

DESERT OAKS PLAZA

COMPARABLES

rentpropertyname1

rentpropertyaddress1

rentpropertyname1

rentpropertyaddress1

rentpropertyname1

rentpropertyaddress1

21

SALES COMPARABLES

6

TORREY PINES SHOPPING CENTER

1000 S TORREY PINES DR, LAS VEGAS, NV, 89107

Annual Per SF

Expenses $4,328 $0.74

NOI $110,390 $18.90

Tenants Lease Type

Close Of

Escrow:11/29/2016 Market & Smokes NNN

Sales Price: $1,330,000 New York Pizza & Rib NNN

Price/SF: $228.00 America's Insurance NNN

CAP Rate: 8.30% Pico Barbershops NNN

Year Built: 1966

7

CRAIG PLAZA

2445 W CRAIG RD, NORTH LAS VEGAS, NV, 89032

Annual Per SF

Expenses $6,994 $1.26

NOI $75,600 $13.63

Tenants Lease Type

Close Of

Escrow:12/8/2016 Dollar Loan Center NNN

Sales Price: $1,080,000 B Nails & Spa NNN

Price/SF: $195.00 D L C Empire NNN

CAP Rate: 7.00%

Year Built: 2006

8

SOUTHFORK POINTE

9985 S EASTERN AVE, LAS VEGAS, NV, 89183

Annual Per SF

NOI $228,000 $30.95

Tenants Lease Type

Close Of

Escrow:1/5/2017 Verizon Wireless NNN

Sales Price: $3,800,000 Jimmy John's NNN

Price/SF: $516.00 Wing's Restaurant NNN

CAP Rate: 6.00%

Year Built: 2005

DESERT OAKS PLAZA

22

MARKET

OVERVIEW

MARKET OVERVIEW

Las Vegas-Henderson-Paradise Metro

Market Highlights

Robust employment growth

Nearly 100,000 jobs are forecast to be created through 2020, topping the national rate of growth.

Strong population gains

Over the next five years the metro’s population is expected to expand by 240,000 people,

dramatically outpacing the national growth rate.

Vast tourism industry

Tourism reached an all-time high in 2015 with 42 million visitors, placing Las Vegas among the top

10 of all U.S. cities.

LAS VEGAS

The Las Vegas metro, which comprises Clark County, is situated at the southeastern tip of Nevada. The

county is bordered by the state of California on the southwest and Hoover Dam, the Colorado River

and Lake Mead define the border with the state of Arizona to the east. The city proper is largely

bounded by mountains, government lands and military facilities, limiting developable land. Las Vegas,

the largest city in the county as well as state is know as "the live entertainment capital of the world."

Geography

DESERT OAKS PLAZA

23

MARKET OVERVIEW

Interstates 215 and 515 form a beltway around the Las Vegas metro, facilitating development in outlying

areas. The area is also served by Interstate 15, which stretches from Southern California to Salt Lake

City. U.S. 93 travels south, linking Las Vegas to Interstate 40, and U.S. 95 runs northwest to Reno.

McCarran International Airport, located minutes from the Las Vegas Strip, accommodates about 40

million passengers annually. Other air service is provided by North Las Vegas Airport, Henderson

Executive Airport, Jean Sport Aviation Center and Overton/Perkins Field.

RTC Transit operates the public bus system in Las Vegas, Henderson, North Las Vegas and the suburbs.

In addition, a monorail system connects some of the casinos along the Strip. Union Pacific offers freight

rail service connecting the area directly to California and Salt Lake City, facilitating the region’s

distribution capabilities.

Infrastructure

The Las Vegas Metro is:

270 miles from Los Angeles

285 miles from Phoenix

450 miles from Reno

570 miles from San Francisco

Airports

McCarran International Airport

Four general aviation airports

Major Roadways

Interstates 15, 215 and 515

U.S. 93 and 95

Rail

Freight – Union Pacific

Monorail between the casinos

The Las Vegas metro boasts 2.1 million people, accounting for more than 70 percent of Nevada’s total

population. Henderson, North Las Vegas, Spring Valley and Las Vegas were among the fastest-growing

cities in the United States in recent years. Las Vegas is the most populated city in the metro, with roughly

613,000 persons.

Metro

Largest Areas in Metro by Population

Las Vegas 613,000

Henderson 273,000

Paradise 234,100

North Las Vegas 233,700

Sunrise Manor 199,800

Spring Valley 188,600

* Forecast

Sources: Marcus & Millichap Research Services; U.S. Census

Bureau; Experian

LAS VEGAS

DESERT OAKS PLAZA

24

MARKET OVERVIEW

The Las Vegas economy is diversifying from tourism and gaming. The metro's

business-friendly environment, access to Western markets, large labor force, and

the availability of high speed data attract companies. A powerful data network

being built by Switch is helping to draw tech firms, while lower business costs

and a large skilled labor pool lure back-office operations. In addition, relatively

affordable land compared to other major metros is attracting large logistics and

manufacturing companies.

With all 10 of the nation’s largest hotels located in Las Vegas tourism and gaming

remain the significant drivers for the Las Vegas economy. New additions to the

strip this year will include MGM's 20,000-seat Las Vegas arena and Park

promenade and the Wynn Plaza shopping center will debut next year. Along with

tourism and gaming, conventions also play an integral part in the local economy.

Convention attendance neared 5.9 million delegates in 2015, the third

consecutive year of topping 5 million and providing a significant boost to the local

economy. The Las Vegas Convention Center is one of the largest in the world.

Population-serving sectors of the economy, such as education, healthcare and

retail trade, have grown in importance over the past two decades due to the

population nearly tripling in size. These sectors will continue to have a major roll

as population growth is forecast to exceed the national annual average.

Economy

* ForecastSources: Marcus & Millichap Research Services; Bureau ofEconomic Analysis; Moody’s Analytics; U.S. Census Bureau; Las Vegas Convention and Visitors Authority

LAS VEGAS

DESERT OAKS PLAZA

25

MARKET OVERVIEW

Las Vegas has an employment base of approximately 921,600 jobs. Job growth exceeded the national

expansion rate over the previous five years and this trend is projected to continue through 2020. During this

period, roughly 98,800 nonfarm jobs could be added, an annual increase of 2.1 percent, with all major sectors

expected to post gains. This is much higher than the expected national growth rate of 1.3 percent annually over

the same time period.

While Las Vegas has achieved considerable economic diversification over the past few decades, the leisure

and hospitality sector still provides the dominant share of metro jobs, accounting for 32 percent of total

employment. Growth in this sector is expected to accelerate through 2020, with the creation of nearly 36,000

positions. Given the size and importance of this sector to the region’s economy, such healthy growth in this

segment is an indicator of positive economic conditions going forward.

The improving economy and housing market are moving developments forward. As a result, construction,

which currently comprises 6 percent of area jobs, will be the fastest-growing employment sector in the coming

five years, with gains expected to average 3.7 percent annually. It is followed by financial activities, which will

expand 3.2 percent each year during this time.

Labor

* Forecast

Sources: Marcus & Millichap Research Services; BLS; Moody’s

Analytics

LAS VEGAS

DESERT OAKS PLAZA

26

MARKET OVERVIEW

Resorts and casinos continue to dominate the list of largest private employers in the county, including Wynn Las Vegas, MGM Grand and Caesars Palace.

Back-office operations have become increasingly prevalent in the metro. Factors such as a low cost of living allow major companies to affordably staff call centers and fill

data-entry positions. Office-using employment growth will outpace the national average this year.

Distribution centers and light manufacturing facilities are located throughout the metro. Digitek and Europa Sports have recently opened distribution centers. OfficeMax,

Zappos, Sysco Foods, Pepsi Bottling and Fellowes Manufacturing also maintain local facilities. As the need for industrial space mounts, Las Vegas’ proximity to other

major metros, more affordable land costs and an available labor pool will draw additional distributors.

The Nevada Test and Training Range along with Nellis and Creech Air Force Bases employ more than 10,000 military personnel and 4,000 civilians. Nellis AFB contains

the most squadrons of any Air Force installation. Nellis’ primary role is warfare training, and the base is the home of the United States Air Force Warfare Center, Air

Combat Command.

Employers

Major Employersaa

Wynn Resorts

Station Casinos

MGM Resorts

Las Vegas Sands

Caesars Entertainment

Boyd Gaming

The Valley Health System

Cosmopolitan of Las Vegas

Dignity Health-St. Rose Dominican

United Healthcare of Nevada

* Forecast

Sources: Marcus & Millichap Research Services; BLS; Moody’s

Analytics; Experian

LAS VEGAS

DESERT OAKS PLAZA

27

MARKET OVERVIEW

The Las Vegas metro registered substantial population growth over the last couple of decades and is expected to reach nearly 2.3 million residents over the next five years,

with the addition of 240,000 people during this period. This growth is attracting new businesses, retail and residential options in areas such as Downtown and Summerlin,

where a 400-acre project continues to be developed; the retail phase is already in place.

Las Vegas is not only a popular destination for retirees and vacationers, but families are also drawn to the area for jobs. Roughly 27.0 percent of residents are under the age

of 20, compared with 26.2 percent for the nation. In addition, a greater percentage of the local population is in prime child-bearing years of 25 to 44 than the U.S. Net

migration still accounts for the majority of the county’s population growth. This trend will continue over the decade as Las Vegas’ affordable housing and numerous

employment opportunities attract new residents to the metro.

The median household income in the metro, at $53,400 per year, is slightly below that of $56,100 annually for the nation. The median income level is expected to rise 2.8

percent annually through 2020. The median home price, at $225,100, is slightly below that of the U.S. median of $225,800. Just 53 percent of households own their home,

providing a large rental market.

Demographics

LAS VEGAS

* Forecast

Sources: Marcus & Millichap Research Services; AGS; Experian;

Moody’s Analytics; U.S. Census Bureau

DESERT OAKS PLAZA

28

MARKET OVERVIEW

With approximately 320 days of sunshine annually and an average temperature of 80 degrees, residents and visitors alike have plenty to do besides enjoy the resorts and

casinos in Clark County.

Water-sports enthusiasts can take advantage of various activities at Lake Mead and the Colorado River, including boating, fishing, water skiing and sailing. Red Rock

Canyon Conservation Area, located less than 20 miles from the Strip, offers outstanding hiking and mountain-climbing opportunities. Just 40 miles northwest of Las Vegas

is the Las Vegas Ranger District, which encompasses the 316,000-acre Toiyaba National Forest. The area has 52 miles of hiking trails, 150 campsites and snow skiing at

Lee Canyon.

Las Vegas is home to the University of Nevada-Las Vegas (UNLV), which offers higher education to an annual enrollment of more than 28,000 students. The institution has

received national recognition for its hotel management, criminal justice and social work programs. Other institutions of higher learning in Las Vegas include the College of

Southern Nevada, which has an annual enrollment of 44,000 students.

The Smith Center for the performing arts in downtown Las Vegas is a cultural complex that contains three theaters for the arts and an outdoor park used for concerts. The

Center is part of a larger downtown redevelopment project that includes housing, shops, museums, restaurants and galleries.

* Forecast

Sources: Marcus & Millichap Research Services; Moody’s

Analytics; National Association of Realtors; U.S. Census Bureau

Quality of Life

LAS VEGAS

DESERT OAKS PLAZA

29

MARKET OVERVIEW

2016 Retail Forecast

Construction: Builders will bring

610,000 square feet of retail space on

the market this year, the second highest

annual completion total since 2009.

Developers delivered more than 331,000

square feet in 2015, approximately

215,000 square feet of which came

during the second half of the year.

Vacancy: The metrowide vacancy ratewill drop 100 basis points this year to9.5 percent as net absorption reachesthe greatest level in 10 years. Anincrease in the vacancy rate of 30 basispoints was registered in 2015 on netabsorption of nearly 80,000 square feet.

Rents: Following a 2.5 percent rise in2015, the average asking rent in LasVegas will advance 2.5 percent to$16.80 per square feet.

Employment: The local economy will

gain 28,500 jobs in 2016, a 3.1 percent

expansion. Last year, employers in the

metro created 21,300 positions, led by

gains in the education and health

services sector.

DESERT OAKS PLAZA

30

LAS VEGAS METRO AREA

Retail Spending Increasing, Pushing Vacancy to Post-Downturn Best

Intense demand outstrips development, boosting property operations. Tourism dollars and an

expanding local economy will enable the Las Vegas retail market to record vacancy and rent

improvements this year despite healthy construction. Underlying demand in the retail sector is

strong as the metro’s gaming and convention industries continue to attract out-of-town spenders to

the market. Convention attendance in particular is exploding, rising nearly 15 percent year over year.

Additionally, the metrowide workforce has regained all the jobs lost during the recession, with

construction and healthcare fields leading growth. Robust market performance has encouraged

developers to increase their output. Retail construction is on pace for one of the greatest periods of

building since 2009 with projects by Ikea and Restoration Hardware headlining deliveries. The rise in

completions will not hinder the decline of the vacancy rate to a post-recession low. Tight market

conditions amid steady demand will lift rents for the third consecutive year. Despite the increase,

lease rates remain well below the prior peak, indicating plenty of runway for future improvements.

Property operators have kept rent hikes in check in an effort to maintain occupancy. However, as

available space continues to dwindle, well-located retail sites will see steady rent appreciation in the

months to come.

High returns and improving operations drive demand. The convergence of a strong pool of

buyers and a recent upswing in listings has ignited trade activity in the Las Vegas retail market.

Annual deal volume reached a post-recession high this year with both private and institutional

investors becoming more active. Buyer demand remains elevated as intense cap rate compression

in many West Coast markets draws investors to Las Vegas, where returns average in the low-7

percent range. These out-of-town buyers often leverage their considerable access to capital to

target larger, more expensive assets, leaving small to mid-size properties ripe for acquisition. On the

seller side, motivation is largely valuation driven with property owners looking to capitalize on

elevated pricing. Those who list often reinvest into existing retail centers, pay down debt or develop.

increase

in total

employment

610,000

3.1%

sq. ft.

will be

completed

basis point

decrease in

vacancy

100

2.5%

increase

in asking

rents

MARKET OVERVIEW

Economy

Construction

* Forecast

Sources: Marcus & Millichap Research Services; CoStar Group, Inc.

* Forecast

Sources: Marcus & Millichap Research Services; Bureau of Labor

Statistics; Economy.com

DESERT OAKS PLAZA

31

LAS VEGAS METRO AREA

Employers added 16,700 workers in the first half of 2016, contributing to a year-over-year job gain of 26,400

positions. This is a modest slowdown from the previous 12-month period, when Las Vegas establishments

created 34,100 jobs.

Payrolls at building firms are booming as infrastructure improvements and new developments progress

throughout the city. The construction sector expanded 13.7 percent in the past 12 months with approximately

7,000 workers gaining employment. The education and health services sector also registered strong growth,

adding more than 7,400 headcounts in the past year.

The unemployment rate fell 60 basis points in the past four quarters to 6.2 percent at midyear, one of the

lowest points since the recession. In the previous year, the unemployment rate tumbled 140 basis points.

Outlook: In 2016, local employers will add 28,500 jobs, expanding payrolls 3.1 percent year over year. A gain

of 2.4 percent was registered in 2015.

Developers delivered more than 660,000 square feet of retail space in the last 12 months, led by a substantial

influx in the second quarter this year. During the same span one year earlier, 680,000 square feet was

completed.

The Southwest Las Vegas area was the most targeted submarket in the metro, receiving more than 366,600

square feet of space in the past year. Meanwhile, the North Las Vegas submarket garnered the second-most

attention from builders, with nearly 115,000 square feet coming online.

Swedish furniture dealer Ikea opened a 351,000-square-foot location in the first half of 2016 at the corner of

Durango Drive and the 215 Beltway. The completion is far and away the largest development of the past year

and is bringing additional traffic to the Southwest Las Vegas area.

Outlook: Builders will finalize nearly 610,000 square feet of retail space in 2016, an acceleration from 2015.

MARKET OVERVIEW

Vacancy

Rents

* Forecast

Sources: Sources: Marcus & Millichap Research Services;

CoStar Group, Inc.

* Forecast

Sources: Marcus & Millichap Research Services; CoStar Group, Inc.

LAS VEGAS METRO AREA

32

The metrowide vacancy rate slid 100 basis points in the last four quarters, reaching 9.8 percent in June. In the

prior 12-month period, negative net absorption of 367,000 square feet in the first half of 2015 raised the

marketwide vacancy rate 30 basis points to 10.8 percent.

The Downtown Las Vegas submarket is the tightest area in the metro with the vacancy rate falling 70 basis

points in the past year to 3.7 percent. Meanwhile, the Central North Las Vegas submarket recorded the

greatest vacancy contraction, plummeting 210 basis points to 4.8 percent at midyear.

Multi-tenant vacancy improvements outpaced the single-tenant sector for the first time in several quarters.

The vacancy rate for multi-tenant properties fell 100 basis points in the last year on more than 296,000 square

feet of net absorption.

Outlook: Strong demand in the west and southwest will place downward pressure on the vacancy rate, which

is on track to fall 100 basis points to 9.5 percent in 2016, the lowest point since the recession.

The market is finally recording consecutive years of rent improvements after a prolonged recovery kept rent

growth in check. In the last four quarters ending at midyear, the average asking rent advanced 1.5 percent to

$16.38 per square foot. An increase of 2.5 percent was posted in the prior 12-month period.

The Southwest Las Vegas submarket is the most expensive area in the metro with retailers paying an average

of $18.72 per square foot for marketed space. Despite having rents surge 12.6 percent year over year, the

most affordable sites can be found in the Central North Las Vegas area, which has an average asking rate of

$12.16 per square foot.

Falling vacancy for multi-tenant space is spurring rent improvements for strip and shopping centers. In the

past 12 months, the average asking rate jumped 2.8 percent to $17.02 per square foot. The rise built on an 8.0

percent rent increase registered in the prior annual period.

Outlook: Tightening market conditions will support another rent hike in 2016. The average asking rent is on

track to reach $16.80 per square foot, an increase of 2.5 percent. Last year, Las Vegas also registered an

improvement of 2.5 percent.

DESERT OAKS PLAZA

MARKET OVERVIEW

Single-Tenant Sales Trends**

Multi-Tenant Sales Trends**

** Trailing 12-month period through 2Q

Sources: Marcus & Millichap Research Services; CoStar Group, Inc.;

Real Capital Analytics

** Trailing 12-month period through 2Q

Sources: Marcus & Millichap Research Services; CoStar Group, Inc.;

Real Capital Analytics

LAS VEGAS METRO AREA

33

Similar to the single-tenant sector, deal flow for multi-tenant assets surged 64 percent in the last 12 months

and trading occurred throughout the market. In the prior four-quarter period, transaction velocity was

virtually unchanged.

The average price climbed 13.4 percent in the past four quarters to nearly $255 per square foot, marking four

consecutive years of double-digit growth. In 2015, the average price rose 13 percent.

The average cap rate fell 25 basis points in the last four quarters as prices continue to rise. Well-located

grocery-anchored centers with favorable leases will command cap rates in the low- to mid-6 percent range.

Outlook: In the near term, investors looking to capitalize on outsize pricing will continue to bring assets

to market.

Intense demand for single-tenant offerings drove a 48 percent acceleration in deal flow during the last four

quarters. Trades involving fast-food properties were the main reason for the increase in transaction velocity.

Investors heavily targeted the Central East Las Vegas submarket, sparking a doubling in deal volume over the

last year. The Southwest Las Vegas area was also particularly sought after as multifamily development heated

up in the submarket.

The average price rose nominally in the past 12 months with investors paying more than $421 per square foot

at midyear. As a result, cap rates have continued to compress with the average first-year return falling to the

low-7 percent range. Yields remain among the highest in the nation, despite the contraction.

Outlook: The influence of California buyers is still a dominant force in the market. However, local players are

beginning to expand their presence as the Las Vegas economy builds steam.

DESERT OAKS PLAZA

MARKET OVERVIEW

Capital Markets

Local Highlights

DESERT OAKS PLAZA

34

LAS VEGAS METRO AREA

Global capital markets have remained stable over the past few weeks, even as Brexit and the continued devaluation of the Chinese yuan have induced bouts of volatility into

stock and bond markets. Meanwhile, U.S. economic data has proved resilient, with increases in retail sales and steady hiring supporting a measured pace of growth.

Additionally, higher bond prices have lowered prospective yields, boosting the appeal of commercial real estate.

As the current economic cycle has continued, retail vacancy descended to 5.8 percent by the end of the second quarter. A focus on net-leased construction for pre-leased

tenants and mixed-use developments has limited development activity in relation to prior cycles, supporting robust increases in average asking rents. Builders will deliver 46

million square feet of retail space this year, with more than two-thirds of new supply slated as single-tenant structures. This environment will sponsor a fourth straight year of

average asking rent growth, with advancement projected to exceed inflation over the same period.

Capital markets remain highly competitive, with a broad assortment of fixed-rate products available through commercial banks, life-insurance companies and CMBS lenders.

Loans are generally offered at terms up to 10 years at maximum leverage of 65 to 75 percent. For 10-year terms, rates will typically reside in the high-3 to mid-4 percent

range, depending on leverage and underwriting criteria. Floating bridge loans and financing for repositionings are typically underwritten with LTVs above 80 percent, while

pricing at 300 basis points above Libor for recourse deals and extending to 470 basis points above Libor for non-recourse transactions.

The NHL recently approved Las Vegas for an expansion team that will begin play in the 2017-2018 season. The franchise will take the recently opened T-Mobile Arena as its

home ice, bolstering retail and multifamily demand in the surrounding area. The franchise will be the first major sports team to operate in the metro.

Restoration Hardware has a 70,000-square-foot development under construction in the Northwest Las Vegas submarket. RH Gallery is the home-furnishing firm’s newest

design concept and offers customers a larger retail space in which to shop in an attempt to differentiate itself from other competitors like Pottery Barn. Traditional brick-and-

mortar stores are transitioning to focus on consumer experience and atmosphere as they look to compete with the ongoing emergence of e-commerce.

A new Asian-focused boutique resort and casino dubbed Lucky Dragon will open later this year, staking an area near the north end of the Strip. The Lucky Dragon

announced that it plans to hire 800 positions to staff the business, bringing more jobs to the Resort Corridor and bolstering retail offerings in the area.

PROPERTY NAME

MARKETING TEAM

DESERT OAKS PLAZA

DEMOGRAPHICS

Source: © 2016 Experian

Created on February 2017

POPULATION 1 Miles 3 Miles 5 Miles

2020 Projection

Total Population 16,972 178,050 456,842

2015 Estimate

Total Population 15,663 157,122 409,007

2010 Census

Total Population 14,686 145,625 382,533

2000 Census

Total Population 11,253 93,269 267,556

Current Daytime Population

2015 Estimate 10,821 95,618 323,211

HOUSEHOLDS 1 Miles 3 Miles 5 Miles

2020 Projection

Total Households 6,029 59,842 152,697

2015 Estimate

Total Households 5,457 52,444 135,966

Average (Mean) Household Size 2.89 2.95 2.94

2010 Census

Total Households 5,106 48,884 127,989

2000 Census

Total Households 3,869 31,746 91,952

Occupied Units

2020 Projection 6,029 59,842 152,697

2015 Estimate 5,774 57,063 149,577

HOUSEHOLDS BY INCOME 1 Miles 3 Miles 5 Miles

2015 Estimate

$150,000 or More 3.39% 5.21% 5.15%

$100,000 - $149,000 14.92% 13.94% 12.35%

$75,000 - $99,999 16.28% 16.08% 13.41%

$50,000 - $74,999 25.51% 23.92% 20.96%

$35,000 - $49,999 15.09% 14.70% 15.91%

Under $35,000 24.32% 25.31% 31.21%

Average Household Income $70,511 $71,235 $68,019

Median Household Income $61,005 $60,207 $53,153

Per Capita Income $24,591 $23,861 $22,837

HOUSEHOLDS BY EXPENDITURE 1 Miles 3 Miles 5 Miles

Total Average Household Retail Expenditure

$68,139 $68,359 $65,552

Consumer Expenditure Top 10 Categories

Housing $18,402 $18,385 $17,696

Transportation $12,625 $12,749 $12,157

Shelter $11,218 $11,322 $10,968

Food $7,264 $7,326 $7,050

Personal Insurance and Pensions $6,448 $6,439 $5,840

Health Care $4,302 $4,021 $3,818

Utilities $3,665 $3,612 $3,457

Entertainment $3,068 $3,014 $2,832

Cash Contributions $1,960 $1,859 $1,735

Apparel $1,632 $1,686 $1,635

POPULATION PROFILE 1 Miles 3 Miles 5 Miles

Population By Age

2015 Estimate Total Population 15,663 157,122 409,007

Under 20 26.90% 29.23% 29.79%

20 to 34 Years 17.69% 19.77% 20.94%

35 to 39 Years 6.31% 6.89% 6.91%

40 to 49 Years 15.67% 14.82% 14.31%

50 to 64 Years 20.21% 17.83% 17.16%

Age 65+ 13.22% 11.46% 10.87%

Median Age 39.34 35.74 34.47

Population 25+ by Education Level

2015 Estimate Population Age 25+ 10,524 100,667 258,822

Elementary (0-8) 4.99% 4.37% 6.40%

Some High School (9-11) 9.60% 9.01% 10.30%

High School Graduate (12) 30.92% 32.26% 31.64%

Some College (13-15) 31.66% 27.47% 25.11%

Associate Degree Only 8.09% 8.72% 8.03%

Bachelors Degree Only 9.83% 11.32% 11.36%

Graduate Degree 4.11% 5.41% 5.63%

35

Income

In 2016, the median household income for your selected geography is

$61,005, compare this to the US average which is currently $54,148.

The median household income for your area has changed by 0.96%

since 2000. It is estimated that the median household income in your

area will be $68,911 five years from now, which represents a change

of 12.96% from the current year.

The current year per capita income in your area is $24,591, compare

this to the US average, which is $29,638. The current year average

household income in your area is $70,511, compare this to the US

average which is $77,468.

Population

In 2016, the population in your selected geography is 15,663. The

population has changed by 39.19% since 2000. It is estimated that

the population in your area will be 16,972.00 five years from now,

which represents a change of 8.36% from the current year. The

current population is 49.75% male and 50.25% female. The median

age of the population in your area is 39.34, compare this to the US

average which is 37.55. The population density in your area is

4,982.42 people per square mile.

Households

There are currently 5,457 households in your selected geography. The

number of households has changed by 41.04% since 2000. It is

estimated that the number of households in your area will be 6,029

five years from now, which represents a change of 10.48% from the

current year. The average household size in your area is 2.89 persons.

Employment

In 2016, there are 1,894 employees in your selected area, this is also

known as the daytime population. The 2000 Census revealed that

55.12% of employees are employed in white-collar occupations in

this geography, and 44.75% are employed in blue-collar occupations.

In 2016, unemployment in this area is 4.19%. In 2000, the average

time traveled to work was 31.00 minutes.

Race and Ethnicity

The current year racial makeup of your selected area is as follows:

58.60% White, 14.81% Black, 0.78% Native American and 5.56%

Asian/Pacific Islander. Compare these to US averages which are:

70.98% White, 12.77% Black, 0.19% Native American and 5.25%

Asian/Pacific Islander. People of Hispanic origin are counted

independently of race.

People of Hispanic origin make up 30.69% of the current year

population in your selected area. Compare this to the US average of

17.53%.

PROPERTY NAME

MARKETING TEAM

DESERT OAKS PLAZA

Housing

The median housing value in your area was $161,908 in 2016,

compare this to the US average of $185,104. In 2000, there were

3,528 owner occupied housing units in your area and there were 341

renter occupied housing units in your area. The median rent at the

time was $960.

Source: © 2016 Experian

DEMOGRAPHICS

36