desired target return - · pdf filerecognized as ®post modern portfolio ... into the...

TRANSCRIPT

Desired Target Return®An Upside Potential/Downside Risk Framework

A Desired Target Return® Briefing

Optimal Blending of Active and Passive Investments

Table of Contents

DESIRED TARGET RETURN® OVERVIEW...................................................................................................3Modern Portfolio Theory (MPT) Meets Post Modern Portfolio Theory (PMPT)

Five Fundamental Investment Beliefs

DESIRED TARGET RETURN® PORTFOLIO CONSTRUCTION METHODOLOGY ....................9

THE DTR® CALCULATION ................................................................................................................................10Identifying the DTR® Calculation

Risk/Return Assessment and Measurements

Upside Potential

Downside Risk Deviation

DTR®-Alpha

SURZ STYLE PURE® INDICES.......................................................................................................................12Better Built Indices/Better Built Portfolios

Mutually Exclusive, Exhaustive, Investable and Macro Consistent

Significance of Centric— Segment Between Value and Growth— “Blend” Definition Difference

BOOTSTRAPPING TECHNIQUE ...................................................................................................................14Manager Statistical Data

Data Interpretation

DESIRED TARGET RETURN® SCREENING PROCEDURES ............................................................16

DESIRED TARGET RETURN® PORTFOLIO CONSTRUCTION INTEGRATION .......................18

SUMMARY ..............................................................................................................................................................21

GLOSSARY ...............................................................................................................................................................22

DISCLAIMER ..........................................................................................................................................................27

PAGE 2

• D

TR®

PAGE 3

• D

TR®

D E S I R E D T A R G E T R E T U R N ®

Overview

Desired Target Return® portfolio construction provides a revolutionary advancement in the evolution of portfolio

construction. This advanced Upside Potential/Downside Risk framework of portfolio construction methodology

is based on three Nobel Prize winning theories and other advancements in Post Modern Portfolio Theory

(PMPT) as briefly explained in this white paper.

The Desired Target Return® portfolio construction focus begins with identifying the DTR® calculation that links

the investor’s assets to their financial goals or liabilities. Sortino Investment Advisors (SIA) apply the Upside

Potential/Downside Risk framework as an overlay, which fortifies any Global Investment Committee’s strategic

asset allocation, tactical asset allocation, consultant’s active manager research and consulting services.

Desired Target Return® offers professionally managed portfolios tailored to an Institutional or Private Client’s

specific financial goals. The Upside Potential/Downside Risk (UP/DR) framework provides the “Missing Link”

to Modern Portfolio Theory (MPT). This is made possible by integrating multiple contributing advancements

recognized as Post Modern Portfolio Theory (PMPT) into the Desired Target Return® portfolio construction

methodology discussed in this paper.

Five Fundamental Investment Beliefs

Desired Target Return® has five basic beliefs that establish the foundation for how we approach and structure

client portfolios. These five beliefs are:

BELIEF #1: The Desired Target Return® goal is to meet or exceed the investor’sDTR® calculation. The goal is an absolute return objective and not to beat arbitrary market index(es).

BELIEF #2: The investor’s primary risk is not achieving the Desired Target Return®. Short term volatility is a secondary risk consideration.

BELIEF #3: Most active managers are not style pure. Style mix should be ac-

counted for in the portfolio construction process.

BELIEF #4: Many “Risk Tolerance” profiling techniques and questionnaires ignore the Desired Target Return®. This investor self-assessed risk profiling technique issubject to their emotional bias, which is influenced by varying perceptions of the capital

markets and economic environments.

BELIEF #5: The DTR® calculation is event driven by capital markets and/or investor circumstantial change(s). Event Driven Investing (EDI) is designed to help

avoid the emotional hazards of market timing and other potentially destructive investment

decision making temptations.

PAGE 4

• D

TR®

Ove

rview BELIEF #1: The Desired Target Return® goal is to meet or exceed the investor’s DTR® calculation.

The goal is an absolute return objective and not to beat arbitrary market index(es), as illustrated in Figure 1.

Figure 1: Meaningful Return Measurements

BELIEF #2: The investor’s primary risk is not achieving the Desired Target Return®. Short termvolatility is a secondary risk consideration.

Market volatility is secondary and more of an issue to the investor on the downside. The rationale of this

second belief is illustrated in Figure 2.

Figure 2: Meaningful Volatility(risk) Measurements

...But you miss your DTR® goal

Desired Target Return(DTR®)Actual ReturnRelative Blended Market Return (MR)

Ret

urn

Time

Outperform relative blended Market Return (MR)

Progress Is Measured to the DTR® Goal

Average Return Desired Target Return

Upside and downside risk are treated equally

Emphasis is on downside risk

Industry’s Common Risk Definition

P

Variability

Downside Risk Upside Potential

SIA Advanced Risk Definition

BELIEF #3: Most active managers are not style pure. Style mix should be accounted for in the portfolio

construction process.

Most active managers’ portfolios are an assortment of management styles. This is somewhat intuitive because

for active management to achieve excess return, commonly referenced as “alpha”, the active manager’s port-

folio must be structured differently than the style benchmark mandate.

For example, Figure 3 illustrates a sample of the impurity of active value equity managers. Notice the returns

based style analysis of all these large, mid and small cap value equity funds. The first three (1-3) are large

value funds, the next three (4-6) are mid value funds and the last three (7-9) are small value funds. Few

active managers are pure to their categorized manager style.

Figure 3: Active Managers Style Blends

As evidenced by William Sharpe’s Nobel Prize winning work illustrated in Figure 3, none of the portfolios are

style pure. This is common for all actively managed mutual funds and separately managed accounts.

This is further compounded by the fact that current asset allocation optimizers ignore active managers’ style

blend. Said another way, managers are assumed to be 100% pure in their respective style category. As a

result, most asset allocation strategies are immediately corrupted upon implementation. When Sortino’s Upside

Potential/Downside Risk framework methodology is overlaid in the portfolio construction process this deficiency

is better addressed. For example, the two charts illustrated in Figure 4 and Figure 5 (see next page) demon-

strate how an asset allocation recommendation becomes corrupted under commonly used optimization with

active manager implementation.

PAGE 5

• D

TR®

Ove

rview

Active Managers Are a Mix of Style Indexes

Manager U-P DTR® LrgVal LrgCen LrgGro MidVal MidCen MidGro MinVal MinCen MinGro

Ratio Apha

1 0.98 1.8% 30.00% 11.30% 1.40% 0.00% 0.00% 44.90% 9.10% 0.00% 3.30%

2 1.27 3.5% 23.00% 1.60% 0.00% 0.00% 29.70% 30.70% 9.90% 0.00% 5.10%

3 1.31 3.7% 21.70% 32.20% 0.00% 0.00% 0.00% 34.60% 11.50% 0.00% 0.00%

4 1.61 5.1% 19.60% 0.00% 0.00% 47.70% 4.30% 1.60% 26.80% 0.00% 0.00%

5 1.30 2.1% 0.00% 18.40% 0.00% 41.50% 26.60% 0.00% 0.00% 13.50% 0.00%

6 1.35 7.1% 0.00% 0.00% 0.00% 0.00% 9.10% 17.70% 59.00% 14.20% 0.00%

7 0.70 6.0% 0.00% 0.00% 52.10% 0.00% 0.00% 0.00% 8.30% 34.80% 4.80%

8 0.93 9.5% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 42.90% 39.00% 18.10%

9 0.90 4.8% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 41.40% 38.50% 20.10%

Source: Sortino Investment Advisors, 2006

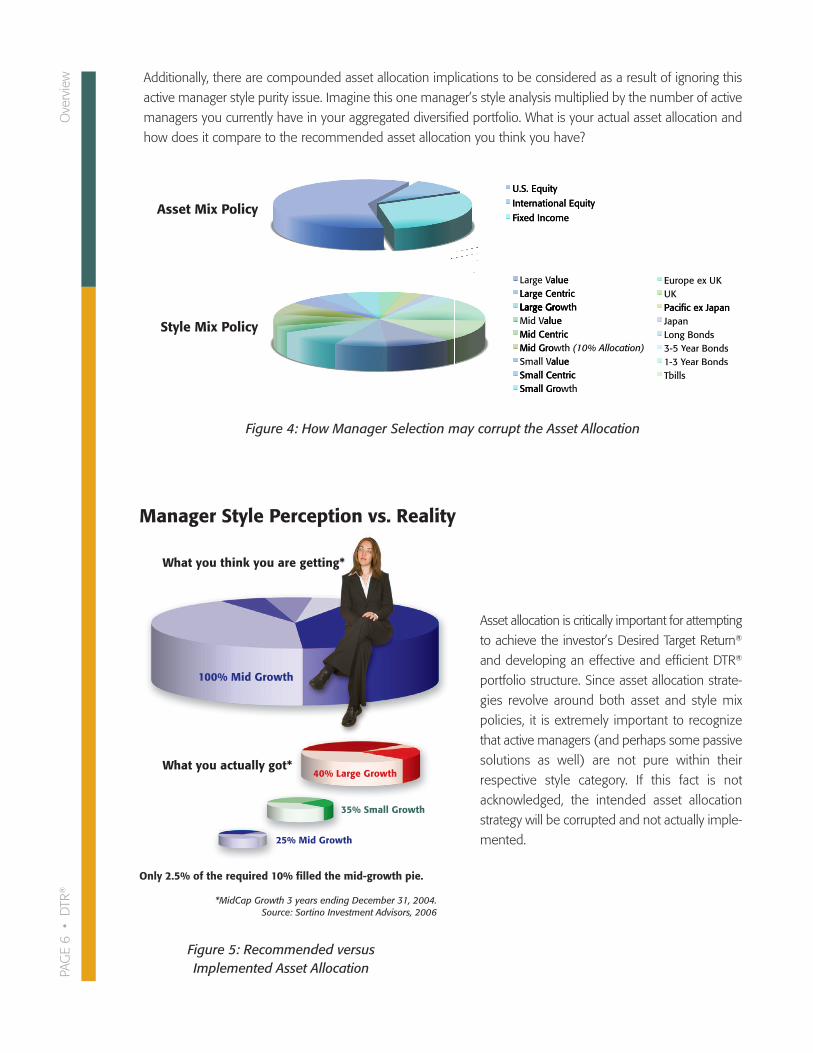

Additionally, there are compounded asset allocation implications to be considered as a result of ignoring this

active manager style purity issue. Imagine this one manager’s style analysis multiplied by the number of active

managers you currently have in your aggregated diversified portfolio. What is your actual asset allocation and

how does it compare to the recommended asset allocation you think you have?

Figure 4: How Manager Selection may corrupt the Asset Allocation

Asset allocation is critically important for attempting

to achieve the investor’s Desired Target Return®

and developing an effective and efficient DTR®

portfolio structure. Since asset allocation strate-

gies revolve around both asset and style mix

policies, it is extremely important to recognize

that active managers (and perhaps some passive

solutions as well) are not pure within their

respective style category. If this fact is not

acknowledged, the intended asset allocation

strategy will be corrupted and not actually imple-

mented.

PAGE 6

• D

TR®

Ove

rview

100% Mid Growth

What you think you are getting*

What you actually got*

25% Mid Growth

35% Small Growth

40% Large Growth

Only 2.5% of the required 10% filled the mid-growth pie.

*MidCap Growth 3 years ending December 31, 2004. Source: Sortino Investment Advisors, 2006

Figure 5: Recommended versus Implemented Asset Allocation

Manager Style Perception vs. Reality

alue VLarge Large CentricLarge Gro

alue Large Centric

th wLarge Gro

K UEurope ex K Uacific ex Japan PLarge Gro

alue VMid Mid CentricMid Gro

alue VSmall Small CentricSmall Gro

th wLarge Groalue

Mid Centric(10% Allocation)th wMid Gro

alue Small Centric

th wSmall Gro

acific ex Japan PJapan Long Bonds

ear Bonds Ye 3-5 ear Bonds YYear Bonds -3 1

bills T

U.S. Equity

International Equity

Fixed Income

U.S. Equity

International Equity

Fixed Income

Asset Mix Policy

Style Mix Policy

BELIEF #4: Many “Risk Tolerance” profiling techniques and questionnaires ignore the DesiredTarget Return®. This investor self-assessed risk profiling technique is subject to their emotional bias, which

is influenced by varying perceptions of the capital markets and economic environments.

The investor’s Desired Target Return® is more essential and uniquely different than some market benchmark’s

volatility, target dated or “age-based” life cycle fund solutions. Falling below the Desired Target Return® is the

primary investor’s risk, market volatility is a secondary risk considered more for investor behavioral and

emotional factors. Yet asset allocation recommendations are frequently based primarily on market volatility

(risk) tolerance to determine an investor’s portfolio structure. It should be apparent that differing Desired Target

Returns® would logically dictate different portfolio constructs as illustrated in Figure 6.

BELIEF #5: The DTR® calculation is event driven by capital markets and/or investor circumstantialchange(s). Event Driven Investing (EDI) is designed to help avoid the emotional hazards of market timing

and other potentially destructive investment decision making temptations.

• Primary risk is not achieving the investor’s DTR® to accomplish their financial goals.

• Contingency risk is market volatility.

• There is an inverse relationship between substantial market events or investor circumstantial changes andtheir DTR® calculation as illustrated in Figure 7 below.

PAGE 7

• D

TR®

Ove

rview

Goal: Fund researchAnnual Need: $500,000CPI: 2.5%Expenses: 1.0%Fund Assets: $6,000,000

Investment Fund B

DTR® = 12%

Goal: Fund researchAnnual Need: $500,000CPI: 2.5%Expenses: 0.5%Fund Assets: $10,000,000

4% Req. ReturnPortfolio

6% Req. ReturnPortfolio

8% Req. ReturnPortfolio

10% Req. ReturnPortfolio

12% Req. ReturnPortfolio

Investment Fund A

DTR® = 8%

These charts are for illustrative purposes only and do not reflect any actual investment product.

Figure 6: Different Desired Target Return® determines portfolio constructs

Decreased DTR®

Month

S&P

500

Mar

ket

Valu

e

Increased DTR®

Sep 990

200400600800

10001200140016001800

Sep 00 Sep 01 Sep 02 Sep 03 Sep 04 Sep 05 Sep 06 Sep 07 Sep 08

Closing Value

Figure 7: DTR® Event Driven Investing

Different Needs, Different Portfolios

Typical Investment Committee’s Portfolio Construction Process

Desired Target Return® integrates the typical investment consulting firm’s portfolio construction process with the

Sortino Upside Potential/Downside Risk (UP/DR) framework as an overlay. The UP/DR framework is designed

to select the best mix of active managers while optimally blending both active and passive management strategies.

The unique Upside Potential/Downside Risk (UP/DR) overlay is integrated with a leading Global Investment

Committee’s portfolio construction process that is time-tested since 1973 and illustrated in Figure 8.

PAGE 8

• D

TR®

Ove

rview

Figure 8: A leading consulting firm’s portfolio construction process

D E S I R E D T A R G E T R E T U R N ®

Portfolio Construction Methodology

Desired Target Return® approaches portfolio construction based on what we define as the investor’s DTR®

calculation for achieving a stated financial goal. The investor’s DTR® calculation is liability driven and considerate

of dynamic market events. The Upside Potential/Downside Risk framework used for DTR® combines the

innovative ideas of leading financial research and academics that include Nobel Prize winners Harry Markowitz,

William F. Sharpe, Daniel Kahneman, and multiple other academics. This Post Modern Portfolio Theory (PMPT),

combined with today’s most advanced statistical models and computer technology, is the keystone for Desired

Target Return's® revolutionary active manager mix selection and active/passive blending methodology.

Dr. Frank Sortino tested and refined the Upside Potential/Downside Risk framework over two decades at the

Pension Research Institute. It has been applied at major institutions globally.

Furthermore, the quantitative methods employed in Desired Target Return® portfolio construction are based

on advanced financial theory developed by some of the leading experts in Investment Theory identified in

Figure 9.

PAGE 9

• D

TR®

GREAT IDEA GREAT THINKERReturns-Based Style Analysis William F. Sharpe* (Stanford University)

Bootstrap Method Bradley Efron (Stanford University)

3-Parameter Lognormal Distribution Aitchison/Brown (Cambridge University)

Downside Risk Peter Fishburn (University of Pennsylvania)

Upside Potential Daniel Kahneman* (Princeton University)

Source: Sortino Investment Advisors, 2007 *Nobel Prize winners

Figure 9: Advancements in Financial Theory

D E S I R E D T A R G E T R E T U R N ®

The DTR® Calculation

Identifying the DTR® Calculation

The foundation to Desired Target Return® portfolio construction is the DTR®. Investors have a rate of return that

will achieve their cash flow withdrawals (liability schedule) relative to their asset inventory and cash contribution

(funding schedule) as illustrated in Figure 8. The DTR® is the return necessary to achieve the investor’s goal.

DTR® identifies the investor’s risk/return profile allowing us to link investment goals to portfolio solutions.

DTR® is the primary benchmark we use to measure performance, to analyze managers’ characteristics and

dynamically monitor and evaluate the portfolio’s risk/return attributes. Each portfolio is customized to each

investor’s unique DTR® profile.

SIA Risk/Return Assessment and Measurements

The DTR® risk assessment methodology

uses uniquely different risk measurement

statistics that are more informative and strin-

gent. The risk measurement statistics are re-

ferred to as Upside Potential/Downside Risk

and DTR®-Alpha. They are more informative

than standard deviation and risk adjusted re-

turn ratios because they provide magnitude,

frequency and whether past returns met or

exceeded the Desired Target Return®. These

important Post Modern Portfolio Theory

(PMPT) advancements are summarized in

Figure 10. They are more stringent because

they rely on monthly data and managers are

penalized more severely for their downside performance than they are given credit for exceeding the Desired

Target Return®. These risk and reward measurements are defined as:

Upside Potential Ratio The average return above the DTR® measures how often and howfar above the Desired Target Return® a portfolio’s returns are likely to occur. Upside Potential,a term coined by Nobel Prize winner Daniel Kahneman, captures investors’ perception ofrisks concerning gains as opposed to risk concerning losses.

Downside Risk Deviation A measure of portfolio risk developed by Peter Fishburn at theUniversity of Pennsylvania, Downside Deviation defines risk as not achieving an investor’sdesired target return. By measuring only deviations below the investor’s target return, Down-side Deviation distinguishes between “good” and “bad” returns—good returns are greater

PAGE 10

• D

TR®

Time

Results

Figure 10: Liability Driven Investing (LDI) approach to determine and monitor

than the target return, and bad returns are below the target return. Only the latter representsrisk. In addition, the more returns fall below the target return, the greater the risk.

DTR®-Alpha A risk-adjusted return measuring the value added by a manager over andabove performance that could have been achieved with its “style benchmark”. A stylebenchmark, versus market index, is a blended benchmark that is representative of the actualstyle assortments in the active managers’ portfolio(s). This is accomplished using Sharpe’sstyle based analysis. The style-blended benchmarks serve as a more precise measurementfor identifying manager skill versus random luck. Sortino’s DTR®-Alpha is the differencebetween the manager’s style blended return and the manager’s customized style blendedbenchmarks return.

Figure 11 below compares Post Modern Portfolio Theory (PMPT) to Modern Portfolio Theory(MPT), which has been the industry standard since 1952. One suspected reason that NobelPrize winner Harry Markowitz selected a mean variance framework for his Modern PortfolioTheory (MPT) work was due to the practicality at the time of processing any more complexcalculations (i.e. semi-variance) on computers with much more limited capacity than today’scomputers. Obviously Post Modern Portfolio Theory (PMPT) and the Upside Potential/Down-side Risk framework benefit from more efficient computer power and portfolio theory advancements since 1952.

PAGE 11

• D

TR®

The DTR

®Calcu

latio

n

Modern Portfolio Theory Post-Modern Portfolio Theory(Industry Standard) (Upside Potential/Downside Risk Standard)

Reward Mean or Expected Return Upside Potential (exceeding DTR®)

Risk Standard Deviation, Beta Downside Risk (falling below DTR®)

Excess Alpha (Excess over Market) DTR®-Alpha (Excess over Style Blend)

Forecast Historical (What did happen) Bootstrap (What could have happened)

Profiles Expected Utility Theory Behavioral Finance

NOTE: DTR® = Desired Target Return

Figure 11: Post Modern Portfolio Theory (PMPT) Advancements

D E S I R E D T A R G E T R E T U R N ®

Surz Style Pure® Indices

As mentioned above, the UP/DR framework

concludes through Sharpe’s style based analysis

that few active managers’ portfolios are 100%

pure to their manager style categories. This is

further flawed if using market indices versus a

style blended benchmark comparisons for iden-

tifying manager skill. Consequently, in order to

determine if the manager adds value (DTR®-

Alpha return) to a diversified portfolio, a man-

ager’s style-blended return needs to be

determined and then measured against a similar

style blended benchmark. However, this analysis

requires the benchmarks used in the analysis to

be style pure. If the benchmarks are not style

pure then all the analytics based on those

benchmarks are misleading.

The popular brand indexes use Price/Book (P/B) to make the determination between value and growth. Low P/B

is value and high P/B is growth. Furthermore, not all indexes are constructed using Price/Book. Some use Price

Earnings (P/E) combined with other factors such as dividend yield. Here dividend yield is a value measure and P/E

is a growth measure. The idea of using both a value and a growth measure is that one confirms the other. A low

P/E and high yield indicates value, just as a high P/E and low yield signifies growth. Stocks with off-setting

characteristics fall in the middle which Surz Style Pure® (SSP®) indices call “Centric.” The SSP® indices use three

factors – Price/Earnings, Dividend Yield and normalized (by sector) Price/Book to create the nine indices matrix

illustrated in Figure 12. Centric is defined as the equities in between value and growth. The other major brand

indices either assign these Centric stocks proportionately divided between value and growth or eliminate them all

together! It matters a lot which factors are used to define equity style classifications.

For these reasons UP/DR uses the Surz’s Style Pure© indices, as illustrated in Figure 12. Currently this matrix

of nine SSP® indices is the purest style benchmarks available today for measuring the style-blended returns

of money managers.

PAGE 12

• D

TR®

Value

Large Middle Small

Centric

Growth Mutually Exclusive & Exhaustive

Source: PPCA Inc., 2005

Figure 12: Matrix of Surz Style Pure®

(SSP®) Indexes

Surz-Style Indexes

UP/DR Risk/Return Assessment and Measurements

The strengths of the Surz Style Pure® indices (SSP®) for portfolio construction purposes are as follows:

1. The SSP® indices used as manager skill benchmarks offer enhanced manager attribution evaluation versus

market indexes.

2. SSP® indices utilization ensures better built portfolios under basic tenets of Modern Portfolio Theory (MPT).

SSP® indices have greater adherence, than other industry popular indices, to MPT’s important fundamental

tenets* of:

a.Mutually exclusive—no asset class should overlap with another

b.Exhaustive—all securities should fit in the set of asset classes

c. Investable—it should be possible to replicate the return of each asset class at relatively

low cost

d.Macro-consistent—the performance of the entire set should be replicable with some

combination of asset classes

*Dr. William F. Sharpe, “Determining a Fund’s Effective Asset Mix,“ Investment Management Review, December, 1988, pages 59-69.

Using the combination of all the above noted academics, Sortino’s Upside Potential/Downside Risk (UP/DR)

framework is a more thorough approach to analyzing a manager’s past performance and determining whether

a manager is skillful based not on an ill-defined market benchmark but on pure style-blended benchmarks

and considering the investor’s Desired Target Return®.

PAGE 13

• D

TR®

Surz Style Pure©

Indice

s

D E S I R E D T A R G E T R E T U R N ®

Bootstrapping Technique

Bootstrapping Manager Statistical Data and Interpretation

Attempting to forecast money managers’ future returns entails a high degree of uncertainty. Therefore, more

data is better than less when seeking the potential for more reliability and meaningful interpretation. Unfortu-

nately managers’ performances are typically categorized into regimented time periods such as 3, 5 and 10-

year quarterly results. This leaves investment advisors/consultants and investors with a limited number of data

points to examine. In addition, the returns are linear so that both good and poor performances fall off (end

point bias) after a period of time. This approach increases the risk of not capturing poor or good performance

data and could potentially lead to inferior active manager selection.

Consequently, Sortino’s UP/DR framework has incorporated a more detailed and informative way to look at

past performance. A technique referred to as “bootstrapping” proposed by Effron and Tibshirani (Stanford

1993) allows an analyst to look at what happened but also what best and worse cases could have happened.

For example, Figure 13 demonstrates the effectiveness of bootstrapping.

In Figure 13 the graphic shows 4 years of monthly returns for a money manager. Typically a consultant will only

have 5 years of quarterly returns, possibly more if rolling periods are used and they will be linear. The worst per-

forming year in our example for this manager was a positive + 30%. However, what if we assumed that next

year’s return is made by compounding a random sample of 12 of the monthly returns, as shown on Figure 13.

PAGE 14

• D

TR®

2 -13 6 11 -5 12 4 7 -6 8 3 1YEAR 1:

YEAR 2:

YEAR 3:

YEAR 4:

4 7 -6 22 -1 13 0 2 -7 9 4 5

5 15 0 2 7 14 5 18 6 9 17 -4

8 1 6 9 7 4 11 21 3 1 13 -12

4 -6 -13 -4 0 -1 -12 1 1 2 -7 -6

what did happen what could have happened

Historical Worst Year = +30%Bootstrap Worst Year = -35%

Four Years of Fictional Monthly Returns

Repeat process 2,000 times

This chart is for illustrative purposes only and does not reflect any actual investment product.

Figure 13: Bootstrapping Trials to Simulate Performance

Our first random draw might be 4% selected from the sixth month of the fourth year. The first draw is replaced

and a second return is randomly selected, in this case negative 6%. Notice this same return is again selected

for the last month of one year that could have happened. We repeat this process with 2000 random trials and

we now have more data points than using the standard approach.

As the graph demonstrated, a negative 35% year is possible. This results in having more downside deviations

and upside potential data, and a measurement of the magnitude of such data as well, for attempting to

determine the Upside Potential Ratio and DTR®-Alpha Return of the money managers.

PAGE 15

• D

TR®

Bootstrapp

ing Te

chniqu

e

D E S I R E D T A R G E T R E T U R N ®

Desired Target Return® Screening Procedures

Desired Target Return® portfolio construction begins with the following screening procedures addressing the

following requirements for more effective portfolio construction:

1. Identify the DTR®. It is the return that links the client’s assets to their liabilities and financial goals. This is anongoing review process as these dynamic liabilities, goals and market conditions change.

2. Determine the Desired Target Return® asset and style mix strategy needed to achieve the DTR®.

3. Desired Target Return® optimizes the combination of both active and passive managers to meet or exceedthe investors’ DTR®.

4. Desired Target Return® monitors and re-balances the portfolio for dynamic market shifts or changes to theclient’s DTR® or financial situation.

5. This Desired Target Return® overlay serves as the mortar to fortify the Global Investment Committee’s strategicand tactical asset allocation, active manager research and portfolio construction process.

PAGE 16

• D

TR®

Top Half of Universe Ranked by U-P Ratio?

Non-Proprietary Manager Universes

Manager vs. Style Benchmark R2 > .70?

Funds Drop Out

Funds are Candidates for Optimizer

Funds Drop Out

Funds Drop Out

Funds Stay In

Fund’s DTR®-Alpha> 0%?

Funds Stay In

Asset and Style Mix Policy

Client’s DTR® solution set

Figure 14: SIA screening process to best meet investor’s Desired Target Return®

SIA Screening Process

STEP 1. SIA Screening ProcessQuantitatively analyze over 30,000 plusseparately managed accounts, mutualfunds and ETFs for their style purity. AnR squared value of .70 or higher quali-fies for the first screen as illustrated inthe top box of Figure 14.

STEP 2. Universe Ranking by U-PRatio Determine the Upside PotentialRatio of the manager with the bottom50% being eliminated for consideration asillustrated in the second box of Figure 14the U-P Ratio has historically demon-strated a difference and probably maymake a difference in future analysis.

STEP 3. DTR®-Alpha Determinewhether or not the style blended return of the manager exceeds a similar passive style blended benchmark.If the manager adds value, DTR®-Alpha, they are considered for the portfolio. If not the passive investment op-tion is employed. This step is represented in the third box of Figure 14 and further illustrated in Figure 15.

STEP 4. Asset & Style Mix Policy The DTR® links the investor’s profile to the best portfolio combination ofactive and passive managers. The portfolio is designed to identify the DTR® asset allocation recommendationin adherence to the client’s investment policy guidelines, as illustrated in the fourth box of Figure 14 and inmore detail in Figure 16.

These advanced Upside Potential/Downside Risk framework components are necessary in order to create bet-

ter portfolio performance results.

PAGE 17

• D

TR®

Des

ired Target Return Sc

reen

ing Proc

edures

Period 1 Rank

Funds Ranked by Omega Excess Return 1981-1996

Period 2 Rank

1 2

3 4

1

2

3

4

0%

10%

20%

30%

40%

50%

60%

70%

3

1. Almost 70% of funds in the top quartile in Period 1 stayed in the top quartile in Period 2

2. Almost 70% of funds in the bottom quartile stayed in the bottom quartile

3. Few top-ranked funds fell to the bottom quartile

2 1

Figure 15: DTR®-Alpha historical reliability

The Predictive Power of DTR®-Alpha

Linking it all together

Goal: Fund liabilitiesAnnual Contribution: $500,000Annual Distribution: $800,000Assets: $35,000,000

DTR® = 8%The Investor

Active Fund A $8,575,000Passive A 2,940,000Active Fund B 7,105,000Passive B 6,825,000Fund C 3,255,0001-3 Year Bonds 6,300,000

The Portfolio

Figure 16: Linking the investor’s DTR® Desired Target Return® to a Portfolio Construct

D E S I R E D T A R G E T R E T U R N ®

Portfolio Construction Integration

The Upside Potential/Downside Risk framework is overlaid in a utilitarian application across non-proprietary

manager universes. There are three basic integrating steps to Desired Target Return® portfolio construction,

which are as follows:

STEP 1: Global Investment Committee Asset Allocation

Global Investment Committee’s Strategic and Tactical Asset Allocation recommendation is the first step of the

portfolio construction procedure as illustrated in Figure 17.

PAGE 18

• D

TR®

Larg

e Va

lue

Larg

e C

ore

Larg

e G

row

th

Mid

Val

ue

Mid

Cor

e

Mid

Gro

wth

Smal

l Val

ue

Smal

l Cor

e

Smal

l Gro

wth

Tbill

s

1-3

Year

Bon

ds

3-5

Year

Bon

ds

Long

Bon

ds

Euro

pe

U.K

.

Paci

fic

Japa

n

U.S. Equity U.S. Fixed Income International Equity

Figure 17: Step 1—Strategic and Tactical Allocation

Global Investment Committee’s Asset Allocation Recommendation

STEP 2: Consultant’s Manager Research

Manager research and due diligence of traditional Separately Managed Account (SMAs), Exchange Traded

Funds (ETFs) or other investment alternatives represents the next step of the portfolio construction procedure,

as illustrated in Figure 18. All fund managers in this open architecture consist of non-proprietary Separately

Managed Accounts (SMAs) or other investment vehicles.

STEP 3: Sortino Upside Potential/DownsideRisk Framework Overlay

Upside Potential/Downside Risk framework

serves as an overlay and finishing step for the

portfolio construction integration procedure.

It serves as the “mortar” for securing the integrity

of the Global Investment Committee’s asset

allocation and consultant’s manager research/

due diligence “building blocks,” as illustrated in

Figure 19 and Figure 20.

PAGE 19

• D

TR®

Portfolio Con

struction Integration

Investment Advisorsover 24,000

Consulting Group Manager Databasesrepresenting over 4,700 products

1,430

Search Process

Step 1: Initial Qualificationsapprox.100

Step 2: Quantitative Screensapprox.25

Step 3: QualitativeScreensapprox.12

CandidateList

approx.3-6

Selected Investment Manager(s)

Figure 18: Step 2—Manager Research and Due Diligence

Top half of style stay in

Manager Universe

Filter for UP Ratio

Manager Universe

Source: Sortino Investment Advisors, 2005

Figure 19: Step 3—SIA Overlay

SIA Screens Manager Universe

STEP 4: Identifying Manager Skill

The Upside Potential/Downside Risk frame-

work overlay first identifies active managers

who consistently demonstrate an ability to

outperform their style benchmarks on a risk-

adjusted basis.

Next, the active managers are optimally

mixed to obtain the best combination of ac-

tive managers for a portfolio.

Finally, the overlay seeks to ensure the rec-

ommended asset allocation is preserved

when these active managers are imple-

mented in a portfolio. This is accomplished

by identifying the actual style blends using

Surz Style Pure© (SSP®) indices from each

active manager’s portfolio. Passive manage-

ment is then blended where suitable to best

align the portfolio to its intended asset allo-

cation recommendation.

This overlay enhances the probability of

meeting or exceeding the investor’s DTR®.

Each Desired Target Return® custom con-

structed portfolio seeks to achieve a distinctive

DTR® and utilizes a wide diversification of

fixed income investments, money market

vehicles, indices exchange traded funds, active

mutual funds and separately managed accounts. This approach allows us to focus on the individual or

institution’s DTR®, and to take a liability driven investment approach to providing investment portfolio strategies.

Desired Target Return® seeks to measure success by achieving each client’s DTR®, as opposed to unrelated

past performance of market returns, as illustrated in Figure 21.

PAGE 20

• D

TR®

Portfolio Con

struction Integration

Style Bucket Small Cap Value Large Cap Value

Large Value 0.0% 36.4%

Large Centric 0.0% 23.0%

Large Growth 0.0% 26.1%

Mid Value 33.3% 7.8%

Mid Centric 0.0% 2.8%

Mid Growth 0.0% 0.0%

Small Value 61.5% 0.0%

Small Centric 0.0% 0.6%

Small Growth 0.0% 3.3%

Europe 0.0% 0.0%

U.K. 0.0% 0.0%

Pacific 0.0% 0.0%

Japan 0.0% 0.0%

Long Bonds 0.0% 0.0%

3-5 Year Bonds 0.0% 0.0%

1-3 Year Bonds 0.0% 0.0%

T-bills 5.2% 0.0%

100.0% 100.0%

R-Squared 90% 90%

Style Analysis William F. SharpeSource: Sortino Investment Advisors, 2005

Figure 20: Step 3—Active Manager Style Determination

4% Req. Return 6% Req. Return 8% Req. Return 9% Req. Return 10% Req. Return 11% Req. Return 12% Req. Return

Defensive High Growth

SIA solves for each desired target return’s optimal combination of: 1. Active Manager mix; 2. Passive blend

Source: Sortino Investment Advisors, 2006

Figure 21: DTR® Active Manager Mixing and Passive Blending Process

Active Mix and Passive Blend Process

D E S I R E D T A R G E T R E T U R N ®

SummaryThe Desired Target Return® portfolio construction process results in an optimal mix of managers and an optimal

blend of active and passive investment strategies. The optimal active manager mix and passive blend strategies

are designed to ensure that the recommended asset allocation results in the actual implemented asset

allocation strategy.

The integration of Modern Portfolio Theory (MPT) with Post Modern Portfolio Theory (PMPT) and today’s tech-

nology results in a revolutionary advancement in the evolution of portfolio construction. Desired Target Return®

portfolio construction is designed to build more effective custom portfolios for better portfolio performance

with less portfolio risk for investors.

PAGE 21

• D

TR®

D E S I R E D T A R G E T R E T U R N ®

Glossary

Bootstrap Method

A statistical method developed by Bradley Effron of Stanford University that is used by Sortino Investment Ad-

visors (SIA) to develop better estimates of risk and return. With the Bootstrap Method, a manager’s performance

is simulated by developing a distribution of possible returns through random sampling with replacement.

The process is as follows: Twelve returns are selected at random from historical monthly returns of a manager’s

style benchmark and combined to make a single annual return. Each monthly return can be drawn more than

once. This is repeated many times to construct a full distribution of possible annual returns.

Bootstrapping avoids the dual problems of time sensitivity (beginning/ending date) and limited data because

it is not dependent on an arbitrarily selected single period of history. By randomly sampling from a manager’s

actual historical monthly returns to simulate future performance, this method measures what could have hap-

pened rather than what did happen.

Desired Target Return® (DTR®)

The Desired Target Return® an investor must earn in order to accomplish his/her financial goal. While returns

above the Desired Target Return® are welcome, returns below this level represent risk to the investor. For

example, a 50-year-old investor with $100,000 in retirement assets who is looking to retire at age 65 with

$600,000 in assets and is willing to contribute $10,000 a year will need to earn at least an 8% annual return.

Thus the Desired Target Return® is 8%; if the actual return falls below 8%, the investor will have to contribute

more and/or retire with fewer assets.

The following performance measures are calculated based on the DTR®: Downside Deviation, DTR®-Alpha

Return, Omega Return, Sortino Ratio, Upside Potential, and U-P Ratio.

Downside Deviation

A measure of portfolio risk developed by Peter Fishburn at the

University of Pennsylvania, Downside Deviation defines risk as

not achieving an investor’s target return (“TR”). By measuring

only deviations below the investor’s TR, Downside Deviation

distinguishes between “good” and “bad” returns—good returns

are greater than the TR, and bad returns are below the TR.

Only the latter represents risk. In addition, the farther returns

fall below the TR, the greater the risk.

Because it is stated in relation to a TR, a portfolio’s risk, as

measured by Downside Deviation, may be perceived differ-

ently by investors with a different Desired Target Return®.

PAGE 22

• D

TR®

Risk Reward

Target Return (TR)

Mean

Lower Returns Higher Returns

Source: Sortino Investment Advisors

Figure 22

Downside Probability

The probability, or likelihood, that a portfolio’s return will fall below the DTR®.

Downside Risk

See Downside Deviation.

Holdings-Based Style Analysis

See Style Analysis.

DTR®-Alpha Return

A risk-adjusted return measuring the value added by a manager over and above performance that could have

been achieved with its style benchmark. DTR®-Alpha Return is the difference between the manager’s Omega

Return and the style benchmark’s Omega Return.

Mathematically,DTR Alpha® Return = OmegaMgr – OmegaBenchmark

Where,OmegaMgr = Manager’s Omega ReturnOmegaBenchmark= Style Benchmark’s Omega Return

Omega Return

A measure of risk-adjusted performance that indicates whether a manager was compensated for the level of

risk taken.

Mathematically,Omega Return = RMgr – 3 (Style Beta * DVarBenchmark)

Where,RMgr = Manager’s ReturnDVarBenchmark = Downside Variance of Style Benchmark

R-Squared

A statistical measure that represents the percentage of a manager’s returns that are explained by returns in

the manager’s style benchmark. R-Squared ranges from 0 to 100 where 100 means that all movements of a

portfolio are completely explained by movements in the style benchmark.

PAGE 23

• D

TR®

Glossary

Return Distribution

Because a portfolio’s return cannot be predicted

with certainty, a probability distribution is used to

represent many possible outcomes. It incorporates

the range of possible returns and the probability of

each return occurring.

A discrete return distribution has a discrete number

of values, each of the discrete values has a certain

probability of occurrence that is between zero and

one, and the sum of these probabilities must be

one (i.e., at least one of the values has to occur).

A continuous return distribution has theoretically an infinite number of points over a continuous interval. Prob-

abilities are measured over intervals, not single points as is done for a discrete distribution. That is, the area

under the curve between two distinct points (e.g., between two returns) defines the probability for that interval.

Sortino Investment Advisors uses the Three-Parameter Lognormal Distribution developed by Aitchison and

Brown to fit a continuous curve over a discrete return distribution to improve the accuracy of risk and return

estimates. See Three-Parameter Lognormal Distribution.

Returns-Based Style Analysis

See Style Analysis.

Sortino Ratio

A measure of risk-adjusted performance, indicating how many units of return in excess of the investor’s Target

Return are provided per unit of Downside Risk (where Downside Risk is Downside Deviation).

Mathematically,Sortino Ratio = (R - TR)/DD

Where,R = Expected ReturnTR = Target ReturnDD = Downside Deviation

Standard Deviation

A statistical measure of risk reflecting the extent to which rates of return for a portfolio may vary from period

to period and gauges the dispersion of monthly returns around the average return. The larger the standard

deviation, the greater the range of possible returns and, therefore, the more risky the portfolio.

If the distribution is normal, the Standard Deviation gives a good estimate of its dispersion around the average.

If the distribution is non-symmetric, the standard deviation measure can give misleading information.

PAGE 24

• D

TR®

Glossary Risk Reward

Required Return

Upside PotentialAverage DownsidePotential

Great Thinkers: Sharpe, Efron, Aitchison, Fishburn, Kahneman

Figure 23

Style Analysis

Style Analysis is used to determine the investment style (e.g., growth versus value, large cap versus small cap)

of a portfolio. Returns-Based Style Analysis (RBSA), developed by Nobel Prize winner William Sharpe, uses

the manager’s historical monthly returns to find a blend of passive indices that replicates the manager’s per-

formance. Holdings-Based Style Analysis (HBSA) classifies a manager’s style orientation based on the charac-

teristics of the portfolio’s underlying securities.

Sortino Investment Advisors (SIA) uses RBSA to determine a manager’s style benchmark and to measure risk-

adjusted performance and value added. HBSA is used to validate this assessment, and where the two

approaches differ considerably, provides the basis for further investigation.

Style Benchmark

A set of passive indices developed with Returns-Based Style Analysis (RBSA) that replicates the style and

performance of an active manager. SIA uses the following style indices:

U.S. Equities: Large Value, Large Centric, Large Growth, Mid Value, Mid Centric, Mid Growth,Small Value, Small Centric, Small Growth

International Equities: Europe ex U.K., Pacific ex Japan, Japan

Fixed Income: 7-10 Year Bonds, 3-5 Year Bonds, 1-3 Year Bonds, and Treasury Bills

Style Beta

The ratio of the manager’s Downside Risk to the Style-Blended Benchmark’s Downside Risk for a given TR.

Style Beta indicates whether the manager takes more or less risk than is inherent in their style where risk is

measured by Downside Deviation. The higher the ratio, the greater the manager’s risk per unit of style risk.

Values greater than 1.0 indicate proportionately more risk than the Style Benchmark, and values less than 1.0

indicate proportionately less risk.

Mathematically,Style Beta = DDMgr/DDBenchmark

Where,DD = Downside DeviationMgr = ManagerBenchmark = Style Benchmark

Three-Parameter Lognormal Distribution

A method, developed by Aitchison and Brown of Cambridge University, for fitting a continuous curve over a

discrete return distribution. The three parameters are the mean, the standard deviation, and the extreme value

of the annual returns. It allows for both normal and skewed return distributions.

Sortino Investment Advisors (SIA) uses the Three-Parameter Lognormal Distribution to fit a curve to the boot-

strapped distribution of possible annual returns so that a variety of statistical characteristics — including average,

standard deviation, downside risk, upside potential, etc. — can be estimated. PAGE 25

• D

TR®

Glossary

Surz Style Pure® (SSP®) Indices

Style groupings are based on data provided by Compustat. Two security databases are used. The U.S. database

covers more than 6000 firms, with total capitalization exceeding $18 trillion. The non-U.S. database coverage

exceeds 15,000 firms, 20 countries, and $31 trillion – substantially broader than EAFE.

To construct style groupings, Surz first break the Compustat database for the region into size groups based on

market capitalization, calculated by multiplying shares outstanding by price per share. There are 3 regions

maintained in our system: U.S., Foreign and Global. Beginning with the largest capitalization company, Surz

adds companies until 65% of the entire capitalization of the region is covered. This group of stocks is then

categorized as “large cap” (capitalization). There are generally about 200 companies in this group for the U.S.,

800 for Foreign, and 1000 for Global. The second size group represents the next 25% of market capitalization

and is called “mid cap”. There are generally about 1000 companies in this group for U.S., 2700 for Foreign,

and 3500 for Global. Finally, the bottom 10% is called “small cap”. There are generally 5000 U.S. securities

in this group, 10,000 Foreign, and 15,000 Global.

Then within each size group, a further breakout is made on the basis of orientation. Value, centric, and growth

stock groupings within each size category are defined by establishing an aggressive measure. Aggressiveness

is a proprietary measure that combines dividend yield and price/earnings ratio. The top 40% (by count) of

stocks in aggressiveness are designated as “growth,” while the bottom 40% are called, “value,” with the 20%

in the middle of falling into “centric.”

Upside Potential

The average return above the Desired Target Return®, measuring how often and how far above the Desired

Target Return® a portfolio’s returns are likely to occur. Upside Potential, a term coined by Nobel Prize winner

Daniel Kahneman, captures investors’ perception of risks concerning gains as opposed to risk concerning losses.

U-P Ratio (Upside Potential Ratio)

The ratio of Upside Potential to Downside Deviation at a given DTR® Desired Target Return®, measuring how

much upside potential is provided by a manager at a given level of downside risk.

Mathematically,U-P Ratio = UP/DD

Where,UP = Upside Potential DD = downside deviation

PAGE 26

• D

TR®

Glossary

D E S I R E D T A R G E T R E T U R N ®

DisclaimerThe material presented in this brochure is for illustration purposes only and is an attempt to communicate a

complex subject in a simplified fashion. For more information regarding Sortino’s Upside Potential/Downside

Risk optimization methodology you can visit www.sortino.com or www.sortinoim.com. Sortino’s methodology

strives to take a cautious approach to analyze past performance in order to predict future results in a world of

uncertainty. Many calculations are performed as it related to protecting the investor on the downside. From

Style Beta, Downside Deviation, Risk Aversion and DTR®-Alpha, in essence each statistic measurement is

calculated by design to penalize each active manager solution more severely for performing below than giving

them credit for meeting or exceeding the Target Rate of Return. Passive management is integrated where this

scrutinized satisfactory active manager is absent and to budget active manager risk.

The culmination of over 40 years of work by Dr. Sortino and the work of highly acclaimed academics and

Noble Prize winners has brought us to a new paradigm of investing — one that focuses on the return needed to

accomplish an investor’s goal while at the same time providing the downside protection every investor seeks.

The Desired Target Return® Program does not take into consideration the investor’s tax situation, debt or future

changes in assets or income needs. The investor should evaluate their level of risk tolerance based on their own

investment knowledge, experience, demographics and net worth and consider either adjusting their portfolio

risk, investigating alternative investment options, or consulting with an investment advisor to consider their

specific situation and needs. The program assumes that the DTR® is the underlying goal of the investor, and

the possibility of the investor failing to reach the Desired Target Return® accordingly is a primary investor risk.

Investing in financial securities involves risk. The higher the Desired Target Return® the greater the potential for

significant loss of principle in your retirement account balance. Ignoring or under estimating the Desired Target

Return® increases the risk of not replacing a sufficient amount of pre-retirement salary. Sortino Investment Ad-

visors, LLC (SIA) makes no assurances, implied or implicit, that the Desired Target Return® assigned to each

participant will be achieved nor if achieved will result in replacing a significant amount of pre-retirement salary.

Past performance is no guarantee of future results. SIA, its affiliates, and its employees are not in the business

of providing tax or legal advice. These materials and any tax-related statements are not intended or written to

be used, and cannot be used or relied upon, by any such taxpayer for the purpose of avoiding tax penalties.

Tax-related statements, if any, may have been written in connection with the “promotion or marketing” of the

transaction(s) or matters(s) addressed by these materials, to the extent allowed by applicable law. Any such

taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor.

PAGE 27

• D

TR®