determinants of non-performing loans in indian banking systempsrcentre.org/images/extraimages/27...

TRANSCRIPT

Abstract—This paper investigates the determinants of

nonperforming loans (NPL) in the Indian banking system with the

help of panel data modelling. Panel dataset of 31 Indian banks with

yearly data that spans the period of 2000 to 2012 totalling 372 firm

years has been analysed. It is found that higher growth rate in savings

and GDP is associated with lower NPLs in Indian banks. Higher

interest and inflation rates contribute positively to rising non

performing loans.

Keywords— Non performing Loans, Panel data, Interest rates,

Inflation rates.

I. INTRODUCTION

ISING Nonperforming loans (NPL) in Indian banking

system in the post financial crisis is catching up attention

of all the cross sections of stakeholders. Regulators, policy

makers and rating agencies started investigating the reasons.

The central bank of the country Reserve bank started advising

banks on proactive steps to manage and arrest the growth.

In general an asset/loan becomes non-performing when it

ceases to generate income for the bank. The economic and

financial costs of NPL’s are significant. Graham and

Humphrey (1978) suggested that, banks with larger amounts of

NPL have greater tendency to incur large amount of future

losses, and hence, NPL should be included as an indicator of

the banking system stability [1]. Fofack (2005) pointed out

that, these loans may negatively affect the level of private

investment, increase deposit liabilities and constrain the scope

of bank credit [2].

The economic development of a nation and stability of

banking system are invariably interrelated. International

experience shows that if NPA is not managed properly, it will

leads to banking failures and nationwide financial fragility.

Regular monitoring of loan quality is thus essential to ensure a

sound finical system and possibly provides an early alarm to

regulatory authorities of banking system.

Given the above discussion, it is necessary to identify the

determinants of NPLs which is the major motivation for this

study. Using panel data modelling, this study empirically

investigates the determinants of nonperforming loans in the

Indian banking system. The purpose of this study is to provide

and insight into the linkages between macro-economic factors

and non-performing loans of banks functioning in India.

Dr.P.Krishna Prasanna, Associate Professor, Indian Institute of

Technology, Madras, India, Email id: [email protected].

II. DETERMINISTIC MACRO ECONOMIC FACTORS

INCLUDED IN ANALYSIS

Recent literature across the countries identified the

following macro economic variables to influence the level of

non-performing loans.

GDP Growth: it is considered as an indicator of a country’s

standard of living. A growing economy is likely to be

associated with rising incomes and reduced financial distress (

Nkusu (2011)[3]. Hence growth in GDP increases the

capability of borrowers to repay their debt and is expected to

contribute to a lower NPL.

Construction Expenditure Growth: Construction sector

expenditure at constant terms is an independent variable that is

expected to influence NPLs.(Vogiazas 2011)[4].

Foreign Reserves Growth: It is a proxy for the growth in the

international trade of the country and hence, the Non

performing loans are expected to decrease with the rise of

foreign reserves.

Stock Market Index Growth: Buoyant stock markets reflects

outlook on firms’ profitability and improved the financial

health of the nation (Bofondi et al .,2011) that is likely to have

impact on the non performing loans[5].

Stock Market Volatility:: Merton’s theory predicts that the

probability of default is positively related to the stock market

volatility (Simons (2009)[6].

Inflation: According to Qu (2008), it is viewed as a hidden

risk pressure which provides an incentive for those with

savings to invest them, rather than have the purchasing power

of those savings erode through inflation[7]. On the other hand,

Nkusu (2011)[3], stated that higher inflation can make debt

servicing easier by reducing the real value of outstanding

loans. There is divided evidence on both the directions in the

literature.

Exchange Rate: According to Nkusu (2011)[3], on the one

hand, increase in exchange rate can reduce the ability of

investor to pay back by weakening their competitiveness of

export. On the other hand, it can improve the debt servicing

capacity of borrowers who borrow in foreign currency. Hence,

an increase in exchange rate can have mixed implications.

Growth Rate in per Capital Income in NNP: It is a

macroeconomic indicator which reflects the strength and

behaviour of per capital income. An increase in GRRT

indicates that the people earns more and hence will have

increased ability to pay back, which results in less NPL.

Determinants of Non-Performing Loans

in Indian Banking System

Dr. P. Krishna Prasanna

R

3rd International Conference on Management, Behavioral Sciences and Economics Issues (ICMBSE'2014) Feb. 11-12, 2014 Singapore

115

Repo/ Reverse Repo Rate: Short term interest rates such as

repo rate and reverse repo rate have played a crucial role in

RBI monetary policy stance, Rajiv&Chandra (2011)[8]. RBI

injects liquidity in the system through Repos and absorbs

liquidity from the system from reverse repos. The objective of

monetary policy has been unidirectional to reduce inflation so

the relationship is expected to be opposite with respect to

inflation variable.

Saving Growth Rate: Swamy (2012)[9] stated that savings

level in an economy explain the economic surplus available, in

general, which is directly proportional to the repayment

capacity of the borrowers of the banking sector. Hence it is

expected to show negative relation with NPL.

Rate of Unemployment: Bofondi et al (2011)[5] mentioned

that increase in the unemployment rate curtail the present and

future purchasing power of household. Hence, it is expected to

have a positive relationship with NPL.

All the above variables are included as exogenous in this

research study. The variables with absolute rupee values were

quantified using natural logarithmic values. In respect of other

variables growth rates were used to proxy the exogenous

variable. In literature, NPL’s are measured on either gross

basis or on net basis. Gross NPLs reflects the quality of loans

portfolio of banks and net NPLs shows the actual load on the

banks. In this study percentage ratio of Gross NPL to total

advances and percentage ratio of Net NPL to total advances

has been considered as dependent variables for the analysis.

III. PANEL DATA ANALYSIS AND INFERENCES

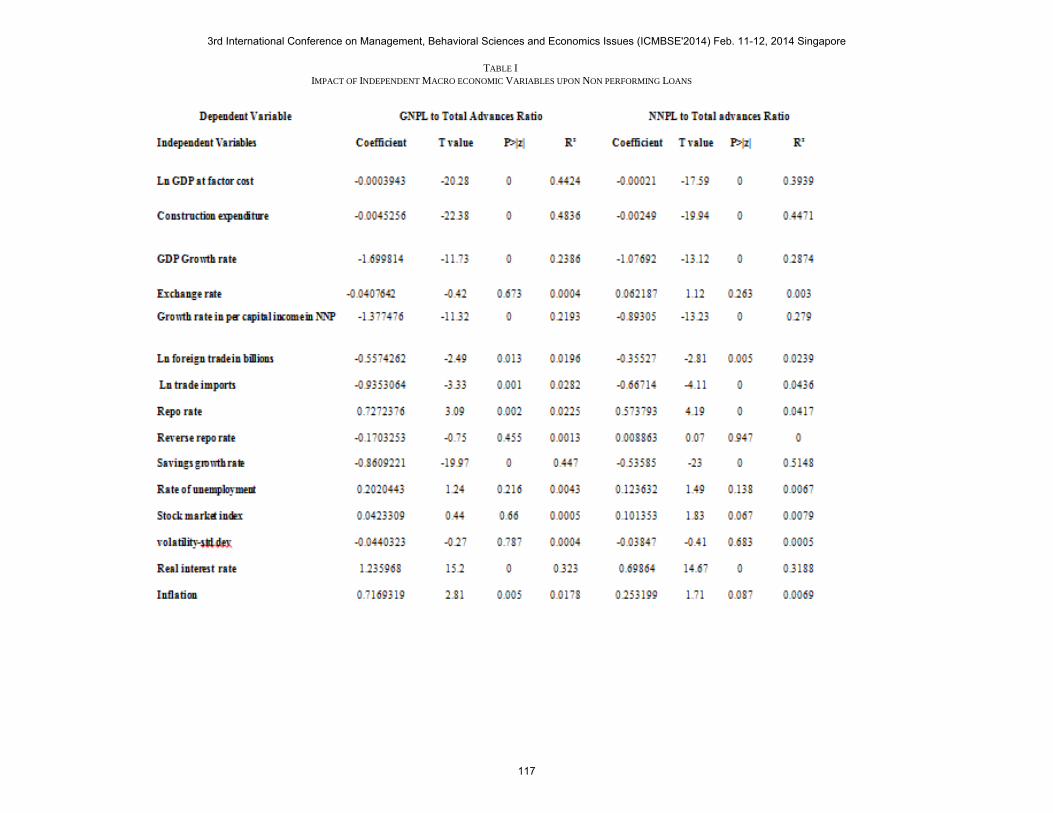

The bivariate regression analysis is conducted to identify the

independent relationship of each macroeconomic variable

upon the gross and net NPL ratio. The data set was a panel

data of 31 banks Indian banks with yearly data from 2000-

2012 totalling 372 firm years. The random effects GLS model

was used to capture and estimate both the cross section as well

as time effects in the variables. Table I presents the impact of

macroeconomic variable up on the non performing loans.

Subsequently the statistically significant variables have been

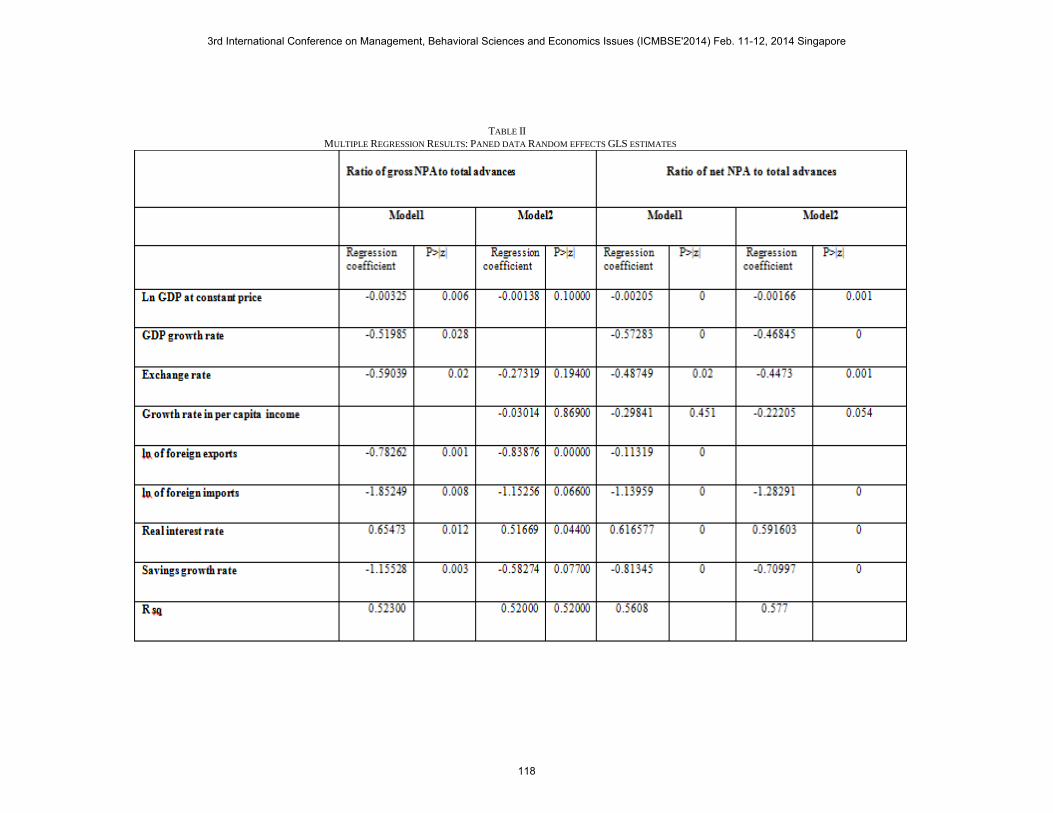

considered to run multiple regressions. The table II presents

the multiple regression results using Random effects GLS

model.

It is found that Ln GDP at factor cost, GDP Growth rate,

Growth rate in per capital income, foreign trade proxies,

Savings growth rate have significant inverse impact upon non

performing loans. Higher growth rates in savings, per capital

Income and GDP result in lowering non performing loans

significantly. GDP growth rate and savings growth rate had R

square of 44% which explain that they were most influencing

variables in determining level of nonperforming assets

.Exchange rates and stock market volatility also indicated

inverse relationship but were not found statistically significant.

Inflation and Interest rates have significant positive impact

on non performing loans. Higher interest rates results in higher

nonperforming assets. Interest rate had 33% impact on the non

performing assets across the banks and across 12 years study

time. Rate of unemployment was found to have positive impact

but was not significant.

The multiple regression results reconfirm the relationship

observed in bivariate relationship. These macro variables

together contribute 52% of changes in nonperforming loans.

Bank specific policies or customer specific characteristics

explain only the remaining 48% of changes.

IV. CONCLUSION

Impact of macroeconomic variables up on in gross NPL and

net NPL ratio to total advances has been investigated for

Indian banking system in the period of 2000-2012. Our

empirical results indicate that 52% of changes in the non

performing assets are determined by macro economic

variables. Growth rates in GDP, Savings, and per capita

income have significant inverse relationship which inflation

and interest rates have significant positive impact on the level

of nonperforming loans.

REFERENCES

[1] Graham, David R.; David Burras Humphrey., ‘Banks Examination Data

as Predictors of Bank Net Loans Losses’ (1978): Journal of Money,

Credit and Banking, November, Vol 10,No. 4, 491-504.

[2] Fofack, Hippolyte., ‘Nonperforming Loans in Sub-Saharan Africa:

Causal Analysis and Macro-Economic Implications’ (2005): World

Bank Policy Research Working Paper 3769.

[3] Nkusu, Mwanza., ‘Nonperforming Loans and Macrofinancial

Vulnerabilities in Advanced Economies’ (2011): IMF Working Paper,

WP/11/161.

[4] Vogiazas, D. Sofoklis.;Nikolaidou, Eftychia., ‘Investigating the

Determinants of Nonperforming Loans in the Romanian Banking

System: An Empirical Study with Reference to the Greek Crisis’ (2011):

Economics Research International, Vol 2011, Article ID 214689

[5] Bofondi, Marcello.;Ropele, Tiziano., ‘Macroeconomic Determinants of

Bad Loans: Evidence from Italian Banks’ (2011): Occasional Papers.

[6] Simons, Dietske.;Rowles, Ferdinand., ‘Macroeconomic Default

Modelling and Stress Testing’ (2009): International Journal of Central

Banking.

[7] Qu, Yiping., ‘Macro economic Factors and Probability of Default’

(2008): European Journal of economics, Finance and Administrative

Sciences, ISSN 1450-2275, Issue 13.

[8] Ranjan, Rajiv.; Dhal, Sarat Chandra., ‘Non-Performing Loans and Term

of Credit of Public Sector Banks in India: An Empirical Assessment’

(2003): Reserve Bank of India Occasional Papers, Vol. 24, No. 3.

[9] Swamy, Vigneswara., ‘Impact of Macroeconomic and Endogenous

Factors on Non-Performing Banks Assets’ (2012): International Journal

of Banking and Finance, Volume 9 | Issue 1, Article 2.

3rd International Conference on Management, Behavioral Sciences and Economics Issues (ICMBSE'2014) Feb. 11-12, 2014 Singapore

116

TABLE I

IMPACT OF INDEPENDENT MACRO ECONOMIC VARIABLES UPON NON PERFORMING LOANS

3rd International Conference on Management, Behavioral Sciences and Economics Issues (ICMBSE'2014) Feb. 11-12, 2014 Singapore

117

TABLE II

MULTIPLE REGRESSION RESULTS: PANED DATA RANDOM EFFECTS GLS ESTIMATES

3rd International Conference on Management, Behavioral Sciences and Economics Issues (ICMBSE'2014) Feb. 11-12, 2014 Singapore

118