digital finance plus readiness in tanzania: full version

TRANSCRIPT

CGAP Digital Finance +

Readiness Framework

and Assessment for

Tanzania

1

Agenda

Readiness framework

Access to and reach of mobile infrastructure

Adoption and reach of digital finance infrastructure

Role of the government and regulation

Sector analysis – water

Sector analysis – education

Sector analysis – energy

Sector analysis – health

Sector analysis – agriculture

2

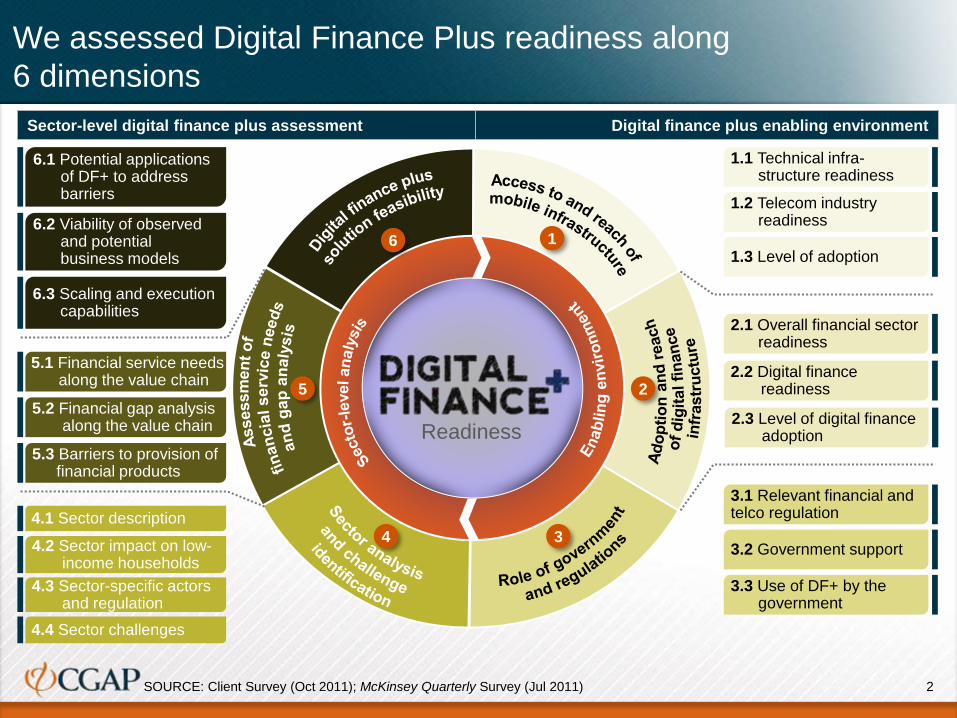

We assessed Digital Finance Plus readiness along

6 dimensions

SOURCE: Client Survey (Oct 2011); McKinsey Quarterly Survey (Jul 2011)

Digital finance plus enabling environmentSector-level digital finance plus assessment

4.1 Sector description

4.2 Sector impact on low-income households

5.1 Financial service needs along the value chain

5.2 Financial gap analysis along the value chain

5.3 Barriers to provision of financial products

4.3 Sector-specific actors and regulation

6.1 Potential applications of DF+ to address barriers

6.2 Viability of observed and potential business models

6.3 Scaling and execution capabilities

4.4 Sector challenges

6

5

4 3

2

1

Readiness

1.1 Technical infra-structure readiness

1.2 Telecom industry readiness

1.3 Level of adoption

3.1 Relevant financial andtelco regulation

3.2 Government support

3.3 Use of DF+ by the government

2.2 Digital finance readiness

2.3 Level of digital finance adoption

2.1 Overall financial sector readiness

3

Digital finance readiness assessment framework detail (1 of 6)

Questions Functional area

1. Access

to and

reach of

mobile

infra-

structure

1.1 Technical

infrastructure

readiness

1.2 Telecom

industry

readiness

Phase

How many nationwide mobile

phone providers exist and how is

the industry changing?

▪ Describe the industry’s structure (number and size of

national and regional players), competitive dynamics,

and where experts see the industry going

How much do mobile services

cost and how have these prices

changed?

▪ Evaluate cost information for a phone, SIM card, 1

SMS, 10 minutes of call time, 1 MB of mobile data,

and trends across geographies

▪ How ubiquitous is mobile

phone and internet coverage

in the country and how might

it change?

▪ What type of networks exist?

▪ What is their quality and how

reliable are they?

▪ Evaluate the percentage of people with coverage by

region and available network speed with a particular

focus on the differences between rural and urban

areas and projected changes over the next 2-3 years

Analyses to conduct

How much of the country actually

uses mobile services?

▪ Examine trends in the percentage of adults with

mobile phone subscriptions and mobile internet

access across regions with a focus on rural vs. urban

How often are these services

used?

▪ Examine frequency of use and types of plans

1.3 Level of

adoption

4

Digital finance readiness assessment framework detail (2 of 6)

Questions Functional area

2. Adoption

and reach

of digital

finance

infra-

structure

2.1 Overall

financial sector

readiness

2.2 Digital

finance

readiness

Phase

What products does the financial

sector offer?

▪ Describe products/services offered and their distribution

What types of digital finance

products exist?

▪ List digital finance products (distinguish between payment,

savings, credit, insurance etc.)

Analyses to conduct

2.3 Level of

digital finance

adoption

How many adults have adopted

digital finance products?

What are these products used for?

▪ Determine the percentage of adults using digital finance

products, the percentage of transactions (payment,

savings, insurance) done via them, and reasons for any

low levels of adoption

How many adults and businesses

would be open to using digital

finance products?

▪ Determine the percentage of adults and businesses

familiar with and open to using digital finance

▪ Evaluate this across regions with a focus on urban vs. rural

What is the competitive landscape

in the financial sector and how is it

changing?

▪ Describe the industry’s structure (number and size of

national and regional players), the role and reach of non-

traditional financial players, competitive dynamics, and

where experts see the industry going

What access to them do different

segments of the population have?

▪ Evaluate access to different financial products/services

across regions

How are these products distributed

and what are the minimum

requirements for use?

▪ Describe reach of typical distribution channel

What types of providers offer digital

finance products and how might the

landscape change over the next few

years?

▪ Map products to different types of providers (e.g.,

traditional financial institutions, telcos, microfinance)

▪ Describe major product, technology, and distribution trends

5

Digital finance readiness assessment framework detail (3 of 6)

Questions Functional area

3. Role of

the

govern-

ment and

regulation

3.1 Relevant

financial and

telco regulation

3.2 Government

support

Phase

What are government digital

finance regulations?

▪ Examine additional rules specific to digital finance entry,

operations, and end users; these include partnership

requirements to offer products, architecture

(interoperability requirements), e-payment, product

offerings, accounting practices, anti-money laundering,

who can act as agents, and KYC regulation

▪ Identify regulatory gaps and barriers preventing or

slowing the implementation of DF+

What are government regulations

around information tracking?

▪ Examine rules about what data digital finance providers

can keep, use, and sell

What are government finance

regulations?

▪ Examine the rules on who can offer what products and

how they must be sold, and the clarity of these rules

Analyses to conduct

Does the government help expand

mobile/digital payment

infrastructure?

▪ Research on budget and subsidies allocated to these

infrastructures

▪ Identify policies that would help the spread of DF+

Does the government take action

to increase the number of digital

finance players?

▪ Evaluate of awareness raising and budget allocated to

organizations for digital finance

▪ Form qualitative view of the encouragement of new

entrants and joint ventures

3.3 Use of DF+

by the

government

Does the government use digital

finance products?

▪ Identify government benefit programs/transfer schemes

that actively use DF+ (and other spending and salary

payments)

6

Digital finance readiness assessment framework detail (4 of 6)

Questions Functional area

4. Sector

analysis

and

challenge

identifi-

cation

4.1 Sector

description

4.2 Sector

impact on low-

income

households

Phase

4.4 Sector

challenges

What is the overall value chain

for the industry and structure at

each step?

▪ Describe actors and industry structure (number of

players, size, and competitive dynamics) for each

relevant step

What is the role of the

government in each step of the

value chain?

▪ Describe the role of public financing/provision,

subsidies, and relevant regulation

What is the significance of the

sector in the country’s economy?

▪ Determine the percentage of GDP accounted for by

sector, the percentage of workforce employed within

the sector, quality of services, productivity and

competitiveness accounting for regional variance and

international comparisons

What trends will shape the

sector?

▪ Describe relevant policy, technology, and macro

changes

What services are and are not

provided to low-income

households and what determines

access to these services?

▪ Describe actual services delivered to low-income

households and identify the variation in provision by

geography, income, and other attributes

What are the key challenges

in the sector?

▪ Overview of key shortcomings in the sector along the

value chain

Analyses to conduct

4.3 Sector-

specific actors

and regulation

What is the sector-specific

regulation affecting the delivery

of services?

▪ Describe sectors specific regulation, including

competitive regulation, product regulation , access

regulation, minimum service standards, customer

protection etc.

7

Digital finance readiness assessment framework detail (5 of 6)

Questions Functional area

5. Asses-

ment of

financial

service

needs and

gap

analysis

5.1 Financial

service needs

along the value

chain

5.2 Financial

gap analysis

along the value

chain

Phase

5.3 Barriers to

provision of

financial

products

What financial service gaps exist

at each step of the value chain?

▪ Evaluate financial service needs not being served at

all by current products or being served inadequately

across regions and provide a view of what existing

services are missing

How would the closing of each

gap increase accessibility and

affordability?

▪ Develop a perspective on which gap closings would

have the highest impact

What type of financial needs

exist for interactions across the

value chain?

▪ Evaluate financial product needed at each step

(payment access, financing, mediation, market

information, insurance, savings, etc.) and key

attributes of identified service (speed, simplicity,

timing, etc.)

What barriers to the provision of

the identified financial services

exist?

▪ Identify barriers, including a lack of physical financial

infrastructure (agent network/brick and mortar

financial institutions), information asymmetry between

actors, a lack of a cost-effective provision of the

financial service, etc.

Analyses to conduct

8

Digital finance readiness assessment framework detail (6 of 6)

Questions Functional area

6. Digital

finance

plus

solution

feasibility

6.1 Potential

applications of

DF+ to address

barriers

6.2 Viability of

observed and

potential

business

models

Phase

Is there a feasible business

model for the product?

▪ Evaluate if there could be a financially viable business

model for this product given sector dynamics

Is there a feasible go-to-market

model to introduce this product?

▪ Evaluate go-to-market model that could achieve

necessary scale

Could a digital finance product

address the market failure?

▪ Determine if an existing or novel digital finance

product could address the market gap and overcome

the identified barriers

Analyses to conduct

What capabilities would be

necessary for a business to

successfully implement this

model?

▪ Develop perspective on capabilities and distribution

network necessary for a company to implement go-to-

market model and business model

How do those capabilities

compare with those of existing

enterprises?

▪ Map current provider capabilities to required ones

Are there actors capable of scal-

ing the existing business model?

▪ Identify the landscape of the actors in the sector and

evaluate scaling efforts6.3 Scaling and

execution

capabilities

9

Agenda

Readiness framework

Sector analysis – agriculture

Sector analysis – health

Sector analysis – energy

Sector analysis – education

Sector analysis – water

Access to and reach of mobile infrastructure

Adoption and reach of digital finance infrastructure

Role of the government and regulation

10

Summary of mobile infrastructure readiness assessment

1.1 Technical infrastructure readiness

• Tanzania’s four nation-wide MNOs operate a series of networks and standards ranging from 2G to

3.5G networks

• The penetration of these networks ranges from selected cities on 3.5G networks to 85% of the

population on 2G networks

• All major MNOs have committed to and are in the process of making major capital investments in 4G

networks, while continuing to expand coverage of existing 2G networks

1.2 Telco industry readiness

• Tanzania’s telco industry features 4 main competitors, Vodacom, Airtel, Tigo, and Zantel, with the first

3 accounting for 90% of the subscriber base

• Strong four-way competition has led to competitive prices and continued product innovation, with all

players offering mobile money and selected players launching mobile savings and credit products

1.3 Level of adoption

• Mobile phone adoption in Tanzania currently stands at ~60% and, below the regional average of 74%

• However, penetration over the past 4 years has been growing at approximately 10-12% per annum

• The continued extension of network coverage, declining mobile phone costs and growing household

income are expected to raise penetration to 70-80% over the next 2-3 years

11

Tanzania has been rapidly extending mobile coverage,

which has allowed the country to rapidly catch up to its peers

1.1 TECHNICAL INFRASTRUCTURE READINESS

SOURCE: Telegeography; press

Percentage of population living in areas with mobile

phone coverage

%, 2013

Overall assessment

Percentage of population living

in areas with mobile phone

coverage

%, historically

… but coverage is quickly increasing

Tanzania’s mobile coverage is slightly lower

than that of its peers …

Type of network,

% of population

covered

Ethiopia

Ghana

Kenya

Nigeria

Rwanda

South Africa

Tanzania

Uganda

India

Bangladesh

Pakistan

Myanmar

• Tanzania lags its peers in mobile

phone coverage, with 15% of the

population living without access to

a mobile network

• At the same time, mobile coverage

has been growing at close to 20%

per annum over the past 3 years

• Mobile coverage is expected to

reach 90+ % of the population by

2016

99

99

99

95

95

95

90

90

87

85

60

35

85

75

60

50

1312112010 2016

90++19% p.a.

70

85

3G2G

12

Tanzania’s MNOs operate a series of networks covering 60

to 85% of the population, depending on network generation

1.1 TECHNICAL INFRASTRUCTURE READINESS

2G 3.5G 1G 3.5GGene-

ration

2.5G 2.5G 3G 2G 2.5G 2.5G 3G 3.5G 2.5G 2.5G 3G 3G2G 3.5G

Platform GSM GSM GSM W-CDMA W-CDMA ETACS GSM GSM GSM W-

CDMA

W-

CDMA

W-

CDMA

GSM GSM CDMA2000 CDMA2000 W-CDMA W-CDMA

Evolution None GPRS EDGE None HSDPA None None GPRS EDGE None HSPA+ DC-

HSPA+

None GPRS 1x 1xEV-DO None HSPA+

Frequency 900/1800 900/1800 900/1800 Unknown Unknown 900 900/

1800

900/

1800

900/

1800

- - - 900/1800 900/1800 800 800 Unknown Unknown

Launch Nov-01 Apr-06 Apr-06 Dec-08 Dec-08 Sep-94 Aug-00 Aug-06 Aug-06 Q1 2011 May-13 Sep-13 Aug-99 - Nov-06 Nov-06 May-12 May-12

Status Live Live Live Live Live Shut

down

Live Live Live Live Live Live Live Live Live Live Live Live

Network

Details

Jan-14:

~85%; Dec-

11: 65-70%

(est.)

Jan-14:

88%; Dec-

11: 65-70%

(est.)

Jan-14:

~75%; Dec-

11: 65-70%

(est.)

Jan-14:

70% (est.);

Sep-11: Dar

es Salaam

Jan-14:

~70% (est.),

Sep-11: Dar

es Salaam

- Jan-14:

85%

(est.);

Dec-11:

67%

(1,173

BTS);

Dec-10:

63%

(1,057

BTS);

Dec-09:

60%

Jan-14:

80%

(est.);

Dec-11:

62%

(est.);

Dec-10:

60%

(est.)

Jan-14:

50%

(est.);

Dec-11:

35%

(est.);

Dec-10:

30%

(est.)

Jan-14:

70%

(est.)

Jan-14:

~20

cities

and

towns

(est.)

Jan-14:

only

selected

city

centers

Jan-14:

70% (est.);

Dec-11:

60% (est.);

Sep-10:

50% (est.)

Jan-14:

~50% (est.),

main towns

and cities

only

Jan-14:

Zanzibar,

Pemba, and

Dar es

Salaam

Jan-14:

Zanzibar,

Pemba, and

Dar es

Salaam

Jan-14:

Zanzibar

only (plans

expansion

to Dar es

Salaam and

other cities)

Jan-14:

Zanzibar

only (plans

expansion

to Dar es

Salaam)

2G 4G2.5G 2.5G 3G 3.5G 3.5G

GSM GSM GSM W-

CDMA

W-

CDMA

W-

CDMA

LTE

None GPRS EDGE None HSDPA HSUPA None

900 900 900 2100 2100 2100 800/

1800

Jul-99 Apr-06 Jul-07 Feb-07 Feb-07 Feb-07 -

Live Live Live Live Live Live In

deploy-

ment

Jan-14:

85%-90

(est.);

Dec-11:

75.8%

Jan-14:

85%-

90%

(est.);

Dec-11:

75.8%

Jan-14:

>50%

(select-

ed towns

and

cities)

Jan-14:

70%

(est.);

available

in

around

40 towns

and

cities

Jan-14:

70%

(est.);

available

in

around

40 towns

and

cities

Jan-14:

70%

(est.);

available

in

around

40 towns

and

cities

Laun-

ched six-

month

trial in

Msasani

Penin-

sular

district of

Dar es

Salaam

with

NSN in

Jan-13

2G network at ~85% 2G network at ~85% 2G network at ~85% 2G network at ~70%

SELF-REPORTED FIGURES MIGHT BE OVERSTATED

13

93 7

The top four MNOs in Tanzania own 99% of the mobile

market (1/2)

1.2 TELECOM INDUSTRY READINESS

Assessment

Number of mobile phone providers in Tanzania

Growing number of providersHigh market shares of top three operators

2013

8

12

8

11

7

2010

7

Market share of top 3-5 players, %Number of MNOs1 No

84 15

93 7

83 17

100

1 Mobile network operator

SOURCE: WCIS

98

2

82 17

Tigo Tanzania 6,297

52

Zantel 1,803

8,996

Vodacom Tanzania 10,289

Benson Informatics

0

Smile Tanzania

0Telesis

Hits

1

3

Sasatel 4

TTCL

Airtel Tanzania

Number of subscribers

000s

100

55 24

1089

72 28

100

4

12

8

8

3

Ghana

Kenya

Nigeria

Rwanda

South Africa

Tanzania

Uganda

5

6

1Ethiopia

1

1

1

1

India

Bangladesh

Pakistan

Myanmar

Top 3

Top 4

Top 3

Top 3

Top 5

Top 3

Top 5

Top 3

Top 5

Top 3

Top 5

Top 3

Top 5

Top 1

Top 3

Top 3

Top 3

Top 1

Top 5

Top 5

Top 5

MNO

• Tanzania’s mobile phone industry is dominated

by 4 relevant players that control more than 99%

of the market; this consolidation is similar to that

observed in peer countries

• The number of providers has roughly stayed the

same over the past few years

• All major providers cover the key population

centers allowing for significant competition

14SOURCE: WCIS; Telegeography; BMI

Assessment

Airtel

Benson

Tigo

Zantel

Vodacom

Tanzania

Number of subscribers

000s; 2013

0

0

10,289

8,996

4

52

3

1

6,297

1,803

TTCL

Smile1

Description/history

Telesis

1 Smile is a wireless broadband operator, it does not offer voice services

Hits

Sasatel

Tanzania’s MNOs have taken different strategies to acquire and retain customers

• The Tanzanian mobile phone market

features strong competition with

incumbents and new entrants

actively competing for market share

• Players compete <_> diverse

strategies including innovative

service offering (Vodacom), network

coverage (Airtel), and low pricing

(Zanzibar Telecom)

• Ahead of competition on introducing innovative

services but only regains subscribers after

2011/2012 loss

• Substantial investments resulted in the widest

mobile broadband coverage, but high prices

limit service uptake

• Aggressively expanding coverage, low tariffs,

and promotions enable it to quickly gain

market share

• Owns modern infrastructure, capable of

providing fast data services, but reliance on

CDMA blocks smooth migration to LTE

• High prices and limited coverage prevent quick

customer uptake despite modern infrastructure

• Simple tariffs and affordable broadband

enable growth but lack of scale prevents fast

expansions

• 20 years of mobile experience in Tanzania

combined with developed infrastructure

enables it to maintain third place in the market;

recently aggressive in marketing

The top four MNOs in Tanzania own 99% of the mobile

market (2/2)

1.2 TELECOM INDUSTRY READINESS

15

Tanzania’s MNOs offer an advanced set of digital finance

products

SOURCE: GSMA “Mobile Money Tracker”; Operators websites

Similar services offered by playersSimple mobile payments offering

Rwanda

Ghana

Kenya

Tanzania

Uganda

0

1

1

2

3

3

3

4

4

4

4

7

0

0

1

1

0

0

0

1

1

3

3

0

Simple digital

payment

product1

Advanced

digital

payment

product2

Number of MNOs offering digital finance products Description of product offering for biggest telco providers

Airtel

MIC

Tanzania

Limited

Vodacom

Tanzania

Zantel

South Africa

India

Nigeria

Bangladesh

Pakistan

Ethiopia

Myanmar

Basic Advanced

1 Simple: operator offers only bill payments, airtime top up, domestic money transfers, bulk payments, merchant payments

2 Advanced: in addition to the above, operator offers services such as loan repayments, debit, insurance, other banking products

Assessment

• Vodacom leads

the digital financial

service innovation

in Tanzania

offering the

broadest digital

finance product

portfolio

• Tanzania’s telco

industry compares

favorably with

other countries

based on its

offering of digital

finance products

1.2 TELECOM INDUSTRY READINESS

16

Mobile phone access remains relatively expensive in Tanz-

ania, smaller players/new entrants provide lower price options

Assessment

5

10

11

6

5

14

70

50

45

54

50

47

6

6

5

5

4

3

Cost per

sec1

Cost per

SMS

Cost per 1

MB2

Airtel

Benson

Tigo

Zantel

Vodacom

Tanzania

New entrants and smaller players are providing lower cost

options

SOURCE: WCIS; company websites

TTCL

Smile3

1 For calls to other networks (off-net); 2 Based on monthly bundled plan of 5GB except Smile for which 3GB data plan was analyzed;

3 Smile Tanzania offers only mobile broadband services

n/a n/a

n/a4

5

7

8

10

11

13

14

Cost of comparable monthly prepaid access1

USD at PPP

n/a

n/a

n/a

n/a

South Africa

Tanzania

Uganda

Nigeria

Ethiopia

Kenya

Rwanda

Ghana

Pakistan

Bangladesh

India

Myanmar

Mobile phone access remains relatively expensive

in Tanzania

• Tanzania’s mobile

phone sector offers

a healthy set of

prices with new

entrants providing

low-cost

alternatives to

incumbents

1.2 TELECOM INDUSTRY READINESS

in TZS

17

Mobile phone penetration in Tanzania remains below peer

average, however penetration is rising quickly

1.3 LEVEL OF ADOPTION

12

27

58

60

63

67

69

70

72

73

109

138

2

3

1

1

2

2

1

1

9

n/a

n/a

n/a

Mobile pene-

tration1

% of population

Mobile

internet

penetration

% of population

1 Not adjusted for multi-SIMming, i.e., individuals may own more than one SIM card and be counted multiple times

60

55

50

42

201312112010

+12% p.a.

Overall assessmentGrowing mobile penetrationTanzania’s mobile penetration is similar to its peers

Ghana

Nigeria

South Africa

Tanzania

Kenya

Mobile penetration

% of population

SOURCE: Analyses Mason; WCIS

Uganda

India

Rwanda

Bangladesh

Ethiopia

Pakistan

Myanmar

2013

• Tanzania’s mobile phone

penetration is below its regional

peers

• Over the past 3 years, Tanzania

has added approximately 5% of its

population to the subscriber base

annually

• Often penetration does not fully

reflect true access of different

people within a household, leaving

some question as to female access

to services

18

Access to mobile phone for rural, unbanked, and low-income

households is substantially lower than middle-/high-income households

Tanzania’s mobile phone access differs by household groups

SOURCE: FITS household survey

2012

• A substantial gap in mobile

phone access exists

between the group of

rural/unbanked/low-income

households (55-57%) and

the group of middle-/high-

income households (76%)

Household

consumption

above$2/day

Rural

Unbanked

Household

consumption

below $2/day

76.0

57.0

58.0

55.0

63.0

Households

that have or

can borrow a

mobile phone

Assessment

Percentage of total households

1.3 LEVEL OF ADOPTION

19

Agenda

Readiness framework

Adoption and reach of digital finance infrastructure

Role of the government and regulation

Sector analysis – agriculture

Sector analysis – health

Sector analysis – energy

Sector analysis – education

Sector analysis – water

Access to and reach of mobile infrastructure

20

Summary of digital finance infrastructure readiness

assessment

2.1 Overall financial sector readiness

• Tanzania’s banking sector includes 50 licensed banks and a number of regulated and unregulated

microfinance institutions

• Despite the large number of licensed institutions, the formal banking sector serves only 14% of the

population, focusing predominantly on the urban salaried workers and commercial lending

• A number of attempts by large commercial banks to extend their products to the unbanked have

resulted in significant write-offs and their subsequent withdrawal from this segment

• Micro-finance institutions are the only players extending significant credit to low-income households,

credit procedures and collateral / guarantor requirements are however burdensome and constitute a

serious barrier to credit

2.3 Level of digital finance adoption

• Mobile money has experienced exponential growth over the past 5 years

• Starting from virtually no use in 2009, mobile money uptake has increased to over 11 million users in

2013, which equals 49% of the adult population

• Key uses of mobile money are sending and receiving money (predominantly from remittances

payments,) which account for almost 70% of all mobile money transactions

2.2 Digital finance readiness

• A notable barrier to mobile money adoption is still the lack of access to mobile phones for significant

parts of the population

• Rural penetration of mobile money remains relatively low and account activitiy while growing is still

low

21

10

14

19

40

50

Uganda

Rwanda

South Africa

Kenya

Tanzania

Tanzania’s banking sector includes 50 licensed banks, with the top 10

banks accounting for ~75% of lending and ~85% of deposits

Number of licensed banks

Assessment

255,553

303,036

319,813

399,950

413,818

438,583

491,904

654,446

1,354,770

1,806,865

444,562

313,715

556,359

686,711

700,927

886,162

1,291,335

2,288,263

2,582,328

3,918,095

20.6

15.4

7.5

5.6

5.0

4.7

4.6

3.6

3.5

2.9

23.4

15.4

13.7

7.7

5.3

4.2

4.1

3.3

2.7

1.9

2.1 OVERALL FINANCIAL SECTOR READINESS

…and market share is split among the leaders

M/s, %

Top 10 banks hold 73.3% of the loan market

Top 10 banks hold 83.6% of the deposit market

Top 10 banks in Tanzania by deposits, 2012

Top 10 banks in Tanzania by loans, 2012

Total loan volume in TSH millions

Total deposit volume in TSH millions

Tanzania has more banks than its peers…

• Tanzania has a diverse

banking sector with over 50

licensed players

• While the formerly state-

owned banks still dominate,

a number of regional and

international banks have

achieved considerable

market share

SOURCE: Bank of Tanzania

22

Tanzania’s banking sector has become more competitive,

but it still lags peer countries

0.56

0.30

0.10

0.35

0.47

0.27

0.11

0.19

Ethiopia

Kenya

Uganda

Bangladesh

Tanzania

Ghana

Nigeria

India

Rwanda

South Africa

n/a

2005 2010

0.59

0.36

0.31

0.29

0.27

0.24

0.22

0.16

0.15

0.15

• Tanzania’s

competitiveness

has substantial

improved over the

last couple of

years

• Compared to ist

regional peers

especially South

Africa and Rwanda

competitiveness

remains low

Top 3 banks’ market power (Lerner index) Assessment

2.1 OVERALL FINANCIAL SECTOR READINESS

SOURCE: Tanzania Banking Survey

23

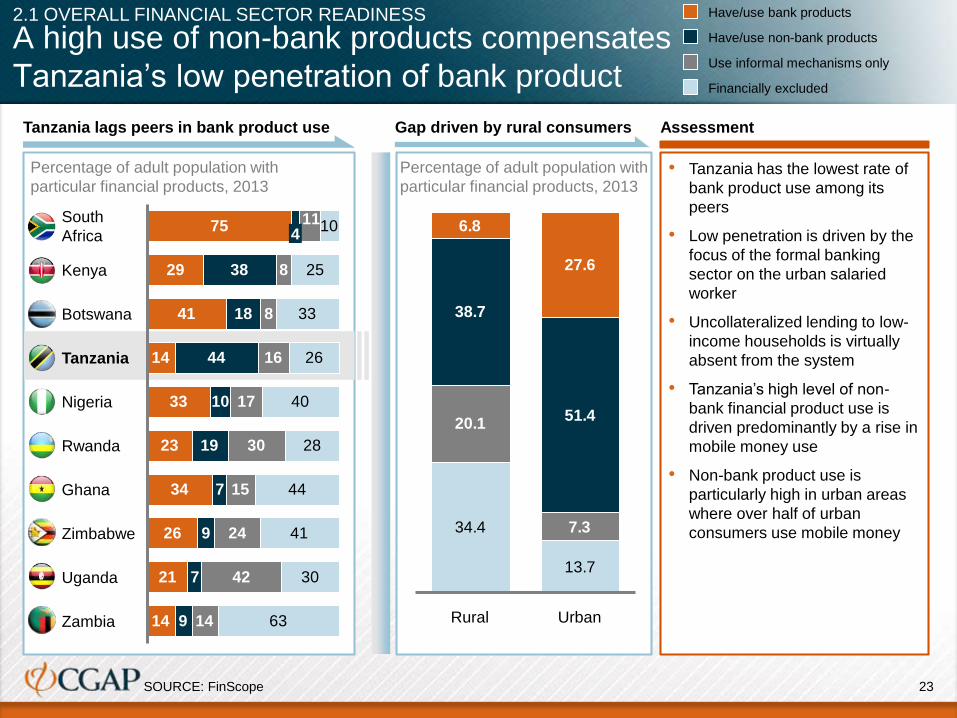

A high use of non-bank products compensates

Tanzania’s low penetration of bank product

Assessment

29

41

14

33

23

34

26

21

14

38

18

44

10

19

7

9

7

9

8

8

16

17

30

15

24

42

14

10

25

33

26

40

28

44

41

30

63

75 11

Rwanda

Nigeria

Zambia

Uganda

Zimbabwe

Ghana

South

Africa 4

Tanzania

Botswana

Kenya

Financially excluded

Use informal mechanisms only

Have/use non-bank products

Have/use bank products

34.4

13.7

20.1

7.3

38.7

51.4

6.8

27.6

Rural Urban

Tanzania lags peers in bank product use Gap driven by rural consumers

2.1 OVERALL FINANCIAL SECTOR READINESS

• Tanzania has the lowest rate of

bank product use among its

peers

• Low penetration is driven by the

focus of the formal banking

sector on the urban salaried

worker

• Uncollateralized lending to low-

income households is virtually

absent from the system

• Tanzania’s high level of non-

bank financial product use is

driven predominantly by a rise in

mobile money use

• Non-bank product use is

particularly high in urban areas

where over half of urban

consumers use mobile money

Percentage of adult population with

particular financial products, 2013

Percentage of adult population with

particular financial products, 2013

SOURCE: FinScope

24

MFIs are the only financial institutions extending significant credit to

low-income households

Tanzania market profile

MFIs Borrowers

AccessBank – TZA 15,819

Akiba 27,111

BRAC – TZA 104,225

ECLOF – TZA 5,051

Equity Bank Tanzania 7,176

FINCA – TZA 82,288

IDYDC -

K–Finance 572

MBF 2,478

Mbinga Community Bank 6,053

Mtoni 1,351

MuCoBa 5,601

Mwanga Community Bank 8,314

NMB -

Opportunity Tanzania 8,959

PRIDE – TZA 100,055

PTF 6,108

SEF – TZA 1,198

SELFINA 7,746

Tujijenge 8,265

Victoria Finance 155

VisionFund TZA 33,394

YOSEFO

Loans

USD

32,596,119

46,766,487

20,267,459

1,467,041

60,487,310

29,593,107

354,157

194,029

212,031

908,172

2,004,364

4,024,608

5,140,608

773,508,940

6,206,129

37,028,179

1,147,468

263,569

4,002,088

775,268

342,857

7,080,836

2,521,617 18,120

1. NGO MFI

(not regulated)

2. Microfinance companies

(regulated by BoT with lower capital

requirements than regular banks)

3. Commercial and community banks

(regulated by BoT)

4. Savings and credit cooperative

societies

(regulation limited to annual audit)

Tanzania recognizes 4 types of

microfinance institutions with

different levels of regulation

Lending to low-income households

requires:

- Significant collateral

- Multiple guarantors

- An involved application process

with often multiple visits

- rates vary between 30-80 p.a.

2.1 OVERALL FINANCIAL SECTOR READINESS

SOURCE: Tanzania Banking Survey

25

Tanzanian access to formal sector finance has increased in

recent years largely because of the adoption of mobile money

Adults served

by the

non-bank

formal sector

Banked adults

55.9

13.1

13.8

9.1 6.3

Insurance

13.0

49.0

1.1

Use mobile

money

4.5

MFI/SACCOS

member

4.4

Assessment

13.6m

2.8m

3.4m

1.9m

11.9m

0.2m

3.1m

1.3m

Percent

1.1m

1.0m

% of adults 2009% of adults 2013

This increase in non-bank service is driven

by mobile money

Growth has been driven by the non-bank

formal sector

2.2 LEVEL OF DIGITAL FINANCE ADOPTION

• The rise of mobile

money is driving

Tanzanians’ increased

financial access

• Banks and insurance

providers have also

played a substantial role

in this rise as each

industry increased users

by over 1 million

between 2009 and 2013

• MFI/SACCOS

membership remained

relatively constant,

suggesting enrollment

may have plateaued

SOURCE: FinScope

26

Approximately 70% of mobile money users predominantly

use the service to send or receive money

25.6

Pay bills,

fees, and

business

transactions

37.6

Save or store

money

33.1Send money

Receive money

9.9

Assessment

8.0

Percent

2.4

Uses of mobile money

2.2 LEVEL OF DIGITAL FINANCE ADOPTION

• While mobile money

has seen significant

growth, subscribers

predominantly use it

for sending and

receiving money

• Efforts to expand

usage to general

business transactions

are in early stages

11.9

Use mobile

money

9.1

6.2

SOURCE: FINSCOPE

Millions, in million Households, in

million

27

Use of mobile money differs substantially between

rural/unbanked/low-income and mid-/high-income households

Tanzania’s mobile money penetration

SOURCE: FITS household survey

• Tanzania’s mobile phone

penetration is in line with its

peers

• Over the past 3 years,

Tanzania has added

approximately 5% of its

population to the subscriber

base

• Often penetration does not

fully reflect the access of

different people within the

household, leaving some

question as to female access

to services

Household

consumption

above$2/day

Rural

Unbanked

Household

consumption

below $2/day

53.0

29.0

29.0

25.0

35.0

Mobile money

user in houshold

Assessment

2.2LEVEL OF DIGITAL FINANCE ADOPTION

2012, Percent

28

Of the non-users of mobile money, the majority quote the

lack of a mobile phone as the key barrier

Assessment

PercentFor products beyond payment, more fun-

damental product questions need to be

addressed first, not addressed in chart

The lack of a mobile phone is the main

barrier to mobile money adoption

2.3 DIGITAL FINANCE READINESS

• The lack of a mobile

phone remains a

serious obstacle to

adoption for mobile

payments

• For other mobile

products such as

insurance and credit,

knowledge of the

product itself is the key

barrier

• Digital finance can

address these problems

more effectively than

bricks and mortar

branches by using

mobile technology to

educate and reach

potential consumersHigh fees

Knowledge

about registration

4.5

8.3

Distance to mobile

money agent8.5

Don’t have

mobile phone60.4

4.8

5.6

Don’t know

product

Cannot

afford15.4

Does notknow howit works

Does notknow whereto purchase

64.2

Insurance

Credit product

8.0

Don’t know

product

Cannot

afford35.2

Does not

know where

to purchase

37.5

SOURCE: FinScope

29

Agenda

Readiness framework

Sector analysis – agriculture

Sector analysis – health

Sector analysis – energy

Sector analysis – education

Sector analysis – water

Role of the government and regulation

Access to and reach of mobile infrastructure

Adoption and reach of digital finance infrastructure

30

The telco industry is regulated by the Tanzanian Communication Regula-

tory Authority that is implementing a series of key regulatory initiatives (1/2)

Telco regulatory framework

• Tanzanian Communication

Regulatory Authority

• Provide effective

competition

• Protect consumer interest

• Regulate rates and

changes

• Manage radio frequencies

Stability • In place since 2003, and

has introduced significant

regulation

i. Interconnection fees regulation

Termination charge set by TCRA, TZS

• Significant focusing of lowering termination charges to

increase competition among mobile phone subscribers

• Introduction of rate schedule that is designed to reduce

termination charges from 112 TZS to 26.96 TZS by 2017

26.9628.5730.5832.4034.12

112.00

2017161514132012

Telco

Regulatory playing field Key regulatory initiatives

3.1 RELEVANT FINANCIAL AND TECLO REGULATION

Regulator

Task

31

The telco industry is regulated by the Tanzanian Communication Regula-

tory Authority that is implementing a series of key regulatory initiatives (2/2)

Telco regulatory framework

ii. Mobile SIM registration

Telco

Key regulatory initiatives

• Compulsory registration of all active SIM cards

nation-wide

• Hosted June 2009, final deadline postponed to 2013

• Disconnection of 650,000 subscribers for failure

to register

iii. Mobile number portability

• Regulatory initiative to enable the portability of

mobile numbers when switching MNOs

• Part overall reform package aimed at increasing

competition between MNOs

• Originally planned for 2013, postponed to 2014 to

allow for technical implementation

iv. Universal Service Access Fund

• Dedicated financing vehicle to increase mobile

connectivity in rural areas

• Bid-based tenders for subscribers to expand

coverage to underserved areas

• A number of contracts awarded in 2013 to all

four major MNOs

3.1 RELEVANT FINANCIAL AND TECLO REGULATION

32

The banking sector is regulated by the Bank of Tanzania

Banking regulatory framework

• Bank of Tanzania

• Prudential regulation

• Operational guideline and

regulation

• Sector-wide and player-

specific risk management

• Further financial inclusion

• Regulator for over 15 years

i. Credit bureau

• The BoT has recently licensed two credit bureaus to

compile data from all licensed banks and MFIs

• Credit bureaus are currently establishing reporting

relationships

Telco

Regulatory playing field Key regulatory initiatives

i. National ID card system

• Tanzania is introducing a national ID system that uniquely

identifies each citizen

• In conjunction with the credit bureau, this system is

expected to significantly raise credit provision

i. Agency banking

• The BoT has recently introduced a new agency banking

framework enabling the delivery of banking service through

licensed agencies

• Agency banking is expected to substantially lower cost and

widen access to financial services

Stability

Regulator

Task

3.1 RELEVANT FINANCIAL AND TECLO REGULATION

33

Agenda

Readiness framework

Sector analysis – agriculture

Sector analysis and challenge identification

Assessment of financial service needs and gap analysis

Digital finance plus feasibility assessment

Sector analysis – energy

Sector analysis – water

Sector analysis – health

Sector analysis – education

SOURCE: Source

Access to and reach of mobile infrastructure

Adoption and reach of digital finance infrastructure

Role of the government and regulation

34

Key takeaways: Agricultural sector analysis and challenge

identification

AGRICULTURE – SECTOR ANALYSIS AND CHALLENGE IDENTIFICATION

4.1 Sector description

4.3 Sector-specific actors and regulation

4.2 Sector impact on low-income households

4.4 Sector challenges

• The Agriculture sector suffers from low productivity, which can be understood by evaluating several drivers across the

value chain (land, inputs, mechanization, extension, aggregation, marketing), including

– Small average plot size per farmer relative to peers, lack of widespread access to improved seeds and fertilizer, weak

irrigation infrastructure, inadequate provision of extension services, low access to agronomic information, and low

producer prices due to lack of bargaining power and poor dissemination of market information

• The government has recently relaxed its regulation of the sector – farmers are able to circumvent the burdensome

(government-controlled) cooperative legislation to self-organize into free-enterprise associations. Export restrictions on

cereals have also been relaxed, enabling farmers to net higher incomes

• However, there is still inadequate public investment in the sector – the government has only dedicated 6% of the

national budget to the sector, falling short of its 10% commitment under the Maputo Declaration

• The great majority of farmers in Tanzania are smallholders – there are estimated to be more than 5 million farming

households in the country

• A majority of smallholders are subsistent agriculturalists – they consume a majority of what they produce and bring a very

small surplus to market

• Tanzania is highly dependent on agriculture for economic output and employment, as it constitutes 27% of GDP and

accounts for ~75% of employment

• Two out of three Tanzanian farmers produce food crops - 85% of cereal production consists of maize and rice (paddy),

which are the two most important crops

• The sector has several stakeholders – inputs (seeds, fertilizer, chemicals) are supplied by major international input

companies and local agro-dealers, production is mostly done by smallholder farmers, with a few large-scale commercial

farms for cash crops (e.g., horticulture, legumes), extension support is provided by the Ministry of Agriculture,

aggregation (where it exists) is done by producer associations, and marketing is done by traders; several local and

international NGOs also play along the value chain

35

Tanzania is highly dependent on agriculture for economic output

and employment, similar to other developing economies in Africa

SOURCE: World Bank (2010); CIA Factbook; team analysis

Other

75

5

20

Agriculture

100% =

2011

Industry

Services

25.59 million

employed

With a strong majority of the workforce employed by agriculture, this sector will be critical to reducing poverty

4.1 AGRICULTURE – SECTOR DESCRIPTION

Mozambique

5%

10%

15%

20%

25%

30%

35%

250 500 750 1,000 1,250 6,000 10,000 50,000

0%

-5%

0

Tanzania

Kenya

Uganda

Zambia

China

South

Africa

Brazil

USA

GNI/Capita

% of agriculture contribution in national GNI Workforce breakdown by sector, %

36

100

90

80

70

60

50

40

30

20

10

0

2020E2015E20102000

The majority of agricultural activity is focused on cereal

production

SOURCE: Kilimo Kwanza; ASDP; ASDS; CAADP Compact. CIA Factbook; FAO (2013)

Market value by

agricultural product

%

Area planted by crop

type

100% = 8.8 million ha

Area planted by

cereal type

100% = 5.8 million ha

70

16

10

4

Maize

Paddy

Sorghum

Millet

Wheat

2010

1

72

15

8

6

Crops

Livestock

Hunting and

forestry

Fishing

2010

100% =

TZS 4.1 trillion

66

11

11

7

Cereals

Pulses

Oil seeds &

oil nuts

Cash crops

Roots & tubers

Fruits &

vegetables

2010

31

Agriculture

Services

Manufacturing/Industry

Key takeaways

Real GDP by sector

%• Agriculture

contributes a

significant share to

GDP, although the

relative GDP

contribution is

projected to

decline over time

• Cereal production

comprises the

largest share of

agricultural

production, with

maize being the

most important

crop

4.1 AGRICULTURE – SECTOR DESCRIPTION

37

The Tanzanian agriculture sector suffers from low productivity

as evidenced by the poor yields in its major crop

SOURCE: Ministry of Agriculture; FAO (2013); FAOSTAT

Tanzania scores at the bottom of its peers in maize yields

Zambia 2,244

Uganda 2,686

Mozambique 854

Tanzania 1,366

Kenya 1,393

Malawi 1,650

Ghana 1,737

Ethiopia 2,137

749

1,667

2,193

1,240

1,871

3,059

2,655

2,499

2008 2012

CAGR

%

-2

4

9

2

7

5

-2

-3

Maize yield

Kg/ha

Key takeaways

• One of the major

impediments to agricultural

growth is the low

productivity of land and

labor

• Maize yields of 1.2 MT/ha

are ~40% lower than

peers’ average

• Tanzania’s maize

productivity has declined

even as peers have

registered large

productivity gains over a 5-

year period

• Key factors driving the

poor performance include

– Low public expenditure

on R&D, inadequate

financing, poor

production techniques,

underdeveloped

markets, poor rural

infrastructure

4.1 AGRICULTURE – SECTOR DESCRIPTION

38

Growth in the agricultural sector is hindered by a number of

bottlenecks along the value chain and beyond

▪ Small arable land

utilization: only

30% of potentially

productive area

under agricultural

production

▪ Limited average

plot size:

smallholders

control 0.9-3.0 ha

on average

▪ Onerous

administrative

procedures:15-

step process to

obtain a land title

▪ Inconsistently

enforced land

rights

▪ Low fertilizer

application: Only 9

kg/ha used, ~40%

lower than peer

average

▪ Weak demand for

improved seeds:

farmers are unable

to purchase even

limited offerings on

market, only

absorbing 40% of

stock

▪ Underdeveloped

capacity of agro-

dealers: lack of

business skills and

unattractive margins

to serve

smallholders

▪ Inefficient

government input

subsidies: late

payments and non-

functioning vouchers

▪ Farmer information

constraints:

inadequate agrono-

mic knowledge on all

aspects of production

▪ Inadequate

extension services:

too little staff with

inadequate resources

and underdeveloped

capacity

▪ Low level of

mechanization: only

24% use animal

traction and 13% use

mechanical power

▪ Budget constraints:

insufficient allocation

and late

disbursement of

funds by government

to extension works

▪ Heavy reliance on

natural elements:

predominantly rain-

fed agriculture is

highly susceptible to

adverse weather

conditions

▪ Unavailability of

long-term storage:

only 1% of farmers

have access, forcing

remainder to sell at

low prices to avoid

spoilage

▪ Cash flow

constraints:

farmers have urgent

need for cash so

can’t afford to hold

produce

▪ Underdeveloped

physical

infrastructure:

dearth of all-weather

roads in rural

regions

▪ Low level of

private investment:

smallholders and

enterprises lack

access to financing

▪ Weak market

linkages:

underdeveloped

relationships

between agro-

processors and

producers,

especially in value-

adding schemes

Ch

all

en

ge

s

▪ Low level of

commercialization:

majority of produce

consumed in the

home

▪ Non-consolidated

aggregation/off-

take: fragmented

producer base with

weak negotiating

power

▪ Poor price

discovery: non-

transparent

commodity pricing

▪ Weak market

linkages:

underdeveloped

relationships

between agro-

processors and

producers

1 432 65

1.1

1.2

1.3

1.4

2.1

2.2

2.3

2.4

3.1

3.2

3.3

3.4

3.5

4.1

4.2

4.3

5.1

5.2

5.3

5.4

6.1

6.2

4.4 AGRICULTURE – SECTOR CHALLENGES

39

Several actors are involved in the agricultural value chain

Private

sector

Govern-

ment

FBO

NGOs

Key value-chain focus

Stakeholder Examples Land Input

Prod-

uction

Sto-

rage

Marke-

ting

Pro-

cessingDescription

Seed and

input

companies,

agro-dealers

Mix of international and local companies

import/produce seed, fertilizer, and crop protection

products; distribution happens at the local level by

agro-dealers

Commercial

farms

Large scale, mechanized crop production and value-

added processing ; could also involve model plots

and outgrower schemes for and knowledge transfer

initiatives to involve smallholders

Traders Small-scale traders purchase commodities at the

farmgate and sell them on to agro-processors (e.g.,

mills, food processors)

Warehouse

receipt

program

Warehouse operators provide infrastructure and tools

for fumigation, storage; and packaging of

commodities. Collateral managers also provide

receipt verification, financing, and deposit insurance .

Development

institutions,

social

enterprises

Organizations provide support to farmers and fund

initiatives all along the value chain, including by

providing inputs, giving agronomic and business skill

training, and enhancing market linkages

Extension

agents

Free locally based government agents providing

farmers with training on an ad hoc basis, including

through field demonstrations and test plots

Farmer

cooperatives,

SACCOs

Producer associations whose objectives include

increasing access to improved inputs, extension

services and market; some organizations, like

SACCOs, have a long history of effectively providing

loans and facilitating access to capital

4.4 AGRICULTURE – SECTOR CHALLENGES

40

Currently, Tanzania is only utilizing

~30% of 37 million hectares of arable land

SOURCE: FAOSTAT

Non-arable

50.5 mil ha (53%)

11

15

20

30

31

41

48

65

Mozambique

Zambia

Kenya

Ghana

Tanzania

Ethiopia

Uganda

Malawi

Share of arable land used under agricultural

production, %

Total arable

land

Million ha

Total Tanzania land

100% = 88.5 million haArable land utilization

100% =

Non-arable

Arable

2011

88,580

58

42

5

14

36

37

16

27

23

49

1

4.4 AGRICULTURE – SECTOR CHALLENGES

41

Key takeaways

3

1

5

17

18

32

36

42

Uganda

Mozambique

Tanzania

Ethiopia

Ghana

Zambia

Kenya

Malawi

SOURCE: Ministry of Agriculture; FAO; FAOStats; IFPRI

8

9

22

29

49

28

30

2

Tanzanian farmers make negligible use of fertilizers on their plots

2007 2011

CAGR

%

-8

-7

11

13

7

15

29

10

Fertilizer usage

Kg/ha

Tanzania has very poor usage of inputs: fertilizer

4.4 AGRICULTURE – SECTOR CHALLENGES

• Although fertilizer use

in Tanzania has gone

up in the past few years,

Tanzanian farmers continue to

apply ~40% less fertilizer/ha

than their peers’ average

usage

• Low fertilizer usage is driven

by a few factors

– Poor access to credit:

both farmers and

importers/wholesalers

suffer from financing gaps

– Farmer information

constraints: inadequate

agronomic knowledge on

proper use of fertilizer for

specific crop types and

ecological conditions

Related to

financing gap2

42

…as they face several challenges in accessing and purchasing

them, despite their many benefits

83

17

100% =

2011

37.2 M ha

Planted area with improved seeds, %

With improved

seeds

Without improved

seeds

Tanzanian farmers make little use of

improved seeds …

SOURCE: FAOStats; team analysis

Tanzania has very poor usage of inputs:

improved seeds

• Demand for improved seed by Tanzanian farmers is diminished

because of number of factors, including

– Lack of smallholder pricing power: fragmentation of farmer

base inhibits negotiating power through bulk purchases

– Inadequate access to financing: credit provision for farmers

and agro-dealers is limited; banks do almost no lending to the

former, and do limited lending to latter via credit guarantees

– Poor government subsidy program administration:

government subsidy payments to agro-dealers are often late and

sometimes subsidy vouchers are not honored at point of

redemption

– Underdeveloped capacity of agro-dealers: low incentive to

serve smallholders because of the high cost of service and lack of

business skills to weather low-margin business

Related to

financing gap

4.4 AGRICULTURE – SECTOR CHALLENGES

2

43

67

33

100% = 5.8 M households

Households receiving extension

advice, %

Extension advice

received

Extension advice

not received

SOURCE: National Sample Census of Agriculture 2007/2008; Wageningen University and Research Center; IFPRI

… and even those receiving them face serious challenges in the

quality and efficacy of services provided

Relatively few smallholder households

have access to extension services…

Tanzanian farmers receive low-quality extension

services to assist them in their cultivation practices

• Extension services are essential to enhancing agricultural

productivity by teaching smallholders farm management skills

including, inter alia, correct land preparation, timely planting, pest and

disease control, and soil nutrient balancing

• Extension in Tanzania is almost entirely financed by the

government via the Ministry of Agriculture Food Security and

Cooperatives (MAFC)

• The provision of adequate extension services is limited by a few

factors, including

– Low budget allocation: insufficient funding to hire an adequate

number of personnel and provide them with resources to carry out

impactful demonstrations and field experiments

– Late budget disbursement: sporadic and often delayed

payments of extension workers and for tools

– Poor capacity: extension workers suffer from low education

levels and weak morale, thus limiting their ability to counsel

farmers

– Weak transport infrastructure: absence of reliable means

(roads, public transport, etc.) for extension workers to reach

farmers

Related to

financing gap

4.4 AGRICULTURE – SECTOR CHALLENGES

3

44SOURCE: National Sample Census of Agriculture 2007/2008; IFAD; Team analysis

1.8%

2.1%

Not stored 16.4%

In locally made traditional structure 33.6%

In sacks/open drum 44.5%

In airtight drum

In improved locally made structure

Few Tanzanian farmers have access to proper storage options …

Method of harvest storage

%

… due to the absence of infrastructure

and financing options

Although 90% of smallholders store their produce, most

use suboptimal conditions and put their commodities at riskRelated to

financing gap

Ideal storage

methods

• Having adequate access to storage

facilities is important because it enables

producers to maintain the integrity of

their surplus produce; post-harvest

losses range from 25 to 35% of yield in

areas where that lack proper facilities

• Storage is also crucial to enable farmers

to hold their post-harvest commodities to

take advantage pricing cycles

• However, a dearth of storage

infrastructure, a lack of access to

credit, and their immediate need for

cash prevents farmers from investing in

storage infrastructure and/or holding on

to their commodities for the desired

length of time

4.4 AGRICULTURE – SECTOR CHALLENGES

4

45SOURCE: National Sample Census of Agriculture 2007/2008; Team analysis

0%

1%

1%

1%

2%

3%

5%

5%

15%

67%

Government regulatory problems

Marketing problems

Cooperative problems

No buyer

Lack of market information

No transport

Crop market too far

Transport cost too high

No problem

Open market price too low

Low prices are the biggest driver of dissatisfaction for farmers

Several challenges remain in redressing

marketing gaps

Farmers experience various marketing

problems when selling their produceRelated to

financing gap

• Most households report that the open

market price for their produce is too low;

this is driven by a number of factors,

including

– Non-consolidated aggregation/off-

take: fragmentation of producer base

leads to weak negotiating power against

traders

– Poor price discovery: inadequate

farmer ability to discern market prices

and drivers

– Weak market linkages: few

relationships between farmers and agro-

processors/other end customers in high-

touch production and marketing

arrangements (e.g., outgrower schemes,

contract farming)

– Government policy: export bans on

staple crops prevent farmers from taking

advantage of higher prices in neighboring

countries

4.4 AGRICULTURE – SECTOR CHALLENGES

5

46SOURCE: Comprehensive Africa Development program (CAADP); TAFSIP

99

1

Share of agro-products processed, %

Not processedProcessed

Tanzania does negligible value addition

to its agro product The challenges to the agro-processing industry are manifold

The level of value addition through agro-

processing in Tanzania is very lowRelated to

financing gap

• Tanzania is exporting unprocessed agro-products when the

agro-processing industry cannot meet domestic demand

• Only an estimated 1% of Tanzania agricultural produce is

processed compared to between 20 and 70% for some

medium-level third-world countries

• The low capacity in agro-processing is driven by a number of

factors, including

– Poor physical infrastructure in rural areas, with a dearth

of all-weather roads

– Limited private-sector participation and a low level of

investment by farmers and agribusiness enterprises,

accentuated by the reluctance of banks to lend for

agricultural and agro-industrial investments

– Limited knowledge of value-adding opportunities and

innovative marketing approaches such as contract farming,

outgrower schemes, warehouse receipts, commodity

exchanges, options trading etc.

4.4 AGRICULTURE – SECTOR CHALLENGES

6

47

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

16,000

0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

12-201311-1210-1109-1008-0907-08

% of the total budget

Total government budget

Total agriculture sector budget

Key takeaways

SOURCE: Calculations based on MAFAP public expenditure database for the URT

Comparison between agriculture sector

budget against total government budget,

TZS Billions

Government spending in agriculture and related services is low

Public expenditure in direct and indirect support

of the agriculture sector has lagged targets

1 Agricultural research, extension services, payment to producers, storage, training, inspection etc.

• The Comprehensive Africa

Agriculture Development program

(CAADP) targets 6% annual

growth in the agricultural real

GDP by allocating 10% of the

national budget to the

agricultural sector1

• However, this is not the case as

the agriculture sector has only

been getting an average of ~6%

of the national budget for the

past 6 years

• TBD

4.4 AGRICULTURE – SECTOR CHALLENGES

6

48

A number of stakeholders are driving several initiatives to

improve value chain dynamics

Description

Southern Agriculture

Growth Corridor for

Tanzania (SAGCOT)

• Facilitating the establishment of linkages between

smallholders and large commercial farms

• Modern irrigation system will increase productivity

Agricultural Sector

Development

Program (ASDP)

• Improvement of farm inputs accessibility

• Construction and rehabilitation of infrastructure

• Promotion of agricultural mechanization

Agro-dealer program

• Improved input use and increased output

• Increased number of traders involved in agribusiness

Marketing

Infrastructure, Value

Addition, and Rural

Finance (MIVARF)

• Kilimo Kwanza (Agriculture First) is an initiative aimed

at mobilizing all sectors of the economy to bring about

an agricultural revolution in Tanzania.

• The pillars of Kilimo Kwanza are: financing, policy,

and regulatory incentives for increased private sector

investments

Rural Micro, Small,

and Medium

Enterprise Support

Program (MUVI)

• Radio Stations used to spread the message regarding

the Muvi programs

• In rural areas, stations took the initiative to get the

local people to assist with the training to interview

people with the aim of covering issues/areas within

the Muvi program

Southern Highlands

Food Systems

Program (SHFS)

Main sponsor (s)

• The Southern Highlands Food Systems Project is

under implementation by FAO in Tanzania, with

funding from Germany

Type

• Improve productivity

and security in the

southern region

• Improve production

and productivity

• Enhance input

access and build

capability

• Increase financing

and development of

market

infrastructure

• Provide financing

services

• Enhance technical

support and

capacity building

4.4 AGRICULTURE – SECTOR CHALLENGES

49

Agenda

SOURCE: Source

Sector analysis – agriculture

Sector analysis and challenge identification

Assessment of financial service needs and gap analysis

Digital finance plus feasibility assessment

Readiness framework

Access to and reach of mobile infrastructure

Adoption and reach of digital finance infrastructure

Role of the government and regulation

Sector analysis – energy

Sector analysis – water

Sector analysis – health

Sector analysis – education

50

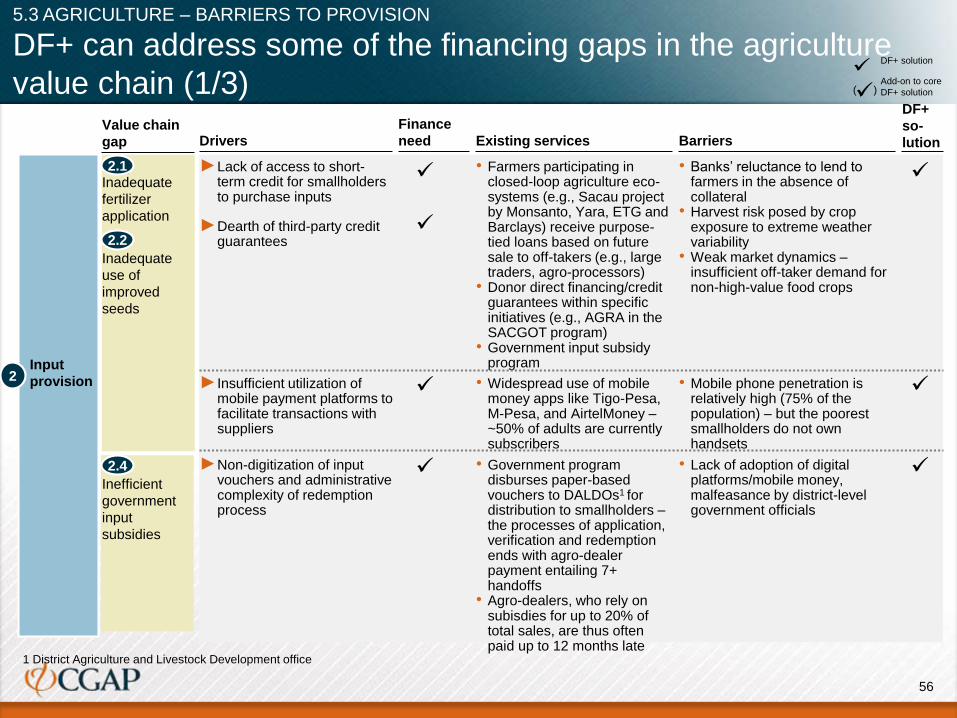

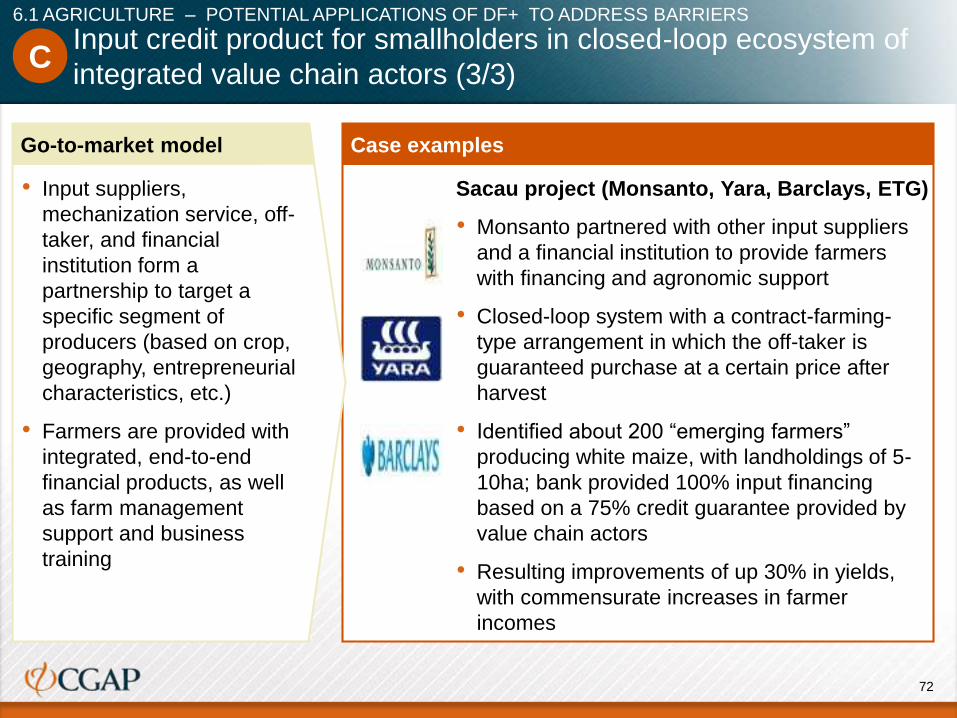

Key takeaways: Agriculture sector financial service need and

gap analysis

AGRICULTURE – FINANCIAL SERVICE NEEDS AND GAP ANALYSIS

5.1 Financial service need along value chain

5.2 Financial gap analysis along value chain

5.3 Barriers to provision of financial products

• Similar to many peer countries in SSA, there is a clear disconnect between the importance of agriculture to the Tanzanian economy

and general access to financing – although agriculture accounts for ~30% of the GDP, only ~10% of commercial lending goes to the

sector

• Even where financial products are offered to farmers, they are only available to a small niche relative to the wider smallholder base –

beneficiaries tend to belong to strong producer associations, grow horticultural or other types of cash crops and have strong relationships

with a monopsonic value chain actor (e.g., outgrower and contract farming schemes with agroprocessors)

• The needs of smallholders are only being met to a limited extent

– Loans: minimal access of credit to farmers; few national banks lend to select producer associations with extremely high collateral

requirements at market rates of 25%; MFIs (e.g., FINCA, Pride) also lend to producer associations, but at high rates of 50-200%,

while village-level moneylenders extend credit at extremely burdensome rates of up to 300%

– Insurance: extremely rare, except for nascent efforts within “closed loop” market ecosystems in which a partnership of value chain

actors (e.g., Sacau project by Monsanto, Yara, Barclays) provide weather-indexed crop insurance bundled with other financial

products (e.g., input credit) and collateralized with warehouse deposits, often only covering the value of inputs (not the entire harvest

value)

– Agronomic, weather, and market information: only 7,000 extension workers nationally, thus providing minimal frequency and

quality of agronomic support to farmers; however, there are a number of mobile-based applications (e.g., Tigo Kilimo by Tigo, by

Kilimo Salama by Snygenta Foundation), directly reaching farmers via helplines and SMS to provide advice on farm management,

weather forecasts, market price information, etc.

• Smallholder farmers and other players have a range of finance-related needs across the value chain, including

– Loans: short and long term lending for acquisition of inputs (seeds, fertilizer, agro nutrients), access to mechanization during plan-

ting (tractor rentals), harvesting once crops are ready (extra labor hire), to market based on pricing cycles

– Insurance: protection against extreme hydrological conditions (e.g., drought, excess rainfall) to recoup investment in inputs and

labor

– Agronomic, weather, and market information: knowledge on farm management best practices (e.g., input application, disease

control), localized weather forecasts, and market prices by crop and geography

– Smallholder farmers/SMEs in the agriculture sector are a low priority segment for most financial institutions due to the

unmanageable risk and high cost-to-serve, low presence of collateral, and variability of harvest performance

51SOURCE: IMF; Central Bank data

30

22

30

24

29

25

44

2831

144

68

101112

15

NigeriaKenyaMozam-

bique

Sub-

Saharan

Africa2

EthiopiaTan-

zania

Malawi GhanaUganda

Agriculture as a share of GDP and commercial bank lending, 20081 , in %

% Lending% GDP

1 2008 reflects latest available data

2 Commercial bank lending across SSA is estimated at <10%, with the exception of Malawi, Tanzania and Uganda

5.1 AGRICULTURE – FINANCIAL SERVICE NEEDS ALONG THE VALUE CHAIN

As in much of SSA, a clear disconnect exists between the importance of

agriculture to the Tanzanian economy and general access to financing

Key takeaways

• Agriculture is a

key driver of

the Tanzanian

economy,

contributing

28% of GDP

• The agriculture

sector has

limited access

to commercial

bank lending:

it receives on

average 2-3

times less

credit than its

fair share

based on GDP

contribution

52

Many of the value chain gaps are related to limitations in the

meeting of smallholder and other actors’ financing needs

The nature of the agricultural sector makes providing financing less desirable

• Unique risks

– High operational and price risks due to weather, disease/pests, makes it hard to

diversify for banks in many monoculture regions

– Seasonal and multiyear cycles

• Time inconsistency

– Lag exists between investment needs and expected revenues

– Need patient capital with a long horizon and a tolerance for risk

• High transaction costs

– Loans are often in small amounts

– Borrowers are often dispersed in remote/rural areas with no distribution access

• Informality leads to a lack of collateral and information

– Absence of land titles or registered assets

– No financial statements or credit score from credit bureau

• Low level of financial literacy

– Limited understanding of the benefits of financial services and products

• Governance

– Substantial government intervention is increasing uncertainty

– Subsidies and repeated debt forgiveness are creating a moral hazard

5.1 AGRICULTURE – FINANCIAL SERVICE NEEDS ALONG THE VALUE CHAIN

53

Financing for staple crops, which constitute the largest share of

Tanzanian production, is especially challenging

SOURCE: Expert interviews; literature review

Markets for staple

crops are often

highly politicized

Staple crops

require significant

economies of

scale to attract

financing

Lack of product

differentiation

makes it harder to

finance staple crop

value chains

• Small producers often compete with larger, more

efficient producers in the country/region

• Scale is often required to ensure quality (e.g.,

through mechanization, storage infrastructure)

• The presence of multiple traders and

intermediaries increases the risk of diversion and

side selling unlike in cash crops, which are more

integrated

• Food reserve purchasing by governments creates

unpredictability

• Legacy of government supply/subsidy of inputs

distorts the market but is hard to reform

5.1 AGRICULTURE – FINANCIAL SERVICE NEEDS ALONG THE VALUE CHAIN

54

Smallholder farmers and other value chain players have a range

of finance-related needs across the agricultural value chain

SH = smallholder

AD = agro-dealer

EA = extension agents

PS = other private sector

Gov = government

1 432 65

Fin

an

cin

g n

ee

ds

• PS: long-term

loans to private

enterprise to:

a) build agro-

processing plants;

and b) on-lend to

farmers

participating in

outgrower/contract

farming schemes

• SH: market

information

systems to enable

easy price

discovery

• SH: depository

accounts

(checking and

saving) to park

cash following

commodity sales

• SH: payment

receipt for

commodity

transactions

• SH: short-term

loans and credit

guarantees to

store commodities

until ideal market

period

• PS: long-term