digital finance use cases

TRANSCRIPT

Digital Finance: Use Cases

Paris, 10 March 2016

Case Study: DigiLand

Each group is a consulting team; and should develop ideas/concepts to drive financial inclusion for the following audiences:

1. Banks and/or MFIs: what new services should banks innovate to add clients/revenue?

2. Government: what digital capabilities should be leveraged that improve social safety nets and make links to financial inclusion?

3. MNOs (and their mobile payment subsidiaries): what are promising new services to improve market share and add new revenue?

4. FinTech Start-ups: what opportunities could be pursued in digital finance and which partners should they prioritize?

2

Digital Finance+The use of digital financial services to make basic, essential services

and utilities - in energy, health, education, and water - more accessible.

Finance is not an end itself but a means to help solve significant development challenges in order to improve the lives of the poor.

PAYG Solar – Off-Grid:ElectricCustomer signs up for “solar-as-a-service” contract

Technician installs solar system at customer’s home

Customer enjoys low-risk, prepaid energy services

Customer enters code, product unlocks for prepaid time

Automatically disables service when credit expires

Customer pre-pays for energy days via mobile money

Receives unique usage code via SMS

5

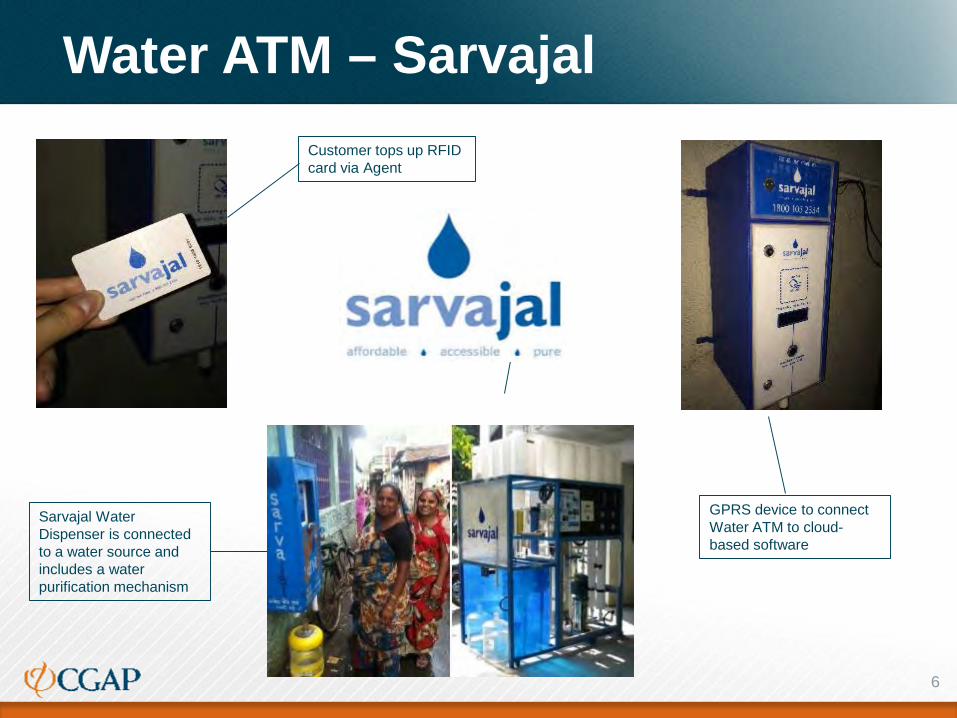

Water ATM – SarvajalCustomer tops up RFID card via Agent

Sarvajal Water Dispenser is connected to a water source and includes a water purification mechanism

GPRS device to connect Water ATM to cloud-based software

6

Digital Finance Plus – Sector Overview

• >100 DF+ Enterprises across energy, water,

health, agriculture, education

• High concentration in East Africa

• Startups drive innovation, but need digital

payments and distribution partners

• Massive un-tapped markets, limited

competition

• Grants/risk capital for model demonstration• Equity investment, innovations in off-balance-

sheet financing and structured debt• Energy/water access policies that embrace DF+

business models

• Improved mobile money integration tools (APIs)

What is needed?

Digital Credit9

Digital Credit

Conventional Credit

People’s Judgment Automated

In Person Remote

Days Instant

sending information & payments

risk management process

time to take decisions

Definitions

10

Small Business/Farmer

Variety of Digital Credit Approaches

Individual

Direct to Individuals

…. who may also run small businesses or farm

• Credit risk on individual• Initially reliance on alternative data• Track record builds shifts to behavioral data

1

Lender + Its Partners

Digital credit

11

Variety of Digital Credit Approaches

Individual Small Business

Indirect: Merchant Acquirer or Distributor• Credit risk on business volumes• Embedded in distribution relationship• Collections from electronic sales

2

Lender + Its Partners

Merchant Acquirer or Distributor

Digital credit

12

Variety of Digital Credit Approaches

Individual Farmer

Indirect: Value Chain Aggregator• Credit risk on business volumes• Embedded with aggregator relationships

3

Lender + Its Partners

Value Chain Aggregator

Digital credit

13

M-Shwari: a savings and loan bank account

exclusively accessed through M-PESA

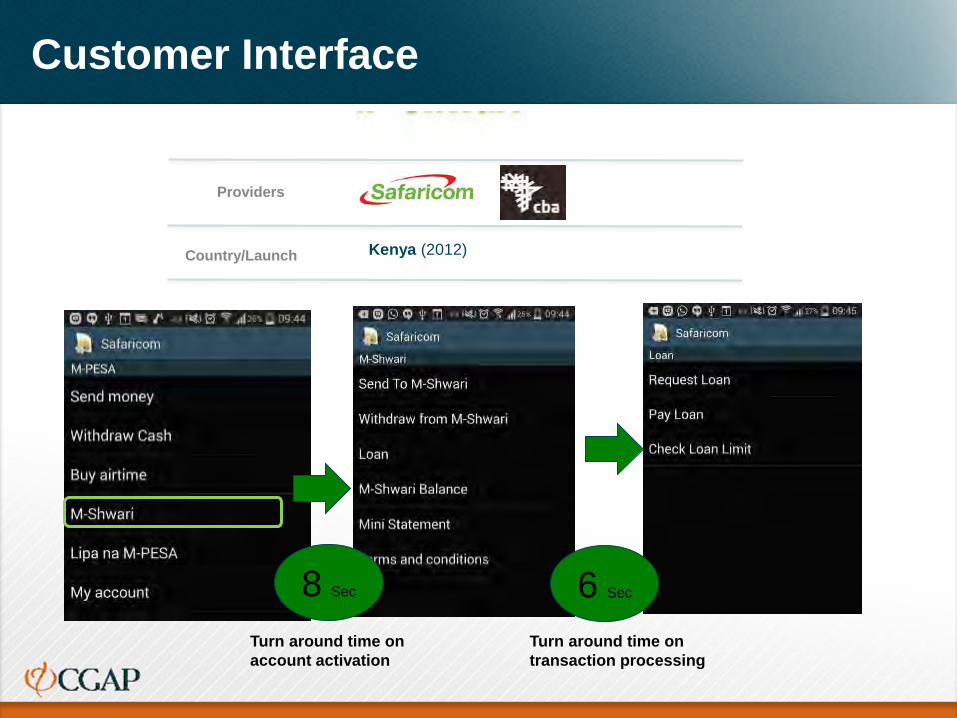

Customer Interface

Kenya (2012)Country/Launch

Providers

.

8 Sec

Turn around time on account activation

6 Sec

Turn around time on transaction processing

Instantly opened

Interest bearing, 2 – 5%

Insured

Only accessible via M-PESA

12

34

4 REASONS FOR HCD IMPACT: M-Shwari Savings Account

Instantly opened

Interest bearing, 2 – 5%

Insured

Only accessible via M-PESA

12

34

4 REASONS FOR HCD IMPACT: M-Shwari Savings Account

Instantly opened

Interest bearing

Insured

Only accessible via M-PESA

12

34

4 REASONS FOR HCD IMPACT: M-Shwari Savings Account

Interest bearing, 2 – 5%

Instantly opened

Interest bearing

Insured

Only accessible via M-PESA

12

34

4 REASONS FOR HCD IMPACT: M-Shwari Savings Account

Interest bearing, 2 – 5%

Fast– 6 seconds turnaround, credit scoring based on MNO data

Small – Average $30

Short-term– 30 day loan (7.5% facilitation fee)

1

2

3

4 REASONS FOR HCD IMPACT: M-Shwari Loan

Fast– 6 seconds turnaround, credit scoring based on MNO data

Small – Average $30

Short-term– 30 day loan (7.5% facilitation fee)

1

2

3

4 REASONS FOR HCD IMPACT: M-Shwari Loan

Fast– 6 seconds turnaround, credit scoring based on MNO data

Small – Average $30

Short-term– 30 day loan (7.5% facilitation fee)

1

2

3

4 REASONS FOR HCD IMPACT: M-Shwari Loan

Loan Uptake

Total Kenyans with personal

bank loansQ1 2013

M-Shwariactive loans

Q4 2014

• Total of $782 million disbursed (about 26m loans)

• Non-performing loans about 2%

700k

1.8m63,000

loans disbursed

daily

Source: FinAccess 2013, CBA 2014

M-Shwari has catapulted CBA from focus on narrow elite into mass market

banking

Prior to M-Shwari, CBA had:

Just 89,000 loan accounts

$20,000 average deposit balance

Children missed school 5 times in one year due to shortfall in school fees

August 2012 October 2013

Eldest daughter misses important

exams due to shortfall of $40

$250

$200

$150

$50

Monthly income

Source: Kenya Financial Diaries

M-Shwari offers easy access to small amounts of liquidity in a way that fits how low-income people think about finances.

“My son was bleeding a lot from the nose and I was just

back from the market and had used all of the money. I

needed $12 and that money helped a lot.”

“I am in transport business. Not all the time do I have

money so I can borrow money to help out my drivers when

they are caught by the police.”

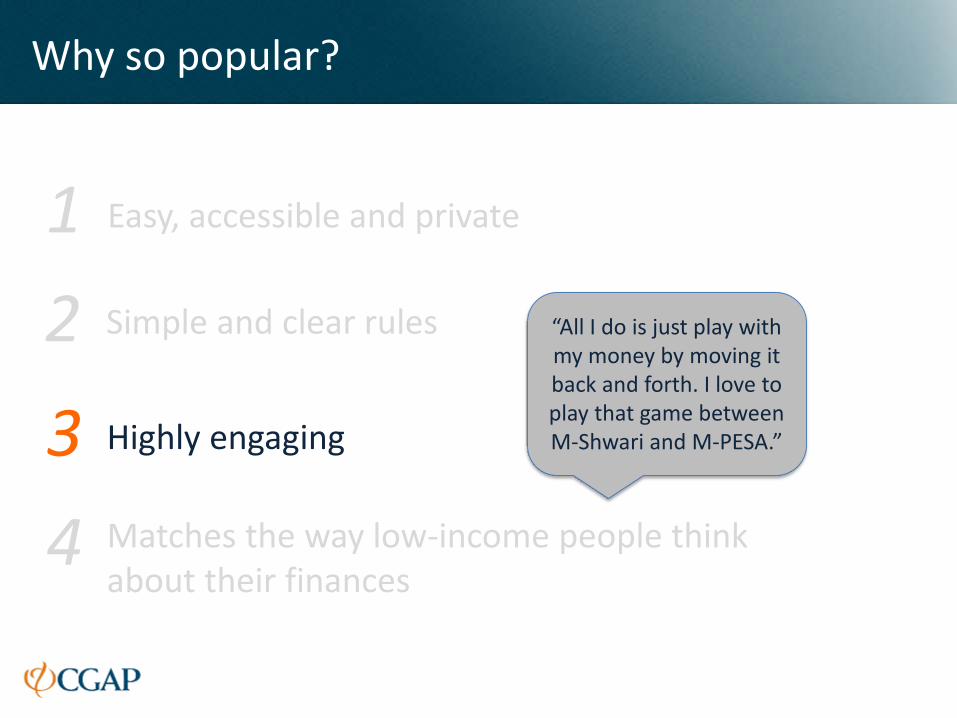

Easy, accessible and private

Simple and clear rules

Highly engaging

Matches the way low-income people think about their finances

12

34

4 REASONS FOR HCD IMPACT: Why so popular?

Easy, accessible and private

Simple and clear rules

Highly engaging

Matches the way low-income people think about their finances

12

34

4 REASONS FOR HCD IMPACT: Why so popular?

Easy, accessible and private

Simple and clear rules

Highly engaging

Matches the way low-income people think about their finances

12

34

4 REASONS FOR HCD IMPACT: Why so popular?

“All I do is just play with my money by moving it back and forth. I love to play that game between M-Shwari and M-PESA.”

Easy, accessible and private

Simple and clear rules

Highly engaging

Matches the way low-income people think about their finances

12

34

4 REASONS FOR HCD IMPACT: Why so popular?

Digital Credit: A Global Trend

Tanzania

Zimbabwe

China

Mexico

Rwanda

PhilippinesGhana

Pakistan?

ChileDRC

Uganda Kenya

NigerVenezuela

34

Merchant Solutions35

In Kenya, just 1% of expendituresare made electronically

(Even though 2/3 of the population are active mobile money users)

Based on 300 low-income households, Kenya Financial Diaires

Safaricom struggles with activity rates amongst merchants

Only 16% of merchants are active

37

Greater recognition that digital payments

are a “hard sell” to small merchants

who have other needs and challenges

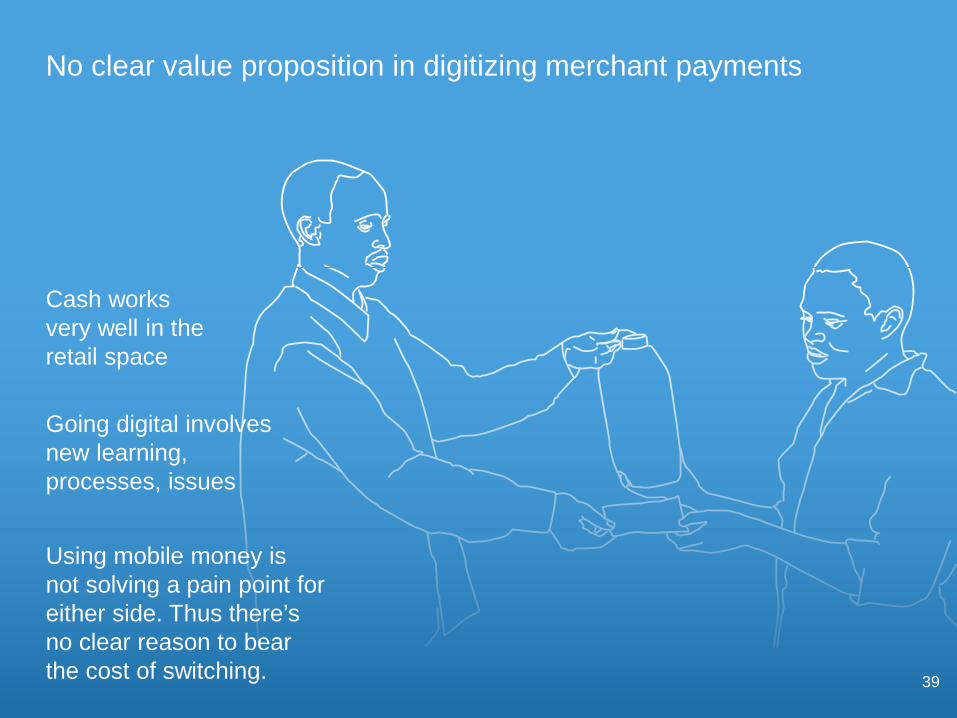

No clear value proposition in digitizing merchant payments

Using mobile money is not solving a pain point for either side. Thus there’s no clear reason to bear the cost of switching.

Cash works very well in the retail space

Going digital involves new learning, processes, issues

39

But merchants have pain points that digital can address

If providers offer some of these features in a bundled product, merchants consistently say they would use it.

MSMEs struggle with basics• Customer Relationship Management

in a highly competitive space• Bookkeeping and accounting• Sales tracking and employee monitoring• Business intelligence• Inventory management• Payment to suppliers• Store credit / layaway for customers• Access to capital

Merchant needs consistent across countries

• CRM• Loyalty• Promotions• Store credit• Layaway

• Sales tracking• Accounting• Staff tracking• Peer stats• Forecasting

• Inventory management

• Paying suppliers• Working capital

Customer relationships

Business intelligence

Inventory and capital

$

41

Customer relationship management

43

Customer relationship management

If you give customers a special incentive to come on their birthday, 40% will come in to redeem their gift

44

$010010010110101001011101100101011101000

Inventory and Capital

Digitizing FMCG suppliers creates new ways to incentivize both customers and merchants

The working capital loan factor is very strong

Merchants much more willing to push digital payments if linked with working capital loan

$ $

46

Early proof points show that offering VAS does drive transaction volumes

Change in transaction volume with Value Added Services in place

Source: Kopo Kopo Kenya and CGAP analysis

Could store credit be the killer app?

Merchant Acquirer may already extend credit to the small business

Individuals sometimes need credit from the small businesses they visit

“Can I pay next week?”

Small businesses need to stay in business and so will extend credit to individuals

A formal lender stands to gain vetted customers because of the small business’ credit history reports. This could remove store credit from merchants’ worries and provide a more reliable, private source of credit to customers.

“Let me check my records.”

RELIABLE!

✔

“Me too?”

$

Merchants consistently say they would use these features.

With these features digital payment acceptance would naturally increase

CRM

Sales tracking

Inventory management

Customer relationships

Business intelligence

Layaway

Loyalty Promotion

Store credit

Inventory and capital

Working capital

Paying suppliers $

Accounting

Staff tracking

Peer stats

Forecasting