digital payments strategy for u.s. retail banks - cognizant · digital payments strategy for ... at...

TRANSCRIPT

• CognizantReports

cognizant reports | september 2015

DigitalPaymentsStrategyforU.S.RetailBanks

The digital transformation of payments has put power in the hands of the customer and allowed nimble-footed nonbank competitors to create a potential threat to retail banks’ domination by provid-ing mobile apps to carry out transactions. Banks will not only need to provide strong payments offerings, but do so by embracing a mobile-centric app and open API-based approach.

cognizant reports 2

ExecutiveSummaryDigitization is transforming banking products and services that have remained unchanged for sev-eral decades. It can be argued that no other ser-vice has been impacted as much by this phenom-enon as payments, a traditional stronghold for retail banks. By empowering the consumer, digi-tization has allowed nonbank players to threaten banks’ hegemony in the area.

Digital payments are a direct result of the digitiza-tion of almost all types of payments. They cover all payments and transfers made through electronic formats, including online payments, mobile pay-ments and crypto-currencies through instruments such as mobile wallets, digital wallets and contact-less cards. These innovations are fairly recent and consumer adoption levels in the U.S. are low as of now but are expected to grow. A surge in nonbank activity in the digital payments arena has meant that the marketplace is currently characterized by a fragmentation of solutions and platforms, with a clear winner yet to emerge. Banks, however, seem to have taken a wait-and-watch approach to digital payments. This will need to change, as millennials and gen-X-ers emerge as the leading adopters of mobile payments; banks need to be prepared to attract and retain this key demographic. To this end, they need to adopt technologies and strat-egies that will allow them to maintain their rele-vance in the payments market.

At the heart of the digital revolution in payments sits the smartphone. With its pricey real estate up for grabs, nimble-footed nonbank players, unhin-dered by legacy systems, have been quick to seize the opportunity. Along with successful disruptors such as PayPal and Square, tech giants such as Google, Apple and Facebook have made inroads into the payments landscape and are looking to push banks into the payments back office. Banks need to catch up with the nonbank competitors. However, they can build on the inherent strengths of the banking system. These include extensive infrastructure, deep customer relationships, mul-tichannel capabilities and a strong focus on data security and privacy. The go-forward strategies of banks need to consider crucial strategic and tech-nological aspects of the digital transformation:

• Make payments a key part of the larger digital transformation initiative.

• Create payment offerings based on an open API infrastructure and a collaborative approach.

• Leverage social, mobile, analytics and cloud (aka SMAC Stack) capabilities.

• Focus on understanding customer payment behavior.

• Create a secure payments environment that also protects consumer privacy.

• Embed Code HaloTM

thinking1 to derive unique

customer insights from multiple channels and differentiate offerings.

• Employ an agile approach to product develop-ment to enable fast and continuous evolution.

Digital:TheThreatandOpportunityforU.S.BanksDigital’sImpactonPaymentsSmartphones have changed the banking habits of Americans. This is especially true for the younger demographics. The Federal Reserve found that 22% of all mobile users made a mobile payment. Among the age groups of 18-29 and 30-34, mobile payments were made by 34% and 31% users, respectively, in 2014.

2 These numbers are impressive, but mobile-

based payments currently represent a minuscule portion of the mammoth $16 trillion U.S. consumer payments market. Nevertheless, contactless pay-ments are the fastest growing mobile payment type, set to grow at 56% annually between 2014 and 2019, according to Forrester.

3 Mobile in-store pay-

ments are expected to grow at 154% CAGR between 2013 and 2018, reaching $189 billion.

4

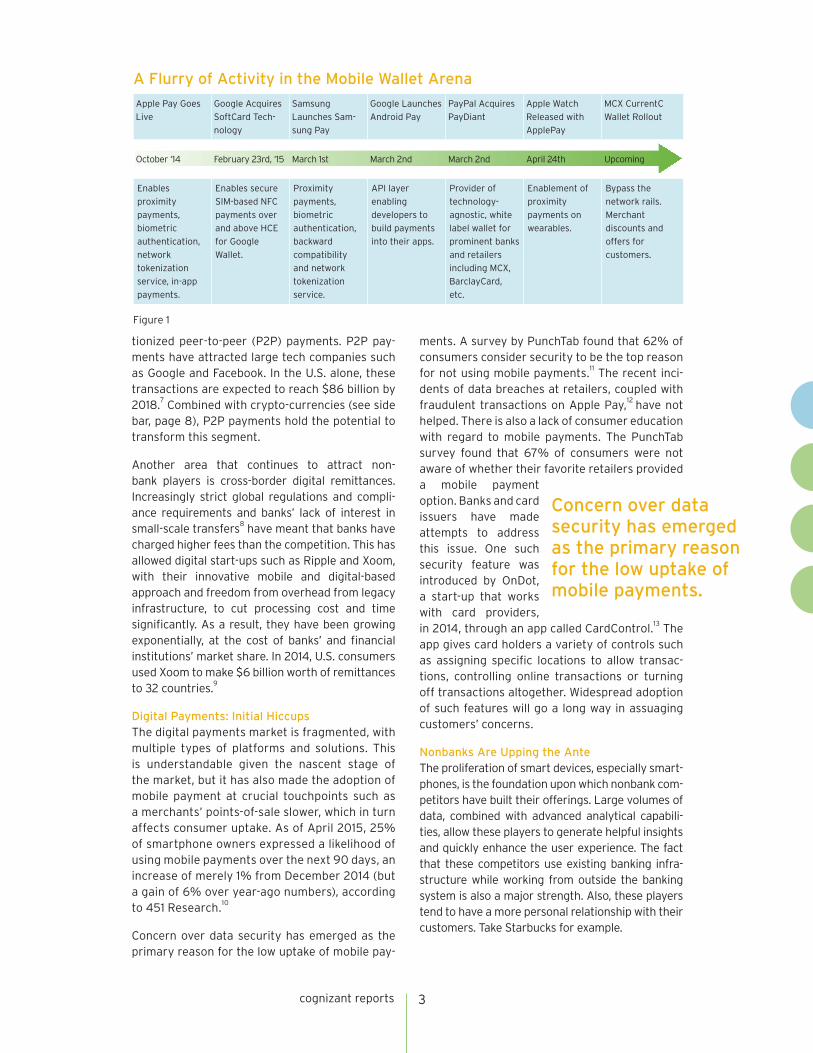

Smartphone makers head the nonbank seg-ment in the mobile payments landscape, led by Google (Google Wallet) and Apple (Apple Wallet). Given their size and reach, Apple and Google have been able to recruit a large num-ber of consumers in a very short time. The bus-tle of activity (see Figure 1) in the mobile wallet space shows how serious these companies are about digital payments.

Digital’s impact is pervasive across payment types. In digital bank transfers, for example, digi-tal technology is allowing start-ups to reduce the time taken for check transfers.

5 Meanwhile, U.S.

households are increasingly using e-bill payment systems, which accounted for 23% of total bills presented in 2014.

6

Social payments are the best example of how digital has transformed payments. By allowing people to transfer small amounts to each other through their mobile phones, digital has revolu-

cognizant reports 3

tionized peer-to-peer (P2P) payments. P2P pay-ments have attracted large tech companies such as Google and Facebook. In the U.S. alone, these transactions are expected to reach $86 billion by 2018.

7 Combined with crypto-currencies (see side

bar, page 8), P2P payments hold the potential to transform this segment.

Another area that continues to attract non-bank players is cross-border digital remittances. Increasingly strict global regulations and compli-ance requirements and banks’ lack of interest in small-scale transfers

8 have meant that banks have

charged higher fees than the competition. This has allowed digital start-ups such as Ripple and Xoom, with their innovative mobile and digital-based approach and freedom from overhead from legacy infrastructure, to cut processing cost and time significantly. As a result, they have been growing exponentially, at the cost of banks’ and financial institutions’ market share. In 2014, U.S. consumers used Xoom to make $6 billion worth of remittances to 32 countries.

9

DigitalPayments:InitialHiccupsThe digital payments market is fragmented, with multiple types of platforms and solutions. This is understandable given the nascent stage of the market, but it has also made the adoption of mobile payment at crucial touchpoints such as a merchants’ points-of-sale slower, which in turn affects consumer uptake. As of April 2015, 25% of smartphone owners expressed a likelihood of using mobile payments over the next 90 days, an increase of merely 1% from December 2014 (but a gain of 6% over year-ago numbers), according to 451 Research.

10

Concern over data security has emerged as the primary reason for the low uptake of mobile pay-

ments. A survey by PunchTab found that 62% of consumers consider security to be the top reason for not using mobile payments.

11 The recent inci-

dents of data breaches at retailers, coupled with fraudulent transactions on Apple Pay,

12 have not

helped. There is also a lack of consumer education with regard to mobile payments. The PunchTab survey found that 67% of consumers were not aware of whether their favorite retailers provided a mobile payment option. Banks and card issuers have made attempts to address this issue. One such security feature was introduced by OnDot, a start-up that works with card providers, in 2014, through an app called CardControl.

13 The

app gives card holders a variety of controls such as assigning specific locations to allow transac-tions, controlling online transactions or turning off transactions altogether. Widespread adoption of such features will go a long way in assuaging customers’ concerns.

NonbanksAreUppingtheAnteThe proliferation of smart devices, especially smart-phones, is the foundation upon which nonbank com-petitors have built their offerings. Large volumes of data, combined with advanced analytical capabili-ties, allow these players to generate helpful insights and quickly enhance the user experience. The fact that these competitors use existing banking infra-structure while working from outside the banking system is also a major strength. Also, these players tend to have a more personal relationship with their customers. Take Starbucks for example.

Apple Pay Goes

Live

Google Acquires

SoftCard Tech-

nology

Samsung

Launches Sam-

sung Pay

Google Launches

Android Pay

PayPal Acquires

PayDiant

Apple Watch

Released with

ApplePay

MCX CurrentC

Wallet Rollout

October ‘14 February 23rd, ‘15 March 1st March 2nd March 2nd April 24th Upcoming

Enables

proximity

payments,

biometric

authentication,

network

tokenization

service, in-app

payments.

Enables secure

SIM-based NFC

payments over

and above HCE

for Google

Wallet.

Proximity

payments,

biometric

authentication,

backward

compatibility

and network

tokenization

service.

API layer

enabling

developers to

build payments

into their apps.

Provider of

technology-

agnostic, white

label wallet for

prominent banks

and retailers

including MCX,

BarclayCard,

etc.

Enablement of

proximity

payments on

wearables.

Bypass the

network rails.

Merchant

discounts and

offers for

customers.

Figure 1

AFlurryofActivityintheMobileWalletArena

Concernoverdatasecurityhasemergedastheprimaryreasonforthelowuptakeofmobilepayments.

cognizant reports 4

striking then that 53% of respondents in the Teme-nos survey said that an overhaul of IT systems was unlikely at their organizations unless regulators forced their hand.

19 Nevertheless, some banks such

as JP Morgan have acknowledged the threat posed by the digital disruptors and are looking at ways to improve their services and offerings.

20

WhyDigitalPaymentsMatterandHowBanksCanStayRelevantThe fact that banks need to compete to hold on to their payments revenue base is a given. How-ever, digital will open up a host of possibilities if banks are able to get it right. To begin with, the ubiquity of a mobile device will increase the num-ber of interactions customers have with banks, allowing banks to understand their needs better. By offering a bouquet of payment services such as mobile, mobile wallets, P2P transfers, PoS mobile card readers and international remittances, banks stand to unlock new high-growth opportunities through increased transactions, in the form of fees charged. Creating tailored payment solutions will also allow banks to reach out to the unbanked and the underbanked, thus increasing their reach. These could include mobile money transfer ser-vices – such as M-Pesa – which have been success-ful in the developing world.

21 Another example is

the American Express Bluebird GPR cards aimed at the unbanked population, which have been sold at Walmart since 2012.

22 Simultaneously, banks

should look to understand their customers’ digital behavior and extend value-added services to meet specific needs across the banking value chain.

StartCompetingIf banks are to win against nonbank players, they need to create compelling and competi-tive digital payment offerings. The building

Going by the latest numbers, 13 million of its customers are using the company’s mobile app, with 7 million mobile transactions per week.

14 Its

recent pilot for mobile order and pay in Portland, OR, was also a success and is expected to increase its reach in mobile payments and customer loy-alty.

15 Starbucks’ success was a bolt from the blue

for industry observers; but it is due mainly to two crucial factors: its technology infrastructure that supports mobile payments and a loyal customer base. Retail giant Walmart now offers inexpen-sive full service prepaid accounts from American Express aimed at more than 70 million unbanked and underbanked Americans.

16

Although mobile payments uptake is slow, cus-tomers have shown a positive attitude toward nonbanks. A survey by Cisco found that, on aver-age, 80% of respondents would trust a nonbank for traditional banking products such as checking accounts, credit cards and mortgages.

17 A survey of

senior banking executives by Temenos18

found that 23% of respondents believe these data-driven and agile competitors from outside the financial sector are banks’ most significant competition. Yet, banks have so far adopted a wait-and-watch approach to nonbank competition. This may be due, in part, to the fact that the digital payments ecosystem is crowded at present and it is uncharted territory for banks. However, such an approach does not bode well as it increases the threat of disintermediation and the possibility of nonbanks becoming the face of consumers’ financial activities, while banks are pushed to a less lucrative, back-office role.

Nonbanks do not face the handicaps of growing regulations, legacy systems and processes, and a multiplicity of systems and processes. As a result, they are better placed to focus on improving cus-tomer experience on mobile devices and online. It is

MillennialsandGen-XLeadMobilePaymentAdoption

Source: Consumers and Mobile Financial Services 2015, March 2015, Federal ReserveFigure 2

Use of mobile payments in the past 12 months by agePercentages, except as noted

Age group 2011 2012 2013 2014

18-29 20 26 28 34

30-44 16 18 21 31

45-59 8 9 13 16

60+ 5 8 7 7

Total 12 15 17 22

Number of respondents 2,002 2,291 2,341 2,603

Note: Percentages are of those in each group who have mobile phones.

cognizant reports 5

FocusonCreatingaDelightfulCustomerExperienceThe entry of the new competitors makes it imper-ative for banks to focus on creating a banking experience built around their customers’ payment behavior. To this end, banks need to eliminate pro-cess silos to create a unified view of every cus-tomer’s activities across channels. Banks need to realize that their success in the battle for digital payments will depend on their ability to match the seamless, elegant and simplified user experience offered by the likes of Google and Apple.

BuildonCoreCompetenciesIn a digitized payments landscape, banks will have to adopt a start-up-like approach to under-standing the customer, building compelling cus-tomer experiences and offering value-added services. The key here is customer data, which banks are uniquely placed to derive insights from. They are in a position to offer personal-ization of experience, and contextual offers and coupons. Banks could also generate new reve-nue streams by extending data services leverag-ing aggregated anonymized data and by building new and innovative products through big data analytics-enabled insights.

A comprehensive mobile wallet strategy will fit neatly into a bank’s digitization strategy and pro-vide substantial benefits (see Figure 3). Such a wal-

blocks of such an offering will have to be part of banks’ broader digital-first strategy, with a focus on creating an omnichannel banking experience. For competing with nonbanks, banks’ greatest strengths will be their cus-tomer relationships, focus on security and mul-tichannel capabilities.

DemographicFactorsOne key feature of the U.S. payments landscape is the deep penetration of debit and credit cards. The U.S. has more than 160 million card-holders.

23 This adds to retailers’ disinclination

to move to a new form of digital payment, and in turn affects customer uptake. However, the leading adopters of mobile payments are the millennial and gen-X demographics (see Figure 2, previous page). Going forward, these will be the customers shaping digital payments. More-over, this demographic is also more digitally inclined, craves personalization and is more likely to be frustrated with their primary banks than other age groups.

24 Very soon, these

customers will form the largest share of banks’ revenues.

Ifbanksaretowinagainstnonbankplayers,theyneedto

createcompellingandcompetitivedigitalpaymentofferings.

TheMobileWalletAdvantage

Source: Cognizant Figure 3

Cross-Sell/Up-Sell

Compete with Digital

Disruptors

Access to New and Richer Data Sets

Mobile Key Componentof Digital Banking Strategy

Mass Personalization

New Revenue Streams

Realize True 360o View of Customer

Offer True Omnichannel

Experience

Win Over the Millennials

Why a Bank Mobile Wallet?

Enable Data-Driven Contextual Services

cognizant reports 6

Money and clearXchange for enabling seamless domestic fund transfers. U.S. Bank’s partnership with Western Union

26 is an example of how banks

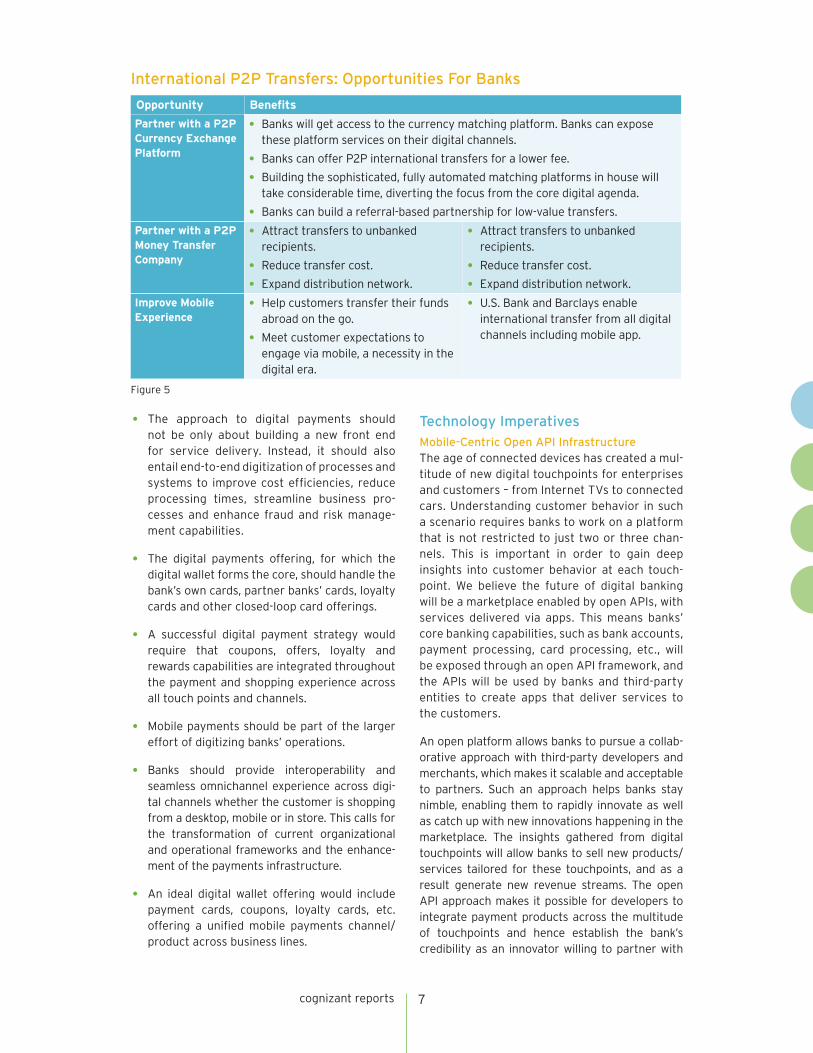

can tackle the regulatory maze of international payments. The service is available to customers who meet the eligibility criteria set by the bank and allows money transfers to over 200 countries. Figure 5 (next page) gives a view of what banks can gain by providing international P2P transfers.

The key considerations for banks can be summed up as follows:

• Although at a nascent stage, the digital pay-ments market is growing fast. The time is right for banks to start considering strategic options to tackle nonbank competitors.

• In the face of growing nonbank competition, banks must strengthen relationships with the younger generations.

• For a quality digital payments offering, banks should enable big data analytics capabilities by leveraging existing data sets, tapping into new data sets enabled by mobile and the Internet of Things, and purchasing external third-party data to deliver contextual and real-time cus-tomer experiences.

• Banks should leverage social media capabili-ties into the payment ecosystem to develop new payment products; and then tap into the treasure trove of information offered by social media platforms to enhance payment experi-ences and promote and market these products.

let would need to be open, modular, flexible and scalable to add card products from issuers and merchants and adopt new payment methods. Banks should also use in-house capabilities and partner with external service providers to add new features and value-added services. Apart from providing their own mobile wallets, banks should also consider actively participating in prominent e-wallets in the market. This would ensure that they do not lose out on a share of the digital payments traffic coming through these wallets. More importantly, a mobile wallet allows banks to embed more digital touch-points in the mobile commerce experience, which in turn will create opportunities for:

• New data sources.

• Better understanding of the customer, leading to better servicing and selling capabilities.

• Richer customer experience.

• New services.

• New revenue streams

Similarly, a simplified, cost-effective and fast domestic (see Figure 4) and international P2P offering will allow banks to gain a greater share of digital payments. A strong P2P offering will allow banks to reach out to a large base of domestic and immigrant populations looking to transfer money to their friends and families overseas.

25 So far, very

few U.S. banks have been willing to use mobile as a channel in transfers. For domestic P2P transfers, banks could leverage P2P networks such as Pop-

Focus Area Key Use Cases

Improve Ease of Use

• In-app calculator to split the bill and add a tip.

• Pay phonebook contacts or social media contacts.

• Pay nearby recipients not in contact list.

• Initiate money transfer in social media.

• Request money from friends.

• Enable B2C payments through P2P platform (Example: Bank of America – Digital Disbursements).

Embed Social Experience

• Personalized messages while sending or requesting payments (ability to comment, send a thank-you note or a personalized e-mail).

• Buy e-gift vouchers and send to friends.

• Donate to charity.

Security and Control

• Secure access using biometrics.

• Limit-based security features.

• Security PIN/OTP for redeeming money.

DomesticandInternationalP2POffering

Figure 4

cognizant reports 7

TechnologyImperativesMobile-CentricOpenAPIInfrastructureThe age of connected devices has created a mul-titude of new digital touchpoints for enterprises and customers – from Internet TVs to connected cars. Understanding customer behavior in such a scenario requires banks to work on a platform that is not restricted to just two or three chan-nels. This is important in order to gain deep insights into customer behavior at each touch-point. We believe the future of digital banking will be a marketplace enabled by open APIs, with services delivered via apps. This means banks’ core banking capabilities, such as bank accounts, payment processing, card processing, etc., will be exposed through an open API framework, and the APIs will be used by banks and third-party entities to create apps that deliver services to the customers.

An open platform allows banks to pursue a collab-orative approach with third-party developers and merchants, which makes it scalable and acceptable to partners. Such an approach helps banks stay nimble, enabling them to rapidly innovate as well as catch up with new innovations happening in the marketplace. The insights gathered from digital touchpoints will allow banks to sell new products/services tailored for these touchpoints, and as a result generate new revenue streams. The open API approach makes it possible for developers to integrate payment products across the multitude of touchpoints and hence establish the bank’s credibility as an innovator willing to partner with

• The approach to digital payments should not be only about building a new front end for service delivery. Instead, it should also entail end-to-end digitization of processes and systems to improve cost efficiencies, reduce processing times, streamline business pro-cesses and enhance fraud and risk manage-ment capabilities.

• The digital payments offering, for which the digital wallet forms the core, should handle the bank’s own cards, partner banks’ cards, loyalty cards and other closed-loop card offerings.

• A successful digital payment strategy would require that coupons, offers, loyalty and rewards capabilities are integrated throughout the payment and shopping experience across all touch points and channels.

• Mobile payments should be part of the larger effort of digitizing banks’ operations.

• Banks should provide interoperability and seamless omnichannel experience across digi-tal channels whether the customer is shopping from a desktop, mobile or in store. This calls for the transformation of current organizational and operational frameworks and the enhance-ment of the payments infrastructure.

• An ideal digital wallet offering would include payment cards, coupons, loyalty cards, etc. offering a unified mobile payments channel/product across business lines.

Opportunity Benefits

Partner with a P2P Currency Exchange Platform

• Banks will get access to the currency matching platform. Banks can expose these platform services on their digital channels.

• Banks can offer P2P international transfers for a lower fee.

• Building the sophisticated, fully automated matching platforms in house will take considerable time, diverting the focus from the core digital agenda.

• Banks can build a referral-based partnership for low-value transfers.

Partner with a P2P Money Transfer Company

• Attract transfers to unbanked recipients.

• Reduce transfer cost.

• Expand distribution network.

• Attract transfers to unbanked recipients.

• Reduce transfer cost.

• Expand distribution network.

Improve Mobile Experience

• Help customers transfer their funds abroad on the go.

• Meet customer expectations to engage via mobile, a necessity in the digital era.

• U.S. Bank and Barclays enable international transfer from all digital channels including mobile app.

InternationalP2PTransfers:OpportunitiesForBanks

Figure 5

cognizant reports 8

need for a Code Halo approach becomes more important. The proliferation of wearable technolo-gies such as smartwatches, glasses and health tracking devices will allow banks greater insights into their customers’ lives than ever before. At present, running algorithms on customer pay-ment data is allowing banks to identify patterns of spend behavior. CapitalOne

32 uses algorithms on

customer card transactions to determine where else customers of a given retailer are most likely to spend money. Similarly, American Express

33 uses

data from 90 million cards in over 125 countries to gauge the spending behavior of consumers and businesses and track developing trends. Going for-ward, Code Halos will allow banks to track evolv-ing customer habits and preferences. These will in turn enable banks to offer personalized products and services based on channel usage and payment behavior. Importantly, this will allow banks to com-pete on code and differentiate their offerings from the digital disruptors.

FocusonTokenization,SecurityandPrivacyTo address the security concerns related to digi-tal payments, it is imperative that the two primary members of the ecosystem, merchants and con-

developers among millennials and gen-X custom-ers used to the experience offered by Google and Apple.

In an open ecosystem, it will be up to the customer to choose the servicing apps of the bank or a third-party provider. The open nature of the ecosystem means banks will have to compete harder to retain customers, but it also gives them the best chance to fight the constantly innovating digital disrup-tors. Banks will be able to launch their own app stores, driving traffic away from the Google and Apple platforms. Early successful adopters of open APIs include Visa, MasterCard, PayPal, Dwolla and the payments gateway, Braintree. Some banks have gone a step further. For example, in 2014 Spain’s Banco Sabadell invited developers to a “hackathon” to create apps for managing personal finances and initiating payments.

31

EnableCodeHaloThinkingThe growing number of digital touchpoints, com-bined with advanced analytics, allows banks to create unique profiles of their individual and insti-tutional customers based on their Code Halos. As customers become more socially connected, the

Crypto-CurrenciesDespite the mostly negative coverage they have received in the past few years, crypto-currencies are among the top disruptions in the payments landscape – and they are gaining popularity. A survey by Ponemon Institute and HP found that 79% of U.S. consumers planned to support digital currencies such as Bitcoin in the future.

27 Moreover, 80% of

the respondents expect digital currencies to overtake paper currencies in the future. There are more than 580 different crypto-currencies on the market right now vying for the top spot, with Bitcoin leading the pack.

28

A few prominent banks have taken an interest in Bitcoin’s distributed ledger-based approach known as BlockChain technology for generating efficiencies and security improvements in payments.

29 Crypto-curren-

cies hold the potential to transform payments, especially when combined with mobile P2P payments. The Bank of England observed as much in its recently published analysis.

30

Given this untapped potential of crypto-currencies, U.S. banks will do well to make provisions for supporting these currencies in

their future digital payments offerings. They are also in a position to provide value-added services in the crypto-currency ecosystem.

Current Trends in Crypto-Currencies

• Slow but steady progress in adoption.

• Prone to price volatility.

• Regulatory uncertainty as regulators continue to debate.

• Alternative applications being researched.

Risks and Challenges

• Consumer adoption: Price stability, trust in service providers and a compelling value proposition will be the keys for boosting adoption.

• Regulations: There is a need for a univer-sally defined regulatory framework and to address concerns over money laundering and customer protection.

• Technological innovation: Information system risks are currently very high; transactions cannot be reversed; and the current technology architecture is prone to phishing and malware attacks.

cognizant reports 9

• Employ an agile approach to product develop-ment that allows for quicker market feedback and continuous evolution.

• Design the mobile wallet strategy considering millennials and gen-X-ers as primary target customers.

• Embed touchpoints throughout the payment experience to increase customer engagement and create monetization opportunities.

• Create well-defined authentication capabilities and risk-management strategies.

• Privacy of information – in the apps, in the cloud and with partners – should be accounted for throughout the product lifecycle and the partner selection process.

• Develop a clear tokenization strategy keeping in mind its future implications and potential future use cases.

• User experience design should be simple, intuitive, clutter-free, frictionless and uniform across channels.

• Build big data analytics capabilities that lever-age structured and unstructured data to gen-erate useful insights and enhance risk man-agement.

• Enable mass personalization and rich data visualizations leveraging analytics capabilities.

• For a mobile wallet, build an effective and contextual coupons, offers, and loyalty and rewards strategy to increase customer engage-ment and market share.

• Develop a social media roadmap to engage customers, provide new value-added services and enable payment touchpoints in the social media platforms.

sumers, feel secure in accepting and making digital payments. From a merchant’s perspective, tokeni-zation and encryption of the payment information has helped mitigate breaches while the payment information is at rest and also while it is in transit to the payment processors. While tokenization and encryption is considered a niche add-on feature, we believe very soon it will be commoditized and become the norm. For consumers, a multifactor authentication mechanism could be the one thing that expands the size of the digital payments pie. The authentication product from Encap Security is a solution that seems to have found the sweet spot between security and user experience.

FocusonUserExperienceDesignOne of the key differentiators for digital disruptors is the user experience that they provide across touchpoints. Achieving an engaging, personalized and contextual digital user experience requires banks to approach design from an end-to-end – people, process and technology – perspective. To this end, banks will have to reimagine how they interact with customers, using the possibilities generated by next-generation digital technolo-gies and the associated business practices. Impor-tantly, the digital experience should be designed to seamlessly engage the customer across bank-ing channels without any kind of rework or loss of information. A poorly designed authentication sys-tem with a bad user experience, for example, could boomerang.

LookingForward:Recommendations

• Adopt an open-platform approach to digital payments that allows for easy integration with service providers, banks and merchants and makes the platform(s) scalable and acceptable to partners.

• Future-proof the platform(s) by designing them to be flexible, scalable and modular to adapt to a continuously changing landscape.

• Pursue a collaborative approach as more part-ners mean more value-added services, broader market acceptance and a deeper set of fea-tures.

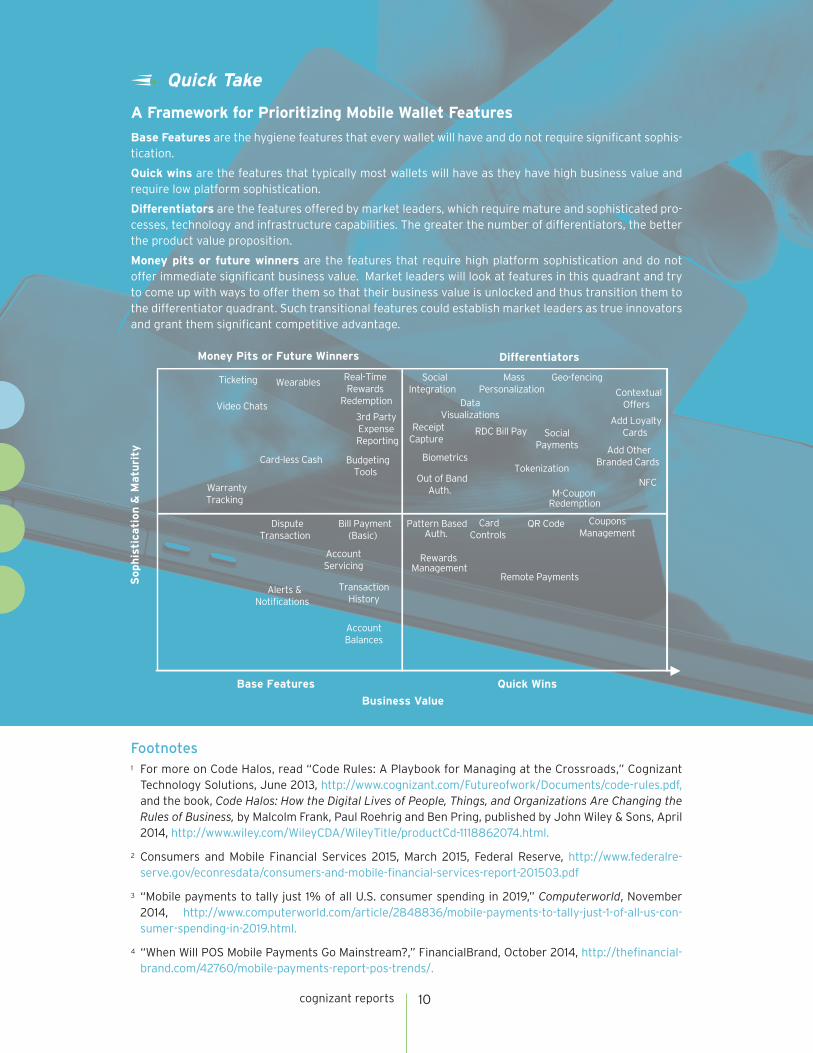

• Quick Take

A Framework for Prioritizing Mobile Wallet Features

Base Features are the hygiene features that every wallet will have and do not require significant sophis-tication.

Quick wins are the features that typically most wallets will have as they have high business value and require low platform sophistication.

Differentiators are the features offered by market leaders, which require mature and sophisticated pro-cesses, technology and infrastructure capabilities. The greater the number of differentiators, the better the product value proposition.

Money pits or future winners are the features that require high platform sophistication and do not offer immediate significant business value. Market leaders will look at features in this quadrant and try to come up with ways to offer them so that their business value is unlocked and thus transition them to the differentiator quadrant. Such transitional features could establish market leaders as true innovators and grant them significant competitive advantage.

Soph

isti

cati

on

& M

atu

rity

Business Value

Base Features Quick Wins

Alerts &Notifications

3rd Party Expense Reporting

Account Servicing

Account Balances

Bill Payment(Basic)

Transaction History

QR Code

Remote Payments

Coupons Management

Rewards Management

Out of BandAuth.

BudgetingTools

CardControls

Real-Time Rewards

Redemption

WarrantyTracking

DisputeTransaction

Video Chats

Ticketing

Card-less Cash

NFC

Social Payments

Geo-fencing

ContextualOffers

Biometrics

ReceiptCapture

Add LoyaltyCards

Add OtherBranded Cards

RDC Bill Pay

SocialIntegration

MassPersonalization

M-Coupon Redemption

Data Visualizations

Tokenization

Wearables

Pattern Based Auth.

Money Pits or Future Winners Differentiators

cognizant reports 10

Footnotes1 For more on Code Halos, read “Code Rules: A Playbook for Managing at the Crossroads,” Cognizant

Technology Solutions, June 2013, http://www.cognizant.com/Futureofwork/Documents/code-rules.pdf, and the book, Code Halos: How the Digital Lives of People, Things, and Organizations Are Changing the Rules of Business, by Malcolm Frank, Paul Roehrig and Ben Pring, published by John Wiley & Sons, April 2014, http://www.wiley.com/WileyCDA/WileyTitle/productCd-1118862074.html.

2 Consumers and Mobile Financial Services 2015, March 2015, Federal Reserve, http://www.federalre-serve.gov/econresdata/consumers-and-mobile-financial-services-report-201503.pdf

3 “Mobile payments to tally just 1% of all U.S. consumer spending in 2019,” Computerworld, November 2014, http://www.computerworld.com/article/2848836/mobile-payments-to-tally-just-1-of-all-us-con-sumer-spending-in-2019.html.

4 “When Will POS Mobile Payments Go Mainstream?,” FinancialBrand, October 2014, http://thefinancial-brand.com/42760/mobile-payments-report-pos-trends/.

cognizant reports 11

5 “Coaxing U.S. Banking and Payments Into the 21st Century,” TechCrunch, February 2015, http://tech-crunch.com/2015/02/25/coaxing-us-banking-and-payments-into-the-21st-century/.

6 “It’s Time To Accelerate e-Bill Adoption,” FinancialBrand, March 2015, http://thefinancialbrand.com/50604/ebilling-billpay-banking-opportunity-research/.

7 “THE PEER-TO-PEER PAYMENTS REPORT: The exploding market for smartphone apps that transfer money,” Business Insider, May 2015, http://www.businessinsider.com/growth-in-peer-to-peer-payment-apps-report-2015-4#ixzz3bQlikF2p.

8 “Over the sea and far away,” Economist, March 2012, http://www.economist.com/node/21554740.

9 “Why 2015 Will Be the Year of Remittances,” BankInnovation.net, March 2015, http://bankinnovation.net/2015/03/why-2015-will-be-the-year-of-remittances/.

10 “Apple Pay Outperforming PayPal in Mobile Payments, According to New 451 Research Survey,” PRWeb.com, April 2015, http://www.prweb.com/releases/2015/04/prweb12667796.htm.

11 Mobile Payments: Consumer Insights & Recommendations, PunchTab Consumer Research Series, Octo-ber 2014, http://engagement.punchtab.com/mobile_payments_consumer_insights_whitepaper.

12 “Retail security breaches come back to haunt Apple Pay,” VatorNews, March 2015, http://vator.tv/n/3c70.

13 “Ondot Launches Remote Control for Credit Cards,” Mashable, April 2014, http://mashable.com/2014/04/24/ondot-cardcontrol-app/.

14 “Starbucks’ Mobile Payments Jolt,” PYMNTS.com, January 2015, http://www.pymnts.com/in-depth/2015/starbucks-mobile-payments-jolt/.

15 Ibid.

16 “American Express Expands Its Serve Prepaid Card to Walmart,” Forbes, March 2014, http://www.forbes.com/sites/tomgroenfeldt/2014/04/21/american-express-expands-its-serve-debit-card-to-walmart/.

17 The Advice Advantage – How Banks Can Close the ‘Value Gap’ and Regain Customer Trust,” Cisco, February 2015, https://origin-www.cisco.com/c/dam/en/us/solutions/collateral/executive-perspectives/ioe-financial-services-white-paper.pdf.

18 “Banks see Amazon, Apple and Google as growing threat, report claims,” ComputerworldUK, October 2014, http://www.computerworlduk.com/news/it-vendors/banks-see-amazon-apple-google-as-major-threat-3580074/.

19 Ibid.

20 “The CEO of America’s biggest bank is worried about Silicon Valley and Bitcoin stealing his business,” Mashable, April 2015, http://mashable.com/2015/04/10/jp-morgan-ceo-letter/.

21 M-Pesa helps world’s poorest go to the bank using mobile phones, Christian Science Monitor, January 2014, http://www.csmonitor.com/World/Making-a-difference/Change-Agent/2014/0106/M-Pesa-helps-world-s-poorest-go-to-the-bank-using-mobile-phones.

22 “American Express Expands Its Serve Prepaid Card to Walmart,” Forbes, March 2014, http://www.forbes.com/sites/tomgroenfeldt/2014/04/21/american-express-expands-its-serve-debit-card-to-walmart/.

23 “U.S. Expected To Lag China In Digital Payments Growth As Plastic Stays Popular,” Forbes, Septem-ber 2014, http://www.forbes.com/sites/russellflannery/2014/09/24/u-s-expected-to-lag-china-in-digital-payments-growth-as-plastic-stays-popular/.

24 Reimagining the Digital Bank – How U.S. Banks Can Transform Customer Interactions To Increase Prof-itability,” Cisco, 2014, http://www.cisco.com/c/dam/en/us/solutions/collateral/executive-perspectives/Internet-of-Everything-executive-summary.pdf.

25 “Marketplace Lending: A Maturing Market Means New Partner Models, Business Opportunities,” Cog-nizant Reports, http://www.cognizant.com/InsightsWhitepapers/Marketplace-Lending-A-Maturing-Mar-ket-Means-New-Partner-Models-Business-Opportunities-codex989.pdf.

WorldHeadquarters

500 Frank W. Burr Blvd.Teaneck, NJ 07666 USAPhone: +1 201 801 0233Fax: +1 201 801 0243Toll Free: +1 888 937 3277Email: [email protected]

EuropeanHeadquarters

1 Kingdom StreetPaddington CentralLondon W2 6BDPhone: +44 (0) 207 297 7600Fax: +44 (0) 207 121 0102Email: [email protected]

IndiaOperationsHeadquarters

#5/535, Old Mahabalipuram RoadOkkiyam Pettai, ThoraipakkamChennai, 600 096 IndiaPhone: +91 (0) 44 4209 6000Fax: +91 (0) 44 4209 6060Email: [email protected]

©Copyright2015,Cognizant. All rights reserved. No part of this document may be reproduced, stored in a retrieval system, transmitted in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the express written permission from Cognizant. The information contained herein is subject to change without notice. All other trademarks mentioned herein are the property of their respective owners.

AboutCognizant

Cognizant (NASDAQ: CTSH) is a leading provider of information technology, consulting, and business process out-sourcing services, dedicated to helping the world's leading companies build stronger businesses. Headquartered in Teaneck, New Jersey (U.S.), Cognizant combines a passion for client satisfaction, technology innovation, deep industry and business process expertise, and a global, collaborative workforce that embodies the future of work. With over 100 development and delivery centers worldwide and approximately 218,000 employees as of June 30, 2015, Cognizant is a member of the NASDAQ-100, the S&P 500, the Forbes Global 2000, and the Fortune 500 and is ranked among the top performing and fastest growing companies in the world.

Visit us online at www.cognizant.com or follow us on Twitter: Cognizant.

AuthorandAnalystAuthorandAnalystAkhil Tandulwadikar, Senior Researcher, Cognizant Research Center

SubjectMatterExpertsRatish Gopal, Manager – Consulting, Banking & Financial Services Projects, Cognizant Technology Services

Anang Mankad, Manager – Consulting, Banking & Financial Services Projects, Cognizant Technology Service

DesignMary McBride

26 “U.S. Bank integrates with Western Union to simplify mobile money transfers,” Mobilecommercedaily, September 2013, http://www.mobilecommercedaily.com/u-s-bank-integrates-with-western-union-to-simplify-mobile-money-transfers.

27 “Security & Compliance Trends in Innovative Electronic Payments,” Ponemon Institute, October 2014, http://www.nfcidea.pl/wp-content/uploads/2014/12/hp-ponemon-payments-white-paper.pdf.

28 “Crypto-Currency Market Capitalizations,” coinmarketcap.com, http://coinmarketcap.com/all/views/all/.

29 “Why Banks Are Testing Bitcoin’s Blockchain (Without Bitcoin),” June 2015, http://www.americanbanker.com/news/bank-technology/why-banks-are-testing-bitcoins-blockchain-without-bitcoin-1074622-1.html.

30 “Bitcoin revolution could be the next internet, says Bank of England,” Telegraph UK, February 2015, http://www.telegraph.co.uk/finance/currency/11434904/Bitcoin-revolution-could-be-the-next-internet-says-Bank-of-England.html.

31 “Banco Sabadell’s Hackathon Asks Developers to Imagine the Future of Digital Banking,” Program-mableWeb.com, September 2014, http://www.programmableweb.com/news/banco-sabadells-hack-athon-asks-developers-to-imagine-future-digital-banking/2014/09/11.

32 “10 Payments Companies Competing in Analytics,” letstalkpayments, January 2014, http://letstalkpay-ments.com/10-payments-companies-competing-analytics/.

33 Ibid.