digital services & distribution budget presentation fiscal year 2008 february 2007

TRANSCRIPT

Digital Services & DistributionBudget Presentation

Fiscal Year 2008

February 2007

2

Agenda

1. Executive Summary

2. Digital Distribution

3. Mobile Entertainment

4. Digital Services / Grouper

5. EBIT Reconciliation

3

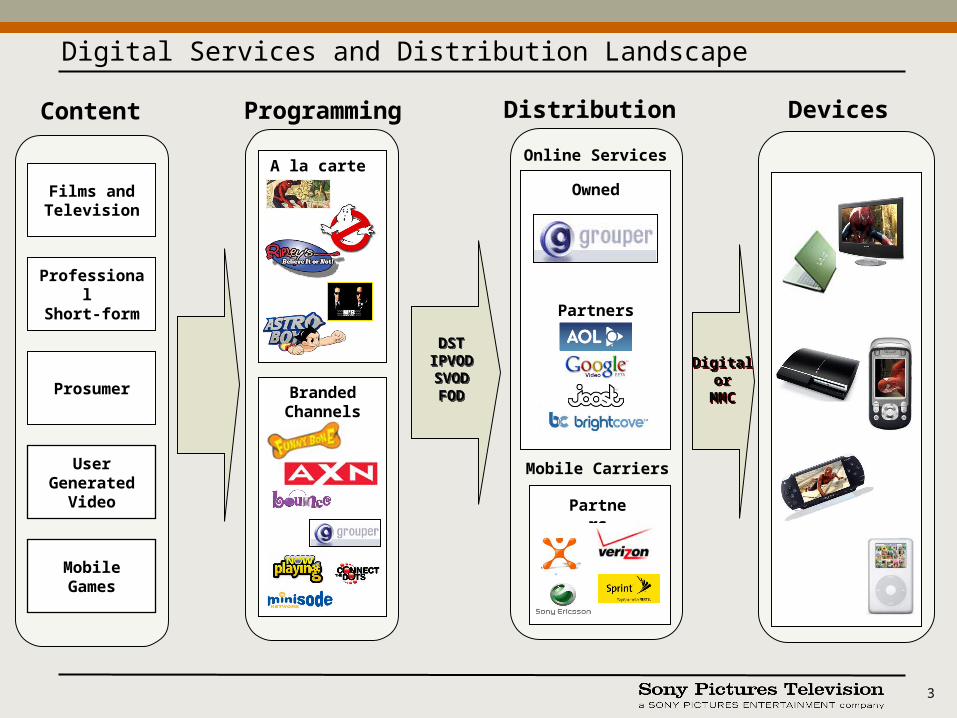

Programming

A la carte

Branded Channels

Content

Films andTelevision

Professional Short-form

Prosumer

User Generated

Video

Distribution

Owned

DSTIPVODSVODFOD

DSTIPVODSVODFOD

MobileGames

Mobile Carriers

Partners

Digitalor

MMC

Digitalor

MMC

Devices

Digital Services and Distribution Landscape

Online Services

Partners

4

• Traditional media players are experimenting with new models for digital distribution

–Networks are launching branded online channels and streaming ad-supported episodes (ABC.com, CBS.com & Innertube, NBC.com & DotComedy, Turner & Super Deluxe)

–Digital sell-through is gaining broad support (iTunes is selling films from Disney and Paramount; television episodes from major networks)

–Fox / NBC / Viacom exploring concept of a dedicated JV for online content distribution

• Historically game-based, mobile is also proving viable for video distribution

–Adoption of 3G handsets continues to grow and is improving viewing experience

–Carriers are seeking video content to attract and retain customers

• A wide range of players is competing for quality UGV content and audience

–Google’s acquisition of YouTube raised the bar for critical mass

–Quality of viral video is increasing as traditional media players enhance their owned services (Fox / MySpace, Viacom / Atom Films)

–Online pure-plays (Heavy, Break) are compensating content creators by acquiring videos

Competition is Increasing as Demand for Digital Content Grows

5

• Key accomplishments in FY07

–Launched multiple new business models for digital distribution–Launched mobile video–Significantly expanded distribution relationships across internet services,

mobile carriers, and hardware partners–Created and launched first branded cross-platform channels –Acquired and integrated Grouper; grew unique users by 40%

• Focus areas for continued growth in FY08

–Add 21 distribution partners in 2008–Grow distribution revenue 140% from $16.5MM in FY07 to $39.7MM in FY08;

contribute $27.8MM to other SPE divisions–Broaden digital content offering, including acquired and produced content–Increase number of branded digital channels and expand distribution–Re-launch “Grouper 3.0” with differentiated content and service offer–Continue to grow Grouper user base and begin monetizing audience

Success in FY07 Established Foundation for Growth in FY08

6

Digital Services & Distribution – Revenue OverviewDigital Services & Distribution – Revenue Overview

$3.0

$18.6

$10.6

$21.2

$16.5

$31.7

$39.7

$0

$10

$20

$30

$40

$50

$60

'07 Budget '07 Forecast '08 MRP '08 Budget

($ in MM)

Grouper Digital Distribution

$50.3 $50.3

$16.5

$24.2

$8.7 $6.7 $10.4 $14.0

($15.0) ($15.1) ($18.4) ($32.0)EBIT

DD – Op Income

($10.0) ($10.0) ($10.1) ($18.2)Grouper - EBIT

($5.0) ($5.1) ($8.3) ($13.8)DD – EBIT

7

Launched in 2007 In Progress for 2008

Digital Imaging

• Memory Card bundles with games and films

• Grouper in firmware

• Memory Stick Entertainment Pack

• Grouper service and SPE promotional channels on IP Bravia

• All US VAIOs shipping with SPE Movies

• Early discussions for digital delivery of films day-and-date with DVD

• Licensing content for digital delivery to the PlayStation 3

• Potential metadata R&D project

• Grouper video and HOME service

• Integrating Grouper for online video sharing

• Grouper screen saver on VAIOs

• Selling mobile products through “Music Box”

• Distributing Sony BMG games

• Project X

DSD Continues to Provide Support for “Sony United”

8

Agenda

1. Executive Summary

2. Digital Distribution

3. Mobile Entertainment

4. Digital Services / Grouper

5. EBIT Reconciliation

9

FY07: $5.8MMLaunched a wide range of business models

across 20 total partners

FY08: $19.7MMExpand to 41 partners and broaden relationship

with existing accounts

New Business Models and Partners Enable Growth in FY08

Broad Launch of Digital Sell-Through

Expanded Digital Rental

Expanded Digital Subscription

Launched Ad Supported Channels

10

• Established and launched new business models

– Launched download-to-own business

– Launched cross-platform digital channels

• Expanded distribution relationships

– Secured deals with Amazon, Wal-Mart, Movielink, CinemaNOW, AOL, ClickStar,

GUBA, AT&T, Best Buy, and NetFlix

• Supported cross-Sony digital entertainment initiatives

– Launched first secure digital content program for the PSP

– Provided content bundles for VAIO and Sony Ericsson

• Established end-to-end operational processes with SPHE, SPT, WPF and DigiPol

to operate these emerging digital businesses

Key FY07 Successes

11

• More feature film titles available in the marketplace than any other studio (over 300)

• Business to-date is largely new release driven, but there is demonstrated demand for “long tail” product

• All titles in the program have been purchased by end consumers

Top 10 DST Titles

1. The Da Vinci Code

2. Click

3. Talladega Nights

4. Underworld Evolution

5. Ultraviolet

6. RV

7. Silent Hill

8. The Covenant

9. Monster House

10. Memoirs of a Geisha

FY07 Demonstrated Demand for a Wide Range of Studio Product

12

• Aggressively build on the existing distribution network– Strike partnerships across the complete spectrum of traditional and on-line players– Expand partners to include: Starz, Apple, Microsoft, Best Buy, Transworld, Target

(significant opportunity for incremental revenue in an Apple deal)

• Expand the overall content offering– Broaden selection of film and TV product– Launch DST of TV product by end of year– Introduce the most compelling short-form/original content

• Continue to lead market in innovating digital product offerings and usage models

• Continue to operate an industry-leading digital organization – Provide end-to-end asset delivery and digital operations – Create innovative marketing and promotional programs

• Grow the business from $5.7MM in FY07 to $18.1MM in FY08

FY08 Digital Sell-Through / IP-VOD Strategy

13

• Continue to expand SPE’s digital channel offering– Comedy (Funny Bone) - Who’s The Boss, NewsRadio– Action (AXN) - SWAT, Charlie’s Angels– Kids (Bounce) - Jackie Chan, Animated MIB, – International Programming (World Channel)– Anime (Animax) - Samurai X– Movies on Demand (Now Playing/Hollywood Hits)– The Minisode Network– Grouper “Off the Hook”

• Introduce additional film and television properties complemented by a blend of original programming and interactive features

• Establish relationships with 3rd party content holders to improve channel offerings– Nelvana for Bounce (e.g., Rescue Heroes, Rolie Polie Olie, Babar)– Ban Dai for Animax (e.g., Gundam)

• Aggressively expand channel distribution to high-traffic destinations across platforms

FY08 Digital Channel Strategy

14

Digital Distribution – Revenue OverviewDigital Distribution – Revenue Overview

$2.5$1.6

$5.0$5.7

$11.5

$18.1

$0

$5

$10

$15

$20

$25

'07 Budget '07 Forecast '08 MRP '08 Budget

($ in MM)

Advertising / Sponsorships Licensing

$14.0

$19.7

$5.8$5.0

$0.1

15

Digital Distribution – Summary P&L

P&L ($000s) '07 Budget '07 Forecast Variance '08 MRP '08 Budget Variance

Total Revenue $5,000 $5,762 $762 $14,000 $19,675 $5,675

Total COGS ($1,790) ($1,071) $719 ($2,100) ($1,950) $150

Gross Profit $3,210 $4,691 $1,481 $11,900 $17,725 $5,825

Total Operating Expenses ($3,875) ($3,296) $579 ($4,615) ($7,930) ($3,315)

Operating Income ($665) $1,395 $2,060 $7,285 $9,795 $2,510

Less: Contribution ($845) ($3,009) ($2,164) ($9,445) ($13,950) ($4,505)

EBIT ($1,510) ($1,614) ($104) ($2,160) ($4,155) ($1,995)

Headcount 11 11 - 14 20 6

16

Agenda

1. Executive Summary

2. Digital Distribution

3. Mobile Entertainment

4. Digital Services / Grouper

5. EBIT Reconciliation

17

PersonalizationPersonalization

Mobile GamesMobile Games

SMSInteractivity

SMSInteractivity

Mobile Video

Mobile Video

MobileApplications

MobileApplications

Full Suite of Mobile Content Products

Comprehensive Marketing and Distribution Footprint

CarriersCarriers

HandsetsHandsets

AggregatorsAggregators

Direct to ConsumerDirect to

Consumer

+

New management team put in place to run daily operations

FY07 was Profitable and Provided Critical Foundation for FY08 Growth

18

0

50,000

100,000

150,000

200,000

April May J une J uly Aug Sept Oct Nov Dec

Uni

ts S

old

• Despite having ½ as many games in the market in FY07, MEG managed to increase total monthly unit sales

• Generated significantly higher unit-sales-per-game through:

– Tighter carrier relationships

– Strategic handset porting and ops management

– Targeted marketing and product rollout

– Better product selection

Games in FY07: New Approach Proving Successful

6,000

8,000

10,000

12,000

14,000

16,000

18,000

April May J une J uly Aug Sept Oct Nov Dec

Uni

ts S

old

Ratchet and Clank

Wheel of Fortune – ‘07

5,000

10,000

15,000

20,000

25,000

30,000

April May J une J uly Aug Sept Oct Nov Dec

Uni

ts S

old

James Bond: Casino Royale

Case I: Re-Launch• Drove new sales of popular

PlayStation title • Porting, placement and

marketing drove re-launch• Sales now exceeding original

title launch – not typical in the games industry

Case II: Re-Fresh• Top-selling mobile brand

grew 12% after distribution of a new version of the game

• More strategic handset porting, mixed with securing better deck placement

Case III: New Game Launch• First new title release in nearly 12

months• Strategically planned around

movie release• Strategic handset porting, secured

deck placement and marketing• Sales exceeding Jeopardy,

previous number 2 title for MEG

Re-launch

Re-fresh

Launch

19

Ratchet & Clank

Q*Bert

Balloon Breaker

Elevator Action

Snoop Dogg Boxing

Casino Royale

Wheel of Fortune 2007

Ghostbusters

Launch New Games(current slate)

Grow Distribution for Catalog(carriers, handset, online)

Snoop Dogg Cruisin’

JEOPARDY! 2007

Fish’n Tunes

Spider-Man 3Spider-Man 3

Spider-Man 3 PuzzleSpider-Man 3 Puzzle

Bond vs. Bond Bond vs. Bond

Ivan Moscovich PuzzleIvan Moscovich Puzzle

Jump That CarJump That Car

God of WarGod of War

JEOPARDY – Rock & RollJEOPARDY – Rock & Roll

OCT

MAY

JUNE

JULY

AUG

SEPT

APR

Untold Legends Untold Legends NOV

Q*Bert “2” Q*Bert “2” DEC

Wheel of Fortune Wheel of Fortune JAN

JEOPARDY! JEOPARDY! FEB

Bond Driving Bond Driving MAR

• Launch 1 new game per month; strategically manage the portfolio/roadmap• Aggressively optimize carrier deck placement• Expand existing Motorola and Sony Ericsson embed programs, and land new OEM deals• Utilize consumer product marketing approach• Strike relationship with leading publisher (e.g., Glu) to secure game pipeline• Grow revenue from $7.0M to $13.2M in FY08

’08 Strategy

Mobile Games in FY08: More Games, Expanded Distribution

20

Sony “Sneak Peeks” Movies “Hollywood Hits” (launching in March)

• Sony Pictures is now distributing full-length

movies over-the-air on mobile carriers’ video

services

• Sprint Movies offers pay-per-view service with

DVD features

• Offer 7 movies at a time

• Average view time ~ 1.5 hours

• Negotiating with other carriers for distribution

• Promotional channel featuring clips

from theatrical, television, PlayStation,

FearNet and mobile games

• Currently at 350k streams / month on

Sprint and Verizon – increased

programming to 20% growth month-

over-month

• The only linear looping movie channel within Sprint’s Basic + tier of video

• Two looping channels with four classic movies on each channel; movies include comedy, action and drama

• One movie on each channel refreshed weekly

• Optimizes library value by utilizing unused inventory on a spot basis

• Sony Pictures pioneered delivering full-length movies to mobile handsets via memory cards

• Successful handset bundle programs launched in the UK, France, Germany, Switzerland, ItalyNetherlands, & S. Africa

Memory Cards

Over-the-Air

Sony Pictures•Exclusives•In Theatres•Coming to Theatres•On DVD •Coming to DVD•Game Previews•FearNet•PlayStation

FY08 Will Build on Launch of Video Services

21

Ad Supported Transactional

Fee-per-sub

…using a range of business models

On-demand

Sell-through Linear streaming

…and consumer experiences

• Concentrate on biggest video distributors (in order)- Sprint, Verizon, Cingular

• Launch quality video services in multiple genres, with a breadth of business models, addressing a variety of consumer experiences

• Aggressively optimize deck placement and marketing tactics• Draft off marketing for IP-video and other mobile products where possible

’08 Strategy

Extend Channel Brands to Mobile

SPT Channels

Premium Video Services Launched into Carriers’ “Basic Tiers” in FY08

Short-form programs

Long-form programs

22

Handsets Aggregators D – to - CCarriers

FY07: Grew relationships, marketing and tech ops capabilities with partners

Carriers: Continue to focus aggressively on top 3 players in the market, push T-Mobile and Alltel for growth, and add additional strategic players (e.g., Virgin)

Handsets: Continue to push on embed deals with Motorola; secure deals with Nokia and Sony Ericsson

Online Aggregators: Increase reach by licensing to a select group of top online retailers

Direct-to-Consumer: Establish direct-to-consumer distribution, leveraging applications and web

’08 Strategy

Large Footprint Secured in FY07 will Serve as Foundation for Future Growth

23

Mobile Entertainment – Revenue Overview

$4.0 $3.5

$9.7

$7.0

$10.2

$13.2

$1.5

$0.6

$3.5

$3.3

$3.1$5.0

$0

$5

$10

$15

$20

$25

'07 Budget '07 Forecast '08 MRP '08 Budget

($ in MM)

Retail / Online Product Games Licensing, D2C, Personalization, & Ad

$17.7

$20.0

$10.7

$16.2

24

Mobile Entertainment – Summary P&L

P&L ($000s) '07 Budget '07 Forecast Variance '08 MRP '08 Budget Variance

Total Revenue $16,150 $10,728 ($5,422) $17,725 $19,975 $2,250

Total COGS ($2,400) ($1,113) $1,287 ($7,735) ($4,940) $2,795

Gross Profit $13,750 $9,615 ($4,135) $9,990 $15,035 $5,045

Total Operating Expenses ($3,155) ($2,879) $276 ($5,065) ($5,565) ($500)

Operating Income $10,595 $6,736 ($3,859) $4,925 $9,470 $4,545

Less: Contribution ($12,790) ($8,848) $3,942 ($9,290) ($13,800) ($4,510)

EBIT ($2,195) ($2,112) $83 ($4,365) ($4,330) $35

Headcount 13 13 - 17 14 (3)

25

Digital Distribution & Mobile Entertainment – Consolidated P&L

P&L ($000s) '07 Budget '07 Forecast Variance '08 MRP '08 Budget Variance

Total Revenue $21,150 $16,490 ($4,660) $31,725 $39,650 $7,925

Total COGS ($4,190) ($2,184) $2,006 ($9,835) ($6,890) $2,945

Gross Profit $16,960 $14,306 ($2,654) $21,890 $32,760 $10,870

Operating ExpensesG&A ($5,025) ($4,931) $94 ($6,480) ($12,171) ($5,691)Other ($3,255) ($2,655) $600 ($4,975) ($6,625) ($1,650)

Total Operating Expenses ($8,280) ($7,586) $694 ($11,455) ($18,796) ($7,341)

G&A as a % of Revenue * 36% 45% 30% 31%

Operating Income $8,680 $6,720 ($1,960) $10,435 $13,964 $3,529

Less: Contribution ($13,635) ($11,857) $1,778 ($18,735) ($27,750) ($9,015)

EBIT ($4,955) ($5,137) ($182) ($8,300) ($13,786) ($5,486)

HeadcountIP 11 11 - 14 20 6 Mobile 13 13 - 17 14 (3) ExecOps 2 4 2 6 7 1

Total 26 28 2 37 41 4

* 2007 and 2008 MRP are Pro Forma to include the transfer of Executive headcount and legal allocation

26

Headcount Reconciliation

FY08 Additions

• Expanding to support growth in new accounts

• Driving growth in new accounts

• Developing new products; creating marketing and programming assets

2 Sales

4 Product / Asset Creation

4 Account Mgmt.

Digital Distribution and Mobile: Requested Increase in Headcount

Forecast End of FY07

Transfer from within ODE

Transfer from Other SPE Additions

FY 2008 Budgeted

Digital Distribution 11 2 - 7 20 Mobile Entertainment 13 (2) 1 2 14 Executive 4 - 2 1 7

Total 28 - 3 10 41

Revenue per Head $0.6MM 64% Growth $1.0MM

Fiscal Year 2008 Budget

27

Agenda

1. Executive Summary

2. Digital Distribution

3. Mobile Entertainment

4. Digital Services / Grouper

5. EBIT Reconciliation

28

2008 represents an opportunity to address a gap in the marketby blending Hollywood quality with the viral nature of UGV

FY07 Accomplishments FY08 Focus Areas

• Successful integration with Sony Pictures

• Developed content and programming strategy

• Retained and grew initial user base

• Supported “Sony United” by integrating with other divisions

• Launch 3.0 to address market gap

• Capitalize on market opportunity to grow and monetize the service

Recent Progress and FY08 Focus Areas

29

Integrated with SPE

Integrated Across Sony

Expanded User Base

• Grouper in PSP firmware

• Integration with IP-enabled Bravia

• Working on PS3 prototype

• Grew users 40% to 9MM

• Grew daily video streams to 1.6MM

1.92.5

3.0

4.5

5.3

6.0

0

1

2

3

4

5

6

7

8

9

10

October November December

Mo

nth

ly U

niq

ue

Use

rs (

mil

lio

ns)

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

Dai

ly S

trea

ms

(mil

lio

ns)6.4

7.89.0

• Unique SPE content offering -- ScreenBites

• DVD promotion for Seinfeld Season 7

• Contests for SPE theatrical releases (Pursuit of Happyness launched, Spider-Man 3 in process)

FY07: Integrated Grouper and Expanded User Base

30

• Establish Grouper as a trusted and recognized brand for online video by combining the viral nature of user-generated video with the quality of “Hollywood” content

• Build a large base of high quality short-form video– Attract content creators through a “path to recognition”– Identify and invest in the best videos– Produce original short-form content

• Offer users a compelling content syndication proposition

• Implement a differentiated, channel-based programming strategy

• Improve overall user experience through a superior content guide, high-quality playback, easy publishing to other sites

Vision

Execution

Launching Grouper 3.0 in June 2007

Grouper 3.0

31

“The Red Carpet” (Potential Show on “All Access” Channel)

Attend premieres

and interview

celebrities

Guest Host on

“Red Carpet” Show

All Content Uploaded to Channel

Featured Content (Views, Ratings, Editorial)

Content Featured

in “Best of” Show

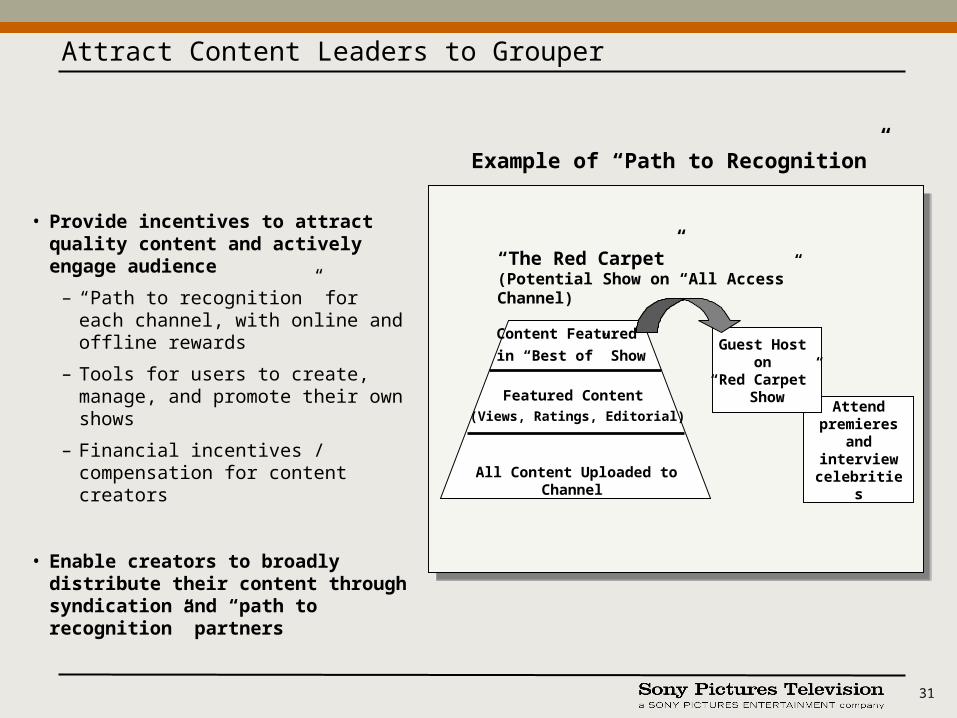

• Provide incentives to attract quality content and actively engage audience

– “Path to recognition” for each channel, with online and offline rewards

– Tools for users to create, manage, and promote their own shows

– Financial incentives / compensation for content creators

• Enable creators to broadly distribute their content through syndication and “path to recognition” partners

Example of “Path to Recognition”

Attract Content Leaders to Grouper

32

• Short-form, higher production quality

• Shows developed for specific channels

• Mix of in-house (60%) and commissioned 3rd party shows (40%)

• Quality UGV content with an established online audience

• Grouper will acquire or license for a fixed fee or revenue share on an exclusive basis

• Opportunistic acquisition of content with lower production value but proven audience appeal

• Fixed fee paid for exclusive distribution rights

OriginalProduction

Prosumer General UGVNiche

Collections

AcquiredProduced

Investing $3.9MM to produce 450 short episodes and acquire roughly 5,000 videos

Invest in Differentiated Content

33

Tier Content Focus Sample Channel Concepts

Tier 1Branded channels focused on well-defined genres with depth of content and originally produced shows

Tier 2 Broader content categories with breadth of user-uploaded content and hand-picked featured videos

Tier 3General UGV, with featured content largely based on user ratings and input

• Quick Laugh

• Election 2008

• Instant Karma

• All Access

• Project X

• Sexy • Travel• Citizen Journalist• How-To

• Holiday / Events• Don’t Try at Home• Trends / Lifestyle• Action Sports

• Pets & Animals• Car Culture• Video Games• Family Friendly

• Blog!• Colleges• Spirituality

Launch Grouper 3.0 with 5 to 6 Channels in June10 Channels Live by End of Fiscal Year

Program on a Channel Basis

34

Q4 FY07 Q3 FY08Q2 FY08Q1 FY08

• 2.5 Launch

• Continuous playlists

• Multi-file upload

• Enhanced external player

• New home page

• Advertising

• 1-click to new distribution partners

• Syndicate Grouper to network partners

• Channel home pages with shows

• 3.0 Launch

• Re-branding

• New content strategy implemented

• Path to recognition in place

• Multi-site publishing

• “My Show”

• Enhanced external player with ads and sponsor support

• Family filter

• Updated advertising technology

• Enhancements

• Talent show

• Content creator self promotion tools

• Web-based groups

• Recommendation engine

• Web-based IM integration

• Update advertising technology

• Mobile sharing 1.0

• Sony Ericsson syndication

• Enhancements

• Mobile sharing 2.0

• Hardware integration

– Cameras

– PCs

– Devices

• Client re-launch

• Geo sharing

Improve Overall User Experience: Product Roadmap

35

Attract New Users through Marketing

Extend Reach through 3rd Party Distribution Partners

Social Networks

Online Portals

Hardware / Embed deals

Verticals

Online Marketing

Project X Prizes

Cross-Sony Support

Leverage SPE

$2.5MM investment in Grouper Marketing and Distribution$3.0MM in Prizes for Project X

Extending Audience Reach Through Marketing & Distribution

Path to Recognition

Partners

36

Non-Channel-Based Sponsorship Revenue

Channel-Based Sponsorship RevenueAdvertising Revenue

$4 MM $2.8 MM $3.8 MM

Branded Channels

• Custom Channels dedicated to a single brand (i.e. ‘Mini

Cooper’ channel)

• 20 total in FY08 at average price of $20k - $30k each

Project X

• Competitions within Project X talent categories

• Talent-based sponsorships

Channel Sponsorships

• Advertiser pays fees for persistent branding,

enticements, and sponsored downloads from a channel

Video Interstitials

• Sponsor receives dedicated portion of video interstitial

inventory w/ companion rich media ad at a premium CPM

Video Interstitials

• Run-of-Site video advertising inventory (max ad ratio 1:3

videos)

Banners

• 1 banner per page; 2 impressions per stream

User Initiated Video

•Ad placement against sponsored terms

Remnant

• Domestic and Int’l banner and domestic video interstitial

inventory sold at a discount

Advertising and sponsorships forecast to deliver $10.6MM in FY08 revenue

Revenue Strategy

37

Growth in Audience and TrafficGrowth in Audience and Traffic

Domestic / International Mix On-Site / Off-Site Mix

3.06.5

8.611.9

15.66.0

9.9

10.0

10.4

10.4

0

5

10

15

20

25

30

Dec '06 Q1 Q2 Q3 Q4

(MM) Domestic UU International UU

26.0

9.0

6.17.7

10.213.06.3

10.4

10.9

12.1

13.0

2.70

5

10

15

20

25

30

Dec '06 Q1 Q2 Q3 Q4

(MM) On-Site UU Off-Site UU

26.0

9.0

33% 60%% Domestic

30% 50%% On-Site

Growing domestic, on-site user base increases user activity, generates additional inventory, and ultimately drives more revenue

MRP16.9

MRP37.2

MRP16.9

MRP37.2

38

Ending FY08 Grouper Audience (domestic, on-site) vs. Current Competitor Audience Sizes (1)

(1) Most recent available unique user numbers per Nielsen and Comscore unless otherwise noted, domestic on-site users only(2) Per the company(3) At peak months of April and May(4) Combined 1.8MM Addicting Clips & 1.2MM Atom Films

MM

MySpace 55.3

YouTube 38.0

Break (2) 9.8

Heavy 7.8

Grouper FY08 Budget 7.8

PureVideo (2) 5.5

American Idol (3) 4 - 5

Daily Motion 3.9

eBaum’s World 3.8

Addicting Clips / Atom Films (4) 3.0

iFilm 2.3

Audience Benchmarks

39

• Addressed disruption caused by litigation to ensure continued growth–Disabled Grouper client and downloads as a precaution–Although growth was dampened, grew audience 40% since acquisition

• Delayed launch of advertising to remain competitive and solidify customer base–Key competitors, including YouTube, waiting to roll-out advertising–Launching full advertising initiative in conjunction with Grouper 3.0 service

• Adjusting business model to mitigate impact on revenues–Launching Grouper 3.0 to differentiate service and ensure continued user growth–Increasing proportion of domestic traffic; more easily monetized–Increasing proportion of on-site traffic; drives greater usage and ad inventory–Expanding revenue models to include sponsorships

Factors Impacting FY08 Revenues

40

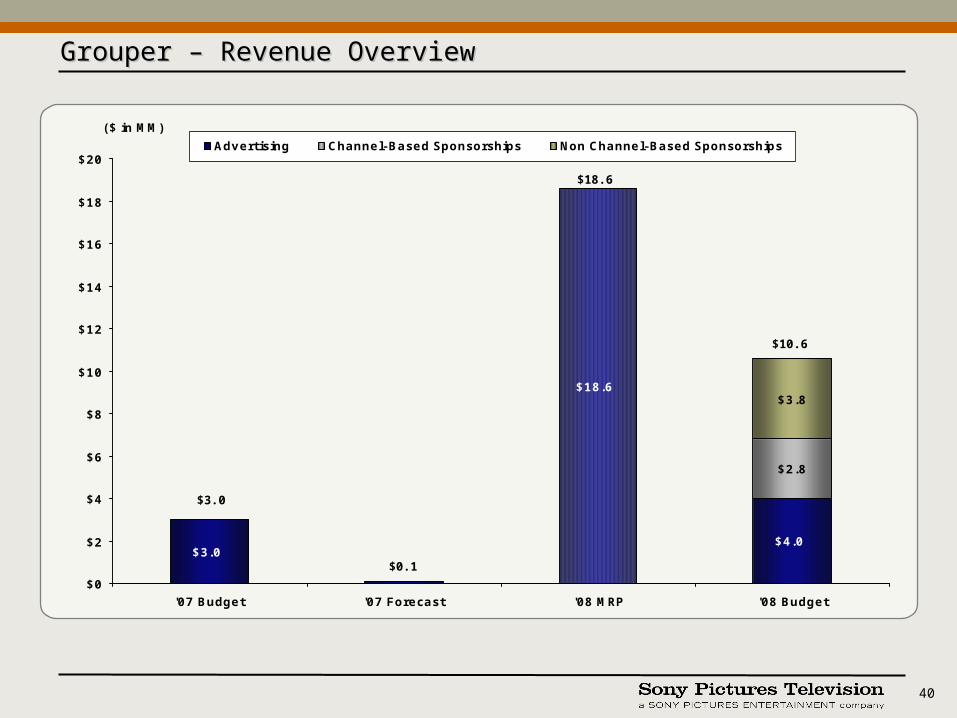

Grouper – Revenue OverviewGrouper – Revenue Overview

$18.6

$4.0

$2.8

$3.8

$3.0

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

$20

'07 Budget '07 Forecast '08 MRP '08 Budget

($ in MM)

Advertising Channel-Based Sponsorships Non Channel-Based Sponsorships

$18.6

$10.6

$0.1

$3.0

41

Grouper – Summary P&L

P&L ($000s) '07 Budget '07 Forecast Variance '08 MRP '08 Budget Variance

Total Revenue $3,000 $100 ($2,900) $18,598 $10,604 ($7,994)

Total COGS ($2,989) ($1,500) $1,489 ($8,185) ($7,590) $595

Gross Profit $11 ($1,400) ($1,411) $10,413 $3,014 ($7,399)

Total Operating Expenses ($9,011) ($7,637) $1,374 ($19,538) ($25,663) ($6,125)

Deal Amortization ($1,000) ($963) $37 ($949) ($820) $129

EBIT Before Special Items ($10,000) ($10,000) $0 ($10,074) ($23,469) ($13,395)

Special ItemsTrade Name / URL Expense $0 $0Legal $0 $0Minority Interest $5,279 $5,279

Total $0 $0 $0 $0 $5,281 $5,281

EBIT ($10,000) ($10,000) $0 ($10,074) ($18,188) ($8,114)

HeadcountGrouper 52 49 (3) 62 66 4 Project X 10 10 Ad Sales / Collections 2 2 5 5 -

Total 52 51 1 67 81 14

42

End of FY07

Grouper 49

End of FY08

Grouper 66

Project X 10

Sales / Collections 5

Total 81

MRP/Acq. Model 67

End of FY07

Grouper 49

End of FY08

Grouper 66

Project X 10

Sales / Collections 5

Total 81

MRP/Acq. Model 67

Incremental 14 Headcount vs. MRP /

Acquisition Model

GrouperContent 4

Project XTalent Mgmt 4 Judge Staff 4Editorial 2

Total 14

Incremental 14 Headcount vs. MRP /

Acquisition Model

GrouperContent 4

Project XTalent Mgmt 4 Judge Staff 4Editorial 2

Total 14

Headcount / Org Chart

J. Felser & D. SamuelCo Presidents

A. EyalCTO

T. LianoVP, Programming

J. ShambroonVP, Prod/Marktg

M. SitrinVP, Partnerships

S. GenslerDir, Biz Dev

General Mgmt

Engineering & Development

Content

Products

Customer / Acct Management

Business Development

C. Amen-KroegerVP, Engineering

TBD

Ad Sales

Project X

29

14

11

4

4

10

5

Total HeadcountEnd of FY08

4

81

SPT

43

Agenda

1. Executive Summary

2. Digital Distribution

3. Mobile Entertainment

4. Digital Services / Grouper

5. EBIT Reconciliation

44

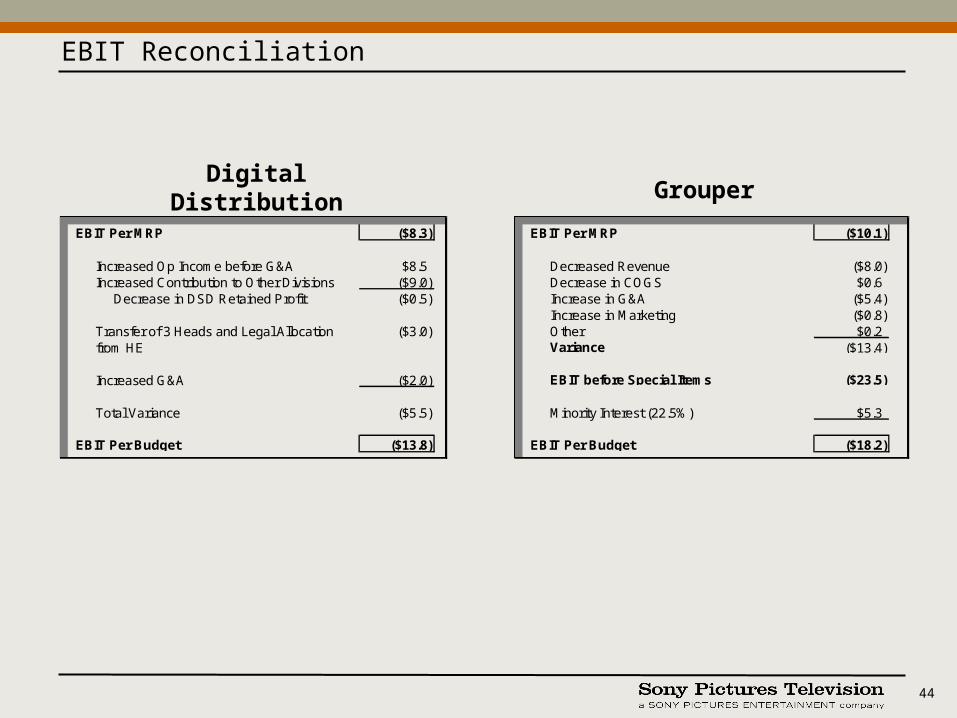

Digital Distribution Grouper

EBIT Reconciliation

EBIT Per MRP ($8.3) EBIT Per MRP ($10.1)

Increased Op Income before G&A $8.5 Decreased Revenue ($8.0)Increased Contribution to Other Divisions ($9.0) Decrease in COGS $0.6

Decrease in DSD Retained Profit ($0.5) Increase in G&A ($5.4)Increase in Marketing ($0.8)

Transfer of 3 Heads and Legal Allocation ($3.0) Other $0.2from HE Variance ($13.4)

Increased G&A ($2.0) EBIT before Special Items ($23.5)

Total Variance ($5.5) Minority Interest (22.5%) $5.3

EBIT Per Budget ($13.8) EBIT Per Budget ($18.2)