digitization of trade finance - un escap. session 2...3. is fintech the right solution? 2 2016 trade...

TRANSCRIPT

DIGITIZATION OF TRADE FINANCE IMPACT AND IMPLICATIONS FOR SMES

1

Alisa DiCaprio

Research Economist

Asian Development Bank

3 QUESTIONS

1. How big is the trade finance problem?

2. What happens when SMEs don’t get financed?

3. Is fintech the right solution?

2

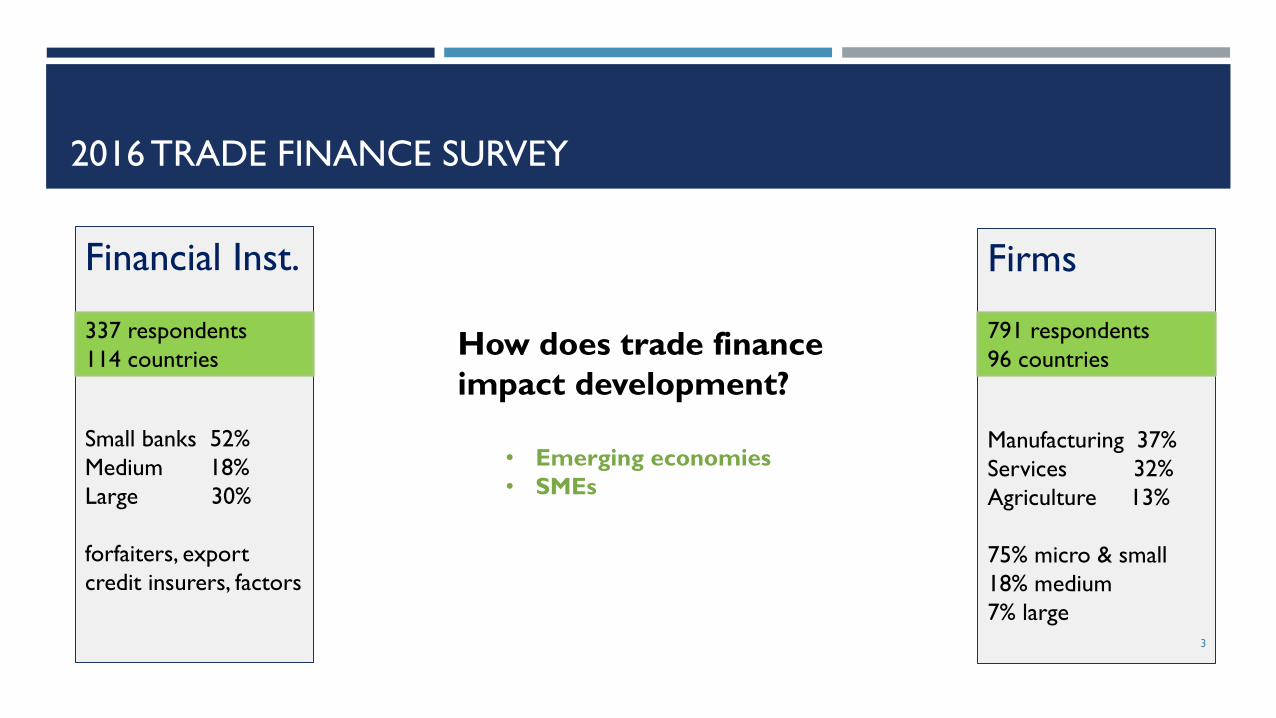

2016 TRADE FINANCE SURVEY

Financial Inst.

Small banks 52%

Medium 18%

Large 30%

forfaiters, export

credit insurers, factors

Firms

Manufacturing 37%

Services 32%

Agriculture 13%

75% micro & small

18% medium

7% large

337 respondents

114 countries

791 respondents

96 countries

3

How does trade finance

impact development?

• Emerging economies

• SMEs

HOW BIG IS THE TRADE FINANCE PROBLEM? Q1

4

Risk mitigation

Payment facilitation

Finance

Global gap

SME rejection rate

Regulatory compliance

2016 TRADE FINANCE GAP

$1.6 trillion Unmet demand for trade finance

5

WHAT DOES A $1.6 TRILLION GAP LOOK LIKE?

• Americas: lowest rejection rate

• Asia: highest need, highest

rejections

US banks report low rejection rates

(for trade finance proposals)

6

Rejection share

45% 44% 20%

53% 35% 9%

Proposal share

SMEs

Large corporates

MNCs

Gaps by client

segment

7

IT IS NOT EXPECTED TO ABATE IN 2017

8

Cost of due diligence on a

partner bank (annual)

• 2016: $75,000

• 2017: $150,000 (e)

Impediments to expanding trade finance volumes

RESULT: EXCLUDED CLIENT SEGMENTS

9

WHAT HAPPENS

WHEN SMES DON’T GET FINANCED? Q2

10

REJECTION: CAPITAL MISALLOCATION

46

32

35

64

58

63

30

18

22

30

39

43

0 20 40 60 80

All respondents

Europe

LAC

North America

Africa

Asia

Required trade finance (% of trade-

dependent activities)

Trade dependent (% of total

business)

11

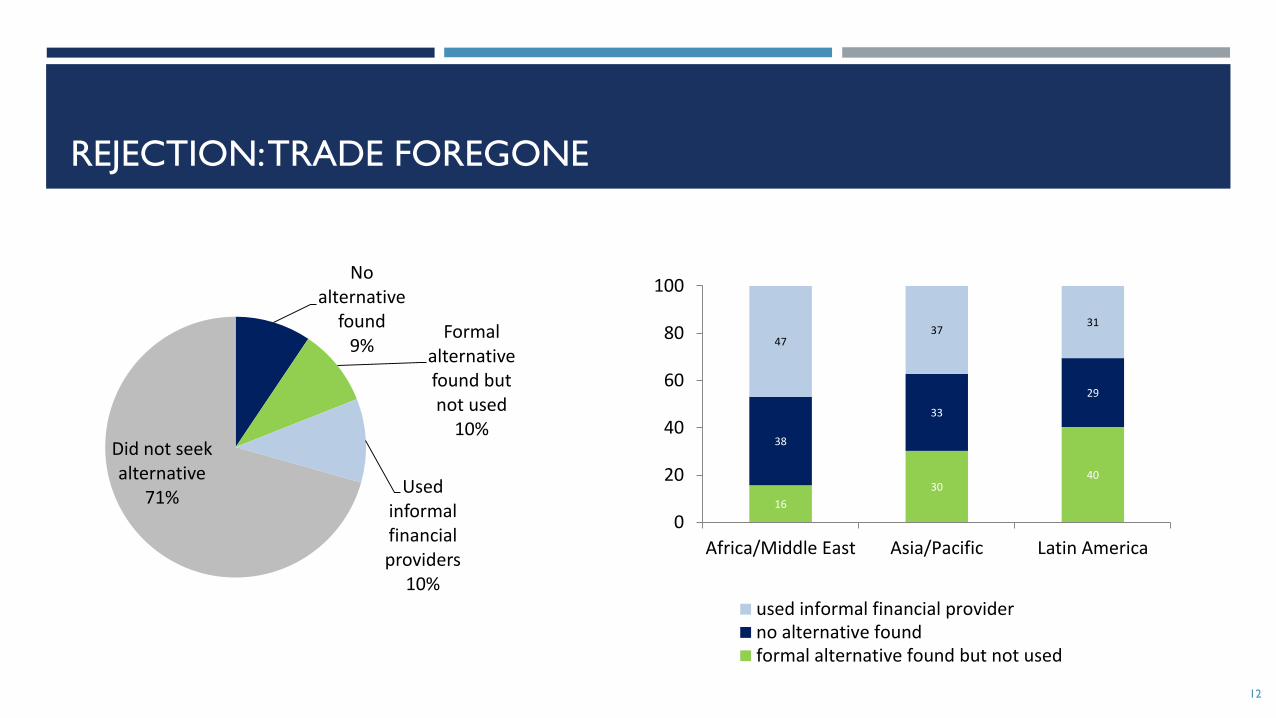

REJECTION: TRADE FOREGONE

No alternative

found 9%

Formal alternative found but not used

10%

Used informal financial providers

10%

Did not seek alternative

71% 16

30 40

38

33

29

47 37

31

0

20

40

60

80

100

Africa/Middle East Asia/Pacific Latin America

used informal financial providerno alternative foundformal alternative found but not used

12

IS FINTECH THE SOLUTION? Q3

13

Banks

Fintech

DIGITIZATION IS CHANGING 2 AREAS

Faster transactions

Increase efficiency

Reduce cost of providing

Reduce the cost of finance targets underserved

populations

Increase access to finance

not trade finance

Ban

ks

Fin

tech

14

DIGITIZATION LIMITED TO GLOBAL BANKS

15

• OCR

• Electronic

documents

RECOGNITION AND UPTAKE

• 70% firms unfamiliar with

Fintech

• Uptake for P2P highest

overall (54% in Africa)

16

USERS OF FINTECH ARE DISTINCT

No difference by firm size, sector, trade dependence or market with which they’re trading

0%

10%

20%

30%

40%

50%

60%

70%

rejection rate by banks propensity to seek

alternative when rejected

female ownership

fintech user non-users

27%

14%

32%

59%

43%

31%

• Higher rejection rates

by banks

• Higher propensity to

seek alternatives

• women-led firms more

likely to pursue digital

finance (35% vs 20%)

17

WHAT DOES ALL THIS MEAN

18

Cost reduction (banks)

Financial access (SMEs)

Size of the market (fintech)

WHAT DOES ALL THIS MEAN

19

FINTECH

is making inroads to trade

finance, creating new

visibility measures

PROFITABLITY increasing recognition that

SMEs are a potentially

profitable segment

DATA

shows no evidence that

SMEs as a client segment

are gaining

BANKS Still matter. Fintech is not

replacing traditional trade

finance

VISIBILITY

remains a problem for SMEs

Identify and scale up new

methods of credit assessment

REALIZING OPPORTUNITIES

20

Still matter

BANKS

Legal Entity Identifiers

Collateral registries for

movable assets

SMEs FINTECH