dinero banca luis daniel

TRANSCRIPT

Luis Daniel Ávila Cordero – Dinero y Banca – Máster en Economía de la E.A. – Universidad Rey juan Carlos

The Great Recession and Monetary Disequilibrium

W. William Woolsey

Presented by Luis Daniel Ávila Cordero

IntroducFon

• What happened in the Great Recession of 2008? An approach suggests that the collapse was caused by a monetary disequilibrium (the desired amount of money exceeded the exisAng quanAty of it)

• The individuals efforts to adjust their desired money holdings to actual money holdings caused disrupFve changes in interest rates, real producFon, amployment and income

Luis Daniel Ávila Cordero – Dinero y Banca – Máster en Economía de la E.A. – Universidad Rey juan Carlos

Part 1: Direct and Indirect Effects of Monetary Disequilibrium on Money Expenditures

Luis Daniel Ávila Cordero – Dinero y Banca – Máster en Economía de la E.A. – Universidad Rey juan Carlos

Direct Effects of monetary Disequilibrium on Money Expenditures

• Money is an asset serving as medium of exchange. Not only is held but also something that flows through cash balances.

• Shortage of money: individuals reduce expenditures in final goods

and nonmonetary assets. Firms adjust the expenditure of current cash flows on new capital goods à decrease in the demand for output. Excess of output is called Glut of goods

• The evidence for 2008 suggests that the quanAty of money was less than the demand to hold money.

• The adjustement would be possible if the prices of goods, services and salaries had dropped in proporAon with money expenditures but they conFnued to increase…

Luis Daniel Ávila Cordero – Dinero y Banca – Máster en Economía de la E.A. – Universidad Rey juan Carlos

Indirect Effects of Monetary Disequilibrium on Monetary Expenditures

• There are several ways to save rather than accumulate money. Nonmonetary assets as bonds, stocks or real estate can be purchased to those who need financing

• With less money, restricAons of expenditures or sales of

nonmonetary assets must conAnue unFl the demand to hold money adjust to the exisFng quanFty.

• Unfortunately, policies follow keynesian approach focusing

the impact of asset sales on the yields of them (especially bonds) driving consumpAon and investment down.

Luis Daniel Ávila Cordero – Dinero y Banca – Máster en Economía de la E.A. – Universidad Rey juan Carlos

Indirect Effects of Monetary Disequilibrium on Monetary Expenditures

Interest Rates and Long-‐Run Equilibrium • Interest rates are the prices that provide inter – temporal coordinaFon between

consumpFon and producFon aims. They depend on the supply of saving and demand for investment. Saving shiVs consumpAon from the present to the future.

• “Natural” interest rate equals saving and investment; Interest rates above

“natural”: incenAve to accumulate assets rather than spending in order to purchase more goods in the future.

• In a growing economy, added saving reflects a smaller decrease in relaFve spending on consumer goods now (smaller increase in absolute terms), and a larger increase in spending on capital goods now. The result is a larger increase in the producFon of consumer goos in the future (and viceversa)

• In a growing economy, the most plausible scenario is that the decreased demand for investment reflects a more rapid increase in spending on consumer goods now and smaller increase in the demand for capital goods.

Luis Daniel Ávila Cordero – Dinero y Banca – Máster en Economía de la E.A. – Universidad Rey juan Carlos

Indirect Effects of Monetary Disequilibrium on Monetary Expenditures

Luis Daniel Ávila Cordero – Dinero y Banca – Máster en Economía de la E.A. – Universidad Rey juan Carlos

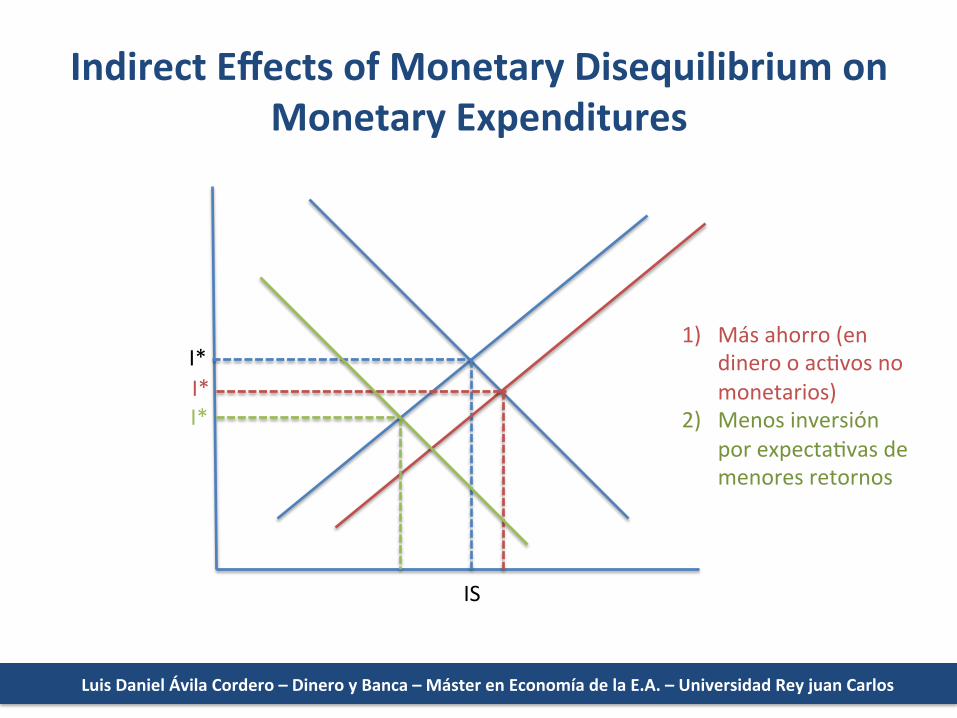

IS

I* 1) Más ahorro (en

dinero o acAvos no monetarios)

2) Menos inversión por expectaAvas de menores retornos

I* I*

Indirect Effects of Monetary Disequilibrium on Monetary Expenditures

• Keynes rejected classical account of the interest rate arguing that it assumed full employment of labor.

• Changes in employment and income influence saving and the level of real interest rate. So, natural interest rate would be the level of real interest rate consistent with saving equaling investment at a level of real output and income that matches the producFve capacity of the economy.

• This fact can be illustrated through a variaAon of “IS curve” (relaAonship between natural interest rate and the producAve capacity of the economy / negaFve between real interest rate and planned real expenditure)

• Increase in saving or decrease in investment reduce the natural interest rate.

Real interest rates below the natural interest rate create incenAves to spend beyond the producAve capacity of the economy. On the other hand, real interest rates above the natural interest rates, create incenAves to spend in a lower level compared to the producAve capacity of the economy: it generates a “glut of goods”

Luis Daniel Ávila Cordero – Dinero y Banca – Máster en Economía de la E.A. – Universidad Rey juan Carlos

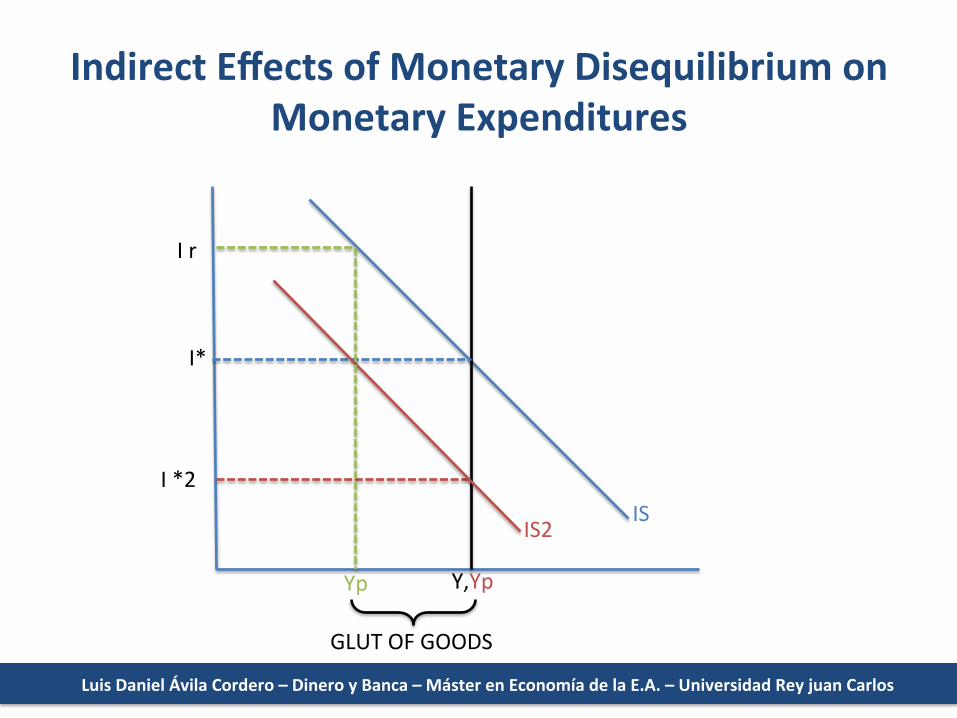

Indirect Effects of Monetary Disequilibrium on Monetary Expenditures

Luis Daniel Ávila Cordero – Dinero y Banca – Máster en Economía de la E.A. – Universidad Rey juan Carlos

I*

I *2

Y,Yp

I r

Yp

IS IS2

GLUT OF GOODS

Indirect Effects of Monetary Disequilibrium on Monetary Expenditures

The “Liquidity Effect” and Monetary Disequilibrium • Usual reacAon when facing a shortage of money is reducing purchases of financial

assets or selling part of the current holdings à lower prices and higher returns should be expected.

• If nominal yield of money is sAcked to zero, changes in nominal yields of assets impact the opportunity cost of holding money. I.e: Shortage of money à prices of bonds fall à interest rate rises VS yield on money transacAons fails to rise in proporAon à oportunity cost of holding money grow à money more abundant. But this neither guarantee increasing supply of saving or demand for investment, nor coordinate both automaFcally.

• The indirect effect of a shortage of money acFng on the prices and yields on financial assets tends to force the market insterest rate above the natural interest rate and reduce the real volume of expenditures to a general glut of goods

Luis Daniel Ávila Cordero – Dinero y Banca – Máster en Economía de la E.A. – Universidad Rey juan Carlos

Indirect Effects of Monetary Disequilibrium on Monetary Expenditures

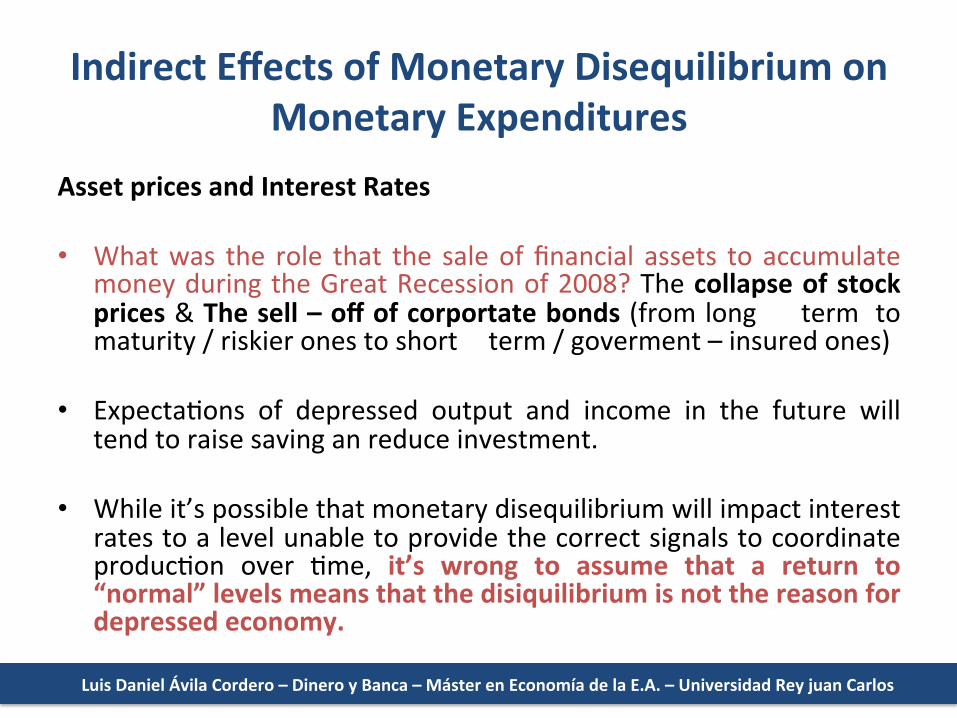

Asset prices and Interest Rates • What was the role that the sale of financial assets to accumulate

money during the Great Recession of 2008? The collapse of stock prices & The sell – off of corportate bonds (from long term to maturity / riskier ones to short term / goverment – insured ones)

• ExpectaAons of depressed output and income in the future will tend to raise saving an reduce investment.

• While it’s possible that monetary disequilibrium will impact interest rates to a level unable to provide the correct signals to coordinate producAon over Ame, it’s wrong to assume that a return to “normal” levels means that the disiquilibrium is not the reason for depressed economy.

Luis Daniel Ávila Cordero – Dinero y Banca – Máster en Economía de la E.A. – Universidad Rey juan Carlos

Part 2: Keynesian ExplanaFons of Depressed Money Expenditures and Recession

Luis Daniel Ávila Cordero – Dinero y Banca – Máster en Economía de la E.A. – Universidad Rey juan Carlos

Monetary Disequilibrium and the Paradox of Thrid

• Paradox of Thrid: Individual may increase saving by reduce consumpAon but and increase in saving in the economy can result in reduced money expenditures, reduced output and growing number of poors unable to save.

• RelaFon to monetary disequilibrium: that part of the income not spent (decreasing quanAty of money in the market) is saved (increasing demand to hold money by families and firms).

• It’s possible to sell output in order to accumulate the income as nonmonetary assets. Then there is a decrease in money expenditures on output without an incresase in the demand for money. Can this way of saving reproduce the paradox of thriV vicious circle? … but what’s up with the sellers of those assets?

• Money disequilibrium can be a consequence of other economic changes, i.e: changes in asset prices due to an increased demand, nonmonetary assets with yields lower than money’s as an incenAve to hold the last one…

Luis Daniel Ávila Cordero – Dinero y Banca – Máster en Economía de la E.A. – Universidad Rey juan Carlos

Money and Credit Confused

• Common errors on monetary market: Defined as Supply vs Demand of Loans / relaAonship between changes in the Supply of credit and money expenditures / relaAonship between delevering, reduced expenditures and output.

• If there’s an imbalance between the demand to hold money and the quanAty of money, reduced lending simply shids expenditures away from borrowers to the potenAal lenders, and repayments of exisAng debts shiVs expenditures away from debtors to the creditors

Luis Daniel Ávila Cordero – Dinero y Banca – Máster en Economía de la E.A. – Universidad Rey juan Carlos

Keynesian “MulFplier” and the Yeager effect

• “Paradox of Thrid” with a mulFplier effect: Saving reduce spending à potenAal sellers produce less à income and employment contract à less spending àless producAon, income, employment… and so on (progressive shortage of money in every stage of the process)

• This is nothing but a monetary disequilibrium without the

money • “Yeager effect”: mulAplier effect is only possible in a

context of monetary disequilibrium. As income and employment decrease, demand to hold money falls. We would need a surplus of money in balances to revert it.

Luis Daniel Ávila Cordero – Dinero y Banca – Máster en Economía de la E.A. – Universidad Rey juan Carlos

Monetary Disequilibrium and the Liquidity Trap

• There are situaAons in which monetary policy is ineffecFve to boost money expenditures.

• Problems related with the lower bound on interest rates must be connected with an excess demand for money. This derives in a glut of goods. The only plausible shortage to match a surplus of output is a shortage of money.

• The logic of the zero nominal bound is that if the interest rate becomes too low, people will hold money rather than lend.

Luis Daniel Ávila Cordero – Dinero y Banca – Máster en Economía de la E.A. – Universidad Rey juan Carlos

Part 3: Supply shocks and conclusions

Luis Daniel Ávila Cordero – Dinero y Banca – Máster en Economía de la E.A. – Universidad Rey juan Carlos

Supply Shocks and Monetary Disequilibrium

• The imbalance between the quanFty of money and the demand to hold money may be caused not only by reduced money expenditures but a decrease in potenFal output (a supply shock). Examples: poor harvest, disrupAon in oil supply or… lack of credit for investments

• Scenario #1: reduced income leads to an excess supply of money. When those balances are spent, demand and prices in final goods grow, so the demand for money increases unAl the equilibrium is reached (when people is saAsfied enough to hold exisAng quanAty of money)

• Scenario #2: decreased demand for homes VS increased demand for capital and consumer goods. à shiV in demand is similar to a decrease in producAve capacity so… fall in home producAon / boilenecks in capital and consumer goods. Gradually, when labor shiVs and appropiate capital goods are produced (because some factors are very specific and non tradable among sectors), output recovers.

Luis Daniel Ávila Cordero – Dinero y Banca – Máster en Economía de la E.A. – Universidad Rey juan Carlos

The monetary disiquilibrium approach conclusion

• What is monetary equilibrium? QuanAty of money = demand to hold money , so the monetary authority should keep it through adjusAng the quanAty of money to avoid a general glut of goods.

• Monetary policy task is to avoid monetary disequilibrium and keep money expenditures growing with the producAve capacity of the economy.

• Diagnosis: The decrease in money expenditures in the fall of 2008 was due to a

shortage of money VS the demand to hold money… • What should be done? Consistent with a laissez – faire altude, lelng the prices

fall to reach the equilibrium (painful but needed)… • AlternaFves? The FED increasing the quanAty of money enough to meet the

demand to hold money. To target a constant growth path for money expenditures keeping a responsible non -‐ inflaAonary pace…

• And how much base money should be created? This approach doesn’t consider quanAtaAve but qualitaAve judgements so, in this case (2008 great recession), the creaAon of of money by the FED should have been higher and earlier than it was.

Luis Daniel Ávila Cordero – Dinero y Banca – Máster en Economía de la E.A. – Universidad Rey juan Carlos

Luis Daniel Ávila Cordero – Dinero y Banca – Máster en Economía de la E.A. – Universidad Rey juan Carlos

The Great Recession and Monetary Disequilibrium

W. William Woolsey