dipartimento di politiche pubbliche e scelte collettive...

TRANSCRIPT

Dipartimento di Politiche Pubbliche e Scelte Collettive – POLIS Department of Public Policy and Public Choice – POLIS

Working paper n. 67

February 2006

Bank Ownership and Lending Behavior

Alejandro Micco and Ugo Panizza

UNIVERSITA’ DEL PIEMONTE ORIENTALE “Amedeo Avogadro” ALESSANDRIA

1

Bank Ownership and Lending Behavior

Alejandro Micco Ugo Panizza*

Abstract

This paper checks whether state-ownership of banks is correlated with lending behavior over the business cycle and finds that their lending is less responsive to macroeconomic shocks than the lending of private banks.

Keywords: State-owned banks; Credit Cycle

JEL Codes: G21; H11; E44

* Research Department, Inter-American Development Bank. [email protected]; [email protected]. We would like to thank an anonymous referee and Arturo Galindo for useful comments and Monica Yañez and Erwin Hansen for research assistance. The views expressed in this paper are the authors’ and do not necessarily reflect those of the Inter-American Development Bank. The usual caveats apply.

2

1. Introduction

While most of the existing literature on the role of state-owned banks focuses on their effect on

growth and financial development (La Porta et al., 2002), this paper tests whether state ownership

of banks is correlated with bank-lending behavior over the business cycle.1

There are four possible reasons why state-owned banks may stabilize credit. The first has

to do with the fact that their principal (the state) internalizes the benefits of a more stable

macroeconomic environment. Therefore, credit stabilization is part of the objective function of

state-owned banks. The second has to do with the fact that if bank failures are more likely during

recessions and if depositors think that public banks are safer than private banks (because of either

implicit or explicit full deposit insurance), the former can enjoy a more stable deposit base and

hence be better able to smooth credit. A third, less benign explanation, is that lower cyclicality is

due to the fact that managers of state-owned banks do not have a proper set of incentives and that

lower cyclicality is due to the behavior of “lazy” public bank managers. The fourth explanation

relates to the possibility that politicians may direct the lending of public banks in order to

maximize their probability of reelection (Dinc, 2004, finds that lending of state-owned banks is

correlated with the electoral cycle). It is not clear, however, if this would lead to credit

stabilization. Such result would require the assumption that the probability of recession is higher

during electoral years. This is the opposite of what is predicted by standard political business

cycle models.

2. Regressions Results

We use the following econometric specification:

( ) ( )( ) tjitjitjitj

tjitjtjitjtjitji

PUBELECTIONSIZEYGR

FORYGRPUBYGRGRL

,,,,,,

,,,2,,,1,,,

)*(*

**

εφδ

γγβα

+++

++++= (1)

Where tjiGRL ,, measures the growth rate of loans by bank i in country j at time t (measured as

the difference between log-loans at time t and log-loans at time t-1), iα is a bank fixed effect,

tj ,β is a country-year fixed effect that controls for all factors that are country-year specific. PUB

1 The literature on the relationship between bank ownership and bank performance (Demirgüç -Kunt and Huzinga, 2000, and Micco et al., 2004) is less related to questions addressed in this paper.

3

is a dummy variable that takes value 1 if more than 50 per cent of the bank is owned by the public

sector; FOR is a dummy variable that takes value 1 if more than 50 per cent of the bank is

foreign-owned; SIZE is a variable that measures relative average bank size (bank’s i average total

assets divided by average total assets of the banking system in country j); ELECTION is a dummy

variable that takes value 1 if country j has a major election in year t;2 tjYGR , measures GDP

growth of country j at time t and proxies for macroeconomic shocks. The interactions

tjitj PUBYGR ,,, * and tjitj FORYGR ,,, * measure how lending of public and foreign banks react

(relative to private domestically owned banks) to shocks (the main effect of tjYGR , is controlled

for by tj ,β ). The interaction between bank size and GDP growth ( itj SIZEYGR *, ) is included to

control for a possible correlation between ownership type and bank size. We also recognize that,

in presence of a correlation between political and business cycle, 1γ might capture the effect of

political lending (Dinc, 2004) and control for political lending by including the interaction

between public ownership and the election dummy ( tjitj PUBELECTION ,,, * ).3

We use a new dataset based on Bankscope but with a more accurate coding of the

ownership variable (see Micco et al., 2004, for details). The original dataset covers the 1995-2002

period and includes 49,804 observations (corresponding to 6,628 banks), but the dataset used in

this paper is significantly smaller (25,325 observations). There are four reasons for this drop in

the number of observations: (i) As we work with growth rates, we lose at least one observation

for each bank;4 (ii) We only include banks for which all the dependent variables used in all

regressions are available. (iii) We drop all country-years for which we do not have at least 5

banks; (iv) We drop outliers by excluding the top and bottom 2 percent of observations for each

dependent variable and by dropping all observations in which bank-level loan growth is bigger

than 100 percent (in absolute value) and aggregate loan growth is bigger than 50 percent.

To make sure that our results are not driven by the behavior of few countries with a large

number of banks, we weight each observation by the bank’s share in total bank assets (this is

equivalent to giving each country the same weight).

2 We define major elections as legislative elections in countries with a parliamentary system and presidential elections in a country with a presidential system. 3 We would like to thank an anonymous referee for this suggestion. 4 We may lose more than one observation per bank because whenever a bank changes ownership we code it as a new bank. We also drop all the bank-year observations in which there is a change in ownership.

4

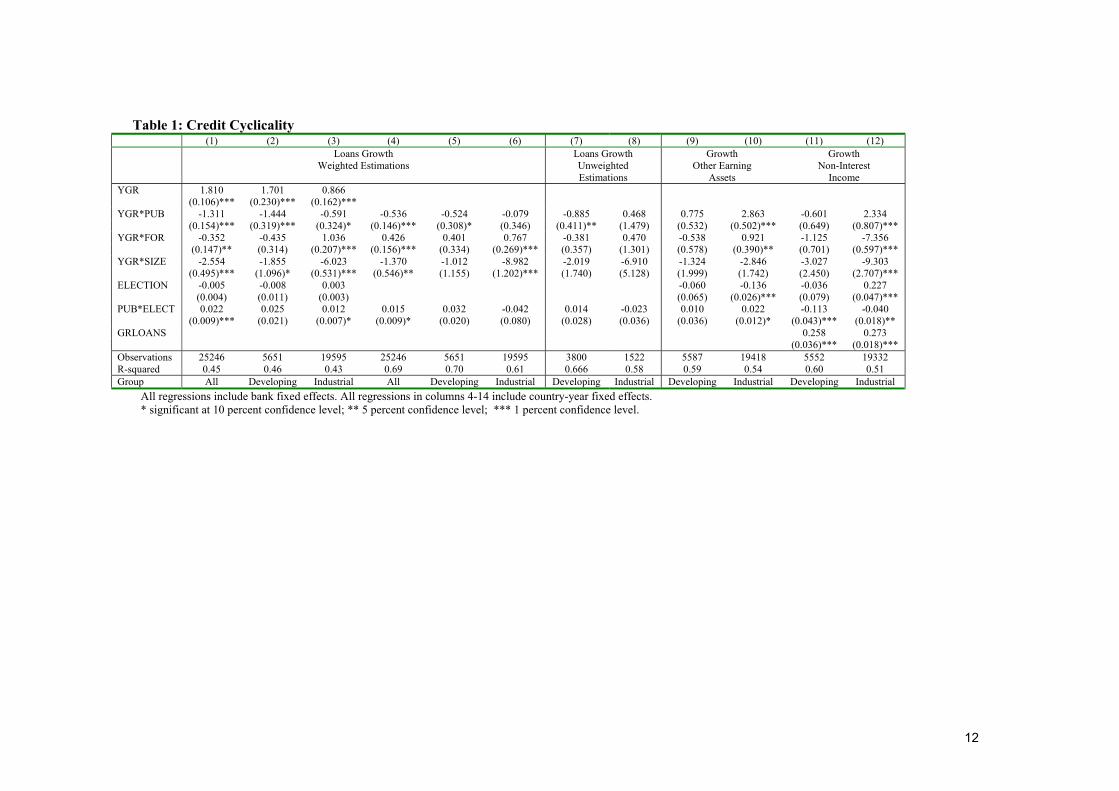

Regression results are reported in Table 1. We will focus the discussion of the results on

our main parameter of interest ( 1γ ).5 A negative value of this coefficient indicates that state-

owned banks smooth credit; a positive coefficient indicates the opposite. We start by estimating

the model of Equation (1) by substituting the country-year fixed effects with the main effect of

GDP growth (columns 1-3). We do this to show that loan growth is indeed correlated with

macroeconomic shocks as measured by GDP growth. Column 1 shows that a one percent increase

in GDP is associated with a 1.8 percent increase in lending of private domestic banks. The

coefficient of PUBYGR* is –1.3, indicating that lending of state-owned banks is much less

procyclical than that of private domestic banks. Column 2 focuses on developing countries and

finds results that are essentially identical to those of Column 1. Column 3 focuses on industrial

countries and shows that credit cyclicality is much lower in this sub-sample (the elasticity goes

from 1.8 to 0.9), but also in this case we find that the lending activity of state-owned banks is less

procyclical than that of private banks.

In all three regressions we that find that tjitj PUBELECTION ,,, * has a positive

coefficient and point estimates similar to what found by Dinc (2004). While this provides some

evidence for political lending, it is worth mentioning that the coefficients are rarely statistically

significant.6

In columns 4-6 we estimate the specification described by Equation 1 (as we include

country-year fixed effects we cannot include the main effect of YGR). As before, we find that

that state-owned bank lending is less pro-cyclical than lending by domestic private banks.

Column 4 indicates that state-owned banks are 50 percent less procyclical than domestic private

banks. Column 5 shows that the results for the sub-sample of developing countries are basically

identical to the results for the whole sample. This is not surprising, because our estimation

method gives the same weight to each country and three quarters of our sample consists of

developing countries (hence, from now on we will not discuss the regressions that include both

developing and industrial countries). Column 6 shows that in industrial countries the coefficient is

5 While we control for foreign ownership we do not discuss the cyclicality of foreign lending because this would require a more complex model (Galindo et al. 2004). All the results discussed here are robust to including the lagged dependent variable and to estimating the model in levels. 6 Like Dinc (2004) we find that the coefficients are larger for developing countries but unlike Dinc (2004) we never find that the coefficient is significant in developing countries and not significant in industrial countries (sometimes we find the opposite). This is probably due to differences in the sample. While Dinc (2004) focuses on 36 countries and 2058 observations, our sample includes 119 countries and more than 25,000 observations. The main difference consists in the fact that Dinc (2004) focuses on industrial and emerging market countries and our sample of developing countries includes both emerging market and low income countries.

5

much smaller and not statistically significant indicating that lending of state-owned banks is not

less procyclical than that of domestic private banks.

The results of columns 5 and 6 are interesting because they indicate that lending of public

banks located in developing countries is not more pro-cyclical than lending of public banks

located in industrial counties.7 This is in contrast with the well-known finding that monetary and

fiscal policies are countercyclical in industrial countries and procyclical in developing countries

(see Gavin and Perotti, 1997, and Kaminsky et al., 2004, for empirical evidence and Guerson,

2005, for a theoretical model).

Columns 7 and 8 test the robustness of the previous results by using estimations without

weights.8 While the results for developing countries are similar to the ones described before, we

now find that 1γ is large and positive (but not statistically significant) in the sub-sample of

industrial countries.

2.1 Do they smooth or are they just lazy?

So far we provided evidence in support of the idea that state-owned banks play a smoothing role.

A less benign interpretation would be that public banks managers are just “lazy” and, lacking

incentives to maximize profits, they do not aggressively look for lending opportunities during

expansions and do not cut lending during recessions when risk increases. A possible way to

discriminate the “useful smoothers” hypothesis from the “lazy managers” hypothesis is to

compare how the non-lending activities of public and private banks vary over the business cycle.

The last four columns of Table 1 report regressions similar to those of columns 5 and 6 but

substitute loans growth with the growth rate in other earning assets (earning assets which are

different from loans) and the growth rate of non-interest income (income that derives from fees

and services and not from lending activities). The key idea is that, if the previous results where

driven by the behavior of lazy public bank managers, columns 9-12 should yield results that are

similar to those of columns 5 and 6 (there is no reason why managers of public banks should have

a mandate to stabilize non-lending activities).

7 While the estimations of columns 5 and 6 suggest that lending of public banks located in developing countries is less procyclical than lending of public banks located in industrial countries, a formal test shows that the two coefficients are not significantly different from each other (results available upon request). 8 To avoid problems related to including a large number of small banks, we drop all banks which have assets that are less than 1 percent of total bank assets in the country. This reduces our sample to 5322 observations. In a previous version of the paper, we also tested for reverse causality (countries that have a large share of state-owned banks may be subject to smaller shocks because of the smoothing role

6

Columns 9 and 10 show that the growth rate of other earning assets held by state-owned

banks is never less procyclical than that of private domestic banks. In fact, in the case of

industrial countries, we find that it is significantly more procyclical (possibly due to the fact that

state-owned banks smooth more lending than deposits and hence need to substitute lending with

other earning assets).

When we focus on non-interest income, we find no statistically significant difference

between the behavior of public and private banks located in developing countries and, as in the

case of other earning assets, we find that public banks located in industrial countries are more

procyclical than their private counterparts.9

While our results tend to be consistent with the credit smoothing interpretation, it is

difficult to draw strong conclusions from the exercise described above (other earning assets and

non-interest income are defined as residual entities and may mean very different things in

different types of banks). Hence, we cannot rule out that the observed behavior of public bank

managers is driven by either “laziness” or political motives (Sapienza, 2004, documents that

lending of Italian public banks is mainly driven by political motives).

3. Conclusions

This paper provides evidence for the fact that state-owned banks may play a credit smoothing

role. It shows that their lending is less responsive to macroeconomic shocks than the lending of

private banks (both domestically and foreign-owned). This suggests that state-owned banks could

play a useful role in the transmission of monetary policy (this is in contrast with the findings of

Cecchetti and Krause, 2001, who, however, focus on a different test).

One interesting finding is that lending of public banks located in developing countries

seem to be less procyclical (or at least not more procyclical) than lending of public banks located

in industrial countries. This suggests that public bank lending in developing countries has a very

different response to the business cycle with respect to monetary policy.10

In future research it would be interesting to explore the determinants of the relationship

between bank ownership and credit cyclicality. Is it really true that public bank managers try to

performed by these banks) by replacing GDP growth with its exogenous component. We found that controlling for reverse causality strengthens our basic findings of a smoothing role of state owned banks. 9 In the regression for non-interest income we control for loans growth because some fees might be related to lending activity. The results are unchanged if we drop this control. When we focus on growth of other earning assets, we find that the coefficient for YGR*PUB in the industrial countries regression is not significantly different form that of the developing countries regression. However, the two coefficients are significantly different in the regression for non-interest income (full results available upon request).

7

smooth the business cycle or are there other motives that lead to the behavior documented in this

paper? It would also be interesting to test whether the smoothing behavior documented in this

paper is optimal or is just a waste of resources. This last question is particularly important for at

least two reasons. First of all, public banks might increase credit but direct it to sectors with low

productivity and hence lead to a misallocation of resources. Second, the methodology used in this

paper does not allow to investigate the general equilibrium effects of our results. It may be

possible that state-owned bank lending crowds out private lending and does not affect aggregate

lending during the business cycle. Analyzing such a hypothesis goes beyond the purpose of this

paper because it would require moving from micro to macro data leading to much more serious

endogeneity issues.

10 We would like to thank an anonymous referee for suggesting this interpretation.

8

References

Cecchetti, S., and S. Krause. 2001. “Structure, Macroeconomic Stability and Monetary Policy.” NBER WP 8354. Demirgüç-Kunt, A. and H. Huizinga. 2000. “Determinants of Commercial Bank Interest Margins and Profitability: Some International Evidence.” World Bank Economic Review, 13: 379-408. Dinc, S. (2004), "Politicians and Banks: Political Influences on Government-Owned Banks in Emerging Countries," Journal of Financial Economics, forthcoming. Galindo, A., Micco, A. and Powell, A. 2003. “Loyal Lending or Fickle Financing: Foreign Banks in Latin America.” Mimeo IADB. Gavin M. and Perotti R. 1997. “Fiscal Policy in Latin America.” NBER Macroeconomics Annual Cambridge, MA: MIT Press, pp. 11-61 Guerson A. 2005. “On the Optimality of Procyclical Fiscal Policy when the Government can Default,” mimeo The Word Bank Kaminsky G., Reinhart C. and Vegh C. 2004. ”When it Rains it Pours: Procyclical Capital Flows and Macroeconomic Policies. ” NBER WP 10780. La Porta, R., F. López-de-Silanes, and A. Shleifer. 2002. “Government Ownership of Banks.” Journal of Finance 57: 265-301. Micco, A. U. Panizza, and M. Yañez 2004. “Bank Ownership and Performance.” mimeo, Inter-American Development Bank. Sapienza, P. 2004. “The Effects of Government Ownership on Bank Lending.” Journal of Financial Economics. Vol. 72 pp. 357-384.

9

Appendix: Description of the data11 The purpose of this appendix is to describe the steps used in constructing the dataset used in this

paper. As mentioned in the text, our main source of data is Bankscope (BSC) but we do a lot of

additional work to avoid duplication and improve the coding of the ownership variables. We

obtain data for the 1995-1999 period from the June 2001 update of BSC and data for the 2000-

2002 period from the February 2004 update of BSC. Processing the date required two main steps

that we describe below.

Avoiding duplications. For most banks, BSC reports balance sheet data at both the

consolidated and unconsolidated levels. In order to avoid duplications, it is necessary to use only

one of the two definitions. This could be easily done by just dropping either all the consolidated

or unconsolidated statements if BSC reported both type of statements for all banks. However,

some banks only have a consolidated statement and other only have an unconsolidated statement,

hence dropping just one category would lead to loss of information. Furthermore, it is impossible

to automatically keep the, say, unconsolidated statement if the consolidated is missing because, in

some cases, there are slight changes in the reported name of the bank when one moves across

different levels of consolidation. An even more difficult problem to solve is that in some cases

BSC reports information for the same bank several times. This is especially the case at time of

mergers. An example may be helpful here. Consider the case of INTESA, the largest Italian

banking group. INTESA was created in 1998 with the merger of CARIPLO and

AMBROVENETO. In 1999, Banca Commerciale Italiana (COMIT) joined the INTESA group

and in 2001 COMIT completely merged with INTESA that took the name of INTESABCI. As of

2000, BSC reports data for (i) COMIT; (ii) AMBROVENETO; (iii) CARIPLO; (iv)

INTESABCI. Clearly, considering all these four banks would lead to a large overestimation of

Italian banking assets. To address this problem, we make use of a variable included in BSC that

ranks banks within a country and it is built in order to limit duplications (the variable name is

CTRYRANK). In the above case, CTRYRANK takes value one for INTESABCI (recognizing

that this is the largest bank in the country) 5 for CARIPLO and 12 for AMBROVENETO.

COMIT is not ranked (CTRYRANK takes the value NR). Therefore, dropping the banks that are

coded as non-ranked can help us in avoiding duplication. There are, however, still two problems

with this strategy. First, the dataset would still include INTESABCI and two of its component

(AMBROVENETO and CARIPLO). Second, the ranking variable refers to the last year, and

hence if we were to drop all the banks that are not ranked, we would drop COMIT also for the

11 This appendix is from Micco et al. (2004) and it is introduced for the ease of the referees. We plan to

10

1995-1999 period. To address this issue, we adopted looked at all the banks that have assets that

are greater than the country average that are coded as non-ranked and explored their merger

history. This led to a massive amount of recoding that helped us to include in the dataset most of

the relevant information and avoid duplications.12 After eliminating duplications, we end up with

a total of 49,804 observations, corresponding to a number of banks that ranges between 5,445 (in

1995) and 6,628 (in 2001). Banks located in industrial countries represent approximately 70

percent of total observations and banks located in developing countries the remaining 30 percent.

It is interesting to note that the share of banks located in developing countries increased by two

percentage points between 1995 and 2002.

Coding Ownership BSC includes an ownership variable (measuring whether a given bank

is owned by the public sector or by foreign investors) but this variable has limited coverage

(question for Monica what percentage of banks are coded in BSC) and is only available for the

current year (so BSC does not provide ownership history). Therefore, coding ownership history

require to look at one bank at a time (we use different sources, the internet, bank websites,

publications like Euromoney, or directly calling experts in a given country), as this is a

particularly time consuming and difficult endeavor and the cost of coding all banks included in

the dataset would have been too high, we decided to adopt some cut-off points under which a

bank would not be coded. The cut-off was as follows. In all countries we coded the 10 largest

banks (this is the strategy followed by La Porta et al., 2002) and, if these banks represented less

that 75 percent of total assets of the banking system we coded all the banks up to 75 percent of

total assets of the banking system. In Latin American and industrial countries, we coded the

larges 20 banks. Again, if these 20 banks represented less that 75 percent of total assets of the

banking system, we coded up to 75 percent of assets of the banking system. If a bank was not

among the top twenty or in the 75th percentile but the coding was obvious (for instance in the

case of foreign branches) it was also coded. 13

In coding ownership, we followed the same strategy of La Porta et al. (2002) and

assumed that if X percent of bank A is owned by company B and that Y percent of company B is

owned by a foreign company (alternately state owned), then we code bank A as being X*Y

drop this appendix from the final version of the paper. 12 In the case of the example described above, we adopted the following strategy. We re-ranked (and hence included in the dataset) COMIT from 1995 to 1999 and de-ranked (and hence excluded from the dataset) Ambroveneto and CARIPLO for 2000-2002 and Intesa BCI for 1995-1999. After dropping the non-ranked bank we end up with three banks (COMIT, Ambroveneto and CARIPLO) operating for the 1995-1999 period and one banks (IntesaBCI) operating for the 2000-2002 period. 13 Even with this cut-off, coding ownership required two months of work of a full-time research assistant.

11

percent foreign (state) owned (in order to code ownership, we always went back at least two steps

in the ownership structure).

12

Table 1: Credit Cyclicality (1) (2) (3) (4) (5) (6) (7) (8) (9) (10) (11) (12)

Loans Growth Weighted Estimations

Loans Growth Unweighted Estimations

Growth Other Earning

Assets

Growth Non-Interest

Income YGR 1.810 1.701 0.866 (0.106)*** (0.230)*** (0.162)*** YGR*PUB -1.311 -1.444 -0.591 -0.536 -0.524 -0.079 -0.885 0.468 0.775 2.863 -0.601 2.334 (0.154)*** (0.319)*** (0.324)* (0.146)*** (0.308)* (0.346) (0.411)** (1.479) (0.532) (0.502)*** (0.649) (0.807)*** YGR*FOR -0.352 -0.435 1.036 0.426 0.401 0.767 -0.381 0.470 -0.538 0.921 -1.125 -7.356 (0.147)** (0.314) (0.207)*** (0.156)*** (0.334) (0.269)*** (0.357) (1.301) (0.578) (0.390)** (0.701) (0.597)*** YGR*SIZE -2.554 -1.855 -6.023 -1.370 -1.012 -8.982 -2.019 -6.910 -1.324 -2.846 -3.027 -9.303 (0.495)*** (1.096)* (0.531)*** (0.546)** (1.155) (1.202)*** (1.740) (5.128) (1.999) (1.742) (2.450) (2.707)*** ELECTION -0.005 -0.008 0.003 -0.060 -0.136 -0.036 0.227 (0.004) (0.011) (0.003) (0.065) (0.026)*** (0.079) (0.047)*** PUB*ELECT 0.022 0.025 0.012 0.015 0.032 -0.042 0.014 -0.023 0.010 0.022 -0.113 -0.040 (0.009)*** (0.021) (0.007)* (0.009)* (0.020) (0.080) (0.028) (0.036) (0.036) (0.012)* (0.043)*** (0.018)** GRLOANS 0.258 0.273 (0.036)*** (0.018)*** Observations 25246 5651 19595 25246 5651 19595 3800 1522 5587 19418 5552 19332 R-squared 0.45 0.46 0.43 0.69 0.70 0.61 0.666 0.58 0.59 0.54 0.60 0.51 Group All Developing Industrial All Developing Industrial Developing Industrial Developing Industrial Developing Industrial

All regressions include bank fixed effects. All regressions in columns 4-14 include country-year fixed effects. * significant at 10 percent confidence level; ** 5 percent confidence level; *** 1 percent confidence level.

Working Papers The full text of the working papers is downloadable at http://polis.unipmn.it/

*Economics Series **Political Theory Series ε Al.Ex Series

2006 n.67* Alejandro Micco and Ugo Panizza: Bank ownership and lending behavior

2006 n.66* Angela Fraschini: Fiscal federalism in big developing countries: China and India

2006 n.65* Corrado Malandrino: La discussione tra Einaudi e Michels sull'economia pura e sul metodo della storia delle dottrine economiche

2006 n.64ε Stefania Ottone: Fairness: a survey

2006 n.63* Andrea Sisto: Propensity Score matching: un'applicazione per la creazione di un database integrato ISTAT-Banca d'Italia

2005 n.62* P. Pellegrino: La politica sanitaria in Italia: dalla riforma legislativa alla riforma costituzionale

2005 n.61* Viola Compagnoni: Analisi dei criteri per la definizione di standard sanitari nazionali

2005 n.60ε Guido Ortona, Stefania Ottone and Ferruccio Ponzano: A simulative assessment of the Italian electoral system

2005 n.59ε Guido Ortona and Francesco Scacciati: Offerta di lavoro in presenza di tassazione: l'approccio sperimentale

2005 n.58* Stefania Ottone and Ferruccio Ponzano, An extension of the model of Inequity Aversion by Fehr and Schmidt

2005 n.57ε Stefania Ottone, Transfers and altruistic punishment in Solomon's Game experiments

2005 n. 56ε Carla Marchese and Marcello Montefiori, Mean voting rule and strategical behavior: an experiment

2005 n.55** Francesco Ingravalle, La sussidiarietà nei trattati e nelle istituzioni politiche dell'UE.

2005 n. 54* Rosella Levaggi and Marcello Montefiori, It takes three to tango: soft budget constraint and cream skimming in the hospital care market

2005 n.53* Ferruccio Ponzano, Competition among different levels of government: the re-election problem.

2005 n.52* Andrea Sisto and Roberto Zanola, Rationally addicted to cinema and TV? An empirical investigation of Italian consumers .

2005 n.51* Luigi Bernardi and Angela Fraschini, Tax system and tax reforms in India

2005 n.50* Ferruccio Ponzano, Optimal provision of public goods under imperfect intergovernmental competition.

2005 n.49* Franco Amisano e Alberto Cassone, Proprieta’ intellettuale e mercati: il ruolo della tecnologia e conseguenze microeconomiche

2005 n.48* Tapan Mitra e Fabio Privileggi, Cantor Type Attractors in Stochastic Growth Models

2005 n.47ε Guido Ortona, Voting on the Electoral System: an Experiment

2004 n.46ε Stefania Ottone, Transfers and altruistic Punishments in Third Party Punishment Game Experiments.

2004 n.45* Daniele Bondonio, Do business incentives increase employment in declining areas? Mean impacts versus impacts by degrees of economic distress.

2004 n.44** Joerg Luther, La valorizzazione del Museo provinciale della battaglia di Marengo: un parere di diritto pubblico

2004 n.43* Ferruccio Ponzano, The allocation of the income tax among different levels of government: a theoretical solution

2004 n.42* Albert Breton e Angela Fraschini, Intergovernmental equalization grants: some fundamental principles

2004 n.41* Andrea Sisto, Roberto Zanola, Rational Addiction to Cinema? A Dynamic Panel Analisis of European Countries

2004 n.40** Francesco Ingravalle, Stato, groβe Politik ed Europa nel pensiero politico di F. W. Nietzsche

2003 n.39ε Marie Edith Bissey, Claudia Canegallo, Guido Ortona and Francesco Scacciati, Competition vs. cooperation. An experimental inquiry

2003 n.38ε Marie-Edith Bissey, Mauro Carini, Guido Ortona, ALEX3: a simulation program to compare electoral systems

2003 n.37* Cinzia Di Novi, Regolazione dei prezzi o razionamento: l’efficacia dei due sistemi di allocazione nella fornitura di risorse scarse a coloro che ne hanno maggiore necessita’

2003 n. 36* Marilena Localtelli, Roberto Zanola, The Market for Picasso Prints: An Hybrid Model Approach

2003 n. 35* Marcello Montefiori, Hotelling competition on quality in the health care market.

2003 n. 34* Michela Gobbi, A Viable Alternative: the Scandinavian Model of “Social Democracy”

2002 n. 33* Mario Ferrero, Radicalization as a reaction to failure: an economic model of islamic extremism

2002 n. 32ε Guido Ortona, Choosing the electoral system – why not simply the best one?

2002 n. 31** Silvano Belligni, Francesco Ingravalle, Guido Ortona, Pasquale Pasquino, Michel Senellart, Trasformazioni della politica. Contributi al seminario di Teoria politica

2002 n. 30* Franco Amisano, La corruzione amministrativa in una burocrazia di tipo concorrenziale: modelli di analisi economica.

2002 n. 29* Marcello Montefiori, Libertà di scelta e contratti prospettici: l’asimmetria informativa nel mercato delle cure sanitarie ospedaliere

2002 n. 28* Daniele Bondonio, Evaluating the Employment Impact of Business Incentive

Programs in EU Disadvantaged Areas. A case from Northern Italy

2002 n. 27** Corrado Malandrino, Oltre il compromesso del Lussemburgo verso l’Europa federale. Walter Hallstein e la crisi della “sedia vuota”(1965-66)

2002 n. 26** Guido Franzinetti, Le Elezioni Galiziane al Reichsrat di Vienna, 1907-1911

2002 n. 25ε Marie-Edith Bissey and Guido Ortona, A simulative frame to study the integration of defectors in a cooperative setting

2001 n. 24* Ferruccio Ponzano, Efficiency wages and endogenous supervision technology

2001 n. 23* Alberto Cassone and Carla Marchese, Should the death tax die? And should it leave an inheritance?

2001 n. 22* Carla Marchese and Fabio Privileggi, Who participates in tax amnesties? Self-selection of risk-averse taxpayers

2001 n. 21* Claudia Canegallo, Una valutazione delle carriere dei giovani lavoratori atipici: la fedeltà aziendale premia?

2001 n. 20* Stefania Ottone, L'altruismo: atteggiamento irrazionale, strategia vincente o

amore per il prossimo?

2001 n. 19* Stefania Ravazzi, La lettura contemporanea del cosiddetto dibattito fra Hobbes e Hume

2001 n. 18* Alberto Cassone e Carla Marchese, Einaudi e i servizi pubblici, ovvero come contrastare i monopolisti predoni e la burocrazia corrotta

2001 n. 17* Daniele Bondonio, Evaluating Decentralized Policies: How to Compare the Performance of Economic Development Programs across Different Regions or

States.

2000 n. 16* Guido Ortona, On the Xenophobia of non-discriminated Ethnic Minorities

2000 n. 15* Marilena Locatelli-Biey and Roberto Zanola, The Market for Sculptures: An Adjacent Year Regression Index

2000 n. 14* Daniele Bondonio, Metodi per la valutazione degli aiuti alle imprse con specifico target territoriale

2000 n. 13* Roberto Zanola, Public goods versus publicly provided private goods in a two-class economy

2000 n. 12** Gabriella Silvestrini, Il concetto di «governo della legge» nella tradizione repubblicana.

2000 n. 11** Silvano Belligni, Magistrati e politici nella crisi italiana. Democrazia dei

guardiani e neopopulismo

2000 n. 10* Rosella Levaggi and Roberto Zanola, The Flypaper Effect: Evidence from the

Italian National Health System

1999 n. 9* Mario Ferrero, A model of the political enterprise

1999 n. 8* Claudia Canegallo, Funzionamento del mercato del lavoro in presenza di informazione asimmetrica

1999 n. 7** Silvano Belligni, Corruzione, malcostume amministrativo e strategie etiche. Il ruolo dei codici.

1999 n. 6* Carla Marchese and Fabio Privileggi, Taxpayers Attitudes Towaer Risk and

Amnesty Partecipation: Economic Analysis and Evidence for the Italian Case.

1999 n. 5* Luigi Montrucchio and Fabio Privileggi, On Fragility of Bubbles in Equilibrium Asset Pricing Models of Lucas-Type

1999 n. 4** Guido Ortona, A weighted-voting electoral system that performs quite well.

1999 n. 3* Mario Poma, Benefici economici e ambientali dei diritti di inquinamento: il caso della riduzione dell’acido cromico dai reflui industriali.

1999 n. 2* Guido Ortona, Una politica di emergenza contro la disoccupazione semplice, efficace equasi efficiente.

1998 n. 1* Fabio Privileggi, Carla Marchese and Alberto Cassone, Risk Attitudes and the Shift of Liability from the Principal to the Agent

Department of Public Policy and Public Choice “Polis” The Department develops and encourages research in fields such as:

• theory of individual and collective choice; • economic approaches to political systems; • theory of public policy; • public policy analysis (with reference to environment, health care, work, family, culture,

etc.); • experiments in economics and the social sciences; • quantitative methods applied to economics and the social sciences; • game theory; • studies on social attitudes and preferences; • political philosophy and political theory; • history of political thought.

The Department has regular members and off-site collaborators from other private or public organizations.

Instructions to Authors

Please ensure that the final version of your manuscript conforms to the requirements listed below:

The manuscript should be typewritten single-faced and double-spaced with wide margins.

Include an abstract of no more than 100 words. Classify your article according to the Journal of Economic Literature classification system. Keep footnotes to a minimum and number them consecutively throughout the manuscript with superscript Arabic numerals. Acknowledgements and information on grants received can be given in a first footnote (indicated by an asterisk, not included in the consecutive numbering). Ensure that references to publications appearing in the text are given as follows: COASE (1992a; 1992b, ch. 4) has also criticized this bias.... and “...the market has an even more shadowy role than the firm” (COASE 1988, 7). List the complete references alphabetically as follows: Periodicals: KLEIN, B. (1980), “Transaction Cost Determinants of ‘Unfair’ Contractual Arrangements,” American Economic Review, 70(2), 356-362. KLEIN, B., R. G. CRAWFORD and A. A. ALCHIAN (1978), “Vertical Integration, Appropriable Rents, and the Competitive Contracting Process,” Journal of Law and Economics, 21(2), 297-326. Monographs: NELSON, R. R. and S. G. WINTER (1982), An Evolutionary Theory of Economic Change, 2nd ed., Harvard University Press: Cambridge, MA. Contributions to collective works: STIGLITZ, J. E. (1989), “Imperfect Information in the Product Market,” pp. 769-847, in R. SCHMALENSEE and R. D. WILLIG (eds.), Handbook of Industrial Organization, Vol. I, North Holland: Amsterdam-London-New York-Tokyo. Working papers: WILLIAMSON, O. E. (1993), “Redistribution and Efficiency: The Remediableness Standard,”

Working paper, Center for the Study of Law and Society, University of California, Berkeley.