diploma thesis final - assaif islamic... · liquidity management ... daruah doctrine of necessity...

TRANSCRIPT

GEORG-SIMON-OHM-HOCHSCHULE NÜRNBERG

Islamic banking – a worthwhile challenge for German banks?

The current supply situation of Islamic financial products in selected European markets and potential domestic market demand in

Germany.

Diploma Thesis

submitted to obtain the academic agree

“Diplom Betriebswirt (FH)”

Faculty of International Business

Prof. Dr. Klaus Stocker

handed in by

Kati Colditz

Matriculation Number: 2018613

Lößnitzer Straße 57

08297 Zwönitz

Nuremberg, 3 March 2009

ii

CONTENTS

FIGURES .................................................................................................................................................... VI

TABLES .................................................................................................................................................... VIII

GLOSSARY OF ARABIC TERMS..................................................................................................................... IX

ABSTRACT ................................................................................................................................................. XI

INTRODUCTION ........................................................................................................................................... 1

FOUNDATIONS AND BASIC PRINCIPLES OF ISLAMIC BANKING ....................................................................... 3

1.1. ISLAMIC LEGAL AND ECONOMIC SYSTEM ............................................................................................................. 3

1.1.1. Shariah and Fiqh .............................................................................................................................. 3

1.1.2. The four root transactions and the concept of partnership ............................................................. 5

1.1.3. Religious principles guiding investment behavior ........................................................................... 5

1.2. ISLAMIC FINANCING TECHNIQUES AND PRODUCTS ................................................................................................ 9

1.2.1 Equity-based financing techniques ................................................................................................ 10

1.2.2 Debt-based financing techniques .................................................................................................. 13

1.2.3 Leasing ........................................................................................................................................... 15

1.2.4 Capital market instruments ........................................................................................................... 17

1.2.5 Funding operations/ Accounts ....................................................................................................... 24

1.2.6 Takaful ........................................................................................................................................... 26

1.2.7 Use of Islamic financing techniques and products and profitability .............................................. 28

1.3. GOVERNANCE AND COMPLIANCE STRUCTURE OF ISLAMIC BANKS ........................................................................... 29

1.3.1. Shariah Supervisory Board standards ............................................................................................ 29

1.3.2. Characteristics of a Shariah Supervisory Board ............................................................................. 30

1.3.3. Functions of a Shariah Supervisory Board ..................................................................................... 31

1.3.4. Product innovation process ........................................................................................................... 32

1.3.5. Inconsistency of fatawa ................................................................................................................. 33

1.4. REGULATORY FRAMEWORK ........................................................................................................................... 34

1.4.1. Standardization and Harmonization.............................................................................................. 34

1.4.2. Regulation ..................................................................................................................................... 36

1.4.3. Accounting, Reporting and Zakat .................................................................................................. 36

1.5. RISK AND LIQUIDITY MANAGEMENT OF ISLAMIC BANKS ....................................................................................... 37

1.5.1. Liquidity Management .................................................................................................................. 37

1.5.2. Risk Management .......................................................................................................................... 40

1.6. HISTORY AND CURRENT DEVELOPMENT OF ISLAMIC FINANCE ................................................................................ 45

iii

1.6.1. Historical milestones...................................................................................................................... 45

1.6.2. Approaches to expansion and development .................................................................................. 48

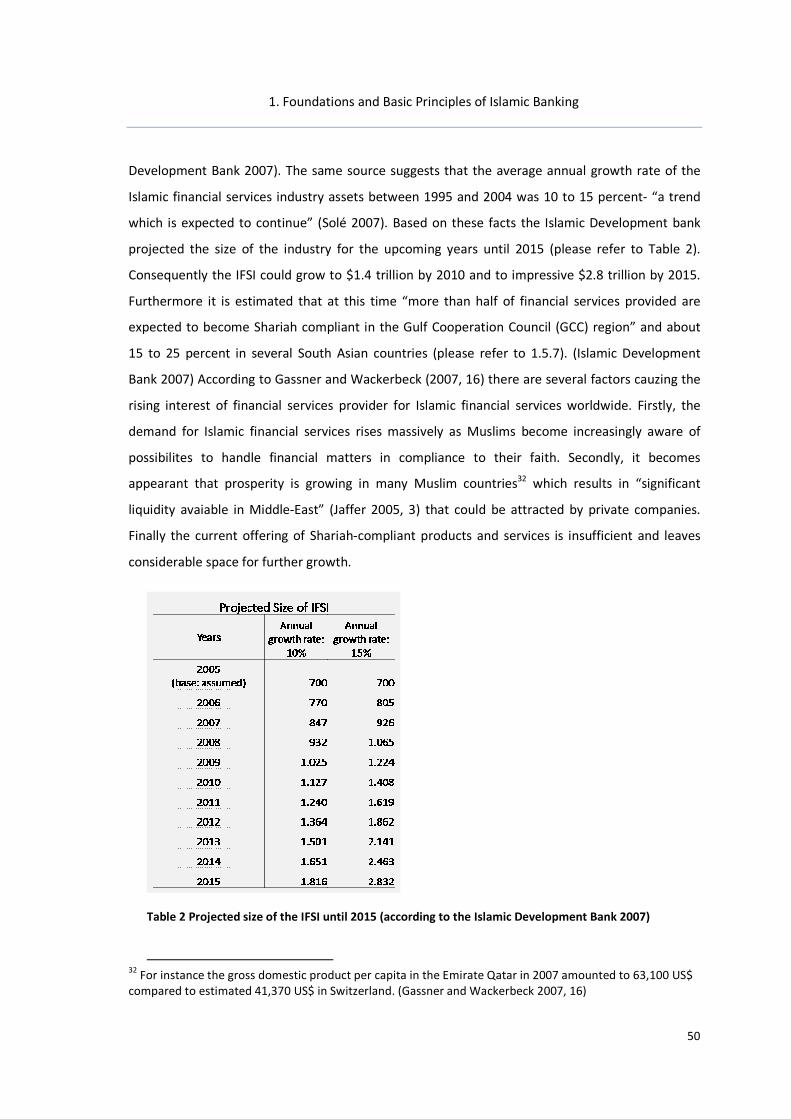

1.6.3. Estimated size of the industry and growth trends ......................................................................... 49

1.6.4. Islamic financial centres ................................................................................................................ 53

1.7. LATEST DEVELOPMENTS IN MIDDLE EAST AND SOUTHEAST ASIA ........................................................................... 53

1.7.1. Geographical classification ............................................................................................................ 53

1.7.2. Financial markets in Middle East and Southeast Asia ................................................................... 54

1.7.3. Development of the Islamic banking sector in GCC countries and Malaysia ................................. 55

1.8. PROSPECTS FOR ISLAMIC FINANCIAL INDUSTRY .................................................................................................. 57

2. EVOLUTION OF ISLAMIC BANKING IN WESTERN EUROPE ...................................................................... 59

2.1. UNITED KINGDOM ............................................................................................................................................ 61

2.1.1. Establishment of London as the Western centre for Islamic finance ............................................. 61

2.1.2. Muslims in the United Kingdom..................................................................................................... 63

2.1.3. Government initiatives and cooperation ....................................................................................... 65

2.1.4. The current Islamic financial market in the United Kingdom ........................................................ 66

2.1.5. Future outlook and trends for the United Kingdom ....................................................................... 76

2.2. SWITZERLAND ............................................................................................................................................. 77

2.2.1. Market players ............................................................................................................................... 77

2.2.2. Future outlook ............................................................................................................................... 80

2.3. FRANCE ..................................................................................................................................................... 80

2.3.1. Muslims in France and Islamic market potential ........................................................................... 80

2.3.2. Government initiatives .................................................................................................................. 82

2.3.3. Market players ............................................................................................................................... 82

2.3.4. Future prospects ............................................................................................................................ 84

2.4. ITALY ........................................................................................................................................................ 84

2.5. AUSTRIA .................................................................................................................................................... 86

2.6. OTHER EUROPEAN MARKETS ......................................................................................................................... 88

3. GERMAN MARKET POTENTIAL FOR ISLAMIC BANKING ACTIVITIES ........................................................ 89

3.1. MUSLIMS IN GERMANY ................................................................................................................................ 89

3.2. BANKING BEHAVIOR AND TRENDS IN DEMAND FOR CONVENTIONAL BANKING SERVICES OF MUSLIMS IN GERMANY ......... 92

3.2.1. General banking potential ............................................................................................................. 92

3.2.2. Current banking demands and trends ........................................................................................... 92

3.2.3. Particularities of German Muslim consumers (having a Turkish background) .............................. 94

3.3. POTENTIAL DEMAND FOR SHARIAH COMPLIANT FINANCIAL SERVICES ...................................................................... 95

3.4. REGULATORY FRAMEWORK AND FEASIBLE BUSINESS MODELS ............................................................................... 98

iv

3.4.1. Regulation and licensing of financial business entities in Germany .............................................. 98

3.4.2. Tax conditions ................................................................................................................................ 99

3.4.3. Feasible business models for Islamic banking operations in Germany ........................................ 100

3.5. MARKET PLAYERS IN GERMANY .................................................................................................................... 101

3.5.1. Current business activities of German Islamic financial service providers ................................... 102

3.5.2. Marketing strategies and distribution channels used ................................................................. 107

3.5.3. Obstacles and hindrances experiences ........................................................................................ 108

3.5.4. Scope of activities and future plans for Islamic financial service business .................................. 109

3.5.5. Estimations on future market development in Europe and Germany in particular ..................... 111

3.5.6. Approaches to provide Islamic financial services in the German market .................................... 112

3.6. ETHNO-MARKETING APPROACHES AND ETHICAL INVESTMENTS .......................................................................... 114

3.6.1. Ethno-Marketing approaches ...................................................................................................... 114

3.6.2. Promoting ethical investments .................................................................................................... 116

4. CONCLUSIONS .................................................................................................................................. 117

4.1. FUTURE OUTLOOK FOR THE DEVELOPMENT OF THE ISLAMIC FINANCIAL SERVICES INDUSTRY IN EUROPE ...................... 117

4.2. CHALLENGES FOR THE ISLAMIC FINANCIAL INDUSTRY IN EUROPE ......................................................................... 119

4.3. RECOMMENDATIONS FOR GERMAN FINANCIAL INSTITUTIONS ............................................................................ 120

WORKS CITED .......................................................................................................................................... 122

APPENDIX A ................................................................................................................................................ I

APPENDIX A1: THE FOUR VERSES IN THE QUR’AN DEALING WITH RIBA .................................................................................. I

APPENDIX A2: THE FIVE PILLARS OF ISLAM .................................................................................................................... II

APPENDIX B .............................................................................................................................................. III

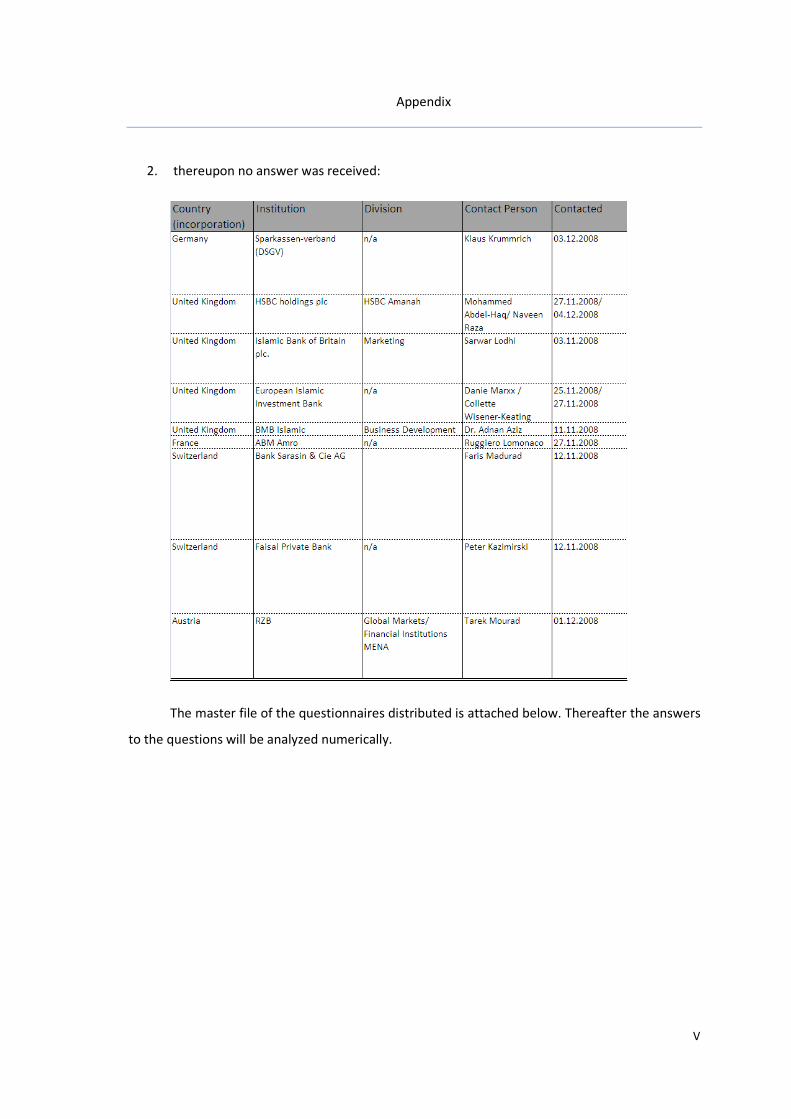

APPENDIX B1: INSTITUTIONS AND COMPANIES CONTACTED .............................................................................................. IV

APPENDIX B2: QUESTIONNAIRE DISTRIBUTED ................................................................................................................ VI

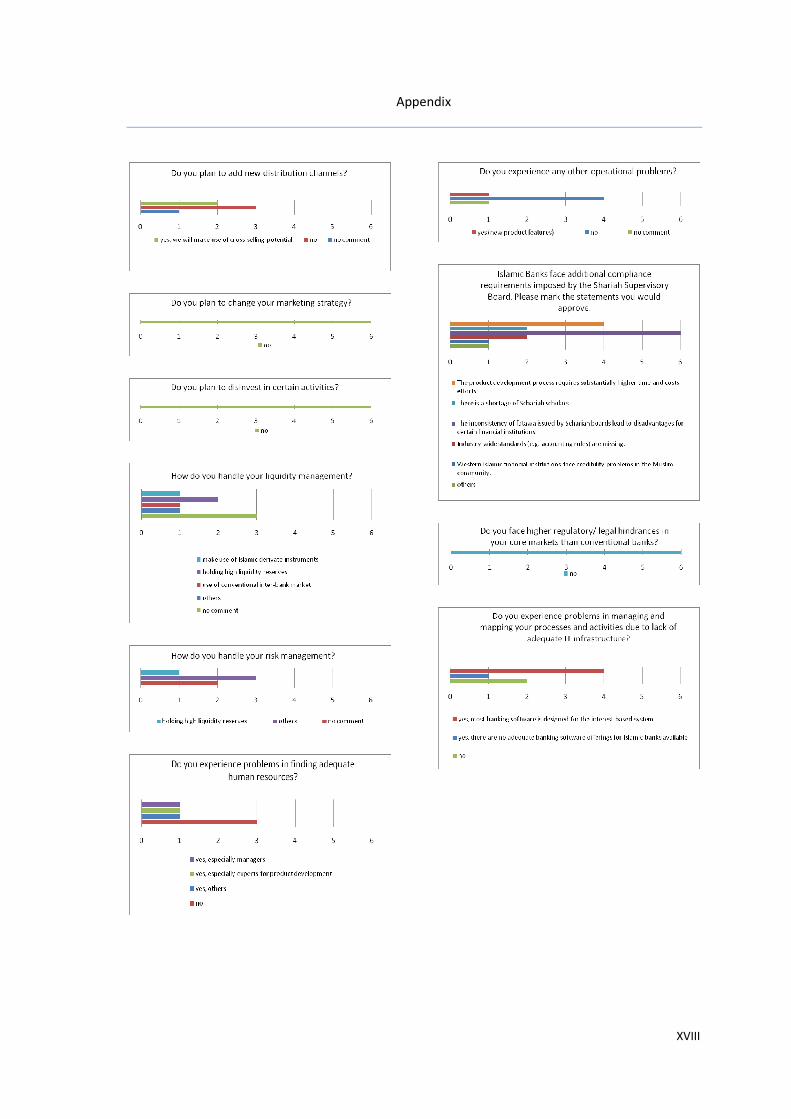

APPENDIX B3: ANALYSIS OF ANSWERS RECEIVED ........................................................................................................... XV

v

Erklärung gemäß §31 Abs. 7 RaPO

Ich versichere, dass ich die Arbeit selbstständig angefertigt habe, nicht anderweitig für

Prüfungszwecke vorgelegt, alle benutzten Quellen und Hilfsmittel angegeben sowie

wörtliche und sinngemäße Zitate als solche gekennzeichnet habe.

_________________________________

Kati Colditz

Nürnberg, den 03. März 2009

vi

Figures

Figure 1 Definition of Riba (according to Iqbal and Mirakhor 2007, 56) 7

Figure 2 Example of a Mudaraba transaction from Gassner and Wackerbeck (2007, 64) 11

Figure 3 Permanent Musharaka transaction from Gassner and Wackerbeck (2007, 67) 12

Figure 4 Murabaha transaction (own illustration) 14

Figure 5 Salam transaction (own illustration) 14

Figure 6 Pure Ijarah transaction (own illustration) 16

Figure 7 Islamic equity fund based on Mudaraba partnership from Gassner and Wackerbeck 2007,

135 19

Figure 8 Transaction structure “Stichting Sachsen Anhalt Trust” (aligned with el-Mogaddedi 2007

and Bergmann 2008, 113) 21

Figure 9 Example for a mirrored Forex Swap transaction according to Shariah principles (own

illustration) 24

Figure 10 Takaful model based on Mudaraba transaction from Gassner and Wackerbeck 2007, 148

28

Figure 11 Commodity Murabaha Liquidity Management from Bank Negara Malaysia (2005) 39

Figure 12 Liquidity Management via Sukuk (own illustration) 40

Figure 13 Composition of the Islamic Financial Services industry (according to Islamic Development

Bank 2007) 48

Figure 14 Total Sukuk issuance (International Islamic Financial Market 2007) 52

Figure 15 Number of Islamic mutual equity funds (according to Gassner and Wackerbeck 2007,

137) 52

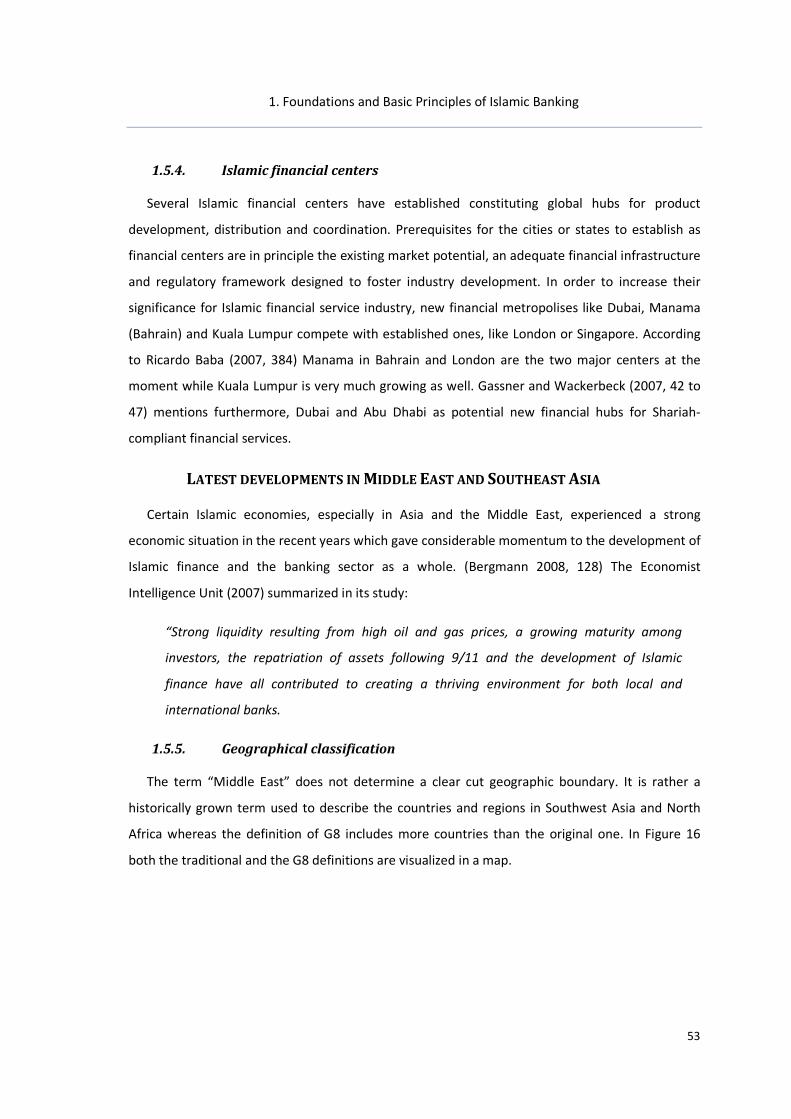

Figure 16 Countries of Middle East (Nationmaster 2003-2005) 54

vii

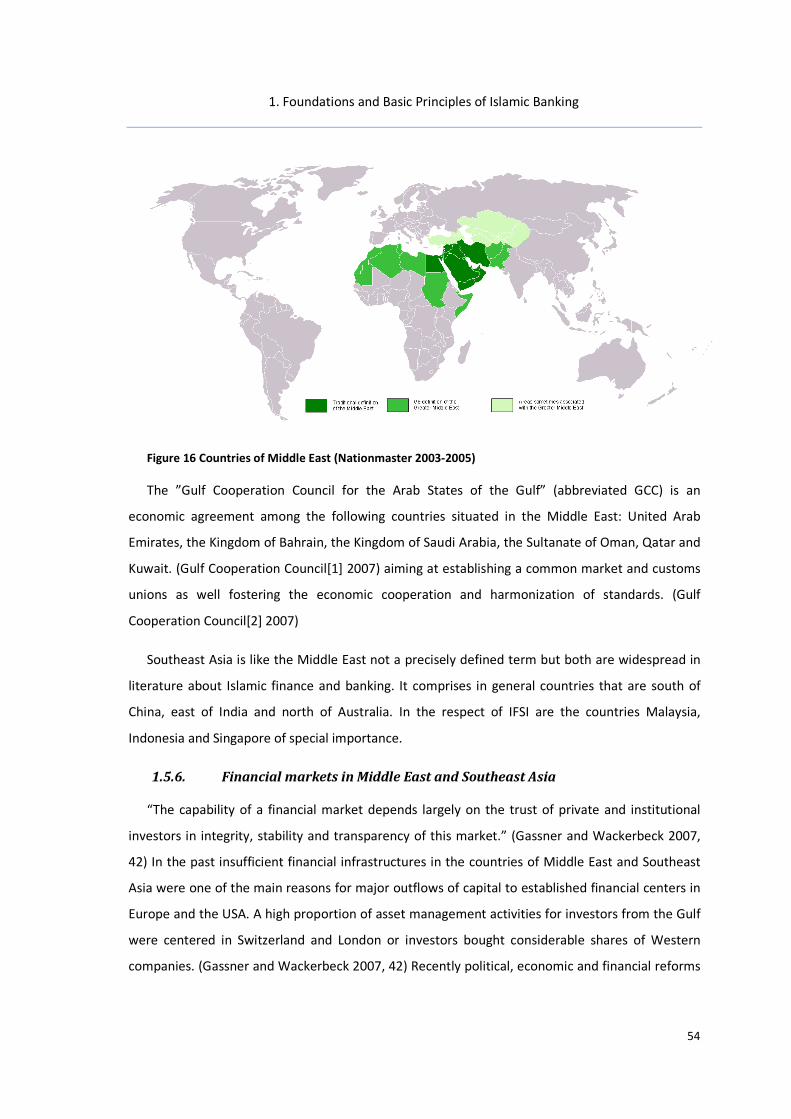

Figure 17 Development of assets held by Islamic banks (according to Islamic Development Bank

2008) 56

Figure 18 Market share of Islamic products and services in assets, deposits and financing as at end-

2005 in Malaysia (Bank Negara Malaysia 2005) 57

Figure 19 Muslim population in selected Western European countries (according to BBC 2008) 59

Figure 20 UK Muslims by ethnic group, April 2001 (Office for National Statistics 2003) 64

Figure 21 Muslims in Germany by country of origin (according to Bertelsmann Stiftung 2008) 90

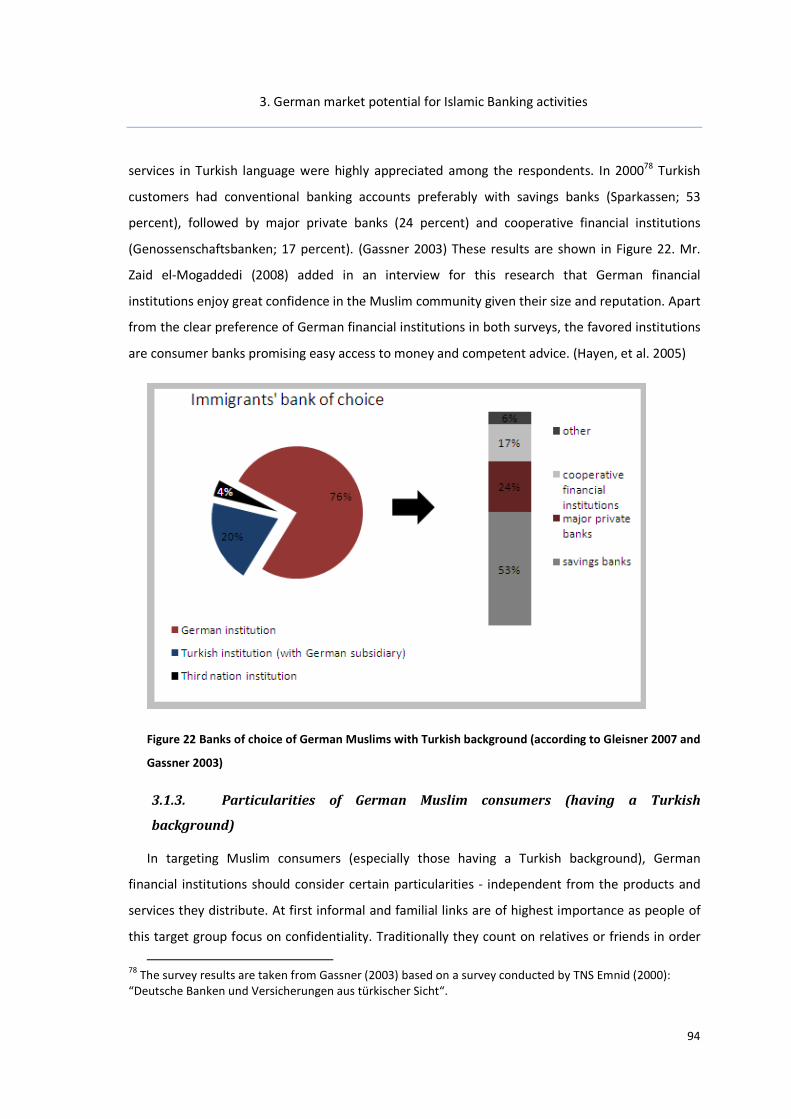

Figure 22 Banks of choice of German Muslims with Turkish background (according to Gleisner 2007

and Gassner 2003) 94

Figure 23 Importance of Islamic investments for German Muslims (by religiousness and in total)

(according to survey results of Hayen, et al. 2005) 96

Figure 24 Distribution channels used by German financial institutions offering Islamic financial

services 107

Figure 25 Promotion of Islamic financial services by German financial institutions 108

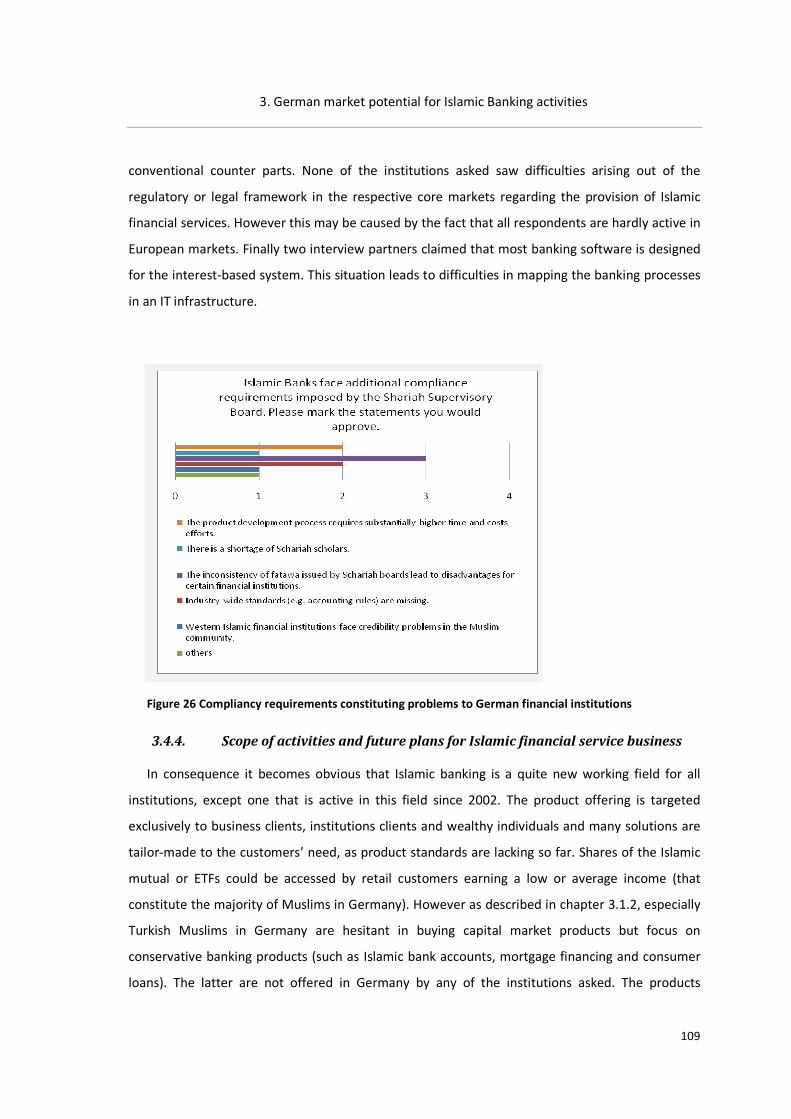

Figure 26 Compliancy requirements constituting problems to German financial institutions 109

viii

Tables

Table 1 Estimated size of IFSI Segments in 2005 (according to the Islamic Development Bank 2007)

49

Table 2 Projected size of the IFSI until 2015 (according to the Islamic Development Bank 2007) 50

Table 3 Regulatory initiative in the United Kingdom (Financial Services Authority 2007) 66

Table 4 Fully-fledged Islamic banks in the United Kingdom (according to Islamic Bank of Britain

2007, European Islamic Investment Bank 2007, Bank of London and the Middle East 2007 and

Gatehouse Bank 2007) 69

Table 5 Islamic financial service offering by German institutions (according to questionnaire and

interview results) 106

Table 6 Scope of Islamic financial activities of German institutions 110

ix

Glossary of Arabic terms1

Al wadiah Principle to keep or deposit something in

custody

Amanah Describes both a relationship of trust and items

in safekeeping

Bay Salam A contract determining a pre-paid purchase

Daruah Doctrine of necessity

Fatwa (plural: fatawa) An authoritative legal opinion issued by a

Shariah Supervisory Board/ single Shariah

scholars, based on the Shariah

Fiqh Practical Islamic jurisprudence (jurists’ law)

Fiqh Mu’amalat Islamic commercial jurisprudence (rules of

transaction)

Hadithe Technical term for sources related to the

sayings and doings of the Prophet, authentic

traditions

Ijarah / Ijarah wa Iqtina A contract determining a leasing agreement/

A lease-purchase agreement

Istisnaa A contract of sale of specified goods to be

manufactured

Manfa’a The right to use an asset

Mudaraba A partnership contract in which one partner

contributes capital and the other partner

1 The explanations are aligned with the Glossaries of Hassan and Lewis 2007 and Jaffer 2005.

x

invests time and effort

Mudarib The entrepreneur or manager in a Mudaraba

contract

Murabaha The resale of goods with an agreed upon profit

mark-up on the cost

Musharaka A partnership contract in which both parties

contribute capital and may form a joint

management

Qard Hassan A benevolent (interest-free) loan

Qirad A dormant partnership (for example in a

Mudaraba contract)

Rabb al mal The partner in a Mudaraba agreement

providing the funds

Shariah Islamic religious law derived from the Holy

Qur’an and the Hadithe

Sukuk (plural of sakk) Participation securities, coupons, investment

certificate

Tabarru Donation

Takaful A Shariah compliant insurance concept (similar

to conventional mutual insurances)

Tawarruq The purchase of goods on deferred payment

and their subsequent sale (to raise cash)

Wakala An agency contract

xi

Abstract

The thesis concentrates on the potentials in the future development of the Islamic financial

service industry in Europe, in particular in Germany. In a period of continuous growth worldwide in

the recent years the United Kingdom played a major role as innovative financial centre,

establishing itself as European pioneer in Islamic finance. Domestic institutions cater foreign

customers as well as the local Muslim communities. This example, the increasing demand for

ethno-oriented banking offerings as well as financial inclusion considerations for Muslim

minorities living in Europe gave rise to the estimation that there might exist considerable domestic

market potential in other European markets too, in particular in Germany. Therefore it was

investigated on the question whether the provision of Islamic financial services for the domestic

market could constitute a worthwhile approach for German financial institutions. Furthermore the

current Shariah compliant financial product offerings in Europe were scrutinized in light of

domestic preconditions such as characteristics of the local Muslim population and governmental

initiatives. The research was built on questionnaires and interviews targeting representatives of

European financial institutions and Islamic financial industry experts. Additionally results of market

surveys and working papers issued by industry organizations and online information were included

in the analysis. It was shown that there are substantial cultural and religious differences between

Muslims living in different European countries resulting from their origins. For this reason it

cannot be concluded from the success of Islamic financial service offerings in the United Kingdom

that this approach is promising for the German market. Apparently the domestic demand among

Muslims living in Germany, predominantly of Turkish origin is not sufficient to justify the

considerable initial efforts required to enter the Islamic financial service market. This applies to

most of the other European markets analyzed, too where the supply of Islamic financial services

for local Muslim communities is currently very limited. This situation may be a result of the low-

socio economic status of many Muslim migrants in Europe on the one side, making them a rather

unattractive customer group at this point of time, as well as low market awareness for Shariah

compliant financial products on the other side, leading to only very moderate demand. For the

German market the targeting of local Turkish customers in the scope of ethno-oriented marketing

approaches as well as the limited offering of Shariah compliant financial products within a broader

concept of ethical investments were identified as interesting alternatives in contrast to the focus

on Islamic financial services, only. In an international context it was assessed that only the United

Kingdom and Switzerland might play a major role in the global Islamic financial service industry

given their establishment as international financial centers in investment and private banking.

xii

Nevertheless it appears promising for German financial institutions as well as for those from other

European countries to invest in Islamic financial product offerings targeted to Muslim majority

countries, for example the Gulf Cooperation Council, in order to attract funds for the domestic

market.

Introduction

1

Introduction

It is unusual for the Western world to make the financial system subject to religious

prescriptions. The conviction that religious and worldly affairs need to be separated especially

when it comes to economics and politics is deep-seated. People from secular states look skeptical

to Muslim majority countries like Saudi Arabia or Pakistan having a state religion. Believers there

respect increasingly the principles of Islamic law (Shariah) when handling financial matters.

Following many years of conventional banking, Muslims show more an more interest for

investment and financing possibilities that are in compliance with their faith. This development

supported by privately or state-owned financial institutions, Shariah scholars as well as

governmental and non-governmental organizations, initiated the dynamic growth of the Islamic

financial service industry that was observable in the recent decades. But not only in Muslim

majority countries has the trend gained importance. Several market players in established

European financial centers cater the rising demand for Shariah compliant services providing know

how and innovative solutions. The United Kingdom became the most important Western Islamic

financial centre and home to the first fully-fledged European Islamic banks as well as to numerous

conventional banks offering Islamic financial services (Islamic Windows). This development was

actively fostered by governmental authorities. Apart from foreign customers, industry experts

suggest European financial institutions to target the large local Muslim minorities (for example in

France or Germany) by providing respective offerings. This approach would foster the financial

inclusion as well as the overall integration of these customer groups in European societies. But not

only Muslims could be in the focus. Facing the severe financial crisis experienced in these days

fostered by highly-leveraged financial contracts and non-transparent investments, the banks’

customers call for more transparency, credibility and moral behavior. These values are inherent in

the Shariah compliant banking system in which all products and services are based on assets in

order to foster economic development and trade. Therefore it is reasonable to encourage

European financial institutions to offer financial products and services to the domestic markets

that are in compliance with the Shariah. However it remains questionable whether such

approaches bear promising potential for success. Can we conclude from the success experiences in

the United Kingdom to other European markets?

Introduction

2

The research has two major targets. Firstly, a market overview of Shariah compliant financial

products and services offerings will be developed offered for selected European markets being the

United Kingdom, Switzerland, Italy and Austria. Thereby the domestic Muslim populations as well

as governmental and regulatorary reactions and initiatives are analyzed. Secondly, the German

domestic market potential will be scrutinized. Given the large percentage of people originating

from Turkey - mostly adhering to Islamic faith, a substantial demand for Islamic financial services

could be assumed. The thesis will investigate on characteristics and banking behavior of Muslims

living in Germany in order to give recommendations for domestic financial institutions. In this

context alternative concepts are mentioned to target Turkish migrants separately without

offerings Shariah compliant financial products or to offer ethical investments without reference to

Islamic faith.

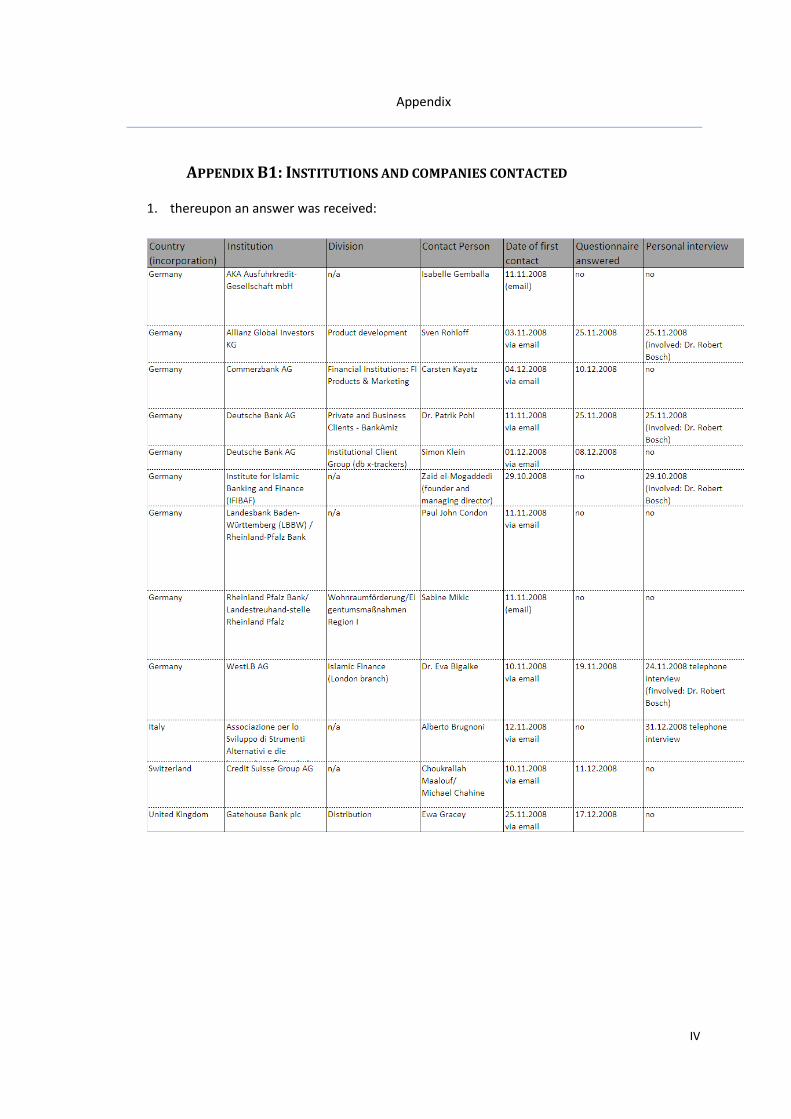

Within the course of this research major European financial institutions were approached with

the purpose to gain information about their activities in the field of Islamic banking and finance.

Answers could be retrieved from four German institutions being the Deutsche Bank, the

Commerzbank, Allianz Global Investors as well as a German federal state bank. Furthermore

representatives of the Gatehouse Bank, one of London’s newly established fully-fledged Islamic

banks, and of Credit Suisse participated in the survey. The questionnaires and interview guidelines

were designed to investigate on current and planned Shariah compliant product offerings,

obstacles observed and estimations for future trends. In the case of Germany and Italy the results

were confronted with opinions expressed by the Islamic financial industry experts Zaid el-

Mogaddedi and Alberto Brugnoni. Additionally, already conducted market surveys, working papers

and online information were used to form a comprehensive view on the subject.

The basis for the market analyses will be a literature review in the first chapter describing the

theoretical background of the Islamic financial service concept. In this respect some remarks are

made to development and status in Muslim majority countries.

1. Foundations and Basic Principles of Islamic Banking

3

1. FOUNDATIONS AND BASIC PRINCIPLES OF ISLAMIC BANKING

The Islamic economic system differs substantially from the Western conventional, capitalistic

one as it is goes beyond the pure financial and economic sphere. Its most important foundations

are the Islamic religion and the Shariah – the Islamic law- providing a religious framework as well

as social and ethical boundaries for Islamic finance and banking activities. (Gassner and

Wackerbeck 2007, 20 and 21)

1.1. ISLAMIC LEGAL AND ECONOMIC SYSTEM

The Islam is not only a religion but a “codification of general standards of behavior that reach

far beyond the contents of belief” (Gassner and Wackerbeck 2007, 21). It declares a holistic

approach to life as it regards economy, politics, social aspects and religion as closely interlinked.

(Gassner and Wackerbeck 2007, 21) “Concomitant with the statement of Islamic faith, the

individual agrees to observe the rules of Islamic law (Shariah) in private and public affairs.” (Iqbal

and Mirakhor 2007, 5) This applies also to financial matters. In this respect “believers are expected

to respond with enthusiasm to banks that offer products that respect Islamic principles of finance”

(Jaffer 2005, 31). For practical reasons, there exists a doctrine of necessity that allows Muslims to

make use of conventional banking products if adequate Shariah-compliant alternatives are not

offered (principle of Daruah). (Jaffer 2005, 31) However, after several decades of conventional

banking, people in Muslim majority countries and other parts of the world, demand increasingly

investment and financing possibilities that comply with their faith. This development gave rise to

the current dynamic growth of the Islamic financial service industry (please refer to chapter 1.5.).

1.1.1. Shariah and Fiqh

The Islamic legal system is based on Shariah and Fiqh.

Shariah can be translated as “the way to the source of life” (Algaoud and Lewis 2007, 38) and is

used to denominate a legal system which promotes a certain code of behaviour described by the

Holy Qur’an and the Hadithe (the authentic tradition). It includes a set of duties and pracitices

such as prayer, manners and morals, marriage etc. (Algaoud and Lewis 2007, 38) The Holy Qur’an

is the “Divine Books revealed to Prophet Muhammad” and is referred to as “guidance for

mankind” (Iqbal and Mirakhor 2007, 10 and 14). “As such it does not rely on the authority of any

earthly lawmaker.” (Algaoud and Lewis 2007, 38) Additionally to the Holy Qur’an, the Shariah is

1. Foundations and Basic Principles of Islamic Banking

4

based on “judgments given by the Prophet himself, reflecting the application of rules, principles

and injunctions already enunciated in the Holy Qur’an” called the Hadithe2 (Algaoud and Lewis

2007, 38). In practice there is “no universality of Islamic law [Shariah]” (Lewis and Algaoud 2001,

39) as it is applied adhering to the principles of “analogical reasoning” and “independent human

reasoning of those specialized in law”. The former is based on analogies existing between new

problems and those existing in primary sources, such as the Holy Qur’an and the Hadithe.3 (Iqbal

and Mirakhor 2007, 15). The latter refers to Shariah scholars, being experts in Islamic law, who can

interpret the Shariah themselves.4 Both principles result in a “great flexibility” (Iqbal and Mirakhor

2007, 15) in law making5.

Fiqh is the collection of all sources of law including Qur’an, Sunna2, Qiyas3 and Ijma4 and

constitutes the Islamic jurisprudence. It regulates the relationship between men and Allah

(Fiqh´Ibadah) as well as all aspects and relationships of men among each other (Fiqh Mu´amalat).

The latter comprises the regulation of commercial and financial transactions and financial

institutions. The Shariah gives important incentives according to religious beliefs whereas Fiqh

adjusts to the pressure of society as it is subject to political influences and public opinions

(Bergmann 2008, 25).

In the Western basic understanding6, individual pursuit of economic profit maximization leads

simultaneously to profit maximization for the whole society. In contrast Muslim individuals have

not only to adhere to the Shariah principles but also “to keep in mind the impact of their activities

on others and the society of a whole” (Ayub 2007, 30). In this way they should consider the pursuit

of equality and brotherhood within the society of Muslims in every economic activity. (Gassner

and Wackerbeck 2007, 22) Trade and commerce are encouraged by the Holy Qur’an as long as

2 The Hadithe are in other literature sources referred to as “Sunna” (Bergmann 2008, 28 and Iqbal and

Mirakhor 2007,13 and 14)

3 The practice of analogical reasoning is in other literature sources referred to as „Qiyas“ (Bergmann 2008,

28)

4 The principle of independent human reasoning is in other literature sources referred to as “Ijmas”

(Bergmann 2008, 28)

5 These general principles result in inconsistencies in decisions of Shariah Supervisory Boards, discussed in

chapter 1.3.5.

6 For example according to the teachings of Adam Smith, who confessed that “an individual pursuing his

own self-interest tends to simultaneously promote the good of his community as a whole” (Kaufmann,

Smith and Krüsselberg 1984, 30).

1. Foundations and Basic Principles of Islamic Banking

5

they are honest and legitimate7. People should be able to “earn their living, support their families

and give charity to those less fortunate” (Lewis and Algaoud 2001, 27).

Islamic financing is based upon four root transactions which lead finally to the very important

concepts of partnership or profit and loss sharing. Furthermore there are five essential religious

principles that have to be obeyed (Lewis and Algaoud 2001, 27 and 28). These basic elements are

explained in the following subchapters in order to build a solid ground for the understanding of

the product and compliance structures in Islamic financial institutions.

1.1.2. The four root transactions and the concept of partnership

The four root transactions according to Shariah are sales (Bay), hire (Ijâra), gift (Hiba) and loan

(Ariyah) describing respectively the transfer of ownership, the transfer of the right to use, the

gratuitous transfer of ownership and the gratuitous transfer of the right to use. These basic forms

are applied to specific transactions such as pledge, deposit and guarantee and build the basis for

all transaction structures in Islamic finance. (Lewis and Algaoud 2001, 27)

The traditionally most accepted and most correct forms of Islamic financing are the profit-and-

loss sharing contracts: Mudaraba and Musharaka. According to Algaoud and Lewis (2007, 28) this

form of equity based financing is considered as the “backbone of Islamic banking practice” as it

represents the idea of the Holy Qur’an, namely that every investment should foster economic

development by providing capital to companies and infrastructure projects (Gassner and

Wackerbeck 2007, 67). As can be derived from the name, profits and losses are shared between

the creditor and the borrower on a predetermined basis. Consequently it is considered as a

“return-bearing” contract in contrast to an “interest-bearing” contract in conventional banking

(Mirakhor and Zaidi 2007, 49). The two basic concepts Mudaraba and Musharaka and will be

explained in section chapter 1.2.1.

1.1.3. Religious principles guiding investment behavior

As already mentioned before there are certain key assumptions that distinguish Islamic Finance

essentially from conventional financing activities. The four most important principles are described

below.

7 The Islam prescribes further ethic an moral standards to be obeyed, such as “justice and fair dealing,

gentleness, fulfilling of covenants and paying liabilities, mutual cooperation and removal of hardship, free

marketing and free pricing, freedom of Dharar (detriment)” (Ayub 2007, 64-70).

1. Foundations and Basic Principles of Islamic Banking

6

1.1.1.1. Riba – the prohibition of interest

The issue of Riba is the most controversial and, at the same time, the most far reaching aspect

in the Islamic financial system. Its interpretation is subject to many debates around the world8. It

can be translated into English as “increase”, “access”, “growth”, “addition”, “usury” (Algaoud and

Lewis 2007, 42) or simply “prohibited gain” (Ayub 2007, 47). A common consensus about the

actual sense has not been reached yet. Most Islamic scholars agree that the Holy Qur’an prohibits

the payment and taking of any interest (for the detailed Qur’an content please refer to Appendix

A1). Some more liberal experts argue that only “usury” in the sense of exorbitant, excessive

interest should be banned (Algaoud and Lewis 2007, 42f.). The latter opinion was followed by

believers of Hinduism, Judaism and Christianity, too. (Lewis and Algaoud 2001, 64). Over the years

the prohibition lost its importance in the other world religions. In the Muslim world there is a

substantial difference between profits resulting from entrepreneurial activities and profits

generated by granting loans. The latter is defined as “receiving a monetary advantage without

giving a counter value” (Algaoud and Lewis 2007, 42) and is therefore forbidden according to the

Holy Qur’an. It declares that those who take Riba are at war with God and his Prophet Muhammad

because Riba deprives the wealth of God’s blessing and encourages the wrongful appropriation of

property belonging to others and harms Muslims’ welfare. In transactions only the principal should

be paid and in case the counterparty is unable to pay it should be forgone. (Lewis and Algaoud

2001, 28 and 29)

There are several subcategories of Riba to be considered. The most high-level distinction can be

drawn between Riba Nasiah and Riba Al-Fadl. In conventional banking the borrower is charged for

the time it takes to redeem the loan. Therefore an increase on the original principal is paid.

Shariah scholars do not regard this time period generating the interest as an asset constituting

value (Gassner and Wackerbeck 2007, 27). Riba Al-Nasiah relates to all forms of money-to-money

exchange “provided the exchange is delayed or deferred and additional charge is associated with

such deferment” (Iqbal and Mirakhor 2007, 55). All profits, fixed in advance, resulting from

granting a time delay in the redemption of loans are not-admissible as no “counter value” is given

(Algaoud and Lewis 2007, 42). The second form Riba Al-Fadl is involved in barter exchanges (or

hand-to-hand exchanges). It is required that “commodities are exchanged for cash instead of

8 Some popular revisionists’ views are outlined in Algaoud and Lewis 2007, 44ff.

1. Foundations and Basic Principles of Islamic Banking

7

barter since there may be differences in the quality of the goods” (Iqbal and Mirakhor 2007, 56) so

that an “unjust increase, being Riba” (Iqbal and Mirakhor 2007, 55) could emerge.

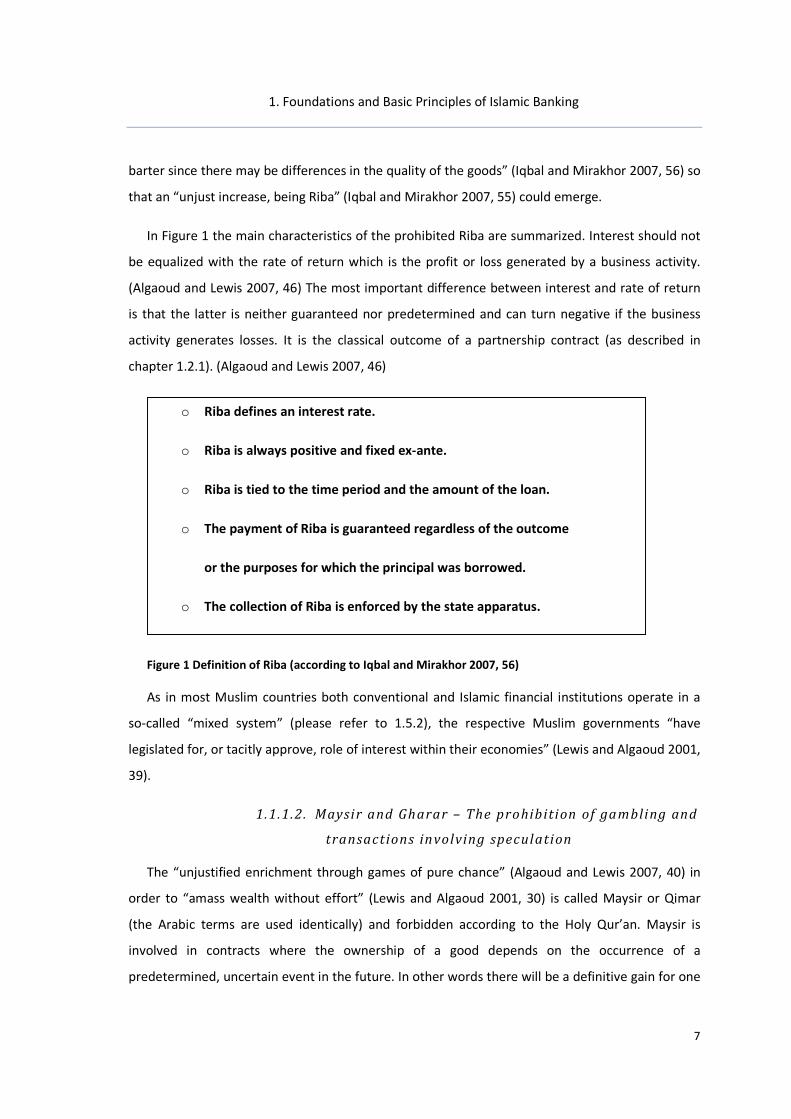

In Figure 1 the main characteristics of the prohibited Riba are summarized. Interest should not

be equalized with the rate of return which is the profit or loss generated by a business activity.

(Algaoud and Lewis 2007, 46) The most important difference between interest and rate of return

is that the latter is neither guaranteed nor predetermined and can turn negative if the business

activity generates losses. It is the classical outcome of a partnership contract (as described in

chapter 1.2.1). (Algaoud and Lewis 2007, 46)

Figure 1 Definition of Riba (according to Iqbal and Mirakhor 2007, 56)

As in most Muslim countries both conventional and Islamic financial institutions operate in a

so-called “mixed system” (please refer to 1.5.2), the respective Muslim governments “have

legislated for, or tacitly approve, role of interest within their economies” (Lewis and Algaoud 2001,

39).

1.1.1.2. Maysir and Gharar – The prohibition of gambling and

transactions involving speculation

The “unjustified enrichment through games of pure chance” (Algaoud and Lewis 2007, 40) in

order to “amass wealth without effort” (Lewis and Algaoud 2001, 30) is called Maysir or Qimar

(the Arabic terms are used identically) and forbidden according to the Holy Qur’an. Maysir is

involved in contracts where the ownership of a good depends on the occurrence of a

predetermined, uncertain event in the future. In other words there will be a definitive gain for one

o Riba defines an interest rate.

o Riba is always positive and fixed ex-ante.

o Riba is tied to the time period and the amount of the loan.

o The payment of Riba is guaranteed regardless of the outcome

or the purposes for which the principal was borrowed.

o The collection of Riba is enforced by the state apparatus.

1. Foundations and Basic Principles of Islamic Banking

8

party and a definitive loss for the other party, but when the contract is signed it is not sure who

will be the winner or the looser. (Gassner and Wackerbeck 2007, 31) The Qur’an tells about this

principle among others in verse 219 which states:

“They ask thee concerning wine and gambling. Say: ‘In them is great sin and some benefit

for people; but the sin is greater than the benefit’.” (4:219) (Ayub 2007, 62)

According to Lewis and Algaoud (2001, 39) Gharar means “to undertake a venture blindly

without sufficient knowledge or to undertake an excessively risky transaction”. Consequently

every contract that is built on speculative assumptions is void. Transactions containing excessive

risk are supposed to foster uncertainty and fraudulent behavior. However minor uncertainties and

a certain degree of risk are permitted as it is involved in every economic activity. A clear definition

to which extent risk taking is Halal9 does not exist. (Ayub 2007, 58)

In an economic context the ban of Maysir and Gharar has particular relevance for financial

markets notably the derivatives market and the insurance business. As a derivative financial

instrument speculates in general on the development of its underlying value (for example in future

contracts or short-selling transactions) the concept of Gharar applies (Algaoud and Lewis 2007,

40). Therefore the trade of all conventional derivate instruments is impossible in Islamic finance.

The current lack of Shariah compliant derivatives is critical (please refer to 1.2.4.3 for Islamic

derivatives and to 1.4 for Risk and Liquidity Management of Islamic banks). Consequently market

participants invest considerable efforts in developing Shariah compliant derivative instruments. In

the same way Maysir and Gharar influence to a large extent the Islamic insurance business.

According to Shariah scholars, the Western style insurance products comprise Gharar and Maysir

(for explanations please refer to 1.1.4.).Therefore Islamic insurance companies have to change

their business model accordingly and offer Takaful, a mutual insurance product.

1.1.1.3. Halal and Haram – Code of “ethical investment”

As already mentioned in the beginning of chapter 1.1, there exist several ethical and social

criteria for exclusion regarding the investment targets and financial products allowed for Muslims.

The forbidden and not admissible actions and businesses are called Haram whereas legal and

permitted activities are referred to as Halal. Neither private investors nor companies or banks are

9 The concept of Halal is defined later in this chapter. It describes permitted transactions or goods in

contrast to Haram, meaning prohibited or wrong transactions or goods.

1. Foundations and Basic Principles of Islamic Banking

9

allowed to invest in Haram businesses dealing with, for instance, “alcohol, tobacco, pork-related

products, […], gambling, cinema, pornography, music and suchlike” (Khan and Bhatti 2008, 59).

This “ethical investment” code has to be strictly obeyed and even firms that conduct only small

parts of their business in the pre-mentioned Haram domains are excluded10 (Khan and Bhatti

2008, 59). Another industry that is affected by the code and cannot be target of investment is the

financial service industry. As already described before, Riba is condemned by Muslim scholars

(please refer to 1.1.1.1). Thus, securities issued by banks and insurance companies that operate in

the conventional, interest-based financial system are not admissible for Muslim investors.

Furthermore it is forbidden to invest in companies that are debt-ridden. (Bergmann, 2008, 37 and

38) These Shariah requirements are of special importance in stock investment and Islamic mutual

funds. In order to separate Halal investments from Haram stocks, a sophisticated screen process

has to be executed (please refer to chapter 1.2.4.1.).

1.1.1.4. Zakat –The social duty to benef it society

In Islam, wealth is regarded as a trust from God and should therefore take over a social duty in

order to benefit society. It is an obligation for the Islamic state to guarantee a fair standard of

living (called Nisab) to its people and to balance social imbalances. The most important

mechanism in this context is Zakat (Lewis & Algaoud, 2001, 29). It is one out of the five pillars of

Islam11 and constitutes a religious levy or almsgiving required in the Holy Qur’an (Algaoud and

Lewis 2007, 40). In consequence approximately “2.5 percent assessment on assets held for a full

year (after a small initial exclusion, the Nisab)” has to be dispensed (Lewis & Algaoud, 2001, 29). In

particular, Islamic financial institutions have to establish a Zakat fund to collect and redistribute

Zakat to the deserving poor, either directly or via religious institutions. The concerned assets

include initial capital, reserves and profits. (Lewis & Algaoud, 2001, 29 and 30) The calculation and

payment of the Zakat is overseen by the Shariah Supervisory Board (please refer to chapter 1.3).

(Iqbal and Mirakhor 2007, 289)

1.2. ISLAMIC FINANCING TECHNIQUES AND PRODUCTS

Islamic banking and finance was developed in the first place to finance trade and commerce (in

compliance with the Shariah) and consequently to foster the economic development in the

10

According to the common opinion in the literature reviewed a business activity up to 5 percent in Haram

businesses is allowed. 11

The Five Pillars of Islam can be found in the Appendix.

1. Foundations and Basic Principles of Islamic Banking

10

respective countries (please refer to chapter 1.5.1). Nowadays the financing of private

investments is also a huge market (for instance home financing), however originally it was

forbidden to take loans for private persons as it would encourage them to “live beyond their

means” (Altundag & Nadia, 2005, 48).

Each Islamic financing technique is based upon either of two basic principles. These are “profit

and loss sharing” and “mark-up” (also referred to as “cost-plus financing”). The profit and loss

sharing technique is used for equity-based financing modes as the bank invests directly in business

ventures and participates in generated profits or losses. In contrast the mark-up technique is

applied in debt-financing techniques as the customer appears as debtor to the bank, paying the

original purchase price of a commodity plus a predetermined mark-up.

In the following the structures of both financing techniques are described and examples for

implementation are given. It has to be mentioned that the nomenclature of Shariah compliant

products is not uniform. For this reason it is possible that some of the products presented below

are named differently depending on the literature. The list is not exhaustive and points out only

some of the most popular examples of Islamic financial products.

1.2.1. Equity-based financing techniques

Equity-based financing modes in Islamic banking constitute the ideal form of financing for

Shariah scholars as the bank participated directly in the business venture and forms together with

the entrepreneur a partnership. Therefore the two forms presented below are known as “twin

pillars of Islamic banking” (Lewis and Algaoud 2001, 45). It is referred to as “variable return

financing” because the return cannot be determined in advance but only the ratio of participation

in profit or loss generated (Dar 2007, 85). However for the banks the following techniques are the

most risky ones and they “show strong preference for other less risky modes” (Lewis & Algaoud,

2001, 48) (please refer to chapter 1.4.2).

1.2.1.1. Mudaraba

The Mudaraba contract is a two tiered transaction for an Islamic bank. On the asset side it

provides money, for example for an entrepreneur called “Mudarib”, and finances its project as so-

called “Rabb al-mal”. As such it possesses all assets but does not have any active part in the

enterprise. At the end of the contract the investment is redeemed by the entrepreneur and the

1. Foundations and Basic Principles of Islamic Banking

11

bank participates in the generated profit on a predetermined basis. However if the project fails it

participates simultaneously in the losses and can, in the worst case, lose all its investment (but not

more). The entrepreneur manages the project and provides his economic and technical knowhow.

He is liable to the bank in case of gross negligence and might lose his income. As he has not

invested capital, his financial damage will be very limited (Mirakhor and Zaidi 2007, 49 to 52 and

Gassner, and Wackerbeck 2007, 63). The funds used by the bank are usually held in trusteeship

from savings or investment account holders, i.e. depositors (liability side). The depositors share in

turn the profits and losses experienced by the bank and thus participate in the earnings of the

projects or companies the bank has invested in. To come to full circle their rate of return depends

from the real sector and cannot be considered as interest (please refer to chapter 1.1.1.1)

(Mirakhor and Zaidi 2007, 51 and 52). As the bank only provides capital but no management

expertise this form of financing is also called “Qirad”, to be translated as “dormant partnership”

(Lewis and Algaoud 2001, 27 and 28). The mechanism of a Mudaraba contract between a bank and

a company (i.e. the asset side) is shown in Figure 2.

Figure 2 Example of a Mudaraba transaction from Gassner and Wackerbeck (2007, 64)

1.2.1.2. Musharaka

The Musharaka partnerships are very similar to the Mudaraba form however in contrast to the

former both, entrepreneur and bank, provide capital for the project and form de facto a kind of

Joint Venture. Both partners have the rights (but not the obligation) to participate in the

management and share profits according to a predetermined ratio and losses in proportion to

their respective capital invested. Consequently both have the incentive to invest wisely and should

1. Foundations and Basic Principles of Islamic Banking

12

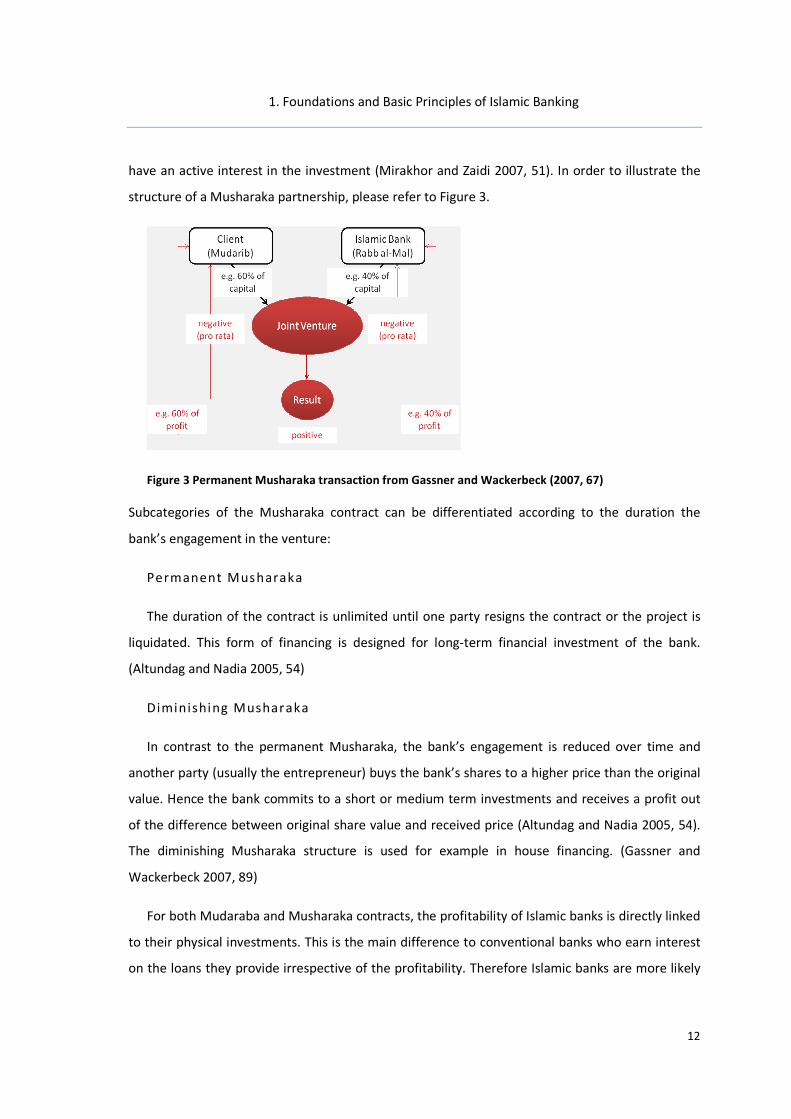

have an active interest in the investment (Mirakhor and Zaidi 2007, 51). In order to illustrate the

structure of a Musharaka partnership, please refer to Figure 3.

Figure 3 Permanent Musharaka transaction from Gassner and Wackerbeck (2007, 67)

Subcategories of the Musharaka contract can be differentiated according to the duration the

bank’s engagement in the venture:

Permanent Musharaka

The duration of the contract is unlimited until one party resigns the contract or the project is

liquidated. This form of financing is designed for long-term financial investment of the bank.

(Altundag and Nadia 2005, 54)

Diminishing Musharaka

In contrast to the permanent Musharaka, the bank’s engagement is reduced over time and

another party (usually the entrepreneur) buys the bank’s shares to a higher price than the original

value. Hence the bank commits to a short or medium term investments and receives a profit out

of the difference between original share value and received price (Altundag and Nadia 2005, 54).

The diminishing Musharaka structure is used for example in house financing. (Gassner and

Wackerbeck 2007, 89)

For both Mudaraba and Musharaka contracts, the profitability of Islamic banks is directly linked

to their physical investments. This is the main difference to conventional banks who earn interest

on the loans they provide irrespective of the profitability. Therefore Islamic banks are more likely

1. Foundations and Basic Principles of Islamic Banking

13

to demand a continuous, complete flow of information from their counterparty which might lead

to higher transparency and stability. They tend to be more interested in stable long-term

relationships with their clients. (Mirakhor and Zaidi 2007, 49) According to Bergmann (2008, 38)

these forms of equity financing fosters the better understanding and monitoring of the business

and involved risks from the bank’s side. However Gassner and Wackerbeck (2007, 67) argue that

the current use of equity-based forms in Islamic finance is very low (approximately 5 percent on

the asset side in Islamic banks). This is mainly due to the high risk involvement of the banks, an

obvious principal-agent problem12 and the increasing innovation in the Islamic finance industry

evolving debt-based instruments, leasing forms and efficient capital market instruments (please

refer to the chapters 1.2.2, 1.2.3 and 1.2.4).

1.2.2. Debt-based financing techniques

In contrast to the techniques described above, debt-based financing is referred to as “fixed

return financing” (Dar 2007, 85) based on the “mark-up” or “cost-plus” concept.

In order to visualize the structure and its implication the most popular financing instrument,

Murabaha, is outlined below. It is used as basis in 70 to 80 percent of all Islamic financing

transaction according to Altundag und Nadia (2005, 51) and Bergmann (2008, 50).

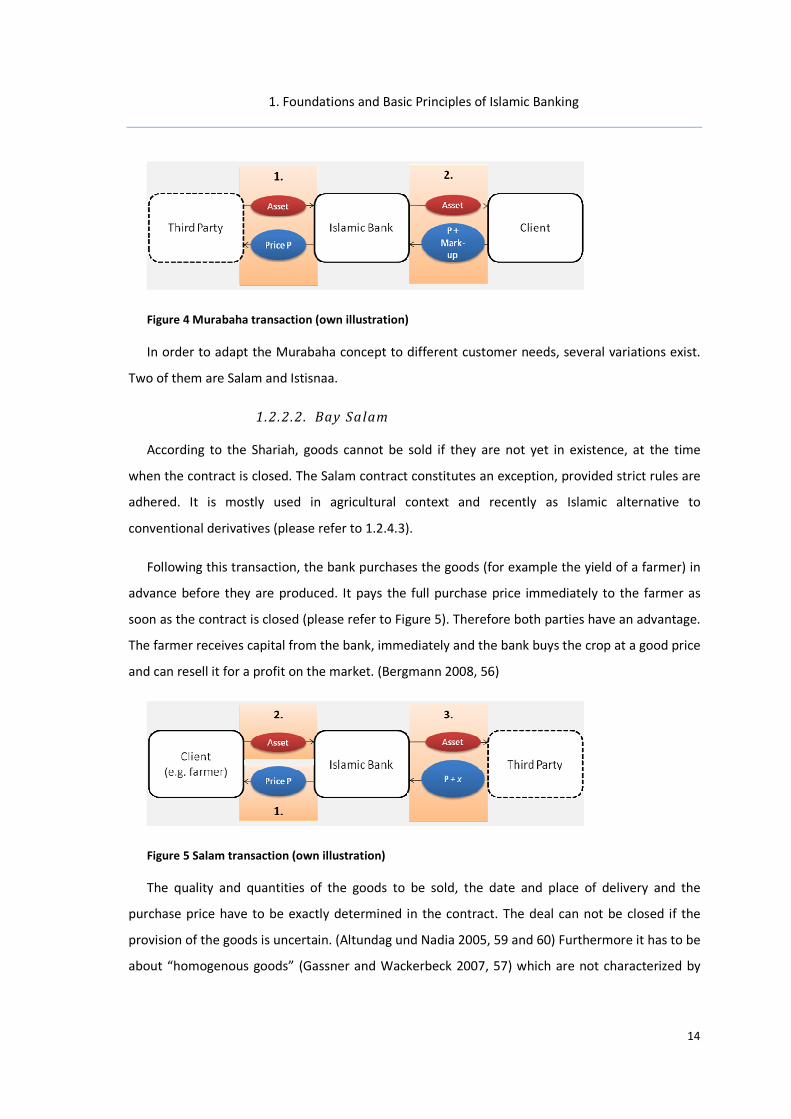

1.2.2.1. Murabaha

In Islamic banking business, loans to private and business clients have to be granted for a

specific purpose (for example to buy a specific commodity). In this way the Islamic bank purchases

the commodity from a third party on behalf of its client. Before reselling it to him it adds a

predetermined mark-up on the spot price constituting the return for its services. The client

redeems the amount either immediately or on a deferred payment basis-called “Murabaha-bi-

muajjal”. (Mirakhor and Zaidi 2007, 52 and Lewis and Algaoud 2001, 52) The mark-up is fixed in a

contract before hand and can not be changed during the duration of the contract. Therefore it is

to be clearly differentiated from interest at it is not linked to the duration but “computed on

transaction basis for services rendered” (Lewis and Algaoud 2001, 52 and 53). The bank bears an

associated risk as it owns the assets between purchase and resale. (Mirakhor and Zaidi 2007, 52)

12

If managers are agents of the financiers, called the principals, moral hazard might be involved as “the

managers […] may act in their own interest rather than in the interest of the principals” (Mishkin 2003, 193).

1. Foundations and Basic Principles of Islamic Banking

14

Figure 4 Murabaha transaction (own illustration)

In order to adapt the Murabaha concept to different customer needs, several variations exist.

Two of them are Salam and Istisnaa.

1.2.2.2. Bay Salam

According to the Shariah, goods cannot be sold if they are not yet in existence, at the time

when the contract is closed. The Salam contract constitutes an exception, provided strict rules are

adhered. It is mostly used in agricultural context and recently as Islamic alternative to

conventional derivatives (please refer to 1.2.4.3).

Following this transaction, the bank purchases the goods (for example the yield of a farmer) in

advance before they are produced. It pays the full purchase price immediately to the farmer as

soon as the contract is closed (please refer to Figure 5). Therefore both parties have an advantage.

The farmer receives capital from the bank, immediately and the bank buys the crop at a good price

and can resell it for a profit on the market. (Bergmann 2008, 56)

Figure 5 Salam transaction (own illustration)

The quality and quantities of the goods to be sold, the date and place of delivery and the

purchase price have to be exactly determined in the contract. The deal can not be closed if the

provision of the goods is uncertain. (Altundag und Nadia 2005, 59 and 60) Furthermore it has to be

about “homogenous goods” (Gassner and Wackerbeck 2007, 57) which are not characterized by

1. Foundations and Basic Principles of Islamic Banking

15

special features that could make it difficult to find a substitute. The contract is binding. In this way

that the seller (farmer) has to buy the goods on the market if he is not able to provide them at the

agreed date. (Gassner and Wackerbeck 2007, 57) Usually the Islamic financial insitutions tries to

resell the goods immediately as it does not want to be in the physical possession of it.

Consequently they might enter a parallel contract. Either the goods are resold to the original seller

or to a third party for a higher price than the purchase price, so that the Islamic financial

institutions makes a profit. (Bacha 1999)

1.2.2.3. Istisnaa

The Istisnaa contract can be seen as subcategory of Salam, designed for a special purpose, such

as the financing of manufacturing on contract or for project financing. (Bergmann 2008, 59)

The structure becomes obvious using an example from Gassner and Wackerbeck (2007,59): A

customer approaches the Islamic bank because he needs a specific good (for example a machine),

which is not yet produced and which he cannot pay immediately. After the Istisnaa contract is

closed, the bank assigns a respective supplier with the production of the machine according to the

specifications of its customer. The manufacturer receives a first installment from the bank at the

start and further payments as the production advances until the machine is finished. Subsequently

the machine is handed over to the bank and later on to the customer who pays the purchase price

plus a predetermined margin to the bank in regular installments after he has received the good.

Additionally to Salam and Istisnaa there exist further forms of contracts that are based on the

Murabaha concept (for example Arbun) which will not be explained in the context of this paper.13

1.2.3. Leasing

In chapter 1.1.2 “the transfer of the right to use” (Ijarah) was mentioned as one out of four root

transactions in Islamic banking. Ijarah contracts are quite similar to the conventional concept of

leasing, however some aspects are different in order to avoid Riba and Gharar (please refer to

chapters 1.1.1.1 and 1.1.1.2). They are very popular with Islamic financial institutions and can be

found in the structures of the most innovative structures (please refer, for example, to Ijarah

Sukuk in chapter 1.2.4.2) owing their great flexibility. In one of the largest Islamic financial centres,

Malaysia, 31.6 percent of the total Islamic financing activities in 2005 was based on the Ijarah

13

Further information can be retrieved from for example from Gassner and Wackerbeck (2007, 53 to 63) or

Lewis and Algaoud (2001, 55 to 59).

1. Foundations and Basic Principles of Islamic Banking

16

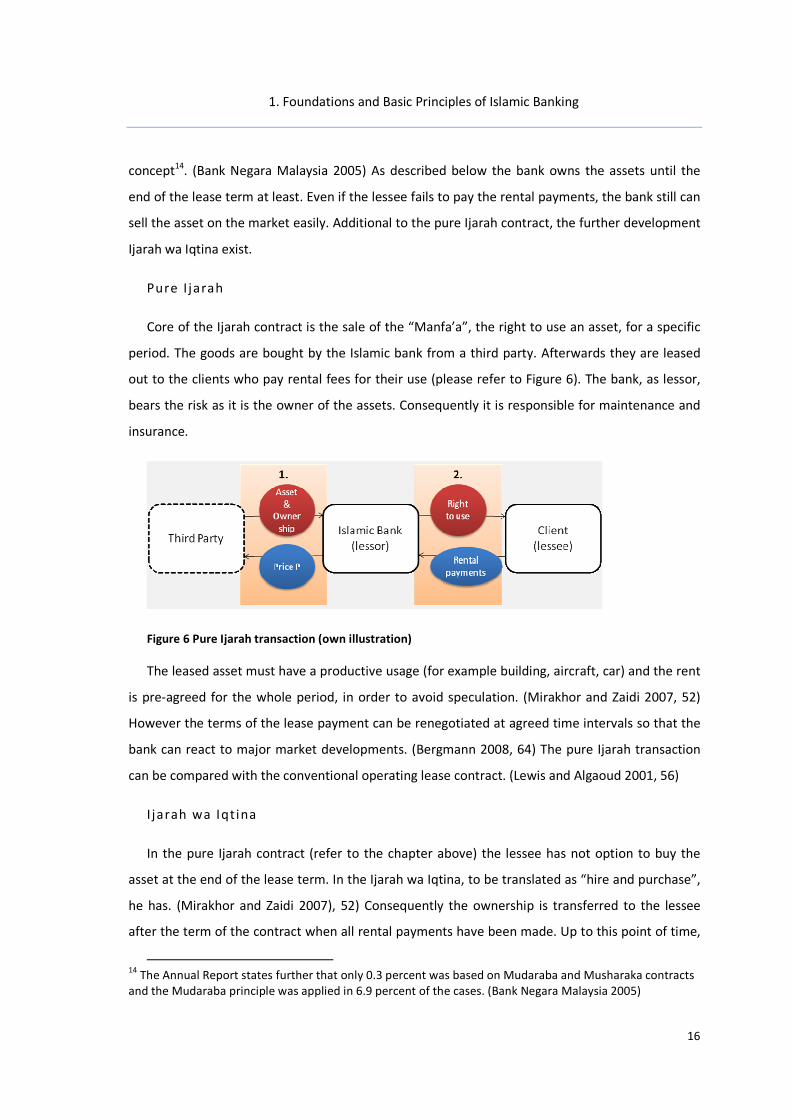

concept14. (Bank Negara Malaysia 2005) As described below the bank owns the assets until the

end of the lease term at least. Even if the lessee fails to pay the rental payments, the bank still can

sell the asset on the market easily. Additional to the pure Ijarah contract, the further development

Ijarah wa Iqtina exist.

Pure I jarah

Core of the Ijarah contract is the sale of the “Manfa’a”, the right to use an asset, for a specific

period. The goods are bought by the Islamic bank from a third party. Afterwards they are leased

out to the clients who pay rental fees for their use (please refer to Figure 6). The bank, as lessor,

bears the risk as it is the owner of the assets. Consequently it is responsible for maintenance and

insurance.

Figure 6 Pure Ijarah transaction (own illustration)

The leased asset must have a productive usage (for example building, aircraft, car) and the rent

is pre-agreed for the whole period, in order to avoid speculation. (Mirakhor and Zaidi 2007, 52)

However the terms of the lease payment can be renegotiated at agreed time intervals so that the

bank can react to major market developments. (Bergmann 2008, 64) The pure Ijarah transaction

can be compared with the conventional operating lease contract. (Lewis and Algaoud 2001, 56)

I jarah wa Iqtina

In the pure Ijarah contract (refer to the chapter above) the lessee has not option to buy the

asset at the end of the lease term. In the Ijarah wa Iqtina, to be translated as “hire and purchase”,

he has. (Mirakhor and Zaidi 2007), 52) Consequently the ownership is transferred to the lessee

after the term of the contract when all rental payments have been made. Up to this point of time,

14

The Annual Report states further that only 0.3 percent was based on Mudaraba and Musharaka contracts

and the Mudaraba principle was applied in 6.9 percent of the cases. (Bank Negara Malaysia 2005)

1. Foundations and Basic Principles of Islamic Banking

17

the lessor bears all risks for possible losses or damages regarding the lease asset, except they are

caused by gross negligence of the lessee. (Gassner and Wackerbeck 2007, 69) The Ijarah wa iqtina

contract is similar to a financing lease arrangement in the conventional system. (Lewis and

Algaoud 2001, 56)

1.2.4. Capital market instruments

Due to the infancy of the Islamic financial industry the number of Shariah-compliant capital

market instruments is very small compared to the conventional market. However numerous

product innovations have been developed in the last decades in order to create competitive

products for private and business customers as well as for the Islamic financial institutions

themselves. To give some examples, this chapter will focus on Islamic stocks, mutual equity funds,

Sukuk and Islamic derivatives.

1.2.4.1. Islamic stocks and equity funds

Investment in shares is very interesting for Muslim investor as no element of Riba (please refer

to 1.1.1.1) is involved in contrast to other capital market instruments, like bonds for example.

From the point of view of Shariah scholars, equity shares are preferred instruments because the

capital is provided for productive purposes and the shareholder participates directly in the

entrepreneurial success. However investment targets have to be filtered following two processes:

the “industry screen” and the “financial-ratio screen”. (Dow Jones Indexes 2008)

Industry screen

Firstly there exist restrictions regarding the industry in which the target company operates.

According to the code of ethical investment that distinguishes between Haram and Halal

investments (please refer to 1.1.1.3), Muslims are only allowed to invest in shares of Halal

businesses. The Dow Jones Islamic Market Index (presented later in this chapter) that constitutes a

major benchmark in the Islamic financial service industry summarizes on its homepage Haram

businesses that are excluded for stock investments (Dow Jones Indexes[2] 2008):

“Excluded from the indexes are producers of alcohol and pork-related products, providers

of conventional financial services (banking, insurance, etc.) and providers of

entertainment services (hotels, casinos/gambling, cinema, pornography, music, etc.).

1. Foundations and Basic Principles of Islamic Banking

18

Tobacco manufacturers and defence and weapons companies, although not strictly

forbidden for investment under Islamic Law, are excluded from the indexes as well.

Financial -ratio screen

As soon as a stock passed the industry screen its financial parameters are scrutinized.

Firstly the debt to equity ratio15 has to be lower than 33 percent. Secondly the percentage of

cash and interest bearing securities has to be lower than 33 percent in reference to market

capitalization. The same is true for the relation between accounts receivables and market

capitalization. (Dow Jones Indexes 2008)

Due to complexity of modern companies, in cannot be avoided that firms are to a very limited

extend active in Haram businesses. Therefore more liberal Shariah scholars argue that the ratio of

Haram business in relation to total revenues must not exceed 5%. However this ratio is

controversial and not applied by all Shariah Supervisory Boards. (Gassner and Wackerbeck 2007,

128)

As can been seen from both the industry and financial-ratio screen it is rather complicated for a

private investor to find a Shariah-compliant investment. Therefore Islamic equity indices are very

popular as the screening processes are executed by professional firms and supervised by a Shariah

supervisory board. The major Islamic equity indices are the Dow Jones Islamic Market Index series,

the Standard and Poor’s Shariah Indices and the FTSE Global Islamic Index Series. Many Islamic

funds as well as private and business investors align their portfolio with these indices.

Is lamic equity funds

Islamic equity funds can be structured in two ways- either as a Mudaraba partnership (please

refer to 1.2.1.1) or according to the Wakala model16. In both cases a Shariah Supervisory Board has

to supervise the Shariah-conformity of the investment decisions and the investment companies

operations.

15

The debt to equity ratio is calculated by dividing the total debt by the 12-months average of equity capital

or the firm’s market capitalization. (Dow Jones Indexes 2008) 16

Literally Wakala means “looking after, taking custody” (Ayub 2007, 347) and describes an agency contract

in Islamic finance.

1. Foundations and Basic Principles of Islamic Banking

19

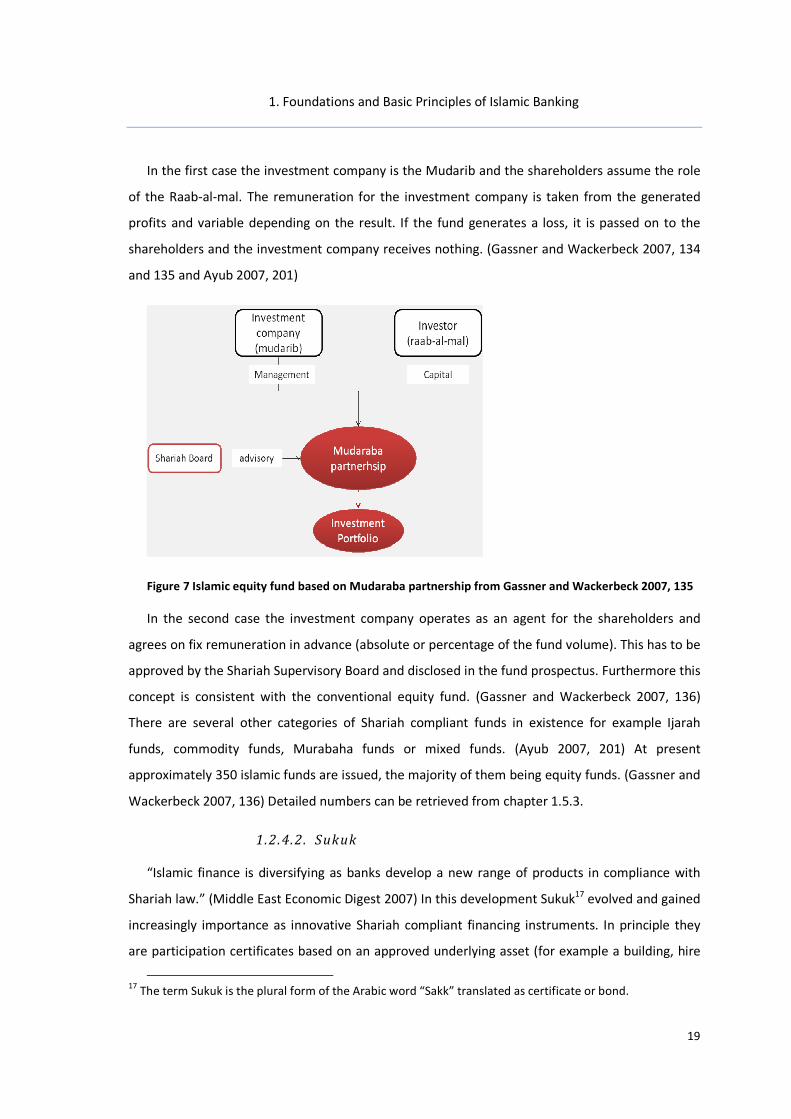

In the first case the investment company is the Mudarib and the shareholders assume the role

of the Raab-al-mal. The remuneration for the investment company is taken from the generated

profits and variable depending on the result. If the fund generates a loss, it is passed on to the

shareholders and the investment company receives nothing. (Gassner and Wackerbeck 2007, 134

and 135 and Ayub 2007, 201)

Figure 7 Islamic equity fund based on Mudaraba partnership from Gassner and Wackerbeck 2007, 135

In the second case the investment company operates as an agent for the shareholders and

agrees on fix remuneration in advance (absolute or percentage of the fund volume). This has to be

approved by the Shariah Supervisory Board and disclosed in the fund prospectus. Furthermore this

concept is consistent with the conventional equity fund. (Gassner and Wackerbeck 2007, 136)

There are several other categories of Shariah compliant funds in existence for example Ijarah

funds, commodity funds, Murabaha funds or mixed funds. (Ayub 2007, 201) At present

approximately 350 islamic funds are issued, the majority of them being equity funds. (Gassner and

Wackerbeck 2007, 136) Detailed numbers can be retrieved from chapter 1.5.3.

1.2.4.2. Sukuk

“Islamic finance is diversifying as banks develop a new range of products in compliance with

Shariah law.” (Middle East Economic Digest 2007) In this development Sukuk17 evolved and gained

increasingly importance as innovative Shariah compliant financing instruments. In principle they

are participation certificates based on an approved underlying asset (for example a building, hire

17

The term Sukuk is the plural form of the Arabic word “Sakk” translated as certificate or bond.

1. Foundations and Basic Principles of Islamic Banking

20

cars, oil or gas pipelines) for specified financial consideration. For this reason they can be regarded

as asset backed securities. (Middle East Economic Digest 2007) However it is to be clearly

differentiated from conventional bonds as the latter present an debt to the issuer only, whereas

Sukuk represent “additionally an ownership stake in an asset or project” (Mirakhor and Zaidi 2007,

57)

Sukuk can be based on several Islamic commercial contracts. The categories that are most

common are Sukuk al-Murabaha (debt based), Sukuk al-Mudaraba (equity based), Sukuk al-

Musharaka (equity based), Sukuk al-Ijarah (debt based), Sukuk al-Salam (debt based), Sukuk al-

Istisnaa (debt based) and hybrid Sukuk forms. (el-Mogaddedi 2007)

As the Sukuk al-Ijara are among the most popular forms of Sukuk they will be taken as an

example in the following. The structure comprises the use of a specified asset through the lessee

whilst the ownership remains with the lessor. Mostly the former is the original owner of the asset

and enters a sale-and-lease back arrangement with a so-called Special Purpose Vehicle (SPV). The

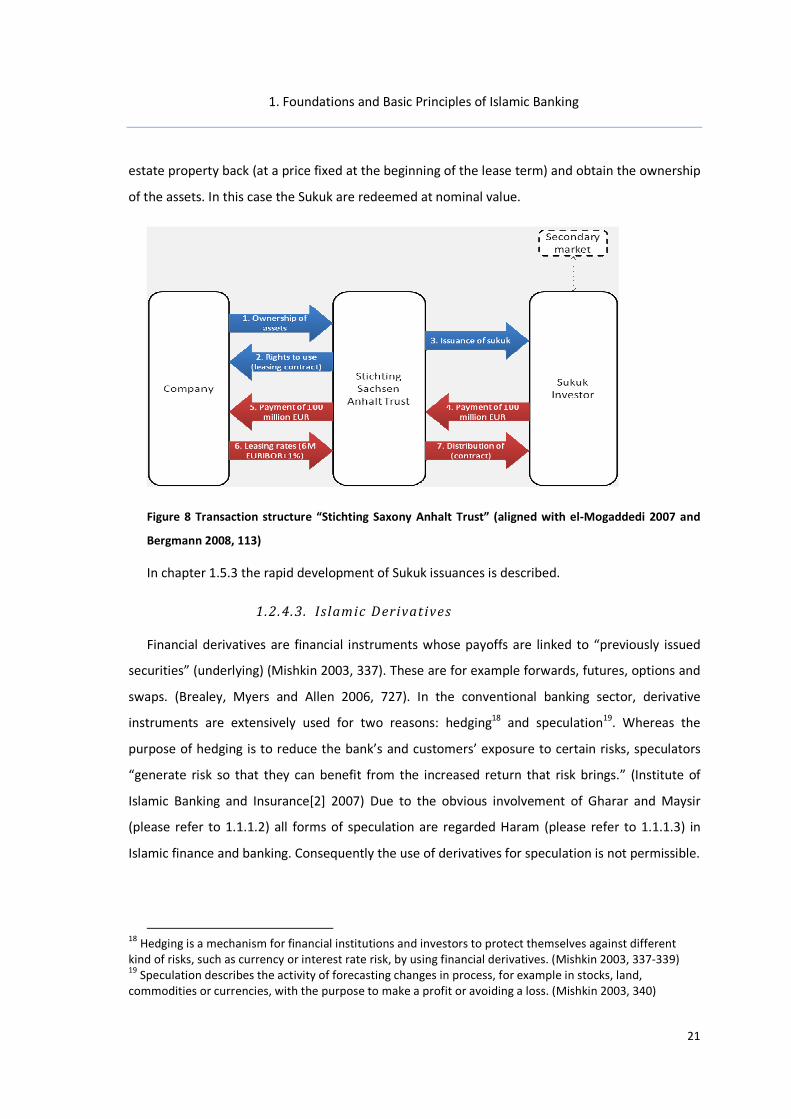

leasing project could be a real estate investment, for example. In 2004 the German federal state

Saxony Anhalt carried out the first sovereign Sukuk issuance in Germany. This prominent example

of the “Stichting Saxony Anhalt Trust” which will be used to present the basic structure of a Sukuk

al-Ijara transaction.

Firstly Saxony Anhalt found a Special Purpose Vehicle, in this case the “Stichting Saxony Anhalt

Trust” which was established in the Netherlands for tax reasons. Subsequently Saxony Anhalt sold

some of its real estate property, mostly used by fiscal authorites, to this trust and entered

simoultanuously a leasing contract for a time period of five years in order to obtain the rights to

use back. The “Stichting Saxony Anhalt Trust” issued Sukuk amounting to € 100 million in 2004 on

the basis of the acquired real estate property. The Sukuk investors (60 percent originating from

the Gulf states and 40 percent from Europe according to Bergmann (2008, 113)) paid the € 100

million to the trust that forwarded the capital to the federal state. The latter payed predetermined

leasing rates based on the six months EURIBOR plus 1 percent. These payments were distributed

to the Sukuk investors according to the contracts signed. In most cases Sukuk can be traded on a

secondary market, provided there is sufficient liquidity. The transaction can be better

comprehended looking at Figure 8. After the period of five years, Saxony Anhalt may buy the real

1. Foundations and Basic Principles of Islamic Banking

21

estate property back (at a price fixed at the beginning of the lease term) and obtain the ownership

of the assets. In this case the Sukuk are redeemed at nominal value.

Figure 8 Transaction structure “Stichting Saxony Anhalt Trust” (aligned with el-Mogaddedi 2007 and

Bergmann 2008, 113)

In chapter 1.5.3 the rapid development of Sukuk issuances is described.

1.2.4.3. Islamic Derivat ives

Financial derivatives are financial instruments whose payoffs are linked to “previously issued

securities” (underlying) (Mishkin 2003, 337). These are for example forwards, futures, options and

swaps. (Brealey, Myers and Allen 2006, 727). In the conventional banking sector, derivative

instruments are extensively used for two reasons: hedging18 and speculation19. Whereas the

purpose of hedging is to reduce the bank’s and customers’ exposure to certain risks, speculators

“generate risk so that they can benefit from the increased return that risk brings.” (Institute of

Islamic Banking and Insurance[2] 2007) Due to the obvious involvement of Gharar and Maysir

(please refer to 1.1.1.2) all forms of speculation are regarded Haram (please refer to 1.1.1.3) in

Islamic finance and banking. Consequently the use of derivatives for speculation is not permissible.

18

Hedging is a mechanism for financial institutions and investors to protect themselves against different

kind of risks, such as currency or interest rate risk, by using financial derivatives. (Mishkin 2003, 337-339) 19

Speculation describes the activity of forecasting changes in process, for example in stocks, land,

commodities or currencies, with the purpose to make a profit or avoiding a loss. (Mishkin 2003, 340)

1. Foundations and Basic Principles of Islamic Banking

22

Hedging, however, is basically allowed for Islamic financial institutions as soon as the derivative

instruments and the underlying assets are structured and chosen in conformity with Shariah

requirements. (Gassner and Wackerbeck 2007, 153)

As already mentioned in chapter 1.4, adequate alternatives to conventional derivatives are very

rare in the young Islamic financial industry but substantial efforts are taken to fill the void.

(Institute of Islamic Banking and Insurance[1] 2007) In the context of derivatives the need for

innovation arises out of the unconformity of conventional derivatives with the Shariah in various

aspects. According to Gassner and Wackerbeck (2007, 154) the following features of conventional

derivatives contradict with Shariah requirements. Firstly the underlying asset is never delivered

and just a price difference, for example between spot and future market, is balanced. In this way

the contract is about a“fictious good” which contradicts the philosophy of Islamic banking,

namingly the promotion of commerce and trade. Secondly for many conventional derivatives both

payment and (fictional) delivery take place in the future. This is generally non-permissible for

Islamic finance contract as well as the trade of liabilities. Finally the evaluation of conventation

derivatives, like options for example, is often based on the interest-based models, such as the

Black-Scholes-formula (please refer to 1.1.1.1). Hence conventional derivatives cannot be used for

risk mitigation by Islamic financial institutions or Muslim investors.

However there are two general approaches to find a solution. On the one hand “a number of

instruments/ contracts exist in Islamic finance that could be considered a basis for derivative

contracts within an Islamic framework.” (Bacha 1999, 18). These are especially Bay Salam (please

refer to chapter 1.2.2.1) structures. On the other hand new Islamic products are developed, which

are not applied in practice so far, for example Khiyar and Istijrar. For both approaches the

admissibility is disputed by Shariah scholars. The Islamic Financial Services Board (please refer to

chapter 1.3.6.2) holds the following:

“For risk mitigation instruments (in particular, derivatives) such as the Islamic profit rate

swap, foreign exchange swap, forward (using the Salam principle), forward foreign

exchange (using the Wa`d principle), options (using the `urbun principle), futures contract

and Bay` al-Istijrar contracts, only half of the jurisdictions surveyed accepted these

contracts as Shari`ah permissible. The different Shari`ah interpretations among

jurisdictions – and among Shari`ah boards of IIFS – have also resulted in non-uniformity in

1. Foundations and Basic Principles of Islamic Banking

23

the acceptance and design of Shari`ah-compliant alternatives.” (Islamic Financial Services

Board[1] 2008)

In order to give an example for the application of traditional Islamic contracts as hedging

instruments, the use of the Bay Salam contract will be explained. For the basic understanding of

Bay Salam contract please refer back to chapter 1.2.2.1. In principle the structure can “closely

resemble forwards20” (Bacha 1999, 19) with the difference that the buyer of the commodity in the

first place, pays the full purchase price as soon as the contract is closed and not at the end of the

contract term. Another difference is that the “predetermined price is normally lower than the

prevailing spot price” (Bacha 1999, 18) because the buyer is compensated for the full payment in

advance so that he can resell the asset with profit. Whereas in a conventional forward contract the