dire straits for central bankers - custprd.comcustprd.com/rsch/velocity.pdfdire straits for central...

TRANSCRIPT

P a g e | 1 www.custprd.com

Hong Kong Tokyo

Salt Lake City

Dire Straits for central bankers

Money for nothing brothers in arms are out of ammunition 17th June 2016

Mike Newman

It is a clash of titans between

economic theory and

social reality

Social disruption

7 realities in today’s

markets

Executive Summary Better to sit down. We will be entering some pretty bleak conclusions in this report. The world’s

central banks have hit stall speed. They have lost control and do not have enough altitude to

recover. How bad can things get? There are two things at play here. One is economic (explicitly

monetary) policy. The other is social reality (explicitly hardship). Both have become dysfunctional.

Reckless central bank monetary expansion sold behind the banner of ‘nothing to see here’ has

backfired. Money velocity (or the power of money) across the globe is plummeting to record lows.

While the GFC was easily avoidable the post disaster mop up operation consists of printing our

way out of the disastrous debt pile by inflating it away. Even negative interest rates leave inflation

well below targets. Deflation still prevails. Poverty and post-GFC destitution has reached boiling

point. When people feel robbed of their identity and increasingly their democracy we should not be

surprised to see the rise of nationalism and non mainstream candidates and sadly violence,

especially in Europe. This social disruption should not be ignored because the experimental

financial engineering that was supposed to wiggle us from the bondage of moral hazard has had

the complete opposite effect.

Here are 7 things to ponder;

1) A recent US Federal Reserve survey found that 47% of Americans couldn’t raise $400 in

emergency cash were the need to arise. 5% unemployment rate belies financial

difficulties.

2) A banksurvey in Australia showed 50% of people wouldn’t be able to meet their financial

obligations if unemployed for more than 3 months. Housing price to income ratio almost

twice the level pre-GFC. Private debt: GDP ratio at 160%. Credit rating downgrade

imminent.

3) c.60% of ETF purchases in Japan and c. 100% of sovereign bond purchases are bought

by the Bank of Japan which now owns 38% of outstanding government debt. 15 year

Japanese government bonds now yield -0.004%. Japan’s move to negative rates has

caused a run on sales of mini-vaults as people look to store their own cash.

4) M2/M3 money velocity has hit all time lows in the US, ECB, Australia, China & Japan.

5) Italian banks non performing loans (NPLs) are approaching 20% and as high as 50% in

the south of the country. The ECB is breaching their own covenants to hide the mess.

Belgian Optima Bank has just been shut down for not being able to meet obligations.

Many more?

6) Over 25% of those in the EU live below the poverty line and youth unemployment is c.25%

with long term unemployment now 50%. In Greece those numbers are 36%, 58% and

P a g e | 2 www.custprd.com

Hong Kong Tokyo

Salt Lake City

Money velocity is

falling

Confidence is faltering

Central banks

continue to burn lower

quality

Companies invest when they see the

cycle

sense of déjà vu

Manipulated

markets

History often lies in the

non-consensus

view

History often sides against

the consensus

view

72%.

7) China’s industrial sector among others shows clear signs of recording sales without much

hope of being paid with receivables ballooning in some cases leaping to over 5 years of

reported revenue pointing to a sharp uptick in corporate debt insolvency & NPLs to follow.

Central banks have not only lost the battle with monetary policy they’ve lost the war. Of

course we will hear otherwise in the media and reserve bank press releases. Money velocity

continues to decline despite central banks pumping more into the system on the expectation

growth will come. Of course velocity will mathematically fall when central banks are monetising

debt at the aggressive clip they are. However one word ‘confidence’ is the only thing that keeps

any financial system from collapsing. Sadly we are rapidly approaching the date that central banks

lose that trust. There is plenty of evidence to suggest this is already happening. Confidence relies

on trust. Without it market participants seek refuge wherever they can find it.

Simply put, central bankers continue to pour lower and lower grade lumps of coal into a top fuel

dragster engine (aka the global economy) and still expect it to shatter record times in the quarter-

mile. Sadly the only thing that is set to shatter is the internals of that engine. Declining velocity is

the failed result of trying to create more power from a knackered engine in need of a major

overhaul. The engine will simply suffer a catastrophic failure. It is not a matter of if, but when.

The ECB and BoJ have been explicit in imposing negative rates for the simple idea that punitive

rates will encourage banks to take on riskier lending. Flooding the system with liquidity is not

having the expected impact of priming the economy. Companies and people invest because

they have a clear vision of the future not because rates are low. The BoJ is buying up ETFs at

such a frenetic pace that in time Japanese corporates will become state owned enterprises

eventually.

Markets are supposed to be all about the ‘invisible hand’ but never have we reached a point of so

much proactive manipulation of currency, credit and equity markets. The discount rates pursued

by central banks have only fuelled the overcapacity that prevents us escaping deflation. This déjà

vu in markets reminds me of 2001. There are times I sit back like Michael J. Burry M.D. and

wonder to myself “this isn’t crazy. It’s logical!”

I recall being laughed out of court when I told many of my clients and colleagues in late 2001 that

Greenspan would go down in history as one of the most hated central bankers. The criticism I

copped only exacerbated after pundits labeled him ‘Maestro’ and Her Majesty bestowed him with

a knighthood in 2002. To me it confirmed all this would go to his head and it would be carte

blanche to ‘experiment’ with monetary policy. Investors and politicians alike waited with bated

breath on his next musings. While I never expected markets to implode in 2002, I stuck resolutely

by my criticism of his time at the helm of The Fed because I could clearly visualise the downside

of reckless experiments to see whether the world could be printed out of trouble.

Let us not forget that history has at times proven not to be on the side of conventional wisdom, or

the consensus view, but on the side of those who dissented from them. More significantly, the

media and financial community failed by not being rigorous and questioning enough, resulting in

many anomalies taking too long to be discovered. We have seen so often that the time of

greatest certainty is, in fact, the time to be most sceptical. If we spent more time on biopsies in

journalism, as Adrianna Huffington suggested, there would be far fewer autopsies.

P a g e | 3 www.custprd.com

Hong Kong Tokyo

Salt Lake City

Wild distortion of

asset values

Divergence of asset markets

We never recovered

from the GFC

World Bank trims global

growth again

What this excess liquidity has led to is wild distortions in asset values. With over $10 trillion of

sovereign bonds yielding less than zero interest, bond investors are forced to move further out the

yield curve which carries even more risk when taking duration into account. With some equity

markets approaching all time highs the smart money would appear to be to switch into precious

metals, primarily gold. These have been some of the worst performing assets and in a world

where mean reversion is long overdue the relative outperformance should be striking.

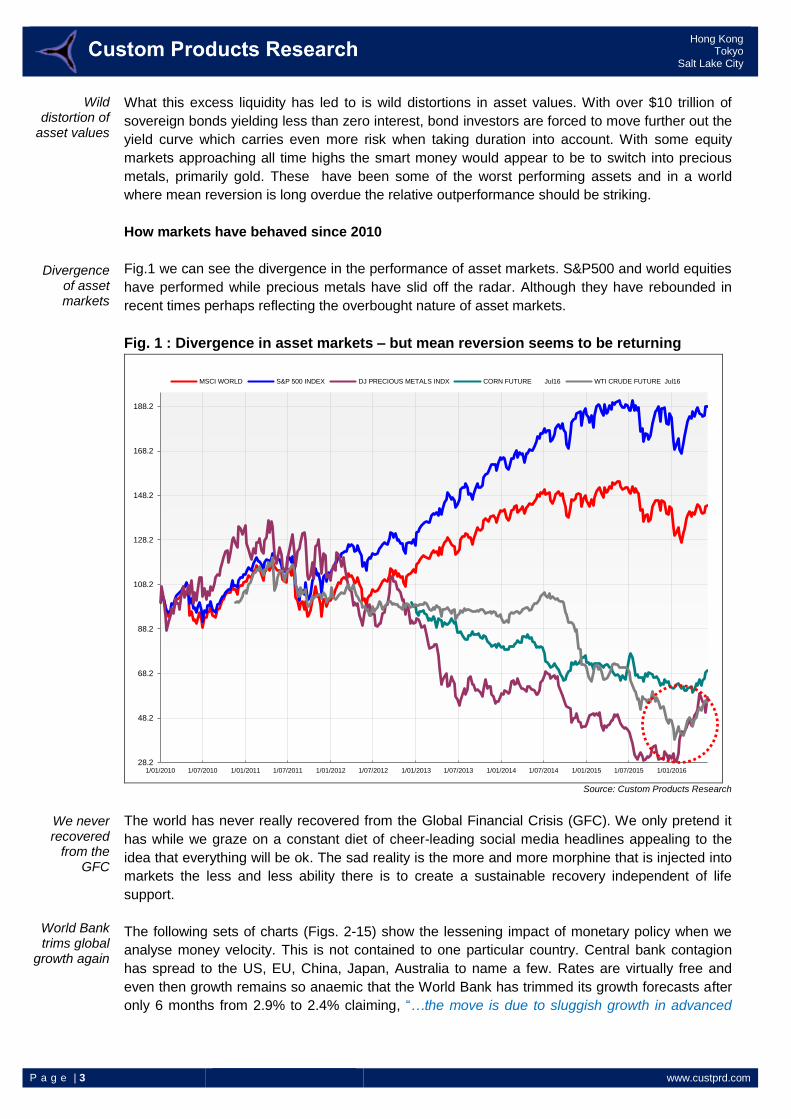

How markets have behaved since 2010

Fig.1 we can see the divergence in the performance of asset markets. S&P500 and world equities

have performed while precious metals have slid off the radar. Although they have rebounded in

recent times perhaps reflecting the overbought nature of asset markets.

Fig. 1 : Divergence in asset markets – but mean reversion seems to be returning

Source: Custom Products Research

The world has never really recovered from the Global Financial Crisis (GFC). We only pretend it

has while we graze on a constant diet of cheer-leading social media headlines appealing to the

idea that everything will be ok. The sad reality is the more and more morphine that is injected into

markets the less and less ability there is to create a sustainable recovery independent of life

support.

The following sets of charts (Figs. 2-15) show the lessening impact of monetary policy when we

analyse money velocity. This is not contained to one particular country. Central bank contagion

has spread to the US, EU, China, Japan, Australia to name a few. Rates are virtually free and

even then growth remains so anaemic that the World Bank has trimmed its growth forecasts after

only 6 months from 2.9% to 2.4% claiming, “…the move is due to sluggish growth in advanced

28.2

48.2

68.2

88.2

108.2

128.2

148.2

168.2

188.2

1/01/2010 1/07/2010 1/01/2011 1/07/2011 1/01/2012 1/07/2012 1/01/2013 1/07/2013 1/01/2014 1/07/2014 1/01/2015 1/07/2015 1/01/2016

MSCI WORLD S&P 500 INDEX DJ PRECIOUS METALS INDX CORN FUTURE Jul16 WTI CRUDE FUTURE Jul16

P a g e | 4 www.custprd.com

Hong Kong Tokyo

Salt Lake City

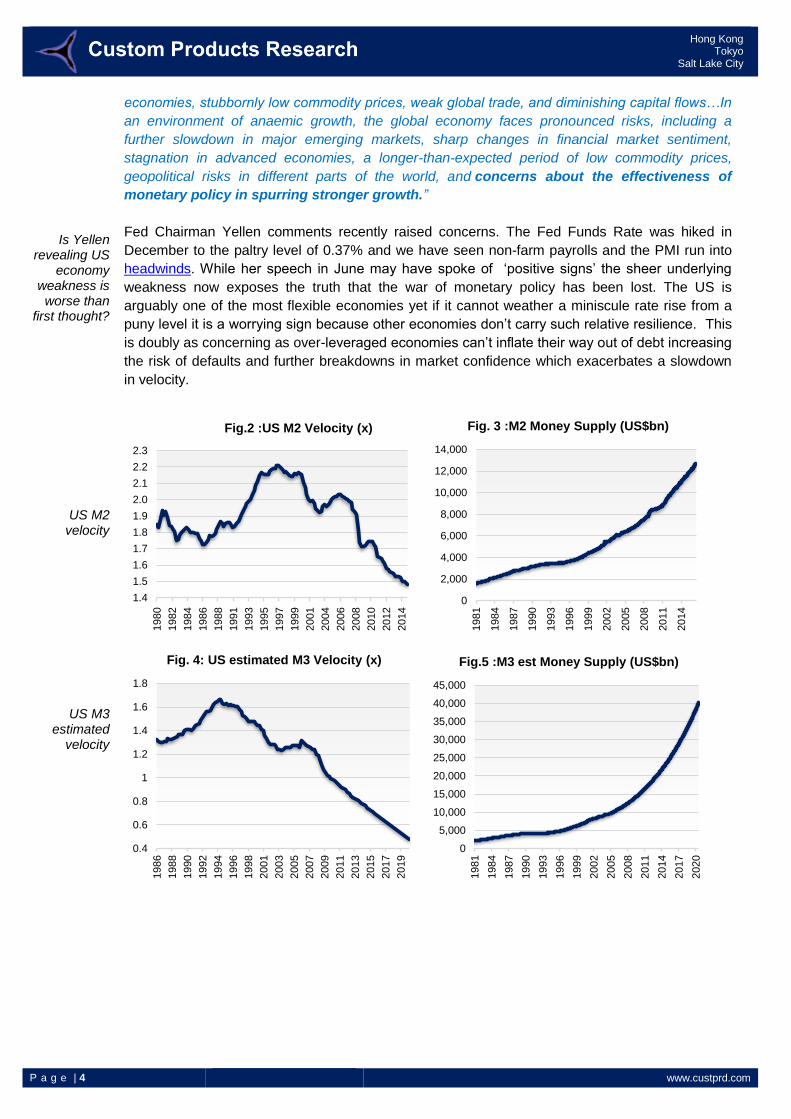

Is Yellen revealing US

economy weakness is worse than

first thought?

US M2 velocity

US M3 estimated

velocity

economies, stubbornly low commodity prices, weak global trade, and diminishing capital flows…In

an environment of anaemic growth, the global economy faces pronounced risks, including a

further slowdown in major emerging markets, sharp changes in financial market sentiment,

stagnation in advanced economies, a longer-than-expected period of low commodity prices,

geopolitical risks in different parts of the world, and concerns about the effectiveness of

monetary policy in spurring stronger growth.”

Fed Chairman Yellen comments recently raised concerns. The Fed Funds Rate was hiked in

December to the paltry level of 0.37% and we have seen non-farm payrolls and the PMI run into

headwinds. While her speech in June may have spoke of ‘positive signs’ the sheer underlying

weakness now exposes the truth that the war of monetary policy has been lost. The US is

arguably one of the most flexible economies yet if it cannot weather a miniscule rate rise from a

puny level it is a worrying sign because other economies don’t carry such relative resilience. This

is doubly as concerning as over-leveraged economies can’t inflate their way out of debt increasing

the risk of defaults and further breakdowns in market confidence which exacerbates a slowdown

in velocity.

1.4

1.5

1.6

1.7

1.8

1.9

2.0

2.1

2.2

2.3

1980

1982

1984

1986

1988

1991

1993

1995

1997

1999

2001

2004

2006

2008

2010

2012

2014

Fig.2 :US M2 Velocity (x)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1981

1984

1987

1990

1993

1996

1999

2002

2005

2008

2011

2014

Fig. 3 :M2 Money Supply (US$bn)

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

1986

1988

1990

1992

1994

1996

1998

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

Fig. 4: US estimated M3 Velocity (x)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

1981

1984

1987

1990

1993

1996

1999

2002

2005

2008

2011

2014

2017

2020

Fig.5 :M3 est Money Supply (US$bn)

P a g e | 5 www.custprd.com

Hong Kong Tokyo

Salt Lake City

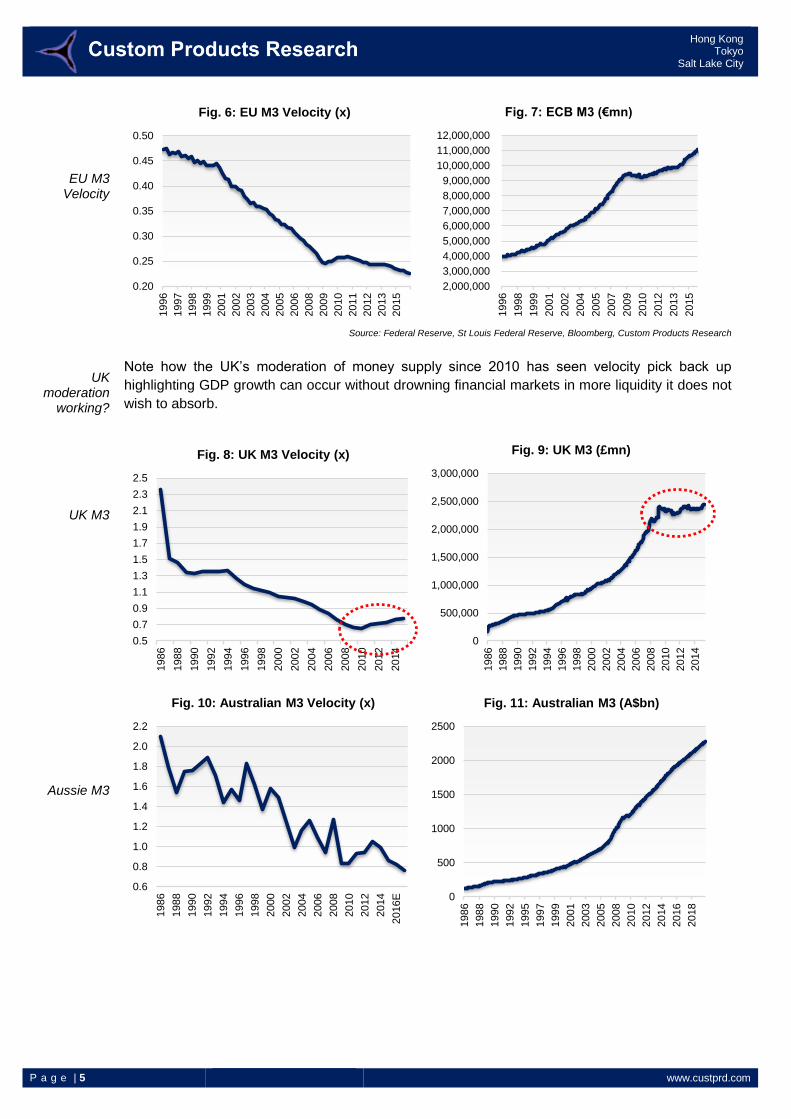

EU M3 Velocity

UK moderation

working?

UK M3

Aussie M3

Source: Federal Reserve, St Louis Federal Reserve, Bloomberg, Custom Products Research

Note how the UK’s moderation of money supply since 2010 has seen velocity pick back up

highlighting GDP growth can occur without drowning financial markets in more liquidity it does not

wish to absorb.

0.20

0.25

0.30

0.35

0.40

0.45

0.50

1996

1997

1998

1999

2001

2002

2003

2004

2005

2006

2008

2009

2010

2011

2012

2013

2015

Fig. 6: EU M3 Velocity (x)

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

9,000,000

10,000,000

11,000,000

12,000,000

1996

1998

1999

2001

2002

2004

2005

2007

2009

2010

2012

2013

2015

Fig. 7: ECB M3 (€mn)

0.5

0.7

0.9

1.1

1.3

1.5

1.7

1.9

2.1

2.3

2.5

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

Fig. 8: UK M3 Velocity (x)

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

Fig. 9: UK M3 (£mn)

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016E

Fig. 10: Australian M3 Velocity (x)

0

500

1000

1500

2000

2500

1986

1988

1990

1992

1995

1997

1999

2001

2003

2005

2008

2010

2012

2014

2016

2018

Fig. 11: Australian M3 (A$bn)

P a g e | 6 www.custprd.com

Hong Kong Tokyo

Salt Lake City

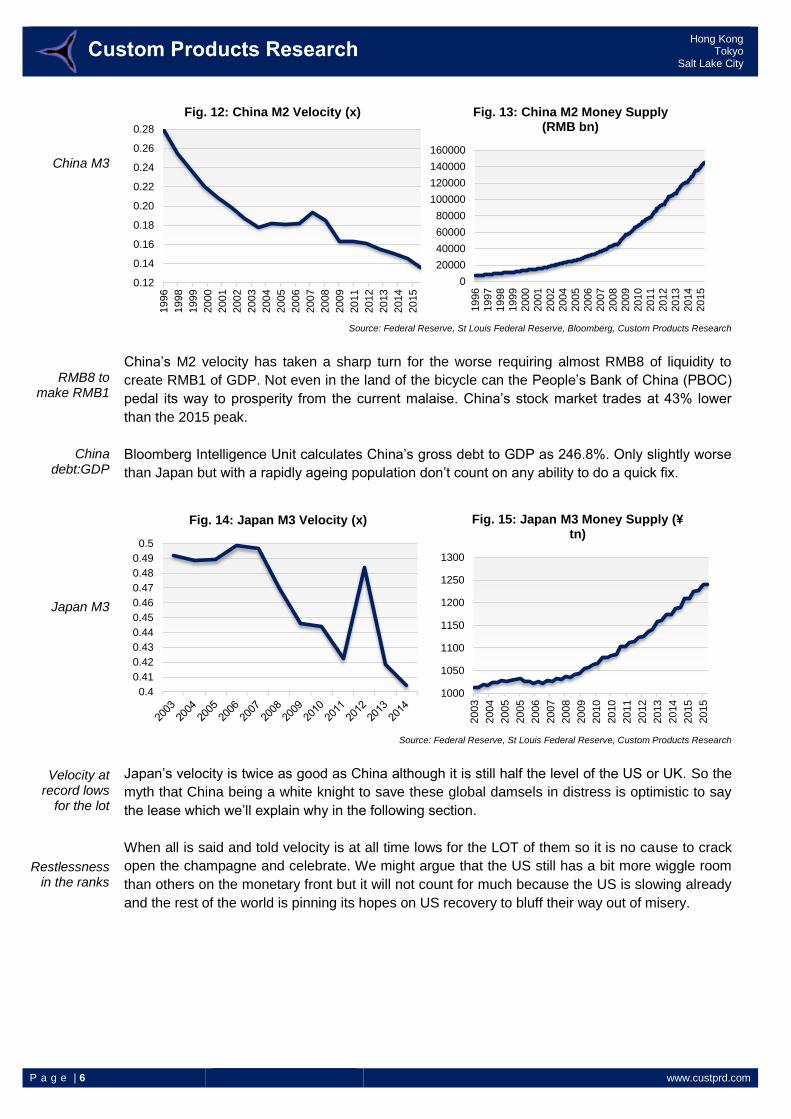

China M3

RMB8 to make RMB1

China debt:GDP

Japan M3

Velocity at record lows

for the lot

Restlessness in the ranks

Source: Federal Reserve, St Louis Federal Reserve, Bloomberg, Custom Products Research

China’s M2 velocity has taken a sharp turn for the worse requiring almost RMB8 of liquidity to

create RMB1 of GDP. Not even in the land of the bicycle can the People’s Bank of China (PBOC)

pedal its way to prosperity from the current malaise. China’s stock market trades at 43% lower

than the 2015 peak.

Bloomberg Intelligence Unit calculates China’s gross debt to GDP as 246.8%. Only slightly worse

than Japan but with a rapidly ageing population don’t count on any ability to do a quick fix.

Source: Federal Reserve, St Louis Federal Reserve, Custom Products Research

Japan’s velocity is twice as good as China although it is still half the level of the US or UK. So the

myth that China being a white knight to save these global damsels in distress is optimistic to say

the lease which we’ll explain why in the following section.

When all is said and told velocity is at all time lows for the LOT of them so it is no cause to crack

open the champagne and celebrate. We might argue that the US still has a bit more wiggle room

than others on the monetary front but it will not count for much because the US is slowing already

and the rest of the world is pinning its hopes on US recovery to bluff their way out of misery.

0.12

0.14

0.16

0.18

0.20

0.22

0.24

0.26

0.28

1996

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2011

2012

2013

2014

2015

Fig. 12: China M2 Velocity (x)

0

20000

40000

60000

80000

100000

120000

140000

160000

1996

1997

1998

1999

2000

2001

2002

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Fig. 13: China M2 Money Supply (RMB bn)

0.4

0.41

0.42

0.43

0.44

0.45

0.46

0.47

0.48

0.49

0.5

Fig. 14: Japan M3 Velocity (x)

1000

1050

1100

1150

1200

1250

1300

2003

2004

2005

2005

2006

2007

2008

2009

2010

2010

2011

2012

2013

2014

2015

2015

Fig. 15: Japan M3 Money Supply (¥ tn)

P a g e | 7 www.custprd.com

Hong Kong Tokyo

Salt Lake City

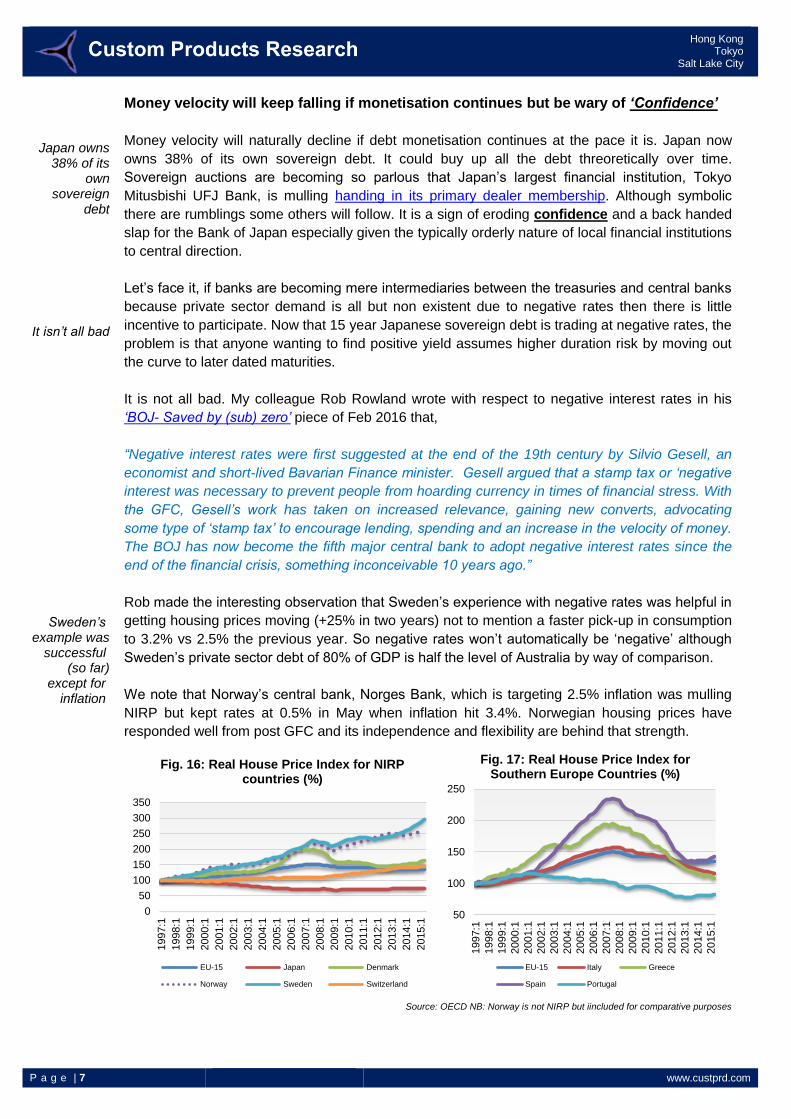

Japan owns 38% of its

own sovereign

debt

It isn’t all bad

Sweden’s example was

successful (so far)

except for inflation

Money velocity will keep falling if monetisation continues but be wary of ‘Confidence’

Money velocity will naturally decline if debt monetisation continues at the pace it is. Japan now

owns 38% of its own sovereign debt. It could buy up all the debt threoretically over time.

Sovereign auctions are becoming so parlous that Japan’s largest financial institution, Tokyo

Mitusbishi UFJ Bank, is mulling handing in its primary dealer membership. Although symbolic

there are rumblings some others will follow. It is a sign of eroding confidence and a back handed

slap for the Bank of Japan especially given the typically orderly nature of local financial institutions

to central direction.

Let’s face it, if banks are becoming mere intermediaries between the treasuries and central banks

because private sector demand is all but non existent due to negative rates then there is little

incentive to participate. Now that 15 year Japanese sovereign debt is trading at negative rates, the

problem is that anyone wanting to find positive yield assumes higher duration risk by moving out

the curve to later dated maturities.

It is not all bad. My colleague Rob Rowland wrote with respect to negative interest rates in his

‘BOJ- Saved by (sub) zero’ piece of Feb 2016 that,

“Negative interest rates were first suggested at the end of the 19th century by Silvio Gesell, an

economist and short-lived Bavarian Finance minister. Gesell argued that a stamp tax or ‘negative

interest was necessary to prevent people from hoarding currency in times of financial stress. With

the GFC, Gesell’s work has taken on increased relevance, gaining new converts, advocating

some type of ‘stamp tax’ to encourage lending, spending and an increase in the velocity of money.

The BOJ has now become the fifth major central bank to adopt negative interest rates since the

end of the financial crisis, something inconceivable 10 years ago.”

Rob made the interesting observation that Sweden’s experience with negative rates was helpful in

getting housing prices moving (+25% in two years) not to mention a faster pick-up in consumption

to 3.2% vs 2.5% the previous year. So negative rates won’t automatically be ‘negative’ although

Sweden’s private sector debt of 80% of GDP is half the level of Australia by way of comparison.

We note that Norway’s central bank, Norges Bank, which is targeting 2.5% inflation was mulling

NIRP but kept rates at 0.5% in May when inflation hit 3.4%. Norwegian housing prices have

responded well from post GFC and its independence and flexibility are behind that strength.

Source: OECD NB: Norway is not NIRP but iincluded for comparative purposes

0

50

100

150

200

250

300

350

1997:1

1998:1

1999:1

2000:1

2001:1

2002:1

2003:1

2004:1

2005:1

2006:1

2007:1

2008:1

2009:1

2010:1

2011:1

2012:1

2013:1

2014:1

2015:1

Fig. 16: Real House Price Index for NIRP countries (%)

EU-15 Japan Denmark

Norway Sweden Switzerland

50

100

150

200

250

1997:1

1998:1

1999:1

2000:1

2001:1

2002:1

2003:1

2004:1

2005:1

2006:1

2007:1

2008:1

2009:1

2010:1

2011:1

2012:1

2013:1

2014:1

2015:1

Fig. 17: Real House Price Index for Southern Europe Countries (%)

EU-15 Italy Greece

Spain Portugal

P a g e | 8 www.custprd.com

Hong Kong Tokyo

Salt Lake City

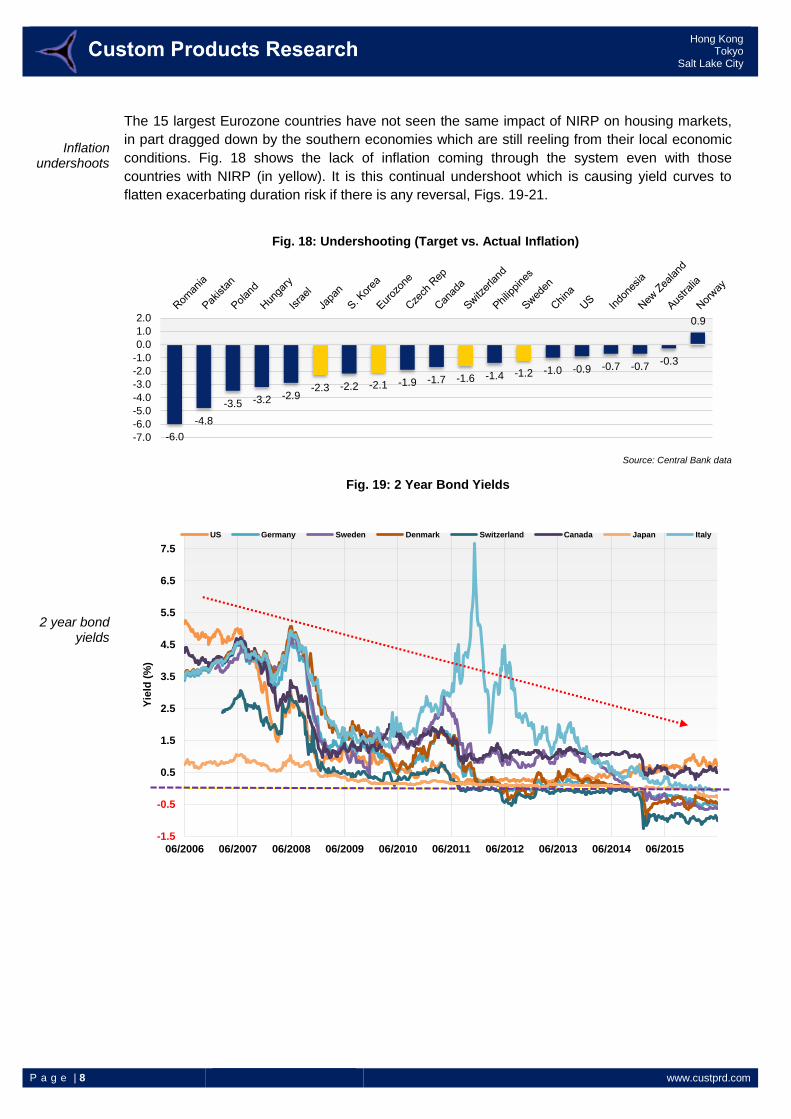

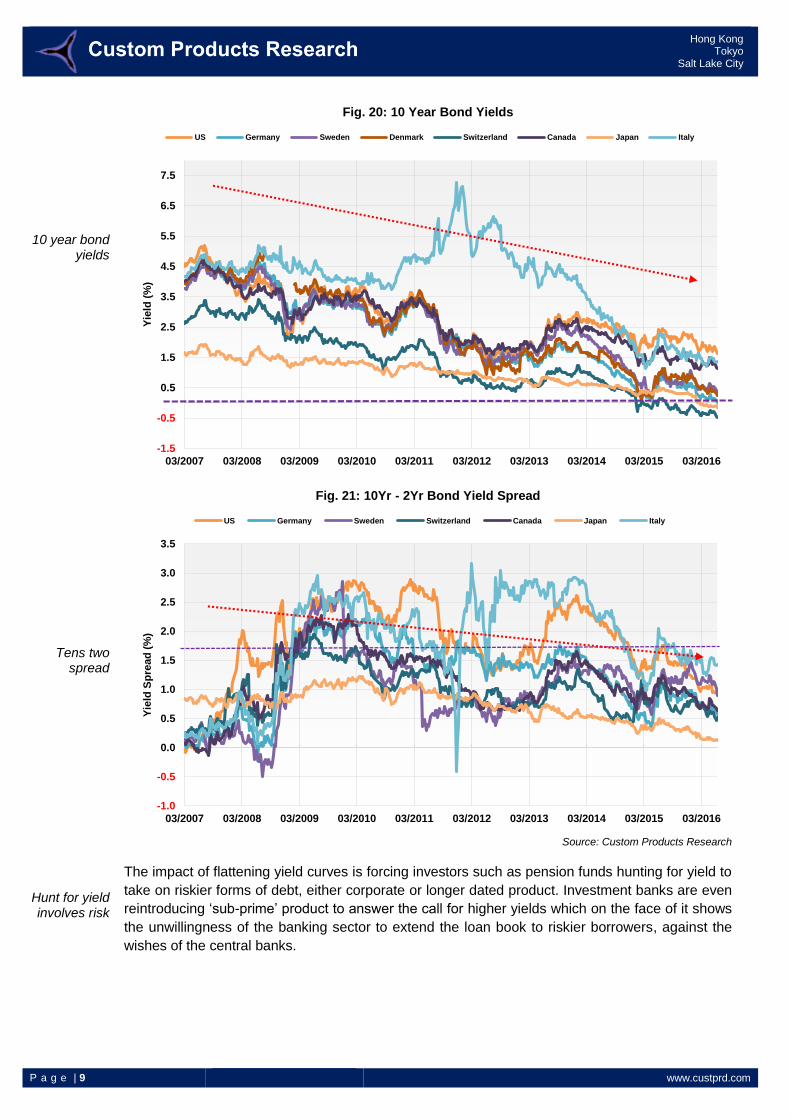

Inflation undershoots

2 year bond yields

The 15 largest Eurozone countries have not seen the same impact of NIRP on housing markets,

in part dragged down by the southern economies which are still reeling from their local economic

conditions. Fig. 18 shows the lack of inflation coming through the system even with those

countries with NIRP (in yellow). It is this continual undershoot which is causing yield curves to

flatten exacerbating duration risk if there is any reversal, Figs. 19-21.

Source: Central Bank data

-6.0

-4.8

-3.5 -3.2 -2.9-2.3 -2.2 -2.1 -1.9 -1.7 -1.6 -1.4 -1.2 -1.0 -0.9 -0.7 -0.7

-0.3

0.9

-7.0

-6.0

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

Fig. 18: Undershooting (Target vs. Actual Inflation)

-1.5

-0.5

0.5

1.5

2.5

3.5

4.5

5.5

6.5

7.5

06/2006 06/2007 06/2008 06/2009 06/2010 06/2011 06/2012 06/2013 06/2014 06/2015

Yie

ld (

%)

Fig. 19: 2 Year Bond Yields

US Germany Sweden Denmark Switzerland Canada Japan Italy

P a g e | 9 www.custprd.com

Hong Kong Tokyo

Salt Lake City

10 year bond yields

Tens two spread

Hunt for yield involves risk

Source: Custom Products Research

The impact of flattening yield curves is forcing investors such as pension funds hunting for yield to

take on riskier forms of debt, either corporate or longer dated product. Investment banks are even

reintroducing ‘sub-prime’ product to answer the call for higher yields which on the face of it shows

the unwillingness of the banking sector to extend the loan book to riskier borrowers, against the

wishes of the central banks.

-1.5

-0.5

0.5

1.5

2.5

3.5

4.5

5.5

6.5

7.5

03/2007 03/2008 03/2009 03/2010 03/2011 03/2012 03/2013 03/2014 03/2015 03/2016

Yie

ld (

%)

Fig. 20: 10 Year Bond Yields

US Germany Sweden Denmark Switzerland Canada Japan Italy

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

03/2007 03/2008 03/2009 03/2010 03/2011 03/2012 03/2013 03/2014 03/2015 03/2016

Yie

ld S

pre

ad

(%

)

Fig. 21: 10Yr - 2Yr Bond Yield Spread

US Germany Sweden Switzerland Canada Japan Italy

P a g e | 10 www.custprd.com

Hong Kong Tokyo

Salt Lake City

Banks not wanting to

take on more risk.

A recent Fed survey says

47% of Americans can’t raise $400 in an

emergency

5% UR but 40yr low

participation

Class 8 truck orders

plunging

Bloated inventories

That point is already being demonstrated by the actions of banks. Commerzbank in Germany is

considering parking its excess deposits in its own vaults than have it earn negative returns in the

vaults of the ECB. Munich Re is also of the same view. When the Japanese went to negative

rates, the country ran out of personal use safes such was the demand to avoid punitive rates.

However we must ask ourselves, has this mass monetary priming ended up helping the average

man and woman on the street?

The woe of the average Joe and Joanne…

A recent Federal Reserve survey in the US found only 53 percent of respondents indicate that

they could cover a hypothetical emergency expense costing $400 without selling something or

borrowing money. Thirty-one percent of respondents report going without some form of medical

care in the past year because they could not afford it. So that is 47% who cannot raise $400 in an

emergency. 30 million Americans are registered as having a disability. A recent ME Bank survey

in Australia found only 46 per cent of households were able to save each month. Just 32 per cent

could raise $3000 in an emergency and 50 per cent aren’t confident of meeting their obligations if

unemployed for three months.

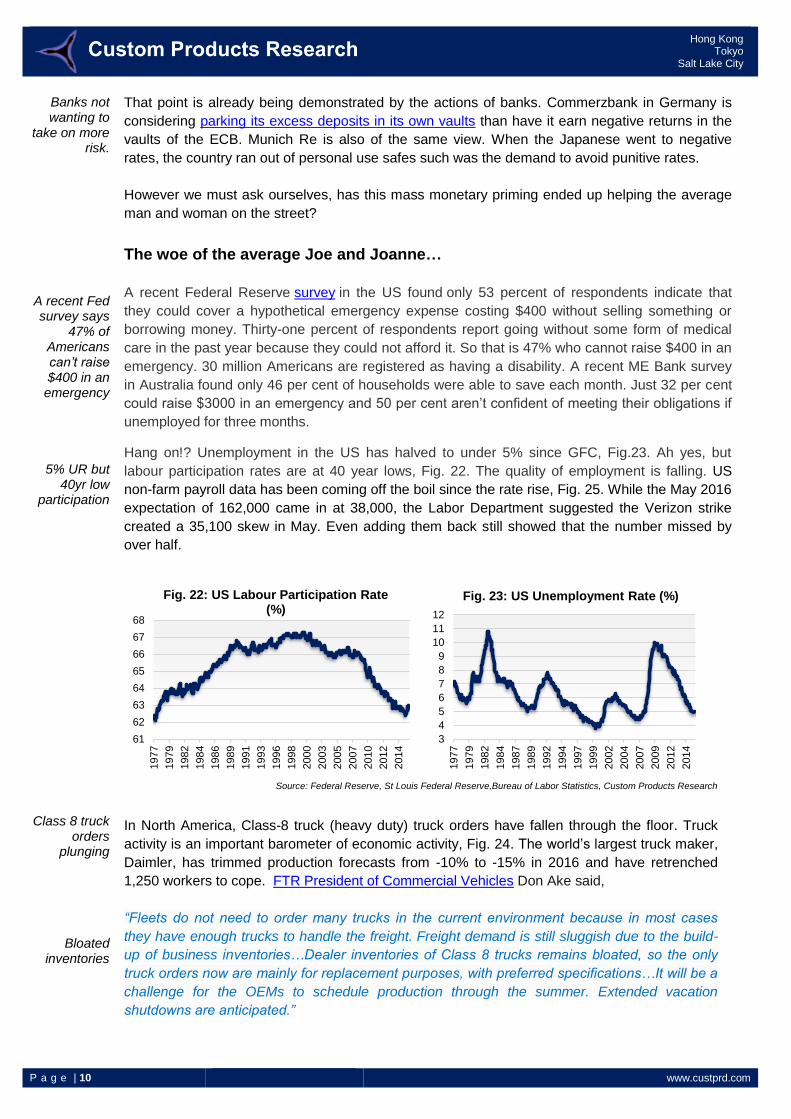

Hang on!? Unemployment in the US has halved to under 5% since GFC, Fig.23. Ah yes, but

labour participation rates are at 40 year lows, Fig. 22. The quality of employment is falling. US

non-farm payroll data has been coming off the boil since the rate rise, Fig. 25. While the May 2016

expectation of 162,000 came in at 38,000, the Labor Department suggested the Verizon strike

created a 35,100 skew in May. Even adding them back still showed that the number missed by

over half.

Source: Federal Reserve, St Louis Federal Reserve,Bureau of Labor Statistics, Custom Products Research

In North America, Class-8 truck (heavy duty) truck orders have fallen through the floor. Truck

activity is an important barometer of economic activity, Fig. 24. The world’s largest truck maker,

Daimler, has trimmed production forecasts from -10% to -15% in 2016 and have retrenched

1,250 workers to cope. FTR President of Commercial Vehicles Don Ake said,

“Fleets do not need to order many trucks in the current environment because in most cases

they have enough trucks to handle the freight. Freight demand is still sluggish due to the build-

up of business inventories…Dealer inventories of Class 8 trucks remains bloated, so the only

truck orders now are mainly for replacement purposes, with preferred specifications…It will be a

challenge for the OEMs to schedule production through the summer. Extended vacation

shutdowns are anticipated.”

61

62

63

64

65

66

67

68

1977

1979

1982

1984

1986

1989

1991

1993

1996

1998

2000

2003

2005

2007

2010

2012

2014

Fig. 22: US Labour Participation Rate (%)

3

4

5

6

7

8

9

10

11

12

1977

1979

1982

1984

1987

1989

1992

1994

1997

1999

2002

2004

2007

2009

2012

2014

Fig. 23: US Unemployment Rate (%)

P a g e | 11 www.custprd.com

Hong Kong Tokyo

Salt Lake City

25% of EU in poverty

LT jobless keeps

growing

Source: FTR Transport Intelligence, Bureau of Labour Statistics

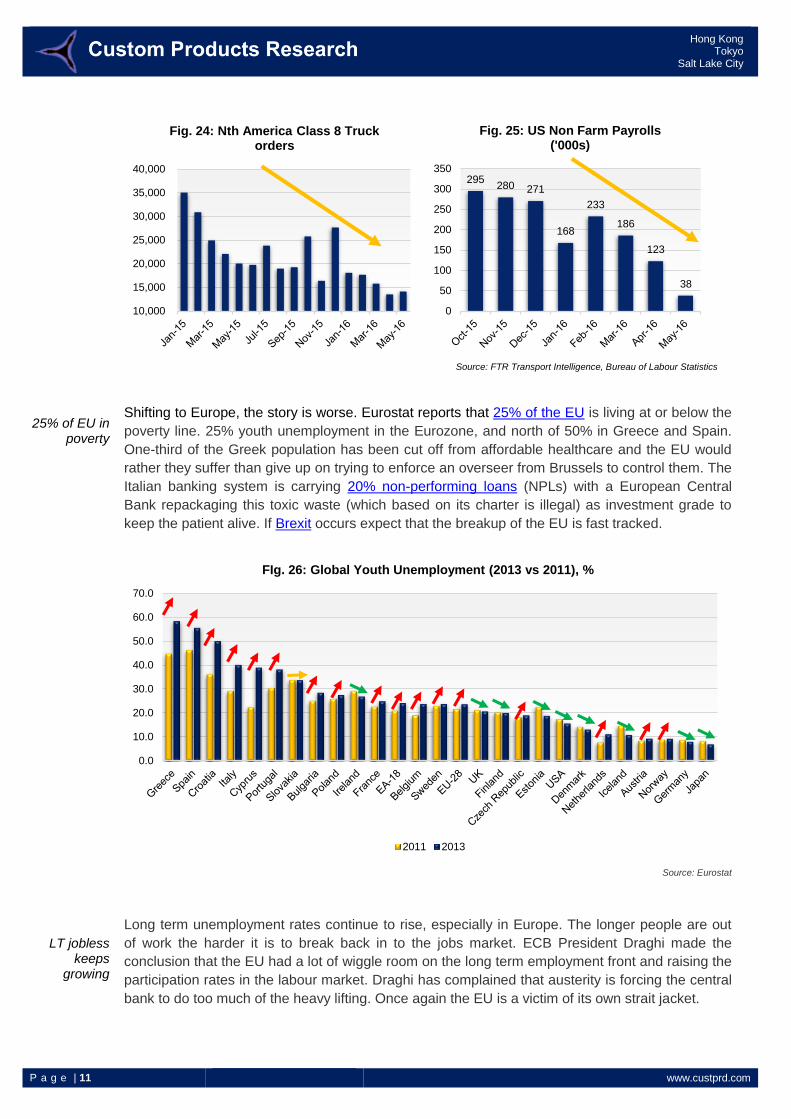

Shifting to Europe, the story is worse. Eurostat reports that 25% of the EU is living at or below the

poverty line. 25% youth unemployment in the Eurozone, and north of 50% in Greece and Spain.

One-third of the Greek population has been cut off from affordable healthcare and the EU would

rather they suffer than give up on trying to enforce an overseer from Brussels to control them. The

Italian banking system is carrying 20% non-performing loans (NPLs) with a European Central

Bank repackaging this toxic waste (which based on its charter is illegal) as investment grade to

keep the patient alive. If Brexit occurs expect that the breakup of the EU is fast tracked.

Source: Eurostat

Long term unemployment rates continue to rise, especially in Europe. The longer people are out

of work the harder it is to break back in to the jobs market. ECB President Draghi made the

conclusion that the EU had a lot of wiggle room on the long term employment front and raising the

participation rates in the labour market. Draghi has complained that austerity is forcing the central

bank to do too much of the heavy lifting. Once again the EU is a victim of its own strait jacket.

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Fig. 24: Nth America Class 8 Truck orders

295280 271

168

233

186

123

38

0

50

100

150

200

250

300

350

Fig. 25: US Non Farm Payrolls ('000s)

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

FIg. 26: Global Youth Unemployment (2013 vs 2011), %

2011 2013

P a g e | 12 www.custprd.com

Hong Kong Tokyo

Salt Lake City

SGP

Source: Eurostat

The Stability and Growth Pact (SGP) was set up to keep EU finances in check. Member States

had to try to keep budget deficits inside 3% of GDP and debt inside 60% of GDP. Gross debt

continues to climb in many countries, Fig. 28 and as such failing to comply with self-mandated

deadlines.

Source: Eurostat

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

Fig. 27: Long Term Unemployment as % of Total Unemployment

2006 2015

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

200.0

Fig. 28: EU Gross Debt: GDP (%)

2011 2014

P a g e | 13 www.custprd.com

Hong Kong Tokyo

Salt Lake City

Global jobless rates

rising

Japanese pensioners

breaking into prison

Source: Eurostat

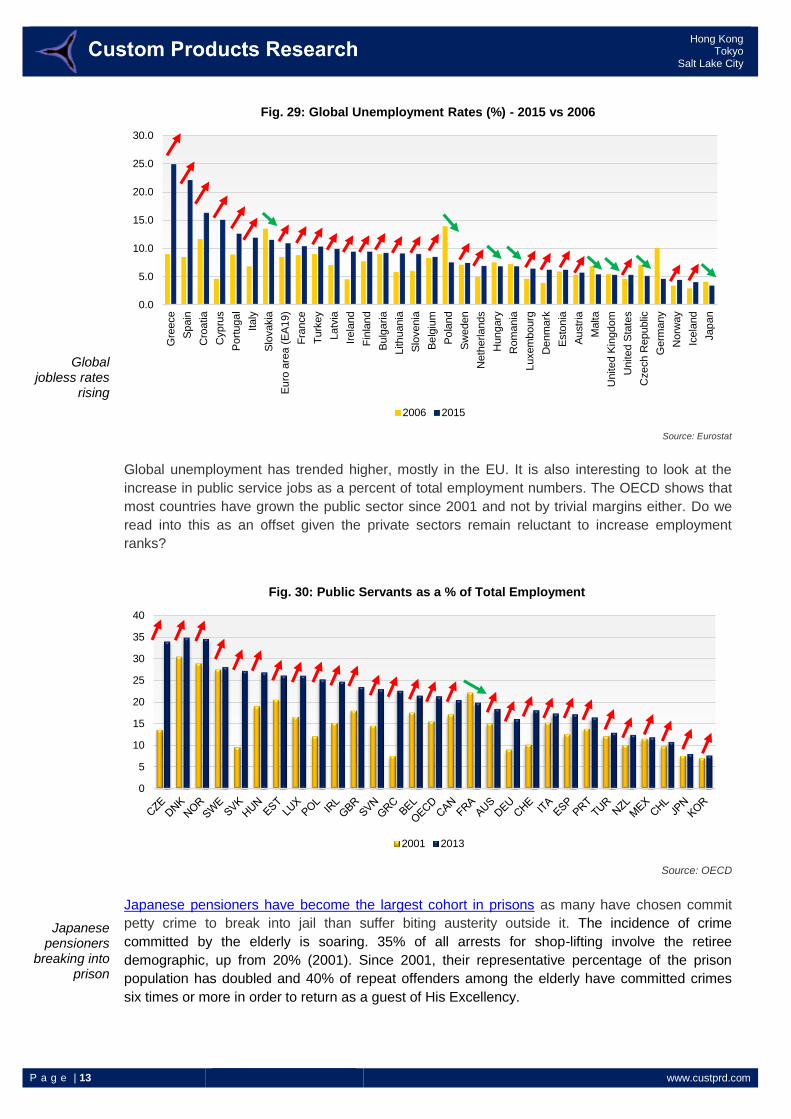

Global unemployment has trended higher, mostly in the EU. It is also interesting to look at the

increase in public service jobs as a percent of total employment numbers. The OECD shows that

most countries have grown the public sector since 2001 and not by trivial margins either. Do we

read into this as an offset given the private sectors remain reluctant to increase employment

ranks?

Source: OECD

Japanese pensioners have become the largest cohort in prisons as many have chosen commit

petty crime to break into jail than suffer biting austerity outside it. The incidence of crime

committed by the elderly is soaring. 35% of all arrests for shop-lifting involve the retiree

demographic, up from 20% (2001). Since 2001, their representative percentage of the prison

population has doubled and 40% of repeat offenders among the elderly have committed crimes

six times or more in order to return as a guest of His Excellency.

0.0

5.0

10.0

15.0

20.0

25.0

30.0

Gre

ece

Sp

ain

Cro

atia

Cyp

rus

Po

rtuga

l

Italy

Slo

vakia

Eu

ro a

rea (

EA

19)

Fra

nce

Tu

rkey

Latv

ia

Irela

nd

Fin

lan

d

Bu

lga

ria

Lith

uania

Slo

venia

Be

lgiu

m

Po

lan

d

Sw

eden

Neth

erla

nds

Hungary

Rom

ania

Luxem

bourg

Denm

ark

Esto

nia

Au

str

ia

Ma

lta

United K

ingdom

United S

tate

s

Cze

ch R

epublic

Germ

any

Norw

ay

Icela

nd

Jap

an

Fig. 29: Global Unemployment Rates (%) - 2015 vs 2006

2006 2015

0

5

10

15

20

25

30

35

40

Fig. 30: Public Servants as a % of Total Employment

2001 2013

P a g e | 14 www.custprd.com

Hong Kong Tokyo

Salt Lake City

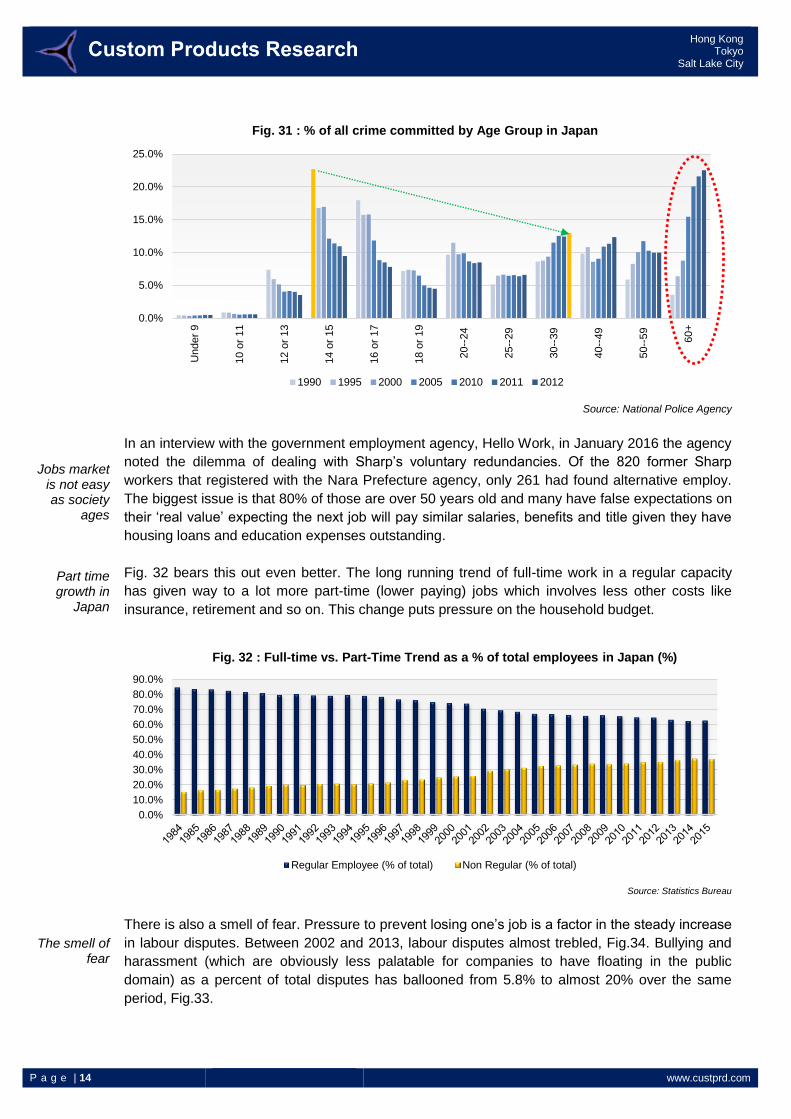

Jobs market is not easy as society

ages

Part time growth in

Japan

The smell of fear

Source: National Police Agency

In an interview with the government employment agency, Hello Work, in January 2016 the agency

noted the dilemma of dealing with Sharp’s voluntary redundancies. Of the 820 former Sharp

workers that registered with the Nara Prefecture agency, only 261 had found alternative employ.

The biggest issue is that 80% of those are over 50 years old and many have false expectations on

their ‘real value’ expecting the next job will pay similar salaries, benefits and title given they have

housing loans and education expenses outstanding.

Fig. 32 bears this out even better. The long running trend of full-time work in a regular capacity

has given way to a lot more part-time (lower paying) jobs which involves less other costs like

insurance, retirement and so on. This change puts pressure on the household budget.

Source: Statistics Bureau

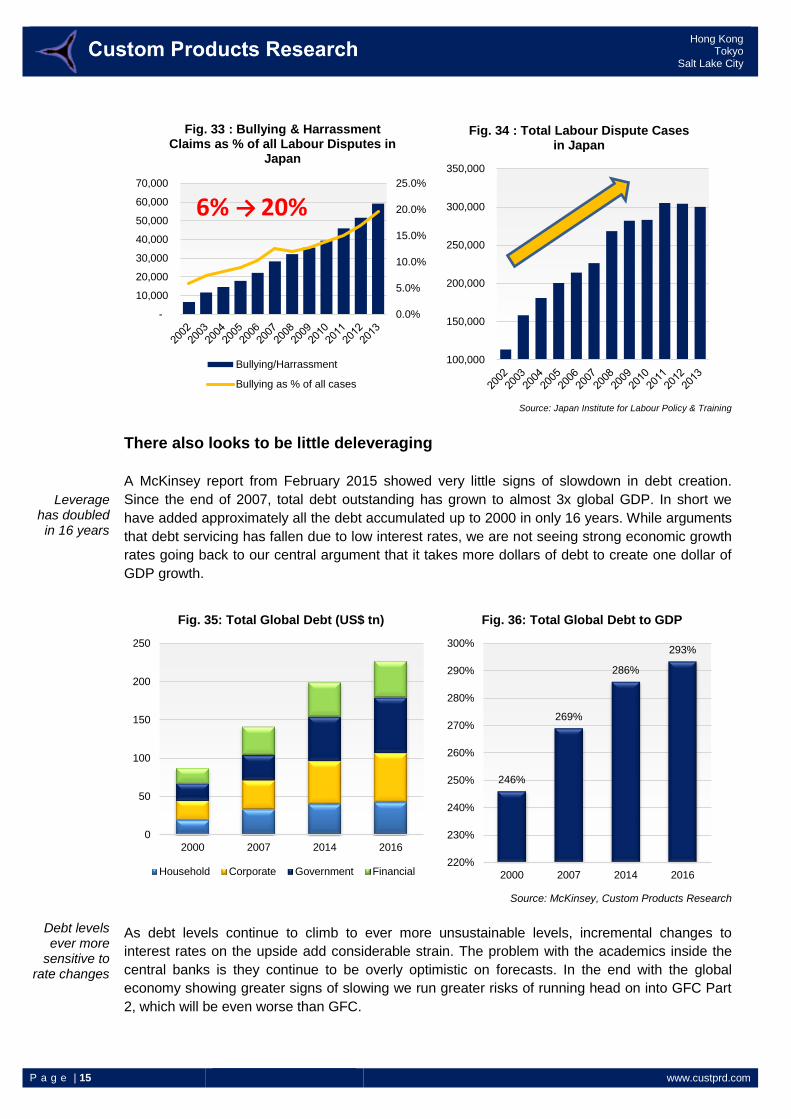

There is also a smell of fear. Pressure to prevent losing one’s job is a factor in the steady increase

in labour disputes. Between 2002 and 2013, labour disputes almost trebled, Fig.34. Bullying and

harassment (which are obviously less palatable for companies to have floating in the public

domain) as a percent of total disputes has ballooned from 5.8% to almost 20% over the same

period, Fig.33.

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Under

9

10 o

r 11

12 o

r 13

14 o

r 15

16 o

r 17

18 o

r 19

20--

24

25--

29

30--

39

40--

49

50--

59

60+

Fig. 31 : % of all crime committed by Age Group in Japan

1990 1995 2000 2005 2010 2011 2012

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

Fig. 32 : Full-time vs. Part-Time Trend as a % of total employees in Japan (%)

Regular Employee (% of total) Non Regular (% of total)

P a g e | 15 www.custprd.com

Hong Kong Tokyo

Salt Lake City

Leverage has doubled in 16 years

Debt levels ever more

sensitive to rate changes

Source: Japan Institute for Labour Policy & Training

There also looks to be little deleveraging

A McKinsey report from February 2015 showed very little signs of slowdown in debt creation.

Since the end of 2007, total debt outstanding has grown to almost 3x global GDP. In short we

have added approximately all the debt accumulated up to 2000 in only 16 years. While arguments

that debt servicing has fallen due to low interest rates, we are not seeing strong economic growth

rates going back to our central argument that it takes more dollars of debt to create one dollar of

GDP growth.

Source: McKinsey, Custom Products Research

As debt levels continue to climb to ever more unsustainable levels, incremental changes to

interest rates on the upside add considerable strain. The problem with the academics inside the

central banks is they continue to be overly optimistic on forecasts. In the end with the global

economy showing greater signs of slowing we run greater risks of running head on into GFC Part

2, which will be even worse than GFC.

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Fig. 33 : Bullying & Harrassment Claims as % of all Labour Disputes in

Japan

Bullying/Harrassment

Bullying as % of all cases

6% → 20%

100,000

150,000

200,000

250,000

300,000

350,000

Fig. 34 : Total Labour Dispute Cases in Japan

0

50

100

150

200

250

2000 2007 2014 2016

Fig. 35: Total Global Debt (US$ tn)

Household Corporate Government Financial

246%

269%

286%

293%

220%

230%

240%

250%

260%

270%

280%

290%

300%

2000 2007 2014 2016

Fig. 36: Total Global Debt to GDP

P a g e | 16 www.custprd.com

Hong Kong Tokyo

Salt Lake City

Overcapacity in China

China’s construction

machinery companies not getting

paid

It is a worry

China to be our saviour?

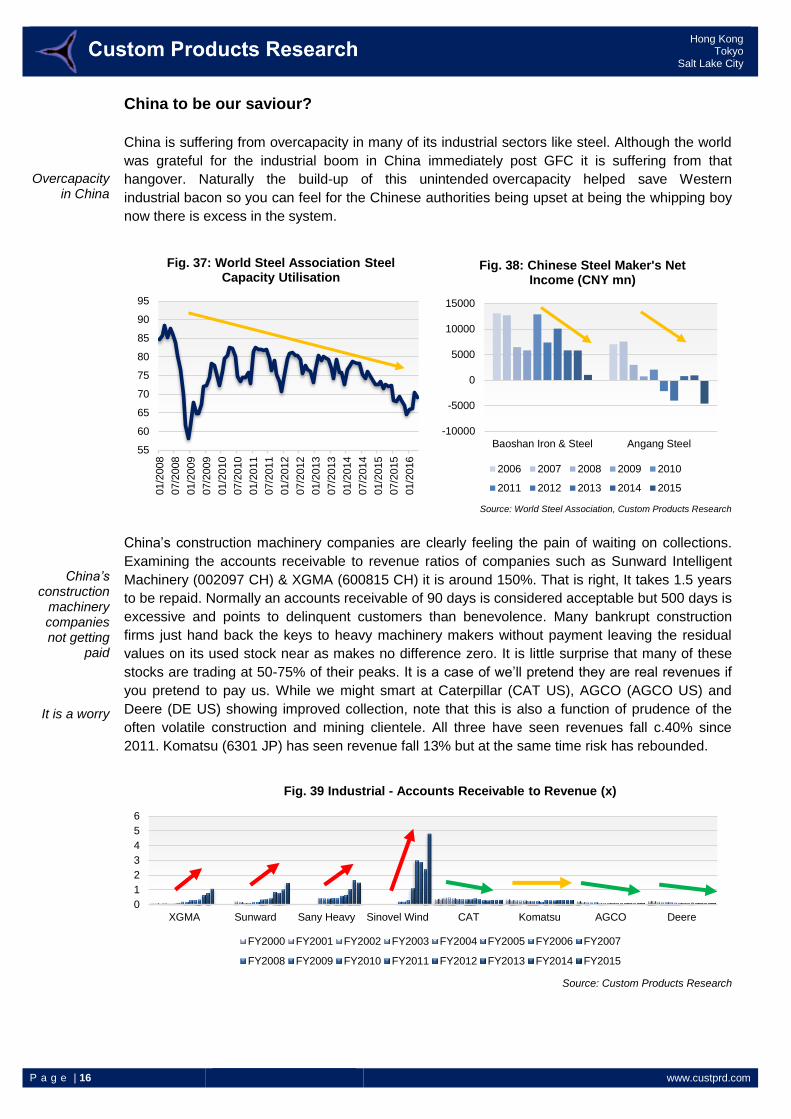

China is suffering from overcapacity in many of its industrial sectors like steel. Although the world

was grateful for the industrial boom in China immediately post GFC it is suffering from that

hangover. Naturally the build-up of this unintended overcapacity helped save Western

industrial bacon so you can feel for the Chinese authorities being upset at being the whipping boy

now there is excess in the system.

Source: World Steel Association, Custom Products Research

China’s construction machinery companies are clearly feeling the pain of waiting on collections.

Examining the accounts receivable to revenue ratios of companies such as Sunward Intelligent

Machinery (002097 CH) & XGMA (600815 CH) it is around 150%. That is right, It takes 1.5 years

to be repaid. Normally an accounts receivable of 90 days is considered acceptable but 500 days is

excessive and points to delinquent customers than benevolence. Many bankrupt construction

firms just hand back the keys to heavy machinery makers without payment leaving the residual

values on its used stock near as makes no difference zero. It is little surprise that many of these

stocks are trading at 50-75% of their peaks. It is a case of we’ll pretend they are real revenues if

you pretend to pay us. While we might smart at Caterpillar (CAT US), AGCO (AGCO US) and

Deere (DE US) showing improved collection, note that this is also a function of prudence of the

often volatile construction and mining clientele. All three have seen revenues fall c.40% since

2011. Komatsu (6301 JP) has seen revenue fall 13% but at the same time risk has rebounded.

Source: Custom Products Research

55

60

65

70

75

80

85

90

95

01/2

008

07/2

008

01/2

009

07/2

009

01/2

010

07/2

010

01/2

011

07/2

011

01/2

012

07/2

012

01/2

013

07/2

013

01/2

014

07/2

014

01/2

015

07/2

015

01/2

016

Fig. 37: World Steel Association Steel Capacity Utilisation

-10000

-5000

0

5000

10000

15000

Baoshan Iron & Steel Angang Steel

Fig. 38: Chinese Steel Maker's Net Income (CNY mn)

2006 2007 2008 2009 2010

2011 2012 2013 2014 2015

0

1

2

3

4

5

6

XGMA Sunward Sany Heavy Sinovel Wind CAT Komatsu AGCO Deere

Fig. 39 Industrial - Accounts Receivable to Revenue (x)

FY2000 FY2001 FY2002 FY2003 FY2004 FY2005 FY2006 FY2007

FY2008 FY2009 FY2010 FY2011 FY2012 FY2013 FY2014 FY2015

P a g e | 17 www.custprd.com

Hong Kong Tokyo

Salt Lake City

Frightening tale

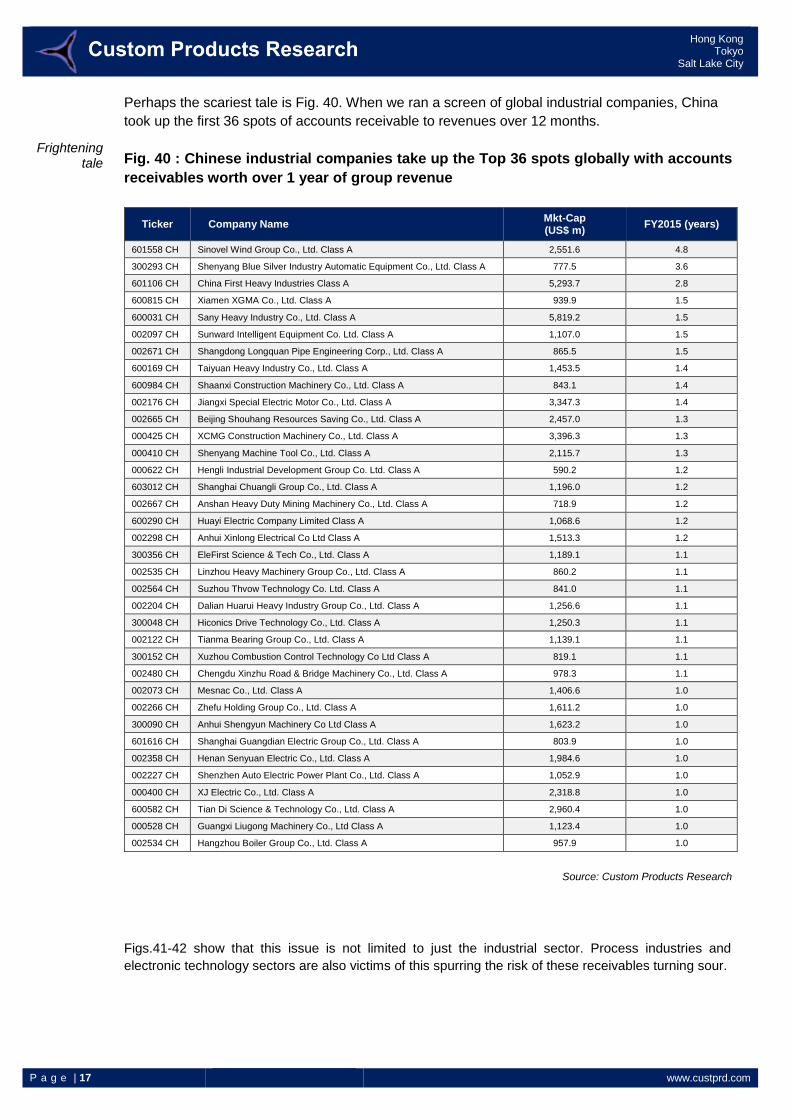

Perhaps the scariest tale is Fig. 40. When we ran a screen of global industrial companies, China

took up the first 36 spots of accounts receivable to revenues over 12 months.

Fig. 40 : Chinese industrial companies take up the Top 36 spots globally with accounts

receivables worth over 1 year of group revenue

Ticker Company Name Mkt-Cap (US$ m)

FY2015 (years)

601558 CH Sinovel Wind Group Co., Ltd. Class A 2,551.6 4.8

300293 CH Shenyang Blue Silver Industry Automatic Equipment Co., Ltd. Class A 777.5 3.6

601106 CH China First Heavy Industries Class A 5,293.7 2.8

600815 CH Xiamen XGMA Co., Ltd. Class A 939.9 1.5

600031 CH Sany Heavy Industry Co., Ltd. Class A 5,819.2 1.5

002097 CH Sunward Intelligent Equipment Co. Ltd. Class A 1,107.0 1.5

002671 CH Shangdong Longquan Pipe Engineering Corp., Ltd. Class A 865.5 1.5

600169 CH Taiyuan Heavy Industry Co., Ltd. Class A 1,453.5 1.4

600984 CH Shaanxi Construction Machinery Co., Ltd. Class A 843.1 1.4

002176 CH Jiangxi Special Electric Motor Co., Ltd. Class A 3,347.3 1.4

002665 CH Beijing Shouhang Resources Saving Co., Ltd. Class A 2,457.0 1.3

000425 CH XCMG Construction Machinery Co., Ltd. Class A 3,396.3 1.3

000410 CH Shenyang Machine Tool Co., Ltd. Class A 2,115.7 1.3

000622 CH Hengli Industrial Development Group Co. Ltd. Class A 590.2 1.2

603012 CH Shanghai Chuangli Group Co., Ltd. Class A 1,196.0 1.2

002667 CH Anshan Heavy Duty Mining Machinery Co., Ltd. Class A 718.9 1.2

600290 CH Huayi Electric Company Limited Class A 1,068.6 1.2

002298 CH Anhui Xinlong Electrical Co Ltd Class A 1,513.3 1.2

300356 CH EleFirst Science & Tech Co., Ltd. Class A 1,189.1 1.1

002535 CH Linzhou Heavy Machinery Group Co., Ltd. Class A 860.2 1.1

002564 CH Suzhou Thvow Technology Co. Ltd. Class A 841.0 1.1

002204 CH Dalian Huarui Heavy Industry Group Co., Ltd. Class A 1,256.6 1.1

300048 CH Hiconics Drive Technology Co., Ltd. Class A 1,250.3 1.1

002122 CH Tianma Bearing Group Co., Ltd. Class A 1,139.1 1.1

300152 CH Xuzhou Combustion Control Technology Co Ltd Class A 819.1 1.1

002480 CH Chengdu Xinzhu Road & Bridge Machinery Co., Ltd. Class A 978.3 1.1

002073 CH Mesnac Co., Ltd. Class A 1,406.6 1.0

002266 CH Zhefu Holding Group Co., Ltd. Class A 1,611.2 1.0

300090 CH Anhui Shengyun Machinery Co Ltd Class A 1,623.2 1.0

601616 CH Shanghai Guangdian Electric Group Co., Ltd. Class A 803.9 1.0

002358 CH Henan Senyuan Electric Co., Ltd. Class A 1,984.6 1.0

002227 CH Shenzhen Auto Electric Power Plant Co., Ltd. Class A 1,052.9 1.0

000400 CH XJ Electric Co., Ltd. Class A 2,318.8 1.0

600582 CH Tian Di Science & Technology Co., Ltd. Class A 2,960.4 1.0

000528 CH Guangxi Liugong Machinery Co., Ltd Class A 1,123.4 1.0

002534 CH Hangzhou Boiler Group Co., Ltd. Class A 957.9 1.0

Source: Custom Products Research

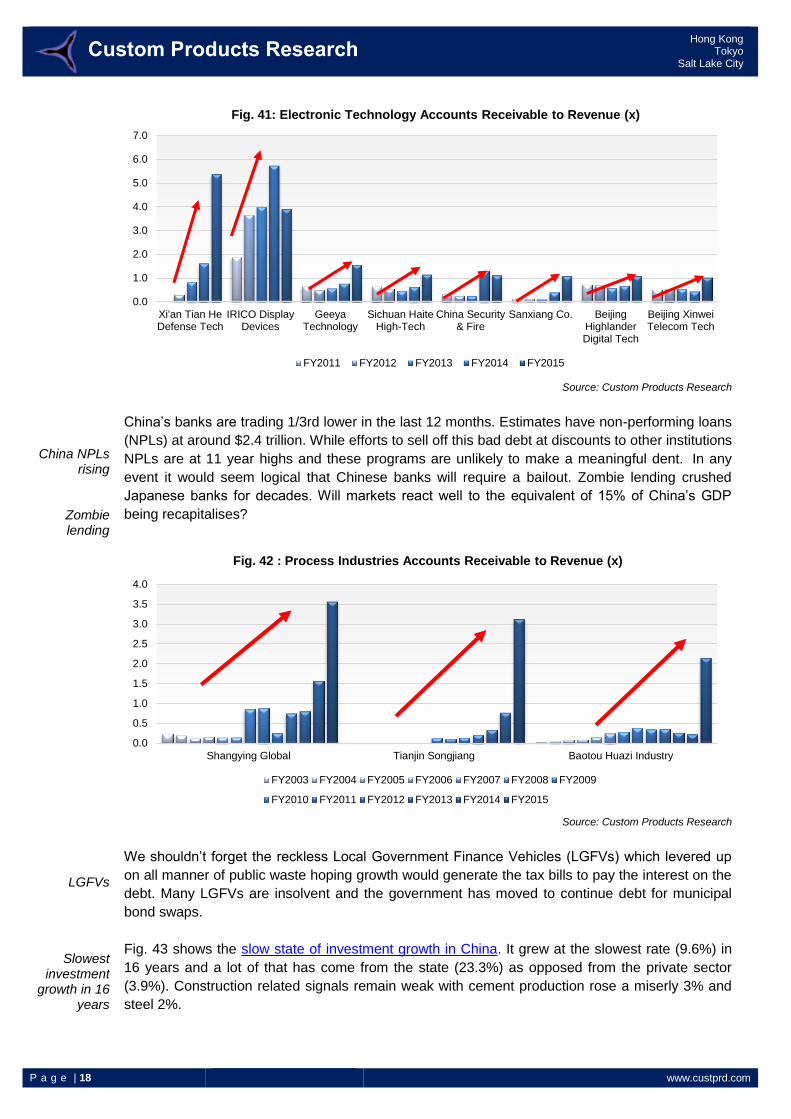

Figs.41-42 show that this issue is not limited to just the industrial sector. Process industries and

electronic technology sectors are also victims of this spurring the risk of these receivables turning sour.

P a g e | 18 www.custprd.com

Hong Kong Tokyo

Salt Lake City

China NPLs rising

Zombie lending

LGFVs

Slowest investment

growth in 16 years

Source: Custom Products Research

China’s banks are trading 1/3rd lower in the last 12 months. Estimates have non-performing loans

(NPLs) at around $2.4 trillion. While efforts to sell off this bad debt at discounts to other institutions

NPLs are at 11 year highs and these programs are unlikely to make a meaningful dent. In any

event it would seem logical that Chinese banks will require a bailout. Zombie lending crushed

Japanese banks for decades. Will markets react well to the equivalent of 15% of China’s GDP

being recapitalises?

Source: Custom Products Research

We shouldn’t forget the reckless Local Government Finance Vehicles (LGFVs) which levered up

on all manner of public waste hoping growth would generate the tax bills to pay the interest on the

debt. Many LGFVs are insolvent and the government has moved to continue debt for municipal

bond swaps.

Fig. 43 shows the slow state of investment growth in China. It grew at the slowest rate (9.6%) in

16 years and a lot of that has come from the state (23.3%) as opposed from the private sector

(3.9%). Construction related signals remain weak with cement production rose a miserly 3% and

steel 2%.

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Xi'an Tian HeDefense Tech

IRICO DisplayDevices

GeeyaTechnology

Sichuan HaiteHigh-Tech

China Security& Fire

Sanxiang Co. BeijingHighlanderDigital Tech

Beijing XinweiTelecom Tech

Fig. 41: Electronic Technology Accounts Receivable to Revenue (x)

FY2011 FY2012 FY2013 FY2014 FY2015

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Shangying Global Tianjin Songjiang Baotou Huazi Industry

Fig. 42 : Process Industries Accounts Receivable to Revenue (x)

FY2003 FY2004 FY2005 FY2006 FY2007 FY2008 FY2009

FY2010 FY2011 FY2012 FY2013 FY2014 FY2015

P a g e | 19 www.custprd.com

Hong Kong Tokyo

Salt Lake City

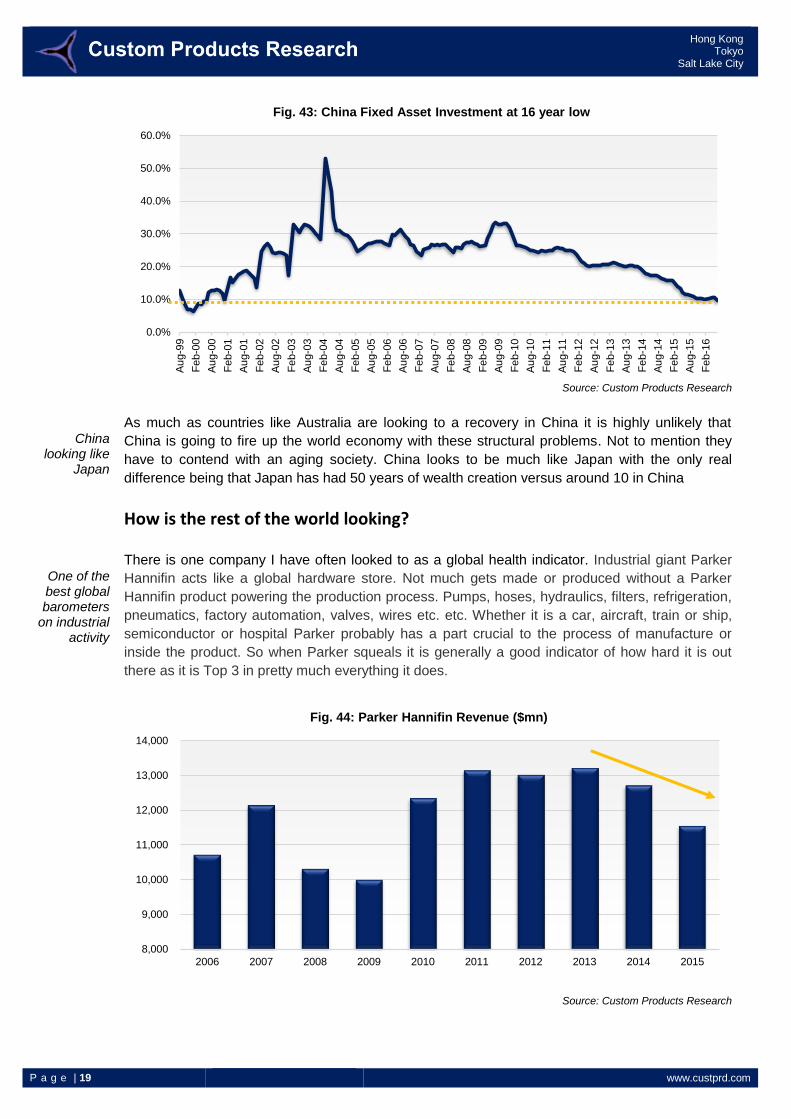

China looking like

Japan

One of the best global barometers

on industrial activity

Source: Custom Products Research

As much as countries like Australia are looking to a recovery in China it is highly unlikely that

China is going to fire up the world economy with these structural problems. Not to mention they

have to contend with an aging society. China looks to be much like Japan with the only real

difference being that Japan has had 50 years of wealth creation versus around 10 in China

How is the rest of the world looking?

There is one company I have often looked to as a global health indicator. Industrial giant Parker

Hannifin acts like a global hardware store. Not much gets made or produced without a Parker

Hannifin product powering the production process. Pumps, hoses, hydraulics, filters, refrigeration,

pneumatics, factory automation, valves, wires etc. etc. Whether it is a car, aircraft, train or ship,

semiconductor or hospital Parker probably has a part crucial to the process of manufacture or

inside the product. So when Parker squeals it is generally a good indicator of how hard it is out

there as it is Top 3 in pretty much everything it does.

Source: Custom Products Research

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

Au

g-9

9

Fe

b-0

0

Au

g-0

0

Fe

b-0

1

Au

g-0

1

Fe

b-0

2

Au

g-0

2

Fe

b-0

3

Au

g-0

3

Fe

b-0

4

Au

g-0

4

Fe

b-0

5

Au

g-0

5

Fe

b-0

6

Au

g-0

6

Fe

b-0

7

Au

g-0

7

Fe

b-0

8

Au

g-0

8

Fe

b-0

9

Au

g-0

9

Fe

b-1

0

Au

g-1

0

Fe

b-1

1

Au

g-1

1

Fe

b-1

2

Au

g-1

2

Fe

b-1

3

Au

g-1

3

Fe

b-1

4

Au

g-1

4

Fe

b-1

5

Au

g-1

5

Fe

b-1

6

Fig. 43: China Fixed Asset Investment at 16 year low

8,000

9,000

10,000

11,000

12,000

13,000

14,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Fig. 44: Parker Hannifin Revenue ($mn)

P a g e | 20 www.custprd.com

Hong Kong Tokyo

Salt Lake City

Sales down at home and

abroad falling

Orders at home and

abroad falling

Capacity utilisation

across the world

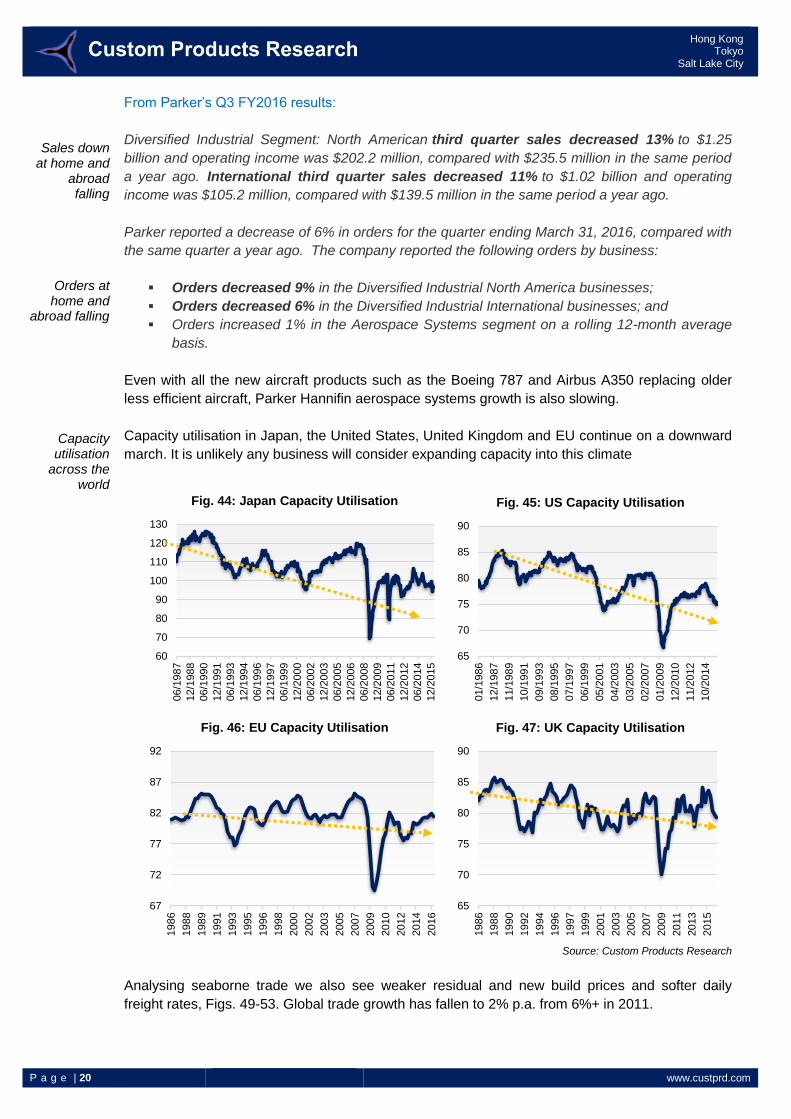

From Parker’s Q3 FY2016 results:

Diversified Industrial Segment: North American third quarter sales decreased 13% to $1.25

billion and operating income was $202.2 million, compared with $235.5 million in the same period

a year ago. International third quarter sales decreased 11% to $1.02 billion and operating

income was $105.2 million, compared with $139.5 million in the same period a year ago.

Parker reported a decrease of 6% in orders for the quarter ending March 31, 2016, compared with

the same quarter a year ago. The company reported the following orders by business:

Orders decreased 9% in the Diversified Industrial North America businesses;

Orders decreased 6% in the Diversified Industrial International businesses; and

Orders increased 1% in the Aerospace Systems segment on a rolling 12-month average

basis.

Even with all the new aircraft products such as the Boeing 787 and Airbus A350 replacing older

less efficient aircraft, Parker Hannifin aerospace systems growth is also slowing.

Capacity utilisation in Japan, the United States, United Kingdom and EU continue on a downward

march. It is unlikely any business will consider expanding capacity into this climate

Source: Custom Products Research

Analysing seaborne trade we also see weaker residual and new build prices and softer daily

freight rates, Figs. 49-53. Global trade growth has fallen to 2% p.a. from 6%+ in 2011.

60

70

80

90

100

110

120

130

06/1

987

12/1

988

06/1

990

12/1

991

06/1

993

12/1

994

06/1

996

12/1

997

06/1

999

12/2

000

06/2

002

12/2

003

06/2

005

12/2

006

06/2

008

12/2

009

06/2

011

12/2

012

06/2

014

12/2

015

Fig. 44: Japan Capacity Utilisation

65

70

75

80

85

90

01/1

986

12/1

987

11/1

989

10/1

991

09/1

993

08/1

995

07/1

997

06/1

999

05/2

001

04/2

003

03/2

005

02/2

007

01/2

009

12/2

010

11/2

012

10/2

014

Fig. 45: US Capacity Utilisation

67

72

77

82

87

92

1986

1988

1989

1991

1993

1995

1996

1998

2000

2002

2003

2005

2007

2009

2010

2012

2014

2016

Fig. 46: EU Capacity Utilisation

65

70

75

80

85

90

1986

1988

1990

1992

1994

1996

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

Fig. 47: UK Capacity Utilisation

P a g e | 21 www.custprd.com

Hong Kong Tokyo

Salt Lake City

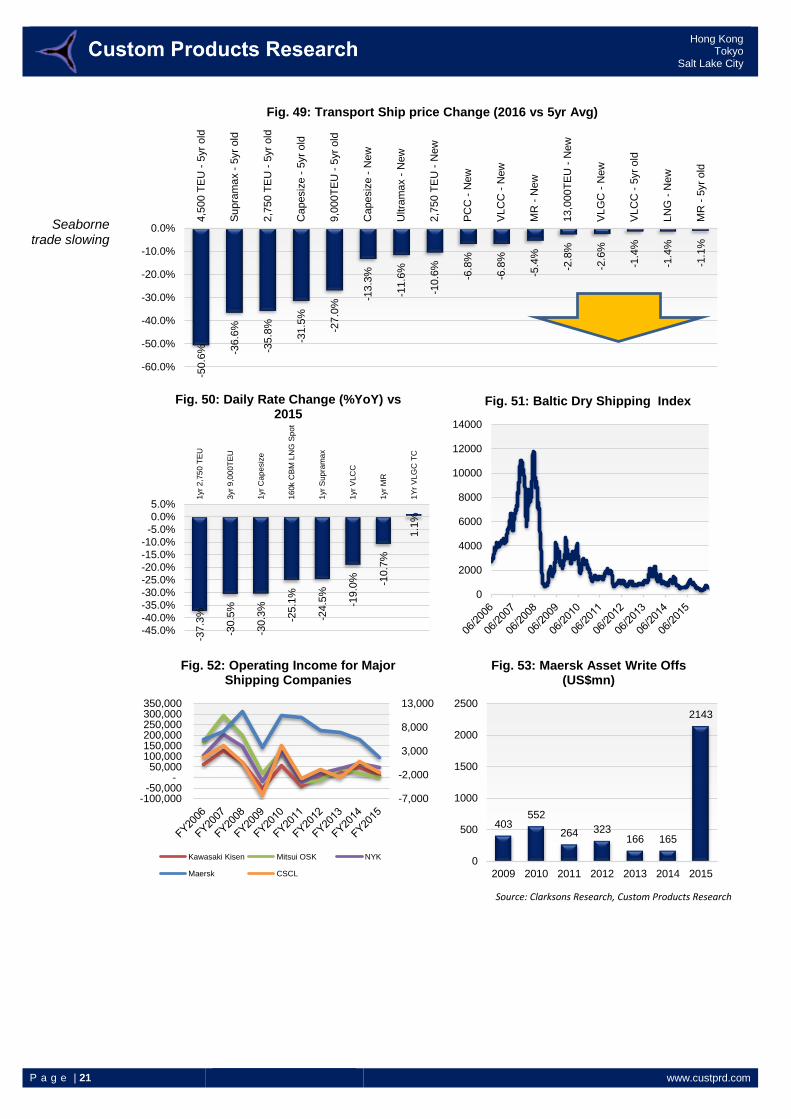

Seaborne trade slowing

Source: Clarksons Research, Custom Products Research

-50.6

% -36.6

%

-35.8

%

-31.5

%

-27.0

%

-13.3

%

-11.6

%

-10.6

%

-6.8

%

-6.8

%

-5.4

%

-2.8

%

-2.6

%

-1.4

%

-1.4

%

-1.1

%

-60.0%

-50.0%

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

4,5

00 T

EU

- 5

yr

old

Su

pra

ma

x -

5yr

old

2,7

50 T

EU

- 5

yr

old

Capesiz

e -

5yr

old

9,0

00T

EU

- 5

yr

old

Capesiz

e -

New

Ultra

max -

New

2,7

50 T

EU

- N

ew

PC

C -

New

VL

CC

- N

ew

MR

- N

ew

13,0

00T

EU

- N

ew

VL

GC

- N

ew

VL

CC

- 5

yr

old

LN

G -

New

MR

- 5

yr

old

Fig. 49: Transport Ship price Change (2016 vs 5yr Avg)

-37.3

%

-30.5

%

-30.3

%

-25.1

%

-24.5

%

-19.0

% -10.7

%

1.1

%

-45.0%

-40.0%

-35.0%

-30.0%

-25.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

1yr

2,7

50 T

EU

3yr

9,0

00T

EU

1yr

Ca

pe

siz

e

16

0k C

BM

LN

G S

po

t

1yr

Sup

ram

ax

1yr

VLC

C

1yr

MR

1Y

r V

LG

C T

C

Fig. 50: Daily Rate Change (%YoY) vs 2015

0

2000

4000

6000

8000

10000

12000

14000

Fig. 51: Baltic Dry Shipping Index

-7,000

-2,000

3,000

8,000

13,000

-100,000-50,000

- 50,000

100,000 150,000 200,000 250,000 300,000 350,000

Fig. 52: Operating Income for Major Shipping Companies

Kawasaki Kisen Mitsui OSK NYK

Maersk CSCL

403552

264 323166 165

2143

0

500

1000

1500

2000

2500

2009 2010 2011 2012 2013 2014 2015

Fig. 53: Maersk Asset Write Offs (US$mn)

P a g e | 22 www.custprd.com

Hong Kong Tokyo

Salt Lake City

Gluskin Sheff makes good

point on central banks

Write downs will

accelerate

Already seeing banks

become insolvent?

Central banks should

not be independent

anymore

Gluskin Sheff economist David Rosenberg said, “Despite the best efforts from the world’s central

banks to ignite a self-sustaining expansion, it is our contention that in this post-bubble, mean-

reverting process, the ability for policymakers to recreate a credit cycle and trigger a wealth effect

on spending is being thwarted by secular changes in attitudes towards credit, savings, and

discretionary spending.”

We should prepare ourselves for a global slowdown to put more pressure on doubtful debts,

further write downs in asset values which will impair balance sheets affecting confidence

concatenering into higher unemployment and even slower growth. Unfortunately the rescue plan

will require the private sector to feel condifent they can see an end to the carnage. That can only

come about by massive cuts in taxation that incentivise business, not large government spending

programs paid for with more printed money.

ZeroHedge wrote recently that Belgian Optima Bank has been shut down by the National Bank of

Belgium (NBB) and the ECB on the basis it couldn’t make its commitments. ZeroHedge noted that

the NBB didn’t bother to publish a release in English despite doing so for all other releases. They

argue that a special commissioner had already been in place before the banking license was

revoked opening up questions about other banks in similar predicaments being hid from the

public. If a run in Eurozone banks was to ensue it would be pandamonium in markets.

Central Bank independence is no longer a wise policy choice

1. While financial pundits often bang on about the independence of central banks around the world

evidence suggests that they need a watchdog, much in the manner Nobel Prize winner Milton

Friedman supported. As a monetarist, Friedman promoted the idea that sensible monetary

expansion was the best policy for stable economic growth with a free market mentality to fairly

allocate capital. He wasn’t joking when he said, “Nobody spends somebody else’s money as

carefully as he spends his own. Nobody uses somebody else’s resources as carefully as he uses

his own. So if you want efficiency and effectiveness, if you want knowledge to be properly utilized,

you have to do it through the means of private property.”

2.

0.00.10.10.20.20.30.30.40.40.5

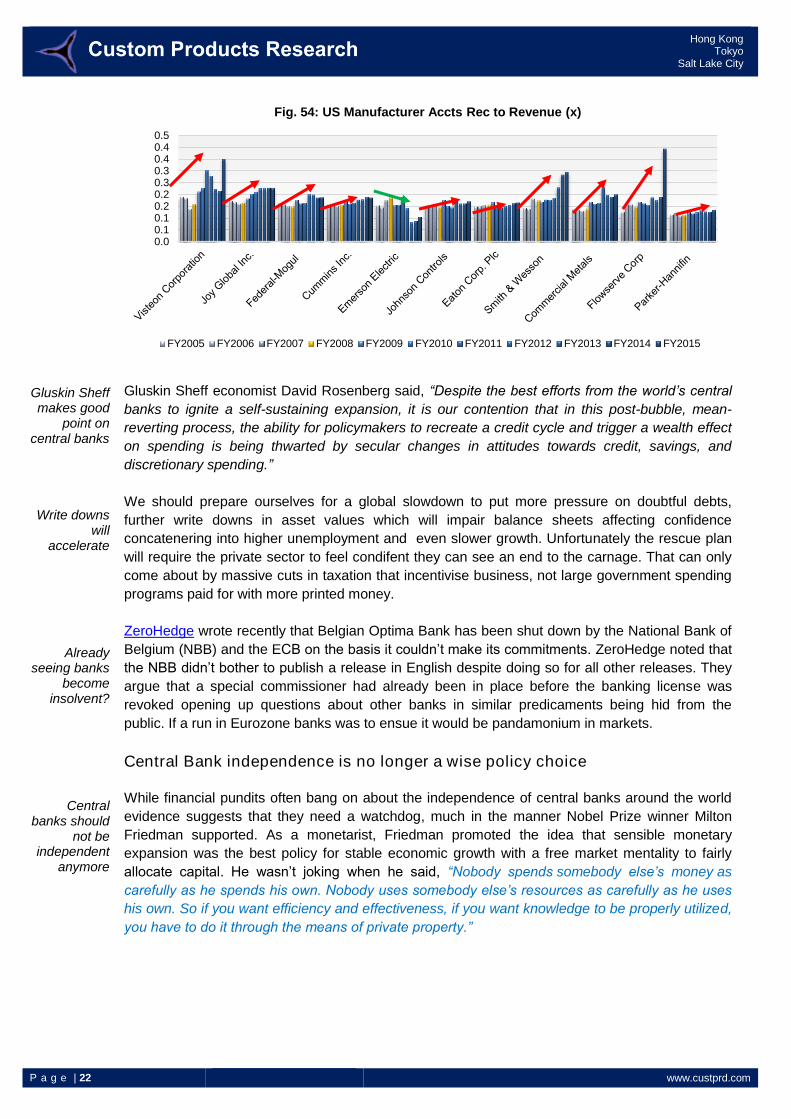

Fig. 54: US Manufacturer Accts Rec to Revenue (x)

FY2005 FY2006 FY2007 FY2008 FY2009 FY2010 FY2011 FY2012 FY2013 FY2014 FY2015

P a g e | 23 www.custprd.com

Hong Kong Tokyo

Salt Lake City

The idea of central banks firing central

blanks

Flawed

Japan’s still has a Y40-50tn gap to

fill yearly

Can’t print our way to prosperity

The Nikkei raised the idea of turning the ten quadrillion yen ($10.5 trillion) of sovereign debt into

zero interest rate perpetuals. So what value would Japanese debt have in the future? Remember

that Japanese officials need to raise ¥40-50 trillion every year to fund the budget deficit. If the BoJ

can print this deficit every year then once again the value of the currency would be trashed.

Financial markets cannot overlook that two years worth of GDP being turned into zero even under

the cloak of packaging it as still existing.

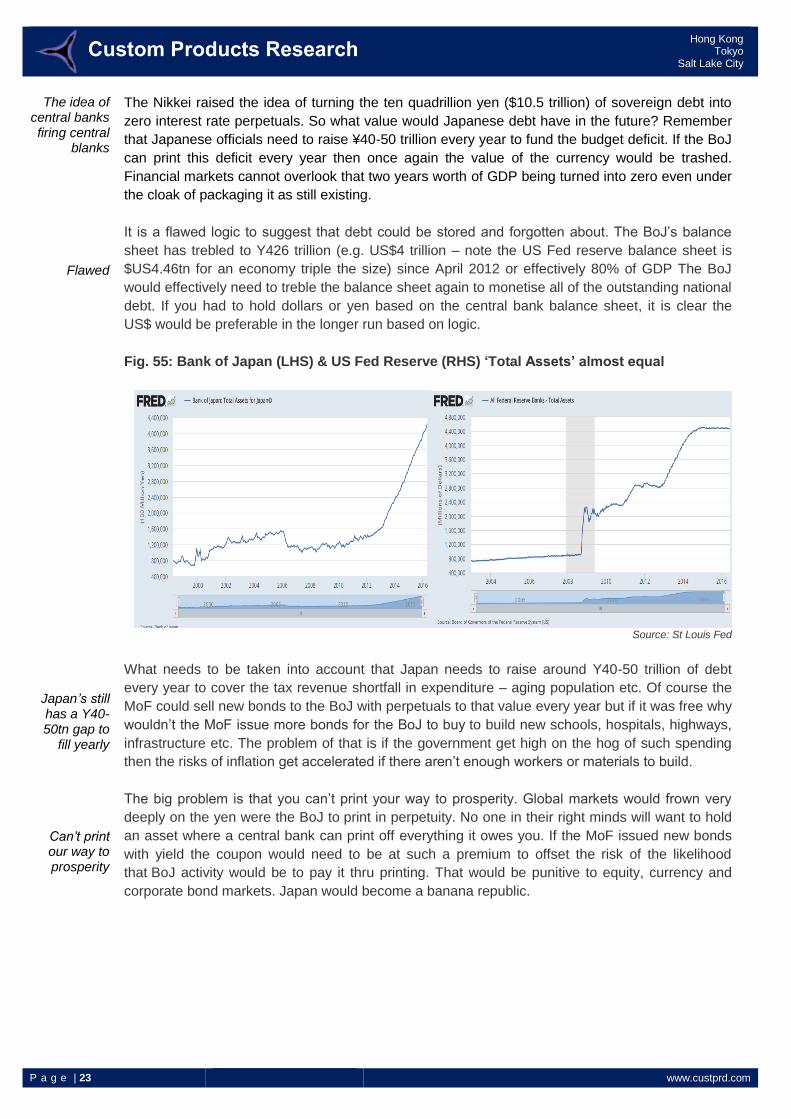

It is a flawed logic to suggest that debt could be stored and forgotten about. The BoJ’s balance

sheet has trebled to Y426 trillion (e.g. US$4 trillion – note the US Fed reserve balance sheet is

$US4.46tn for an economy triple the size) since April 2012 or effectively 80% of GDP The BoJ

would effectively need to treble the balance sheet again to monetise all of the outstanding national

debt. If you had to hold dollars or yen based on the central bank balance sheet, it is clear the

US$ would be preferable in the longer run based on logic.

Fig. 55: Bank of Japan (LHS) & US Fed Reserve (RHS) ‘Total Assets’ almost equal

Source: St Louis Fed

What needs to be taken into account that Japan needs to raise around Y40-50 trillion of debt

every year to cover the tax revenue shortfall in expenditure – aging population etc. Of course the

MoF could sell new bonds to the BoJ with perpetuals to that value every year but if it was free why

wouldn’t the MoF issue more bonds for the BoJ to buy to build new schools, hospitals, highways,

infrastructure etc. The problem of that is if the government get high on the hog of such spending

then the risks of inflation get accelerated if there aren’t enough workers or materials to build.

The big problem is that you can’t print your way to prosperity. Global markets would frown very

deeply on the yen were the BoJ to print in perpetuity. No one in their right minds will want to hold

an asset where a central bank can print off everything it owes you. If the MoF issued new bonds

with yield the coupon would need to be at such a premium to offset the risk of the likelihood

that BoJ activity would be to pay it thru printing. That would be punitive to equity, currency and

corporate bond markets. Japan would become a banana republic.

P a g e | 24 www.custprd.com

Hong Kong Tokyo

Salt Lake City

Aggressive tax reform

required

Markets must be freed up

from state manipulation

Beef up on clamping down on

fraud

Market integrity

depends on it

The lessons of failures the

last time

Whistle blowing

What is required to save the supertanker from sinking?

Aggressive tax reform. Wholesale flat taxes at 10%. Pumping more dollar after dollar has not

resulted in any meaningful economic recovery. We continue to struggle through orchestrated and

misguided fiscal and monetary policy. The private sector must be let loose from the shackles of

over-regulation and if governments want to get their citizens out from under the debt load, taxing

then any more will not work.

Markets must be freed from over-regulation. Although proper policing through regulators would

come from hiring former traders and market participants who can spot inconsistencies (aka fraud)

rather than relying on lawyers who couldn’t find a market anomaly if they fell over it. Regulators

should be self funded from fees charged to market participants enabling them to properly plan

years in advance not having to worry about a cut from Treasury.

Industry associations are behind paying higher user fees. Rick A. Fleming of the SEC’s Investor

Advocate said in August 2014,

“To some, the idea of a “user fee” sounds a lot like a tax. But several industry associations that

represent investment advisers have actually endorsed the concept of user fees. They recognize

that a rogue adviser not only harms investors, but also leaves a stain on the advisory industry, so

they support an increased regulatory presence and are willing to pay for it. Let me repeat that –

they are willing to pay more money to the SEC so that it can conduct more examinations of

advisers.”

Regulators have a vital role to play in preventing fraud. Market integrity depends on it. However

without adequate funding regulators face pressures on many fronts. The SEC was publicly

admonished by Congress for its failure to catch Bernard L. Madoff Investment Securities (BMIS)

LLC despite being presented with evidence multiple times from a whistle-blower pointing to the

Ponzi scheme for over 9 years. It issued the following statement:

“The Office of the Inspector General (OIG) investigation did find, however, that the SEC received

more than ample information in the form of detailed and substantive complaints over the years to

warrant a thorough and comprehensive examination and/or investigation of Bernard Madoff and

BMIS for operating a Ponzi scheme, and that despite three examinations and two investigations

being conducted, a thorough and competent investigation or examination was never performed.”

Whistleblowing should be encouraged like the American system which grants people who

legitimately uncover fraud a 10-30% cut of recovered monies. The US has seen a 10 fold increase

in whistleblowing cases since the law was revised in 2011 with one person awarded $30 million.

P a g e | 25 www.custprd.com

Hong Kong Tokyo

Salt Lake City

The BoJ to create SoEs?

Beware new financial lexicon

Sell side still getting it

wrong

Source: FSA & SEC

So what to do? Time to buy beaten up asset classes

If the BoJ continues to gobble up ETFs at a rate of 58% of the market then at some stage in the

future we might as well consider Japanese corporates to be little more than state owned

enterprises as many a corporate would seem to reflect without.

What always shows up as a red flag is financial jargon. In the lead up to the first GFC, words such

as NINJA (no income, no job, no assets) loans became part of daily lexicon. Now we have TINA

(there is no alternative) in equity markets where investors have little choice but to pay unrealistic

prices because there is no alternative.

The sell-side broking community keeps chasing unrealistic assumptions for their bullishness. We

showed that the distortion created by ETFs meant that sell-side analysts share price target

upgrades were mostly based on multiple expansion not based on earnings and dividends but

hope. Only seven sectors out of 33 in our screen showed a decline in the ratio of buy to sell

recommendations.

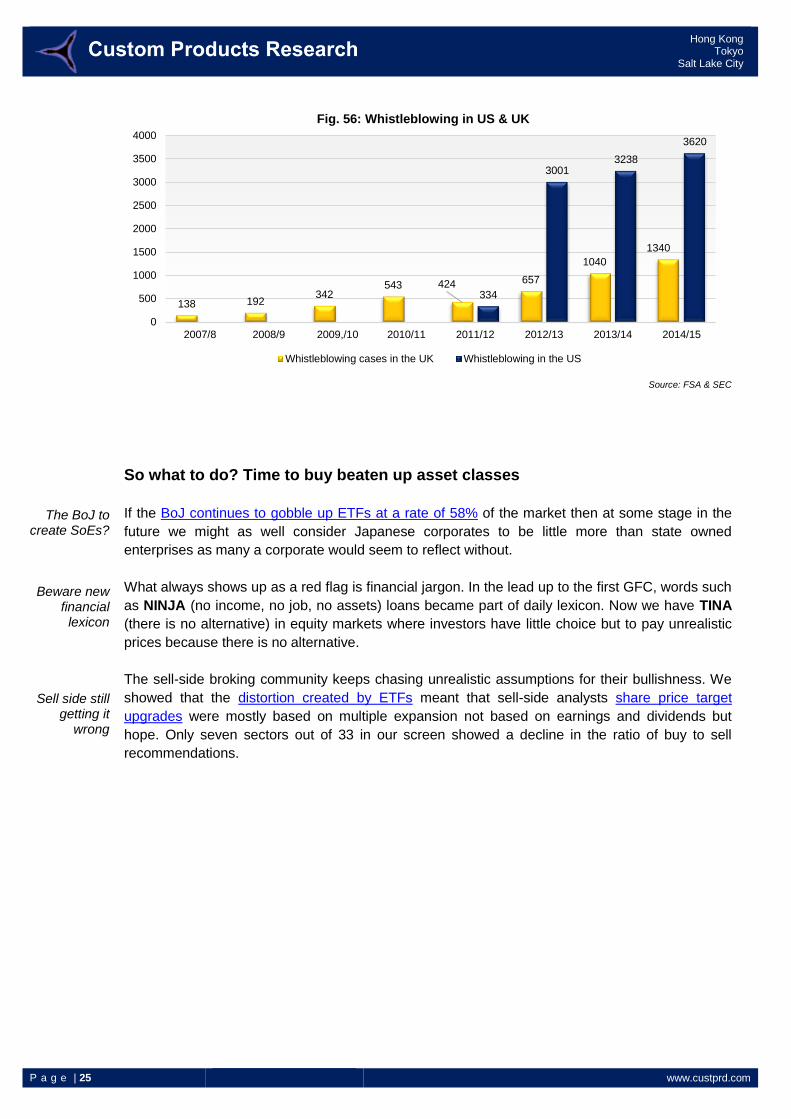

138 192342

543 424 657

1040

1340

334

30013238

3620

0

500

1000

1500

2000

2500

3000

3500

4000

2007/8 2008/9 2009,/10 2010/11 2011/12 2012/13 2013/14 2014/15

Fig. 56: Whistleblowing in US & UK

Whistleblowing cases in the UK Whistleblowing in the US

P a g e | 26 www.custprd.com

Hong Kong Tokyo

Salt Lake City

Herd mentality

makes for contrarian

indicator

Source: Custom Products Research

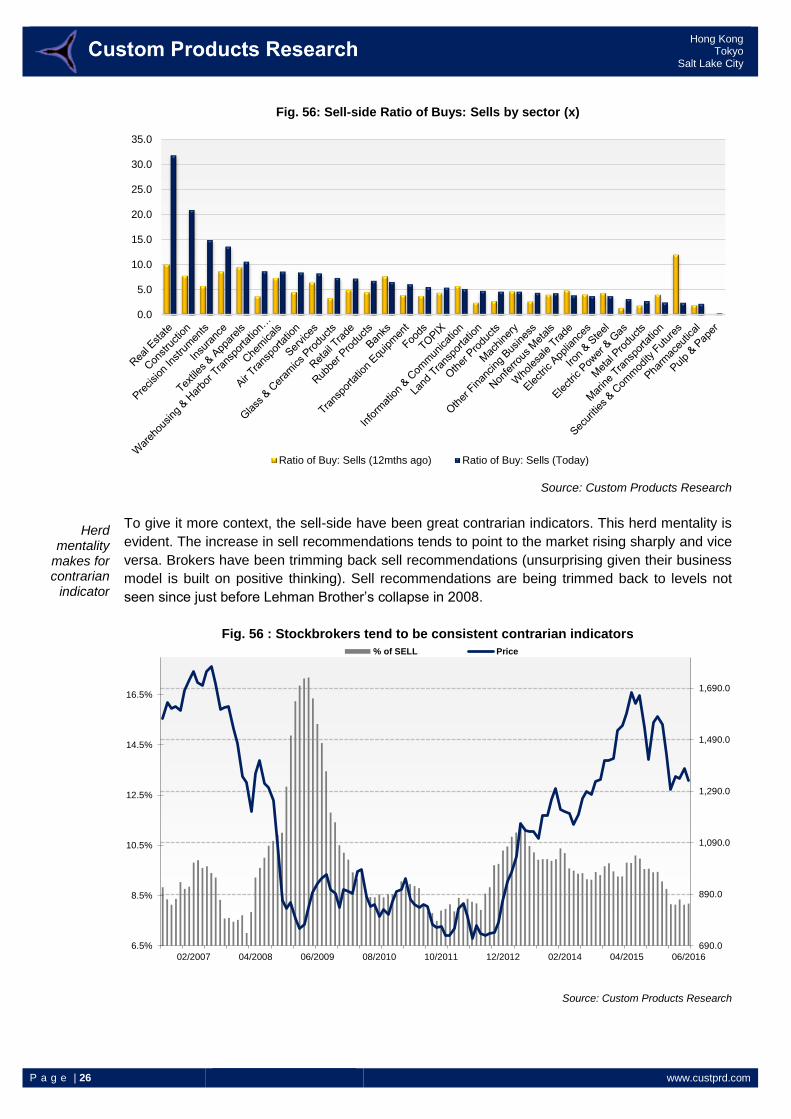

To give it more context, the sell-side have been great contrarian indicators. This herd mentality is

evident. The increase in sell recommendations tends to point to the market rising sharply and vice

versa. Brokers have been trimming back sell recommendations (unsurprising given their business

model is built on positive thinking). Sell recommendations are being trimmed back to levels not

seen since just before Lehman Brother’s collapse in 2008.

Fig. 56 : Stockbrokers tend to be consistent contrarian indicators

Source: Custom Products Research

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

Fig. 56: Sell-side Ratio of Buys: Sells by sector (x)

Ratio of Buy: Sells (12mths ago) Ratio of Buy: Sells (Today)

6.5%

8.5%

10.5%

12.5%

14.5%

16.5%

690.0

890.0

1,090.0

1,290.0

1,490.0

1,690.0

06/201604/201502/201412/201210/201108/201006/200904/200802/2007

% of SELL Price

P a g e | 27 www.custprd.com

Hong Kong Tokyo

Salt Lake City

Market mean reversion

looks imminent

VIX volatility rising

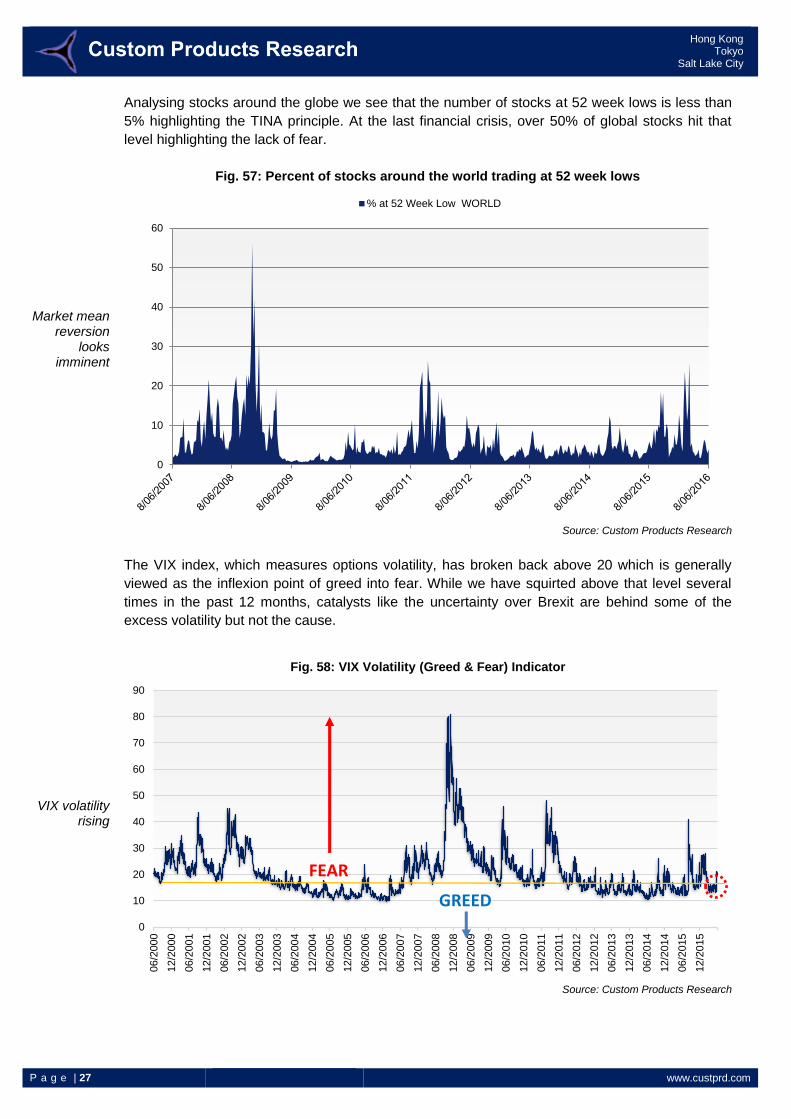

Analysing stocks around the globe we see that the number of stocks at 52 week lows is less than

5% highlighting the TINA principle. At the last financial crisis, over 50% of global stocks hit that

level highlighting the lack of fear.

Fig. 57: Percent of stocks around the world trading at 52 week lows

Source: Custom Products Research

The VIX index, which measures options volatility, has broken back above 20 which is generally

viewed as the inflexion point of greed into fear. While we have squirted above that level several

times in the past 12 months, catalysts like the uncertainty over Brexit are behind some of the

excess volatility but not the cause.

Source: Custom Products Research

0

10

20

30

40

50

60

% at 52 Week Low WORLD

0

10

20

30

40

50

60

70

80

90

06/2

000

12/2

000

06/2

001

12/2

001

06/2

002

12/2

002

06/2

003

12/2

003

06/2

004

12/2

004

06/2

005

12/2

005

06/2

006

12/2

006

06/2

007

12/2

007

06/2

008

12/2

008

06/2

009

12/2

009

06/2

010

12/2

010

06/2

011

12/2

011

06/2

012

12/2

012

06/2

013

12/2

013

06/2

014

12/2

014

06/2

015

12/2

015

Fig. 58: VIX Volatility (Greed & Fear) Indicator

FEAR

GREED

P a g e | 28 www.custprd.com

Hong Kong Tokyo

Salt Lake City

Recession?

Perennial bullishness

has gone too far

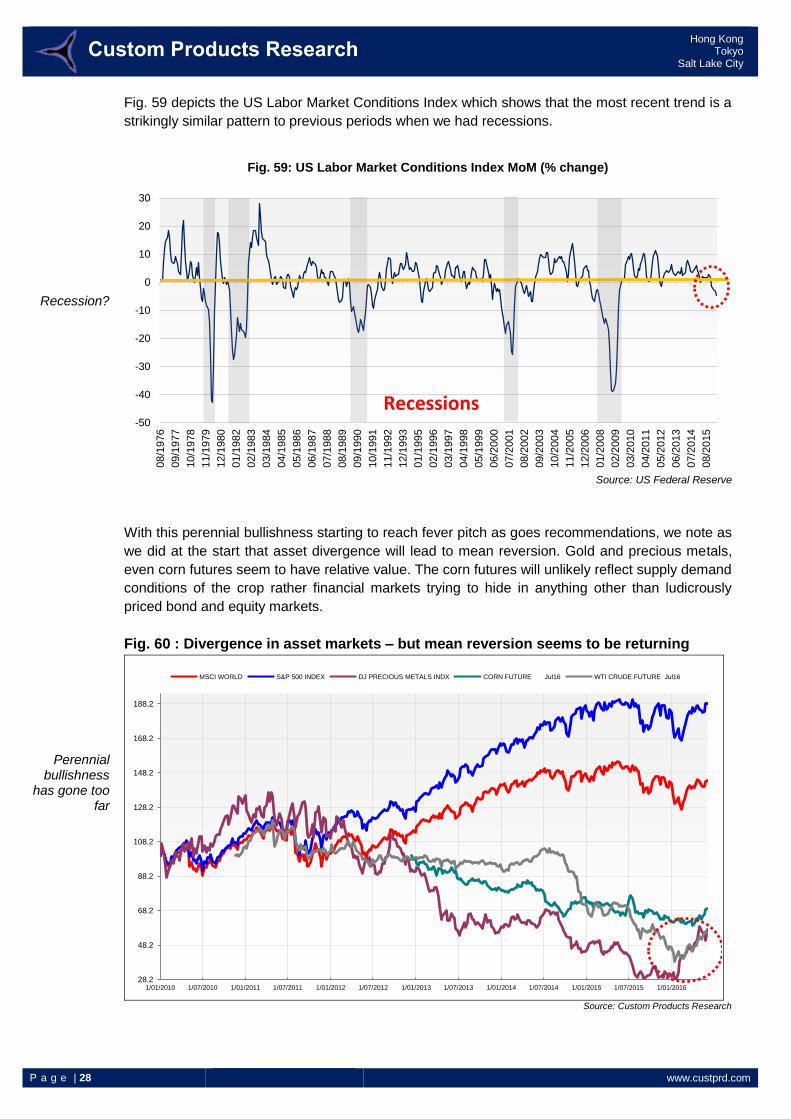

Fig. 59 depicts the US Labor Market Conditions Index which shows that the most recent trend is a

strikingly similar pattern to previous periods when we had recessions.

Source: US Federal Reserve

With this perennial bullishness starting to reach fever pitch as goes recommendations, we note as

we did at the start that asset divergence will lead to mean reversion. Gold and precious metals,

even corn futures seem to have relative value. The corn futures will unlikely reflect supply demand

conditions of the crop rather financial markets trying to hide in anything other than ludicrously

priced bond and equity markets.

Fig. 60 : Divergence in asset markets – but mean reversion seems to be returning

Source: Custom Products Research

-50

-40

-30

-20

-10

0

10

20

30

08/1

976

09/1

977

10/1

978

11/1

979

12/1

980

01/1

982

02/1

983

03/1

984

04/1

985

05/1

986

06/1

987

07/1

988

08/1

989

09/1

990

10/1

991

11/1

992

12/1

993

01/1

995

02/1

996

03/1

997

04/1

998

05/1

999

06/2

000

07/2

001

08/2

002

09/2

003

10/2

004

11/2

005

12/2

006

01/2

008

02/2

009

03/2

010

04/2

011

05/2

012

06/2

013

07/2

014

08/2

015

Fig. 59: US Labor Market Conditions Index MoM (% change)

Recessions

28.2

48.2

68.2

88.2

108.2

128.2

148.2

168.2

188.2

1/01/2010 1/07/2010 1/01/2011 1/07/2011 1/01/2012 1/07/2012 1/01/2013 1/07/2013 1/01/2014 1/07/2014 1/01/2015 1/07/2015 1/01/2016

MSCI WORLD S&P 500 INDEX DJ PRECIOUS METALS INDX CORN FUTURE Jul16 WTI CRUDE FUTURE Jul16

P a g e | 29 www.custprd.com

Hong Kong Tokyo

Salt Lake City

You should be worried

Central banks losing

confidence is a smoking

gun

Velocity of money the

danger

We can’t muddle through

anymore

Payback is arriving

Summary

It is bad out there. No matter which way you look the hallmarks point to a deep recession looming.

What is evident is that the world is as indebted as ever yet the sensitivity to interest rates is

growing larger. Should the economy slowdown at the rate it looks then monetary policy is unlikely

to make any appreciable difference. Central banks are losing control and a loss of confidence will

be catastrophic. For central banks It is the worst possible scenario for them.

If reports about the ECB secretly bailing out local Eurozone banks and installing ‘special

commissioners’ to oversee smooth transitions become more widespread it will only undermine

what little market confidence is left. Central banks are prone to these tactics. M3 reporting was

unceremoniously dumped by then Fed Reserve Chairman Alan Greenspan in 2006 one cynically

suspects was to mask unlimited monetary priming. We estimated (based on historical growth

rates) that the $10 trillion point of 2006 has likely grown to $25 trillion and as velocity continues to

slow, we believe it could hit $40 trillion by 2021.

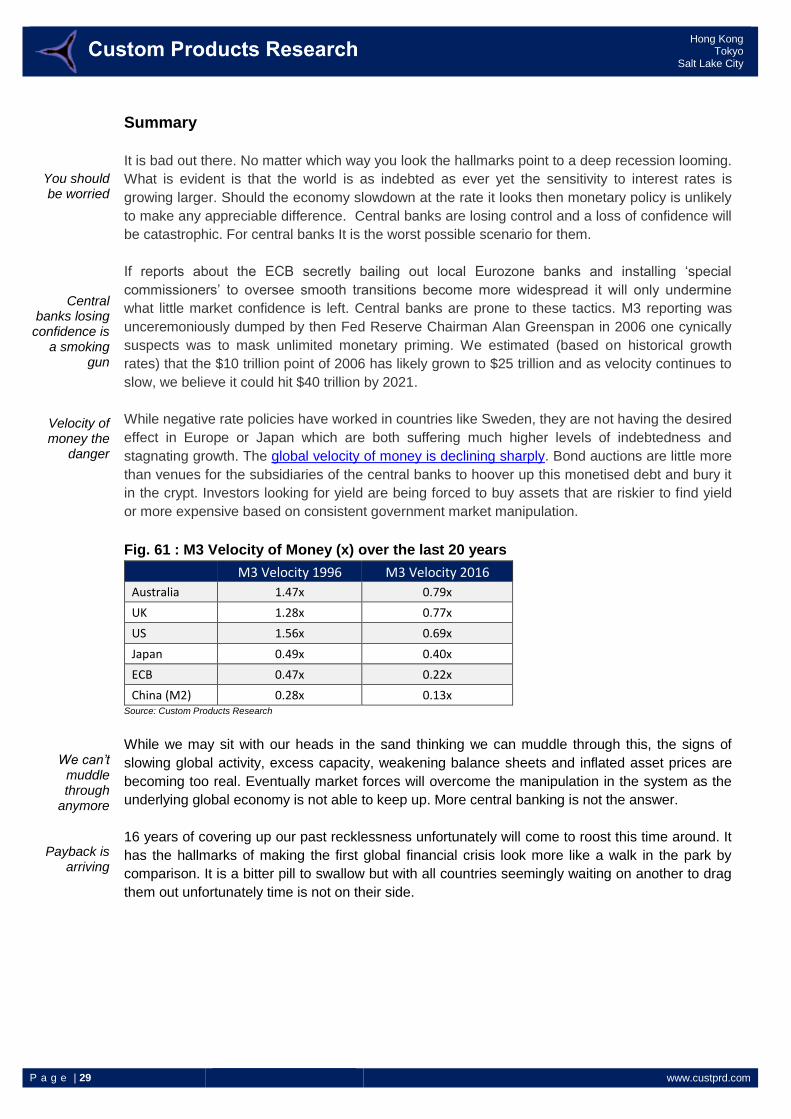

While negative rate policies have worked in countries like Sweden, they are not having the desired

effect in Europe or Japan which are both suffering much higher levels of indebtedness and

stagnating growth. The global velocity of money is declining sharply. Bond auctions are little more

than venues for the subsidiaries of the central banks to hoover up this monetised debt and bury it

in the crypt. Investors looking for yield are being forced to buy assets that are riskier to find yield

or more expensive based on consistent government market manipulation.

Fig. 61 : M3 Velocity of Money (x) over the last 20 years

M3 Velocity 1996 M3 Velocity 2016

Australia 1.47x 0.79x

UK 1.28x 0.77x

US 1.56x 0.69x

Japan 0.49x 0.40x

ECB 0.47x 0.22x

China (M2) 0.28x 0.13x Source: Custom Products Research

While we may sit with our heads in the sand thinking we can muddle through this, the signs of

slowing global activity, excess capacity, weakening balance sheets and inflated asset prices are

becoming too real. Eventually market forces will overcome the manipulation in the system as the

underlying global economy is not able to keep up. More central banking is not the answer.

16 years of covering up our past recklessness unfortunately will come to roost this time around. It

has the hallmarks of making the first global financial crisis look more like a walk in the park by

comparison. It is a bitter pill to swallow but with all countries seemingly waiting on another to drag

them out unfortunately time is not on their side.

P a g e | 30 www.custprd.com

Hong Kong Tokyo

Salt Lake City

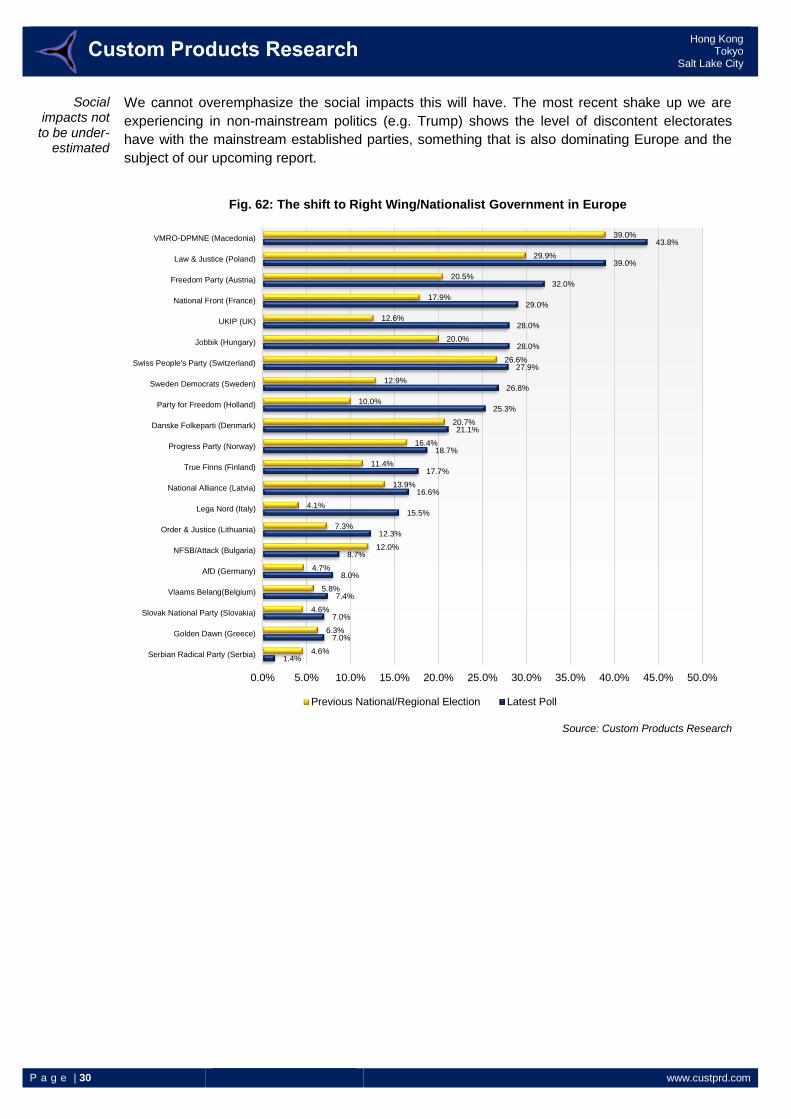

Social impacts not

to be under-estimated

We cannot overemphasize the social impacts this will have. The most recent shake up we are

experiencing in non-mainstream politics (e.g. Trump) shows the level of discontent electorates

have with the mainstream established parties, something that is also dominating Europe and the

subject of our upcoming report.

Source: Custom Products Research

1.4%

7.0%

7.0%

7.4%

8.0%

8.7%

12.3%

15.5%

16.6%

17.7%

18.7%

21.1%

25.3%

26.8%

27.9%

28.0%

28.0%

29.0%

32.0%

39.0%

43.8%

4.6%

6.3%

4.6%

5.8%

4.7%

12.0%

7.3%

4.1%

13.9%

11.4%

16.4%

20.7%

10.0%

12.9%

26.6%

20.0%

12.6%

17.9%

20.5%

29.9%

39.0%

0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0% 35.0% 40.0% 45.0% 50.0%

Serbian Radical Party (Serbia)

Golden Dawn (Greece)

Slovak National Party (Slovakia)

Vlaams Belang(Belgium)

AfD (Germany)

NFSB/Attack (Bulgaria)

Order & Justice (Lithuania)

Lega Nord (Italy)

National Alliance (Latvia)

True Finns (Finland)

Progress Party (Norway)

Danske Folkeparti (Denmark)

Party for Freedom (Holland)

Sweden Democrats (Sweden)

Swiss People's Party (Switzerland)

Jobbik (Hungary)

UKIP (UK)

National Front (France)

Freedom Party (Austria)

Law & Justice (Poland)

VMRO-DPMNE (Macedonia)

Fig. 62: The shift to Right Wing/Nationalist Government in Europe

Previous National/Regional Election Latest Poll

P a g e | 31 www.custprd.com

Hong Kong Tokyo

Salt Lake City

Hong Kong 15/F Langham Place 8 Argyle Street Mong Kok, Kowloon Hong Kong S.A.R.

Tokyo 17/F Roppongi Hills North Tower 6-2-31 Roppongi, Minato-ku, Tokyo Japan 106-0032

Office Locations

Hong Kong Simon Rigney

+852-3958-2394 (HK) +81-3-5786-3712 (Tokyo) [email protected]

Tokyo Robert Rowland

+81-3-5786-3711 [email protected]

Michael Newman

+81-3-5786-3713 [email protected]

Contacts

Salt Lake City Patrick Hansen

+852-8191-6925 (HK) +1-801-230-4796 (SLC) [email protected]

Important Disclosures:

This material was prepared for you and is for your information and use only. This material

should only be distributed to other members of that organization on a need to know basis and

should not be distributed or disseminated to any other person or entity.

This material is for information purposes only and it should not be regarded as an offer to sell or

as a solicitation of an offer to buy the securities or other instruments mentioned in it. This

material is based on current public information that Custom Products Group Limited ("Custom

Products") considers reliable, but we make no representation that it is accurate or complete,

and it should not be relied on as such. No investment opinion or advice is provided, intended,

or solicited. Custom Products offers no warranty, either expressed or implied, regarding the

veracity of data or interpretations of data included in this report. This material is provided with

the understanding that Custom Products is not acting in a fiduciary capacity. Opinions

expressed herein reflect the opinion of Custom Products and are subject to change without

notice.

The products mentioned in this document may not be eligible for sale in some states or

countries, and they may not be suitable for all types of investors. The value of and the income

produced by products may fluctuate, so that an investor may get back less than they invested.

Value and income may be adversely affected by exchange rates, interest rates, or other

factors. Past performance is not necessarily indicative of future results. If a product is income

producing, part of the capital invested may be used to pay that income. © 2015 Custom

Products Group Limited. All rights reserved.

Salt Lake City 299 South Main Street Suite 1300 Salt Lake City, UT United States, 84111