discussion and analysis of the administration on … · the results of operations and financial...

TRANSCRIPT

RESULTS Fourth Quarter Audited , 2013

1

www.pinfra.com.mx (55) 2789 0200

DISCUSSION AND ANALYSIS OF THE ADMINISTRATION ON

THE RESULTS OF OPERATIONS AND FINANCIAL

CONDITION OF THE COMPANY

Promotora y Operadora de Infraestructura, S.A.B. de C.V., announces

non-audited financial results for the Fourth Quarter of 2013.

Pinfra’s solid business model, management and strategy achieve the

company’s best quarter historically. April 30, 2014. Promotora y Operadora de Infraestructura, S.A.B. de C.V. (BMV) a company dedicated to the promotion, development, construction, financing and operating infrastructure projects in Mexico, today announces its non-audited quarterly results for the Fourth quarter ending on December 31,

2013. Regarding this document, unless indicated otherwise, variations refer to changes between the fourth quarter of 2013 and the same period of 2012.

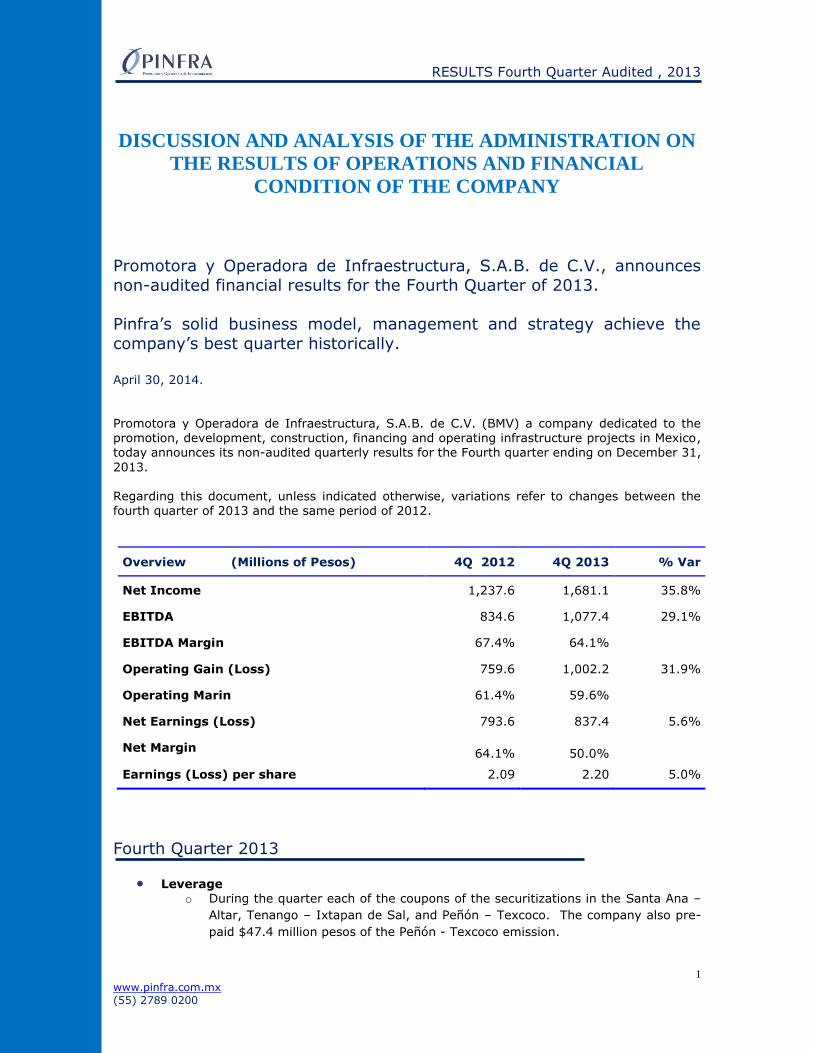

Overview (Millions of Pesos) 4Q 2012 4Q 2013 % Var

Net Income 1,237.6 1,681.1 35.8%

EBITDA 834.6 1,077.4 29.1%

EBITDA Margin 67.4% 64.1%

Operating Gain (Loss) 759.6 1,002.2 31.9%

Operating Marin 61.4% 59.6%

Net Earnings (Loss) 793.6 837.4 5.6%

Net Margin 64.1% 50.0%

Earnings (Loss) per share 2.09 2.20 5.0%

Fourth Quarter 2013

Leverage o During the quarter each of the coupons of the securitizations in the Santa Ana –

Altar, Tenango – Ixtapan de Sal, and Peñón – Texcoco. The company also pre-

paid $47.4 million pesos of the Peñón - Texcoco emission.

RESULTS Fourth Quarter Audited , 2013

2

www.pinfra.com.mx (55) 2789 0200

Analysis of the Creation of Value o The company increased its cash during the quarter by $32.4 million pesos. It

generated $493.4 million pesos from its operations. It invested $456.5 million pesos for the Marquesa – Lerma, Peñón – Pirámides, Tlaxcala – Puebla, Tenango – Ixtapan de la Sal and the Siglo XXI Highway.

o Key Financial Figures Sales of $1,681.1 million pesos, higher by 35.8% compared with the same

quarter of the previous year.

Concessions, the most important activity in the company representing

70.83% of revenues increased its sales year-over-year by 16.6%

amounting to $1,190.8 million pesos.

Operating profits of $1,002.2 million pesos, 31.9% more than in the fourth

quarter of 2012.

The company’s EBITDA was $1,077.4 million pesos, an increase of 29.1%

versus the same period of the previous year.

Net profits were $837.4 million pesos, 5.6% higher than the third quarter

of 2012.

Earnings per share of 2.20 pesos, a year-over-year increase of 5.0%.

Growth of New Assets

o On November 28, the company obtained the concession to the Siglo XXI Toll road, from “Jantetelco – El Higueron” with an approximate length of 61.8 kilometers. It has a 30-year term and an approximate investment of $2,885 million pesos with a $723 million pesos grant from FONADIN. Pinfra has a 51% ownership on the

project with GBM and Aldesa owning the rest. In the quarter, the company contributed $149 million pesos corresponding to its equity participation in the project.

o In the continuation of the Mexico – Marquesa toll road concession that will now

run up Lerma, the company invested $185 million pesos and now has obtained 44% of the land needed.

o The Tlaxcala – Puebla toll road had an economic advance of 48.0%.

o We continued liberating the right of way for the vía Peñón – Pirámides at the end of the quarter, 56.0% were obtained and we had substantial negations on course.

We invested $36.5 million pesos during the period.

Key Operating Figures o The average daily traffic in the highways operated or which Pinfra has participation

was 208,403 vehicles per day. Revenues for the toll roads that consolidate were

$11.2 million pesos per day, a year-over-year increase of 7.8%. It is important

to mention that total revenues of our consolidating toll roads grew by 17.6% with

revenues of $1,023.0 million pesos again due to the Puebla Package, which

operated for a complete quarter, and income of $105.4 million pesos.

o Infraestructura Portuaria Mexicana increased the cargo it managed by 8.0% in

containers, its most important and profitable activity, 14.9% in steel while there

was a decrease of 0.6% in general cargo and 12.2% in chasis. This brought an

EBITDA 11.4% higher than in the same quarter of the previous year amounting to

$60.5 million pesos.

RESULTS Fourth Quarter Audited , 2013

3

www.pinfra.com.mx (55) 2789 0200

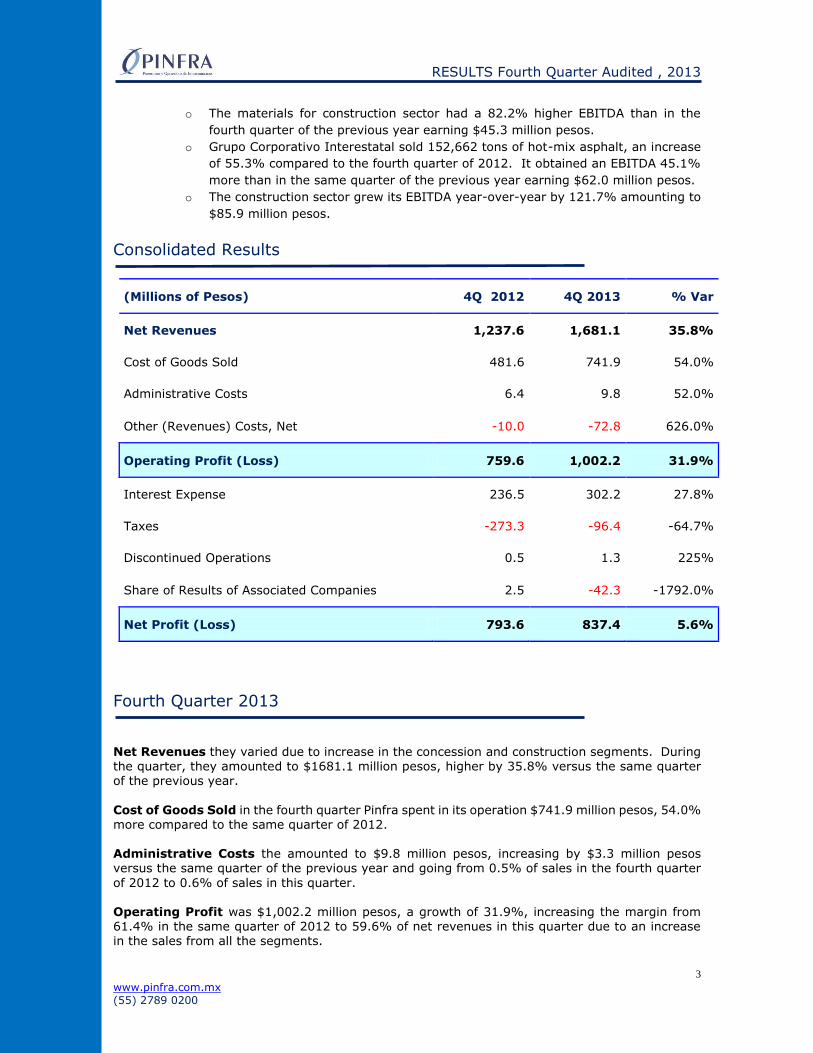

o The materials for construction sector had a 82.2% higher EBITDA than in the

fourth quarter of the previous year earning $45.3 million pesos.

o Grupo Corporativo Interestatal sold 152,662 tons of hot-mix asphalt, an increase

of 55.3% compared to the fourth quarter of 2012. It obtained an EBITDA 45.1%

more than in the same quarter of the previous year earning $62.0 million pesos.

o The construction sector grew its EBITDA year-over-year by 121.7% amounting to

$85.9 million pesos.

Consolidated Results

(Millions of Pesos) 4Q 2012 4Q 2013 % Var

Net Revenues 1,237.6 1,681.1 35.8%

Cost of Goods Sold 481.6 741.9 54.0%

Administrative Costs 6.4 9.8 52.0%

Other (Revenues) Costs, Net -10.0 -72.8 626.0%

Operating Profit (Loss) 759.6 1,002.2 31.9%

Interest Expense 236.5 302.2 27.8%

Taxes -273.3 -96.4 -64.7%

Discontinued Operations 0.5 1.3 225%

Share of Results of Associated Companies 2.5 -42.3 -1792.0%

Net Profit (Loss) 793.6 837.4 5.6%

Fourth Quarter 2013

Net Revenues they varied due to increase in the concession and construction segments. During the quarter, they amounted to $1681.1 million pesos, higher by 35.8% versus the same quarter of the previous year.

Cost of Goods Sold in the fourth quarter Pinfra spent in its operation $741.9 million pesos, 54.0% more compared to the same quarter of 2012. Administrative Costs the amounted to $9.8 million pesos, increasing by $3.3 million pesos versus the same quarter of the previous year and going from 0.5% of sales in the fourth quarter

of 2012 to 0.6% of sales in this quarter. Operating Profit was $1,002.2 million pesos, a growth of 31.9%, increasing the margin from 61.4% in the same quarter of 2012 to 59.6% of net revenues in this quarter due to an increase in the sales from all the segments.

RESULTS Fourth Quarter Audited , 2013

4

www.pinfra.com.mx (55) 2789 0200

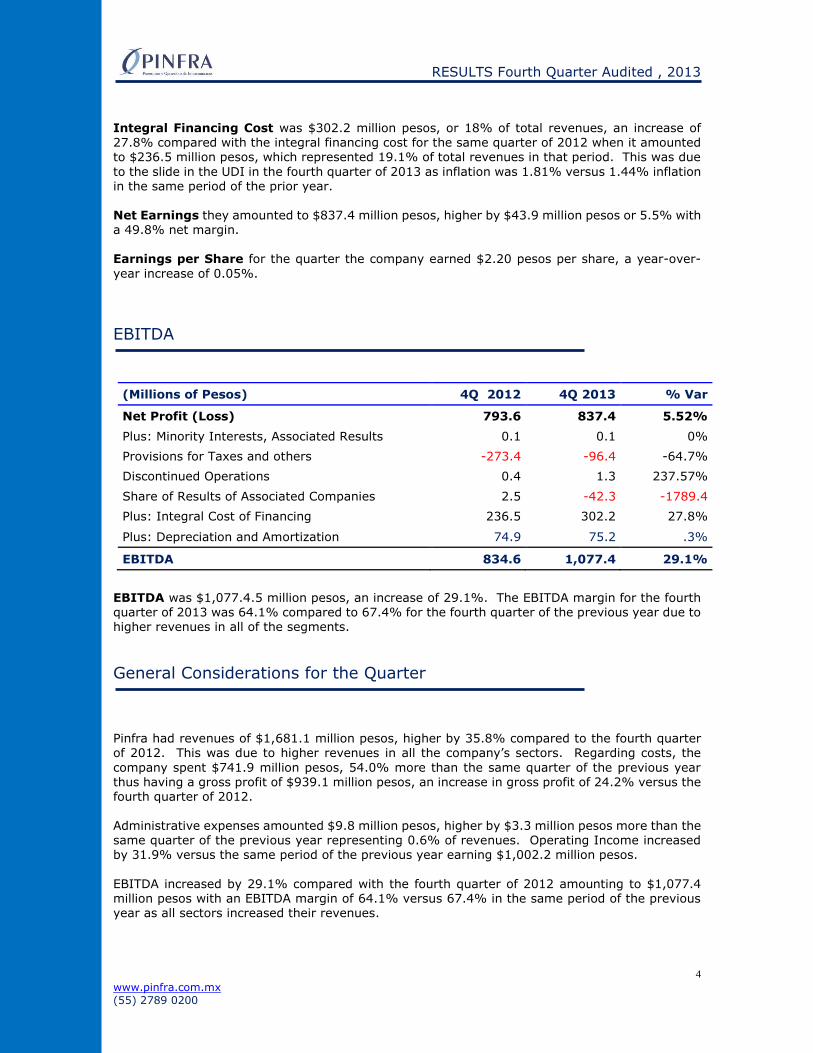

Integral Financing Cost was $302.2 million pesos, or 18% of total revenues, an increase of 27.8% compared with the integral financing cost for the same quarter of 2012 when it amounted to $236.5 million pesos, which represented 19.1% of total revenues in that period. This was due

to the slide in the UDI in the fourth quarter of 2013 as inflation was 1.81% versus 1.44% inflation in the same period of the prior year. Net Earnings they amounted to $837.4 million pesos, higher by $43.9 million pesos or 5.5% with a 49.8% net margin. Earnings per Share for the quarter the company earned $2.20 pesos per share, a year-over-

year increase of 0.05%.

EBITDA

(Millions of Pesos) 4Q 2012 4Q 2013 % Var

Net Profit (Loss) 793.6 837.4 5.52%

Plus: Minority Interests, Associated Results 0.1 0.1 0%

Provisions for Taxes and others -273.4 -96.4 -64.7%

Discontinued Operations 0.4 1.3 237.57%

Share of Results of Associated Companies 2.5 -42.3 -1789.4

Plus: Integral Cost of Financing 236.5 302.2 27.8%

Plus: Depreciation and Amortization 74.9 75.2 .3%

EBITDA 834.6 1,077.4 29.1%

EBITDA was $1,077.4.5 million pesos, an increase of 29.1%. The EBITDA margin for the fourth quarter of 2013 was 64.1% compared to 67.4% for the fourth quarter of the previous year due to higher revenues in all of the segments.

General Considerations for the Quarter

Pinfra had revenues of $1,681.1 million pesos, higher by 35.8% compared to the fourth quarter of 2012. This was due to higher revenues in all the company’s sectors. Regarding costs, the

company spent $741.9 million pesos, 54.0% more than the same quarter of the previous year thus having a gross profit of $939.1 million pesos, an increase in gross profit of 24.2% versus the fourth quarter of 2012.

Administrative expenses amounted $9.8 million pesos, higher by $3.3 million pesos more than the same quarter of the previous year representing 0.6% of revenues. Operating Income increased by 31.9% versus the same period of the previous year earning $1,002.2 million pesos.

EBITDA increased by 29.1% compared with the fourth quarter of 2012 amounting to $1,077.4 million pesos with an EBITDA margin of 64.1% versus 67.4% in the same period of the previous year as all sectors increased their revenues.

RESULTS Fourth Quarter Audited , 2013

5

www.pinfra.com.mx (55) 2789 0200

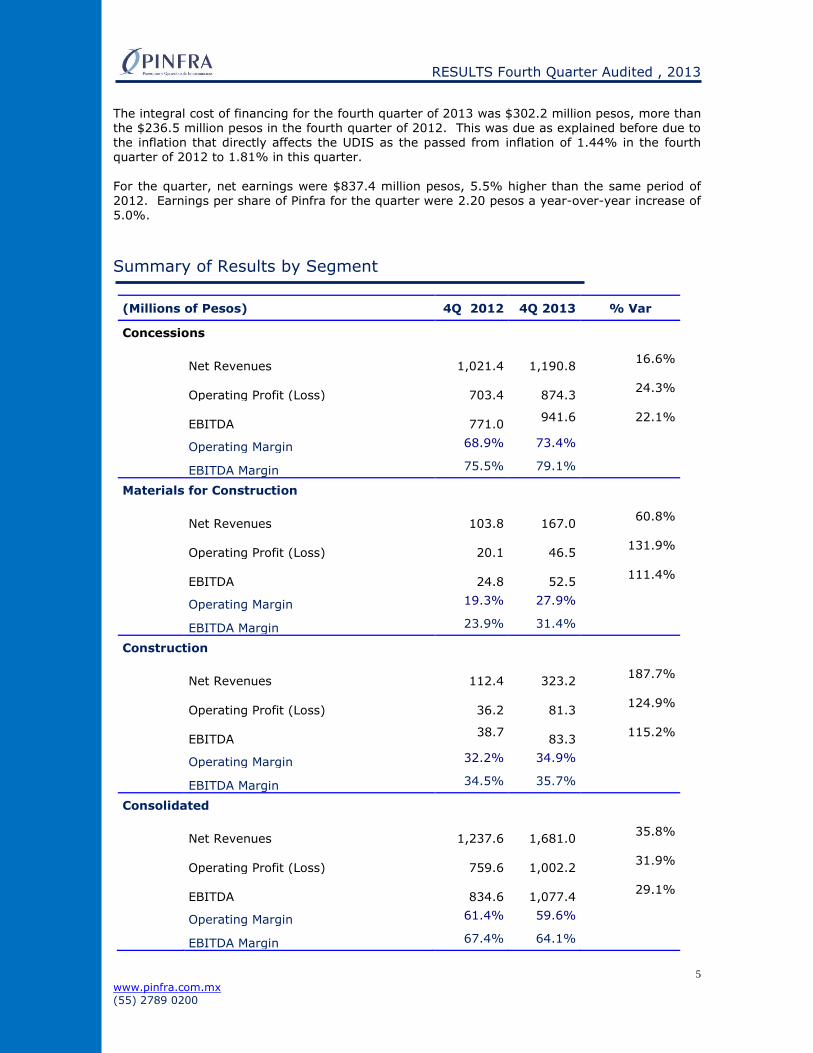

The integral cost of financing for the fourth quarter of 2013 was $302.2 million pesos, more than the $236.5 million pesos in the fourth quarter of 2012. This was due as explained before due to the inflation that directly affects the UDIS as the passed from inflation of 1.44% in the fourth quarter of 2012 to 1.81% in this quarter.

For the quarter, net earnings were $837.4 million pesos, 5.5% higher than the same period of 2012. Earnings per share of Pinfra for the quarter were 2.20 pesos a year-over-year increase of 5.0%.

Summary of Results by Segment

(Millions of Pesos) 4Q 2012 4Q 2013 % Var

Concessions

Net Revenues

1,021.4

1,190.8 16.6%

Operating Profit (Loss)

703.4

874.3 24.3%

EBITDA

771.0 941.6 22.1%

Operating Margin 68.9% 73.4%

EBITDA Margin 75.5% 79.1%

Materials for Construction

Net Revenues

103.8

167.0 60.8%

Operating Profit (Loss)

20.1

46.5 131.9%

EBITDA

24.8

52.5 111.4%

Operating Margin 19.3% 27.9%

EBITDA Margin 23.9% 31.4%

Construction

Net Revenues

112.4

323.2 187.7%

Operating Profit (Loss)

36.2

81.3 124.9%

EBITDA 38.7

83.3

115.2%

Operating Margin 32.2% 34.9%

EBITDA Margin 34.5% 35.7%

Consolidated

Net Revenues

1,237.6

1,681.0 35.8%

Operating Profit (Loss)

759.6

1,002.2 31.9%

EBITDA

834.6

1,077.4 29.1%

Operating Margin 61.4% 59.6%

EBITDA Margin 67.4% 64.1%

RESULTS Fourth Quarter Audited , 2013

6

www.pinfra.com.mx (55) 2789 0200

Concessions Segment

For the quarter, revenues increased 16.6% versus the same quarter of the previous year, receiving $1,190.8 million pesos. Income without VAT for the fourth quarter were $405.3 million pesos in the México – Toluca, $116.7 million pesos in the Ecatepec – Pirámides, $100.2 million pesos in

the Armería – Manzanillo, $102.9 million pesos in the Peñón – Texcoco, $34.8 million pesos in the Tenango – Ixtapan de la Sal, $46.0 million pesos in the Atlixco – Jantetelco, $44.1 million pesos in the Santa Ana – Altar, $3.4 million pesos in the la San Luis Río Colorado, $39.6 million pesos in the San Martín Texmelucan, $9.7 million pesos in the Lengua de Vaca, Vía Atlixcáyotl $51.2 million pesos, Virreyes – Teziutlán $29.1 million pesos, Apizaco – Huauchinango $25.0 million pesos and $157.2 million pesos in the Altamira Port Terminal. As the Puebla Package became operational cost increased 31.0% compared to the same quarter of the previous year amounting

to $369.1 million pesos. The EBITDA for the quarter was $948.5 million pesos 23.0% higher than in the same quarter of 2012.

* The Puebla Toll Road Package started operating December 8, 2012, thus the periods are not comparable regarding average income or

traffic as the last few days of the December quarter have more traffic than those in a full quarter such as 2013. ** It is important to mention that the Michoacán Package does not consolidate in the company’s financial statements.

In the fourth quarter in all of the toll roads, which Pinfra has participation, average daily traffic was 208,403 vehicles, a year-over-year decrease of 2.8%. This is the result of not having a full quarter operation regarding the Puebla Package skewing the results of the ADI and ADT. The average EBITDA margin for the toll roads that consolidate in Pinfra’s financial statements was 82.9%.

Quarter Ended on December 31

4Q 2012 4Q 2013 % Var

Average Daily Income (thousands of pesos)

Toll Roads Operated for more than a year $ 10,490.6 $ 10,141.6 -3.3%

Puebla Toll Road Package* $ 1,156.5 $ 1,145.1 -1.0%

Michoacán Package**

$

1,566.7 $ 1,821.4 16.3%

Total Average Daily Income (thousands of pesos)

$12,057.4 $

13,108.1 8.7%

Average Daily Traffic

Toll Roads Operated for more than a year 144,962 146,322 0.9%

Puebla Toll Road Package* 30,949 25,640 -17.2%

Michoacán Package** 38,528 36,441 -5.4%

RESULTS Fourth Quarter Audited , 2013

7

www.pinfra.com.mx (55) 2789 0200

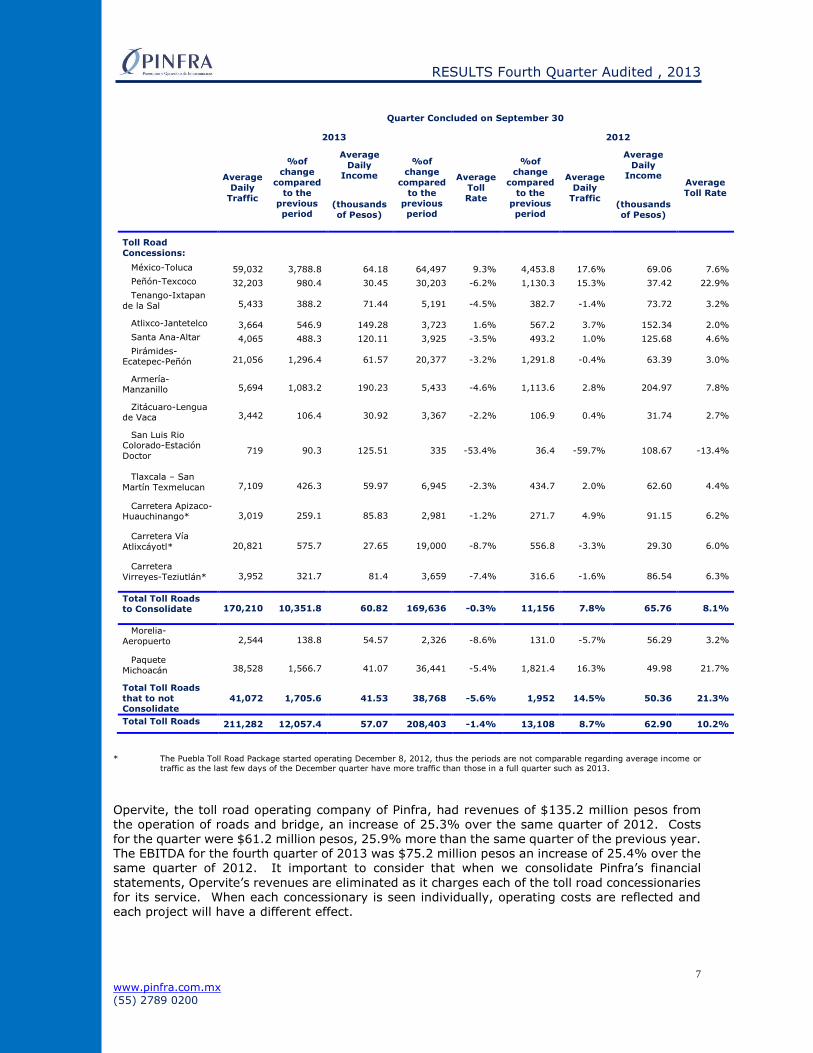

Quarter Concluded on September 30

2013 2012

Average

Daily

Traffic

%of

change

compared

to the

previous period

Average

Daily Income

%of

change

compared

to the

previous period

Average

Toll

Rate

%of

change

compared

to the

previous period

Average

Daily

Traffic

Average

Daily Income

Average

Toll Rate

(thousands

of Pesos)

(thousands

of Pesos)

Toll Road

Concessions:

México-Toluca 59,032 3,788.8 64.18 64,497 9.3% 4,453.8 17.6% 69.06 7.6%

Peñón-Texcoco 32,203 980.4 30.45 30,203 -6.2% 1,130.3 15.3% 37.42 22.9%

Tenango-Ixtapan

de la Sal 5,433 388.2 71.44 5,191 -4.5% 382.7 -1.4% 73.72 3.2%

Atlixco-Jantetelco 3,664 546.9 149.28 3,723 1.6% 567.2 3.7% 152.34 2.0%

Santa Ana-Altar 4,065 488.3 120.11 3,925 -3.5% 493.2 1.0% 125.68 4.6%

Pirámides-Ecatepec-Peñón 21,056 1,296.4 61.57 20,377 -3.2% 1,291.8 -0.4% 63.39 3.0%

Armería-Manzanillo 5,694 1,083.2 190.23 5,433 -4.6% 1,113.6 2.8% 204.97 7.8%

Zitácuaro-Lengua de Vaca 3,442 106.4 30.92 3,367 -2.2% 106.9 0.4% 31.74 2.7%

San Luis Rio Colorado-Estación

Doctor 719 90.3 125.51 335 -53.4% 36.4 -59.7% 108.67 -13.4%

Tlaxcala – San

Martín Texmelucan 7,109 426.3 59.97 6,945 -2.3% 434.7 2.0% 62.60 4.4%

Carretera Apizaco-Huauchinango* 3,019 259.1 85.83 2,981 -1.2% 271.7 4.9% 91.15 6.2%

Carretera Vía

Atlixcáyotl* 20,821 575.7 27.65 19,000 -8.7% 556.8 -3.3% 29.30 6.0%

Carretera

Virreyes-Teziutlán* 3,952 321.7 81.4 3,659 -7.4% 316.6 -1.6% 86.54 6.3%

Total Toll Roads to Consolidate 170,210 10,351.8 60.82 169,636 -0.3% 11,156 7.8% 65.76 8.1%

Morelia-

Aeropuerto 2,544 138.8 54.57 2,326 -8.6% 131.0 -5.7% 56.29 3.2%

Paquete

Michoacán 38,528 1,566.7 41.07 36,441 -5.4% 1,821.4 16.3% 49.98 21.7%

Total Toll Roads

that to not Consolidate

41,072 1,705.6 41.53 38,768 -5.6% 1,952 14.5% 50.36 21.3%

Total Toll Roads 211,282 12,057.4 57.07 208,403 -1.4% 13,108 8.7% 62.90 10.2%

* The Puebla Toll Road Package started operating December 8, 2012, thus the periods are not comparable regarding average income or

traffic as the last few days of the December quarter have more traffic than those in a full quarter such as 2013.

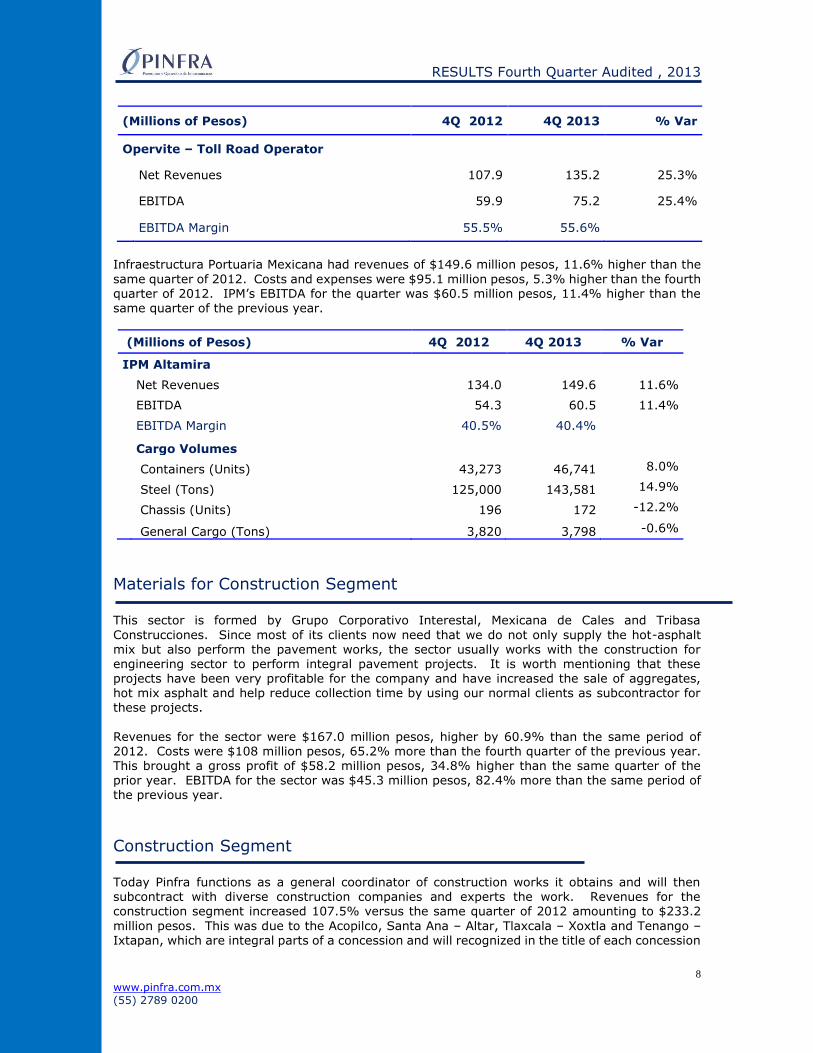

Opervite, the toll road operating company of Pinfra, had revenues of $135.2 million pesos from the operation of roads and bridge, an increase of 25.3% over the same quarter of 2012. Costs for the quarter were $61.2 million pesos, 25.9% more than the same quarter of the previous year. The EBITDA for the fourth quarter of 2013 was $75.2 million pesos an increase of 25.4% over the same quarter of 2012. It important to consider that when we consolidate Pinfra’s financial

statements, Opervite’s revenues are eliminated as it charges each of the toll road concessionaries for its service. When each concessionary is seen individually, operating costs are reflected and each project will have a different effect.

RESULTS Fourth Quarter Audited , 2013

8

www.pinfra.com.mx (55) 2789 0200

(Millions of Pesos) 4Q 2012 4Q 2013 % Var

Opervite – Toll Road Operator

Net Revenues 107.9 135.2 25.3%

EBITDA 59.9 75.2 25.4%

EBITDA Margin 55.5% 55.6%

Infraestructura Portuaria Mexicana had revenues of $149.6 million pesos, 11.6% higher than the

same quarter of 2012. Costs and expenses were $95.1 million pesos, 5.3% higher than the fourth quarter of 2012. IPM’s EBITDA for the quarter was $60.5 million pesos, 11.4% higher than the same quarter of the previous year.

(Millions of Pesos) 4Q 2012 4Q 2013 % Var

IPM Altamira

Net Revenues 134.0 149.6 11.6%

EBITDA 54.3 60.5 11.4%

EBITDA Margin 40.5% 40.4%

Cargo Volumes

Containers (Units) 43,273 46,741 8.0%

Steel (Tons) 125,000 143,581 14.9%

Chassis (Units) 196 172 -12.2%

General Cargo (Tons) 3,820 3,798 -0.6%

Materials for Construction Segment

This sector is formed by Grupo Corporativo Interestal, Mexicana de Cales and Tribasa

Construcciones. Since most of its clients now need that we do not only supply the hot-asphalt mix but also perform the pavement works, the sector usually works with the construction for engineering sector to perform integral pavement projects. It is worth mentioning that these projects have been very profitable for the company and have increased the sale of aggregates, hot mix asphalt and help reduce collection time by using our normal clients as subcontractor for these projects.

Revenues for the sector were $167.0 million pesos, higher by 60.9% than the same period of 2012. Costs were $108 million pesos, 65.2% more than the fourth quarter of the previous year. This brought a gross profit of $58.2 million pesos, 34.8% higher than the same quarter of the prior year. EBITDA for the sector was $45.3 million pesos, 82.4% more than the same period of the previous year.

Construction Segment

Today Pinfra functions as a general coordinator of construction works it obtains and will then subcontract with diverse construction companies and experts the work. Revenues for the construction segment increased 107.5% versus the same quarter of 2012 amounting to $233.2

million pesos. This was due to the Acopilco, Santa Ana – Altar, Tlaxcala – Xoxtla and Tenango – Ixtapan, which are integral parts of a concession and will recognized in the title of each concession

RESULTS Fourth Quarter Audited , 2013

9

www.pinfra.com.mx (55) 2789 0200

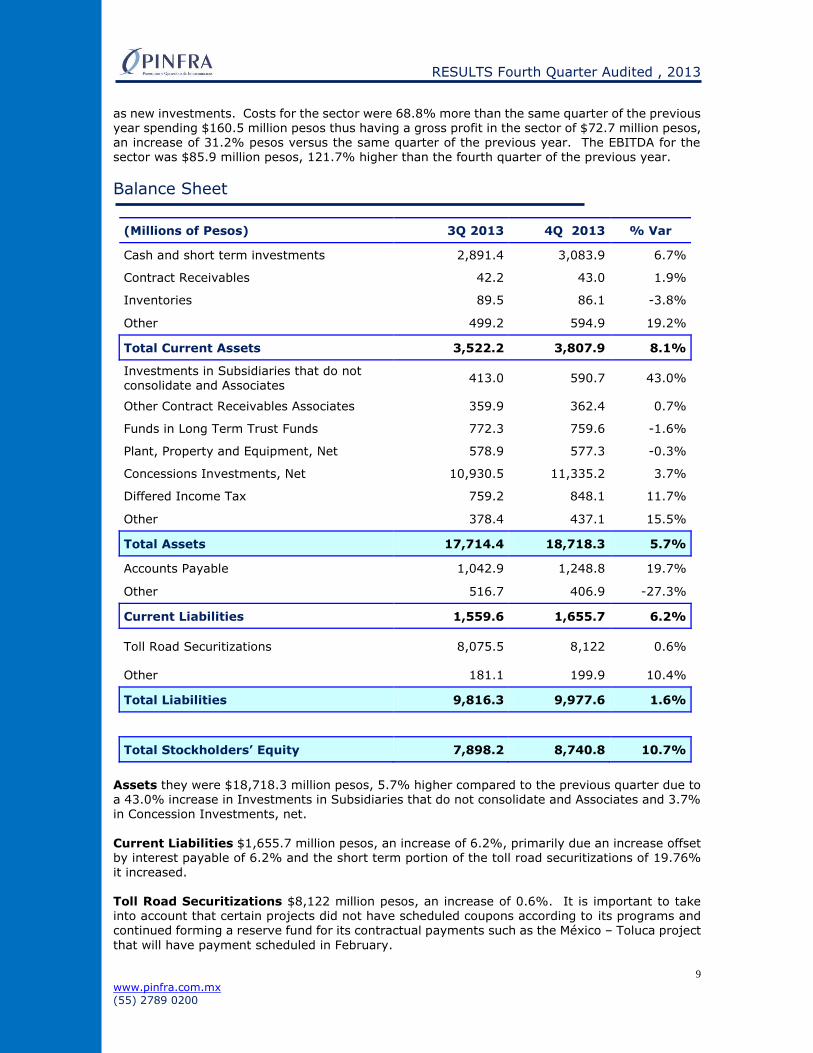

as new investments. Costs for the sector were 68.8% more than the same quarter of the previous year spending $160.5 million pesos thus having a gross profit in the sector of $72.7 million pesos, an increase of 31.2% pesos versus the same quarter of the previous year. The EBITDA for the sector was $85.9 million pesos, 121.7% higher than the fourth quarter of the previous year.

Balance Sheet

(Millions of Pesos) 3Q 2013 4Q 2013 % Var

Cash and short term investments 2,891.4 3,083.9 6.7%

Contract Receivables 42.2 43.0 1.9%

Inventories 89.5 86.1 -3.8%

Other 499.2 594.9 19.2%

Total Current Assets 3,522.2 3,807.9 8.1%

Investments in Subsidiaries that do not consolidate and Associates

413.0 590.7 43.0%

Other Contract Receivables Associates 359.9 362.4 0.7%

Funds in Long Term Trust Funds 772.3 759.6 -1.6%

Plant, Property and Equipment, Net 578.9 577.3 -0.3%

Concessions Investments, Net 10,930.5 11,335.2 3.7%

Differed Income Tax 759.2 848.1 11.7%

Other 378.4 437.1 15.5%

Total Assets 17,714.4 18,718.3 5.7%

Accounts Payable 1,042.9 1,248.8 19.7%

Other 516.7 406.9 -27.3%

Current Liabilities 1,559.6 1,655.7 6.2%

Toll Road Securitizations 8,075.5 8,122 0.6%

Other 181.1 199.9 10.4%

Total Liabilities 9,816.3 9,977.6 1.6%

Total Stockholders’ Equity 7,898.2 8,740.8 10.7%

Assets they were $18,718.3 million pesos, 5.7% higher compared to the previous quarter due to a 43.0% increase in Investments in Subsidiaries that do not consolidate and Associates and 3.7%

in Concession Investments, net.

Current Liabilities $1,655.7 million pesos, an increase of 6.2%, primarily due an increase offset by interest payable of 6.2% and the short term portion of the toll road securitizations of 19.76% it increased. Toll Road Securitizations $8,122 million pesos, an increase of 0.6%. It is important to take into account that certain projects did not have scheduled coupons according to its programs and continued forming a reserve fund for its contractual payments such as the México – Toluca project

that will have payment scheduled in February.

RESULTS Fourth Quarter Audited , 2013

10

www.pinfra.com.mx (55) 2789 0200

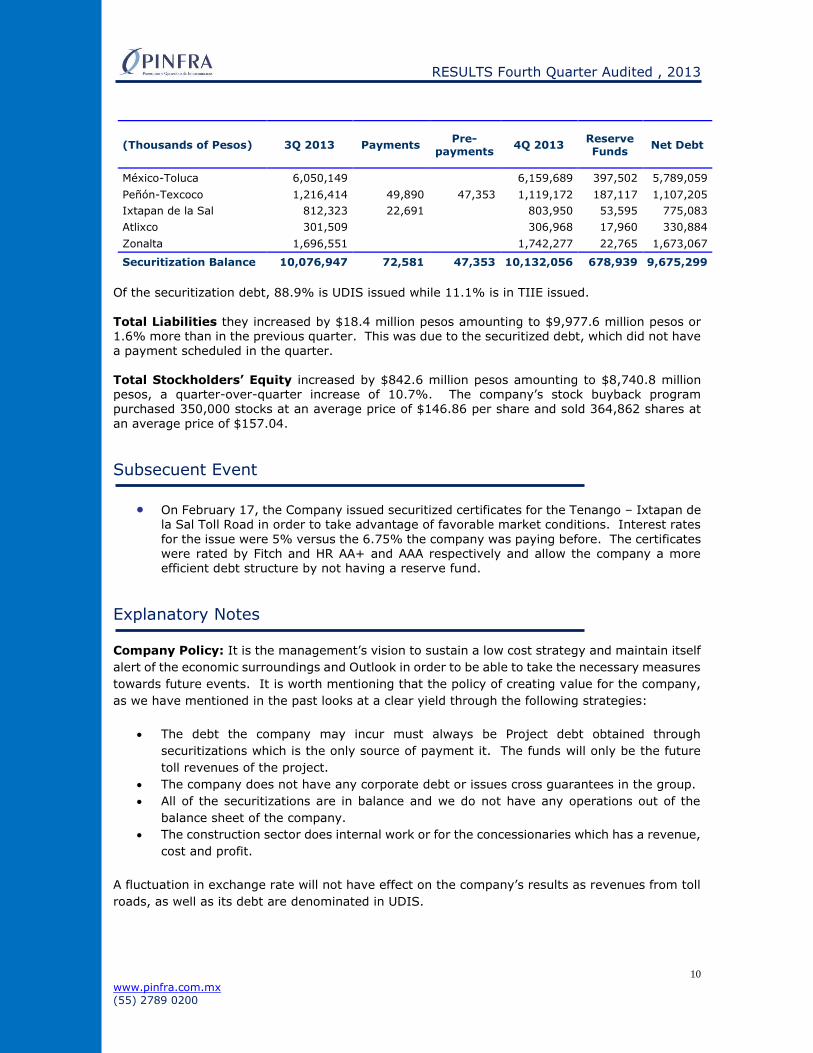

(Thousands of Pesos) 3Q 2013 Payments Pre-

payments 4Q 2013

Reserve Funds

Net Debt

México-Toluca 6,050,149 6,159,689 397,502 5,789,059

Peñón-Texcoco 1,216,414 49,890 47,353 1,119,172 187,117 1,107,205

Ixtapan de la Sal 812,323 22,691 803,950 53,595 775,083

Atlixco 301,509 306,968 17,960 330,884

Zonalta 1,696,551 1,742,277 22,765 1,673,067

Securitization Balance 10,076,947 72,581 47,353 10,132,056 678,939 9,675,299

Of the securitization debt, 88.9% is UDIS issued while 11.1% is in TIIE issued.

Total Liabilities they increased by $18.4 million pesos amounting to $9,977.6 million pesos or 1.6% more than in the previous quarter. This was due to the securitized debt, which did not have

a payment scheduled in the quarter. Total Stockholders’ Equity increased by $842.6 million pesos amounting to $8,740.8 million pesos, a quarter-over-quarter increase of 10.7%. The company’s stock buyback program purchased 350,000 stocks at an average price of $146.86 per share and sold 364,862 shares at

an average price of $157.04.

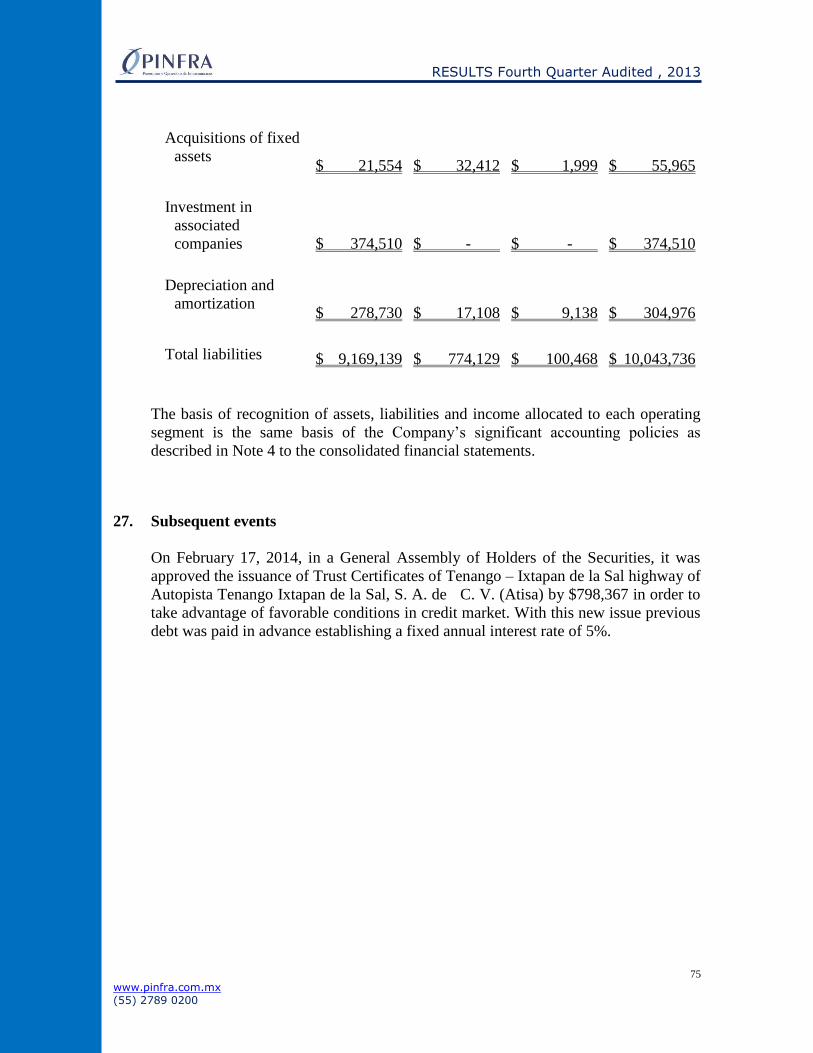

Subsecuent Event

On February 17, the Company issued securitized certificates for the Tenango – Ixtapan de

la Sal Toll Road in order to take advantage of favorable market conditions. Interest rates

for the issue were 5% versus the 6.75% the company was paying before. The certificates were rated by Fitch and HR AA+ and AAA respectively and allow the company a more efficient debt structure by not having a reserve fund.

Explanatory Notes

Company Policy: It is the management’s vision to sustain a low cost strategy and maintain itself

alert of the economic surroundings and Outlook in order to be able to take the necessary measures

towards future events. It is worth mentioning that the policy of creating value for the company,

as we have mentioned in the past looks at a clear yield through the following strategies:

The debt the company may incur must always be Project debt obtained through

securitizations which is the only source of payment it. The funds will only be the future

toll revenues of the project.

The company does not have any corporate debt or issues cross guarantees in the group.

All of the securitizations are in balance and we do not have any operations out of the

balance sheet of the company.

The construction sector does internal work or for the concessionaries which has a revenue,

cost and profit.

A fluctuation in exchange rate will not have effect on the company’s results as revenues from toll

roads, as well as its debt are denominated in UDIS.

RESULTS Fourth Quarter Audited , 2013

11

www.pinfra.com.mx (55) 2789 0200

Fiscal Consolidation: The Company has no consolidated for fiscal terms since the year ending in 1999, thus the numbers presented in this report will not be affected concerning this with the new fiscal reform.

Non-Audited Financial Statements: The amounts in this letter have not been audited for the year 2013. Previous period: Unless stated previous period means the comparison of the financial and operating numbers versus the same quarter of the previous year.

Method of Expressing mounts: Unless noted differently all of the amounts in this release are in Mexican Pesos. This release may contain information and statements in the future tense. Future tense statements are not historical facts. These statements are only predictions based on our expectations and

projections regarding future events. Statements in the future tense can be identified with the words "consider" "expect", "anticipate", "handle", or similar expressions. While PINFRA

management believes that the expectations reflected in such statements in the future tense are reasonable, becomes knowledge of the investors that the information and statements in the future tense are subject to various risks and uncertain events, which are difficult to predict and are generally beyond the control of PINFRA, and they may cause actual results and performance to differ materially from those expressed uninvolved or designed by information and statements in the future tense. These risks and uncertain events include, without limitation, that included in...

PINFRA assumes no responsibility regarding the public update of their statements or information in future time, whether as a result of new information, future events or any other circumstance.

RESULTS Fourth Quarter Audited , 2013

12

www.pinfra.com.mx (55) 2789 0200

INDEPENDENT ANALYST

Promotora y Operadora de Infraestructura, S.A.B. de C.V., advises that in order to comply with

provisions of regulation within the BMV in the 4.033.01 Article Fracc. VIII in respect of

maintenance requirements, declare that we do not require independent analyst, in virtue of

which follow us financial institutions below, and give coverage analysis to our action.

BBVA Bancomer

Lic. Francisco Chávez Martínez

Tel. 5621 9703 y 5621 9404

Mail: [email protected]

Credit Suisse Institución de Banca Múltiple

Lic. Eugenio Amador

Tel. 5283 89 69

Mail: [email protected]

JP Morgan

Sr. Fernando Abdalla

Tel. 00 (55 11) 4950 34 63

Mail: [email protected]

Grupo Financiero Interacciones

Sr. Heber Marvin Longhurst Leany

Tel. 5326-8600 ext. 6162

Mail: [email protected]

Ixe

Lic. Josè Espitia

Tel. 5004 51 44

Mail: [email protected]

Banco Ve por Más

Lic. Marco Mèdina Zaragoza

Tel. 5625 15 00 x 1453

Mail: [email protected]

RESULTS Fourth Quarter Audited , 2013

13

www.pinfra.com.mx (55) 2789 0200

GBM Grupo Bursátil Mexicano

Lic. Javier Gayol

Tel. 5480 58 00 x 4563

Mail: [email protected]

Vector Casa de Bolsa

Lic. Hugo Mendoza

Tel. 5262 36 08 x 3255

Mail: [email protected]

Itaú BBA

Equity Research Transportation

Sr. Renato Salomone

Tel. 5262 0674

Mail: [email protected]

RESULTS Fourth Quarter Audited , 2013

14

www.pinfra.com.mx (55) 2789 0200

FINANCIAL STATEMENT COMPLEMENTARY NOTES

Promotora y Operadora de Infraestructura, S. A. B. de C. V. and

Subsidiaries

Notes to Consolidated Financial Statements For the years ended December 31, 2013 and 2012

(In thousands of Mexican pesos)

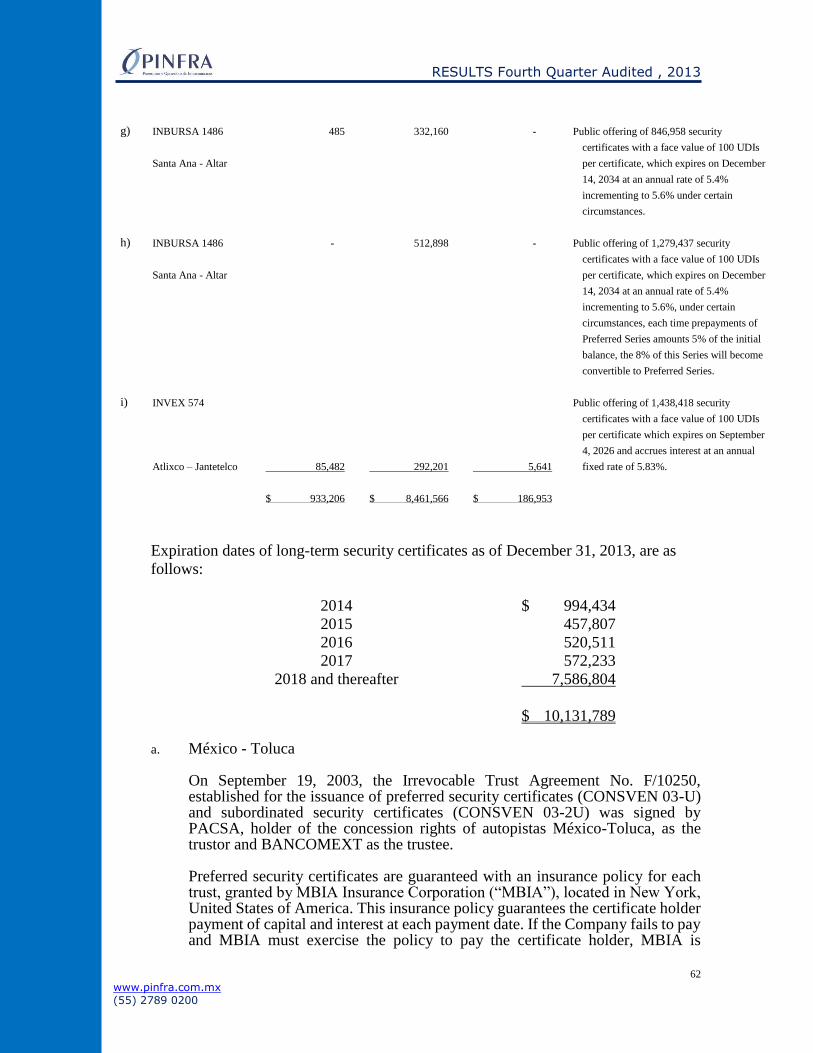

1. Nature of business Promotora y Operadora de Infraestructura, S. A. B. de C. V. and Subsidiaries (collectively, the Company) are engaged in the use and operation of concessions, related to highways, ports and other types of concessions. The Company also obtains revenues from the sale of asphalt mix and aggregates (crushed basalt) mainly used for asphalt layers, and the construction of engineering works projects. The Company is incorporated in Mexico City and its address is Bosque de Ciruelos 130, Col. Bosques de las Lomas, 11700 México D. F.

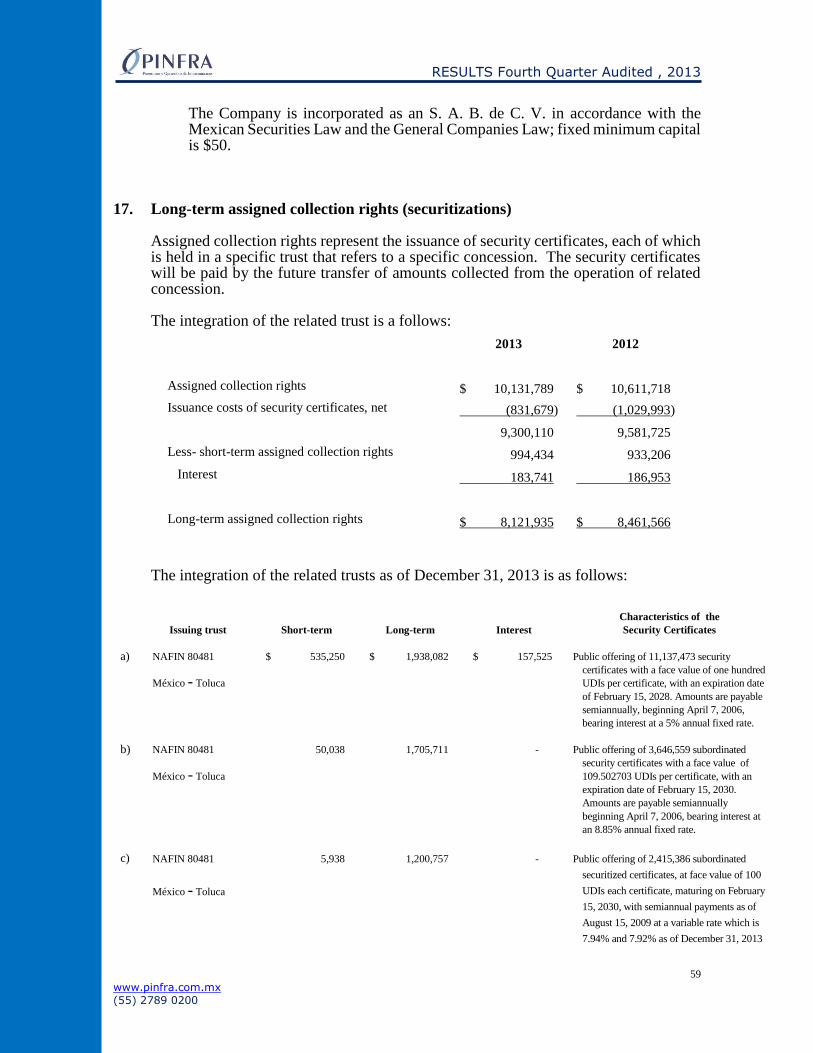

2. Significant events The relevant events in the period are as follows:

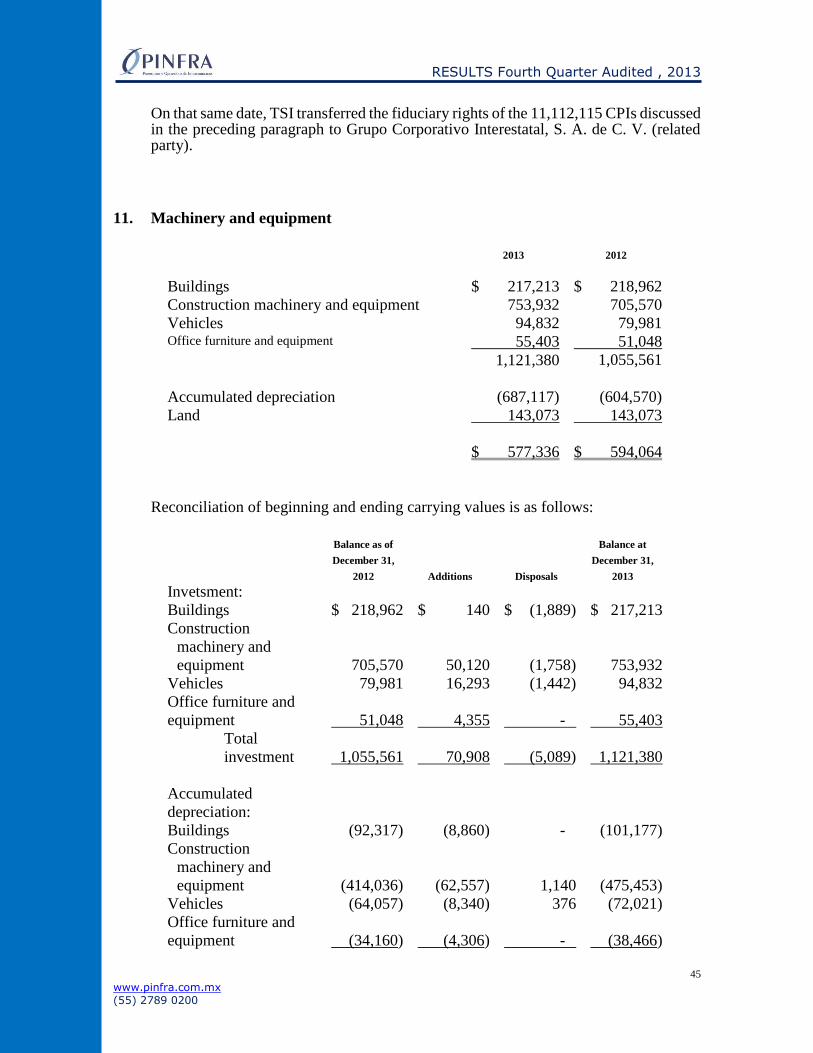

a. Siglo XXI concession acquisition On November 28, 2013, the Company together with a consortium of investors, won a bid for the construction, operation and maintenance for 30 years of Jantetelco – El Higuerón highway (Siglo XXI) with a length of 61.8 kilometers and an investment of $2,885,000 and a grant from the National investment Fund (Fondo Nacional de Inversión, FONADIN) of approximately $723,000. The Company is a partner with 51% of Empresa Concesionaria de Autopistas de Morelos, S. A. de C. V., which is included in investment in shares of associated companies and joint ventures. On December 18, 2013, Empresa Concesionaria de Autopistas de Morelos, S. A. de C. V. obtained the concession and on the same date, the Company made a contribution to the joint venture of $135,424.

b. Paquete Michoacán Acquisition

On December 16, 2011, the Company, together with a consortium of investors, won a bid for the construction and operation, during 30 years, of the Morelia and

RESULTS Fourth Quarter Audited , 2013

15

www.pinfra.com.mx (55) 2789 0200

Uruapan beltways and the Pátzcuaro-Uruapan-Lázaro Cardenas highway (Paquete Michoacán). The Paquete Michoacán concession was executed on March 30, 2012. The Company is a partner in the consortium, owning 25.2% of Concesionaria de Autopistas de Michoacán, S. A. de C. V., Operadora de Autopistas de Michoacán. S. A. P. I. de C. V. and Constructora de Autopistas de Michoacán, S. A. de C. V. (collectively, Paquete Michoacán), such investment is accounted as an investment in associated companies. As part of its participation in the concession, the Company paid a guarantee deposit as of December 31, 2013 and 2012, through a letter of credit, for $243,703, which has been recognized within other assets line item in the balance sheet. The resources of this letter of credit will be released until the Company obtain the respective rights and start the construction.

c. Modification of concession contracts Peñón - Texcoco - On July 5, 2013, the Company obtained the 4th amendment to the concession of the Peñón - Texcoco road, whose concessionary is Concesionaria Pac, S. A. de C. V. (CPAC, subsidiary company), in order to authorize the Company's construction of improvements or interconnection on local or federal highways or other investments. The Company may obtain a compounded annual real rate of return of 10.47% on these investments from tolls, if they are funded from the surplus revenues of the Peñón – Texcoco highway. According to this amendment, the actual investment under this scheme by $115,000 have been approved for the repair of a damaged expansion subsection of highway Tenango - Ixtapan de la Sal, in the State of Mexico. Also, the concession title allows extending the concession maturity of Peñón - Texcoco up to 30 years more or that which is necessary, not exceeding the maximum term provided by law which is on March 18, 2053 for the concessionaire to recover the investment made along with the corresponding return. México-Toluca - On May 31, 2012, the Company was granted with the 7th amendment to the concession title held by Promotora y Administradora de Carreteras, S. A. de C. V. (PACSA, subsidiary company), which authorizes the Company to make improvements or provide for construction of interconnections on federal highways. The Company is entitled to an internal rate of return of 12% on these investments from tolls charged on the related infrastructure, provided that it does not affect other financial creditors and trustees of the issuing trust for the Mexico - Toluca highway. Based on the terms of this amendment, as of December 31, 2013 and 2012 the Company has been authorized investment under this scheme of $2,397,500 and $1,220,000, among which are the extension of the tollbooths of Reforma-Constituyentes-Lilas in Mexico City, upgrading of Chalco-Nepantla highway, among others. Also, on August 31, 2012, term was extended for the concession of the Mexico-Toluca up to July 4, 2030, which, as of that date it will have covered the financial obligations of the concession. On July 23, 2013, the Company was granted with the 9th amendment to the concession title for the Mexico-Toluca high way, held with Promotora y Administradora de Carreteras, S. A. de C. V. (PACSA, subsidiary company), which authorizes the Company investments for the construction of La Marquesa – Lerma de Villada road by around $3,500,000 appoximately. The Company may obtain a compounded annual real rate of return of 12% on these investments from

RESULTS Fourth Quarter Audited , 2013

16

www.pinfra.com.mx (55) 2789 0200

tolls, provided that the existing financial creditors are not affected highway Mexico - Toluca.

d. Prepayment of Security Certificates of Zonalta On June 11, 2012, in a General Assembly of Holders of the Securities, it was approved the partial prepayment of the Securities (ZonalCB 06U) of Concesionaria Zonalta, S. A. de C. V. (Zonalta) for $389,900 and $10,100 provided for major maintenance, with a remaining debt of $1,616,900. This aims to strengthen the debt profile. On June 19, 2012, the Technical Committee signed the Amended Trust No. F/1486 previously authorized by the Secretary of Communications and Transportation ("SCT"), in which the exchange took place of ZonalCB 06U Securities dividing the debt in three series with different characteristics. The redemption of the Securities was as follows:

1. A preferred series for an amount equivalent to 50% of the debt for

211,739,500 IDUs ("Preferred Series "), maturing on December 14, 2033 at a real interest rate of 5.40%, gradually incrementing to 5.60%, if they are not totally paid by December 14, 2031. Principal is payable at maturity but there is a semiannual prepayment option. Interest is paid semiannually.

2. A subordinated series ("Subordinated Series") for an amount equivalent to 20% of the debt for 84,695,800 IDUs at a real interest rate of 5.40% until December 14, 2031, after this date it will be gradually increased to 5.60% until the date of settlement of debt which matures on December 14, 2034. Once the Preferred Series has been fully paid and if there is a surplus of cash, the Subordinated series will be paid in advance, to the extent of the available resources. This series will be paid at maturity regardless the option of prepayment exists. Interests are paid semiannually, if there were sufficient resources.

3. A convertible series to Preferred Series ("Convertible Series ") for an amount equivalent to 30% of the debt which amounts to 127,043,700 UDIs at a real interest rate of 5.40% until December 4, 2031, after this date it will be gradually increased to 5.60% up to the date of settlement of the debt. Each time the

accumulated prepayments of the Preferred Series is up to 5% of the beginning balance of the debt, 8% of the Securities Series will be converted to Preferred Series.

The issued series are Series 06U Series, Series 06-2U and Series 06-3U, respectively. The Company determined that the terms of the Securities were not substantially modified; and therefore, the change was not recognized as a settlement of debt. This update of the Securities did not generate nor required cash flows.

e. Construction of road sections on Sonora SCT authorized the Company an amount up to $400,000 for the work of the extension from two to four lanes of the "Altar-Pitiquito" road, which is

RESULTS Fourth Quarter Audited , 2013

17

www.pinfra.com.mx (55) 2789 0200

concessioned to the Company and the extension from two to four lanes of Pitiquito - Caborca road; both are located in the State of Sonora. The Company has incurred construction in progress of $382,130 and $8,500 as of December 31, 2013 and 2012, respectively.

f. Public offering of equity On October 4, 2012, the Company made a national and international public offering of its shares for $1,365,733 with a price of $63 Mexican pesos per share through the Mexican Stock Exchange. Therefore 21,678,314 shares, ordinary, nominative, without par value were subscribed, including 375,014 shares acquired by the Company under the repurchase of shares line item. This issuance was recorded as an increase in stockholders' equity, net of issuance expenses of $83,880. At the same time, there was a secondary offering of $3,068,995. The Company did not receive funds as a result of the secondary portion of the offer.

g. Acquisition of the “Paquete Puebla” concession On December 7, 2012, the Company, through its subsidiary PAPSA, obtained the concession to operate and maintain the roads "Via Atlixcáyotl", "Virreyes-Teziutlan" and "Apizaco-Huauchinango" with a total length of 142 km (collectively, the "Paquete Puebla"). The concession expiration is for 30 years. The initial consideration was $2,150,008 and a regular consideration consisting of a variable portion based on the fulfillment of certain appraisals and a fixed portion of the 1% of the toll fees, payable annually. In addition, expenses were spent on obtaining the concession totaling $290,600 that have been capitalized along with the value of the initial consideration. At the same time, three trusts were created to ensure the deposit of toll fees and to establish the priority of payments for the operation and maintenance of the concession.

h. Increased concession period in Port Concession On August 24, 2012, the Mexican subsidiary Infraestructura Portuaria Mexicana, S. A. de C. V. obtained an extension to the concession title for a period of 20 years effective June 20, 2016 (date of expiration of the original contract).

i. Reduction of common stock During the year ended December 31, 2012, nominal common stock was reduced by $3,442, through a redemption of 1,807,100 of the Company´s shares. These shares were previously repurchased shares, which had been held by the Company for over a year without having been offered again to public investors. The spread between the reacquisition value of the shares and their par value, of $84,460, was charged against the reserve for share acquisition, which is maintained for the repurchase and retirement of shares.

RESULTS Fourth Quarter Audited , 2013

18

www.pinfra.com.mx (55) 2789 0200

j. Current status of Mexicana de Gestión de Agua, S. A. de C. V. (MGA)

concession A contract, dated December 4, 1996, was executed between MGA, a subsidiary of the Company, and the Board of Directors of the Municipal Operating Agency for Potable Water, Drains and Sanitation of Navojoa, Sonora (the “Municipality”), whereby MGA was to provide operational, preservation and maintenance services related to drinking water as well as the sewage system and the sanitation system of Navojoa Sonora. During September 2005, the Municipality filed an administrative legal proceeding to rescind the aforementioned services contract upon claims of noncompliance. The outcome of the proceeding also required the immediate delivery of the physical and financial administration of the potable water public system to the Municipality, including the physical possession of all assets used to render the services and any accounting, monetary or other rights that form part of the administration of the potable water system. MGA filed protection (seeking court relief on constitutional grounds) against the ruling issued, which ultimately granted relief to MGA and requires the Municipality to provide immediate delivery of the water service operation. After various legal proceedings, the Municipality has returned wells, operating equipment and certain real estate subject of the original contract, but has not turned over the entire operation. However the constant requirements by MGA and juridical authority following the default of the file protection by the operator, seventh district Judge of Sonora state promoted an incident of non-compliance of the judgment. The handling of this incident is aimed to make the operator meets the purposes of the filled protection granted to MGA and return the operation of water supply systems and waste water. At the date of these consolidated financial statements, Navojoa municipality of Sonora state and the Company, are in the process of negotiating the value of assets to be returned.

3. Basis of presentation

a. Explanation for translation into English

The accompanying consolidated financial statements have been translated from Spanish into English for use outside of Mexico. These consolidated financial statements are presented on the basis of International Financial Reporting Standards (“IFRS”). Certain accounting practices applied by the Company that conform with IFRS may not conform with accounting principles generally accepted in the country of use.

b. New and revised IFRSs affecting amounts reported and/or disclosures in the financial statements

In the current year, the Company has applied a number of new and revised IFRSs issued by the International Accounting Standards Board (IASB) that are

RESULTS Fourth Quarter Audited , 2013

19

www.pinfra.com.mx (55) 2789 0200

mandatorily effective for an accounting period that begins on or after January 1, 2013. Amendments to IFRS 7 Disclosures – Offsetting Financial Assets and Financial Liabilities The Company has applied the amendments to IFRS 7 Disclosures – Offsetting Financial Assets and Financial Liabilities for the first time in the current year. The amendments to IFRS 7 require entities to disclose information about rights of offset and related arrangements (such as collateral posting requirements) for financial instruments under an enforceable master netting agreement or similar arrangement. The amendments to the IFRS 7, have been applied retrospectively. As the Company does not have any offsetting arrangements in place, the application of the amendments has had no material impact on the disclosures or on the amounts recognized in the consolidated financial statements. New and revised Standards on consolidation, joint arrangements, associates and disclosures In May 2011, a package of five standards on consolidation, joint arrangements, associates and disclosures was issued comprising IFRS 10 Consolidated Financial Statements, IFRS 11 Joint Arrangements, IFRS 12 Disclosure of Interests in Other Entities, IAS 27 (as revised in 2011) Separate Financial Statements and IAS 28 (as revised in 2011) Investments in Associates and Joint Ventures. Subsequent to the issue of these standards, amendments to IFRS 10, IFRS 11 and IFRS 12 were issued to clarify certain transitional guidance on the first-time application of the standards. In the current year, the Company has applied for the first time IFRS 10, IFRS 11, IFRS 12 and IAS 28 (as revised in 2011) together with the amendments to IFRS 10, IFRS 11 and IFRS 12 regarding the transitional guidance. IAS 27 (as revised in 2011) is not applicable to the Company as it deals only with separate financial statements. IFRS 10 IFRS 10 replaces the parts of IAS 27 Consolidated and Separate Financial Statements that deal with consolidated financial statements and SIC-12 Consolidation – Special Purpose Entities. IFRS 10 changes the definition of control such that an investor has control over an investee when a) it has power over the investee, b) it is exposed, or has rights, to variable returns from its involvement with the investee and c) has the ability to use its power to affect its returns. All three of these criteria must be met for an investor to have control over an investee. Previously, control was defined as the power to govern the financial and operating policies of an entity so as to obtain benefits from its activities. Additional guidance has been included in IFRS 10 to explain when an investor has control over an investee. Some guidance included in IFRS 10 that deals with whether or not an investor that owns less than 50% of the voting rights in an investee has control over the investee is relevant to the Company. IFRS 11 IFRS 11 replaces IAS 31 Interests in Joint Ventures, and the guidance contained in a related interpretation, SIC-13 Jointly Controlled Entities – Non-Monetary

RESULTS Fourth Quarter Audited , 2013

20

www.pinfra.com.mx (55) 2789 0200

Contributions by Venturers, has been incorporated in IAS 28 (as revised in 2011). IFRS 11 deals with how a joint arrangement of which two or more parties have joint control should be classified and accounted for. Under IFRS 11, there are only two types of joint arrangements – joint operations and joint ventures. The classification of joint arrangements under IFRS 11 is determined based on the rights and obligations of parties to the joint arrangements by considering the structure, the legal form of the arrangements, the contractual terms agreed by the parties to the arrangement, and, when relevant, other facts and circumstances. A joint operation is a joint arrangement whereby the parties that have joint control of the arrangement (i.e. joint operators) have rights to the assets, and obligations for the liabilities, relating to the arrangement. A joint venture is a joint arrangement whereby the parties that have joint control of the arrangement (i.e. joint ventures) have rights to the net assets of the arrangement. Previously, IAS 31 contemplated three types of joint arrangements – jointly controlled entities, jointly controlled operations and jointly controlled assets. The classification of joint arrangements under IAS 31 was primarily determined based on the legal form of the arrangement (e.g. a joint arrangement that was established through a separate entity was accounted for as a jointly controlled entity). The initial and subsequent accounting of joint ventures and joint operations is different. Investments in joint ventures are accounted for using the equity method (proportionate consolidation is no longer allowed). Investments in joint operations are accounted for such that each joint operator recognizes its assets (including its share of any assets jointly held), its liabilities (including its share of any liabilities incurred jointly), its revenue (including its share of revenue from the sale of the output by the joint operation) and its expenses (including its share of any expenses incurred jointly). Each joint operator accounts for the assets and liabilities, as well as revenues and expenses, relating to its interest in the joint operation in accordance with the applicable Standards. The Company’s management reviewed and assessed the classification of the Company's investments in joint arrangements in accordance with the requirements of IFRS 11. The Company’s management concluded that the Company’s investment in Proyecto Michoacán, Concesionaria Purépecha, S. A. de C. V., Purépecha, Posco Mesdc, S. A. de C. V. (Posco), y Construcciones y Drenajes Profundos, S. A. de C. V. (Drenajes Profundos), was classified as a joint venture under IFRS 11 and accounted for using the equity method. IFRS 12 IFRS 12 is a new disclosure standard and is applicable to entities that have interests in subsidiaries, joint arrangements, associates and/or unconsolidated structured entities. In general, the application of IFRS 12 has resulted in more extensive disclosures in the consolidated financial statements (please see notes 4d and 13 for details). IFRS 13 Fair Value Measurement The Company has applied IFRS 13 for the first time in the current year. IFRS 13 establishes a single source of guidance for fair value measurements and disclosures about fair value measurements. The scope of IFRS 13 is broad; the fair value measurement requirements of IFRS 13 apply to both financial instrument items and non-financial instrument items for which other IFRSs require or permit fair value measurements and disclosures about fair value measurements, except for share-based payment transactions that are within the

RESULTS Fourth Quarter Audited , 2013

21

www.pinfra.com.mx (55) 2789 0200

scope of IFRS 2 Share-based Payment, leasing transactions that are within the scope of IAS 17 Leases, and measurements that have some similarities to fair value but are not fair value (e.g. net realizable value for the purposes of measuring inventories or value in use for impairment assessment purposes). IFRS 13 defines fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction in the principal (or most advantageous) market at the measurement date under current market conditions. Fair value under IFRS 13 is an exit price regardless of whether that price is directly observable or estimated using another valuation technique. Also, IFRS 13 includes extensive disclosure requirements. IFRS 13 requires prospective application from January 1, 2013. In addition, specific transitional provisions were given to entities such that they need not apply the disclosure requirements set out in the Standard in comparative information provided for periods before the initial application of the Standard. Amendments to IAS 1 Presentation of Items of Other Comprehensive Income The Company has applied the amendments to IAS 1 Presentation of Items of Other Comprehensive Income for the first time in the current year. The amendments introduce new terminology, whose use is not mandatory, for the statement of comprehensive income and income statement. Under the amendments to IAS 1, the ‘statement of comprehensive income’ is renamed as the ‘statement of profit or loss and other comprehensive income’ and the ‘income statement’ is renamed as the ‘statement of profit or loss’. The amendments to IAS 1 retain the option to present profit or loss and other comprehensive income in either a single statement or in two separate but consecutive statements. However, the amendments to IAS 1 require items of other comprehensive income to be grouped into two categories in the other comprehensive income section: (a) items that will not be reclassified subsequently to profit or loss and (b) items that may be reclassified subsequently to profit or loss when specific conditions are met. Income tax on items of other comprehensive income is required to be allocated on the same basis – the amendments do not change the option to present items of other comprehensive income either before tax or net of tax. The application of the amendments to IAS 1 does not result in any impact on profit or loss, other comprehensive income and total comprehensive income. IAS 19 Employee Benefits (as revised in 2011) In the current year, the Company has applied IAS 19 Employee Benefits (as revised in 2011) and the related consequential amendments for the first time. IAS 19 (as revised in 2011) changes the accounting for defined benefit plans and termination benefits. The most significant change relates to the accounting for changes in defined benefit obligations and plan assets. The amendments require the recognition of changes in defined benefit obligations and in the fair value of plan assets when they occur, and hence eliminate the ‘corridor approach’ permitted under the previous version of IAS 19 and accelerate the recognition of past service costs. All actuarial gains and losses are recognized immediately through other comprehensive income in order for the net pension asset or liability recognized in the consolidated statement of financial position to reflect the full value of the plan deficit or surplus. Furthermore, the interest cost and expected return on plan assets used in the previous version of IAS 19 are replaced with a ‘net interest’ amount under IAS 19 (as revised in 2011), which is calculated by applying the discount rate to the net defined benefit liability or asset. These changes have had an impact on the amounts recognized in profit or loss and other comprehensive income in prior years (see the tables below for details). In

RESULTS Fourth Quarter Audited , 2013

22

www.pinfra.com.mx (55) 2789 0200

addition, IAS 19 (as revised in 2011) introduces certain changes in the presentation of the defined benefit cost including more extensive disclosures.

c. New and revised IFRSs in issue but not yet effective

The Company has not applied the following new and revised IFRSs that have been issued but are not yet effective:

IFRS 9 Financial Instruments3 Amendments to IFRS 9 and IFRS 7 Mandatory Effective Date of IFRS 9 and

Transition Disclosures² Amendments to IFRS 10, IFRS 12 and IAS 27 Investment Entities¹ Amendments to IAS 32 Offsetting Financial Assets and Financial

Liabilities¹ ¹ Effective for annual periods beginning on or after January 1, 2014, with earlier application permitted. ² Effective for annual periods beginning on or after January 1, 2015, with earlier application permitted. 3 Effective for annual periods beginning on or after January 1, 2016, with earlier application permitted. IFRS 9 Financial Instruments IFRS 9, issued in November 2009, introduced new requirements for the classification and measurement of financial assets. IFRS 9 was amended in October 2010 to include requirements for the classification and measurement of financial liabilities and for derecognition. Key requirements of IFRS 9: All recognized financial assets that are within the scope of IAS 39

Financial Instruments: Recognition and Measurement are required to be subsequently measured at amortized cost or fair value. Specifically, debt investments that are held within a business model whose objective is to collect the contractual cash flows, and which have contractual cash flows that are solely payments of principal and interest on the principal outstanding balance is generally measured at amortized cost at the end of the subsequent accounting periods. All other debt investments and equity investments are measured at their fair value at the end of subsequent accounting periods. In addition, under IFRS 9, entities may make an irrevocable election to present subsequent changes in the fair value of an equity investment (that is not held for trading) in other comprehensive income, with only dividend income generally recognized in consolidated net income.

With regard to the measurement of financial liabilities designated as of fair

value through profit or loss, IFRS 9 requires that the amount of change in the fair value of the financial liability that is attributable to changes in the credit risk of that liability is presented in other comprehensive income, unless the recognition of the effects of changes in the liability’s credit risk in other comprehensive income would create or enlarge an accounting mismatch in profit or loss. Changes in fair value attributable to a financial liability’s credit risk are not subsequently reclassified to profit or loss. Under IAS 39, the entire amount of the change in the fair value of the financial liability designated as fair value through profit or loss is presented in profit or loss.

RESULTS Fourth Quarter Audited , 2013

23

www.pinfra.com.mx (55) 2789 0200

The Company’s management anticipate that the application of IFRS 9 in the future may have a significant impact on amounts reported in respect of the Company’s financial assets and financial liabilities. However, it is not practicable to provide a reasonable estimate of the effect of IFRS 9 until a detailed review has been completed. Amendments to IFRS 10, IFRS 12 and IAS 27 Investment Entities The amendments to IFRS 10 define an investment entity and require a reporting entity that meets the definition of an investment entity not to consolidate its subsidiaries but instead to measure its subsidiaries at fair value through profit or loss in its consolidated and separate financial statements. To qualify as an investment entity, a reporting entity is required to: Obtain funds from one or more investors for the purpose of providing them

with professional investment management services. Commit to its investor(s) that its business purpose is to invest funds solely

for returns from capital appreciation, investment income, or both. Measure and evaluate performance of substantially all of its investments

on a fair value basis. The Company’s management does not anticipate that the investment entities amendments will have any effect on the consolidated financial statements as the Company is not an investment entity. Amendments to IAS 32 Offsetting Financial Assets and Financial Liabilities The amendments to IAS 32 clarify the requirements relating to the offset of financial assets and financial liabilities. Specifically, the amendments clarify the meaning of ‘currently has a legally enforceable right of set-off’ and ‘simultaneous realization and settlement’. The Company’s management does not anticipate that the application of these amendments to IAS 32 will have a significant impact on the consolidated financial statements as the Company does not have any financial assets and financial liabilities that qualify for offset.

4. Summary of significant accounting policies

a. Statement of compliance The consolidated financial statements of the Company have been prepared in

accordance with International Financial Reporting Standards (IFRS, for its

acronym in English) and its adaptations and interpretations issued by the

International Accounting Standards Board (IASB, for its acronym in English), in

effect as of December 31, 2013. The accompanying consolidated financial

statements have been prepared in conformity with the IFRS issued by the IASB,

which require that management make certain estimates and use certain

assumptions that affect the amounts reported in the financial statements and their

related disclosures; however, actual results may differ from such estimates. The

RESULTS Fourth Quarter Audited , 2013

24

www.pinfra.com.mx (55) 2789 0200

Company’s management, upon applying professional judgment, considers that

estimates made and assumptions used were adequate under the circumstances.

The significant accounting policies of the Company are as follows:

b. Historical cost

The consolidated financial statements have been prepared on an historical cost

basis except for certain financial instruments, which are valued at fair value.

i. Historical cost

Historical cost is generally based on the fair value of the consideration given in exchange for goods and services.

ii. Fair value

Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date, regardless of whether that price is directly observable or estimated using another valuation technique. In estimating the fair value of an asset or a liability, the Company takes into account the characteristics of the asset or liability if market participants would take those characteristics into account when pricing the asset or liability at the measurement date. Fair value for measurement and/or disclosure purposes in these consolidated financial statements is determined on such a basis, except for share-based payment transactions that are within the scope of IFRS 2, leasing transactions that are within the scope of IAS 17, and measurements that have some similarities to fair value but are not fair value, such as net realizable value in IAS 2 or value in use in IAS 36. In addition, for financial reporting purposes, fair value measurements are categorized into Level 1, 2 or 3 based on the degree to which the inputs to the fair value measurements are observable and the significance of the inputs to the fair value measurement in its entirety, which are described as follows:

Level 1 inputs are quoted prices (unadjusted) in active markets for

identical assets or liabilities that the entity can access at the measurement date;

Level 2 inputs are inputs, other than quoted prices included within Level 1, that are observable for the asset or liability, either directly or indirectly; and

Level 3 inputs are unobservable inputs for the asset or liability.

c. Basis of consolidation The consolidated financial statements incorporate the financial statements of the Promotora y Operadora de Infraestructura, S. A. B. de C. V. and its subsidiaries controlled by it. Control is achieved when the Company: Has power over the investee; Is exposed, or has rights, to variable returns from its involvement with the

investee; and Has the ability to use its power to affect its returns. The Company reassesses whether or not it controls an investee if facts and circumstances indicate that there are changes to one or more of the three elements

RESULTS Fourth Quarter Audited , 2013

25

www.pinfra.com.mx (55) 2789 0200

of control listed above. When the Company has less than a majority of the voting rights of an investee, it has power over the investee when the voting rights are sufficient to give it the practical ability to direct the relevant activities of the investee unilaterally. The Company considers all relevant facts and circumstances in assessing whether or not the Company’s voting rights in an investee are sufficient to give it power, including: The size of the Company holding of voting rights relative to the size and

dispersion of holdings of the other vote holders; Potential voting rights held by the Company, other vote holders or other

parties; Rights arising from other contractual arrangements; and Any additional facts and circumstances that indicate that the Company has,

or does not have, the current ability to direct the relevant activities at the time that decisions need to be made, including voting patterns at previous shareholders’ meetings.

Consolidation of a subsidiary begins when the Company obtains control over the subsidiary and ceases when the Company loses control of the subsidiary. Specifically, income and expenses of a subsidiary acquired or disposed of during the year are included in the consolidated statement of profit or loss and other comprehensive income from the date the Company gains control until the date when the Company ceases to control the subsidiary. Net income and each component of other comprehensive income are attributed to the owners of the Company and to the non-controlling interests. Total comprehensive income of subsidiaries is attributed to the owners of the Company and to the non-controlling interests even if this results in the non-controlling interests having a deficit balance. Pinfra’s shareholding percentage in the capital stock of its main subsidiaries is shown below:

Ownership

percentage as

of

December 31, Activity

Construction sector: 2013 and 2012

Pinfra Sector Construcción,

S. A. de C. V. 100% Holding company

Experconstructores Zacatecana,

S. A. de C. V. 100% Holding company

Adepay, S. A. de C. V. 100% Holding company

Concemex, S. A. de C. V. 100%

Construction, operation and

conservation of highways

Equivent, S. A. de C. V. 100% General construction

Materials sector:

Tribasa Sector Materiales e Insumos de la

Construcción, S. A. de C. V. (1) 100% Holding company

Grupo Corporativo Interestatal,

S. A. de C. V. 100% Production of asphalt mix

Tribasa Construcciones, S. A. de

C. V. 100% General construction

Concession sector:

Grupo Concesionario de México,

S. A. de C. V. 100% Holding company

RESULTS Fourth Quarter Audited , 2013

26

www.pinfra.com.mx (55) 2789 0200

Ownership

percentage as

of

December 31, Activity

Promotora y Administradora de

Carreteras, S. A. de C. V. 100%

Construction, operation and

conservation of highways

Promotora de Autopistas del Pacífico, S.

A. de C. V. 100%

Construction, operation and

conservation of highways

Concesionaria Pac, S. A. de C. V. 100%

Construction, operation and

conservation of highways

Autopista Tenango-Ixtapan de la Sal, S. A.

de C. V. 100%

Construction, operation and

conservation of highways

Concesionaria Monarca, S. A. de

C. V. 100%

Construction, operation and

conservation of highways

Opervite, S. A. de C. V. 100% Concessioned highways operator

Concesionaria Zonalta, S. A. de

C. V. 100%

Construction, operation and

conservation of highways

Infraestructura Portuaria Mexicana, S.A.

de C. V. 100% Ports operator

Real property sector:

Tribasa Sector Inmobiliario,

S. A. de C. V. 100% Holding company and leasing property. (1) As of December 31, 2013 and 2012, Tribasa Sector Materiales e Insumos de la

Construcción, S. A. de C. V. owns 77.75% of the common stock of Mexicana de Cales, S. A. de C. V. Wich represent the noncontrolling interest on the Consolidated Statemts of Financial Position.

In addition to the above, the Company consolidates certain trusts over which it

has determined it controls.

Significant intercompany balances and transactions have been eliminated in these

consolidated financial statements.

Investment in associated companies is accounted for using the equity method.

The Company’s foreign subsidiaries comprise its investments in concessions in

Chile and Ecuador, which are in the process of liquidation and are presented as

discontinued operations.

1. Changes in the Company’s ownership interests in existing subsidiaries

Changes in the Company’s ownership interests in subsidiaries that do not result in the Company losing control over the subsidiaries are accounted for as equity transactions. The carrying amounts of the Company’s interests and the non-controlling interests are adjusted to reflect the changes in their relative interests in the subsidiaries. Any difference between the amount by which the non-controlling interests are adjusted and the fair value of the consideration paid or received is recognized directly in equity and attributed to owners of the Company. When the Company loses control of a subsidiary, a gain or loss is

recognized in profit or loss and is calculated as the difference between (i)

RESULTS Fourth Quarter Audited , 2013

27

www.pinfra.com.mx (55) 2789 0200

the aggregate of the fair value of the consideration received and the fair

value of any retained interest and (ii) the previous carrying amount of the

assets (including goodwill), and liabilities of the subsidiary and any non-

controlling interests. All amounts previously recognized in other

comprehensive income in relation to that subsidiary are accounted for as if

the Company had directly disposed of the related assets or liabilities of the

subsidiary (i.e. reclassified to profit or loss or transferred to another

category of equity as specified/permitted by applicable IFRSs). The fair

value of any investment retained in the former subsidiary at the date when

control is lost is regarded as the fair value on initial recognition for

subsequent accounting under IAS 39, when applicable, the cost on initial

recognition of an investment in an associate or a joint venture.

d. Investments in associates and joint ventures An associate is an entity over which the Company has significant influence. Significant influence is the power to participate in the financial and operating policy decisions of the investee but is not control or joint control over those policies. A joint venture is a joint arrangement whereby the parties that have joint control of the arrangement have rights to the net assets of the joint arrangement. Joint control is the contractually agreed sharing of control of an arrangement, which exists only when decisions about the relevant activities require unanimous consent of the parties sharing control. The results and assets and liabilities of associates or joint ventures are incorporated in these consolidated financial statements using the equity method of accounting, except when the investment, or a portion thereof, is classified as held for sale, in which case it is accounted for in accordance with IFRS 5. Under the equity method, an investment in an associate or a joint venture is initially recognized in the consolidated statement of financial position at cost and adjusted thereafter to recognize the Company’s share of the profit or loss and other comprehensive income of the associate or joint venture. When the Company’s share of losses of an associate or a joint venture exceeds the Company’s interest in that associate or joint venture, The Company discontinues recognizing its share of further losses. Additional losses are recognized only to the extent that the Company has incurred legal or constructive obligations or made payments on behalf of the associate or joint venture. An investment in an associate or a joint venture is accounted for using the equity method from the date on which the investee becomes an associate or a joint venture. On acquisition of the investment in an associate or a joint venture, any excess of the cost of the investment over the Company’s share of the net fair value of the identifiable assets and liabilities of the investee is recognized as goodwill, which is included within the carrying amount of the investment. Any excess of the Company’s share of the net fair value of the identifiable assets and liabilities over the cost of the investment, after reassessment, is recognized immediately in profit or loss in the period in which the investment is acquired. The requirements of IAS 39 are applied to determine whether it is necessary to

RESULTS Fourth Quarter Audited , 2013

28

www.pinfra.com.mx (55) 2789 0200

recognize any impairment loss with respect to the Company’s investment in an associate or a joint venture. When necessary, the entire carrying amount of the investment is tested for impairment in accordance with IAS 36 Impairment of Assets as a single asset by comparing its recoverable amount (higher of value in use and fair value less costs to sell) with its carrying amount. Any impairment loss recognized forms part of the carrying amount of the investment. Any reversal of that impairment loss is recognized in accordance with IAS 36 to the extent that the recoverable amount of the investment subsequently increases. The Company discontinues the use of the equity method from the date when the investment ceases to be an associate or a joint venture, or when the investment is classified as held for sale. When the Company retains an interest in the former associate or joint venture and the retained interest is a financial asset, the Company measures the retained interest at fair value at that date and the fair value is regarded as its fair value on initial recognition in accordance with IAS 39. The difference between the carrying amount of the associate or joint venture at the date the equity method was discontinued, and the fair value of any retained interest and any proceeds from disposing of a part interest in the associate or joint venture is included in the determination of the gain or loss on disposal of the associate or joint venture. In addition, the Company accounts for all amounts previously recognized in other comprehensive income in relation to that associate or joint venture on the same basis as would be required if that associate or joint venture had directly disposed of the related assets or liabilities. Therefore, if a gain or loss previously recognized in other comprehensive income by that associate or joint venture would be reclassified to profit or loss on the disposal of the related assets or liabilities, the Company reclassifies the gain or loss from equity to profit or loss when the equity method is discontinued.

The Company continues to use the equity method when an investment in an

associate becomes an investment in a joint venture or an investment in a joint

venture becomes an investment in an associate. There is no remeasurement to

fair value upon such changes in ownership interests.

When the Company reduces its ownership interest in an associate or a joint

venture but the Company continues to use the equity method, the Company

reclassifies to profit or loss the proportion of the gain or loss that had previously

been recognized in other comprehensive income relating to that reduction in

ownership interest if that gain or loss would be reclassified to profit or loss on

the disposal of the related assets or liabilities.

When a group entity transacts with an associate or a joint venture of the

Company, profits and losses resulting from the transactions with the associate or

joint venture are recognized in the Company’s consolidated financial statements

only to the extent of interests in the associate or joint venture that are not related

to the Company.

e. Classification of costs and expenses – Costs and expenses were classified

according to their function because this is the practice of the sector to which the

Company belongs

RESULTS Fourth Quarter Audited , 2013

29

www.pinfra.com.mx (55) 2789 0200

f. Recognition of the effects of inflation - Inflation is recognized only when

cumulative inflation rate for the past three fiscal years approaches or exceeds

100%, for example in hyperinflationary economies. The Mexican economy has

not been considered hyperinflationary since 1999.

g. Leasing- Leases are classified as finance leases whenever the terms of the lease

transfer substantially all the risks and rewards of ownership to the lessee. All

other leases are classified as operating leases.

i. The Company as lessor

Rental income from operating leases is recognized on a straight-line basis

over the term of the relevant lease. Initial direct costs incurred in

negotiating and arranging an operating lease are added to the carrying

amount of the leased asset and recognized on a straight-line basis over the

lease term.

ii. The Company as lessee

Operating lease payments are recognized as an expense on a straight-line basis over the lease term, except where another systematic basis is more representative of the time pattern in which economic benefits from the leased asset are consumed. Contingent rentals arising under operating leases are recognized as an expense in the period in which they are incurred.

h. Translation of financial statements of foreign subsidiaries - To consolidate

financial statements of foreign subsidiaries, they are modified using the currency

in which translations are recorder to appear under IFRSs the financial statements

are subsequently translated into Mexican pesos considering the following

methodology:

Foreign operations whose recording and functional currency is the same they

convert their financial statements using the following exchange rates: 1) the

closing date currency for assets and liabilities and 2) historical currency for

equity and 3) the rate on the date of accrual for revenues, costs and expenses. In

2013 and 2012, there were no significant effects of conversion.

i. Cash and cash equivalents - Cash consists mainly of bank deposits in checking

accounts. Cash equivalents are short-term investments, highly liquid and easily

convertible into cash, maturing within three months as of their acquisition date,

and which are subject to insignificant changes in value. Cash is stated at nominal

value and cash equivalents are valued at fair value.

j. Restricted Trust Funds - Represents reserve funds required to ensure coverage and

interest payments and capital expenditures assigned collection rights.

RESULTS Fourth Quarter Audited , 2013

30

www.pinfra.com.mx (55) 2789 0200

k. Financial assets - Financial assets are initially measured at fair value, plus

transaction costs, except for those financial assets classified as fair value through

profit or loss, which are initially valued at fair value. Subsequent valuation

depends on the category in which they are classified.

Note 16 describes the categories of financial assets the Company maintains.

i). Classification of financial assets

Financial assets are classified into the following specified categories:

financial assets ‘at fair value through profit or loss', ‘held-to-maturity'

investments, ‘available-for-sale' financial assets and ‘loans and

receivables'. The classification depends on the nature and purpose of the

financial assets and is determined at the time of initial recognition.

ii). At fair value through profit or loss

Financial assets are classified as at fair value through profit or loss when

the financial asset is either held for trading or it is designated as at fair value

through profit or loss.

A financial asset is classified as held for trading if:

- It has been acquired principally for the purpose of selling it in the

near term; or

- on initial recognition it is part of a portfolio of identified financial

instruments that the Company manages together and has a recent

actual pattern of short-term profit-taking; or

- I

t is a derivative that is not designated and effective as a hedging

instrument.

The Company classifies instruments held for trading purposes as short-

term, except when there are restrictions on the use of the funds invested for

at least the 12 months following the date of the statement of financial

position.

The Company has not designated any financial assets as at fair value

through profit or loss

Financial assets at fair value through profit or loss are stated at fair value,

with any gains or losses arising on remeasurement recognized in profit or

loss. The net gain or loss recognized in profit or loss incorporates any

dividend or interest earned on the financial asset Fair value is determined

in the manner described in Note 16.

RESULTS Fourth Quarter Audited , 2013

31

www.pinfra.com.mx (55) 2789 0200

iii). Investments held-to-maturity Held-to-maturity investments are non-derivative financial assets with fixed

or determinable payments and fixed maturity dates that the Company has

the positive intent and ability to hold to maturity. Subsequent to initial

recognition, held-to-maturity investments are measured at amortized cost

using the effective interest method less any impairment.