discussion paper 45 - university college cork · pdf filethere are many factors that are...

TRANSCRIPT

Department of Food Business and Development

Discussion Paper Series

Conjoint analysis as a market-oriented new product design tool: the case of

functional meal replacement beverages

By

Joe Bogue, Alex Hofler and Douglas Sorenson

Agribusiness Discussion Paper No. 45

April 2005

Department of Food Business and Development

University College, Cork

Ireland

Ollscoil na hÉireann, Corcaigh - National University of Ireland, Cork

2

TABLE OF CONTENTS

PAGE

Abstract 4

SECTION I: INTRODUCTION 1.1 Functional Beverages: Meal Replacements 5

1.1.1 Key Drivers of Meal Replacements for On-the-Go Consumption 6

1.1.2 NPD Activity in the Meal Replacement Category 6

1.2 Market-oriented NPD 7

1.2.1 Market-oriented NPD Process 8

1.3 Product Design: Foods On-the-Go 9

1.4 Conjoint Analysis 10

SECTION II: RESEARCH OBJECTIVES AND METHODOLOGY 2.1 Research Objectives 11

2.2 Methodology 11

2.3 Interviews 11

2.4 Conjoint Experimental Design 12

2.4.1 Conjoint Questionnaire 13

2.4.2 Data Analysis 13

2.4.3 Validity of the Conjoint Model 14

SECTION III: RESULTS AND ANALYSIS 3.1 Results of the Interviews 14

3.1.1 Consumer Profiles 14

3.1.2 Breakfast Eating Habits 14

3.1.3 Eating On-the-Go 16

3.1.4 Meal Replacement Beverages 18

3.2 Results of the Conjoint Questionnaires 20

3.2.1 Eating Habits and Travel Patterns 21

3.2.2 Results of Conjoint Analysis 22

3.2.3 Cluster Analysis 24

3.2.4 Cluster Preferences and Socio-demographic Profiles 25

3.2.5 Simulations 27

3

SECTION IV: RESEARCH CONCLUSIONS AND RECOMMENDATIONS 4.1 Meal Replacement: Meeting the Challenges of Consumer Demands 30

4.2 Qualitative Consumer Research 30

4.3 Segmentation and Product Design 31

4.4 Premium Pricing Strategies for a Functional Product 32

4.5 Positioning Strategies and Communication 33

4.6 The Importance of Market Research in NPD 33

4.7 Research Recommendations 34

4.8 Suggestions for Further Research 34

References 35

Appendix A 39

Appendix B 46

Appendix C 61

Appendix D 62

4

Conjoint analysis as a market-oriented new product design tool: the case of

functional meal replacement beverages1

1 This research was funded by the Department of Agriculture and Food under the National Development Plan, 2000-2006, Food Institutional Research Measure (FIRM).

Abstract Meal replacement beverages represent a significant opportunity for Irish food firms

to provide consumers with healthy, convenient beverages that are suitable for

‘consuming on-the-go’. The objectives of this research were: to identify the key

intrinsic and extrinsic product design attributes for meal replacement beverages; and

to identify successful segmentation and positioning strategies. Conjoint analysis was

used to help identify design attributes for meal replacement beverages. This initially

involved conducting eight interviews followed by a 300 respondent consumer survey.

The interviews identified positioning the meal replacement beverage as a healthy

natural drink, as the product is targeted at the breakfast meal occasion. The key

product design attributes of a meal replacement beverage identified from the conjoint

analysis were: price, functional health benefits, the flavour and the base product. The

conjoint-based study revealed five consumer segments based on their preferences for

meal replacement beverage concepts. The group level simulation analysis helped

identify new meal replacement beverage concepts that could be targeted more

effectively at each market segment. This research generated information on consumer

utility for a number of product design attributes that can be used by technical

personnel to design meal replacement beverages that gain consumer acceptance.

5

SECTION I: INTRODUCTION

1.1 Functional Beverages: Meal Replacements

According to Hollingsworth (2000) the functional beverage market is the fastest

growing market segment in the beverage industry and has out performed all other

functional food segments. Zenith International (2000) reported that sales of

functional beverages in Western Europe, US and Japanese markets experienced an

increase of 77 per cent in volume from 1995 to 1999, to 8.2 billion litres. The growth

of the functional beverages market was further outlined by Starling (2002).

Functional beverages were defined by Zenith International (2000: 1) as:

“Drinks providing a health benefit beyond their basic nutrition content, by

virtue of their physiologically active components”.

Meal replacements represent over 30 per cent of the functional beverage category in

the US (Prepared Foods, 1999). Delahanty (2002) defined a meal replacement as a

portion controlled, pre-packaged product, which replaced an entire meal or snack.

He also noted that meal replacements for specific market segments were designed to

be low in fat and calories, with a calorie content of 200 to 300 calories, and a

macronutrient content of roughly 3 grams of fat, 10 grams of protein, up to 25 grams

of carbohydrates and various vitamins and minerals. The Nutrition Business Journal

Report (2002) reported that the meal replacement category in the USA, which

included both bars and drinks, was valued at $US 2.3 billion annually.

According to Prince (2002) the concept of a meal worldwide is changing

significantly due to healthy eating habits, weight concerns and time constraints. Sloan

(1999) reported that meal replacements offer consumers a healthy and convenient

product. Furthermore, meal replacements represent an opportunity for manufacturers

to develop products that offer a mainstream retail product opportunity, with

convenient packaging, and a broad demographic appeal (Prince, 2002).

6

1.1.1 Key Drivers of Meal Replacements for On-the-Go Consumption

There are many factors that are driving the development of meal replacement

products for the on-the-go market. One of the major factors reported by Watson

(2003) concerned the liberalising of social rule, where consumers no longer felt

embarrassed to eat in public places or in front of work colleagues at their desks.

Gofton (1995) referred to a ‘time famine’ as people worked longer and travel further

to work, and consequently had less time in the morning for a formal breakfast. It was

also reported by Watson (2003) that consumers were increasingly health and diet

conscious.

The convenience food market has experienced strong growth of seven to ten per cent

year on year in Ireland since 2000 (Horgan, 2004). According to Groves (2002) this

growth was attributed to: consumer demand for food without preparation;

consumers’ time constraints; and the adoption of individualistic lifestyles resulting in

a demand for easy-to-serve portion controlled convenience foods. As time pressures

increase, consumers look for non-intrusive foods that may be consumed on-the-go,

during work, travel and leisure (Datamonitor, 2001). In addition, Groves (2002)

reported that the increase in the number and variety of places where food was

available, together with more impulsive and impatient consumers, was driving the

move towards more informal dining and a decline in traditional fixed meal times.

Innovations in packaging have also driven the growth of the meal replacement

market. There is a growth in the market for single-serve products using PET2

bottles, as an alternative to cans, as they are lighter, more portable, easier and more

hygienic to drink from, and they are resealable (Leatherhead Food International,

2003).

1.1.2 NPD Activity in the Meal Replacement Category

New Product Development (NPD) activity in the meal replacement category has

focused on the development of meal replacement products for the on-the-go market

and the repositioning of traditional meal replacements for broader consumer appeal.

2 Polyethylene Terephthalate (PET) is a plastic resin used to make bottles for soft drinks.

7

Prince (2002) referred to a new generation of meal replacements that are leveraging

functional beverages into mainstream markets. These enriched beverages contain

roughly 220 calories, contain less that five grams of fat, contain less then twenty-five

grams of sugar, are enriched with ten to twenty grams of protein and fortified with

vitamins and minerals. One such product is the Snapple-A-Day meal replacement

beverage launched by the Cadbury Schweppes group, which is a fruit flavoured soy-

based drink. This beverage offers both convenience and health in a single package

(New Nutrition Business, 2003).

Manufacturers have been particularly active developing meal replacements designed

to replace the breakfast meal occasion. Mellentin (2003) reported that 20 to 30 per

cent of consumers in the US skip breakfast causing manufacturers to address the

problem of decreasing sales of breakfast cereals. Beverages such as Sanitarium’s Up

and Go and cereal bars such as Kellogg’s Nutri-Grain bar are currently on the

market. In addition, innovation in the yoghurt and cereal bars category has resulted

in products gaining a broader consumer appeal (Roberts, 2003).

The repositioning of meal replacement products is a strategy being used by a number

of firms to gain broader consumer appeal. This strategy was used for both Ensure and

Boost, which were brands initially designated for use in hospitals, primarily for tube

feeding and elderly care. Hollingsworth (2003) reported that recently both these

products have been repositioned by altering their packaging and their formulation to

market the brands to the broader consumer market. Similarly, the Slim-Fast brand,

which includes bars and beverages targeting the weight loss market, has also adopted

a repositioning strategy to broaden its appeal to the healthy lifestyle consumer

segment (Hollingsworth, 2003).

1.2 Market-oriented NPD

Consumers’ needs and wants evolve as a result of changing attitudes, demographics

and lifestyles. Consequently, manufacturers need to continually develop new

products to satisfy the changing needs of the consumer (Food Agency Co-operation

Council, 2003). Buisson (1995) noted that the factors which influenced increased

levels of new product activities were: changing consumer needs; the need for product

8

differentiation; advances in technologies; increased competitive pressure; and a

shortening of product life cycles. However, Urban and Hauser (1993) emphasised

changes in demographics and lifestyles as key driving forces in the development of

new products.

Traill and Grunert (1997) reported that 90 per cent of new products in the food

industry fail in their first year. However, Cooper (1993) found that having a market-

orientation was a critical success factor for successful NPD and Narver and Slater

(1990) reported that it was an important determinant of profitability for firms. A lack

of market-orientation can result in: inadequate market analysis; a failure to

understand consumer needs and wants; and insufficient attention to the marketplace.

Grunert et al. (1996) reported that a major factor influencing the move of the food

industry from being product-oriented towards being market-oriented was the

increased importance of added-value in the NPD process.

1.2.1 Market-oriented NPD Process

Cooper (1993) reported that there are three essential elements to developing a

successful new product: having a strong commitment and orientation to the

marketplace; having a logical and stepwise flow of activities in the NPD process; and

that there is interaction between people from different functional groups within a

firm. According to Calatone and Cooper (1979), successful NPD is dependent upon a

product being unique and superior; understanding consumer wants, needs and

preferences; effective communication between the product development team

personnel; top management support and effective product marketing. Hoban (1998)

had similar views on the success factors of NPD. He found that the NPD success

factors included: the involvement of senior management; the use of internal multi-

functional teams; conducting market research to understand consumer trends and

needs; and the use of information from retail and external sources.

Cooper’s (1993) Stage-Gate New Product Process is a market-oriented NPD process.

This process is multi-functional and activities occur parallel to each other. The gates

between each stage act as quality control checkpoints. The key stages in this model

include: a preliminary investigation stage; a detailed investigation; product

9

development; the testing and validation stages; and the full production and market

launch.

1.3 Product Design: Foods On-the-Go

Product design features can have a strong influence on whether a product is

ultimately successful on the market or not. It was reported by Childs (1997) that for

food products the attributes of taste, convenience, and value for money remained the

primary factors that influenced product success. In terms of functional foods the

benefits from the added ingredients also influence product success. Moskowitz et al.

(2002) identified that the consumer’s needs for eating on-the-go included small

portion size and controllable packaging with the introduction of single-serve packs

and individual portion formats were important packaging features that aided the

development of the on-the-go sector (Eurofood, 2001). Other developments in

packaging materials science that have aided the development of the on-the-go sector

are the shift away from glass and cans to PET bottles which offer a more convenient,

resealable option for consumers with active lifestyles (Leatherhead Food

International, 2003).

Price is a significant element of most marketing strategies. According to Heasman

and Mellentin (2001) the key issue concerning the pricing strategy adopted for

functional foods relates to identifying the premium which consumers are willing to

pay for such foods. Sloan (2003) reported that consumers were willing to pay a

higher price for convenient functional products.

Impulse outlets such as convenience stores and petrol forecourts, where products are

now normally available chilled for immediate consumption, have been successful

points of sale for drinks designed for on-the-go consumption (Leatherhead Food

International, 2003). Business Wire (2002) noted that vending machines were a

strategic element of a distribution strategy for products designed for consumption on-

the-go. Berry (1999) outlined their suitability for on-the-go products due to their 24

hour availability in strategic locations. Business Wire (2002) reported that vending

machines sell products directly to the consumer, allowing consumers to avoid store

queues.

10

Promotion and brand awareness play an important role in the on-the-go market due to

the competitive nature of this impulse driven market. Promotional activities used in

the confectionery and savoury snack markets include the licensing of characters, tie-

ins with special events, and endorsements by sports people and celebrities

(Leatherhead Food RA, 2002).

1.4 Conjoint Analysis

Conjoint analysis is a quantitative methodology described by Steenkamp (1987) as a

consumer-oriented methodology which seeks to quantify and predict consumers’

overall judgement of a product on the basis of the underlying product attributes.

Green and Srinivasan (1978) stated that conjoint analysis provided information for

the researcher about the structure of consumer preferences, which were obtained

from their overall judgement of a set of alternative combination levels of different

attributes. Furthermore, Green and Krieger (1991) pointed out the potential

usefulness of conjoint analysis for the development of new multi-attribute products

with optimal utility levels, for the estimation of market shares in alternative

competitive scenarios, and to enhance market segmentation and promotional

strategies. According to Steenkamp (1987) there are two basic assumptions

underpinning conjoint analysis. The first assumption is that a product can be

described as a combination of levels of a set of attributes, and secondly, that these

levels determine consumers’ overall judgement of a product.

The full-profile approach is referred to by Gil and Sánchez (1997) as being the most

common method of data collection used in conjoint analysis. This approach to

conjoint analysis involves asking consumers to score each alternative product

concept based on their preferences (Green and Srinivasan, 1978). There are a number

of advantages to using the full-profile approach. Green and Srinivasan (1978)

reported that it utilised a more complete set of attributes than other forms of conjoint

analysis. Aaker et al. (1998) reported that the description of the concepts was a more

realistic way of representing a product concept when the full profile approach was

used. Another advantage of the full profile approach is that it is flexible in that either

rank orders or ratings may be applied (Green and Srinivasan, 1978). However, a

major limitation of the full profile approach is the limit to the number of attributes

11

that may be used. Green and Srinivasan (1978) recommended that five or six

attributes should be used in the full-profile approach.

SECTION II: RESEARCH OBJECTIVES AND METHODOLOGY

2.1 Research Objectives

The objectives of this research were: i) to identify the key intrinsic and extrinsic

attributes, in terms of product design, that influence consumer acceptance of meal

replacement beverages; and ii) to identify the key components of successful market-

oriented strategies that gain consumer acceptance, including segmentation and

positioning strategies.

2.2 Methodology

Conjoint analysis was used to identify the key design attributes of the meal

replacement beverage and to identify consumer segments and positioning strategies.

This initially involved conducting interviews to identify product attributes and their

associated levels. The information generated from the interviews was used in the next

step of the research to construct hypothetical meal replacement products that were

rated by consumers using the conjoint questionnaire.

2.3 Interviews

Interviews were used to gain an insight into peoples’ eating habits and to establish

the important product characteristics for meal replacement products. Punch (1998)

stated that interviews were useful in generating an insight into consumers’

experiences, opinions, attitudes and feelings. Kumar (1999) outlined that interviews

were flexible and provided researchers with rich qualitative information.

Patton (1990) described an interview guide as a list of questions that are explored

during an interview and which enable the interviewer to probe and explore issues

that explain and enlighten that particular subject. The first section of this interview

guide contained questions that were relevant to the meal replacement product. These

questions were concerned with consumers’ eating habits with a particular focus on

breakfast, consumer behaviour relating to eating on-the-go, and issues to do with the

12

marketing strategy for a meal replacement beverage. The second section of the

interview guide contained questions relating to a meal complement beverage

followed by questions concerning consumer socio-demographic details. The

interview guide was pilot tested to eliminate mistakes, to ensure that the questions

could be fully understood and to test the time required to conduct the interview (See

Appendix A).

According to Patton (1990) a qualitative inquiry typically examines a relatively small

sample. Convenience sampling was the methodology selected for the interviews.

Participants were recruited by advertising on campus at University College Cork.

The sample consisted of a broad range of age groups. Age categories from 18 to 64

years were represented. The interviews were held in a conference room at University

College Cork. Eight interviews were conducted in March 2004. Each interview was

tape-recorded and lasted between forty-five minutes to one hour. The interviews were

transcribed from the tape-recordings and then coded. Codes were developed and

assigned to responses to the interview guide. All interview transcripts were evaluated

and significant quotes and comments were highlighted. This information was used to

guide the selection of attributes and levels used in the conjoint survey to construct

hypothetical meal replacement products (Gil and Sánchez, 1997).

2.4 Conjoint Experimental Design

The conjoint model was designed using SPSS Conjoint (SPSS, 2001). From the

interviews, the attributes and levels selected for the conjoint design were: the type of

drink, flavour, functional health benefit, price, packaging format and portion size.

The hypothetical products were generated using the Generate Orthogonal Design

dialog in SPSS (SPSS, 2001). A fractional-factorial design was used to select a

sample of product profiles to determine the relative importance of a product’s multi-

dimensional attributes. This enabled data to be gathered on a large number of product

profiles while consumers only rated a limited number of product profiles. The

conjoint preference model incorporated six attributes and their associated levels,

which were used by the orthogonal design function in SPSS conjoint to generate 22

hypothetical products. The design consisted of 18 products and 4 holdouts. Holdouts

13

are product profiles which are ranked or rated by consumers but not used in the

estimation of utility values.

2.4.1 Conjoint Questionnaire

A questionnaire was designed which presented 22 hypothetical product profiles to

consumers who rated their preferred products. Additional questions were included in

the questionnaire concerning consumer eating habits, lifestyles and socio-

demographic information. Respondents were presented with 22 product profiles and

were then asked to rate each of the product profiles, according to their purchase

intentions on a scale from 1 (least preferred) to 9 (most preferred) (see Appendix B).

A significant methodological critique of the full-profile conjoint analysis method

concerns the increased possibility of respondent fatigue, which can result in

reliability and validity problems, as the number of attributes and associated attribute

levels increase. A number of steps were therefore taken in order to reduce the

possibility of respondent fatigue. Firstly, in-depth one-to-one interviews were

initially conducted with consumers to identify the most relevant product attributes

that influence consumers’ purchase decisions. Secondly, the resulting conjoint survey

was then pilot tested to determine: the validity of the models, consumer

understanding of the procedure, and the time required to complete the questionnaire.

A high Kendall’s tau value for the four-holdout cards was obtained which indicated

good agreement between the card ratings and model predictions, which further

validated the questionnaire (SPSS, 2001). Questionnaires were distributed using a

mixture of the ‘drop-off and collect’ method to houses, and the ‘intrusive’ method by

distributing them in leisure centres and shopping centres. The sample was selected

using stratified random sampling of the Irish population from the 2002 census (CSO,

2002). The survey was conducted in Dublin and Cork in May 2004. Three hundred

questionnaires were collected and six of these were deemed unusable, resulting in a

total sample of 294 respondents.

2.4.2 Data Analysis

The first step in the conjoint analysis was to calculate the utility values, which

indicated how each factor level related to consumer preferences. For rating-based

14

conjoint surveys a positive utility value indicates that the attribute’s level is

positively related to preferences and a negative utility value indicates that consumers

have a low preference for the factor level. Importance values are also calculated

which indicate the importance of each attribute to preference ordering. ‘K-means’

cluster analysis was used to help identify market segments based on their preferences

and socio-demographic characteristics. Finally, simulation tests were conducted to

predict consumers’ preferences for hypothetical products, which were not actually

rated by consumers.

2.4.3 Validity of the Conjoint Model

The validity of the conjoint model assessed how well the model fitted the ratings for

an individual. The validity of the model was assessed by association measures and

holdout cards (SPSS, 2001). The model had a good fit as both the association

measures, Pearson’s R (0.998) and Kendall’s tau (0.974) measures were close to one,

which indicated that there was a good agreement between the average card rating and

the card utilities predicted by the model. The Kendall’s tau value for the four-holdout

cards was also very high (1.0) which indicated that there was a good agreement

between the card ratings and model predictions, which further validated the model.

SECTION III: RESULTS AND ANALYSIS

3.1 Results of the Interviews

This section presents the qualitative findings on consumers’ breakfast eating habits,

eating on-the-go and the product characteristics of a meal replacement beverage.

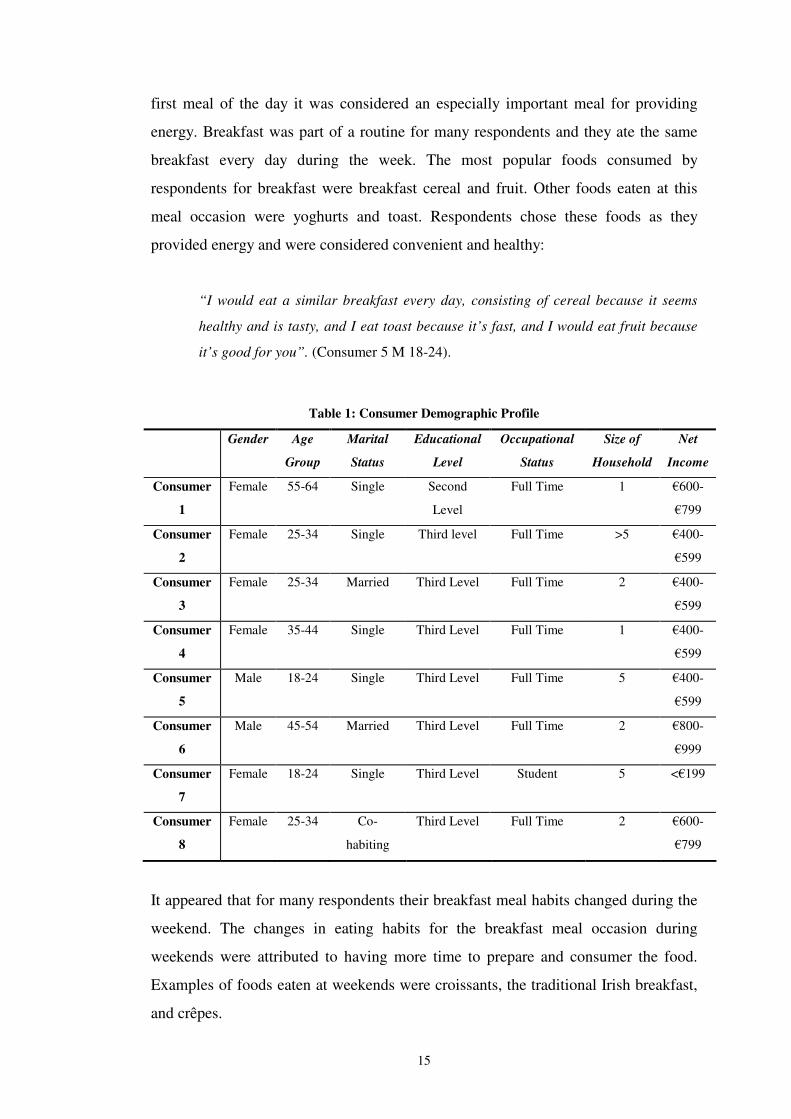

3.1.1 Consumer Profiles

The consumer profiles for the interviews are shown in Table 1. Eight in-depth

interviews were conducted with six females and two males. The majority of

respondents were single, had completed third level education, and were in full-time

employment.

3.1.2 Breakfast Eating Habits

Breakfast was considered an important meal by the majority of respondents. As the

15

first meal of the day it was considered an especially important meal for providing

energy. Breakfast was part of a routine for many respondents and they ate the same

breakfast every day during the week. The most popular foods consumed by

respondents for breakfast were breakfast cereal and fruit. Other foods eaten at this

meal occasion were yoghurts and toast. Respondents chose these foods as they

provided energy and were considered convenient and healthy:

“I would eat a similar breakfast every day, consisting of cereal because it seems

healthy and is tasty, and I eat toast because it’s fast, and I would eat fruit because

it’s good for you”. (Consumer 5 M 18-24).

Table 1: Consumer Demographic Profile

Gender Age

Group

Marital

Status

Educational

Level

Occupational

Status

Size of

Household

Net

Income

Consumer

1

Female 55-64 Single Second

Level

Full Time 1 �600-

�799

Consumer

2

Female 25-34 Single Third level Full Time >5 �400-

�599

Consumer

3

Female 25-34 Married Third Level Full Time 2 �400-

�599

Consumer

4

Female 35-44 Single Third Level Full Time 1 �400-

�599

Consumer

5

Male 18-24 Single Third Level Full Time 5 �400-

�599

Consumer

6

Male 45-54 Married Third Level Full Time 2 �800-

�999

Consumer

7

Female 18-24 Single Third Level Student 5 <�199

Consumer

8

Female 25-34 Co-

habiting

Third Level Full Time 2 �600-

�799

It appeared that for many respondents their breakfast meal habits changed during the

weekend. The changes in eating habits for the breakfast meal occasion during

weekends were attributed to having more time to prepare and consumer the food.

Examples of foods eaten at weekends were croissants, the traditional Irish breakfast,

and crêpes.

16

Respondents generally ate breakfast at home. However, a young female consumer

frequently ate her breakfast while at work. This consumer stated that due to a lack of

time in the mornings she would skip breakfast at home, but would eat something at

work later in the morning:

“I don’t eat breakfast as I would not have the time in the mornings. The first time I

would eat would be at 11 o’clock”. (Consumer 2 F 25-34).

Consumers were aware of the consequences of skipping breakfast. The effects

mentioned were a lack of energy, poor performance and concentration. It was also

mentioned by consumers that as a result of skipping breakfast there was an increase

in snacking throughout the day:

“My performance at work would be hindered if I skipped breakfast as I would be

just waiting for lunch and watching the clock. It would also effect your energy as

you wouldn’t have eaten in maybe 14 hours”. (Consumer 5 M 18-24).

“If I skipped breakfast I would get hungry quicker, so I would need to eat again

quicker”. (Consumer 7 F 18-24).

3.1.3 Eating On-the-Go

A majority of respondents snacked between their meals throughout the day. The

reasons for this included hunger, provision of energy to replace missed meals, and

out of routine:

“If I know that I am not going to get a meal later on, my dinner for example, I know

that I need to get some food into my body and anything will do”. (Consumer 4 F 35-

44).

“I would snack in the morning and afternoon, as I probably need a bit of energy to

keep me awake and help my concentration during lectures”. (Consumer 7 F 18-24).

Respondents mentioned numerous occasions throughout the day when they snacked.

These snacking occasions occurred mid-morning, mid-afternoon, and in the evening

while watching television. The types of snacks consumed included the following:

17

fruit, biscuits, crisps, chocolate and cereal bars. These snack foods were chosen for

their convenience, satiating qualities and taste. A young female respondent noted:

“You can eat a bar of chocolate while walking along a street as it’s convenient,

small, it’s quick and it makes you feel better afterwards”. (Consumer 8 F 25-34).

Drinks, which were considered suitable for snacking included tea, coffee, water, fruit

juice and energy drinks. Healthy alternatives to indulgent snack foods included: fruit,

nuts, yoghurts, and cereal bars.

“I would consider yoghurts a healthy snack as they have different types of bacteria

in them. They are natural, they are good for your bones as there is a lot of calcium

in them, and they are tasty as well”. (Consumer 5 M 18-24).

Fruit was considered a good example of a food product that could be consumed on-

the-go. Bananas were chosen for eating on-the-go because they were easy to eat and

are covenient, while satsumas, rather than oranges, were chosen to eat on-the-go

because they were small and easy to peel:

“I would normally eat bananas when I’m on-the-go as you can just grab it and eat it

from the hand. Bananas are easy, good for you, and they are filling”. (Consumer 8

F 25-34).

Respondents also mentioned cereal and energy bars as foods chosen for eating on-

the-go as they were considered filling and tasty. Savoury products such as popcorn

and crisps were eaten because they were seen as convenient.

A number of problems associated with eating on-the-go were reported by

respondents. One problem experienced by respondents whilst eating on-the-go was a

lack of cleanliness associted with consuming certain foods. Other problems reported

were the lack of provision of utensils for products such as salads and yoghurts, the

disposal of packaging, and the package size:

“Oranges are very messy and I generally wouldn’t choose an orange when eating

18

on-the-go as I would have to find a bin and wash my hands. The little mandarin

oranges are much handier. I find smaller foods are much easier to cope with than

bigger foods when eating on-the-go”. (Consumer 2 F 25-34).

Suggestions for ways in which products could be modified for ease of eating on-the-

go included: making portion sizes smaller; providing utensils such as spoons, forks

and straws; more portable and user-friendly packaging; and drinkable products such

as yoghurts for ease of eating on-the-go. A young female consumer noted the lack of

provision of cutlery for healthy products such as salads:

“A huge criticism I would have is that a lot of Irish supermarkets sell salads, but if

you were to snack on something like that in the car, you rarely get cutlery with it.

So I would see it as a deterrent to people eating good food on-the-go. It is easier to

eat a burger, chips or crisps”. (Consumer 3 F 25-34).

3.1.4 Meal Replacement Beverages

Interviewees had mixed views on the meal replacement beverage concept. An elderly

female respondent had a negative attitude towards the meal replacement beverage:

“A meal replacement beverage wouldn’t appeal to me at all. I like my cereal and I

like to sit down and relax over it for 10 to 15 minutes. I like to enjoy my meal and

prepare it my self”. (Consumer 1 F 55-64).

However, there were also respondents who had positive attitudes towards the meal

replacement beverage. A middle-aged female consumer perceived meal replacements

as ideal for her busy lifestyle:

“I would purchase one, because everyone is more aware of nutritional value these

days and you need more energy to keep going, because people have busy schedules

and are normally travelling somewhere”. (Consumer 4 F 35-44).

Respondents did not think that the meal replacement beverage was a full substitute

for a solid breakfast and therefore would not consume the beverage every day during

the week:

19

“No I wouldn’t consume one every day during the week. I don’t think it could fully

replace solid food”. (Consumer 5 M 18-24).

The most significant attributes for consumers for the meal replacement beverages

were: health benefits, packaging, price and taste. The health benefits of the meal

replacement beverage were important for respondents, and, in particular, the vitamin

and mineral content. Respondents deemed breakfast an important meal in terms of

aquiring their intake of vitamins and minerals and they said that the breakfast drink

should contain similar vitamins and minerals to the meal it was designed to

substitute. The addition of healthy ingredients was seen as an extra benefit, and an

opportunity to gain some extra vitamins and minerals or an additional health benefit

from the product:

“The drink should be healthy. You don’t want to be buying something that

has been processed and modified and isn’t a healthy alternative. It should be

equal to what you would have eaten”. (Consumer 8 F 25-34).

The packaging of the meal replacement drink was also important to respondents. For

an on-the-go product, the most important packaging attributes were that it was

portable and resealable:

“If it’s a complete meal on-the-go beverage it would have to be portable.

You want it to be handy so you can carry it along as you walk”. (Consumer 5

M 18-24).

The packaging formats favoured by consumers for the meal replacement beverage

were the pouch, the plastic bottle and the carton. The glass bottle was deemed

unsuitable for an on-the-go beverage due to its weight, poor resealability and the

possibility of it breaking:

“I think the pouch would probably be the best because it is squeezable, it’s easy to

fold away when it’s finished unlike the plastic or glass bottles”. (Consumer 5 M 18-

20

24).

“I would eliminate the glass bottle and the can as I just don’t like drinking out of a

can and the glass would be too heavy”. (Consumer 3 F 24-34).

The general view from respondents was that breakfast was not an expensive meal,

and should cost in the region of �2. If the product was too expensive it would affect

the purchase intention for some consumers. Alternatively, some respondents justified

paying �5 for a complete meal:

“I would pay around �2. If it was too cheap people probably wouldn’t buy it or

trust it, but if it’s too expensive people probably wouldn’t buy it either”. (Consumer

7 F 18-24)

Flavour was also one of the important attributes for respondents regarding the meal

replacement beverage and the most popular flavours were strawberry and orange.

Some examples of other flavours mentioned by respondents were pineapple, banana,

and apple. Respondents continually referred to breakfast as being a healthy meal

throughout the interviews. Therefore, it was not surprising that the positioning

statement most favoured by respondents for the meal replacement product was: ‘a

healthy way to start the day’. Respondents also favoured the ‘healthy and natural’

statement. A young male’s view on the product positioning statement is presented

below:

“I would prefer the option: “a healthy way to start the day”. Generally my breakfast

would be healthy so I would like to replace that with a healthy option”. (Con 5 M

18-24)

3.2 Results of the Conjoint Questionnaires

The attributes and their associated levels to be used in the conjoint questionnaire for

the meal replacement beverage were selected by combining attributes generated from

the interviews for the meal replacement beverage and product design features

identified by process engineers engaged in the project. These attributes and their

levels are shown in Table 2. The profile of the respondents is in Table 3.

21

Table 2: Attributes and levels to be used in the conjoint study

Attribute Level Type of Drink Rice Milk Oat Bran and Carrot Fruit Soup Fruit Flavour Strawberry Orange Banana Health Benefit Boosts the Immune System Aids the Digestive System None Size 250ml 330ml 500ml Packaging Format Plastic Bottle Pouch Carton Price �1.50 �2.50 �4.00

3.2.1 Eating Habits and Travel Patterns

A high proportion (49 per cent) of consumers skipped breakfast at least occasionally

during the week. For 59 per cent of those consumers who skipped breakfast this was

due to time constraints. However, hunger was the main reason why 47 per cent of

respondents chose to eat breakfast. There was a high frequency of snacking

throughout the day by the consumers surveyed, with hunger being the main reason

why 43 per cent of the respondents snacked. Cars were the main mode of transport

used by 61 per cent of the respondents to travel to work with journey times ranging

from 15 minutes to 1 hour.

22

Table 3: Consumer demographic profile (n = 294)

Factor n % Gender Male 115 39.1 Female 179 60.9 Age Group 18-24 78 26.5 25-34 111 37.8 35-44 61 20.7 45-54 29 9.9 55-65 15 5.1 Marital Status Single 163 55.4 Married 104 35.4 Co-habiting 21 7.1 Separated/Divorced 4 1.4 Widowed 2 0.7 Educational Level Primary 2 0.7 Secondary 76 25.8 Third level 216 73.5 Occupational Status Full-Time 189 64.3 Part-Time 35 11.9 Student 45 15.3 Retired 4 1.4 Unemployed 1 0.3 Other 20 6.8 Household Income Less than �199 28 9.5 �200-399 42 14.3 �400-599 48 16.3 �600-799 18 6.1 �800-999 23 7.8 �1000 and above 48 16.3 Declined to answer 87 29.6

3.2.2 Results of Conjoint Analysis

The first stage of the conjoint analysis was to identify consumers’ overall preferences

for meal replacement beverages. Figure 1 summarises the averaged results for the

overall conjoint analysis. The column on the extreme left indicates the importance for

each factor as it relates to the ratings and the utility column contains the utility

estimates for levels of the factors. The utilities indicate how each factor level relates

to preferences. Results from Figure 1 indicated that price was the most important

attribute overall (importance = 22.59) to the respondents surveyed. Both the health

benefit and flavour were also important attributes and had similar importance values

23

of 19.83 and 19.41 respectively. Size and packaging format were the least important

of the factors to respondents, with importance values of 11.23 and 9.74 respectively.

Averaged Importance Utility Factor ���������� FLAVOUR Flavour �19.41 � .4101 �-- Orange � ��������� -.6075 --� Banana � .1975 �- Strawberry � ��������� CARRIER Base Product �17.21 � .2207 �- Rice � �������� -.3309 -� Oat Bran and Carrot � .1102 � Fruit Soup � ���������� FUNCTION Health Benefit �19.83 � .4911 �-- Boosts ImmuneSystem � ��������� .4299 �-- Aids DigestiveSyste � -.9210 ----� None � ����������� PRICE Price �22.59 � .8432 �--- �1.50 � ���������� .1589 �- �2.50 � -1.0021 ----� �4.00 � ������ SIZE Size 11.23� � -.0899 � 250ml � ����� -.0571 � 330ml � .1470 �- 500ml � ����� PACKAGIN Packaging Format 9.74 � � .0523 � Plastic Bottle � ���� .0104 � Pouch � -.0627 � Carton � 4.7118 CONSTANT

Figure 1: Conjoint analysis subfile summary

When analysing the utilities for each attribute, a clearer image of consumers’

preferences can be seen. As expected, the lower price of �1.50 was most preferred by

consumers. Respondents were responsive to price, as there was a preference for both

prices of �1.50 and �2.50, but respondents did not score the price of �4.00 highly

(See Appendix C, Figure 1). Of the 294 respondents, 78 respondents indicated that

they preferred a higher price of either �2.50 or �4.00 to that of the lower price of

�1.50. This could be explained by the fact that for these subjects there may have been

interaction between price and perceptions of quality.

24

In terms of health benefits respondents had a strong preference for the presence of a

health benefit and had a slightly higher overall preference for the health benefit

‘boosting the immune system’ over ‘aiding the digestive system’’ (See Appendix C,

Figure 2). The flavour most preferred by respondents was the orange flavour

followed by the strawberry flavour. Respondents did not score the banana flavour

highly (See Appendix C, Figure 3). The carrier that respondents most preferred was

rice milk, followed by fruit soup. Overall, there was a much lower preference for the

carrier of oat bran and carrot than for the other two (See Appendix C, Figure 4).

Respondents indicated that product size and packaging format were the least

important attributes of the meal replacement beverage. Respondents most preferred

the 500ml size and they had least preference for the 250ml and 330ml pack sizes

(See Appendix C, Figure 5). There was a preference for two packaging formats: the

plastic bottle and the pouch, with the plastic bottle being the most preferred.

Respondents had a lower preference for carton packaging (See Appendix C, Figure

6).

3.2.3 Cluster Analysis

The K-means cluster analysis revealed five clusters within the sample of 294 subjects

(See Figure 2).

Number of Cases in each Cluster

41.000114.00042.00065.00032.000

294.000.000

12345

Cluster

ValidMissing

Figure 2: Cluster group size

All five groups exhibited the expected relationship between price and utility, with a

preference for the lower price of �1.50. Other similarities across all consumer groups

included a preference for a functional meal replacement beverage and a low

preference for the banana flavour (See Figure 3).

25

Final Cluster Centers

1.32 .08 .21 .57 .35-2.35 -.27 -.62 -.31 -.141.03 .19 .42 -.26 -.21

.19 .05 .92 -.08 .55-.25 -.16 -2.34 -.10 1.12.06 .10 1.42 .18 -1.68.40 .20 .10 1.16 .79.11 .18 .34 1.23 .23

-.51 -.38 -.43 -2.39 -1.02.68 .71 .69 1.18 1.05.14 .13 -.03 .37 .12

-.82 -.84 -.66 -1.55 -1.16-.03 -.14 -.22 -.02 .03.05 .00 -.21 -.28 .25

-.02 .13 .44 .30 -.28.16 .02 .29 .07 -.31

-.19 .04 -.28 .06 .44.03 -.06 -.01 -.13 -.13

OrangeBananaStrawberryRiceOat Bran and CarrotFruit SoupBoosts Immune SystemAids Digestive SystemNone�1.50�2.50�4.00250ml330ml500mlPlastic BottlePouchCarton

1 2 3 4 5Cluster

Figure 3: Mean attribute utility values for each cluster

3.2.4 Cluster Preferences and Socio-demographic Profiles

There are differences in preferences between different demographic groups (See

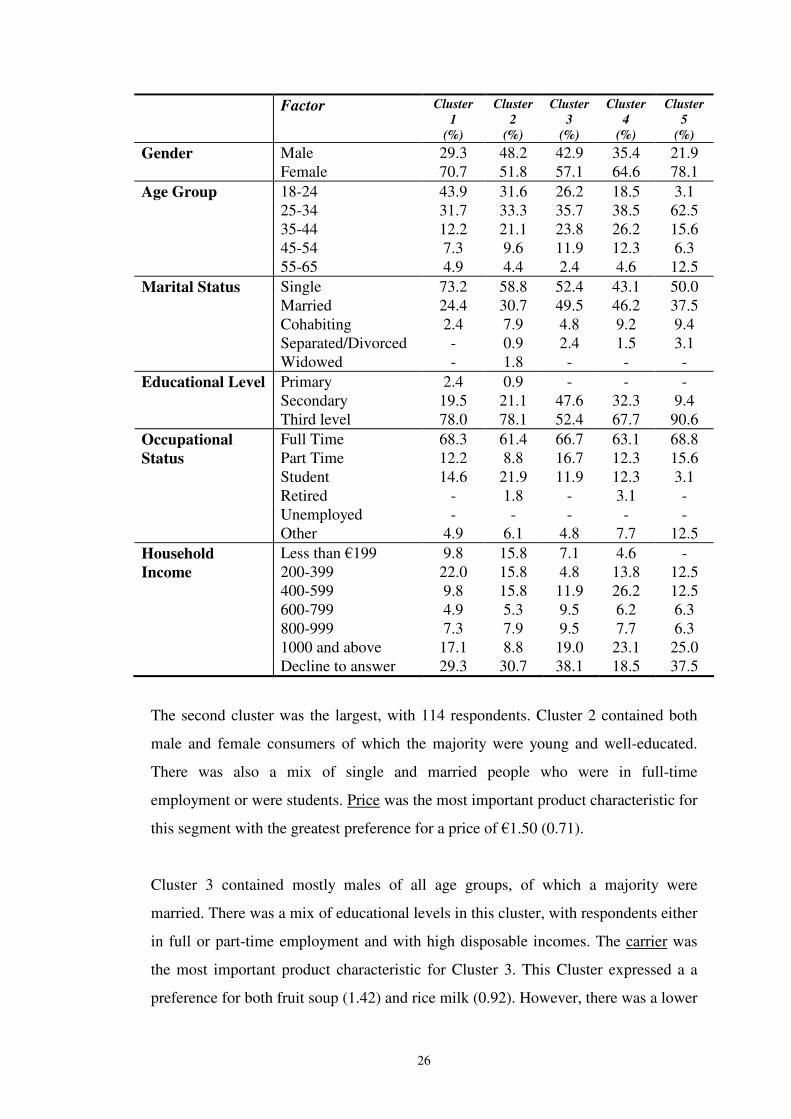

Appendix D). Table 4 shows the demographic profile for each cluster. Each cluster is

broken down in terms of gender, age group, marital status, educational level,

occupational status and household net income.

Cluster 1 contained 41 consumers who were mainly young single females with

relatively low disposable incomes. Flavour was the most important product

characteristic for this segment of consumers. There was a preference for both orange

(utility=1.32) and strawberry (0.98) flavours. The banana flavour had a lower

preference (-2.35).

Table 4: Demographic profile for clusters

26

Factor Cluster 1

(%)

Cluster 2

(%)

Cluster 3

(%)

Cluster 4

(%)

Cluster 5

(%) Gender Male 29.3 48.2 42.9 35.4 21.9 Female 70.7 51.8 57.1 64.6 78.1 Age Group 18-24 43.9 31.6 26.2 18.5 3.1 25-34 31.7 33.3 35.7 38.5 62.5 35-44 12.2 21.1 23.8 26.2 15.6 45-54 7.3 9.6 11.9 12.3 6.3 55-65 4.9 4.4 2.4 4.6 12.5 Marital Status Single 73.2 58.8 52.4 43.1 50.0 Married 24.4 30.7 49.5 46.2 37.5 Cohabiting 2.4 7.9 4.8 9.2 9.4 Separated/Divorced - 0.9 2.4 1.5 3.1 Widowed - 1.8 - - - Educational Level Primary 2.4 0.9 - - - Secondary 19.5 21.1 47.6 32.3 9.4 Third level 78.0 78.1 52.4 67.7 90.6

Full Time 68.3 61.4 66.7 63.1 68.8 Occupational Status Part Time 12.2 8.8 16.7 12.3 15.6 Student 14.6 21.9 11.9 12.3 3.1 Retired - 1.8 - 3.1 - Unemployed - - - - - Other 4.9 6.1 4.8 7.7 12.5

Less than �199 9.8 15.8 7.1 4.6 - 200-399 22.0 15.8 4.8 13.8 12.5 400-599 9.8 15.8 11.9 26.2 12.5

Household Income

600-799 4.9 5.3 9.5 6.2 6.3 800-999 7.3 7.9 9.5 7.7 6.3 1000 and above 17.1 8.8 19.0 23.1 25.0 Decline to answer 29.3 30.7 38.1 18.5 37.5

The second cluster was the largest, with 114 respondents. Cluster 2 contained both

male and female consumers of which the majority were young and well-educated.

There was also a mix of single and married people who were in full-time

employment or were students. Price was the most important product characteristic for

this segment with the greatest preference for a price of �1.50 (0.71).

Cluster 3 contained mostly males of all age groups, of which a majority were

married. There was a mix of educational levels in this cluster, with respondents either

in full or part-time employment and with high disposable incomes. The carrier was

the most important product characteristic for Cluster 3. This Cluster expressed a a

preference for both fruit soup (1.42) and rice milk (0.92). However, there was a lower

27

preference for the use of oat bran and carrots (-2.34) for this group. Price was the

second most important attribute with a preference (0.69) for the lowest price of

�1.50.

Cluster 4 consumers were middle-aged female consumers who were married, had

mixed educational levels, and had medium range disposable incomes. For those in

Cluster 4, the functional health benefit was the most important attribute. There were

similar preferences for having either of the health benefits, ‘boosting the immune

system’ (1.16) or ‘aiding the digestive system’ (1.23). Price was also important to

cluster 4, with a preference for the lower price of �1.50 (1.18).

Cluster 5 consumers were mostly young females, both single and married, who were

well educated and had high disposable incomes. For this cluster of consumers the

carrier was the most important factor. However, unlike Cluster 3, there was a

preference for oat bran and carrot (1.12) and a lower preference for the use of fruit

soup carrier (-1.68). Both price and health benefit were important to this conumer

segment. The lower price of �1.50 was preferred (1.05) and there was also a

preference for a health benefit ‘boosting to the immune system’ (0.79).

3.2.5 Simulations

Five alternative meal replacement beverage concepts were developed from

information generated from the qualitative aspect of this research and from technical

personnel, process engineers and sensory scientists, working on the project. The

market shares for these hypothetical product profiles were tested for the five

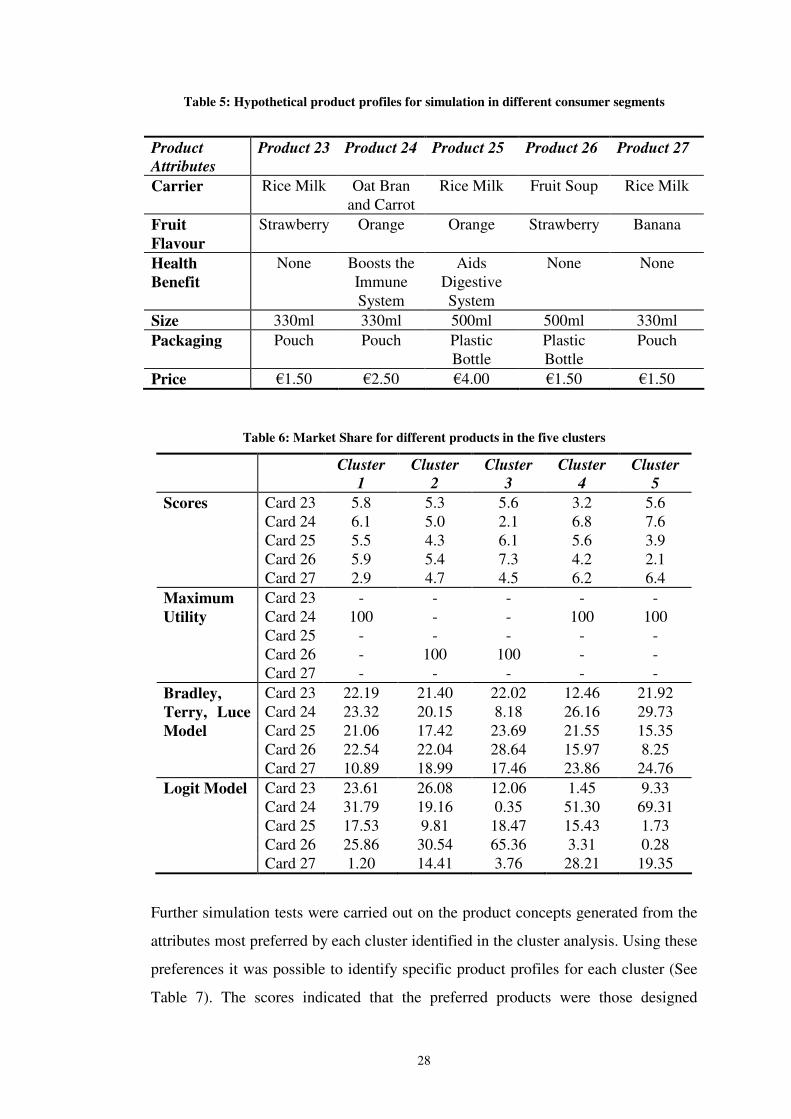

segments identified in this study (See Table 5).

Clusters 1, 4 and 5 most preferred Product 24 (oat bran and carrot, orange flavour,

boosts the immune system, 330ml, pouch, �2.50) and Product 26 (fruit soup,

strawberry flavour, no health benefit, 500ml, plastic bottle, �1.50) was most preferred

by Clusters 2 and 3 (See Table 6). The probability choice models, the maximum

utility, the Bradley, Terry, Luce and Logit models values corresponded with the

results found for the preference score for each cluster (See Table 6).

28

Table 5: Hypothetical product profiles for simulation in different consumer segments

Product Attributes

Product 23 Product 24 Product 25 Product 26 Product 27

Carrier Rice Milk Oat Bran and Carrot

Rice Milk Fruit Soup Rice Milk

Fruit Flavour

Strawberry Orange Orange Strawberry Banana

Health Benefit

None Boosts the Immune System

Aids Digestive System

None None

Size 330ml 330ml 500ml 500ml 330ml Packaging Pouch Pouch Plastic

Bottle Plastic Bottle

Pouch

Price �1.50 �2.50 �4.00 �1.50 �1.50

Table 6: Market Share for different products in the five clusters

Cluster 1

Cluster 2

Cluster 3

Cluster 4

Cluster 5

Scores Card 23 5.8 5.3 5.6 3.2 5.6 Card 24 6.1 5.0 2.1 6.8 7.6 Card 25 5.5 4.3 6.1 5.6 3.9 Card 26 5.9 5.4 7.3 4.2 2.1 Card 27 2.9 4.7 4.5 6.2 6.4

Card 23 - - - - - Maximum Utility Card 24 100 - - 100 100 Card 25 - - - - - Card 26 - 100 100 - - Card 27 - - - - -

Card 23 22.19 21.40 22.02 12.46 21.92 Card 24 23.32 20.15 8.18 26.16 29.73

Bradley, Terry, Luce Model Card 25 21.06 17.42 23.69 21.55 15.35 Card 26 22.54 22.04 28.64 15.97 8.25 Card 27 10.89 18.99 17.46 23.86 24.76 Logit Model Card 23 23.61 26.08 12.06 1.45 9.33 Card 24 31.79 19.16 0.35 51.30 69.31 Card 25 17.53 9.81 18.47 15.43 1.73 Card 26 25.86 30.54 65.36 3.31 0.28 Card 27 1.20 14.41 3.76 28.21 19.35

Further simulation tests were carried out on the product concepts generated from the

attributes most preferred by each cluster identified in the cluster analysis. Using these

preferences it was possible to identify specific product profiles for each cluster (See

Table 7). The scores indicated that the preferred products were those designed

29

specifically for each cluster: Product 28 was most preferred by Cluster 1; Product 29

was preferred by Cluster 2; Product 30 was preferred by Cluster 3; Product 31 was

preferred by Cluster 4; and Product 32 was preferred by Cluster 5 (See Table 8). The

probability values assigned through the Maxim Utility, the Bradley, Terry, Luce and

Logit models correspond with the results found for the score for each cluster.

Table 7: Product profiles for simulation tests within segments

Product Attributes

Product 28

Product 29

Product 30

Product 31

Product 32

Carrier Rice Milk Fruit Soup Fruit Soup Fruit Soup Oat Bran and

Carrot Fruit Flavour

Orange Strawberry Strawberry Orange Orange

Health Benefit

Boosts the Immune System

Boosts the Immune System

Aids Digestive System

Aids Digestive System

Boosts the

Immune System

Size 330ml 500ml 500ml 500ml 330ml Packaging Plastic

Bottle Pouch Plastic

Bottle Plastic Bottle

Pouch

Price �1.50 �1.50 �2.50 �2.50 �2.50

30

Table 8: Market share for different products in the five clusters

Cluster

1 Cluster

2 Cluster

3 Cluster

4 Cluster

5 Scores Card 28 7.5 5.7 6.6 7.7 7.2 Card 29 6.5 6.0 7.3 7.7 4.7 Card 30 6.0 5.4 7.4 7.0 2.4 Card 31 6.4 5.3 7.2 7.8 3.0 Card 32 6.1 5.0 2.1 6.8 7.6

Card 28 100 - - - - Maximum Utility Card 29 - 100 - - - Card 30 - - 100 - - Card 31 - - - 100 - Card 32 - - - - 100

Card 28 22.89 20.86 21.42 20.72 28.99 Card 29 20.05 22.00 23.99 20.89 18.74 Card 30 18.55 19.73 24.21 18.91 9.76

Bradley, Terry, Luce Model

Card 31 19.65 19.34 23.56 21.07 11.97 Card 32 18.86 18.07 6.83 18.42 30.53 Logit Model Card 28 44.31 23.68 13.37 24.13 38.92 Card 29 17.58 32.37 29.37 25.71 3.00 Card 30 10.79 17.34 31.37 12.36 0.32 Card 31 15.42 15.61 25.74 27.47 0.55 Card 32 11.91 11.00 0.15 10.32 57.21

SECTION IV: RESEARCH CONCLUSIONS AND RECOMMENDATIONS

4.1 Meal Replacement: Meeting the Challenges of Consumer Demands

The meal replacement product category represents an important new food type

identified by the food industry. Consumer trends driving the development of meal

replacement beverages include: the demand for food without preparation; consumers’

time consciousness and the adoption of individualistic lifestyles (Groves, 2002).

There are important product design features that need to be addressed by food

manufacturers to be successful in the development of meal replacement products.

4.2 Qualitative Consumer Research

Qualitative research was used to determine consumers’ attitudes towards meal

replacement beverages and to refine the product concept identified from previous

research. In particular, specific product design issues were addressed (Seymour,

2003). Respondents had mixed attitudes towards the meal replacement for breakfast.

31

A majority of respondents had positive views of meal replacement beverages,

deeming them an ideal way to consume ‘breakfast on-the-go’ for time conscious

consumers. However, meal replacement beverages were thought to be suitable for

occasional rather than consistent replacement of solid foods for breakfast.

One important association with breakfast identified from the interviews was the

consumption of fruit, dairy and cereal-based products. These food constituents should

be considered key ingredients on which the meal replacement product should be

based. The interviews also showed that consumers expected the products consumed

at breakfast time to be healthy as breakfast was considered important in terms of

vitamin and mineral intake. Consumers also expected foods consumed at breakfast

time to be low in fat and calories, high in fibre, natural and to be satiating. Other key

design features necessary for products developed for the ‘on-the-go’ market are

portability, convenience and provision of utensils if required.

4.3 Segmentation and Product Design

The conjoint analysis methodology was very useful for identifying key product

design attributes and consumer segments (Bogue et al., 2002). It helped to identify

consumer segments that expressed a preference for a functional meal replacement

beverage and represented viable market opportunities. The key consumer drivers for

the meal replacement beverage were price, functional health benefit, flavour and the

base product. These key drivers represent opportunities for the optimal refinement of

innovative meal replacment beverages.

Conjoint analysis allowed the identification of the key factors that influenced

consumers’ purchase decisions for a meal replacement beverage. For example, this

research revealed that consumers most preferred orange and strawberry flavour

profiles and least preferred the banana flavoured meal replacement beverage. The

inclusion of a functional health benefit would also aid in the success of the meal

replacement product, with certain segments having a preference for the health benefit

‘boosting the immune system’ and other segments having a preference for the health

benefit ‘aiding the digestive system’. Therefore, it is possible to design alternative

products for each of the consumer segments in a market-oriented fashion.

32

Cluster 2 represented the most attractive business opportunity, contained the greatest

number of consumers, and had a broad socio-demographic representation. This

cluster had a preference for a strawberry flavoured fruit soup-based beverage with the

health benefit “boosts the immune system”. There was a preference for a volume of

500ml, in a pouch packaging and having a price of �1.50. Cluster 4 may be the most

viable cluster to develop a product for as it was driven by functionality.

There was a further segment of health conscious consumers who had a preference for

a meal replacement beverage based on rice milk or oat bran and carrot. This cluster,

Cluster 5, contained young well-educated consumers with high disposable incomes.

A product developed specifically for these consumers would have an oat bran and

carrot base, with and orange flavour, contain the health benefit “boosts the immune

system”, have a volume of 330ml, be packaged in a pouch and be priced at �2.50.

4.4 Premium Pricing Strategies for a Functional Product

Numerous researchers, such as Gil and Sánchez (1997) and Poulsen (1999), have

identified the conjoint technique as a powerful tool, which allowed companies to test

alternative pricing strategies and to analyse consumers price sensitivity for a product.

According to Heasman and Mellentin (2001) the key issue concerning the pricing

strategy for functional foods relates to identifying the premium which consumers are

willing to pay.

This research found that a majority of consumers were unwilling to pay a high price

(�4) for a meal replacement beverage. While the price of �1.50 was preferred, they

were willing to pay a price of �2.50. The consumers who indicated that they preferred

a higher price in the conjoint questionnaire were prepared to pay the higher price of

�4.00 as they equated price with quality. According to Childs (1997) the ability to

achieve a premium for nutritional functionality depends on the perception of the

product as a quality product. Therefore, manufacturers need to focus on setting the

optimum price for new meal replacement products targeted at specific segments.

4.5 Positioning Strategies and Communication

33

Breakfast was perceived as a healthy and natural meal and, therefore, a meal

replacement product designed to replace breakfast should be positioned as a healthy

and natural product. The preference for the positioning statement of ‘a healthy way to

start the day’ for the meal replacement product reflected this consumer association of

‘health’ with breakfast.

The communication of the meal replacement’s nutritional profile and health benefits

was important to consumers. These health aspects could be communicated to

consumers by way of in-store education of consumers and the use of health and

nutritional informational leaflets. The promotional tool of in-store product sampling

could be used to allow consumers to experience sensory aspects of the meal

replacements. Consumers also need to be informed of the product’s satiating

properties to differentiate it from similar products on the market. Therefore, the

positioning of meal replacement products should be on a healthy and natural

platform.

4.6 The Importance of Market Research in NPD

This study highlighted the role of market research throughout the NPD process.

Qualitative research was essential for guiding and refining the meal replacement

concept at the early stages of the NPD process. The involvement of the consumer was

vital in selecting the key attributes for the meal replacement beverage, which were

then used in the quantitative part of the study.

Conjoint analysis helps food product developers understand product design attributes

that meet specific consumer value; analyse consumer price sensitivities, and estimate

market shares in alternative competitive scenarios. Conjoint analysis also generated

information for market segmentation through identifying the intrinsic and extrinsic

attributes that were of most importance to specific consumer groups.

The use of qualitative and quantitative research throughout the NPD process can give

guidance to all members of the NPD team for the development of the meal

replacement beverage.

34

4.7 Research Recommendations

Much research has been conducted to identify strategies to improve the success rate

of developing new products. Consumer-oriented NPD, which involves integrating the

consumer throughout the whole NPD process, has been identified as an important

strategy to increase the consumer acceptance of new products. It is recommended that

new product developers incorporate qualitative research into the early stages of the

development process so as to identify and refine new product concepts. The

qualitative and quantitative research identified consumer expectations and

requirements associated with the breakfast meal occasion. These requirements can be

addressed by marketers seeking opportunities in the meal replacement part of the

food market. Design features which should be incorporated by manufacturers for the

meal replacement beverage are that it should be based on either fruit, cereal or dairy

products, avoid strong flavours, and have a functional health benefit. An important

element, which manufacturers need to decide on, is the pricing strategy for functional

beverages. A final element of the marketing strategy is the positioning of the meal

replacement as a healthy and natural drink.

4.8 Suggestions for Further Research

This research demonstrated the usefulness of the conjoint analysis methodology in

identifying the intrinsic and extrinsic drivers of consumer food choice for meal

replacement beverages and the market segments to which such a product appeals.

Further quantitative studies using conjoint and cluster analysis to identify consumer

preferences for a range of meal complement beverages could be useful. The

apparently irrational preferences for higher priced products that were revealed in the

conjoint analysis could also be investigated. Further qualitative research with

selected market segments that seek to optimise the meal replacement and meal

complement product concepts, would contribute to product design information. This

would provide market-oriented information for technical personnel.

35

REFERENCES Aaker, D.A., Kumar, V. and Day, G.S. (1998). Marketing Research, New York:

John Wiley and Sons Inc.

Berry, D. (1999). Buy me! Dairy Foods, May.

Bogue, J., Sorenson, D. and Delahunty, C. (2002). Determination of Consumers’

Sensory Preferences for Full-fat and Reduced-fat Dairy Products, Agribusiness

Discussion Paper No. 37, Department of Food Economics, University College Cork,

Cork.

Buisson, D. (1995). Developing New Products for the Consumer. In: Food Choice

and the Consumer, (Marshall, D.W., Ed.), London: Blackie Academic and

Professional.

Business Wire. (2002). Quench Bottled Water Adding Major New Distribution

Channel With High Visibility Vending Machines to Build Brand Awareness and

Sales, Business Wire, December 3.

Calatone, R.J. and Cooper, R.G. (1979). A Discriminate Model for Identifying

Scenarios of Industrial New Product Development Failure, Journal of Academy of

Marketing Science, 7, 163-183.

Childs, N.M. (1997). Functional Foods and the Food Industry: Consumer, Economic

and Product Development Issues, Journal of Nutraceuticals, Functional and Medical

Foods, 1, 2, 25-43.

Cooper, R.G. (1993). Winning at New Products: Accelerating the Process from Idea

to Launch, United States of America: Addison-Wesley Publishing Company.

CSO. (2002). Central Statistics Office Ireland, Census of Population 2002,

www.cso.ie

Datamonitor. (2001). ‘On-The-Go’ Snack Market, In: Food On-The-Go Increasing

as Habits Change, Eurofood, May 10.

Delahanty, L. (2002). Do Meal Replacements Work? American Dietetics

Association, April.

Eurofood. (2001). Food On-The-Go Increasing as Habits Change, Eurofood, May

10.

Food Agency Co-operation Council. (2003). Market Led New Product

Development in the Food and Drink Industry. Dublin: Department of Agriculture

and Food.

36

Gil, J.M. and Sánchez, M. (1997). Consumer Preferences for Wine Attributes: a

Conjoint Approach, British Food Journal, 99, 1, 3-9.

Green, P.E. and Krieger, A.M. (1991). Segmenting Markets with Conjoint

Analysis, Journal of Marketing, 55, 4, 20-31.

Green, P.E. and Srinivasan, V. (1978). Conjoint Analysis in Consumer Research:

Issues and Outlook, Journal of Consumer Research, 5, September, 103-122.

Gofton, L. (1995). Convenience and the moral status of consumer practices. In:

Food choice and the consumer, (Marshall, D.W., Ed.), London: Blackie Academic

and Professional.

Groves, A.M, (2002). Food Consumption 2002. UK: Institute of Grocery

Distribution. Watford: IGD Business Publication.

Grunert, K.G., Baadsgaard, A., Larsen, H.H. and Madsen, T.K. (1996). Market

Orientation in Food and Agriculture, USA: Kluwer Academic Publishers. Heasman, M. and Mellentin, J. (2001). The Functional Foods Revolution. Healthy

People, Healthy Profits? Surrey: Leatherhead International.

Hoban, T.J. (1998). Improving the Success of New Product Development, Food

Technology, 52, 1, 46-49.

Hollingsworth, P. (2000). Functional Beverage Juggernaut Faces Tighter

Regulations, Food Technology, 54, 11, 50-53.

Hollingsworth, P. (2003). Food and the Ageing Consumer, Food Technology, 57, 7,

28-30.

Horgan, M. (2004). Demand for Food-on-move Keeps Producers on their Toes, Irish

Examiner, June 18.

Kumar, R. (1999). Research Methodology: a Step-by-Step Guide for Beginners,

London: Sage Publications.

Leatherhead Food International. (2003). Drinks On The Go - International Trends

and Developments, Leatherhead Food International. Surrey: January.

Leatherhead Food RA. (2002). Food On The Go - A Global Analysis, Leatherhead

Food RA. Surrey: July.

Mellentin, J. (2003). Functional Foods Turns out to be a Beverage Business, New

Nutrition Business, 8, 4.

37

Moskowitz, H.R., Flores, L., Beckley, J., Mascuch, T.C., Cleveland, C.E. and

Ewald, J.D. (2002). Crossing the Knowledge and Corporate Boundaries to

Systematize Invention and Innovation, ESOMAR Congress, Barcelona, September.

Narver, J.C. and Slater, S.F. (1990). The effect of a Market-Orientation on

Business Profitability, Journal of Marketing, 54, 4, 20-34.

New Nutrition Business. (2003). Cadbury aims to take Meal Replacements

Mainstream, New Nutrition Business. 8, 4, 13.

Nutrition Business Journal. (2002). In: Meals without Replacements - The

Replacements, Beverage World, November.

Patton, M.Q. (1990). Qualitative Evaluation and Research Methods, London: Sage

Publications.

Poulsen, J.B. (1999). Danish Consumers’ Attitudes Towards Functional Foods,

MAPP Working Paper, No. 62, February, Denmark: Aarhus School of Business.

Prepared Foods. (1999). New Smoothie Brands Touts Health, June,

http//www.preparedfoods.com .

Prince, G.W. (2002). Meals without Replacements - The Replacements, Beverage

World, November, 47-48.

Punch, K.F. (1998). Introduction to Social Research: Quantitative and Qualitative

Approaches, London: Sage Publications.

Roberts, W.A. (2003). Bar None, Prepared Foods, April.

http//.www.preparedfoods.com.

Seymour, C. (2003). Consumer-oriented Development of New Functional Drinks:

Meal Replacements and Meal Complements, Unpublished MSc Food Business

Thesis, Department of Food Business and Development, University College Cork.

Sloan, A.E. (1999). The New Market: Foods for the not so Healthy, Food

Technology, 53, 2, 54-60.

Sloan, A. E. (2003). What, When, and Where Americans Eat: 2003, Food

Technology. 57, 8, 48-68.

SPSS. (2001). SPSS Training for Conjoint Analsysis. Dublin: SPSS Ireland.

Starling, S. (2002). Functional Beverages Pour It On, Functional Foods and

Nutraceuticals, July/August.

Steenkamp, J-B.E.M. (1987). Conjoint Measurement in Ham Quality Evaluation,

Journal of Agricultural Economics, 38, 3, 473-480.

38

Traill, B. and Grunert, K. (1997). Product and Process Innovation in the Food

Industry, London: Blackie Academic and Professional.

Urban, G.L. and Hauser, J.R. (1993). Design and Marketing of New Products,

New York: Ridge Press/Random House.

Watson, K. (2003). No bar to Breakfast, Food Manufacture, Supplement,

September, 25-26.

Zenith International. (2000). International Market for Functional Soft Drinks, In

association with The Centre for Food and Health Studies, Bath: Zenith International

Ltd.