dish tv india limited

TRANSCRIPT

Dish TV India LimitedInvestor Presentation

Some of the statements made in this presentation are forward-looking statements and are based on the current

beliefs, assumptions, expectations, estimates, objectives and projections of the directors and management of Dish

TV India Limited about its business and the industry and markets in which it operates.

These forward-looking statements include, without limitation, statements relating to revenues and earnings. The

words “believe”, “anticipate”, “expect”, “estimate", "intend”, “project” and similar expressions are also intended to

identify forward looking statements.

These statements are not guarantees of future performance and are subject to risks, uncertainties and other factors,

some of which are beyond the control of the Company and are difficult to predict. Consequently, actual results could

differ materially from those expressed or forecast in the forward-looking statements as a result of, among other

factors, changes in economic and market conditions, changes in the regulatory environment and other business and

operational risks. Dish TV India Limited does not undertake to update these forward-looking statements to reflect

events or circumstances that may arise after publication.

Disclaimer

2

INR 976 BnTV industry size

INR 475 BnTV industry size

66%TV penetration (of total HHs) 62%

C&S penetration (of TV HHS)

Indian M&E Industry Snapshot

257 , 44%

475 , 46%

976 , 50%

175 , 30%

263 , 26%

387 , 20%

89 ,15%

126 ,12%

204 ,10%

66 ,11%

161 , 16%

397 , 20%

2009

2014

2019

M&E industry composition & revenue size (INR bn.)

TV Print Films Others

2014

2019

231 270

301

134 169

197

101 140

169

2009 2014 2019

Total HHs TV HHs C&S HHs

Indian television market statistics (HHs mn.)

Source: M&E industry composition & size: FICCI-KPMG 2015, Indian television statistics & broadcasting and distribution industry : MPA Report 2014

2014 2019

Total households

83% 86%

CAGR of ~ 15.5%

(2014-2019E)

301 Mn270 Mn

Total TV households 197 Mn169 Mn

Distribution industry

DTH

28%

Analog

Cable

52%Digital

Cable

20%

Broadcasting industry

Multiple broadcasters

producing content in

15 languages

across

7 genres

beaming

~800 channels

3

Distribution Industry

4

Digital Addressable Systems - DAS

Source: *MPA Report 2014

Phase I

Delhi, Mumbai,

Calcutta & Chennai

30-June-2012

Phase II

38 notified cities

31-Mar-2013

Cable Land grab seeding at throw away prices

No addressability/KYC

Working backwards to fill critical gaps; packaging-billing-

dunning

DTH Seeding ground for High-Definition

Potential subscribers for upselling – high value packs

Bulk of the potential DAS converts

Limited coverage by large MSOs due to dispersed population

Very high DTH recognition

DTH best suited considering terrain

Key target markets with more than 60% incremental potential for DTH

5

Phase IV

Rest of India

31-Dec-2016

Phase III

7,709 urban areas

31-Dec-2015

Stayed by High Courts in 10 states

No analog switch -off on sunset date

No spike in demand around deadline

Traction seen post deadline due to industry push

Ph

ase I

II

Distribution Industry - Cable

Analog signal - limited carrying capacity, broadcasters jostling for PCS

Placement & Carriage fees - bulk of MSOs top-line

Massive under declaration – ignored to maintain MSOs ‘reach.’ Reason behind LCOs prosperity

No incentive to raise ARPUs

Digital signal - fatter pipe, larger carrying capacity

Placement fees mindset

B2B Net billing

100% postpaid. Element of bad debts?

Impairment of Set-Top-Box (STB)?

Rising content cost / content negotiation bottlenecks

3 Tiered Structure

MSOs(more than 115 )

Distributors (at least 1 in

each locality)

LCOs (more than

50,000)

Pre-DAS

Post-DAS

6

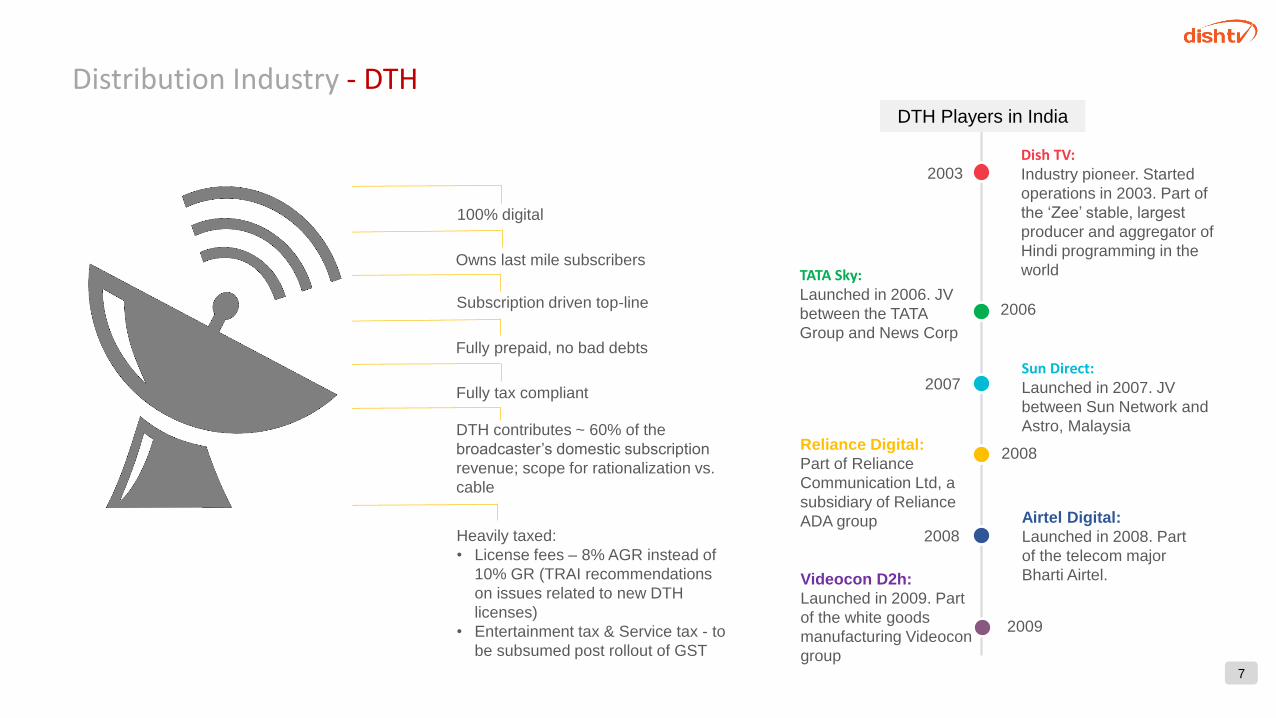

Dish TV:Industry pioneer. Started

operations in 2003. Part of

the ‘Zee’ stable, largest

producer and aggregator of

Hindi programming in the

worldTATA Sky:Launched in 2006. JV

between the TATA

Group and News Corp

Sun Direct:Launched in 2007. JV

between Sun Network and

Astro, MalaysiaReliance Digital:

Part of Reliance

Communication Ltd, a

subsidiary of Reliance

ADA group Airtel Digital:

Launched in 2008. Part

of the telecom major

Bharti Airtel.Videocon D2h:

Launched in 2009. Part

of the white goods

manufacturing Videocon

group

Distribution Industry - DTH

2003

2006

2007

2008

2009

100% digital

Owns last mile subscribers

Subscription driven top-line

Fully prepaid, no bad debts

DTH contributes ~ 60% of the

broadcaster’s domestic subscription

revenue; scope for rationalization vs.

cable

Heavily taxed:

• License fees – 8% AGR instead of

10% GR (TRAI recommendations

on issues related to new DTH

licenses)

• Entertainment tax & Service tax - to

be subsumed post rollout of GST

Fully tax compliant

2008

7

DTH Players in India

8

Many Firsts To Its Credit

9

2007

2009

2010

2012

2012

201320142015

2003

2015

First DTH

in India

First to negotiate

content on a

fixed fee basis

First to launch

Live TV for

moving vehicles

First to achieve

operational break-

even in the Indian

DTH industry

First to

launch High

Definition

First to offer

unlimited

recording

First to be FCF

positive in the

Indian DTH

industry

First to launch

online TV for

DTH viewers –

‘Dish Online

First to launch a

sub-brand

targeting regional

language

markets– ‘Zing’

First to be PAT

positive in the

Indian DTH

industry

First to launch

Home Video

System–DishFlix

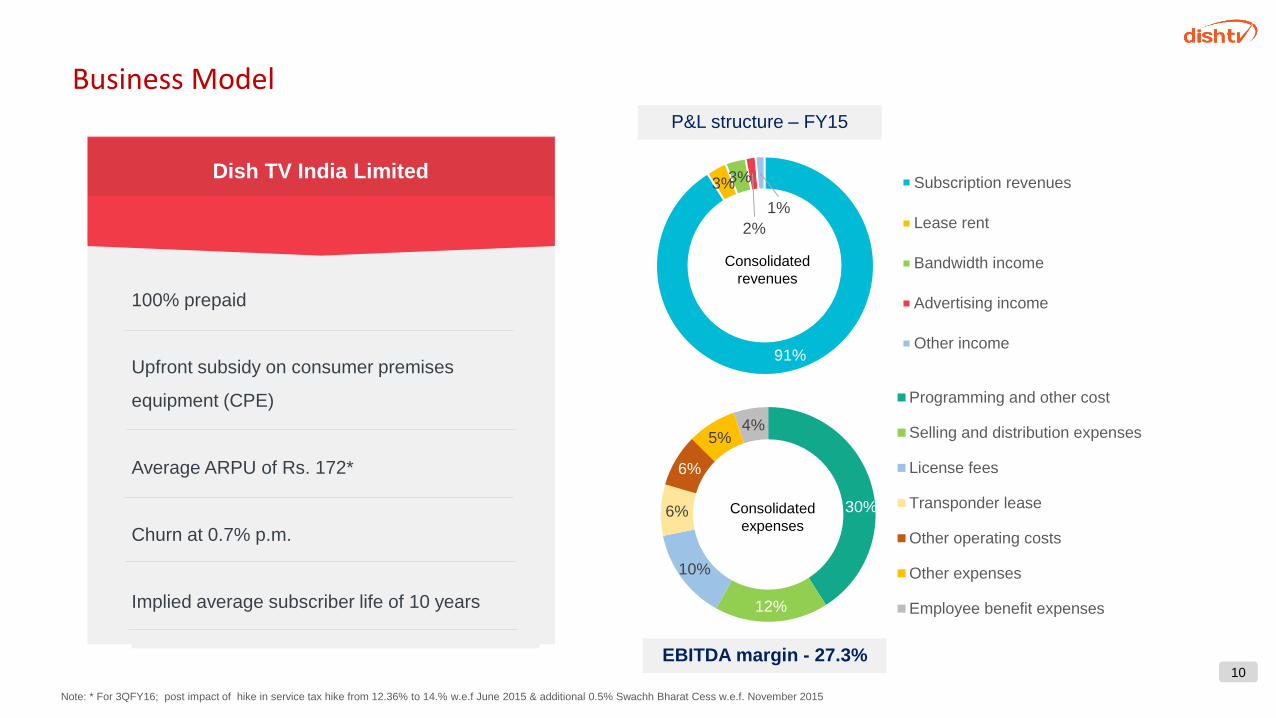

91%

3%3%

2%

1%

Subscription revenues

Lease rent

Bandwidth income

Advertising income

Other income

Consolidated

revenues

30%

12%

10%

6%

6%

5%4%

Programming and other cost

Selling and distribution expenses

License fees

Transponder lease

Other operating costs

Other expenses

Employee benefit expenses

Consolidated

expenses

100% prepaid

Upfront subsidy on consumer premises

equipment (CPE)

Average ARPU of Rs. 172*

Churn at 0.7% p.m.

Implied average subscriber life of 10 years

Dish TV India Limited

Business Model

10

P&L structure – FY15

EBITDA margin - 27.3%

Note: * For 3QFY16; post impact of hike in service tax hike from 12.36% to 14.% w.e.f June 2015 & additional 0.5% Swachh Bharat Cess w.e.f. November 2015

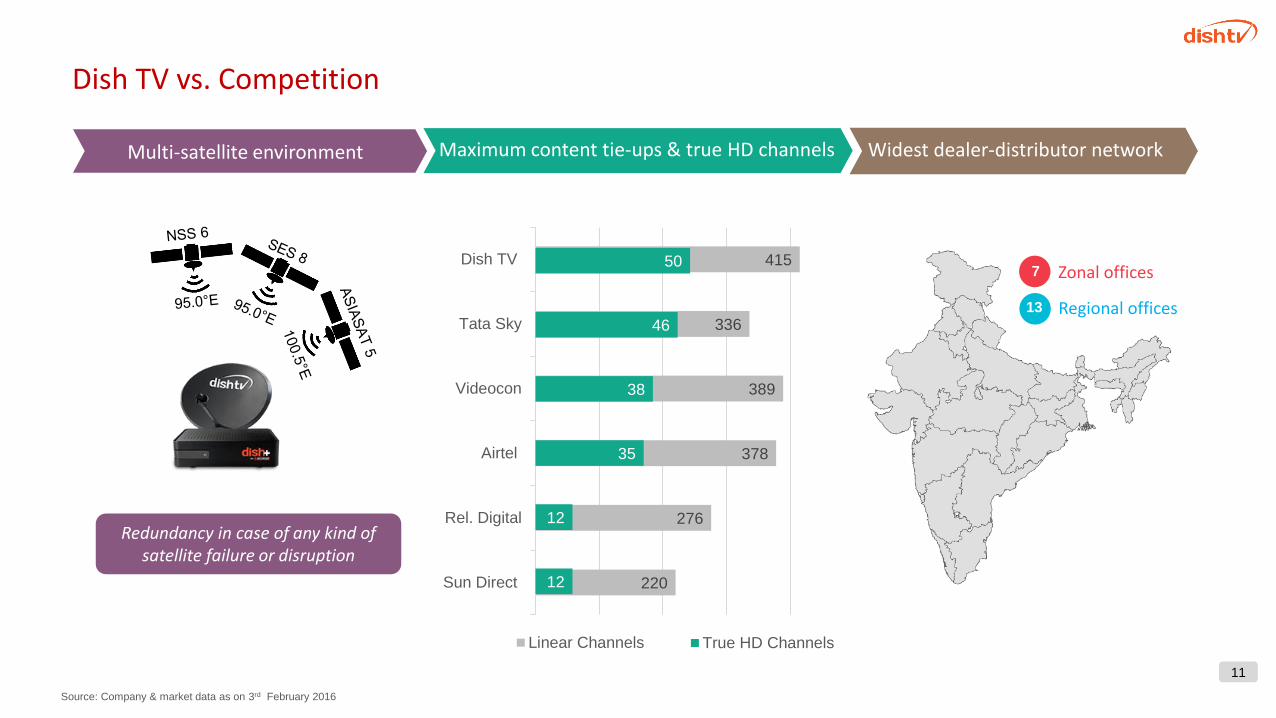

Dish TV vs. Competition

Multi-satellite environment Maximum content tie-ups & true HD channels Widest dealer-distributor network

220

276

378

389

336

415

Sun Direct

Rel. Digital

Airtel

Videocon

Tata Sky

Dish TV

Linear Channels

12

12

35

38

46

50

True HD Channels

Zonal offices7

Regional offices 13

Source: Company & market data as on 3rd February 2016

11

Redundancy in case of any kind of satellite failure or disruption

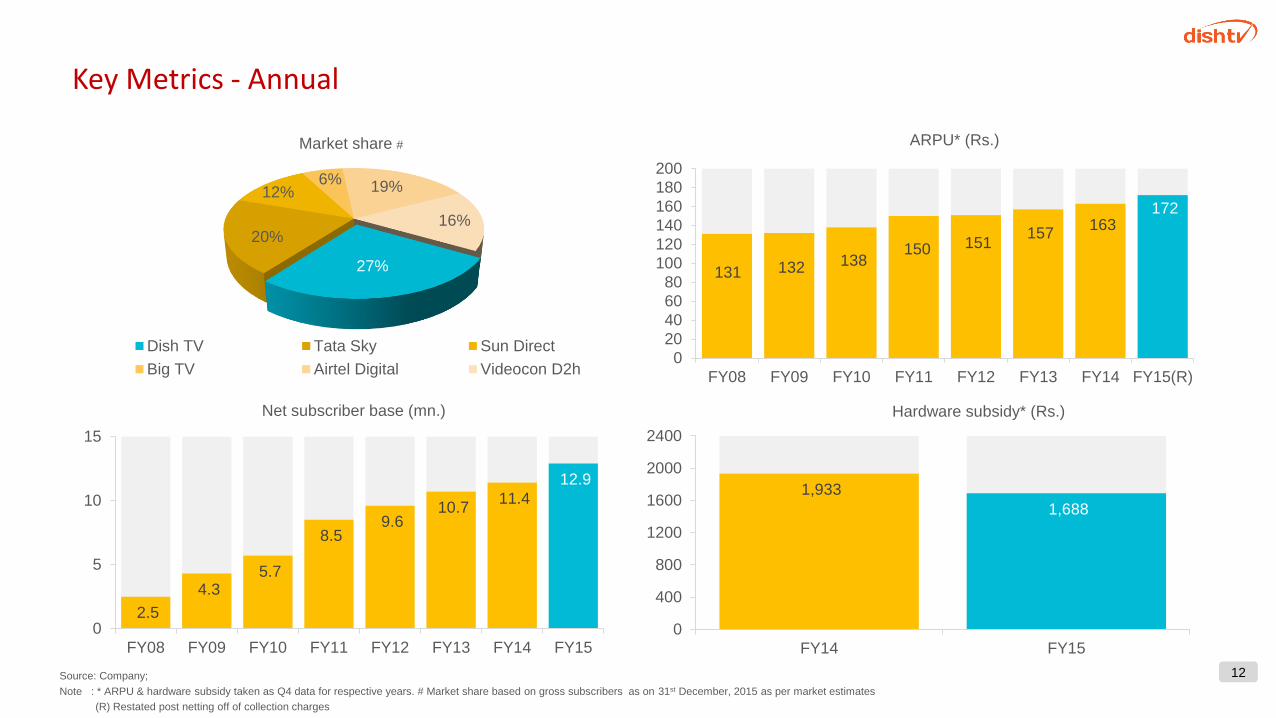

Key Metrics - Annual

Source: Company;

Note : * ARPU & hardware subsidy taken as Q4 data for respective years. # Market share based on gross subscribers as on 31st December, 2015 as per market estimates

(R) Restated post netting off of collection charges

131 132 138 150 151

157 163

172

0

20

40

60

80

100

120

140

160

180

200

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15(R)

ARPU* (Rs.)

27%

20%

12%6% 19%

16%

Dish TV Tata Sky Sun Direct

Big TV Airtel Digital Videocon D2h

Market share #

1,933

1,688

0

400

800

1200

1600

2000

2400

FY14 FY15

Hardware subsidy* (Rs.)

2.5

4.3 5.7

8.5 9.6

10.7 11.4

12.9

0

5

10

15

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

Net subscriber base (mn.)

12

Key Metrics - Annual

Note : * Including prior period items

: (R) FY15 Subscription revenue is restated, netting off of collection charges

(2,084)(1,233)

1,117 2,380

4,960 5,794 6,240

7,331

-4000

-2000

0

2000

4000

6000

8000

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

EBITDA (Rs. mn.)

71%

59%52%

42%36% 34% 34% 33%

0%

10%

20%

30%

40%

50%

60%

70%

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15(R)

3,288 5,897

8,353

11,927

16,639 19,228

22,681 24,499

-

5,000

10,000

15,000

20,000

25,000

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15(R)

Subscription revenue (Rs. mn.)

Programming and other costs as % of subscription revenues

(4,141)(4,807)

(2,622)

(1,920)(1,331)

(660)(1,576)

31

-5500

-4500

-3500

-2500

-1500

-500

500

1500

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

Net profit/(loss) (Rs. mn.)

13

*

Key Metrics - Quarterly

0.4160.338 0.317

0

0.1

0.2

0.3

0.4

0.5

3QFY15 2QFY16 3QFY16

Net subscriber additions (mn.)

171 171 172

160

170

180

3QFY15 2QFY16 3QFY16

ARPU* (Rs.)

6,316

6,926 7,111

0

2000

4000

6000

8000

3QFY15 2QFY16 3QFY16

Subscription revenue (Rs. mn.)

1,908

2,550 2,654

27.6%

33.9% 34.4%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

0

500

1000

1500

2000

2500

3000

3QFY15 2QFY16 3QFY16

EBITDA (Rs. mn.) & EBITDA margin

(26)

870

685

-300

100

500

900

3QFY15 2QFY16 3QFY16

Net profit (Rs. mn.)

298

849

1,296

0

300

600

900

1200

1500

3QFY15 2QFY16 3QFY16

FCF (Rs. mn.)

14Note: * ARPU is post netting-off of collections charges. 3QFY16 ARPU is post impact of service tax hike from 12.36% to 14% w.e.f.June’15 & additional Swachh Bharat Cess of 0.5% w.e.f. November’2015.

Strategy and Outlook

15

DAS Phase III & IV

Zing DigitalPresent in 8 regional

markets

16

Specific vernacular markets

‘Zing’

Set-Top-Box

matlab DishTV

Dish99Packs starting @ just ₹ 99

MANDATORY subscription to a minimum 3 of the above mentioned

add-on packs on subscribing to

Dish 99

Any of the Family add-on packs

@ ₹ 25 each p.m.

Any of the Sports add-on packs

@ ₹ 50 each p.m.

Any of the English add-on packs

@ ₹ 75 each p.m.

Across phase III & IV markets

‘Dish 99’

Regional first; regional language channels , regional look and feelFTA channels + any 3 of Family / Sports / English

OR

OR

Easy transition for first time digital subscribers

Value for money offering; digital quality picture at the price of cable

Customized content in digital quality

Healthy margins

+

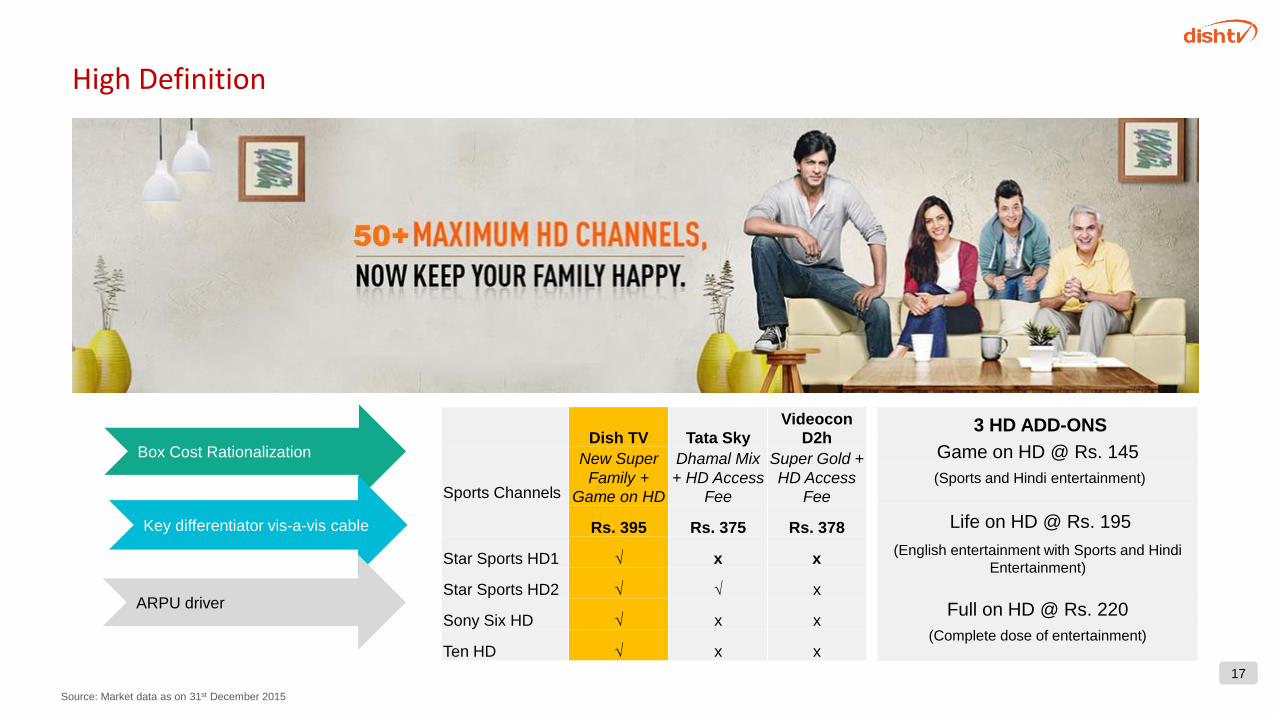

3 HD ADD-ONS

Game on HD @ Rs. 145

(Sports and Hindi entertainment)

Life on HD @ Rs. 195

(English entertainment with Sports and Hindi

Entertainment)

Full on HD @ Rs. 220

(Complete dose of entertainment)

Dish TV Tata Sky

Videocon

D2h

Sports Channels

New Super

Family +

Game on HD

Dhamal Mix

+ HD Access

Fee

Super Gold +

HD Access

Fee

Rs. 395 Rs. 375 Rs. 378

Star Sports HD1 √ x x

Star Sports HD2 √ √ x

Sony Six HD √ x x

Ten HD √ x x

High Definition

Source: Market data as on 31st December 2015

17

Box Cost Rationalization

Key differentiator vis-a-vis cable

ARPU driver

23, 70%3, 9%

7, 21%

DTH revenue Cable TV revenue IPTV revenue

151

579

976

122

435

730

22 54 133

7 90 113

-

200

400

600

800

1,000

2008 2014E 2020E

Pay TV Subs DTH Subs Cable Subs IPTV Subs

International Expansion - Sri Lanka

Sri Lanka

Population ~ 20 million

TV penetration at 77%

High digital penetration; 90% of total Pay

TV subscribers

DTH maintains dominance with ~ 72%

market share. Cable, distant second

despite being 4 years older

ARPU ~ USD 7 pm

Zero subsidy on CPE sales

Source: MPA 2014

Pay TV industry revenue (USD mn.)

Pay TV subscribers (000)

18

Financials

19

Quarter ended

Quarter ended

Rs. million Dec. – 2014 Dec. – 2015

Operating revenues 6,901 7,715

Expenditure 4,993 5,060

EBITDA 1,908 2,654

EBITDA margin (%) 27.6 34.4

Other income 170 42

Depreciation 1,616 1,463

Financial expenses 478 549

Profit / (Loss) before prior period & tax (16) 685

Prior period items - -

Tax expense/(write back) 10 -

Net Profit / (Loss) for the period (26) 685

3QFY 2015 vs. 3QFY 2016Operating revenue break-up

(Rs. mn)

3QFY - 2016

Summarized Consolidated P&L - Quarterly

20

11.8

1.3

39.1

(75.4)

(9.5)

14.7

Variance(3QFY15 vs.3QFY16) in %

7,111

99

281 129 95

Subscriptionrevenue

Lease rentals

Bandwidthcharges

Advertisementincome

Teleportservices, CPE& Other

Rs. million Sept. 2015 (Unaudited)

EQUITY AND LIABILITIES

Shareholders’ funds

(a) Share capital 1,066

(b) Reserves and surplus (2,773)

(1,707)

Non-current liabilities

(a) Long-term borrowings 7,549

(b) Other long term liabilities 519

(c) Long-term provisions 174

8,243

Current liabilities

(a) Short-term borrowings 166

(b) Trade payables 2,036

(c) Other current liabilities 14,988

(d) Short-term provisions 10,491

27,682Total 34,217

Consolidated Balance Sheet

21

Rs. million Sept. 2015 (unaudited)

ASSETS

Non-current assets

(a) Fixed assets

(i) Tangible assets 16,124

(ii) Intangible assets 96

(iii) Capital work-in-progress 5,015

(b) Non-current investments 2,000

(c) Long-term loans and advances 2,971

(d) Other non-current assets 312

26,518

Current assets

(a) Current investments -

(b) Inventories 202

(c) Trade receivables 852

(d) Cash and bank balances 3,091

(e) Short-term loans and advances 3,348

(f) Other current assets 206

7,700

Total 34,217

Consolidated Balance Sheet (continued)

22

Annexure

23

One of India's largest vertically integrated media and entertainment group, and also one of the leading producers, content aggregators and distributors of

Indian programming globally

One of the largest producers and aggregators of Hindi programming in the world

Other Businesses

Essel Group

Media

Launched in 1992

One of India’s largest media

and general TV entertainment

network

Launched in 1992

Strong presence in national

and regional news genre

Founded by Dr. Subhash Chandra

Group Market Cap ( Listed entities under Essel Group ): Rs 534.4 bn(1)

Source: Company websites, BSE, MPA Report 2014

Note: (1) Market capitalization as on 5th February, 2016

Market Cap: Rs 391.3 bn(1) Market Cap: Rs 8.9 bn(1)

Launched in 2005

Asia’s largest DTH service

provider

Launched in 2006

One of India’s largest MSO,

presence across 54 cities

Daily News & Analysis

Market Cap: Rs 85.6 bn(1) Market Cap: Rs 24.2 bn(1)

Launched in 2005

English broadsheet daily with

presence across Mumbai,

Bangalore, Pune,

Ahmedabad, Jaipur & Indore

Content Distribution

Launched in 1976, Essel Group is one of India’s largest business houses, with a dominant presence in Media

Zee Entertainment Zee Media Corp. Ltd. Dish TV SITI Cable Network

Packaging (Essel Propack)

– Market Cap: Rs 24.4 bn(1)

Theme Parks: Essel World and

Water Kingdom

Playwin: India’s first and largest

online gaming company

Cornership: Animation studio

Cyquator Technologies: IT

Infrastructure outsourcing

Infrastructure

Education

Precious Metals

Healthy Lifestyle & Wellness

Essel Group

24

Thank You

25