diversified uranium developerazargauranium.com/wp-content/uploads/page/azz.pdf · shares...

TRANSCRIPT

Diversified uranium developer Investor Presentation – November 2014

TSX: AZZ / FRA: P8AA

2

Disclaimer / safe harbor statement

Certain statements in this presentation are forward-looking statements, which reflect the expectations of management regarding Azarga Uranium Corp. (“Azarga” or the “Company”)'s future operations. Forward-looking statements consist of statements that are not purely historical, including any statements regarding beliefs, plans, expectations or intentions regarding the future. Such statements may include, but are not limited to, statements with respect to the future financial or operating performance of the Company and its mineral projects, the estimation of mineral resources, the timing and amount of estimated future production and capital, operating and exploration expenditures. Such statements are subject to risks and uncertainties that may cause actual results, performance or developments to differ materially from those contained in the statements. No assurance can be given that any of the events anticipated by the forward-looking statements will occur or, if they do occur, what benefits the Company will obtain from them. These forward-looking statements reflect management's current views and are based on certain expectations, estimates and assumptions which may prove to be incorrect, including that permits required for the Company’s operations will be obtained in a timely basis, that skilled personnel and contractors will be available as the Company’s operations continue to grow, that the price of uranium will be at levels that render the Company’s mineral projects economic and that the Company will be able to continue raising the necessary capital to finance its operations and realize on mineral resource estimates. A number of risks and uncertainties could cause our actual results to differ materially from those expressed or implied by the forward-looking statements, including: (1) a downturn in general economic conditions in North America and internationally; (2) the inherent uncertainties and speculative nature associated with uranium exploration; (3) a decreased demand for uranium; (4) any number of events or causes which may delay or cease exploration and development of the Company's property interests, such as environmental liabilities, weather, mechanical failures, safety concerns and labour problems; (5) the risk that the Company does not execute its business plan; (6) an inability to retain key employees; (7) an inability to finance operations and growth; (8) an inability to obtain all necessary environmental and regulatory approvals; (9) an increase in the number of competitors with larger resources; and (10) other factors beyond the Company's control. These forward-looking statements are made as of the date of this presentation and, except as required by applicable securities laws, the Company assumes no obligation to update these forward-looking statements, or to update the reasons why actual results differed from those projected in the forward-looking statements. Additional information about these and other assumptions, risks and uncertainties are set out in the "Risks and Uncertainties" section in the Company's MD&A filed with Canadian security regulators. Certain technical data in this presentation was taken from the technical report entitled “NI 43-101 Technical Report and Preliminary Economic Assessment for the Dewey-Burdock Project, Custer and Fall Counties, South Dakota” dated April 2012, prepared by Allan V. Moran, R.G., CPG of SRK Consulting, Frank A. Daviess, MAusIMM, and John I. Kyle, P.E. of Lyntek Incorporated (the “Technical Report and PEA”) and is subject to all of the assumptions, qualifications and procedures described therein. The Technical Report and PEA is preliminary in nature and includes inferred mineral resources that are considered too speculative in geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves. There is no certainty that the results of the Technical Report and PEA will be realized. Mr. Richard Clement is the Qualified Person who supervised the preparation of the exploration technical data in this presentation. This presentation shall not constitute an offer to sell or the solicitation of an offer to buy securities.

3

Azarga Uranium overview

§ October: Reverse merger listing on TSX, with C$5m placement at C$0.60/share § August: Data purchase agreement with Energy Fuels § April: Final Nuclear Regulatory Commission license issued for Dewey Burdock

§ Highest grade US in-situ recovery (ISR) development mine § Partially permitted with first production and revenue planned 2016/17 § PEA with US$109.1m NPV1

Centennial Project

§ PEA with US$51.8m NPV2

§ Revised mine plan being prepared to move to permitting

Investments

§ US$5.2m of investment holdings in Anatolia Energy (ASX: AEK) and Black Range Minerals (ASX: BLR)

Centennial

Investments

Dewey Burdock

Last 12-Months Achievements

Notes: 1. Source: NI 43-101 Preliminary Economic Assessment Dewey-Burdock Project, SRK, 17 April 2012. 2. Source: NI 43-101 Preliminary Assessment Powertech Uranium Corp. Centennial Uranium Project Weld County, Colorado, SRK, 2 June 2010.

TSX: AZZ

4

Capital structure and key people

Share price (TSX: AZZ)1 C$0.49/share

Shares outstanding 59.4m

Market cap (CAD) C$29.1m

Market cap (USD) US$25.9m

Long term debt2 US$1.8m

Cash2 US$4.1m

Enterprise value US$23.6m Notes: 1. As at 5 November 2014. 2. Pro-forma as at 31 October 2014.

Capitalization summary Key people

§ CEO SouthGobi Resources (2009-2012) (Ivanhoe Group) § 10-years+ as a specialist resources banker, 5-years as a minerals

industry senior executive and entrepreneur

Insiders / management 29.8%

Blumont Group (SGX: A33) 30.4%

Key shareholders

Alexander Molyneux, Chairman and founder Azarga Group

§ Professional geologist with 35-years+ experience in uranium § CEO of Powertech Uranium since 2006

Richard Clement, CEO and Director

§ 20-years+ experience in design, construction and operation of ISR uranium mines

§ Formerly Chief Mining Engineer, UrAsia Energy, Superintendent of Wellfield Construction, Smith Ranch / Highland project

John Mays, COO

§ 18-years mining and exploration experience, 8-years based in Central Asia

Curtis Church, VP International Operations and Director

§ SouthGobi Resources (2009-2013) including Finance Director and prior Deloitte in Audit and Financial Advisory practices

Blake Steele, CFO

5

Uranium A positive outlook

Uranium spot price and analysts’ forecast

US$/lb

Source: TradeTech for historical spot. Analysts’ forecast is based on average of 17 analyst forecasts as shown in latest available reports (analysts include: BAML; BMO; Cantor; CIBC; CIMB; Comark; CS; Dundee; JPM; Raymond James; RBC; RFC Ambrian; Salman; Scotiabank; TD; and UBS).

§ 2014 spot price range US$28-37/lb – A nine-year low

§ Price driven down by post-Fukushima demand withdrawal (black swan event)

§ Nuclear power is growing and will hit record in 2017 – 72 reactors under construction in BRICS, Middle East, USA and others)

§ Demand growth of 4-5% per year to 2020 is low-risk – Construction already commenced

§ Supply cut back in downturn – Kaylekera and Honeymoon shutdown, Areva and Cameco on growth moratoria

§ Supply deficit predicted 2017 to beyond the end of the decade

§ Mined supply +40% needed to address deficit by 2020 but current price levels don’t support any growth – Incentive price of US$80/lb+ required

20

30

40

50

60

70

80

Nov

-09

Jun-

10

Jan-

11

Aug

-11

Mar

-12

Oct

-12

May

-13

Dec

-13

Jul-1

4 Fe

b-15

S

ep-1

5 A

pr-1

6 N

ov-1

6 Ju

n-17

Ja

n-18

A

ug-1

8

39

48

57

67 Fukushima

Uranium at nine-year low

Analysts’ forecast

6

Uranium The start of a big market inflection could be happening now

§ Fukushima impacted demand more than just the loss of Japan’s 23m lbs of annual demand – Non-Japan utilities cut purchases due to concern Japan’s 100m lbs inventory might hit the market

§ Demand was literally crushed – Observed uranium transactions dropped to average of c. 100m lbs for each of 2013 and 2014 YTD vs. typical levels of 200m lbs+ per year

§ Fuel buyers are now becoming more confident Japan will re-start – Sendai has received NRA approval and a favorable local district vote

§ China is looming larger (eg, purchase of 25% of Paladin’s Langer Heinrich Mine and contract to buy Uzbek uranium) – Commentary in China suggests additional nuclear construction approvals beyond what’s already forecast (ie, 68Gw vs 58Gw by 2020)

§ Severity of last two years downturn means miners will not close the supply deficit until beyond 2020

§ 12 to 18-month cycle to convert U3O8 into nuclear fuel means utilities will be covering the deficit years needs in 2015 and 2016

§ Analysts may well be underestimating the speed and scale of the move up in price – In early 2006 when uranium was in mid-US$30s, analysts were projecting a move to US$50/lb in 2008 for a looming deficit… BUT by mid-2007, prices were already above US$130/lb!!!

Conventional vs. ISR grade and cash cost comparison using Cameco as a guide

7

Uranium Key to uranium investment is that grade is not king!... ISR mining amenability is!

§ In-situ recovery (ISR) has been the fastest growing source of uranium production – Now >48% of global total production

§ No movement of rock, no dust or tailings § Solution is pumped into the ground and

returns to surface containing the dissolved uranium particles

§ Average global cash costs are c. 25% cheaper than non-ISR

§ Capital costs per lb of production around 65% cheaper

§ New projects in Athabasca can be high-grade but in general fail to achieve project economics of ISR in USA or Kazakhstan

§ Only sandstone hosted deposits with the right hydrological and geological conditions are amenable to ISR

0

10

20

0

10

20

30

McArthur River &

Key Lake

Cigar Lake

Inkai Nebraska &

Wyoming

Conventional ISR

Res

erve

s gr

ade

(% U

3O8)

C

ash

cost

(U

S$/

lb)

Ave = 17.3%

Ave = 0.1%

Ave = US$23/lb Ave = US$21/lb

Grades of Athabasca assets average 200x more than ISR… BUT ISR has 10% lower cash cost!

Notes: Data sourced from Dundee’s Cameco research note of 29 October 2014. Cash cost numbers are 2016’F to take into account when all comparable assets are in steady state production (ie, after Cigar Lake has ramped up to 8m lb pa).

8

þ Highest grade Highest grade of projects in North American ISR focused companies

ISR mining In-situ recovery (ISR) is the preferred route for low cost uranium production – Now 48% of global uranium production

Low capex Initial capital expenditure of US$42.5m1 (approximately US$5/lb of U3O8 production)

Competitive operating costs

Total ‘all in’ operating cash costs of US$29/lb1 – below the midpoint for global primary uranium production

Moving to the construction

phase

Nuclear Regulatory Commission license issued April 2014 – Now finalizing EPA and South Dakota state permits

þ þ þ þ

Note: 1. Source: NI 43-101 Preliminary Economic Assessment Dewey-Burdock Project, SRK, 17 April 2012 – excluding contingency.

Dewey Burdock: Premier US ISR project Key features highlight Dewey Burdock as a premier near-term US ISR project

9

Commentary Location

§ Edgemont uranium district discovered in 1950s

§ Azarga controls US federal claims, private minerals rights and surface rights covering approximately 18,000 acres

§ Previous operator, Tennessee Valley Authority drilled more than 4,000 holes

§ 88 miles of measured ore trends – only 18 miles drilled to date

NI 43-101 Resources

Category

Indicated

Inferred

Contained U3O8 (lbs)

6,684,285

4,525,500

Average grade

0.214%

0.179%

Dewey Burdock: Premier US ISR project Located in Edgemont, South Dakota directly adjacent to Wyoming border

10

Potential for optimization Summary of existing PEA1

1.0m lbs Annual U3O8 production

9 years Mine life

8.4m lbs Total LOM production2

US$42.5m or US$5/lb Initial capital expenditure3

US$29.00/lb

US$13.17/lb US$3.91/lb US$2.07/lb US$2.37/lb US$7.48/lb

Cash operating costs3 - Well fields (incl. development) - CPP / ponds - Restoration / De-commissioning - Site management / overhead - Production taxes and royalties

US$194.9m Free cash flow4

US$109.1m Pre-tax NPV (8% discount)4

48% IRR3 Notes: 1. Source: NI 43-101 Preliminary Economic Assessment Dewey-Burdock Project, SRK, 17 April 2012. 2. Includes some Inferred Resources in production. 3. Excluding contingency. 3. At US$65/lb uranium price and including a 20% contingency on costs and capital expenditure.

Phased ramp-up

§ Phased start-up of first well field over a three year period instead of one year period

§ Central processing plant delayed until the third year

§ Internal modeling suggests first three years capital expenditure can be significantly reduced

§ Lower initial capital expenditures could result a significant NPV enhancement

Vanadium recovery

§ Resource doesn’t include vanadium – not enough vanadium sampling completed - but assay results indicate that vanadium is present

§ Historical production at Edgemont averaged 1.5lbs vanadium per 1lb of uranium

TREC has been retained to update the PEA for Q4 2014

Dewey Burdock: Premier US ISR project Robust project economics mean project is feasible in a low uranium price environment

11

Project

Azarga Uranium

8.4m lbs 28.0m lbs 3.3m lbs

0.21% 0.05% 0.11% 0.05%

9.2m lbs

Lance2 Dewey Burdock1 Nichols Ranch3 Lost Creek4

Owner Peninsula Energy Uranerz Ur-Energy

Resource grade

Total LOM production

US$4/lb US$10/lb Initial capex US$5/lb US$5/lb

Cash costs (excl. tax and royalty)5 US$19.51/lb US$21.52/lb US$24.31/lb US$23.82/lb

Cash costs (incl. tax and royalty)5 US$23.48/lb US$29.00/lb US$30.65 US$34.79/lb

Notes: 1. Source: NI 43-101 Preliminary Economic Assessment Dewey-Burdock Project, SRK, 17 April 2012. Includes some Inferred Resources in production. 2. Sources: Lance Feasibility Study, 3 May 2012; Optimization Study, 21 March 2013; and Wellfield Optimization Study, 9 September 2013. 3. Sources: Preliminary Assessment Nichols Ranch In-Situ Recovery Project Powder River Basin, Wyoming USA, 25 July 2008. 4. Source: Preliminary Economic Assessment of The Lost Creek Property, Sweetwater County, Wyoming, 30 December 2013. 5. Well field development post initial production is included and where possible, contingencies have been excluded.

Dewey Burdock: Premier US ISR project Highest grade among peers, with other features comparing well

12

EPA: Draft permits in Q1 2015, final in Q2 2015

2014 2015

Current anticipated project timeline: permitting complete by late-2015, production 2016/17

NRC: Final license

issued Apr 8 SD State: Q2/Q3 2015 hearings for water rights and large-scale mining

SD State: BLM Plan of

Operations issued Q1 2015

1

þ

2

3

§ NRC license has been issued § Once EPA issues its permits, South Dakota can proceed to finalize its permits § Project construction timeline of approximately 12-months, 2016 production remains

feasible

Dewey Burdock: Premier US ISR project Moving towards the construction phase

13

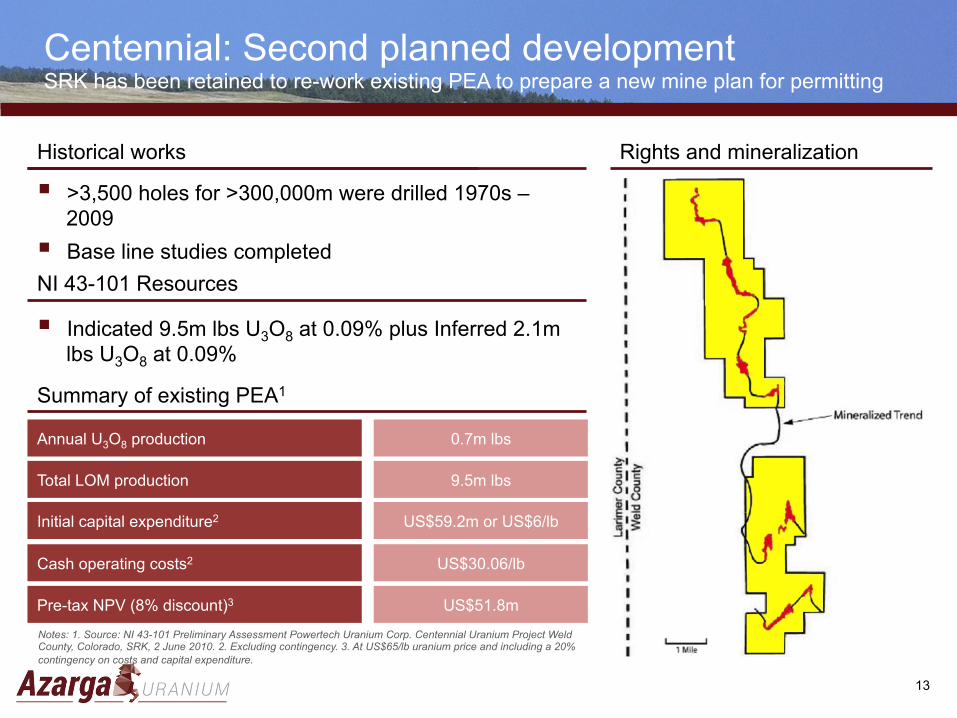

§ >3,500 holes for >300,000m were drilled 1970s – 2009

§ Base line studies completed

Rights and mineralization Historical works

NI 43-101 Resources

§ Indicated 9.5m lbs U3O8 at 0.09% plus Inferred 2.1m lbs U3O8 at 0.09%

0.7m lbs Annual U3O8 production

9.5m lbs Total LOM production

US$59.2m or US$6/lb Initial capital expenditure2

US$30.06/lb Cash operating costs2

Summary of existing PEA1

US$51.8m Pre-tax NPV (8% discount)3

Notes: 1. Source: NI 43-101 Preliminary Assessment Powertech Uranium Corp. Centennial Uranium Project Weld County, Colorado, SRK, 2 June 2010. 2. Excluding contingency. 3. At US$65/lb uranium price and including a 20% contingency on costs and capital expenditure.

Centennial: Second planned development SRK has been retained to re-work existing PEA to prepare a new mine plan for permitting

14

Investments US$5.2m of current market value and large strategic shareholdings of two promising players

§ Owner of Temrezli ISR project in Turkey: § 11.3m lbs Measured plus Indicated Resource at 0.13%

U3O8 and 2.0m lbs Inferred Resource at 0.09% U3O81

§ PEA1 for 1m lb per year U3O8 production for 10 years with NPV8 of US$187m and IRR of 109% at US$60/lb uranium

§ Operating license in place

Investment Commentary

ASX: AEK Azarga int: 12% Value: US$2.1m

ASX: BLR Azarga int: 19% Value: US$3.1m

§ Owner of Hansen / Tayor Ranch deposit in Colorado: Indicated Resources are 39.4m lbs at 0.062% uranium plus Inferred of 51.0m lbs at 0.058%2

§ 50% owner of ‘game changing’ Ablation processing technology being commercialized in Casper, Wyoming (see Appendix: 4.2)

Notes: 1. Source: Temrezli ISR Uranium Project Peliminary Economic Assessment UPDATE, WWC Engineering, 8 May 2014. 2. Source: Hansen / Taylor Ranch Uranium Project – JORC Code 2012 Mineral Resource Estimate, Rex C. Bryan, 23 April 2014.

15

Next steps Key upcoming catalysts will lead to value improvement and de-risking of our assets

§ EPA draft permit and then finalization – Anticipated Q1 2015 and Q2 2015 respectively

§ South Dakota permits – Anticipated Q2/Q3 2015

1 Dewey Burdock permitting

§ Revised TREC PEA – Expected Q4 2014

2 Dewey Burdock project economics

§ Revised SRK PEA – Expected Q2 2015

3 Centennial plan and project economics

Peer trading comparison Sum-of-the-parts valuation

16

Trading valuations of US asset owner peers

Notes: Share prices selected as at 3 November 2014. Net debt calculated based on last reported. Resources are calculated as the sum of Measured plus Indicated NI 43-101 Resources other than for Peninsula where it is the sum of Measured plus Indicated JORC Resources.

§ Using project PEA NPVs for DB and Cent. plus market value of investments and book value of net debt implies a value assessment 8x current level

Two ways to look at value Azarga Uranium appears undervalued on a peer comparison and absolute basis

EV

/ R

esou

rces

(Mea

s. +

Ind.

)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Ave = US$3.1/lb

§ Azarga currently trades at US$1.1 per pound of Measured plus Indicated Resources – A 3x re-rating would bring it in line with peers

0 20 40 60 80

100 120 140 160 180

1091

522 53 24 168

Equity valuation – Proj. NPVs and market ?

US

$m

Actual current market cap (US$21.2m)

Notes: 1, Source: NI 43-101 Preliminary Economic Assessment Dewey-Burdock Project, SRK, 17 April 2012. 2. Source: NI 43-101 Preliminary Assessment Powertech Uranium Corp. Centennial Uranium Project Weld County, Colorado, SRK, 2 June 2010. 3. Market value as at 3 November 2014. 4. Balance sheet pro-forma as at 31 October 2014.

17

Appendix 1

Resources

18

U3O8 (m lbs) Grade

U3O8 (m lbs) Grade

U3O8 (m lbs) Grade

U3O8 (m lbs) Grade

Summary of NI 43-101 Resources1

Measured Inferred Meas. + Ind. Indicated

Project

Dewey Burdock (100% – SD, USA) – – 6.68 0.214% 6.68 0.214% 4.53 0.179%

Centennial2 (100% – CO, USA) – – 10.61 0.086% 10.61 0.086% 1.94 0.077%

Aladdin (100% – WY, USA) – – 1.04 0.111% 1.04 0.111% 0.10 0.119%

Kyzyl Ompul (80% – Kyrgyz Republic) – – – – – – 7.51 0.023%

Total – – 18.33 0.134% 18.33 0.134% 14.08 0.081%

Notes: 1. Source: NI 43-101 technical reports published on the Company’s website and SEDAR. 2. Centennial resource figures have been reduced from those published in most recent technical report due to the expiry of an option over rights covering some resources.

Resources

19

Appendix 2

Management and Directors

20

Alexander Molyneux (Chairman)

§ Chairman of Celsius Coal (ASX: CLA) 2012 – , Director of Goldrock Mines (TSX-V: GRM) 2012 – , Director of Ivanhoe Energy (TSX: IE) 2010 – 2014

§ CEO of SouthGobi Resources (TSX: SGQ) (Ivanhoe Mines Group) 2009 – 2012

§ 10-years+ experience as a specialist natural resources investment banker, 5-years as a minerals industry senior executive and entrepreneur

Richard Clement Jr. (CEO, Director)

§ CEO of Powertech Uranium Corp since 2006

§ Professional geologist with 35-years+ experience in uranium recovery

§ Experience covers exploration, development and production in Australia and USA

Blake Steele (Chief Financial Officer)

§ Former SouthGobi Resources (2009-2013) including Finance Director and prior Deloitte in Audit and Financial Advisory practices

§ Canadian Chartered Accountant and Chartered Business Valuator

Curtis Church (VP International

Operations, Director)

§ SouthGobi Resources 2008-2012, including COO

§ 18-years mining and exploration experience, 8-years based in Central Asia

John Mays (Chief Operating Officer)

§ 20-years+ experience in design, construction and operation of ISR uranium mines world-wide

§ Former Chief In-Situ Mining Engineer, UrAsia Energy, former Superintendent of Wellfield Construction, Power Resources’ Smith Ranch / Highland project

Senior management

21

Douglas Eacrett (Independent Director)

§ 20-years+ experience in corporate securities law and 30-years+ experience as a Chartered Accountant

§ Has extensive public company CFO and Company Secretary experience

Joseph Havlin (Director)

Paul Struijk (Independent Director)

§ Formerly Executive Director, Winsway Coking Coal Holdings (HKEX: 1733)

§ Interim CEO of Grand Cache Coal following its acquisition by Winsway

Matthew O’Kane (Independent Director)

§ CFO of Celsius Coal (ASX: CLA)

§ Previously VP and then CFO of SouthGobi Resources (2011-2012)

§ 18-years+ experience in finance roles in mining and manufacturing industries

§ Experience covers exploration, development and production in Australia and USA § 25-years+ US CPA, former CFO Alpha Prime Development and Asian American Coal

§ Direct underground mining experience and extensive mining finance experience

Independent and Non-Executive Directors

22

Appendix 3

Exploration assets

23

Aladdin1 Dewey Terrace

§ 13,000 acres of claims covering the extension of Dewey Burdock

§ Extensive 1970s and 1980s drilling including data acquired from Teton – 298 drill holes, with 208,500 feet logged

§ 20 new holes were drilled confirming the presence of several zones of uranium mineralization

§ Dewey Terrace likely contains uranium prospects that could extend the useful life of Dewey Burdock Project

§ 15,000 acres in Crook County (same county as Peninsula’s Lance Project)

§ NI 43-101 Resources: Indicated 1.0m lbs U3O8 at 0.11% plus Inferred 0.1m lbs U3O8 at 0.12%

§ Conceptual resource potential estimated at 5-11m lbs in the range of 0.11-0.12% U3O8

Savageton

§ 6,000 acres in Campbell County (same county as Uranium One’s Moore Ranch and Uranerz’s Nichols Ranch)

§ Historic resource of approximately 1.0m lbs U3O8 was calculated in 1976 by data generated by Getty Oil Company

Note: 1. Source: NI 43-101 Technical Report on the Aladdin Uranium Project Cook County, Wyoming, Jerry D. Bush, 21 June 2012.

Wyoming exploration Dewey Terrace extension of Dewey Burdock and two additional locations

Commentary

24

Kyrgyz Republic in Central Asia

§ Three exploration licenses comprising over 200,000 acres

§ Kyzyl Ompul license NI 43-101 Resources: Inferred 7.5m lbs U3O8 at 0.02%1

§ Conceptual resource increase target of 1.9-6.5m lbs on immediately adjacent areas1

§ Key themes for Kyrgyz exploration: § Strategic location – Operating

uranium mill in country (265km away by rail) and close to China

§ Prospective for rare earths – 2012-2013 physical exploration (incl. drilling) showed a number of prospective rare earths results

Project area

China

Kazakhstan

Kara Balta uranium processing facility

KCMP rare earth processing facility

Railway

Legend:

Note: 1. Source: NI 43-101 Technical Report on the Kyzul Ompul License, Kyrgyz Republic, Ravensgate Mining Industry Consultants, 14 April 2014.

Kyrgyzstan exploration Kyzyl Ompul license in Kyrgyzstan hosts the largest known uranium deposit in that country

25

Appendix 4

Investments

26

Appendix 4.1

Anatolia Energy (ASX: AEK) – 12%

§ Anatolia has a market capitalization of approximately US$20m and its main asset is the Temrezli uranium deposit in Turkey

§ About Temrezli § 11.3m lbs Measured plus Indicated Resource at 0.13% U3O8 and 2.0m lbs Inferred

Resource at 0.09% U3O81

§ Average depth <100m production potential for around 1m lbs uranium per year § Has operating license (equivalent of mine license) § Substantial exploration upside

§ Class leading project economics1

§ PEA for 1m lbs per year U3O8 production for 10 years § Capital expenditure US$30m and cash costs of US$20.22/lb § NPV8 of US$187m and IRR of 109% at US$60/lb uranium price § NPV8 of US$76m and IRR of 65% at US$40/lb uranium price

§ Turkey approved a nuclear program with the first construction contracts of eight planned reactors initiated – strong support for Anatolia from Turkish government and institutions

27

Note: 1. Source: Temrezli ISR Uranium Project Peliminary Economic Assessment UPDATE, WWC Engineering, 8 May 2014.

Overview Sector leading project economics for ISR that’s viable at current uranium price levels

28

Appendix 4.2

Black Range Minerals (ASX: BLR) – 19%

§ Hansen Indicated Resources are 39.4m lbs at 0.062% uranium plus Inferred of 51.0m lbs at 0.058%1

§ Plan to commence production within the Hansen sub-deposit

§ Production by underground borehole mining combined with Ablation and conventional milling § 7-8 years production of 2m lbs

uranium (U3O8) per year § Cash costs c. US$27/lb § Pre-production capex

US$45m § NPV8 c. US$224m and IRR

123%

29

Hansen / Taylor Ranch sub-deposits Commentary

Note: 1. Source: Hansen / Taylor Ranch Uranium Project – JORC Code 2012 Mineral Resource Estimate, Rex C. Bryan, 23 April 2014.

Hansen / Taylor Ranch deposit Fully explored deposit in Colorado ready to commence permitting in 2017

30

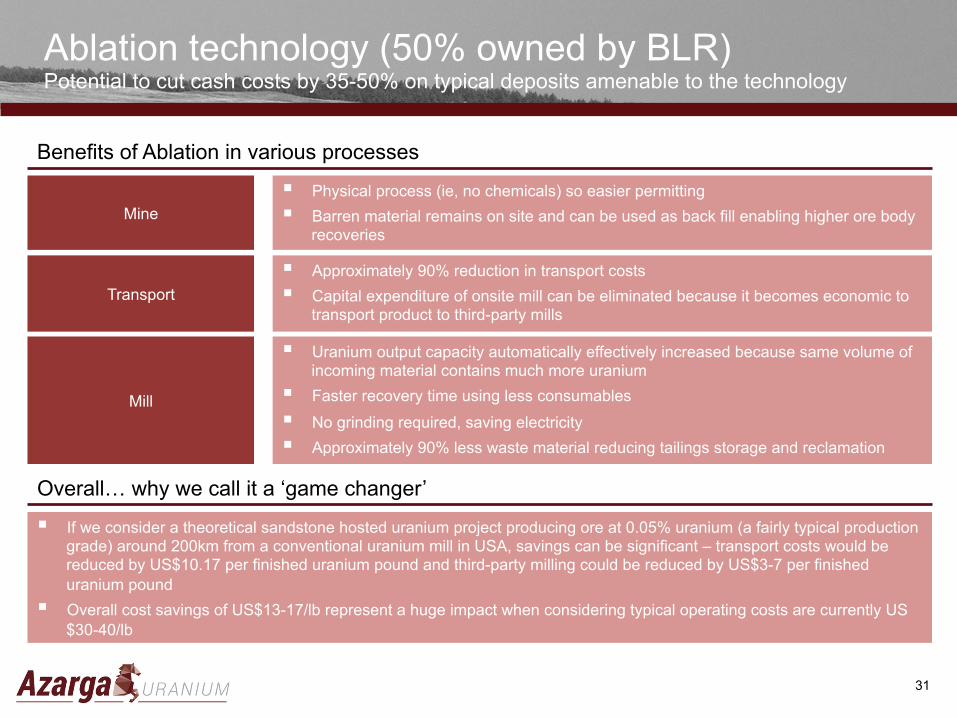

§ Applicable to sandstone hosted uranium deposits – uranium minerals are present as a patina (outer coating) around individual sand grains within mineralized sandstone rock

§ Uses kinetic energy and water to force sand grains to collide with each other, breaking off the patina leaving intact barren sand grains

§ Fine uranium mineralized material then separated from barren sand grains with screening § Test work consistently recovers 90-95% of uranium into concentrate with 90% mass

reduction – recoveries can also be improved towards 99% with secondary circuit § Low-volume concentrate can economically be transported to mill for processing to salable

yellowcake

Post-Ablation barren material

Pre-Ablation ore

Ablation technology (50% owned by BLR) Unique physical pre-concentration technology invented in USA

31

Benefits of Ablation in various processes

Mine § Physical process (ie, no chemicals) so easier permitting § Barren material remains on site and can be used as back fill enabling higher ore body

recoveries

Transport § Approximately 90% reduction in transport costs § Capital expenditure of onsite mill can be eliminated because it becomes economic to

transport product to third-party mills

Mill

§ Uranium output capacity automatically effectively increased because same volume of incoming material contains much more uranium

§ Faster recovery time using less consumables

§ No grinding required, saving electricity § Approximately 90% less waste material reducing tailings storage and reclamation

Overall… why we call it a ‘game changer’

§ If we consider a theoretical sandstone hosted uranium project producing ore at 0.05% uranium (a fairly typical production grade) around 200km from a conventional uranium mill in USA, savings can be significant – transport costs would be reduced by US$10.17 per finished uranium pound and third-party milling could be reduced by US$3-7 per finished uranium pound

§ Overall cost savings of US$13-17/lb represent a huge impact when considering typical operating costs are currently US$30-40/lb

Potential to cut cash costs significantly by 35-50% on typical deposits amenable to the technology

Ablation technology (50% owned by BLR) Potential to cut cash costs by 35-50% on typical deposits amenable to the technology

Corporate office Powertech (USA) Inc. Suite #140, 5575 DTC Parkway Greenwood Village, Colorado USA 80111 International operations Azarga Uranium Corp. Level 5-1, Suite 9, Sun’s Group Centre 200 Gloucester Road Wanchai Hong Kong SAR Jenya Mesh, Manager Investor and Public Relations Tel: +852 6466 6218/ +1 416 625 6686 Email: [email protected] Web: www.azargauranium.com Twitter: @AzargaUranium