dividends: the case for income-oriented investors

TRANSCRIPT

Investment products: No bank guarantee I Not FDIC insured I May lose value

G L O B A L E Q U I T I E S W H I T E PA P E R

OUTLINE

1 | The “value” of a dividend-investing strategy (page 2)

1.1 Dividends: the basics (page 2)

1.2 Dividends: a compelling source of potential return for

equities (page 3)

1.3 Dividends: attractive risk characteristics (page 5)

1.4 Dividends: a global opportunity (page 7)

1.5 Sustainability of dividends (page 9)

1.6 Dividends as inflation or deflation hedge? (page 10)

2 | Potential buy signals for equities in times of low

bond yields (page 12)

2.1 Slow growth in developed markets increases

attractiveness of dividends (page 12)

2.2 Potential buy signal: flows (page 14)

2.3 Potential buy signal: equity yields vs. government bond

yields (page 15)

2.4 Potential buy signal: equity yields vs. corporate bond

yields (page 16)

3 | Conclusion (page 18)

After 30 years of perpetually declining interest rates, we

believe that the tailwind for fixed-income investments

is waning. Given today’s demographics—older, more

conservative investors seeking income—we believe income

alternatives such as dividend-paying stocks could come

into focus. Thus, in this white paper, we build the case for

dividend-paying stocks. In section 1, we first review the

value of a dividend-investing strategy: We highlight the

impact dividends have had on total equity returns in various

market environments as well as the relatively attractive

risk characteristics of dividend-paying stocks; we examine

the opportunity global dividend-paying stocks present to

enhance portfolios; and we look at the impact of inflation

and deflation on equities and the implications of utilizing a

dividend strategy. In section 2, we examine several potential

buy signals for equities, including a turnaround in fund flow

imbalances and attractive yields relative to bonds.

Dividends: the case for income-oriented investors

Today’s low fixed-income yields and expectations of prolonged slower growth in developed countries could lead to the re-emergence of dividend-paying stocks as an important component of investors’ portfolios. This white paper will explore three core concepts: the intrinsic value of dividend-investing strategies; alternative sources of yield in a low-interest-rate environment; and dividends as a potential inflation hedge.

A U G U S T 2 0 1 2

Contributors » Stephen Noll, CFA, senior product specialist

» David Wertheim, head of DWS U.S. product specialist team

» Kevin Walsh, product specialist

» Dr. Oliver Plein, head of DWS European product specialists (equities)

» Andreas Korsa, European product specialist (equities)

INTERNATIONAL/ GLOBAL EQUITY FUNDS

2 » Dividends: the case for income-oriented investors

GLOBAL EQUITIES WHITE PAPER I AUGUST 2012

1.1. DIVIDENDS: THE BASICS

Near-term changes in asset prices are difficult to predict, but

in this section, we consider the potential long-term benefits

of harnessing income by investing in equities. By investing

in income-generating equities, investors can participate in

real income growth coupled with long-term capital growth.

There are a number of reasons to consider companies

that pay regular dividends. First, dividends return cash to

shareholders, thereby creating confidence in economic

success. Second, scarce resources (such as earnings

after dividends) tend to be used more efficiently (as we

explain in more detail in section 1.5). Third, a consistent

dividend policy sends a strong message about continuity

and reliability. Fourth, dividends, unlike earnings, are rarely

cut, and may offer a cushion on the downside.

Do dividends matter? Yes, but investing in equities should

not be a gamble, and therefore investment decisions need

to be proven by evidence. According to T.H. Huxley, “The

deepest sin against the human mind is to believe things

without evidence.” Therefore it is vital to set forth a number

of studies, largely from academia, analyzing the importance

of dividends and the association of high dividend yields

with attractive investment returns over long periods.

Much has been written about dividends, and what is

contained herein is not meant to be an exhaustive analysis,

but rather a sampling of persuasive arguments examining

the impact of dividends on total investment returns. We

hope it will provide added insight and confidence, as it did to

us long ago, in pursuing a yield-oriented investment strategy.

One of the most important things corporations must

determine is how best to utilize the free cash flow

generated from their operations. Typically, they have

four options: reinvesting in their business to generate

future growth, repurchasing shares of their stock, paying

shareholders via cash dividends or leaving the cash on

1 I The “value” of a dividend strategy

their balance sheets. Which choice a company makes

reflects how management views the company’s growth

prospects, which in turn depends on what industry the

company is in, what stage of its lifecycle the company is

in and where the economy is within the business cycle.

Typically, young companies that are in the early stages

of their growth path need to retain their earnings in order

to reinvest in their business, and therefore tend to not

pay a dividend. In contrast, mature companies that have

achieved more stable cash flows may repurchase shares or

pay dividends. Dividends are often associated with quality

companies because paying regular dividends reflects

the company’s confidence that it will be able to support

payments via expected earnings.

Similarly, dividend policies tend to differ by industry.

Companies in capital-intensive industries, such as airlines,

engineering and construction, need to reinvest their cash

flow in order to support their business models; they

thus will rarely pay a dividend. Companies in industries

with stable cash flows, such as telecommunications and

utilities, typically pay high dividends.

Decisions to pay cash as dividends will also be impacted by

macroeconomic factors. During economic contractions, cash

flows of many cyclical companies are greatly diminished,

increasing these companies’ need to preserve capital in order

to ensure their future existence. During the most recent

recession, the availability of credit dried up, resulting in many

companies hoarding cash. However, in the current economic

environment, companies hold a record high amount of their

net worth in cash. Potential uses are illustrated in Figure 1.

FIGURE 1: POSSIBLE USES OF BALANCE-SHEET CASH

Cash on thebalance sheet

Mergers andacquisitions

Dividends

Share purchases Wage increasesCapital

expenditures

GLOBAL EQUITIES WHITE PAPER I AUGUST 2012

Dividends: the case for income-oriented investors » 3

1.2. DIVIDENDS: A COMPELLING SOURCE

OF POTENTIAL RETURN FOR EQUITIES

One of the most notable statistics about dividends is

the impact they have on long-term equity returns. The

reinvestment of dividends has accounted for 43.5% of

the total returns of the S&P 500 Index since 1926. Over

this period, the average annual price appreciation of the

S&P 500 Index was 5.56%. The return of the index with

Source: Morningstar as of 6/30/12. Performance is historical and does not guarantee future results. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. It is not possible to invest directly in an index. See page 19 for index definitions.

FIGURE 2: AVERAGE ANNUAL RETURNS OF THE S&P 500 INDEX (1/4/26–6/30/12)

Since 1926

2000s

1990s

1980s

1970s

1960s

1950s

1940s

1930s

Total returns

Dividends Price appreciation

–10% –5% 0% 5% 10% 15% 20%

4.28%9.84%

–0.95%

5.56%

1.77%

–2.72%

2.89%

15.32%

4.95%

12.59%

4.25%

1.60%

4.39%

5.77%

13.58%

6.18%

2.98%

5.21%

–5.27%

3.41%

18.21%

17.55%

5.86%

7.81%

9.17%

–0.05%

19.35%

dividends, in contrast, was 9.84%. Moreover, by dissecting

the returns of the S&P 500 Index by decade, we can see

that dividends helped cushion the equity price declines of

the 1930s and 2000s and also helped equity returns during

periods of moderate equity price appreciation—a scenario

that may be more realistic than the strong price appreciation

experienced in the 1980s and 1990s. (See Figure 2.)

4 » Dividends: the case for income-oriented investors

GLOBAL EQUITIES WHITE PAPER I AUGUST 2012

An even longer-term analysis appeared in the Financial

Analysts Journal in 2003. In “Dividends and the Three

Dwarfs,” Robert D. Arnott pointed out that from 1802 to

2002, dividends were by far the main source of the real

return from equities, dwarfing the other constituents, which

included inflation, rising valuation and real dividend growth.

From 1802 to 2002, the average annual return of equities was

7.9%, which broke down as follows: 5.0% from dividends,

1.4% from inflation, 0.8% from real dividend growth and

0.6% from rising valuations. The numbers show that 63%

of the total return of equities has come from dividends and

a combined 73% from dividends and dividend growth. The

author’s conclusion: “Unless corporate managers can provide

sharply higher real growth in earnings, dividends are the main

source of real return we expect from stocks.”

We admit that even for investors primarily focused on

strategic asset allocation, 200 years might not necessarily

be the correct investment horizon. Moreover, for yield

hunters who charge around in markets trying to guess

the next month´s earnings number, the dividend-investing

strategy seems completely irrelevant. However, for

investors between these poles, dividends may be a vital

and essential element of return. To illustrate the importance

of dividends, we review a paper written by James Montier,

a member of the asset management team at GMO, a

privately held global investment management firm, entitled

“A Man from a Different Time.” In it, Montier concludes

that over a one-year time horizon, only roughly 20% of the

total return of the S&P 500 Index has been generated by

dividend yield and real dividend growth. In contrast, roughly

80% has been generated by fluctuations in valuations.

Source: GMO as of August 2010. Performance is historical and does not guarantee future results. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. It is not possible to invest directly in an index. See page 19 for index definitions.

FIGURE 3: S&P 500 INDEX COMPONENT RETURNS BY TIME HORIZON (1971–AUGUST 2010)

0%

20%

40%

60%

80%

100%Change in valuation Change in valuation

Dividend growth

Dividend yieldDividend growth

Dividend yield

5-year1-year

If we switch to a five-year time horizon, the story looks

very different: Fundamentals now play a prominent role in

explaining total return, with the dividend camp accounting

for roughly 80% of the return. (See Figure 3.)

GLOBAL EQUITIES WHITE PAPER I AUGUST 2012

Dividends: the case for income-oriented investors » 5

FIGURE 5: DOWNSIDE AND UPSIDE CAPTURE RATIOS OF HIGH-DIVIDEND-YIELDERS (7/1/27–12/31/11)

1.3. DIVIDENDS: ATTRACTIVE RISK

CHARACTERISTICS

High-dividend-yielding stocks have also provided better

risk attributes than non-dividend-yielding stocks, including

lower volatility and stronger downside protection when

markets decline.

As figure 4 indicates, the standard deviation of high-

dividend-yielding stocks has been significantly lower

than that of non-dividend-yielding stocks over various

long-term periods.

Even more attractive has been the downside protection

provided by high-dividend-yielding stocks. Since 1927,

high-dividend-yielding stocks have held up better than the

broader market during downturns. In fact, the downside

capture ratio of high-dividend-yielding stocks has been

81% or lower over various long-term periods. Put another

way, during months that the S&P 500 Index declined,

dividend-yielding stocks declined by nearly 19% less than

the broader market. (See Figure 5)

Source: Kenneth French as of 12/31/11. Performance is historical and does not guarantee future results. Standard deviation is often used to represent the volatility of an investment; it depicts how widely an investment’s returns vary from the investment’s average return over a certain period. The higher the standard deviation, the greater the volatility. Downside capture ratio measures a portfolio’s performance in down markets relative to the investment universe (with down markets defined as those that have a negative monthly return); the lower the downside capture ratio, the better the portfolio performed during a market downturn. Upside capture ratio measures a portfolio’s performance in up markets relative to the investment universe (with up markets defined as those that have a positive monthly return); the higher the upside capture ratio, the better the portfolio performed during a market upturn. Non-dividend-yielders include all U.S. stocks that do not pay a dividend at the time of reconstitution. The remaining stocks are divided by dividend yield into three categories: highest 30%, middle 40% and lowest 30%. High-dividend-yielders are represented by the highest 30% of dividend yielders. Portfolios are reconstituted annually. Index returns assume reinvestment of all distributions and do not reflect fees |or expenses. It is not possible to invest directly in an index. See page 19 for index definitions.

FIGURE 4: STANDARD DEVIATION OF HIGH-DIVIDEND-YIELDERS VS. NON-DIVIDEND-YIELDERS (8/1/27–12/31/11)

High-dividend-yielders

Non-dividend- yielders

Since 1927 20.31% 30.34%

50-year 14.05% 24.59%

30-year 14.22% 22.90%

10-year 16.41% 19.96%

5-year 19.96% 21.99%

Upside capture ratio

Downside capture ratio

Since 1927 92.14 81.53

50-year 87.69 67.45

30-year 86.06 65.86

20-year 85.95 65.83

10-year 95.30 81.61

While the data in Figure 4 makes a compelling case for

high dividend-yielding stocks, one should not rely on

screening for the highest-yielding stocks. There are several

other characteristics that should also be considered, such

as sustainability of dividend as well as growth of dividends.

To illustrate, consider a recent study by Ned Davis Research,

which looked at the performance of dividend growers

vs. stable dividend payers (those with no change in

dividends) and dividend cutters. From 1/31/72 through

6/30/12, companies that grew their dividends significantly

outperformed companies that cut their dividends, with

annualized returns of 9.46% and –0.41%, respectively.

In addition, dividend growers outpaced stable dividend

payers by an annualized 2.48 percentage points over the

same period.

6 » Dividends: the case for income-oriented investors

GLOBAL EQUITIES WHITE PAPER I AUGUST 2012

The importance of dividends becomes even clearer when you consider the power of compounding those dividends

over time. An initial investment of $100 in non-dividend-yielding stocks starting in 1972 would have grown to $181 by

6/30/12. In comparison, the same amount invested in dividend-growing stocks would have grown to $3,886, or 21.5

times that of non-dividend-yielding stocks. In the end, we believe investors should favor dividend payers over non-payers

and dividend growers over cutters, and should tilt their core equity strategy towards payers and growers. (See Figure 6.)

20112005200019951990198519801975

Dividend growers: 3,786% cumulative return, 9.46% annual return

Constant dividend payers: 1,435% cumulative return, 6.98% annual return

Non-dividend payers: 81% cumulative return, 1.48% annual return

Dividend cutters: –15% cumulative return, –0.41% annual return

$0

$1,000

$2,000

$3,000

$4,000

$5,000

Source: Ned Davis Research as of 6/30/12. Performance is historical and does not guarantee future results. Returns are based on the monthly equal-weighted geometric average of total returns of S&P 500 Equal Weight Index component stocks with components reconstituted monthly. The index returned a cumulative 1,407% and an average annual 6.93% from 1/31/72 to 6/30/12. Index returns assume reinvestment of all distributions and do not reflect any fees or expenses. It is not possible to invest directly in an index. See page 19 for index definitions.

FIGURE 6: U.S. DIVIDEND GROWERS AND DIVIDEND PAYERS HAVE GENERATED LONG-TERM VALUE (growth of $100 in S&P 500 Equal Weight Index stocks, 1/31/72–6/30/12)

U.S. dividend-growing stocks have generated value, returning a cumulative 3,786% from 1/31/72 through 6/30/12.

GLOBAL EQUITIES WHITE PAPER I AUGUST 2012

Dividends: the case for income-oriented investors » 7

In contrast, many other sectors in other regions provide

attractive yields, such as financials in developed Europe

and information technology in emerging Europe. It is

interesting to note that the region with the highest dividend

yield varies by sector, but North America does not have the

highest yield for any of the sectors. (See Figure 8.)

While investors in developed markets often have a certain

appreciation for dividends, this is not the case with most of

them when it comes to emerging markets. Investors with

relative high risk appetites tend to focus more on capital

appreciation than income within the emerging-market

universe. However, they may want to consider dividends, as

income is generally more secure than capital appreciation.

As Figure 9 illustrates, over the past 10 years, dividends have

contributed 19.4% to total returns in emerging markets.

On the other hand, risk-averse investors may consider

emerging-market equity investments relatively risky. While

the returns earned on well diversified and well structured

portfolios in past years may not necessarily support this

view, investors who consider emerging-market equity

investments too risky but don’t want to miss out on the

upside potential of fast-growing markets and companies

may want to consider combining emerging markets

with dividend income. Fast-growing companies can also

pay high dividends, and high dividends may provide a

measure of downside protection in volatile equity markets.

Thus, risk-averse investors who are attracted to potential

dividends do not have to forgo growth opportunities.

1.4. DIVIDENDS: A GLOBAL OPPORTUNITY

The importance of dividends is not just a U.S. phenomenon;

combining dividend yield and real dividend growth in different

regions shows a similar pattern to that of the United States.

In our opinion, dividends often matter even more when

investing globally. In certain developed European markets,

for example, nearly 100% of total returns have come from

dividends because change in valuation has been slightly

negative, according to GMO, a privately held global

investment management firm.

The importance of dividends to overseas stock markets

has resulted in a culture of strong dividend policies, so the

international equity markets also provide a broader universe

of high dividend yielding stocks: While there were 129 U.S.

stocks with a dividend yield greater than 5% as of 6/30/12,

there were 996 non-U.S. stocks that met that criteria, accord-

ing to Morningstar. Thus, we believe investors may want

to consider the vast opportunities available via international

stock markets when implementing a dividend strategy.

As depicted in Figure 7, all regional stock markets outside

of North America, developed and emerging, have offered

higher dividend yields as of 6/30/12. Currently, the average

dividend yield of developed Europe is more than double

the average dividend yield of North America.

Finally, an international or global portfolio may also

improve a portfolio’s diversification by sector. Many of the

highest-yielding U.S. stocks tend to be concentrated in

a few sectors, such as utilities and telecommunications.

Source: FactSet as of 6/30/12. Performance is historical and does not guarantee future results. Regions are MSCI regions. Diversification can neither ensure a profit nor protect against a loss.

FIGURE 7: AVERAGE REGIONAL DIVIDEND YIELD

0%

2%

4%

6%

Developed Europe

EmergingEurope

DevelopedAsia

EmergingAsia

Latin America North America

4.1% 4.0% 2.9% 2.8% 2.3% 1.8%

8 » Dividends: the case for income-oriented investors

GLOBAL EQUITIES WHITE PAPER I AUGUST 2012

Source: FactSet as of 6/30/12. Performance is historical and does not guarantee future results. Sectors are MSCI/S&P sectors. Regions are MSCI regions. Yellow boxes denote highest regional dividend yield per global sector. Diversification can neither ensure a profit nor protect against a loss.

Sector Developed Asia

Developed Europe

Developed North America

Emerging Asia

Emerging Europe

Latin America

Consumer discretionary 2.4% 3.8% 1.4% 2.3% 3.0% 1.6%

Consumer staples 2.7% 2.8% 2.5% 2.1% 1.7% 1.3%

Energy 3.2% 3.8% 1.1% 3.3% 3.7% 0.4%

Financials 3.5% 4.8% 2.6% 2.7% 3.2% 2.1%

Health care 2.8% 2.5% 1.0% 1.2% 1.8% 2.2%

Industrials 2.7% 3.6% 1.9% 2.5% 2.8% 1.8%

Information technology 2.2% 2.6% 1.1% 3.4% 4.5% 3.7%

Materials 3.1% 3.0% 2.0% 3.3% 4.1% 1.8%

Telecommunication services 4.9% 8.8% 3.4% 3.7% 11.0% 5.6%

Utilities 4.1% 6.1% 3.7% 2.0% 3.5% 3.9%

Regional average 2.9% 4.1% 1.8% 2.8% 4.0% 2.3%

FIGURE 8: GOING GLOBAL MAY INCREASE DIVIDENDS

Source: Bloomberg as of 6/30/12. Performance is historical and does not guarantee future results. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. It is not possible to invest directly in an index. See page 19 for index definitions.

FIGURE 9: HISTORIC DIVIDEND AND CAPITAL RETURNS IN EMERGING MARKETS (10 YEARS ENDING 6/30/12)

Annualized capital appreciation

Annualized dividend returns

Annualized total returns

Dividends as % of total return

MSCI Emerging Markets Index 11.35% 2.73% 14.08% 19.4%

GLOBAL EQUITIES WHITE PAPER I AUGUST 2012

Dividends: the case for income-oriented investors » 9

1.5. SUSTAINABILITY OF DIVIDENDS

In sports there is a saying that “offense wins games;

defense wins championships.” We believe this also holds

true for dividend-investing strategies as well.

It is often suggested that by following an income-focused

strategy, investors may suffer because they are investing

only in companies that have low or no growth potential. The

thinking is that dividend-yielding companies are distributing

such large amounts of their cash flow as dividends or

buybacks that they can’t retain sufficient cash for future

growth projects. We believe this argument is flawed. In our

opinion, exposure to companies that are capable of growing

their free cash flows and are trading at reasonable (growth-

adjusted) prices is a sound strategy.

However, when discussing dividend-investing strategies,

it is important to balance all relevant factors. We believe a

successful long-term dividend strategy must get the most

from dividends. Of course, income is important, but we

are cautious about being overexposed to dividend yield.

As illustrated previously in figure 6, investing in companies

that are growing their dividends has historically been a

winning strategy, while investing in companies that pay no

dividends has led to less favorable results. But an additional

factor that must be considered is if the dividend that a

company is paying is sustainable. If it is not, you could end

up owning a stock that falls in the “dividend-cutters” camp.

Dividends are paid from a company’s cash flow, not its

operating earnings. While on the surface this may seem

like a trivial distinction, it actually says quite a bit about

the types of firms that pay dividends. Companies often

manipulate earnings with accounting rules, which allows

some discretion regarding earnings numbers. This can lead

to distorted views of a company’s success, and can make

it appear that struggling firms are actually producing strong

results. In contrast, cash flows do not allow the reporting

discretion of earnings. If a company has more cash going

out than coming in, this is clear in the company’s cash

flow statement. Dividends are paid in cash, so a company

that has paid a consistent dividend over time likely has a

steady stream of incoming cash. Therefore, dividend-paying

companies most likely have solid business models that

may allow them to navigate down markets more easily.

Monitoring a firm’s cash flows will give an investor a strong

indication or whether or not the dividend is sustainable.

Obviously, if firms have negative cash flows but are paying

a dividend anyway, they should be regarded cautiously.

Another important factor to consider regarding dividend

sustainability is a company’s dividend payout ratio, which is

the fraction of net income a firm pays to its shareholders in

dividends. While high dividends are important, if a company

is paying out nearly all of its earnings in dividends, this

may be a sign that the dividend is not sustainable. Also, a

dividend payout ratio that increases over time may indicate

that earnings growth is not keeping up with dividend

growth and the dividend may not be sustainable. However,

companies with strong cash flows and low to moderate

dividend payout ratios may have room to grow the dividend

and also tend to exhibit positive price appreciation.

In a 2003 study published in the CFA Institute’s Financial

Analyst Journal, “Surprise! Higher Dividend = Higher Earnings

Growth,” Robert D. Arnott and Clifford S. Asness argue that

contrary to financial theory, empirical evidence suggests that

companies with high dividend payout ratios have achieved

higher earnings growth than companies with lower payout

ratios. Dividend-paying companies have typically been

viewed as fundamentally strong companies with potentially

slower growth prospects. In essence, the company believes

that paying out dividends will add more value to shareholders

than utilizing cash for new projects. In contrast, non-dividend-

paying companies have traditionally been viewed as higher-

growth companies that can increase shareholder value by

retaining earnings to reinvest in new projects or grow through

mergers and acquisitions. Arnott and Asness concluded that

the higher earnings growth experienced by dividend-paying

companies most likely reflects better allocation of capital.

High dividend payout ratios impose discipline on corporate

management teams to only invest in those projects with the

best chance of adding value, while low dividend payout ratios

may lead to inefficient empire-building in which companies

fund less-than-ideal projects or investments.

10 » Dividends: the case for income-oriented investors

GLOBAL EQUITIES WHITE PAPER I AUGUST 2012

1.6. DIVIDENDS AS INFLATION

OR DEFLATION HEDGE?

Many investors believe we are on the path to a great

inflation spike driven by reckless printing of money by the

world’s central banks. We would therefore like to discuss

the influence of inflation on stocks, especially on high-

dividend-paying stocks.

Historical data shows that equities have generally

performed best when inflation, as represented by the

Consumer Price Index (CPI), has ranged from –3% to

3%. (See Figure 10.) At the extremes, equities have

tended to perform poorly (which is mainly caused by

a compression of price-to-earnings (P/E) ratios, as we

show later in Figure 11).

If we look at growth of equity prices, earnings, dividends

and P/E ratios in different inflationary backdrops, we see

that dividends have tended to grow more than equity

prices in inflationary periods. This is due to the fact that

they are affected by nominal variables and get a lift from

Source: JPMorgan as of June 2009. Performance is historical and does not guarantee future results. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. It is not possible to invest directly in an index. See page 19 for index definitions.

Year-over-year CPI growth % time occurred Year-over-year S&P 500 Index growth

–15% to –10% 3% –0.9%

–10% to –3% 12% 1.9%

–3% to 0% 9% 15.4%

0% to 1.5% 15% 7.7%

1.5% to 3% 21% 10.7%

3% to 5% 17% 2.4%

5% to 8% 14% 0.3%

8% to 15% 7% 5.6%

15%-plus 3% –6.3%

FIGURE 10: AVERAGE ANNUAL S&P 500 PERFORMANCE IN DIFFERENT INFLATION REGIMES (1872–2009)

rising inflation, but do not suffer the same declines

as P/E ratios, which is normally the result of rising

bond yields, which most equities endure. As Figure 11

indicates, dividends continued to grow during periods

of high inflation.

As global growth is likely to fall back to trend following

one of the most severe financial crises in history, a serious

risk exists for the developed world to fall into a Japan-like

deflation. Although we don’t expect to see deflation, it is

a serious risk that one should consider hedging against—

because while equities do not like high inflation, they do

not like deflation, either.

The first way in which deflation affects stocks is corporate

profitability. When interest rates are near zero, a drop in

expected inflation causes real interest rates to rise and

increases the cost of capital, which in turn hurts corporate

profitability. Consumers and companies respond to the

increase in real interest rates by reducing spending, which

in turn hurts growth.

GLOBAL EQUITIES WHITE PAPER I AUGUST 2012

Dividends: the case for income-oriented investors » 11

Source: JPMorgan as of June 2009. Performance is historical and does not guarantee future results. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. It is not possible to invest directly in an index. See page 19 for index definitions.

FIGURE 11: EQUITY PERFORMANCE IN PERIODS OF HIGH INFLATION (>5%)

Inflation period S&P 500 Index return Earnings growth Dividend growth P/E ratio growth

May 1872 to November 1872 –4% 4% 9% –8%

October 1879 to September 1880 23% 28% 26% –4%

August 1881 to August 1882 –3% –6% 8% 3%

January 1893 to June 1893 –16% –15% 2% –2%

June 1899 to August 1900 –4% 19% 32% –19%

April 1902 to March 1903 –1% 14% 4% –13%

October 1906 to October 1907 –34% –8% 13% –28%

February 1909 to July 1910 –5% 25% 13% –24%

April 1912 to February 1913 –4% 11% 2% –13%

March 1916 to November 1920 –19% –18% 13% –1%

August 1941 to September 1943 17% –4% –13% 22%

July 1946 to October 1948 –13% 155% 31% –66%

December 1950 to December 1951 18% –13% –1% 35%

March 1969 to January 1971 –8% –11% 1% 4%

April 1973 to October 1982 18% 95% 116% –39%

August 1990 to February 1991 1% –2% 3% 3%

Median –4% 1% 9% –6%

In addition, wage rigidities mean that deflation reduces

output prices by more than input prices and puts

additional pressure on corporate profitability. The

Japanese experience of the 1990s provides an example

of the erosion in corporate margins in a deflationary

environment. Overall, equities have delivered subdued

returns in these instances, with earnings and dividends

performing particularly poorly.

However, companies with strong pricing power, long-

duration asset bases, unleveraged balance sheets and

strong earnings momentum have performed well in

deflationary environments. Cyclical stocks have tended

to perform poorly compared to defensive stocks during

periods of falling bond yields. Therefore, defensive,

bond-like sectors such as telecommunications, consumer

staples and health care may be preferable, as well as

high-dividend-paying stocks.

Last but not least, investors may want to remember that

deflation fears could turn into inflation risks very suddenly.

12 » Dividends: the case for income-oriented investors

GLOBAL EQUITIES WHITE PAPER I AUGUST 2012

2.1. SLOW GROWTH IN DEVELOPED

MARKETS INCREASES ATTRACTIVENESS OF

DIVIDENDS

The world has changed dramatically for investors, with the

subprime crisis, stimulus packages, ultra-loose monetary

policy and European sovereign debt crisis dominating

discussions. It feels as if we are living in a bipolar world.

(See Figure 12.)

How does this influence the big picture going forward?

Emerging-market countries continue to deliver structurally

better economic growth prospects than developed-market

countries. Therefore, monetary policies around the globe

differ remarkably. In our opinion, loose (or what some

would call ultra-loose) monetary policies of the United

States, Japan, the United Kingdom and the European

Union will likely continue, while tighter monetary

conditions will persist in the emerging markets. This is

partially due to differing outlooks on consumer prices.

2 I Potential buy signals for equities in times of low bond yields

FIGURE 12: DOES A LOW-GROWTH WORLD EQUAL A LOW-RETURN WORLD?

Signs of higher inflation clearly exist in the emerging

markets, primarily as a result of commodity prices and

the heavy weight they hold in price indices. But in the

developed markets, there is a danger of deflation, or at

least strong disinflation. This also reaches into currency

markets, as emerging-market currencies are believed to

be undervalued and are expected to appreciate relative to

their peers in the developed markets. Last but not least,

investors are more than worried about sovereign debt

in the developed markets, especially in the Eurozone,

and the debt problem should not be ignored in the

United States, Japan or the United Kingdom. In contrast,

sovereign debt and budget deficits are not a problem in

the emerging markets, as it appears that emerging-market

countries learned their lessons well during the Asian crisis.

With governments and central banks around the globe

attempting to repair defective credit markets and prevent

recession, yields on most asset classes have changed

significantly. Most notably, interest payments on various

fixed-income instruments have fallen precipitously. In the

United States, the only time 10-year bond yields were

lower than they were during periods in 2010, 2011 and

2012 was in the 1940s (according to according to Bank of

America Merrill Lynch using data dating back to 1800).

High (structural) growthLow sovereign debtStrong currenciesIncreasing inflation

Emerging markets

Low (structural) growthHigh sovereign debtWeak currenciesIncreasing deflation

Advanced markets

GLOBAL EQUITIES WHITE PAPER I AUGUST 2012

Dividends: the case for income-oriented investors » 13

The strong demand for government bonds likely reflects

five factors: fear of a double-dip recession, fear of

deflation, extreme liquidity levels in the global financial

system, high risk aversion and short-term investors buying

bonds in anticipation of more quantitative easing, primarily

from the U.S. Federal Reserve Board (Fed). However, for

this last factor, we must consider that these investors are

buying bonds for capital gains rather than income. If the

growth outlook improves, all of these factors may prove

transitory and yields could rise.

Due to structural effects (such as de-leveraging) that

resulted from the financial crisis, yields could remain low

for longer, especially in real terms. Post-crisis adjustment

processes have previously shown that these adjustments

often take time and that deleveraging is typically coupled

with subdued economic growth. Also, when thinking about

long-term growth prospects in the developed markets,

we must consider that many countries are facing severe

structural debt problems and huge demographic shifts.

Not only have government bond yields fallen significantly,

but so have corporate bond yields. Appetite for yield has

been so great that investors have entered virtually any

fixed-income asset class that offers higher yields. Credit

spreads have tightened significantly as yield-hungry

investors have chosen to take on credit exposure. Credit

yields are usually higher than dividend yields in a growing

economy, as coupons are fixed while dividends grow.

So, a negative yield differential implies that the market

anticipates dividends will be cut over time. As long as

dividend streams are sustainable, as we believe they

will be, investors may want to consider equity dividends

instead of bond yields.

Given today’s yield environment, equity dividend yields

appear more attractive than bond yields. This is true

regardless of whether we are comparing equity dividend

yields to government bond yields or investment-grade

corporate bond yields. While some fixed-income asset

classes offer higher yields, such as emerging-market

bonds or high-yield bonds, the risk-return profile of

these assets is more comparable to equities than to

conventional bonds.

Are dividend yields attractive in current and expected

capital market conditions? We believe they are, because

it appears a tug of war is taking place between debtors

(who have high expected return rates) and creditors

(who are simply seeking the highest and most secure yields

available). The longer interest rates stay low, the more

investors will come under pressure to generate an adequate

return. Thus, since there is little opportunity within fixed

income, we believe many investors will have to turn to

equities—namely, stocks with high dividend yields.

14 » Dividends: the case for income-oriented investors

GLOBAL EQUITIES WHITE PAPER I AUGUST 2012

2.2. POTENTIAL BUY SIGNAL: FLOWS

After two major equity bear markets over the past 10 years, investors have flooded into the perceived safety of fixed-

income products. Net flows into fixed-income funds outpaced net flows into equity funds for nine consecutive quarters

from the third quarter of 2008 through the third quarter of 2010, resulting in a total flow imbalance of nearly $600 billion.

The last time bonds drew in greater net flows relative to equities for nine consecutive quarters was during the recession

of the early 1990s, as highlighted in Figure 13.

FIGURE 13: FLOWS INTO EQUITIES AND FIXED INCOME, IN BILLIONS (Q2 1990 TO Q3 2010)

Source: Simfunds as of 6/30/12.

By the fall of 2010, this flight to safety, combined with expectations that the Fed will maintain low rates for an extended

period of time, had pushed the yield on the 10-Year U.S. Treasury bonds below 2.5% for the first time since 1954,

according to DeAM.

The conclusion of the previous period of robust bond flows (the third quarter of 1992 to the third quarter of 1993)

proved to be a compelling entry point for stock investors, as the MSCI World Index returned 20.24% over the one-year

period, 47.95% over the three-year period and 108.73% over the five-year period on a cumulative basis, according to

Morningstar as of 6/30/12. Of course, past performance does not guarantee future results.

–$90

–$60

–$30

$0

$30

$60

$90

$120

$150

Fixed-income flowsEquity flows

Q2

1990

Q2

1992

Q2

1994

Q2

1996

Q2

1998

Q2

2000

Q2

2002

Q2

2004

Q2

2006

Q2

2008

Q3

2010

Q2

2010

GLOBAL EQUITIES WHITE PAPER I AUGUST 2012

Dividends: the case for income-oriented investors » 15

Source: DeAM as of 6/30/12. Performance is historical and does not guarantee future results. Yield spread refers to the 10-year U.S. Treasury bond yield minus the S&P 500 Index average dividend yield. Fixed-income investments are subject to interest-rate risk, and their value will decline as interest rates rise. The values of equity investments are more volatile than those of other securities. This data is for illustrative purposes and does not represent any DWS fund. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. It is not possible to invest directly in an index. See page 19 for index definitions.

FIGURE 14: DIFFERENCE BETWEEN 10-YEAR U.S. TREASURY BOND YIELD AND S&P 500 INDEX DIVIDEND YIELD (4/30/53–6/30/12)

2.3. POTENTIAL BUY SIGNAL: EQUITY

YIELDS VS. GOVERNMENT BOND YIELDS

We believe equities, especially dividend-paying equities,

appear attractive relative to bonds. Yields on a number of

fixed-income investments, particularly government bonds,

have fallen recently. Typically, government bond yields

exceed the dividend yield of equities. In fact, dating back

to 1953, the earliest records kept by the Fed, the median

spread between the yield of the 10-year U.S. Treasury

bond and the dividend yield of the S&P 500 Index was

326 basis points. However, as of August 10, 2011, the

yield of the 10-year U.S. Treasury bond dipped below

the dividend yield of the S&P 500 Index. Historically, a

convergence between U.S. Treasury yields and equity

yields has been a robust buy signal for equities. Since

1953, U.S. stocks have returned an average 23.53% over

the one-year period following a yield convergence to

50 basis points or less. (See Figure 14.)

An additional factor that must be considered is the

duration risk that exists in bonds. Since 1981, when the

10-year U.S. Treasury bond rate has exceeded 15%, we

have been in a decreasing-interest-rate environment. This

has led to a nearly 30-year bull market in bonds. Now we

face a much different situation: There is little room for

interest rates to move lower, and we believe we could

see interest-rate increases over the next several years.

Since bond prices have an inverse relationship with

interest rates, this could have a devastating effect on bond

prices. For yield-hungry investors, this makes dividend-

paying stocks all the more attractive, as stocks don’t have

duration risk. The perceived safety of bonds has been

based, in part, on a favorable interest rate environment.

When we factor in the duration risk, equities suddenly

don’t look much riskier than bonds. This should only

increase the crossover effect that we anticipate seeing.

Average one-year return following

Best one-year return following

Worst one-year return following

When spread is less than 50 bps 23.53% 53.62% –10.78%

–4%

–2%

0%

2%

4%

6%

8%

10%

7/1953 7/1963 7/1973 7/1983 7/1993 7/2003 6/2012

Median spread3.22%

Potential buy signal spread0.50%

Yields as of 6/30/12S&P 500 Index=2.21%

10-year U.S. Treasury bond=1.67%

16 » Dividends: the case for income-oriented investors

GLOBAL EQUITIES WHITE PAPER I AUGUST 2012

0 5 10 15 20 25 30 4035

Consumer staples

Financials

Utilities

Industrials

Consumer discretionary

Health care

Information technology

Energy

Telecommunications

Materials

36

33

32

30

22

17

15

11

10

4

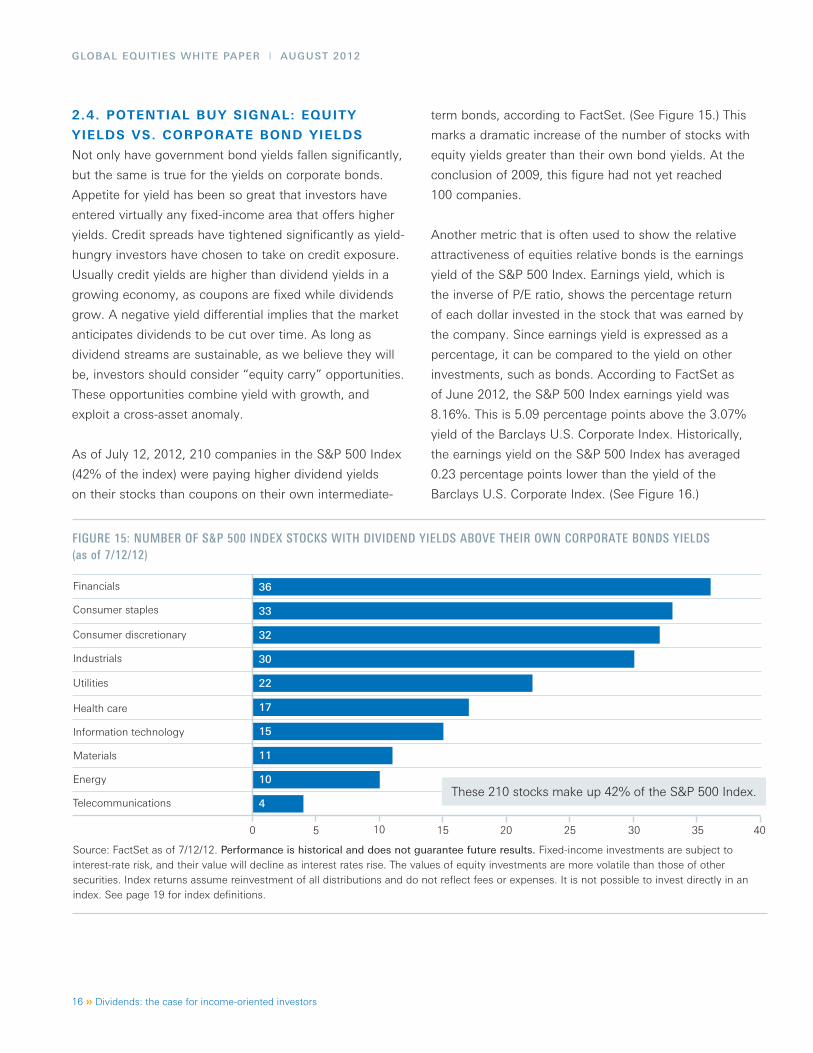

Source: FactSet as of 7/12/12. Performance is historical and does not guarantee future results. Fixed-income investments are subject to interest-rate risk, and their value will decline as interest rates rise. The values of equity investments are more volatile than those of other securities. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. It is not possible to invest directly in an index. See page 19 for index definitions.

FIGURE 15: NUMBER OF S&P 500 INDEX STOCKS WITH DIVIDEND YIELDS ABOVE THEIR OWN CORPORATE BONDS YIELDS (as of 7/12/12)

2.4. POTENTIAL BUY SIGNAL: EQUITY

YIELDS VS. CORPORATE BOND YIELDS

Not only have government bond yields fallen significantly,

but the same is true for the yields on corporate bonds.

Appetite for yield has been so great that investors have

entered virtually any fixed-income area that offers higher

yields. Credit spreads have tightened significantly as yield-

hungry investors have chosen to take on credit exposure.

Usually credit yields are higher than dividend yields in a

growing economy, as coupons are fixed while dividends

grow. A negative yield differential implies that the market

anticipates dividends to be cut over time. As long as

dividend streams are sustainable, as we believe they will

be, investors should consider “equity carry” opportunities.

These opportunities combine yield with growth, and

exploit a cross-asset anomaly.

As of July 12, 2012, 210 companies in the S&P 500 Index

(42% of the index) were paying higher dividend yields

on their stocks than coupons on their own intermediate-

term bonds, according to FactSet. (See Figure 15.) This

marks a dramatic increase of the number of stocks with

equity yields greater than their own bond yields. At the

conclusion of 2009, this figure had not yet reached

100 companies.

Another metric that is often used to show the relative

attractiveness of equities relative bonds is the earnings

yield of the S&P 500 Index. Earnings yield, which is

the inverse of P/E ratio, shows the percentage return

of each dollar invested in the stock that was earned by

the company. Since earnings yield is expressed as a

percentage, it can be compared to the yield on other

investments, such as bonds. According to FactSet as

of June 2012, the S&P 500 Index earnings yield was

8.16%. This is 5.09 percentage points above the 3.07%

yield of the Barclays U.S. Corporate Index. Historically,

the earnings yield on the S&P 500 Index has averaged

0.23 percentage points lower than the yield of the

Barclays U.S. Corporate Index. (See Figure 16.)

These 210 stocks make up 42% of the S&P 500 Index.

GLOBAL EQUITIES WHITE PAPER I AUGUST 2012

Dividends: the case for income-oriented investors » 17

Source: FactSet as of 6/30/12. Performance is historical and does not guarantee future results. Fixed-income investments are subject to interest-rate risk, and their value will decline as interest rates rise. The values of equity investments are more volatile than those of other securities. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. It is not possible to invest directly in an index. See page 19 for index definitions.

FIGURE 16: EQUITIES ARE HISTORICALLY ATTRACTIVE VS. CORPORATE BOND YIELDS (9/1/87–6/30/12)

1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 06/122011

S&P 500 Index earnings yield

S&P 500 Index earnings yield minus Barclays U.S. Corporate Index yield

Barclays U.S. Corporate Index yield to worst

Average S&P 500 Index earnings yield minus Barclays U.S. Corporate Index yield

–6%

–4%

–2%

0%

2%

4%

6%

8%

10%

12%

14%

18 » Dividends: the case for income-oriented investors

GLOBAL EQUITIES WHITE PAPER I AUGUST 2012

In this white paper, we have explored the implications

of corporate dividend policies, the attributes of dividend-

paying and non-dividend-paying stocks, equity dividend

yields relative to fixed-income yields and global

dividend-investing opportunities.

We believe that dividend yields are attractive in the

current capital market environment because it appears

a tug of war is taking place between debtors (who have

high expected return rates) and creditors (who are simply

seeking the highest and most secure yields available).

The longer interest rates stay low, the more investors will

come under pressure to generate an adequate return.

Given this backdrop of extremely low fixed-income yields,

we believe there is a strong potential for “crossover” buyers

to enter the equity markets. In other words, investors who

have historically sought the perceived safety and steady

income of bonds may be drawn into equities.

3 I Conclusion Yields on government and corporate bonds are so low

that dividends, in many cases, offer more income than

bonds. As we have noted, almost half of S&P 500 Index

companies currently pay a dividend that exceeds the yield

on their intermediate-term corporate bond. This means

equity holders not only have the opportunity to benefit

from price appreciation; they are also receiving more

income than bond holders.

At a time when many analysts believe that equity prices

are attractive, it makes sense to think that investors who

would typically flock to bonds might be attracted to

dividend-paying stocks.

In addition, many of these investors have seen significant

deterioration of their portfolios in recent years. While they

might be hesitant to enter the equity markets, they might

also realize that they need to be in stocks if they have any

hope of regaining their wealth.

Thus, in our opinion, many investors will have to turn to

equities—namely, stocks with high dividend yields—and

this will lead dividend-paying stocks to re-emerge as an

important component of investors’ portfolios.

GLOBAL EQUITIES WHITE PAPER I AUGUST 2012

Dividends: the case for income-oriented investors » 19

INDEX DEFINITIONS

The Barclays Capital U.S. Corporate Index tracks the performance of the investment-grade, fixed-rate, taxable,

corporate bond market.

One basis point equals 1/100 of a percentage point.

Credit spread refers to the excess yield various bond sectors offer over Treasuries with similar maturities. When spreads

widen, yield differences are increasing between bonds in the two sectors being compared. When spreads narrow,

the opposite is true.

Duration, which is expressed in years, measures the sensitivity of the price of a bond or bond fund to a change in

interest rates.

The MSCI Emerging Markets Equity Index tracks the performance of stocks in select emerging markets.

Price-to-earnings ratio (P/E) ratio compares a company’s current share price to its per-share earnings.

The S&P 500 Equal Weight Index is the equally-weighted version of the S&P 500 Index, which is capitalization-

weighted; the index has the same constituents as the S&P 500 Index, but each company is allocated a fixed weight of

0.20%, rebalanced quarterly.

The S&P 500 Index tracks the performance of 500 leading U.S. stocks and is widely considered representative

of the U.S. equity market.

The yield curve is a graphical representation of how yields on bonds of different maturities compare. Normally, yield

curves slant up, as bonds with longer maturities typically offer higher yields than short-term bonds.

Yield to worst is the lowest potential yield that can be received on a bond without the issuer actually defaulting. The

opinions and forecasts expressed herein by the authors do not necessarily reflect those of DWS Investments, are as of

9/1/11 and may not come to pass.

© 2012 DWS Investments Distributors, Inc. All rights reserved. PM123918 R-19781-2 (8/12) DIV-WHITE

OBTAIN A PROSPECTUS To obtain a summary prospectus, if available, or prospectus, download one from www.dws-investments.com, talk to your financial representative or call (800) 621-1048. We advise you to carefully consider the product’s objectives, risks, charges and expenses before investing. The summary prospectus and prospectus contain this and other important information about the investment product. Please read the prospectus carefully before you invest.

IMPORTANT RISK INFORMATIONAny fund that concentrates in a particular segment of the market will generally be more volatile than a fund that invests more broadly. The fund may use derivatives, including as part of its global alpha strategy. Investing in derivatives entails special risks relating to liquidity, leverage and credit that may reduce returns and/or increase volatility. Investing in foreign securities, particularly those of emerging markets, presents certain risks, such as currency fluctuations, political and economic changes, and market risks. Dividends are not guaranteed. The fund lends securities to approved institutions. Any decline in value of a portfolio security that is out on loan by the fund will adversely affect performance. Financial failure of the borrower may mean a delay in recovery or loss of rights in the collateral. Stocks may decline in value. See the prospectus for details.

Investment products offered throughDWS Investments Distributors, Inc. Advisory services offered through Deutsche InvestmentManagement Americas, Inc.

The opinions and forecasts expressed herein by the fund managers and product specialist do not necessarily reflect those of

DWS Investments, are as of 6/30/12 and may not come to pass.

C000000

DWS Investments is part of Deutsche Bank’s Asset Management division and, within the U.S., represents the retail asset management activities of Deutsche Bank AG, Deutsche Bank Trust Company Americas, Deutsche Investment Management Americas Inc. and DWS Trust Company.

DWS Investments Distributors, Inc.222 South Riverside Plaza Chicago, IL 60606-5808www.dws-investments.com [email protected] (800) 621-1148