divya

TRANSCRIPT

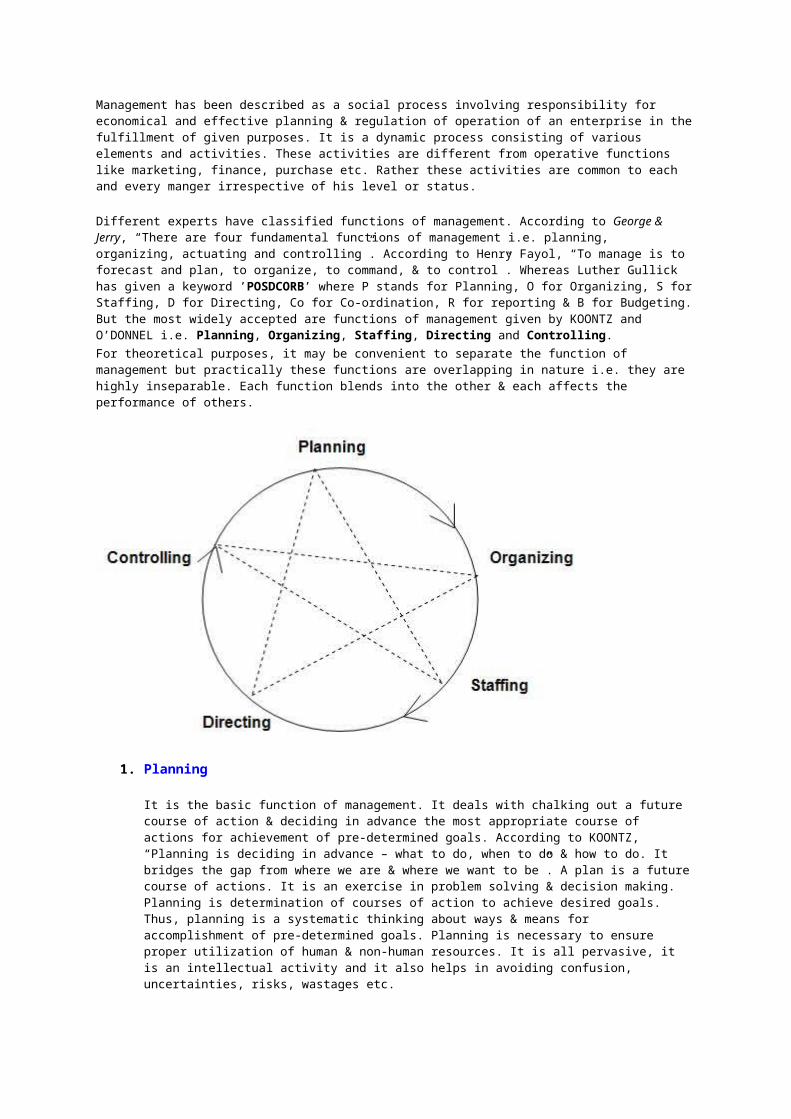

Management has been described as a social process involving responsibility for economical and effective planning & regulation of operation of an enterprise in the fulfillment of given purposes. It is a dynamic process consisting of various elements and activities. These activities are different from operative functions like marketing, finance, purchase etc. Rather these activities are common to each and every manger irrespective of his level or status.

Different experts have classified functions of management. According to George & Jerry, “There are four fundamental functions of management i.e. planning, organizing, actuating and controlling”. According to Henry Fayol, “To manage is to forecast and plan, to organize, to command, & to control”. Whereas Luther Gullick has given a keyword ’POSDCORB’ where P stands for Planning, O for Organizing, S for Staffing, D for Directing, Co for Co-ordination, R for reporting & B for Budgeting. But the most widely accepted are functions of management given by KOONTZ and O’DONNEL i.e. Planning, Organizing, Staffing, Directing and Controlling.For theoretical purposes, it may be convenient to separate the function of management but practically these functions are overlapping in nature i.e. they are highly inseparable. Each function blends into the other & each affects the performance of others.

1. Planning

It is the basic function of management. It deals with chalking out a future course of action & deciding in advance the most appropriate course of actions for achievement of pre-determined goals. According to KOONTZ, “Planning is deciding in advance – what to do, when to do & how to do. It bridges the gap from where we are & where we want to be”. A plan is a future course of actions. It is an exercise in problem solving & decision making. Planning is determination of courses of action to achieve desired goals. Thus, planning is a systematic thinking about ways & means for accomplishment of pre-determined goals. Planning is necessary to ensure proper utilization of human & non-human resources. It is all pervasive, it is an intellectual activity and it also helps in avoiding confusion, uncertainties, risks, wastages etc.

2. Organizing

It is the process of bringing together physical, financial and human resources and developing productive relationship amongst them for achievement of organizational goals. According to Henry Fayol, “To organize a business is to provide it with everything useful or its functioning i.e. raw material, tools, capital and personnel’s”. To organize a business involves determining & providing human and non-human resources to the organizational structure. Organizing as a process involves:

Identification of activities. Classification of grouping of activities. Assignment of duties. Delegation of authority and creation of responsibility.

Coordinating authority and responsibility relationships. 3. Staffing

It is the function of manning the organization structure and keeping it manned. Staffing has assumed greater importance in the recent years due to advancement of technology, increase in size of business, complexity of human behavior etc. The main purpose o staffing is to put right man on right job i.e. square pegs in square holes and round pegs in round holes. According to Kootz & O’Donell, “Managerial function of staffing involves manning the organization structure through proper and effective selection, appraisal & development of personnel to fill the roles designed un the structure”. Staffing involves:

Manpower Planning (estimating man power in terms of searching, choose the person and giving the right place).

Recruitment, selection & placement. Training & development. Remuneration. Performance appraisal. Promotions & transfer.

4. Directing

It is that part of managerial function which actuates the organizational methods to work efficiently for achievement of organizational purposes. It is considered life-spark of the enterprise which sets it in motion the action of people because planning, organizing and staffing are the mere preparations for doing the work. Direction is that inert-personnel aspect of management which deals directly with influencing, guiding, supervising, motivating sub-ordinate for the achievement of organizational goals. Direction has following elements:

Supervision Motivation Leadership Communication

Supervision- implies overseeing the work of subordinates by their superiors. It is the act of watching & directing work & workers.

Motivation- means inspiring, stimulating or encouraging the sub-ordinates with zeal to work. Positive, negative, monetary, non-monetary incentives may be used for this purpose.

Leadership- may be defined as a process by which manager guides and influences the work of subordinates in desired direction.

Communications- is the process of passing information, experience, opinion etc from one person to another. It is a bridge of understanding.

5. Controlling

It implies measurement of accomplishment against the standards and correction of deviation if any to ensure achievement of organizational goals. The purpose of controlling is to ensure that everything occurs in conformities with the standards. An efficient system of control helps to predict deviations before they actually occur. According to Theo Haimann, “Controlling is the process of checking whether or not proper progress is being made towards the objectives and goals and acting if necessary, to correct any deviation”. According to Koontz & O’Donell “Controlling is the measurement & correction of performance activities of subordinates in order to make sure that the enterprise objectives and plans desired to obtain them as being accomplished”. Therefore controlling has following steps:

a. Establishment of standard performance. b. Measurement of actual performance. c. Comparison of actual performance with the standards and finding out deviation if any. d. Corrective action.

Henri Fayol, the father of the school of Systematic Management, was motivated to create a theoretical foundation for a managerial educational program based on his experience as a successful managing director of a mining company. In his day, managers had no formal training and he observed that the increasing complexity of organisations would require more professional management.

Fayol's legacy is his generic Principles of Management. Of Fayol's six generic activities for industrial undertakings (technical, commercial, financial, security, accounting, managerial), the most important were The Five Functions of Management that focused on the key relationships between personnel and its management.

The Five Functions are:

1. PLANNING

drawing up plans of actions that combine unity, continuity, flexibility and precision given the organisation's resources, type and significance of work and future trends. Creating a plan of action is the most difficult of the five tasks and requires the active participation of the entire organisation. Planning must be coordinated on different levels and with different time horizons;

2. ORGANISING

providing capital, personnel and raw materials for the day-to-day running of the business, and building a structure to match the work. Organisational structure depends entirely on the number of employees. An increase in the number of functions expands the organisation horizontally and promotes additional layers of supervision;

3. COMMANDING

optimising return from all employees in the interest of the entire enterprise. Successful managers have personal integrity, communicate clearly and base their judgments on regular audits. Their thorough knowledge of personnel creates unity, energy, initiative and loyalty and eliminates incompetence;

4. COORDINATING

unifying and harmonizing activities and efforts to maintain the balance between the activities of the organisation as in sales to production and procurement to production. Fayol recommended weekly conferences for department heads to solve problems of common interest;

5. CONTROLLING

identifying weaknesses and errors by controlling feedback, and conforming activities with plans, policies and instructions. Fayol's management process went further than Taylor's basic hierarchical model by allowing command functions to operate efficiently and effectively through co-ordination and control methods. For Fayol, the managing director overlooked a living organism that requires liaison officers and joint committees.

The American Luther Gulick and Brit Lydnall Urwick expanded Fayol's list to seven executive management activities summarised by the acronym POSDCORB:

planning: determine objectives in advance and the methods to achieve them; organising: establish a structure of authority for all work; staffing: recruit, hire and train workers; maintain favourable working conditions; directing: make decisions, issue orders and directives; coordinating: interrelate all sectors of the organisation; reporting: inform hierarchy through reports, records and inspections; budgeting: depend on fiscal planning, accounting and control.

assets:

five tasks of management

ProvenModels editor PM version 0.2 62 KB

pros:Fayol provided a language to communicate management theory and establish a foundation for management training.

Managers should perceive organisations as living organisms that require constant attention rather than as mechanical machines.

cons:The principles describe a vision rather than reality and are based on Fayol's own experience rather than empirical research. Later studies by Mintzberg and Kotter found that successful managers spend little time carrying out Fayol's activities and rely more on cultivating networks and personal contacts.

references:General and industrial management (Administration, industrielle et generale)

Henri Fayol 1949 Pitman

United Kingdom ISBN 0879421789

Management theory

John Sheldrake 1996 Thomson United Kingdom ISBN 1861521995

Notes on the Theory of Organization

Luther Halsey Gulick 1937 Institute of Public

Definition, Meaning and characteristics of Management.

Management is a continuous, lively and fast developing science. Management is needed to convert the disorganized resources of men, machines, materials and methods into a useful and effective enterprise. management is a pipeline, the inputs are fed at the end and they are proceeded through management functions and ultimately we get the end results or inputs in the form of goods, services, productivity, information and satisfaction. Management is a comprehensive word which is used in different sciences in the modern business and industrial world. In the narrow sense, it signifies the technique of taking work from others. In this way a person who can take work from others is called manager. In the wide sense, the management is an art, as well as science, which is concerned with the different human efforts so as achieve the desired objective.

Management has been defined by different authors in a number of ways. Some call it a process of managing. Some call it a coordination of resources, some call it body of personnel challenged in the task of managing while others call it as an organized distinct discipline. The following are some of the main definitions of management:

1. Management as process:

Kimball, koontz and O'Donnell, Newmann and Summer, Stanley Vance, Theo Haimann, F.C. Hooper and E.F.T Breach they all call it a process. It is evident from the following definitions also:

According the Kimball-management may be broadly defined as the art of applying the economic principles that underlie the control of men and materials in the enterprise under consideration.

According to Koontz, "Management is the art of getting things done through and with people in formally organized groups."

According to Theo haimann, "Management is the function of getting things done through people and directing the efforts of individuals towards a common objective."

According to Sisks, "Management is the process of working of with and other to effectively achieve organizational objectives by efficiently using limited resources in changing environment."

2. Management as an Activity:

According to this approach management consists of those activities, which are performed by managers in attaining the predetermined objectives of the business. This approach may be referred to Henry Fayol, who classified management activities into the following categories:

Technical - referred to production department. Commercial - relates to buying, selling and exchange. Financial concerned with maximum utilization of capital. Security concurred with protection of property and person. According concerned with maintenance of accounts, presentation and statistics and

Management concerned to planning, organizing, commanding, coordinating and controlling.

3. Management as a group of personnel:

According to this approach human factor plays an important role in accomplishing business objectives. management is concerned with those who have been managing the affairs of the business. Managers are assigned duties and are also granted requisite authority to perform their duties efficiently and thus, management is effective direction, coordination and control of individual and group efforts to accomplish business objective.

This approach is advocated by management authorities like Taylor, Wilson and others. They have defined management as following. As per F.W. Taylor's approach, "Management is the art of knowing exactly what you want your men to do and then seeing that they do it in the best and cheapest way."

4. Management as a discipline:

Some times the term 'Management' is used to connote neither the activity nor the personnel who exercise it, but as a substantive describes the subject, the body of knowledge and practices of management as a subject of study. Management is being taught in different college and universities as a district subject.

Thus, management, as such is a process, an activity, a discipline and as effort to coordination, control and direct individual and group efforts towards desired goal of the business.

Characteristics / Nature / Features of Management:

The main characteristics of management are as follows:

Management is an activity: Management is an activity which is concerned with the efficient utilization of human and non-human resources of production.

Invisible Force: Management is an invisible force. Its existence can be felt through the enterprise or institution it is managing.

Goal Oriented: Management is goal oriented as it aims to achieve some definite goals and objectives. According to the Haimann, "Effective management is always management by objectives". Managers and other personnel officers apply their knowledge, experience and skills to achieve the desired objectives.

Accomplishment through the efforts of Others: Managers cannot do everything themselves. They must have the necessary ability and skills to get work accomplished through the efforts of others.

Universal activity: Management is universal. Management is required in all types or organizations. Wherever there are some activities, there is management. The basic principles of management are universal and can be applied anywhere and in every field, such as business, social, religious, cultural, sports, administration, educational, politics or military.

Art as well as Science: Management is both an art and a science. It is a science as it has an organized body of knowledge which contains certain universal truths and an art as managing requires certain skills which apply more or less in every situation.

Multidisciplinary Knowledge: Though management is a distinct discipline, it contains principles drawn from many social sciences like psychology, sociology etc.

Management is distinct from ownership: In modern times, there is a divorce of management from ownership. Today, big corporations are owned by a vast number of shareholders while their management is in the hands of paid qualified, competent and experienced managerial personnel.

Need at all levels: According to the nature of task and scope of authority, management is needed at all levels of the organization, i.e., top level, middle and lower level.

Integrated process: Management is an integrated process. It integrates the men, machine and material to carryout the operations of the enterprise efficiently and successfully. This integrating process is result oriented.

Submitted to RB by Girish Sharmaa

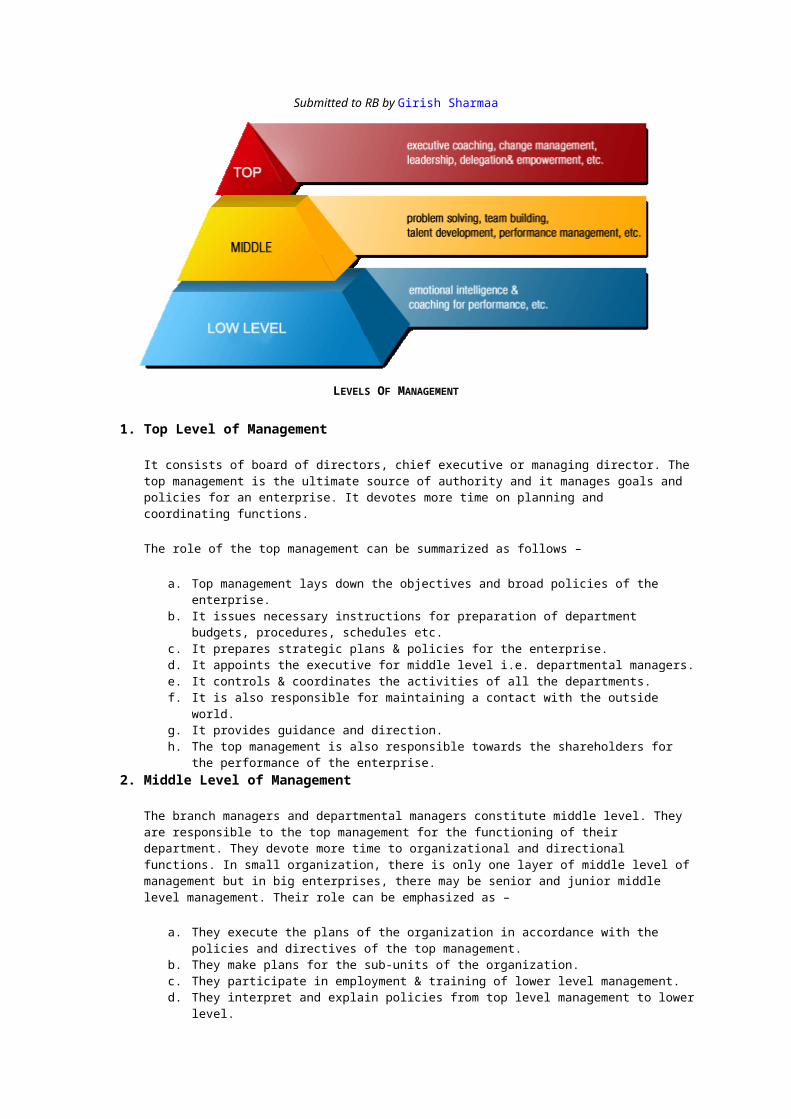

LEVELS OF MANAGEMENT

1. Top Level of Management

It consists of board of directors, chief executive or managing director. The top management is the ultimate source of authority and it manages goals and policies for an enterprise. It devotes more time on planning and coordinating functions.

The role of the top management can be summarized as follows –

a. Top management lays down the objectives and broad policies of the enterprise. b. It issues necessary instructions for preparation of department budgets, procedures, schedules

etc. c. It prepares strategic plans & policies for the enterprise. d. It appoints the executive for middle level i.e. departmental managers. e. It controls & coordinates the activities of all the departments. f. It is also responsible for maintaining a contact with the outside world. g. It provides guidance and direction. h. The top management is also responsible towards the shareholders for the performance of the

enterprise. 2. Middle Level of Management

The branch managers and departmental managers constitute middle level. They are responsible to the top management for the functioning of their department. They devote more time to organizational and directional functions. In small organization, there is only one layer of middle level of management but in big enterprises, there may be senior and junior middle level management. Their role can be emphasized as –

a. They execute the plans of the organization in accordance with the policies and directives of the top management.

b. They make plans for the sub-units of the organization. c. They participate in employment & training of lower level management. d. They interpret and explain policies from top level management to lower level. e. They are responsible for coordinating the activities within the division or department. f. It also sends important reports and other important data to top level management. g. They evaluate performance of junior managers. h. They are also responsible for inspiring lower level managers towards better performance.

3. Lower Level of Management

Lower level is also known as supervisory / operative level of management. It consists of supervisors, foreman, section officers, superintendent etc. According to R.C. Davis, “Supervisory management refers to those executives whose work has to be largely with personal oversight and direction of operative

employees”. In other words, they are concerned with direction and controlling function of management. Their activities include –

a. Assigning of jobs and tasks to various workers. b. They guide and instruct workers for day to day activities. c. They are responsible for the quality as well as quantity of production. d. They are also entrusted with the responsibility of maintaining good relation in the organization. e. They communicate workers problems, suggestions, and recommendatory appeals etc to the

higher level and higher level goals and objectives to the workers. f. They help to solve the grievances of the workers. g. They supervise & guide the sub-ordinates. h. They are responsible for providing training to the workers. i. They arrange necessary materials, machines, tools etc for getting the things done. j. They prepare periodical reports about the performance of the workers. k. They ensure discipline in the enterprise. l. They motivate workers. m. They are the image builders of the enterprise because they are in direct contact with the

workers

4. Managerial Ethics5. The word ethics is derived from the Greek work ethos, which refers to 6. the character and sentiment of the community, and standards of behavior. 7. Ethical means conforming to the standards of a given profession or group. Any 8. group can set its own ethical standards and then live by them or not. Ethical 9. standards, whether they are established by an individual, a corporation, a 10. profession, or a nation, help to guide a person's decisions and actions. The 11. commonly accepted definition of ethics is rules or standards that govern 12. behavior. Managerial decision making is the type of behavior that managers 13. are paid to do. They must make choices among alternatives and these may 14. vary in terms of their perceived ethicality. 15. The argument might be that ethics and morality ought to be kept as an 16. exclusive part of religious and educational organizations. When morality 17. intrudes on the business organization, it has a potential of diverting from the 18. organization's main objective, to make money, and as a result lead to deprive 19. stockholders returns. But there is an increased realization that managers 20. needs to be more responsible, not just to their stockholders but also to their

Harvard Business Online June 20, 2008, 3:40PM EST text size: TT

Today's Top 10 Talent-Management Challenges

Tammy Erickson on the dilemmas and problems managers and companies must contend with

by Tammy Erickson

Related Items

Visit HarvardBusiness.org Subscribe to Harvard Business Review Visit Harvard Business Review Online Visit Leadership & Managing People Resource Center Visit Harvard Business Review Answers

Story Tools

post a comment e-mail this story print this story order a reprint digg this save to del.icio.us

Posted on Across the Ages: June 19, 2008 11:12 PM

I had the pleasure last week of moderating a panel of senior talent development officers representing three very different industries and diverse geographies: Deb Wheelock of Mercer (a high-end professional services firm, recruiting highly educated knowledge workers), Pamela Stroko of The Gap (a retailer faced with the classic industry challenges of creating a differentiating employee proposition and enhancing retention of its large workforce), and Sujaya Banerjee of the Essar Group (a diversified India-based enterprise participating in a variety of industrial sectors, including steel, energy, and communications).

Interestingly, even with this diversity of perspectives, we found our views on today's top talent challenges to be surprisingly aligned. I thought you might like to see our list—and would love to hear your thoughts on things you're wrestling with that we missed.

Here goes:

1. Attracting and retaining enough employees at all levels to meet the needs of organic and inorganic growth. All three companies are facing a talent crunch. Essar, for example, has grown from 20 thousand employees to a staggering 60 thousand in the past 3 years. Fifty-five percent of their employees have less than two years of tenure.

2. Creating a value proposition that appeals to multiple generations. With four generations in today's workplace, most companies are struggling to create an employee experience that appeals to individuals with diverse needs, preferences and assumptions. The Gap, for example, has 153,000 people in its workforce. The stores have a high percentage of Gen Y employees, while corporate roles and leadership ranks are primarily made up of Gen X'ers and Boomers. How does one create a compelling employee value proposition for the organization?

3. Developing a robust leadership pipeline. I believe one of the biggest potential threats to many corporations is a lack of a robust talent pool from which to select future leaders. This is in part a numbers issue—the Gen X cohort is small and therefore, as I like to say, precious. But it's also an interest issue—many members of Gen X are simply not particularly excited about being considered for these roles. There was wide agreement among the panelists that a lack of individuals ready to move into senior client manager and leadership roles is a critical challenge.

4. Rounding out the capabilities of hires who lack the breadth of necessary for global leadership. It's relatively straightforward to identify and assess experts in specific functional or technical arenas, but much more difficult to determine whether those individuals have the people skills, leadership capabilities, business breadth, and global diversity sensibilities required for the nature of leadership today. Increasingly, the challenge of developing these broader skill sets falls to the corporations. Essar has formed an academy specifically to develop and groom its own leaders.

5. Transferring key knowledge and relationships. The looming retirement of a significant portion of the workforce challenges all companies, but particularly those who are dependant on the strength of tacit knowledge, such as that embedded in customer relationships, a key to Mercer's business success.

6. Stemming the exodus of Gen X'ers from corporate life. A big threat in many firms today is the exodus of mid-career talent—people in whom the organization has invested heavily and in whom it has pinned it hopes for future leadership. For example, developing talent management practices and programs calibrated to leverage technology and create greater work/life balance has been a priority for Mercer over recent years.

7. Redesigning talent management practices to attract and retain Gen Y's. The challenge of calibrating talent management practices and programs to attract and engage our young entrants is critically important to all firms and particularly so for firms that depend on a strong flow of top talent, such professional service firms like Mercer. All three panelists agreed that making the business infrastructure more attractive to Gen Y is a high priority.

8. Creating a workplace that is open to Boomers in their "second careers." Age prejudice still exists, but smart companies are looking for ways to incorporate the talents of Boomers and even older workers in the workforce. In many cases, this requires rethinking roles and work relationships.

9. Overcoming a "norm" of short tenure and frequent movement. Some industries, such as specialty retail, are known for having a very disposable view of talent. Companies intent on changing that norm, such as The Gap, must address both external influences in the marketplace and an internal mindset. The Gap believes retaining employees in roles for 3+ years will be a key to their future earnings growth.

10. Enlisting executives who don't appreciate the challenge. Many talent executives complain that business leaders still believe that people are lined up outside the door because of the power of the company's brand. The challenge of enlisting the support of all executives for the transition from a talent culture that has traditionally operated with a "buy" strategy to one that places more emphasis on "build" is widely shared.

Harvard Business Online June 20, 2008, 3:40PM EST text size: TT

Today's Top 10 Talent-Management Challenges

Tammy Erickson on the dilemmas and problems managers and companies must contend with

by Tammy Erickson

Related Items

Visit HarvardBusiness.org Subscribe to Harvard Business Review Visit Harvard Business Review Online Visit Leadership & Managing People Resource Center Visit Harvard Business Review Answers

Story Tools

post a comment e-mail this story print this story order a reprint digg this save to del.icio.us

Posted on Across the Ages: June 19, 2008 11:12 PM

I had the pleasure last week of moderating a panel of senior talent development officers representing three very different industries and diverse geographies: Deb Wheelock of Mercer (a high-end professional services firm, recruiting highly educated knowledge workers), Pamela Stroko of The Gap (a retailer faced with the classic industry challenges of creating a differentiating employee proposition and enhancing retention of its large workforce), and Sujaya Banerjee of the Essar Group (a diversified India-based enterprise participating in a variety of industrial sectors, including steel, energy, and communications).

Interestingly, even with this diversity of perspectives, we found our views on today's top talent challenges to be surprisingly aligned. I thought you might like to see our list—and would love to hear your thoughts on things you're wrestling with that we missed.

Here goes:

1. Attracting and retaining enough employees at all levels to meet the needs of organic and inorganic growth. All three companies are facing a talent crunch. Essar, for example, has grown from 20 thousand employees to a staggering 60 thousand in the past 3 years. Fifty-five percent of their employees have less than two years of tenure.

2. Creating a value proposition that appeals to multiple generations. With four generations in today's workplace, most companies are struggling to create an employee experience that appeals to individuals with diverse needs, preferences and assumptions. The Gap, for example, has 153,000 people in its workforce. The stores have a high percentage of Gen Y employees, while corporate roles and leadership ranks are primarily made up of Gen X'ers and Boomers. How does one create a compelling employee value proposition for the organization?

3. Developing a robust leadership pipeline. I believe one of the biggest potential threats to many corporations is a lack of a robust talent pool from which to select future leaders. This is in part a numbers issue—the Gen X cohort is small and therefore, as I like to say, precious. But it's also an interest issue—many members of Gen X are simply not particularly excited about being considered for these roles. There was wide agreement among the panelists that a lack of individuals ready to move into senior client manager and leadership roles is a critical challenge.

4. Rounding out the capabilities of hires who lack the breadth of necessary for global leadership. It's relatively straightforward to identify and assess experts in specific functional or technical arenas, but much more difficult to determine whether those individuals have the people skills, leadership capabilities, business breadth, and global diversity sensibilities required for the nature of leadership today. Increasingly, the challenge of developing these broader skill sets falls to the corporations. Essar has formed an academy specifically to develop and groom its own leaders.

5. Transferring key knowledge and relationships. The looming retirement of a significant portion of the workforce challenges all companies, but particularly those who are dependant on the strength of tacit knowledge, such as that embedded in customer relationships, a key to Mercer's business success.

6. Stemming the exodus of Gen X'ers from corporate life. A big threat in many firms today is the exodus of mid-career talent—people in whom the organization has invested heavily and in whom it has pinned it hopes for future leadership. For example, developing talent management practices and programs calibrated to leverage technology and create greater work/life balance has been a priority for Mercer over recent years.

7. Redesigning talent management practices to attract and retain Gen Y's. The challenge of calibrating talent management practices and programs to attract and engage our young entrants is critically important to all firms and particularly so for firms that depend on a strong flow of top talent, such professional service firms like Mercer. All three panelists agreed that making the business infrastructure more attractive to Gen Y is a high priority.

8. Creating a workplace that is open to Boomers in their "second careers." Age prejudice still exists, but smart companies are looking for ways to incorporate the talents of Boomers and even older workers in the workforce. In many cases, this requires rethinking roles and work relationships.

9. Overcoming a "norm" of short tenure and frequent movement. Some industries, such as specialty retail, are known for having a very disposable view of talent. Companies intent on changing that norm, such as The Gap, must address both external influences in the

marketplace and an internal mindset. The Gap believes retaining employees in roles for 3+ years will be a key to their future earnings growth.

10. Enlisting executives who don't appreciate the challenge. Many talent executives complain that business leaders still believe that people are lined up outside the door because of the power of the company's brand. The challenge of enlisting the support of all executives for the transition from a talent culture that has traditionally operated with a "buy" strategy to one that places more emphasis on "build" is widely shared.

Three Management ApproachesBased on these definitions, three different managerial approaches to implementation and management can be identified, each reflecting:

different types of technologies involved; degree of complexity in program delivery; objectives (specific / diffused); and process timeframes and the transition from project to passive

approaches to eDemocracy (see Section 2.3.4).

The approaches characterised in this guide are:

the active listening role as a passive form of management; the cultivating role focusing on capacity-building and the stimulation of

action by others; and the steering role, being a programmatic approach with high levels of

management and control.

Active ListeningThe desire by some governments to present themselves as technologically advanced and responsive to the community has tended to lead to situations where electronic democracy is interpreted as a ‘thing’ to be delivered to the waiting (passive and presumably grateful) public.

During the late 1990s this was reflected in a tendency for governments to formulate specific eDemocracy policy statements combined with a number of high profile activities. The best example of this approach can be seen in the United Kingdom under the early period of the Blair Labour government.

This can be beneficial in advancing the eDemocracy agenda. However, the approach can be seen to assume that ICTs are a ‘push’ (one-way) medium like television in which information is formulated centrally and then delivered to a passive audience.

The interactive nature of new digital technologies means that one of the important characteristics of the technology is the open participation by citizens and stakeholders in discussions of public interest. These discussions can include:

unstructured conversation on email lists, through chat facilities, or on bulletin board systems (for example Yahoo! Groups; http://groups.yahoo.com/);

expression of public opinion through alternative and non-profit online news publications (such as the OnLine Opinion magazine [http://www.onlineopinion.com.au/] or more specialist internet media); and

the increasing number of ‘citizen journalists’ publishing on personal websites, blogs, or syndicated multimedia (podcasting or video blogging).

Listening management approaches are common throughout the public sector to allow for quick reactions to emerging issues or problems. This is particularly so amongst policy officers who are routinely tasked with monitoring mainstream media on behalf of their agency and Minister.

While this 'listening' is often undertaken in a relatively ad hoc manner, the inclusion of ICT-based listening approaches can be useful in that:

information can often travel through electronic networks much faster than conventional media, thereby offering the potential for increased responsiveness;

there is a range of commercial and free services [3] that automatically identify key terms and phrases from established media and alternative media and provide instant, or periodic, updates; and

the introduction of RSS-type subscription services [4] allows for the customisation of news and information aggregation via desktop and mobile software.

While some might assume that a listening management approach is a euphemism for inactivity, an effective listening approach does require specific planning and management. Active listening requires:

an investment in time to undertake environmental scanning to identify important sources of information. These sources need to be refreshed and renewed on a regular basis;

a specific allocation of staff time to the collection of information (monitoring);

establishing a mechanism by which information can be stored, searched, indexed, retrieved and interpreted in a meaningful way; and

some means of establishing and assessing the value of the investment in active listening, either for the purposes of appropriately valuing and rewarding staff time, or as a mechanism for justifying this activity given its relative opportunity cost. One of the ongoing concerns associated with this form of eDemocracy activity can be the high ‘noise to signal’ ratio, being the poor return in terms of valuable information that can be gathered given the investment of time required to sift through irrelevant, uninformed, or misleading views and opinions.

Regardless of these concerns, listening approaches can be valuable precursors to the introduction of more structured eEngagement processes. They can provide the means

for understanding the existing tenor of conversation, collecting useful background information and identifying elements of a policy issue that may be particularly engaging to the public.

It is entirely possible that key decision-makers in government will increasingly be as attuned to blog and website discussions of policy as they have traditionally been to television, radio and newspaper reporting.

Listening approaches are often employed following the conclusion of more structured eEngagement processes, either as a means of establishing popular views about the outcomes and impacts of policy decisions, or where the formal process has stimulated an active group of engaged stakeholders to oversight policy implementation.

Exhibit 9: ‘Mass Listening’ as Passive eEngagement Management

Elizabeth Richard of the Public Works and Government Services agency of the Canadian federal government notes that the internet provides public sector managers effective and interesting ‘mass listening’ tools. The proliferation of non-government, public email discussion lists on policy issues can give public sector managers interested in alternative views on policy and program implementation, avenues to undertake informal and unstructured listening to public views without necessarily engaging in formal consultative processes in the first instance.

The benefit of this approach lies in:

the capacity to gather information informally, without the pressures of specific consultative timeframes;

the ability to identify potential participants in formal consultative processes; hearing relatively candid points of view which may not be the same as arguments

put in formal submissions – particularly where an issue is contested; the ability to absorb the level of debate (complexity, language used, degree of

public understanding of policy issues) to allow public documents to be pitched at the right level;

relative anonymity (‘lurking'); and the ability to manage information gathering, particularly where there is concern

that public consultation will lead to a large number of submissions (volume management).

CultivatingLike the listening approach, cultivating or ‘facilitative’ management approaches rely on utilising existing skills found in civil society as the basis for successful community participation. Whereas active listening approaches can be valuable where there is an identifiable community of interest around the issue of concern, ‘cultivating’ recognises the need for outside assistance in stimulating participation.

In many policy areas, it may not be possible to identify existing communities of interest with which to engage. The public sector manager may find that the target audience lacks the technical capacity to use ICTs to participate in policy debate (where interested stakeholders are diffused through the society), or there has not been a recognition of a shared issue or concern that has given rise to mobilisation of interests.

Cultivation requires a number of activities:

the identification of a specific and definable community of concern based on locale (such as a local community that has high levels of unemployment or crime) or non-geographic factors such as shared experience, or other identifiable characteristics (e.g. during 2005 the Victorian Office of Women's Policy undertook an online consultation associated with the experiences of working mothers across Victoria);

definition of the characteristics of particular problems, which may be specific (lack of access to public transport, for example) or generalised (such as issues associated with school retention rates);

determination of required inputs to address issue(s) of concern; development of participatory structures to deliver the required solutions; stimulation of collective activity; and development of the skills required to manage within the community

(including appropriate governance and reporting requirements).

Depending upon the nature of the specific area of concern, the level of community involvement in initial planning and preparation may be limited or specific. This will depend on the nature of the problem and the existing capacity of local individuals or organisations to participate in early planning processes.

There are distinctly different approaches to ‘cultivating’ community participation, depending on whether:

there is a clear recognition of a specific deficit which needs to be countered (the ‘provision’ model); or

the community (geographical, policy, or community-of-interest) is active in defining the need, for example, customising a specific response to a social concern (the ‘partnership’ model).

The exact character of the response by the administering agency or agencies (cultivating models often necessitate partnerships across government) can be highly programmatic in character, or may be more intangible. Some programmatic examples include:

the provision of ICTs (hardware); skills development; community training programs; and/or volunteering schemes.

It is also important to consider that less formalised activities can also fall under this approach. A good example is capacity-building in community groups that results from their inclusion in consultation and management processes. Inclusion enhances the position of organisations, thereby encouraging growth in membership and enhancing their representativeness. The result can be a stakeholder group of greater value to the public sector manager.

While these approaches can be used cynically,[5] they can be powerful in stimulating active organisations outside of government. Developing long term relations with formative groups can be important for the public sector manager with a medium term objective of creating a future partnership.

Given the nature of this type of management process, cultivation generally focuses on ‘before and after’ comparisons to determine measures of public value. For some projects this can be quite crude (e.g. percentage of free access terminals per capita) and others more complex and sophisticated (e.g. measures of social inclusiveness or similar ‘social capital’ metrics[6]).

Often, the key issues associated with cultivation management relate to the capacity to assess changes over time, particularly where programmatic activities have concluded, but there is an expectation of ongoing value creation.

SteeringIn contrast to the above approaches, the final type of management response – steering – reflects a far more instrumental project management approach to policy delivery. Steering management approaches are common in developing eEngagement projects because of the emphasis placed on delivering short-term, specific and instrumental (policy development, acceptance testing and decision-making) outcomes.

Exhibit 10: Cultivating Approaches to eEngagement Management

Cultivating management approaches can yield powerful outcomes in the areas of community development, capacity building and the stimulation of active communities of interest.

Examples of this type of approach include:

The Argyll and Bute Council of Scotland introduced a number of community telecentres in three remote island communities (Islay, Jura and Colonsay) offering personal computers with internet access and videoconferencing. The services have been highly popular, particularly during harsh winter months, with the services used to facilitate business operations, provide personal access to medical consultations (eService outcomes) and have been used extensively by the farming community to lobby the European Union over farm tenancy issues. While some of these applications were planned and expected by project managers, the use to which the videoconferencing service have been employed have been wider than expectations, leading to a multiplier effect of the technological investment.

The New South Wales government established the communitybuilders.nsw website as a centralised clearing house for information associated with social, economic and environmental renewal through community-based organisations, non-profit groups and volunteering projects. The website provides information about organisation and management, financial assistance and planning and includes an extensive online discussion forum where people involved in these areas can exchange information and advice. While the Department of Community Services hosts and manages the website, the real value gained is through the interaction between citizens and citizens groups to solve local problems. See: http://www.communitybuilders.nsw.gov.au

A variation of the communitybuilders model has been introduced by the British Broadcasting Corporation as its Action Network website (http://www.bbc.co.uk/dna/actionnetwork/). While community builders focuses on local renewal projects, Action Network has a more overtly political focus, allowing citizens to chat about political issues, start campaigns and network with like-minded individuals.

While steering approaches generally include participatory design elements appropriate to the anticipated stakeholder community, (either through the establishment of formal reference groups, or ad hoc consultation and negotiation), steering management approaches tend to be agency-driven.

This is due to the agency having:

the capacity to develop a comprehensive engagement strategy; the resources to develop or acquire the appropriate technologies; and the ability to provide a ‘hook’ (access point) into the formal process of

policy development in government.

Effective steering requires detailed preparation for the development of the eEngagement process, with clear process planning and well-defined timeframes. Flexibility in this approach is normally accommodated through reflective management and contingency planning. This is often important where the engagement process forms part of a specific policy initiative associated with the executive, or, where the consultation must meet the necessary timeframes for parliamentary reporting or legislative drafting.

The key aspects of appropriate steering management are:

the integration of project development within wider strategic planning processes;

the development of clearly articulated project deliverables, checkpoints and delivery timeframes;

the need for specific program evaluation and reporting; and the tendency for these processes to be assessed against very specific

outcome requirements (commonly expressed in terms of numerical metrics, such as numbers of participants, or output-based performance criteria).

Exhibit 11: The ‘Electronic Discussion List’ Model as eEngagement

The City of Darebin eForum pilot project in Melbourne reflects a conventional ‘steering’ approach to eEngagement management. The Council undertook to develop a structured online discussion forum which included Council staff and members of the community to discuss a range of local issues over a set period of time. Using basic email management technology, the council developed an engagement and promotional plan. A project officer recruited from local community groups moderated and summarised discussions and fed information collected back into the policy-making officers and Councillors at the end of each structured discussion. This approach was highly programmatic in character, with clear timeframes for action, close management of activities and control of interaction through the process of moderation.

Relationship Between the Three Approaches While eEngagement activities tend to focus on cultivating and steering, [7] it is highly likely that a single project may require a number of different management approaches at different points of the planning and implementation process. A clear recognition of the relationship between project initiation, development, implementation, evaluation and closeout stages of any eEngagement activity can be extremely valuable in allowing the

management group to recognise the appropriate management style for the particular phase of activity.

In addition, some reflection by project team members on their particular strengths and preferences can be useful in managing the transition between management approaches appropriate for different phases of project implementation.

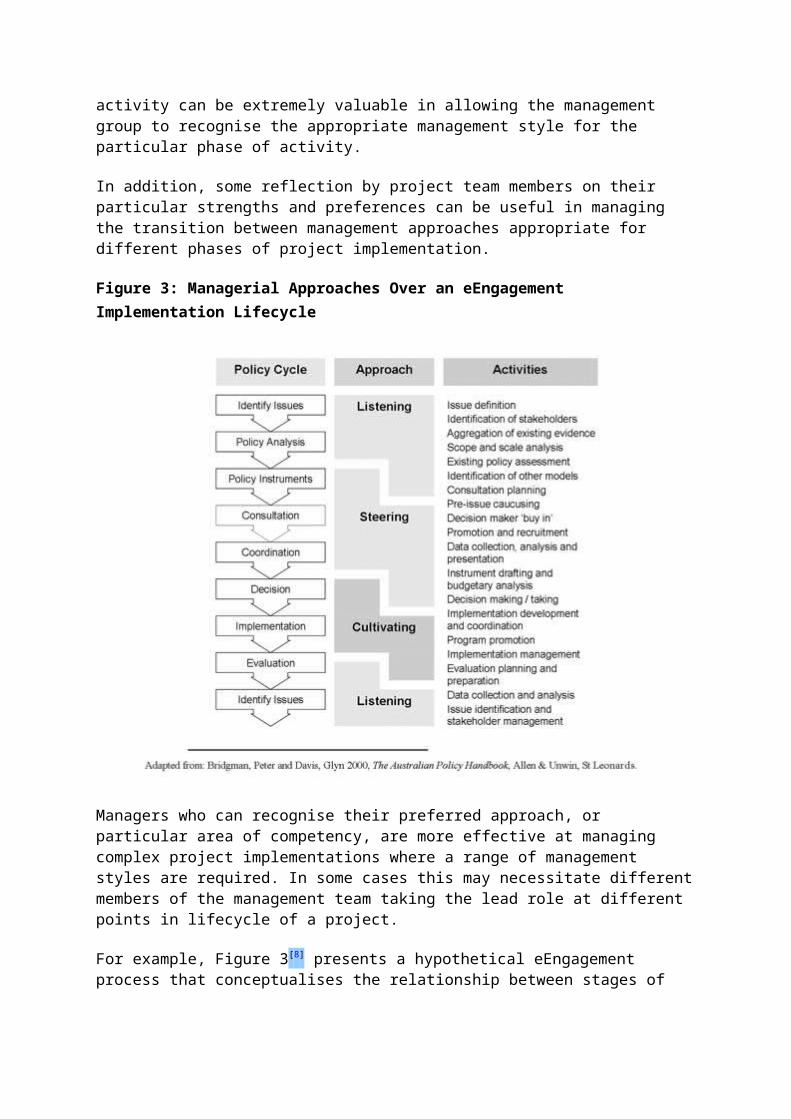

Figure 3: Managerial Approaches Over an eEngagement Implementation Lifecycle

Managers who can recognise their preferred approach, or particular area of competency, are more effective at managing complex project implementations where a range of management styles are required. In some cases this may necessitate different members of the management team taking the lead role at different points in lifecycle of a project.

For example, Figure 3[8] presents a hypothetical eEngagement process that conceptualises the relationship between stages of the policy cycle and the range of different management approaches.

Communication for Rural DevelopmentSummary2.2.2 Communication for rural development

Strategies that include communication for rural development as a significant aspect of agricultural and rural development are sorely needed. Efforts in this direction are being made, but

governments have yet to recognize fully the potential of this factor in promoting public awareness and information on agricultural innovations, as well as on the planning and development of small business, not to mention employment opportunities and basic news about health, education and other factors of concern to rural populations, particularly those seeking to improve their livelihoods and thereby enhance the quality of their lives.

Rural development is often discussed together with agricultural development and agricultural extension. In fact "agricultural extension" is often termed "rural extension" in the literature. In contrast, rural development includes but nonetheless expands beyond the confines of agriculture, and furthermore requires and also involves developments other than agriculture. Accordingly, government should consider the establishment of a communication policy that while supporting agricultural extension for rural development also assumes the role of a "rural extension" service aimed as well at diffusing non-agricultural information and advice to people in rural areas.

A communication policy would aim to systematically promote rural communication activities, especially interactive radio but also other successful media such as tape recorder and video instructional programmes. Computers and the Internet may not yet be accessible to rural communities but they serve the communication intermediaries and agricultural extension agents who provide information to rural populations. Other devices such as cell phones hold considerable promise for the transfer and exchange of practical information.

For reaching the final agricultural and basic needs information users in rural areas today, radio is the most powerful and cost-effective medium. However, other traditional and modern communication methods are equally valuable, depending on the situation and availability, like face-to-face exchanges (via demonstration and village meetings); one-way print media (such as, newspapers, newsletters, magazines, journals, posters); one-way telecommunication media (including non-interactive radio, television, satellite, computer, cassette, video and loud-speakers mounted on cars); and two-way media: (telephone, including teleconferencing, and interactive (Internet) computer).

Information and communication technologies (ICTs) have proved to be important for Internet users and for the intermediate users who work with the poor. Pilot experiences show that various media are valuable for assisting agricultural producers with information and advice as to agricultural innovations, market prices, pest infestations and weather alerts.

ICTs also serve non-farming rural people with information and advice regarding business opportunities relating to food processing, wholesale outlets and other income-generating opportunities. In the case of non-agricultural rural development interests, a communication for rural development policy would aim to promote diffusion of information about non-agricultural micro-enterprise development, small business planning, nutrition, health and generally serve to provide useful, other-than-agriculture information.

By its very nature as mass media, communication for rural development can provide information useful to all segments of rural populations. However, it would serve as a first effort toward advancement of "rural extension" services and activities aimed at rural development concerns beyond those of agriculture. Thus, extension and communication activities would be expected to work in tandem, allied in the common cause of supporting income-generating activities, both agricultural and non-agricultural.

Communication as related to extension services immediately suggests several avenues of mutual support. For example: these would include national services relating to extension and communication, specialized extension communication services, extension services promoted by producers, commercialized extension services, and mass media extension-related services. A similar orientation toward other aspects of rural development information and technical advice is evident considering the de Janvry-Sadoulet rural development pathways and other related rural development needs such as information and assistance with health problems, most notably Human Immunodeficiency Virus/Acquired Immunodeficiency Syndrome (HIV/AIDS) in case of sub-Saharan Africa.

Rural extension and radio need to be more purposely connected. Radio, according to contemporary specialists (FAO 2003c), is under utilized at present. While ICTs and their connection to radio hold

promise for the future, some consider radio to be "the one to watch" (FAO 2003c). In this connection, regional networks are being launched. Examples are The World Association for Community Radio Broadcasters (AMARC) and the Latin American Association for Radio Education (ALER). Global initiatives have begun: Developing Countries Farm Radio Network (DCFRN) and UNESCO Community Media Centres.

Strategic PlanningDefined and Differentiated

Purpose Time Horizon

Distribution Hallmarks

Strategic Planning

To bring the entire community together working toward the same future vision of success in the context of its core values

A Strategic Plan is a framework for strategic thinking that helps a school stay competitive, live into its core values, ward off threats and take advantage of opportunities.

3-5 years As wide as possible Mission Vision Core Values Statements Overarching Goals Strategies Initiatives Evaluation System

Organic in areas of strategy and initiatives; static for the duration of the plan in areas of mission, vision, values and goals.

Process hallmarks are:

inclusivity, accountability, shared responsibility, evaluation and institutionalization.

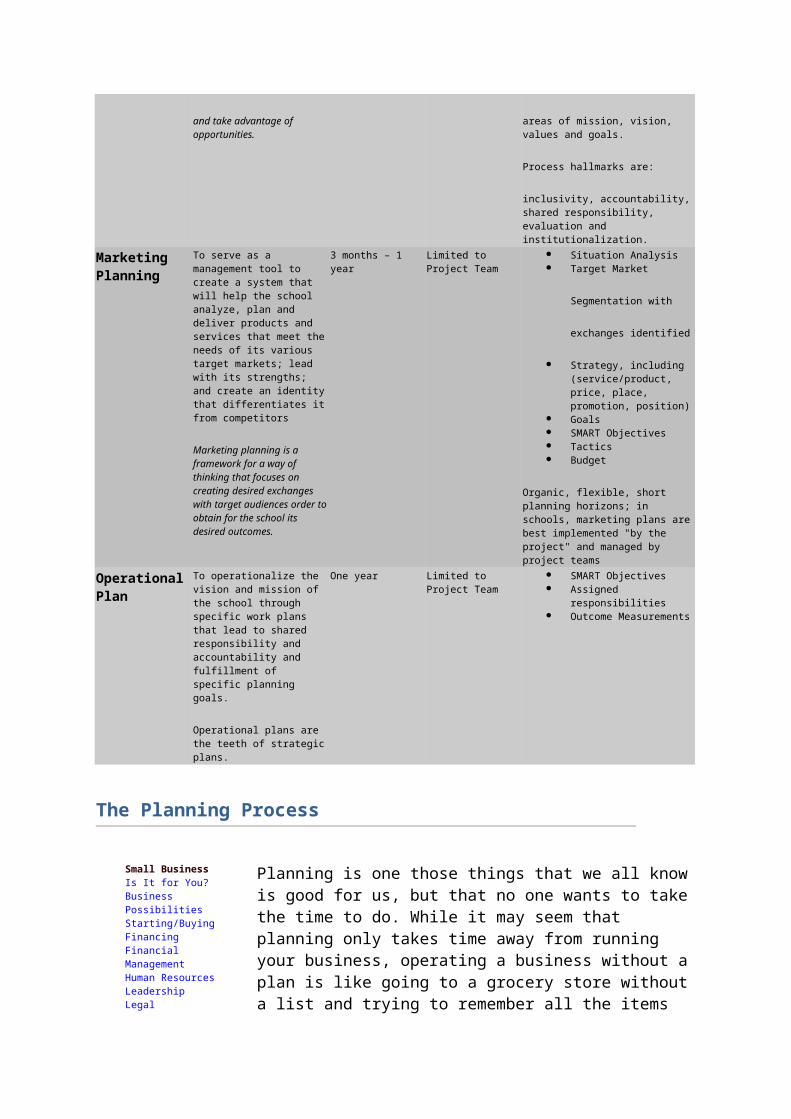

Marketing Planning

To serve as a management tool to create a system that will help the school analyze, plan and deliver products and services that meet the needs of its various target markets; lead with its strengths; and create an identity that differentiates it from competitors

Marketing planning is a framework for a way of thinking that focuses on creating desired exchanges with target audiences order to obtain for the school its desired outcomes.

3 months – 1 year Limited to Project Team

Situation Analysis Target Market

Segmentation with

exchanges identified

Strategy, including (service/product, price, place, promotion, position)

Goals SMART Objectives Tactics Budget

Organic, flexible, short planning horizons; in schools, marketing plans are best implemented "by the project" and managed by project teams

Operational Plan

To operationalize the vision and mission of the school through specific work plans that lead to shared responsibility and accountability and fulfillment of specific planning goals.

Operational plans are the teeth of strategic plans.

One year Limited to Project Team

SMART Objectives Assigned responsibilities Outcome Measurements

The Planning Process

Small Business Is It for You?Business PossibilitiesStarting/BuyingFinancingFinancial ManagementHuman ResourcesLeadershipLegalManagementMarketingOfficePlanningTaxes

Resources About Small BusinessBooksBusiness SchoolsEducationFederal GovernmentGlossaryHistory of BusinessInternationalQuotationsState Government

Interests African-AmericanAsian-AmericanDisabledFamily-OwnedGay/LesbianHispanicHome-basedNative AmericanRuralSecond CareerSocial EnterpriseVeteransWomenYoung

Planning is one those things that we all know is good for us, but that no one wants to take the time to do. While it may seem that planning only takes time away from running your business, operating a business without a plan is like going to a grocery store without a list and trying to remember all the items that are needed. One comes out of the store having forgotten something critical - and having purchased a number of items that are totally frivolous and may never be used. It is the same for a business operating without a plan. Critical issues do not get addressed - and some tasks get done that have no relationship to the direction the business needs to go. For a business, however, the consequences of these unaddressed issues can range from inconvenience to bankruptcy.

Part of this reluctance is due to how complicated the process is viewed. Yet a complicated plan is almost as useless as none. The real question is how to make something simple that fits your business' needs. Can a good grocery list system be devised that isn't unnecessarily burdensome for all involved? Of course. Let's take a look as what planning really entails.

The word "plan" originated from then Medieval Latin word planus which meant a level or flat surface. This evolved in French into being a map or a drawing of any object made by projection upon a flat surface. In English this has become a more general sense of a scheme of action, design or method. Planning in its current usage in business implies a consciousness of what is happening in the business. It does not preclude creativity or instinct, but it does add a layer of awareness that spells the difference between survival and extinction in a changing environment. Planning does involve:

an understanding of the business' history an examination of the business' environment an assessment of the business' mission goals a process for reaching those goals a process for gathering information a realization that planning is a continuing process that is

constantly evolving

Planning does not necessarily mean trying to project the future, but being aware of a range of likely futures and being prepared for them as occur.

Business PlanA business plan is used when one is starting a new business or a new process or product within a business. It includes not only a description of the new business, process or product, but also a discussion of how one plans on managing the marketing, development, production, and financing of this new venture.

Organizational Plan

Organizational planning, when it does occur, too often is spurred by crisis, focused on the short term, and not well thought out. To create healthy futures, organizations must construct processes for creating their futures that are not fueled by crisis and turmoil. It can be done.

One of the most confusing aspects for those who want to plan is the variety of terms that are used in conjunction with planning. How do you differentiate between a business plan, a financial plan, a marketing plan, a human resources plan, an operations plan, a strategic plan, a long-range plan and just plain general planning? The simple answer is that each area of your business needs planning so each area should have its own grocery list of what it wishes to accomplish in the future.

Strategic PlanA strategic plan usually refers to the overall direction you wish your business to take over the longer term. Consequently, a long-range plan and a strategic plan are often used synonymously. Within that overall strategy a business will have shorter term financial goals, marketing goals, production goals, and human resource goals that will each need some type of plan if they are to be achieved.

Just because a strategic plan is longer term does not mean it is never changed, however. One of the most serious mistakes businesses make is not revising their strategic plan regularly. The environment the business is operating in is changing constantly. The plan must be revisited at regular intervals to reflect the impact on the business of these external factors.

There are some universal principles that are true across all types of planning. Before tackling more specific planning models, it is wise to gain an understanding of the basic principles of general planning.

Planning Principles

Any plan should include who, what, when, where, how, and why.

Who is needed to accomplish this task? What needs to be done? When does it start and end? Where will it take place? How will it happen? Why must we do it?

Along with the answers to these questions there needs to be some operational scheme to organize the tasks needed to achieve the goal.

A helpful approach is to work backward from the goal to decide

what must be done to reach it. The backward approach is a way of looking at the big picture first, and then planning all tasks, conditions, and details in a logical sequence to make the big picture happen. From this a to-do list can easily be made. This list will become a checklist to ensure everything is progressing as planned. Adjustments can be made based on changing circumstances. The plan (list) should be referenced often as a set of signposts on the journey towards the goals.

For many of us who left corporate America in favor of a smaller work environment, the idea of drafting a plan may seem offensive. After all, isn't frustration with all that busywork one of the reasons we left in the first place? We all have an aversion to doing anything on our job that doesn't immediately help the situation we are now experiencing. However, isn't it also true that a little foresight and action before the fact can help eliminate many of the problems we face each day. Wouldn't it be nice to anticipate something like a price cut by your major competitor or a rise in the interest rate on your credit line? Of course it would. And with that anticipation comes an organized and effective response

m

A managerial economist helps the management by using his analytical skills and highly developed techniques in solving complex issues of successful decision-making and future advanced planning.

The role of managerial economist can be summarized as follows:

1. He studies the economic patterns at macro-level and analysis it’s significance to the specific firm he is working in.

2. He has to consistently examine the probabilities of transforming an ever-changing economic environment into profitable business avenues.

3. He assists the business planning process of a firm.4. He also carries cost-benefit analysis.5. He assists the management in the decisions pertaining to internal functioning of a firm such as

changes in price, investment plans, type of goods /services to be produced, inputs to be used, techniques of production to be employed, expansion/ contraction of firm, allocation of capital, location of new plants, quantity of output to be produced, replacement of plant equipment, sales forecasting, inventory forecasting, etc.

6. In addition, a managerial economist has to analyze changes in macro- economic indicators such as national income, population, business cycles, and their possible effect on the firm’s functioning.

7. He is also involved in advicing the management on public relations, foreign exchange, and trade. He guides the firm on the likely impact of changes in monetary and fiscal policy on the firm’s functioning.

8. He also makes an economic analysis of the firms in competition. He has to collect economic data and examine all crucial information about the environment in which the firm operates.

9. The most significant function of a managerial economist is to conduct a detailed research on industrial market.

10. In order to perform all these roles, a managerial economist has to conduct an elaborate statistical analysis.

11. He must be vigilant and must have ability to cope up with the pressures.12. He also provides management with economic information such as tax rates, competitor’s price and

product, etc. They give their valuable advice to government authorities as well.13. At times, a managerial economist has to prepare speeches for top management

Managerial Economics - Definition

3. Managerial economics is best defined as

a. the study of economics by managers.

b. the study of the aggregate economic activity.

c. the study of how managers make decisions about the use of scarce resources.

d. all of the above are good definitions.

1

The Nature and Scopeof ManagerialEconomicsDr. Mohammad Abdul Mukhyi, SE., MM4/18/2010 Managerial Economic 2

_ Economics is the social science that studies theproduction, distribution, and consumption of goodsand services._ Managerial economics (sometimes referred to asbusiness economics), is a branch of economics thatapplies microeconomic analysis to decisionmethods of businesses or other management units.As such, it bridges economic theory and economicsin practice. It draws heavily from quantitativetechniques such as regression analysis andcorrelation, Lagrangian calculus (linear). If there isa unifying theme that runs through most ofmanagerial economics it is the attempt to optimizebusiness decisions given the firm's objectives andgiven constraints imposed by scarcity, for examplethrough the use of operations research andprogramming.24/18/2010 Managerial Economic 3

Managerial Economics_ Manager_ A person who directsresources to achieve astated goal._ Economics

_ The science of makingdecisions in the presenceof scare resources._ Managerial Economics_ The study of how to directscarce resources in theway that most efficientlyachieves a managerialgoal.4/18/2010 Managerial Economic 4The Global Trade EconomyThe MetropolitanBioregional EconomyMarketSectorsCommodity Agriculture (wheat, rice, soybeans,beef, coffee, bananas, etc.)ElectronicsVehiclesHigh Tech Health Care, PharmaceuticalsHardwareMass Produced Clothing, Cloth GoodsHydrocarbon-Based EnergyFinancial ServicesShort term R&DOrganic & Specialty AgricultureLocal Commerce (locallyproduced goods and services)Construction (Housing, etc.)Education (basic, lifemanagement, citizenship)Basic & Holistic Health Care &EducationHand CraftsArtsSportsChild CareElder CareHome & Yard CarePublicGoods(The"Commons")Global EcologyFair Trade PoliciesNational DefenseLong Range R&DCatastrophic Reinsurance (health, disasters, etc.)Coordination of Health, Education, Welfare(Information and infrastructure investments)Major (Corporate, Foundations, etc.) PhilanthropySustainable Land UseEmployment SecurityEducation (basic, lifemanagement, citizenship)Urban Environment & SocialWelfare ServicesConservation & RecreationLocal PhilanthropyBernard Lietaer and Art Warmoth, © 1999

34/18/2010 Managerial Economic 54/18/2010 Managerial Economic 6

How Is Managerial EconomicsUseful?_ Evaluating Choice Alternatives_ Identify ways to efficiently achieve goals._ Specify pricing and production strategies._ Provide production and marketing rules to help

maximize net profits._ Making the Best Decision_ Managerial economics can be used to efficientlymeet management objectives._ Managerial economics can be used tounderstand logic of company, consumer, andgovernment decisions.44/18/2010 Managerial Economic 7

Definisi:Managerial economic refers to the application ofeconomic theory and the tools of analysis ofdecision science to examine how an organizationcan achieve its aims or objectives most efficiently.The scope of managerial economics:- Economic sciences- Decision sciences- Other science having an effect on to decisionmaking.4/18/2010 Managerial Economic 8

SCOPE & IMPORTANCE OFMANAGERIAL ECONOMICS:Out of two major managerial functions served by thesubject matter under managerial economics are decisionmaking and forward planning:Lets explore the scope for decision making:1. Decision relating to demand.2. Decision related to Cost and production.3. Decision relating to price and market.4. Decision relating to profit management.5. Macro economic factor.54/18/2010 Managerial Economic 9Relationship to economic theory1. Micro economic2. Macro economicPenekanan:1. Normative economic2. Positif economicRelationship to the decision sciencesIlmu ekonomi memberikan kerangka teoritis pengambilankepusuan manajerial untuk membentuk model-modelkeputusan, menganalisis pengaruh serangkaian tindakanalternatif dsan mengevaluasi hasil-hasil yang diperoleh.4/18/2010 Managerial Economic 10

Relatioinship to the functional areas ofbusiness Administration studies.Bidang Fungsional Akuntansi, keuangan, pemasaran,

personalia, produksiBidang alat Akuntansi, sistem informasimanajemen, ekonomi manajerial,perilaku organisasi, metode kuantitatiff,riset operasional, statistik, matematik.Bidang khusus Perbankan, asuransi, bisnisinternasional, regulasiMata kuliahterpaduKebijakan perusahaan, ekonomimanajerial64/18/2010 Managerial Economic 11

Theory of the Firm_ Expected Value Maximization_ Owner-managers maximize short-run profits._ Primary goal is long-term expected value maximization._ Constraints and the Theory of the Firm_ Resource constraints._ Social constraints_ Limitations of the Theory of the Firm_ Alternative theory adds perspective._ Competition forces efficiency._ Hostile takeovers threaten inefficient managers.4/18/2010 Managerial Economic 12

Economic vs. AccountingProfits_ Accounting Profits_ Total revenue (sales) minus dollar cost ofproducing goods or services_ Reported on the firm’s income statement_ Economic Profits_ Total revenue minus total opportunity cost74/18/2010 Managerial Economic 13

Opportunity Cost_ Accounting Costs_ The explicit costs of the resources needed toproduce produce goods or services_ Reported on the firm’s income statement_ Opportunity Cost_ The cost of the explicit and implicit resourcesthat are foregone when a decision is made_ Economic Profits_ Total revenue minus total opportunity cost4/18/2010 Managerial Economic 14

Why Do Profits Vary AmongFirms?_Disequilibrium Profit Theories_Rapid growth in revenues._Rapid decline in costs._ Compensatory Profit Theories_Better, faster, or cheaper thanthe competition is profitable.84/18/2010 Managerial Economic 15

Role of Business in Society_ Why Firms Exist_ Business is useful in satisfying consumerwants._ Business contributes to social welfare_ Social Responsibility of Business_ Serve customers._ Provide employment opportunities._ Obey laws and regulations.4/18/2010 Managerial Economic 16

94/18/2010 Managerial Economic 17

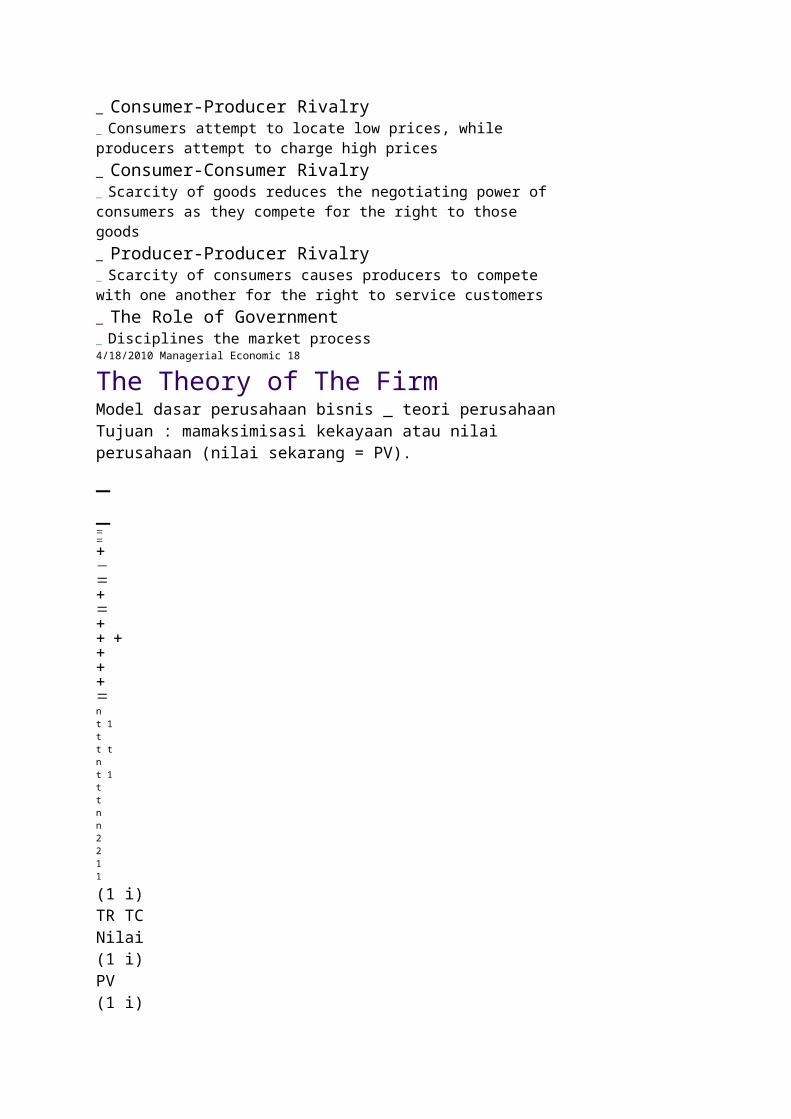

Market Interactions_ Consumer-Producer Rivalry_ Consumers attempt to locate low prices, whileproducers attempt to charge high prices_ Consumer-Consumer Rivalry_ Scarcity of goods reduces the negotiating power ofconsumers as they compete for the right to thosegoods_ Producer-Producer Rivalry_ Scarcity of consumers causes producers to competewith one another for the right to service customers_ The Role of Government_ Disciplines the market process4/18/2010 Managerial Economic 18

The Theory of The FirmModel dasar perusahaan bisnis _ teori perusahaanTujuan : mamaksimisasi kekayaan atau nilaiperusahaan (nilai sekarang = PV)._

_−nt 1tt tnt 1ttnn2211(1 i)TR TCNilai(1 i)PV(1 i)....(1 i) (1 i)PV104/18/2010 Managerial Economic 19

Constraint on the operationof the firmConstraint :1. Sumberdaya2. Kuantitas dan kualitas output3. Hukum4/18/2010 Managerial Economic 20

Firm Valuation_ The value of a firm equals the present value ofall its future profits_ PV = S pt / (1 + i)t

_ If profits grow at a constant rate, g < i, then:_ PV = po ( 1+i) / ( i - g), po = current profit level._ Maximizing Short-Term Profits_ If the growth rate in profits < interest rate and bothremain constant, maximizing the present value of all

future profits is the same as maximizing currentprofits.114/18/2010 Managerial Economic 21

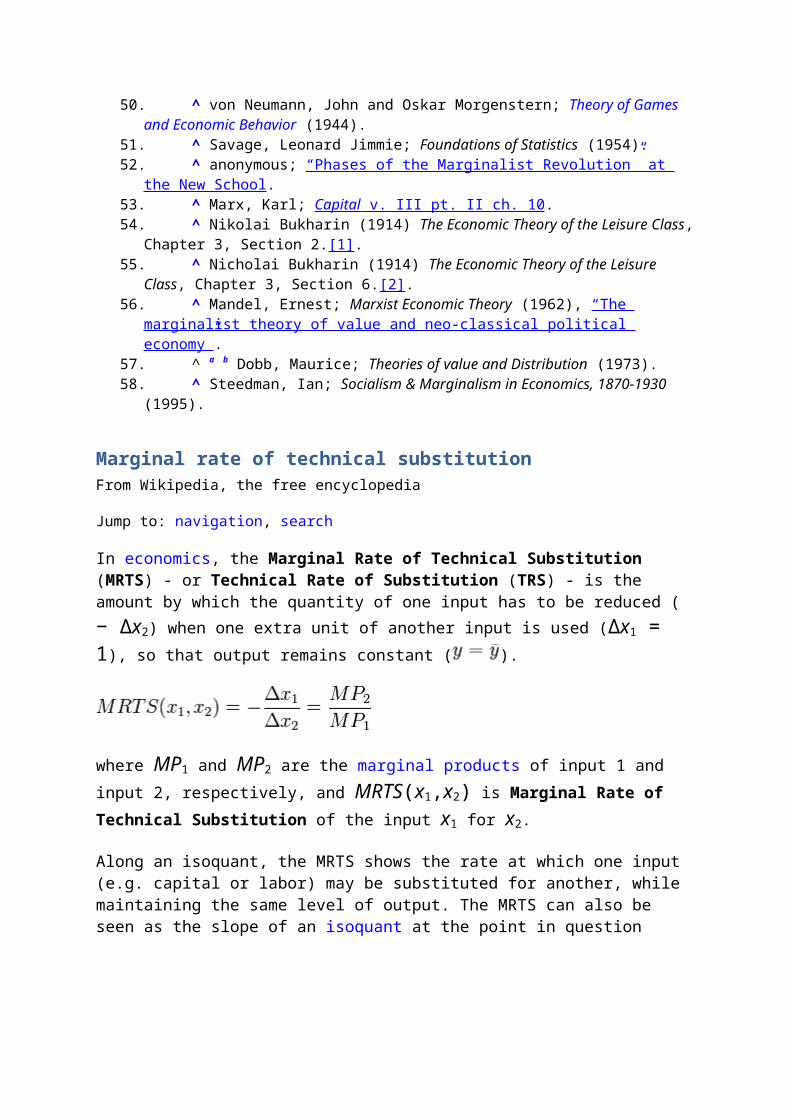

_ Control Variables_ Output_ Price_ Product Quality_ Advertising_ R&D_ Basic Managerial Question: How much ofthe control variable should be used tomaximize net benefits?Marginal (Incremental)Analysis4/18/2010 Managerial Economic 22

Net Benefits_ Net Benefits = Total Benefits - Total Costs_ Profits = Revenue - Costs124/18/2010 Managerial Economic 23

Marginal Benefit (MB)_ Change in total benefits arising from achange in the control variable, Q:MB = DB / DQ_ Slope (calculus derivative) of the totalbenefit curve4/18/2010 Managerial Economic 24

Marginal Cost (MC)_ Change in total costs arising from a changein the control variable, Q:MC = DC / DQ_ Slope (calculus derivative) of the total costcurve134/18/2010 Managerial Economic 25

Marginal Principle_ To maximize net benefits, the managerialcontrol variable should be increased upto the point where MB = MC_ MB > MC means the last unit of thecontrol variable increased benefits more

than it increased costs_ MB < MC means the last unit of thecontrol variable increased costs morethan it increased benefits4/18/2010 Managerial Economic 26

The Geometry of OptimizationQBenefits & CostsBenefitsCostsQ*BCSlope = MCSlope =MB144/18/2010 Managerial Economic 27

Literatur_ Michael R. Baye, Managerial Economics andBusiness Strategy, 6e. ©The McGraw-HillCompanies, Inc., 2008_ Dominick Savatore, Managerial Economic,Oxford University Press, 2007_ Mark Hirschey, MANAGERIAL ECONOMICS11th EditionProblem1. Review the decision criteria that you took intoaccount in choosing your college or university; inwhat sense was the choice a managerial decision?...an entrepreneurial decision?2. Explain how the existence of multiple possiblegoals may be accommodated in a decisionanalysis.3. 3. Explain how the achievement of profit in thebusiness firm may be a by-product of otheractivities rather than an object of direct pursuit;what are the managerial implications?4/18/2010 Managerial Economic 28

Basic economic tools in managerial economics for decision makingYou are Here:

Home > Managerial Economics > Basic economic tools in managerial economics for decision making

Share

Business decision making is essentially a process of selecting the best out of alternative opportunities open to the firm. The steps below put managers analytical ability to test and determine the appropriateness and validity of decisions in the modern business world. Following are the various steps in decision making process:

1. Establish objectives2. Specify the decision problem3. Identify the alternatives

.

4. Select the best alternatives5. Implement the decision6. Monitor the performance

Modern business conditions are changing so fast and becoming so competitive and complex that personal business sense, intuition and experience alone are not sufficient to make appropriate business decisions. It is in this area of decision making that economic theories and tools of economic analysis contribute a great deal.

Basic economic tools in managerial economics for decision making:

Economic theory offers a variety of concepts and analytical tools which can be of considerable assistance to the managers in his decision making practice. These tools are helpful for managers in solving their business related problems. These tools are taken as guide in making decision.

Following are the basic economic tools for decision making:

1. Opportunity cost2. Incremental principle3. Principle of the time perspective4. Discounting principle5. Equi-marginal principle

1) Opportunity cost principle:

By the opportunity cost of a decision is meant the sacrifice of alternatives required by that decision.

For e.g.

a) The opportunity cost of the funds employed in one’s own business is the interest that could be earned on those funds if they have been employed in other ventures.

b) The opportunity cost of using a machine to produce one product is the earnings forgone which would have been possible from other products.

c) The opportunity cost of holding Rs. 1000as cash in hand for one year is the 10% rate of interest, which would have been earned had the money been kept as fixed deposit in bank.

Its clear now that opportunity cost requires ascertainment of sacrifices. If a decision involves no sacrifices, its opportunity cost is nil. For decision making opportunity costs are the only relevant costs.

2) Incremental principle: