dls contract

TRANSCRIPT

The following handbook of information relating to the construction industry has been compiled by:

Davis Langdon & Seah Hong Kong Limited38/F Two Landmark East 100 How Ming Street Kwun Tong, Kowloon Hong Kong Telephone : (852) 2830 3500Fax : (852) 2576 0416Email : [email protected] : www.dlsqs.com

© Davis Langdon & Seah Hong Kong Limited 2012

All rights reserved. No part of this publication may be re-produced or copied in any form without prior written permission from Davis Langdon & Seah Hong Kong Limited.

The information contained herein should be regarded as indicative and for general guidance only. Whilst every effort has been made to ensure accuracy, no responsibility can be accepted for errors and omissions, however caused.

If advice concerning individual projects is required, we would be happy to assist.

Unless otherwise stated, costs reflected in this handbook are Hong Kong costs at 4th Quarter 2011.

Davis Langdon & Seah Hong Kong Limited would like to acknowledge the assistance of Knight Frank and Baker & McKenzie in providing additional data and information for this publication.

ISO 9001 : 2008Certificate No. : CC271

Published by Davis Langdon & Seah Hong Kong LimitedPrinted : January 2012 by R&R Publishing Limited

Electronic Cost Handbook

We have a number of options for accessing an electronic version of our Cost Handbook: 1. Download the PDF version from our website to your

Smart Phone. Install an appropriate file management application

(e.g. USB Disk etc) from the App Store or Android Market

Using your phone’s web browser, go to www.dlsqs.com Click “Research” at the top menu Click “Cost Handbook” at menu on the left Click “Construction Cost Handbook China &

Hong Kong 2012” Click “Download” Click "Open in USB Disk" (if you have used the

USB Disk application) from your Smart Phone You can then go to USB Disk to read the

downloaded 2012 Construction Cost Handbook, even when your Smart Phone is in Airplane mode

2. Alternatively, scan the QR code below to directly access the PDF file. From there follow the same instructions as above.

3. Or download our App to your iPhone or iPad by searching for DLS Cost Handbook in the App Store (Note: Android version coming soon).

TABLE OF CONTENTS

1 2

Table of Contents 1About Us 3Quality Management System 4Calendars 5

1. CONSTRUCTION COST DATA

Construction Costs for Hong Kong 9M&E Costs for Hong Kong 11ACMV Costs for Various Designs and Developments in Hong Kong 13Construction Cost Specification for Hong Kong 15Fit-out Costs for Hong Kong 17Unit Costs for Ancillary Facilities for Hong Kong 19Construction Costs for Selected Asian Cities 21M&E Costs for Selected Asian Cities 27Major Rates for Selected Asian Cities 33Construction Costs for Selected International Cities 39

2. GENERAL CONSTRUCTION DATA

2012 Outlook 43Building Cost Trends in Hong Kong 47Labour Index in Hong Kong 50Material Prices in Hong Kong 51Progress Payments 54Estimating Rules of Thumb and Design Norms for Hong Kong 55Construction Activity in Hong Kong 59Construction Value in Hong Kong 60FIREE Recordals Tracker: November 2011 Update 61Hong Kong General Construction Insurance 65Specified Forms for Buildings Ordinance or Regulations for Hong Kong 67Summary of Building Regulations for Hong Kong 69Percentage Site Coverage and Plot Ratios for Hong Kong 70

3. PROPERTY

Property Commentary 75Property Indicators 79Gross Floor Area (GFA) Calculations in Hong Kong 81Gross Floor Area (GFA) Calculations in PRC 83Construction Floor Area (CFA) Definition 85

4. FINANCIAL

Financial Definitions 87 Financial Formulae 88Mortgage Repayment Table 89Composite CPI 90Exchange Rates 91Currency Charts 93Prime Rates 95Hang Seng Index 97

5. OTHER INFORMATION

Utility Costs for Selected Asian Cities 99Conversion Factors 103IDD Codes and Time Differences 105Public Holidays 107Davis Langdon & Seah Professional Services 117DLS Infrastructure Team 119DLS Interior Fitting Out Team 121DLS Project Monitoring Team 123DLS Sustainability Services Team 126Directory of Offices 129Telephone Directory 149

DAVIS LANGDON & SEAH

ABOUT US

First established in 1934 in Singapore under the name "Waters and Watson" we survived the Second World War to become the pre-eminent Quantity Surveying and Construction Cost Management firm in Asia - operating for many years as Langdon Every and Seah. One of our early partners, Mr. Seah Mong Hee, was the first Asian Chartered Surveyor (RICS) in the world.

Our Hong Kong office opened in 1949 and we quickly established ourselves as the leading firm in the profession.

Following a series of global mergers, Davis Langdon & Seah International was founded in 1990. As we begin 2012, Davis Langdon & Seah has grown to almost 3,000 staff in 40 offices across Asia, and continues to cooperate with Davis Langdon in Europe & Middle East, USA, Australia & New Zealand and Africa - forming a network of over 100 offices across more than 30 countries.

We entered the China market in 1984, introducing modern cost management techniques to its newly evolving construction market. Our initial commissions were from Hong Kong and foreign developers investing in China, although we have since then further developed our client base to include state owned enterprises and local private developers. We now have 16 offices across China located in Hong Kong, Shanghai, Beijing, Guangzhou, Shenzhen, Macau, Chongqing, Wuhan, Tianjin, Shenyang, Chengdu, Foshan, Hangzhou, Dalian, Sanya and Suzhou with a total staff count of around 1,400.

For over 60 years, DLS Hong Kong/China has been proactively providing world-class construction consulting services for all types of building and infrastructure projects. We are committed to further extending our professional expertise to related fields and further expanding our activities in China to support the needs of our clients as they explore one of the world's largest and fastest growing markets.

3 4

QUALITY MANAGEMENT SYSTEM

Nowadays an effective Quality Management System is one of the core elements in any kind of business. Davis Langdon and Seah Hong Kong Limited aims to provide not merely quant i ty surveying services but also the highest quality services to meet clients' requirements.

We launched our Quality Management System in 1993 and have continually upgraded our quality standards since then.

Davis Langdon & Seah Hong Kong Limited achieved certification to ISO 9001:1987 by the Hong Kong Quality Assurance Agency in October 1994 to cover quantity surveying services. We were certified to ISO 9001:1994 in October 1995.

The following further displays our commitment to the continual improvement of our Quality Management System:

(i) June 2009 saw Davis Langdon & Seah Hong Kong Limited being certified to the ISO 9001:2008 standard.

(ii) In December 2009, the Hong Kong office of Davis Langdon & Seah China Limited was certified to the ISO 9001:2008 standard.

(iii) In September 2010, Davis Langdon & Seah Macau Limited was certified to the ISO 9001:2008 standard.

Plans are currently well advanced to further extend our HKQAA ISO certification to all our offices in China.

2 0 1 4

2 0 1 3

2 0 1 2

2 0 1 1 2011 JANUARY FEBRUARY MARCH S M T W T F S S M T W T F S S M T W T F S 1 1 2 3 4 5 1 2 3 4 5 2 3 4 5 6 7 8 6 7 8 9 10 11 12 6 7 8 9 10 11 12 9 10 11 12 13 14 15 13 14 15 16 17 18 19 13 14 15 16 17 18 19 16 17 18 19 20 21 22 20 21 22 23 24 25 26 20 21 22 23 24 25 26 23/30 24/31 25 26 27 28 29 27 28 27 28 29 30 31

APRIL MAY JUNE S M T W T F S S M T W T F S S M T W T F S 1 2 1 2 3 4 5 6 7 1 2 3 4 3 4 5 6 7 8 9 8 9 10 11 12 13 14 5 6 7 8 9 10 11 10 11 12 13 14 15 16 15 16 17 18 19 20 21 12 13 14 15 16 17 18 17 18 19 20 21 22 23 22 23 24 25 26 27 28 19 20 21 22 23 24 25 24 25 26 27 28 29 30 29 30 31 26 27 28 29 30

JULY AUGUST SEPTEMBER S M T W T F S S M T W T F S S M T W T F S 1 2 1 2 3 4 5 6 1 2 3 3 4 5 6 7 8 9 7 8 9 10 11 12 13 4 5 6 7 8 9 10 10 11 12 13 14 15 16 14 15 16 17 18 19 20 11 12 13 14 15 16 17 17 18 19 20 21 22 23 21 22 23 24 25 26 27 18 19 20 21 22 23 24 24/31 25 26 27 28 29 30 28 29 30 31 25 26 27 28 29 30

OCTOBER NOVEMBER DECEMBER S M T W T F S S M T W T F S S M T W T F S 1 1 2 3 4 5 1 2 3 2 3 4 5 6 7 8 6 7 8 9 10 11 12 4 5 6 7 8 9 10 9 10 11 12 13 14 15 13 14 15 16 17 18 19 11 12 13 14 15 16 17 16 17 18 19 20 21 22 20 21 22 23 24 25 26 18 19 20 21 22 23 24 23/30 24/31 25 26 27 28 29 27 28 29 30 25 26 27 28 29 30 31

2012 JANUARY FEBRUARY MARCH S M T W T F S S M T W T F S S M T W T F S 1 2 3 4 5 6 7 1 2 3 4 1 2 3 8 9 10 11 12 13 14 5 6 7 8 9 10 11 4 5 6 7 8 9 10 15 16 17 18 19 20 21 12 13 14 15 16 17 18 11 12 13 14 15 16 17 22 23 24 25 26 27 28 19 20 21 22 23 24 25 18 19 20 21 22 23 24 29 30 31 26 27 28 29 25 26 27 28 29 30 31

APRIL MAY JUNE S M T W T F S S M T W T F S S M T W T F S 1 2 3 4 5 6 7 1 2 3 4 5 1 2 8 9 10 11 12 13 14 6 7 8 9 10 11 12 3 4 5 6 7 8 9 15 16 17 18 19 20 21 13 14 15 16 17 18 19 10 11 12 13 14 15 16 22 23 24 25 26 27 28 20 21 22 23 24 25 26 17 18 19 20 21 22 23 29 30 27 28 29 30 31 24 25 26 27 28 29 30

JULY AUGUST SEPTEMBER S M T W T F S S M T W T F S S M T W T F S 1 2 3 4 5 6 7 1 2 3 4 1 8 9 10 11 12 13 14 5 6 7 8 9 10 11 2 3 4 5 6 7 8 15 16 17 18 19 20 21 12 13 14 15 16 17 18 9 10 11 12 13 14 15 22 23 24 25 26 27 28 19 20 21 22 23 24 25 16 17 18 19 20 21 22 29 30 31 26 27 28 29 30 31 24/30 24 25 26 27 28 29

OCTOBER NOVEMBER DECEMBER S M T W T F S S M T W T F S S M T W T F S 1 2 3 4 5 6 1 2 3 1 7 8 9 10 11 12 13 4 5 6 7 8 9 10 2 3 4 5 6 7 8 14 15 16 17 18 19 20 11 12 13 14 15 16 17 9 10 11 12 13 14 15 21 22 23 24 25 26 27 18 19 20 21 22 23 24 16 17 18 19 20 21 22 28 29 30 31 25 26 27 28 29 30 23/30 24/31 25 26 27 28 29

2013 JANUARY FEBRUARY MARCH S M T W T F S S M T W T F S S M T W T F S 1 2 3 4 5 1 2 1 2 6 7 8 9 10 11 12 3 4 5 6 7 8 9 3 4 5 6 7 8 9 13 14 15 16 17 18 19 10 11 12 13 14 15 16 10 11 12 13 14 15 16 20 21 22 23 24 25 26 17 18 19 20 21 22 23 17 18 19 20 21 22 23 27 28 29 30 31 24 25 26 27 28 24/31 25 26 27 28 29 30

APRIL MAY JUNE S M T W T F S S M T W T F S S M T W T F S 1 2 3 4 5 6 1 2 3 4 1 7 8 9 10 11 12 13 5 6 7 8 9 10 11 2 3 4 5 6 7 8 14 15 16 17 18 19 20 12 13 14 15 16 17 18 9 10 11 12 13 14 15 21 22 23 24 25 26 27 19 20 21 22 23 24 25 16 17 18 19 20 21 22 28 29 30 26 27 28 29 30 31 23/30 24 25 26 27 28 29

JULY AUGUST SEPTEMBER S M T W T F S S M T W T F S S M T W T F S 1 2 3 4 5 6 1 2 3 1 2 3 4 5 6 7 7 8 9 10 11 12 13 4 5 6 7 8 9 10 8 9 10 11 12 13 14 14 15 16 17 18 19 20 11 12 13 14 15 16 17 15 16 17 18 19 20 21 21 22 23 24 25 26 27 18 19 20 21 22 23 24 22 23 24 25 26 27 28 28 29 30 31 25 26 27 28 29 30 31 29 30

OCTOBER NOVEMBER DECEMBER S M T W T F S S M T W T F S S M T W T F S 1 2 3 4 5 1 2 1 2 3 4 5 6 7 6 7 8 9 10 11 12 3 4 5 6 7 8 9 8 9 10 11 12 13 14 13 14 15 16 17 18 19 10 11 12 13 14 15 16 15 16 17 18 19 20 21 20 21 22 23 24 25 26 17 18 19 20 21 22 23 22 23 24 25 26 27 28 27 28 29 30 31 24 25 26 27 28 29 30 29 30 31

2014 JANUARY FEBRUARY MARCH S M T W T F S S M T W T F S S M T W T F S 1 2 3 4 1 1 5 6 7 8 9 10 11 2 3 4 5 6 7 8 2 3 4 5 6 7 8 12 13 14 15 16 17 18 9 10 11 12 13 14 15 9 10 11 12 13 14 15 19 20 21 22 23 24 25 16 17 18 19 20 21 22 16 17 18 19 20 21 22 26 27 28 29 30 31 23 24 25 26 27 28 23/30 24/31 25 26 27 28 29

APRIL MAY JUNE S M T W T F S S M T W T F S S M T W T F S 1 2 3 4 5 1 2 3 1 2 3 4 5 6 7 6 7 8 9 10 11 12 4 5 6 7 8 9 10 8 9 10 11 12 13 14 13 14 15 16 17 18 19 11 12 13 14 15 16 17 15 16 17 18 19 20 21 20 21 22 23 24 25 26 18 19 20 21 22 23 24 22 23 24 25 26 27 28 27 28 29 30 25 26 27 28 29 30 31 29 30

JULY AUGUST SEPTEMBER S M T W T F S S M T W T F S S M T W T F S 1 2 3 4 5 1 2 1 2 3 4 5 6 6 7 8 9 10 11 12 3 4 5 6 7 8 9 7 8 9 10 11 12 13 13 14 15 16 17 18 19 10 11 12 13 14 15 16 14 15 16 17 18 19 20 20 21 22 23 24 25 26 17 18 19 20 21 22 23 21 22 23 24 25 26 27 27 28 29 30 31 24/31 25 26 27 28 29 30 28 29 30

OCTOBER NOVEMBER DECEMBER S M T W T F S S M T W T F S S M T W T F S 1 2 3 4 1 1 2 3 4 5 6 5 6 7 8 9 10 11 2 3 4 5 6 7 8 7 8 9 10 11 12 13 12 13 14 15 16 17 18 9 10 11 12 13 14 15 14 15 16 17 18 19 20 19 20 21 22 23 24 25 16 17 18 19 20 21 22 21 22 23 24 25 26 27 26 27 28 29 30 31 24/30 24 25 26 27 28 29 28 29 30 31

CALENDARS

5 6

CONSTRUCTION COST DATAConstruction Costs for Hong Kong

M&E Costs for Hong Kong ACMV Costs for Various Designs and

Developments in Hong Kong

Construction Cost Specification for Hong Kong Fit-out Costs for Hong Kong

Unit Costs for Ancillary Facilities for Hong Kong Construction Costs for Selected Asian Cities

M&E Costs for Selected Asian Cities Major Rates for Selected Asian Cities

Construction Costs for Selected International Cities

1. CONSTRUCTION COST DATA

CONSTRUCTION COSTS FOR HONG KONG

The a

bove

costs

are a

t 4th

Qua

rter 2

011 l

evels

.

CO

NST

RU

CTI

ON

CO

STS

FOR

HO

NG

KO

NG

9 10

BU

ILD

ING

TYP

EH

K$/

m2

BU

ILD

ING

SER

VIC

ESTO

TAL

DO

MES

TIC

Publi

c ren

tal ho

using

, high

rise

6,0

55

- 6,8

10

1,045

-

1,350

7,1

00

- 8,1

60Pr

ivate

hous

ing es

tates

, high

rise

14

,035

- 14

,780

2,4

55

- 3,3

20

16,49

0 -

18,10

0Pr

ivate

luxur

y apa

rtmen

ts, hi

gh ris

e

15,80

5 -

up

3,325

-

4,220

19

,130

up

Terra

ced h

ouse

s

19,06

5 -

20,49

0

2,255

-

2,860

21

,320

- 23

,350

Indivi

dual

pres

tige h

ouse

s

27,48

5

up

2,455

-

3,610

29

,940

up

OFF

ICE/

CO

MM

ERC

IAL

Aver

age s

tanda

rd of

fices

, high

rise

12

,340

- 13

,350

4,1

50

- 5,2

80

16,49

0 -

18,63

0Pr

estig

e offic

es, h

igh ris

e

16,47

0

up

4,850

-

6,130

21

,320

up

Aver

age s

tanda

rd sh

oppin

g cen

tres

11

,840

- 14

,770

4,7

00

- 5,4

30

16,54

0 -

20,20

0Pr

estig

e sho

pping

centr

es

16,42

0

up

4,900

-

6,130

21

,320

up

HO

TELS

3-sta

r bud

get h

otels,

inclu

sive o

f F.F.

& E

.

15,07

0 -

16,63

0

4,930

-

5,700

20

,000

- 22

,330

5-sta

rt lux

ury h

otels,

inclu

sive o

f F.F.

& E

.

21,47

0

up

5,330

-

6,550

26

,800

up

IND

UST

RIA

L

Light

duty

flatte

d fac

tories

, 7.5

kpa (

150 l

b.) lo

ading

6,9

80

- 7,4

10

1,750

-

2,330

8,7

30

- 9,7

40He

avy d

uty fla

tted f

actor

ies an

d war

ehou

ses,

15

kpa (

300 l

b.) lo

ading

7,6

40

- 8,5

90

2,000

-

2,580

9,6

40

- 11

,170

OTH

ERS

Carp

arks

, abo

ve gr

ound

6,2

10

- 6,4

80

1,300

-

2,050

7,5

10

- 8,5

30Pr

imar

y and

seco

ndar

y sch

ools

9,1

20

- 9,3

30

2,050

-

2,850

11

,170

- 12

,180

Inter

natio

nal s

choo

ls

10,96

0 -

11,68

0

3,000

-

3,950

13

,960

- 15

,630

Stud

ent h

ostel

s

8,790

-

10,06

0

3,150

-

3,950

11

,940

- 14

,010

Spor

ts clu

bs in

clusiv

e of F

.F. &

E.

15

,270

- 16

,970

5,3

50

- 6,9

00

20,62

0 -

23,87

0

1. CONSTRUCTION COST DATA

M&E COSTS FOR HONG KONG

M&

E C

OST

S FO

R H

ON

G K

ON

G

11 12

BU

ILD

ING

TYP

EH

K$/

m2

MEC

HANI

CAL

SERV

ICES

ELEC

TRIC

AL

SERV

ICES

FIR

E

SERV

ICES

LIFT

S/

ES

CALA

TORS

HYD

RA

ULI

C

SERV

ICES

TOTA

L

SE

RVIC

ES

DO

MES

TIC

Publi

c ren

tal ho

using

, high

rise

- -

450 -

55

0

75 -

120

20

0 -

250

32

0 -

430

1,04

5 - 1,

350

Priva

te ho

using

estat

es, h

igh ris

e

650 -

85

0

850 -

1,05

0

75 -

120

33

0 -

550

55

0 -

750

2,45

5 - 3,

320

Priva

te lux

ury a

partm

ents,

high

rise

1,10

0 - 1,

300

1,05

0 - 1,

300

75

- 1

20

450

- 65

0

650

- 85

0 3

,325 -

4,22

0Te

rrace

d hou

ses

85

0 - 1,

100

85

0 - 1,

050

55

- 1

10

- -

50

0 -

600

2,25

5 - 2,

860

Indivi

dual

pres

tige h

ouse

s

850 -

1,40

0 1

,050 -

1,50

0

55 -

110

- -

50

0 -

600

2,45

5 - 3,

610

OFF

ICE/

CO

MM

ERC

IAL

Aver

age s

tanda

rd of

fices

, high

rise

1,60

0 - 1,

950

1,30

0 - 1,

650

43

0 -

550

55

0 -

750

27

0 -

380

4,15

0 - 5,

280

Pres

tige o

ffices

, high

rise

1,90

0 - 2,

350

1,60

0 - 1,

950

43

0 -

550

65

0 -

900

27

0 -

380

4,85

0 - 6,

130

Aver

age s

tanda

rd sh

oppin

g cen

tres

1,95

0 - 2,

150

1,40

0 - 1,

600

43

0 -

550

65

0 -

750

27

0 -

380

4,70

0 - 5,

430

Pres

tige s

hopp

ing ce

ntres

1,95

0 - 2,

400

1,60

0 - 1,

950

43

0 -

550

65

0 -

850

27

0 -

380

4,90

0 - 6,

130

HO

TELS

3-star

budg

et ho

tels,

inclus

ive of

F.F.

& E.

1,75

0 - 1,

950

1,50

0 - 1,

750

43

0 -

550

45

0 -

550

80

0 -

900

4,93

0 - 5,

700

5-star

t luxu

ry ho

tels,

inclus

ive of

F.F.

& E.

1,85

0 - 2,

150

1,75

0 - 2,

150

43

0 -

550

45

0 -

650

85

0 - 1

,050

5,33

0 - 6,

550

IND

UST

RIA

LLig

ht du

ty fla

tted f

actor

ies, 7

.5 kp

a

(1

50 lb

.) loa

ding

38

0 -

500

45

0 -

650

25

0 -

300

45

0 -

550

22

0 -

330

1,75

0 - 2,

330

Heav

y duty

flatte

d fac

tories

and

wa

rehou

ses,

15 kp

a (30

0 lb.)

load

ing

380 -

50

0

650 -

85

0

250

- 30

0

500

- 60

0

220

- 33

0 2

,000 -

2,58

0

OTH

ERS

Carp

arks

, abo

ve gr

ound

20

0 -

550

45

0 -

650

25

0 -

300

25

0 -

350

15

0 -

200

1,30

0 - 2,

050

Prim

ary a

nd se

cond

ary s

choo

ls

550 -

85

0

850 -

1,05

0

250

- 35

0

150

- 25

0

250

- 35

0 2

,050 -

2,85

0Int

erna

tiona

l sch

ools

1,30

0 - 1,

600

1,05

0 - 1,

400

25

0 -

350

15

0 -

250

25

0 -

350

3,00

0 - 3,

950

Stud

ent h

ostel

s

650 -

85

0 1

,400 -

1,60

0

350

- 45

0

150

- 25

0

600

- 80

0 3

,150 -

3,95

0Sp

orts

clubs

inclu

sive o

f F.F.

& E

. 2

,500 -

3,00

0 1

,800 -

2,50

0

450

- 60

0

250

- 35

0

350

- 45

0 5

,350 -

6,90

0

The a

bove

costs

are a

t 4th

Qua

rter 2

011 l

evels

.

1. CONSTRUCTION COST DATA

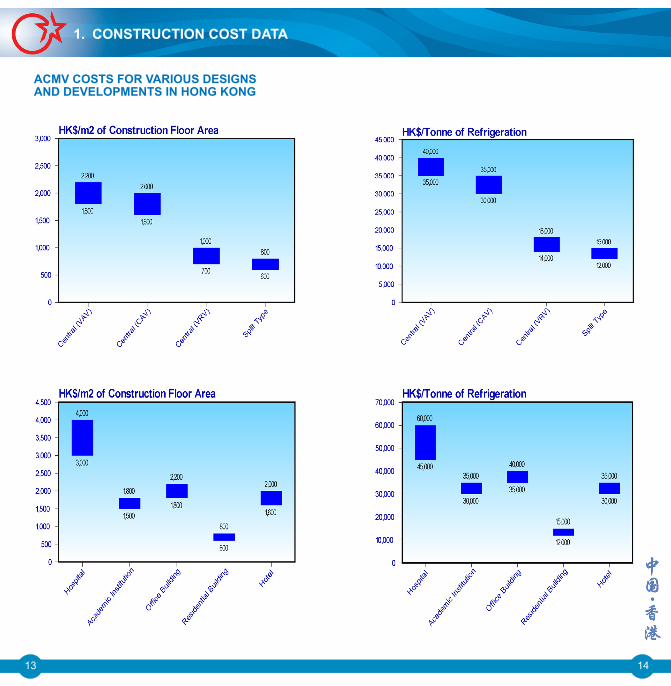

ACMV COSTS FOR VARIOUS DESIGNSAND DEVELOPMENTS IN HONG KONG

13 14

1. CONSTRUCTION COST DATA

CONSTRUCTION COST SPECIFICATION FOR HONG KONG

The costs for the respective categories given on the previous pages are averages based on fixed price competitive tenders. It must be understood that the actual cost of a building will depend upon the design and many other factors and may vary from the figures shown.

The costs per square metre are based on construction floor areas measured to the outside face of the external walls/external perimeter including lift shafts, stairwells, balconies, plant rooms, water tanks and the like.

All buildings are assumed to have no basement (unless otherwise stated) and to be built on flat ground, with normal soil conditions. The costs exclude external works, land costs, professional fees, finance and legal expenses.

The standards for each category of buildings vary from country to country. Standards representing by the construction costs of other regions published hereinafter do not necessarily follow those of Hong Kong.

DOMESTIC

Public rental housing is based on Hong Kong Housing Authority Non-standard Cruciform Block design.

Private housing estates are based on blocks containing 30-50 storeys, with average unit size not greater than 100 m2. Single glazed windows. Tiled or plastered finishes in general.

Air conditioning, kitchen cabinets and home appliances are included for private housing estates, private luxury apartments, terraced houses and prestige houses.

All types of domestic construction include provision of functional light fittings only and no feature light fittings have been allowed. Fitting out works and loose furniture are also not included.

OFFICE/COMMERCIAL

Office based on buildings 20-30 storeys high with floor plans minimum 1,000 m2 per level.

Average standard offices and shopping centres exclude finishes, A/C ducting and light fittings to tenants areas.

Prestige offices have curtain wall elevations and granite finished lobbies, with raised floor, suspended ceiling, A/C ducting and light fittings to tenants areas.

INDUSTRIAL

Flatted factories exclude manufacturing equipment, air-conditioning, electrical distribution systems and special services provisions to tenants areas.

HOTELS

F.F. & E. includes interior decoration and loose furniture etc. but excludes pre-opening expenses and hotel operation system and equipment costs (e.g. cutlery, crockery, linen, uniform, etc.).

Includes 1 level of basement.

OTHERS

Carparks to be multi-storey.

Primary and secondary schools with standard government provisions.

International Schools with upgraded facilities.

Student hostels to university standard.

Sports club to the standard of the Government's indoor recreational centre.

15 16

1. CONSTRUCTION COST DATA

FIT-OUT COSTS FOR HONG KONG

BUILDING TYPE HK$/m2

HOTELS

Public Areas (Front of House) : 3-start Hotel 7,600 - 11,500

4-start Hotel 12,000 - 16,000

5-start Hotel 17,000 up

Guest Rooms : 3-start Hotel 6,000 - 7,400

4-start Hotel 7,500 - 10,000

5-start Hotel 10,000 up

Notes : 1. Includesfurniture,floor,wallandceiling

finishes, drapery, sanitary fittings andlightfittings.

2. Excludespartitioning,M&Eworks,buildingshell,chandeliers,operationalitemsandequipment (e.g. cutlery, crockery, linen,television, refrigerator etc.), openingexpenses,stageequipmentandcomputersystems.

OFFICES

General office 4,800 - 7,400

Executive office 7,500 - 10,500

Prestige office 10,500 up

Notes :1. Local/Taiwanese/PRCfurnitureallowed

forgeneraloffices.2. Includesfurniture,partitioning,electrical

work,minoralterationtoair-conditioning,fire servicesand suspended ceiling tosuitlayout.

3. Excludestelephones,datacabling,officeequipment(e.g.computers,photocopiers,faxmachines,UPS,etc).

BUILDING TYPE HK$/m2

DEPARTMENT STORES

General department store 6,000 - 9,300Prestige department store 10,000 up

Notes : 1. Includeselectricalwork,additionalFCU

andminoralterationof fireservices tosuitlayout.

2. Excludes facademodification, datacabling,operationalitemsandequipment(e.g.computers,P.O.S.,officeequipment)andopeningexpenses.

RESTAURANTS

General dining restaurant 7,600 - 15,000

Fine dining restaurant 16,000 up

Notes :1. Includesfurniture,floor,wallandceiling

finishes,electricalwork,minoralterationto air-conditioning and fire servicesinstallation to suit layout, exhaust forkitchen.

2. Excludesexhaustflue,operationalitems(e.g.cutlery,crockery,linen,utensils,etc.).

17 18

1. CONSTRUCTION COST DATA

19 20

DESCRIPTION UNIT HK$

SQUASH COURTS

Single court with glass backwall including associated mechanical and electrical services but excluding any public facilities (enclosing structure not included).

per court 420,000

TENNIS COURTS

Single court on grade with acrylic surfacing and complete with chain link fence.

per court 870,000

Single court on grade with artificial turf surfacing and complete with chain link fence.

per court 980,000

Extra for lighting. per court 300,000

SWIMMING POOLS

Half Olympic (25m x 10.50m) outdoor swimming pool built into ground, fully tiled; complete with 5m wide deck and associated pool equipment and ozonesystem.

per pool 5,500,000

PLAYGROUND EQUIPMENT

Outdoor playground equipment comprising various activities. per set

250,000 to

650,000

UNIT COSTS FOR ANCILLARY FACILITIESFOR HONG KONG

DESCRIPTION UNIT HK$

SAUNAS

Sauna room for 4-6 people complete with all accessories (enclosing structure not included).

per room 130,000

STEAM BATHS

Steam bath for 4-6 people complete with all accessories (enclosing structure not included).

per room 130,000

GOLF COURSES

(Based on average cost of an 18-hole golf course)

Excluding associated buildings and equipment.

per hole

7,000,000 to

13,000,000

GOLF SIMULATOR

Golf simulation system complete with projector, high impact projection screen, artificial turf, recording system and control computer with software (enclosing structure not included). per set 550,000

1. CONSTRUCTION COST DATA

BU

ILD

ING

TYP

EU

S$/m

2

HONG

KO

NG +

SHA

NGHA

I + B

EIJI

NG +

GUA

NGZH

OU/

SH

ENZH

EN +

CHO

NGQ

ING

+CH

ENG

DU +

DO

MES

TIC

Detac

hed h

ouse

s and

bung

alows

3,8

38

1,096

77

6

622

76

0

780

Terra

ced h

ouse

s

2,863

82

2

528

43

9

480

50

0Av

erag

e stan

dard

apar

tmen

ts, hi

gh ris

e

2,217

65

8

560

52

5

440

47

0Lu

xury

apar

tmen

ts, hi

gh ris

e

2,453

98

7

993

60

5

800

1,0

00

OFF

ICE/

CO

MM

ERC

IAL

Aver

age s

tanda

rd of

fices

, high

rise

2,2

51

987

94

7

760

86

0

940

Pres

tige o

ffices

, high

rise

2,7

33

1,316

1,2

69

1,044

1,1

00

1,250

Shop

ping c

entre

s

2,545

1,2

06

1,090

98

3

900

95

0

HO

TELS

Reso

rt ho

tels

N/

A

1,370

N/

A

N/A

N/

A

N/A

3-sta

r bud

get h

otels,

inclu

sive o

f F.F.

& E

.

2,713

1,0

96

1,116

N/

A

1,050

1,1

005-

star lu

xury

hotel

s, inc

lusive

of F.

F. &

E.

3,436

2,1

93

1,919

1,5

17

1,880

2,1

50

IND

UST

RIA

LLig

ht du

ty fla

tted f

actor

ies

1,184

N/A

N/

A

N/A

N/

A

N/A

Heav

y duty

flatte

d fac

tories

and

wa

reho

uses

1,3

34

N/A

N/

A

N/A

N/

A

N/A

Sing

le sto

rey c

onve

ntion

al fac

tory o

f

struc

tural

steelw

ork

N/

A

548

58

6

520

55

0

550

Owne

r ope

rated

factp

ries,

low ris

e

1,805

73

5

765

64

8

N/A

N/

A

OTH

ERS

Base

ment

carp

arks

(< 3

levels

)

1,900

83

0

780

75

9

700

70

0El

evate

d car

parks

(< 4

levels

)

1,028

39

8

456

35

3

390

39

0Pr

imar

y and

seco

ndar

y sch

ools

1,4

97

598

63

2

415

48

0

500

Stud

ent h

ostel

s

1,663

34

3

335

26

6

330

33

0Sp

orts

clubs

inclu

sive o

f F.F.

& E

.

2,852

1,0

51

970

79

8

900

99

0

Exch

ange

Rate

Use

d : U

S$1 =

HK$7

.8RM

B6.35

RMB6

.35RM

B6.35

RMB6

.35RM

B6.35

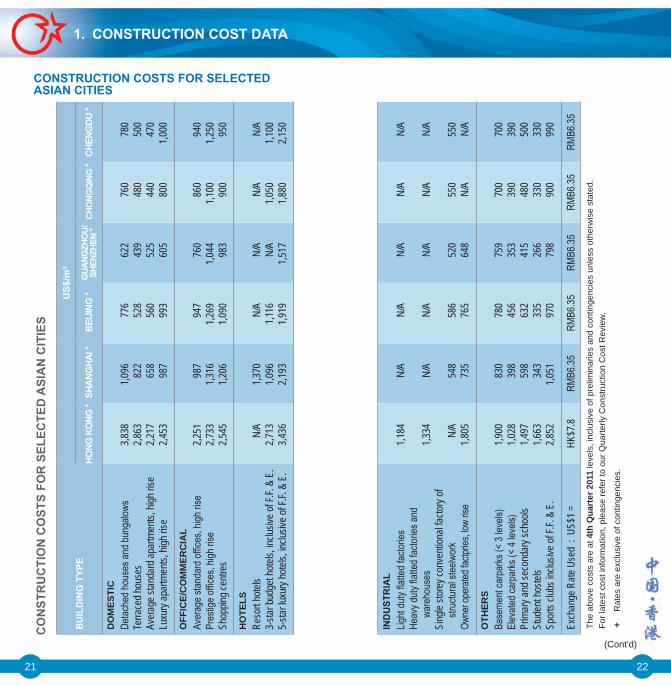

CONSTRUCTION COSTS FOR SELECTEDASIAN CITIES

CO

NST

RU

CTI

ON

CO

STS

FOR

SEL

ECTE

D A

SIA

N C

ITIE

S

The

abov

e co

sts

are

at 4

th Q

uart

er 2

011

leve

ls, i

nclu

sive

of p

relim

inar

ies

and

cont

inge

ncie

s un

less

oth

erw

ise

stat

ed.

For l

ates

t cos

t inf

orm

atio

n, p

leas

e re

fer t

o ou

r Qua

rterly

Con

stru

ctio

n C

ost R

evie

w.

+ R

ates

are

exc

lusi

ve o

f con

tinge

ncie

s.

(Cont'd)

21 22

1. CONSTRUCTION COST DATA

BU

ILD

ING

TYP

EU

S$/m

2

MAC

AU Ђ

SING

APO

RE Φ

KUAL

ALU

MPU

R B

RUNE

I IN

DIA

₲ M

ANIL

A Ω

DO

MES

TIC

Detac

hed h

ouse

s and

bung

alows

3,4

55

2,400

96

2

751

40

9

1,210

Terra

ced h

ouse

s

3,015

2,0

40

317

52

5

300

62

0Av

erag

e stan

dard

apar

tmen

ts, hi

gh ris

e

1,545

1,6

80

463

87

1

347

84

5Lu

xury

apar

tmen

ts, hi

gh ris

e

2,230

2,7

60

1,070

1,0

71

439

1,0

70

OFF

ICE/

CO

MM

ERC

IAL

Aver

age s

tanda

rd of

fices

, high

rise

2,2

00

2,080

75

2

871

40

6

820

Pres

tige o

ffices

, high

rise

2,5

20

2,320

1,1

05

1,192

51

4

1,080

Shop

ping c

entre

s

2,710

2,2

40

917

1,0

97

470

96

0

HO

TELS

Reso

rt ho

tels

N/

A

2,480

1,3

33

1,438

72

3

1,290

3-sta

r bud

get h

otels,

inclu

sive o

f F.F.

& E

.

2,560

2,5

60

1,537

1,5

59

817

1,2

305-

star lu

xury

hotel

s, inc

lusive

of F.

F. &

E.

3,480

3,4

40

2,241

2,1

63

1,588

1,6

00

IND

UST

RIA

LLig

ht du

ty fla

tted f

actor

ies

1,245

1,120

43

8

483

26

3

430

Heav

y duty

flatte

d fac

tories

and

ware

hous

es

N/A

1,3

60

521

N/

A

313

47

5Si

ngle

store

y con

venti

onal

factor

y of

str

uctur

al ste

elwor

k

N/A

96

0

435

44

1

252

41

0Ow

ner o

perat

ed fa

ctprie

s, low

rise

N/

A

N/A

53

0

N/A

31

7

440

OTH

ERS

Base

ment

carp

arks

(< 3

levels

)

1,230

1,3

10

505

N/

A

254

48

0El

evate

d car

parks

(< 4

levels

)

910

76

0

286

49

4

222

46

5 Pr

imar

y and

seco

ndar

y sch

ools

N/

A

1,055

32

7

693

17

8

590

Stud

ent h

ostel

s

N/A

1,1

60

413

79

3

228

69

5Sp

orts

clubs

inclu

sive o

f F.F.

& E

.

N/A

1,7

70

854

N/

A

605

1,2

60

Exch

ange

Rate

Use

d : U

S$1 =

MOP7

.97S$

1.25

RM3.1

5B$

1.26

INR5

0PH

P43

CONSTRUCTION COSTS FOR SELECTEDASIAN CITIES

CO

NST

RU

CTI

ON

CO

STS

FOR

SEL

ECTE

D A

SIA

N C

ITIE

S (C

ont'd

)

₲

Rat

es b

ased

on

proj

ects

in B

anga

lore

and

are

net

t of

VAT

and

Ser

vice

Tax

. Mum

bai c

osts

are

gen

eral

ly 8

% h

ighe

r.Ω

R

ates

are

exc

lusi

ve o

f con

tinge

ncie

s an

d in

clud

e 12

% V

AT.

(Cont'd)

23 24

The

abov

e co

sts

are

at 4

th Q

uart

er 2

011

leve

ls, i

nclu

sive

of p

relim

inar

ies

and

cont

inge

ncie

s un

less

oth

erw

ise

stat

ed.

For l

ates

t cos

t inf

orm

atio

n, p

leas

e re

fer t

o ou

r Qua

rterly

Con

stru

ctio

n C

ost R

evie

w.

Ђ

Rat

es a

re e

xclu

sive

of c

ontin

genc

ies

and

any

man

agem

ent

co

ntra

ct fe

e.

Φ R

ates

are

net

t of G

ST

and

excl

usiv

e of

con

tinge

ncie

s.

1. CONSTRUCTION COST DATA

BU

ILD

ING

TYP

EU

S$/m

2

KAR

ACHI

BAN

GKO

K #

JAK

ARTA

^ H

O C

HI M

INH

# S

EOUL

$TO

KYO

♣

DO

MES

TIC

Detac

hed h

ouse

s and

bung

alows

985

- 1,1

50

967

47

5

500 -

600

1,9

30

2,760

Terra

ced h

ouse

s

250 -

350

58

3

N/A

42

5 - 48

5

1,605

N/

AAv

erag

e stan

dard

apar

tmen

ts, hi

gh ris

e

580 -

775

82

8

595

63

5 - 76

0

1,310

2,2

30Lu

xury

apar

tmen

ts, hi

gh ris

e 8

70 -

1,150

1,1

62

800

81

5 - 94

5

1,630

3,1

00

OFF

ICE/

CO

MM

ERC

IAL

Aver

age s

tanda

rd of

fices

, high

rise

57

5 - 72

5

750

57

5

760 -

880

1,1

70

2,680

Pres

tige o

ffices

, high

rise

950

- 1,1

50

983

86

0

890 -

1,13

0

1,330

3,2

00Sh

oppin

g cen

tres

69

5 - 90

0

800

49

5

695 -

815

1,4

80

2,190

HO

TELS

Reso

rt ho

tels

1,96

5 - 2,

305

2,2

67

1,200

1,19

5 - 1,

500

1,5

35

3,510

3-sta

r bud

get h

otels,

inclu

sive o

f F.F.

& E

. 1

,125 -

1,45

0

1,367

98

0 1

,495 -

1,75

0

1,730

3,4

80

5-sta

r luxu

ry ho

tels,

inclus

ive of

F.F.

& E.

1,80

0 - 2,

100

1,9

33

1,395

1,82

5 - 2,

060

2,3

00

5,100

IND

UST

RIA

LLig

ht du

ty fla

tted f

actor

ies

300 -

375

60

0

N/A

23

8 - 39

0

N/A

1,5

40He

avy d

uty fla

tted f

actor

ies an

d

wa

reho

uses

35

0 - 45

0

N/A

N/

A

395 -

510

N/

A

2,040

Sing

le sto

rey c

onve

ntion

al fac

tory o

f

struc

tural

steelw

ork

43

5 - 45

0

600

26

0

385 -

510

69

0

1,760

Owne

r ope

rated

factp

ries,

low ris

e

325 -

425

N/

A

N/A

39

5 - 49

5

N/A

N/

A

OTH

ERS

Base

ment

carp

arks

(< 3

levels

)

275 -

325

68

3

390

64

0 - 73

0

965

N/

AEl

evate

d car

parks

(< 4

levels

)

200 -

250

35

0

260

34

0 - 45

5

565

1,6

90Pr

imar

y and

seco

ndar

y sch

ools

55

0 - 67

5

N/A

N/

A

475 -

500

1,8

20

2,070

Stud

ent h

ostel

s

410 -

540

N/

A

N/A

50

0 - 63

0

1,080

1,8

90Sp

orts

clubs

inclu

sive o

f F.F.

& E

.

810 -

900

N/

A

N/A

75

5 - 84

0

1,460

2,2

80

Exch

ange

Rate

Use

d : U

S$1 =

PKR8

9.42

BAHT

30ID

R8,91

0VN

D21,0

11KR

W1,1

44JP

Y78.1

4

CONSTRUCTION COSTS FOR SELECTEDASIAN CITIES

CO

NST

RU

CTI

ON

CO

STS

FOR

SEL

ECTE

D A

SIA

N C

ITIE

S (C

ont'd

)

$ R

ates

are

net

t of V

AT a

nd e

xclu

sive

of c

ontin

genc

ies.

♣ R

ates

exc

lude

con

tinge

ncie

s, c

onsu

ltant

fees

and

con

sum

ptio

n ta

x.

25 26

The

abov

e co

sts

are

at 4

th Q

uart

er 2

011

leve

ls, i

nclu

sive

of p

relim

inar

ies

and

cont

inge

ncie

s un

less

oth

erw

ise

stat

ed.

For l

ates

t cos

t inf

orm

atio

n, p

leas

e re

fer t

o ou

r Qua

rterly

Con

stru

ctio

n C

ost R

evie

w.

# R

ates

are

net

t of V

AT a

nd c

ontin

genc

ies.

^ R

ates

are

net

t of V

AT.

1. CONSTRUCTION COST DATA

BU

ILD

ING

TYP

EH

ON

G K

ON

GSH

AN

GH

AI

BEI

JIN

GG

UA

NG

ZHO

U/

SHEN

ZHEN

CH

ON

GQ

ING

CH

ENG

DU

HK

$/m

2R

MB

/m2

RM

B/m

2R

MB

/m2

RM

B/m

2R

MB

/m2

MEC

HA

NIA

L SE

RVI

CES

Offic

es

1,600

- 2,3

50

761 -

96

6

750 -

99

0

650 -

88

0

700 -

90

0

700 -

1,00

0Ind

ustria

l *

380 -

50

0

173 -

28

9

160 -

27

0

135 -

24

0

150 -

25

0

150 -

25

0Ho

tels

1,7

50 -

2,150

97

1 - 1

,265

91

0 - 1

,110

89

0 - 1

,115

75

0 - 1

,000

75

0 - 1

,200

Shop

ping C

entre

s

1,950

- 2,4

00

1,050

- 1,1

03

790 -

95

0

660 -

89

0

600 -

85

0

600 -

1,00

0Ap

artm

ent

65

0 - 1

,300

31

0 -

410

13

0 -

370

10

5 -

325

10

0 -

300

10

0 -

300

ELEC

TRIC

AL

SER

VIC

ESOf

fices

1,3

00 -

1,950

59

3 -

651

46

0 -

670

45

0 -

650

45

0 -

650

45

0 -

700

Indus

trial *

*

450 -

85

0

305 -

43

1

320 -

45

0

260 -

40

0

300 -

40

0

300 -

40

0Ho

tels

1,5

00 -

2,150

65

1 -

830

70

5 -

898

56

5 -

765

55

0 -

700

55

0 -

800

Shop

ping C

entre

s

1,400

- 1,9

50

520 -

65

1

481 -

66

3

450 -

61

0

450 -

60

0

450 -

70

0Ap

artm

ent

85

0 - 1

,300

25

2 -

368

25

3 -

386

24

0 -

380

25

0 -

350

25

0 -

350

HYD

RA

ULI

C S

ERVI

CES

Offic

es

270 -

38

0

110 -

16

3

95 -

140

10

5 -

140

70

- 13

0

70 -

130

Indus

trial

22

0 -

330

89

- 13

1

95 -

140

75

- 10

2

70 -

120

70

- 12

0

Hot

els

80

0 - 1

,050

36

8 -

488

36

0 -

470

32

5 -

410

30

0 -

400

30

0 -

400

Shop

ping C

entre

s

270 -

38

0

137 -

18

4

140 -

20

0

105 -

14

0

70 -

130

70

- 13

0Ap

artm

ent

55

0 -

850

16

8 -

226

16

5 -

225

12

5 -

220

12

0 -

200

12

0 -

200

FIR

E SE

RVI

CES

Offic

es

430 -

55

0

226 -

32

0

180 -

26

5

190 -

29

5

180 -

25

0

180 -

25

0Ind

ustria

l

250 -

30

0

168 -

27

8

140 -

21

5

125 -

24

0

150 -

25

0

150 -

25

0Ho

tels

43

0 -

550

28

9 -

399

21

5 -

370

23

0 -

345

20

0 -

330

20

0 -

330

Shop

ping C

entre

s

430 -

55

0

268 -

38

3

215 -

37

0

230 -

34

5

220 -

33

0

220 -

33

0Ap

artme

nt

75 -

120

47

- 11

6

60 -

125

55

- 10

5

50 -

100

50

- 10

0LI

FTS

/ ESC

ALA

TOR

SOf

fices

55

0 -

900

27

5 -

540

29

4 -

577

25

0 -

410

35

0 -

550

35

0 -

600

Indus

trial

45

0 -

600

13

0 -

380

14

5 -

400

13

5 -

390

15

0 -

350

15

0 -

350

Hotel

s

450 -

65

0

215 -

48

5

232 -

52

0

200 -

39

0

300 -

45

0

300 -

50

0Sh

oppin

g Cen

tres

65

0 -

850

32

0 -

485

32

7 -

520

30

5 -

430

30

0 -

400

30

0 -

450

Apar

tmen

t

330 -

65

0

160 -

32

0

175 -

28

9

105 -

23

0

140 -

25

0

140 -

25

0

M&

E C

OST

S FO

R S

ELEC

TED

ASI

AN

CIT

IES

M&E COSTS FOR SELECTED ASIAN CITIES

The

abov

e co

sts

are

at 4

th Q

uart

er 2

011

leve

ls, e

xclu

sive

of c

ontin

genc

ies

unle

ss o

ther

wis

e st

ated

.

* G

ener

ally

with

out A

/C.

**

Exc

lude

s sp

ecia

l pow

er s

uppl

y.

(Cont'd)

27 28

1. CONSTRUCTION COST DATA

BU

ILD

ING

TYP

EM

AC

AU

SIN

GA

POR

E Φ

KU

ALA

LUM

PUR

BR

UN

EI IN

DIA

₲ M

AN

ILA

Ω

MO

P/m

2S$

/m2

RM

/m2

B$/

m2

INR

/m2

PHP/

m2

MEC

HA

NIA

L SE

RVI

CES

Offic

es

N/A

15

3 - 2

28

350

- 455

13

3 - 1

66

3,600

- 4,7

00

3,000

- 4,3

00Ind

ustria

l *

N/A

29

- 13

6

60 -

90

17 -

29

1,600

- 2,8

00

650 -

1,30

0Ho

tels

1,8

50 -

2,150

15

0 - 2

89

280

- 450

21

4 - 2

47

4,500

- 4,8

50

3,000

- 6,0

00Sh

oppin

g Cen

tres

1,6

00 -

2,150

15

8 - 2

14

280

- 410

15

2 - 1

81

3,500

- 4,5

00

2,500

- 3,7

00Ap

artm

ent

55

0 -

650

95

- 19

2

200

- 283

15

7 - 1

81

2,000

- 2,5

00

1,900

- 3,0

00EL

ECTR

ICA

L SE

RVI

CES

Offic

es

N/A

20

3 - 3

06

220

- 465

17

1 - 2

14

2,800

- 4,0

00

3,300

- 6,0

00Ind

ustria

l **

N/

A

58 -

148

14

0 - 1

57

143

- 171

1,8

00 -

3,100

2,0

00 -

3,500

Hotel

s

1,900

- 2,3

00

202

- 340

24

0 - 5

90

214

- 280

3,2

00 -

4,900

4,4

00 -

8,400

Shop

ping C

entre

s

1,900

- 2,1

00

170

- 275

20

0 - 2

60

162

- 233

3,0

00 -

4,000

3,6

00 -

5,400

Apar

tmen

t

650 -

85

0

109

- 252

85

- 21

0

185

- 233

1,2

00 -

1,600

3,2

00 -

4,800

HYD

RA

ULI

C S

ERVI

CES

Offic

es

N/A

31

- 71

23

- 52

12

- 29

57

5 -

850

90

0 - 2

,000

Indus

trial

N/

A

19 -

39

36 -

45

8 -

14

375 -

65

0

700 -

1,20

0

Hot

els

85

0 - 1

,050

97

- 13

6

173

- 235

45

- 62

3,0

00 -

4,500

1,7

50 -

3,800

Shop

ping C

entre

s

300 -

40

0

49 -

75

23 -

30

9 -

30

825 -

1,50

0

650 -

1,10

0Ap

artm

ent

55

0 -

750

75

- 15

9

18 -

45

28 -

44

1,300

- 1,8

00

1,300

- 2,6

00FI

RE

SER

VIC

ESOf

fices

N/

A

32 -

64

57 -

80

24 -

29

900 -

1,20

0

600 -

1,20

0Ind

ustria

l

N/A

24

- 54

45

- 60

9

- 14

40

0 -

550

60

0 -

900

Hotel

s

500 -

60

0

49 -

78

65 -

90

19 -

36

1,000

- 1,3

00

600 -

1,10

0Sh

oppin

g Cen

tres

40

0 -

500

38

- 63

60

- 80

24

- 48

85

0 -

950

60

0 -

900

Apart

ment

10

0 -

150

19

- 53

20

- 25

19

- 38

45

0 -

550

60

0 - 1

,300

LIFT

S / E

SCA

LATO

RS

Offic

es

N/A

62

- 17

7

88 -

400

7

- 24

65

0 -

900

1,6

00 -

2,900

Indus

trial

N/

A

46 -

114

54

- 19

0

3 -

14

400 -

55

0

N/A

Hotel

s

500 -

70

0

76 -

138

85

- 37

0

9 -

33

800 -

1,00

0

1,500

- 3,0

00Sh

oppin

g Cen

tres

40

0 -

600

83

- 20

0

85 -

110

9

- 27

80

0 - 1

,100

70

0 - 1

,700

Apar

tmen

t

400 -

50

0

27 -

123

63

- 10

5

8 -

19

500 -

70

0

800 -

1,50

0

M&

E C

OST

S FO

R S

ELEC

TED

ASI

AN

CIT

IES

(Con

t'd)

M&E COSTS FOR SELECTED ASIAN CITIES

₲

Rat

es a

re b

ased

on

proj

ects

in B

anga

lore

and

are

net

t of V

AT a

nd S

ervi

ce

Tax.

Mum

bai c

osts

are

gen

eral

ly 8

% h

ighe

r.Ω

Tr

ansf

orm

er, i

nclu

ded

in E

lect

rical

Ser

vice

s.

* G

ener

ally

with

out A

/C.

**

Exc

lude

s sp

ecia

l pow

er s

uppl

y.Φ

Rat

es a

re n

ett o

f GS

T.

(Cont'd)

29 30

The

abov

e co

sts

are

at 4

th Q

uart

er 2

011

leve

ls, e

xclu

sive

of c

ontin

genc

ies

unle

ss o

ther

wis

e st

ated

.

1. CONSTRUCTION COST DATA

BU

ILD

ING

TYP

EK

AR

AC

HI

BA

NG

KO

K ⱷ

JA

KA

RTA

#H

O C

HI M

INH

SEO

UL

$ T

OK

YO ♣

PKR

/m2

BH

T/m

2ID

R'0

00/m

2VN

D'0

00/m

2K

RW

'000

/m2

JPY/

m2

MEC

HA

NIA

L SE

RVI

CES

Offic

es

3,750

- 8,5

00

3,900

- 4,8

00

625

- 735

1,5

90 -

2,267

20

0 - 2

80

21,00

0Ind

ustria

l *

1,085

- 1,8

90

1,250

- 1,4

00

195

- 455

N/

A

87 -

150

11

,200

Hotel

s

7,600

- 9,9

50

4,500

- 5,1

00

625

- 840

N/

A

205

- 330

14

,800

Shop

ping C

entre

s

7,600

- 9,9

50

4,400

- 4,8

00

570

- 680

N/

A

144

- 240

7,1

00Ap

artm

ent

2,6

00 -

3,500

4,4

00 -

4,500

57

0 - 7

30

1,198

- 1,7

29

92 -

169

3,0

00EL

ECTR

ICA

L SE

RVI

CES

Offic

es

4,425

- 5,4

13

2,250

- 2,5

00

510

- 680

1,9

62 -

2,337

25

0 - 3

65

19,60

0Ind

ustria

l **

2,4

31 -

3,392

1,6

50 -

1,700

28

0 - 4

50

N/A

11

5 - 1

50

10,40

0Ho

tels

5,8

50 -

9,925

2,7

50 -

3,200

51

0 - 7

30

N/A

35

0 - 4

60

18,80

0Sh

oppin

g Cen

tres

4,7

15 -

7,825

2,1

50 -

2,400

45

0 - 5

70

N/A

20

0 - 2

30

7,600

Apar

tmen

t

2,000

- 3,2

70

2,390

- 2,9

50

510

- 680

1,7

40 -

2,197

13

0 - 1

65

12,20

0H

YDR

AU

LIC

SER

VIC

ESOf

fices

76

5 - 1

,205

75

0 -

890

12

0 - 1

90

263 -

502

32

- 55

12

,600

Indus

trial

63

0 -

835

70

0 -

780

71

- 13

0

N/A

20

- 30

5,7

00

Hot

els

3,2

00 -

4,845

1,3

50 -

1,490

51

0 - 7

40

N/A

57

- 89

16

,600

Shop

ping C

entre

s

465 -

1,24

0

780 -

95

0

120

- 190

N/

A

27 -

56

5,400

Apar

tmen

t

1,360

- 1,9

70

1,150

- 1,3

50

510

- 730

51

4 - 1,

171

49

- 65

18

,300

FIR

E SE

RVI

CES

Inc

luded

in

abov

e

Offic

es

1,285

- 1,6

75

760 -

85

0

160

- 250

61

4 - 1,

019

40

- 65

Indus

trial

1,1

25 -

2,025

72

0 -

750

70

- 13

0

N/A

27

- 30

Hotel

s

1,285

- 2,6

50

750 -

85

0

150

- 250

N/

A

56 -

87Sh

oppin

g Cen

tres

1,1

25 -

2,025

76

0 -

790

16

0 - 2

10

N/A

42

- 69

Apart

ment

85

0 - 1

,350

76

0 -

850

16

0 - 2

10

420 -

528

32

- 65

LIFT

S / E

SCA

LATO

RS

Offic

es

1,745

- 3,1

00

1,000

- 1,0

50

270

- 740

56

3 - 1,

079

45

- 60

5,6

00Ind

ustria

l

1,745

- 3,1

00

N/A

N/

A

N/A

16

- 25

2,5

00Ho

tels

3,5

00 -

8,100

1,0

00 -

1,100

27

0 - 6

80

N/A

11

0 - 1

55

5,100

Shop

ping C

entre

s

1,745

- 3,1

00

210 -

49

0

205

- 540

1,1

61 -

1,642

55

- 78

3,6

00Ap

artm

ent

1,7

45 -

3,100

45

0 -

500

26

0 - 5

40

633 -

920

27

- 38

2,7

00

M&

E C

OST

S FO

R S

ELEC

TED

ASI

AN

CIT

IES

(Con

t'd)

(Cont'd)

M&E COSTS FOR SELECTED ASIAN CITIES

# Al

l rat

es a

re n

ett o

f VAT

. R

ates

for E

lect

rical

Ser

vice

s ar

e ex

clud

ing

gens

et.

Rat

es

for H

ydra

ulic

Ser

vice

s ar

e ex

clud

ing

STP.

Rat

es fo

r Mec

hani

cal S

ervi

ces

refe

r to

ACM

V R

ates

onl

y.♣

All c

osts

are

ave

rage

. Spr

inkl

er s

yste

m, fi

re h

ose

reel

are

incl

uded

in H

ydra

ulic

Se

rvic

es. S

mok

e sp

ill ex

haus

t sys

tem

is in

clud

ed in

Mec

hani

cal S

ervi

ces.

Fire

al

arm

sys

tem

, em

erge

ncy

PA s

yste

m a

re in

clud

ed in

Ele

ctric

al S

ervi

ces.

* G

ener

ally

with

out A

/C.

**

Exc

lude

s sp

ecia

l pow

er s

uppl

y.ⱷ

Ba

sed

upon

net

t enc

lose

d ar

ea a

nd n

ett o

f VAT

.$

Rat

es a

re n

ett o

f VAT

.

The

abov

e co

sts

are

at 4

th Q

uart

er 2

011

leve

ls,

excl

usiv

e of

con

tinge

ncie

s un

less

oth

erw

ise

stat

ed.

31 32

1. CONSTRUCTION COST DATA

DES

CR

IPTI

ON

UNIT

HONG

KO

NGSH

ANG

HAI

BEIJ

ING

GUA

NGZH

OU/

SH

ENZH

ENCH

ONG

QIN

GCH

ENG

DU

HK

$R

MB

RM

BR

MB

RM

BR

MB

1. Ex

cava

ting b

asem

ents

≤ 2.0

0m de

epm3

11

5

30

15

25

16

202.

Exca

vatin

g for

footin

gs ≤

1.50

m de

epm3

11

0

25

18

30

18

253.

Remo

ve ex

cava

ted m

ateria

ls off

site

m3

190 *

10

5

25

68

43

354.

Hardc

ore be

d blin

ded w

ith fin

e mate

rials

m3

650

16

8

120

15

5

120

13

05.

Mass

conc

rete g

rade 1

5m3

90

0

400

50

0

380

38

0

380

6. Re

inforc

ed co

ncret

e grad

e 30

m3

1,130

47

0

560

46

5

420

42

07.

Mild

steel

rod re

inforc

emen

tkg

9.8

6

6.3

6.2

6.3

6.3

8. Hi

gh te

nsile

rod r

einfor

ceme

ntkg

9.8

6

6.3

6.2

6.3

6.3

9. Sa

wn fo

rmwo

rk to

soffit

s of s

uspe

nded

slabs

m2

180

55

65

45

55

55

10. S

awn f

ormwo

rk to

colum

ns an

d wall

sm2

18

0

55

55

45

55

5511

. 112

.5mm

thick

brick

wall

sm2

19

0

60 @

90

58

47

50

12. "

Kliplo

k Colo

rbond

" 0.64

mm pr

ofiled

ste

el sh

eetin

gm2

60

0

N/A

N/

A

N/A

N/

A

N/A

13. A

lumini

um ca

seme

nt wi

ndow

s, sin

gle

glaze

dm2

1,7

00

600

78

0 **

55

0

750 *

*

750 *

*14

. Stru

ctural

stee

lwork

- bea

ms, s

tanch

ions

and t

he lik

ekg

25

12

11

14

12

12

15. S

teelw

ork - a

ngles

, cha

nnels

, flats

and

the

like

kg

27

10

11

11

10

1016

. 25m

m ce

ment

and s

and (

1:3) p

aving

m2

80

35

20

21

22

2517

. 20m

m ce

ment

and s

and (

1:4) p

laster

to

walls

m2

95

28

22

18

17

2018

. Cera

mic t

iles b

edde

d to fl

oor s

creed

(m

/s)m2

27

0

160

12

0

115

12

0

120

19. 1

2mm

fibrou

s plas

terbo

ard ce

iling l

ining

m2

430

17

0

140

15

7

130

13

020

. Two

coats

of em

ulsion

paint

to pl

aster

ed

surfa

ces

m2

44

32

30

26

30

30Av

erage

expe

cted p

relim

inarie

s%

10

- 15

3 -

8

5 - 10

5 -

10

5 - 10

5 -

10

MA

JOR

RAT

ES F

OR

SEL

ECTE

D A

SIA

N C

ITIE

S

MAJOR RATES FOR SELECTED ASIAN CITIES

(Cont'd)

The

abov

e co

sts

are

at 4

th Q

uart

er 2

011

leve

ls a

nd a

re b

ased

on

lum

p su

m fi

xed

pric

e co

ntra

ct r

ates

exc

lusi

ve o

f pr

elim

inar

ies

and

cont

inge

ncie

s un

less

oth

erw

ise

stat

ed.

**

Rat

es fo

r dou

ble

glaz

ed w

indo

w.

* R

ate

incl

udin

g w

aste

cha

rges

impl

emen

ted

on 1

Dec

. 200

5.@

R

ates

for 1

20m

m th

ick

conc

rete

blo

ck w

alls

.

33 34

1. CONSTRUCTION COST DATA

DES

CR

IPTI

ON

UNIT

MAC

AUSI

NGAP

ORE

ΦKU

ALA

LUM

PUR

BRUN

EIIN

DIA

₲M

ANIL

A

MO

PS$

RM

B$

INR

PHP

1. Ex

cava

ting b

asem

ents

≤ 2.0

0m de

epm3

11

0

16.5

15

- 20

3.5

13

0

350

2. Ex

cava

ting f

or foo

tings

≤ 1.

50m

deep

m3

105

16

.5

15 -

20

3

145

25

03.

Remo

ve ex

cava

ted m

ateria

ls off

site

m3

60

15

20 -

25

3

100

20

04.

Hardc

ore be

d blin

ded w

ith fin

e mate

rials

m3

580

50

60

- 70

37

3,0

60

2,500

5. Ma

ss co

ncret

e grad

e 15

m3

680

20

2 Φ Φ

23

0 - 25

0

117

4,2

00

3,500

6. Re

inforc

ed co

ncret

e grad

e 30

m3

730

15

5 - 17

0

250 -

280

13

2

5,125

4,8

007.

Mild

steel

rod re

inforc

emen

tkg

9.5

1.6

- 1.7

5

3.5 -

3.8

0.98

40

47

8. Hi

gh te

nsile

rod r

einfor

ceme

ntkg

9.5

1.6

- 1.7

5

3.5 -

3.8

0.98

42

48

9. Sa

wn fo

rmwo

rk to

soffit

s of s

uspe

nded

slabs

m2

160

30

- 33

30

- 38

14

.5

425

85

010

. Saw

n form

work

to co

lumns

and w

alls

m2

160

30

- 33

30

- 38

14

45

0

800

11. 1

12.5m

m thi

ck br

ick w

alls

m2

250

30

- 35

32

- 45

18

.5

700

N/

A12

. "Kli

plok C

olorbo

nd" 0

.64mm

profi

led

steel

shee

ting

m2

N/A

43

55

- 60

56

96

0

900

13. A

lumini

um ca

seme

nt wi

ndow

s, sin

gle

glaze

dm2

2,0

00

290

35

0 - 50

0

166 -

216

3,7

00

9,000

Ω

14. S

tructu

ral st

eelw

ork - b

eams

, stan

chion

s

an

d the

like

kg

35

4.8- 5

.8

6 - 7.

5

3

75

100

15. S

teelw

ork - a

ngles

, cha

nnels

, flats

and

the

like

kg

32

4.8 -

5.8

6 - 7.

5

2.7

75

9516

. 25m

m ce

ment

and s

and (

1:3) p

aving

m2

80

11

15 -

22

7.5

300

35

017

. 20m

m ce

ment

and s

and (

1:4) p

laster

to

walls

m2

95

15.5

15

- 22

8

23

0

350

18. C

erami

c tile

s bed

ded t

o floo

r scre

ed

(m/s)

m2

400

65

.5

50 -

70

23

1,100

1,2

0019

. 12m

m fib

rous p

laster

board

ceilin

g lini

ngm2

46

0

30

30 -

45

28

850

1,3

0020

. Two

coats

of em

ulsion

paint

to pl

aster

ed

surfa

ces

m2

80

3.5 -

4

3.5 -

4

5

130

35

0Av

erage

expe

cted p

relim

inarie

s%

8 -

15

12 -

15

6 - 12

5 -

8

5 - 10

8 -

15

MA

JOR

RAT

ES F

OR

SEL

ECTE

D A

SIA

N C

ITIE

S (C

ont'd

)

MAJOR RATES FOR SELECTED ASIAN CITIES

(Cont'd)

The

abov

e co

sts

are

at 4

th Q

uart

er 2

011

leve

ls a

nd a

re b

ased

on

lum

p su

m fi

xed

pric

e co

ntra

ct r

ates

exc

lusi

ve o

f pr

elim

inar

ies

and

cont

inge

ncie

s un

less

oth

erw

ise

stat

ed.

₲

Rat

es a

re b

ased

on

proj

ects

in B

anga

lore

and

are

net

t of

VAT

and

Serv

ice

tax.

Mum

bai c

osts

are

gen

eral

ly 8

% h

ighe

r.Ω

R

ate

for a

lum

iniu

m w

ith a

nodi

zed

finis

h; 6

mm

thic

k.

Φ R

ates

are

net

t of G

ST.

Φ Φ

Rat

e fo

r lea

n co

ncre

te b

lindi

ng.

35 36

1. CONSTRUCTION COST DATA

DES

CR

IPTI

ON

UNIT

KARA

CHI

BA

NG

KO

K #

JAK

AR

TA #

HO

CH

I

MIN

H #

SEO

UL

$TO

KYO

PKR

BH

TID

R'0

00VN

D'0

00K

RW

JPY

1. Ex

cava

ting b

asem

ents

≤ 2.0

0m de

epm3

38

5 - 63

5

100

23

69

2,1

00

890

2. Ex

cava

ting f

or foo

tings

≤ 1.

50m

deep

m3

320 -

495

10

0

30

64

2,100

94

03.

Remo

ve ex

cava

ted m

ateria

ls off

site

m3

180 -

280

10

0

25

66

12,00

0

3,140

4. Ha

rdcore

bed b

linde

d with

fine m

ateria

lsm3

1,17

0 - 1,

413

60

0

270

30

6

26,50

0

8,100

5. Ma

ss co

ncret

e grad

e 15

m3 5,

000 -

5,50

0

2,000

71

0

1,352

57

,000

11

,200

6. Re

inforc