domestic payments gateway to financial inclusion? · domestic payments—gateway to financial...

TRANSCRIPT

Domestic Payments—Gateway to

Financial Inclusion?

Rodger Voorhies, Director

Financial Services for the Poor

Survey Data from 11 African Countries

March 1, 2013

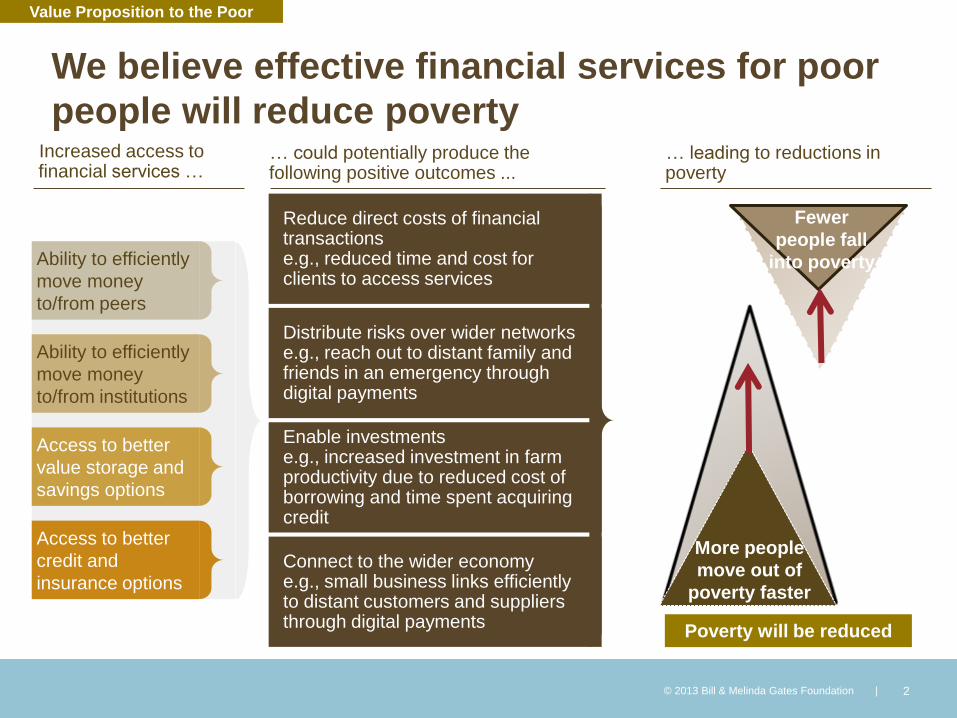

We believe effective financial services for poor

people will reduce poverty

© 2013 Bill & Melinda Gates Foundation | 2

Poverty will be reduced

More people

move out of

poverty faster

Fewer

people fall

into poverty

… leading to reductions in poverty

Increased access to financial services …

… could potentially produce the following positive outcomes ...

Distribute risks over wider networks e.g., reach out to distant family and friends in an emergency through digital payments

Enable investments e.g., increased investment in farm productivity due to reduced cost of borrowing and time spent acquiring credit

Reduce direct costs of financial transactions e.g., reduced time and cost for clients to access services

Connect to the wider economy e.g., small business links efficiently to distant customers and suppliers through digital payments

Ability to efficiently

move money

to/from peers

Ability to efficiently

move money

to/from institutions

Access to better

value storage and

savings options

Access to better

credit and

insurance options

Value Proposition to the Poor

© 2013 Bill & Melinda Gates Foundation | 3

Customer Activation

Distribution Payments Front-End

Payments Back-End

Integration Products Analytics

© 2013 Bill & Melinda Gates Foundation | 3

What If: We could turn a 30 day sign up process into 30 seconds?

What If: Everyone was an agent?

What If: Anyone with a phone could send or receive money?

What If: Payment processing was digital and close to zero in cost?

What If: You could send money to any person in the world?

What If: Every mobile phone came with a savings account and insurance?

What If: Assessing risk for a billion new customers was cost-effective?

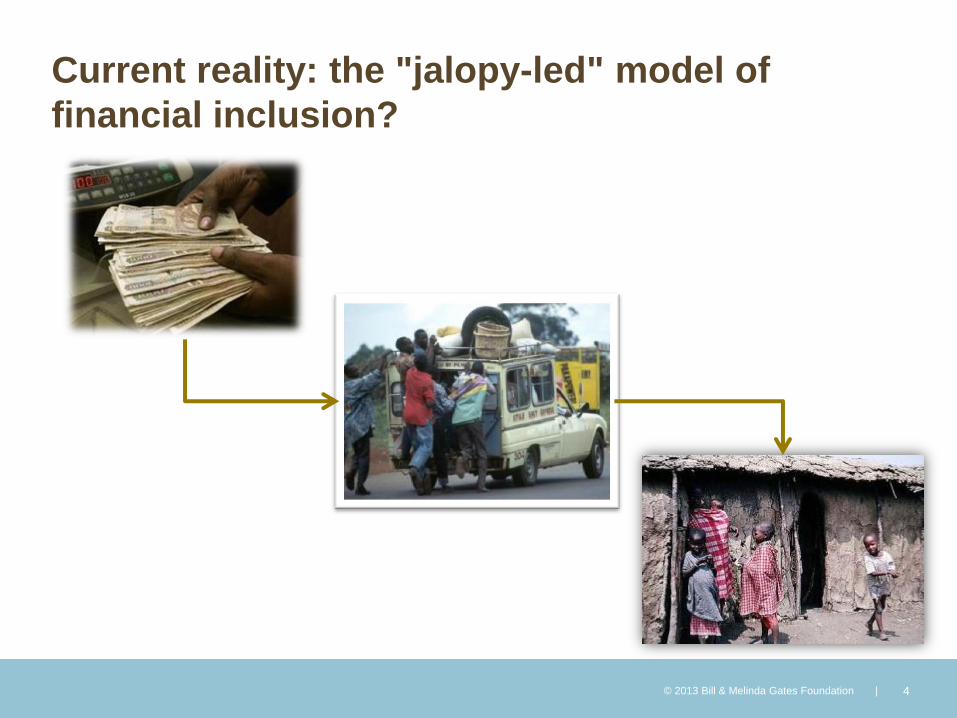

Current reality: the "jalopy-led" model of

financial inclusion?

© 2013 Bill & Melinda Gates Foundation | 4

© 2013 Bill & Melinda Gates Foundation | 5

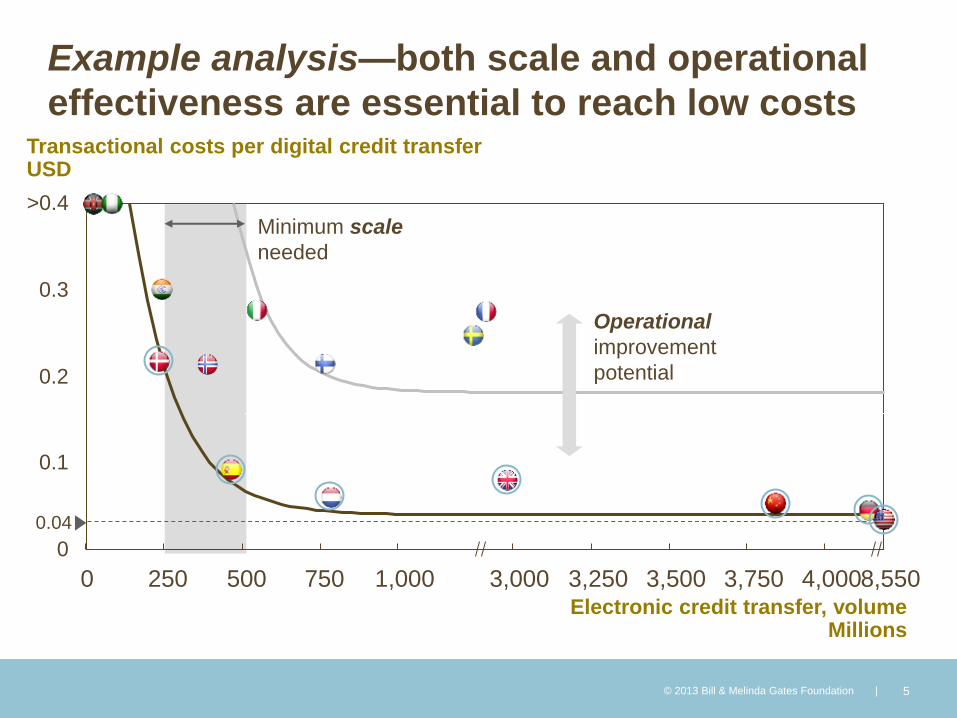

>0.4

0.3

0.2

3,250 3,000 1,000 750 500 250 0 3,750 4,000 8,550 Electronic credit transfer, volume

Millions

0

0.1

3,500

Transactional costs per digital credit transfer USD

Example analysis—both scale and operational

effectiveness are essential to reach low costs

Minimum scale

needed

0.04

Operational

improvement

potential

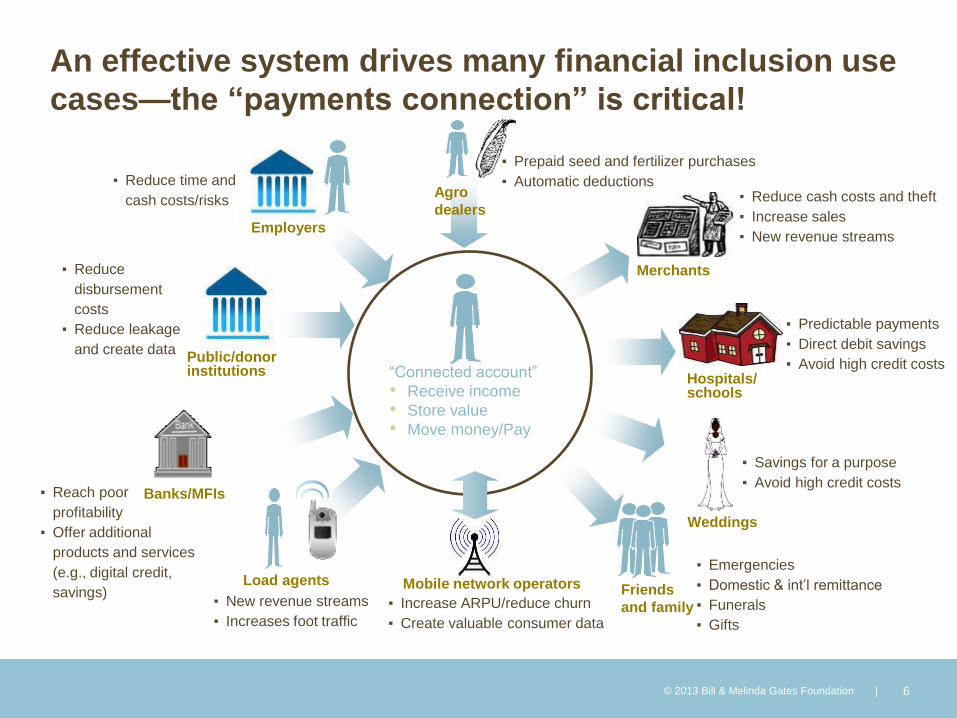

An effective system drives many financial inclusion use

cases—the “payments connection” is critical!

© 2013 Bill & Melinda Gates Foundation | 6

Public/donor institutions

Employers

Load agents Mobile network operators

Hospitals/ schools

Weddings

Agro

dealers

Merchants

Banks/MFIs

“Connected account”

• Receive income

• Store value

• Move money/Pay

▪ Emergencies

▪ Domestic & int’l remittance

▪ Funerals

▪ Gifts

▪ Savings for a purpose

▪ Avoid high credit costs

▪ Predictable payments

▪ Direct debit savings

▪ Avoid high credit costs

▪ Reduce cash costs and theft

▪ Increase sales

▪ New revenue streams

▪ Prepaid seed and fertilizer purchases

▪ Automatic deductions ▪ Reduce time and

cash costs/risks

▪ Reduce

disbursement

costs

▪ Reduce leakage

and create data

▪ Increase ARPU/reduce churn

▪ Create valuable consumer data

▪ New revenue streams

▪ Increases foot traffic

▪ Reach poor

profitability

▪ Offer additional

products and services

(e.g., digital credit,

savings) Friends

and family

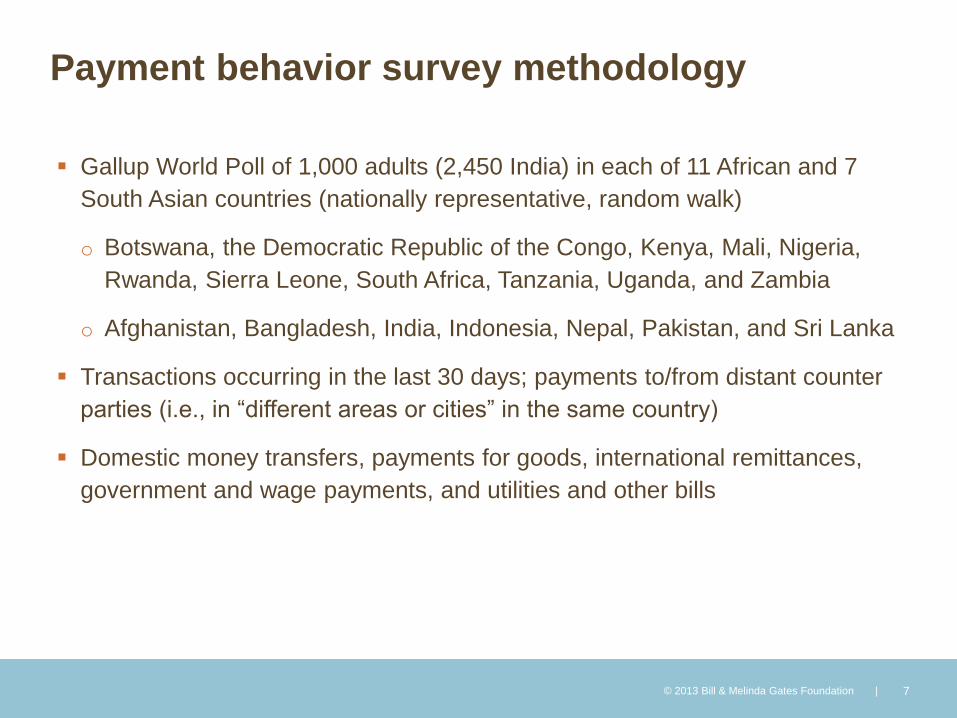

Payment behavior survey methodology

Gallup World Poll of 1,000 adults (2,450 India) in each of 11 African and 7

South Asian countries (nationally representative, random walk)

o Botswana, the Democratic Republic of the Congo, Kenya, Mali, Nigeria,

Rwanda, Sierra Leone, South Africa, Tanzania, Uganda, and Zambia

o Afghanistan, Bangladesh, India, Indonesia, Nepal, Pakistan, and Sri Lanka

Transactions occurring in the last 30 days; payments to/from distant counter

parties (i.e., in “different areas or cities” in the same country)

Domestic money transfers, payments for goods, international remittances,

government and wage payments, and utilities and other bills

© 2013 Bill & Melinda Gates Foundation | 7

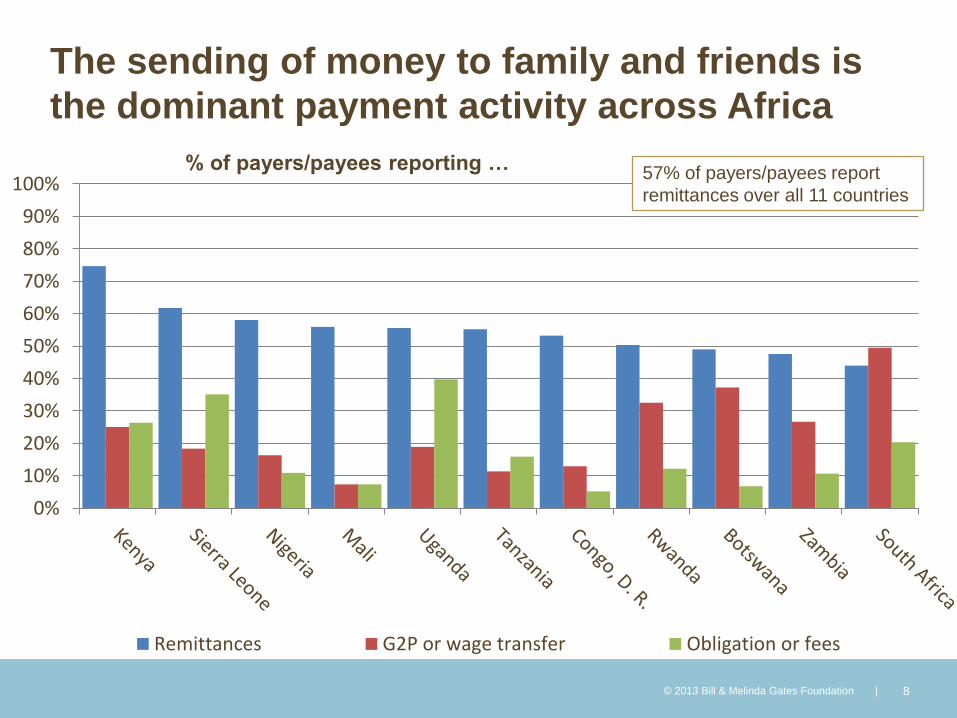

The sending of money to family and friends is

the dominant payment activity across Africa

© 2013 Bill & Melinda Gates Foundation | 8

% of payers/payees reporting …

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Remittances G2P or wage transfer Obligation or fees

57% of payers/payees report

remittances over all 11 countries

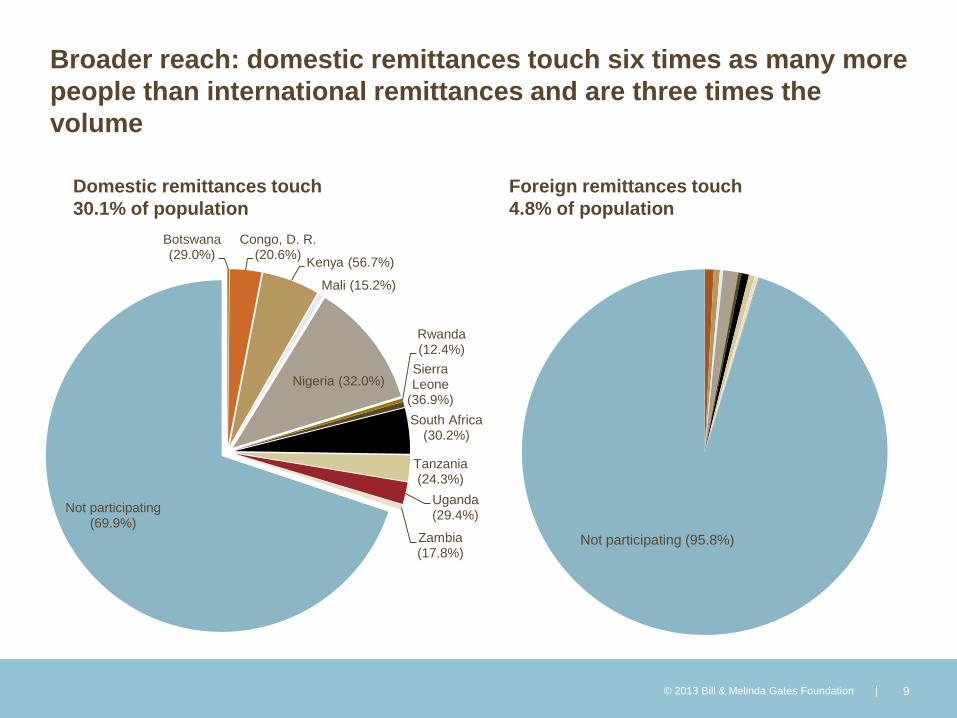

Broader reach: domestic remittances touch six times as many more

people than international remittances and are three times the

volume

© 2013 Bill & Melinda Gates Foundation | 9

Botswana (29.0%)

Congo, D. R. (20.6%)

Kenya (56.7%)

Mali (15.2%)

Nigeria (32.0%)

Rwanda (12.4%)

Sierra Leone

(36.9%)

South Africa (30.2%)

Tanzania (24.3%)

Uganda (29.4%)

Zambia (17.8%)

Not participating (69.9%)

Not participating (95.8%)

Domestic remittances touch

30.1% of population

Foreign remittances touch

4.8% of population

© 2013 Bill & Melinda Gates Foundation | 10

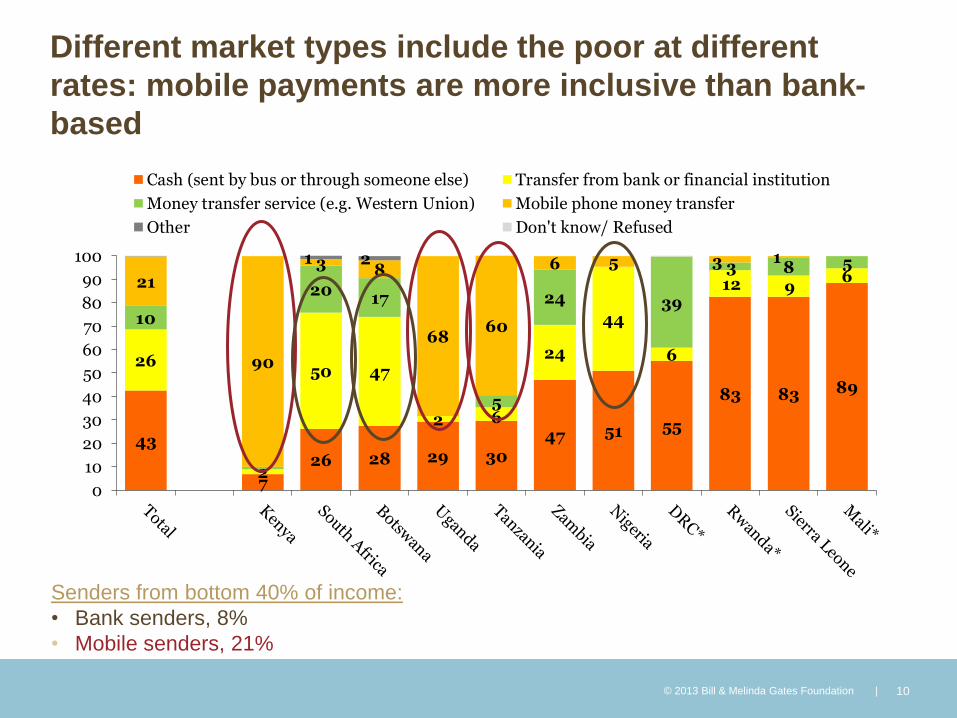

Channels Used To Send Money

How did you send this money?% by country

Total = population-weighted average* Less than 10% of respondents in these countries were asked this question

43

7

26 28 29 30

47 51 55

83 83 89

26

2

50 47

2 6

24

44

6

12 96

10

2017

5

24 39

3 8 521

90

3 8

6860

6 5 3 11 2

0

10

20

30

40

50

60

70

80

90

100

Cash (sent by bus or through someone else) Transfer from bank or financial institution

Money transfer service (e.g. Western Union) Mobile phone money transfer

Other Don't know/ Refused

Senders from bottom 40% of income:

• Bank senders, 8%

• Mobile senders, 21%

Different market types include the poor at different

rates: mobile payments are more inclusive than bank-

based

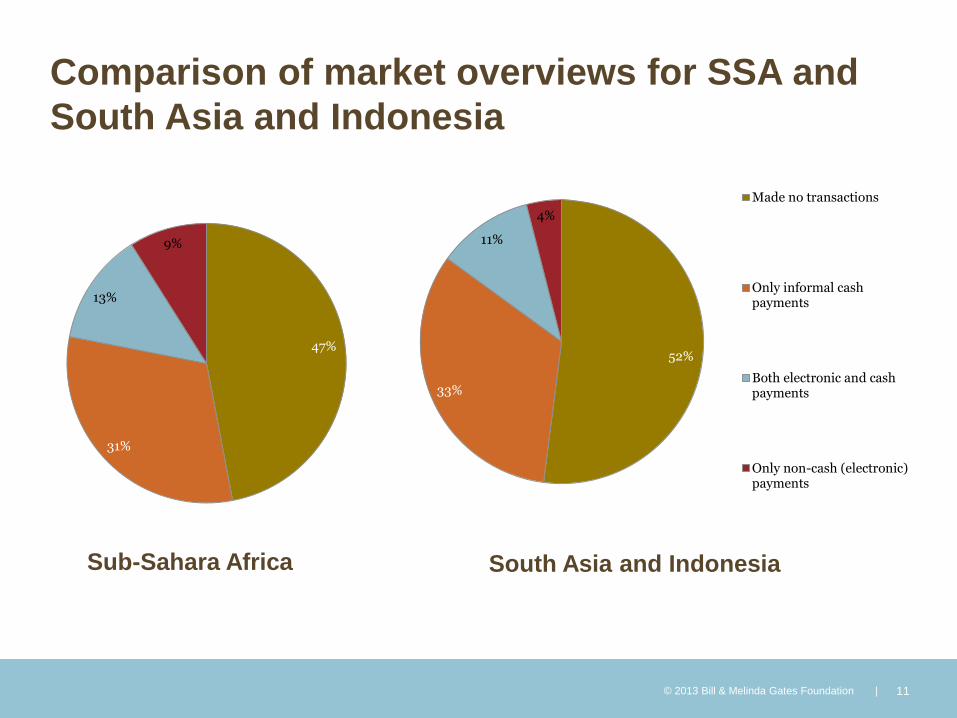

Comparison of market overviews for SSA and

South Asia and Indonesia

© 2013 Bill & Melinda Gates Foundation | 11

47%

31%

13%

9%

Sub-Sahara Africa

52%

33%

11%

4%

Made no transactions

Only informal cashpayments

Both electronic and cashpayments

Only non-cash (electronic)payments

South Asia and Indonesia

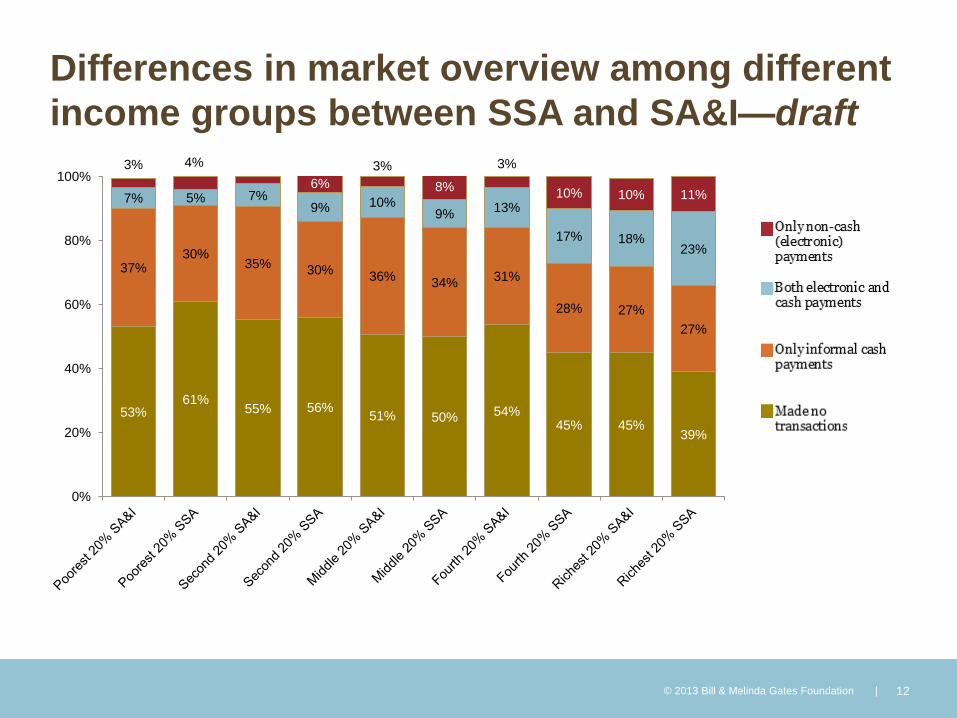

Differences in market overview among different

income groups between SSA and SA&I—draft

© 2013 Bill & Melinda Gates Foundation | 12

53% 61%

55% 56% 51% 50% 54%

45% 45% 39%

37% 30%

35% 30%

36% 34%

31%

28% 27%

27%

7% 5% 7% 9% 10%

9% 13%

17% 18% 23%

3% 4%

6%

3%

8%

3%

10% 10% 11%

0%

20%

40%

60%

80%

100%

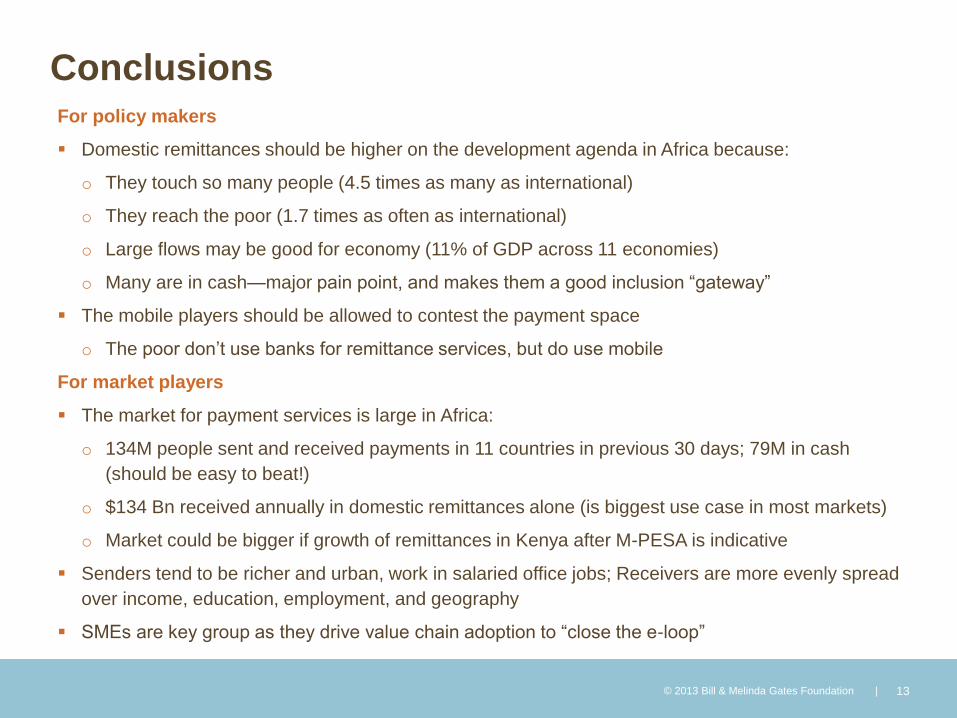

Conclusions For policy makers

Domestic remittances should be higher on the development agenda in Africa because:

o They touch so many people (4.5 times as many as international)

o They reach the poor (1.7 times as often as international)

o Large flows may be good for economy (11% of GDP across 11 economies)

o Many are in cash—major pain point, and makes them a good inclusion “gateway”

The mobile players should be allowed to contest the payment space

o The poor don’t use banks for remittance services, but do use mobile

For market players

The market for payment services is large in Africa:

o 134M people sent and received payments in 11 countries in previous 30 days; 79M in cash

(should be easy to beat!)

o $134 Bn received annually in domestic remittances alone (is biggest use case in most markets)

o Market could be bigger if growth of remittances in Kenya after M-PESA is indicative

Senders tend to be richer and urban, work in salaried office jobs; Receivers are more evenly spread

over income, education, employment, and geography

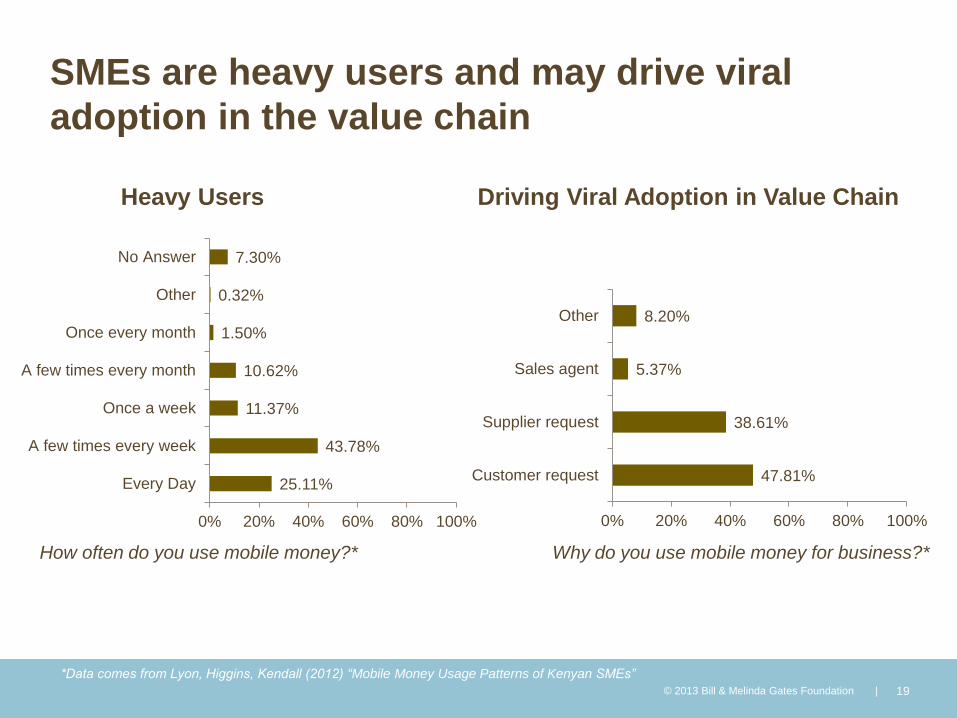

SMEs are key group as they drive value chain adoption to “close the e-loop”

© 2013 Bill & Melinda Gates Foundation | 13

Thank You

© 2013 Bill & Melinda Gates Foundation. All Rights Reserved. Bill & Melinda Gates Foundation is a registered trademark in the United States and other countries.

Appendix

© 2013 Bill & Melinda Gates Foundation | 15

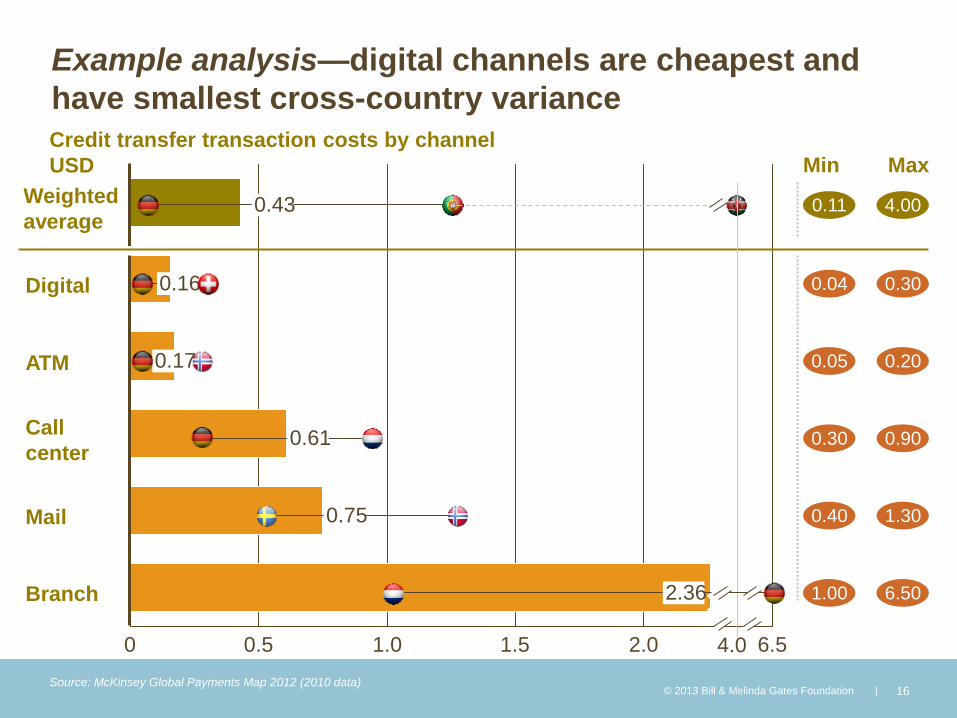

Example analysis—digital channels are cheapest and

have smallest cross-country variance

© 2013 Bill & Melinda Gates Foundation | 16

ATM

6.5 2.0 1.5 1.0 0.5 0

Branch

Call

center

Digital

Weighted

average

USD

Credit transfer transaction costs by channel

Min Max

0.16 0.04 0.30

0.43 0.11 4.00

4.0

0.75 0.40 1.30

0.61 0.30 0.90

2.36 1.00 6.50

0.17 0.05 0.20

Source: McKinsey Global Payments Map 2012 (2010 data)

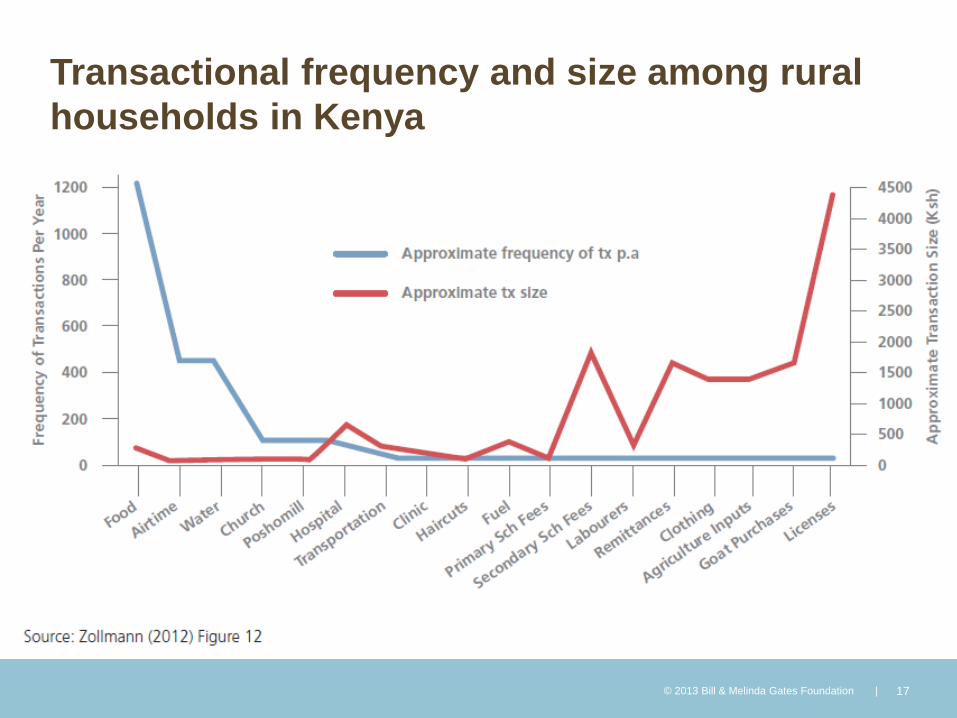

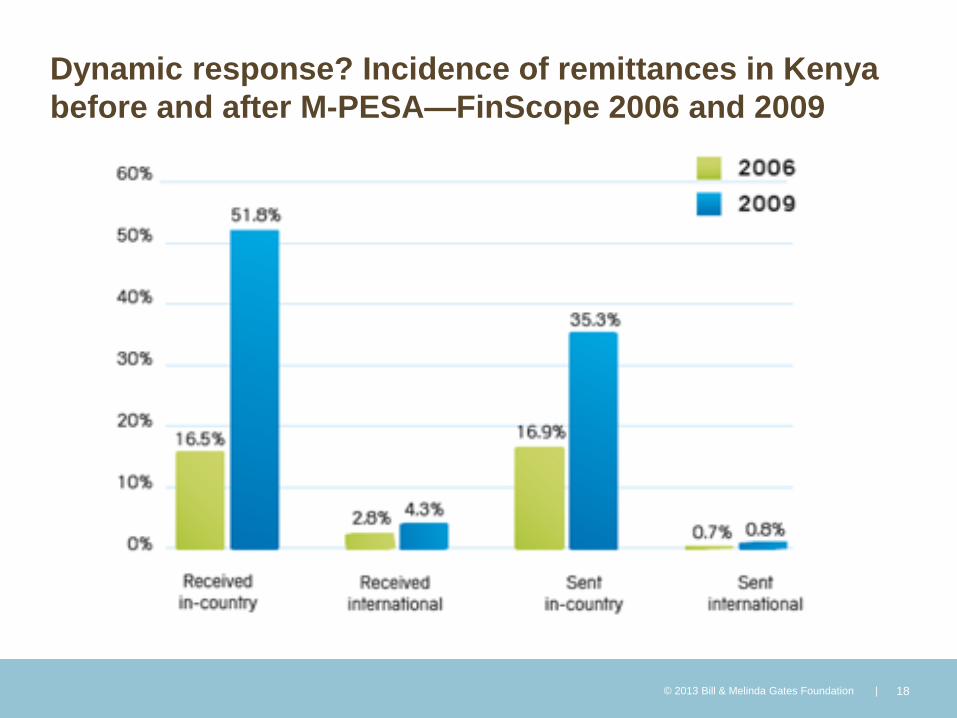

Transactional frequency and size among rural

households in Kenya

© 2013 Bill & Melinda Gates Foundation | 17

Dynamic response? Incidence of remittances in Kenya

before and after M-PESA—FinScope 2006 and 2009

© 2013 Bill & Melinda Gates Foundation | 18

SMEs are heavy users and may drive viral

adoption in the value chain

© 2013 Bill & Melinda Gates Foundation | 19

25.11%

43.78%

11.37%

10.62%

1.50%

0.32%

7.30%

0% 20% 40% 60% 80% 100%

Every Day

A few times every week

Once a week

A few times every month

Once every month

Other

No Answer

47.81%

38.61%

5.37%

8.20%

0% 20% 40% 60% 80% 100%

Customer request

Supplier request

Sales agent

Other

Why do you use mobile money for business?* How often do you use mobile money?*

*Data comes from Lyon, Higgins, Kendall (2012) “Mobile Money Usage Patterns of Kenyan SMEs”

Heavy Users Driving Viral Adoption in Value Chain

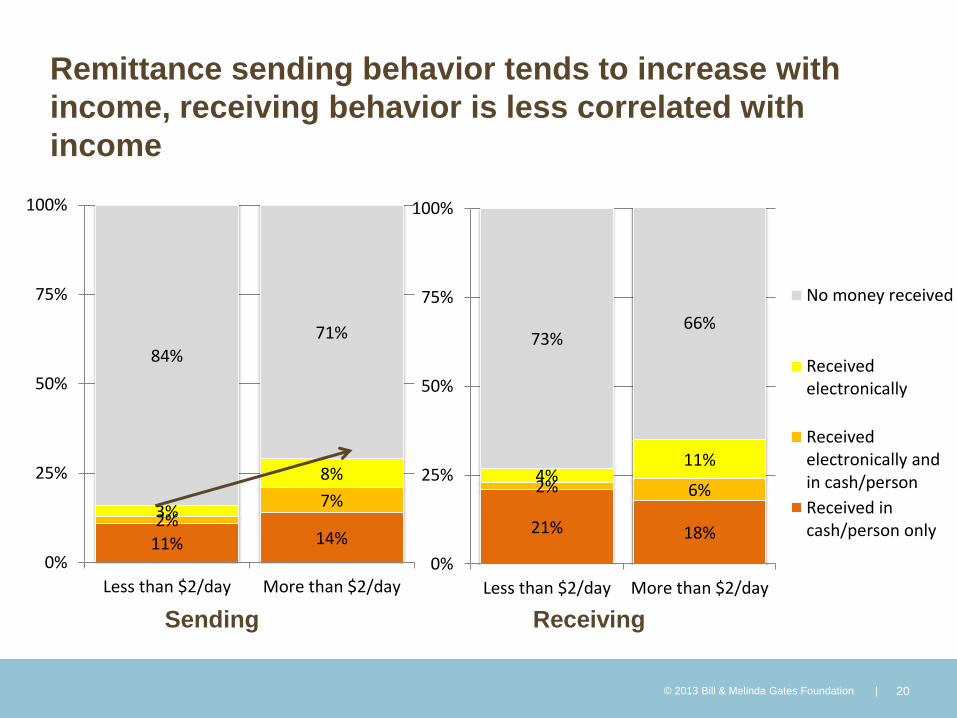

Remittance sending behavior tends to increase with

income, receiving behavior is less correlated with

income

© 2013 Bill & Melinda Gates Foundation | 20

11% 14% 2%

7% 3%

8%

84% 71%

0%

25%

50%

75%

100%

Less than $2/day More than $2/day

21% 18%

2% 6% 4%

11%

73% 66%

0%

25%

50%

75%

100%

Less than $2/day More than $2/day

No money received

Receivedelectronically

Receivedelectronically andin cash/person

Received incash/person only

Receiving Sending

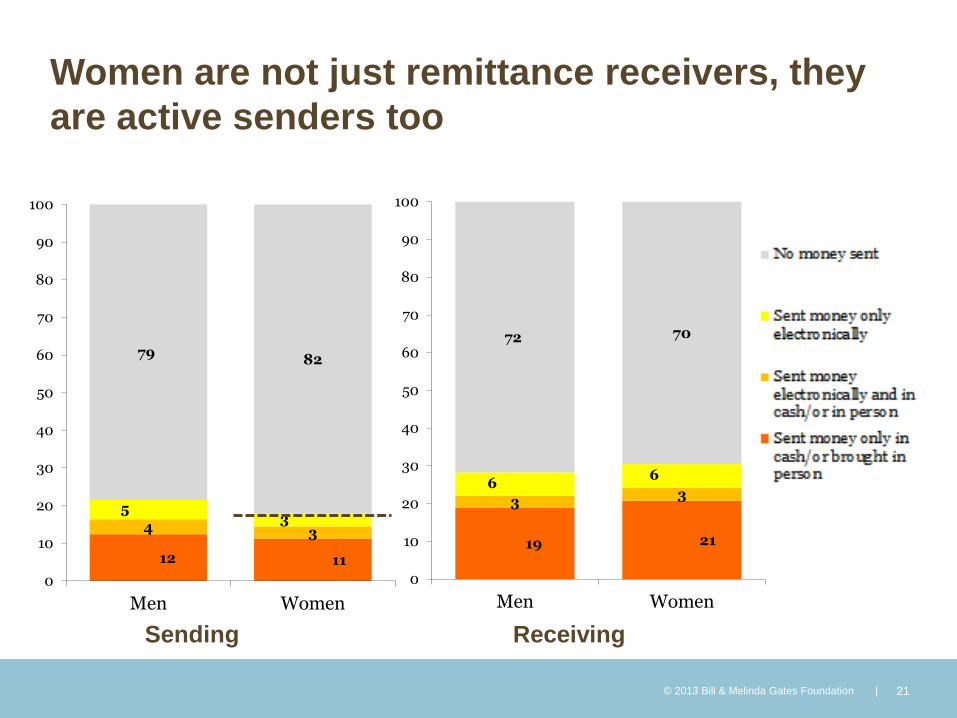

Women are not just remittance receivers, they

are active senders too

© 2013 Bill & Melinda Gates Foundation | 21

19 21

3 3

6 6

72 70

0

10

20

30

40

50

60

70

80

90

100

Men Women

12 11

4 3

5 3

79 82

0

10

20

30

40

50

60

70

80

90

100

Men Women

Receiving Sending

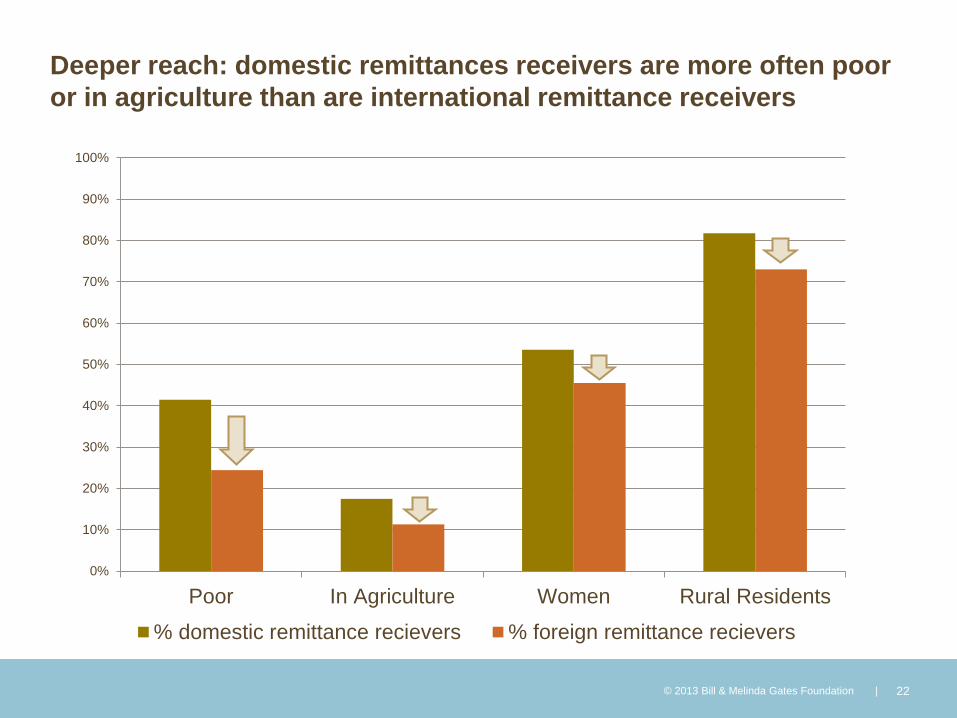

Deeper reach: domestic remittances receivers are more often poor

or in agriculture than are international remittance receivers

© 2013 Bill & Melinda Gates Foundation | 22

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Poor In Agriculture Women Rural Residents

% domestic remittance recievers % foreign remittance recievers

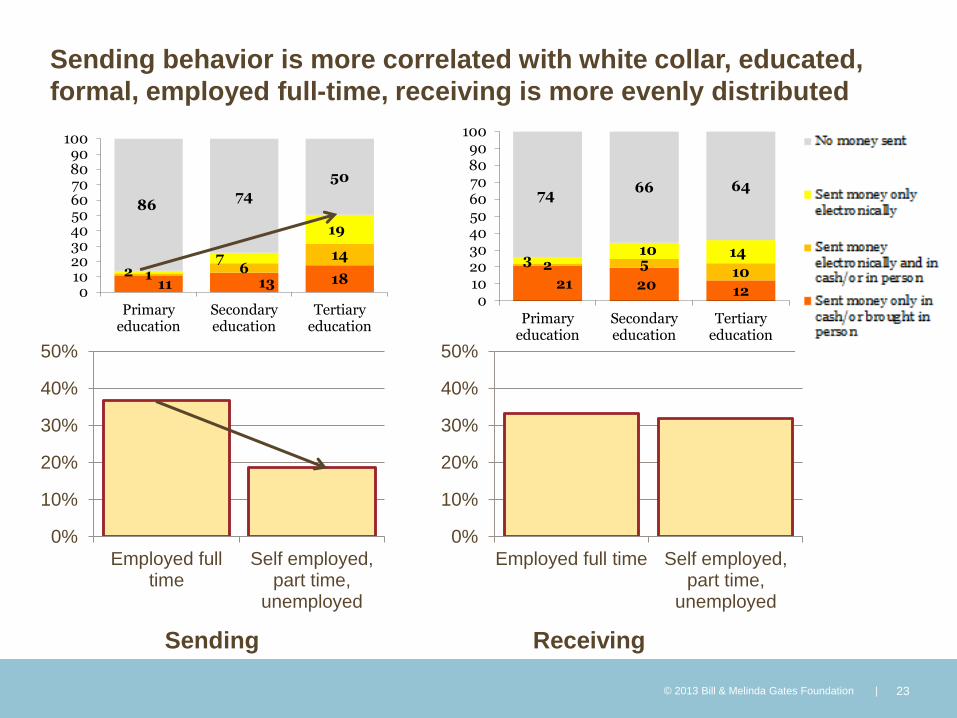

Sending behavior is more correlated with white collar, educated,

formal, employed full-time, receiving is more evenly distributed

© 2013 Bill & Melinda Gates Foundation | 23

0%

10%

20%

30%

40%

50%

Employed fulltime

Self employed,part time,

unemployed

0%

10%

20%

30%

40%

50%

Employed full time Self employed,part time,

unemployed

Receiving Sending

11 13 18 1 6 14

2 7

19

86 74

50

0102030405060708090

100

Primaryeducation

Secondaryeducation

Tertiaryeducation

21 20 12

2 5 10

3 10 14

74 66 64

0102030405060708090

100

Primaryeducation

Secondaryeducation

Tertiaryeducation

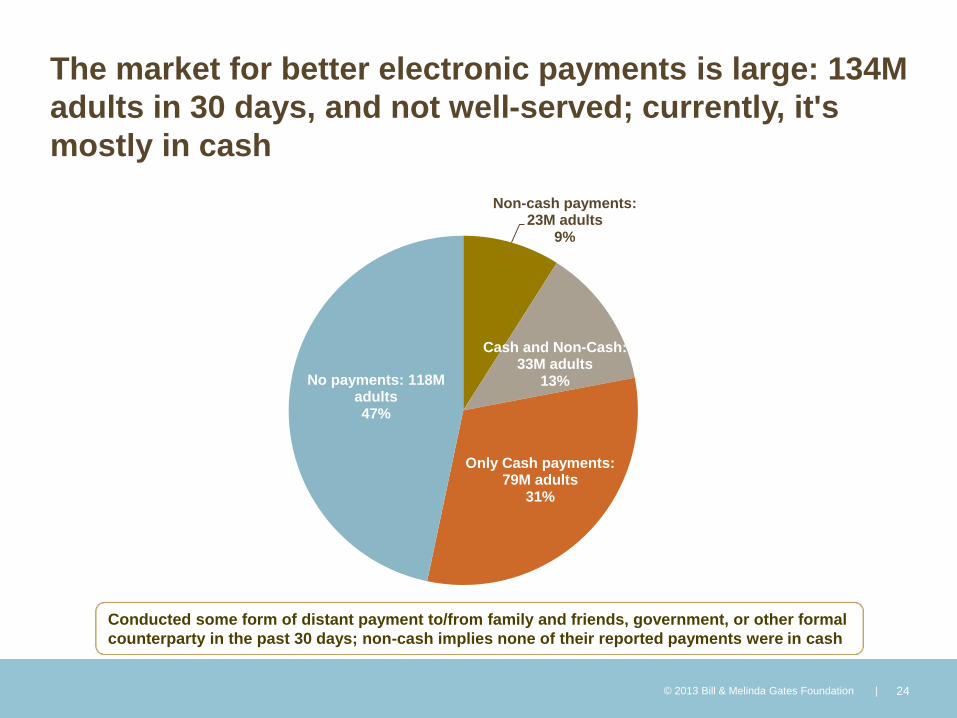

The market for better electronic payments is large: 134M

adults in 30 days, and not well-served; currently, it's

mostly in cash

© 2013 Bill & Melinda Gates Foundation | 24

Non-cash payments: 23M adults

9%

Cash and Non-Cash: 33M adults

13%

Only Cash payments: 79M adults

31%

No payments: 118M adults 47%

Conducted some form of distant payment to/from family and friends, government, or other formal

counterparty in the past 30 days; non-cash implies none of their reported payments were in cash