domestic resource mobilization in west africa… · domestic resource mobilization in west africa:...

TRANSCRIPT

DOMESTIC RESOURCEMOBILIZATION IN WEST AFRICA:MISSED OPPORTUNITIES

FEBRUARY 2015

A Study by Dalberg, commissioned by the

Open Society Initiative for West Africa

DOMESTIC RESOURCE MOBILIZATION IN WEST AFRICA: MISSED OPPORTUNITIES 2

ACKNOWLEDGMENTS

This report was made possible thanks to the generous contributions of time and expert

knowledge from many individuals and organizations. The Open Society Initiative for West

Africa (OSIWA) team provided invaluable insight, guidance, and support throughout the

preparation of this report. We would particularly like to thank Ibrahima Aidara, Mohamed

Sultan, and Vera Mshana. In addition, special thanks go to all the individuals who took part in

the interviews, sharing their wealth of experience, understanding, and data on fiscal policy in

West Africa.

ABWA Association of Accountancy Bodies in West Africa

AfDB African Development Bank

ALP Arm's-Length Principle

APA Advance Pricing Agreement/Arrangement

ATAF African Tax Administration Forum BEPS Base Erosion and Profit Shifting

CEMAC Central African Economic and Monetary Community

CET Common External TariffCGI General Tax Code CSO Civil Society Organization

CT Corporate tax

DGID Direction Générale des Impôts et Domaines - Senegal's Tax administration

DITA Directorate of Investigations and Tax Audits

DTA Double Tax Agreement (DTA)

EAC East African Community

ECOWAS Economic Community of West African States

EITI Extractive Industries Transparency Initiative

EIU Economic Intelligence Unit

EPZ Export Processing Zone

FCFA Franc de la Communauté Financière Africaine - African financial community franc

FDI Foreign Direct Investment

FIRS Federal Inland Revenue ServiceGDP Gross Domestic Product GFI Global Financial Integrity

IFAC International Federation of AccountantsIFFs Illicit Financial FlowsIMF International Monetary Fund

ISO International Organization for Standardization

KRA Kenya Revenue Authority

MENA Middle East and North AfricaMERCOSURMercado Común del Sur (Common Market of the South)

MTT Multilateral Tax Treaty

ODA Official Development Aid

OECD Organisation for Economic Co-operation and Development

ABBREVIATIONS

DOMESTIC RESOURCE MOBILIZATION IN WEST AFRICA: MISSED OPPORTUNITIES 3

ABBREVIATIONS

WBIC World Bank Investment Climate

WBG World Bank Group

WAEMU West African Economic and Monetary UnionVAT Value-Added Tax USA United States of AmericaUS United StatesUNECA United Nations Economic Commission for Africa

UNCTAD United Nations Conference on Trade and Development

UNCTAD United Nations Conference on Trade and DevelopmentUN United Nations

TPA Transfer Pricing Associates

TPA Transfer Pricing Associates

TIWG Tax Incentives Working Group

TIWB Tax Inspectors Without Borders

SYSCOA West African Accounting System (Système Comptable Ouest African or SYSCOA)

SADC Southern African Development Community

RPRSP ECOWAS Regional Poverty Reduction Strategy Paper

OSIWA Open Society Initiative for West Africa

ONECCA - Senegal Senegalese Accountancy Body (Ordre National des Experts Comptables et Comptables Agréés - Senegal

WTO World Trade Organization

DOMESTIC RESOURCE MOBILIZATION IN WEST AFRICA: MISSED OPPORTUNITIES 4

Abusive Transfer Pricing

GLOSSARY

Advance Pricing Agreement (APA)

Advance Pricing Agreement Arrangement (APA)

This takes place when prices are manipulated to maximize profits or reduce losses when two

companies that are part of the same multinational group trade with each other. Abusive

transfer pricing is sometimes referred to as “profit shifting” or “transfer pricing manipulation”

or “transfer mispricing”.Source: Tax Justice Network

An APA is an arrangement in respect of certain specified transactions that determines in

advance the appropriate criteria for determining transfer pricing. The agreement may be made

by the taxpayer unilaterally with the tax administration or may be a bilateral or multilateral

agreement involving the tax administrations of other countries.Source: United Nations Practical Manual on Transfer Pricing for Developing Countries

See Advance Pricing Agreement (APA)

Arm's-Length Principle (ALP)

The ALP for transfer pricing states that the amount charged by one related party to another for

a given product must be the same as if the parties were not related. An arm's-length price for a

transaction is therefore what the price of that transaction would be on the open market. Source: United Nations Practical Manual on Transfer Pricing for Developing Countries

Automatic Tax Information Exchange requires governments to collect from financial

institutions data on income, gains, and property paid to non-resident individuals, corporations,

and trusts. It also mandates that data collected be automatically provided to the governments

where the non-resident entity is located.Source: Global Financial Integrity

Automatic Tax Information Exchange

Beneficial Ownership Disclosure requires that the control and beneficial ownership of

companies, trusts and foundations be readily available on public record to facilitate effective

due diligence. It also explicitly requires and enforces that financial institutions identify the

ultimate beneficial owners or controllers of any company, trust or foundation seeking to open

an account.Source: Tax Justice Network, Financial Secrecy Index

Beneficial Ownership Disclosure

DOMESTIC RESOURCE MOBILIZATION IN WEST AFRICA: MISSED OPPORTUNITIES 5

DOMESTIC RESOURCE MOBILIZATION IN WEST AFRICA: MISSED OPPORTUNITIES 6

GLOSSARY

Financial Secrecy

There is no generally agreed definition of what financial secrecy is: the phenomenon has many

different aspects and no definition captures them all. Following is a short description that takes

a broad view of the phenomenon: A secrecy jurisdiction provides facilities that enable people

or entities to escape (and frequently undermine) the laws, rules and regulations of other

jurisdictions elsewhere, using secrecy as a prime tool. Source: Tax Justice Network, Financial Secrecy Index

Formulary Appointment

Under formulary apportionment a formula is used to apportion the group's net income

between the various entities and branches in the group. The formula normally uses some

combination of factors such as property, payroll, turnover, capital invested or manufacturing

costs.Source: United Nations Practical Manual on Transfer Pricing for Developing Countries

Double Taxation

Double taxation refers to the inclusion of the same income in the taxable bases of two different

taxpayers. For example, assume that a subsidiary located in Nigeria (Company A) is subject to a

transfer pricing adjustment (by means of the application of Regulations No 1, 2012 in October

2012) in relation to a transaction with an associated enterprise (Company B) located in the US; if

Nigeria increases Company A's tax burden through such an adjustment and the US fail to

reduce (relieve) this amount from the tax base of Company B, then the same income will be

subjected to tax in both countries, hence double taxationSource: World Bank Investment Climate, 2013

Capital flight refers to unrecorded movement of funds between a country and the rest of the

world. Source: World Bank, 1985

Capital Flight

Country-by-Country Reporting

The concept is to require the inclusion in annual audited financial statements of a profit and

loss account for each jurisdiction in which a multinational corporation had operations during

the year. These profit and loss accounts would include disclosure of both third party and intra-

group transactions, which for these purposes are those trades that take place across national

boundaries but between companies under common ownership or control. They would be

required to be reconciled with the overall group results. In addition, limited cash flow and

balance sheet data would also be required to be published. Source: Murphy, Benefits of Country-by-Country Reporting

Transfer Pricing Manipulation

See Abusive Transfer Pricing.

Tax Expenditure

The amount of revenues lost by a government after granting of tax incentives and exemptions.Source: Tax Policy Center, Tax Expenditures: What are they and how are they structured

Profit Shifting

See Abusive Transfer Pricing.

Tax Incentives

Tax incentives – also known as tax preferences – grant preferential tax treatment to specific

taxpayer groups, investment expenditures or returns, through targeted tax deductions, credits,

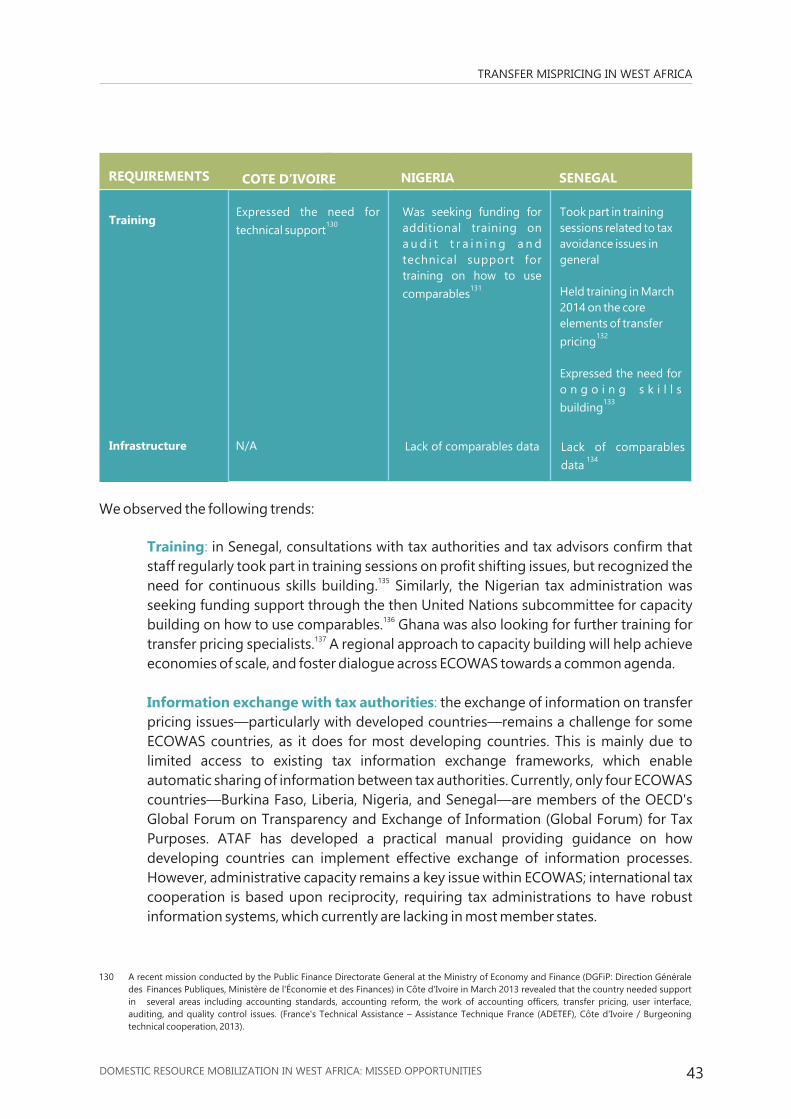

exclusions or exemptions. Source: African Development Bank, Domestic Resource Mobilization across Africa:

Trends, Challenges and Policy Options

Thin Capitalization

When the capital of a company is made up of a much greater contribution of debt than of

equity, it is said to be “thinly capitalized”. This is because it may sometimes be more

advantageous from a taxation viewpoint to finance a company by way of debt (i.e., leveraging)

rather than by way of equity contributions as typically the payment of interest on the debts may

be deducted for tax purposes whereas distributions are non-deductible dividends. Source: United Nations Practical Manual on Transfer Pricing for Developing Countries

Trade Mispricing

Trade misinvoicing – also referred to as trade mispricing - is a method for moving money illicitly

across borders, which involves deliberately misreporting the value of a commercial transaction

on an invoice submitted to customsSource: Global Financial Integrity

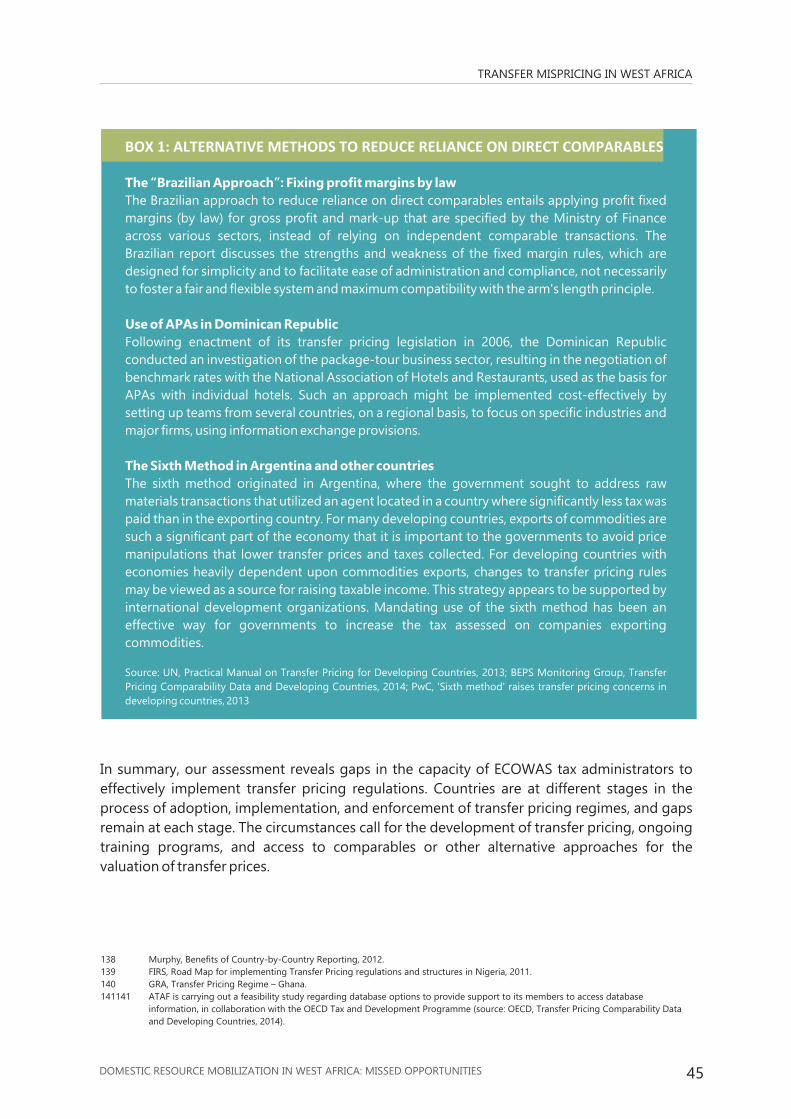

Transfer Mispricing

See Abusive Transfer Pricing.

Transfer Pricing

The general term for the pricing of cross-border, intra-group transactions in goods, intangibles

or services. Source: United Nations Practical Manual on Transfer Pricing for Developing Countries

DOMESTIC RESOURCE MOBILIZATION IN WEST AFRICA: MISSED OPPORTUNITIES 7

GLOSSARY

DOMESTIC RESOURCE MOBILIZATION IN WEST AFRICA: MISSED OPPORTUNITIES 8

GLOSSARY

Illicit Financial Flows (IFFs)

IFFs generally refer to movements of money that is illegally earned, transferred or used. Source: Global Financial Integrity

Unitary Taxation/Tax System

Under a unitary tax system, the profits of the various branches of an enterprise or the various

corporations of a group are calculated as if the entire group is a unity. A formula, such as

Formulary Apportionment, is used to allocate the global profits of a multinational group

among the associated enterprises on the basis of a combination of multiple factors such as

property, payroll, sales, capital invested, and manufacturing costsSource: Organisation for Economic Co-operation and Development, International Tax Terms

FOREWORDest Africa is at a critical juncture in its development. Crucial decisions need to be

made to reduce dependency on foreign aid, increase public investment in Wdevelopment initiatives and reduce extreme poverty. There are gargantuan

numbers floating around regarding the magnitude of capital flight from the region. Though

these numbers are often debated, they are telling. The debate about the magnitude of the

problem, whilst important, should not distract from the real issue - it is imperative for our

governments to shift the current paradigm which sees Africa losing billions, if not trillion, of

dollars in illicit financial flows.

There are many reports that have been published on this subject matter. While this report

cannot address all the nuances and complexity of tax policy reform in the region, it addresses

two key aspects, which if taken together, represent opportunities for West African

governments to raise capital, and ensure that the private sector profits from its natural

resources and its growing markets plays a just and fair role in providing resources to support

endogenous socio-economic and development programmes.

We chose to focus on tax incentives and transfer mispricing because as a Foundation we focus

primarily on governance. We believe that the enactment and effective implementation of

comprehensive regulations provides the best immediate returns. Some issues that need to be

urgently addressed include abuse of discretionary powers, lack of parliamentary oversight,

opaque or non-existent cost benefit analysis, weakness of tax and revenue agency capacity, as

well as corruption in all its forms. We do understand that there will be a strong focus on the

assumptions behind the numerical projections this report provides, and we welcome any

constructive ideas on how to improve that methodology. The key issue that the report

addresses nonetheless is the importance of taxation to work for West Africa's developmental

prospects.

Taxation is a concrete manifestation of leadership and future planning – or lack thereof. It is

extremely complex and technical in its implementation, but quintessentially human at its core.

Adequate tax systems are undoubtedly one of the most sustainable sources of financing

development for West African countries. Governments have a duty to its citizens to ensure that

the exploitation of natural resources, be they mineral or agricultural, is done subject to

adequate and fair compensation. This is why governance is such a key part of this process.

DOMESTIC RESOURCE MOBILIZATION IN WEST AFRICA: MISSED OPPORTUNITIES 10

FOREWARD

We should all care about it because it affects the State's ability to define its developmental

policies. For instance, it dictates how much a government will put towards supporting

agriculture and tackling food insecurity and how much will be set aside to provide wide

ranging and better education and medical coverage, particularly to those traditionally

marginalized.

Our region is replete with examples of a dearth of leadership, short-sightedness and

inefficiency in the management of state resources and revenues. Continued pressure and

increased demands from inter alia local communities and civil society can lead to the kind of

transformative reforms that will benefit our populations. We hope that this report

commissioned by OSIWA and prepared by Dalberg will meaningfully contribute to this

conversation.

Abdul Tejan-cole

Executive Director

Open Society Initiative for West Africa

EXECUTIVE SUMMARY

1

1 2010 report by the African Development Bank (AfDB) identified abusive transfer

pricing and excessive granting of tax incentives as the main challenges eroding the 2Aalready shallow tax base in most African countries . In the Economic Community of

West African States (ECOWAS), these two factors represent real missed opportunities for

member states to generate badly needed domestic resources for potentially transformative

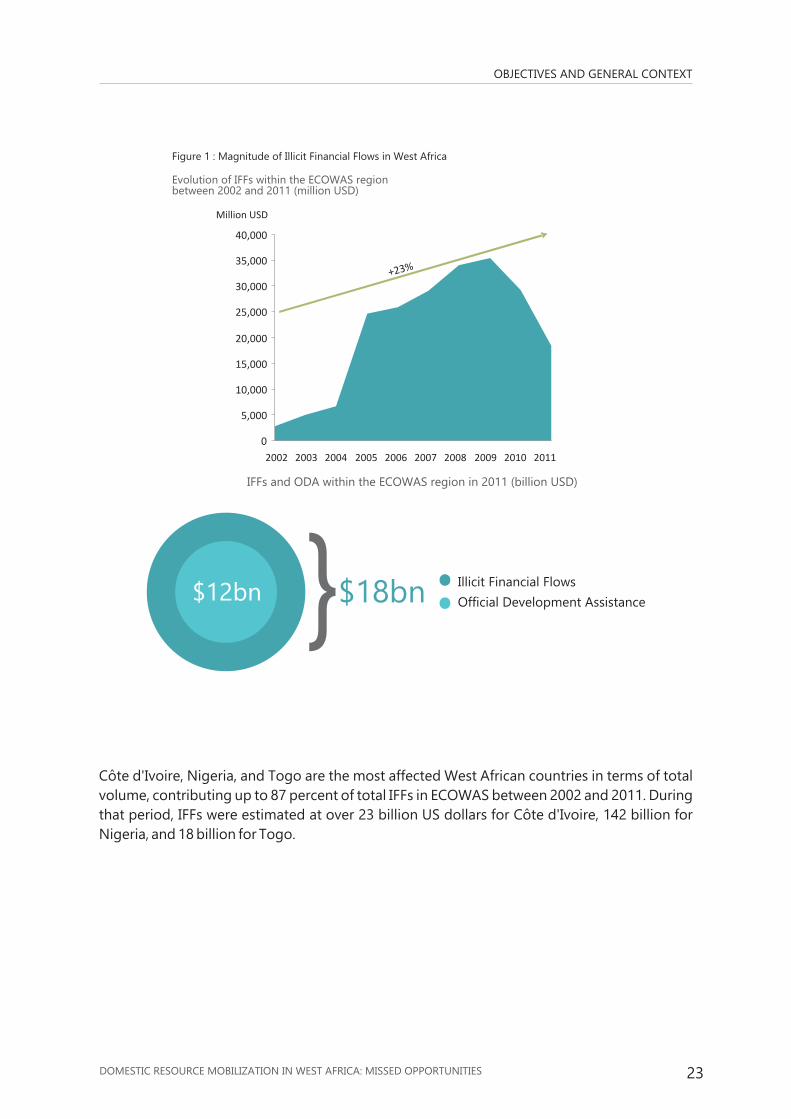

social and economic projects. Over the last decade, illicit financial flows (IFFs)—i.e., movements 3

of money that is illegally earned, transferred or used —have grown at an annual rate of 23

percent within ECOWAS, rising from less than 3 billion US dollars in 2002 to more than 18 billion 4US dollars in 2011. Although estimates vary greatly and are heavily debated, a general

consensus among economic observers is that IFFs from Africa likely exceed aid flows and

investment in volume. In 2011, for example, official development assistance (ODA) totaled 12 5billion US dollars. The United Nations Economic Commission for Africa (UNECA) estimates

6that 60 percent of IFFs derive from abusive transfer pricing, and sub-Saharan Africa countries 7

still mobilize less than 17 percent of their gross domestic product (GDP) in tax revenues.

Transfer mispricing occurs when multinational companies take advantage of their

organizational structure to shift profit out of higher-tax jurisdictions into lower-tax 8

jurisdictions, primarily by means of under-invoicing and over-invoicing. Unlike abusive

transfer pricing, which erodes the tax base as a result of fraudulent manipulation of prices of

intragroup transactions, tax incentives grant targeted tax deductions, credits, exclusions, or

exemptions to specific taxpayer groups, investment expenditures, or investment returns.

However, tax incentives can create significant tax revenue losses and other unforeseen effects,

such as harmful tax competition among ECOWAS countries, and do not necessary achieve their

stated purpose of attracting foreign direct investment (FDI).

1. AfDB, Domestic Resource Mobilization across Africa: Trends, Challenges and Policy Options, 2010.2. Tax incentives—also known as tax preferences—grant preferential tax treatment to specific taxpayer groups, investment expenditures, or returns,

through targeted tax deductions, credits, exclusions or exemptions. (AfDB, 2010) 3. Global Financial Integrity. 4. Global Financial Integrity, IFF Data By Country: http://wwwgfintegrity.org/issues/data-by-country/, 2002-2012.5. World Bank, WDI – Net official development assistance received (current US$), 2011.6. UNECA, The Dimension of Illicit Financial Flows as a Governance Challenge, 2013.7. OECD, Illicit Financial Flows from Developing Countries, 2014.8. ATAF, Transfer Pricing in the Extractives Industry: A taxing exercise for Sub-Saharan Africa, 2014.

DOMESTIC RESOURCE MOBILIZATION IN WEST AFRICA: MISSED OPPORTUNITIES 12

EXECUTIVE SUMMARY

Foregone tax revenue due to transfer mispricing represents the loss of a significant

opportunity for West African governments to define their development priorities with a

degree of agency difficult to achieve when financing is levied from international aid or debt.

The following assumptions underlie our estimation of the extent of revenue losses over the

next five years due to transfer mispricing:

Trends will hold steady for FDI, imports, and exports, over the next five years.9IFFs will continue to grow at 23 percent annually over the next five years. This is the

annual growth rate calculated based on the Global Financial Integrity (GFI) estimates.10

Transfer mispricing will make up about 60 percent of IFFs, as per UNECA estimates,

which are based on GFI data. These estimates consider that 60 percent of IFFs derive

from “commercial transactions through multinational companies.” These are global

estimates, but the hypothesis is that they are of about the same order of magnitude (if

not higher) for West Africa. Also of note, these estimates are questioned by some

experts in this space. Regardless, they provide for an estimated base of calculation of

transfer mispricing volumes, in a field where data is lacking for the reasons this report

aims to uncover.

If IFFs stemming from transfer mispricing were retained in ECOWAS and duly declared

to tax authorities, they would be taxed at the corporate income tax (CIT) rate,

generating additional tax revenues for governments.

CIT rates in the ECOWAS countries will remain the same, resulting in an average rate of 11

29 percent for ECOWAS as a whole.

Based on these assumptions, we estimate that global capital leakage from transfer pricing will 12

increase from 11 billion US dollars in 2011 (60 percent of the total of IFFs in 2011) to 78 billion

US dollars in 2018, leading to losses in government revenues from 3 billion US dollars in 2011

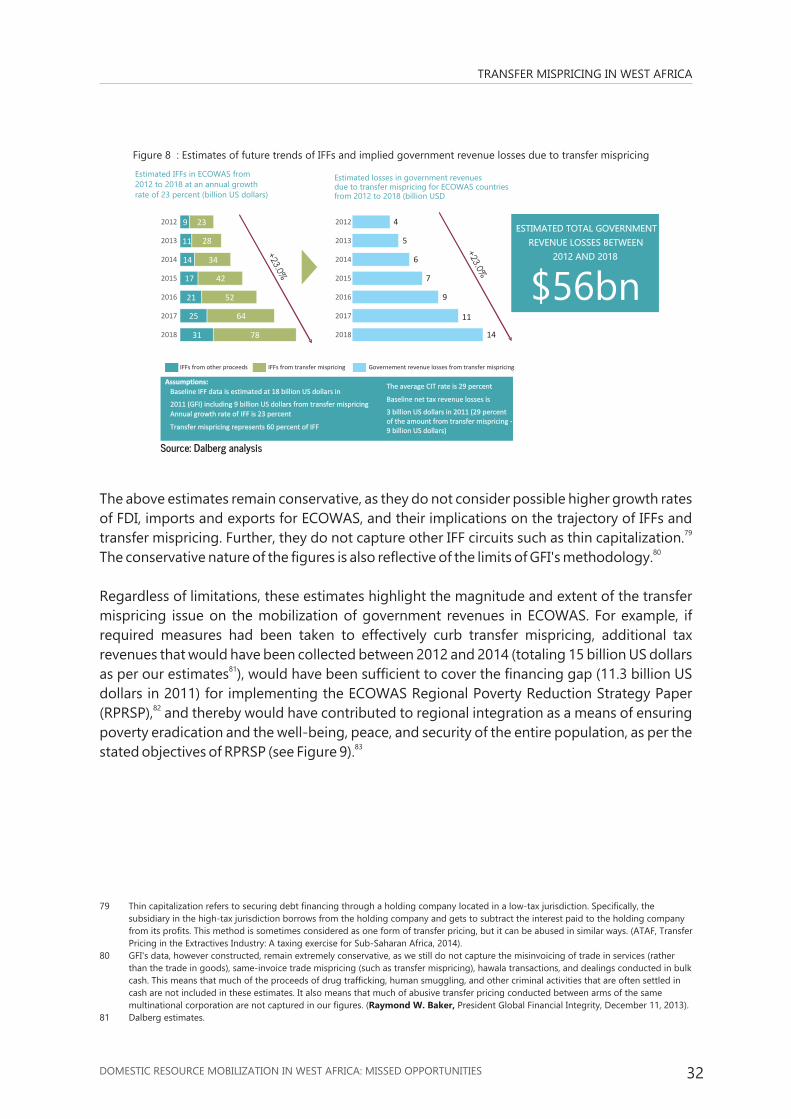

to 14 billion US dollars in 2018. The figure below presents the estimated future trends of

transfer mispricing and their implied losses in government revenues from 2012 to 2018.

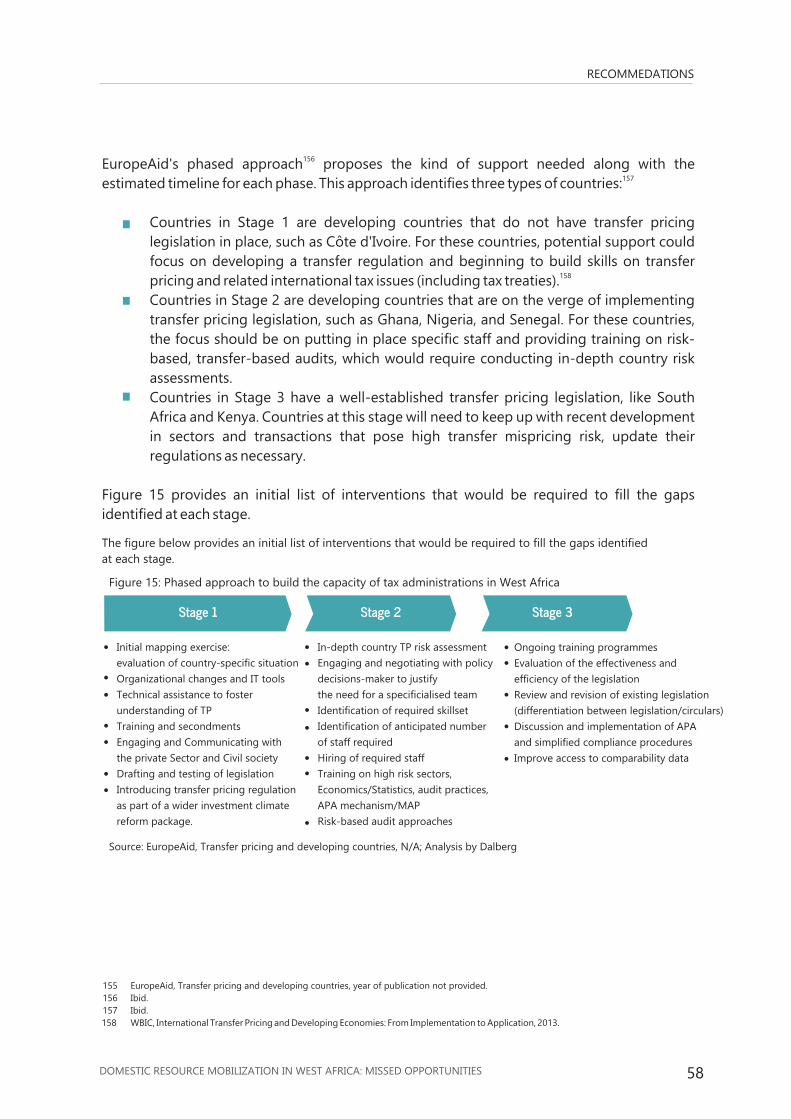

1.1.1 WHAT IS A STAKE?

1.1 CHALLENGES AND IMPLICATIONS OF TRANSFER MISPRICING IN WEST AFRICA

9. This is the annual growth rate calculated for the GFI estimates.

10 UNECA, Third Meeting of the Committee on Governance and Popular Participation, 2013.

11 Dalberg calculation, 2014; This is the average of individual country CIT rates as indicated in the Heritage Foundation's 2014 Index of

Economic Freedom.

12 This is based on GFI estimates for the main components of IFFs.

DOMESTIC RESOURCE MOBILIZATION IN WEST AFRICA: MISSED OPPORTUNITIES 13

13. Dalberg estimates (cf. the above figure “Estimates of future trends of IFFs and implied government revenue losses due to transfer

mispricing”).

14 The Borgen Project, ECOWAS Adopts New Strategy For Reducing Poverty, 2011 available at http://borgenproject.org/ecowas-adopts-new-

strategy-for-reducing-poverty/.

15 World Bank, International Transfer Pricing and Developing Economies: From Implementation to Application, 2013.

EXECUTIVE SUMMARY

Estimated IFFs in ECOWAS from 2012 to 2018 at an annual growth rate of 23 percent (billion US dollars)

9 23

14 34

17 42

21 52

25 64

31 78

2811

2012

2013

2014

2015

2016

2017

2018 14

11

9

7

6

5

4

Estimated losses in government revenues due to transfer mispricing for ECOWAS countries from 2012 to 2018 (billion USD

2012

2013

2014

2015

2016

2017

2018

+23.0%

+23.0%

IFFs from other proceeds IFFs from transfer mispricing Governement revenue losses from transfer mispricing

Assumptions:

• Baseline IFF data is estimated at 18 billion US dollars in

2011 (GFI) including 9 billion US dollars from transfer mispricing

• Annual growth rate of IFF is 23 percent

• Transfer mispricing represents 60 percent of IFF

• The average CIT rate is 29 percent

• Baseline net tax revenue losses is

3 billion US dollars in 2011 (29 percent of the amount from transfer mispricing - 9 billion US dollars)

Source: Dalberg analysis

To put this lost tax revenue in perspective, if measures had been taken to effectively curb

transfer mispricing (and assuming that the captured transfer mispricing would be subject to

tax), ECOWAS would have collected an additional 15 billion US dollars between 2012 and 132013, more than enough to cover the financing gap of the ECOWAS Regional Poverty

14Reduction Strategy Paper (RPRSP).

A sound transfer pricing regime—one that achieves the dual objective of protecting a country's 15tax base while at the same time maintaining an attractive investment climate —can contribute

to effectively curbing IFFs stemming from transfer mispricing and can mobilize more tax

revenues to fill the funding gaps in developing both national and regional projects. However,

there are obstacles to immediately putting such a regime in place, including the lack of a

comprehensive and harmonized transfer pricing legal framework in the region, the limited

capacity of tax administrators, and the inherent risk of capital flight from the region as a result

of stricter tax policies.

EXECUTIVE SUMMARY

Lack of a comprehensive and harmonized transfer pricing legal framework in ECOWAS

The level of sophistication of the legal frameworks for monitoring cross-border related-party

transactions varies considerably across ECOWAS countries. Only Ghana and Nigeria have

developed dedicated policies on transfer pricing, while nine other member states have

“emerging regimes”; meanwhile, four member states (Niger, Togo, Guinea-Bissau, and Cape

Verde) do not yet have transfer pricing policies in place.

Limited capacity of tax administrators

A recent study by the African Tax Administration Forum (ATAF) found that transfer pricing

remains a serious issue in most countries in West Africa. According to the study, the lack of tax

professionals who specialize in transfer pricing poses a major challenge to monitoring the

practice. Those who do have expertise are in need of ongoing and specialized training in

transfer pricing in sectors such as mining, oil and gas, information and communications

technology, intellectual property industries, and on particular issues such as the treatment of

assets and the branding and sales of companies.

Inherent risk of decreased FDI in the region as a result of stricter tax policies

The compliance burden of a transfer pricing regime tends to be high, particularly at the

beginning of implementation. A 2011 survey by Deloitte conducted for the European

Commission estimated that transfer pricing compliance costs (transfer pricing documentation,

clearances and rulings, and mutual agreement procedures) directly or indirectly account for

about 60 percent of all corporate tax-related compliance costs for a new subsidiary in the 16European Union of a multinational enterprise with a large parent. The compliance costs would

be on the same order of magnitude for a subsidiary in ECOWAS within existing transfer pricing 17

regimes in West Africa as all of these are based on the arm's-length principle (ALP). In some

cases, the compliance burden for multinationals could be significantly higher in the context of

West Africa, especially when the lack of necessary capacity or experience by the tax

administration leads to what could be perceived by taxpayers as untargeted transfer pricing 18

audits, unnecessarily protracted disputes, and/or inadequate documentation and disclosure

requirements.

OBSTACLES AGAINST SOUND TRANSFER PRICING REGIME

16 World Bank Investment Climate (WBIC), International Transfer Pricing and Developing Economies: From Implementation to Application,

2013.

17. There is a fundamental consistency between the UN Manual (for developing countries) and the OECD Transfer Pricing Guidelines (for

developed countries), in applying the ALP found in Article 9 of both the UN Model Convention and the OECD Model Convention.

While there are some differences between the two, those tend to reflect differences in perspective and emphasis, rather than

differences in the principles to be applied (Source: Deloitte, Arm's Length Standard, 2013).

18 For example, when tax administrators impose informational requirements on taxpayers that exceed the needs and capacity of the tax

administration (Source: WB Investment Climate, 2013).

DOMESTIC RESOURCE MOBILIZATION IN WEST AFRICA: MISSED OPPORTUNITIES 15

EXECUTIVE SUMMARY

The risk of double taxation also increases for multinationals as a result of transfer pricing

adjustments. Ernst & Young's 2003 Global Transfer Pricing Survey reports that 40 percent of 19transfer pricing adjustments resulted in double taxation. As such, double taxation imposes an

additional transactional cost on multinational enterprise groups, which hampers international

trade and foreign investment.

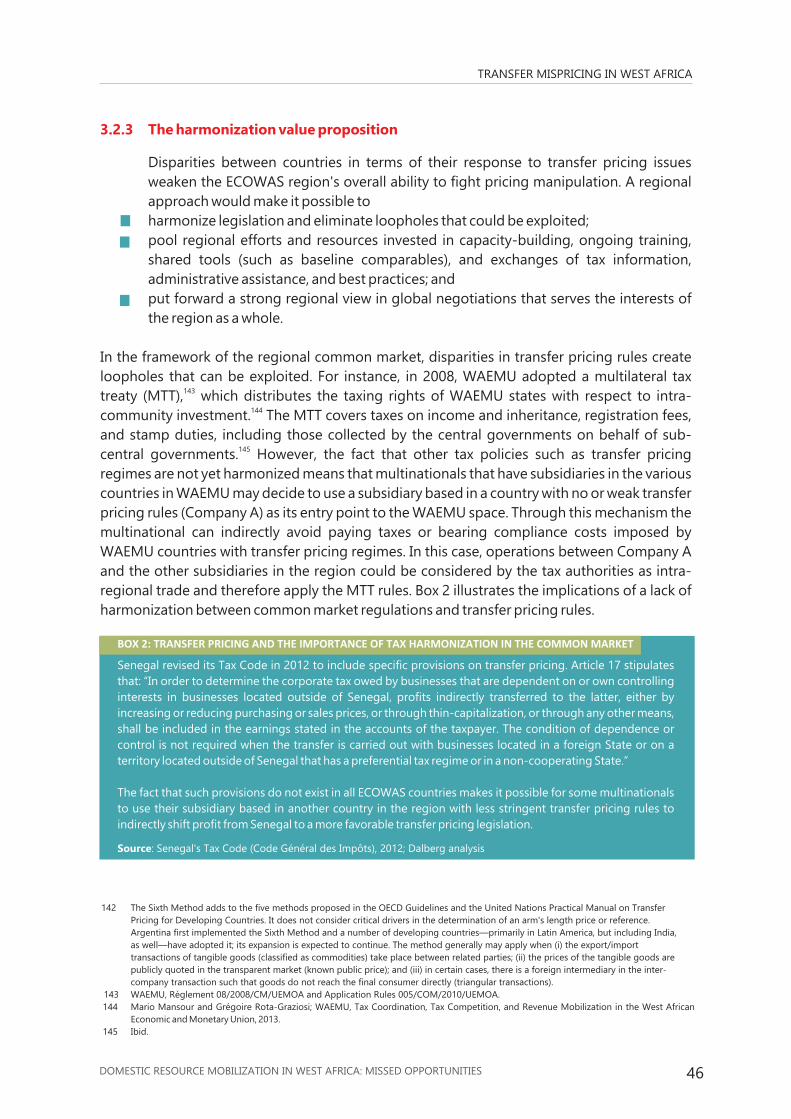

In the framework of the regional common market, disparities in transfer pricing rules create

loopholes that companies can exploit. For instance, in 2008 the West African Economic and 20Monetary Union (WAEMU) adopted a multilateral tax treaty (MTT) that distributes the taxing

21rights of WAEMU states with respect to intra-community investments. The MTT covers taxes

on income, including those collected by the central governments on behalf of sub-national 22governments. Multinationals that have subsidiaries in various countries in WAEMU may

decide to use the subsidiary (Company A) based in a WAEMU country with no or weak transfer

pricing rules as their entry point into the zone. Such a multinational will benefit from an

unintended tax advantage over other multinationals that locate their subsidiaries in WAEMU

countries with transfer pricing regimes. Operations between Company A and its subsidiaries

could be considered by the tax authorities as part of intra-regional trade and therefore apply

the MTT rules. A regional approach would make it possible to harmonize legislation and

eliminate loopholes.

ECOWAS member states highlighted both the lack of staff that specialize in transfer pricing and

capacity gaps that hinder the development and application of transfer pricing regulations.

Regional efforts should therefore also focus on identifying common needs across ECOWAS

countries and designing programs to address those needs centrally. The ECOWAS Commission

is best positioned to play this role. Examples of new programs include pooling the pricing and

transaction data available in each country to establish regionally meaningful comparables (i.e.,

databases on independent transactions that are used to assess whether transactions between

related parties are priced based on the market value).

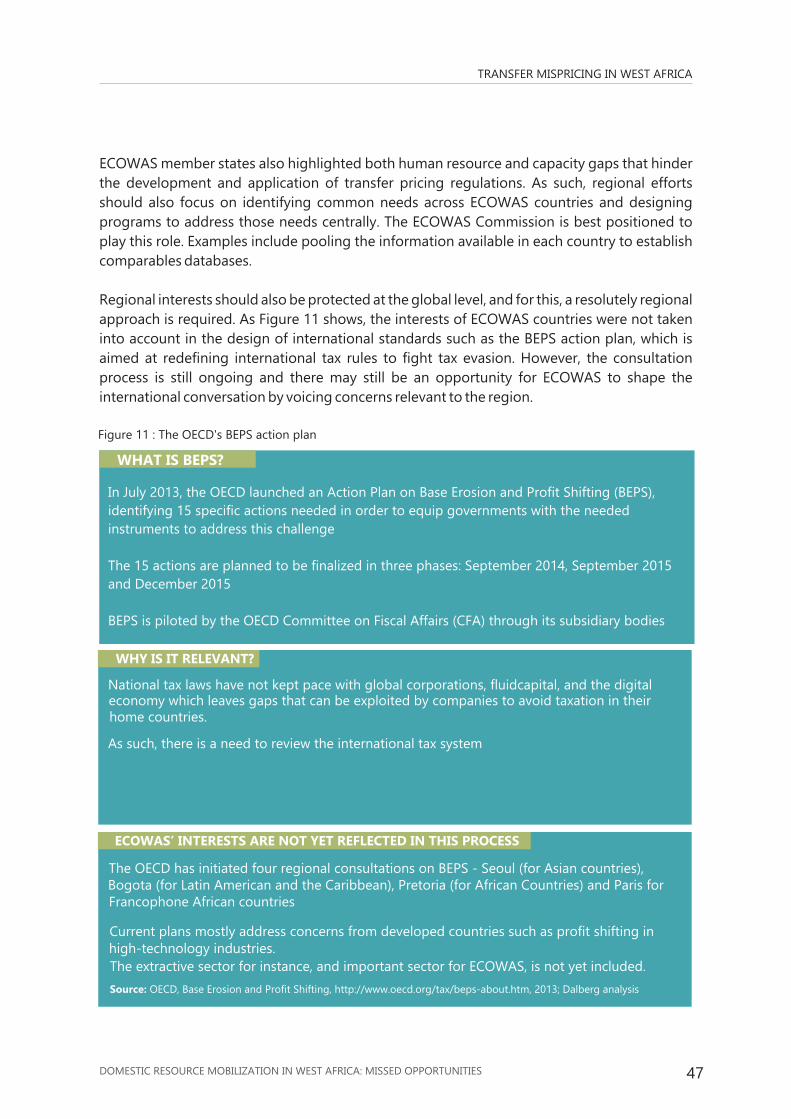

Regional interests should also be protected at the global level, and for this, a resolutely

regional approach is required. ECOWAS countries have not been parties to the Action Plan on

Base Erosion and Profit Shifting (BEPS), an initiative of the Organization for Economic Co-

operation and Development (OECD) aimed at redefining international tax rules to fight tax

evasion. The consultation process is still ongoing, and ECOWAS should make efforts to serve as

the region's voice on this issue.

1.1.2 Call to action

19 WBIC, International Transfer Pricing and Developing Economies: From Implementation to Application, 2013.

20 WAEMU, Règlement 08/2008/CM/UEMOA and Application Rules 005/COM/2010/UEMOA.

21 Mario Mansour and Grégoire Rota-Graziosi; WAEMU, Tax Coordination, Tax Competition, and Revenue. Mobilization in the West African

Economic and Monetary Union, 2013.

22 Ibid.

DOMESTIC RESOURCE MOBILIZATION IN WEST AFRICA: MISSED OPPORTUNITIES 16

EXECUTIVE SUMMARY

1.2 LOSSES OF GOVERNMENT REVENUE AND HARMFUL TAX COMPETITION BETWEEN COUNTRIES AS A RESULT OF TAX INCENTIVES

1.2.1 What is at stake?

1.2.2 Call to action

Tax incentives are simply too costly in West Africa, eroding the tax base for public resource

mobilization. Further, tax incentives can create competition between ECOWAS countries, 23

leading to a net loss at the regional level. A recent International Monetary Fund (IMF) study

showed that tax incentives in a given country can, to a large extent, have negative spillovers on

policies implemented in other countries. A one-point reduction in the corporate tax (CT) rate

globally causes a 3.7 percent reduction in the corporate tax base in a given country over the 24short term. In the agriculture and manufacturing sectors, the granting of tax incentives has

also resulted in harmful tax competition that has effectively reduced corporate tax rates across

the ECOWAS region.

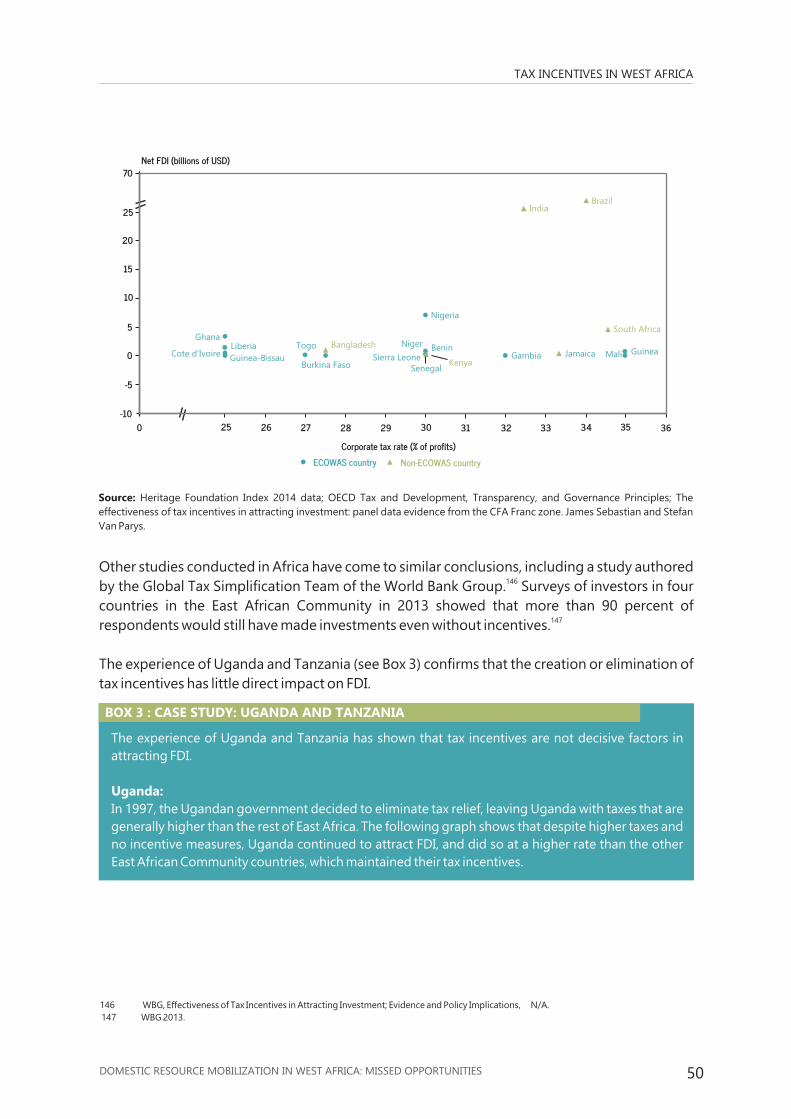

Yet, despite their high cost, tax incentives are not always a key factor in attracting FDI and ,25,26

driving economic growth. A study by Stefan Van Parys and Sebastian James concludes that

tax changes in the CFA Franc zone did not have significant impact on flows of FDI or fixed

capital formation. The study shows that other factors—such as increasing investor confidence

by broadening legal guarantees and simplifying the tax system—were, however, successful in

drawing more foreign investment.

ECOWAS and WAEMU have issued directives and guidelines that include more coherent tax

policies among member countries. These initiatives include the adoption of a common

external tariff (CET) within ECOWAS, which implies that all goods entering the customs territory

of any ECOWAS country will be assessed at the same rate of customs duty (0 percent, 5 percent, 27

10 percent, 20 percent, and 35 percent). The CET is expected to go into effect in 2015 within

the ECOWAS region. WAEMU has also issued directives that limit tax rates. However, a recent

review of harmonization efforts at the WAEMU level has shown that policies other than tax

legislation, such as investment codes, may be used by member states as a means of 28circumventing regional guidelines.

29All WAEMU states depart from the tax treatment under their general tax laws by providing

preferential tax regimes, often as part of investment codes at the national level, some of which

have been established after (and despite) the release of WAEMU guidelines.

23 IMF, Spillovers in international corporate taxation, 2014.

24 This study was conducted for the period 1980-2013 on a sample of 173 countries, including all ECOWAS countries (Source: IMF, Spillovers

in international corporate taxation, 2014).

25 Stefan Van Parys and Sebastian James, Why Tax Incentives May be an Ineffective Tool to Encouraging Investment? – The Role of

Investment Climate, 2009.

26 They sought to analyze theoretically how the investment climate affects the impact of the corporate tax rate on investment using a model

where the tax revenues are used to improve the investment climate.

27 ECOWAS, 2014; Gret-Iram, Etude prospective sur les mesures de protection nécessaires pour le développement du secteur agricole en

Afrique de l'Ouest (illustration sur quelques filières stratégiques).

28 Mario Mansour and Grégoire Rota-Graziosi; WAEMU, Tax Coordination, Tax Competition, and Revenue Mobilization in the West African

Economic and Monetary Union, 2013.

29 Ibid.

1.3 RECOMMENDATIONS

DOMESTIC RESOURCE MOBILIZATION IN WEST AFRICA: MISSED OPPORTUNITIES 17

EXECUTIVE SUMMARY

Overall, there is a strong need to develop and implement a West Africa regional initiative

focused on transfer pricing and to harmonize and rationalize tax incentives. Political will is an

essential underpinning of any such initiative; national governments, working with the ECOWAS

Commission, must be committed to jointly engaging in fiscal policy reforms. Below we offer our

specific recommendations for transfer pricing and tax incentives, respectively.

Regional reform of transfer pricing policy is a large undertaking, but we believe the

following are three key initial steps: (i) choosing between the ALP approach and

alternative methods—such as formulary apportionment—as the most appropriate

transfer pricing regime for the region; (ii) improving information exchange among

ECOWAS states; and (iii) advocating for and influencing change at the international

level.

ECOWAS should make a strategic decision either to adapt the OECD ALP or to develop

alternative methods, such as formulary apportionment (FA). As a starting point, ECOWAS

should examine the advantages and limitations of each method, taking into account the

regional context. What follows are brief presentations of the ALP and formulary apportionment

methods, as well as what we believe to be the key steps for the implementation and

enforcement of a transfer pricing regime in the region. These serve simply as starting points

and would require further analysis and adjustment, alongside careful consideration of other

methods.

· ALP standards. ALP is the OECD standard for determining for tax purposes the

conditions of commercial and financial transactions between associated enterprises.

However, there are some practical difficulties in its application: i) it requires

considerable documentation on the part of taxpayers; (ii) it is time- and resource-

intensive to implement and enforce; and (iii) it requires comparables, which are lacking

in the ECOWAS region.

1.3.1 Recommendations on transfer pricing

A. Choosing an appropriate transfer pricing regime for the region

30 Murphy, Benefits of Country-by-Country Reporting, 2012.

31 UN Practical Manual on Transfer Pricing for Developing Countries, 2012.

32 Ibid.

33 EuropeAid, Transfer pricing and developing countries, year of publication not provided.

DOMESTIC RESOURCE MOBILIZATION IN WEST AFRICA: MISSED OPPORTUNITIES 18

34 UEMOA, Règlement N° 08/CM/UEMOA.

35 TNJ, Financial Secrecy Index – next steps.

36 Sebastian James, Tax and Non-Tax Incentives and Investments: Evidence and Policy Implications, 2013.

EXECUTIVE SUMMARY

· Formulary apportionment. One alternative to the ALP approach is a formulary

apportionment (FA) method, also referred to as unitary taxation. Under unitary

taxation, the profits of the various branches of an enterprise or the various 30corporations of a group are calculated by treating the entire group as a unit. The FA

method is used to allocate the global profits of a multinational group among the

associated enterprises on the basis of a combination of multiple factors such as 31

property, payroll, sales, capital invested, and manufacturing costs. This method is not

without its limitations: (i) the arbitrariness of predetermined formulas makes it difficult

to reflect the particular circumstances of each multinational enterprise; (ii) FA relies

heavily on foreign-based information; (iii) implementation is difficult as it requires 32

substantial international coordination and consensus; and (iv) FA runs the risk of

creating disagreements among countries as each may wish to emphasize or include

different factors in the apportionment formula based on the activities or factors that

predominate in its jurisdiction.

The ECOWAS Commission should consider creating an “adapted” Transfer Pricing Advisory

Body, bringing together representatives of tax administrators, accounting and tax advisors,

and multinationals. The body would serve as a platform for consultation, experience sharing,

and discussion on transfer pricing issues in West Africa. The European Union (EU) has brought

together a group of experts from the public and private sectors to form an “EU Joint Transfer

Pricing Forum” (EU JTPF); ECOWAS could use this example to set up its own advisory body to

reinforce its collaboration with other groups specializing in tax matters, such as the

Association of Accountancy Bodies in West Africa (ABWA).

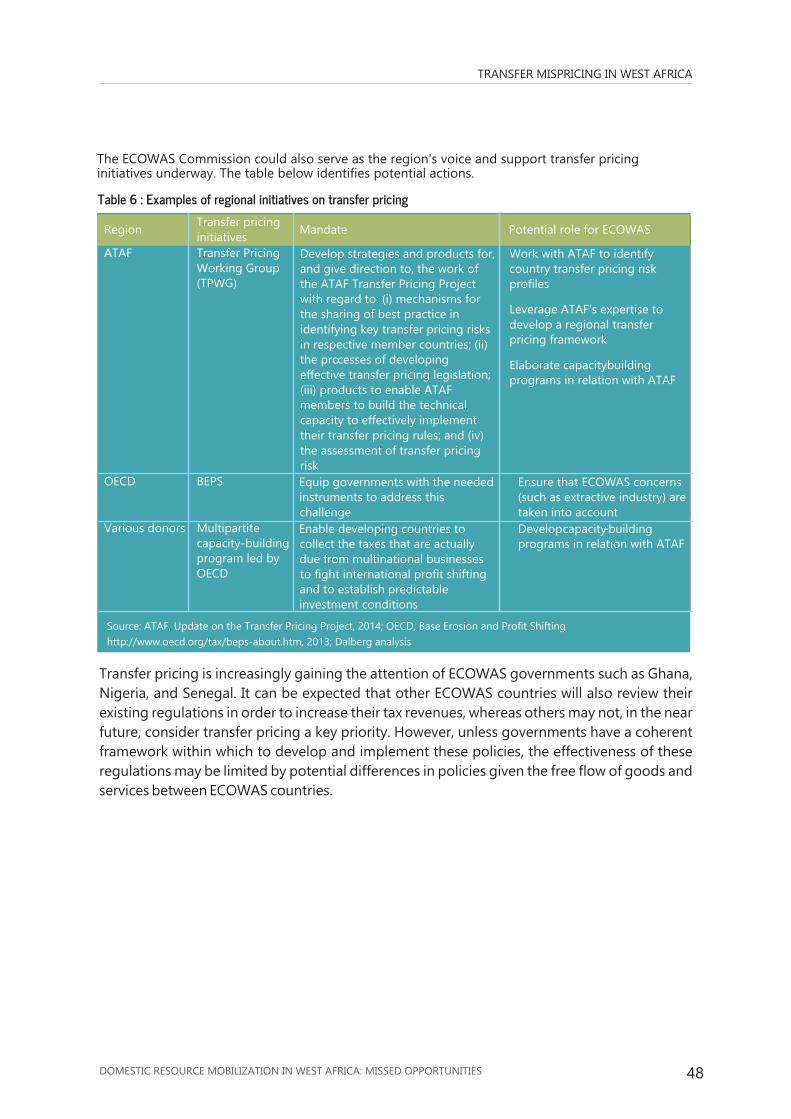

Through a collaboration with the Transfer Pricing Advisory Body, ATAF could support the

ECOWAS Commission in establishing guidelines for a harmonized transfer pricing regime. The

guidelines should focus on providing comprehensive details on different steps to be taken at

the local level toward the adoption of a transfer pricing regime, valuation methods of cross-

border related-party transactions, documentation requirements, and dispute resolution

mechanisms.

Setting up a regional coordination and advisory unit on transfer pricing

Issuing a comprehensive regional transfer pricing regulation framework

DOMESTIC RESOURCE MOBILIZATION IN WEST AFRICA: MISSED OPPORTUNITIES 19

EXECUTIVE SUMMARY

37 The draft code proposes only weak enforcement mechanisms and emphasizes tax harmonization more than regional cooperation. Also, it

does not oblige EAC states to undertake tax expenditure analyses to better assess the efficacy of tax incentives in realizing development

objectives. (Source: Tax Justice Network-Africa & ActionAid International, Tax competition in East Africa: A race to the bottom?, 2011).

38 Sebastian James, Tax and Non-Tax Incentives and Investments: Evidence and Policy Implications, 2013.

Strengthening the capacity of national tax administrators to enforce transfer pricing

policies

B. Improving information exchange

Tax administrators need to build up transfer pricing capacity and expertise, with a particular 33

focus on sectors and transactions that pose the greatest transfer mispricing risks. Equally

important will be for governments to retain newly trained and specialized talent since the

private sector will require the same skills in order to comply with regulations—and typically has

more resources than governments to attract and retain skilled financial professionals. Instilling

the necessary capabilities within the appropriate government departments of member states

will require long-term assistance and effort, and will demand that tax administrations undergo

significant changes, such as rapidly developing specific expertise on sectors and transactions

that pose the greatest transfer mispricing risks.

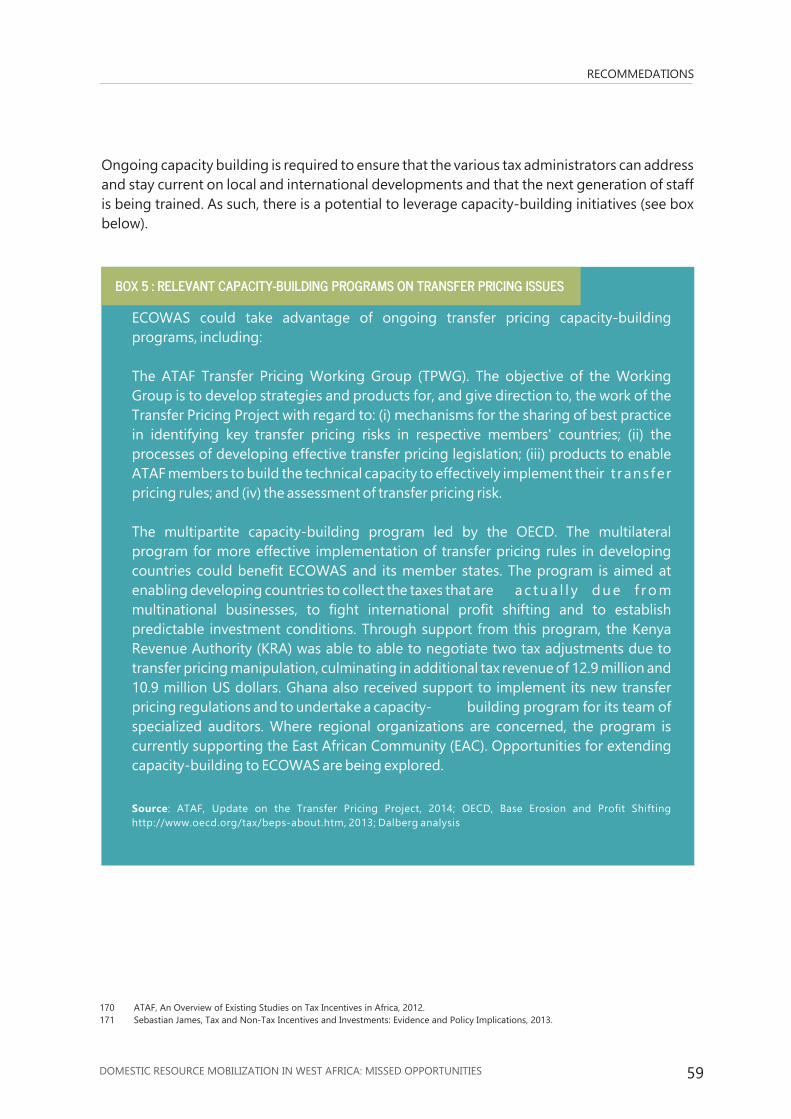

There is a potential to leverage capacity-building initiatives such as the ATAF Transfer Pricing

Working Group (TPWG), which aims to develop strategies and products for, and give direction

to, the work of the Transfer Pricing Project with regard to (i) mechanisms for the sharing of best

practices in identifying key transfer pricing risks in respective members' countries; (ii) the

processes of developing effective transfer pricing legislation; (iii) products to enable ATAF

members to build the technical capacity to effectively implement their transfer pricing rules;

and (iv) the assessment of transfer pricing risk.

In order to provide tax administrators with alternatives to information self-reported by

taxpayers, ECOWAS member states must cooperate more effectively on information exchange. 34This can build on existing frameworks such as (i) the WAEMU legal framework for avoiding

double taxation within the WAEMU space and providing assistance in the exchange of

information and tax collection; (ii) the ATAF Agreement on Mutual Assistance in Tax Matters;

and (iii) the ATAF Practical Guide on Exchange of Information for Developing Countries. As tax

cooperation should extend beyond the boundaries of economic communities, it will be

important for ECOWAS and other African economic unions (Southern African Development

Community [SADC], East African Community [EAC], Central African Economic and Monetary

Community [CEMAC], etc.) to work jointly on this initiative with support from ATAF and the UN

Tax Committee. The result would be that the vast majority of African countries would have the

administrative capacity and appropriate data standards (such as the OECD automatic

information exchange framework) to share data with others.

DOMESTIC RESOURCE MOBILIZATION IN WEST AFRICA: MISSED OPPORTUNITIES 20

EXECUTIVE SUMMARY

In addition, governments should make beneficial ownership disclosure compulsory at least for

the sectors with high risk of abusive transfer pricing. Beneficial ownership disclosure requires

that the control and beneficial ownership of companies, trusts, and foundations be readily 35available in the public record to facilitate effective due diligence.

To more effectively influence change, civil society should endeavor to find a creative way to

incentivize multinationals by demonstrating that they have much to gain from adopting the

country-by-country reporting system. An example could be to create a "transparency label" for

multinationals that comply with country-by-country reporting standards. Regardless of

whether or not country-by-country reporting becomes international law, the idea is to develop

voluntary international standards on tax and financial transparency within multinationals. A

"transparency label" would be similar to what the International Organization for

Standardization (ISO) is doing to provide world-class specifications for products, services, and

systems in order to ensure quality, safety and efficiency.

Finally, we recommend that the Commission take an active role in global talks and

consultations conducted with a view to drawing up international standards, such as the BEPS

action plan aimed at redefining international tax rules and combating tax evasion. Civil society

should also work closely with ATAF and the UN Tax Committee in tax policy design and

administration.

To broaden the tax base through tax incentives reform, priority interventions should focus on

(I) setting region-wide guidelines for tax exemptions, (ii) improving transparency in the

governance of tax incentives, and (ii) advocating for and influencing change at the

international level.

The ECOWAS Commission should strive for the rationalization and coordination of tax

incentives by working in close collaboration with the WAEMU Commission. Both organizations

should come together through a joint committee, such as the ECOWAS-WAEMU Joint CET

Management Committee, to stop the region's race to the bottom on tax incentives. To that

end, ECOWAS and WAEMU can learn from the successes and challenges of other regional

C. Advocating for and influencing change

A. Setting guidelines for tax exemptions

1.3 .2 Recommendations on tax incentives

DOMESTIC RESOURCE MOBILIZATION IN WEST AFRICA: MISSED OPPORTUNITIES 21

EXECUTIVE SUMMARY

communities that have undertaken the tax incentive regime harmonization process. For

example, the East African Community (EAC) recently made significant progress toward a

system of harmonizing their tax incentive regime through the use of a “Code of Conduct,” 36 37though it has yet to be adopted. The Code of Conduct, despite some limitations, aims to

formalize an existing arrangement whereby each year the Finance Ministers of the five

countries that make up the EAC meet before their budget speeches are made and discuss their

budget proposals. This provides the opportunity for Finance Ministers to dissuade other 38

members from proposing any new tax incentive that puts other countries at a disadvantage.

Governments should systematically carry out cost-benefit analyses and subject tax exemption

measures to oversight by parliament—existing in all ECOWAS member states —and the

citizenry. Tax incentives should be reviewed and approved by parliament before they are

definitively granted, and only after an objective study of the expected costs and benefits have

been presented to parliament, through annual tax expenditure analysis, as part of the budget

process. Morocco is one of the few African countries that are currently reporting their tax 39incentives in their tax expenditure reports. These reports aim to guide the allocation of

resources, strengthen public financial management, and contribute to fiscal transparency by

providing information for the comparison of the cost and effectiveness of direct spending and

tax expenditure programs.

Through advocacy, civil society should ensure that tax incentives are granted transparently and

are in the best interests of the ECOWAS countries.

B. Improving transparency in the governance of tax incentives

C. Advocating for and influencing change

39 OECD, Tax Incentives for Investment – A Global Perspective: experiences in MENA and non-MENA countries, 2007.

OBJECTIVES AND GENERAL CONTEXT

2

1

The Open Society Initiative for West Africa (OSIWA) aims to promote inclusive democratic

governance, transparency, and the sense of responsibility in the management of institutions as

well as active citizenship in West Africa (www.osiwa.org). As part of its push to produce

evidence-based research to help the Economic Community of West African States (ECOWAS)

to refine its regional integration agenda, OSIWA contracted Dalberg Global Development

Advisors (www.dalberg.com) to conduct two studies, one of which explores missed

opportunities to increase the tax base in West Africa by addressing challenges posed by

transfer mispricing and tax incentives. The study aims to identify policy changes that are

required to curb transfer mispricing and to ensure that tax incentives are beneficial to the

region, with a particular focus on engaging the West African civil society and the private sector

in the process of formulating, implementing, and monitoring these policies. The second study

aims to promote the formulation and implementation of more effective agricultural and

industrial policies for integrated development in West Africa.

40A 2010 report by the African Development Bank (AfDB) identified abusive transfer pricing and

excessive granting of tax incentives as the main challenges eroding the already shallow tax

base in most African countries. These two challenges result in missed opportunities to mobilize

badly needed public resources in the ECOWAS region. Over the last decade, illicit financial

flows (IFFs) have grown at an annual rate of 23 percent within ECOWAS, rising from less than 3 41

billion US dollars in 2002 to more than 18 billion US dollars in 2011. Although estimates vary

greatly and are heavily debated, there is a general consensus that IFFs from Africa likely exceed

aid flows and investment in volume. In 2011, for example, official development assistance 42 43(ODA) totaled 12 billion US dollars. UNECA estimates that 60 percent of IFFs derive from

abusive transfer pricing, and that sub-Saharan Africa countries still mobilize less than 17 44

percent of their gross domestic Product (GDP) in tax revenues.

40 AfDB, Domestic Resource Mobilization across Africa: Trends, Challenges and Policy Options, 2010.

41 Global Financial Integrity (GFI), IFF Data By Country: http://wwwgfintegrity.org/issues/data-by-country/, 2002-2012.

42 World Bank, WDI – Net official development assistance received (current US$), 2011.

43 UNECA, Third Meeting of the Committee on Governance and Popular Participation, 2013.

44 OECD, Illicit Financial Flows from Developing Countries, 2014.

DOMESTIC RESOURCE MOBILIZATION IN WEST AFRICA: MISSED OPPORTUNITIES 23

Evolution of IFFs within the ECOWAS region between 2002 and 2011 (million USD)

Million USD

IFFs and ODA within the ECOWAS region in 2011 (billion USD)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

+23%

20082003 2005 200720062002 20092004 20112010

Figure 1 : Magnitude of Illicit Financial Flows in West Africa

Source: GFI, IFF Data by Coun try: http: / / wwwgfintegrity. org/ issues/ data- by- coun try/ , 2002- 2011; GFI, Illicit Financial Flows

from Africa: Hidden Resource for Development, 2010; World Bank, WDI – Net official development assistance received

( current US dollars) , 2011; Dalberg analysis

$18bn$12bn { Illicit Financial Flows

Official Development Assistance

Côte d'Ivoire, Nigeria, and Togo are the most affected West African countries in terms of total

volume, contributing up to 87 percent of total IFFs in ECOWAS between 2002 and 2011. During

that period, IFFs were estimated at over 23 billion US dollars for Côte d'Ivoire, 142 billion for

Nigeria, and 18 billion for Togo.

OBJECTIVES AND GENERAL CONTEXT

DOMESTIC RESOURCE MOBILIZATION IN WEST AFRICA: MISSED OPPORTUNITIES 24

Nigeria

Guinea

Sierra Leone

Liberia

Senegal

Guinea Bisau

Ghana

Benin

Cape Verde

Gambia

IvoryCoast

Mali Niger

Togo

Burkina-Faso

11

387

557

587

714

1,129

2,963

3,128

3,754

10,256

18,467

142,274

23,138

3,164

413

45Estimates by Global Financial Integrity (GFI) break down IFFs, at a global level, as follows:46

· 60 to 65 percent from private business practices such as trade misinvoicing.

· 30 to 35 percent from criminal activities such as money laundering, drug trafficking and

human trafficking.

· 3 percent from corruption.

Trade misinvoicing moves more illicit money across borders than any other conduit of IFFs. GFI

estimates the average annual loss to Sub-Saharan Africa associated with trade misinvoicing at 4738.4 billion US dollars between 2008 and 2010. In Guinea, Mali, and Togo, the average annual

loss from trade misinvoicing was estimated respectively at 16 percent, 25 percent, and 13 48

percent of government revenues between 2002 and 2006.

OBJECTIVES AND GENERAL CONTEXT

45. United Nations Economic Commission for Africa (UNECA), Third Meeting of the Committee on Governance and Popular Participation,

2013.

46 Transfer pricing—defined as the price an entity of a company charges to a different entity of the same company for a good or service

(Farlex Financial Dictionary, 2012)—is not, in itself, illegal or necessarily abusive. It becomes illegal or abusive when it involves

manipulating prices to minimizing the tax burden or increasing apparent losses to make profits look as small as possible also known as

transfer mispricing, transfer pricing manipulation, or abusive transfer pricing (Tax Justice Network).

47 The Africa Center, Africa Rising? From resource potential to shared prosperity, 2014,

48 GFI, Implied Tax Revenue Loss from Trade Mispricing, 2010.

DOMESTIC RESOURCE MOBILIZATION IN WEST AFRICA: MISSED OPPORTUNITIES 25

Unlike abusive transfer pricing, which erodes the tax base as a result of fraudulent manipulation

of prices of intragroup transactions, tax incentives are concessions by governments on

potential additional tax revenues. Tax incentives—also known as tax preferences—grant

preferential tax treatment to specific taxpayer groups, investment expenditures, or investment

returns, through targeted tax deductions, credits, exclusions, or exemptions. Governments cite

various arguments for the use of tax incentives, ranging from addressing different types of 49

market failures to attracting foreign firms to stimulating exports.

In Sierra Leone, international companies were granted tax exemptions amounting to 224

million US dollars in 2012, equivalent to 55 percent of government revenues, eight times the 50

health budget, and seven times the education budget. In Ghana, these tax expenditures 51

accounted for 42 percent of government tax revenue in 2011, equaling 6 percent of GDP. In

Senegal, tax exemptions were estimated at 20 percent of total tax revenues in 2009, equating to 523 percent of the country's GDP. Nigeria lost over 425 million US dollars in 2006 through tax

53incentives, while the tax losses generated by tax preferences in Côte d'Ivoire reached 160

54million US dollars in 2013.

OBJECTIVES AND GENERAL CONTEXT

49 AfDB, Domestic Resource Mobilization across Africa: Trends, Challenges and Policy Options, 2010.

50 Christian Aid, Losing Out: Sierra Leone's massive revenue losses from tax incentives, 2014.

51 OECD, Analysis of Tax Expenditures in Ghana, 2013.

52 DGID – Sénégal, incitations fiscales à l'investissement: Coût et efficacité, 2014.

53 Fakile, Adeniran Samuel Adegbie, Festus Faboyede, Olusola Samuel, Tax Expenditure in Sub Saharan Africa: The Nigerian Experience,

2012.

54 IMF, Côte d'Ivoire - Technical Assistance Report, 2014.

TRANSFER MISPRICINGIN WEST AFRICA

3

3.1 Scale, impact and trajectory of transfer mispricing in

West Africa

Transfer mispricing occurs when multinational companies take advantage of their

organizational structure to shift profit out of high-tax jurisdictions into lower-tax jurisdictions 55

using different vehicles, including

· under-invoicing: selling goods, services, or intangibles to a related company at a

below-market rate. For example, under-invoicing can occur when an ECOWAS-based

subsidiary sells raw materials to its parent company based out of the ECOWAS zone.

· over-invoicing: buying goods, services, or intangibles from a related company at a

higher-than-market rate. For example, over-invoicing can occur when an ECOWAS-

based subsidiary buys goods or services from its parent company based out of

ECOWAS at an abnormally high price, in such a way as to artificially lower its profits.

The risk of transfer mispricing is likely to increase as multinationals become more active in the

region, particularly through subsidiaries. The analysis below seeks to estimate the magnitude

of the potential risk of transfer mispricing in the ECOWAS region. The study does recognize the

critical importance of foreign direct investment (FDI) in ECOWAS, and does not conclude that

the increased activity of multinationals in West Africa automatically leads to increased transfer 56

mispricing. However, the risk is real and calls for policy that strikes the right balance between

FDI and tax losses.

The dominant role of multinationals in West Africa makes the region particularly vulnerable to

transfer pricing manipulation. UNECA estimates that 60 percent of global IFFs stem from the 57

commercial transactions of multinational corporations. Country profiles issued by the United

Nations Conference on Trade and Development (UNCTAD) in 2004 revealed that the 90 largest

55 ATAF, Transfer Pricing in the Extractives Industry: A taxing exercise for Sub-Saharan Africa, 2014.

56 The analysis did not identify any correlation between IFFs and FDI.

57 UNECA, Third Meeting of the Committee on Governance and Popular Participation, 2013.

DOMESTIC RESOURCE MOBILIZATION IN WEST AFRICA: MISSED OPPORTUNITIES 27

2,250

2,331

1,633

3,678

16

16

15

15

15

14 737

Largest affiliates of multinationals in select countries in 2004 in the tertiary* and industrial sectors (#)

Sales of largest affiliates of multinationals in select countries in 2004 in the tertiary* and industrial sectors (million US dollars)

3,883

6,009

31

31

29 847

110

(*) Not inclusive of the financial sector

(**) GDP, current prices, billion US dollars in 2004 Tertiary Industrial

Source: UNCTAD, FDI/TNC database, Country Profiles, 2004; AfDB, Open Data for Africa database, 2004; Dalberg analysis

Figure 3 : Importance of multinational activity in West Africa

COTE D’IVORE

NIGERIA

SENEGAL

27 7

Magnitude of sales of largest affiliates of multinationals in select countries in 2004 (% of GDP**)

COTE D’IVORE NIGERIA SENEGAL

11

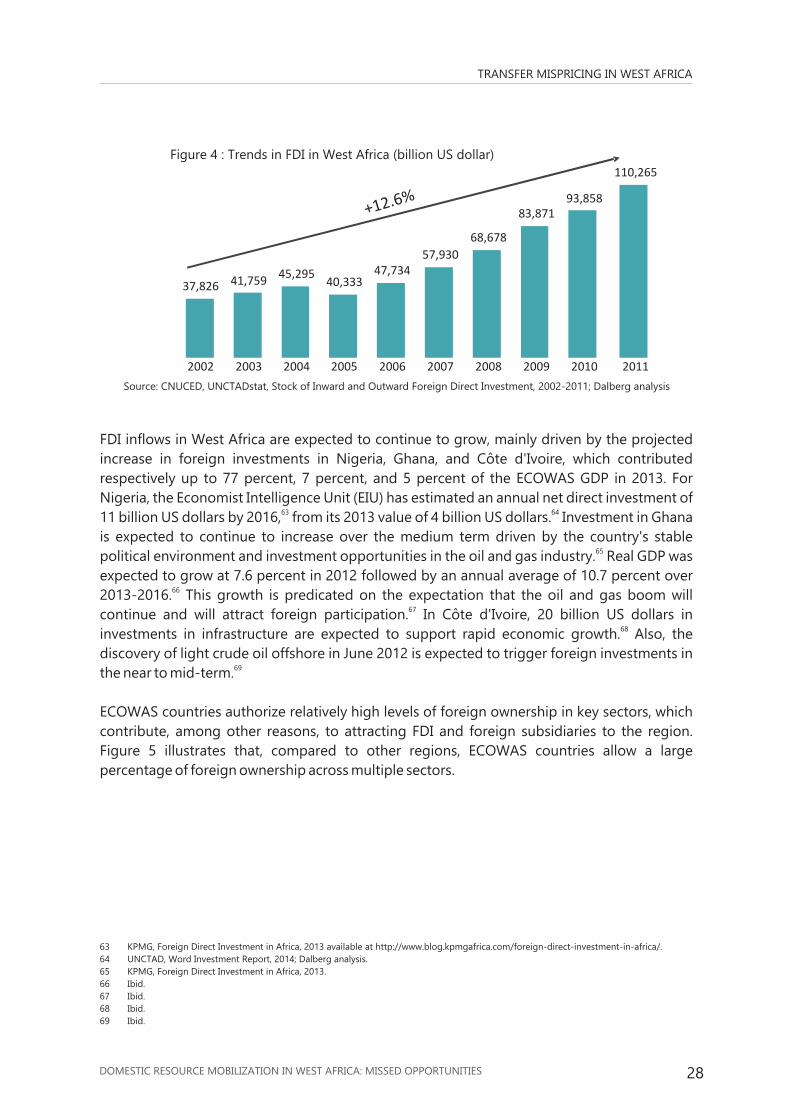

61Foreign investments continue to increase in ECOWAS, from 38 billion US dollars in 2002 to

62over 110 billion US dollars in 2011 , with an average annual growth rate of 13 percent, as

shown by the figure below.

TRANSFER MISPRICING IN WEST AFRICA

58subsidiaries of foreign firms operating in the industrial and tertiary sectors in Côte d'Ivoire, 59Nigeria, and Senegal reported 11 billion US dollars in net sales. Figure 3 highlights, for 2004,

the number and net sales of foreign subsidiaries based in Côte d'Ivoire, Nigeria, and Senegal

and the respective magnitude of their net sales compared to the countries' GDP. For Côte

d'Ivoire, for example, net sales of the 31 largest foreign subsidiaries represented 27 percent of 60the country's GDP in 2004. This trend is likely to continue throughout ECOWAS as FDI

continues to increase.

58 Not inclusive of companies operating in the financial sector.

59 UNCTAD, FDI/TNC database, Country Profiles, 2004; Dalberg analysis.

60 More recent data not available

61 CNUCED, UNCTADstat, Stock of Inward and Outward Foreign Direct Investment, 2002-2011; Dalberg analysis

62 Ibid

DOMESTIC RESOURCE MOBILIZATION IN WEST AFRICA: MISSED OPPORTUNITIES 28

110,265

93,85883,871

68,678

57,93047,734

40,33345,295

41,75937,826

+1 .2 6%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Source: CNUCED, UNCTADstat, Stock of Inward and Outward Foreign Direct Investment, 2002-2011; Dalberg analysis

Figure 4 : Trends in FDI in West Africa (billion US dollar)

FDI inflows in West Africa are expected to continue to grow, mainly driven by the projected

increase in foreign investments in Nigeria, Ghana, and Côte d'Ivoire, which contributed

respectively up to 77 percent, 7 percent, and 5 percent of the ECOWAS GDP in 2013. For

Nigeria, the Economist Intelligence Unit (EIU) has estimated an annual net direct investment of 63 64

11 billion US dollars by 2016, from its 2013 value of 4 billion US dollars. Investment in Ghana

is expected to continue to increase over the medium term driven by the country's stable 65

political environment and investment opportunities in the oil and gas industry. Real GDP was

expected to grow at 7.6 percent in 2012 followed by an annual average of 10.7 percent over 662013-2016. This growth is predicated on the expectation that the oil and gas boom will

67continue and will attract foreign participation. In Côte d'Ivoire, 20 billion US dollars in 68investments in infrastructure are expected to support rapid economic growth. Also, the

discovery of light crude oil offshore in June 2012 is expected to trigger foreign investments in 69the near to mid-term.

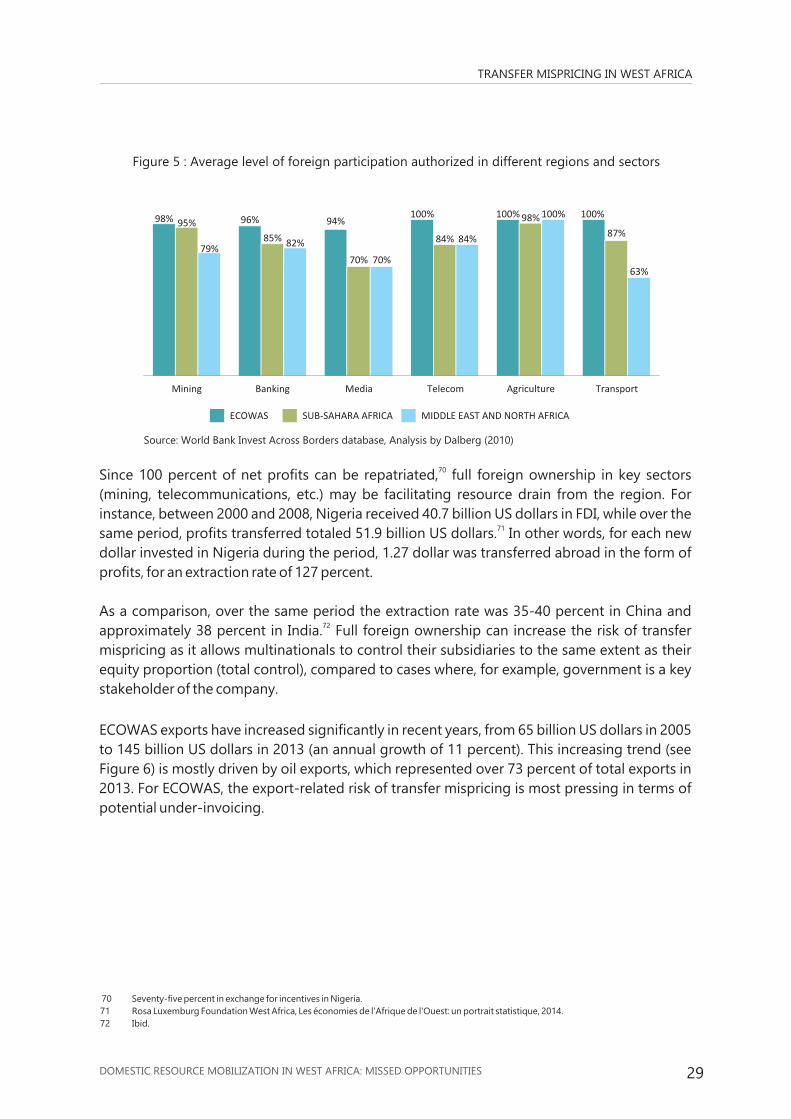

ECOWAS countries authorize relatively high levels of foreign ownership in key sectors, which

contribute, among other reasons, to attracting FDI and foreign subsidiaries to the region.

Figure 5 illustrates that, compared to other regions, ECOWAS countries allow a large

percentage of foreign ownership across multiple sectors.

TRANSFER MISPRICING IN WEST AFRICA

63 KPMG, Foreign Direct Investment in Africa, 2013 available at http://www.blog.kpmgafrica.com/foreign-direct-investment-in-africa/.

64 UNCTAD, Word Investment Report, 2014; Dalberg analysis.

65 KPMG, Foreign Direct Investment in Africa, 2013.

66 Ibid.

67 Ibid.

68 Ibid.

69 Ibid.

DOMESTIC RESOURCE MOBILIZATION IN WEST AFRICA: MISSED OPPORTUNITIES 29

Source: World Bank Invest Across Borders database, Analysis by Dalberg (2010)

ECOWAS SUB-SAHARA AFRICA MIDDLE EAST AND NORTH AFRICA

95%

79%

98% 96%

85% 82%

94%

70% 70%

100%

84% 84%

100% 98% 100% 100%

87%

63%

Mining Banking Media Telecom Agriculture Transport

Figure 5 : Average level of foreign participation authorized in different regions and sectors

70Since 100 percent of net profits can be repatriated, full foreign ownership in key sectors

(mining, telecommunications, etc.) may be facilitating resource drain from the region. For

instance, between 2000 and 2008, Nigeria received 40.7 billion US dollars in FDI, while over the 71

same period, profits transferred totaled 51.9 billion US dollars. In other words, for each new

dollar invested in Nigeria during the period, 1.27 dollar was transferred abroad in the form of

profits, for an extraction rate of 127 percent.

As a comparison, over the same period the extraction rate was 35-40 percent in China and 72approximately 38 percent in India. Full foreign ownership can increase the risk of transfer

mispricing as it allows multinationals to control their subsidiaries to the same extent as their

equity proportion (total control), compared to cases where, for example, government is a key

stakeholder of the company.

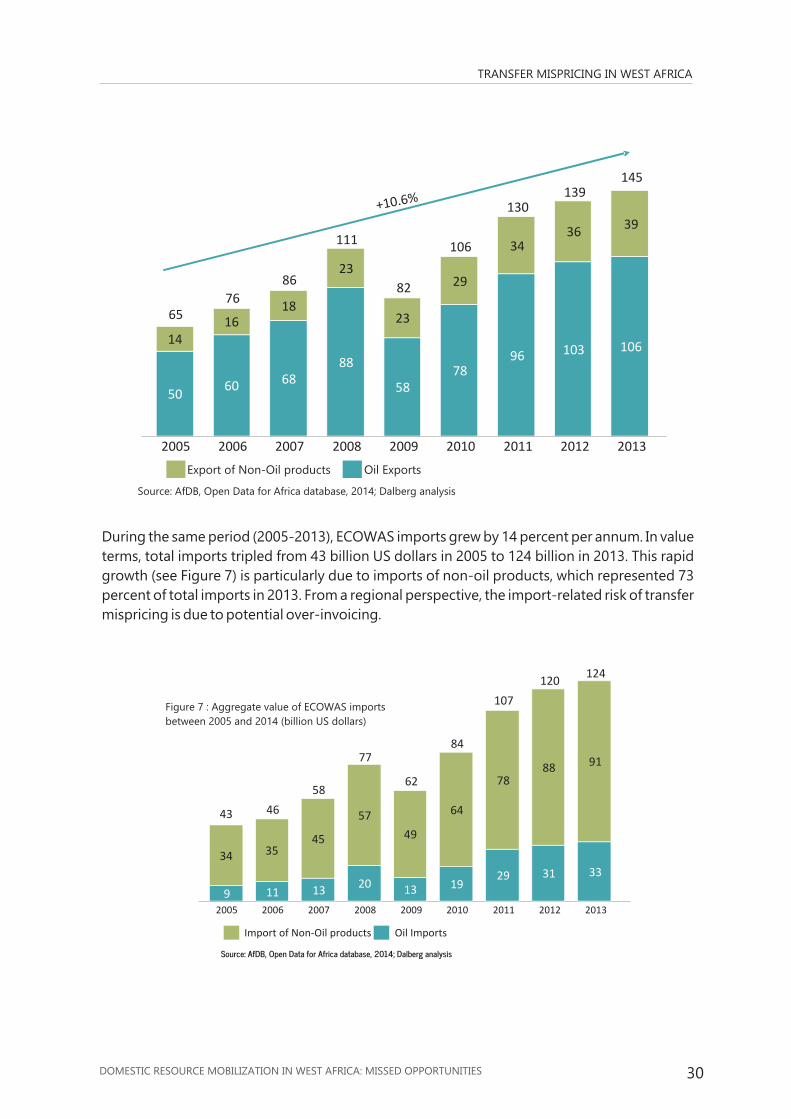

ECOWAS exports have increased significantly in recent years, from 65 billion US dollars in 2005

to 145 billion US dollars in 2013 (an annual growth of 11 percent). This increasing trend (see

Figure 6) is mostly driven by oil exports, which represented over 73 percent of total exports in

2013. For ECOWAS, the export-related risk of transfer mispricing is most pressing in terms of

potential under-invoicing.

TRANSFER MISPRICING IN WEST AFRICA

70 Seventy-five percent in exchange for incentives in Nigeria.

71 Rosa Luxemburg Foundation West Africa, Les économies de l'Afrique de l'Ouest: un portrait statistique, 2014.

72 Ibid.

DOMESTIC RESOURCE MOBILIZATION IN WEST AFRICA: MISSED OPPORTUNITIES 30

50

14

60

16

68

18

88

23

58

23

78

29

96

34

103

36

106

39

2005 2006 2007 2008 2009 2010 2011 2012 2013

+10 6. %

6576

86

111

82

106

130139

145

Figure 6: Aggregate value of ECOWAS exports between 2005 and 2014 ( billion USD)

Export of Non-Oil products Oil Exports

Source: AfDB, Open Data for Africa database, 2014; Dalberg analysis

During the same period (2005-2013), ECOWAS imports grew by 14 percent per annum. In value

terms, total imports tripled from 43 billion US dollars in 2005 to 124 billion in 2013. This rapid

growth (see Figure 7) is particularly due to imports of non-oil products, which represented 73

percent of total imports in 2013. From a regional perspective, the import-related risk of transfer

mispricing is due to potential over-invoicing.

Figure 7 : Aggregate value of ECOWAS imports

between 2005 and 2014 (billion US dollars)

Import of Non-Oil products Oil Imports

Source: AfDB, Open Data for Africa database, 2014; Dalberg analysis

34

20

57

13

49

19

64

29

78

31

88

33

91

45

13

35

119

43 46

58

77

62

84

107

120124

2005 2006 2007 2008 2009 2010 2011 2012 2013

TRANSFER MISPRICING IN WEST AFRICA

DOMESTIC RESOURCE MOBILIZATION IN WEST AFRICA: MISSED OPPORTUNITIES 31

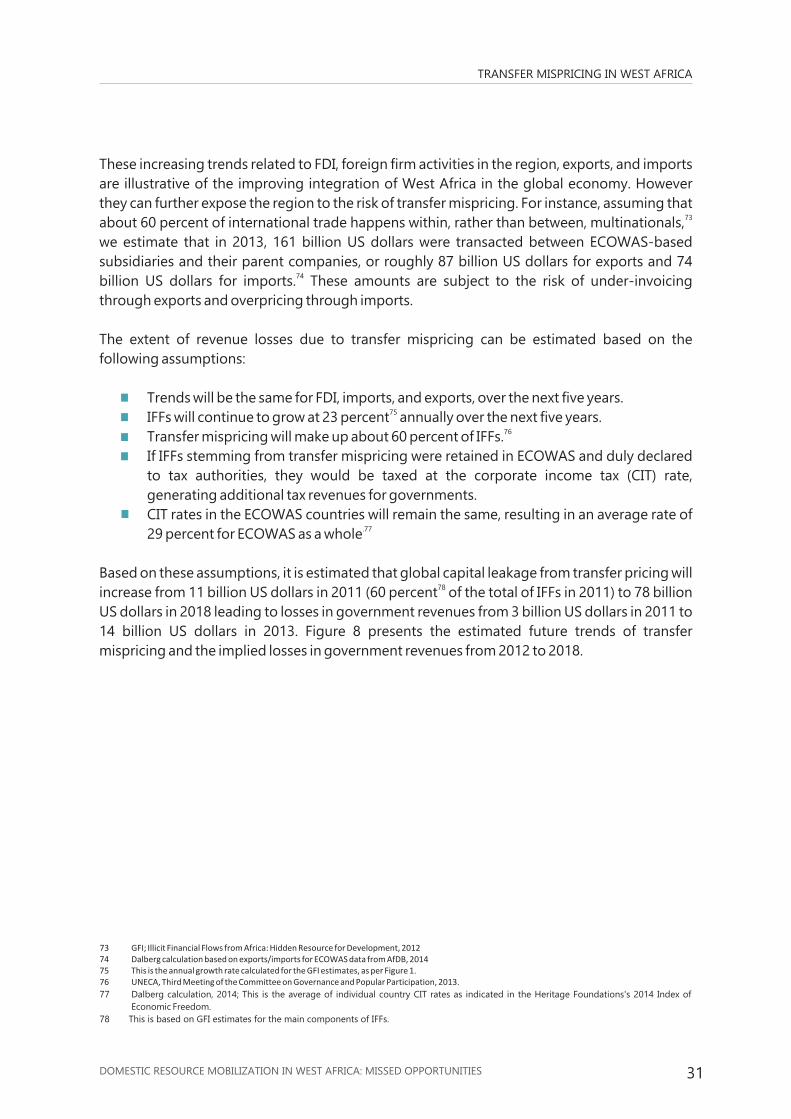

These increasing trends related to FDI, foreign firm activities in the region, exports, and imports

are illustrative of the improving integration of West Africa in the global economy. However

they can further expose the region to the risk of transfer mispricing. For instance, assuming that 73about 60 percent of international trade happens within, rather than between, multinationals,

we estimate that in 2013, 161 billion US dollars were transacted between ECOWAS-based

subsidiaries and their parent companies, or roughly 87 billion US dollars for exports and 74 74billion US dollars for imports. These amounts are subject to the risk of under-invoicing

through exports and overpricing through imports.

The extent of revenue losses due to transfer mispricing can be estimated based on the

following assumptions:

· Trends will be the same for FDI, imports, and exports, over the next five years.75· IFFs will continue to grow at 23 percent annually over the next five years.

76· Transfer mispricing will make up about 60 percent of IFFs.

· If IFFs stemming from transfer mispricing were retained in ECOWAS and duly declared

to tax authorities, they would be taxed at the corporate income tax (CIT) rate,

generating additional tax revenues for governments.

· CIT rates in the ECOWAS countries will remain the same, resulting in an average rate of .77

29 percent for ECOWAS as a whole

Based on these assumptions, it is estimated that global capital leakage from transfer pricing will 78

increase from 11 billion US dollars in 2011 (60 percent of the total of IFFs in 2011) to 78 billion

US dollars in 2018 leading to losses in government revenues from 3 billion US dollars in 2011 to

14 billion US dollars in 2013. Figure 8 presents the estimated future trends of transfer

mispricing and the implied losses in government revenues from 2012 to 2018.

73 GFI; Illicit Financial Flows from Africa: Hidden Resource for Development, 201274 Dalberg calculation based on exports/imports for ECOWAS data from AfDB, 201475 This is the annual growth rate calculated for the GFI estimates, as per Figure 1.76 UNECA, Third Meeting of the Committee on Governance and Popular Participation, 2013.

77 Dalberg calculation, 2014; This is the average of individual country CIT rates as indicated in the Heritage Foundations's 2014 Index of

Economic Freedom.

78 This is based on GFI estimates for the main components of IFFs.

TRANSFER MISPRICING IN WEST AFRICA

DOMESTIC RESOURCE MOBILIZATION IN WEST AFRICA: MISSED OPPORTUNITIES 32

79 Thin capitalization refers to securing debt financing through a holding company located in a low-tax jurisdiction. Specifically, the

subsidiary in the high-tax jurisdiction borrows from the holding company and gets to subtract the interest paid to the holding company

from its profits. This method is sometimes considered as one form of transfer pricing, but it can be abused in similar ways. (ATAF, Transfer

Pricing in the Extractives Industry: A taxing exercise for Sub-Saharan Africa, 2014).

80 GFI's data, however constructed, remain extremely conservative, as we still do not capture the misinvoicing of trade in services (rather

than the trade in goods), same-invoice trade mispricing (such as transfer mispricing), hawala transactions, and dealings conducted in bulk

cash. This means that much of the proceeds of drug trafficking, human smuggling, and other criminal activities that are often settled in

cash are not included in these estimates. It also means that much of abusive transfer pricing conducted between arms of the same

multinational corporation are not captured in our figures. (Raymond W. Baker, President Global Financial Integrity, December 11, 2013).

81 Dalberg estimates.

TRANSFER MISPRICING IN WEST AFRICA

Figure 8 : Estimates of future trends of IFFs and implied government revenue losses due to transfer mispricing

Estimated IFFs in ECOWAS from

2012 to 2018 at an annual growth

rate of 23 percent (billion US dollars)

9 23

14 34

17 42

21 52

25 64

31 78

2811

2012

2013

2014

2015

2016

2017

2018 14

11

9

7

6

5

4

Estimated losses in government revenues due to transfer mispricing for ECOWAS countries from 2012 to 2018 (billion USD

2012

2013

2014

2015

2016

2017

2018

+2

03.

%

+2

.3 0%

IFFs from other proceeds IFFs from transfer mispricing Governement revenue losses from transfer mispricing

Assumptions:

• Baseline IFF data is estimated at 18 billion US dollars in

2011 (GFI) including 9 billion US dollars from transfer mispricing

• Annual growth rate of IFF is 23 percent

• Transfer mispricing represents 60 percent of IFF

• The average CIT rate is 29 percent

• Baseline net tax revenue losses is

3 billion US dollars in 2011 (29 percent of the amount from transfer mispricing - 9 billion US dollars)

ESTIMATED TOTAL GOVERNMENT

REVENUE LOSSES BETWEEN

2012 AND 2018

$56bn

Source: Dalberg analysis

The above estimates remain conservative, as they do not consider possible higher growth rates

of FDI, imports and exports for ECOWAS, and their implications on the trajectory of IFFs and 79

transfer mispricing. Further, they do not capture other IFF circuits such as thin capitalization. 80

The conservative nature of the figures is also reflective of the limits of GFI's methodology.

Regardless of limitations, these estimates highlight the magnitude and extent of the transfer

mispricing issue on the mobilization of government revenues in ECOWAS. For example, if

required measures had been taken to effectively curb transfer mispricing, additional tax

revenues that would have been collected between 2012 and 2014 (totaling 15 billion US dollars 81

as per our estimates ), would have been sufficient to cover the financing gap (11.3 billion US

dollars in 2011) for implementing the ECOWAS Regional Poverty Reduction Strategy Paper 82

(RPRSP), and thereby would have contributed to regional integration as a means of ensuring

poverty eradication and the well-being, peace, and security of the entire population, as per the 83

stated objectives of RPRSP (see Figure 9).

DOMESTIC RESOURCE MOBILIZATION IN WEST AFRICA: MISSED OPPORTUNITIES 33

TRANSFER MISPRICING IN WEST AFRICA

Potential additional tax revenues in 2012-2018 from a more effective transfer pricing regime

Additional funding needed by ECOWAS to implement the RPRSP (2011)

Available funding for ECOWAS to implement the RPRSP (2011)

$56bn

$11.3bn

$3.7bn

Source: Dalberg analysis

As another illustration of the missed opportunity, it's worth noting that a basic ECOWAS regional

infrastructure package that would enable additional electricity supply, complete a regional road

network, and lay down fiber optic links connecting all countries to submarine cables would cost 84

1.6 billion US dollars annually if implemented over a decade.

This, too, is less than potential additional revenues from adequate transfer pricing policies and

their implementation.

A sound transfer pricing regime can contribute to effectively curbing transfer mispricing and

can mobilize additional tax revenues to fill the funding gaps for transformational projects, both

at the ECOWAS regional and national levels. However, there are challenges to establishing such

a regime and ensuring its efficacy—among them, the lack of a comprehensive and harmonized

transfer pricing legal framework in the region and the limited capacity of tax administrators.

82 The Borgen Project, ECOWAS Adopts New Strategy For Reducing Poverty, 2011 available at http://borgenproject.org/ecowas-adopts-

new-strategy-for-reducing-poverty/.

83 Ibid.

84 The International Bank for Reconstruction and Development / The World Bank, ECOWAS's Infrastructure:

A Regional Perspective, 2011.

DOMESTIC RESOURCE MOBILIZATION IN WEST AFRICA: MISSED OPPORTUNITIES 34

TRANSFER MISPRICING IN WEST AFRICA

3.2 MAIN DRIVERS OF ABUSIVE TRANSFER PRICING IN WEST AFRICA

This section aims to identify the factors that support and challenge the establishment of a

regional approach to curbing transfer mispricing. Our analysis starts by first reviewing existing

transfer pricing policies in select countries in order to identify harmonization challenges across

transfer pricing regimes and incentives for implementing such policies throughout the

ECOWAS region. This section aims to also demonstrate how the lack of a regional approach to

transfer pricing policies and implementation is a net loss to ECOWAS as a whole.

Several ECOWAS countries have in place a legal framework to monitor cross-border related-

party transactions, but the level of sophistication of such frameworks varies across countries.

The 2011 United Nations Practical Manual on Transfer Pricing for Developing Countries listed

nine ECOWAS member states out of 15 under “Countries with Emerging Regimes”: Burkina

Faso, Côte d'Ivoire, Ghana, Liberia, Mali, Nigeria, Senegal, Sierra Leone, and The Gambia. The

figure below highlights the diversity in the level of sophistication of transfer pricing regimes in

ECOWAS.

3.2.1 Assessment of transfer pricing regimes in ECOWAS

Figure 10 : Highlights of transfer

pricing regimes in ECOWAS

Guinea

Sierra Leone

Liberia

Senegal

Guinea Bisau

Cape Verde

Gambia

IvoryCoast

MaliNiger

Nigeria

Ghana

Beni

nT

ogo

Burkina Faso

Source: United Nations, United Nations Practical Manual on Transfer Pricing for Developing Countries, 2011; Transfer Pricing

Associates (TPA), Country summaries, 2013-2014; Dalberg analysis

Countries with specific legal framework and on TP and dedicated institutional mechanism

Countries with specific provisions related to TP or general anti-avoidance rules in their tax codesor revenue acts

Countries not listed amongst those with “merging Regime”

DOMESTIC RESOURCE MOBILIZATION IN WEST AFRICA: MISSED OPPORTUNITIES 35

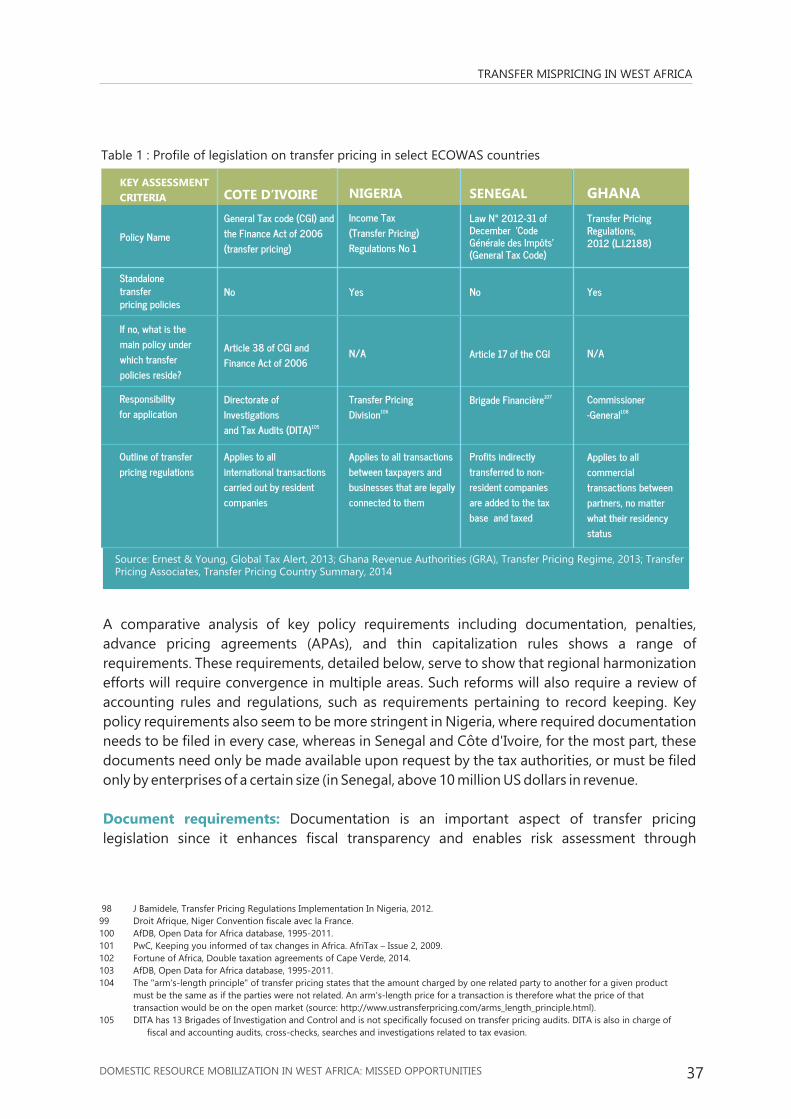

The following observations stand out:

· Only Ghana and Nigeria have developed dedicated policies on transfer pricing:

Transfer Pricing Regulations, 2012 (L.I.2188) in Ghana and Income Tax (Transfer Pricing)

Regulations No. 1 in Nigeria. The justification for these policies may stem from the

relative importance of the oil sector in government revenue, estimated at 79 percent for 85Nigeria in 2012, and the strong political will to monitor capital outflows in the oil

86sector. UNECA estimates that the oil sector contributed to over 30 percent (equivalent

87to 70 billion US dollars) of total transfer mispricing in Africa between 2000 and 2009.

Nigeria claims that it loses 5 billion US dollars in annual tax revenue due to offshore oil 88contracts. Besides Nigeria, Ghana is the only other country in ECOWAS that is

beginning to see oil contribute to government revenue, accounting for 1 percent in 89

2012. The oil sector and other extractives have also drawn particular attention from

civil society and the international community for their lack of transparency. For

example, Ghana and Nigeria were among the four countries (and the only two in Africa) 90

that piloted the Extractive Industries Transparency Initiative (EITI) in 2003. EITI focuses

on informing debates on windfall taxes, transfer pricing, production figures, and anti-91corruption. It is possible that the EITI process incentivized governments to address

related issues such as transfer pricing. This is likely to have contributed to the setting up

of dedicated transfer pricing policies in these two countries, in addition to a strong

incentive to curb the effect of transfer mispricing on government revenue. Transfer