dor ir q2'12 eng vf web12_eng_vf web.pdf · companycompanys’s effective income tax rate as a...

TRANSCRIPT

INVESTOR PRESENTATIONINVESTOR PRESENTATION

SECOND QUART E RS ECOND QUART E RS ECOND QUART E RS ECOND QUART E RA u g u s t 2 0 1 2A u g u s t 2 0 1 2

ForwardForward‐‐Looking StatementLooking Statement

Except for historical information provided herein, this presentation may containinformation and statements of a forward‐looking nature concerning the futureperformance of Dorel Industries Inc. These statements are based on suppositions andperformance of Dorel Industries Inc. These statements are based on suppositions anduncertainties as well as on management's best possible evaluation of future events. Thebusiness of the Company and these forward‐looking statements are subject to a numberof risks and uncertainties that could cause actual results to differ from expected results.Important factors which could cause such differences may include, without excludingImportant factors which could cause such differences may include, without excludingother considerations, increases in raw material costs, particularly for key input factorssuch as particle board and resins; increases in ocean freight container costs; thecontinued ability to develop product and support brand names; changes to theCompany’s effective income tax rate as a result of changes in the anticipated geographicCompany s effective income tax rate as a result of changes in the anticipated geographicmix of revenues; the impact of price pressures exerted by competitors, and settlementsfor product liability cases which exceed the Company’s insurance coverage limits. Adescription of the above mentioned items and certain additional risk factors arediscussed in the Company’s Annual MD&A and Annual Information Form, filed with thediscussed in the Company s Annual MD&A and Annual Information Form, filed with theCanadian securities regulatory authorities. The risk factors outlined in the previouslymentioned documents are specifically incorporated herein by reference. The Company’sbusiness, financial condition, or operating results could be materially adversely affectedif any of these risks and uncertainties were to materialize. Given these risks andif any of these risks and uncertainties were to materialize. Given these risks anduncertainties, investors should not place undue reliance on forward‐looking statementsas a prediction of actual results.Note: All figures are in US dollars.

2

Dorel Overview

• Marking 50 years of operations

• 3 major segments

• Juvenile products (2011 revenue ‐ US$980 million)

• Bicycles/recreational products (2011 revenue ‐ US$862 million)

• Home furnishings (2011 revenue ‐ US$522 million)

• $2.4 billion in sales annually

• 5000 employees

• Sales to 100+ countries

• Operations in 22 countries

3

Dorel’s Key BrandsDorel’s Key Brands

4

Dividend IncreaseDividend Increase

• The Board of Directors of Dorel declared an increase in the Company’s quarterly dividend to US$0.30 from US$0.15 on the Class A Multiple Voting Shares, Class B Subordinate Voting Shares and Deferred Share Units (DSU) of the Company

• The first increased dividend amount of US$0.30 per share and DSU will be payable on September p p y p6th, 2012 to shareholders of record at the close of business on August 23rd, 2012

5

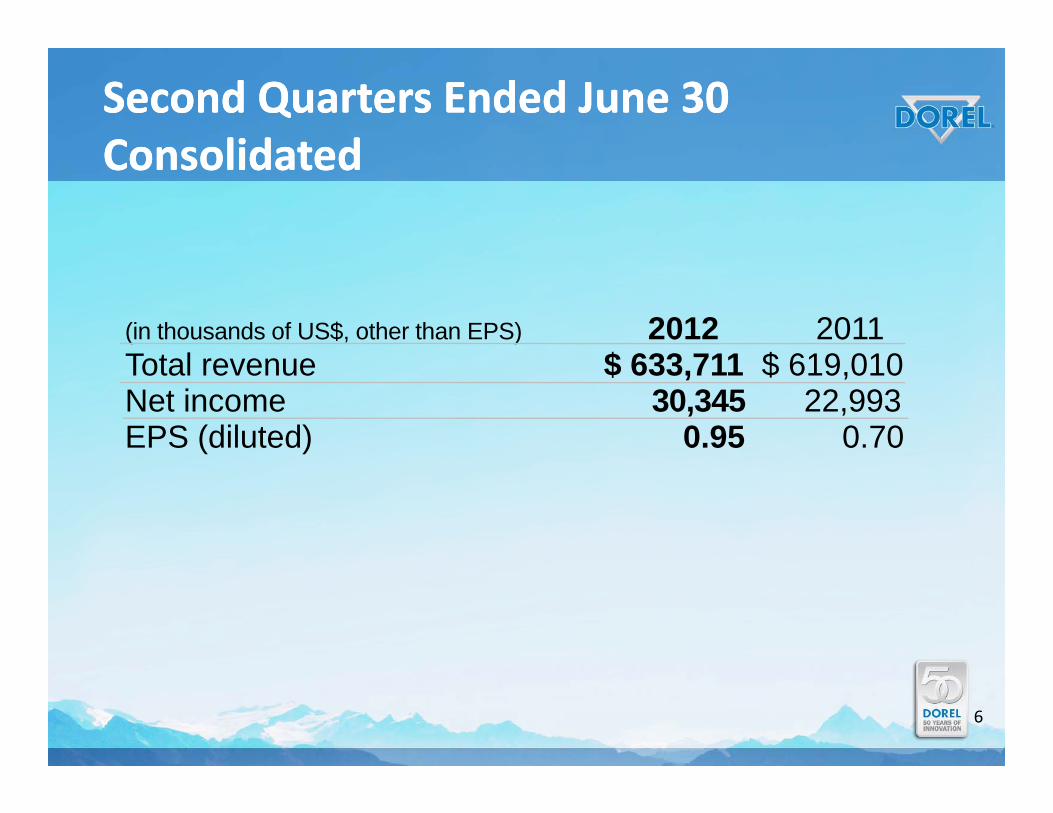

SSecondecond Quarters Ended June 30Quarters Ended June 30ConsolidatedConsolidatedConsolidatedConsolidated

(in thousands of US$, other than EPS) 2012 2011T t l $ 633 711 $ 619 010Total revenue $ 633,711 $ 619,010Net income 30,345 22,993EPS (diluted) 0.95 0.70

6

Juvenile SegmentJuvenile Segment

Second Quarters Ended June 30

(in thousands of US$) 2012 2011Total revenue $ 254,781 $ 243,965Gross profit 69,391 61,736Operating profit 17,118 14,855

7

Second QuarterSecond QuarterJuvenile HighlightsJuvenile HighlightsJuvenile HighlightsJuvenile Highlights• Positive momentum of Q4 2011 maintained

• Largest factor in earnings improvement – DJG USA;Largest factor in earnings improvement DJG USA; revenue up approximately 5%, margins benefitted from more stable costs

• Earnings increase would have been almost 40% if currencies had been consistent year‐over‐year

l h l ’ h l l l b d• Dorel Chile’s wholesale & retail operations contributed positively to profit

• Dorel Europe improved earnings when expressed in• Dorel Europe – improved earnings when expressed in Euros

• International brands – Quinny & Maxi‐Cosi performingInternational brands Quinny & Maxi Cosi performing well in U.S.

8

Penetrating New MarketsPenetrating New Markets

• Program of tuck‐in acquisitions to strategically expand global juvenile footprintexpand global juvenile footprint

•Partnering with established local operators•Brazil – Q1 2009•Brazil – Q1 2009•Chile, Peru, Argentina, Bolivia – Q4 2011P lt d Q1 2012•Poltrade – Q1 2012

9

A World Leader in JuvenileA World Leader in JuvenileI ti i N th A iI ti i N th A iInnovation in North AmericaInnovation in North America

• New G‐cell HX Superior Side Impact technology• New G‐cell HX Superior Side Impact technologydeveloped at Dorel Technical Center with specialists in race car cockpit crash protectionp p p

• Air Protect® ‐ side impact technology

• FlexTech™ Energy Management System – internalFlexTech Energy Management System internal truss design which absorbs and mitigates crash forces

• Tiny Fit™ System – removable insert providing better fit for smaller babies

10

A World Leader in JuvenileA World Leader in JuvenileLatest Development in Car Seat Safety

Maxi‐Cosi PreziMaxi Cosi Prezi11

A World Leader in JuvenileA World Leader in Juvenile

Dorel Europe• A major player – over $450 million in sales annually

• Strong brands

• Traditionally sales made to Juvenile product chains, boutiques, independents

• Building mass merchant relationships; products successfully introduced in mid‐price point categories eg Safety 1stcategories, eg. Safety 1st

• Maintaining market share in difficult economic environmentenvironment

12

Innovation Innovation ‐‐ EuropeEurope•QUINNY MOODD ‐ The ultra modern stroller that automatically unfoldsautomatically unfolds.

•QUINNY YEZZ – FeaturesQUINNY YEZZ Featureshigh‐performance plastic frame and parachute fabric seat. Weighs only 5 kg. Easily foldable to a compact package and can be carriedpackage and can be carried on your back. Recipient of several awards.

13

Recreational/Leisure SegmentRecreational/Leisure Segment

Second Quarters Ended June 30

(in thousands of US$) 2012 2011Total revenue $ 251,911 $ 249,094Gross profit 63,183 60,592Operating profit 21,606 21,274

14

Second QuarterSecond QuarterRecreational/Leisure HighlightsRecreational/Leisure HighlightsRecreational/Leisure HighlightsRecreational/Leisure Highlights•Revenue/operating profit grew marginally

E d li USD ti l i t d b• Euro decline vs USD negatively impacted revenue by approximately 2%

•Certain mass merchant customers reduced orders•Certain mass merchant customers reduced orders to lower inventory

•Cycling Sports Group gross margin dollars reduced•Cycling Sports Group gross margin dollars reduced by approximately US$2.5 million due to Euro decline – 50% of CSG revenue outside U.S.

•Apparel division (SUGOI) continuing to improve

•Cannondale’s sponsorship of pro‐cycling teamCannondale s sponsorship of pro cycling team continues to highlight brand

15

Strategic and Comprehensive PortfolioStrategic and Comprehensive Portfolio

16

Recreational/Leisure SegmentRecreational/Leisure Segment

Three distinct operating divisions

Cycling Sports Group (CSG)Cycling Sports Group (CSG)

• IBD Division

• Premium Brands• Premium Brands

• Growing dealer network

CSG l i idl t id• CSG sales growing rapidly outsideNorth America

• Innovation – continuing focus• Innovation – continuing focus

• Building Dorel’s bike business to # 1 position

17

Recreational/Leisure SegmentRecreational/Leisure SegmentP ifi C lPacific Cycle

• Mass merchants/sporting goods chains

• Bicycle parts/accessories • Full service provider – bikes, parts and accessories,branded apparel

• Brand building has enhanced Schwinn’sawareness

• 2012 marketing to target Mongoose

18

Recreational/Leisure SegmentRecreational/Leisure Segment

Apparel Footwear Group (AFG)

P f l di i i i t• Performance apparel division incorporates strong SUGOI brand

i l• New management team in place

• Division was a positive contributor in H1 to earnings

• Turnaround on track

19

Home Furnishings SegmentHome Furnishings Segment

Second Quarters Ended June 30

(in thousands of US$) 2012 2011Total revenue $ 127,019 $ 125,951Gross profit 16,574 15,603Operating profit 6,694 6,267

20

OutlookOutlook

Pre‐tax earnings for the second half of the year are expected to behigher than last year, driven by advances in the Juvenile segment.g y , y gSignificant progress in North America and a greater contribution fromLatin America will ensure that Dorel improves upon the disappointingthird quarter in 2011. Recreational / Leisure remains on track tot d qua te 0 ec eat o a / e su e e a s o t ac toexceed last year’s record earnings, whereas it is expected that HomeFurnishings’ operating profit will be slightly below last year’s levels. Asignificant tax recovery in last year’s third quarter will not re‐occur thissignificant tax recovery in last year s third quarter will not re occur thisyear. The 2012 tax rate is expected to remain in the 15% to 20% range.Input costs should remain relatively stable in the foreseeable future,however exchange rates can be volatile and are difficult to predicthowever exchange rates can be volatile and are difficult to predict.Dorel’s pre‐tax income improvement expected for the balance of theyear assumes exchange rates similar to those of today, but a furtherdecline in currencies especially the Euro could negatively impactdecline in currencies, especially the Euro, could negatively impactfuture earnings.

21

WhyWhy InvestInvest in in DorelDorel??

• A record of successfully integrated acquisitions

A f J il d Bik h D l i k l• A focus on Juvenile and Bikes where Dorel is a key player

• Strategically growing Juvenile with tuck‐in acquisitions

• A portfolio of known, premium brands

• Product development capabilities that drive growth

• Established customer relationships

• A 4% yield quarterly dividend (US$1.20/year/share)

• Strong generator of cash flow to support acquisitions

22

APPENDIXAPPENDIX

23

Financial Performance Financial Performance –– 5 Years5 Years(In thousands of U.S. dollars, except per share amounts)(In thousands of U.S. dollars, except per share amounts)

24

Growth Through AcquisitionsGrowth Through Acquisitions

• 1988 Cosco Inc (DJG)

• 1990 Charleswood Corporation

• 1994 Maxi‐Miliaan B.V. (Maxi Cosi)( )

• 1998 Ameriwood Industries

• 2000 Safety 1st Inc.2000 Safety 1 Inc.

• 2001 Quint B.V. (Quinny)

• 2003 Ampa France (Dorel Europe)• 2003 Ampa France (Dorel Europe)

• 2004 Pacific Cycle

• 2007 IGC Australia (55% interest)• 2007 IGC Australia (55% interest)

25

Growth Through AcquisitionsGrowth Through Acquisitions

• 2008 Cannondale/SUGOI

• 2008 PTI Sports

• 2009 Baby Art

• 2009 Dorel Brazil (70% interest)

• 2009 Iron Horse Bicycles y

• 2009 Gemini Bicycles (Australia)

• 2009 Hot Wheels, Circle Bikes (UK)2009 Hot Wheels, Circle Bikes (UK)

• 2011 Silfa Group (Chile, Peru, Bolivia, Argentina; 70% interest)

• 2012 Poltrade (Poland)26

Total Revenue by SegmentTotal Revenue by Segment

2011 2010

42%22%

45%22%

36% 33%

JUVENILE RECREATIONAL/LEISURE HOME FURNISHINGS

27

Geographical Distribution of Total RevenueGeographical Distribution of Total Revenue(by customer)(by customer)

7% 7%

2011 2010

61%6%

26%7%

61%6%

26%7%

US CANADA EUROPE OTHER

28

SustainabilitySustainability PhilosophyPhilosophy

• Active in sustainability on several fronts throughout all th tthree segments

• Dorel Home Products facility is FSC certified

• Cornwall RTA plant recycling for 10 years

• 98% of materials are recycled or sold98% of materials are recycled or sold

• DJG’s sustainability initiatives include zero landfill, water usage reduced by 98%; high efficiency lighting systemsusage reduced by 98%; high‐efficiency lighting systems

• Strict policy in place to ensure sustainable business ti f lipractices of suppliers

29