download the fiscal guide

TRANSCRIPT

01-2017 EN

ALD AUTOMOTIVE

VEHICLE TAXATION

2

INTRODUCTION 2

TABLE OF CONTENTS 2

BENEFITS IN KIND 3

For drivers 3

For employers 4

VAT 5

Method 1 5

Method 3 5

Method 4 6

VEHICLE REGISTRATION TAXES 7

The Brussels-Capital Region and Walloon Region 7

The Flemish Region 7

VEHICLE EXCISE DUTY 8

CO2 TAX 9

TOTAL COST OF OWNERSHIP (TCO) 10

INTRODUCTION

Want to know exactly what is happening in the field of vehicle tax? We’ve collected it all for you in this handy guide. It includes all the latest changes, such as information on the Benefit in Kind and the CO2 contribution.

Would you like further information? Go to the site of the Federal Public Service for Finances for explanations about:

The purchase of a vehicle: http://minfin.fgov.be/portail2/nl/themes/transport/vehicles-purchase.htm

http://minfin.fgov.be/portail2/fr/themes/transport/vehicles-purchase.htm

The use of a vehicle http://minfin.fgov.be/portail2/nl/themes/transport/vehicles-use.htm

http://minfin.fgov.be/portail2/fr/themes/transport/vehicles-use.htm

TABLE OF CONTENTS

3

BENEFITS IN KIND

Benefits in kind (BIK) – more frequently referred to as ‘Employee Benefits’ – are non-monetary benefits that a company or organisation gives to a staff member. These can include company cars.

FOR DRIVERS

Since 1 January 2012, the distance between the place of residence and the workplace has not been taken into account when calculating benefits in kind. Instead, it has been calculated on the basis of the CO2 emissions from the vehicle and its catalogue value.

� ‘Catalogue value’ is understood to mean ‘the catalogue price of the vehicle when in new condition’ for sale to an individual, inclusive of options and taxes paid for the additional value, without taking

into account any discount, reduction in price, or rebate.

�The base CO2 coefficient includes 5.5% for CO2 emissions of 87g/km for diesel vehicles or 105g/km for petrol, LPG or NGV vehicles. When the CO2 emissions are higher than these reference emission levels, the coefficient is increased by 0.1% per gram of CO2 above the reference point (up to a maximum of 18%). When the CO2 emissions are lower than the set reference, the coefficient is reduced by 0.1% per gram of CO2 below the reference point (to a maximum of 4%).

In 2017, the BIK cannot be less than €1,280.

The BIK is calculated using the following formula:

TOTAL CATALOGUE VALUE

(Catalogue value + options) + ((Catalogue value + options – discounts) x 0.21)

CO2 COEFFICIENT

Diesel: ((CO2 emissions - 87) x 0,1) + 5,5) / 100 Petrol: ((CO2 emissions - 105) x 0,1) + 5,5) / 100 min: 4% max 18%

BENEFIT IN KIND

Total catalogue value x CO2 coefficient x 6/7

Example:

Catalogue value of vehicle excluding VAT: € 20 000 Value of the options: € 6 000 Discount: € 5 000 CO2 emissions: 99 gr/km Fuel: Diesel

Catalogue value: (€ 20 000 + € 6 000) + ((€ 20 000 + € 6 000 - € 5 000) x 0,21) = € 30 410

CO2 coefficient: (((99 - 87) x 0,1) + 5,5) / 100 = 6,7% Min 4% -> OK Max 18% -> OK

BIK: (€ 30 410 x 6,7%) x 6/7 = € 1 746,40

4

Overview of the fiscal deductibility based on CO2 emissions:

CO2 Diesel CO2 Petrol CO2 electric Fiscale deductibility

0 g 120%

0 - 60 g 0 - 60 g 100%

61 - 105 g 61 - 105 g 90%

106 - 115 g 106 - 125 g 80%

116 - 145 g 126 - 155 g 75%

146 - 170 g 156 - 180 g 70%

171 - 195 g 181 - 205 g 60%

>195 g > 205 g 50%

Interest, costs for fixed mobile telephone systems and the CO2 tax are still 100% deductible. Fuel is still 75% deductible.

Formula for employer contribution

Employer contribution = (Benefit in kind x 17%) x Base taxation rate*

*Standard base taxation rate = 33.99%

Example

We will continue to use the earlier example of a new vehicle with a BIK of €1,694.27.

The cost for the employer can be calculated using the formula below:

(€1,694.27 x 17%) x 33.99% = €97.90

Besides this, the government decided to reduce the benefit by 6% every year, to a minimum of 70%. For the calculation, the following rule applies:

Period of time Reduction of BIK

From 0 to 12 months 100%

From 13 to 24 months 94%

From 25 to 36 months 88%

From 37 to 48 months 82%

From 49 to 60 months 76%

From 61 months 70%

FOR EMPLOYERS

As of 1 January 2012, a part of the BIK for the employee is calculated in this manner as an additional disallowed expense (non-deductible business expense) borne by the employer. This part constitutes 17% of the BIK. In 2017this part will increase to 40%

if the employer provides his employee with a fuel card.

Warning! In corporate taxes, this additional tax is counted with the already existing deductible limit for fuel costs and the disallowed expenses arising from the ceiling for the deduction of vehicle costs (with the variable depending on CO2 emissions and the type of fuel used).

The deductibility of costs (including the non-deductible VAT) that are linked to the purchase and the use of a vehicle already varies depending on the type:

�Company vehicles (light trucks): 100% deductible.

�Cars (personal vehicles): deductible depending on the level of CO2 emissions (the deductibility is still 75% for independents and liberal professions).

5

VAT

The VAT owed for the purchase or the running costs of vehicles can be recuperated if the company or organisation (or a self-employed person) is required to pay VAT.

At the end of 2010, the laws regarding VAT were changed to take into account a case from the European Court of Justice from 2009 (the Seeling case). This case specifies that the VAT on a mixed-use, non-movable item is deductible in function of its use. In Belgium, vehicles were grouped with these goods. In other words, the deductibility of the VAT linked to the purchase and use of a vehicle is limited to the professional use of the vehicle.

Examples

Professional use: 10% Private use: 90% VAT is therefore 10% deductible

BUT

Private use: 10% Professional use: 90% The deductibility of the VAT is limited to 50%.

Addendum E.T. 119.650/3 from 11 December 2012 and Addendum E.T. 119.650/4 from 9 September 2013 clarify the practical modalities that the tax requirements must make possible in order to specify the private use of a company asset, and consequently the non-deductible percentage that needs to be applied to the VAT. Specifications that were changed by Addendum E.T. 119.650/4 have been in effect since 1 January 2013.

The link between private and professional use of a vehicle can be specified through use of the following four methods:

METHOD 1

The tax payer keeps a manual log or uses an automated system (adjusted GPS system) for the administration of travel.

With this method, the use of each individual vehicle needs to be specified. A properly maintained logbook serves as the basis for determining the right to a deduction. Article 45 § 2 of the VAT legislation (detailing a maximum deductibility of 50%) needs to

be applied at all times.

Professional use, determined in accordance with this method, in relation to Year X, is valid in the rule as a means of estimating the professional use in Year X+1. For 2013, the estimation is done in retrospect, based on actual usage.

METHOD 2

This method is for tax payers who do not wish to keep a logbook. They are able to determine their professional use in a manner linked to the actual use of each vehicle. For simplification, the administration accepts the following formula:

%Private use = (((Distance between home and work x 2 x 200 work days) + 6,000km private)) x 100

Total distance

%Professional use = 100% - %Private use

Using this method, it is necessary to calculate the individual use for each vehicle. This calculation serves as the base for determining the right to deduction. Article 45 § 2 of the VAT legislation (detailing a maximum deductibility of 50%) needs to be applied at all times.

Professional use, determined in accordance with this method, in relation to Year X, is valid in the rule as a means of estimating the professional use in Year X+1. For 2013, the estimation is done in retrospect, based on actual usage.

Note: Methods 1 and 2 can be applied accumulatively within the same fleet.

METHOD 3

As the application of Methods 1 and 2 results in a considerable administrative burden in fleets with multiple vehicles, the administration accepts the professional use of assets following a general forfeiture determined as:

%Professional use = 35%

6

The tax payer is not able to combine Method 3 with another method. This method needs to be applied to all vehicles being used, for economic activity as well as for other means, and needs to be applied for a minimum of four fiscal years.

METHOD 4

Since 1 January 2012, there has been a special system for use with ‘fiscal light trucks’. For an accurate definition of the vehicle types and categories that qualify, use the following links: https://emeia.ey-vx.com/603/27399/landing-pages/et-119-650---4-nl.pdf

https://emeia.ey-vx.com/603/27399/landing-pages/et-119-650---4-fr.pdf

When fiscal light trucks are also used for non-professional means, the VAT deductibility only applies for the professional use of the vehicle. To determine this usage, two methods can be employed:

�The system for the calculation of actual usage (Method 1 as applied to vehicles).

�A general forfeiture of 85%. This method is actually only applicable if the light truck is primarily used for the transport of goods in the course of economic activity. If this is not the case, the professional use is determined using the general forfeiture: Professional use = 35%.

The old system with 100% deductibility is only applied if the tax payer is able to demonstrate that the light truck is exclusively used for professional means.

Note: Methods 1 and 4 can be used accumulatively in the same fleet of light trucks.

What falls under the right to deduction?

The right to deduction can be applied on the VAT levied on:

� the hire and purchase of a vehicle;

� the purchase of fuel;

�costs relating to repair and maintenance;

� the purchase of accessories.

Further reading

The full text of Addendum E.T. 119.650/3 from 11 December 2012 can be downloaded via the following links:http://ccff02.minfin.fgov.be/KMWeb/document.do?method=view&nav=1&id=0b4683fb-2b75-4209-a654-a2d1cee99639&disableHighlightning=true&documentLanguage=nl#findHighlighted

http://ccff02.minfin.fgov.be/KMWeb/document.do?method=view&nav=1&id=79bf7f9a-7506-4659-ba5d-0cb7a4de0793&disableHighlightning=true&documentLanguage=fr#findHighlighted

The full text of Addendum E.T. 119.650/4 can be downloaded via the following links: https://emeia.ey-vx.com/603/27399/landing-pages/et-119-650---4-nl.pdf.

https://emeia.ey-vx.com/603/27399/landing-pages/et-119-650---4-fr.pdf

It also provides information about the intended forms of transport and defines the “home-to-work commute”.

7

VEHICLE REGISTRATION TAXES

THE BRUSSELS-CAPITAL REGION AND WALLOON REGION

BIV or TMC for 1 July 2015 to 30 June 2016

hp 0 - 8 9 -10 11 12 - 14 15 16 - 17 >17

Kw 0 - 70 71 - 85 86 - 100 101 - 110 111 - 120 121 - 155 >155

Engine size 0,1 - 1,5 l 1,6 - 1,9 l 2,0 - 2,1 l 2,2 - 2,7 l 2,8 - 3 l 3,1 - 3,4 l >3,5

New 61,50 123,00 495,00 867,00 1 239,00 2 478,00 4 957,00

1 d - 1 yr 61,50 123,00 495,00 867,00 1 239,00 2 478,00 4 957,00

1 - 2 yr 61,50 110,70 445,00 780,30 1 115,10 2 230,20 4 461,30

2 - 3 yr 61,50 98,40 396,00 693,60 991,20 1 982,40 3 965,60

3 - 4 yr 61,50 86,10 346,50 609,90 837,30 1 734,60 3 469,90

4 - 5 yr 61,50 73,80 297,00 520,20 743,40 1 486,80 2 974,20

5 - 6 yr 61,50 67,65 272,25 476,85 681,45 1 362,90 2 726,35

6 - 7 yr 61,50 61,50 247,50 433,50 619,50 1 239,00 2 478,50

7 - 8 yr 61,50 61,50 222,75 390,15 557,55 1 115,10 2 230,65

There is a special form of vehicle registration tax in Belgium, known in Dutch as the Belasting op de Inverkeerstelling (BIV) or in French as the Taxe de Mise en Circulation (TMC). It is paid only once, when cars, vehicles for dual use (station wagons or estate cars), vans, mini-buses, motorbikes and other motorised two-wheel vehicles are purchased. The tax is calculated based on the capacity of the

motor, and the amount of output, expressed in fiscal horsepower (hp) or kilowatts (kW). If two motors with the same capacity deliver different amounts of power, measured in fiscal hp or kW, the highest amount will be used to calculate the rate of tax to be paid. The vehicle registration tax also takes into account the age of the vehicle, based upon the date on which it was first registered in Belgium or abroad.

THE FLEMISH REGION

Please consult the website below for the BIV / TMC rates for Flanders: https://belastingen.fenb.be/vfp-portal-pub2-web/simulatieVerkeersbelasting.html#/q/top

8

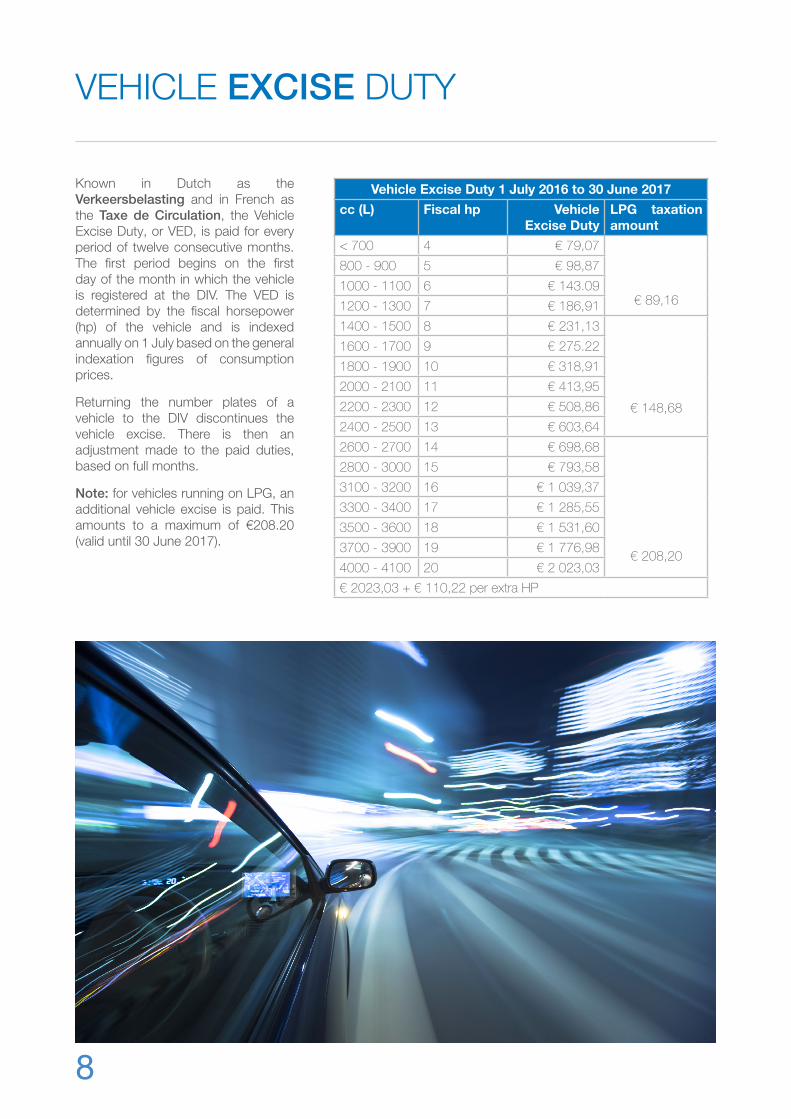

VEHICLE EXCISE DUTY

Known in Dutch as the Verkeersbelasting and in French as the Taxe de Circulation, the Vehicle Excise Duty, or VED, is paid for every period of twelve consecutive months. The first period begins on the first day of the month in which the vehicle is registered at the DIV. The VED is determined by the fiscal horsepower (hp) of the vehicle and is indexed annually on 1 July based on the general indexation figures of consumption prices.

Returning the number plates of a vehicle to the DIV discontinues the vehicle excise. There is then an adjustment made to the paid duties, based on full months.

Note: for vehicles running on LPG, an additional vehicle excise is paid. This amounts to a maximum of €208.20 (valid until 30 June 2017).

Vehicle Excise Duty 1 July 2016 to 30 June 2017

cc (L) Fiscal hp Vehicle Excise Duty

LPG taxation amount

< 700 4 € 79,07

€ 89,16

800 - 900 5 € 98,87

1000 - 1100 6 € 143.09

1200 - 1300 7 € 186,91

1400 - 1500 8 € 231,13

€ 148,68

1600 - 1700 9 € 275.22

1800 - 1900 10 € 318,91

2000 - 2100 11 € 413,95

2200 - 2300 12 € 508,86

2400 - 2500 13 € 603,64

2600 - 2700 14 € 698,68

€ 208,20

2800 - 3000 15 € 793,58

3100 - 3200 16 € 1 039,37

3300 - 3400 17 € 1 285,55

3500 - 3600 18 € 1 531,60

3700 - 3900 19 € 1 776,98

4000 - 4100 20 € 2 023,03

€ 2023,03 + € 110,22 per extra HP

9

CO2 TAX

Since 2005, employers have been required to calculate a patronal solidarity contribution on company cars. It is to be paid to the National Office for Social Security. The payments are to be made every quarter, coinciding with the payments for social security contributions for employees. Known in Dutch as the CO2 bijdrage and in French as the Cotisation CO2, this CO2 tax is calculated based on the CO2 emissions of a vehicle and a forfeit amount that relates to the vehicle fuel type.

The CO2 tax is to be paid regardless of the manner in which the vehicle is purchased, and for everything other than professional use. The burden of evidence is placed on the company or organisation that therefore needs to enforce strict rules, perform checks and apply sanctions as necessary (Car Policy).

Self-employed persons and independent company leaders in general do not need to pay the CO2 tax. The tax is indexed on 1 January every year.

New: On 1 January 2017, the index coefficient rose from 1.2267 to 1.2488. The monthly amount can therefore not be any lower than € 26.01. That is also the forfeit amount applied to electric vehicles.

The payment of the CO2 tax is strictly enforced and infringements result in the rate being doubled!

Note: The personal contribution of the employee in the financing and the use of the vehicle may not be reduced by the calculation of the CO2 tax owed on company cars.

The following formula is used for the calculation of the CO2 tax:

DIESEL ((CO2 emissions x € 9) - € 600) / 12 x 1,2488

PETROL ((CO2 emissions x € 9) - € 768) / 12 x 1,2488

LPG ((CO2 emissions x € 9) - € 990) / 12 x 1,2488

ELECTRIC 26,01 €

Example

If we continue with our earlier example in which the vehicle had the following specifications:

CO2 emissions: 99 g/km

Diesel

We calculate the CO2 tax as follows:

((99 x € 9) - € 600) / 12 x 1,2488 = € 30,28 per month

10

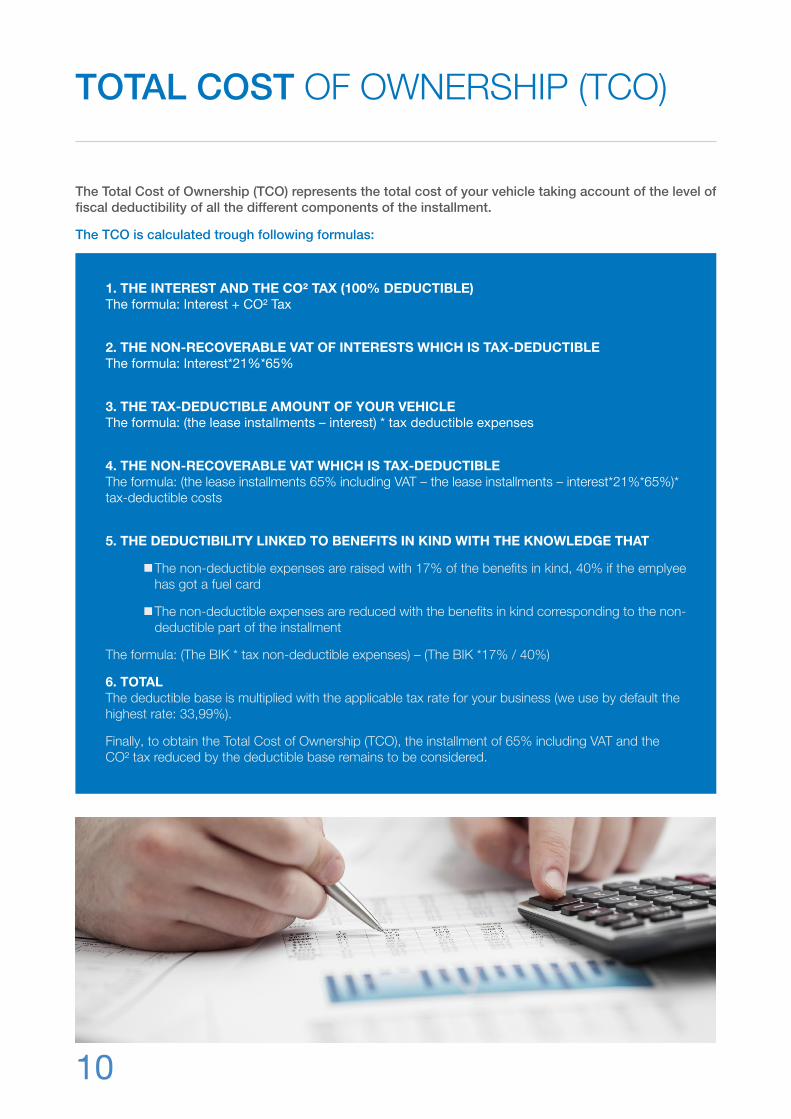

TOTAL COST OF OWNERSHIP (TCO)

The Total Cost of Ownership (TCO) represents the total cost of your vehicle taking account of the level of fiscal deductibility of all the different components of the installment.

The TCO is calculated trough following formulas:

1. THE INTEREST AND THE CO² TAX (100% DEDUCTIBLE) The formula: Interest + CO² Tax

2. THE NON-RECOVERABLE VAT OF INTERESTS WHICH IS TAX-DEDUCTIBLE The formula: Interest*21%*65%

3. THE TAX-DEDUCTIBLE AMOUNT OF YOUR VEHICLE The formula: (the lease installments – interest) * tax deductible expenses

4. THE NON-RECOVERABLE VAT WHICH IS TAX-DEDUCTIBLE The formula: (the lease installments 65% including VAT – the lease installments – interest*21%*65%)* tax-deductible costs

5. THE DEDUCTIBILITY LINKED TO BENEFITS IN KIND WITH THE KNOWLEDGE THAT

�The non-deductible expenses are raised with 17% of the benefits in kind, 40% if the emplyee has got a fuel card

�The non-deductible expenses are reduced with the benefits in kind corresponding to the non-deductible part of the installment

The formula: (The BIK * tax non-deductible expenses) – (The BIK *17% / 40%)

6. TOTAL The deductible base is multiplied with the applicable tax rate for your business (we use by default the highest rate: 33,99%).

Finally, to obtain the Total Cost of Ownership (TCO), the installment of 65% including VAT and the CO² tax reduced by the deductible base remains to be considered.

11

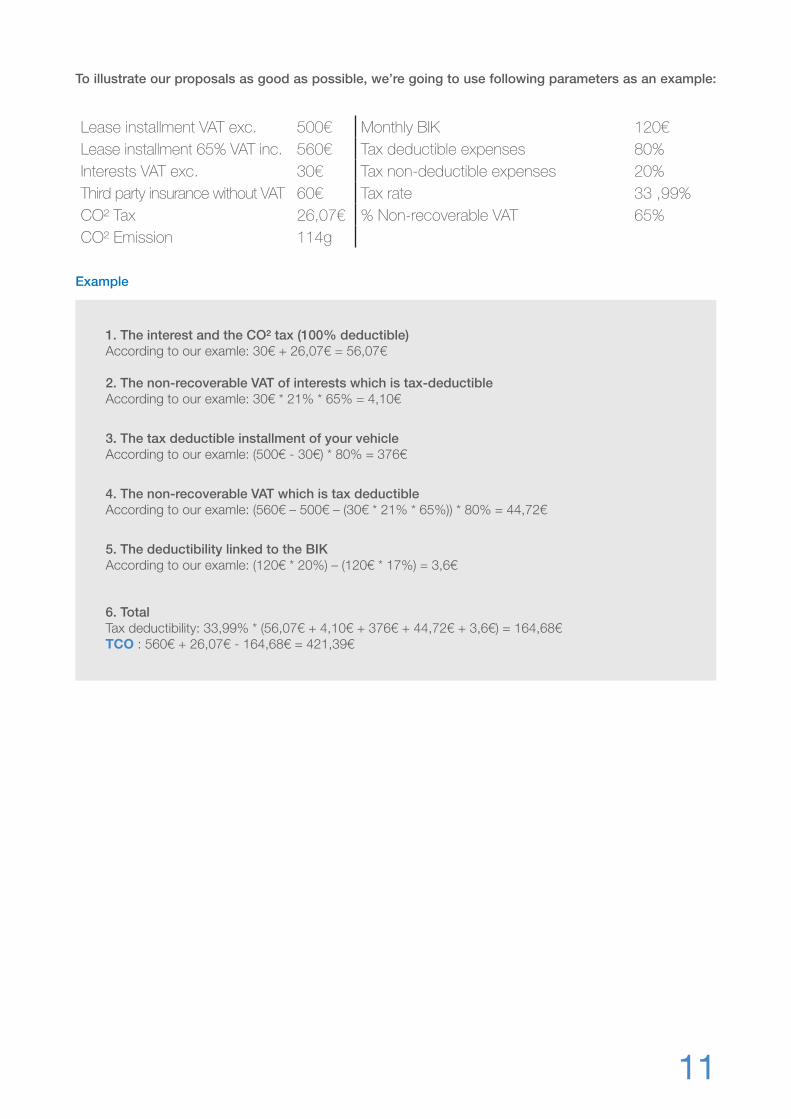

To illustrate our proposals as good as possible, we’re going to use following parameters as an example:

Lease installment VAT exc. 500€ Monthly BIK 120€Lease installment 65% VAT inc. 560€ Tax deductible expenses 80%Interests VAT exc. 30€ Tax non-deductible expenses 20%Third party insurance without VAT 60€ Tax rate 33 ,99%CO² Tax 26,07€ % Non-recoverable VAT 65%CO² Emission 114g

Example

1. The interest and the CO² tax (100% deductible) According to our examle: 30€ + 26,07€ = 56,07€ 2. The non-recoverable VAT of interests which is tax-deductible According to our examle: 30€ * 21% * 65% = 4,10€

3. The tax deductible installment of your vehicle According to our examle: (500€ - 30€) * 80% = 376€

4. The non-recoverable VAT which is tax deductible According to our examle: (560€ – 500€ – (30€ * 21% * 65%)) * 80% = 44,72€

5. The deductibility linked to the BIK According to our examle: (120€ * 20%) – (120€ * 17%) = 3,6€

6. Total Tax deductibility: 33,99% * (56,07€ + 4,10€ + 376€ + 44,72€ + 3,6€) = 164,68€ TCO : 560€ + 26,07€ - 164,68€ = 421,39€

ALD AUTOMOTIVE BELGIUM KOLONEL BOURGSTRAAT 120 1140 BRUSSELS TEL: 02 706 41 41 www.aldautomotive.be

ALD AUTOMOTIVE

ALD Automotive is the long-term vehicle rental and fleet management department of the Société Générale Group. ALD Automotive is an absolute reference on the international market of companies that are active in the area of vehicle fleet management:

■ Present in 41 countries.

■ 4,500 staff members.

■ Managing more than 1.35 million vehicles worldwide

ALD Automotive combines professionalism with quality and develops solutions for external fleet management for companies, on a national as well as an international level.