BusinessRecoveryServices

TMA Meeting – Brighton7th March 2007

BusinessRecoveryServices

Securing Value for Intangibles in TurnaroundAMA – A Different Way

7 March 2007

BusinessRecoveryServices

PricewaterhouseCoopers LLP 3

Who am I?

Karen Dukes – Director• Specialist in business reviews, exits and work-outs since 1990 in the mid-market• Leads the BRS practice in Kent, Surrey and Sussex, part of South Deal Team• Examples of assignments include: advising management of £60m turnover retail group on

management strategy for return to profitability, and expansion into foreign markets, the AMA of Accuracy International Ltd a manufacturer of precision rifles, the managed exit of an investment in a £10m turnover manufacturer, and the AMA of Zenith Entertainment Limited in 2006.

PricewaterhouseCoopers LLP 4

Agenda

1. Key Messages

2. Why are intangibles important

3. Matrix of issues

4. What is AMA?

5. Case Study

6. Questions

PricewaterhouseCoopers LLP 5

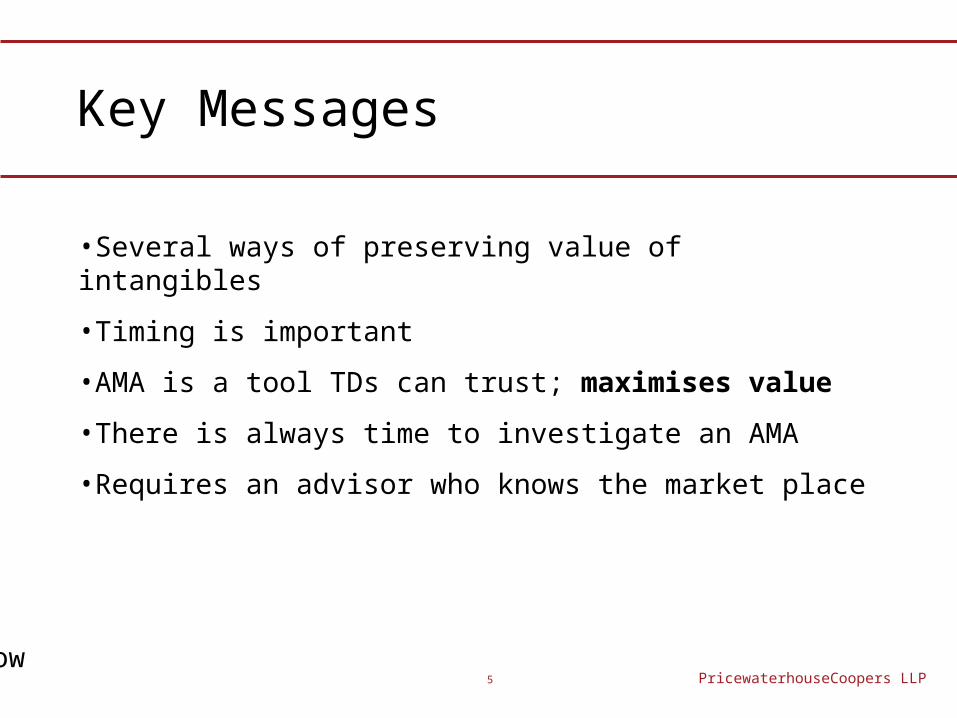

Key Messages

•Several ways of preserving value of intangibles

•Timing is important

•AMA is a tool TDs can trust; maximises value

•There is always time to investigate an AMA

•Requires an advisor who knows the market place

PricewaterhouseCoopers LLP 6

Background

Britain in 1960 Britain in 2007

Manufacturing

Heavy Industry

Mining

B2B

Media

B2C

PricewaterhouseCoopers LLP 7

The corporate life cycle©

IDEA

M&A ACTIVITY

GOING PUBLIC

RAPID GROWTH

MATURITY

Fix it

Flog it

Finish it

PricewaterhouseCoopers LLP 8

Intangible Assets: a matrix

Impairment Review

Knowhow Ownership

Commodity Or “USP”? Third Party

RiskLifetime Of Asset

Location,Location,Location

Financial Operational

Security of Asset

Commercial Reality

Brand Valuation

Relationship Management

RegistrationLicencesEvidence

PricewaterhouseCoopers LLP 9

Historical Playing Field

The Usual Game

• IP introduced to client in difficulty

• Significant intangible value

• IP recommends an insolvency appointment

• Tries to sell the company’s assets to recover the chargeholder debt

The Final Score

• Loss of intangible value

• Loss of jobs

• Loss of reputation

• An unhappy outcome

PricewaterhouseCoopers LLP 10

What is AMA?

Corporate Finance

RestructuringTax Skills

InsolvencyCorporate Finance

RestructuringTax Skills

Insolvency

Corporate Finance

RestructuringTax Skills

InsolvencyCorporate Finance

RestructuringTax Skills

Insolvency

PricewaterhouseCoopers LLP 11

When is AMA appropriate?

Potential AMA assignment

Problems trading in insolvency

Burning platformValue in parts of business but not all

Value in goodwillFew tangible assets / many

intangible

Overgeared / Cashburn

Company experiencing

difficulties

Non-core Activities

PricewaterhouseCoopers LLP 12

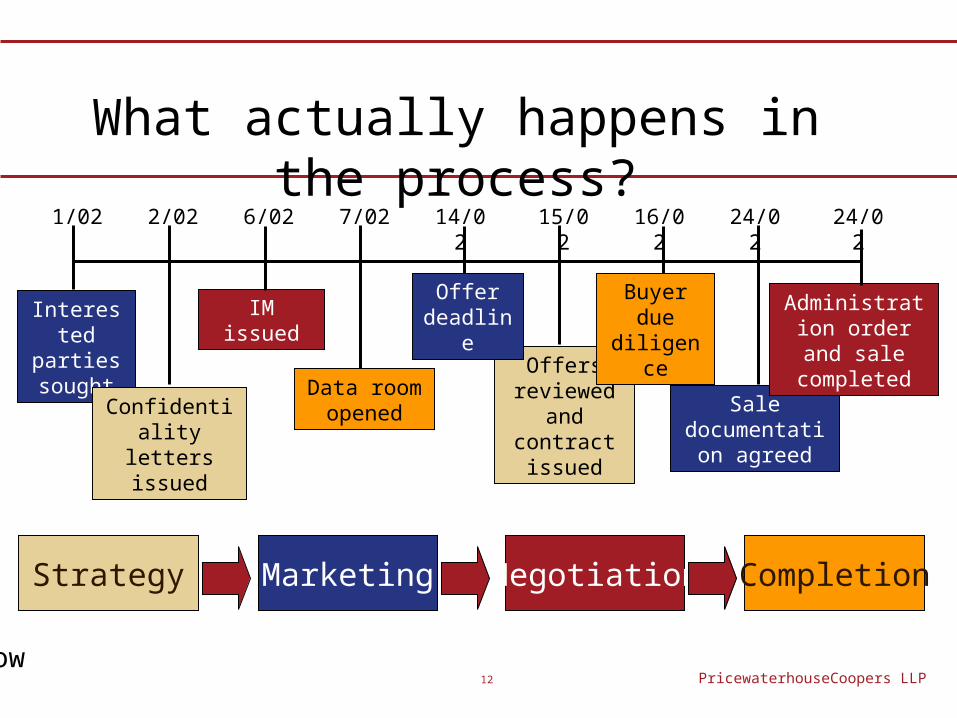

Interested parties sought

Confidentiality letters issued

Offers reviewed

and contract issued

Sale documentation

agreed

Administration order and sale

completed

IM issued

Data room opened

Offer deadline

Buyer due diligence

1/02 2/02 24/0224/026/02 7/02 14/02 15/02 16/02

What actually happens in the process?

Marketing Negotiation CompletionStrategy

PricewaterhouseCoopers LLP 13

Window – Case Study

• Group of Media Companies

• £17m turnover

• History of successful programmes

• Lack of commissioning in 2005/2006

• End of a key series

• Failed share sale

• Immediate cash crunch!

PricewaterhouseCoopers LLP 14

Window – Issues and Solutions

Potential AMA assignment

Other assets

to sell

Comfort in market

exposure

Vendor Due Diligence

Competing

purchasers

Acceleration Directors Personal risks

– wrongful trading

Nature of

contracts

PricewaterhouseCoopers LLP 15

Window – Benefits

Benefits

• Preserved intangible asset values

– goodwill

– contracts

• Robust and reliable process

• Avoids tyre kickers

• Stakeholders on course to be repaid

• Preservation of jobs

• Avoids adverse publicity, key in reputational business

PricewaterhouseCoopers LLP 16

Key Messages

•Several ways of preserving value of intangibles

•Timing is important

•AMA is a tool TDs can trust; maximises value

•There is always time to investigate an AMA

•Requires an advisor who knows the market place

This document is protected under the copyright laws of the United Kingdom and other countries. It contains information that is proprietary and confidential to PricewaterhouseCoopers LLP, and shall not be disclosed outside the recipient's company or duplicated, used or disclosed in whole or in part by the recipient for any purpose other than to evaluate this document. Any other use or disclosure in whole or in part of this information without the express written permission of PricewaterhouseCoopers LLP is prohibited.

© 2006 PricewaterhouseCoopers LLP. All rights reserved. "PricewaterhouseCoopers" refers to PricewaterhouseCoopers LLP (a limited liability partnership in the United Kingdom) or, as the context requires, other member firms of PricewaterhouseCoopers International Limited, each of which is a separate and independent legal entity.