MIK Holding IPO and

RMBS Issuance

Strictly Private & Confidential 2016

Mongolian Mortgage Corporation LLC

HQ Building of TDB, 10th Floor, Peace

Avenue 19, /14210/, 1st khoroo,

Sukhbaatar District, Ulaanbaatar, Mongolia

Tel: +976 11 328 267

Fax: +976 11 313 338

MIK HFC LLC’s Securitization Performance and RMBS Issuance

RMBS Activity Summary

Contents

Summary Activities to MIK HFC LLC…………………………….…3-6

Business and Financial Performance Indicators of MIK Group........8

MIK Holding JSC’s IPO and trading performance...........…….….9-11

RMBS’s Cover Pool Portfolio Characteristics………….….….…12-15

Sustainable Mortgage Financing Program for Middle-and-Low

Income Group Affordable Housing…………………….…………16-20

Key Transaction Parties, Scope of Works of Securitization, RMBS

Issuance Transaction Structure, Mortgage Lending and Eligibility

Criteria……………………………………......................................21-31

RMBSs Issued performance………….………………………..……...32

Page 2

Summary Activities to MIK HFC LLC.

Institutional Goal

Mongolia’s first Secondary mortgage market institution, “The

Mongolian Mortgage Corporation (MIK) HFC” LLC. was established on

October 6, 2006 by the decision of the Shareholders Meeting

represented by the Bank of Mongolia (BoM) and 10 private commercial

banks.

The main goal of “MIK HFC” LLC. is to contribute to primary and

secondary mortgage market development by issuing and selling

Mortgage-backed securities predominantly on domestic capital market,

to implement and ensure a sustainable long-term housing financing

market development, contribute to better accessibility and affordability

of home ownership, support environmentally healthy urban

development.

Page 4

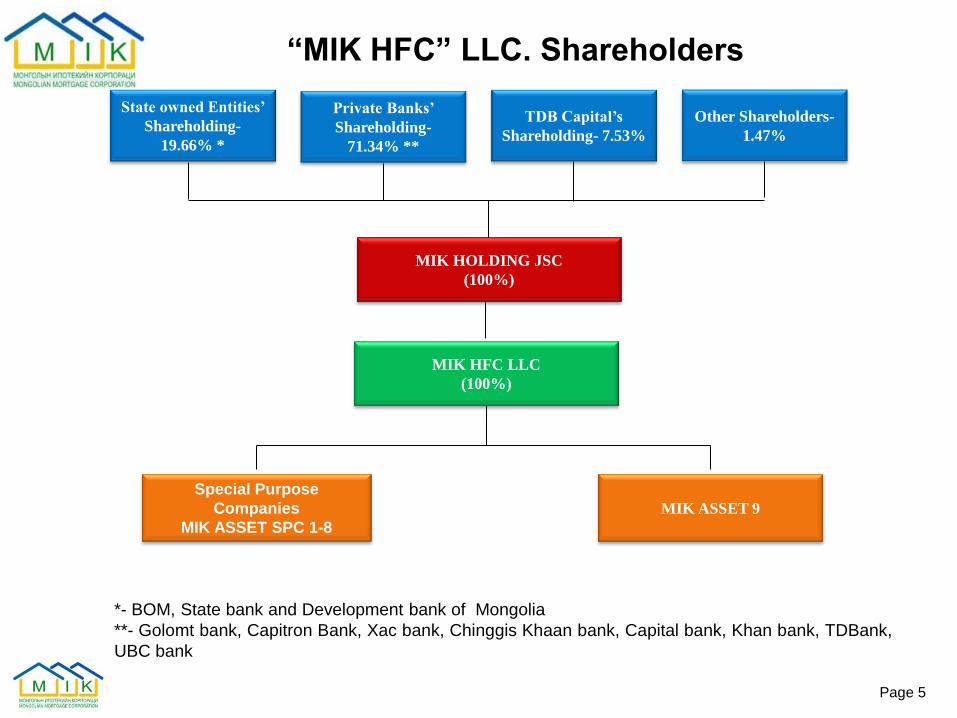

“MIK HFC” LLC. Shareholders

State owned Entities’

Shareholding-

19.66% *

Private Banks’

Shareholding-

71.34% **

TDB Capital’s

Shareholding- 7.53%

Other Shareholders-

1.47%

MIK HOLDING JSC

(100%)

MIK HFC LLC

(100%)

Special Purpose

Companies

MIK ASSET SPC 1-8

MIK ASSET 9

Page 5

*- BOM, State bank and Development bank of Mongolia

**- Golomt bank, Capitron Bank, Xac bank, Chinggis Khaan bank, Capital bank, Khan bank, TDBank,

UBC bank

Organizational Structure of MIK Holding JSC. (as of 2015.12.31)

Page 6

SHAREHOLDERS MEETING

BOARD OF DIRECTORS

Board

Secretariat

Internal

Audit

Legal and

Operations

Committee

Finance

and Audit

Committee

Nomination

and

Remuneration

Committee

Risk

Management

Committee

CHIEF EXECUTIVE

OFFICER

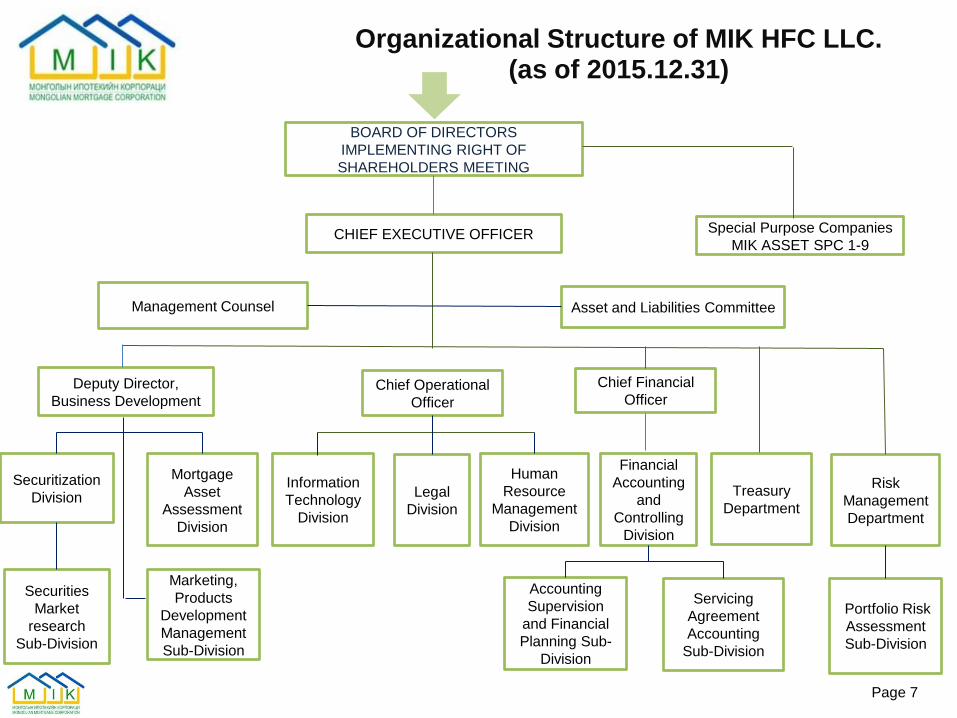

Organizational Structure of MIK HFC LLC. (as of 2015.12.31)

Page 7

BOARD OF DIRECTORS

IMPLEMENTING RIGHT OF

SHAREHOLDERS MEETING

CHIEF EXECUTIVE OFFICER

Management Counsel Asset and Liabilities Committee

Special Purpose Companies

MIK ASSET SPC 1-9

Deputy Director,

Business Development

Securitization

Division

Securities

Market

research

Sub-Division

Marketing,

Products

Development

Management

Sub-Division

Mortgage

Asset

Assessment

Division

Chief Operational

Officer

Information

Technology

Division

Legal

Division

Human

Resource

Management

Division

Chief Financial

Officer

Financial

Accounting

and

Controlling

Division

Accounting

Supervision

and Financial

Planning Sub-

Division

Servicing

Agreement

Accounting

Sub-Division

Treasury

Department

Risk

Management

Department

Portfolio Risk

Assessment

Sub-Division

Business and Financial Performance Indicators of MIK GROUP

Page 8

Key Indicators(In 000.MNT): 2013 2014 2015

Current asset, of which 355,195,470 878,796,405 2,153,815,841

Residential mortgage loan portfolio 322,893,517 826,127,184 2,017,371,457

Newly purchased mortgage portfolio,

incremental : 326,304,190 551,746,231 1,311,812,757

Nr. of Transactions for the period: 7 3 9

Total assets 356,420,135 893,948,819 2,169,174,333

Total liabilities, of which 332,246,086 847,669,235 2,050,365,056

RMBS outstanding 322,901,700 831,338,000 2,026,603,800

Total Equity 24,174,049 46,279,584 118,809,276

Total Interest Income 3,203,537 41,840,929 125,520,407

Total Interest and Coupon Expense

Total Net Interest Income

1,204,191 24,539,111 76,446,697

1,999,346 17,301,817 49,073,710

Total Operating Expenses, of which 1,209,027 5,209,222 13,474,121

Professional Service Fee Expenses¹ 205,843 4,739,124 14,103,060

HR and Administration Expenses 677,897 1,470,825 2,341,501

Total Net Earnings before Taxes 869,417 12,487,307 36,930,824

Retained Earnings after Taxes 816,230 12,105,535 35,613,988

Number of Shares 14,298,856 16,798,856 20,709,320

EPS, MNT 57 721 1,720

Key Indicators(In %): 2013 2014 2015

Equity / Total Assets 6.78% 5.18% 5.48%

Debt / Total Assets 93.22% 94.82% 94.52%

Net Profit Margin (NPM) 25.48% 28.93% 28.37%

Annual Return on Assets, (ROA) 0.23% 1.35% 1.64%

Annual Return on Equity (ROE) 3.38% 26.16% 29.98%

¹ - Servicing fee, TA fee, Legal service, Audit expenses

MIK HOLDING JSC’s IPO and trading

performance

MIK HOLDING JSC. IPO performance

Page 10

Secondary Market:

Trading information of company in the first 26 days after IPO

Offering: IPO of 3,106,398 common shares

15% of total shares

Price: MNT 12,000 per Share

Total Amount: MNT 37.28 billion

Closing date: December 24, 2015

№ Date Price Trading

High Low Open Close Volume Total Amount

1 1/19/2016 12,500 12,500 12,500 12,500 10 125,000

2 1/15/2016 12,300 12,300 12,300 12,300 369 4,538,700

3 1/13/2016 12,300 12,300 12,300 12,300 25 307,500

4 1/11/2016 12,220 12,200 12,210 12,220 303 3,702,030

5 1/8/2016 12,300 12,200 12,300 12,210 35 427,200

6 1/7/2016 12,200 12,200 12,200 12,200 2,022 24,668,400

7 1/6/2016 12,200 12,200 12,200 12,200 1,120 13,664,000

8 1/5/2016 12,400 12,100 12,200 12,180 107 1,303,300

9 1/4/2016 12,200 12,100 12,100 12,100 3,056 36,979,300

Total 7,047 85,715,430

Primary Market:

Residential Mortgage Loan

Purchase plan up to 2018

Page 11

31-Jan 29-Feb 31-Mar 30-Apr 31-May 30-Jun 31-Jul 31-Aug 30-Sep 31-Oct 30-Nov 31-Dec

Purchase portfolio by

RMBS, bill.MNT185.0 130.0 150.0 255.0 720.0

Purchase portfolio by other

funding source, bill.MNT2.0 2.0 5.0 10.0 13.5 6.7 39.2

31-Jan 29-Feb 31-Mar 30-Apr 31-May 30-Jun 31-Jul 31-Aug 30-Sep 31-Oct 30-Nov 31-Dec

Purchase portfolio by

RMBS, bill.MNT200.0 200.0 200.0 600.0

Purchase portfolio by other

funding source, bill.MNT2.5 15.0 17.5

DateTotal

amount

2017

Total

amount

2016

Date

RMBS’s Cover Pool Portfolio Characteristics,

Sustainable Mortgage Financing Program for

Middle-and-Low Income Group Affordable Housing

MIK ASSET SPC 1-7 Issued RMBSs’ Brief Summary (in Bln.MNT 2015.12.31)

№ SPCs

RMBS

Amount

(at Issuance

date)

Senior RMBS

Outstanding

balance

Junior RMBS

Outstanding

balance

Total RMBS

Coupon Paid Total coupon

paid

(cumulative)

Total RMBS

redeemed

(cumulative)

Total Mortgage

cover pool

outstanding

balance Senior Junior

1 MIK Asset One 322.90 237.14 32.29 23.57 6.76 30.33 60.24 261.84

2 MIK Asset Two 222.05 179.97 22.21 10.62 2.90 13.52 24.42 193.25

3 MIK Asset Three 324.60 274.28 32.46 12.61 3.37 15.98 23.79 296.53

4 MIK Asset Four 452.28 391.69 45.22 13.34 3.53 16.87 23.11 423.19

5 MIK Asset Five 294.34 260.06 29.43 5.86 1.53 7.39 9.36 283.09

6 MIK Asset Six 261.70 235.53 26.17 2.64 0.69 3.33 4.21 255.76

7 MIK Asset Seven 293.86 264.48 29.39 0.00 0.00 0.00 0.00 292.47

TOTAL 2,171.73 1,843.15 217.17 68.64 18.78 87.42 145.13 2,006.13

Page 13

COVER Pool MORTGAGE Portfolio

Characteristics /as of 2015.12.31/

MIK Asset

One SPC

MIK Asset

Two SPC

MIK Asset

Three SPC

MIK Asset

Four SPC

MIK Asset

Five SPC

MIK Asset

Six SPC

MIK Asset

Seven SPC

Cover Pool Mortgage Portfolio

Outstanding /Bln.MNT/: 261.84 193.25 296.53 423.19 283.09 255.76 292.47

Number of Mortgages: 6,896 5,433 6,747 9,684 5,904 5,244 5,450

Average loan size (Mln. MNT): 37.97 35.57 43.95 43.70 47.95 48.77 53.66

Interest rate (Fixed, % p.a): 8.00% 8.00% 8.00% 8.00% 8.00% 8.00% 8.00%

Remaining life to maturity (Weighted

average) (Years): 13.39 13.59 14.31 14.69 14.96 15.49 15.93

Loan-to-Value Ratio (Weighted average): 68.04% 61.40% 62.36% 62.71% 62.61% 64.16% 63.73%

Loan seasoning (Weighted average)

(Months): 36.23 34.17 28.02 27.07 22.90 18.16 13.93

Monthly Installment (Weighted average): 454,260 419,031 485,375 470,563 503,946 499,131 536,257

Geographical Concentration: 6,896 5,433 6,747 9,684 5,904 5,244 5,450

- Ulaanbaatar city : 5,754 3,812 5,130 6,588 4,687 3,988 3,970

- Rural area: 1,142 1,621 1,617 3,096 1,217 1,256 1,480

RMBS1-7 Aggregate Portfolio Characteristics (2015.12.31)

Aggregate Portfolio Characteristics Aggregate Portfolio Information

Type of Mortgage Loan asset: Residential Apartment Mortgage Loan Assets

Loan Portfolio Amount (Bln.MNT): 2,006.13

Number of Loans: 45,358

Average Loan Size (Mln.MNT): 44.23

W.A.Interest Rate (%): 8.00%

W.A.Loan Remaining Life to Maturity

(Years): 14.68

W.A.Loan-to-Value Ratio (%): 63.55%

W.A.Loan Seasoning (Months): 25.37

Average Monthly Instalment (MNT): 479,664

W.A.Debt-to-Income Ratio (%): 32.60%

Eligible Mortgage Asset Portfolio Description and Characteristics:

Page 14

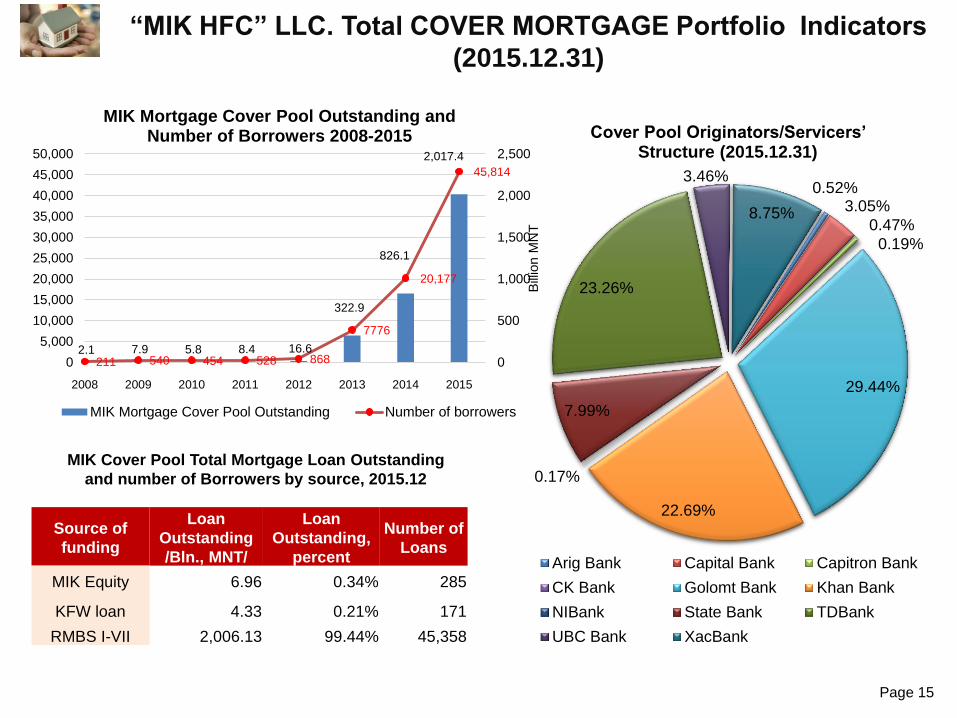

“MIK HFC” LLC. Total COVER MORTGAGE Portfolio Indicators

(2015.12.31)

Source of

funding

Loan

Outstanding

/Bln., MNT/

Loan

Outstanding,

percent

Number of

Loans

MIK Equity 6.96 0.34% 285

KFW loan 4.33 0.21% 171

RMBS I-VII 2,006.13 99.44% 45,358

MIK Cover Pool Total Mortgage Loan Outstanding

and number of Borrowers by source, 2015.12

Page 15

2.1 7.9 5.8 8.4 16.6

322.9

826.1

2,017.4

211 540 454 528 868

7776

20,177

45,814

0

500

1,000

1,500

2,000

2,500

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

2008 2009 2010 2011 2012 2013 2014 2015

Bill

ion M

NT

MIK Mortgage Cover Pool Outstanding and Number of Borrowers 2008-2015

MIK Mortgage Cover Pool Outstanding Number of borrowers

0.52% 3.05%

0.47%

0.19%

29.44%

22.69%

0.17%

7.99%

23.26%

3.46%

8.75%

Cover Pool Originators/Servicers’ Structure (2015.12.31)

Arig Bank Capital Bank Capitron Bank

CK Bank Golomt Bank Khan Bank

NIBank State Bank TDBank

UBC Bank XacBank

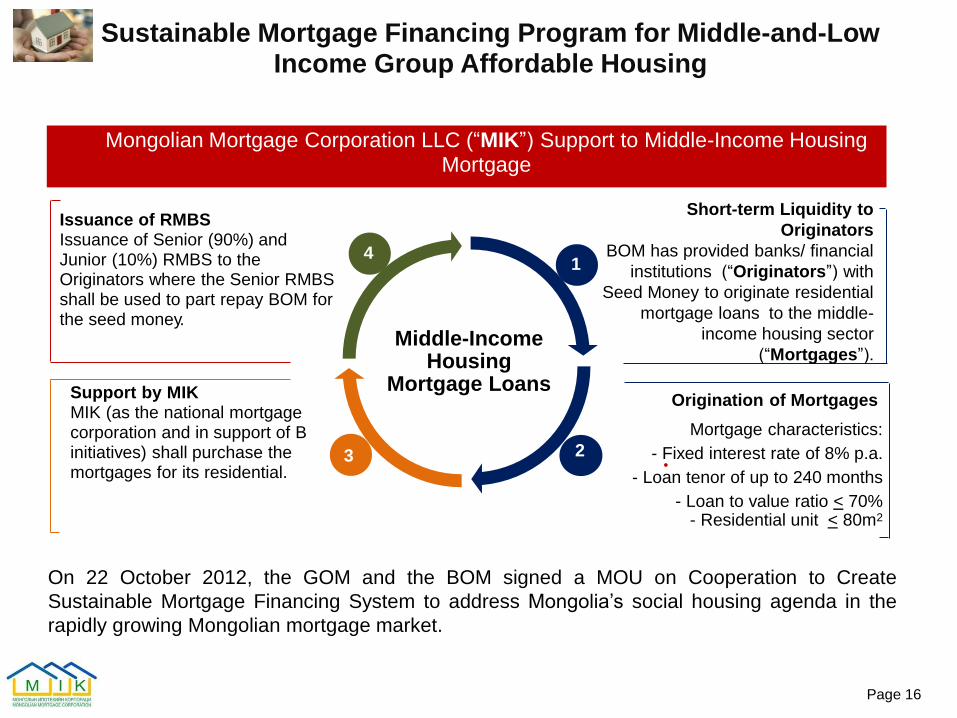

Sustainable Mortgage Financing Program for Middle-and-Low Income Group Affordable Housing

4 1

Middle-Income Housing

Mortgage Loans

2 3 •

On 22 October 2012, the GOM and the BOM signed a MOU on Cooperation to Create

Sustainable Mortgage Financing System to address Mongolia’s social housing agenda in the

rapidly growing Mongolian mortgage market.

Support by MIK MIK (as the national mortgage corporation and in support of B initiatives) shall purchase the mortgages for its residential.

Origination of Mortgages

Mortgage characteristics:

- Fixed interest rate of 8% p.a.

- Loan tenor of up to 240 months

- Loan to value ratio < 70% - Residential unit < 80m2

Issuance of RMBS Issuance of Senior (90%) and Junior (10%) RMBS to the Originators where the Senior RMBS shall be used to part repay BOM for the seed money.

Short-term Liquidity to

Originators

BOM has provided banks/ financial

institutions (“Originators”) with

Seed Money to originate residential

mortgage loans to the middle-

income housing sector

(“Mortgages”).

Mongolian Mortgage Corporation LLC (“MIK”) Support to Middle-Income Housing Mortgage

Page 16

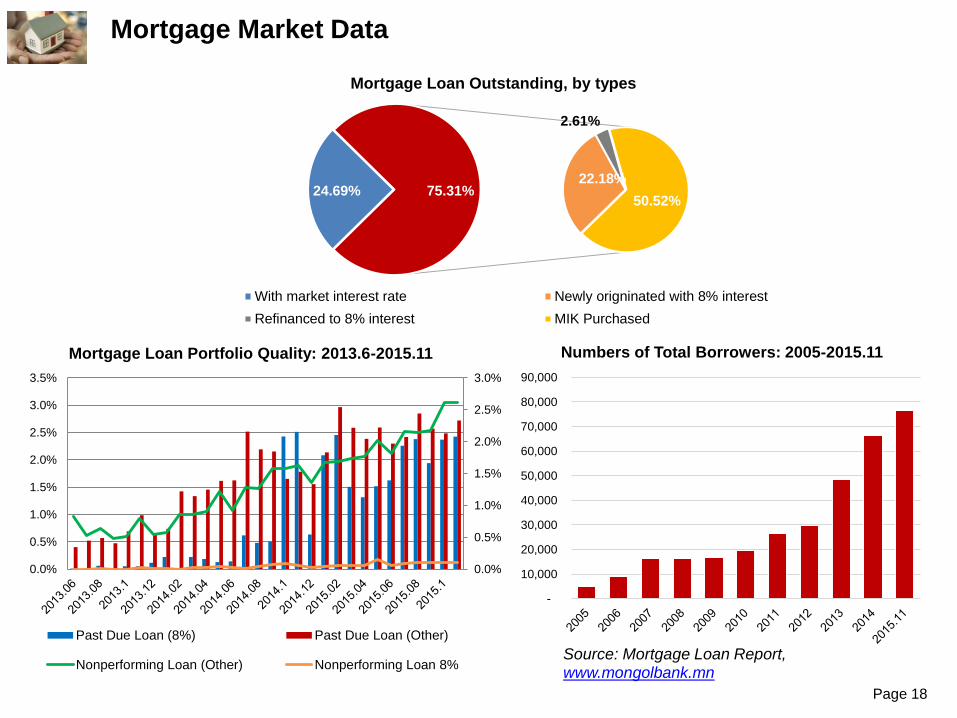

Banking Sector Mortgage Lending Market Data ( including Middle-Income Affordable Housing Mortgage Loans)

Market indicators end of periods 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015.11

Households Residential Mortgage

Loans (Bln., MNT) 30.84 74.32 164.63 217.98 226.04 333.78 656.49 845.20 1,938.95 2,844.61 3,412.93

Share of Mortgage lending market

of total bank loans outstanding, (%) 2.3% 3.3% 8.0% 8.3% 8.6% 10.7% 11.6% 12.1% 18.0% 22.8% 28.70%

Share of Mortgage lending market

outstanding at GDP (%) 0.01% 1.85% 3.32% 3.33% 3.43% 3.42% 4.98% 5.06% 10.11% 12.94% 20.31%*

Banking sector total loan

outstanding (Bln, MNT) 1,334.08 2,230.51 2,056.06 2,635.55 2,632.03 3,112.50 5,641.23 6,990.55 10,764.17 12,502.53 11,889.31

Average size of single mortgage

loan (Mln, MNT) 6.46 8.27 10.01 13.19 13.59 16.94 24.78 28.28 40.13 42.88 44.57

Total number of mortgage loans 4,774 8,984 16,444 16,522 16,628 19,700 26,491 29,887 48,320 66,334 76,583

Mortgage Market weighted

average Interest rate (%, pa.) 14.7% 17.8% 16.0% 18.7% 17.7% 16.0% 14.8% 15.3% 10.6% 10.1% 10.0%

As of November of 2015, total mortgage

loan outstanding at commercial banks

amounted MNT3,413 Billion, Number of

total mortgage borrowers was 76,583

middle-income housing mortgages with 8%

p.a interest rate reached MNT 2,570.2

Billion, constituting 75.31% of total

mortgages outstanding in the banking

sector.

Source: Mortgage Loan Report, www.mongolbank.mn

National Statistic Report, Page 17

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

0.0

500.0

1,000.0

1,500.0

2,000.0

2,500.0

3,000.0

3,500.0

4,000.0Mortgage market trend : 2005-2015.11

Mortgage market debt outstanding (billion MNT)

Mortgage market share of Systemic Loan market , %

* - as of third quarter of 2015

Mortgage Market Data

Page 18

Source: Mortgage Loan Report, www.mongolbank.mn

24.69% 22.18%

2.61%

50.52% 75.31%

Mortgage Loan Outstanding, by types

With market interest rate Newly origninated with 8% interest

Refinanced to 8% interest MIK Purchased

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

Mortgage Loan Portfolio Quality: 2013.6-2015.11

Past Due Loan (8%) Past Due Loan (Other)

Nonperforming Loan (Other) Nonperforming Loan 8%

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

Numbers of Total Borrowers: 2005-2015.11

Housing Price Index as of 2015.IVQ

Source: “Tenkhleg zuuch” LLC - Realtor and Research Company Page 19

1.00 1.01 1.02 1.02 1.02 1.05

1.06

1.12 1.13

1.18 1.19 1.20

1.21

1.24 1.26 1.25

1.23 1.25 1.25 1.24

1.23 1.21

1.20 1.19 1.18 1.17 1.17 1.17 1.17

1.14 1.12 1.12

1.09 1.07 1.06 1.06

1.00

1.05

1.10

1.15

1.20

1.25

1.30

HPI (pricing index commenced, as of January 2013)

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

1/1

/20

14

2/1

/20

14

3/1

/20

14

4/1

/20

14

5/1

/20

14

6/1

/20

14

7/1

/20

14

8/1

/20

14

9/1

/20

14

10/1

/20

14

11/1

/20

14

12/1

/20

14

1/1

/20

15

2/1

/20

15

3/1

/20

15

4/1

/20

15

5/1

/20

15

6/1

/20

15

7/1

/20

15

8/1

/20

15

9/1

/20

15

10/1

/20

15

11/1

/20

15

12/1

/20

15

Annual changes of UB-HPI (%)

Economic and Social Impact of Affordable Housing Program

Page 20

Middle-and low-income households’ mortgage monthly debt obligation pressure eased,

households consumption pattern and behavior modified

Banking sector’s asset and liabilities duration mismatch and gap risks reduced and

partly mitigated

Banks’ capital requirement compliance pressure eased

Banks’ traditionally offered services and products income sources enhanced through

diversification of off balance contingent asset management products

Banks’ short term liabilities structure diversified and local currency deposit average cost

of funding decreased, compared with conventional retail time deposit cost of funding

Private labeled debt instrument, RMBS newly developed and introduced in securities

market, supporting the diversification and availability of capital market tradable

products

Construction developers market and urban areas real estate market development

supported leading to urban households better quality of life in Ulaanbaatar city and

provincial centers

Households personal wealth accumulation supported, construction and infrastructure

sectors employment and productivity maintained sustainably in adverse cycle of

commodity driven economic growth slowdown period

Key Transaction Parties, Scope of work of

Securitization, RMBS Issuance Transaction Structure,

Mortgage Lending and Eligibility Criteria

Financial Securities Regulator

Key Transaction Parties & Scope of Work of Securitization Regulators & Banks

Key roles and responsibilities of transaction parties include, without limitation, the following:

Pre RMBS Issuances Post RMBS Issuance

Financial Regulatory Commission

Bank of Mongolia

Banks

Originators

Servicers & Junior RMBS Holder

Junior RMBS Holder.

Collection and transfer of amounts

collected from the Mortgages to a

Collection Account for a Servicer Fee (2%

of collected amount).

Recovery of defaulted Mortgages.

Provision of periodic Servicer Reports.

Keeping of records, books, accounts, etc.

Originators of Mortgages

Origination of Mortgages meeting

BOM’s Residential Mortgage Loan

Financing Procedure 2013.

Sale of identified Mortgage Pools

(meeting Eligibility Criteria) to MIK-SPC.

Sale on a “willing buyer willing seller”

basis to achieve accounting true sale.

Part repayment of soft loans via RMBS.

Senior RMBS Holder

Senior RMBS holder (Senior RMBS shall be

transferred to BOM as part repayment of the

soft loans).

Regulation of capital treatment framework

for the RMBS investors.

Regulator & Seed Money Provider

Regulates Mongolia’s banking system.

Key driver in the provision of middle-

income housing via soft loans to banks for

the origination of Mortgages.

Refer to BOM Residential Mortgage

Loan Financing Procedure 2013.

Formulating proposals to improve the legal environment of the Securities Market

Developing rules, criteria, procedures, regulation, methodology, and recommendations

within the aim of providing stability of the securities market). Regulatory approval for issuance of securities, including RMBS.

Page 22

Key Transaction Parties & Scope of Works of Securitization– MIK

Key roles and responsibilities of transaction parties include, without limitation, the following:

Key Roles Key Benefits & Considerations

Financial Agent / Security Trustee

Responsible for the administrative aspects

of the security.

Making distributions to the secured lenders

on enforcement.

Ensures the beneficial rights of the security

package to existing and/or new investors.

Potential Conflict & Mitigating Factors

Potential conflict of interest given that MIK

is responsible for the investments of cash

flows and acts in a fiduciary role in the

interest of the bondholders.

Mitigated by appointment of two (2)

independent directors (2 out of 3).

MIK-SPC as Issuer

Wholly owned subsidiary to purchase the

Mortgage Pools from multiple Originators

(banks).

Approval from FRC for RMBS issuance.

Issuance of Senior and Junior RMBS as

purchase consideration.

Ring Fencing of Mortgage Pool

Issuance from a special purpose vehicle

will ensure the segregation of mortgage

pool from MIK’s other assets.

No cross default between issuances.

Potential consolidation under IAS 39.

Administrator & Transaction Administrator

Periodic analysis of the Mortgage Pool’s performance e.g. default analysis.

Preparation and reconciliation of collections with the Servicer Reports.

Verification of amounts due to the various parties.

Source of Income / Information

Fixed annual fee on the outstanding

mortgage pool.

Historical analysis to enable assessment

of pool for future issuances.

Monthly reporting requires robust tracking

system

MIK SPC

MIK

Page 23

RMBS Issuance Transaction Structure

BOM provides 6 to 9 months’ unconventional below the market rate priced loans at 4% p.a. to eligible Banks.

1

Borrowers (Obligors)

2 Middle income mortgages

(Founder) Originators to provide middle income housing mortgages at 8%

p.a. to eligible borrowers based on

pre-determined eligibility criteria.

@ 8% 2

Banks shall sell their respective pools of mortgages to MIK-SPC.

3

Banks 1

MIK-SPC to issue RMBS in Senior

and Junior tranches as purchase

consideration to respective Banks.

4

Soft loans

@ 4%

Placement

of Senior

tranche The Junior

return of

subscribed

tranche with a target

10.5% p.a. will be

by respective Banks

Subscribed by the Originators

5 Investors

5a whilst the Senior tranche with a

target return of 4.5% p.a. shall be

sold to BOM. Bank of Mongolia Subscribed by

the Originators

90% Senior

10% Junior

Banks / Financial Inst. (Originator / Servicer)

3

MIK-SPC (RMBS Issuer)

Commingled

Mortgage Pool Sale of

Mortgage Pool 4

5b

Issuance

of RMBS

Page 24

RMBS Issuance Targeted Planning and Execution

Due

Diligence

• Data collation of pool analysis by economic parameters;

• To conduct secondary analysis on each loan account;

• To illustrate financial model and cash flow assumptions;

• Financial and legal Due Diligence.

Pre

Issuance process

• Establishment of the Issuer;

• Submission of RMBS documents to FRC for approval;

• Review over transaction documents;

• Opinion on legal & accounting true sale.

RMBS Issuance

• Regulatory approval for issuance;

• Review and finalization of transaction docs;

• Legal opinion on meeting pre issuance terms and conditions;

• Issuance of Senior RMBS and Junior RMBS as purchase consideration.

Transfer of Senior RMBS to BoM;

Execution of purchase contract for Mortgage pool (Transaction

Administrator Agreement, Trust Deed Agreement, Security Agent

Agreement package, Servicing agreement, etc);

Page 25

Performance

and Reporting (post RMBS)

Legal Documentation and Parties to RMBS Issuances

26

Clearing

House

Originator/

Servicer

(banks)

SPC

(Issuer)

MIK

SPA Servicing

agreement Subscription

agreement

Clearing

House

agreement Transaction

Administration

agreement

Trust

Deed

Agreement

Security

Documents

Page 26

Legal Contacts, Agreements, Documents and Fee Structure

# Types of Agreements Parties Servicing Fee

1 Sale and Purchase

Agreement

“MIK ASSET SPC ” LLC

and Banks

A purchase price equal to the principal amount

outstanding on such Mortgage Asset. No

purchasing fee.

2 Servicing Agreement,

Trust Account Agreement

“MIK ASSET SPC ” LLC

and Banks

Equal to 2.5% of the quarterly total collections

(interest, principal and recovery) and is

payable quarterly.

3 Transaction Administration

Agreement

“MIK ASSET SPC ” LLC

and MIK

Equal to 0.5% of beginning balance of the

Mortgage Pool every quarter is payable

quarterly.

4 Trust Deed “MIK ASSET SPC ” LLC

and MIK

Quarterly payable fee included in Transaction

Administrator’s fee of 0.5% p.a.

5 Security Agent Documents “MIK ASSET SPC ” LLC

and MIK

Quarterly payable fees included in Transaction

Administrator’s fee of 0.5% p.a.

6 Clearing house agreement “MIK ASSET SPC ” LLC

and SCHCD

SCHCD accounting and ownership registration

fee is equal to 0.045% (0.05%).

7 External auditor, legal

advisor and other financial

institutions

“MIK ASSET SPC ” LLC

and other institutions

It’s included in Transaction Administration

agreement on actual contracted amount,

subject approval by SPC’s BOD and

Shareholders annually.

Page 27

Newly originated Residential mortgage loans shall comply to the following:

Mortgage Lending Criteria of the Originators (1)

The Originators disburse mortgage loans in compliance with lending criteria to borrowers defined in “Mortgage

Loan Financing Procedure” approved by the Bank of Mongolia procedure dated 14.06.2013.

the Obligor should be a Mongolian citizen, at least 18 years old and has full legal capacity;

Obligor must not have any delinquent loans, unpaid balances, or any other outstanding obligations to banking

and financial organizations under the court’s decision.

None of the obligor’s family member has any outstanding loan under the Government of Mongolia’s “Civil

Servant Mortgage Loan Program” or “100,000 Housing Program” (which is publicly referred to the Mortgage Loan

Program with the interest rate of 6%);

The Obligor has to be covered with Life Insurance during the loan term

If the applicant is an employee of a company which has co-operation contract with State bank or a self-employed

good customer.

The applicant must currently be in employment for more than twelve (12) months or must provide information

about previous employment if the current employment is less than 12 months.

The prepayment should be placed in State bank’s account or escrow account of the bank.

Debt to income ratio of Obligors is not greater than 45% of the income before tax;

Page 28

Refinanced, repriced mortgage loans shall meet the following requirements:

Refinancing amount is not greater than outstanding loan of the previous mortgage

The applicant for refinancing should be paid pre-originated residential loans at the rate of not less than 2 by credit

history rating;

Refinancing mortgage loan shall be fully amortizing with a fixed interest rate;

Not less than 30% of the prepayment must be paid by the applicant for refinancing and the amount refinancing will

be determined at 30% of the prepayment amount which had been fully paid. The property price will be considered

as the current price of purchased apartment.

If there is no pledge certificate in pre-originated loan, the pledge certificate must be replaced.

If there is no coverage of obligor’s life insurance and property insurance in pre-originated loan, life and property

insurance must be recovered.

Income source of the applicant for refinancing must not be less than in the level of origination and the applicant

must have fixed monetary income.

Requirement for Collateral

Mortgage Lending Criteria of the Originators (2)

The collateral must be a residential apartment located in Mongolia.

Newly built apartment 100% completed or old apartment commissioned earlier.

The total size of residential apartment shall not exceed 80 sq. meters according to the

MNS 6058:2009 standard “Methodology of measuring built up area size in residential

apartment”.

Second collateral pledged for the 30% down payment of an mortgage loan should be

borrower’s entitled property.

Collateral(s) must be insured during the lifetime of the mortgage against property damage

No outstanding claims, property ownership should be free from third party encumbrances,

collateral property’s lien must be registered in real estate registration organization.

Pledged collateral must be certified by real estate registration issued certificate of title.

Page 29

Property

insurance

Personal

accident

insurance

Mortgage Insurance Coverage Details (3)

Any damages cause from fire, electric power, plumbing, natural disaster, household, and third party’s intentional or unintentional act.

Page 30

Obligor and co-obligor’s death in any cause. Occupational diseases and industrial accidents and

conditions. Obligor or co-obligor lost 70% or more of his capability due

to natural disaster, third party’s intentional act or other accidents.

Insurance

type

Insurance coverage /Risk/

Insurance fee

0.11-0.13%

0.12-0.18%

Extension of

insurance

duration

Insurance duration is one year. Insurance officer and bank officer have a

responsibility to renew the obligor’s insurance duration.

Amount

estimating

insurance fee

Outstanding loan principal+ Annual interest payment

Eligibility

Criteria

(Financial 9)

Eligibility

Criteria

(Legal 9)

Mortgage Pools’ Securitization Legal /Financial Eligibility Criteria

MIK proposes the following eligibility criteria for the Mortgage Pools for its inaugural RMBS transaction,

subject to further discussion with BOM and the Originators:

MIK-SPC shall purchase the Mortgage Pools on a “willing buyer willing seller” basis (fair value) to be settled via the issuance of RMBS to the Originators (and BOM).

All amounts required to be paid for the purchase of the mortgage property have been paid.

Advanced and repayable in Mongolian Togrogs (“MNT”).

Amount of the financing has been fully disbursed.

Settlement of amounts due from obligors via monthly installments.

Obligors be in employment for more than 12 months with proof of income at origination.

No outstanding obligation to MIK at point of sale.

Not classified as non performing loan (> 91 days in arrears) within the last 24 months.

At least 4 months since date of full disbursement (“Seasoning”).

Paid up to date (current) at point of sale and for the past 4 months.

Legally owned by the Originators free from encumbrances.

Registered at the State Registry with registration certificate under Mongolian law.

Legal, valid and binding obligation of the obligors and enforceable.

Originators not prohibited by law from effecting a transfer of the mortgage transactions.

First ranking pledge having priority to all secured, guaranteed and unsecured claims.

Created in accordance with the Guidelines of BOM on mortgage lending and procedure.

Originator has not granted any additional facilities against the mortgage property.

Obligor must be Mongolians citizen

Obligor has not exercised or indicated an intention to exercise the option for prepayment

Page 31

RMBS issued performance

№ Issue Months Issuer Issue size

(bill. MNT)

1 2013.12 MIK SPC 1 322.90

2 2014.07 MIK SPC 2 222.05

3 2014.11 MIK SPC 3 324.60

4 2015.01 MIK SPC 4 452.28

5 2015.05 MIK SPC 5 294.34

6 2015.08 MIK SPC 6 261.70

7 2015.12 MIK SPC 7 293.86

TOTAL AMOUNT 2,171.73

Page 32

THANK YOU FOR YOUR ATTENTION!

Mongolian Mortgage Corporation LLC

HQ Building of TDB, 10th Floor,

Peace Avenue 19, /14210/,

1st khoroo, Sukhbaatar District,

Ulaanbaatar, Mongolia

Tel: +976 11 328 267

Fax: +976 11 313 338