1Q2018 Financial Results

25 April 2018

2

Agenda

Key Financial Highlights

Market Performance

Conclusion

Appendices

3

Key Financial Highlights

Financial Highlights for 1Q2018

Operating Revenue

Operating Expenses

4

Financial HighlightsHighest 1st quarter PAT since 2007

Operating revenue increased due to higher Securities Trading, Listing and Issuer Services and

Depository Services revenue. The increase was partially offset by lower revenue from Derivatives

Market.

ROE and Cost to Income Ratio both improved by 4 and 3 percentage points to 30% and 42%

respectively.

1Q2018 vs. 1Q2017:

Financial Items 1Q2018

1Q2018

vs.

1Q2017

1Q2018

vs.

4Q2017

Operating Revenue (RM million) 144.8 7.5% 11.4%

Operating Expenses (RM million) 62.9 1.4% 5.3%

PATAMI (RM million) 63.8 12.6% 15.4%

EPS (sen) * 7.9 12.9% 14.5%

Annualised ROE 30%4 percentage

points3 percentage points

Cost to Income Ratio 42%3 percentage

points 5 percentage points

*The EPS shown above has been retrospectively adjusted for the bonus issue which was completed on 13 April 2018

5

Operating RevenueGrowth from securities trading and listing & issuer services

Increase in Securities Trading Revenue from higher ADV-OMT.

Higher Listing & Issuer Services due the increase in the number of corporate

exercises and structured warrants issued.

Higher Depository Services fees contributed by CDS custody fees.

Lower Derivatives Trading Revenue due to revision in guarantee fee and lower

number of FCPO and FKLI contracts traded.

(RM mil)

Total

RM144.8 mil

Total

RM134.7 milGrowth contribution by revenue streams:

Securities Trading Revenue

Derivatives Trading Revenue

Listing & Issuer Services

Depository Services

Market Data

Member Services & Connectivity

BSAS Trading Revenue

Conference Fee & Exhibition-Related Income

67.276.3

21.219.0

4.04.012.7

15.79.810.58.6

8.45.2

5.46.0

5.5

1Q2017 1Q2018

7.5%

1Q2017 1Q2018

+9.1 -2.2 +3.0 +0.7 -0.2 +0.2 -0.5

13.5%

10.5% 23.0%

7.3% 1.4% 5.3% 7.9%

134.7

144.8

6

Total

RM63.8 milTotal

RM62.9 mil

Operating ExpensesDecrease in operating expenses from lower technology costs

Note^ - Other operating expenses include building maintenance, administrative expenses and CDS expenses.

Higher staff cost due to annual salary increment.

Higher marketing and development expenses incurred as more marketing and

engagement activities were carried out.

Decrease in service fees mainly due to lower Globex service fees payable to CME

as a result of the decrease in number of derivatives contracts traded.

Staff costs

Depreciation & amortisation

Marketing & development

IT maintenance

Service fees

Other operating expenses^

1.4%

(RM mil)

Movement of expenses:

63.862.9

1Q2017 1Q2018

34.0 34.8

6.1 5.63.8 4.64.8 4.9

7.2 5.0

7.9 8.0

1Q2017 1Q2018

+0.8 -0.5 +0.8 +0.1 -2.2

+0.1

2.4% 8.4% 21.3% 0.8%

30.3% 1.3%

7

Market Performance

Securities Market Overview

Derivatives Market Overview

Islamic Capital Market Overview

8

34

31

35

Securities Market OverviewHigher retail trades in 1Q18 resulting from improved

market sentimentsAverage Daily Value

(ADV)(RM mil)Market Capitalisation

(RM bil)Fund Raised from New Listings &

Secondary Market (RM bil)

1,350 1,309 1,452

544 484

643

484 523

621

1Q2017 4Q2017 1Q2018

2,316

17.3%

14.2%

2,378

2,716

Velocity (%)

1,740.09 1,796.81

1,863.46

FBMKLCI

0.9

0.0 0.2

3.34.3

2.6

1Q2017 4Q2017 1Q2018

2.8

4.3

No. of New Listing

Fund raised from new listings

Fund raised from secondary

market

ADV of Domestic Institutions

ADV of Retail

ADV of Foreign Institutions Market Capitalisation

43

7

33%

4.2

5.2%

31 Mar

2017

31 Mar

2018

31 Dec

2017

1,801 1,907 1,896

0.6%

35%

9

ADC - Crude Palm Oil Futures

Volatility of Crude Palm Oil Futures

Derivatives Market OverviewTrades influenced by the volatility of the underlying

ADC - OthersADC – FBMKLCI Futures

Volatility of FBMKLCI Futures

Average Daily Contracts (“ADC”)

& VolatilityOpen Interest (No. of Contract)

9,378 7,599 8,940

52,515

46,448 44,516

183

301 564

1Q2017 4Q2017 1Q2018

21% 17% 17%

7% 6%9%

85%

15%

82%

17%

13.0%

54,348

62,076

28 Feb

2018

261,572

30 Mar

2018

283,201

1 Sept 2010

111,548

26 May

2016

337,267

54,020

85%

14%

1% 1%

0.6%

10

Islamic Capital Market Overview30% increase in ADV compared to 1Q2017

No. of Shariah Compliant

Stocks (%)

No. of Trading Participants

Bursa Suq Al-Sila’ (“BSAS”)

ADV (RM bil)

Market Capitalisation of

Shariah Compliant Stocks

(RM bil)

No. of Sukuk

Value of Listed Sukuk (USD bil)

Domestic Foreign Market Capitalisation of Shariah

Compliant Stocks

Domestic Foreign

13.6

16.3 16.2

3.8

5.36.5

1Q2017 4Q2017 1Q2018

17.4

21.6

30.2% 22.6

130

141

146

21.8 25.4 26.1

30.6

30.6 30.9

31 MAR 2017 31 DEC 2017 31 MAR 2018

52.4

56.0 57.0

25 25

26

1.8%

1,123 1,154 1,144

31 MAR 2017 31 DEC 2017 31 MAR 2018

0.9%

1.9%

74%61% 60%

4.6%

8.8%

11

Conclusion

Moving Forward

12

Moving Forward

SECURITIES MARKET• The Securities Market segment is expected to be resilient, given the strong fundamentals of the

economy and the continued improvements of corporate earnings into 2018.

• Trading volatilities however, may be influenced by domestic and external factors, such as monetary

policy shifts in advanced economies and rising trade protectionism by major trading partners.

DERIVATIVES MARKET• Trading and hedging activities will continue to be influenced by volatility in commodity prices and the

underlying equity market.

• The inclusion of traceability feature, extension of trading hours, tenure of contracts and position limits

for FCPO contracts announced by the Exchange during the quarter will further enhance derivatives

trading.

ISLAMIC CAPITAL MARKET• The Exchange will continue with its efforts in promoting Shariah-compliant investing on Bursa Malaysia-i

platform through engagements with market players, focusing on widening the investor base.

• Bursa Suq Al-Sila’, on the other hand, will continue its reach into new regions in 2018.

13

Moving Forward

As part of the continuing initiatives to further enhance the vibrancy and liquidity in the equity market, the

following have been introduced to-date:

• Stamp duty waiver on shares of mid and small cap companies for three (3) years from 1 March 2018 to

28 February 2021;

• Liberalisation of margin financing rules;

• Intra day short selling allowed for all investors;

• A new category of traders who trade on their own account, known as “Trading Specialists”;

• A volume-based incentive programme; and

• All new investors to be given a fee waiver on trading and clearing fees for six (6) months.

The Exchange is currently engaged in the establishment of a stock market trading link between Bursa

Malaysia and Singapore Exchange. In addition, Bursa Malaysia will continue with its initiatives to enhance

the breadth and depth of the ecosystem, which amongst others, through digitalisation of services,

liberalisation of rules framework and greater diversification of the investor base.

With the above initiatives and barring any unforeseen circumstances, the Exchange expects the positive

momentum in the market to continue and to achieve a sustainable performance for the current financial

year.

14

Appendices

Securities Market Trading Activity

Securities Market Trading Participation

Securities Market Foreign Ownership

Foreign Inflow/Outflow

Derivatives Market Activity

Derivatives Market Demography

Islamic Capital Market Activity

15

2,161

1,579 1,732

1,341

1,841

1,439 1,595

1,430 1,643

2,308

2,002

1,686

2,068 2,053 2,196

1,901 2,081

1,913 1,933 2,042 1,981

1,842 1,740 1,690

2,378

2,621

1,951

2,316

2,716

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18

42

3034

27

34

27 2825

28

3731

2530 29 30 28 30 28 29 30 29 27 26 25

34 35

2631

35

34 34 33 3328 30 29 30

2732

35

1,181 1,129 1,454

1,699 1,573 1,915 2,053 1,991

1,812

2,314

2,716

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 1Q18

Turnover Velocity (%)

Quarterly ADV Traded & Velocity

Average Daily Value Traded (OMT, RM mil)

Average Daily Value Traded (OMT, RM mil)Turnover Velocity (%)

Annual ADV Traded & Velocity

Securities Market Trading Activity

16

283 369 392

442 354

424

530 464

372

525

643

7667 73 74 77 78 74 77 79 77 76

2433 27 26 23 22 26 23 21 23 24

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

1Q

18

5873 73 74 74 74 76 73 73 78 77

4227 27 26 26 26 24 27 27 22 23

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

1Q

18

From 2008 to 2009, the statistics were based on Brokers’ submission. From 2010 onwards statistics

were based on Bursa’s internal system.

Retail

(%)

Institutions

(%)Local(%)

Foreign(%)

Retail ADVTraded (RM mil)

Foreign ADV

Traded (RM mil)

Retail vs. Institution Foreign vs. Local

Securities Market Trading Participation

496

323 392 437 404

507 492 544

491 506 630

17

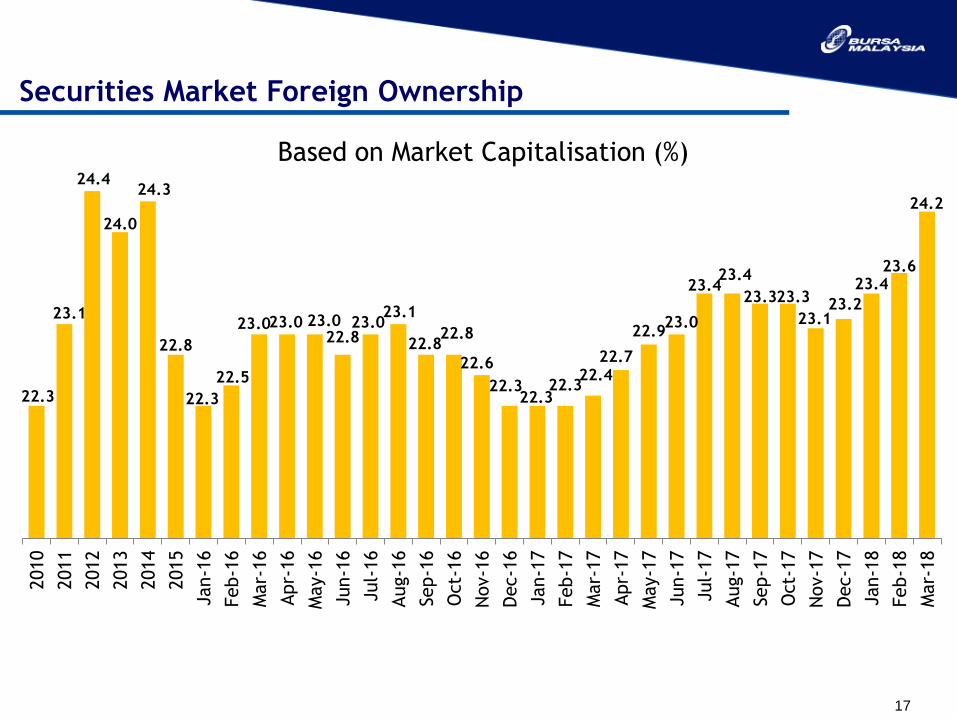

Securities Market Foreign Ownership

22.3

23.1

24.4

24.0

24.3

22.8

22.3

22.5

23.023.0 23.022.8

23.023.1

22.822.8

22.6

22.322.3

22.322.4

22.7

22.923.0

23.423.4

23.323.3

23.123.2

23.423.6

24.2

2010

2011

2012

2013

2014

2015

Jan-1

6

Feb-1

6

Mar-

16

Apr-

16

May-1

6

Jun-1

6

Jul-

16

Aug-1

6

Sep-1

6

Oct-

16

Nov-1

6

Dec-1

6

Jan-1

7

Feb-1

7

Mar-

17

Apr-

17

May-1

7

Jun-1

7

Jul-

17

Aug-1

7

Sep-1

7

Oct-

17

Nov-1

7

Dec-1

7

Jan-1

8

Feb-1

8

Mar-

18

Based on Market Capitalisation (%)

18

-10,000

-5,000

0

5,000

10,000

2015

TNFO: RM19.7 bil

2013

TNFI: RM2.6 bil

2014

TNFO: RM6.9 bil

TNFI: Total Net Foreign Inflow

(RM mil)

TNFO: Total Net Foreign Outflow

Foreign Inflow/Outflow

Monthly foreign inflow/outflow from 2013 to March 2018

4,355

2,6101,977

359 419

-241 -738 -231-15

959

3,376

-1,120

-64

-2,000

-1,000

0

1,000

2,000

3,000

4,000

5,000Monthly foreign inflow/outflow from March 2017 to March 2018(RM mil)

2016

TNFO: RM3.2 bil

1Q2018

TNFI: RM2.2 bil

2017

TNFI: RM10.8 bil

19

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

1Q

18

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

17%

136

162171

152

174

146

172

214

196

213

204196

218

239

288

196

207

229

235

230

283

293

226

237

262263

261

295

283

40

Quarterly Average Daily Contracts (’000)

31

42

35

60

Total Annual Contract (mil)

Crude Palm Oil FuturesOthersOpen Interest (’000)

17%

82%

6.1 6.1 6.2

8.4

9.6

FBMKLCI Futures

37

`

`

82

%3234

44 4542

4642

10.7

50

12.5

44

54

Derivatives Market Activity

55

14.2

62

51

62

56

14.0

5856

62

55

as

14.1

57 5754

156

123

132

152

214196 196

230

237

295

283

54

3.3

20

15 20 21 19 15 18 20 18 14 11 14

46

5244

42

2828 24

23

1918

21

2

3

22

21 2

5

33

3

37

2633

37

55 53 54 55

6468

62

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 1Q18

(%)FKLI

27

36 34 34 36 33 34 31 2823

19

3827

26 24 1917 15

1516

20 26

1

11

1 11

1 1

15 17

1513

12

10 15 2121 23 20

20 1925 28

3239

35 32 34 33 34

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 1Q18

(%)FCPO

1

Local

Domestic Retail

Domestic

Institutions

Foreign Institutions Local

Domestic RetailDomestic

Institutions

Foreign Institutions Foreign Retail

Derivatives Market Demography

21

0.9 1.6 2.75.5

13.5 13.4 15.1 16.2

0.2 0.71.2

1.4

1.7 2.9

4.56.4

2011 2012 2013 2014 2015 2016 2017 1Q18

BSAS Annual Average Daily Value

Local ADV Foreign ADV

1.22.3 3.9

6.9

15.2 16.319.6

22.6(RM bil)

BSAS ADV (RM bil)

13.5

0.9

0.8 0.9 1.1 1.1 1.3 1.5 1.6 1.8 2.6 2.4 2.7 3.2 3.7 3.7 5.9

8.5 10.4

12.0 14.4

16.9 16.1

12.7 12.2 12.6 13.6 15.1 15.5 16.1 16.2

0.2 0.2 0.2 0.3 0.3 0.7 0.9 1.2 1.1 1.0 1.1 1.5 1.4 1.5

1.4

1.4

1.5 1.6

1.6

2.1 2.6

2.7 3.0 3.2 3.8

3.7 4.9

5.6 6.4

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

BSAS Quarterly Average Daily Value(RM bil)

Islamic Capital Market Activity

DISCLAIMER:

These presentation slides are owned by Bursa Malaysia Berhad and/or the Bursa Malaysia group of companies (“Bursa Malaysia”). Whilst Bursa Malaysia endeavors to

ensure that the contents in this presentation are accurate, complete, current and have been obtained from sources believed by Bursa Malaysia to be accurate and

reliable, neither Bursa Malaysia or the presenter of this presentation make any warranty, express or implied, nor assume any legal liability or responsibility for the

accuracy, completeness or currency of the contents of this presentation. In no event shall Bursa Malaysia be liable for any claim, however arising, out of or in relation to

this presentation.

Copyright Bursa Malaysia Berhad 2017 (30632-P)

www.bursamalaysia.com

RASMONA ABDUL RAHMAN

603-2034 7175

E-mail : [email protected]

RAFIDAH AZIZ

603-2034 7262

ADAM ISKANDAR AHMAD ZAHAR

603-2034 7351

INVESTOR RELATIONS CONTACT INFORMATION