2017 LEVERAGED FINANCE CONFERENCEScottsdale, Arizona

October 3, 2017

Sponsored by Deutsche Bank

1

FORWARD-LOOKING STATEMENTS

2

This presentation includes “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of

1934. Forward-looking statements are statements other than statements of historical fact. They include statements that give our current expectations, guidance or forecasts of

future events, production and well connection forecasts, estimates of operating costs, anticipated capital and operational efficiencies, planned development drilling and expected

drilling cost reductions, general and administrative expenses, capital expenditures, the timing of anticipated asset sales and proceeds to be received therefrom, projected cash

flow and liquidity, our ability to enhance our cash flow and financial flexibility, plans and objectives for future operations, and the assumptions on which such statements are

based. Although we believe the expectations and forecasts reflected in the forward-looking statements are reasonable, we can give no assurance they will prove to have been

correct. They can be affected by inaccurate or changed assumptions or by known or unknown risks and uncertainties.

Factors that could cause actual results to differ materially from expected results include those described under “Risk Factors” in Item 1A of our annual report on Form 10-K and

any updates to those factors set forth in Chesapeake’s subsequent quarterly reports on Form 10-Q or current reports on Form 8-K (available at http://www.chk.com/investors/

sec-filings). These risk factors include: the volatility of oil, natural gas and NGL prices; the limitations our level of indebtedness may have on our financial flexibility; our inability

to access the capital markets on favorable terms; the availability of cash flows from operations and other funds to finance reserve replacement costs or satisfy our debt

obligations; our credit rating requiring us to post more collateral under certain commercial arrangements; write-downs of our oil and natural gas asset carrying values due to low

commodity prices; our ability to replace reserves and sustain production; uncertainties inherent in estimating quantities of oil, natural gas and NGL reserves and projecting

future rates of production and the amount and timing of development expenditures; our ability to generate profits or achieve targeted results in drilling and well operations;

leasehold terms expiring before production can be established; commodity derivative activities resulting in lower prices real ized on oil, natural gas and NGL sales; the need to

secure derivative liabilities and the inability of counterparties to satisfy their obligations; adverse developments or losses from pending or future litigation and regulatory

proceedings, including royalty claims; charges incurred in response to market conditions and in connection with our ongoing actions to reduce financial leverage and complexity;

drilling and operating risks and resulting liabilities; effects of environmental protection laws and regulation on our business; legislative and regulatory initiatives further regulating

hydraulic fracturing; our need to secure adequate supplies of water for our drilling operations and to dispose of or recycle the water used; impacts of potential legislative and

regulatory actions addressing climate change; federal and state tax proposals affecting our industry; potential OTC derivatives regulation limiting our ability to hedge against

commodity price fluctuations; competition in the oil and gas exploration and production industry; a deterioration in general economic, business or industry conditions; negative

public perceptions of our industry; limited control over properties we do not operate; pipeline and gathering system capacity constraints and transportation interruptions; terrorist

activities and/or cyber-attacks adversely impacting our operations; potential challenges by SSE’s former creditors of our spin-off of in connection with SSE’s recently completed

bankruptcy under Chapter 11 of the U.S. Bankruptcy Code; an interruption in operations at our headquarters due to a catastrophic event; the continuation of suspended

dividend payments on our common stock; the effectiveness of our remediation plan for a material weakness; certain anti-takeover provisions that affect shareholder rights; and

our inability to increase or maintain our liquidity through debt repurchases, capital exchanges, asset sales, joint ventures, farmouts or other means.

In addition, disclosures concerning the estimated contribution of derivative contracts to our future results of operations are based upon market information as of a specific date.

These market prices are subject to significant volatility. Our production forecasts are also dependent upon many assumptions, including estimates of production decline rates

from existing wells and the outcome of future drilling activity. Expected asset sales may not be completed in the time frame anticipated or at all. We caution you not to place

undue reliance on our forward-looking statements, which speak only as of the date of this presentation, and we undertake no obligation to update any of the information

provided in this presentation, except as required by applicable law. In addition, this presentation contains time-sensitive information that reflects management’s best judgment

only as of the date of this presentation.

We use certain terms in this presentation such as “Resource Potential,” “Net Reserves” and similar terms that the SEC’s guide lines strictly prohibit us from including in filings

with the SEC. These terms include reserves with substantially less certainty, and no discount or other adjustment is included in the presentation of such reserve numbers. U.S.

investors are urged to consider closely the disclosure in our Form 10-K for the year ended December 31, 2016, File No. 1-13726 and in our other filings with the SEC, available

from us at 6100 North Western Avenue, Oklahoma City, Oklahoma 73118. These forms can also be obtained from the SEC by calling 1-800-SEC-0330.

2017 DEUTSCHE BANK LEVERAGED FINANCE CONFERENCE

OUR STRATEGYSTRONG THROUGH COMMODITY PRICE CYCLES

2017 DEUTSCHE BANK LEVERAGED FINANCE CONFERENCE 3

BUSINESS STRATEGIES:

Financial Discipline

Business Development

Profitable and

Efficient Growth from

Captured Resources

Exploration

Delivering the 2017 plan

$2 – $3 billion of asset sales

Focused on cash flow neutrality

Retain posture for growth

Capital allocation focused on

portfolio expansion optionality

2H 2017 and 2018 Priorities

MOMENTUM BUILDING INTO 4Q’17DELAYS OF 3Q’17 ARE BEHIND US

2017 DEUTSCHE BANK LEVERAGED FINANCE CONFERENCE 4

Estimated 3Q’17 total

production of ~542 mboe/d

Estimated 3Q’17 oil production

of ~86 mbo/d

4Q’17 production accelerating

due to TILs

~125 TILs projected for 4Q’17;

~74 in STX

We now expect to average 100

mbo/d in 4Q’17

450

500

550

600

Net pro

ductio

n (

mboe/d

)

Total Company Production

0

20

40

60

80

100

120

140

Q1 2017 Q2 2017 Q3 2017 Q4 2017

Projected 2017 TILs

South Texas Mid-Con Utica Marcellus Rockies Gulf Coast

OPERATIONS SETTING THE STAGE AS WE ENTER 2018

2017 DEUTSCHE BANK LEVERAGED FINANCE CONFERENCE 5

Oil growth, efficiencies creating

margin expansion

Drilling longer laterals

Enhanced completion designs

Testing spacing assumptions

Prolific CHK producers driven

by pushing technology across

the portfolio

Marcellus McGavin 6H ~61 mmcf/d

PRB Rankin 1H ~2,800 boe/d

STX Blakeway 2H ~3,200 boe/d

HSVL Hunter ~38 mmcf/d

More to come with exploitation in PRB (multiple zones),

Louisiana (Bossier), NE PA (Utica) and Mid-Con (Chester)

-

20

40

60

80

100

120

JAN2017

FEB2017

MAR2017

APR2017

MAY2017

JUN2017

JUL2017e

AUG2017e

SEP2017e

OCT2017e

NOV2017e

DEC2017e

Net

pro

duction (

mbo/d

)

Projected Total Oil Production

South Texas Mid-Con Utica Rockies

Powder River Basin

˃ Hotspot advantage

˃ Stacked pay opportunities

˃ Significant resource potential

2017 CAPITAL ALLOCATIONFLEXIBLE PROGRAM – VALUE FOCUSED

2017 DEUTSCHE BANK LEVERAGED FINANCE CONFERENCE 6

Powder River Basin2 Rigs / 1 Frac Crew

25 – 30 Spuds

23 – 28 TILS

POWDER RIVER BASINBUILDING MOMENTUM

Moving to development phase

72017 DEUTSCHE BANK LEVERAGED FINANCE CONFERENCE

Estimate Actual0

5

10

15

20

25

30

35

40

mboe

/d

Net Production Potential

Analyst Day ProjectionOil growth provided by

Sussex, Turner and Niobrara

More Turner and Sussex

TILs in 2H17

Third rig in October –

Turner focused

~325 permits approved Projected 2017 TILs10

5

0AUG 2017 SEP 2017e OCT 2017e NOV 2017e DEC 2017e

POWDER RIVER BASIN – TURNER UPDATEOUTSTANDING INITIAL RESULTS

2017 DEUTSCHE BANK LEVERAGED FINANCE CONFERENCE 8

Rankin 5-33-68 1HTIL 5/17/2017 – 4,500' lateral

Peak rate – 2,886 boe/d (51% oil)

120-day cumulative – 79 mbo, 577 mmcf

Sundquist 9-34-71 13HTIL 3/16/2017 – 7,100' lateral

Peak rate – 2,560 boe/d (80% oil)

180-day cumulative – 209 mbo, 357 mmcf

Graham 23-35-71 15HTIL 9/8/2017 (6 days) – 4,500' lateral

Peak rate to date – ~1,700 boe/d (~80% oil)

Well still cleaning up

OIL

CONDENSATE

10,000

40,000

20,000

30,000

0

0 42 6 8

PRODUCING MONTHS

CU

MU

LA

TIV

E B

OE

/ 1

000F

T

CUM BOE/1000 FT vs Producing Months

Industry Turner Offsets

CHK Turner Producers

10

50,000

Rankin 5-33-68 1H

Sundquist 9-34-71 13H

Graham 23-35-71 15H

POWDER RIVER BASIN – TURNER UPDATEFUTURE TESTS

2017 DEUTSCHE BANK LEVERAGED FINANCE CONFERENCE 9

• Third rig in October –Turner focused

• Potential tests for 2017 – 2018

˃ Spacing Test – 6 wells

• Current assumption 2,640’

˃ Extents Test – 5 wells

˃ Continuing to evaluate high-graded position –3 wells in 2017, 17 wells in 2018

OIL

CONDENSATE

TURNER

460 mmboe

Spacing Test

Extents Test

Highgrade Evaluation

POWDER RIVER BASIN – SUSSEX SANDSTONEHIGHLY ECONOMIC OIL PLAY

• Dominant position in the play

• Development mode

• Utilizing seismic to delineate fairway

• ~165 locations˃ Assumes 1,320' – 1,980' spacing

˃ Overpressured – high deliverability

• Targeted development through 2020˃ EUR: ~750 – 1,350 mboe

˃ Oil breakeven price: ~$30 – $35(1)

˃ ROR: ~ 38% – 55%(2)

2017 DEUTSCHE BANK LEVERAGED FINANCE CONFERENCE 10

51%36%

13%

Sussex Production Mix

Oil Gas NGL

Months on Production

Gro

ss C

um

ula

tive P

roductio

n (

mboe)

CHK Sussex

Industry Sussex

Sussex Performance

(1) PV10 positive breakeven price assuming $3/mcf gas pricing

(2) Assumes $3/mcf gas and $50/bbl oil

SUSSEX

150 mmboe

POWDER RIVER BASIN – SUSSEX SANDSTONEWHERE WE ARE NOW AND WHERE WE ARE GOING

2017 DEUTSCHE BANK LEVERAGED FINANCE CONFERENCE 11

TURNING IN LINE

• 10 gas condensate wells

˃ Finishing completions in September

• 1 black oil appraisal well

UPCOMING LOCATIONS

• 15 volatile oil wells

• 6 gas condensate wells

Condensate Condensate

South Texas

˃ Oil production growth engine

˃ Longer laterals driving value

˃ Enhanced completions

yielding encouraging results

2017 CAPITAL ALLOCATIONFLEXIBLE PROGRAM – VALUE FOCUSED

Eagle Ford Shale6 Rigs / 4 Frac Crews

175 – 195 Spuds

155 – 175 TILS

2017 DEUTSCHE BANK LEVERAGED FINANCE CONFERENCE 12

SOUTH TEXAS – EAGLE FORDACCELERATING VALUE WITH LONGER LATERALS

2017 DEUTSCHE BANK LEVERAGED FINANCE CONFERENCE 13

$21

$15$17

$11$9

2013 2014 2015 2016 2017E

South Texas F&D Cost (1)

($/boe)

Capital efficiency improvesFaster cycle times, longer laterals

Large remaining potential Estimated net resources of > 2.0 bboe

Oil growth engine~10% oil volume growth 4Q’16 vs. 4Q’17

162

279

129

112

0 50 100 150 200 250 300

2014

2015

2016

2017E

Days

Spud to First SalesCycle Time

(1) F&D Costs referenced in this chart are net capital costs divided by net EUR per well. Wells are binned by year in which they were TIL’d and then were averaged across that year

What we are learning

Longer laterals are paying off

Enhanced completions with upspacing

are leading to improved well results

Planning to test spacing concept

across the field

SOUTH TEXAS – EAGLE FORDMORE VALUE, LESS CAPITAL INTENSITY

2017 DEUTSCHE BANK LEVERAGED FINANCE CONFERENCE 14

0

50

100

150

200

250

0 1 2 3 4 5

Cum

ula

tive

Pro

du

ctio

n (

mb

o)

Months on Production

Blakeway 1 C DIM 2H

Blakeway 2H CHK Offsets Industry Offsets

Projected 2017 TILs30

25

20

15

10

5

0AUG 2017e SEP 2017e OCT 2017e NOV 2017e DEC 2017e

Blakeway

915' spacing vs.

330' – 600' in the area

CHK Drilled Lateral

Blakeway 1 C DIM 2H

CHK Leasehold

2017 CAPITAL ALLOCATIONFLEXIBLE PROGRAM – VALUE FOCUSED

2017 DEUTSCHE BANK LEVERAGED FINANCE CONFERENCE 15

Gulf Coast

˃ Longer laterals creating

greater value

˃ Refracs improve capital

efficiency

˃ Bossier resource potential

Haynesville Shale3 Rigs / 2 Frac Crews

30 – 35 Spuds

32 – 37 TILS

HAYNESVILLEDELIVERING EXCEPTIONAL PRODUCTIVITY

(1) Source: Heikkinen Energy Associates, Drillinginfo. Wells are adjusted to a 7,500’ lateral

2017 DEUTSCHE BANK LEVERAGED FINANCE CONFERENCE 16

Delivering monster IPsHunter 1H – 38 mmcf/d, 7,500' lateral, 3Q 2017 TIL

Nguyen 1H – 36 mmcf/d, 9,500' lateral, 3Q 2017 TIL

PH 1H – 33 mmcf/d, 7,500' lateral, 2Q 2017 TIL

Crow 2H – 36 mmcf/d, 7,500' lateral, 2Q 2017

GLD 1H – 42 mmcf/d, 8,200' lateral, 1Q 2017 TIL

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

0 2 4 6

Gro

ss C

um

ula

tive P

roduction (

Mm

cf)

Months on Production

Haynesville Production(1)

CHK Wells

Average

HEA Hville (2 Bcf/1,000') TC

1,200+ locationsPost divestiture and optimized for

longer lateral development

2017 CAPITAL ALLOCATIONFLEXIBLE PROGRAM – VALUE FOCUSED

Appalachia

˃ Optimizing stimulation

designs

˃ Utica oil growth

˃ Significant resource potential

2017 DEUTSCHE BANK LEVERAGED FINANCE CONFERENCE 17

Appalachia2 Rigs / 2 Frac Crews

50 – 65 Spuds

110 – 130 TILS

Strong returns2017E FCF ~$315mm(1)

2017E capital ~$125mm

MARCELLUS SHALEENHANCED COMPLETIONS DELIVERING VALUE

(1) Assumes $3/mcf price deck

(2) 2,900 undrilled locations: 1,500 represent Upper Marcellus locations and the remaining are Lower Marcellus locations

2017 DEUTSCHE BANK LEVERAGED FINANCE CONFERENCE 18

Record results – 61 mmcf/d McGavin E WYO 6H, IP30 55 mmcf/d

Enhanced completion design

TIL 7/28/2017, ~10,500' lateral

$-

$25

$50

$75

$100

0

500

1,000

1,500

2,000

2,500

1/2

01

6

3/2

01

6

5/2

01

6

7/2

01

6

9/2

01

6

11/2

016

1/2

01

7

3/2

01

7

5/2

01

7

7/2

01

7

9/2

01

7

11/2

017

1/2

01

8

3/2

01

8 Net

Opera

ted C

apital ($

mm

)

Gro

ss G

as R

ate

(m

mcf/d)

Production Forecast Actual Production Actual Capital

Core expansion opportunityConfirmed by recent industry

result of 37 mmcf/d in Bradford County

Utica appraisalCore planned for early 2018

~70,000 net perspective acres

McGavin 6H

IP: 61 mmcf/d

Industry Well

OUR STRATEGYSTRONG THROUGH COMMODITY PRICE CYCLES

2017 DEUTSCHE BANK LEVERAGED FINANCE CONFERENCE 19

BUSINESS STRATEGIES:

Financial Discipline

Business Development

Profitable and

Efficient Growth from

Captured Resources

Exploration

Delivering the 2017 plan

$2 – $3 billion of asset sales

Focused on cash flow neutrality

Retain posture for growth

Capital allocation focused on

portfolio expansion optionality

2H 2017 and 2018 Priorities

Appendix

2017 DEUTSCHE BANK LEVERAGED FINANCE CONFERENCE 20

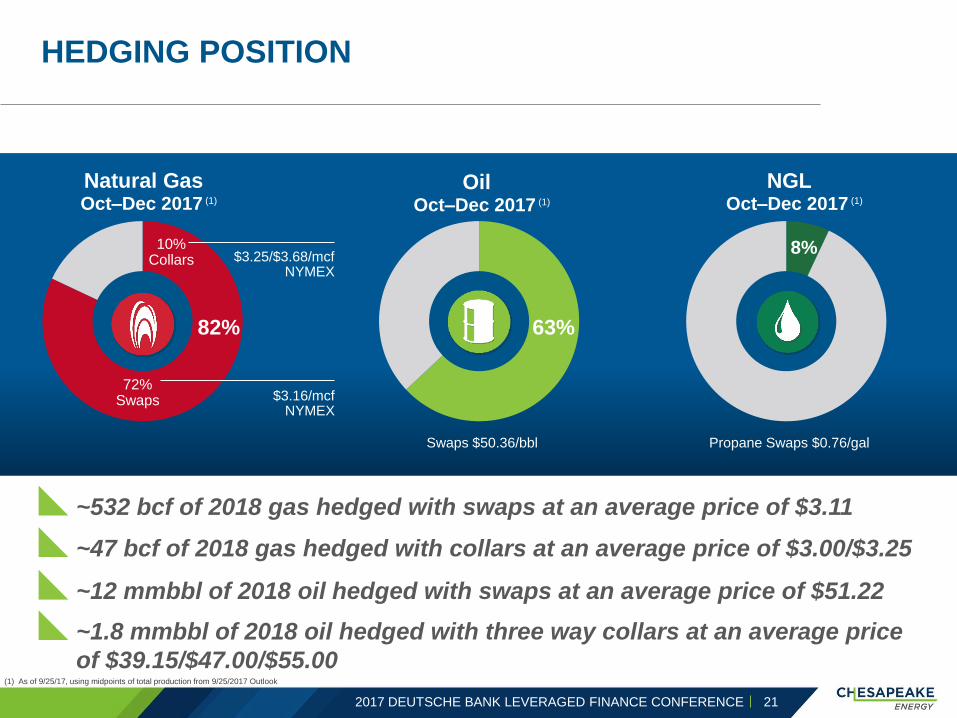

OilOct–Dec 2017 (1)

63%

Swaps $50.36/bbl

NGLOct–Dec 2017 (1)

8%

Propane Swaps $0.76/gal

Natural GasOct–Dec 2017 (1)

82%

72%Swaps

10%Collars $3.25/$3.68/mcf

NYMEX

$3.16/mcfNYMEX

HEDGING POSITION

(1) As of 9/25/17, using midpoints of total production from 9/25/2017 Outlook

~532 bcf of 2018 gas hedged with swaps at an average price of $3.11

~47 bcf of 2018 gas hedged with collars at an average price of $3.00/$3.25

21

~12 mmbbl of 2018 oil hedged with swaps at an average price of $51.22

2017 DEUTSCHE BANK LEVERAGED FINANCE CONFERENCE

~1.8 mmbbl of 2018 oil hedged with three way collars at an average price

of $39.15/$47.00/$55.00

$53

$380

$752

$2,224

$1,868

$338

$1,300 $1,250 $1,300

$0

$500

$1,000

$1,500

$2,000

$2,500

Mill

ion

s

Current Pro Forma

$451

Secured

REDUCED DEBT AND PUSHED BACK MATURITIES

(1) Pro Forma for add-on issuance and expected tender results from liability management transaction announced on 9/27/17

$9.4 billion Principal balance @ 9/30/2017(1)

(1)

22

$724

Pro forma for LM activity announced 9/27/17

~$300 million in additional net proceeds from issuance for

GCP, including repurchase of other indebtedness

$1,500 $1,417

2017 DEUTSCHE BANK LEVERAGED FINANCE CONFERENCE

CORPORATE INFORMATION

2017 DEUTSCHE BANK LEVERAGED FINANCE CONFERENCE 23

HEADQUARTERS

6100 N. Western Avenue

Oklahoma City, OK 73118

WEBSITE: www.chk.com

CORPORATE CONTACTS

ERIK S. FARES

Vice President and Treasurer

DOMENIC J. DELL’OSSO, JR.

Executive Vice President and

Chief Financial Officer

Investor Relations department

can be reached at [email protected]

PUBLICLY TRADED SECURITIES CUSIP TICKER

7.25% Senior Notes due 2018 #165167CC9 CHK18A

3mL + 3.25% Senior Notes due 2019 #165167CM7 CHK19

6.625% Senior Notes due 2020 #165167CF2 CHK20A

6.875% Senior Notes due 2020 #165167BU0 CHK20

6.125% Senior Notes due 2021 #165167CG0 CHK21

5.375% Senior Notes due 2021 #165167CK21 CHK21A

8.00% Senior Secured Second Lien Notes due 2022#165167CQ8 N/A

#U16450AT2 N/A

4.875% Senior Notes due 2022 #165167CN5 CHK22

5.75% Senior Notes due 2023 #165167CL9 CHK23

8.00% Senior Notes due 2025#165167CT2 N/A

#U16450AU99 N/A

8.00% Senior Notes due 2027#165167CV7 N/A

#U16450AV7 N/A

5.50% Contingent Convertible Senior Notes due 2026 #165167CR6 N/A

2.25% Contingent Convertible Senior Notes due 2038 #165167CB1 CHK38

4.5% Cumulative Convertible Preferred Stock #165167842 CHK PrD

5.0% Cumulative Convertible Preferred Stock (Series 2005B)#165167834/

N/A#165167826

5.75% Cumulative Convertible Preferred Stock

#U16450204/

N/A#165167776/

#165167768

5.75% Cumulative Convertible Preferred Stock (Series A)

#U16450113/

N/A#165167784/

#165167750

Chesapeake Common Stock #165167107 CHK