3.1. Introduclion 3 4 S u f The Co-operative Societies are the largest organized f m c i a l

intermediaries functioning in the n k l India. The short and medium term

loans are channellised to the farmers and others through Cooperatives. The

Co-operatives are organized into a three-tier structure with State Co-operative

Bank at the apex level in each state. the District Cwperative Cenfral B a t h

at the district and the Primary Agricultural Credit Societies (PACSs) at the

village levels.

The Ccqeratives can be classified accodag to the purpose into two,

viz., Agricultural Credit Co-operatives and Non-agricultual Cndit Co-

operatives. The Agricultural Co-operatives extend three types of cndit

dependency on the period of time, viz., short-term credit, medium-term credit

and long-term credit.

The short-term credit is given for seasonal agricultural operations

directed towards rising of crop on land. Short-term loans are generally made

for 12 months. They are given for purchasing seeds, manure and fertilizers,

for meeting labour charges, etc. The medium-term loans are given for a period

ranging from over 12 months to 5 years for the purposes such as reclamation

of land, building, other improvements, purchase of live-stock, carts, repairs to

old wells, machinery, etc. The long-term credit is given for a period ranging

between 5 and 20 years for the purposes such as redemption of land,

liquidation of debts, purchase of tractors for sinking of wells, permanent

fencing, purchase of land, purchase of heavy agricultural machinery like

tractors etc. as well as for lift irrigation schemes.

Besides these Agricultural Co-operatives, there are, however, certain

other types of Co-operative Societies at regionall national levels for working

for employees of organizations l i e the railways, etc., whose membership

exceeds beyond one state. These societies come under the purview of the

Central Government and .they are governed by the

91 ~ 6 4 ~

Societies Act, 1984 (Earlier there was Multi-Unit Co-operative Societies Act,

1942) which is a Central Act. ihey fall under the purview of entry 44 of the

Union ~ist ' in the Constitution.

The following figure dtpicts the three-tier strucwe uf cooperatives in

~ndia.'

Figure - 3.1

The Organisational Structure of Cooperatives in India

4 4 Agricultural Societies Non-agricultural Societies

Short-term and Medium-tenn

.1 -.. State Co-operative

Banks

Central Co-operative Bank

primary Grain Agricultural Banks

credit soc~eties '

Long-term State Co- State Industrial

1 operative Banks Co-operative

Central land I I Bapks Mortgagd

Development Banks

Primary Land

t Central Industrial I Banks

Mortgage1 Central Co- Development Banks operative Banks

I +

Pimary Non-agricultural Credit Societies

Of I hich

Employer's Co- Urban Co. operative credit operative

societies Banks

The Co-operatives that provide short and medium credit an o@ed

at three levels, namely the State Cb-operative Banks, Central Co-opemlives

Banks and Primary Agricultural Credit Societies (PACSs) and the Grain

Banks. At the top most tien, the state Co-optive Banks (SCBs) are

organized tit the State level. So, SCB forms the apex of the co-operative credit

structure in. each state. At the second tier, ~ i s k c t Central Co-operative Banks

(DCCBs) or Central Co-operative Banks (CCBs) is organized at the district

level. Primary Agricultural Credit Societies (PACS) are at the lowest tier.

These are organized at the village level.

In each state the affairs of all types of Cwpemwes an administered

by a separate department known as Co-operative Department. The mtm and

strength of the staff of the Co-operative Department vary from state to st*.

With the rapid growth of co-operative movement, there has been a

considerable decentralisation of powers in this department. In most of the

states, the Registrar is the Head of Co-operative Department Exchange, the

overall control over the co-operative Sector. The Registrar is assisted by one

or more Additional or Joint Registrars or other officials at state-level, (Chief

Auditors, Financial Advisors, etc). The division of responsibility among them

is on functional basis. In some of the states the Divisional Officers at a level

between the Registrar, and District Officers are also appointed for

administrative convenience. At the branch' level, the Branch Manager looks

after the administration.

3.2. Co-operative Administration at National Level

Co-operation is in the state list included in the Constitution of India.

Accordingly the State Governments have exclusive legislative and executive

jurisdiction over the co-operative sector speciality in the state. Each State

Government has appointed a Registrar of Co-operative Societies who is the

head of the State Co-operative Department. He is responsible for the control,

supervision and co-ordination of 'the Co-operative Societies and their

programmes and also for administration of the State Co-operative Societies

Act.

At present there is no separate Ministry or Department for Co-

operation at the Centre. However, earlier there was a separate Ministry of

~ommuniti Development and co-operation at this level. There was also a

separate Department of Co-operation in that Ministry. 'Later the subject "Co-

operation" was included in the Ministry of Agriculture which consists of

separate department of co-operation. Subsequently, it was renamed as the

Department of Agriculture and Co-operation in the Ministry of Agriculture.

Generally the Ministry of Agriculture discharges the following hnctions

relating to the co-operative sector.

(i) Co-operation in Agriculture Sector, Agricultural Credit and

Indebtedness.

(ii) General policy in the field of Co-operation and coordination of the

co-operative activities in all sectors (The Ministries concerned are

responsible for Co-operatives in the respective fields).

(iii) Matters relating to National Co-operative Drganisations.

(iv) National Co-operative Development Corporation.

(iv) incorporation regulation and winding up of Co-operative Societies

with objects not confined to one State.

(v) To train the personnel of the Co-operative Departments and

Institutions (including education of members, office bearers and

non-officials).*

3.3. National Level Cosperative Organisations

With the diversification of the co-operative movement in various

directions after the acceptance and implementation of various measures

suggested by the All India Rural Credit Survey Report during the Second Five

2 Minbtv of Agrfculhtre, Department of Agriculture and Codperation. Marendl for Parliamentaty

Cornmiltee on the Weljare of Scheduled Cartes and Scheduled Tribes (New Delhi: 1983). Cytlostyled. p. 7.

Year plan, there occurred a myth of co-operative federal organisations and a gradual taking over of the responsibilities by the federal organisations so far

as promotional and supervisory functions are concerned. This has been

necessary and a gratifying development in the direction of the movement

attaining a greater degree of self-reliance and self-regulation. Among the

National Co-operative Organisations important may be mentioned:

1. The National Agricultural Co-operative Marketing Federation, New

Delhi.

2. National Federation of State Co-operative Banks, Bombay.

3. National Central Land Development Banks' Federation, Bombay.

4. National Federation of Urban Co-operative Banks and Credit Societies

New Delhi.

5. The National Federation of Co-operative Sugar Factories Ltd.,

New Delhi.

6. The National Federation of Industrial Co-operative Ltd., New Delhi.

7. The All India Federation of Co-operative Spinning Mills Ltd.,

Bombay.

8. The Industrial Co-operative Banks Federation, Bombay.

9. The National Co-operative Consumers Federation. New Delhi.

10. The National CoToperative Union of India, New Delhi.

1 1. The All India Handloom Fabric Marketing Co-operative Society,

Bombay.

12. National Federation of Labour Co-operatives Ltd., New Delhi.

13. All India Fishermen Co-operative Federation Ltd., New Delhi.

14. National Co-operative ~ous i& Federation Ltd., New Delhi.

15. National Co-opemfive Dairy Federation.

16. National Heavy Engineering Co-operative Ltd., Pune.

17. India Farmers Fertilizer Co-operative Ltd., New Delhi.

18. Petrofils Co-operatives Ltd., Petrofils Dist., Baroda.

19. The f ishak Bharati Co-operative Ltd., (KRIBHCO), New Delhi.

20. National Co-operative Federation of Tobacco Growers, New Delhi.

3.4. Cooperative Administration at State Level

It is a well known fact that the Co-operative Movement was ushered

into India on the Government's initiative. Eversince the passing of the Co-

operative Societies Act of 1904, the Co-operative Societies were managed by

the Government, both by the Central and State Governments. Thus they

became almost Governmental Institutions. They are allowed some degree of

authority in their working in accordance with the principles of co-operative

aspects.

Generally, the State Governments look after the following aspects of the

movement of Co-operative Societies working the state.

(1) The passing of special legislation for the organisation and working of

Co-operative Institutions in the state.

(2) Protection to Co-operative Societies from the restriciive provisions of

the various debt relief acts and money lender's acts.

(3) The appointment of expert committees from time to time as and when

govemmea felt that something was wrong with the movement and

expert opinion is called for.

(4) The financial commitments by governments in the maintenance of

special co-operative departments with a large staff.

( 5 ) The financial aid given in the form 'of loans, gmts in-aid and

subsidies.

(6) The supply of service pponnel entirely or partly free of charge to

various institutions, which could not other wise afford to employ them.

(7) The moral support in recognising the movement as a sdtable agency

for various activities, particularly during war time, e.g. supply,

procurement and distribution of ration,. conlrolled and other necessary

cominodities, help to cottage industries, etc. and planned economic

development.

(8) Special concessions and privileges such as exemption from income-

tax, stamp W, snd registration fees, execution of awards through

governmeat ag&ies, exemption from a h h e n t of shares of co-

operative Socides, ftee remittance transfer facilities c k ~ ~

3.5. State Co-operative Department:

The systematic maintenance of a Separate Co-operative Department by

State Governments had started in 1904. Separate hnds are earmarked for the

Cosperatives in the State Budgets under the Head, "Co-operation". In course

of time, there had been marked increase in the expenditure incurred by the

State Governments on their Co-operative Departments especially during and

after the Second Five Year Plan. This was necessitated on account of the

corresponding rise in the requirement of. staff in the department for

supervision, inspection and audit of cooperative institutions working at

various levels.

In each state of hdia according to the Co-operative Societies Act, the

Registrar of Co-operative Societies appointed by the Government occupies a

pivotal position in the administrative set up of the Co-operative Department.

He is envisaged not merely as the Registering Oficer as in the case of Joint

Stock Companies, but a captain of the whole team running the co-operative

movement. The success or failure of co-operative movement largely depends

upon the selection of the right type of man as Registrar.

. R e a m Bank of India, Review ofthe Co-opemlive Movement in India 1939-46 (19181. p.89.

According to the Co-operative Societies Acts of several States in India

it is the duty of the Registrar to receive and enquire into appiications for

registrations; to register the bye-laws of the societies to audit the accounts or

cause them to be audited; to make a valuation of assets and liabilities of

society and to prepare a list of overdue loans; to see that the act, rules and

bye-laws are observed; to make special inspections when called upon to do

so; to dissolve or cancel Societies and to cany out their liquidation.

Thus the Registrar occupies a crucial position in thc co-operative

administration at the State level. The Co-operative Department is considered

as "one of the major departments9' in the State. In the words of the

Committee on Co-operative Administration (1964), the Registm is the most

important instrument through which the democratic government has to

translate the social and economic aspirations at the grass root level.

In each state there are Co-operative Banks (SCBs) as the apex level

institutions of the three-tier co-operative short-term credit structure which are

closely linked with the Reserve Bank of India which provide finance to the

District Co-operative Central Banks (DCCBs). They provide liaison between

the Co-operative Societies and the money market. They play a vital role in

mobilizing the financial resources needed by the co-operative movement but

also for deploying them appropriately among the various sectors of the

movement. They establish close contact with their member banks as also with

the Agricultural Credit Societies at the base level. It is observed that "the

State Co-operative Bank is the final link in the chain between the small,

scattered primary societies and the money m k e t as also with the Reserve

Bank of India. It is the Central Banking Authority of the country, which can

be called on for short and medium-term accommodation under certain

condition^"^.

' . Report of the Committee on Co-opera five Administmtion (I%$, p.29. ' Huugh. EM (I 966). The Co.oprraiive Movement in In& (London: Ox/ord University Press). P. 281

The functions of the State Cooperative Banks are to help the State

Governments in formulating development plans with regard to Co-opaative

Institutions; to co-ordinate the po!icies of the co-operatives with the

governments; to formulate and implement uniform credit policies regarding

co-operative development in the state; to act. as bankers bank to DCCBs, to

supervise, control and guide the activities of DCCB; to grant subsidies to

DCCBs for smooth hctioning of Co-operatives and the functions similar to

any Commmial ~ a n k . ~

The State Co-operative Banks finances and controls the workiag of

District Central Co-operative Banks @CCBs) or Central Cooperative Bank

(CCBs) in the State. SCB obtains its working funds from its own share capital

and reserves, deposits from the general public and loans and advances from

NABARD.

3.6. Performance of State Co-operative Banks in different States:

It is clear from table 3.1 that the proportion of owned h d s to the

working capital to the State Co-operative Banks in India decreased from 9.38

per cent in 1960-61 to 8.74 per cent in 1999-2000, indicating the poor

financial resources base. 'However, the own funds increased by 365 times

during 1960-61 to 2002-03. It reflects the poor operational efficiency of State

Co-operative Banks in the country. However, it is a heartening to note that the

ratio of deposits to working capital increased from 32.63 per cent to 84.03 per

cent during the same period. The deposits increased by 5 17 times during the

same period.

6 S u b Red&, S.. and @$urn, P. (2000): "Agricultural Finance and M~(18mun1': Ox/ord and IBH Publishing G m p y Pvt. Lld, New Delhi, pp.18-19.

99

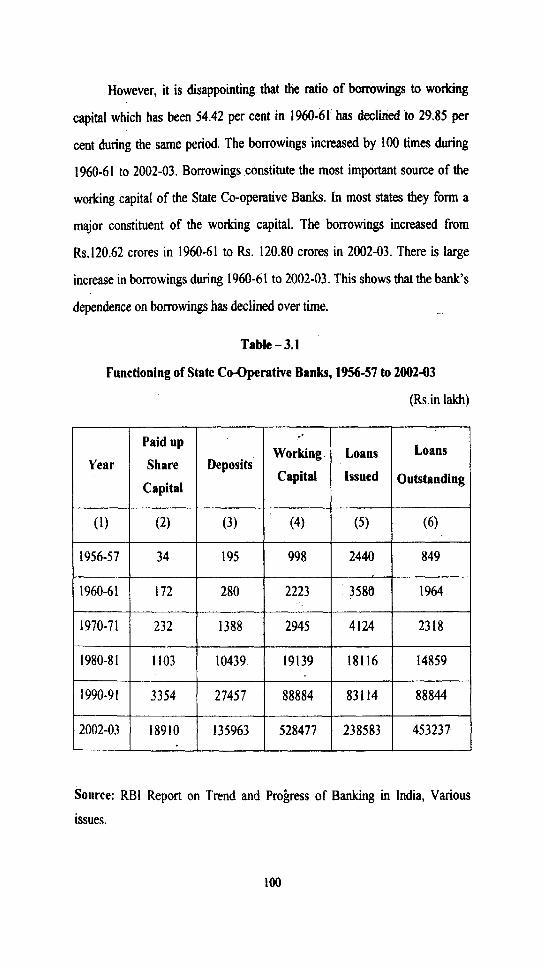

However, it is disappointing that the ratio of borrowings to working

capital which has been 54.42 per cent in 1960-61 has declined to 29.85 per

cent during the same period. The borrowings increased by 100 times during

1960-61 to 2002-03. Borrowings constitute the most important source of the

working capital of the State Co-operative Banks. In most states they form a

major constituent of the working capital. The borrowings increased from

Rs.120.62 crores in 1960-61 to Rs. 120.80 crores in 2002-03. There is large

increase in borrowings during 1960-61 to 2002-03. This shows that the bank's

dependence on borrowings has declined over time.

Table - 3.1

Functioning of State Co-Operative Banks, 1956-57 to 200243

(Rs.in lakh)

Sonrce: RBI Report on Trend and Prokress of Banking in India, Various

issues.

An analysis of table 3.1 shows the paid up share capid of SCBs. The

table reveals that the Share Capital'had increased from Rs.34 lakh 1956-57 to

Rs. 18,910 lakh in 2002-03 showing-an increase of 550 times. The Deposits

increased from Rs.195 lakh to Rs.135963 lakhs during the same period to an

increase of 697 times, the Working Cpital ~incteased from Rs.998 lakh to

Rs.5,28,477 lakh, an increase of 530 times during the same period. The loans

issued increased from Rs.2,440 lakh to Rs.2,38,583 laMn, an inmase of 98

times during the same period. The bans outstanding increased from Rs.849

lakh to Rs.453237 lakh, an increase of 534 times during the same period. The

increase is highest with regard to Deposits, the lowest with regard to loans

issued.

In brief, it can be said that the different types of cooperative

institutions, State Governments, Scheduled Commercial Banks and Regional

Rural Banks (RRBs) provide direct financial assistance to the fanners for

agriculture and allied purposes. It shows the extensive involvement of the Co-

operative Institutions in providing direct fmc ia l assistance to the agriculture

and allied activities. Hence it could be presumed that the contribution of the

Co-operative Institutions is highly significant for the cause of rural

development.

The following table shows progress of State Co-operative Banks in

India during the period from 1960-6 1 to 2002-03.

Table-3.2

Progress of State Co-operntive Banks in India, 1960-61 ta 2002-03 (Rs. in Crores)

Sources : Statistical Statements Relating to Co-operative Movement in India. Reserve Bank of India, Bombay (1960-61 to 1991-92). RBI Report on trend and progress of Banking in India, Various Issues..Statistical Abstract, 2003. Co-operative Credit Structure 2003, NABARD *: The figures in Parentheses are Percentages of Working

Capital. **: the figures in Parentheses are Percentages of Loan

Outstanding.

The above table indicatq that the total advances by the State Co-

operative Banks in India which have stood at Rs.221.65 crore in 1960-61 rose

to Rs.38921.70 crore in 1999-2000. At the same time the percentage of

overdues to the loans outstanding has also been on increase. It has increased

fmin 4.18 per cent in 1960-61 to 81.00 per cent in 200 1-02. This increase in

the overdues indicates the weak recovery performance of these banks.

It can also be observed from the above table that there is an increase in

the amount of deposits of the apex banks. These deposits increased from

Rs.72.33 crore in 1960-61 to Rs.37440 crore in 2002-03.

Regarding the loaning operations of the State Co-operative Banks there

has been a phenomenal increase in the amount of loan operations of the State

Co-operative Banks. The loan amount issued by these banks increased from

Rs. I2 1.65crore in 1960-6 1 to Rs.38320crore in 2002-03. The amount of loan

outstanding overdues moved from Rs.166.67crore in 196M1 to Rs.34860

crore in 2002-03.

The State Co-operative Banks give advance short-term loans for

seasonal agricultural operations and marketing of crops, while medium-term

loans for purchase of cattle and machinery, sinking of well etc.

Table 3.2 further reveals that during the reform period 1992-93 to

2002-03, the loans issued have almost quadrupled. Against these positive

developments, the dues outstanding have almost increased by 39 times since

1975-76 and this accelerated increase is more during the current reform

period. Overdues were not serious problems in the period prior to seventies.

In 1975-76, Rs.4360 crore were the loaned overdues that increased to Rs.29.2

crore by 1985-86. The overdues stood at Rs.133.2 crore in 1995-96, an

increase of 44 per cent over 1992-93. The proportion of overdues to demand

rose from 7 per cent in 1975-76 to an all time high of 84.0 per cent in 2000-

2001 and to fall to 81 per cent in 2001-2002.

On the whole, it can be conclude that the number of SCBs had

increased from 26 in the year 1975-76 to 31 in the year 1%5-86 and declined

to 28 in'the year 1995-96 and again increased to 29 in the year 2002-03.

There is a marginal decline in the number of SCBs during 1975-76 to 2002-

03. As on 3 I* March 2006, the number of SCBs was 30 with 962 branches.

The membership as on date was 1,54,000. The amount of own funds was

Rs.8,43,675, the amount of deposits was Rs.47,67,221 lakh, the borrowings

Rs. 16,87,166, loans advanced Rs.4880354 lakh, loans outstandings

Rs.38,96,099 lakh and the percentage of overdues to demand was 13.76 as on

3 1 " March, 2006. Number of employees was 14,742.

3.7. Caoperative Administration at District Level

In all states, the Deputy or Assistant Registrar or the District Co-

operative Officer with Gazetted Rank acts as the in-charge of Co-operatives in

the district. Where the number of Societies justifies, more-than-one officer at

the district level will be to tun the administration of this department. This

officer has the primary responsibility of promoting and organising co-

operative societies of various types in his district and ensuring that these

societies discharge their obligations in the manner prescribed by the Bye-

laws. The Non-Gazetted Staff working in the District Co-operative

Department consists of two or three categories of oficials, namely sub-

Assistant Registrars, Senior and Junior Inspectors and other Clerical Staff. In

most states, the Co-operative Extension Officers or Assistant Development

Officers (Co-operative) are appointed to look after the affairs of the

cooperative Societies working in the Commudity Development Blocks.

In several states, it so happened that along with the staff for

administration, w i ~ the growing diversification of co-operative activities, a

few functional specialists are also appointed to provide technical advice to the

Registrar in certain technical fields such as marketing, mortgage, banking,

processing, sugar factories, industrial co-operatives, milk co-operatives etc.

The nature and extent of delegation of powers of the Registrar to the officers

of the Co-operation Department shows considerable variation from State to

State. This variation depends uporisthe stage of development of. the co-

operative movement in the State.

Wi+ the establishment of Panchayat ~ a j Institutions d u h g 1960s in

different states in the country, the responsibility for overall development in

the n d are85 including the promotion of co-operation at the village level has

been entrusted to these institutions in certain states. The consequence of the

transfer of certain functions to the Panchayat-Raj bodies is that of dwlity of

control over the Co-operative Department led to the ineffective supervision

over these institutions. It was found that in some places the District Co-

operative Officers were working under the pressure fmm the politicians of the

Panchayat Raj and are not able to inspect or guide the Primary Co-operative

Societies where the interest of the politicians or local leaders were involved.

The District Central Co-operative Banks are federations of PACSs and

their jurisdiction extends over the entire district. These Banks co-ordinate the

activities of top level State Co-Operative Banks and lower level Primary

Credit Societies. Their main task is to lend to Village Societies and to attract

deposits from the general public

In the co-operative structure, the Central Co-operative Banks occupy

the middle tier i.e. the district level. The area of operations and jurisdiction of

a Central Bank is generally confined to a district. The District Central Co-

operative Banks (DCCBs) have opened branches in different parts of the

districts. This branch arrangement helps them to improve their contacts with

and supervision over Primary Agricultural Credit Societies (PACSs). It is the

way it assists also to tap the savings of rural people through deposits. The

DCCB is meant to be the leader of the Credit Co-operative Movement in the

district of its jurisdiction. '

Finding the structure of the central financing agency as very weak, the

Rurd Credit Survey Committee suggested that each state should draw up

plans for the rationalization i d strengthening of Central Co-operative Banks

in several of their financial and administrative aspects. During the First Plan

Period, the statcs began to follow the process of re-organization and

amalgamation of the Central Co-operative Banks. This process was

vigorously followed during the Second Plan period also. The basic principles

prescribed for the Central Bank in each district were followed in all the States.

All the states adopted the policy that there should be only one Central Co-

operative Bank for each district. However, in some states notably, Assam,

Bihar and West Bengal more than one bank are existing.

The functions assigned to the DGCBs are to supervise and inspect the

activities of PACS and help these societies to run smoothly and to maintain

close and continuous contact with the Primary Societies. It provides

leadership to these societies to undertake non-credit activities like supply of

seeds, fertilizers besides sugar, kerosene and other consumer goods. They are

required to provide requisite fimd to the Societies under their control and to

accept deposits from the Member Societies as well as from public.

Besides, several DCCBs do different societies banking business such

as accepting of deposits of various types from the public on current fixed or

saving accounts; collecting bills, cheques, hundis, dividend warrants and

railway receipts. They issue drafts, provide safe custody of valuable goods.

They also take up the purchase and sale of securities and advancing loans at

times to individual members against the fixed deposit receipts.

The DCCBs provide linkages among the three-tier co-operative

structure in each state. The success of PACSs and the apex banks depends

upon the strength and the efficiency of DCCBs. The DCCBs provide

'necessary financial assistance to the PACSs and also support the apex banks

in ensuring greater flow of credit from the NABARD.

As federal organisations,.the DCCBs have an important role to play in

guiding, supervising and directing the financial operations of PACS. The

responsibility of providing timely and adequate credit to the members through

the PACS, for agricultural purposes and providing storage and marketing

facilities to the farmer rests with 3CCBs- The flow of funds from the

NABARD'~~ the co-operative sector depends primarily on the observation of

financial discipline by the DCCB and their capacity to free the over due

problem. As the success of moperative credit in a district depends on the

success of the DCCBs, it is essential to ensure that the f w c i a l base of these

banks is strong and their operations are efficient. The DCCBs arc also

expected to maintain close and continuous touch with the PACSs, be

sympathetic and responsive to their needs and difficulties, and provide

leadership to them from the policy point of view.

It is increasingly appreciated that the DCCBs are eminently suited for

what is described as the financial supervision, i.e, activities relating to

scrutiny as loan applications, verification of disbursement, and watch over

user of loans, prompt recovery through sale of crop and so on7.

After independence, the reorganization and amalgamation, the number

of Central Banks fell from 505 in 1950-5 1 to 478 in 1955-56 and 380 in 1960-

61. However, the number of these banks again fell from 380 in 1960-61 to

346 in 1965-66. On account of this process of rationalization of Central Co-

operative Banks, their number decreased to 341 in 1974. The number of

DCCBs increased from 344 in the year 1975-76 to 352 in 1985-86, 363 in

1995-96,368 in 2001-02 and declined to 343 in 2002-03. On the whole there

is a marginal increase in the DCCBs during last 5 decades. The progress of

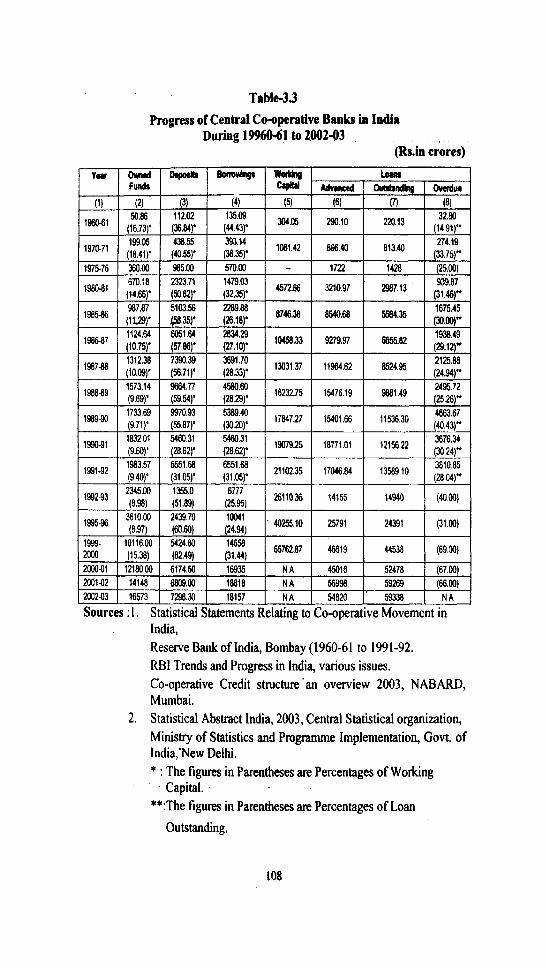

the DCCBs in the country is shown in Table 3.3.

M a r i a , C.B., Op dl. P. 132.

Progress of Central Cooperative Banb in India During ls%o-61 to 2002-03

@.in crires)

India, Reserve Bank of India, Bombay (1960-61 to 199 1-92. RBI Trends and Progress in India, various issues. Co-operative Credit structure 'an overview 2003, NABARD, Mumbai.

2. Statistical Abstract India, 2003, Central Statistical organization, Ministry of Statistics and Programme Implementation, Govt. of India,'New Delhi. * : The figures in Parentheses are Percentages of Working

Capital. **:The figures in Parentheses are Percentages of Loan

Outstanding.

It is clear from the aboye table that the proportion of owned funds to

working capital of DCCBs in India declined from 16.73 per cent in 1960-6 1

to 15.38 per cent in 1999-2000, indicating the p r financial resources base of

these banks. It reflects the operatiod inefficacy of DCCBs.

However, the ratio of deposits to working capital grew from 36.84 per

cent to 82.49 during the same period. At the same time, the ratio of

borrowings to working capital which has been 44.43 per cent in 1960-61 has

deteriorated to 3 1.44 per cent during 1999-2000. This shows that the bank's

dependence on borrowings has declined. The total advances by the DCCBs in

India which have s W at Rs.290.10 c m in 1960-61 hve iwmmd to

Rs.54,820 crore in 2002-03.

The above table indicates that the percentage of overdue to loans

outstanding has been on the increase. It has increased from 14.91 per cent in

1960-61 to 66.00 per cent in 2001-02. This growth in ovcrdues percentage

shows the weak recovery performance of the DCCBs in India.

3.8. Performance of District Central Co-Operative Banks:

The data available on the District Central Co-operative Banks working

in different states show that the number of the District Central Co-operative

Banks (DCCBs) stood at 343 at the end of March, 2003. Similarly the

deposits of DCCBs grew five times between 1975-76 and 1985-86 slightly

more than 2.5 times between 1985-86 and 1992-93. The annual growth in the

deposits of these banks during 1990 decade was to the tune of 40.6 per cent.

The deposits were expected to touch Rs.7298.3 crore by 2003. This growth in

deposits is accompanied by the increased borrowings from the

RBVNABARD. These borrowings were to the tune of Rs.18 15.7 crore in

2002-2003 as against only Rs.570 crore in 1975-76 and rose to Rs.5048.2

crore in 2002-03, an increase of almost 29 times. On the other hand, the loans

outstanding in these banks which stood at R9.142.8 cmfe in 1975-76 rose to

Rs.547.5 crore in 1985-86, indicate 3.8 fold increase. This amount had risen significantly since then and was-Rs.5933.8 crore, an almost I I times increase

since 1985-86. The loans overdue between 1975-76 and 1995-96 grew by 17

times. The proportion of overdues to demand was 25 per cent in 1975-76

which increased to 69 per cent in 199-2000. It rose to the extent of 66 per

cent .in 2001-02 and this kcovery is more significant shce 1995-96. The

volume of business has significantly improved since 1975-76.

3.9. Growth of PACSs in India

The progress of the Primary Agriculture Co-operatives before

independence is shown in the table 3.4.

Table- 3.4

Growth of Co-operative Societies in India during 1906-47

Source: Reserve Bank of India, Review of the Co-operative Movement in India, (Bombay) 1952, P. 1.

Table 3.4 indicates that till the attainment of independence, i.e.

No. (1) 1

1946-47, the Primary Co-operative Societies registered slow progress. There

No. of Societies (In Iakbs)

(3) - 0.02

Year

(2) 1906-10

was a phenomenal increase in the number of these societies, membership and

the working capital. They raised by 85 times, 57 times and 241 times

respectively. No doubt, numerically, the co-operative societies made some

Membership ( in Iakhs)

(4) 1.60

progress but qualitatively it suffered from certain internal as well as external

Working Capital (Rs.in Million)

(5) 6.80

limitations such as illiteracy of the members, willhl default, disloyalty of the

,members, irresponsible administration, mismanagement of funds, irregular

growth, etc.

In spite of all these defiqiencies in the hctioning of the C w p N i v e

Society, they checked the monopoly of money-lenders to certain extent and

also eonsidembly reduced the &rest rates on the loans. Further, the thrift

habit and the spirit of cwperation in&eased urwng the farmers. Commenting

on the role of co-operative sector, a Report of the Reserve Bank of India,

1946 stated: "it had reached a stage where ii could be counted as a factor in

the economic, social and political development of rural ~ndia".

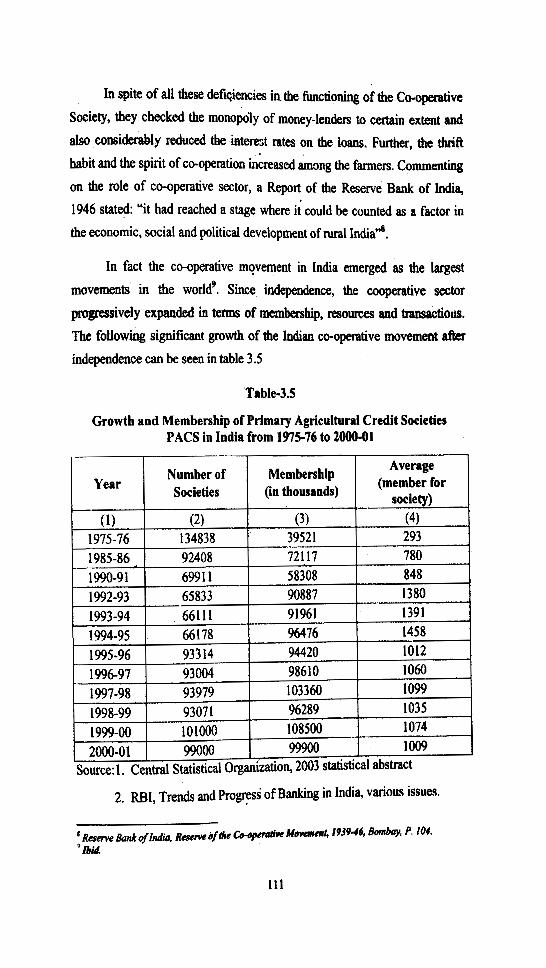

In fact the co-operative movement in India emerged as the largest

movements in the world9. Since independence, the cooperative sector

progressively expanded in tenns of membership, resources and transactous.

The following significant growth of the Indian co-operative movement alter

independence can be seen in table 3.5

Growth and Membership of Primary Agricultural Credit Societies PACS in India from 1975-76 to 200041

2. RBI, Trends and Progress of Banking in India, various issues.

It can be observed from the above data that Co-operatives have made

commendable progress during Five -Year Plans in terms of their membership,

share capifa;l and working capital: Quantitative expansion as measured by the .

number of societies has been stopped by the Reserve Bank since the Third

Plan. It has been the accepted policy of the Reserve Bank since then not to

allow the growth of non-viable and weak societies. Instead, efforts have been

made to merge weak societies with financially strong societies so as to make

the Co-operative Movement stand on its own feet.

It is evident from the table-3.6 that the extent of total loans advanced

by the Primary Agricultural Credit Societies to its members was to the tune of

69807.6 millions in 1992-93 which, has increased to Rs.2,46,388.8 millions in

2000-2001. The short-term loans advanced by the Primary Agricultural Co-

operative Societies accounts for the ajar part, i.e., about 85 per cent out of

total loans advanced, while the medium-term loan form only 15 per cent of

the total advances issued in the year 2000-200 1.

Total Loans Advanced by Primary Agricultural Credit Societies (PACS) in India (1992-93 to 2000-2001)

(Rupees in Miiions)

Source: Analytical study of Primary Agricultural Co-operative Societies in India published by 'NCUI'.

112

At end af IMarch 2001, there were approximately 99,000 PACSs with a membership of 9,99,900. The performance of Primary Agriculw

Cradit Societies shows that the number of borrowing memkrs is much lower

statutory at 46.5 million, i.e., the borrawing members constitute arouad 47 per

cent of the total members. The vast size of over dues resulted in making a

large number of the members ineligible for taking fresh loans. At the end of

March 2001, deposits mobilised by PACS stood at Rs. 1348 1 millions that

increased by 119 times over 1975-76. The 1990s decade registered an

increase of 278 per cent in the d&sits. In other words, the deposits of their

Societies in 1975-76 were Rs.29 which increased to Rs.135, a significant

improvement over the years, but still not significant improvement. Most of

the PACS are dependent on the t i i c e provided by CCBs. In case CCBs are

weak, the PACSs are started of finance, which affects the expansion of both

the credit and non-credit functions of PACSs.

The available statistics reveal that the outstanding borrowings of the

PACS as on March 2001 was to the tune of Rs.25,890 millions. The amount

of loan outstanding with all the PACS in the country increased by 48 per cent

by 1995-96 and it reached Rs.2 1,108 miliibns by the end of March 1999. The

proportion of overdues to the demand that had remained as 40 per cent from

1975-76 till 1992-93 fell sharply to 33 per cent by 1995-96. The PACS a vital

link in the short-term co-operative credit structure, have been fmily weak. A

majority of them are too small in size to be economically viable; when many

are dormant. The PACS continue to rely heavily on external support and have

not yet been able to become self-reliant in respect of resources through

deposit mobilisation, share linkage and share capital. These factors affected

their growth and expansion of business activities. The Co-operative sector

laws are largely responsible for this dismal situatiorl.

On the whole it can concluded at the end of March 2006 the number of

PACSs, FSCS (Farmers Service Co-operative Societies) and LAMPS which

together stands at 1,06,384. The membership in these Societies in 2006 was

1,25,197. The number of.borrowers is 4,60,76,000. The amount of own fiuuls

of their deposits were Rs.92,92,901 lakh, while the amount of @its was to

the tune of Rs.19,56,119 I&, the bomwings Rs.41,01,760 lakh, loans

advanccd Rs.92,91,959 lakh, loan outstanding Rs.51,77,866 lakh and the

percentage of overdues to demand was 30.36 as on 3 1' March, 2006. Number

of employees were 2,4 1,609 for the same date.

Growth of Working Capital of Primary Agricultural Cooperative Societies in India, from 1990-91 to 2000-01

(Rs in crores)

Source: Indian Co-operative Movement - A profile - 2002, Pub. NCUI,

P. 19.

Table 317 shows the gradual growth in extent of working capital of

PACSs in India. This table shows the growth of reserves, deposits and capital

of these societies growth during 1991-92 to 2000-01. It reveals that the total

volume of reserves of these societies had increased from Rs.4156.1 crow to

.Rs.16805.9 crores which indicates an increase of 4 times. Similarly the

deposits of these societies went up by 8 times while the borrowings by 4 times

during the same period.

An Expert Committee of the Planning Commission approved the

formulation of the Model Co-operative Law. The committee suggested that

state shall riot interfere with the management and operation of Co-operative

societies. Towards this end, the state shall' recognisc the Co-operatives as

democratic institutions owned, managed and controlled by the members for

their socio-economic and sxial betterment. The Model Law also simplifies

the procedure for registration of a society and does not give rule making

powers to the go~ernment.

3.10.1. Changes in cooperative laws

The proposed Model Law indicates that (a) the essential basic

principles of Constitution and internal governance which Societies must

observe; (b) specifies the governments' role in ehuring that the spirit of the

law is observed, that elections and annual meetings are held regularly and

audited accounts of prescribed standard are presented at these meetings; and

(c) should restrict the state Government from interfering directly or indinctly

in the internal management of societies, especially in matters affecting the

financial health of the societies. It should explicitly recognise the RBI as the

sole authority to use its powers under the BR Act to ensure observance of

prudential norms by Co-operative Credit Societies, in accepting public (i.e.

non-member) deposits.

The Amended Act of 1912 marked the second phase of the co-

operative movement in Andhra Region. Under the Act, 1912 all lcinds of

societies, credit and non-credit could be registered. The societies were divided

into Agriculture and Non-Agriculture Societies. A large number of Non-

Credit Societies existed for sale of produce, supply of milk, cattle insurance1@.

The Madras Government appointed a committee known as Townsend

Committee in 1927 which recommended among other things to have a

10 Rayudu, C.S., Op. tit, p.69

mitable legislation to remedy the faults in the w o w of 19 12 Act. However,

finally the first Madras Co-operative Societies Act was pwedrby the Madras

Legislative Council in 1932". The striking feature of this stage of movement -

was that it witnessed a hunied expansion in Andhra area of composite Madras

State.

3.1 1. Growth of cooperative sector - DIfTerent forms

By and large, the agricultural development in India is a successful

story. There is a symbiotic relationship between the co-operative development

and agricultural growth in this country. The Co-operative sector provides a

supportive culture for ditlbion of technologies in the agricultural sector in

terms of hardware's (for example sligarcane processing) as well as software's

(farm support and extension services). A salient fmture of the Indian co-

operative movement is that it has not only numerically expanded but has

continuously diversified its activities over the years. In fact it has left almost

no sector of the economy untouched. In addition to traditional activities like

credit, marketing, distribution, etc., it is penetrated into several other fields

like the fisheries, housing, handicrafls and hand loom^'^.

The areas which have recorded substantial agricultural development

are also areas which registered a well developed agricultural Co-operative

management at the grass-root level. Higher production of wheat in Punjab,

sugarcane in Maharashtra, milk and cotton in Gujarat where the cooperative

movement is also well developed illustrates this point.

It is a fact that promotional activities in agriculture, small scale

industry marketing and processing, distribution and supplies are now carried

on through the Co-operatives. The Co-operatives in almost all the states have

made an all-round progress and their role and contribution to agricultural

progress has parti~~~larly been significant. The schemes taken up for the

construction of godowns and the conversion of villages into model villages

, have assumed.greatimpatance in the wake of the green revolution.

--

" hid, P.jSO. I2

~awum. K. Karnra , Op. cit, P.28.

The Co-operative farming is a compmmise between the collective

fanning and the p+s.nt pmprietoikhip and offer all the advantages of l ap

scale fanoing without abolishing the private pmpsny. It implies m

organization of the farmers on the basis of common efforts for common

interests. Under this system, all landowners.in a village form a co-operative

society for tilling the land. The land is pooled, but each farmer retains the

right of property. The produce is distributed by each. They are allowed to

withdraw from the co-operative farm whenever they desire. In India, the

exceedingly small size of holdings is perhaps the most serious defect in our

a&ture. If agriculture has to be impved, the size of tk k d d u g s a k

enlarged. Several types of Co-operatives were formed to serve diffbmt

purpose. Some of them are discussed briefly in the following pages.

3.1 1.1. Commodity Cooperatives

The Commodity Co-operatives have emerged as powehl instruments

for bringing about socio-economic transformation of the rural areas. They are

Milk and Sugarcane Co-operatives whose socio-economic impact on the mi

economy and the people is phenomenal. These societies have accelerated the

pace of rural development in different societies by placing technology and

management in the hands of farmers. The Anand Milk Producers' Union Ltd.,

popularly known as the Amul is a household name in India. It pursues the

famous 'Anand pattern'. i.e., an integrated production oriented system that

enables the rural milk producers to develop scientific temper, thereby

enabling the rural milk producer to lead life of dignity, free from the shaklts

of social and economic exploitation.

The sugar production in India largely occurs in the cooperative sector

(60 per cent), processing of cotton (30 per cent) and Jute (30 per cent) art the

other areas where the Co-operative sectors societies share in the total business

substantial over the years. Apart from the above area, the Co-operative sector

is gaining popularity in several other fields like rice milling, oil seeds

crushing, processing of fruits and vegetables, production and distribution of

chemical fertilisers and pesticides, and distribution of consumer goods. Since

1972, more than 1,000 villages have been covered under the IFFCO's

adoption programmes. Over 2000 seeds-cum-fertiliser drills and over 5000

plant protection equipment5 have been supplied free of costs to the fanners.

Of late, IFFCO has embarked on waste land development though farm

forestry project by establishing Co-operatives for this purpose to enlist

people's participation.

The important goal of a welfare state is to promote and bring about an

element of equality in the society. The mixed-economic model adopted by

planners at the time of independence has led to distortions in income and

employment avenues resulting in skewed pattern of income distribution. It has

become necessary to ensure that rural ~roducers are not unduly exploited by

the market forces controlled by manufacturers and traders. Hence, it is argued

that there is a need to develop a production mechanism controlled by the

producers and the distribution mechanism controlled by the consumers.

Further, it will be desirable for the co-operative sector to come up with sector-

wise vertically and horizontally coordinated plans for development based on a

concept of potentials rather than just economic responsibilities for the weaker

sections and areasI3.

As a sector between the private and public sectors, the cooperative

sector has made remarkable success in the above mentioned fields in recent

years. Its contribution to several productive enterprises, viz., sugar, milk,

cotton, fertilizer, etc., has assigned this sector for bigger role in the socio-

economic development of the country. ow ever, the success of cooperative

sector in the field of agricultural credit was not rated in the past. But in the

recent past, the share of co-operative sector in this field accounts for more

than 60 per cent in a number of states.

IJ M.V. ~Vmjoshi, O.P. Cit, p.549.

There are S~veral ~ W s s e s existing in the worlring of tfie Co-

operatives in the above fields 'which can be attributed mon to the

inadequacies in their operating systems and management system, rather than

the cooperative organisational fmework itself, Their activities their

participatory character, leadership structure p ~ d management systems are of

critical importance to make the Co-operatives function as a living dynamic

entity. The potential of Co-operatives as instruments for rural transformation

have been demonstrated beyond doubt through the outstanding success stories

of the Mulukanoor multi-Co-operative in Andhra Pradesh and the

Warnanagar Sugar Co-operative in Maharashtra. k e m-rpmti~~~.haxc

been evolved on sound organisational principles of co-operation and

management ethos, such as right product-mix committed professionals,

dedicated leadership and application of appropriate management systems.

3.1 1.2. Co-operative Marketing

Apart from providing financial assistance to the farmers, the Co-

operative Societies provide marketing facilities to the farmers to sell away

their produce. The main object of the Co-operative marketing bodies is that

the farmer should get fair value for his produce, his produce should be

measwed in a correct maper and that he should get his payments on time.

3.11.3. Agricultural Processing Co-operative Societies

After the farmer is provided with credit for agricultural activity, by the

network Co-operative societies they require proper processing of produce

them. The Co-operatives step in this process also. The agricultural processing

Societies provide necessary rural capital and labour and thereby secure

reasonable returns to the primary producets. These societies are given

financial assistance for setting up of processing units of agricultural produce

like the Ginning and Pressing in case of the Cotton Growers, Oil Mills, Rice

Mills, Fruit and Vegetable units etc.

3.11.4. Consumers Co-operntive Movement

The consumer co-operative movement gained prominence in the recent

post. These Co-operatives became popular because they help the consumers

get to various essential commodities at fair price, fair weight and fair quality.

The State Co-operative Consumers Federation stands at the top of the

consumers cooperative movement. The federation controls the working of the

Co-operative Consumer Societies which supply goods in wholesale and are

organised district-wise. These wholesale consumer societies distribute the

goods to Primary Co-operative Consumer Societies whose outlets supply

goods to local consumers. Thus the marketing chain is completed.

3.1 1.5. Warehousing facilities by the Co-operatives:

The Agriculture Co-operatives also provide for the storage facilities to

the members under the provisions of the National Grid of Godowns and the

NCDC (National Co-operative Development Corporation) Godowns

Schemes. The Government of India has sanctioned a scheme for

establishment of National Grid Godowns. The main objective of the scheme is

to meet the storage needs of particularly small and marginal fanners. These

godowns are made available to the Agricultural Co-operative Societies,

Agricultural Produce Marketing.

3.12. Contribution by various Cooperative Societies

Over the Last 5 decades the Co-operative sectors have made substantial

contribution to the economic development of country in several ways

particularly t i the rural sector. The folloking table depicts the impressive

progress achieved by the cooperative societies in various fields of the Indian

Economy.

Table-3.8

Share of Different types of Ckperatives in the National Economy

Source: The Co-operator, June 2004

Agricultural Credit Disbursed by ~ & o ~ e m t i v ~ ~ .

Fertilizer Disbursed (6.049 Million Tonne)

Fertilizer Production (3.293 MT- N&P) Nutriknt

Sugar Production (10.400 Million Tonnes)

Wheat Procurement (4.501 Million Tonne)

Animal Feed Production1 Supply

Retail Fair Price Shops (Rurai+Utban)

Milk Procurement to Total Production

Milk Procurement to Marketable Surplus

Ice Cream Manufacture : 45 per cent

Oil Marketed (branded) : 50 per cent

Spindle age in Coops (3.5 18 Million)

Cotton Yarn1 Fabrics Production

Handlooms in Co-operatives

Fishermen in Cg-operatives (active)

Storage Facility (Village Level PACS) '

Direct Employment Generated

Self- Employment Generated for Persons

Self Manufarhlred (18266 Metric Towes)

3.13. Reforms in Co-operative Sector

46.15 per cent

36.22 per cent

27.65 per cent

59.00 per cent

3 1.8 per cent

50 per cent

22 per ccat

7.44 per cent

10.5 per cent

45 per cent

50 per cent

9.5 per cent

23.0 per cent

55.0 per cent

21 .O per cent

65.0 per cent

1.07 Million

14.39 Million

7.6 per cent

The objective of the National Policy on Co-operatives. 2002, is to

facilitate all-round development of Co-operatives in the Counhy. Under this

Policy, the Co-operative Societies would be provided necessary support,

encouragement and assistance to enable them to wok as autonomous, d f -

reliant and democratically managed institutions, which will be accountable to

their members. The policy seeks to achieve hctioning of Co-operatives

based on Co-operative principles and values, reduction of regional

imhalances, professionalisation and greater participation of members in the

management, removal of restrictive regulatory regime and development of an

integrated co-operative stmture etc.

The Central Government has enacted the Multi-State Co-operative

Societies (MSCS) Act, 2002, replacing it's Act passed in 1984. The new Act

removed various restrictive provisions and ensure full hctional autonomy

and democratic management to the Co-operative Societies. The Centre is now

taking up with the State Governments the implementation of legislative and

policy reforms in the co-operative sector."

The Government of India constituted a Task Force under the

Chairmanship of Prof. A. Vaidyanathan in August 2004 to evolve an action

plan for the revival of cooperative credit movement in the country. The Task

Force submitted its Report in 2005, which was accepted by the Government

of India. The important recommendations made by the Task Force are:

(2) Legal and administrative reforms cover the following:

a) Ensuring full voting rights to borrowers and depositors;

b) Removing state intervention in administrative and financial

matters in Co-operatives;

c) Professionalisation of Managements of DCCBs and State Co-

operative Bank,

d) Permitting Co-operatives freedom to take loans from any

financial institution and not necessarily from only the upper tier

and similarly placing their deposits with any financial institution

of their choice;

e) Permitting Co-operatives under the parallel ~ c t s to be members

of upper tiers under the existing Cooperative Societies Acts and

vice versa;

f) Limiting powers of State Governments to supercede Boards

.g) Ensuring timely elections befok the expiry of the term of the

existing Boards;

h) Facilitating fill regulatory powers for RBIMABARD in case of

Co-operative Banks.

After 2004, the extent of cosperative credit to the agricultun was

doubled. Credit Culture, in the effective credit delivery and appropriate credit

pricing were streamlined through necessary steps. The system of credit cards

and no-fiills accounts was initiated. The ~icro-financcprogramme was

intensified and new guidelines for the business facilitator model were issued.

Use of modern technology for rural banking is being encouraged.

3.13.1. Kisan Credit Cards (KCCs)

The newly initiated Kisan Credit Cards System (KCCS) was initiated.

They provide a revolving cash credit facility to the farmers enabling frequent

withdrawals and repayment at the convenienie of the f m r s , which leads to

reduction in the interest burden. It also provides flexibility in the purchase of

inputs from any approved source of fanner's choice; and rescheduling of

loans in case of damage to crops due to natural calamities. This scheme has

been in operation since 1998-99 and 6.45 crore cards have been issued till the

end of 2006. Further, this scheme has extended to the borrowers of the long-

term co-operative credit to meet the requirements of borrowers of the State

Cooperative Agriculture Rural Development Banks (SCARDBs). Under the

KCC system short term/ medium term and long term credit is provided to the

borrowers.

3.13.2. Task Force for Strengthening of Co-operative Credit System:

Under the changed context, the urgent revitalisation of the co-operative

credit structure became an imperative. Towards this end, a Task Force on the

revivcl of Co-operative Credit institutions was constituted under the

chairmanship of A. Vaidhyanathan, to examine the reforms required in the co-

operative banking system. The Task Force recommended

(i) Special financial assistance to wipe out accumulated losses and

strengthen the capital base of Co-operative Credit Institutions;

(ii) Institutional restructuring to ensure democratic institutions; and

(iii) Changes in the legal framework to empower the Reserve Bank of

India (RBI) to enforce prudent financial management.

The Government has accepted the recommendations of the Task Force

in principle and is now working on the modalities for implementation of its

recommendations.

Package for the revival of short-term rural co-operative credit

involving financial assistance of ' Rs. 13,596 crore was announced. The

NABARD is made as the implementing agency. The State Governments are

required to implement the legal, institutional and other reforms as envisaged

in the revival package.