Download - 3Q11 Disclosure and Results

1

Earnings Release | Conference Call – 3Q11November 11th, 2011

2

Summary

Ricardo Ribeiro

COO

Roberto Senna

CEO

Carlos Wollenweber

CFO | IR

3Q11 Highlights

Operational Highlights

Financial Highlights

3Q11 9M11

Launched PSV% Direcional

R$ million 377 1,019

Contracted PSV% Direcional

R$ million 430 863

Sales Over Supply % PSV 36.7% 50.4%

Net Revenues R$ million 298 776

Adjusted Net Income² R$ million 59 151

Adjusted Net Margin² % 20% 19%

Highlights

31. Considering the acquisition of 60% of the residential towers of Parque Ponta Negra project in 2Q11;

2. Adjusted by non-cash expenses (Stock-Options Program).

1

1

4

On September 1st, Direcional signed an agreement with the State of Amazonas and Caixa Economica Federal for the

construction of the 2nd phase of “Meu Orgulho” project in Manaus, with PSV of R$ 313.4 million.

# Units

Segment

Housing PSV

Infrastructure PSV

3,511

MCMV 1st Layer

R$ 149.2 million

R$ 41.4 million

Total PSV R$ 190.6 million

Location Manaus - AM

“Residencial Meu Orgulho” – 1st Phase

Launch 2Q10

# Units

Segment

Housing PSV

Infrastructure PSV

5,384

MCMV 1st Layer

R$ 272.6 million

R$ 40.7 million

Total PSV R$ 313.4 million

Location Manaus - AM

“Residencial Meu Orgulho” – 2nd Phase

Launch 3Q11

Agreement with CEF to develop the 2nd phase of “MeuOrgulho” Project

1st Phase “MCMV”

5

The most relevant player in the very low income segment in Brazil

PAR 2nd Phase “MCMV” RET1+ + +

# of projects: 5

# of Units: 3,602

Total PSV: R$ 153.7 million

Previous to “MCMV”

Program

# of projects: 3

# of Units: 7,391

Total PSV: R$ 380.3 million

# of projects: 2

# of Units: 6,724

Total PSV: R$ 392.5 million

# of projects: 5

# of Units: 2,540

Total PSV: R$ 149.2 million

Units under R$ 75.0

thousand

RET 1% Projects:

# of projects: 5

# of Units: .2,540

PSV: R$ 149.2 million

Very Low Income Projects:

# of projects: 10

# of Units: .17,717

Total PSV: R$ 926.6 million

Large Scale Projects + Industrialized construction process

Petrópolis - AM Meu Orgulho 1st Phase Meu Orgulho 2nd Phase Total Ville Macaé - RJ

Direcional as Contractor Direcional as Developer+

6

Operational Highlights

Launches

Sales

Land Bank

Inventory

Ricardo Ribeiro Operational Highlights

7

Launches

+133%

CAGR 07-10: 82%+56%

Launched PSV

(R$ million)

Launched PSV – Track Record

(R$ million)

162 63

461 575

313

191

313

131

3Q10 3Q11 9M10 9M11

Development MCMV 1st Layer Project Acquisition

1,019

652

377

162

176

710 783

1,067 888

131

2007 2008 2009 2010 9M11

Development Project Acquisition

1,019

Total

(R$'000)

% Direcional

(R$'000)

1 Portal Vistas do Horizonte September Belo Horizonte - MG 95,878 47,939 376 1,172 Medium

2 Total Ville Macaé - 3rd Phase - RET 1 September Macaé - RJ 31,010 15,505 402 1,145 Low-Income

3 Residencial Meu Orgulho - 2nd Phase September Manaus - AM 313,395 313,395 5,384 8,895 MCMV 1 st Layer

440,283 376,839 6,162 11,212

# of Units

Launched

Total Units

(All Phases)Segment

Total

PSV

3Q11 Projects Date City - State

3Q103Q11

9M109M11

60.1%83.2%

58.6% 67.7%

25.7%34.8%

5.6%

14.2% 16.8% 6.7%

26.7%

North Midwest Southeast

3Q103Q11

9M109M11

83.2%

29.2% 35.3%

95.6%

4.1%

46.3%22.4%

4.4%12.7%

21.2%

25.4%

3.2%

5.4%11.5%

MCMV 1st Layer Low-Income Medium Upper-Middle Commercial

Launches Breakdown

Launches

(Segment Breakdown – % PSV)

Launches

(Geographic Breakdown - % PSV)

8

Meu Orgulho 2nd Phase - AM

PSV R$ 313.4 Million

Portal Vistas do Horizonte - MG

PSV R$ 47.9 Million

Total Ville Macaé 3rd Phase - RJ

PSV R$ 15.5 Million

3Q103Q11

9M109M11

35.3%

91.9%

64.3% 68.9%

39.4%

2.5%

22.1% 11.0%

25.3%5.6%

13.6%20.1%

North Midwest Southeast

3Q103Q11

9M109M11

72.8%

30.2% 40.5%

49.2%

11.2%

39.4% 19.8%

24.7%

10.7%

16.2%27.9%

26.1%4.4%

14.2% 7.1%

0.8%

4.8%

MCMV 1st Layer Low-Income Medium Upper-Middle Commercial

143 117

440 461 313

191 313

89

3Q10 3Q11 9M10 9M11

Development MCMV 1st Layer Project Acquisition

143

430

631

863

127

441 661

1,037 774

89

2007 2008 2009 2010 9M11

Development Project Acquisition

863

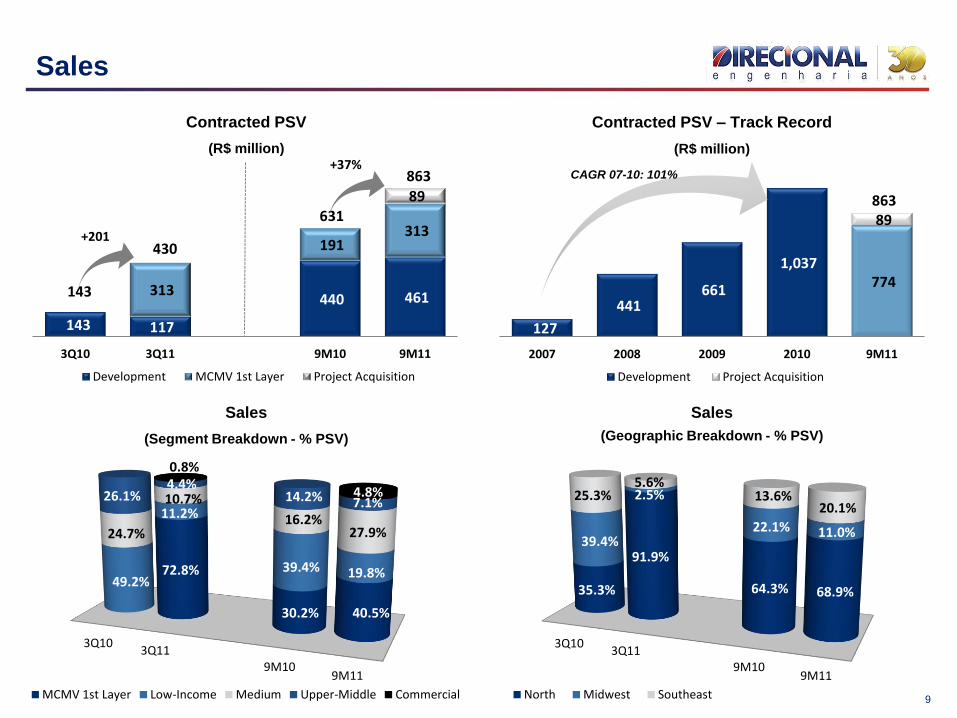

9

Sales

CAGR 07-10: 101%

+201

+37%

Contracted PSV

(R$ million)

Contracted PSV – Track Record

(R$ million)

Sales

(Geographic Breakdown - % PSV)

Sales

(Segment Breakdown - % PSV)

Units Launched in 2Q11 1.732

Contracted Units 700

Contracted in 2Q11 253

Contracted in 3Q11 368

Contracted on October 79

Units to be sold* 1.032

Sales Status: RET1

38.3%

22.1%

36.7%

20.8%

27.6%

18.5%16.0%

3Q10 4Q10 1Q11 2Q11 3Q11

With MCMV 1st Layer project Ex MCMV 1st Layer project

10

Sales Over Supply

(Total PSV)

Sales Speed (%)

(Units)

Sales Status of RET1 Projects (launched in the 2Q11)

Impacted by the lower

launched PSV in the

3Q11

Sales Speed

17%

87%

48%

20%

90%

27%

4%

21%

20%

14%

1%

9%

9% 2%3Q10

4Q10

1Q11

2Q11

3Q11

3M 6M 9M 12M 15M

40%

78%

93%

70%

90%

40%

60%Contracted Units

Units to be sold*

* RET1 sales are subject to the mortgage facility approval by CEF

11

Concluded Projects – 9M11

DF 29%AM

26%

RO 22%

ES 12%

MG 8%

SP 3%

Concluded Projects(Geographic Breakdown % PSV)1 Equilibrium Manaus - AM 2Q11 43,561 136

2 Águas do Madeira Porto Velho - RO 2Q11 40,973 4263 Grand Prix Manaus - AM 2Q11 36,983 1924 Lake View Resort Brasília - DF 2Q11 87,812 2325 Garden Club - Fase 01 Porto Velho - RO 2Q11 27,515 3136 Dream Park Serra - ES 2Q11 35,704 2827 Gran Paradiso Belo Horizonte - MG 3Q11 13,621 1288 Villagio Santa Mônica Belo Horizonte - MG 3Q11 10,219 1209 Vernissage Campinas - SP 3Q11 8,448 58

Total 304,835 1,887

Projects City - StatePSV % Direcional

(R$ '000)UnitsQuarter

Low-Income, 52.4%

Commercial, 4.8% Medium,

36.0%

Upper-Middle,

6.8%

6,757 6,991 581 229

575

4Q10 ACQUIRED LANDSON 9M11

REVIEW OFASSUMPTIONS

LAUNCHES IN9M11

9M1112

Land Bank

59.2% large scale projects (more than 1,000 units);

53.5% in the North and Midwest regions;

52.4% projects in the low-income segment;

45.6% are eligible for the MCMV program.

Geographic Distribution

(PSV % Direcional)

“MINHA CASA, MINHA VIDA”

49.9 thousand units are eligible for the

program, equal to 73.4% of total land bank

Segment Breakdown

(PSV)

ES1.5%

AM13.7%

MG37.6%

RO3.9%

SP6.5%

PA13.4%

DF22.5%

RJ0.9%

Land Bank Evolution 9M11

(PSV - R$ million)

271

286

536

1,050

2,230

2,003

7,984

12,201

9,528

14%

7%

9%

% in Inventory23%

Concluded Projects

2008

2009

2010

2011

Launched Inventory

53

63

95

220

275

886

783

1,067

1,019

7%

12%

21%

% in Inventory27%

Concluded Projects

2008

2009

2010

2011

Launched Inventory

13

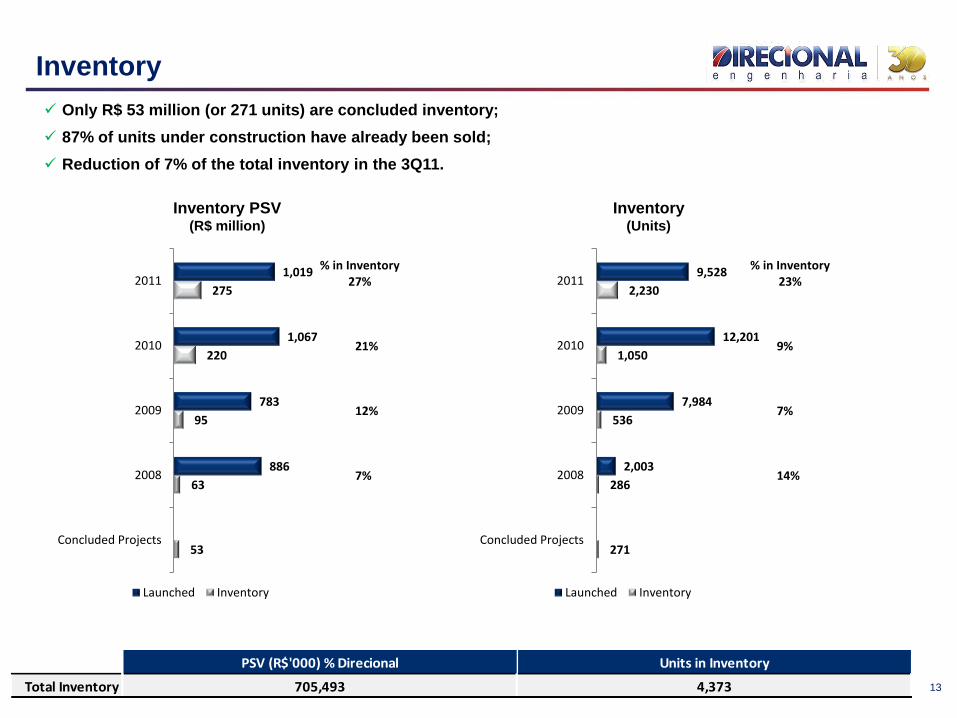

Inventory

Inventory(Units)

Inventory PSV(R$ million)

Only R$ 53 million (or 271 units) are concluded inventory;

87% of units under construction have already been sold;

Reduction of 7% of the total inventory in the 3Q11.

PSV (R$'000) % Direcional Units in Inventory

Total Inventory 705,493 4,373

14

Financial Highlights

Financial Performance

Liquidity Ratios

Deferred Results

DIRR3 Stock Analysis

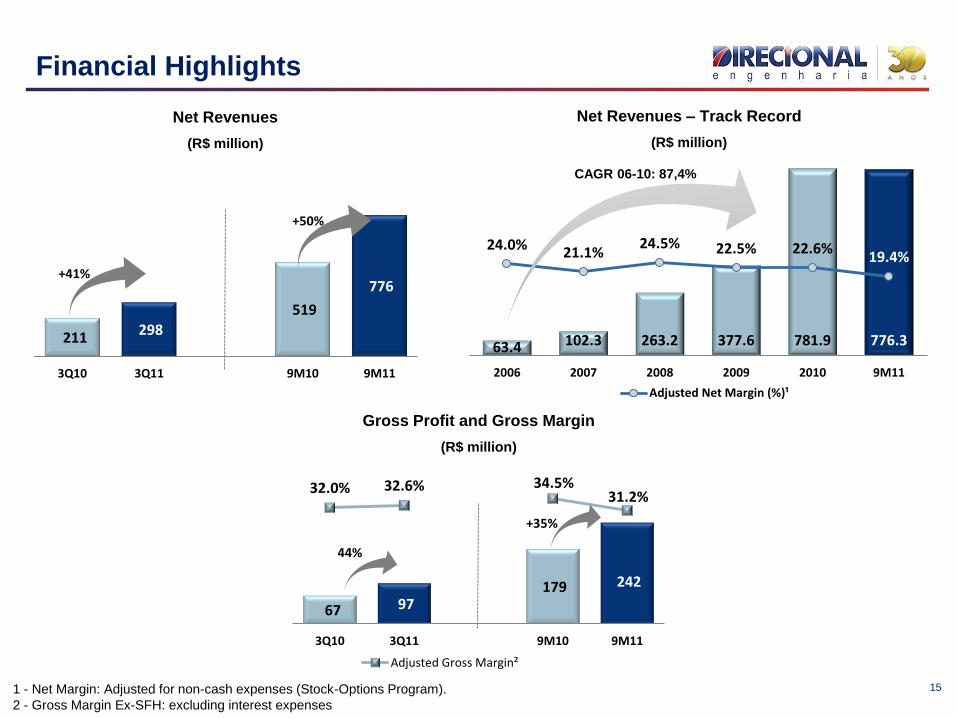

Carlos Wollenweber Financial Highlights

67 97 179 242

32.0% 32.6% 34.5%31.2%

3Q10 3Q11 9M10 9M11

Adjusted Gross Margin²

211 298

519

776

3Q10 3Q11 9M10 9M11

63.4 102.3 263.2 377.6 781.9 776.3

24.0% 21.1%24.5% 22.5% 22.6%

19.4%

2006 2007 2008 2009 2010 9M11

Adjusted Net Margin (%)¹

+41%

+50%

15

Financial Highlights

1 - Net Margin: Adjusted for non-cash expenses (Stock-Options Program).

2 - Gross Margin Ex-SFH: excluding interest expenses

Net Revenues

(R$ million)

CAGR 06-10: 87,4%

Net Revenues – Track Record

(R$ million)

44%

+35%

Gross Profit and Gross Margin

(R$ million)

47 59

126 151

22.4% 20.0%

24.2%

19.4%

3Q10 3Q11 9M10 9M11

Adjusted Net Margin (%)

33 72 69

187

15.2%23.7%

12.8%

23.5%

3Q10 3Q11 9M10 9M11

% Gross Revenue

16

Financial Highlights

Gross Revenues Breakdown 9M11

Adjusted Net Income and Net Margin¹

(R$ million)

Service Revenues

(R$ million)

+120%

+173%

1. Adjusted by non-cash expenses (Stock-Options Program).

+26%

+20%

Development, 76.5%

Management Fee, 0.7%

MCMV 1st Layer, 22.3%

Brokerage Fee, 0.4%

5 6 14 18

2.9%1.3% 1.8% 2.1%

3Q10 3Q11 9M10 9M11

% Sales

13 23

33

57

6.3% 7.8% 6.3% 7.3%

3Q10 3Q11 9M10 9M11

% Net Revenues

51 73

138 179

24.3% 24.6%

26.7%

23.1%

3Q10 3Q11 9M10 9M11

Adjusted EBITDA Margin (%)17

Financial Highlights

Adjusted EBITDA and EBITDA Margin¹

(R$ million)

Adjusted G&A¹

(R$ million)

Commercial Expenses

(R$ million)

+43%

+29%

1. Adjusted by non-cash expenses (Stock-Options Program).

+75%

+74%

+10%

+33%

18

Cash, Debt and Cash Burn

Cash Burn¹ (R$’000)

Loans and Financing

(ex- securitization)

1. Cash Burn: measured by the variation of Net Debt

* 1Q11: Adjusted by R$ 223.8 million of follow-on and R$ 40.3 million of dividends payment

* 3T11: Adjusted in the amount of R$ 15.6 million, from the Share Repurchase Plan

14,52225,312 22,468

32,65741,236

73,695

86,301

100,873

64,967

33,965

51,609

1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11* 2Q11 3Q11*

Moving Average of Last 4 Quarters

3Q11 2Q11 3Q10 D % D %

(R$'000) (a) (b) (c) (a/b) (a/c)

Loans and Financing 437,708 408,630 245,724 7.1% 78.1%

SFH 372,640 341,303 184,243 9.2% 102.3%

Receivables Securitization 35,273 37,216 53,097 -5.2% -33.6%

FINAME and others 9,480 9,149 8,384 3.6% 13.1%

Working Capital 20,315 20,962 0 -3.1% n/a

Cash and Cash Equivalents 343,618 381,768 235,075 -10.0% 46.2%

Net debt 94,090 26,862 10,649

Net debt / Equity 7.9% 2.3% 1.4%

SFH, 92.6%

FINAME and others,

2.4%

Working Capital,

5.0%

19

Deferred Results

REF Recognition Schedule

16.9%

44.5%38.6%

2011 2012 after 2012

Deferred Results Consolidated (R$'000) 3Q11 2Q11 3Q10 D % D %

(a) (b) (c) (a/b) (a/c)

Deferred results Consolidated (1+2) 499,703 413,476 380,825 20.9% 31.2%

Deferred revenues 1,325,614 1,076,829 979,936 23.1% 35.3%

Deferred results - Margin 37.7% 38.4% 38.9% -0.7 p.p. -1.2 p.p.

Deferred results Development (1) 328,803 312,496 278,536 5.2% 18.0%

Deferred revenues 773,964 723,042 673,976 7.0% 14.8%

Deferred results - Margin 42.5% 43.2% 41.3% -0.7 p.p. 1.2 p.p.

Deferred results MCMV 1st Layer projects (2) 170,899 100,979 102,289 69.2% 67.1%

Deferred revenues 551,651 353,787 305,960 55.9% 80.3%

Deferred results - Margin 31.0% 28.5% 33.4% 2.4 p.p. -2.5 p.p.

1,151

1,651

1,345

500

Book Value 3Q11 REF Book Value + REF Market Cap20

Share Repurchase Plan

Market Cap = 82%BV + REF

Date: 11/09/2011

Term 60 days 180 days

Starting date 8/12/2011 10/24/2011

Expiring date 10/11/2011 4/20/2012

Status finished active

# of shares approved by the Board (a) 4,500,000 4,000,000

# of repurchased shares (b) 1,633,800 -

% (b/a) 36.3% 0.0%

Buy back Approved (c) 35,000,000.00 30,000,000.00

Total Expenses 15,618,904.00 0.00

% (d/c) 44.6% 0.0%

Average price 9.56 0.00

Share Repurchase Plan - Details Plan 1 Plan 2

0

20

40

60

80

100

120

140

160

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

19

-No

v-0

9

7-D

ec-0

9

22

-De

c-0

9

12

-Jan

-10

28

-Jan

-10

12

-Fe

b-1

0

3-M

ar-1

0

18

-Mar

-10

5-A

pr-

10

20

-Ap

r-1

0

6-M

ay-1

0

21

-May

-10

9-J

un

-10

25

-Ju

n-1

0

13

-Ju

l-1

0

30

-Ju

l-1

0

17

-Au

g-1

0

6-S

ep

-10

30

-Se

p-1

0

18

-Oct

-10

3-N

ov-

10

23

-No

v-1

0

8-D

ec-1

0

28

-De

c-1

0

13

-Jan

-11

31

-Jan

-11

15

-Fe

b-1

1

2-M

ar-1

1

21

-Mar

-11

5-A

pr-

11

20

-Ap

r-1

1

9-M

ay-1

1

24

-May

-11

8-J

un

-11

24

-Ju

n-1

1

11

-Ju

l-1

1

26

-Ju

l-1

1

10

-Au

g-1

1

25

-Au

g-1

1

12

-Se

p-1

1

27

-Se

p-1

1

13

-Oct

-11

28

-Oct

-11

Pre

ço d

a A

ção

Vo

lum

e (

R$

mil)

Volume (R$ '000)

0

20

40

60

80

100

120

140

160

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

18

-No

v-0

9

4-D

ec-0

9

21

-De

c-0

9

11

-Jan

-10

27

-Jan

-10

11

-Fe

b-1

0

2-M

ar-1

0

17

-Mar

-10

1-A

pr-

10

19

-Ap

r-1

0

5-M

ay-1

0

20

-May

-10

8-J

un

-10

24

-Ju

n-1

0

12

-Ju

l-1

0

29

-Ju

l-1

0

16

-Au

g-1

0

3-S

ep

-10

29

-Se

p-1

0

15

-Oct

-10

1-N

ov-

10

22

-No

v-1

0

7-D

ec-1

0

27

-De

c-1

0

12

-Jan

-11

28

-Jan

-11

14

-Fe

b-1

1

1-M

ar-1

1

18

-Mar

-11

4-A

pr-

11

19

-Ap

r-1

1

6-M

ay-1

1

23

-May

-11

7-J

un

-11

22

-Ju

n-1

1

8-J

ul-

11

25

-Ju

l-1

1

9-A

ug-

11

24

-Au

g-1

1

9-S

ep

-11

26

-Se

p-1

1

11

-Oct

-11

27

-Oct

-11

Sto

ck P

erf

orm

ace

Vo

lum

e (

R$

'00

0)

Average Volume (21 days) Ibovespa IMOB Direcional

21

Shares Performance Since IPO

Since IPO

DIRR3: -14.0%

IBOVESPA: -13.5%

IMOB: -11.5%

22

Disclosure

This presentation contains certain forward-looking statements concerning the business prospects,

projections of operating and financial results and growth potential of the Company, which are based on

management’s current expectations and estimates of the future performance of the Company. Although the

Company believes such forward-looking statements are based on reasonable assumptions, it can give no

assurance that its expectations will be achieved. Expectations and estimates that are based on the future

prospects of the Company are highly dependent upon market behavior, Brazil’s political and economic

situation, existing and future regulations of the industry and international markets and, therefore, are

subject to changes outside the Company’s and management’s control. The Company undertakes no

obligation to update any information contained herein or to revise any forward-looking statement as a result

of new information, future events or other information.

23

Contacts

Carlos WollenweberCFO | IR Officer

Jose Francisco DutraTreasurer | IR

Lucas BousasIR Analyst

Paulo SousaIR Analyst

www.direcional.com.br

+55 (31) 3214-6200

+55 (31) 3214-6450