Accounting For Leases

hapter21

An electronic presentation by Norman Sunderman Angelo State University

An electronic presentation by Norman Sunderman Angelo State University

COPYRIGHT © 2007 Thomson South-Western, a part of The Thomson Corporation. Thomson, the Star logo, and South-Western are trademarks used herein under license.

C

Intermediate AccountingIntermediate Accounting 10th edition 10th edition

Nikolai Bazley JonesNikolai Bazley Jones

2

1. Explain the advantages of leasing.2. Understand key terms related to leasing.

3. Explain how to classify leases of personal property.

4. Account for a lessee’s operating and capital leases.

5. Understand disclosures by the lessee.

Objectives

3

6. Account for a lessor’s operating, direct financing, and sales-type leases.

7. Understand disclosures by the lessor.

8. Explain the conceptual issues regarding leases.

9. Understand lease issues related to real estate, sale-leaseback issues, leveraged leases, and changes in lease provisions (Appendix)

Objectives

4

A lease is an agreement between a lessor and a lessee that conveys to the

lessee the right to use specific property, real or personal, owned by the lessor, for a stated period of time.

In return for this right, the lessee agrees to make periodic cash

payments to the lessor.

A lease is an agreement between a lessor and a lessee that conveys to the

lessee the right to use specific property, real or personal, owned by the lessor, for a stated period of time.

In return for this right, the lessee agrees to make periodic cash

payments to the lessor.

Definition of Lease

5

Financial benefits Risk benefit Tax benefit Financial reporting

benefit-no liability recorded

Billing benefit-pass through on contracts, including interest

Advantages of Leasing from Lessee’s Viewpoint

6

The lease provides 100% financing, so that the lessee acquires the asset without having to make a down payment.

The lease contract contains fewer restrictive provisions and is more flexible than other debt agreements.

The leasing arrangement creates a claim that is against only the leased equipment and not against all assets.

Financial BenefitsFinancial Benefits

Advantages of Leasing from Lessee’s Viewpoint

7

Financial Reporting BenefitFinancial Reporting Benefit

Companies A and B have identical financial data:

Current assets $2,100,000Noncurrent assets 2,900,000Current liabilities 1,000,000Noncurrent liabilities 1,600,000Stockholders’ equity 2,400,000

Companies A and B have identical financial data:

Current assets $2,100,000Noncurrent assets 2,900,000Current liabilities 1,000,000Noncurrent liabilities 1,600,000Stockholders’ equity 2,400,000

ContinuedContinuedContinuedContinued

Advantages of Leasing from Lessee’s Viewpoint

8

On December 31, 2007, A Company purchases equipment with a 10-year life, at a cost of $2,825,112, by signing a 10-year, 12% note requiring $500,000 to be paid at the end of each year beginning December 31, 2008.

On December 31, 2007, A Company purchases equipment with a 10-year life, at a cost of $2,825,112, by signing a 10-year, 12% note requiring $500,000 to be paid at the end of each year beginning December 31, 2008.

Before Acquisition Current Ratio:

$2,100,000

$1,000,000= 2.10

Advantages of Leasing from Lessee’s Viewpoint

9

On December 31, 2007, A Company purchases equipment with a 10-year life, at a cost of $2,825,112, by signing a 10-year, 12% note requiring $500,000 to be paid at the end of each year beginning December 31, 2008.

On December 31, 2007, A Company purchases equipment with a 10-year life, at a cost of $2,825,112, by signing a 10-year, 12% note requiring $500,000 to be paid at the end of each year beginning December 31, 2008.

After Acquisition Current Ratio:After Acquisition Current Ratio:

$2,100,000

$1,446,429= 1.45

ContinuedContinuedContinuedContinued

Advantages of Leasing from Lessee’s Viewpoint

10

On December 31, 2007, B Company leases similar equipment to that leased by A

Company, agreeing to pay $500,000 rent each year for the next 10 years. Assuming

12% interest, the present value of the lease is $2,825,112 ($500,000 x 5.650223).

On December 31, 2007, B Company leases similar equipment to that leased by A

Company, agreeing to pay $500,000 rent each year for the next 10 years. Assuming

12% interest, the present value of the lease is $2,825,112 ($500,000 x 5.650223).

Before Acquisition Current Ratio:

$2,100,000

$1,000,000= 2.10

After Acquisition Current Ratio:

$2,100,000

$1,000,000= 2.10

The ratio of debt to stockholders’ equity would remain at 1.08-to-1.

Advantages of Leasing from Lessee’s Viewpoint

11

The ratio of debt to stockholders’ equity would increase from 1.08 before acquisition

to 2.26 after acquisition.

The ratio of debt to stockholders’ equity would increase from 1.08 before acquisition

to 2.26 after acquisition.

On December 31, 2007, A Company purchases equipment with a 10-year life, at a cost of $2,825,112, by signing a 10-year, 12% note requiring $500,000 to be paid at the end of each year beginning December 31, 2008.

On December 31, 2007, A Company purchases equipment with a 10-year life, at a cost of $2,825,112, by signing a 10-year, 12% note requiring $500,000 to be paid at the end of each year beginning December 31, 2008.

ContinuedContinuedContinuedContinued

Advantages of Leasing from Lessee’s Viewpoint

$2,600,000 $5,425,112$2,400,000 $2,400,000$2,600,000 $5,425,112$2,400,000 $2,400,000

= 1.08 = 2.26

12

Current liabilities-LEASE

$1,000,000Plus: Noncurrent liabilities

1,600,000Equals:

$2,600,000Divided by: Stockholders’ equity

2,400,000Equals: Debt to Equity ratio

1.08

Current liabilities-LEASE

$1,000,000Plus: Noncurrent liabilities

1,600,000Equals:

$2,600,000Divided by: Stockholders’ equity

2,400,000Equals: Debt to Equity ratio

1.08

Current liabilities-PURCHASE $1,500,000Plus: Noncurrent liabilities 3,925,112Equals: $5,425,112Divided by: Stockholders’ equity 2,400,000Equals: Debt to Equity ratio 2.26

Current liabilities-PURCHASE $1,500,000Plus: Noncurrent liabilities 3,925,112Equals: $5,425,112Divided by: Stockholders’ equity 2,400,000Equals: Debt to Equity ratio 2.26

Advantages of Leasing from Lessee’s Viewpoint

13

Bargain purchase option

Bargain renewal optionEstimated economic life

of leased propertyEstimated residual

value of leased propertyExecutory costsFair value of leased

propertyGuaranteed residual

valueInception of the leaseInitial direct costs

There’s more.There’s more.

FASB Statement No. 13 as Amended and

interpreted defines a number of lease terms.

FASB Statement No. 13 as Amended and

interpreted defines a number of lease terms.

Key Terms Related to Leasing

14

Interest rate implicit in the leaseLease termLessee’s incremental borrowing rateManufacturer’s or dealer’s profit or lossMinimum lease payments- present valueMinimum lease payments receivable-

grossUnguaranteed residual valueUnreimbursable cost

Key Terms Related to Leasing

15

Column AA. The lease transfers ownership of the property to

the lessee by the end of the lease term.B. The lease contains a bargain purchase option.C. The lease term is equal to 75% or more of the

estimated economic life of the leased property.D. The present value of the minimum lease payments

is equal to 90% or more of the fair value of the leased property to the lessor.

Criteria applicable to both lessee and lessor.

Classification of Leases Involving Personal Property

16

Column B The collectibility of the minimum lease

payments is reasonably assured. No important uncertainties surround the

amount of unreimbursable costs yet to be incurred by the lessor under the lease.

Criteria applicable only to lessor.

Classification of Leases Involving Personal Property

17

A capital lease meets one or

more of Column A criteria.

A capital lease meets one or

more of Column A criteria.

An operating lease does not meet any of

the Column A criteria.

An operating lease does not meet any of

the Column A criteria.

Classification by Classification by the Lesseethe Lessee

Classification by Classification by the Lesseethe Lessee

Classification of Leases Involving Personal Property

18

LeaseCriteria

andClassifications

19

A sales-type lease must meet one or more of the criteria

listed in Column A and both criteria listed in Column B.

A sales-type lease must meet one or more of the criteria

listed in Column A and both criteria listed in Column B.

Classification by Classification by the Lessorthe Lessor

Sale-type leaseSale-type lease

Classification by Classification by the Lessorthe Lessor

Sale-type leaseSale-type lease

It must involve a transaction giving rise to a manufacturer’s or

dealer’s profit or loss to the lessor.

It must involve a transaction giving rise to a manufacturer’s or

dealer’s profit or loss to the lessor.

Classification of Leases Involving Personal Property

20

It must not involve a transaction giving rise to a manufacturer’s or

dealer’s profit or loss to the lessor.

It must not involve a transaction giving rise to a manufacturer’s or

dealer’s profit or loss to the lessor.

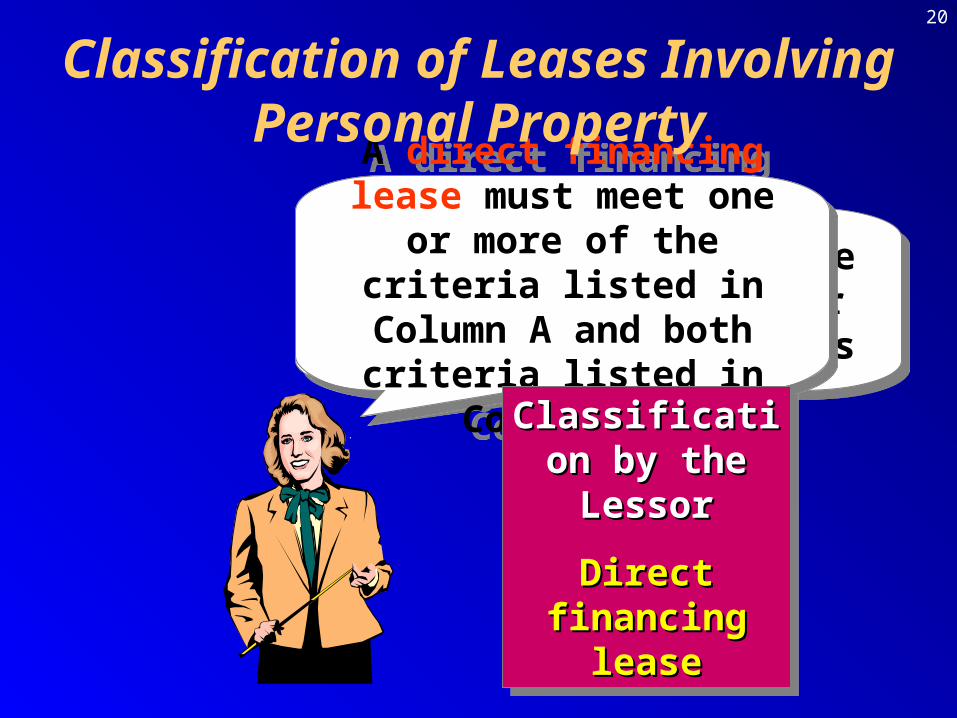

A direct financing lease must meet one or more of the

criteria listed in Column A and both criteria listed in

Column B.

A direct financing lease must meet one or more of the

criteria listed in Column A and both criteria listed in

Column B.

Classification by Classification by the Lessorthe Lessor

Direct financing Direct financing leaselease

Classification by Classification by the Lessorthe Lessor

Direct financing Direct financing leaselease

Classification of Leases Involving Personal Property

21

Classification by Classification by the Lessorthe Lessor

Operating leaseOperating lease

Classification by Classification by the Lessorthe Lessor

Operating leaseOperating lease

An operating lease meets none of the criteria in Column A or does

not meet both criteria in Column B.

An operating lease meets none of the criteria in Column A or does

not meet both criteria in Column B.

Classification of Leases Involving Personal Property

22

User Company signed a lease agreement with Owner Company whereby User Company agrees to pay

$50,000 each year beginning on January 1, 2007, and continuing through January 1, 2011.

Operating Lease (lessee)

23

Go to Example 21-1 and

determine how many of Group A criteria are met.

Go to Example 21-1 and

determine how many of Group A criteria are met.

Since none are met, this is an

operating lease.

Since none are met, this is an

operating lease.

Operating Lease (Lessee)

24

Operating Lease (Lessee)

25

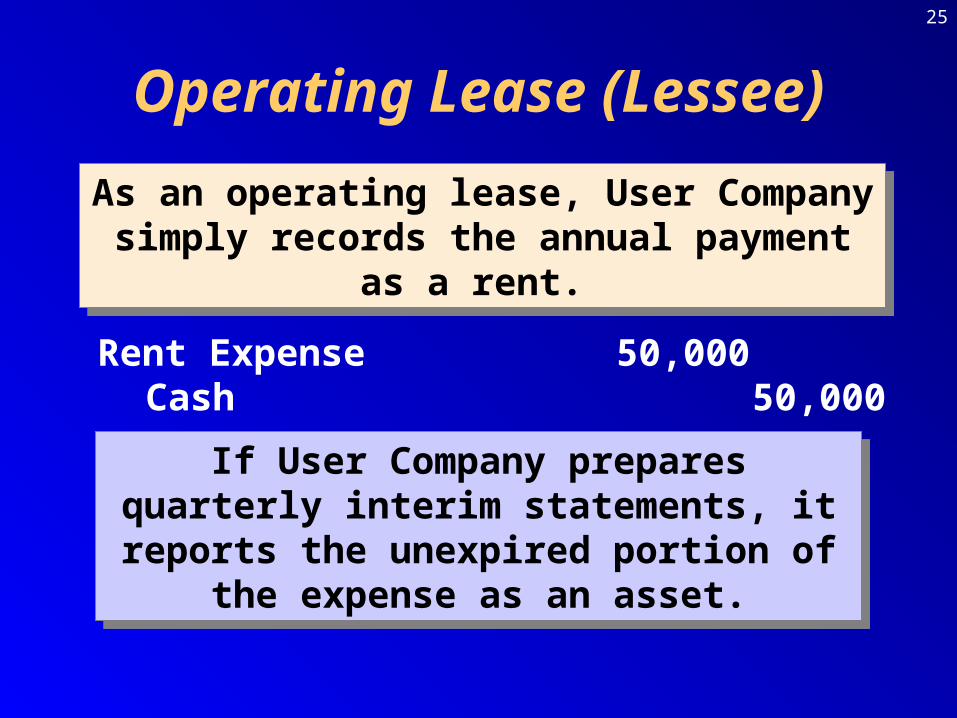

As an operating lease, User Company simply records the annual payment as a rent.

As an operating lease, User Company simply records the annual payment as a rent.

Rent Expense 50,000Cash 50,000

If User Company prepares quarterly interim statements, it reports the unexpired portion of

the expense as an asset.

If User Company prepares quarterly interim statements, it reports the unexpired portion of

the expense as an asset.

Operating Lease (Lessee)

26

The term “minimum lease payments” includes the

present value of1. Minimum rental payments.2. Guaranteed residual value.3. Amount payable for failure to

renew.4. Any bargain purchase option.

Ignore residual, if there is a bargain purchase option.

The term “minimum lease payments” includes the

present value of1. Minimum rental payments.2. Guaranteed residual value.3. Amount payable for failure to

renew.4. Any bargain purchase option.

Ignore residual, if there is a bargain purchase option.

Minimum Lease Payments

27

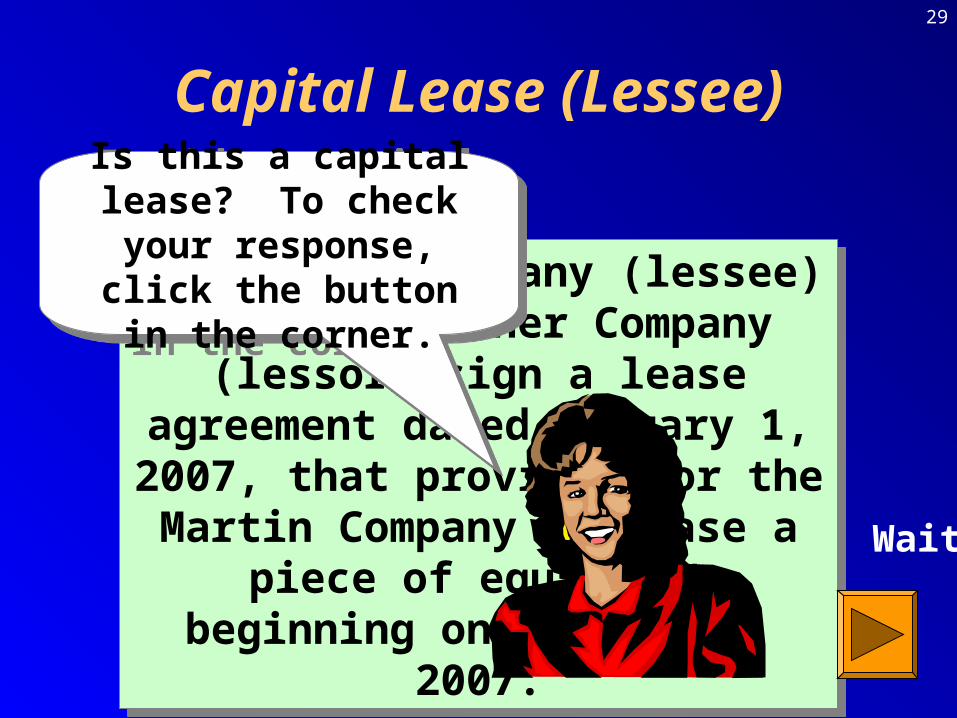

The Martin Company (lessee) and the Gardner Company (lessor) sign a lease agreement dated January 1, 2007, that provides for the Martin

Company to lease a piece of equipment beginning on January 1,

2007.

The Martin Company (lessee) and the Gardner Company (lessor) sign a lease agreement dated January 1, 2007, that provides for the Martin

Company to lease a piece of equipment beginning on January 1,

2007.

Capital Lease (Lessee)

28

LesseeMartin Company (page 1077)

Is this a capital lease?

29

The Martin Company (lessee) and the Gardner Company (lessor) sign a lease agreement dated January 1, 2007, that provides for the Martin

Company to lease a piece of equipment beginning on January 1,

2007.

The Martin Company (lessee) and the Gardner Company (lessor) sign a lease agreement dated January 1, 2007, that provides for the Martin

Company to lease a piece of equipment beginning on January 1,

2007.

Is this a capital lease? To check your response, click the button in the corner.

Is this a capital lease? To check your response, click the button in the corner.

Capital Lease (Lessee)

Wait

30Example 21-5Example 21-5

32,923.45 12,000.00 20,923.45 79,076.55

2. LeasePayment

Cr

Interest 12%Expense

Dr

DecreaseLiability in

BalanceDr Balance

100,000.00

32,923.45 9,489.19 23,434.26 55,642.29

32,923.45 6,677.07 26,246.38 29,395.91

32,923.45 3,527.54 29,395.91 0

31

Initial Recording of Capital Lease on January 1, 2007

Leased Equipment 100,000.00 Capital Lease Obligation 100,000.00

December 31, 2007

Interest Expense 12,000.00Capital Lease Obligation 20,923.45

Cash 32,923.45

12% x $100,00012% x $100,000

$32,923.45 - $12,000.00$32,923.45 - $12,000.00ContinuedContinuedContinuedContinued

Capital Lease (Lessee)

32

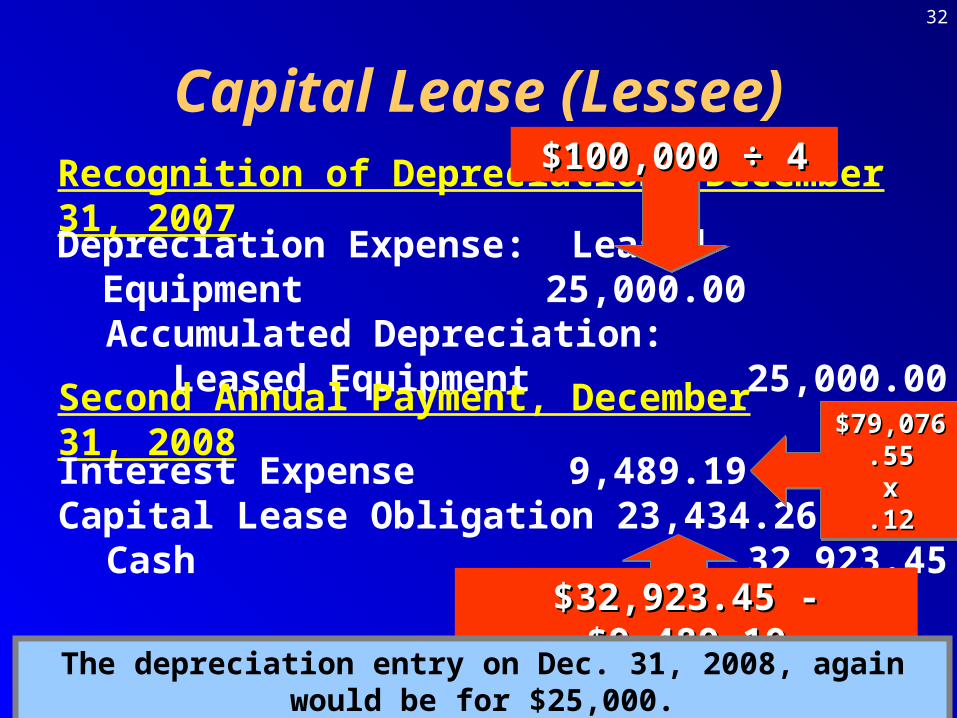

Recognition of Depreciation, December 31, 2007Depreciation Expense: Leased Equipment 25,000.00

Accumulated Depreciation: Leased Equipment 25,000.00

Second Annual Payment, December 31, 2008Interest Expense 9,489.19Capital Lease Obligation 23,434.26

Cash 32,923.45

$100,000 ÷ 4$100,000 ÷ 4

$32,923.45 - $9,489.19$32,923.45 - $9,489.19

The depreciation entry on Dec. 31, 2008, again would be for $25,000.

Capital Lease (Lessee)

$79,076.55$79,076.55xx

.12.12

$79,076.55$79,076.55xx

.12.12

33

Assume that Martin Company is required to make lease payments in advance on January 1 of

each year,...

Assume that Martin Company is required to make lease payments in advance on January 1 of

each year,...

…and that the cost and fair value of the

equipment is $112,000.

…and that the cost and fair value of the

equipment is $112,000.

Present value of four payments of $32,923.45 in advance at 12% = $32,923.45 x

3.401831= $112,000

Capital Lease (Lessee)

34Example 21-6Example 21-6

2007 32,923.45 9,489.19 23,434.26 55,642.29

2008 32,923.45 6,677.07 26,246.38 29,395.91

2. LeasePayment

Cr

Interest 12%Expense

Dr

DecreaseLiability in

BalanceDr Balance

112,000.00

2009 32,923.45 3,527.54 29,395.91 0

1/1/07 32,923.45 79,076.55

35

Initial Recording of Capital Lease on Jan. 1, 2007 Leased Equipment 112,000.00

Capital Lease Obligation 112,000.00

First Payment in Advance, January 1, 2007Capital Lease Obligation 32,923.45

Cash 32,923.45

ContinuedContinuedContinuedContinued

Capital Lease (Lessee)

36

Recognition of Depreciation, December 31, 2007 Depreciation Expense: Leased Equipment 28,000.00

Accumulated Depreciation: Leased Equipment 28,000.00

Recognition of Interest Expense, December 31, 2007

Interest Expense 9,489.19Accrued Interest on Capital Lease Obligation 9,489.19

$112,000 ÷ 4$112,000 ÷ 4

$79,076.55 x 0.12$79,076.55 x 0.12

ContinuedContinuedContinuedContinued

Capital Lease (Lessee)

37

Recognition of Depreciation, December 31, 2008 Depreciation Expense: Leased Equipment 28,000.00

Accumulated Depreciation: Leased Equipment 28,000.00

Second Annual Payment in Advance, January 1, 2008

Accrued Interest on Capital Lease Obligation 9,489.19Capital Lease Obligation 23,434.26

Cash 32,923.45

Capital Lease (Lessee)

38

Redd Company leases equipment for 4 years and agrees to pay $2,000 at the end of the fourth year to purchase the asset. Redd is reasonably assured that it will

exercise the option. Redd’s incremental borrowing rate is 11% and the lessor’s

implicit interest rate is 10%. The cost and fair value of the equipment is $128,160.63.

Redd Company leases equipment for 4 years and agrees to pay $2,000 at the end of the fourth year to purchase the asset. Redd is reasonably assured that it will

exercise the option. Redd’s incremental borrowing rate is 11% and the lessor’s

implicit interest rate is 10%. The cost and fair value of the equipment is $128,160.63.

Does this qualify as a capital lease?

Does this qualify as a capital lease?

Yes…because of the bargain purchase

option.

Yes…because of the bargain purchase

option.

Bargain Purchase Option

39

The minimum lease payments, based on the lower 10% rate, is calculated as follows:

The minimum lease payments, based on the lower 10% rate, is calculated as follows:

Present value of the annual payments discounted at 10% ($40,000 x 3.169865) $126,794.60

Add: Present value of the single sum of $2,000(the bargain purchase option) discounted at 10% ($2,000 x 0.683013) 1,366.03

Present value of the minimum lease payments $128,160.63

Present value of the annual payments discounted at 10% ($40,000 x 3.169865) $126,794.60

Add: Present value of the single sum of $2,000(the bargain purchase option) discounted at 10% ($2,000 x 0.683013) 1,366.03

Present value of the minimum lease payments $128,160.63

Leased Equipment 128,160.63 Capital Lease Obligation 128,160.63

Leased Equipment 128,160.63 Capital Lease Obligation 128,160.63

Bargain Purchase Option

40

Karpas Company leases equipment for 4 years that cost the lessor $147,284.99 (its fair

value) and agrees to pay an annual rent of $40,000 at the end of each year. Karpas Company

agrees to guarantee the estimated residual value of

$30,000 at the end of the fourth year. Assume a 10% interest

rate.

Karpas Company leases equipment for 4 years that cost the lessor $147,284.99 (its fair

value) and agrees to pay an annual rent of $40,000 at the end of each year. Karpas Company

agrees to guarantee the estimated residual value of

$30,000 at the end of the fourth year. Assume a 10% interest

rate.

Guaranteed Residual Value

41

Leased Equipment Under Capital Leases

147,284.99

Accumulated Depreciation: Leased Equipment

117,284.99

Obligation Under Capital Leases

30,000.00

At the end of the lease, both parties agree that the

equipment is worth only $20,000, but the guaranteed

residual was $30,000.

At the end of the lease, both parties agree that the

equipment is worth only $20,000, but the guaranteed

residual was $30,000.

Accumulated Depreciation: Leased Equip. 117,284.99Capital Lease Obligation 30,000.00Loss on Disposal of Leased Equipment 10,000.00

Leased Equipment 147,284.99Cash 10,000.00

Guaranteed Residual Value

117,284.99

42

If the fair value is more than $30,000, the lessee pays the

liability in full by returning the asset to the lessor.

If the fair value is more than $30,000, the lessee pays the

liability in full by returning the asset to the lessor.

Guaranteed Residual Value

43

Exhibit 21-5 provides the disclosure

requirements for a lessee.

Disclosure Requirements for Lessee

44

On January 1, 2007, Brahms Inc. leases equipment with a fair value of $100,000, an

economic life of four years and a lease term of three years. Brahms incremental borrowing rate

is 10%. There is a bargain purchase option at that time of $10,000. The first payment is due

immediately. Find the payment and the amount to be capitalized.

On January 1, 2007, Brahms Inc. leases equipment with a fair value of $100,000, an

economic life of four years and a lease term of three years. Brahms incremental borrowing rate

is 10%. There is a bargain purchase option at that time of $10,000. The first payment is due

immediately. Find the payment and the amount to be capitalized.

Cost Given-Find Rental Payments

45

Cost or fair value of leased asset(amount capitalized if residual guaranteed)

Less: Present value of residual or bargain purchaseYields: Present value to be recovered through rental payments

(amount capitalized if residual unguaranteed)Find: Lease payment for principal and interestPlus: Executory costs (not present valued)Equals: Minimum rental payment

(regardless of whether residual guaranteed)

Cost Given-Find Rental Payments

46

Cost or fair value of leased asset $100,000(amount capitalized if residual guaranteed)

Less: Present value of residual or bargain purchase 7,513Yields: Present value of rental payments $92,487

(amount capitalized if residual unguaranteed)

Find: Lease payment for principal and interest 33,809Plus: Executory costs (not present valued) 0Equals: Minimum rental payment

(regardless of whether residual guaranteed) $33,809

Cost Given-Find Rental Payments

47

Annual Interest Reduction of LeasePayment Expense Obligation Obligation

1/1/07 $100,0001/1/07 $33,809 0 $33,809 66,1911/1/08 33,809 6,619 27,190 39,0011/1/08 33,809 3,900 29,909 9,09212/31/08 10,000 908 9,092 0Lessor’sReceivable $111,427Lessor’s unearned interest$11,427

Annual Interest Reduction of LeasePayment Expense Obligation Obligation

1/1/07 $100,0001/1/07 $33,809 0 $33,809 66,1911/1/08 33,809 6,619 27,190 39,0011/1/08 33,809 3,900 29,909 9,09212/31/08 10,000 908 9,092 0Lessor’sReceivable $111,427Lessor’s unearned interest$11,427

The lessor’s schedule will have the same numbers as the lessee’s schedule with a guaranteed residual.

The lessor’s schedule will have the same numbers as the lessee’s schedule with a guaranteed residual.

Lessee Schedule-Lessee

48

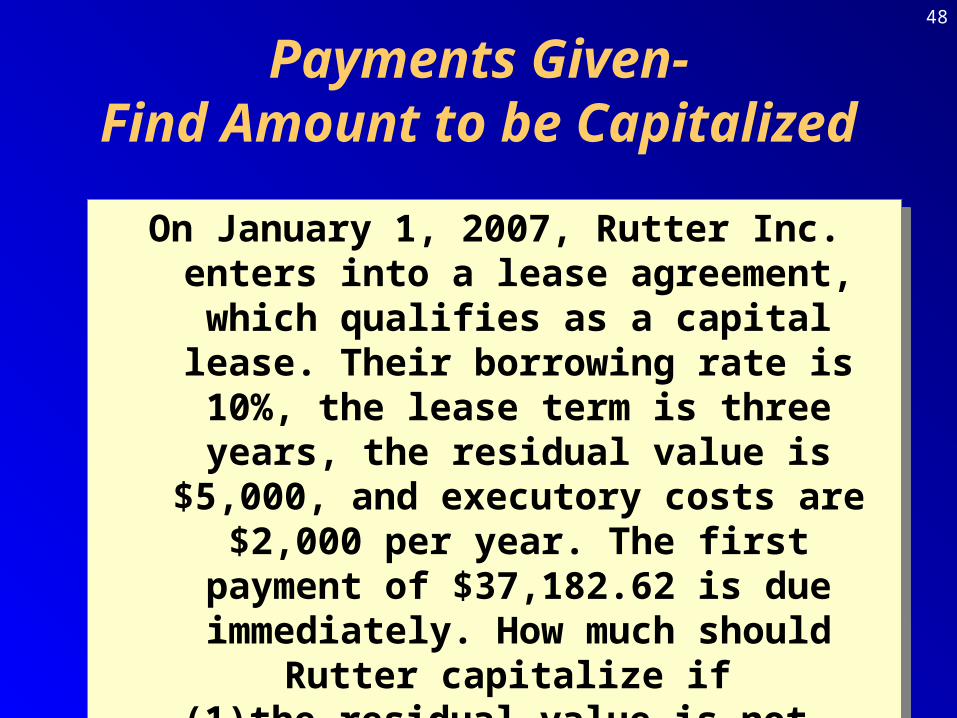

On January 1, 2007, Rutter Inc. enters into a lease agreement, which qualifies as a capital lease. Their borrowing rate is 10%, the lease

term is three years, the residual value is $5,000, and executory costs are $2,000 per

year. The first payment of $37,182.62 is due immediately. How much should Rutter

capitalize if (1) the residual value is not guaranteed, and

(2) the residual value is guaranteed?

On January 1, 2007, Rutter Inc. enters into a lease agreement, which qualifies as a capital lease. Their borrowing rate is 10%, the lease

term is three years, the residual value is $5,000, and executory costs are $2,000 per

year. The first payment of $37,182.62 is due immediately. How much should Rutter

capitalize if (1) the residual value is not guaranteed, and

(2) the residual value is guaranteed?

Payments Given-Find Amount to be Capitalized

49

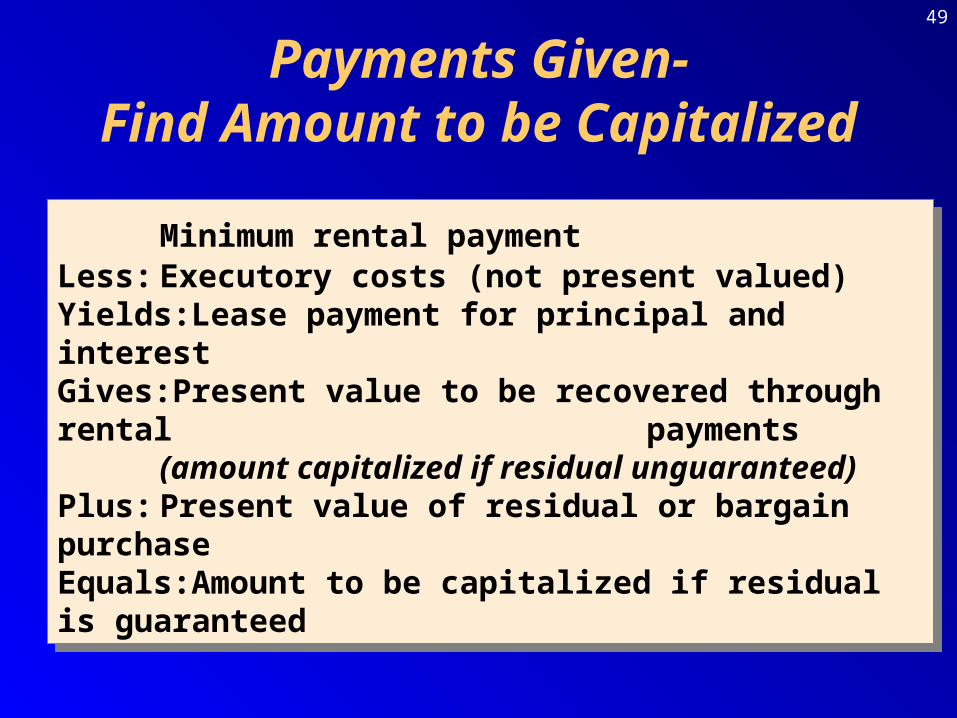

Minimum rental paymentLess: Executory costs (not present valued)Yields: Lease payment for principal and interestGives: Present value to be recovered through rental payments

(amount capitalized if residual unguaranteed)Plus: Present value of residual or bargain purchaseEquals:Amount to be capitalized if residual is guaranteed

Minimum rental paymentLess: Executory costs (not present valued)Yields: Lease payment for principal and interestGives: Present value to be recovered through rental payments

(amount capitalized if residual unguaranteed)Plus: Present value of residual or bargain purchaseEquals:Amount to be capitalized if residual is guaranteed

Payments Given-Find Amount to be Capitalized

50

Minimum rental payment $37,182.62Less: Executory costs (not present valued) 2,000Yields: Lease payment for principal and interest $35,182.62Gives: Present value to be recovered through

rental payments (3 years) $96,243.46(amount capitalized if residual unguaranteed)

Plus: Present value of residual or bargain purchase 3,756.55Equals: Amount to be capitalized if residual

is guaranteed $100,000

Minimum rental payment $37,182.62Less: Executory costs (not present valued) 2,000Yields: Lease payment for principal and interest $35,182.62Gives: Present value to be recovered through

rental payments (3 years) $96,243.46(amount capitalized if residual unguaranteed)

Plus: Present value of residual or bargain purchase 3,756.55Equals: Amount to be capitalized if residual

is guaranteed $100,000

Payments Given-Find Amount to be Capitalized

51

1. With a capital lease, the lessee records depreciation using the firm’s normal depreciation method.

2. Over the economic life if title is transferred or the is a bargain purchase option.

3. Over the term of the lease if the lease term is equal to 75% or more of the economic life, or the present value of the minimum lease payments is at least 90% of the fair value.

4. Any residual (salvage) is ignored if the residual is not guaranteed.

5. Any residual is not discounted (present valued) if the residual is guaranteed.

1. With a capital lease, the lessee records depreciation using the firm’s normal depreciation method.

2. Over the economic life if title is transferred or the is a bargain purchase option.

3. Over the term of the lease if the lease term is equal to 75% or more of the economic life, or the present value of the minimum lease payments is at least 90% of the fair value.

4. Any residual (salvage) is ignored if the residual is not guaranteed.

5. Any residual is not discounted (present valued) if the residual is guaranteed.

Depreciation

52

In the Brahms example above the lease term was three years, the economic life was four years and there

was a bargain purchase option.

In the Brahms example above the lease term was three years, the economic life was four years and there

was a bargain purchase option.

Amount capitalized less salvage = depreciation Economic life

Amount capitalized less salvage = depreciation Economic life

$100,000 - $10,000 = $22,500 per year Four years

$100,000 - $10,000 = $22,500 per year Four years

Depreciation

53

Assume that there was no bargain purchase option and the residual was not guaranteed.

Assume that there was no bargain purchase option and the residual was not guaranteed.

Amount capitalized = depreciation Lease term

Amount capitalized = depreciation Lease term

$92,487 = $30,829 per year 3 years

$92,487 = $30,829 per year 3 years

Depreciation

54

Operating lease

Sales-type lease

Direct financing lease

Leveraged lease

Lessor’s ClassificationsA leveraged lease is a special three-

party lease that is always considered

to be a direct financing lease.

A leveraged lease is a special three-

party lease that is always considered

to be a direct financing lease.

55

Owner Company leases a piece of equipment to User Company for 5 years. User Company agrees to pay

$50,000 at the beginning of each year. Owner Company purchased the equipment for $300,000.

The equipment has an estimated life of 10 years and Owner Company uses straight-line depreciation.

Owner pays the annual insurance premium of $2,000, and on December 15, 2007, it pays for

repairs of $1,500.

Owner Company leases a piece of equipment to User Company for 5 years. User Company agrees to pay

$50,000 at the beginning of each year. Owner Company purchased the equipment for $300,000.

The equipment has an estimated life of 10 years and Owner Company uses straight-line depreciation.

Owner pays the annual insurance premium of $2,000, and on December 15, 2007, it pays for

repairs of $1,500.

Why is this an operating lease?None of the criteria in Column A (Example 21-2) were met; therefore, this lease should be treated as

an operating lease.

None of the criteria in Column A (Example 21-2) were met; therefore, this lease should be treated as

an operating lease.

Operating Lease (Lessor)

56

Purchase of Equipment to Be Leased on Jan. 1, 2007 Equipment Leased to Others 300,000

Cash (or Accounts Payable) 300,000Collection of Annual Payment on January 1, 2007Cash 50,000 Rental Revenue 50,000

ContinuedContinuedContinuedContinued

Payment of Annual Insurance Premium, Jan. 10, 2007Insurance Expense 2,000 Cash 2,000

Operating Lease (Lessor)

57

Payment of Repairs on December 15, 2007 Repair Expense 1,500

Cash 1,500Recognition of Annual Depreciation, Dec. 31, 2007Depreciation Expense: Equipment Leased to Others 30,000 Accumulated Depreciation:

Equipment Leased to Others 30,000

Operating Lease (Lessor)

58

Under a direct financing lease, the lessor “sells” the asset at no gain or

loss. The net amount at which the lessor records the receivable must be equal to the carrying value of the property.

Under a direct financing lease, the lessor “sells” the asset at no gain or

loss. The net amount at which the lessor records the receivable must be equal to the carrying value of the property.

1. The undiscounted minimum lease payments to be received by the lessor (net of executory costs paid by the lessor) plus

2. The unguaranteed residual value accruing to the benefit of the lessor.

The gross receivable of the lessor includes the sum of--

Direct Financing Leases (Lessor)

59

Gardner Company leases equipment to the Martin Company for 4 years. The lease is noncancelable and requires equal payments of $32,923.45. This equipment cost Gardner $100,000. There is no

guaranteed residual value. Martin agrees to pay all executory costs. The equipment reverts back to

Gardner at the end of 4 years. Martin’s incremental borrowing rate is 12.5%, while

Gardner’s is 12%. Martin Company uses straight-line depreciation. All requirements for Column B

are met.

Gardner Company leases equipment to the Martin Company for 4 years. The lease is noncancelable and requires equal payments of $32,923.45. This equipment cost Gardner $100,000. There is no

guaranteed residual value. Martin agrees to pay all executory costs. The equipment reverts back to

Gardner at the end of 4 years. Martin’s incremental borrowing rate is 12.5%, while

Gardner’s is 12%. Martin Company uses straight-line depreciation. All requirements for Column B

are met.

$100,000 ÷ 3.037349$100,000 ÷ 3.037349$100,000 ÷ 3.037349$100,000 ÷ 3.037349

Why is this a direct financing

lease?

Why is this a direct financing

lease?

Direct Financing Leases (Lessor)

60

It is a direct financing lease because it meets the three requirements: (1) one or more of the items listed in

Column A (Exhibit 21-2)—Items 3 and 4.

It is a direct financing lease because it meets the three requirements: (1) one or more of the items listed in

Column A (Exhibit 21-2)—Items 3 and 4.

…(2) both of the criteria listed in Column B (Example 21-2),

and (3) there is no manufacturer’s or dealer’s

profit. See Example 21-7 for more detail.

…(2) both of the criteria listed in Column B (Example 21-2),

and (3) there is no manufacturer’s or dealer’s

profit. See Example 21-7 for more detail.

Direct Financing Leases (Lessor)

61Example 21-8Example 21-8

32,923.45 12,000.00 20,923.45 79,076.55

2. LeasePayment

Cr

Interest 12%Expense

Dr

DecreaseLiability in

BalanceDr Balance

100,000.00

32,923.45 9,489.19 23,434.26 55,642.29

32,923.45 6,677.07 26,246.38 29,395.91

32,923.45 3,527.54 29,395.91 0

62

Initial Recording of the Lease on January 1, 2007Lease Payments Receivable 131,693.80

Equipment 100,000.00Unearned Interest: Leases 31,693.80

Collection of Annual Payment on December 31, 2007Cash 32,923.45 Lease Payments Receivable 32,923.45

ContinuedContinuedContinuedContinued

$32,923.45 x 4$32,923.45 x 4$32,923.45 x 4$32,923.45 x 4

Direct Financing Leases (Lessor)

63

Recognition of Interest Revenue on Dec. 31, 2007Unearned Interest: Leases 12,000.00

Interest Revenue: Leases 12,000.00

Collection of Annual Payment on Dec. 31, 2008Cash 32,923.45 Lease Payments Receivable 32,923.45

$100,000 x 0.12$100,000 x 0.12

Recognition of Interest Revenue on December 31, 2008Unearned Interest: Leases 9,489.19 Interest Revenue: Leases 9,489.19

($100,000 - $20,923.45) x 0.12($100,000 - $20,923.45) x 0.12

Direct Financing Leases (Lessor)

64

Let’s look at a direct financing lease where the

payments will be received in advance.

Let’s look at a direct financing lease where the

payments will be received in advance.

Direct Financing Leases (Lessor)

65

On January 1, 2007, the Watkins Finance Company leases equipment that cost $391,371.20

(which is also the fair value) to the Hutton Company. The term of the lease is 5 years, with

annual payments of $100,000 received in advance. The economic useful life is 5 years. There is no BPO or guaranteed residual value. The lease receipts will yield Watkins a 14% return. The

collectibility is reasonably assured, and there are no uncertainties involved in the lease.

On January 1, 2007, the Watkins Finance Company leases equipment that cost $391,371.20

(which is also the fair value) to the Hutton Company. The term of the lease is 5 years, with

annual payments of $100,000 received in advance. The economic useful life is 5 years. There is no BPO or guaranteed residual value. The lease receipts will yield Watkins a 14% return. The

collectibility is reasonably assured, and there are no uncertainties involved in the lease.

Direct Financing Leases (Lessor)$100,000 X 3.913712$100,000 X 3.913712

66Example 21-10Example 21-10

100,000 291,371.20

2. LeasePaymentReceived

Interest 14%Revenue

Reductionin

NetInvestment

NetInvestment

BalancePV of rental payments but residual not guaranteed 391,371.20

2007 100,000 40,791.97 59,208.03 232,163.17

2008 100,000 32,502.84 67,497.16 164,666.01

2009 100,000 23,053.24 76,946.76 87,719.25

2010 100,000 12,280.75 87,719.25 0

67

Initial Recording of the Lease on January 1, 2007Lease Payments Receivable 500,000.00

Equipment 391,371.20Unearned Interest: Leases 108,628.80

Collection of Annual Payment on January 1, 2007Cash 100,000.00 Lease Payments Receivable 100,000.00

ContinuedContinuedContinuedContinued

$100,000 x 5$100,000 x 5

Direct Financing Leases (Lessor)

68

Recognition of Interest Revenue on Dec. 31, 2007Unearned Interest: Leases 40,791.97

Interest Revenue: Leases 40,791.97

$291,371.20 x 0.14$291,371.20 x 0.14

Direct Financing Leases (Lessor)

69

Take a moment to examine the data in the next slide. Why is this a sales-type

lease? Click on the button to check your response.

Take a moment to examine the data in the next slide. Why is this a sales-type

lease? Click on the button to check your response.

Sales Type Leases (Lessor)

70

Sales Type Leases (Lessor)Cost of Goods SoldCost of Goods Sold Sales RevenueSales Revenue

Lease Payments Lease Payments ReceivableReceivable

($30,000 x 10) + $500($30,000 x 10) + $500

71

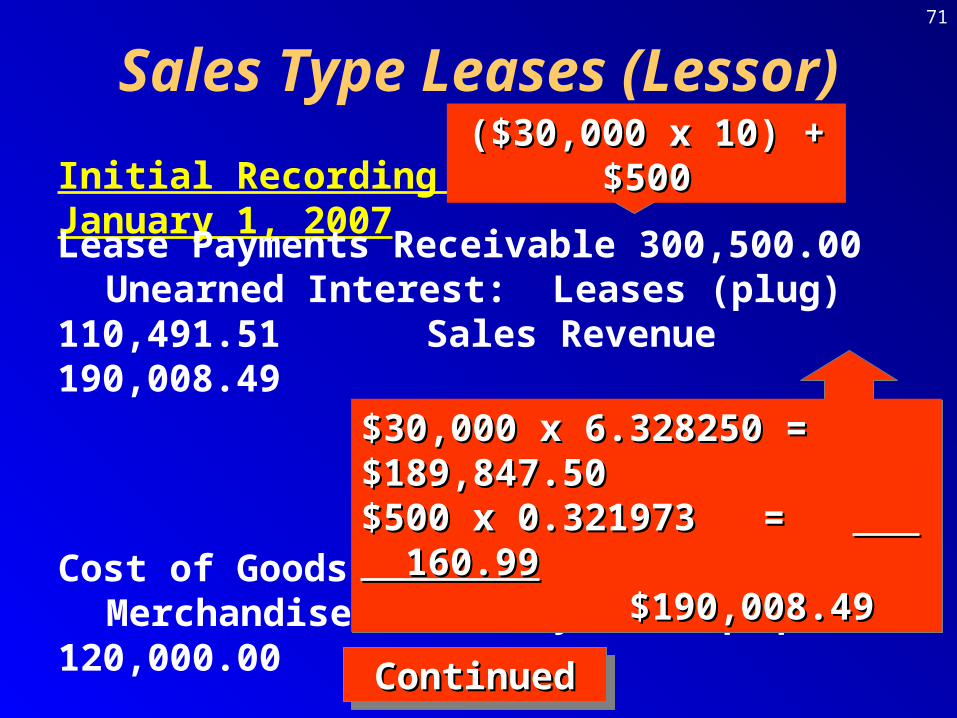

Initial Recording of the Lease on January 1, 2007Lease Payments Receivable 300,500.00

Unearned Interest: Leases (plug) 110,491.51 Sales Revenue 190,008.49

Cost of Goods Sold 120,000.00 Merchandise Inventory (or Equipment) 120,000.00

ContinuedContinuedContinuedContinued

$30,000 x 6.328250 =$30,000 x 6.328250 =$189,847.50$189,847.50$500 x 0.321973 $500 x 0.321973 = = 160.99 160.99

$190,008.49$190,008.49

$30,000 x 6.328250 =$30,000 x 6.328250 =$189,847.50$189,847.50$500 x 0.321973 $500 x 0.321973 = = 160.99 160.99

$190,008.49$190,008.49

Sales Type Leases (Lessor)($30,000 x 10) + $500($30,000 x 10) + $500

72

Collection of Annual Payment on January 1, 2007Cash 30,000.00

Lease Payments Receivable 30,000.00

Recognition of Interest Revenue on December 31, 2007Unearned Interest: Leases 19,201.02 Interest Revenue: Leases 19,201.02

12% x [($300,500 - $30,000) - $110,491.51]12% x [($300,500 - $30,000) - $110,491.51]

Sales Type Leases (Lessor)

73

Initial Direct Costs for Lessor

Costs that a lessor would not have incurred if it had not entered into the lease contract.

Operating lease Expense in proportion to the receipts from the lease over

the term of the lease.

Direct financing lease Reduce “Unearned Interest” and calculate a new (lower)

implicit interest rate.

Sales-type lease Expense in period of sale.

74

Why would a lessee or lessor want to

avoid capitalizing a lease?

Why would a lessee or lessor want to

avoid capitalizing a lease?

The motivation usually comes from the lessee who wants

to avoid reporting the liability.

The motivation usually comes from the lessee who wants

to avoid reporting the liability.

Conceptual Issues

75

Chapter21

Task Force Image Gallery clip art included in this electronic presentation is used with the permission of NVTech Inc.

76

The lease meets two of the criteria: (a) The lease term is 75% or more of the asset’s economic life and (b) the present value of the lease payments is 90% or more of the asset’s fair

value.

The lease meets two of the criteria: (a) The lease term is 75% or more of the asset’s economic life and (b) the present value of the lease payments is 90% or more of the asset’s fair

value.

Return

77

Three of four criteria from Column A (Example 21-7) are

met and both items from Column B, and there is a manufacturer’s

or dealer’s profit.

Three of four criteria from Column A (Example 21-7) are

met and both items from Column B, and there is a manufacturer’s

or dealer’s profit.

Return