Hochschild Mining plc

Analyst teach-in 18 June 2008

DisclaimerSome statements contained in this presentation or in documents referred to in it are or may be forward-looking statements. Actual results may differ from those expressed in such statements, depending on a variety of factors.Past performance of the Company or its shares cannot be relied on as a guide to future performance.Any forward-looking information contained in this presentation has been prepared on the basis of a number of assumptions which may prove to be incorrect, and accordingly, actual results may vary.This presentation does not constitute, or form part of or contain any invitation or offer to any person to underwrite, subscribe for, otherwise acquire, or dispose of any shares in Hochschild Mining plc or advise persons to do so in any jurisdiction, nor shall it, or any part of it, form the basis of or be relied on in any connection with or act as an inducement to enter into any contract or commitment therefore. No reliance may be placed for any purpose whatsoever on the information or opinions contained in this document or on its completeness and no liability whatsoever is accepted for any loss howsoever arising from any use of this document or its contents otherwise in connection therewith. Nothing in this presentation is to be construed as a profit or production forecast. This presentation has been prepared in compliance with English law and English courts will have exclusive jurisdiction over any disputes arising from or connected with this presentation.

1

2

Welcome & introduction

Welcome & introduction

PURPOSE: to generate greater understanding of assets and

their geology to assist forecasting at mine level & to update

on current market conditions

3

Today’s agendaCompany overview

Calculating reserves & resources

Understanding the geology

Financial & political situation

4

Leading precious metals producer

5

Diversified asset base

Growth story

Underground mining and regional expertise

Proven track record in reserve replacement

Hochschild: Almost 100 years in Latin America

Strong financial performance & low cash costs

A responsible operator

Experienced management team

Achieving our goals

6

Lake Shore Gold Corp. C$144 million total investment for 35% ownership

Q1 production in-line with forecast

Consolidated San Felipe ownership — 100% for $52 million

Appointment of Miguel Aramburú as CEO

2008

Achieved production target of 26 moz Ag eq

Completed expansion at Arcata, Ares and Selene

Commenced production at San José, Moris and Pallancata

Increased reserve life

100% hedge free

Declared and paid dividend

2007

Operating in the Americas

7

x

PERUArcata (100%)Ares (100%)Selene (100%)Pallancata (60%) ARGENTINA

San José (51%)

x

x

MEXICOMoris (70%)San Felipe (100%)

CANADALake Shore Gold Corp. (35%)

x

4th largest primary silver producer…

12

13

14

15

16

16

16

17

17

19

34

39

48

No. Company 2007 production (moz Ag) % of global¹

3 Fresnillo plc

2 KGHM Polska Miedz

1 BHP Billiton

7 Volcan

4 Kazakhmys

5 Pan American Silver

6 Goldcorp

8 Buenaventura

9 Polymetal

10 Grupo Mexico

11 Hochschild Mining

12 Rio Tinto

13 Coeur d’Alene

7%

6%

6%

3%

3%

3%

2%

2%

2%

2%

2%

2%

2%12

14

16

17

34

Hochschild

Coeur

Polymetal

Pan American

Primary silver producers

Source: JPMorgan Cazenove/GFMS; Hochschild Mining considered a primary silver producer with approximately 60% of revenue derived from silver¹ Assumes 2007 global production of 670.6 million ounces Excludes production relating to Silver Wheaton purchases, includes attributable production from Luismin, Marlin and La Coipa Includes equity production Minera Yanacocha

Fresnillo

8

…and a mid-sized producer of gold

Source: GFMS, Company filings Assumes 2007 global production of 670.6 million ounces

445

297

285

249

242

231

201

183

182

159

155

Randgold

Peter Hambro

Teck Cominco

Fresnillo

Polymetal

Agnico Eagle

Hochschild Mining

Oceana

BHP

Aruizon

St Barbara

Select companies 2007 production (koz Au) % of global

Randgold

Teck Cominco

Polymetal

Hochschild Mining

Oceana

BHP Billiton

0.6%

0.4%

0.3%

0.3%

0.3%

0.2%

0.2%

Agnico Eagle

Peter Hambro

0.2%

Aurizon

Equigold

0.3%

0.2%

Fresnillo

0.4%

9

Our strategy for growth

1 Maximize the potential of our existing operations through exploration and expansion

Bring into production new, profitable precious metal projects throughout the Americas

2

LONG TERM PROFITABLE GROWTH

10

Delivering on our strategy

11

Expanding existing operations:

San José (+100%)

Arcata (+30%)

Selene-Pallancata (+50%)

1

Q3 2008

Q3 2008

Q4 2008

New projects:

San Felipe feasibility

Lake Shore production

2

Q4 2008

2009

San Felipe production Q4 2010

Exploration, joint ventures, acquisitions

12

Eduardo HochschildExecutive Chairman

Roberto DañinoDeputy Chairman & Executive

Director

Miguel AramburúChief Executive Officer

Jorge BenavidesSenior Vice President

Corporate Development

Ignacio RosadoChief Financial Officer

Javier DurandLegal Counsel

Ignacio BustamanteChief Operating Officer

José Augusto PalmaSenior Adviser, Executive

Committee

Isac BursteinBusiness Development Manager

Raymond Jannas Vice President Exploration &

Geology

Highly experienced management team

Experienced, independent Board

Committed to transparency and good corporate governance

Ongoing evaluation of the Board to ensure it meets the needs of the business as it evolves as a UK listed company

Effective board structure

Combined Code requirement HOC

Chairman and Chief Executive separate roles

½ Board Independent/Non-Exec Directors

Regular re-election of all board directors

Formal & rigorous annual evaluation

13

Eduardo Hochschild, Executive Chairman

Roberto Dañino, Deputy Chairman and Executive Director

Alberto Beeck, Non-Executive Director

Sir Malcolm Field, Non-Executive Director

Jorge Born Jr., Non-Executive Director

Nigel Moore, Non-Executive Director

Dionisio Romero, Non-Executive Director

14

Calculating reserves & resources

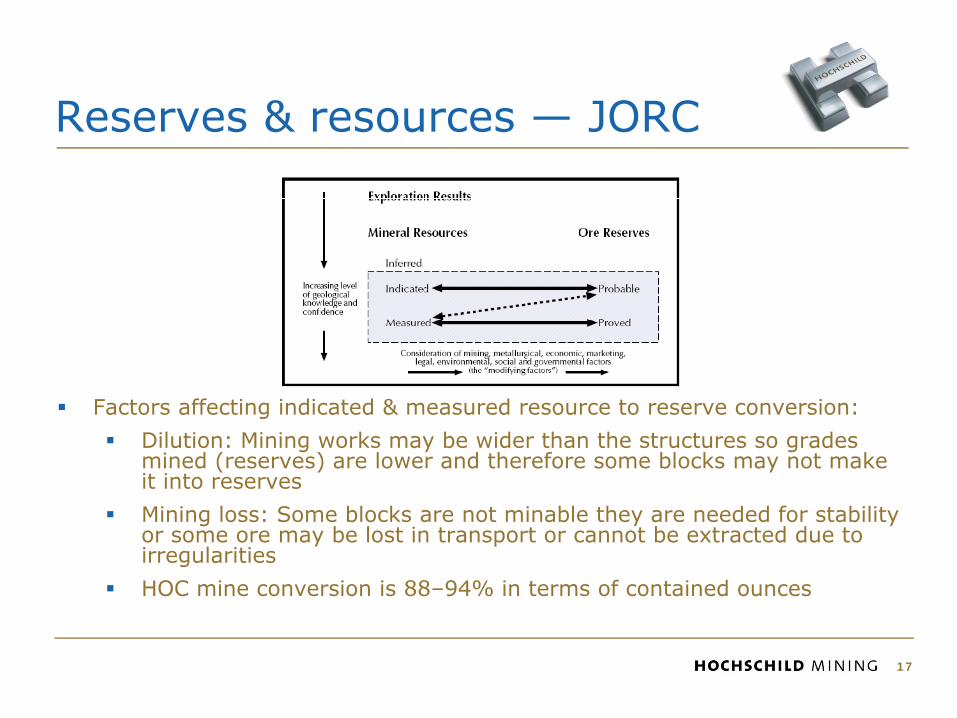

Reserves & resources overview We report reserves semi-annually following the JORC Code

IMC conducts a full audit of reserves and resources annually based on the JORC Code

Cut off policy:

Marginal cost to produce a tonne of ore

Parameters used:

Long term analyst consensus prices

31 December 2007 R&R assumed $600/oz Au & $10.50/oz Ag

Grade is capped according to statistics for each individual deposit

Reserves have an accuracy of 10 – 20%

Inferred resources have an accuracy of 40%

15

Narrow vein mine versus other ore body types

16

Reserves & resources — JORC

Factors affecting indicated & measured resource to reserve conversion:

Dilution: Mining works may be wider than the structures so grades mined (reserves) are lower and therefore some blocks may not make it into reserves

Mining loss: Some blocks are not minable they are needed for stabilityor some ore may be lost in transport or cannot be extracted due toirregularities

HOC mine conversion is 88–94% in terms of contained ounces

17

Underground mine life benchmarking

Mine Life (Resources < 50 M TM)

0

50

100

150

200

Min

e L

ife (

yrs

)

Resource LifeReserve Life

142 UG mines listed (<50 M TM) in the western hemisphere in all ore types126 mines with < 20 yrs LOM based on reservesAverage LOM (reserves): 5.5 yrsAverage LOM (reserves + resources): 9.2 yrs

18

Source: Mineral Economics Group Database

19

LOM examples in other companies

Mine Company Start date 2000 2001 2002 2003 2004 2005 2006 2007

Quiruvilca Pan American 1922 5.5 4.8 4.2 1.4 2.8 4.2 4.1 4.0

Orcopampa Buenaventura 1967 1.3 1.3 1.8 2.7 2.5 2.5 2.5 2.8

Lucky Friday Hecla Mining Co 1942 5.2 5.0 7.5 4.3 4.6 6.0 4.1 4.1

Fresnillo Fresnillo plc 1976 8.3 6.7 6.9 9.0 8.0 5.7 5.2 11.5

Average 5.1 4.5 5.1 4.3 4.5 4.6 4.0 5.6

Source: Cazenove equity research until 2005 company filings thereafter

20

Increasing reserve & resource base GOAL: 4 years reserves + 4 years resources

Attributable resources (moz Ag eq.)1

Jun-06 Dec-06 Jun-07 Dec-07

Attributable reserves (moz Ag eq.)1

Jun-06 Dec-06 Jun-07 Dec-07

Arcata

Ares

Selene

Pallancata

San José

Moris

2007 life of mine2

2.5

3.8

2.3

10.0

10.2

13.0

7.8

2.8

5.1

16.1

2.42.8

LOM (reserves)

LOM (reserves + resources)

1 Includes 35% of Lake Shore Gold Corp’s reserves and resources2 LOM = reserves / yearly plant capacity. Both as of 31 December 20073 Based on 2,000 tpd and subject to completion of feasibility study

San Felipe33.9

12.015.4

Lake shore

-

83104

119138

178202

219 231

Mining average reserve gradesCorporate policy maximizes shareholder value over the long run

Not always feasible

If we mine higher grade, then average grade decreases

Depends on replacement grade

21

Policy for guidance on grades

22

Initial reserve (31 Dec 07) 2008B production

100% kt Ag (g/t) Au (g/t) kt Ag (g/t) Au (g/t)

Arcata 1,838 476 1.2 545 570 1.3

Ares 844 183 5.9 333 165 6.4

Selene 809 269 1.7 307 230 1.6

Pallancata 3,546 289 1.2 504 325 1.2

San José 2,695 403 6.0 365 457 7.3

Moris 2,534 4.8 1.5 1,062 4.6 1.5

Comments:

Reserve and resource information released on 12 March 2008

We will give guidance on grades for the current year

We will publish R&R information semi-annually (prelims & interims)

Based on this information market can interpret data and formulate opinion on future grades

Final grade calculation based on reserves

23

Initial Reserve

MT 1,000,000 A

Ag (g/t) 500 B

Additions

MT 400,000 E

Ag (g/t) 500 F

Production

MT 400,000 C

Ag (g/t) 750 D

Final Reserve Formula

MT 1,000,000 G = (A - C + E)

Ag (g/t) 400 = (B*A - D*C + F*E) / G

- +

Application of calculationBased on previous methodology

24

Calculation of 2009 reserves

100% kt Ag (g/t) Au (g/t)

Arcata 1,293 436 1.2

Ares 511 195 5.6

Selene 502 293 1.8

Pallancata 3,042 283 1.2

San José 2,330 395 5.8

Moris 1,472 5.0 1.5

Comments:

Assumes no reserve replenishment

Ares and Selene may vary 20-30% because we could incorporate low grade material from vein splits that might be economic

25

Understanding the geology

Quality assets

26

Rank Mine/Country Company Prod.(m oz) 1 Cannington*, Australia BHP Billiton 37.472 Fresnillo, Mexico Fresnillo 33.523 Dukat, Russia OJSC Polymetal 10.804 Uchucchacua, Peru Compañia de Minas Buenaventura SA 9.875 Greens Creek**, U.S. Hecla Mining Co 8.656 Arcata, Peru Hochschild Mining 6.557 Pallancata, Peru*** Hochschild Mining 6.008 San Jose, Argentina*** Hochschild Mining 5.509 Imiter, Morocco Société Métallurgique d'Imiter 5.4110 Rochester, U.S. Coeur d'Alene Mines 4.6111 Tayahua***, Mexico Grupo Carso 4.0012 La Colorada, Mexico Pan American Silver Corp 3.9613 Huaron, Peru Pan American Silver Corp 3.8314 Alamo Dorado, Mexico Pan American Silver Corp 3.8115 Selene, Peru Hochschild Mining 3.41

World's Leading Primary Silver Mines in 2007

*reported payable metal in concentrate; **historically a silver mine, Greens Creek's primary revenue stream sw itched to zinc in 2006. GFMS regard this as a short term anomaly and as such have maintained its classif ication as a primary silver mine; ***estimated.

Arcata – a world class silver district

In production since 1964

Total production + resources: ± 240 moz Ag, 400 koz Au to date

Southern part of district mined until 2005

Mariana vein and other structures mined starting in 2005

Average grade mined: 700 grams in the past 10 years

67% of production comes from Mariana

Ag & Au production up 38% and 29%, respectively (2007)

Plant expansion almost completed (capacity to 618 ktpa)

27

Arcata

28

Reserve replenishment — Arcata

29

K TM Ag eq (gr /TM)

M oz Ag Eq. contained K TM Ag eq (gr

/TM) M oz Ag Eq. contained K TM Ag eq (gr

/TM) oz Ag eq

1,990 1,504 666.0 32.2 311 685.8 6.9 4.841,991 1,252 674.0 27.1 262 758.6 6.4 10 4,093.7 1.3 4.781,992 1,159 681.2 25.4 260 778.4 6.5 167 886.5 4.8 4.461,993 1,212 620.4 24.2 259 700.4 5.8 312 461.0 4.6 4.681,994 1,312 649.6 27.4 326 763.0 8.0 426 819.5 11.2 4.021,995 1,477 664.8 31.6 357 817.6 9.4 522 807.5 13.6 4.141,996 1,340 680.0 29.3 357 838.0 9.6 220 1,038.4 7.3 3.751,997 1,028 679.0 22.4 374 847.8 10.2 62 1,675.6 3.3 2.751,998 817 695.4 18.3 375 850.0 10.2 164 1,151.7 6.1 2.181,999 546 498.6 8.8 380 863.6 10.6 109 296.0 1.0 1.442,000 682 507.0 11.1 371 672.2 8.0 507 636.9 10.4 1.842,001 448 479.0 6.9 359 640.4 7.4 125 789.8 3.2 1.252,002 540 618.0 10.7 236 567.6 4.3 328 771.6 8.1 2.292,003 315 800.8 8.1 236 583.4 4.4 11 5,110.4 1.8 1.332,004 440 564.6 8.0 290 683.4 6.4 415 468.3 6.2 1.522,005 769 637.4 15.8 282 610.4 5.5 611 677.4 13.3 2.732,006 1,229 515.2 20.4 314 620.4 6.3 774 436.5 10.9 3.912,007 1,838 547.4 32.3 415 645.8 8.6 1,024 625.9 20.6 4.43

5,764 725.8 134.5 5,787 686.9 127.8 3.13

LOM (years)

Total

Reserves Extracted Replenishment

Year

Arcata — Mariana Vein crosssection

30

Arcata — reserves & resources

M Oz Eq Ag M Oz Eq Ag M + I 13.68 Inferred 13.49

M + I 5.52 Inferred 7.48

M + I 0.69 Inferred 3.99

M + I 23.41 Inferred 10.42

M + I 34.91 Inferred 35.37

ARCATA VEINS Resources Reserves

12.74

Mariana Vein System- Secondary Veins

5.13

Mariana Vein

13.85

Alexia Vein System

NW-SE Vein System

32.35 Total

0.64

31

32

Arcata

Ave

rage

gra

de

(Ag E

q/T

M)

Met

al c

onte

nt

(moz

Ag E

q)

Cut-off (Ag Eq/TM) Cut-off (Ag Eq/TM)

Graphs based on total resource (including inferred). No allowance for dilution or mine loss.

Grade variability at Arcata

Current reserves 476 g/t Ag & 1.19 g/t Au

Mining 2008 at 570 g/t Ag

Grade in 2008 is higher than reserves and resources due to mine configuration

33

Arcata — upside potential & exploration plans

Significant exploration potential in covered areas to the north

The discovery of the vein field of Mariana and the northern structures confirms that the hydrothermal system is larger than previously thought

2008 exploration plans:

40 holes (5,000 metres total) to expand resource base

2,000 metres of development and 3,000 m in short drills to convert known inferred resources into measured & indicated and hence into reserves

34

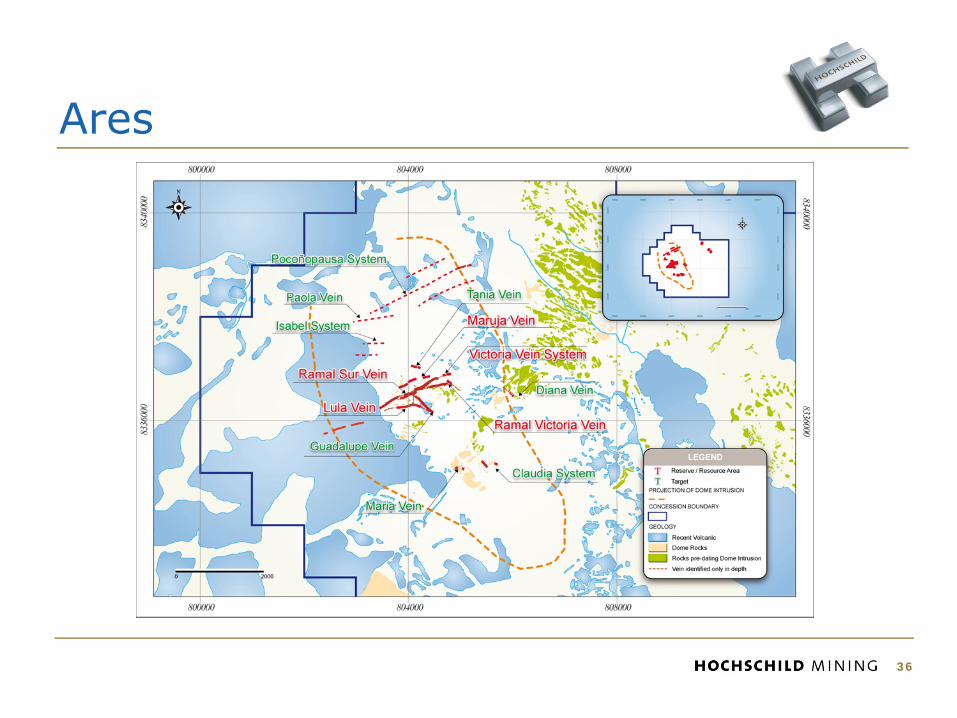

Ares In production since 1998

± 80% - 90% of the production comes from the Victoria Vein and associated structures

1.9 moz Au & 26.8 moz Ag past production

Tonnage mined being consistently replaced albeit with a declining grade

Mature high grade gold deposit

35

Ares

36

Reserve replenishment — Ares

37

K TM Ag eq (gr /TM)

M oz Ag Eq.

contained K TM Ag eq (gr

/TM)

M oz Ag Eq.

contained K TM Ag eq (gr

/TM) oz Ag eq

1,998 1,098 1,658.4 58.5 129 1,607.4 6.7 1,999 656 1,606.6 33.9 241 1,927.6 14.9 (201) 1,504.7 (9.7) 2.72 2,000 838 1,732.2 46.7 273 1,780.0 15.6 455 1,942.0 28.4 3.07 2,001 831 1,686.6 45.1 283 1,502.4 13.7 276 1,359.3 12.1 2.94 2,002 961 1,593.2 49.2 271 1,649.0 14.4 401 1,437.4 18.5 3.55 2,003 1,032 1,657.2 55.0 277 1,642.8 14.6 348 1,822.5 20.4 3.73 2,004 762 1,496.2 36.7 273 1,724.8 15.1 3 (33,085.2) (3.2) 2.79 2,005 828 1,172.8 31.2 281 1,720.0 15.5 347 905.7 10.1 2.95 2,006 845 821.2 22.3 289 1,353.1 12.6 306 375.0 3.7 2.92 2,007 844 539.4 14.6 334 1,153.2 12.4 333 440.0 4.7 2.53

2,651 1,590.8 135.5 2,268 1,165.4 85.0 3.02

LOM (years)

Total

Year

Reserves Extracted Replenishment

Ares — Victoria Vein

38

Ares — reserves & resources

M Oz Eq Ag M Oz Eq Ag M + I 4.71 Inferred 0.08

M + I 7.58 Inferred 0.44

M + I 0.48 Inferred 0.06

M + I 2.83 Inferred 0.50

M + I 15.74 Inferred 1.08

ARES VEINS Resources Reserves

4.05 Victoria Vein

7.11

2.61

0.50

14.64

Victoria System- Secondary Veins

Victoria System- oblique veins

Outlying Veins

Total

39

Exploration potential & plansContinue drilling in the Victoria structural corridor to continuereplenishing tonnes

New exploration model developedto look for another pristine highgrade structure

2008 exploration plans:

± 20 holes (8,000 metres total) to expand resource base

800 metres of development and 4,000 m in short drills to gain reserves around the Victoria Vein

40

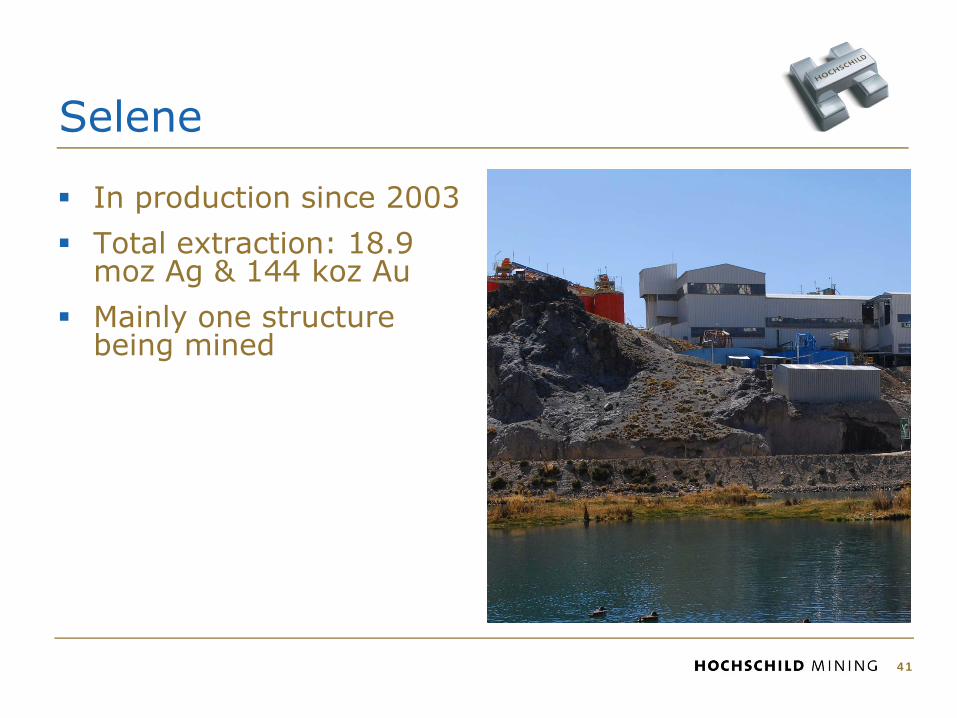

Selene

In production since 2003

Total extraction: 18.9 moz Ag & 144 koz Au

Mainly one structure being mined

41

Reserve replenishment — Selene

42

Selene

43

Selene — Explorador Vein

44

Selene — reserves & resources

45

M Oz Eq Ag M Oz Eq Ag M + I 6.78 Inferred 1.09

M + I 1.61 Inferred 0.89

M + I 1.59 Inferred 5.49

M + I 0.31 Inferred 0.75

M + I 10.28 Inferred 8.21

Secondary Veins in Explorador

Tumiri-Sofia Vein System and Secondary Veins

Outlying Veins

Resources Reserves

Total

Explorador Vein 6.36

1.51

0.30

1.42

SELENE VEINS

9.62

Pallancata Acquired by IMC in late 2002

Discovery holes: 2003

60% acquisition by HOC in mid 2006

In production by mid 2007

Significant exploration upside

46

Pallancata

47

Pallancata — Pallancata Vein

48

Pallancata — reserves & resources

M Oz Eq Ag M Oz Eq Ag M + I 38.17 Inferred 5.91

M + I 5.88 Inferred 0.43

M + I 0.26 Inferred 32.41

M + I 44.39 Inferred 38.78

35.70

5.49

PALLANCATA VEINS Resources Reserves

Veta Oeste

41.43

Other veins associated with the Pallancata Vein System

Veta Cimoide

0.24

Total

49

3,546,271

50

Pallancata

Ave

rage

gra

de

(Ag E

q/T

M)

Cut-off (Ag Eq/TM)

Met

al c

onte

nt

(moz

Ag E

q)

Cut-off (Ag Eq/TM)

Graphs based on total resource (including inferred). No allowance for dilution or mine loss.

Pallancata — exploration upside

Hole ID True Width (m) Ag (gr / TM) Au (gr / TM) Ag Eq (gr / TM

PAC 57 0.40 385 0.86 437 PAC 59 0.30 1,260 3.25 1,455 PAC 60 1.20 622 1.18 693 DLPL-A-61 0.10 1,374 4.10 1,620

0.20 2,520 13.25 3,315 0.30 1,395 14.30 2,253 0.50 575 2.10 701 0.90 535 2.20 667 0.20 383 16.10 1,349

PAC 64 0.90 553 3.61 770 PAC 65 0.70 786 5.05 1,089

0.40 1,275 8.35 1,776 0.20 246 1.11 313 0.40 542 3.06 726 0.20 17 8.51 528

PAC 62

PAC 63

PAC 67

PAC 68

51

San JoséDiscovered in 1998 by Minera Andes

HOC acquired 51% in 2001

In production since mid 2007

50 thousand hectare land package

Over 40 kilometres veins reported, less than 20% explored

52

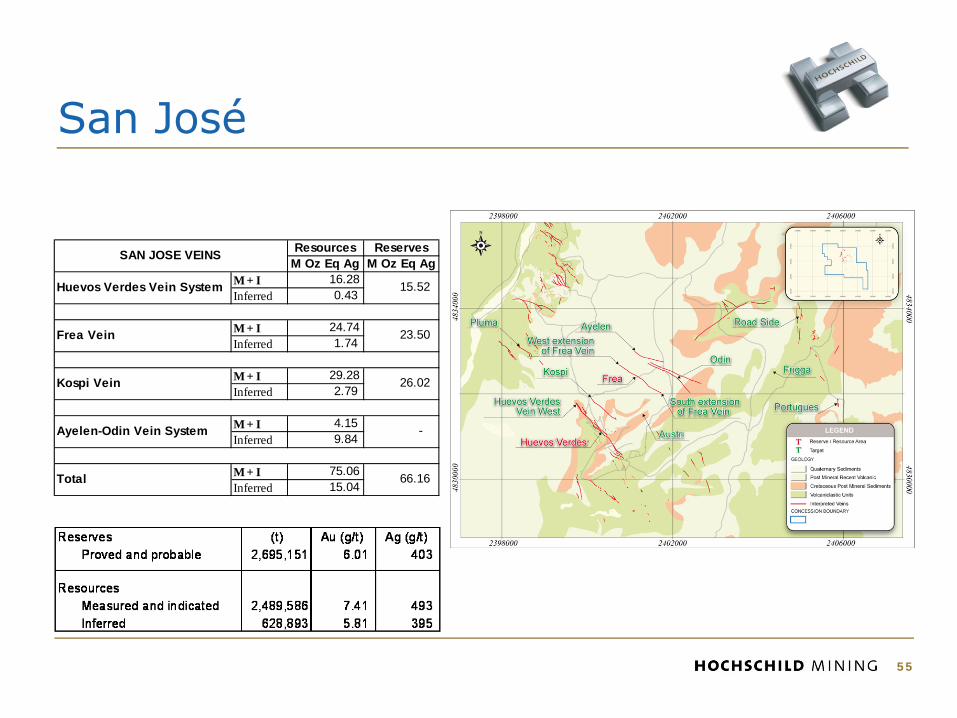

San José

53

San José — Huevos Verdes Vein

54

San José

M Oz Eq Ag M Oz Eq Ag M + I 16.28 Inferred 0.43

M + I 24.74 Inferred 1.74

M + I 29.28 Inferred 2.79

M + I 4.15 Inferred 9.84

M + I 75.06 Inferred 15.04

Ayelen-Odin Vein System

Total

Huevos Verdes Vein System

Frea Vein

Kospi Vein

66.16

26.02

-

15.52

23.50

SAN JOSE VEINS Resources Reserves

55

San José — exploration upside

56

San Felipe

Consolidating ownership: acquired 100% of project for $51.5 million on 5 June 2008

Zn/Pb/Cu/Ag deposit in Sonora, Mexico

Resources:

Indicated: 2.32 M TM @ 7.32% Zn, 3.19% Pb, 0.41% Cu & 71 g/t Ag

Inferred: 0.40 M TM @ 6.25% Zn, 2.98% Pb, 0.27% Cu & 49 g/t Ag

Moving towards feasibility

Only La Ventana structure explored in detail

57

San Felipe

58

59

El Gachi — Mexico (70%)

59

* Measured + indicated + inferred, includes reserves

El Gachi providing additional upside to San Felipe

60 km from San Felipe

2.5 to 8.0 m “manto” identified in the property

Historic (no JORC) resource of ± 100 K TM @ 400 – 500 gr Ag & 15 – 20 % Pb + Zn

Significant upside potential

Lake Shore Gold Corp.

60

HOC increased stake to 35% on 17 June 2008

Canadian (Timmins, Ontario) gold development company

Mining friendly jurisdiction

Fully financed to develop four independent gold assets over the next 18 months to feed the Bell Creek mill. These assets provide production flexibility

Commissioning of the Bell Creek mill expected at the rate of 800 tpd by Q1 2009

Bell Creek mill to be expanded to 3,000 tpd in 2010

215,000 Au oz expected in 2011

Relatively low cost production (lower third of the industry)

Experienced management

Source: Wellington West report dated 4 June 2008

Lake Shore Gold Corp.

61

Exploring the region

Generative

Prospect

Existing mining operations

Resource delineation

Feasibility completed

Target definition

Development projects

AresArcataSelene

San JoséPallancata

MorisNew opportunities To Divest / Drop / JV

62

Exploration offices in Peru, Argentina, Mexico and Chile

554,298 Has. 35,400 Has. 181,425 Has. 60,889 Has.

San Felipe

Peñón Blanco

Gavilanes Pozos

El GachiAzuca

Cacurani

Claudia

El MosquitoCañadón del Moro

Manantiales

Tres Chepas

Encrucijada Parihuana

La Flora

Ccello PuntaMoris Reg.

Quevar (JV)

Tignamar

Calderón

El Pino (JV)

Sierra Mojina (JV)

El Pocito (JV)

San Luis Cordero

Paraiso

Argentina

Chile

Mexico

Peru

CanadaLake Shore

Moctezuma

63

Financial & political situation

2007 unit cost breakdown ($/tonne)

64

Note: costs do not include depreciation. According to IFRS 1 Does not consider Moris which is an open pit mine

2007

Arcata $55

Ares $77

Selene $54

Pallancata $50

San José $189

Moris $18

Weighted average1 $70

Current operating environmentOutlook for 2008 costs

65

Peru

– Impact of incorporating contractor workers in payroll

– US dollar devaluation

– Consumables prices increase affecting mine and plant

– More materials required to support mine to enhance security

– More royalties given higher prices

Argentina

– Personnel expenses increase due to higher salaries (related to market conditions) and higher transportation expenses

– Higher consumables prices and freight rates

– Local inflation pressure higher than expected

Mexico

– Lower tonnage treated

– Increase of maintenance costs and tariffs of contractors

– Greater cement consumption for agglomeration

– Payroll increase due to new market conditions

Selling our productDore versus concentrate

66

Produced at Ares1, San José and Moris (44% of total oz’s produced)

• Frequent pick up from mine

• Risk transfers upon pick up

• 100% of revenuereceived upfront

• Reduced workingcapital requirement

• Stable commercial market conditions

• Fewer discounts

Produced at Arcata, Selene, Pallancata andSan José (56% of total oz’s produced)

Evaluating taking concentrate to doré

• Shipments made on a monthly or quarterly basis

• Risk transfers when mineral reaches smelter

• 85%-90% of revenuereceived upon arrival (30-45 days)

• Increased workingcapital requirement

• Volatile market conditions

• Higher discounts

1 Ares and Selene material treated at Ares

Discounts & selling expenses

67

2009 outlook:

Arcata may become doré in 2Q09Selene and Pallancata 100% doré in 2Q09San José 100% doré in 2Q09Other contracts will remain the same

2007 & 2008 summary & outlook:

1 Doré: includes non payable contents. Other charges such as refining and freights are included in unit cost Concentrates: includes non payable contents, treatment charges, penalties and freights. No charges to unit cost

2 Lower because delivery point changed from Tampico (Mexico) to Callao (Peru)3 Selling expenses include export tax (10% of net sales for concentrate and 5% of net sales for doré)

AresArcataSelenePallancataSan JoséMoris

DoréConcentrateDoré (85%) / Concentrate (15%)ConcentrateDoré (63%) / Concentrate (37%)Doré

0.2%10.2%

2.6%

7.1%

N.A

0.2%

ProductDiscounts

(% gross sales)Selling exp.

(% gross sales)

0.2%14.9%

1.2%

6.4%

2.3%

0.2%

0.1%1.9%

0.6%

1.6%

N.A

-

0.1%1.5%

0.3%

1.3%

6.0%

-

‘07 ‘08E ‘07 ‘08E

2

3

1

Overview of the concentrate market

68

Negotiate annual contracts generally in Oct/Nov of preceding yearHave contracts with Peñoles, Cormin, Doe Run, Norddeutsche Affinerie, and Teck ComincoSurplus base metal concentrate production and tougher environmental regulations regarding deleterious elements results in tougher concentrate market conditionsArcata concentrate most difficult to sell due to arsenic content of 0.6%, down from historic highs of 6% (ideal to have <0.3%)Outlook for concentrate market is to remain difficult as base metal markets (zinc & lead) expected to remain in a surplus stateWe continue to mitigate risk by increasing our production of doré vs. concentrate and increasing our customer base

Cash balanceAdjusting models for investments made this year

69

$ millions

Cash and cash equivalents (Dec. 2007) 301

Less:

Initial investment in LSG1 (65)

San Felipe purchase (incl. IVA) (60)

Second investment in LSG1 (80)

2007 final dividend paid (28)

Capital expenditure (202)

Plus:

Net cash generated from operations ...

Debt Facility 200

We have drawn the $200 million debt facility1 Assumes 1 CAD = 1 USD

Peru political situationNo significant change

70

Mining royalties were introduced in 2004 and dictated by Peruvian legislation

Owners of mining concessions must pay 1%—3% of sales

Sales<US$60m: 1%

US$60m < sales < US$120m: 2%

US$120 million < sales: 3%

Percentage depends on the value of the mineral concentrates according to the international quoted market price published by the Ministry of Energy and Mines

Voluntary social contribution implemented in 2006

Workers’ profit sharing

8% of pre-tax profit

We include 70% in administration expenses and 30% in cost of goods sold

Stability agreement at Ares Unit

Currently do not pay royalties but expires in December 31, 2008

Argentina political situationExport tax included in “selling expense”

71

Mining Royalties vary from province to province. For San José the royalty is fixed at 1.85% of the pit-head value per year when the final product is doré and 2.55% when the final product are mineral concentrates or precipitates.

National Export tax of 5% when the final product is doré and 10% when the final product are gold or silver concentrates although rebates available for the first 3 years if shipped from port (3%, 2% and 1% rebate for years 2007, 2008 and 2009, respectively

Export tax included in “Selling Expense” line of income statement

Stability certificate granted by the Ministry of Mines for San José

National and provincial tax regimes are frozen for a period of 30 years

No workers’ profit sharing

Mexico political situation

72

No mining royalties

No stability agreements

Workers’ profit sharing equal to 10% of pre-tax profit

IETU equal to 16.5% for year 2008; 17% for year 2009; and 17.5% from year 2010 and so on, over cash flow

2008 outlook

73

• Year of consolidation

– Stable production

– Focus on cost containment in inflationary environment

• Advancing on growth strategy through:

– Further expansions

– Feasibility at San Felipe

– Continue to pursue further acquisitions

• Positive on fundamentals for silver and gold

– Global macroeconomic outlook

– Industrial demand for silver especially from China

• Remain on track to achieve production targets

– Q1 2008 production inline with forecast

Contact us

Miguel Aramburú, CEO (Lima)+511 437 6018

Ignacio Rosado, CFO (Lima)+511 437 6007

Wray Barber, Head of Investor Relations (London) +44 20 7907 2934

74