SIA (01957R-AG / V1) 1

Approved Contractor Scheme

Benefits Survey

February 2008

SIA (01957R-AG / V1) 2

CONTENTS

1 SUMMARY OF MAIN FINDINGS ................................................................ 5

2 INTRODUCTION ................................................................................... 11

2.1 Background ........................................................................................ 11

2.2 Methodology ....................................................................................... 11

2.3 Analysis of results ............................................................................... 11

2.4 Structure of this report ........................................................................ 12

3 ACS COMPANIES ................................................................................. 13

3.1 Introduction ....................................................................................... 13

3.2 Company profile .................................................................................. 13

3.2.1 Sector(s) covered ........................................................................ 13

3.2.2 Size of business .......................................................................... 14

3.2.3 Number of clients ........................................................................ 14

3.2.4 Client sites ................................................................................. 15

3.3 Questions about the ACS ...................................................................... 15

3.3.1 Proportion of clients that require the ACS ....................................... 16

3.3.2 Proportion of private sector clients ................................................ 17

3.3.3 Effect of approved status on company turnover ............................... 17

3.3.4 Proportion of turnover change ....................................................... 18

3.3.5 Change attributable to ACS status? ............................................... 19

3.3.6 Work gained from non-SIA approved contractors ............................ 20

3.3.7 Work lost to non-SIA approved contractors ..................................... 20

3.3.8 What are the main benefits of the ACS for your company? ............... 22

3.3.9 What changes has the ACS delivered to your company? ................... 23

3.3.10 How has the ACS changed the way your company operates ........... 24

3.3.11 Are your standards higher as a result of ACS status? .................... 25

3.3.12 Has the ACS raised overall standards in private security industry? .. 26

3.3.13 What benefits has the ACS brought to the security industry?..........27

3.3.14 What have the public gained from the ACS? ................................. 28

3.3.15 What is the general perception of the ACS within buyers of security

services? ............................................................................................ 29

3.3.16 Should the Fast Track route to approval now be phased out? ......... 30

SIA (01957R-AG / V1) 3

3.3.17 Should any refinements be made to the ACS workbook to make it

more user friendly? .............................................................................. 31

3.3.18 Should approved contractors be required to conform to the relevant

British Standards? ............................................................................... 32

3.3.19 Is the 85% licensing requirement still the most appropriate level? If

not is it too high or too low? ................................................................. 33

3.3.20 Is it an appropriate time to raise the standards for some of the

workbook criteria? ............................................................................... 34

3.3.21 What characteristics does a “fit and proper” organisation have? ..... 35

3.3.22 What are the most important changes you would like to see made to

the ACS? ............................................................................................ 36

3.3.23 Are there any observations or feedback you would like to submit? .. 37

4 NON-ACS COMPANIES .......................................................................... 38

4.1 Introduction ....................................................................................... 38

4.2 Company profile .................................................................................. 38

4.2.1 Sector(s) covered ........................................................................ 38

4.2.2 Size of business .......................................................................... 39

4.2.3 Number of clients ........................................................................ 39

4.2.4 Client sites ................................................................................. 40

4.3 Questions about the ACS ...................................................................... 40

4.3.1 Proportion of clients that require the ACS ....................................... 40

4.3.2 Proportion of private sector clients ................................................ 41

4.3.3 Turnover over the past year ......................................................... 42

4.3.4 Percentage change in turnover ...................................................... 42

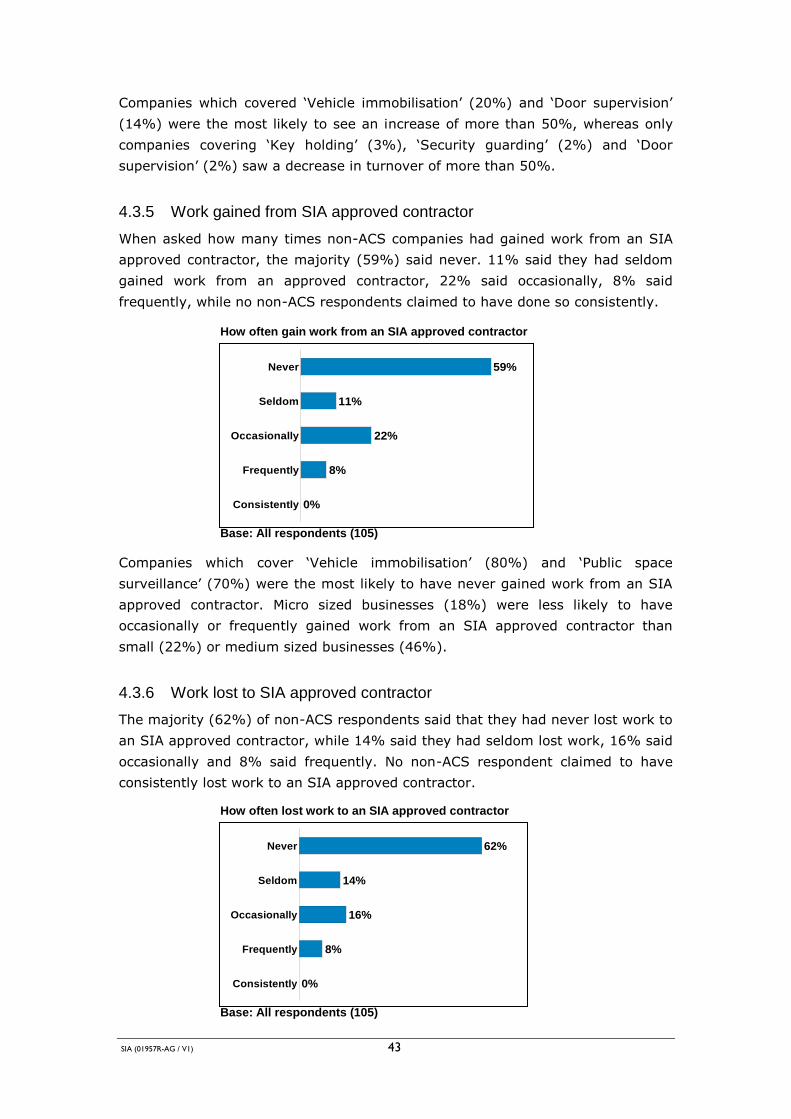

4.3.5 Work gained from SIA approved contractor .................................... 43

4.3.6 Work lost to SIA approved contractor ............................................ 43

4.3.7 What does the ACS mean to you? .................................................. 45

4.3.8 Are you considering applying for the ACS status? ............................ 46

4.3.9 Why have you not pursued gaining the ACS status? ......................... 47

4.3.10 What do you consider to be the main benefits of the ACS .............. 48

4.3.11 What benefits do you think the ACS has brought to the security

industry? ............................................................................................ 49

4.3.12 Has the ACS helped to raise standards in the security industry

overall? ............................................................................................. 50

SIA (01957R-AG / V1) 4

4.3.13 In your view what have the public gained from the ACS ................ 51

4.3.14 What is the general perception of the ACS within buyers of security

services? ............................................................................................ 52

4.3.15 What are the most important changes you would like to see made to

the ACS? ............................................................................................ 53

4.3.16 Are there any other observations or feedback you would like to

submit? ............................................................................................. 54

5 BUYERS OF SECURITY .......................................................................... 55

5.1 Introduction ....................................................................................... 55

5.2 Company profile .................................................................................. 55

5.2.1 Sector(s) covered ........................................................................ 55

5.2.2 Size of business .......................................................................... 55

5.2.3 Number of security providers ........................................................ 56

5.3 Questions about the ACS ...................................................................... 56

5.3.1 Proportion of ACS approved security providers ................................ 56

5.3.2 Frequency of security providers contract review .............................. 57

5.3.3 Use of non-approved contractors ................................................... 58

5.3.4 Why does your policy allow the use of non-approved contractors....... 59

5.3.5 What does the ACS mean to you? .................................................. 60

5.3.6 What are the advantages and disadvantages of using ACS companies

compared to non-ACS? ......................................................................... 61

5.3.7 Standards in the private security industry ...................................... 62

5.3.8 In what areas are the higher standards? ........................................ 63

5.3.9 In what additional areas would you like to see higher standards ........ 64

5.3.10 What benefits do you think the ACS has brought to the security

industry overall? .................................................................................. 65

5.3.11 In your view what have service users gained from the ACS?) ......... 66

5.3.12 If you do not use ACS companies what would make you change your

mind? ...............................................................................................67

5.3.13 What are the most important changes you would like to see made to

the ACS? ............................................................................................ 68

5.3.14 Are there any other observations or feedback you would like to

submit? ............................................................................................. 69

SIA (01957R-AG / V1) 5

1 SUMMARY OF MAIN FINDINGS

ACS COMPANIES

COMPANY PROFILE: Sectors most commonly covered by ACS companies

were „Security guarding‟ (92%) and „Key holding‟ (47%), while „Vehicle

immobilisation‟ (6%) and „Cash and valuables in transit‟ (2%) were the least

commonly selected. The majority of ACS respondents (60%) classified their

business as medium sized, while nearly a quarter (24%) classified their

company size as large, 12% as small, and only 4% as micro sized.

ACS respondents were most likely to provide security for 11-25 clients (21%),

51-100 (19%), or Over 300 (15%). 5% of respondents said they provide

security for 3-5 clients, and only 3% said they did so for 1-2. Respondents

were most likely to cover between 101-300 (20%), 26-50 and Over 300 (both

18%) client sites, and least likely to cover between 1-2 (3%), 3-5 (3%), and

6-10 client sites (7%).

QUESTIONS ABOUT THE ACS: Almost half of approved contractors (47%)

said 0-20% of their clients require the ACS, while 20% of respondents said

that 80-100% required the status. The majority of ACS respondents (56%)

said 81-100% of their clients were private sector. 21% of respondents said

that 61-80% of their clients were from the private sector, while 11% said 41-

60% were, 5% said that 21-40% were, and 7% said that 0-20% were.

51% of ACS respondents said that their company turnover had increased

since they became an SIA approved contractor, 13% said it had decreased,

and 36% said it had stayed the same. The most commonly cited increases in

turnover since ACS companies became approved were 6-10% (17%) and 11-

25% (15%), while the most commonly cited decreases were –25 to –11% and

–10 to –6% (both 4%). When asked what proportion of respondents‟ change

in turnover could be attributed to their ACS status, the majority of approved

respondents (59%) said none. 28% suggested that their status was

responsible for around 25% of the change, 6% said it was responsible for

around 50%, and only 4% of respondents said it was 100% responsible for

their change in turnover.

Over one third (36%) of ACS respondents said that they had occasionally won

work from non-approved contractors, while 31% said they had never done so.

Only 5% of approved contractors said that they consistently won work from

non-approved contractors. 41% said they never lost work to non-approved

contractors, while 31% of approved companies said they did so occasionally

and 2% said they did so consistently.

Common themes from the open ended answers included the fact that while a

significant proportion of respondents believed that the ACS shows a firm is

professional and maintains high quality standards, a large proportion of

respondents also felt that the ACS has brought limited or no benefit to their

company. Firms felt that the accreditation has increased their costs, is time

SIA (01957R-AG / V1) 6

consuming, and has created more administrative work. A large proportion of

ACS companies said that the ACS hasn‟t changed the way they operate as

they were already maintaining high quality levels before they were approved,

while a smaller proportion said that they had improved or introduced new

procedures as a result of their status.

Widespread opinion was that public is generally unaware of the ACS, and that

while some buyers are aware of the accreditation many simply choose to

ignore it in favour of lower costs. Opinion on whether the Fast Track route

should be phased out appeared to be fairly evenly split, as it was on whether

the 85% licensing requirement should be changed. A number of respondents

suggested that British Standards and the ACS should be harmonised or

combined, in order to reduce the cost, administration level and number of

audits required. Some ACS companies felt that the ACS should be made

compulsory for all contractors, while a significant proportion suggested that

the ACS needs to be more widely advertised and communicated, in order to

increase awareness.

NON-ACS COMPANIES

COMPANY PROFILE: The sectors covered most commonly by non-ACS

companies were „Security Guarding‟ (77%), „Door Supervision‟ (41%), and

„Key Holding‟ (32%), while „Vehicle Immobilisation‟ (5%), and „Cash and

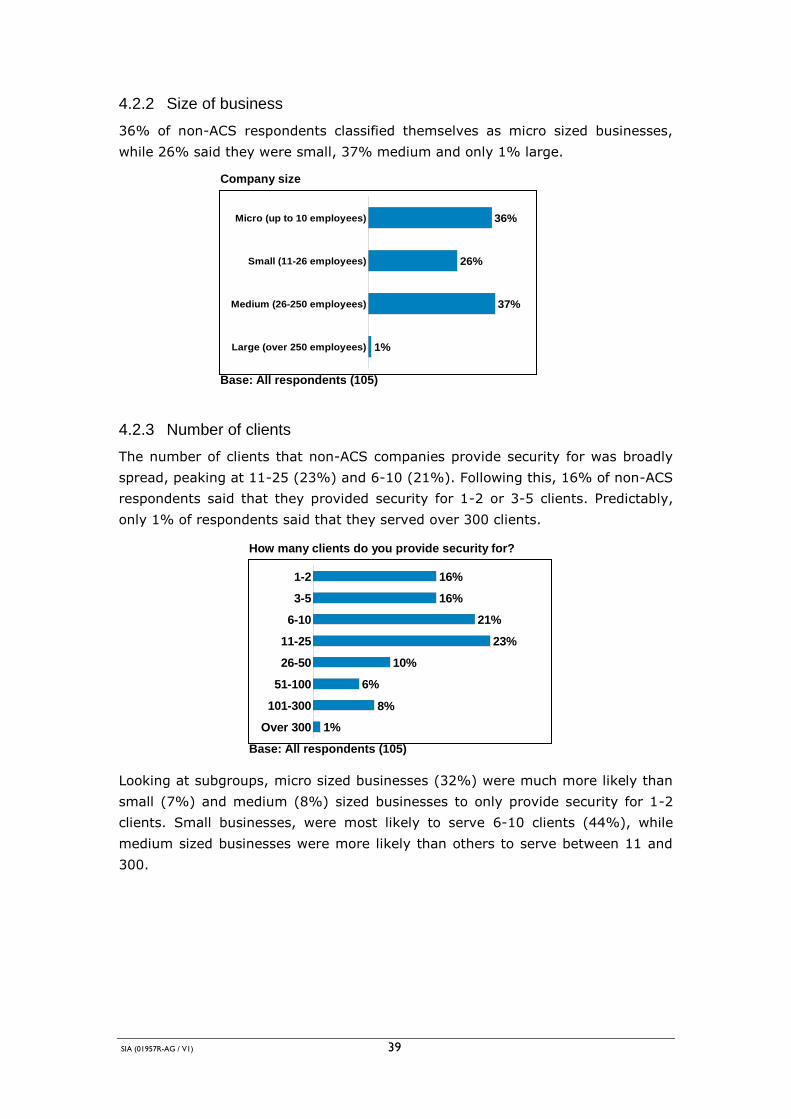

Valuables in Transit‟ (0%) were the least commonly covered. 36% of non-ACS

respondents classified themselves as micro sized businesses, while 26% said

they were small, 37% medium and only 1% large.

Non-ACS companies said they were most likely to provide security for 11-25

(23%) and 6-10 (21%) clients. 16% said that they provided security for 1-2

or 3-5 clients, while only 1% served over 300 clients. 27% of respondents

said they covered 6-10 client sites, and 24% covered 11-25. 51-100 and 101-

300 client sites were both covered by 5% of non-ACS companies, while 2%

said they covered over 300.

QUESTIONS ABOUT THE ACS: 71% of non-ACS respondents said 0-20% of

their clients require the ACS, whilst 8% said 21-40, 9% said 41-60%, 4% said

61-80%, and 9% said 81-100% did so. 41% of non-ACS respondents said

that 81-100% of their clients were private sector, while 19% said that 0-20%

of them were.

58% of non-ACS respondents said that their turnover had increased over the

past year, while 14% said it had decreased, and 28% said it had stayed the

same. 23% of non-ACS companies said that their turnover had increased by

11-25%, and 10% said it had done so by 26-50%. Companies that

experienced a decrease in turnover were most likely to have done so by –50

to –26% (7%).

59% of non-ACS companies said they never gained work from an SIA

approved contractor. 11% said they had seldom done so, while 22% said

occasionally, 8% said frequently, and no non-ACS respondents claimed to

SIA (01957R-AG / V1) 7

have done so consistently. The majority (62%) of non-ACS respondents said

that they had never lost work to an SIA approved contractor, while 14% said

they had seldom done so, 16% said occasionally and 8% said frequently. No

non-ACS respondent claimed to have consistently lost work to an SIA

approved contractor.

Common themes from the open ended answers included the view that for

some non-approved companies, the ACS represents a high standard of quality

and credibility, to which they aspire. However, a large proportion of non-ACS

respondents felt that the ACS is an expensive, unnecessary exercise, and a

waste of their time. A very large proportion of respondents said that they are

considering, or already in the process of applying for ACS status, yet a

significant proportion also said that they were not.

While many non-approved contractors felt that ACS accreditation would give

them recognition within the industry, respondents were likely to say that they

had not persued the accreditation because of financial reasons, suggesting the

cost of becoming accredited was too high, and offered minimal advantages in

return. One commonly held view was that the ACS has brought credibility to

the security industry, while a significant proportion of respondents felt that

the ACS is yet to bring any benefits to the industry, and has simply increased

the cost of operating within it.

With similar responses to the accredited companies, many non-approved firms

felt that the public has not gained anything from the ACS, and that few are

aware of its existence. They agreed that buyers are either unaware of the

ACS, or choose to ignore the accreditation in favour of lower costs. A large

proportion of respondents suggested that the SIA should improve its

communication, reduce the costs associated with the scheme, and simplify the

application process.

BUYERS OF SECURITY

COMPANY PROFILE: 71% of buyers covered the private sector, while 48%

said they covered the public sector. Buyers were most likely to be medium

sized businesses (37%), followed by micro (29%), large (19%) and finally

small (15%). The majority of buyers (53%) said that they only used one

security provider, while 16% said they used two, 7% said three, 4% said four,

and 20% used five or more.

QUESTIONS ABOUT THE ACS: When asked what proportion of their security

providers are ACS approved, one third of buyers (33%) said they used no

approved providers, while a quarter (25%) said that 100% of their security

providers were ACS approved. When asked how frequently buyers of security

review contracts with security providers, 36% said they did so every 0-6

months. Almost one third of buyers (32%) said they reviewed contracts every

7-12 months, while 15% did so every 2 years, 12% every 3 years, and only

5% every 4 years.

SIA (01957R-AG / V1) 8

49% of buyers said they had policies that allow the use of non-approved

contractors, while 51% did not. 52% of buyers agreed that the ACS has

helped to raise standards in the private security, while 48% disagreed.

Common themes from the open ended answers included the view that

approved contractors were often no better than unapproved, yet were more

expensive. Some buyers suggested that they value relationships built up over

time with non-ACS companies, higher than the accreditation itself. For a

number of buyers, the ACS represents certain professional standards within

the industry, and has given them more confidence in the industry as a whole.

However, a significant proportion of buyers regard the accreditation as an

expensive waste of time and money. Suggested advantages of the scheme

included the idea that ACS companies were better managed, meet

professional standards, and are more reliable. However, disadvantages were

also highlighted, including the opinion that ACS companies are more

expensive, require more paperwork, and don't necessarily provide a better

service.

Some buyers suggested that the ACS had increased standards in all areas

across the industry, while others pinpointed more specific areas including

customer care and more professional staff. Although respondents often felt

that the ACS has made the industry more professional and raised minimum

standards, a significant proportion claimed that the ACS has brought no

benefits to the industry as a whole, and is an expensive waste of time. While a

large proportion of buyers suggested that service users have gained nothing

from the ACS, fewer respondents suggested that users have gained from

increased professionalism and well trained staff. In terms of potential

improvements to the scheme, some buyers suggested that the scheme should

be mandatory, that enforcement and regulation should be stricter, and that

communication needs to be improved.

COMPARATIVE QUESTIONS

COMPANY PROFILE: The sector covered most commonly by both ACS and

non-ACS companies was „Security guarding‟ (92% and 77% respectively),

while „Close protection‟ (7% vs 10%), „Vehicle immobilisation‟ (6% vs 5%)

and „Cash and valuables in transit‟ (2% vs 0%) were least likely to be

covered. Respondents from all subgroups were most likely to classify their

business as medium sized. Non-ACS companies were more likely than others

to be either micro sized or small (62%), while ACS respondents were the most

likely to be either medium or large (83%).

Respondents from non-ACS companies were more likely to serve between 1

and 10 clients (53%) than those from ACS companies (21%), while approved

contractors (26%) were more likely than non-approved (9%) to provide

SIA (01957R-AG / V1) 9

security for over 100 clients. Non-ACS companies were significantly more

likely to cover between 1 and 10 client sites (57% vs 14%), while ACS

companies were more likely to cover over 100 client sites (38% vs 7%).

Predictably, the majority of non-ACS companies said that 0-20% of their

clients (71%) do not require the approved status, while more surprisingly

47% of approved contractors also said that this was the case. Respondents

from ACS companies (32%) were more likely than those from non-ACS (12%)

to say that over 60% of their clients require the ACS. Around half (49%) of all

businesses said that 81-100% of their clients are from the private sector.

Non-ACS companies (19%) were more likely than ACS (7%) to say that 0-

20% of their clients are from the private sector, while ACS companies were

significantly more likely to say that over 60% of their clients were (78%) than

non-ACS companies (54%).

Non-ACS companies (58%) were slightly more likely than ACS (51%) to say

they saw an increase in turnover. Responses of ACS and non-ACS companies

appeared similar when asked what proportion their turnover had changed by,

with „no change‟ (31% vs 27%) and an increase of 11 to 25% (15% vs 23%)

being the most commonly selected. Non-ACS companies were more likely to

report a decrease of over 25% (10% compared to 4%), or an increase of over

25% (18% compared to 12%) than ACS companies. While 59% of non-

approved respondents said that they had never gained work from approved

firms, 31% of approved firms said the same about their counterparts. 62% of

non-ACS companies said that they had never lost work to approved firms,

while only 41% of ACS companies said the same. 44% of ACS companies said

that they occasionally, frequently or consistently lost work to non-approved

contractors, while only 24% of non-ACS companies said the same.

Generally the responses of buyers, ACS and non-ACS respondents were very

similar in terms of open ended questions. Many respondents said the ACS

gives a firm recognition within the industry and shows that they meet certain

quality standards, while others suggested it was an expensive waste of time.

While 52% of buyers suggested that the ACS has helped to raise industry

standards, 48% disagreed. While both approved and non-approved

respondents said that the ACS has had very little or no impact on industry

standards, some suggested that it had brought a universal quality standard to

the industry.

Respondents from ACS and non-ACS firms suggested that the public is

generally unaware of the ACS. They also suggested that most buyers were not

aware the accreditation, and that those who were choose to ignore it in favour

of lower costs. However, far more buyers appeared to be aware of the ACS

than approved and non-approved companies thought, although many of them

did admit to ignoring the accreditation in favour of lower costs. A variety of

changes were suggested for the ACS, including the idea that the scheme

SIA (01957R-AG / V1) 10

should be made mandatory and that the ACS needs to be more widely

promoted, in order to increase public awareness and interest in the scheme.

Respondents from all subgroups agreed that the SIA‟s communication needs

to be vastly improved, as do slow administrative processes. Respondents from

the non-ACS and buyers‟ surveys both complained about immigrants working

in the industry illegally.

SIA (01957R-AG / V1) 11

2 INTRODUCTION

The Security Industry Authority (SIA) commissioned Snap SurveyShop to carry

out research into the benefits of the Approved Contractor Scheme (ACS), and

analyse the results. This report contains the research findings.

2.1 Background

The research was undertaken to establish whether the Approved Contractor

Scheme (ACS) is delivering on its purpose i.e. to raise standards in the private

security industry and therefore enhance public protection.

This research aimed to establish the drivers, value for money, interests and

benefits in the ACS. It also aimed to identify who uses ACS companies, why, and

what the impact of ACS is on buyers, end users and keys partners, in order to

determine future promotion and increased buyer recognition.

The research will provide input into an independent review of the scheme being

conducted on the SIA‟s behalf by the Office of Government and Commerce (OGC)

that will report in February 2008.

2.2 Methodology

This research comprised of three surveys, completed by three different groups of

respondents (approved companies, non-approved companies and buyers of

security). Firstly, companies registered on the Approved Contractor Scheme were

targeted by e-shot, as were the second group; Non-ACS companies. Thirdly, the

Communication of the online questionnaire was sent via a news release and

website link through approximately 4 to 5 media partners (including Security

Management Today (SMT), Infologue and the British Institute of Facilities

Management) to buyers of security.

A total of 301 responses were received, giving the ACS survey a response rate of

29% and the Non-ACS a rate of 19%, while the response rate for the buyers

survey is unknown.

Completed responses were collated and sent to Snap Surveys who carried out the

analysis. The principal contacts for the survey were Imogen Harwood at SIA and

Alex Green at Snap Surveys.

2.3 Analysis of results

Figures in this report are generally calculated as a proportion of respondents who

answered each question – that is, excluding "No Reply".

Some subgroup base sizes are small and so results need to be interpreted with

caution.

SIA (01957R-AG / V1) 12

2.4 Structure of this report

The main body of the report is divided into the following sections, which look at

the survey results in detail:

- ACS Companies

- Company profile

- Questions about the ACS

- Non-ACS Companies

- Company profile

- Questions about the ACS

- Buyers of Security

- Company profile

- Questions about the ACS

- Comparative questions

- Company profile

- Questions about the ACS

The appendix contains a copy of the questionnaires, listings of respondents‟

comments, and full sets of data tabulations.

SIA (01957R-AG / V1) 13

3 ACS COMPANIES

3.1 Introduction

This section of the report looks at the ACS questionnaire, and the responses of

companies registered on the Approved Contractor Scheme. It looks at the profiles

of ACS companies that took part in the survey, and their responses to various

questions about the scheme.

3.2 Company profile

This section of the report profiles ACS companies by sectors covered, company

size, and number of clients and client sites covered.

3.2.1 Sector(s) covered

ACS companies were asked which sectors their business covered. The most

commonly covered sectors were „Security guarding‟ (92%) and „Key holding‟

(47%), with „Vehicle immobilisation‟ (6%) and „Cash and valuables in transit‟

(2%) being the least commonly selected.

Sector(s) covered

Base: All respondents (121)

Security Guarding

Key holding

Door Supervision

Public Space Surveillance (CCTV)

Close Protection

Vehicle Immobilisation

Cash and Valuables in Transit

Other 6%

2%

6%

7%

92%

47%

26%

23%

SIA (01957R-AG / V1) 14

3.2.2 Size of business

The majority of ACS respondents (60%) classified their business as medium sized

(26-250 employees). Nearly a quarter (24%) classified their company size as

large (over 250 employees), 12% as small (11-26 employees), and only 4% as

micro sized (up to 10 employees).

Companies that covered „Public space surveillance‟ (71%), „Cash and valuables in

transit‟ (67%) and „Vehicle immobilisation‟ (57%) sectors were most likely to

classify themselves as large, whereas those that covered „Close protection‟ (13%)

were the most likely to classify themselves as a micro sized company.

3.2.3 Number of clients

When asked how many clients they provide security for, ACS respondents were

most likely to say 11-25 (21%), 51-100 (19%), and Over 300 (15%). 5% of

respondents said they provide security or 3-5 clients, and only 3% said they do so

for 1-2.

Looking at subgroups, companies that cover „Cash and valuables in transit‟ (100%

- although it should be noted that this was only three respondents), „Public space

surveillance‟ (29%), and „Key holding‟ (26%) were the most likely to provide

security for over 300 clients. Companies covering the „Vehicle immobilisation‟

sector were more likely than any others to provide security for 1-2 clients (14%),

3-5 clients (14%), and 6-10 clients (29%).

Base: All respondents (121)

Your company size

Micro (up to 10 employees)

Small (11-26 employees)

Medium (26-250 employees)

Large (over 250 employees) 24%

60%

12%

4%

How many clients do you provide security for?

Base: All respondents (121)

1-2

3-5

6-10

11-25

26-50

51-100

101-300

Over 300

12%

19%

12%

15%

3%

5%

13%

21%

SIA (01957R-AG / V1) 15

Predictably, micro firms (40% - again note should be taken that this is a small

base size) were more likely than small (20%), medium (7%) or large (0%)

companies to serve between 1 and 5 clients. Similarly, small companies were

most likely to serve 6-10 clients (40%), medium companies to serve from 26 to

100 clients (40%), and large firms to serve from 101 to over 300 clients (55%).

Less predictably however, micro sized companies were more likely to provide

security at the 11-25 client level (40%), than small (7%), medium (26%) and

large (10%).

3.2.4 Client sites

When asked how many client sites they cover, ACS respondents most commonly

selected 101-300 (20%), 26-50 and Over 300 (both 18%). ACS respondents were

least likely to say that they cover 1-2 (3%), 3-5 (3%), and 6-10 client sites (7%).

In terms of subgroups, there were few clear relationships between the number of

clients covered and the sectors covered by a company. For example, while

companies who cover the „Close protection‟ sector are the most likely to cover 1-2

client sites (14%), they are also the most likely to cover 26-50 (29%) and 101-

300 client sites (43%). It can be noted however that all companies covering the

„Cash and valuables in transit‟ sector said they covered over 300 client sites.

Again, relationships between the size of ACS businesses and the number of client

sites they cover were as expected. Micro companies were most likely to cover 1-2

client sites (40%), small to cover 3-5 and 6-10 (20% and 33% respectively),

medium to cover 26-50 (25%) and 51-100 (22%), and large companies to cover

101-300 and Over 300 (28% and 48% respectively). Again however, micro sized

companies were more likely to cover 11-25 client sites (40%) than small (7%),

medium (19%) or large companies (3%).

3.3 Questions about the ACS

This section looks at the responses of ACS companies when asked what

proportion of their clients require the ACS, if company turnover has been affected

by their approved status, and how regularly work is gained from or lost to non-

Number of client sites covered

Base: All respondents (117)

1-2

3-5

6-10

11-25

26-50

51-100

101-300

Over 300

18%

16%

20%

18%

3%

3%

7%

15%

SIA (01957R-AG / V1) 16

approved contractors. These questions were followed by a series of open-ended

questions, which examine in more detail ACS companies‟ views on the scheme.

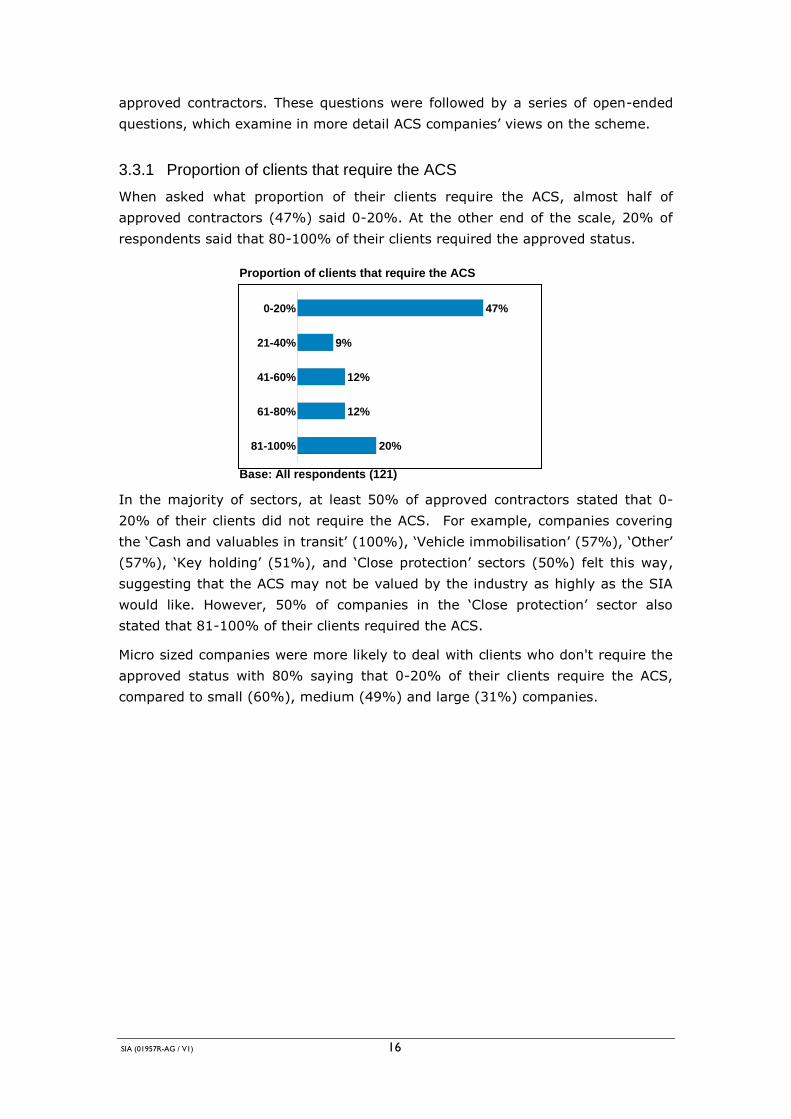

3.3.1 Proportion of clients that require the ACS

When asked what proportion of their clients require the ACS, almost half of

approved contractors (47%) said 0-20%. At the other end of the scale, 20% of

respondents said that 80-100% of their clients required the approved status.

In the majority of sectors, at least 50% of approved contractors stated that 0-

20% of their clients did not require the ACS. For example, companies covering

the „Cash and valuables in transit‟ (100%), „Vehicle immobilisation‟ (57%), „Other‟

(57%), „Key holding‟ (51%), and „Close protection‟ sectors (50%) felt this way,

suggesting that the ACS may not be valued by the industry as highly as the SIA

would like. However, 50% of companies in the „Close protection‟ sector also

stated that 81-100% of their clients required the ACS.

Micro sized companies were more likely to deal with clients who don't require the

approved status with 80% saying that 0-20% of their clients require the ACS,

compared to small (60%), medium (49%) and large (31%) companies.

Proportion of clients that require the ACS

Base: All respondents (121)

0-20%

21-40%

41-60%

61-80%

81-100%

12%

12%

9%

47%

20%

SIA (01957R-AG / V1) 17

3.3.2 Proportion of private sector clients

When asked what proportion of their clients are private sector, the majority of

ACS respondents (56%) said 81-100%. 21% of respondents said that 61-80% of

their clients were from the private sector, while 11% said 41-60% were, 5% said

that 21-40% were, and 7% said that 0-20% were.

Companies covering the „Vehicle immobilisation‟ (86%), „Cash and valuables in

transit‟ (67%) and „Close protection‟ (63%) sectors were the most likely to have

81-100% of their clients in the private sector. However, companies covering the

„Vehicle immobilisation‟ sector (14%) were also the most likely to have 0-20% of

their clients in the private sector, slightly contradicting the information above.

Medium (60%) and large (59%) companies were more likely than small and micro

sized companies (both 40%) to have over 80% of their clients in the private

sector. No micro sized companies said that 0-20% of their clients were in the

private sector, compared to small, medium and large companies (all 7%).

3.3.3 Effect of approved status on company turnover

51% of ACS respondents said that their company turnover had increased since

they became an SIA approved contractor. 13% said that their turnover had

decreased, while 36% said it had stayed the same.

Micro sized companies (60%) were more likely than small (0%), medium (17%)

and large companies (3%) to say their turnover had decreased since they became

Proportion of clients that are private sector

Base: All respondents (121)

0-20%

21-40%

41-60%

61-80%

81-100% 56%

7%

5%

11%

21%

Effect on company turnover

Base: All respondents (121)

Increased

Decreased

Stayed the same

51%

13%

36%

SIA (01957R-AG / V1) 18

an approved contractor, whereas small companies (80%) were the most likely to

say their turnover had stayed the same. Medium (53%) and large companies

(69%) were significantly more likely than small and medium companies (both

20%) to report an increase in turnover since they achieved their approved

contractor status.

Companies covering the „Cash and valuables in transit‟ (100%), „Close protection‟

(63%) and „Door supervision‟ (63%) sectors were the most likely to have

reported an increase in turnover since they became approved contractors. Those

in the „Close protection‟ sector (25%) were the most likely to report a decrease,

whereas those in the „Vehicle immobilisation‟ (57%) and „Other‟ (43%) sectors

were the most likely to see no change in turnover.

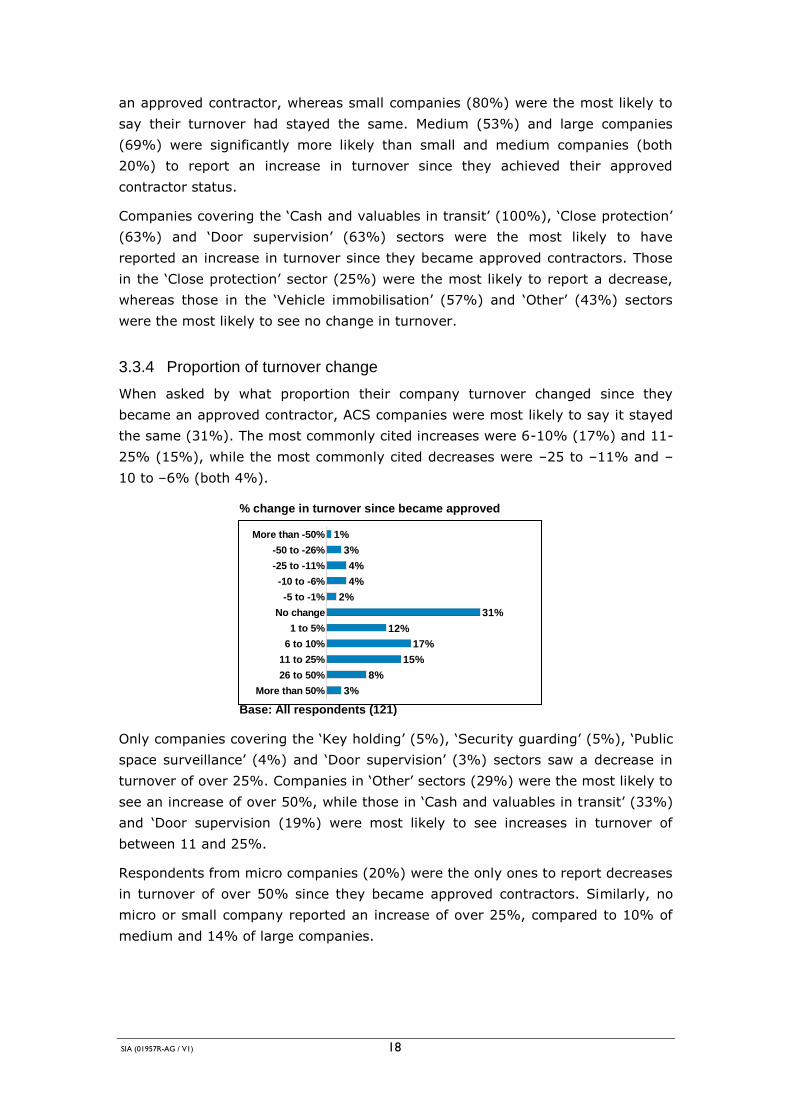

3.3.4 Proportion of turnover change

When asked by what proportion their company turnover changed since they

became an approved contractor, ACS companies were most likely to say it stayed

the same (31%). The most commonly cited increases were 6-10% (17%) and 11-

25% (15%), while the most commonly cited decreases were –25 to –11% and –

10 to –6% (both 4%).

Only companies covering the „Key holding‟ (5%), „Security guarding‟ (5%), „Public

space surveillance‟ (4%) and „Door supervision‟ (3%) sectors saw a decrease in

turnover of over 25%. Companies in „Other‟ sectors (29%) were the most likely to

see an increase of over 50%, while those in „Cash and valuables in transit‟ (33%)

and „Door supervision (19%) were most likely to see increases in turnover of

between 11 and 25%.

Respondents from micro companies (20%) were the only ones to report decreases

in turnover of over 50% since they became approved contractors. Similarly, no

micro or small company reported an increase of over 25%, compared to 10% of

medium and 14% of large companies.

% change in turnover since became approved

Base: All respondents (121)

More than -50%

-50 to -26%

-25 to -11%

-10 to -6%

-5 to -1%

No change

1 to 5%

6 to 10%

11 to 25%

26 to 50%

More than 50%

4%

4%

3%

1%

2%

31%

12%

17%

15%

8%

3%

SIA (01957R-AG / V1) 19

3.3.5 Change attributable to ACS status?

When asked what proportion of respondents‟ change in turnover could be

attributed to their ACS status, the majority of approved respondents (59%) said

none. 28% of respondents suggested that their approved status was responsible

for around 25% of their change in their turnover, while 6% said it was responsible

for around 50%. Only 4% of respondents said that their ACS status was 100%

responsible for their change in turnover.

Companies in the „Cash and valuables in transit‟ (100%), „Public space

surveillance‟ (64%) and „Key holding‟ (58%) sectors were the least likely to

attribute any change in their turnover to their approved status. Those companies

in „Close protection‟ (63%) and „Other‟ (43%) were most likely to attribute around

25% of their turnover change to their status, while those in „Vehicle

immobilisation‟ (14%) were the most likely to suggest their status was

responsible for around 50% of their turnover change. Companies in „Close

protection‟ (13%) were the most likely to suggest that their ACS status was

wholly responsible for their change in turnover.

Small (80%) and large companies (66%) were less likely than micro (20%) and

medium sized (54%) companies to attribute none of their change in turnover to

their approved status, while micro companies (20%) were the most likely to say

ACS status was 100% responsible.

% of change attributable to ACS status

Base: All respondents (121)

None

Around 25%

Around 50%

Around 75%

All

3%

6%

28%

59%

4%

SIA (01957R-AG / V1) 20

3.3.6 Work gained from non-SIA approved contractors

When asked how often they had won work from non-approved contractors, over

one third (36%) of ACS respondents said they had done so occasionally, while the

second most commonly selected answer was never (31%). Only 5% of approved

contractors said that they consistently won work from non-approved contractors.

Respondents from companies in the „Vehicle immobilisation‟ (43%), „Cash and

valuable in transit‟ (33%) and „Security guarding‟ (32%) sectors were the most

likely to say that they had never gained work from a non-SIA approved

contractor. Firms in the „Close protection‟ sector (13%) were the most likely to

say that they consistently gained work from non-SIA approved firms.

There were few differences between the responses of small and medium

businesses in this case, however micro (20%) and large (24%) companies were

less likely to say that they never gained work from non-approved contractors than

small (40%) and medium (32%), and more likely to say they did so consistently

(40% and 7% respectively).

3.3.7 Work lost to non-SIA approved contractors

When asked how often they lose work to non-approved contractors, ACS

companies were most likely to say never (41%). 31% of approved companies said

that they occasionally lost work to non-approved contractors, while only 2% said

they did so consistently.

How often gain work from non-SIA approved contractor

Base: All respondents (121)

Never

Seldom

Occasionally

Frequently

Consistently

3%

36%

25%

31%

5%

How often lose work to non-SIA approved contractor

Base: All respondents (121)

Never

Seldom

Occasionally

Frequently

Consistently

11%

31%

15%

41%

2%

SIA (01957R-AG / V1) 21

No respondents from micro sized companies claimed that they never lost work to

non-approved contractors, compared to 55% of large, 47% of small, and 38% of

medium sized companies. Respondents from medium sized companies (4%) were

the only subgroup to say that they consistently lost work to non-SIA approved

contractors.

Companies in the „Cash and valuables in transit‟ (67%) and „Public space

surveillance‟ (54%) sectors were the most likely to say they never lost work to

non-approved contractors, while those in „Key holding‟ (19%) and „Close

protection‟ (25%) were most likely to say they seldom did so. A large number of

respondents in all sectors said that they occasionally lost work, while companies

in „Vehicle immobilisation‟ (57%) were most likely to say that they did so

frequently. While no respondents from companies covering „Cash and valuable in

transit‟, „Vehicle immobilisation‟ or „Other‟ said they consistently lost work to non-

SIA approved contractors, those firms in the „Close protection‟ sector (13%) were

the most likely to do so.

SIA (01957R-AG / V1) 22

3.3.8 What are the main benefits of the ACS for your company? (open

ended)

The most common themes among the responses of ACS companies included the

view that being an SIA approved contractor is good for corporate image as it

shows that a firm maintains specific quality standards. Respondents were also

likely to mention the fact that they are able to deploy security staff while their

licence applications are being processed as a benefit. However, a significant

proportion of respondents said that the ACS has brought limited or no benefit to

their company.

Below is a representative selection of responses to this question; a full list is

available in the appendix.

"Ability to deploy up to

15% of staff on LDN"

"Because it requires competitor

companies to improve their

standards. Over time it will impact

on Security Officer wages."

"Can honestly say I have seen no benefits at

all, we were already UKAS ISO certificated and

in the first couple of years potential clients do

not appear to be interested in the ACS."

"Holding ACS enables us to

confirm our status within the

industry as one of the blue

chip companies."

"No benefits found to date.

Most of our end-users are

SME's and wouldn't know

anything about the SIA or ACS

if we hadn't told them."

"A good marketing tool for those clients that give a damn. It also puts you in a

different league to non-ACS companies and gives you credibility within the

industry. However, we still meet new clients who have no idea about the SIA or

ACS, which is frustrating considering the effort and expence of attaining and

keeping that status."

"An objective and rigerous

assessment of our ability to

provide guarding services."

SIA (01957R-AG / V1) 23

3.3.9 What changes has the ACS delivered to your company? (open ended)

A large proportion of ACS respondents said that becoming accredited has

increased their costs, is time consuming, and has created more administrative

work, while a significant amount said that is has delivered no changes. Fewer

respondents were reported that they have become more committed to quality and

communication.

Below is a representative selection of responses to this question; a full list is

available in the appendix.

"Better Quality Management as the workbook is a

good guide to operating properly. ACS Workshops

are useful for networking and seeing how others

tackle similar issues. More flexibility due to LDN's."

"ACS has enabled us to market

ourselves as a premier security

services provider for our region"

"Alot more paper work. More

thourough checks carried out and

more flexibility deploying staff."

"Increased bureaucracy,

administration and cost."

"It has helped us

to deliver a

more competent

and efficient end

product to our

clients."

"The ACS as made our and alot of the

other companies more professional in

the way we all deliver our servicers to

all our clients."

"The accreditation has increased our

overhead and administration costs with

no appreciable increase in revenue to

compensate. Clients are not willing to

pay increased rates as a result of our

company being ACS approved.

Furthermore, we have not been able to

increase payrates to the security

officers as we would have liked to or

that the security officers expected."

"It has enabled us to demonstrate to our clients and stakeholders

that we are an organisation which is committed to continual

improvement and development and reflects our determination to

improve the image and standing of our security industry"

"Need to comply to ACS requirements

which is time consuming. ACS is

aiming to drive us where we would

wish to go, but is forcing us to do

comply at their pace, rather than our

own. This is unsustainable financially

without prudent management."

SIA (01957R-AG / V1) 24

3.3.10 How has the ACS changed the way your company operates? (open

ended)

A large proportion of approved contractors said that the ACS hasn‟t changed the

way they operate as they were already maintaining high standards of quality.

Again, respondents mentioned that the ACS has increased costs and

administrative burdens. In this case a smaller proportion of respondents reported

that the ACS has positively changed their procedures and customer service.

Below is a representative selection of responses to this question; a full list is

available in the appendix.

"Completely, we now readily

embrace best practice ,ensure that

our staff are equipted to carry out

their assigned roles and promote the

professional image of an icreasingly

recognised industry that'as playing

an important role in the working life

of the nation"

"It has allowed managers to be

more focused on service

delivery and the care and

deployment of security

officers"

"ACS has not changed the

way we operate at all, but it

has affected how we market

ourselves."

"It has led to the appointment of a corporate head

of security where as previously it was developed at

local level and different throughout the company.

Now it is all standardised."

"Ensured we maintain a

professional approach at all time s"

"More Admin, more training,

more paperwork"

"Very little apart from

the licensing aspect"

"We have promoted ourselves as an ACS company

through varied means. However as stated, it has not

made any difference to any clientele. It has changed

the way this company operates in as much as we have

cut back in other areas to save cost in order to

continue implementing ACS."

"Yes - We only employ staff

who hold an appropriate

license and the requirements

of ACS has allowed us to

focus on our administrative

practices to ensure on-gonig

compliance."

SIA (01957R-AG / V1) 25

3.3.11 Are your standards higher as a result of being an ACS company? (open

ended)

Again, a large proportion of respondents said that their standards remained

fundamentally unchanged as they were already adhering to high quality

standards. A smaller proportion of ACS respondents said that they had improved

or introduced new procedures as a result of their approved status.

Below is a representative selection of responses to this question; a full list is

available in the appendix.

"definitely the standards are higher, the

ACS brought in more direct

responsibility within every organization

from top to bottom and it touches every

aspect of management you can think of

ranging from finance to health & safety

right through to the least person in

every organization has responsibility."

"Our standards are higher in that we are adhering to the legislation, and whilst this

can sometimes make operational decisons more difficult it is the only way as a

company we would want to operate post legislation. I do not believe our standards

are higher if you take of the legislation aspect as we always adhere to BS7499 and

ISO 9000. However, the extra checks and balances of ACS are a benefit."

"Not really, we already had fully

certificated, effectively run

management systems [to ISO 9001,

14001, OHSAS 1800 etc]"

"New policies and procedures

are in place in order to

comply with ACS, however

the standards of service

remain as they have always

been. Actual 'on the ground'

procedures and doing the job

is the same."

"High standards have always been a

priority and are largely unchanged"

"No we always have worked

to a very high standard"

"Yes people have more focus

and a managable template to

follow - due to enhanced

awareness of role."

SIA (01957R-AG / V1) 26

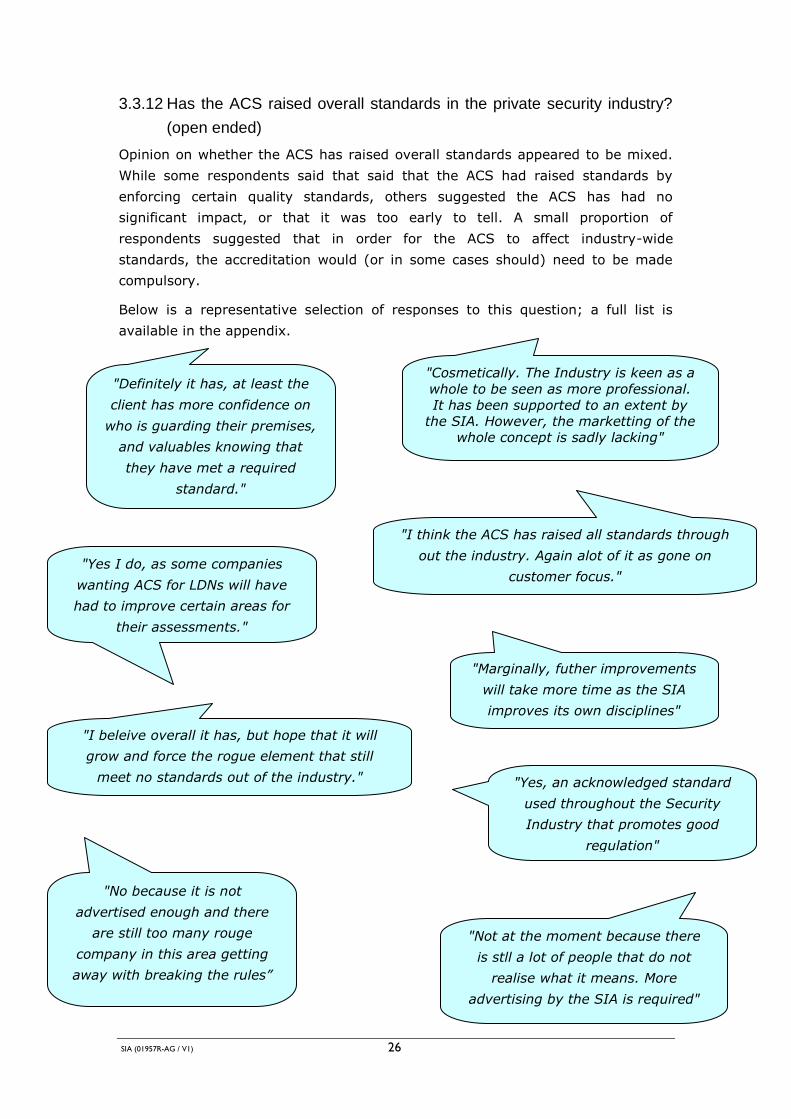

3.3.12 Has the ACS raised overall standards in the private security industry?

(open ended)

Opinion on whether the ACS has raised overall standards appeared to be mixed.

While some respondents said that said that the ACS had raised standards by

enforcing certain quality standards, others suggested the ACS has had no

significant impact, or that it was too early to tell. A small proportion of

respondents suggested that in order for the ACS to affect industry-wide

standards, the accreditation would (or in some cases should) need to be made

compulsory.

Below is a representative selection of responses to this question; a full list is

available in the appendix.

"Definitely it has, at least the

client has more confidence on

who is guarding their premises,

and valuables knowing that

they have met a required

standard."

"No because it is not

advertised enough and there

are still too many rouge

company in this area getting

away with breaking the rules”

"Marginally, futher improvements

will take more time as the SIA

improves its own disciplines"

"I think the ACS has raised all standards through

out the industry. Again alot of it as gone on

customer focus."

"I beleive overall it has, but hope that it will

grow and force the rogue element that still

meet no standards out of the industry."

"Cosmetically. The Industry is keen as a

whole to be seen as more professional.

It has been supported to an extent by

the SIA. However, the marketting of the

whole concept is sadly lacking"

"Yes, an acknowledged standard

used throughout the Security

Industry that promotes good

regulation"

"Not at the moment because there

is stll a lot of people that do not

realise what it means. More

advertising by the SIA is required"

"Yes I do, as some companies

wanting ACS for LDNs will have

had to improve certain areas for

their assessments."

SIA (01957R-AG / V1) 27

3.3.13 What benefits has the ACS brought to the security industry? (open

ended)

While a significant proportion of respondents said that they believed the ACS has

brought a universal quality standard, standardisation and increased awareness to

the security industry, respondents were more likely to say that they believed the

ACS had brought few or no benefits to the industry as a whole.

Below is a representative selection of responses to this question; a full list is

available in the appendix.

"An overall standard as far as guardin is

concerned. Keyholding and Alarm Response

Needs the support of the Approved

Contractors sheme and the SIA"

"ACS has provided the

groundwork, but we won't see

any major benefits unless we

have enforcement."

"Good sytem of regulation and guidance"

"Customers are at last starting

to recognise that ACS

companies meet a level of

standards & criteria"

"Not many in the short term. I think it

is probably going to take at least

another five, maybe ten years for the

benefits, or otherwise, of ACS to be

able to be fully evaluated and

understood"

"The introduction of the SIA/ACS is long overdue and

the benefits will be significant but only when the

controls introduced affect all those who work or are

involved in any aspect of the security industry. If this

does not happen then i think the overall effectiveness

and integrity of the scheme will be damaged"

"It has brought about trust,

confidence and most of all a

standard that is there to stay

from year to year."

"Standards and quality"

"Increased public awarness of

the fact that the industry is

trying to improve standards."

"Unfortunately we are still in

the early stages and we

believe that any advantages

that are to be gained will be

seen as the process

matures"

"It has set a common

standard."

SIA (01957R-AG / V1) 28

3.3.14 What have the public gained from the ACS? (open ended)

Common answers included the idea that the public is generally unaware the ACS

and it‟s aims, or that public gains will take time to become apparent. A significant

proportion of ACS companies suggested that the public has gained confidence and

trust in a more professional security industry, and that the accreditation is slowly

becoming more widely recognised.

Below is a representative selection of responses to this question; a full list is

available in the appendix.

"The knowledge that our industry is

professional"

"Generally if they are

aware of what the ACS

stands for and is set out to

acheive they may be more

inclined to use/trust an

ACS company"

"A little more confidence in the

industry due to regulation though

credibility has been harmed by the

recent media exposure of right to

work issues within certain security

providers."

"Assurance that the security industry is

regulated and is in the main made up of

professional security companies."

"I would like to think that the security

industry is better regulated and more trusted

but we see other security companies still

supplying men in a hut on a minimum wage,

doing the absolute bare minimum to just

about satisfy their client rating. People like

this are a laughing stock to the youth and the

public at large."

"Nothing Apart from making a nice imagie for

security companies, people dont know who the

SIA is and what you do! People working in

security have to, but general public dont know.

There our potential customers"

"No obvious gains to the public.

Reputable companies were working

to a high standard anyway."

"Very littel for the same reasons as

previously stated: many companies

are ignoring the rules, and some

have been accepted onto the ACS

under the fast track mechanism,

without being properly checked"

SIA (01957R-AG / V1) 29

3.3.15 In your view, what is the general perception of the ACS within buyers of

security services? (open ended)

While a number of approved contractors suggest that buyers are aware of the

ACS and the quality standards it carries, a larger proportion of respondents

suggest that buyers are either unaware of the accreditation, or simply choose to

ignore it in favour of lower costs. Respondents have suggested that buyers do not

fully understand the ACS and as such are unaware of its potential advantages.

Below is a representative selection of responses to this question; a full list is

available in the appendix.

"It is starting to be a criteria

for participation"

"A large number of smaller

organisations are still unaware of the

sia let alone the acs"

"It is just another accreditation level"

"Another quango-type org'n

layering on higher costs"

"Not concerned with ACS

more concerned with price

and service."

"Due to lack of advertising from the S.I.A 90% of new

enquiries dont even know about S.I.A licences never mind

what A.C.S is, It needs Advertising on a national basis like

Television in the evenings, Also the consequences of using

unlicensed persons needs to be advertised."

"Slowly filtering through that

ACS companys are the ones

to use."

"The veiw that we get is that

if we are ACS approved

contractors then we must be

doing something right."

"They do not fully understand what it means.

Buying patterns haven't changed and, if

anything, organisations are buying purely on

price. There does not appear to be any premium

attached to ACS membership."

SIA (01957R-AG / V1) 30

3.3.16 Should the Fast Track route to approval now be phased out? (open

ended)

Opinion on whether the Fast Track route should be phased out appeared to be

fairly even split. While some respondents suggested that Fast Track had served its

purpose, others argued that it should never have existed in the first place. Some

suggest that Fast Track should remain in place as up-to-date qualifications are

worth recognition, while others argue that companies have had plenty of time to

meet the new quality standards.

Below is a representative selection of responses to this question; a full list is

available in the appendix.

"I do not believe it needs to

be phased out, as the same

principles apply now as did at

the inception. Perhaps I

would shorten the time for

the initial assessment, e.g.

within six months."

"I believe that in order for

companies to benifit, fast

track should be removed.

The standard route should

be used by all companies

wishing to achieve this

accrditation."

"Fast track should be phased out as most

companies have had the opportunity to be

in a position to apply now. Also the

requirements for ACS are higher."

"No, fast track should be allowed

because contrary to the SIA's beliefs,

a lot of companys already had

excellent quality systems and vetting

procedures in place before the SIA

was even dreamed of."

"As a Company who used the fast track

system to gain A.C.S. having first gained

I.S.O 90001 2000 it should remain. This

will enable companies to experience

systems introduced and improve before

the A.C'S.assessment."

"I think it should be phased out, a lot of companies these days dont

employ unlicensed guards anymore, the initial objective was to help

companies whose employee's are still going through lincensing process

then when their was a lot of back- log it should be phased out i recon."

"Not sure if this is relevant any longer."

"Yes it should be phased out,

as it has proven to be open to

abuse in the past. Also most

genuine quality accredited

companies are in the ACS

already."

SIA (01957R-AG / V1) 31

3.3.17 Should any refinements be made to the ACS workbook to make it more

user friendly? (open ended)

While a number of respondents suggested that the workbook is user friendly in its

current format, a large proportion suggested that it should be simplified in terms

of language and content. Fewer respondents suggested that some content could

be reduced to make it more applicable to smaller companies, and that it could

contain more practical examples.

Below is a representative selection of responses to this question; a full list is

available in the appendix.

"Consider workbook to be

userfriendly in its current

format."

"I fiound the workbook hard to go through,

it was not simple and a lot of the questions

were much the same, the range of answers

were not clear. I found it long and tedious"

"It is manageable and

covers the relevant areas

but it should be reviewed for

repetition and vagueness"

"Add more examples for each

criteria. Possibly provide companies

with a book to assist in their internal

auditting. Produce a workbook for

each sector with the same criteria

but with different examples that are

more applicable to the company in

question. The workbook and the

workbook guide could be combined."

"Once again too many grey areas and a

lot of questions that are not relevant to

the security industry."

"Terminology could be made

clearer, perhaps gaining the

crystal mark would be a

good move"

"There is repetition

throughout the workbook. It

can be shorten and

simplified. On line

completion is not easy."

"Yes. So many sections overlap and the termnology could be

better. Many sections are interprited differently by companys,

auditors and the ACS. From the ACS forums it is clear that

different companies do interprite section differently."

SIA (01957R-AG / V1) 32

3.3.18 Should approved contractors be required to conform to the relevant

British Standards (e.g. BS7858), and if so in what way? (open ended)

A large proportion of respondents from ACS companies said that they believed

approved contractors should meet relevant British standards as a minimum

prerequisite. However, a significant proportion of respondents suggested that

British Standards and the ACS should be harmonised, meaning that while

contractors would still be required to meet both standards, only one audit would

be required.

Below is a representative selection of responses to this question; a full list is

available in the appendix.

"In our opinion, since SIA/ACS are 'government' organisations the law

of the land where appropriate must always be included in any form of

approval. We are open to argument as to how best to achieve this.

We have also always believed that the present practice of inspecting

companies seperately for ACS and ISO 9000 should end and the two

inspections be harmonised. We believe that they are complimentary

schemes."

"All Security Companies should conform to

this standard it is important to the

Industry as a whole but still we have lots

of individuals who for some reason are not

and I cannot think why it’s not in the ACS"

"All Approved Contractors should

demonstrate full compliance with

all relevent standards which apply

to their scope."

"This should be one of the minimum requirements of ACS as

BS7858 has been a benchmark of measurement for a number of

years. All companies should be compliant with this irrespective

of thier status within the industry. Consideration should also be

given to other Britih Standard QMS accreditations such as

BS7499 or BS7984 as appropriate."

"It was hoped that the ACS would

supercede the BS standards.

Having both means additional costs

and paperwork. The ACS should be

a standard alone benchmark for

quality."

"Yes. ACS companies should be

operating to the highest standards

available if the SIA want ACS to

become the gold standard."

"No the SIA Licence should be

sufficient providing the checks

are completed correctly."

SIA (01957R-AG / V1) 33

3.3.19 Is the 85% licensing requirement still the most appropriate level? If not

is it too high or too low? (open ended)

Opinion varied greatly in this area, with ACS respondents suggesting levels from

0% to 100% were appropriate. A large proportion of respondents agreed that the

current level remains appropriate, while a smaller proportion suggested that this

level is too high for small companies and should be lowered.

Below is a representative selection of responses to this question; a full list is

available in the appendix.

"85% is a realistic figure. Although I

would suspect, like us, that most

companies are sitting much higher than

that figure. We are at 98.5%."

"Based on the size of our

company at the moment 85%

is too high. Industry Average

company size I believe it is

acceptable."

"About right"

"Initially it was perceived we would suffer from a lack

of 'licensed' staff and the build up to 85% was

considered valuable. However there does not appear to

be a lack of licensed applicants so I see no reason to

change this level."

"I think it is low enough to achieve some flexibility

and high enough to retain some standard so I think it

should stay at the current level."

"For close protection this rule does not

work and de-values the accreditation.

To achieve ACS status in close

protection licensing must be 100%"

"It seems fine at the

moment and is a good

level of compliance. Would

not object to a small rise in

the figure up to 90%"

"Should be brought down

to 75% at least as some

time jobs come in and 5 or

6 LDN's are not enough.

This definnatly needs to be

looked at."

"Yes. We feel that this is appropriate in general and special

cases would be assessed on an individual basis by the SIA"

SIA (01957R-AG / V1) 34

3.3.20 Is it an appropriate time to raise the standards for some of the

workbook criteria? (open ended)

A large proportion of respondents suggested that current standards were

appropriate and should not be changed. Some suggested that companies should

be given more time to work towards the standards so the processes becomes part

of their everyday routines, rather than being continually updated. The other

commonly cited view was that the ACS schemes should represent the idea of

continual improvement, and as such, workbook criteria should be regularly

updated.

Below is a representative selection of responses to this question; a full list is

available in the appendix.

"As the ACS is voluntary and not to discourage

those applying for it, I believe further proof of the

ACS benefits are needed before any adjustment

in this area."

No - too soon. We need to give

adequate time for all companies

possible to become an ACS

approved contractor before

raising standards. Suggest

increasing standards in April

2010 and giving a minimum six

months notice of the intended

changes."

"It is always a good think to raise

standards but I would be worried that

things may become unachievable for

smaller companies if the requirements

become too stringent"

"I feel we are just getting

used to the existing

standards and have gone

through so much change in

the last few years that a

period of stability would be

good."

"No. A little time longer is needed to

stabilise, and sort out what is happening

with Fast Track. Once all companies are on

a level playing field, standard levels can be

looked at"

"The scheme is about continual

improvement and therefore the

answer is yes."

"yes additional training needs to

be implemented and qulity of

training, to find this out, book

yourself on a course and see the

qulity of this its appaling."

"Yes. If the standards do not increase, then the ACS will go

the way of the NSI and the BSIA."

SIA (01957R-AG / V1) 35

3.3.21 What characteristics does a “fit and proper” organisation have? (open

ended)

The responses of ACS companies varied greatly in this instance as respondents

interpreted „fit and proper‟ in a variety of ways. Common themes included

financial stability, fully trained staff, adhering to recognised quality standards,

good organisational structure and a culture of continuous improvement.

Below is a representative selection of responses to this question; a full list is

available in the appendix.

"A demonstrable commitment to providing

high quality service, a demonstrable

commitment to treating its staff and clients

well and financial stability."

"Integrity, responsibility, customer

satisfaction, profitability, good customer

retention, sound HR and Health and

Safety culture, ability to change in

accordance with customer requirements

and security needs."

"An aspiration to high

standards of excellence,

customer care and fully

trained and motivated staff"

"Financially prudent, adhere to standards

(don't play lip service), have a documented

internal audit process and comply with it."

"A 'fit and proper' organisation should be: - focussed on delivery of the

absolute best to any person(s) impacted upon - and not compliant purely

because they need to be! - concentrated on resolving of issues and ensuring

appropriate preventative measures are put in place. - targeted towards

continual self assessment and improvement as a minimum"

"Financially sound.

Complies to relevant

British Standards and in

rigourously inspected to

that standard."

"Honesty and

transparency in all its

dealings with staff,

clients and contractors"

"Quality Assurance Procedures for all processes Membership of

professional associations"

SIA (01957R-AG / V1) 36

3.3.22 What are the most important changes you would like to see made to

the ACS? (open ended)

Once again, opinion varied greatly in this area, although some common themes

were apparent. For example, a significant proportion of respondents suggested

that the ACS should be made compulsory for all contractors, and also that the

ACS needs to be more widely advertised/communicated in order to increase

awareness. A smaller proportion suggested that the costs of accreditation, and

the amount of administration work associated with the ACS should be reduced,

particularly for smaller companies who are struggling with the current levels.

Below is a representative selection of responses to this question; a full list is

available in the appendix.

"A review of its purpose and

delivery of the benefits it can

actually achieve rather than

those it notionally aspires too."

"Compulsory membership to all companies, or

relaxed rules for all companies. Keep the

playing field level and administrations costs

even for all secuerity companies in relation to

the SIA/ACAS"

"A dedicated telephone line for ACS

Companies not just the main number.

Decated team leader to contact at the

Document Handling Centre.Improved

communication"

"For it to be communicated

and become essential for

government and public bodies

to use only ACS approved

contractors."

"Enforcement and tougher

punishment on those

companies blatently

abusing the ACS scheme"

"Information on attainment

levels published. Regulation

and policing improved. More

publicity and contact with

security purchasers on

advantages of the scheme."

"More consultation"

"More communication about it, more

advertisement re the companies who are

approved, a system of company

participation, i.e. could the SIA not form a

small committee from the approved

companies who could assist in a number of

areas."

"On line system to be improved, enabling 90% of operational

issues to be dealt with on line thus freeing up the telephone

lines for urgent issues"

SIA (01957R-AG / V1) 37

3.3.23 Are there any observations or feedback you would like to submit?

(open ended)

As this is a very general question, there were few recurring themes among the

responses submitted. A large proportion of ACS respondents said that they had

nothing further to add. Again, respondents mentioned high costs, communication

problems and a need for increased publicity of the ACS.

Below is a representative selection of responses to this question; a full list is

available in the appendix.

"ACS accreditation has yet to be

the recognised requirement by

the end user. Too many other

bodies such as the BSIA,

Security Watchdog, NSI etc are

hanging on!"

"Many have been made

over the past months

about illegal staff and

companies all have fallen

on deaf ears, whats the

point, our time is money"

"Better channels of

communication and speedier

administration."

"The ACS meeting in Bristol I found very

useful, Andrew Shepperd and his team are

also very helpful whenever I call. By far

the best people I have dealt with

connected to the SIA, which has not

always been pleasant, but they are getting

there, despite the bad press recently and

still get my vote."

"I believe the benefits of ACS need to be

higlhlighted, and the only way this will truly

happen if non acs companies who are operating

illegaly are procesuted or named and shamed.

There is an expense to the bsuiness post

licencing with ACS membership and companies

will become disallusioned if value for money

cannot be demonstrated."

"On licensing... We fear that the Sia will yet again, not be in a position

to handle the volume of licence renewals. The project anagment and

implementation of the schemes doesn't always deliver."

"We are very happy with

the benefits ACS has

brought to our internal

processes and audits."

"The sia appear to be very presumtios of their position and demand certain

things that can be very hard to achieve (ie they must interview clients) and

would be hard to achieve if the roles were reversed."

SIA (01957R-AG / V1) 38

4 NON-ACS COMPANIES

4.1 Introduction