Today’s artificial intelligence

market is not easy to quantify.

Besides the lack of consensus on a coherent definition for “artificial intelligence” as a term, the

field’s nascent stage of development makes it difficult to carve out silos or hard barriers of where

one industry or application ends, and another begins.

If you’re interested in how developments in machine learning and AI might impact your own

company or then keeping an eye on trends of industry and application growth is pertinent.

We hope that this presentation will be a good jumping off point to some of the most thought-out assessments of AI and it’s “segments” as we could

collate from the web.

We’ll begin by looking through existing efforts to break up and categorize the AI market, and we’ll end by

pulling together what we believe to be the key meta-trends and insights.

CB Insights Various AI Reports (2016)

CB Insights is a New York-based research firm with under 200 employees, specializing in tech

intelligence from various soures, to include venture capital, startups, patents, partnerships, and new

media. They seem to have created some of the most relevant graphics and information about the broad AI

market.

In the graphic above, CB Insights highlights the acquisitions and fundraising deal frequency across various industries. Their own research shows healthcare

topping the list, with marketing / advertising and business intelligence trailing only slightly in 5-year deal volume.

Link to Research

“ Noteable Quotes

AI in healthcare accounted for 15% of all equity deals to artificial intelligence startups in 2015.

Smart money VCs have backed companies including Lumiata, SigTuple, Deep Genomics and

twoXAR.

The previous graphic displays funding activity from major investment firms over the last 5 years. CB Insights shows Intel, Google, and GE topping the list. The data

in this illustration seems to be derived from the number of companies funded rather than number of dollars funded (though there is likely a correlation

between the two). Knowing who is investing in what companies (and which technologies) is useful knowledge for other industry leaders who want to understand where the “smart money” is finding a home in the AI market.

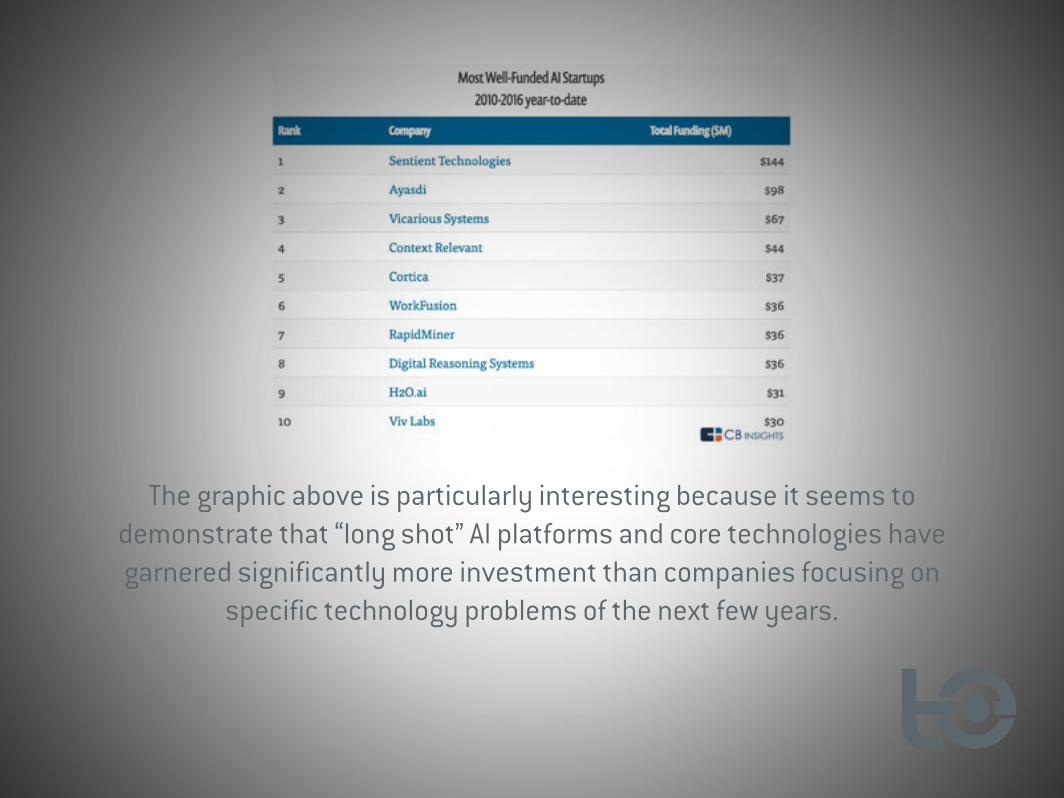

The graphic above is particularly interesting because it seems to demonstrate that “long shot” AI platforms and core technologies have garnered significantly more investment than companies focusing on

specific technology problems of the next few years.

In the days of the internet, there were battles between Netscape, Yahoo, Microsoft, and others, in order to determine who would “win the web.” It might be

said that Google came out as the winner of web search and consumer web applications broadly speaking. Investors are interested in investing the same kind of game-changer technology in AI, which seems to give broadly-focused

companies like Sentient Technologies and Vicarious Systems some of their allure.

It seems prudent to keep an eye on where these aspiring AI “industry standard” companies focus their efforts, as those domains will almost invariably gather

more momentum and excitement as this nascent field looks to new leaders vying to become global AI platforms / solutions for direction and focus.

VentureScanner AI Industry Assessment (March 2016)

http://techemergence.com/wp-content/uploads/2016/07/CB-Investors2-1200x1076.png

The AI Sector Map previously featured breaks down into 13 broad categories, with the total number of active companies in that sector in parentheses. The results

from VentureScanner’s March 2016 report is as follows:

• Deep learning/machine learning (general) (123 companies)• Deep learning/machine learning (apps) (260 companies)• NLP (gen) (154 companies)• NLP (speech rec) (78 companies)• Computer Vision/Image Rec (gen) (106 companies)• Computer Vision/Image Rec (apps) (83 companies)• Gesture control (33 companies)• Virtual personal assistants (92 companies)• Smart robots (65 companies)• Rec engines and collaborative filtering (60 companies)• Context aware computing (28 companies)• Speech to speech translation (15 companies)• Video automatic content recognition (14 companies)

Link to Research

Other charts on the VentureScanner report page show funding by AI category (by far most are in machine learning (ML) apps, followed by NLP); venture investing in AI (most in ML apps, followed by NLP); AI total funding annually (accelerating

since 2010); average funding by AI category (most in ML apps, followed by smart robots and gesture control); average age of technology by AI category (speech to

speech translation oldest, followed by gesture control, video content recommenders, and speech recognition); among others.

A total of 910 companies were accounted for in this report. VentureScanner’s same “sector analysis” for the previous year counted 633 companies.

TechEmergence Executive Consensus on AI Trends (June 2016)

http://techemergence.com/wp-content/uploads/2016/07/CB-Investors2-1200x1076.png

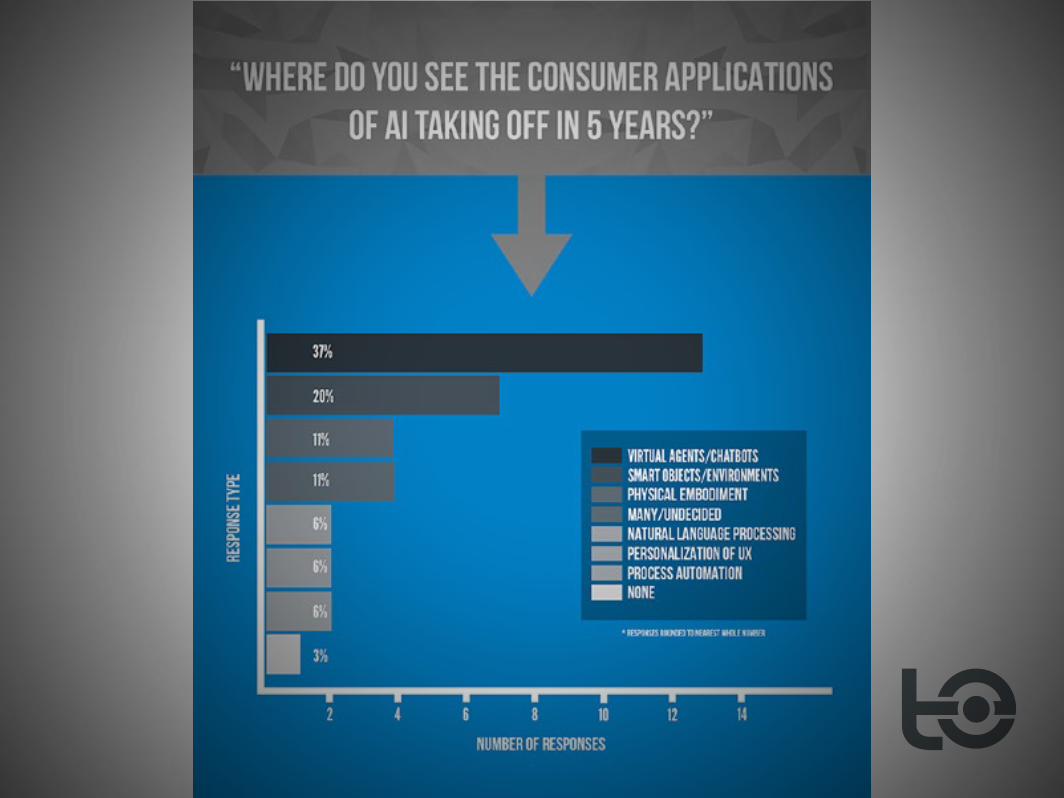

Our own recent AI industry research involved polling over 30 AI startup founders and company executives (with firms as small as six people and as large as 600). Our first consensus question asked about AI consumer technology applications

in the coming five years.

The vast majority of companies interviewed had nothing to do with chat bots or personal assistants, yet over a third of all executive responses expressed

confidence in chat bots as the most influential consumer AI technology in the coming give years.

It’s important to note that the question of technology trends was presented in an open-ended fashion, and categories (such as “smart objects / environment”,

“virtual agents”, etc) were applied after analyzing individual responses.

Link to Research

O’Reilly State of Machine Learning 2.0 (December 2015)

This article was written by Bloomberg’s Shivon Zilis, and it breaks down the “Machine Intelligence Ecosystem” into a number of categories and sub-

segments.

Shivon’s graphic lists dozens of companies, though it seems clear that many more had to be left out due to limitations of the size of this graphic. In this case, we see a different and distinct set of segments than in other research graphics,

as well as the inclusion of non-profits (i.e.: OpenAI) and open source technologies (i.e.: Caffe).

Link to Research

“ Noteable Quotes

The two biggest changes I’ve noted since I did this analysis last year are (1) the emergence of

autonomous systems in both the physical and virtual world and (2) startups shifting away from building broad technology platforms to focusing

on solving specific business problems.

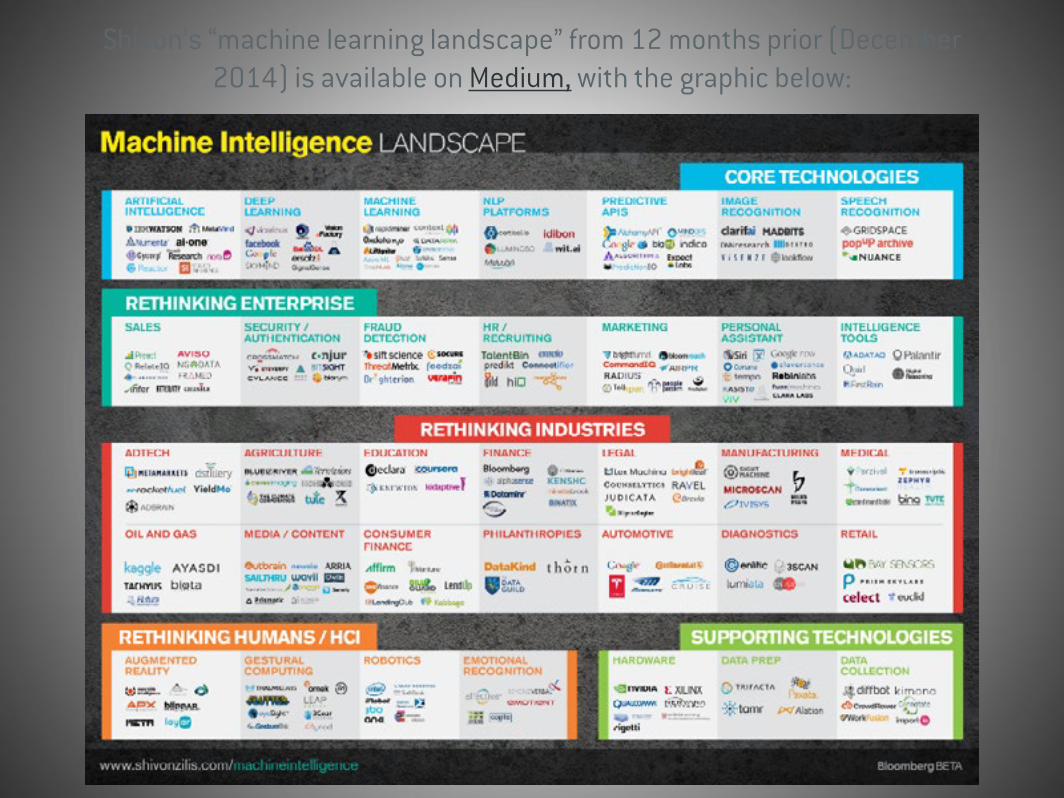

Shivon’s “machine learning landscape” from 12 months prior (December 2014) is available on Medium, with the graphic below:

Comet Labs AI and Robotics Startup Landscape (February 2016)

Comet Labs is a venture fund focused specifically on artificial intelligence-oriented technologies, and they’ve done a good deal of their own

homework in assessing the industry at large. Their own effort to map the land-scape of AI and robotics startups can be in the next slide:

The synopsis of their brief findings can be found below:

While this graphic does draw attention to various discrete industries and compa-nies, it seems to be a bit more broadly focused and includes a number of startup but also a handful of companies like Yaskawa (founded over 100 years ago), Ap-

ple (Siri) and Nvidia, which don’t seem to belong in a graphic labeled as “startups.”

That discretion aside, the article also doesn’t make it clear how many companies were assessed, or how and why the industry delineations were drawn out (where

is “natural language processing” or “assistants” or “marketing / advertising”?)

The graphic does help draw attention to some of the major application areas of AI (and mirrors Comet Labs’ own logo), but doesn’t appear as comprehensive or to

draw conclusive enough insights about the current “industry breakdown” to warrant serious merit.

In the Comet Labs article in which those graphics were featured, there are interesting and useful examples given of the ongoings of specific startups within

the various sectors highlighted.

(Note:We recently interviewed Comet Labs’ Managing Director Saman Farid, and the episode will air on our podcast soon).

BCC Research Smart Machines Market Report (May 2014)

BCC Research presents their growth forecasts for 2019-2024 (in millions) below:

The graphic featured on the previous slide is from the Siemens’ corporate blog. It is interesting to note that BCC predicts the highest aggregate 5-year growth rate in the area of digital assistants, which seems to corroborate with our own 5-year

AI trends executive consensus.

Link to Research

Nvidia’s Report on GPU Usage (January 2016)

Graphics processing unit (GPU) is a specialized electronic circuit, designed to rapidly manipulate and alter memory to accelerate the creation of images in a

frame buffer intended for output to a display (credit). Nvidia is one of the world’s leading GPU manufacturers, and they have chronicled and visualized the growth

of GPU-related sales into various industry segments, as seen in the next slide:

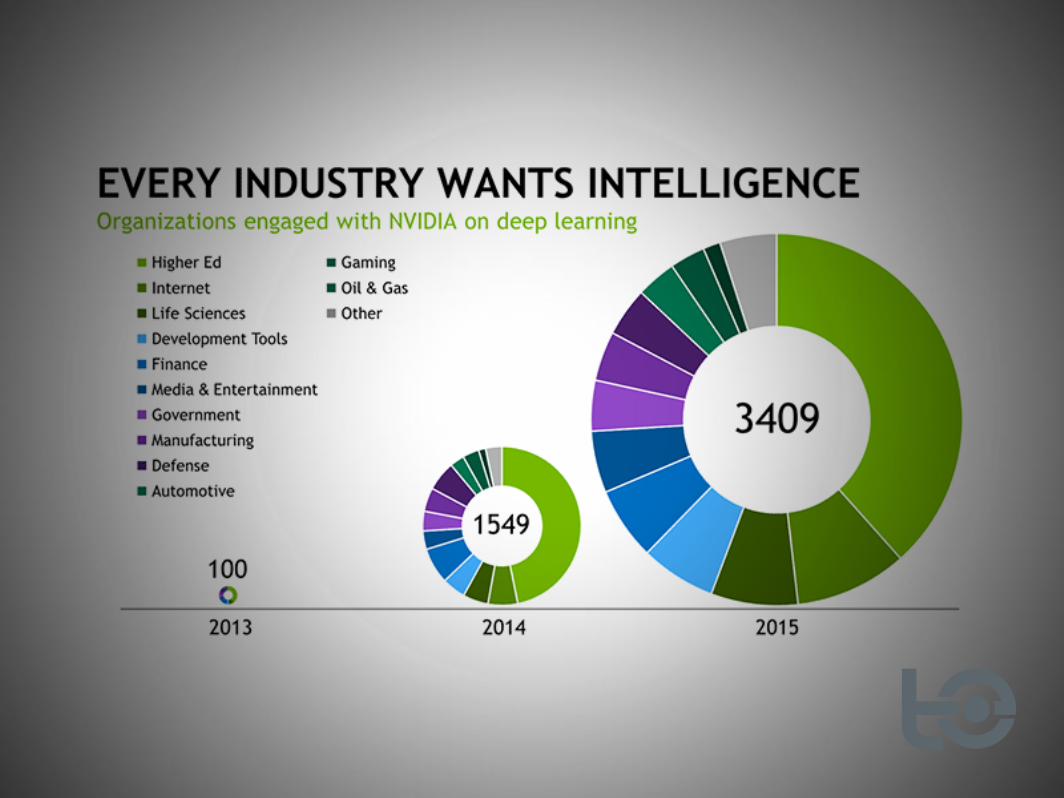

While GPU usage is by no means a causal influence on the applications of AI in a given industry, it provides a certain amount of context on industry growth (Nvid-ia claims to have sold GPUs to nearly 100 times more companies in 2015 than in 2013, a significant leap). Even in 2015, we can see that higher education (which we can presume to imply university research) is the largest consumer of Nvidia’s

GPU technology.

It can be presumed that the shrinking relative percentage of sales to “Higher Ed” will continue as more companies in all sectors begin adapting machine learning

into their regular processes.

Link to Research

“ Noteable Quotes

In just two years, the number of companies NVIDIA collaborates with on deep learning has jumped nearly 35x to over 3,400 companies. Industries such as healthcare, life sciences,

energy, financial services, automotive, manufacturing, and entertainment will benefit by

inferring insight from mountains of data.

Other Vertical BreakdownsThere are a number of other attempts to value and properly segment AI

verticals. The following slides feature a few worth considering:

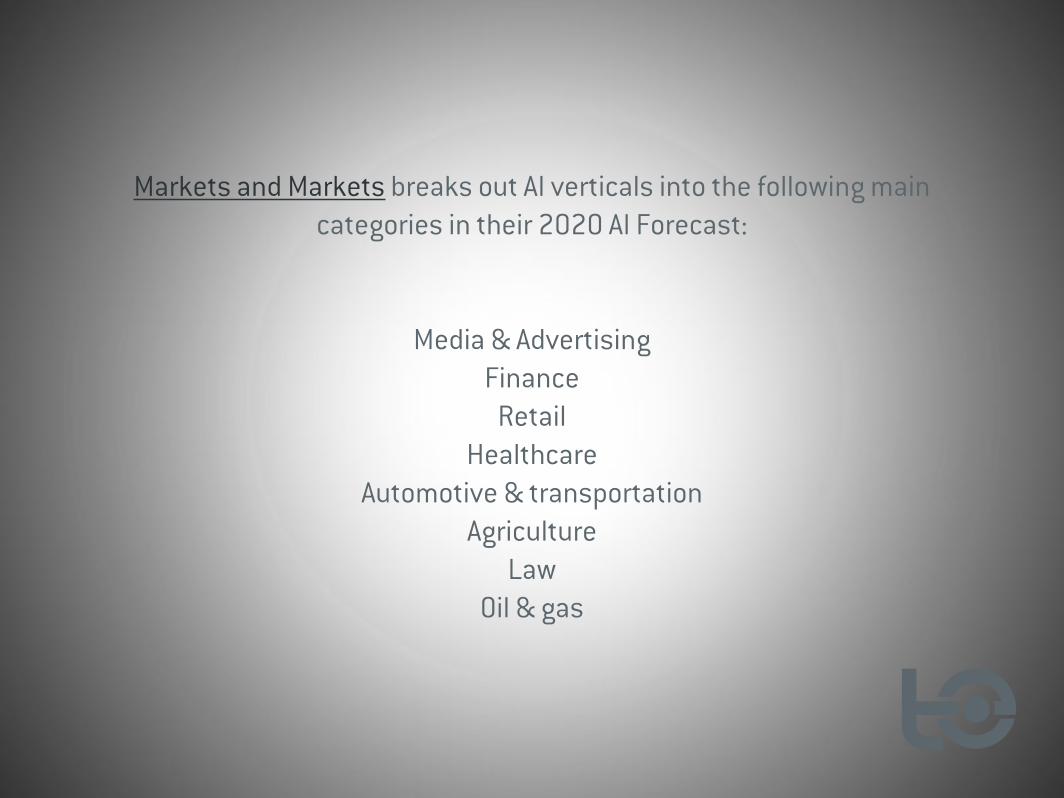

Markets and Markets breaks out AI verticals into the following main categories in their 2020 AI Forecast:

Media & AdvertisingFinance

RetailHealthcare

Automotive & transportationAgriculture

LawOil & gas

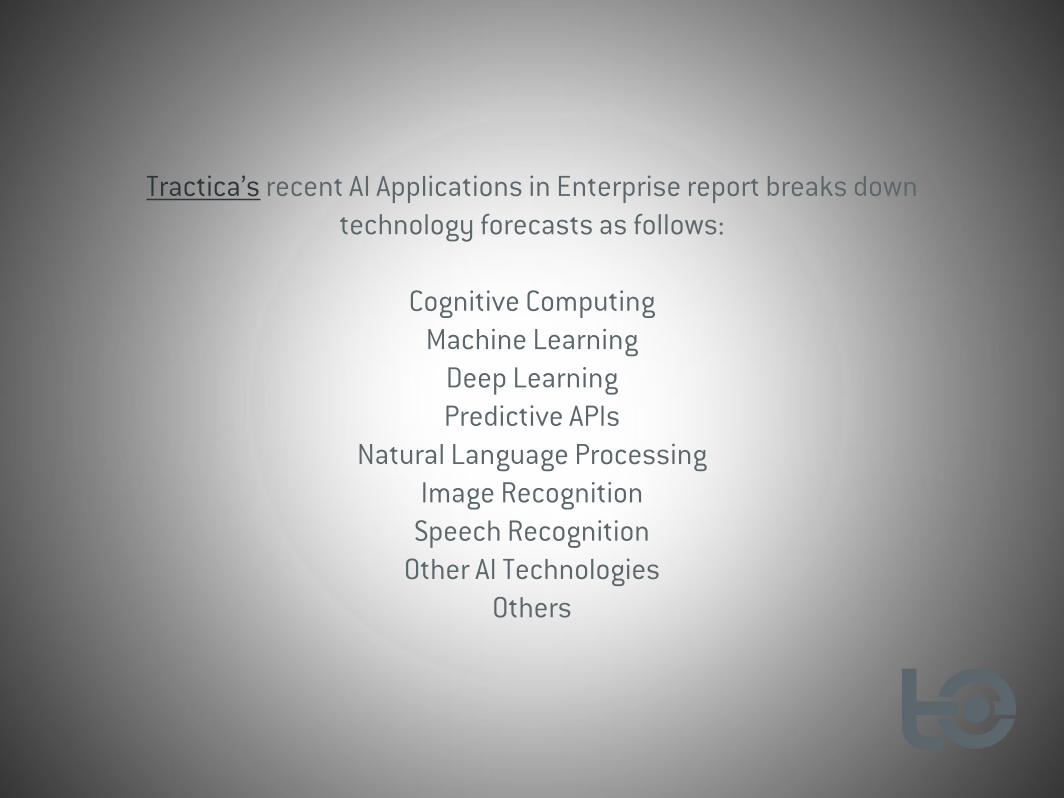

Tractica’s recent AI Applications in Enterprise report breaks down technology forecasts as follows:

Cognitive ComputingMachine Learning

Deep LearningPredictive APIs

Natural Language ProcessingImage Recognition

Speech RecognitionOther AI Technologies

Others

Takeaways on Artificial Intelligence Market Segmentation

The amount of reliable information about the AI market is less than ideal, and far less quantified than more mature and established markets. Regardless, there is still insight to be gained, and below are outlined some of the most important takeaways from an assessment of previous efforts to segment the AI market.

1 – Healthcare, Marketing, and Finance Consistently Appear as Areas of AI

Focus1

CB Insights claims that healthcare has been the domain of greatest deal flow in AI. Google’s DeepMind is honed in on healthcare, IBM set it’s sights on healthcare years ago (and continues to burrow into that market), and many of the biggest

“broad AI” players like Ayasdi are jumping into the healthcare market.

Healthcare also offers a kind of noble “flavor” that other application areas do not. AI companies who begin by working on Wall Street may be perceived as simply

profit-driven, or possibly helping the wrong party, while a company devoting itself to curing disease or improving treatment (even if for the exact same profit

motive) may be viewed in a different light.

It’s our contention that companies like DeepMind who are interested in moving towards strong AI will have to move forward with “friendly” steps into noble fields

like medicine in order to dispell some of the fear around progress towards machines that may (one day) become more intelligent than humans.

Marketing and finance also represent huge areas of AI focus. Sentient Technologies’ Aware software promises to deliver better conversion rates for eCommerce vendors, and Cortica‘s myriad applications for eCommerce and

marketing will be fleshed out in the coming months and years.

All three of these commonly targeted AI segments – health, marketing and fi-nance – involve a tremendous amount of high-volume information, and all three

segments are nearly infinite in size. I’m of the belief that the convoluted sales cycles and market forces in health care will lead to finance, eCommerce, and

marketing leaping ahead in terms of relative AI adoption and innovation, though only the future will tell. What seems certain is that these three fields will be

among the biggest domains of focus for AI firms, and these application areas are themselves likely to spawn many scientific innovations in AI itself.

22 – Segmenting Markets is Qualitatively Messy, but Might Clear Up in Time

Determining segments is a high-level art and science; it is a creative task that requires a well-informed perspective. A market can hypothetically be “sliced” in

an infinite number of ways (depending on one’s purpose), but accurately boxing applications into specific “verticals” involves a lot of grey area...

Consider the following:

CB Insights does not have “natural language processing” (NLP) listed in their vertical break-down of AI deals, though there are a great many companies working on NLP itself, not just

NLP for eCommerce, but for smart homes, etc...

AI can be an entire business (RocketFuel) or a LOT of what a company does (Yahoo) or some of what a company does (IBM) – how much AI does a company or deal need to be directly

involved in order to get placed in an “AI Industry” category?

CometLabs’ industry breakdown doesn’t mention marketing / finance at all, despite the fact that this is one of the most prevalent application areas of AI today and in the near future

The same company could easily be called “eCommerce” by one analyst, “Marketing” by another, and “both” by yet another, an issue that is terribly difficult to work around with an

increasingly large number of possible segments

This is not to say that any of the completed AI industry landscapes are “wrong” (I happen to like CB Insights’ breakdown as a good general breakdown, and BCC has a nice simple segmentation as well), but that fuzzy edges will always be present

in this kind of work, and that a consensus across research firms is unlikely (indeed, a consensus within any one research firm seems unlikely).

The “grey area” around and within a specific AI segment may make it more valu-able to focus on one industry at a time, firmly identifying the grey areas and the direct applications, without having a thousand points of “fuzzy” overlap between 12 or 20 discrete industries. For example, if one is just analyzing “AI for Business

Intelligence,” one can construct a relatively rigorous set of classifying rules to determine what does and does not get couched under the header of “AI” and “Business Intelligence.” Much of our future work here at TechEmergence will

involve specific industry deep dives of this kind.

33 – No One Knows What Will “Take Off,” and This Influences the

Behavior of the Industry

At a recent VentureBeat conference, Robert Stephens (former founder of Geek Squad) mentioned that the world of AI chat bots is at the phase that the internet was at in 1994. We don’t know were applications will pick up, or take off, and in many fields, use cases are still taking shape as “experiments” and not as direct

and succinct drivers of business value.

Hence, many companies are “feeling out” where to apply these technologies (going from “AI platform” to solving specific business problems). Conveying the value of AI has proven difficult for many vendors. Companies like Sentient Tech-nologies have confusingly broad demo videos (see their explainer video here) that could leave one wondering, “What will this do for my business?” IBM has even been criticized for it’s inability to convey the value of Watson to clients.

This “not knowing what will be a big deal” has – we believe – resulted in a number of observable behaviors and patterns in the AI industry:

Consistently huge bets in the future “Google of AI”, ‘industry standard’ AI platforms (that bat-tlefield is still wide open, and it’s uncertain how it will congeal, or if it will continue to

fragment over time)

Companies with broad application areas beginning to explain their technology in “non-PhD” language, and in terms that programmers and CEOs can understand (a good example here is Ayasdi – their technology is tremendously complex but they explain their value proposition

and use cases in this explainer video and this use case video)

AI vendors and large company executives are both looking to the “cool kids” (hottest new AI companies with tens of millions in funding, and the biggest AI tech firms like Facebook,

Google, Amazon) for determining future trends, and where they should go next. Since many AI vendors and large organizations don’t have “traction” in terms of real ROI, they must look

to where they believe traction to exist.

44 – Specifics Up for Grabs, but Optimism Abounds

Despite the disagreements about specific industry or domain application and adoption, the rumble on the tracks (from all directions) seems to liken AI not to a specific tool for a few specific jobs, but as an entirely different (and in large part

unimaginable) paradigm of work, research, and productivity.

Twenty years ago, Bill Gates locked himself away to contemplate “the internet” and decide how important it would be for Microsoft’s future. Thank goodness he took action. Today, Microsoft’s CEO and Google’s CEO have both expressed their

extreme commitment to bringing AI into the core of their business and their plans for growth. It’s not just Silicon Valley companies on the bandwagon anymore, and we could never have prepared for the exact roll-out of massive changes brought about by the internet. Similarly, it is unlikely that we’ll be able to foresee many

of the most powerful applications of AI in business and personal life – but we can keep our ears to the tracks.

Thanks for viewing our presentation. If you’d like to stay ahead of the curve about cutting-edge research trends and insights in the field of artificial intelligence, be

sure to stay connected on social media by clicking the icons below:

[email protected] | www.techemergence.com

© TechEmergence LLC 2016 All Rights Reserved | Design by J. Daniel Samples