AUSTRALIAN HOTEL

MARKET UPDATE

Trading, Development and Investment

July 2015

2

1. Australian Hotel Markets Snapshot 1

2. Snapshot per Key Australian Market 2

3. Australian Hotel Development Pipeline 12

4. New Zealand Update 13

5. Australian Hotel Sales 14

6. Australian Hotel Yields 15

7. Australian Outlook Until Dec 2015 17

8. CBRE Hotels Services 18

TABLE OF CONTENTS

3

% Change

Adelaide -2.0%

Brisbane +0.1%

Cairns +10.9%

Canberra / ACT +2.0%

Darwin -9.1%

Gold Coast +8.5%

Hobart +3.3%

Melbourne +3.1%

Perth -3.1%

Sydney +4.0%

AUSTRALIAN HOTEL MARKETS SNAPSHOT

Australia +2.9%

Source: STR Global, CBRE Hotels

Page 1

OCC & ADR CHANGE VS LAST YEAR (Year Ending June 2015 vs 2014)

Note: in transition means one indicator (OCC or ADR) is positive and the other negative

REVPAR

Year Ending June 2015

vs 2014

% Change

-4.6%

-5.6%

+10.2%

+6.8%

-12.7%

+8.0%

+5.2%

+3.8%

-2.9%

+6.9%

+3.4%

REVPAR

YTD June 2015

vs 2014

Adelaide

Brisbane

Cairns

Canberra/

ACT

Melbourne

Perth

Sydney

Gold Coast

Darwin

Hobart

-11%

-9%

-7%

-5%

-3%

-1%

1%

3%

5%

7%

9%

11%

-11% -9% -7% -5% -3% -1% 1% 3% 5% 7% 9% 11%

%∆

A

DR vs Last Year

%∆ OCC vs Last Year

GROWTH

DECLINE

IN TRANSITION

IN TRANSITION

While the fundamentals in many of Australia’s traditional property asset classes are benign, the dynamic characteristics of the hospitality market continue to place the hotel sector

under the investment spotlight.

The major Australian markets grew by 4.4% in the last year measured by Rooms Revenue. This trend reinforces the shift in Australia's economic activity away from a reliance on

mining to a services based economy. All markets grew with the exception of Perth and Darwin on this metric; however, their performance was well in advance of the correction

being experienced in other industries. The resort markets of Cairns and Gold Coast continued to grow on fundamentals.

In terms of hotel performance, supply surges in Adelaide, Brisbane and Darwin have affected performance. Hotels in the investment favourite markets of Sydney and Melbourne

continue to be solid performers. Canberra, Brisbane and Darwin are in transition and Adelaide has spent its growth pennies while Hobart continues to make strong deposits.

RevPAR growth

RevPAR decline

4

PERFORMANCE (Year Ending Jun 2015)

Source: STR Global, CBRE Hotels

1Based on visitor nights

Source: TRA, CBRE Hotels VFR: Visiting friends and relatives

Selected Recent Openings (in Last 12 Months)

ibis Adelaide 3.5 311 keys Jul-2014

Quest on King William 4 105 keys Aug-2014

Art Series Watson Hotel 4 84 keys Nov-2014

Mayfair Hotel 4 170 keys Jan-2015

SUPPLY (YE Jun 2015)

Existing Hotels, Motels and Serviced Apartments: 109 (8,226 rooms)

Dominant Source Markets1

1. Victoria

2. New South Wales

3. South Australia

ADELAIDE

ADR

AU$149.27

OCC

77.6%

VS. 2014

-2.0%

41%

37%

15%

7%

Purpose of Visit1

Holiday

Business

VFR

Other

Length of Stay

2.9 days

Visitors (‘000): 1,098.10

Visitor Nights (‘000): 3,139.10

Page 2

Room demand generators for the Adelaide market appear to provide a stable foundation.

Adelaide features several major events annually which provide good yielding opportunities

and that showcase the city to a wider international market. In CBRE Hotels’ view, trading

outcomes over the next 12 months will largely reflect limited growth at or around CPI in

RevPAR terms. However, new room supply entering the Adelaide CBD market in the next two

years has the potential to dilute existing demand amongst greater supply and hence lead to

decreased occupancy and/or discounting of room rates. Alternatively, the additional supply

will provide uplift to room rates (each being a new venue) and attract demand which exists in

the market but is unsatisfied due to occupancy constraints. CBRE Hotels anticipates that not

all the new room supply mooted for this market will come to fruition and whilst those

developments which are completed will ‘stretch’ the market, the overall dip in general market

outcomes will be short-lived.

REVPAR

AU$115.79

77%

23%

Visitor Nights

Domestic International

87%

13%

Visitor Arrivals

DEMAND for Hotels, Motels and Serviced Apartments (YE Dec 2014)

Source: STR Global, CBRE Hotels

Selected Projects Likely to Proceed

Holiday Inn Express Adelaide 4 245 keys Apr-2017

Aloft Adelaide (New Mayfield) 4.5 200 keys Jan-2018

Lester Hotel 4.5 244 keys 2018

Selected Mooted Projects

Sheraton Adelaide 4.5 160 keys May-2019

Sofitel Adelaide 5 252 keys Jun-2019

Source: STR Global, CBRE Hotels

Q3 2014

vs '13

Q4 2014

vs '13

Q1 2015

vs '14

Q2 2015

vs '14

-7%

-5%

-3%

-1%

1%

3%

5%

7%

-7% -5% -3% -1% 1% 3% 5% 7%

%∆

A

DR vs Last Year

%∆ OCC vs Last Year

GROWTH

DECLINE

IN TRANSITION

IN TRANSITION

Note: in transition

means one

indicator (OCC or

ADR) is positive

and the other

negative

OCC & ADR CHANGE VS LAST YEAR Note: OCC tracks horizontally and ADR vertically

RevPAR growth

RevPAR decline

5

PERFORMANCE (Year Ending Jun 2015)

Source: STR Global, CBRE Hotels

2Based on visitor nights

Source: TRA, CBRE Hotels VFR: Visiting friends and relatives

Selected Recent Openings (in Last 12 Months)

NEXT Hotel1&2

4 304 keys Sep-2014

Capri by Fraser 4.5 239 keys Mar-2015

SUPPLY (YE Jun 2015)

Existing Hotels, Motels and Serviced Apartments: 205 (15,636 rooms)

Dominant Source Markets2

1. Queensland

2. New South Wales

3. Victoria

BRISBANE

ADR

AU$185.27

OCC

76.1%

VS. 2014

+0.1% Length of Stay

2.5 days

Page 3

The Brisbane hotel market has seen reduced corporate demand from the mining sector and

Government; however, looking forward CBRE Hotels expects continued growth in demand off

the back of strong growth forecasts for domestic and international visitors. The Brisbane

Council's moratorium on infrastructure charges for hotel development approved prior to June

2015 has seen an influx of supply with a number of projects recently completed, under

construction and approved. Hotel performance for the financial year ending 2015 was

boosted by the G20 in November 2014. STR Global results for the 6 months to June 2015,

however, indicate rooms available increased by 7.8% over the same period in 2014, whilst

rooms sold increased by 4.3%, resulting in a decline of 3.3% in occupancy. Over the same

period, room rate declined by 2.4% with RevPAR reflecting a fall of 5.6%. It is anticipated that

ongoing supply will exceed demand for the medium term resulting in lower occupancy levels

and further decline in RevPAR.

REVPAR

AU$141.07

Source: STR Global, CBRE Hotels 1Rebrand / Refurbishment

2Extension

Selected Properties Under Construction

Rydges RNA Hotel 4 208 keys Jan-2016

Holiday Inn Express 4 226 keys Jun-2016

ibis Brisbane 3.5 368 keys Sep-2016

Selected Projects Likely to Proceed

Emporium Southpoint 5 142 keys Dec-2016

111 Mary Street 5 316 keys Dec-2017

W Brisbane 5 305 keys Apr-2018

42 James Street 5 165 keys Sep-2018

DEMAND for Hotels, Motels and Serviced Apartments (YE Dec 2014)

Visitors (‘000): 2,095.97

Visitor Nights (‘000): 5,253.97

43%

35%

11%

11%

Purpose of Visit2

Business

Holiday

VFR

Other

72%

28%

Visitor Nights

Domestic International

81%

19%

Visitor Arrivals

Source: STR Global, CBRE Hotels

Note: in transition

means one

indicator (OCC or

ADR) is positive

and the other

negative

OCC & ADR CHANGE VS LAST YEAR Note: OCC tracks horizontally and ADR vertically

Q3 2014

vs '13

Q4 2014

vs '13

Q1 2015

vs '14

Q2 2015

vs '14

-13%

-11%

-9%

-7%

-5%

-3%

-1%

1%

3%

5%

7%

9%

11%

13%

-13%-11%-9% -7% -5% -3% -1% 1% 3% 5% 7% 9% 11%13%

%∆

A

DR vs Last Year

%∆ OCC vs Last Year

GROWTH

DECLINE

IN TRANSITION

IN TRANSITION

RevPAR growth

RevPAR decline

6

PERFORMANCE (Year Ending Jun 2015)

Source: STR Global, CBRE Hotels

1Based on visitor nights

Source: TRA, CBRE Hotels VFR: Visiting friends and relatives

Selected Mooted Projects

Aquis Great Barrier Reef Resort

(8 luxury resorts)

5 7,500 keys 2020

SUPPLY (YE Jun 2015)

Existing Hotels, Motels and Serviced Apartments: 93 (7,465 rooms)

Dominant Source Markets1

1. Queensland

2. New South Wales

3. China

CAIRNS

ADR

AU$128.35

OCC

77.0%

VS. 2014

+10.9% Length of Stay

3.5 days

Page 4

Cairns is currently one of the best performers in the market, exceeding market

expectations and recording a strong recovery from a low base. Cairns had the highest

RevPAR growth in Australia for the year ending June 2015 and improved occupancy

levels; however, ADR and RevPAR remain well below other destinations. Cairns is

currently witnessing a strong rebound in international and domestic tourist arrival

numbers as a result of increased air capacity into the region, especially from Asia. There

are a lack of developments in the pipeline but recent transactions including the Pullman

Cairns International and Pacific Hotel Cairns reflect renewed interest in existing

properties and an increase in value levels.

REVPAR

AU$98.77

Source: STR Global, CBRE Hotels

OCC & ADR CHANGE VS LAST YEAR Note: OCC tracks horizontally and ADR vertically

DEMAND for Hotels, Motels and Serviced Apartments (YE Dec 2014)

Visitors (‘000): 943.68

Visitor Nights (‘000): 3,304.71

55% 45%

Visitor Nights

Domestic International

53% 47%

Visitor Arrivals

77%

12%

8% 3%

Purpose of Visit1

Holiday

Business

VFR

Other

Source: STR Global, CBRE Hotels

Note: in transition

means one

indicator (OCC or

ADR) is positive

and the other

negative

Q3 2014

vs '13

Q4 2014

vs '13

Q1 2015

vs '14

Q2 2015

vs '14

-11%

-9%

-7%

-5%

-3%

-1%

1%

3%

5%

7%

9%

11%

-11% -9% -7% -5% -3% -1% 1% 3% 5% 7% 9% 11%

%∆

A

DR vs Last Year

%∆ OCC vs Last Year

GROWTH

DECLINE

IN TRANSITION

IN TRANSITION

RevPAR growth

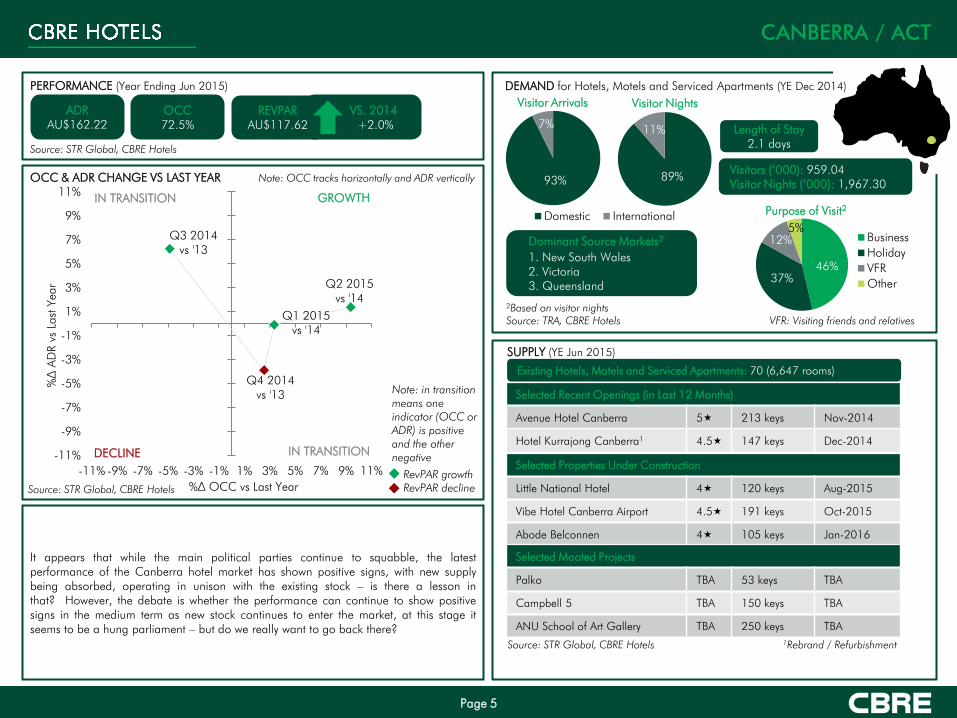

RevPAR decline

7

PERFORMANCE (Year Ending Jun 2015)

Source: STR Global, CBRE Hotels

2Based on visitor nights

Source: TRA, CBRE Hotels VFR: Visiting friends and relatives

Selected Recent Openings (in Last 12 Months)

Avenue Hotel Canberra 5 213 keys Nov-2014

Hotel Kurrajong Canberra1

4.5 147 keys Dec-2014

SUPPLY (YE Jun 2015)

Existing Hotels, Motels and Serviced Apartments: 70 (6,647 rooms)

Dominant Source Markets2

1. New South Wales

2. Victoria

3. Queensland

CANBERRA / ACT

ADR

AU$162.22

OCC

72.5%

VS. 2014

+2.0% Length of Stay

2.1 days

Page 5

It appears that while the main political parties continue to squabble, the latest

performance of the Canberra hotel market has shown positive signs, with new supply

being absorbed, operating in unison with the existing stock – is there a lesson in

that? However, the debate is whether the performance can continue to show positive

signs in the medium term as new stock continues to enter the market, at this stage it

seems to be a hung parliament – but do we really want to go back there?

REVPAR

AU$117.62

Source: STR Global, CBRE Hotels 1Rebrand / Refurbishment

Selected Properties Under Construction

Little National Hotel 4 120 keys Aug-2015

Vibe Hotel Canberra Airport 4.5 191 keys Oct-2015

Abode Belconnen 4 105 keys Jan-2016

Selected Mooted Projects

Palko TBA 53 keys TBA

Campbell 5 TBA 150 keys TBA

ANU School of Art Gallery TBA 250 keys TBA

OCC & ADR CHANGE VS LAST YEAR Note: OCC tracks horizontally and ADR vertically

DEMAND for Hotels, Motels and Serviced Apartments (YE Dec 2014)

Visitors (‘000): 959.04

Visitor Nights (‘000): 1,967.30

46%

37%

12%

5%

Purpose of Visit2

Business

Holiday

VFR

Other

93%

7%

Visitor Arrivals

89%

11%

Visitor Nights

Domestic International

Source: STR Global, CBRE Hotels

Note: in transition

means one

indicator (OCC or

ADR) is positive

and the other

negative

Q3 2014

vs '13

Q4 2014

vs '13

Q1 2015

vs '14

Q2 2015

vs '14

-11%

-9%

-7%

-5%

-3%

-1%

1%

3%

5%

7%

9%

11%

-11% -9% -7% -5% -3% -1% 1% 3% 5% 7% 9% 11%

%∆

A

DR vs Last Year

%∆ OCC vs Last Year

GROWTH

DECLINE

IN TRANSITION

IN TRANSITION

RevPAR growth

RevPAR decline

8

PERFORMANCE (Year Ending Jun 2015)

Source: STR Global, CBRE Hotels

2Based on visitor nights

Source: TRA, CBRE Hotels VFR: Visiting friends and relatives

Selected Recent Openings (in Last 12 Months)

Argus Apartments Darwin 4.5 101 keys Jun-2015

Ramada Suites Zen Quarter1 4 218 keys Jul-2015

SUPPLY (YE Jun 2015)

Existing Hotels, Motels and Serviced Apartments: 41 (4,696 rooms)

Dominant Source Markets2

1. New South Wales

2. Northern Territory

3. Victoria

DARWIN

ADR

AU$184.60

OCC

69.4%

VS. 2014

-9.1% Length of Stay

4.4 days

Page 6

While strong demand levels have produced high occupancies and escalating room rates

due to large projects such as the INPEX Ichthys LNG, the recent contraction in mining

activity has been noticeable. With a number of hotel developments mooted for the

Darwin Tourism Region, coupled with the market coming off a period of unprecedented

growth, CBRE Hotels believe it is more likely hotels will focus on holding occupancies

with pressure on any future rate growth in the short term.

REVPAR

AU$128.15

Source: STR Global, CBRE Hotels 1Rebrand / Refurbishment

2Extension

Selected Properties Under Construction

Rydges Palmerston 4 200 keys Sep-2015

Top End 105 Mitchell Street

4.5 100 keys 2016

Club Tropical Resort Darwin2 4 104 TBA

Selected Projects Likely to Proceed

85 Mitchell Street TBA 200 keys Jan-2017

Casuarina Shell Site TBA 175 keys 2018

Gateway Shopping Centre TBA 195 keys 2019

OCC & ADR CHANGE VS LAST YEAR Note: OCC tracks horizontally and ADR vertically

DEMAND for Hotels, Motels and Serviced Apartments (YE Dec 2014)

Visitors (‘000): 412.89

Visitor Nights (‘000): 1,831.35

40%

40%

6%

14%

Purpose of Visit2

Holiday

Business

VFR

Other

87%

13%

Visitor Arrivals

80%

20%

Visitor Nights

Domestic International

Source: STR Global, CBRE Hotels

Note: in transition

means one

indicator (OCC or

ADR) is positive

and the other

negative

Q3 2014

vs '13

Q4 2014

vs '13

Q1 2015

vs '14

Q2 2015

vs '14

-11%

-9%

-7%

-5%

-3%

-1%

1%

3%

5%

7%

9%

11%

-11% -9% -7% -5% -3% -1% 1% 3% 5% 7% 9% 11%

%∆

A

DR vs Last Year

%∆ OCC vs Last Year

GROWTH

DECLINE

IN TRANSITION

IN TRANSITION

RevPAR growth

RevPAR decline

9

PERFORMANCE (Year Ending Jun 2015)

Source: STR Global, CBRE Hotels

2Based on visitor nights

Source: TRA, CBRE Hotels VFR: Visiting friends and relatives

SUPPLY (YE Jun 2015)

Existing Hotels, Motels and Serviced Apartments: 171 (17,096 rooms)

Dominant Source Markets2

1. Queensland

2. New South Wales

3. Victoria

GOLD COAST

ADR

AU$170.39

OCC

71.9%

VS. 2014

+8.5% Length of Stay

3.6 days

Page 7

After an extended period of minimal growth in supply and demand, due to softer

economic and competitive conditions, the Gold Coast market is seeing a return to form

with the second highest RevPAR growth in the country behind Cairns driven by a recovery

in both domestic and international visitor numbers. This recovery has buoyed investor

confidence, with a number of recent transactions reflecting strong growth in value levels.

The upcoming 2018 Commonwealth Games will see an expansion of infrastructure

including major upgrades to the airport and will spotlight the destination. The Gold

Coast hotel market has enjoyed relatively stable supply over the last five years and going

forward, the supply outlook looks relatively benign. Increased demand from both

domestic and international visitors is expected to result in continual growth in both

occupancy and ADR over the short and medium term.

REVPAR

AU$122.44

OCC & ADR CHANGE VS LAST YEAR Note: OCC tracks horizontally and ADR vertically

DEMAND for Hotels, Motels and Serviced Apartments (YE Dec 2014)

Visitors (‘000): 1,973.00

Visitor Nights (‘000): 7,142.75

Selected Properties Under Construction

Jupiter's Casino Hotel2 5 75 Nov-2017

Jewel Luxury Resort 5 153 Dec-2018

Selected Mooted Projects

Orchid Avenue Short Term

Accommodation Building

TBA 178 2018

Source: STR Global, CBRE Hotels 2Extension

82%

10%

6% 2%

Purpose of Visit2

Holiday

Business

VFR

Other

74%

26%

Visitor Nights

Domestic International

75%

25%

Visitor Arrivals

Source: STR Global, CBRE Hotels

Note: in transition

means one

indicator (OCC or

ADR) is positive

and the other

negative

Q3 2014

vs '13

Q4 2014

vs '13

Q1 2015

vs '14

Q2 2015

vs '14

-7%

-5%

-3%

-1%

1%

3%

5%

7%

-7% -5% -3% -1% 1% 3% 5% 7%

%∆

A

DR vs Last Year

%∆ OCC vs Last Year

GROWTH

DECLINE

IN TRANSITION

IN TRANSITION

RevPAR growth

RevPAR decline

10

PERFORMANCE (Year Ending Jun 2015)

Source: STR Global, CBRE Hotels

1Based on visitor nights

Source: TRA, CBRE Hotels VFR: Visiting friends and relatives

Selected Properties Under Construction

Macquarie Wharf Shed Hotel 4.5 114 keys Dec-2016

Crowne Plaza Hobart 4.5 187 keys Oct-2017

SUPPLY (YE Jun 2015)

Existing Hotels, Motels and Serviced Apartments: 53 (2,807 rooms)

Dominant Source Markets1

1. Victoria

2. New South Wales

3. Tasmania

HOBART

ADR

AU$160.60

OCC

79.3%

VS. 2014

+3.3% Length of Stay

2.8 days

Page 8

’Steady as she goes’ is probably an apt term for the Hobart market outlook in the short term.

Demand generators key to this market should continue to provide seasonal yet consistent

opportunities in the market. There are several potential hotel developments that may be

completed in the medium term which should be absorbed into the market without any great

effect on overall market outcomes. The Government’s commitment to increase funding for

tourism marketing is anticipated to underpin visitation growth from both mainland Australia

and inbound internationals. Room supply over the long term must be tinged with economic

reality. New rooms mooted in the medium term represent an increase of around 50% on

current stock levels; in CBRE Hotels’ view the market would struggle to absorb this supply

volume despite visitation growth expectations. Inevitably, market forces should prevail

meaning that not all mooted developments will proceed.

REVPAR

AU$127.29

Source: STR Global, CBRE Hotels

Selected Mooted Projects

Macquarie Street Hotel

4 296 keys Aug-2016

HOMO at MONA 4 90 keys May-2017

Former Roberts Building 4 80 keys Aug-2017

OCC & ADR CHANGE VS LAST YEAR Note: OCC tracks horizontally and ADR vertically

DEMAND for Hotels, Motels and Serviced Apartments (YE Dec 2014)

Visitors (‘000): 630.12

Visitor Nights (‘000): 1,751.58

70%

17%

12% 1%

Purpose of Visit1

Holiday

Business

VFR

Other

83%

17%

Visitor Nights

Domestic International

87%

13%

Visitor Arrivals

Source: STR Global, CBRE Hotels

Note: in transition

means one

indicator (OCC or

ADR) is positive

and the other

negative

Q3 2014

vs '13

Q4 2014

vs '13

Q1 2015

vs '14

Q2 2015

vs '14

-11%

-9%

-7%

-5%

-3%

-1%

1%

3%

5%

7%

9%

11%

-11% -9% -7% -5% -3% -1% 1% 3% 5% 7% 9% 11%

%∆

A

DR vs Last Year

%∆ OCC vs Last Year

GROWTH

DECLINE

IN TRANSITION

IN TRANSITION

RevPAR growth

RevPAR decline

11

PERFORMANCE (Year Ending Jun 2015)

Source: STR Global, CBRE Hotels

1Based on visitor nights

Source: TRA, CBRE Hotels VFR: Visiting friends and relatives

Selected Recent Openings (in Last 12 Months)

Wyndham Hotel 4 86 keys Dec-2014

BreakFree on Collins1

4 193 keys Jun-2015

SUPPLY (YE Jun 2015)

Existing Hotels, Motels and Serviced Apartments: 366 (32,032 rooms)

Dominant Source Markets1

1. New South Wales

2. Victoria

3. Queensland

MELBOURNE

ADR

AU$186.67

OCC

81.7%

VS. 2014

+3.1% Length of Stay

2.9 days

Page 9

The short term outlook for Melbourne is for continued room demand growth. However,

given the high levels of occupancy currently experienced, this growth is expected to be

somewhat constrained over the next two years due to a lack of additional rooms. As a

consequence, the new supply which will enter the market between 2017 and 2019 is

expected to have only a small negative impact on occupancy. ADR growth is anticipated

to remain subdued largely as a consequence of a cost conscious corporate sector;

average annual growth is expected to increase at or around CPI levels.

REVPAR

AU$152.54

Source: STR Global, CBRE Hotels 1Rebrand / Refurbishment

Selected Properties Under Construction

QT Hotel Melbourne 4 188 keys May-2016

Peppers Docklands 4.5 87 keys Dec-2016

Selected Projects Likely to Proceed

Parkroyal Docklands 5 281 keys Jul-2017

Four Points Docklands 4 320 keys Jan-2017

Aloft Melbourne 4.5 312 keys Aug-2017

80 Collins Street 5 250 keys Sep-2018

Crown Resorts Hotel 4.5 408 keys Jun-2019

OCC & ADR CHANGE VS LAST YEAR Note: OCC tracks horizontally and ADR vertically

DEMAND for Hotels, Motels and Serviced Apartments (YE Dec 2014)

Visitors (‘000): 4,997.70

Visitor Nights (‘000): 14,557.96

47%

36%

10%

7%

Purpose of Visit1

Holiday

Business

VFR

Other

80%

20%

Visitor Arrivals

67%

33%

Visitor Nights

Domestic International

Source: STR Global, CBRE Hotels

Note: in transition

means one

indicator (OCC or

ADR) is positive

and the other

negative

Q3 2014

vs '13

Q4 2014

vs '13

Q1 2015

vs '14

Q2 2015

vs '14

-9%

-7%

-5%

-3%

-1%

1%

3%

5%

7%

9%

-9% -7% -5% -3% -1% 1% 3% 5% 7% 9%

%∆

A

DR vs Last Year

%∆ OCC vs Last Year

GROWTH

DECLINE

IN TRANSITION

IN TRANSITION

RevPAR growth

RevPAR decline

12

PERFORMANCE (Year Ending Jun 2015)

Source: STR Global, CBRE Hotels

1Based on visitor nights

Source: TRA, CBRE Hotels VFR: Visiting friends and relatives

Selected Recent Openings (in Last 12 Months)

Alex Hotel 4 74 keys May-2015

SUPPLY (YE Jun 2015)

Existing Hotels, Motels and Serviced Apartments: 101 (10,367 rooms)

Dominant Source Markets1

1. Western Australia

2. New South Wales

3. Victoria

PERTH

ADR

AU$198.99

OCC

82.5%

VS. 2014

-3.1% Length of Stay

3.5 days

Page 10

Despite the slowdown in respect of the mining and resource sectors of the economy,

demand has remained strong with airlines, hotels, wholesalers etc. now actively targeting

the leisure, groups and events segments with a reduction in ADR being used as a

demand generator. CBRE Hotels has identified there is the potential to add some

5,000+ new rooms over the next three years; however, CBRE Hotels are of the view that

economic reality will ensure a more rational development schedule with the likely supply

equating to some 2,500+ new rooms. Whilst there are a number of new hotels coming

on line, these venues will spend significant expense in respect of marketing, which CBRE

Hotels feel can limit forecast declines in occupancy and ADR. The opening of the new

Perth Stadium in early 2018, coupled with a planned substantial WA Tourism campaign

should also assist to induce demand levels.

REVPAR

AU$164.25

Source: STR Global, CBRE Hotels

Selected Properties Under Construction

Como The Treasury 5 48 keys Sep-2015

Crown Towers Burswood 5 522 keys Dec-2016

Sage Hotel 4 101 keys Mar-2016

Westin Hotel 5 362 keys Jan-2017

DoubleTree Perth 4 205 keys Jan-2017

Selected Projects Likely to Proceed

DoubleTree Perth Waterfront 4 247 keys Jun-2016

AVANI Hotel Perth City Link 4.5 250 keys Oct-2017

Ritz Carlton Perth 5 204 keys Jan-2018

OCC & ADR CHANGE VS LAST YEAR Note: OCC tracks horizontally and ADR vertically

DEMAND for Hotels, Motels and Serviced Apartments (YE Dec 2014)

Visitors (‘000): 1,180.30

Visitor Nights (‘000): 4,156.42

43%

37%

12%

8%

Purpose of Visit1

Business

Holiday

VFR

Other

78%

22%

Visitor Arrivals

62% 38%

Visitor Nights

Domestic International

Source: STR Global, CBRE Hotels

Note: in transition

means one

indicator (OCC or

ADR) is positive

and the other

negative

Q3 2014

vs '13

Q4 2014

vs '13

Q1 2015

vs '14

Q2 2015

vs '14

-6%

-4%

-2%

0%

2%

4%

6%

-6% -4% -2% 0% 2% 4% 6%

%∆

A

DR vs Last Year

%∆ OCC vs Last Year

GROWTH

DECLINE

IN TRANSITION

IN TRANSITION

RevPAR growth

RevPAR decline

13

PERFORMANCE (Year Ending Jun 2015)

Source: STR Global, CBRE Hotels

2Based on visitor nights

Source: TRA, CBRE Hotels VFR: Visiting friends and relatives

Selected Recent Openings (in Last 12 Months)

The Langham1

5 96 keys Dec-2014

SUPPLY (YE Jun 2015)

Existing Hotels, Motels and Serviced Apartments: 353 (38,048 rooms)

Dominant Source Markets2

1. New South Wales

2. Victoria

3. Queensland

SYDNEY

ADR

AU$204.16

OCC

84.5%

VS. 2014

+4.0% Length of Stay

3.0 days

Page 11

The Sydney market is continuing to show signs of strong growth with both occupancies

and ADR now at record levels. With minimal new supply, occupancies are likely to

remain high with room rate growth at inflationary levels at least. CBRE Hotels

understand that a number of the existing hotels are planning refurbishment programs

over the next few years, which will have a direct impact on the market during constrained

periods. The refurbished products will re-enter the market with expectations of achieving

high ADR levels, which should also flow through the market.

REVPAR

AU$172.56

Selected Properties Under Construction

Greenland Primus Hotel 5 173 keys 2016

Four Points by Sheraton2 4 222 keys 2016

The Tank Stream St Giles 4 282 keys 2016

Sofitel Sydney – ICC 5 616 keys 2017

Selected Projects Likely to Proceed

Crown Sydney – Barangaroo 5 350 keys 2019

OCC & ADR CHANGE VS LAST YEAR Note: OCC tracks horizontally and ADR vertically

DEMAND for Hotels, Motels and Serviced Apartments (YE Dec 2014)

Visitors (‘000): 5,442.63

Visitor Nights (‘000): 16,470.14

Source: STR Global, CBRE Hotels 1Rebrand / Refurbishment

2Extension

Selected Properties Exiting Market

The Menzies Hotel 4 -446 keys 2016

Mercure Potts Point 4 -227 keys 2016

47%

36%

9%

8%

Purpose of Visit2

Holiday

Business

VFR

Other

55%

45%

Visitor Nights

Domestic International

71%

29%

Visitor Arrivals

Source: STR Global, CBRE Hotels

Note: in transition

means one

indicator (OCC or

ADR) is positive

and the other

negative

Q3 2014

vs '13

Q4 2014

vs '13

Q1 2015

vs '14

Q2 2015

vs '14

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

-8% -6% -4% -2% 0% 2% 4% 6% 8%

%∆

A

DR vs Last Year

%∆ OCC vs Last Year

GROWTH

DECLINE

IN TRANSITION

IN TRANSITION

RevPAR growth

RevPAR decline

14

AUSTRALIAN HOTEL DEVELOPMENT PIPELINE

Source: STR Global, CBRE Hotels

It is interesting to note that there are approximately 2,500 rooms proposed for each of the City Markets, however, the overall net increase of stock varies significantly.

The limited availability of sites within Sydney, coupled with the removal of existing stock is expected to have minimal effects on demand, whereas the other major cities

could potentially see a surge in supply that will test the strength of demand in these cities. Whilst the local Governments in each of the cities have been actively

encouraging the development of new hotels, the owners of these products will be relying on the tourism markets of their respective states and Tourism Australia to help

facilitate demand to ensure the viability of the venues.

Page 12

Key Australian Markets

City Markets Greater City Regions Markets

(including City and Surrounds)

1Net percentage increase on existing supply in respective markets

Note: 'Likely to Proceed' are based on CBRE's estimates of developments more than 50% likely of occurring (not including rebrands) and opening

before Jan 2019. City was selected for Brisbane, Melbourne, Perth and Sydney due to their size.

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Adelaide Cairns Canberra /

ACT

Darwin Gold

Coast

Hobart

Num

ber of Room

s

Under Construction Likely to Proceed To Be Removed

-1,000

-500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Brisbane

City

Melbourne

City

Perth

City

Sydney

City

Num

ber of Room

s

Under Construction Likely to Proceed To Be Removed

+23.5%1

+14.8%1

+33.1%1

+6.6%1

+8.4%1

+0.0%1

+6.3%1

+17.3%1

+1.3%1

+10.7%1

15

NEW ZEALAND UPDATE

Double-digit RevPAR growth in all key New Zealand

markets (except for Christchurch)

Page 13

The positive news stories emanating from the wider New Zealand economy

and the property market in particular also ring true for the hotel market with

all key performance indicators showing strong growth through 2014 and the

first half of 2015.

Nationwide occupancy levels continued their strong upward trend finishing at

77.5% year to date June 2015 and at 76.1% year ending June 2015. This is

at par with the previous peak of 76% achieved in the 12 months to October

2004.

ADR levels have shown overall growth of 6.6% to the year ending June 2015

compared to 2014, reaching NZ$148.67. This is a new record that is nearly

equivalent to the peak in 2012 associated to the Rugby World Cup.

The combination of strong occupancy and ADR growth have resulted in a

12.4% RevPAR increase for the year ending June 2015. At NZ$113.20,

RevPAR has eclipsed the level achieved during the Rugby World Cup and

further growth is expected through the remaining months of 2015.

% Change

Auckland +11.6%

Christchurch +9.1%

Queenstown +13.5%

Wellington +12.5%

New Zealand +12.4%

REVPAR

Year Ending June 2015 vs 2014

% Change

+12.4%

N/A

+16.8%

+15.2%

+14.4%

REVPAR

YTD June 2015 vs 2014

Source: STR Global, CBRE Hotels

OCC & ADR CHANGE VS LAST YEAR (Year Ending June 2015 vs 2014)

Note: in transition means one indicator (OCC or ADR) is positive and the other negative

Auckland

Wellington

Christchurch

Queenstown

-11%

-9%

-7%

-5%

-3%

-1%

1%

3%

5%

7%

9%

11%

-11% -9% -7% -5% -3% -1% 1% 3% 5% 7% 9% 11%

%∆

A

DR vs Last Year

%∆ OCC vs Last Year

GROWTH

DECLINE

IN TRANSITION

IN TRANSITION

RevPAR growth

RevPAR decline

16

AUSTRALIAN HOTEL SALES

Sales volumes for hotel investment in Australia in 2014 reached AU$2 billion, the highest level ever recorded.

Year to date performance has been particularly strong, already surpassing over AU$1 billion in sales, however, might not reach 2014 levels predominately due

to the limited availability of stock.

The surge in investment activity has been particularly focused on quality hotels, with those based in Sydney being highly sought. With major transactions

including the Shangri-La in 2012, the Four Seasons in 2013, the Sheraton on the Park in 2014 and The Westin Sydney in 2015.

Page 14

0

10

20

30

40

50

60

0

500

1,000

1,500

2,000

2,500

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

YTD

Jun 20

15

Num

ber of H

ote

l Sale

s

Tota

l H

ote

l Sale

s (A

U$

m

illion)

Total Hotel Sales vs Number of Hotels Sold

Total Hotel Sales Total Number of Hotels Sold

Source: CBRE Hotels

17

AUSTRALIAN HOTEL YIELDS

There has been a notable tightening in the yield profile in the year to date performance, with a significant number of large transactions being completed with initial

yields below 6.50%. Traditionally, yields below 6.00% were for underperforming properties with significant upside or for trophy assets such as the Park Hyatt Sydney,

which is reflected in the previous low point in 2007.

The surge of capital emanating from the Asian countries seeking a safe haven in Australia is unprecedented. Asian buyers who understand and respect hotel assets as

an alternate asset class, typically having a long term investment decision, are also prepared to accept lower returns in the short term.

CBRE Hotels note that the yield compression is not only evident in major core destinations such as Sydney but has also been prevalent in places such as the Gold Coast

and Cairns.

Page 15

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

YTD

Jun 20

15

Initial Yield to Stabilised Yield Gap

Initial Yield Stabilised Yield

Source: CBRE Hotels

18

Initial Yields YTD 2015 (Notable Sales)

Surfers Paradise Marriott

Resort & Spa

Yield: ~6.0%

Hilton Sydney

Yield: 6.3%

Westend Hotel Sydney

Yield: 6.8%

Bounce Hotel Sydney

Yield: 7.8%

Quest Dubbo

Yield: 8.7%

Rendezvous Hotel Brisbane

on George

Yield: 6.3%

Hilton Surfers Paradise

Hotel

Yield: ~6.0%

The Westin Sydney

Yield: 4.2%

Crowne Plaza Surfers

Paradise

Yield: 5.5%

Pullman Cairns

International

Yield: 7.0%

AUSTRALIAN HOTEL YIELDS

The yield profile in a number of year to date transaction highlights investor appetite for assets located in both corporate and leisure destinations. The sale of the prime

Sydney assets are a reflection of investors wanting to acquire hotels located in a major global destination which has a strong market outlook. The yield profile for the

transactions in leisure based destinations, such as the Gold Coast and Cairns, indicate purchasers are expecting continued room rate growth in the short to medium term.

Page 16

Source: CBRE Hotels

4% 5% 6% 7% 8% 9%

19

The Australian hotel market

continues to perform

strongly with occupancies

maintaining an upward

trend, aided by the weaker

Australian dollar. Arrivals

from China are increasing

but the traditional inbound

markets remain New

Zealand, the United

Kingdom and the United

States, while domestic

demand remains dominant.

The operating environment

in major city markets in

recent years has been

characterised by ‘full house’

occupancies exceeding

80%, strong ADR growth

and limited new supply.

AUSTRALIAN OUTLOOK UNTIL DEC 2015

Page 17

Underpinning this position of strength has been Australia’s economic growth that has averaged

almost 3% per annum for the last seven years. As the Australian economy transitions from

mining investment to export production and the Australian dollar falls to levels that support the

balance of trade position and tourist visitations, market fundamentals are positioned to support

solid longer term performance well into the future.

Investors continued to display a robust appetite for hotel properties in

Australia with strong sales setting record yields and price points.

The shortage of saleable good quality

and well located assets continues to boost

pricing. Buyers from Asia were very active

over the course of 2014 and YTD 2015,

accounting for virtually all deals for assets

priced over AU$50 million. Domestic

buyers – primarily high net worth

individuals – are generally focusing on

assets below AU$40 million as they feel

competition at the upper end of the

market is too strong at present. Recent

major transactions include the AU$445

million acquisition of the five-star Westin

Hotel in Sydney. The deal set a new

record for a price per room of a hotel

with over 300 rooms in Australia.

The outlook for the remainder of 2015 is

positive with strong trading conditions in

the short to medium term and a large

volume of capital chasing deals,

particularly in the key Sydney and

Melbourne markets.

20

CBRE HOTELS SERVICES

Page 18

For more information,

please contact:

CBRE HOTELS

AUSTRALIA

KEN SMITH

Regional Director, Pacific

O: +61 2 9333 3422

M: +61 413 025 442

Level 21, 363 George Street

Sydney NSW 2000

www.cbrehotels.com

Please click on any of the above icons for more information on CBRE Hotels services.

THROUGHOUT THIS PUBLICATION SOURCE: STR GLOBAL, LTD. REPUBLICATION OR OTHER RE-USE OF

THIS DATA WITHOUT THE EXPRESS WRITTEN PERMISSION OF STR GLOBAL IS STRICTLY PROHIBITED.