AXA EquitableProtection Report – December 2007 - 1

AXA EQUITABLE PROTECTION REPORTLife Insurance needs and realities

Results for USA (with international comparison)

AXA Equitable Protection Report –December 2007 - 2

Table of content

Introduction to the AXA Equitable Protection Report

Methodology

Analysis

Life stage explanation

Part 1: Sample description

Part 2.A: Attitudes towards Life risks

Part 2.B: Behaviors and habits against Life risks

Part 3: Product ownership and habits

Part 4: Theoretical insurance gap

Part 5: Conclusions

Appendices

AXA Equitable Protection Report –December 2007 - 3

Introduction to the AXA Equitable Protection Report An international survey of Life Insurance needs and realities

Life Insurance habits vary in function of population segments and countries.

Which are attitudes towards life risks? What are the usages and habits? How properly are people insured against what they call “life

risks”? How are particular segments not insured?

The AXA Equitable Protection Report analyses these phenomena and tries to bring insights into a subject which might be of crucial importance for large parts of population

AXA Equitable Protection Report –December 2007 - 4

Methodology

People aged 25-65, working and not working (students being excluded)For Non-working, additional question to know if there is at least one income earner in the household (QI: Do you have an income in your household). If not the respondent was excluded.

Sample is national representative in terms of gender, age, occupation status and region.

Next to the USA, 10 countries were involved: Australia, Belgium, France, Germany, Hong-Kong, Italy, Japan, Spain, Switzerland, and the UK. Interviews are comparable.

Fieldwork: Computer Assisted Telephone Interviews (CATI) methodology.

Fieldwork dates: from the 28th March to the 24th of May 2007.

In this survey we introduced the notion of “life risks”, under which we mean: serious illness, disability, death, long-term unemployment, serious car accidents, etc…

By Life insurance we mean an insurance that pays a lump sum or periodic payments as from an agreed age and/or a lump sum or periodic payments to specified beneficiaries when you die = term-life insurance.

AXA Equitable Protection Report –December 2007 - 5

Analysis

Brackets evaluation: all amount or percentage will be presented on a range of brackets; in order to determine the values of the bracket we apply the following rules:

for the smallest bracket we took 0.75 of the bracket value (e.g. “Less than 25,000” bracket was evaluated at 18,750)

for the highest bracket we took 1.5 of the bracket value (e.g. “More than 1,000,000” was evaluated at 1,500,000)

for all other brackets we took the average (e.g. “From 25,000 to 50,000” was evaluated at 37,500)

Minimum bases: base between 30 and 59 will have to be analysed with caution, we will

present it as follows (n= 35*). base under 29 will not be analysed because of too low base, and we will

present it as follows (n= 25**).

Significances are calculated with a 10% risk level.

AXA Equitable Protection Report –December 2007 - 6

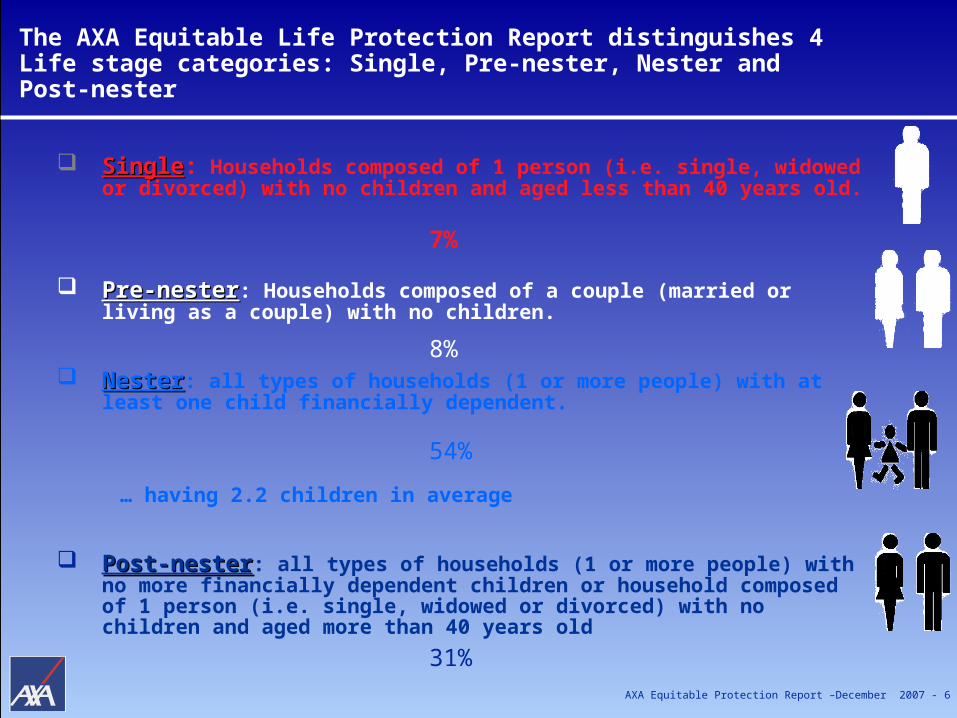

The AXA Equitable Life Protection Report distinguishes 4 Life stage categories: Single, Pre-nester, Nester and Post-nester

SingleSingle: Households composed of 1 person (i.e. single, widowed or divorced) with no children and aged less than 40 years old.

Pre-nesterPre-nester: Households composed of a couple (married or living as a couple) with no children.

NesterNester: all types of households (1 or more people) with at least one child financially dependent.

… having 2.2 children in average

Post-nesterPost-nester: all types of households (1 or more people) with no more financially dependent children or household composed of 1 person (i.e. single, widowed or divorced) with no children and aged more than 40 years old

7%

8%

54%

31%

AXA Equitable Protection Report –December 2007 - 7

Part 1: Sample description: national representation of population aged 25-65

AXA Equitable Protection Report –December 2007 - 8

Male

48%

Female

52%

21%

27%

27%

25%

21%

27%

27%

24%

55-65 years old

45-54 years old

35-44 years old

25-34 years old

Male Female

Gender and Age

QA: Are you….?QB: We are looking to research people within a specific age range, so could you please give me your age?

Average 44.1 y.o. 44.2 y.o.

Base n=172 n=188

Gender

Age

Base : n= 360

AXA Equitable Protection Report –December 2007 - 9

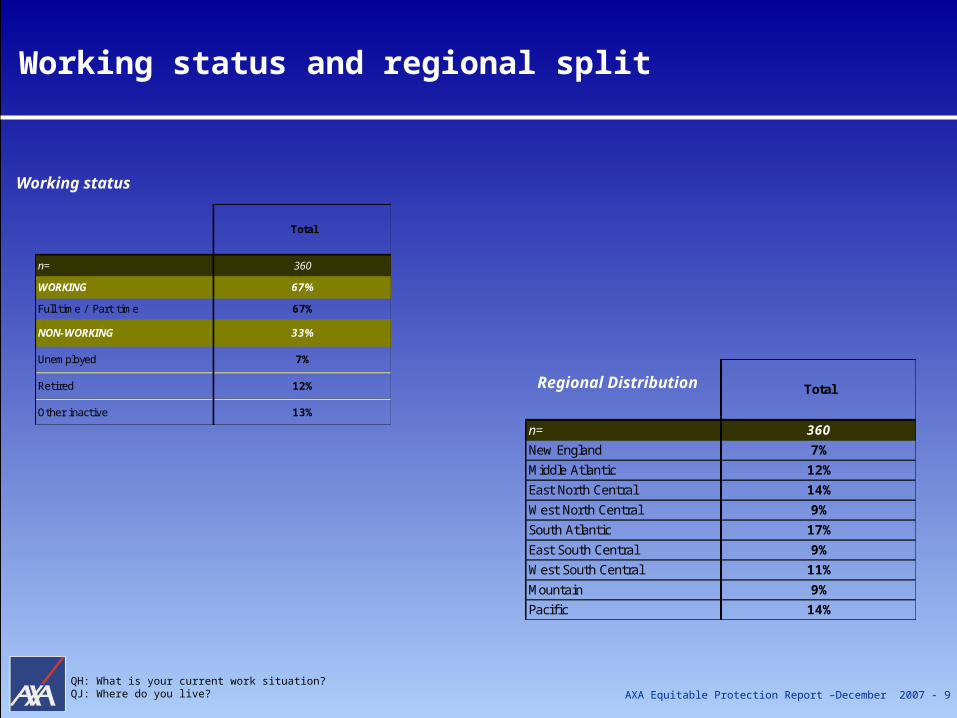

Total

n= 360

New England 7%

Middle Atlantic 12%

East North Central 14%

West North Central 9%

South Atlantic 17%

East South Central 9%

West South Central 11%

Mountain 9%

Pacific 14%

Working status and regional split

QH: What is your current work situation?QJ: Where do you live?

Working status

Regional Distribution

Total

n= 360

WORKING 67%

Full time / Part time 67%

NON-WORKING 33%

Unemployed 7%

Retired 12%

Other inactive 13%

AXA Equitable Protection Report –December 2007 - 10

Part 2: Attitudes & Behaviors

2.A Attitudes towards Life risks

AXA Equitable Protection Report –December 2007 - 11

What do you care about …?For U.S. adults 25 to 65 years old, their health is the most important of the things asked about, but their own financial situation is also very important – especially being prepared for their retirement, saving money and home ownership.

Base : n= 360 * Specific item for France

Top 2 marks 10 & 9

Mid 3 marks 8 & 7 & 6

Bot 5marks 1->5

Mean

9.3 8.4 8.1 8.1 7.5 5.18.7

Q1: I am now going to read you some statements. Using a scale from 1 to 10 where 10 means that this statement is “very important to you” and 1 means that this statement is “not at all important to you”. Please use the scores in-between in order to grade your opinion. Could you please tell me how important you consider…?

8.6

4%9% 10%

15%20% 17%

21%

66%

16%

23%29% 18%

13%

32%

38%

23%

80%

68%61%

67% 67%

51%

41%

11%

Health Financial situationof your retirement

Saving money Home ownership Ensuring one'schildren's future

Reduce financialburden

Career Indulging yourself

AXA Equitable Protection Report –December 2007 - 12

What do you care about …?Among those who have financially dependent children (Nesters), a very high level of importance is placed on ensuring their children’s future – nearly as important as their own health.

Significantly superior to Total Significantly inferior to Total

Q1: I am now going to read you some statements. Using a scale from 1 to 10 where 10 means that this statement is “very important to you” and 1 means that this statement is “not at all important to you”. Please use the scores in-between in order to grade your opinion. Could you please tell me how important you consider…?

Total Male Female SinglePre-

nesterNester

Nester male

Nester female

Post-nester

Feeling very well insured

Feeling somewhat

insured

Feeling not well

insuredn= 360 172 188 27** 29** 193 95 98 112 156 146 58*

Health 9.3 9.0 9.5 9.4 9.1 9.6 9.2 9.3 9.3 9.2

Financial situation of your retirement

8.7 8.5 8.9 8.6 8.5 8.6 9.1 8.7 8.8 8.5

Saving money 8.6 8.3 8.9 8.7 8.5 9.0 8.6 8.6 8.5 8.5

Home ownership 8.4 8.3 8.6 8.8 8.5 9.2 7.9 8.3 8.4 8.7

Reduce financial burden 8.1 7.9 8.3 8.3 8.3 8.2 7.8 7.9 8.3 8.4

Ensuring one's children's future

8.1 7.9 8.3 9.2 9.0 9.4 6.7 7.7 8.2 9.0

Career 7.5 7.6 7.4 7.8 7.8 7.7 6.8 7.3 7.5 7.8

Indulging yourself 5.1 5.1 5.2 4.7 4.4 5.0 5.7 5.2 5.1 4.9

While those who do not feel they are well insured differ little from others in the importance placed on most of the aspects of their lives, they place much more importance on ensuring their children’s future than do others.

AXA Equitable Protection Report –December 2007 - 13

What do you care about …?

Overall, their own health is most important to all, although other

aspects of their lives are also important and differ by life stage.

Those with financially dependent children place a high level of

importance on ensuring their children’s future.

Home ownership and saving money also rank high on most

people’s priority lists.

In contrast, self-indulgence has much lower importance across all

life-stages.

AXA Equitable Protection Report –December 2007 - 14

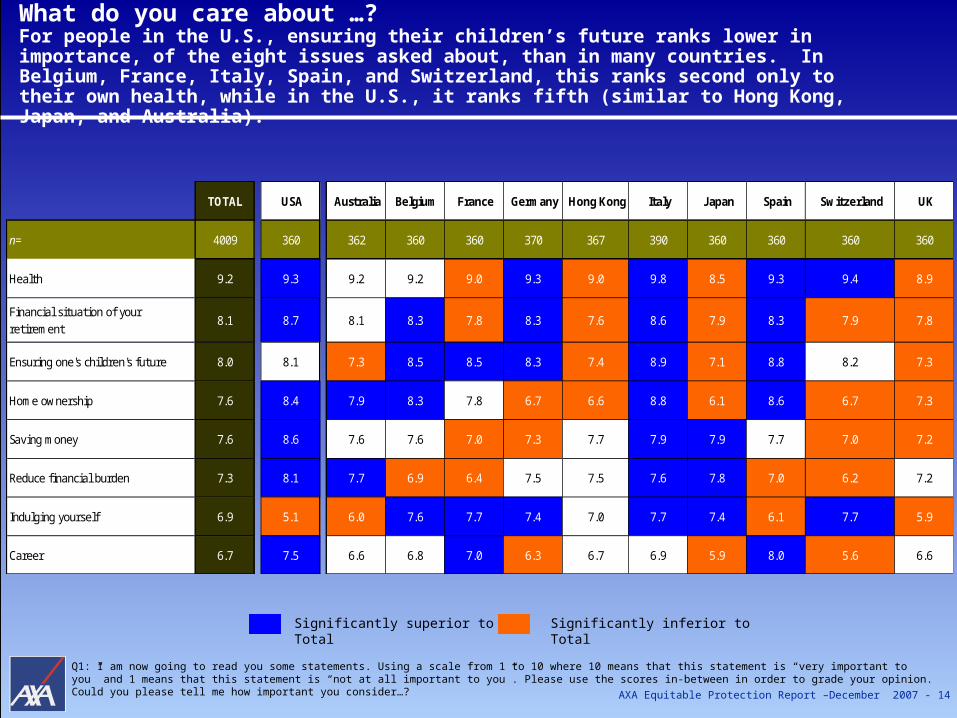

What do you care about …? For people in the U.S., ensuring their children’s future ranks lower in importance, of the eight issues asked about, than in many countries. In Belgium, France, Italy, Spain, and Switzerland, this ranks second only to their own health, while in the U.S., it ranks fifth (similar to Hong Kong, Japan, and Australia).

Q1: I am now going to read you some statements. Using a scale from 1 to 10 where 10 means that this statement is “very important to you” and 1 means that this statement is “not at all important to you”. Please use the scores in-between in order to grade your opinion. Could you please tell me how important you consider…?

TOTAL USA Australia Belgium France Germany Hong Kong Italy Japan Spain Switzerland UK

n= 4009 360 362 360 360 370 367 390 360 360 360 360

Health 9.2 9.3 9.2 9.2 9.0 9.3 9.0 9.8 8.5 9.3 9.4 8.9

Financial situation of your retirement

8.1 8.7 8.1 8.3 7.8 8.3 7.6 8.6 7.9 8.3 7.9 7.8

Ensuring one's children's future 8.0 8.1 7.3 8.5 8.5 8.3 7.4 8.9 7.1 8.8 8.2 7.3

Home ownership 7.6 8.4 7.9 8.3 7.8 6.7 6.6 8.8 6.1 8.6 6.7 7.3

Saving money 7.6 8.6 7.6 7.6 7.0 7.3 7.7 7.9 7.9 7.7 7.0 7.2

Reduce financial burden 7.3 8.1 7.7 6.9 6.4 7.5 7.5 7.6 7.8 7.0 6.2 7.2

Indulging yourself 6.9 5.1 6.0 7.6 7.7 7.4 7.0 7.7 7.4 6.1 7.7 5.9

Career 6.7 7.5 6.6 6.8 7.0 6.3 6.7 6.9 5.9 8.0 5.6 6.6

Significantly superior to Total Significantly inferior to Total

AXA Equitable Protection Report –December 2007 - 15

Which life accidents might happen to them…?Serious illness is seen as the most likely of the negative events asked about, followed by car accidents, with Americans rating their likelihood 5.3 and 4.9 on a 10-point scale. Serious financial problems are judged the third most likely (4.1), nearly identical to the likelihood of natural disasters (4.0), crime (3.8) and unemployment (3.8).

Base : n= 360

Top 2 marks 10 & 9

Mid 3 marks 8 & 7 & 6

Bot 5marks 1->5

Mean

5.3 4.14.9 4.0 3.83.8 3.4 3.33.4 2.2

Q58: Here is a list of risks that could happen to you in life. For each of these, please tell me to what extent you think these risks might happen to you personally, using a scale from 1 to 10 where 10 means that it “certainly will happen to you” and 1 means that it will “certainly not happen to you at all”. Please use the scores in-between to grade your opinion.

63%72%

79% 79%75%

82% 86% 83%89%

96%

26%

22%15% 17%

16%

14%10% 12%

8%2%

11%6% 6% 4%

9%4% 4% 5% 3% 2%

Serious illness Serious car

accident

Serious

financial

problems

Natural

disaster / env.

risks

Crime /

aggression

Unemployment Domestic or

sports

accidents

Work accidents Terrorism Plane crash

AXA Equitable Protection Report –December 2007 - 16

Which life accidents might happen to them…?Those who feel they are not well insured believe that serious financial problems and unemployment could happen to them - higher than do those who feel better insured.

Significantly superior to Total Significantly inferior to Total

Q58: Here is a list of risks that could happen to you in life. For each of these, please tell me to what extent you think these risks might happen to you personally, using a scale from 1 to 10 where 10 means that it “certainly will happen to you” and 1 means that it will “certainly not happen to you at all”. Please use the scores in-between to grade your opinion.

Total Male Female SinglePre-

nesterNester

Nester male

Nester female

Post-nester

Feeling very well insured

Feeling somewhat

insured

Feeling not well

insured

n= 360 172 188 27** 29** 193 95 98 112 156 146 58*

Serious illness 5.3 4.9 5.6 5.0 4.6 5.3 5.9 5.2 5.4 5.3

Serious car accident 4.9 4.8 4.9 4.9 4.8 5.0 4.7 4.7 5.0 5.0

Serious financial problems 4.1 3.8 4.4 4.0 3.8 4.2 4.1 3.2 4.5 5.4

Natural disaster / env. risks 4.0 3.7 4.2 4.1 3.8 4.3 3.8 3.8 3.9 4.5

Crime / aggression 3.8 3.5 4.1 3.8 3.3 4.2 3.9 3.8 3.8 3.9

Unemployment 3.8 3.6 4.1 4.0 3.6 4.4 3.6 3.0 4.1 5.5

Domestic or sports accidents 3.4 3.5 3.3 3.3 3.3 3.3 3.2 3.2 3.6 3.2

Work accidents 3.4 3.8 3.1 3.4 3.7 3.1 3.3 3.0 3.8 3.5

Terrorism 3.3 3.0 3.6 3.2 2.7 3.6 3.3 3.1 3.5 3.3

Plane crash 2.2 2.3 2.1 2.2 2.2 2.2 2.1 2.0 2.5 2.0

AXA Equitable Protection Report –December 2007 - 17

Which life accidents might happen to them?

Health, which ranks first in importance, is a source of worry for people. Serious illness ranks first in terms of likelihood of the negative events asked about in the survey, followed by serious car accidents. Financial problems, natural disasters, crime and unemployment rank next in the likelihood people attach to these events.

Feelings about the adequacy of their insurance coverage are related to Americans beliefs about the likelihood of serious financial problems and unemployment. The less well insured they feel they are, the more likely they believe that one of these two things will happen to them.

AXA Equitable Protection Report –December 2007 - 18

Which life accidents might happen to them …? /In all 11 countries studied, serious illness or car accidents ranked first or second in people’s ratings of the likelihood of these events happening to them. At or near the bottom of the list, for all countries, were plane accidents and terrorism.

Q58: Here is a list of risks that could happen to you in life. For each of these, please tell me to what extent you think these risks might happen to you personally, using a scale from 1 to 10 where 10 means that it “certainly will happen to you” and 1 means that it will “certainly not happen to you at all”. Please use the scores in-between to grade your opinion.

Significantly superior to Total Significantly inferior to Total

TOTAL USA Australia Belgium France Germany Hong Kong Italy Japan Spain Switzerland UK

n= 4009 360 362 360 360 370 367 390 360 360 360 360

Serious illness 5.6 5.3 5.0 5.9 6.4 5.9 4.8 5.6 6.0 5.0 6.0 5.1

Serious car accident 5.5 4.9 4.7 6.2 6.9 6.2 4.4 5.7 6.1 5.1 6.2 4.7

Serious financial problems 4.2 4.1 3.6 4.3 4.7 4.4 4.1 4.3 4.3 3.9 4.3 4.0

Domestic or sports accidents 4.2 3.4 3.4 4.4 5.0 4.9 3.8 4.3 4.6 3.6 5.1 3.4

Unemployment 4.1 3.8 3.1 3.6 4.6 4.7 4.4 4.1 4.3 3.9 4.3 4.1

Natural disaster / env. risks 4.1 4.0 3.4 3.9 4.4 4.3 4.2 4.4 5.3 3.5 4.6 3.3

Crime / aggression 3.9 3.8 3.8 4.4 4.2 4.1 3.6 4.3 3.9 2.8 4.2 4.2

Work accidents 3.8 3.4 3.2 3.7 4.7 4.3 3.4 3.6 4.0 3.8 4.4 3.4

Terrorism 3.2 3.3 2.8 3.2 3.4 3.4 2.5 3.4 3.1 3.5 3.0 3.2

Plane crash 2.8 2.2 2.6 2.9 2.8 2.9 3.0 2.9 3.0 2.4 3.3 2.8

Serious financial problems, which ranked third in likeliness ratings in the U.S., with a rating of 4.1, was rated as likely or more so by people in all counties other than Australia (3.6) and Spain (3.9).

AXA Equitable Protection Report –December 2007 - 19

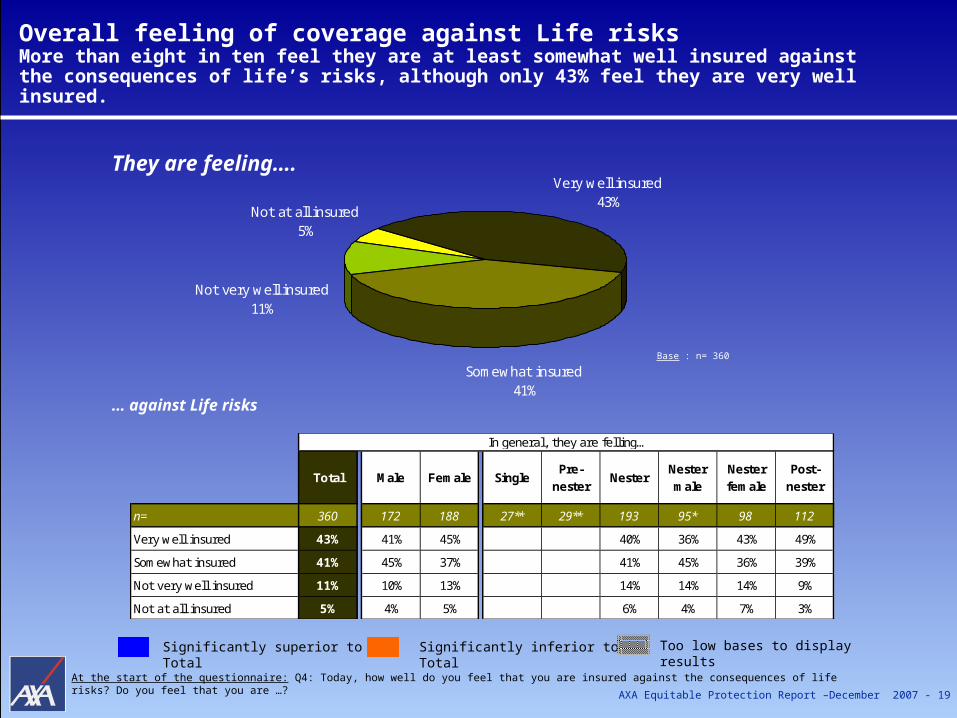

Very well insured43%

Not at all insured5%

Somewhat insured41%

Not very well insured11%

Significantly inferior to Total

Overall feeling of coverage against Life risksMore than eight in ten feel they are at least somewhat well insured against the consequences of life’s risks, although only 43% feel they are very well insured.

Base : n= 360

At the start of the questionnaire: Q4: Today, how well do you feel that you are insured against the consequences of life risks? Do you feel that you are …?

Significantly superior to Total

… against Life risks

Total Male Female SinglePre-

nesterNester

Nester male

Nester female

Post-nester

n= 360 172 188 27** 29** 193 95* 98 112

Very well insured 43% 41% 45% 40% 36% 43% 49%

Somewhat insured 41% 45% 37% 41% 45% 36% 39%

Not very well insured 11% 10% 13% 14% 14% 14% 9%

Not at all insured 5% 4% 5% 6% 4% 7% 3%

In general, they are felling…

Too low bases to display results

They are feeling….

AXA Equitable Protection Report –December 2007 - 20

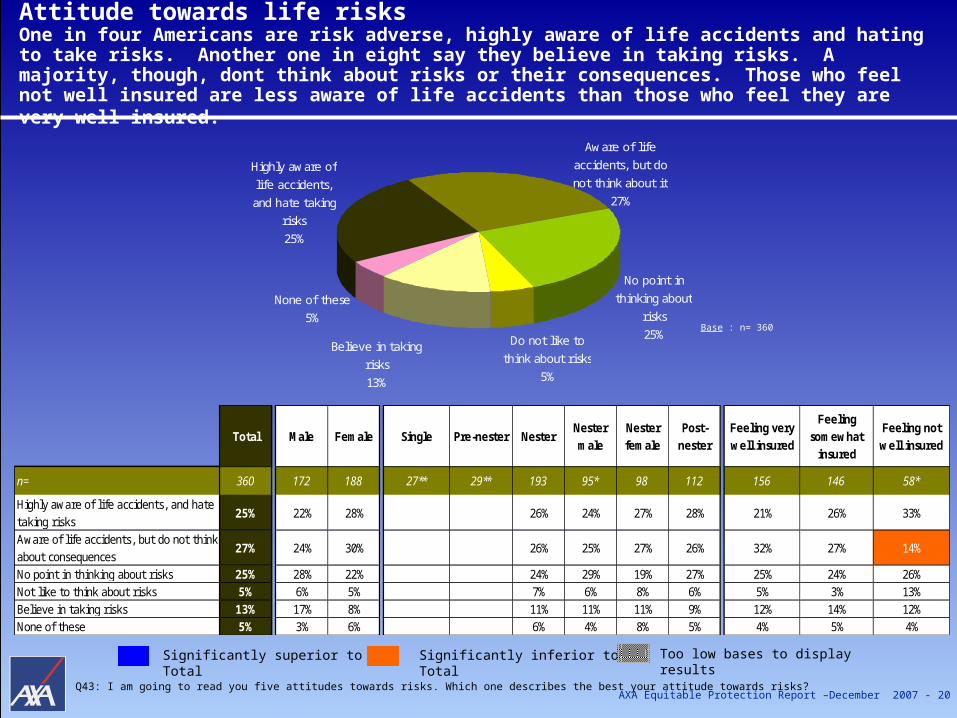

Attitude towards life risksOne in four Americans are risk adverse, highly aware of life accidents and hating to take risks. Another one in eight say they believe in taking risks. A majority, though, dont think about risks or their consequences. Those who feel not well insured are less aware of life accidents than those who feel they are very well insured.

Q43: I am going to read you five attitudes towards risks. Which one describes the best your attitude towards risks?

None of these

5%

Believe in taking

risks

13%

Do not like to

think about risks

5%

No point in

thinking about

risks

25%

Aware of life

accidents, but do

not think about it

27%

Highly aware of

life accidents,

and hate taking

risks

25%

Total Male Female Single Pre-nester NesterNester male

Nester female

Post-nester

Feeling very well insured

Feeling somewhat

insured

Feeling not well insured

n= 360 172 188 27** 29** 193 95* 98 112 156 146 58*

Highly aware of life accidents, and hate taking risks

25% 22% 28% 26% 24% 27% 28% 21% 26% 33%

Aware of life accidents, but do not think about consequences

27% 24% 30% 26% 25% 27% 26% 32% 27% 14%

No point in thinking about risks 25% 28% 22% 24% 29% 19% 27% 25% 24% 26%Not like to think about risks 5% 6% 5% 7% 6% 8% 6% 5% 3% 13%Believe in taking risks 13% 17% 8% 11% 11% 11% 9% 12% 14% 12%None of these 5% 3% 6% 6% 4% 8% 5% 4% 5% 4%

Base : n= 360

Significantly inferior to TotalSignificantly superior to Total Too low bases to display results

AXA Equitable Protection Report –December 2007 - 21

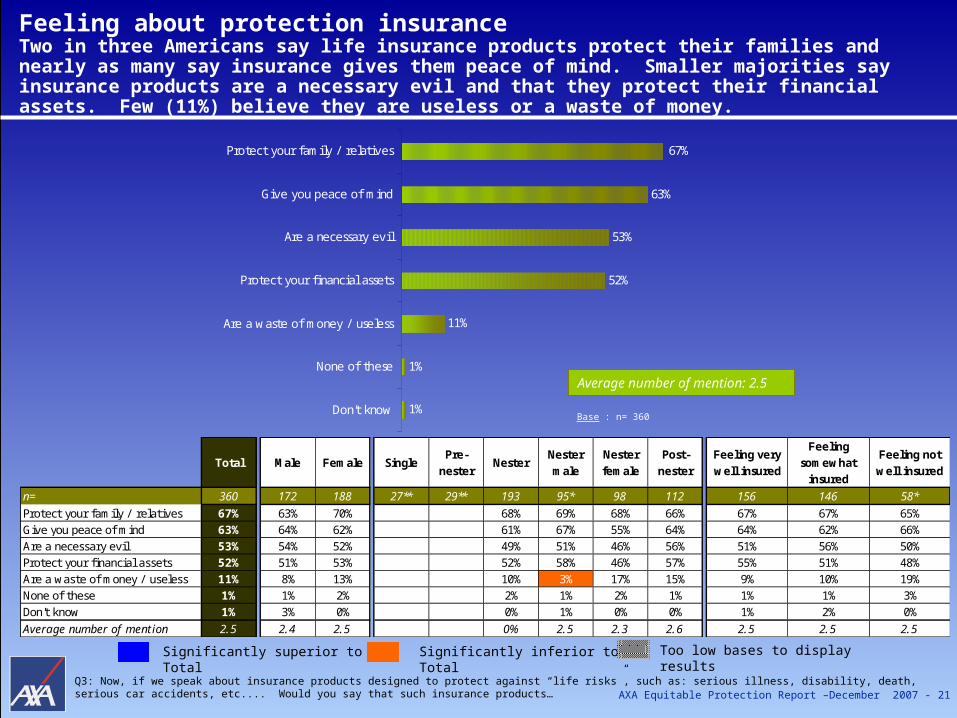

Feeling about protection insuranceTwo in three Americans say life insurance products protect their families and nearly as many say insurance gives them peace of mind. Smaller majorities say insurance products are a necessary evil and that they protect their financial assets. Few (11%) believe they are useless or a waste of money.

Base : n= 360

Q3: Now, if we speak about insurance products designed to protect against “life risks”, such as: serious illness, disability, death, serious car accidents, etc.... Would you say that such insurance products…

Average number of mention: 2.5

Significantly inferior to TotalSignificantly superior to Total Too low bases to display results

1%

1%

11%

52%

53%

63%

67%

Don't know

None of these

Are a waste of money / useless

Protect your financial assets

Are a necessary evil

Give you peace of mind

Protect your family / relatives

Total Male Female SinglePre-

nesterNester

Nester male

Nester female

Post-nester

Feeling very well insured

Feeling somewhat

insured

Feeling not well insured

n= 360 172 188 27** 29** 193 95* 98 112 156 146 58*

Protect your family / relatives 67% 63% 70% 68% 69% 68% 66% 67% 67% 65%Give you peace of mind 63% 64% 62% 61% 67% 55% 64% 64% 62% 66%Are a necessary evil 53% 54% 52% 49% 51% 46% 56% 51% 56% 50%Protect your financial assets 52% 51% 53% 52% 58% 46% 57% 55% 51% 48%Are a waste of money / useless 11% 8% 13% 10% 3% 17% 15% 9% 10% 19%None of these 1% 1% 2% 2% 1% 2% 1% 1% 1% 3%Don't know 1% 3% 0% 0% 1% 0% 0% 1% 2% 0%

Average number of mention 2.5 2.4 2.5 0% 2.5 2.3 2.6 2.5 2.5 2.5

AXA Equitable Protection Report –December 2007 - 22

Attitude towards life risks / Feelings about protection insurance Attitudes towards life risks: Americans are less averse to risks than people in most countries, and are more likely than others to say they believe in taking risks.

TOTAL USA Australia Belgium France Germany Hong Kong Italy J apan Spain Switzerland UK

n= 4009 360 362 360 360 370 367 390 360 360 360 360Highly aware of life accidents, and hate taking risks

31% 25% 29% 22% 34% 38% 18% 36% 29% 51% 18% 34%

Aware of life accidents, but do not think about it 27% 27% 31% 23% 21% 37% 24% 22% 38% 23% 24% 28%

No point in thinking about risks 25% 25% 25% 40% 30% 13% 36% 10% 26% 9% 41% 23%

Not like to think about risks 7% 5% 5% 7% 6% 9% 10% 11% 4% 12% 7% 6%

Believe in taking risks 8% 13% 5% 7% 8% 2% 12% 20% 2% 4% 10% 7%

None of these 2% 5% 4% 2% 1% 1% 1% 1% 2% 1% 1% 0%

Attitude towards life risks

Q43: I am going to read you five attitudes towards risks. Which one describes the best your attitude towards risks?

Significantly superior to Total Significantly inferior to Total

TOTAL USA Australia Belgium France Germany Hong Kong Italy J apan Spain Switzerland UK

n= 4009 360 362 360 360 370 367 390 360 360 360 360

Give you peace of mind 60% 63% 52% 57% 54% 66% 69% 33% 76% 79% 56% 59%

Protect your family / relatives 65% 67% 49% 73% 76% 71% 74% 35% 74% 75% 68% 56%

Protect your financial assets 45% 52% 38% 47% 47% 49% 56% 13% 37% 62% 48% 45%

Are a necessary evil 43% 53% 37% 44% 65% 44% 58% 23% 17% 48% 46% 41%

Are a waste of money / useless 15% 11% 19% 10% 19% 10% 15% 14% 11% 18% 15% 20%

None of these 2% 1% 2% 1% 2% 1% 4% 4% 4% 1% 2% 2%

Don't know 1% 1% 0% 1% 0% 1% 0% 1% 1% 1% 0% 2%

Average number of mention 2.3 2.5 2.0 2.3 2.6 2.4 2.7 1.2 2.1 2.8 2.3 2.2

Feelings about protection insurance

Q3: Now, if we speak about insurance products designed to protect against “life risks”, such as: serious illness, disability, death, serious car accidents, etc.... Would you say that such insurance products…

Feelings about protection insurance: Americans are more likely than those in most other countries to feel that insurance products are a necessary evil, but they are also somewhat less likely than average to consider them a waste of money.

AXA Equitable Protection Report –December 2007 - 23

Part 2: Attitudes & Behaviors

2.B Behaviors and habits against Life risks

AXA Equitable Protection Report –December 2007 - 24

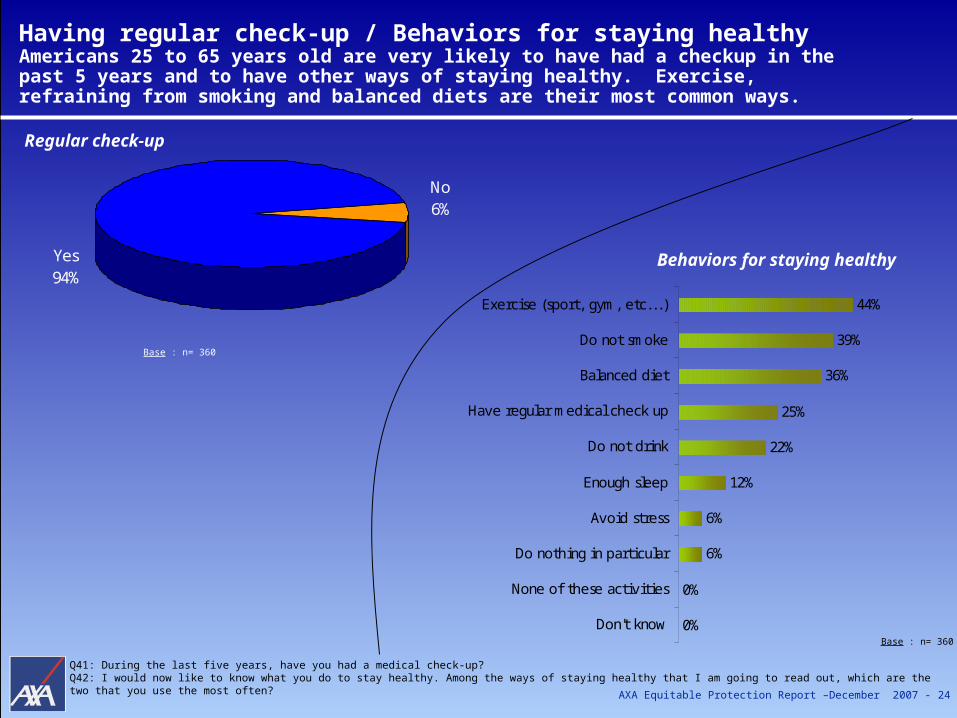

Having regular check-up / Behaviors for staying healthyAmericans 25 to 65 years old are very likely to have had a checkup in the past 5 years and to have other ways of staying healthy. Exercise, refraining from smoking and balanced diets are their most common ways.

Base : n= 360

Base : n= 360

Q41: During the last five years, have you had a medical check-up? Q42: I would now like to know what you do to stay healthy. Among the ways of staying healthy that I am going to read out, which are the two that you use the most often?

0%

0%

6%

6%

12%

22%

25%

36%

39%

44%

Don't know

None of these activities

Do nothing in particular

Avoid stress

Enough sleep

Do not drink

Have regular medical check up

Balanced diet

Do not smoke

Exercise (sport, gym, etc...)

No6%

Yes94%

Regular check-up

Behaviors for staying healthy

AXA Equitable Protection Report –December 2007 - 25

Having regular check-up / Behaviors for staying healthyThose who feel very well insured are more likely than others to have had a checkup in the past 5 years. Nester females are more likely to maintain a balanced diet to stay healthy. Those who feel they are not well insured are more likely than others to say they do nothing in particular to stay healthy.

Significantly superior to Total Significantly inferior to Total

Total Male Female SinglePre-

nesterNester

Nester male

Nester female

Post-nester

Feeling very well insured

Feeling somewhat

insured

Feeling not well

insured

n= 360 172 188 27** 29** 193 95* 98 112 156 146 58*

Yes 94% 90% 97% 95% 93% 96% 96% 98% 91% 89%

No 6% 10% 3% 5% 7% 4% 4% 2% 9% 11%

Total Male Female SinglePre-

nesterNester

Nester male

Nester female

Post-nester

Feeling very well insured

Feeling somewhat

insured

Feeling not well

insured

n= 360 172 188 27** 29** 193 95* 98 112 156 146 58*

Exercise (sport, gym, etc...) 44% 49% 41% 42% 43% 42% 41% 46% 51% 23%

Do not smoke 39% 39% 39% 39% 41% 38% 37% 44% 38% 28%

Balanced diet 36% 31% 40% 42% 36% 49% 28% 36% 36% 34%

Have regular medical check up 25% 23% 27% 25% 25% 25% 30% 24% 27% 25%

Do not drink 22% 23% 20% 26% 30% 22% 17% 19% 23% 26%

Enough sleep 12% 13% 12% 9% 9% 10% 19% 12% 9% 19%

Do nothing in particular 6% 5% 6% 5% 6% 5% 7% 4% 2% 18%

Avoid stress 6% 7% 4% 2% 2% 1% 9% 3% 8% 6%

None of these activities * 0% 0% 0% 0% 1% 0% 1% 0% 0%

Don't know * 0% 0% 0% 0% 0% 1% 0% 0% 0%

Regular check-up

Behaviours for staying healthy

Q41: During the last five years, have you had a medical check-up? Q42: I would now like to know what you do to stay healthy. Among the ways of staying healthy that I am going to read out, which are the two that you use the most often?

AXA Equitable Protection Report –December 2007 - 26

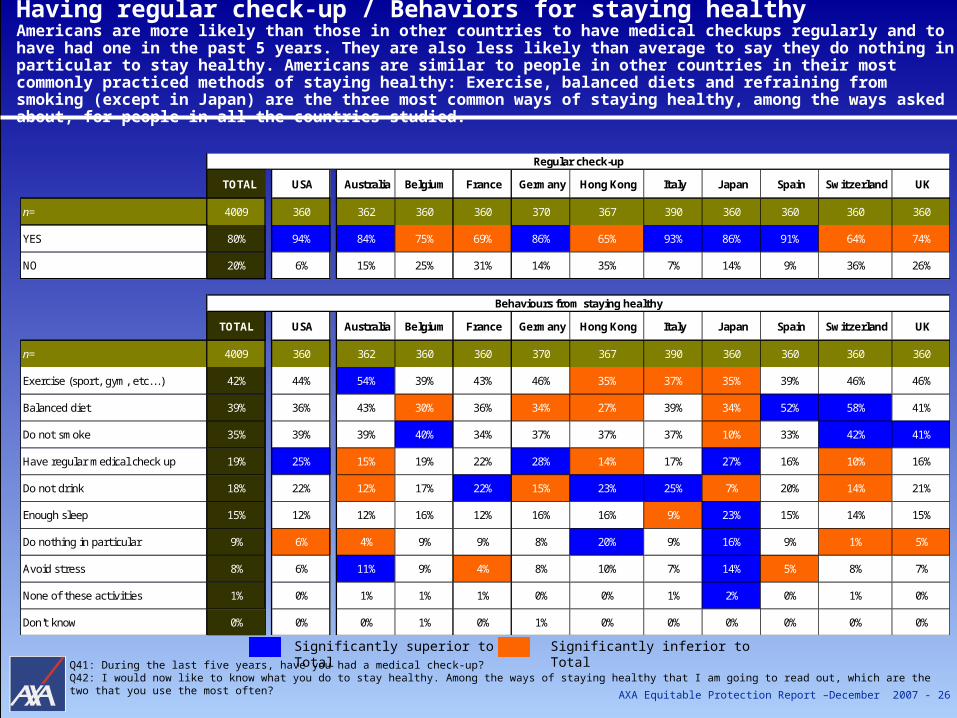

Having regular check-up / Behaviors for staying healthy Americans are more likely than those in other countries to have medical checkups regularly and to have had one in the past 5 years. They are also less likely than average to say they do nothing in particular to stay healthy. Americans are similar to people in other countries in their most commonly practiced methods of staying healthy: Exercise, balanced diets and refraining from smoking (except in Japan) are the three most common ways of staying healthy, among the ways asked about, for people in all the countries studied.

Significantly superior to Total Significantly inferior to TotalQ41: During the last five years, have you had a medical check-up? Q42: I would now like to know what you do to stay healthy. Among the ways of staying healthy that I am going to read out, which are the two that you use the most often?

TOTAL USA Australia Belgium France Germany Hong Kong Italy Japan Spain Switzerland UK

n= 4009 360 362 360 360 370 367 390 360 360 360 360

YES 80% 94% 84% 75% 69% 86% 65% 93% 86% 91% 64% 74%

NO 20% 6% 15% 25% 31% 14% 35% 7% 14% 9% 36% 26%

TOTAL USA Australia Belgium France Germany Hong Kong Italy Japan Spain Switzerland UK

n= 4009 360 362 360 360 370 367 390 360 360 360 360

Exercise (sport, gym, etc...) 42% 44% 54% 39% 43% 46% 35% 37% 35% 39% 46% 46%

Balanced diet 39% 36% 43% 30% 36% 34% 27% 39% 34% 52% 58% 41%

Do not smoke 35% 39% 39% 40% 34% 37% 37% 37% 10% 33% 42% 41%

Have regular medical check up 19% 25% 15% 19% 22% 28% 14% 17% 27% 16% 10% 16%

Do not drink 18% 22% 12% 17% 22% 15% 23% 25% 7% 20% 14% 21%

Enough sleep 15% 12% 12% 16% 12% 16% 16% 9% 23% 15% 14% 15%

Do nothing in particular 9% 6% 4% 9% 9% 8% 20% 9% 16% 9% 1% 5%

Avoid stress 8% 6% 11% 9% 4% 8% 10% 7% 14% 5% 8% 7%

None of these activities 1% 0% 1% 1% 1% 0% 0% 1% 2% 0% 1% 0%

Don't know 0% 0% 0% 1% 0% 1% 0% 0% 0% 0% 0% 0%

Regular check-up

Behaviours from staying healthy

AXA Equitable Protection Report –December 2007 - 27

Frequently25%

Rarely17%

Occasionally53%

Never5%

Thinking about life risksThree out of four think about the consequences of life risks at least occasionally and one out of four think about these frequently. Death and financial hardship are life risks that large majorities say they have though about.

Q5: Generally speaking, how much have you thought about the consequences of life risks? By “life risks” we mean serious illness, disability, death, long-term unemployment, serious car accidents, etc....Q6: When you think about the consequences of life risks, do you think about their impact on …?Q8: Which of the following consequences of life risks have you already thought about? Have you thought about…

AND ABOUT

Base : n= 360

Base : n= 343

Base : n= 343

Thinking about Life risks…

53%

66%

73%

79%

86%

Downsizing your

standard of living

Temporary disability

Permanent disability

Financial hardship

Death

THEI

R CONSE

QUENCES

FOR

* Only asked to divroced or personv being part of a blended family

59%

26%

59%

95%

95%

Other people

Your previous

partner*

Yourself

Your children

Your partner

AXA Equitable Protection Report –December 2007 - 28

Thinking about life risksThose who feel they are not well insured are more likely than others to think about life risks frequently.

Significantly superior to Total Significantly inferior to Total Not asked Too low bases to display resultsQ5: Generally speaking, how much have you thought about the consequences of life risks? By “life risks” we mean serious illness, disability, death, long-term unemployment, serious car accidents, etc....Q6: When you think about the consequences of life risks, do you think about their impact on …?Q8: Which of the following consequences of life risks have you already thought about? Have you thought about…

Total Male Female SinglePre-

nesterNester

Nester

male

Nester

female

Post-

nester

Feeling very well

insured

Feeling somewh

at insured

Feeling not well insured

n= 360 172 188 27** 29** 193 95* 98 112 156 146 58*

Frequently 25% 23% 27% 26% 21% 30% 26% 22% 22% 40%

Occasionally 53% 49% 57% 49% 48% 51% 51% 57% 58% 32%

Rarely 17% 20% 15% 19% 20% 18% 20% 18% 14% 20%

Rarely 5% 8% 1% 6% 11% 1% 3% 3% 5% 7%

n= 343 158 185 24** 29** 182 84* 98 108 151 138 54*

Your partner 95% 100% 91% 96% 100% 92% 94% 96% 95% 96%

Your children 95% 97% 93% 0% 99% 100% 98% 87% 94% 95% 95%

Yourself 59% 53% 64% 55% 48% 61% 58% 56% 66% 47%

Your previous partner* 26% 32% 21% 35% 17% 19%

Other people 59% 53% 64% 58% 48% 67% 55% 57% 63% 53%

None 2% 2% 2% 1% 0% 1% 5% 2% 1% 2%

n= 343 158 185 24** 29** 182 84* 98 108 151 138 54*

Death 86% 86% 86% 87% 85% 89% 84% 88% 89% 74%

Financial hardship 79% 79% 80% 82% 82% 82% 69% 75% 86% 75%

Permanent disability 73% 71% 74% 75% 73% 76% 70% 74% 73% 69%

Temporary disability 66% 65% 67% 69% 67% 71% 64% 68% 67% 56%

Downsizing your standard of living 53% 52% 54% 52% 47% 55% 51% 49% 57% 54%

Nothing 2% 2% 2% 1% 1% 1% 5% 3% 1% 3%

Average number of mention 3.6 3.5 3.6 3.6 3.5 3.7 3.4 3.6 3.7 3.3

Thinking about life risks

Their consequences for …

Thinking about* Only asked to divroced or personv being part of a blended family

AXA Equitable Protection Report –December 2007 - 29

Thinking About Life Risks

Americans do think about the consequences of life risks and, for those with families, especially the consequences on their families.

Death and financial hardship are the life risks the largest numbers of people have already thought about and large majorities have thought about permanent and temporary disabilities as well.

Nearly all of those with spouses or partners say it is the impact on their spouse/partner they think about. Nearly all of those with children say it is the impact on their children they think about.

The insurance that might give people peace of mind, may be most lacking for those who think most about these risks. Those who feel they are not well insured are more likely than others to think about life risks frequently.

AXA Equitable Protection Report –December 2007 - 30

Thinking about life risks Americans are more likely than those in other countries to have thought about their deaths, financial hardships and disabilities. They also think about life risks more frequently than people in other countries.

TOTAL USA Australia Belgium France Germany Hong Kong Italy Japan Spain Switzerland UK

n= 4009 360 362 360 360 370 367 390 360 360 360 360

Frequently 20% 25% 17% 21% 19% 38% 5% 29% 9% 20% 15% 22%Occasionally 46% 53% 50% 49% 43% 43% 40% 38% 66% 45% 37% 48%Rarely 26% 17% 28% 26% 27% 16% 40% 22% 23% 28% 37% 21%Never 8% 5% 6% 4% 11% 4% 15% 11% 1% 7% 11% 9%

TOTAL USA Australia Belgium France Germany Hong Kong Italy Japan Spain Switzerland UK

n= 3702 343 342 344 322 357 311 348 355 334 320 326

Your children 92% 95% 88% 93% 92% 94% 86% 94% 88% 95% 95% 93%Your partner 90% 95% 92% 90% 88% 94% 87% 89% 91% 88% 87% 92%Yourself 66% 59% 50% 63% 66% 79% 84% 83% 69% 65% 56% 56%Your previous partner* 16% 26% 12% 14% 14% 26% 6%Other people 55% 59% 50% 58% 51% 46% 62% 57% 43% 64% 60% 55%None 4% 2% 6% 3% 5% 2% 9% 3% 3% 4% 3% 3%

TOTAL USA Australia Belgium France Germany Hong Kong Italy Japan Spain Switzerland UK

n= 3702 343 342 344 322 357 311 348 355 334 320 326

Death 73% 86% 74% 69% 74% 74% 59% 70% 72% 69% 73% 83%Financial hardship 65% 79% 67% 59% 64% 74% 61% 66% 63% 57% 55% 71%Temporary disability 62% 66% 64% 64% 70% 68% 47% 55% 70% 54% 62% 62%Permanent disability 59% 73% 63% 54% 69% 69% 38% 54% 57% 48% 65% 58%Downsizing your standard of living 57% 53% 44% 59% 67% 67% 53% 59% 66% 54% 55% 43%None 6% 2% 6% 6% 5% 2% 11% 5% 8% 9% 6% 3%Average number of mention 3.4 3.6 3.1 3.1 3.4 4.2 3.2 3.1 3.3 2.8 3.1 3.9

Thinking about life risks

Their consequences for …

Thinking about …

Significantly inferior to TotalSignificantly superior to Total Too low bases to display results

Q5: Generally speaking, how much have you thought about the consequences of life risks? By “life risks” we mean serious illness, disability, death, long-term unemployment, serious car accidents, etc....Q6: When you think about the consequences of life risks, do you think about their impact on …?Q8: Which of the following consequences of life risks have you already thought about? Have you thought about…

* Only asked to divroced or personv being part of a blended family

AXA Equitable Protection Report –December 2007 - 31

35%

23%

27%

30%

49%

44%

65%

87%

None

A tax advisor oraccountant

An attorney / lawyer

A financial advisor

Your friends

An insurance agent /broker

Your family

Your partner*

only in passing

31% never

13%

in detail

56%

With whom do they talk about life risks..?People are more likely to have spoken to family members than to others about the consequences of life risks. Six in ten have spoken about them with their spouse or partner (87% of those who have a spouse or partner) and nearly two thirds have spoken about them with their families. Even among those who have a spouse or partner, though, only a little more than half have talked about these risks in detail. Fewer than half have talked about them to a financial professional. The insurance agent / broker is the professional who is cited mostly.

Base : n= 360

Q9: Have you talked about the consequences of life risks with your partner?Q10: Have you talked about the consequences of life risks with …?

Base : n= 248

How do they talk of it with their partner / spouse ?

Talking about life risks with …

*

* Only asked to people living in couple

With professional

63%

With loved ones84% (for those

not living in couple)

90% (for those living in couple)

AXA Equitable Protection Report –December 2007 - 32

With whom do they talk about life risks..?Those who feel very well insured are much more likely to have spoken with others (both with loved ones and professionals) about the consequences of life risks than are those who do not feel well insured.

Significantly superior to Total Significantly inferior to Total

Q9: Have you talked about the consequences of life risks with your partner?Q10: Have you talked about the consequences of life risks with …?

Not asked

* Only asked to people living in couple

Total Male Female SinglePre-

nesterNester

Nester male

Nester female

Post-nester

Feeling very well insured

Feeling somewhat

insured

Feeling not well insured

n= 360 172 188 27** 29** 193 95* 98 112 156 146 58*

Your partner* 87% 83% 91% 89% 83% 94% 88% 94% 84% 65%

Your family 65% 63% 67% 69% 70% 67% 59% 74% 59% 56%

An insurance agent / broker 49% 44% 53% 53% 48% 58% 42% 65% 42% 20%

Your friends 44% 35% 52% 46% 40% 53% 38% 49% 40% 41%

A financial advisor 30% 26% 35% 31% 27% 35% 32% 41% 26% 13%

A tax advisor or accountant 23% 23% 24% 22% 22% 22% 27% 35% 17% 8%

An attorney / lawyer 27% 26% 28% 31% 29% 33% 26% 35% 20% 25%

None 11% 15% 7% 8% 11% 5% 13% 4% 15% 21%

Talking about life risks with …

AXA Equitable Protection Report –December 2007 - 33

With whom do they talk about life risks..? Compared with people in other countries on average, Americans are more likely to talk with both family and professionals about the consequences of life risks.

Significantly superior to Total Significantly inferior to Total

Q9: Have you talked about the consequences of life risks with your partner?Q10: Have you talked about the consequences of life risks with …?

TOTAL USA Australia Belgium France Germany Hong Kong Italy Japan Spain Switzerland UK

n= 4009 360 362 360 360 370 367 390 360 360 360 360

Your partner* 78% 87% 82% 81% 79% 84% 42% 81% 79% 84% 83% 78%

Your family 56% 65% 45% 56% 54% 74% 30% 56% 70% 58% 61% 49%

Your friends 43% 44% 33% 48% 47% 55% 25% 53% 40% 51% 51% 32%

An insurance agent / broker 42% 49% 24% 48% 48% 66% 25% 49% 28% 38% 53% 38%

A financial advisor 25% 30% 33% 22% 34% 26% 6% 25% 14% 17% 27% 40%

A notary / solicitor 15% 27% 18% 20% 18% 18% 2% 7% 4% 0% 11% 22%

A tax advisor or accountant 15% 23% 23% 16% 17% 16% 0% 15% 8% 15% 17% 17%

None 16% 11% 17% 12% 13% 6% 45% 11% 12% 15% 13% 17%

* Only asked to people living in couple

AXA Equitable Protection Report –December 2007 - 34

Part 3: Product ownership & habits

AXA Equitable Protection Report –December 2007 - 35

Protection insurance ownership (provided by the employer and/or personally purchased)About eight in ten say they have term-life insurance and an equal number have health insurance. Disability insurance is less common (about half) and only about one fourth have long-term care insurance.

Base : n= 360

Q11: I am now going to read you a list of insurance products. Please tell me the ones your employer has taken out for you? Q14: Apart from the ones maybe provided by your company, have you personally taken out any of the following insurance products? Have you PERSONALLY taken out …Q15:I am now going to read you a list of insurance products. Please tell me the ones you have taken out personally? Have you PERSONALLY taken out…

16%

27%

33%

36%

16%

3%

7%

6%

14%

34%

8%

12%

13%

31%

32%

73%

54%

48%

19%

18%

Long term care insurance

Long-term disability insurance

Short-term disability insurance

Health, medical, hospitalisationinsurance

Life insurance

Provided by employer insurance only Provided by employer + personal insurance Personal insurance only None

AXA Equitable Protection Report –December 2007 - 36

Protection insurance ownership (provided by the employer and/or personally purchased)Ownership of all types of insurance is lower among those who feel they are not well insured than among others: Fewer than half of this group has term-life insurance, only six in ten have health insurance, and even fewer have disability or long-term care insurance.

Q11: I am now going to read you a list of insurance products. Please tell me the ones your employer has taken out for you? Q14: Apart from the ones maybe provided by your company, have you personally taken out any of the following insurance products? Have you PERSONALLY taken out …Q15:I am now going to read you a list of insurance products. Please tell me the ones you have taken out personally? Have you PERSONALLY taken out…

Significantly inferior to TotalSignificantly superior to Total Too low bases to display results

Total Male Female SinglePre-

nesterNester

Nester male

Nester female

Post-nester

Feeling very well insured

Feeling somewhat

insured

Feeling not well

insuredn= 360 172 188 27** 29** 193 95* 98 112 156 146 58*

Life insurance 82% 86% 78% 85% 90% 81% 81% 95% 82% 47%

Health, medical, hospitalisation insurance

81% 85% 76% 82% 87% 77% 80% 86% 83% 61%

Disability insurance 60% 65% 56% 63% 64% 62% 52% 67% 62% 38%

Short-term disability insurance 52% 54% 51% 54% 52% 55% 46% 62% 50% 32%

Long-term disability insurance 46% 50% 42% 48% 53% 43% 41% 55% 44% 26%

Long term care insurance 27% 27% 27% 28% 28% 27% 27% 38% 20% 16%

Average number of product individually owned

2.9 3.0 2.7 3.0 3.1 2.8 2.7 3.4 2.8 1.8

Protection insurance ownership

AXA Equitable Protection Report –December 2007 - 37

Personal protection insurance ownershipTwo thirds have purchased life insurance themselves, whether their employer provides any or not, and 44% have purchased health insurance. Far fewer have purchased any of the other insurance products asked about. Those who feel very well insured are more likely than others to have purchased life insurance for themselves.

Q11: I am now going to read you a list of insurance products. Please tell me the ones your employer has taken out for you? Q14: Apart from the ones maybe provided by your company, have you personally taken out any of the following insurance products? Have you PERSONALLY taken out …Q15:I am now going to read you a list of insurance products. Please tell me the ones you have taken out personally? Have you PERSONALLY taken out…

Significantly inferior to TotalSignificantly superior to Total Too low bases to display results

Total Male Female SinglePre-

nesterNester

Nester male

Nester female

Post-nester

Feeling very well insured

Feeling somewhat

insured

Feeling not well

insured

n= 360 172 188 27** 29** 193 95* 98 112 156 146 58*

Life insurance 66% 71% 62% 71% 74% 67% 64% 82% 64% 29%

Health, medical, hospitalisation insurance

44% 44% 44% 41% 39% 43% 43% 48% 45% 33%

Temporary disability insurance 19% 18% 21% 21% 19% 23% 20% 19% 19% 22%

Permanent disability insurance 19% 22% 15% 19% 23% 15% 18% 23% 17% 10%

Long term care insurance 10% 10% 11% 7% 6% 8% 16% 19% 6% 0%

Average number of product individually owned

1.6 1.7 1.5 1.6 1.6 1.6 1.6 1.9 1.5 0.9

Personal ownership protection insurance

AXA Equitable Protection Report –December 2007 - 38

Protection insurance ownership (the more equipped whatever the products) Americans are more likely to be covered by employer-provided insurance (health, life, and disabilty) than are people in the countries in the survey on average.

Significantly superior to Total Significantly inferior to Total

Not asked

TOTAL USA Australia Belgium France Germany Hong Kong Italy Japan Spain Switzerland UK

n= 4009 360 362 360 360 370 367 390 360 360 360 360

Health, medical, hospitalisation insuranceAt least one insurance 69% 81% 59% 88% 91% 85% 65% 34% 83% 51% 82% 40%Provided by employer insurance only 15% 36% 4% 22% 26% 18% 11% 12% 2% 23% 0% 15%Personal insurance only 40% 31% 48% 46% 41% 44% 34% 15% 68% 14% 82% 18%Provided by employer + Personal insurance only 14% 14% 7% 21% 24% 24% 20% 8% 13% 13% 0% 8%None 31% 19% 41% 12% 9% 15% 35% 66% 17% 49% 18% 60%

Life insuranceAt least one insurance 64% 82% 51% 71% 66% 53% 67% 45% 88% 53% 58% 71%

Provided by employer insurance only 9% 15% 10% 11% 18% 4% 5% 6% 1% 13% 13% 8%Personal insurance only 40% 32% 33% 47% 28% 44% 50% 32% 74% 26% 31% 42%Provided by employer + Personal insurance only 15% 34% 8% 13% 20% 5% 12% 7% 14% 15% 14% 21%None 36% 18% 49% 29% 34% 47% 33% 55% 12% 47% 42% 29%

DisabilityAt least one insurance 54% 60% 48% 39% 64% 71% 45% 39% 64% 48% 78% 40%Provided by employer insurance only 16% 33% 17% 17% 24% 3% 7% 9% 3% 21% 35% 12%Personal insurance only 25% 16% 24% 14% 21% 56% 24% 21% 46% 15% 19% 19%Provided by employer + Personal insurance only 13% 12% 8% 8% 20% 12% 14% 9% 16% 12% 24% 9%None 46% 40% 52% 61% 36% 29% 55% 61% 36% 53% 22% 60%

Supplementary pensionn= 2927 360 360 370 367 390 360 360 360

At least one insurance 48% 66% 59% 71% 24% 34% 41% 45% 44%Provided by employer insurance only 13% 13% 30% 11% 7% 6% 15% 5% 16%Personal insurance only 24% 35% 16% 39% 13% 19% 21% 28% 17%Provided by employer + Personal insurance only 11% 18% 13% 22% 4% 8% 5% 11% 11%None 52% 34% 41% 29% 76% 66% 59% 55% 56%

Long term unemployment insurancen= 2917 360 360 367 390 360 360 360 360

At least one insurance 15% 6% 18% 3% 5% 17% 3% 52% 20%Provided by employer insurance only 5% 0% 9% 3% 3% 12% 0% 11% 5%Personal insurance only 8% 6% 6% 30% 1% 3% 3% 34% 12%Provided by employer + Personal insurance only 2% 0% 2% 0% 1% 2% 0% 7% 3%None 85% 94% 82% 97% 95% 83% 97% 48% 80%

AXA Equitable Protection Report –December 2007 - 39

Protection insurance ownership (the least equipped whatever the products) Compared with other countries, the U.S. on average, is not lower in their ownership of any of the insurance prodcuts. Since they are more likely to receive at least some insurance from their employers, they are less likely to have only insurance products they purchased themselves.

Significantly superior to Total Significantly inferior to Total

Not asked

TOTAL USA Australia Belgium France Germany Hong Kong Italy Japan Spain Switzerland UK

n= 4009 360 362 360 360 370 367 390 360 360 360 360

Health, medical, hospitalisation insuranceAt least one insurance 69% 81% 59% 88% 91% 85% 65% 34% 83% 51% 82% 40%Provided by employer insurance only 15% 36% 4% 22% 26% 18% 11% 12% 2% 23% 0% 15%Personal insurance only 40% 31% 48% 46% 41% 44% 34% 15% 68% 14% 82% 18%Provided by employer + Personal insurance only 14% 14% 7% 21% 24% 24% 20% 8% 13% 13% 0% 8%None 31% 19% 41% 12% 9% 15% 35% 66% 17% 49% 18% 60%

Life insuranceAt least one insurance 64% 82% 51% 71% 66% 53% 67% 45% 88% 53% 58% 71%Provided by employer insurance only 9% 15% 10% 11% 18% 4% 5% 6% 1% 13% 13% 8%Personal insurance only 40% 32% 33% 47% 28% 44% 50% 32% 74% 26% 31% 42%Provided by employer + Personal insurance only 15% 34% 8% 13% 20% 5% 12% 7% 14% 15% 14% 21%None 36% 18% 49% 29% 34% 47% 33% 55% 12% 47% 42% 29%

DisabilityAt least one insurance 54% 60% 48% 39% 64% 71% 45% 39% 64% 48% 78% 40%Provided by employer insurance only 16% 33% 17% 17% 24% 3% 7% 9% 3% 21% 35% 12%Personal insurance only 25% 16% 24% 14% 21% 56% 24% 21% 46% 15% 19% 19%Provided by employer + Personal insurance only 13% 12% 8% 8% 20% 12% 14% 9% 16% 12% 24% 9%None 46% 40% 52% 61% 36% 29% 55% 61% 36% 53% 22% 60%

Supplementary pensionn= 2927 360 360 370 367 390 360 360 360

At least one insurance 48% 66% 59% 71% 24% 34% 41% 45% 44%Provided by employer insurance only 13% 13% 30% 11% 7% 6% 15% 5% 16%Personal insurance only 24% 35% 16% 39% 13% 19% 21% 28% 17%Provided by employer + Personal insurance only 11% 18% 13% 22% 4% 8% 5% 11% 11%None 52% 34% 41% 29% 76% 66% 59% 55% 56%

Long term unemployment insurancen= 2917 360 360 367 390 360 360 360 360

At least one insurance 15% 6% 18% 3% 5% 17% 3% 52% 20%Provided by employer insurance only 5% 0% 9% 3% 3% 12% 0% 11% 5%Personal insurance only 8% 6% 6% 0% 1% 3% 3% 34% 12%Provided by employer + Personal insurance only 2% 0% 2% 0% 1% 2% 0% 7% 3%None 85% 94% 82% 97% 95% 83% 97% 48% 80%

AXA Equitable Protection Report –December 2007 - 40

0%

4%

6%

8%

13%

33%

39%

75%

Don't know

None of the reasons

Avoid dipping into your

savings

Bought it with a mortgage

Recommended by a

professional adviser

Preserve your / your family

standard of living

Have peace of mind

Protect your family or

yourself

1%

17%

4%

4%

10%

11%

12%

20%

20%

Don't know

None of these reasons

Event among loved ones

Serious personal illness experience

Advice by a professional

Bought a house/ apartment

First job/ job promotion/ additional revenues

Marriage

/ additional child

Reasons for subscribing to life insurance and triggersAmong those who have individually-purchased life insurance, the most common reason is to protect their families or themselves (75%). The birth of a child and marriage are the events that most frequently prompted them to buy life insurance.

Base : n= 239

Base : n= 239

Q18: You told me that you have personally taken out a life insurance what were the main reasons for taking this out?Q19: Do you remember what led you to take-out your first individual life insurance? Was it?

The 2 main reasons

The first trigger

AXA Equitable Protection Report –December 2007 - 41

Reasons for subscribing to life insurance and triggersWomen are more likely than men to say it was the birth of a child that led them to purchase life insurance.

Q18: You told me that you have personally taken out a life insurance what were the main reasons for taking this out?Q19: Do you remember what led you to take-out your first individual life insurance? Was it?

The 2 main reasons Total Male Female SinglePre-

nesterNester

Nester male

Nester female

Post-nester

Feeling very well insured

Feeling somewhat

insured

Feeling not well insured

n= 239 123 116 11** 21** 136 70* 66* 71 128 94 17**

Protect your family or yourself 75% 74% 76% 81% 80% 82% 69% 68% 83%

Have peace of mind 39% 31% 47% 35% 32% 38% 43% 40% 40%

Avoid dipping into your savings 6% 7% 4% 5% 5% 5% 9% 5% 4%

Preserve your / your family standard of living

33% 37% 27% 35% 41% 29% 25% 41% 25%

Recommended by a professional 13% 13% 13% 13% 11% 15% 9% 16% 9%

Bought it with a mortgage 8% 11% 6% 10% 13% 6% 6% 8% 6%

None of the reasons 4% 4% 3% 0% 0% 0% 7% 2% 7%

Don't know 0% 0% 0% 0% 0% 0% 0% 0% 0%

The first trigger Total Male Female SinglePre-

nesterNester

Nester male

Nester female

Post-nester

Feeling very well insured

Feeling somewhat

insured

Feeling not well insured

n= 239 123 116 11** 21** 136 70* 66* 71 128 94 17**

First child / additional child 20% 13% 28% 24% 14% 34% 20% 15% 22%Marriage 20% 24% 16% 16% 13% 20% 26% 18% 24%First job/ job promotion/ additional. revenues

12% 15% 10% 9% 12% 5% 10% 14% 11%

Bought a house/ apartment 11% 14% 9% 15% 21% 7% 7% 13% 10%Advice by a professional 10% 10% 10% 13% 15% 12% 5% 11% 10%Event among loved ones 4% 2% 5% 2% 1% 4% 4% 5% 3%Serious personal illness experience 4% 3% 5% 4% 3% 4% 5% 4% 5%None of these reasons 17% 17% 18% 16% 17% 15% 21% 19% 15%Don't know 1% 2% 0% 1% 2% 0% 1% 1% 1%

AXA Equitable Protection Report –December 2007 - 42

Reasons for subscribing to a life insurance and triggers Compared with other countries surveyed, Americans on average, are more likely to say the reason they bought life insurance was to protect their families and themselves and less likely to say the main reason was a mortgage. Their purchase was also more likely to have been triggerd by the birth of a child or a marriage.

Q18: You told me that you have personally taken out a life insurance what were the main reasons for taking this out?Q19: Do you remember what led you to take-out your first individual life insurance? Was it?

TOTAL USA Australia Belgium France Germany Hong Kong Italy Japan Spain Switzerland UK

n= 2185 239 146 216 173 180 228 154 315 146 163 225

Protect your family or yourself 60% 75% 55% 37% 61% 66% 72% 57% 72% 47% 50% 51%

Have peace of mind 32% 39% 25% 16% 31% 25% 34% 32% 54% 32% 22% 28%

Preserve your / your family standard of living

23% 33% 18% 18% 18% 29% 21% 14% 30% 13% 30% 18%

Bought it with a mortgage 20% 8% 10% 47% 24% 15% 2% 8% 5% 53% 14% 41%

Recommended by a professional adviser

13% 13% 15% 13% 18% 14% 14% 13% 8% 16% 15% 11%

Avoid dipping into your savings 7% 6% 3% 9% 1% 9% 12% 10% 6% 3% 11% 5%

None of the reasons 3% 4% 5% 4% 3% 2% 4% 5% 2% 3% 4% 1%

Part of your personal insurance 1% 0% 8% 0% 0% 0% 0% 0% 0% 0% 0% 0%

Don't know 0% 0% 0% 1% 1% 0% 0% 0% 0% 0% 2% 1%

Significantly superior to Total Significantly inferior to Total

TOTAL USA Australia Belgium France Germany Hong Kong Italy Japan Spain Switzerland UK

n= 2185 239 146 216 173 180 228 154 315 146 163 225

Bought a house / apartment 22% 11% 17% 51% 25% 28% 4% 6% 1% 55% 15% 40%

Advice by a professional 20% 10% 14% 11% 13% 19% 35% 32% 29% 16% 22% 14%

First child / additional child 11% 20% 16% 4% 32% 8% 10% 8% 7% 3% 13% 8%

Marriage 10% 20% 9% 7% 7% 6% 12% 3% 14% 5% 11% 6%

First job / job promotion / additional revenues

10% 12% 10% 2% 1% 13% 9% 6% 27% 3% 2% 8%

Event among loved ones 4% 4% 1% 3% 9% 1% 6% 9% 1% 2% 2% 4%

Experience of personal serious illness

2% 4% 1% 2% 3% 2% 0% 1% 3% 1% 2% 4%

None of these reasons 18% 17% 16% 17% 9% 21% 23% 34% 15% 14% 29% 8%

Don't know 3% 1% 3% 2% 1% 2% 2% 1% 2% 1% 4% 8%

AXA Equitable Protection Report –December 2007 - 43

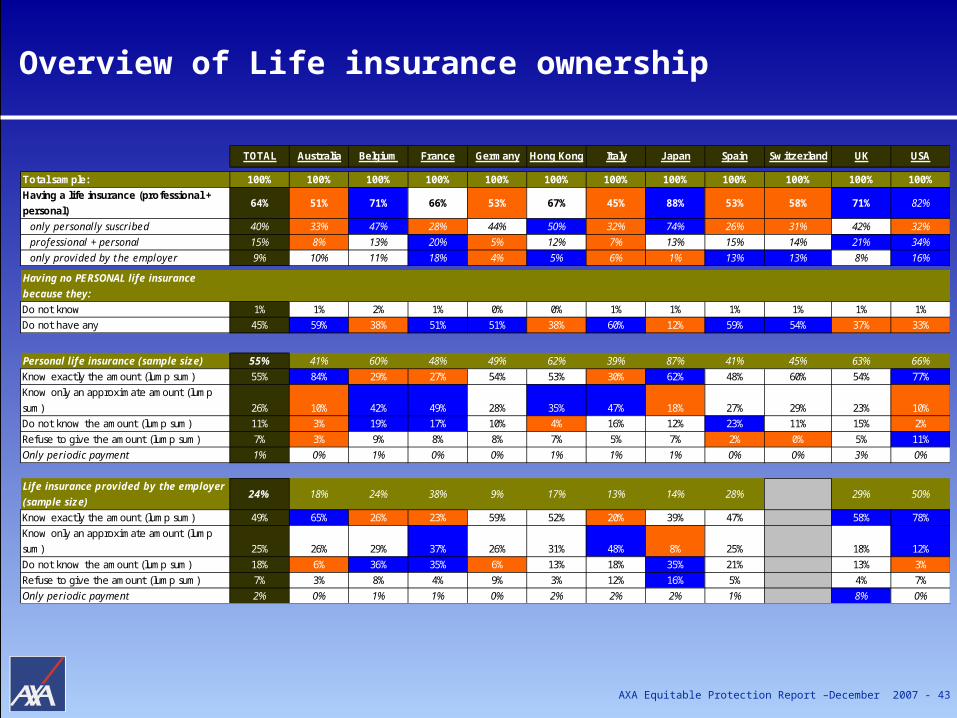

Overview of Life insurance ownership

TOTAL Australia Belgium France Germany Hong Kong Italy J apan Spain Switzerland UK USA

Total sample: 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

Having a life insurance (professional +

personal)64% 51% 71% 66% 53% 67% 45% 88% 53% 58% 71% 82%

only personally suscribed 40% 33% 47% 28% 44% 50% 32% 74% 26% 31% 42% 32%

professional + personal 15% 8% 13% 20% 5% 12% 7% 13% 15% 14% 21% 34%

only provided by the employer 9% 10% 11% 18% 4% 5% 6% 1% 13% 13% 8% 16%

Having no PERSONAL life insurance

because they:

Do not know 1% 1% 2% 1% 0% 0% 1% 1% 1% 1% 1% 1%

Do not have any 45% 59% 38% 51% 51% 38% 60% 12% 59% 54% 37% 33%

Personal life insurance (sample size) 55% 41% 60% 48% 49% 62% 39% 87% 41% 45% 63% 66%

Know exactly the amount (lump sum) 55% 84% 29% 27% 54% 53% 30% 62% 48% 60% 54% 77%

Know only an approximate amount (lump

sum) 26% 10% 42% 49% 28% 35% 47% 18% 27% 29% 23% 10%

Do not know the amount (lump sum) 11% 3% 19% 17% 10% 4% 16% 12% 23% 11% 15% 2%

Refuse to give the amount (lump sum) 7% 3% 9% 8% 8% 7% 5% 7% 2% 0% 5% 11%

Only periodic payment 1% 0% 1% 0% 0% 1% 1% 1% 0% 0% 3% 0%

Life insurance provided by the employer

(sample size)24% 18% 24% 38% 9% 17% 13% 14% 28% 29% 50%

Know exactly the amount (lump sum) 49% 65% 26% 23% 59% 52% 20% 39% 47% 58% 78%

Know only an approximate amount (lump

sum) 25% 26% 29% 37% 26% 31% 48% 8% 25% 18% 12%

Do not know the amount (lump sum) 18% 6% 36% 35% 6% 13% 18% 35% 21% 13% 3%

Refuse to give the amount (lump sum) 7% 3% 8% 4% 9% 3% 12% 16% 5% 4% 7%

Only periodic payment 2% 0% 1% 1% 0% 2% 2% 2% 1% 8% 0%

AXA Equitable Protection Report –December 2007 - 44

13%

29%

1%

1%

1%

2%

2%

2%

3%

3%

4%

5%

18%

26%

Don't know

Other

Too complicated

No insurance company propose it

No insurance company approached me

Having assets to cover it instead

Do not feel concerned about it yet

Never thought about it

Do not know the products

I don't care / it's a waste of money

Do not need it

Having no dependants

Too expensive

Having life insurance provided by my company

Base : n= 121

Q16: Why have you not taken out any INDIVIDUAL LIFE INSURANCE?

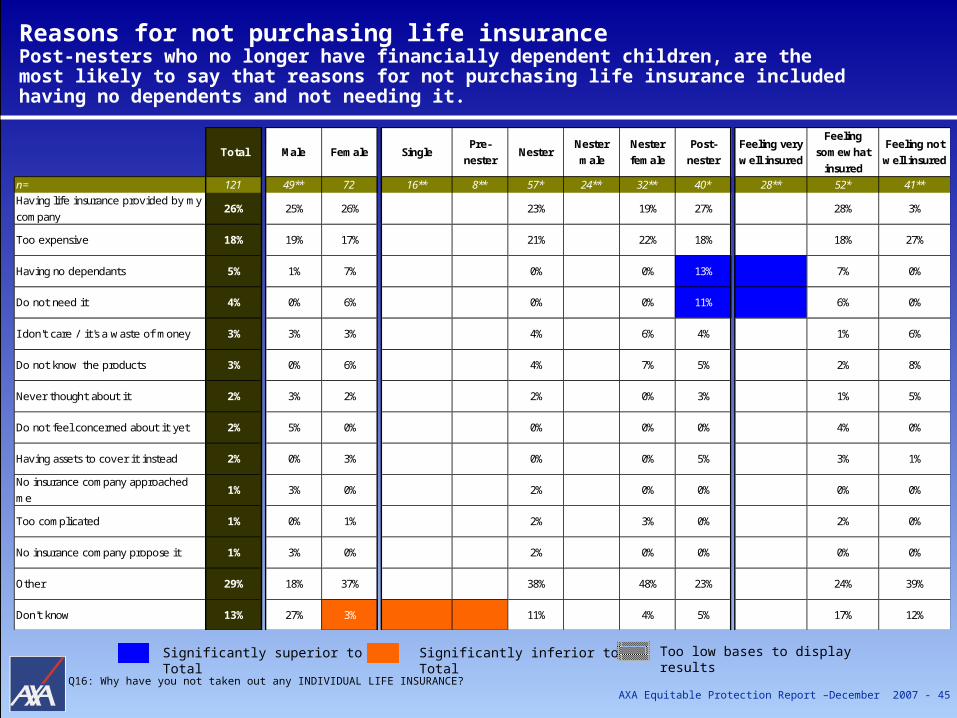

Reasons for not purchasing life insuranceAmong those who have not purchased individual life insurance on their own, the most common reason for not purchasing it was having life insurance provided by their employer (26%). The second most common reason was that they felt it was too expensive (18%).

AXA Equitable Protection Report –December 2007 - 45

Reasons for not purchasing life insurancePost-nesters who no longer have financially dependent children, are the most likely to say that reasons for not purchasing life insurance included having no dependents and not needing it.

Q16: Why have you not taken out any INDIVIDUAL LIFE INSURANCE?

Total Male Female SinglePre-

nesterNester

Nester

male

Nester

female

Post-

nester

Feeling very

well insured

Feeling

somewhat

insured

Feeling not

well insured

n= 121 49** 72 16** 8** 57* 24** 32** 40* 28** 52* 41**Having life insurance provided by my

company26% 25% 26% 23% 19% 27% 28% 3%

Too expensive 18% 19% 17% 21% 22% 18% 18% 27%

Having no dependants 5% 1% 7% 0% 0% 13% 7% 0%

Do not need it 4% 0% 6% 0% 0% 11% 6% 0%

I don't care / it's a waste of money 3% 3% 3% 4% 6% 4% 1% 6%

Do not know the products 3% 0% 6% 4% 7% 5% 2% 8%

Never thought about it 2% 3% 2% 2% 0% 3% 1% 5%

Do not feel concerned about it yet 2% 5% 0% 0% 0% 0% 4% 0%

Having assets to cover it instead 2% 0% 3% 0% 0% 5% 3% 1%

No insurance company approached

me1% 3% 0% 2% 0% 0% 0% 0%

Too complicated 1% 0% 1% 2% 3% 0% 2% 0%

No insurance company propose it 1% 3% 0% 2% 0% 0% 0% 0%

Other 29% 18% 37% 38% 48% 23% 24% 39%

Don't know 13% 27% 3% 11% 4% 5% 17% 12%

Significantly inferior to TotalSignificantly superior to Total Too low bases to display results

AXA Equitable Protection Report –December 2007 - 46

Reasons for not purchasing life insurance People in the U.S. who have not purchased individual life insurance are more likely than those in other countries to say they did not purchase it because their employer provides life insurance. They are less likely than those in other countries to say their reasons included that they did not need it, that they had never thought of it, or that they do not feel concerned about it yet.

Significantly superior to Total Significantly inferior to Total

Q16: Why have you not taken out any INDIVIDUAL LIFE INSURANCE?

TOTAL USA Australia Belgium France Germany Hong Kong Italy Japan Spain Switzerland UK

n= 1824 121 216 144 187 190 139 236 45* 214 197 135

Do not need it 22% 4% 23% 20% 21% 23% 22% 17% 31% 22% 34% 21%

Too expensive 20% 18% 27% 11% 16% 26% 16% 28% 29% 14% 16% 23%

Never thought about it 19% 2% 12% 18% 25% 10% 25% 36% 9% 31% 16% 10%

Having life insurance provided by my company

10% 26% 7% 19% 15% 6% 3% 5% 2% 12% 4% 9%

Do not feel concerned about it yet 9% 2% 5% 6% 20% 10% 4% 11% 20% 6% 8% 11%

I don't care / it's a waste of money 7% 3% 7% 5% 9% 7% 11% 8% 13% 6% 4% 7%

Having life insurance linked to a mortgage 3% 0% * 9% 3% 3% 1% 1% 4% 5% 1% 6%

Do not know the products 3% 3% 2% 3% 2% 5% 2% 6% 9% 2% 3% 2%

Having assets to cover it instead 3% 2% 4% 5% 2% 6% 1% 0% 7% 1% 5% 4%

Having no dependants 3% 5% 4% 6% 3% 3% 1% 1% 4% 0% 4% 7%

Too complicated 2% 1% 0% 1% 2% 3% 1% 3% 9% 1% 1% 2%

Covered by the government 2% 0% 0% 2% 1% 4% 2% 0% 2% 5% 2% 1%

No insurance company propose it 1% 1% 0% 1% 1% 2% 0% 0% 2% 1% 0% 0%

Other 15% 29% 7% 18% 12% 22% 24% 2% 31% 14% 15% 13%

Don't know 4% 13% 4% 8% 2% 7% 2% 0% 0% 2% 6% 4%

AXA Equitable Protection Report –December 2007 - 47

Reasons for purchasing disability insuranceThe most common reasons for Americans purchasing disability insurance are to protect their families or themselves and to have peace of mind.

TEMPORARY disability insurance

PERMANENT disability insurance

0%

0%

7%

27%

30%

55%

60%

Don't know

None of the reasons

Recommended by a professional adviser

Preserve your standard of living, thestandard of living of your family

Avoid dipping into your savings

Protect your family or yourself

Have peace of mind

0%

0%

2%

11%

11%

29%

54%

70%

Don't know

None of the reasons

Bought it with a mortgage

Avoid dipping into your savings

Recommended by a professional adviser

Preserve your standard of living, thestandard of living of your family

Have peace of mind

Protect your family or yourself

Base : n= 40* Base : n= 37*

Q18a: You told me that you have personally taken out a TEMPORARY disability insurance what were the main reasons for taking this out? Q18b: You told me that you have personally taken out a PERMANENT disability insurance what were the main reasons for taking this out?

AXA Equitable Protection Report –December 2007 - 48

Reasons for not purchasing individual disability insuranceFor those who have not purchased individual disabilty insurance, the most common reason is that they had this insurance through their employers. Other reasons included it being too expensive or that they had never thought about it.

Q17: Why have you not taken out any disability insurance?

10%

20%

2%

2%

2%

3%

5%

12%

14%

34%

Don't know

Other

Don't feel concerned about it yet

Having assets to cover it instead

Don't care / waste of money

Do not know the products

I don't need it

I have never thought about it

Too expensive

Having disability insurance provided by my company

Base : n= 183

AXA Equitable Protection Report –December 2007 - 49

Reasons for not purchasing individual disability insuranceFor those who feel very well insured but have not purchased individual disability insurance, the most common reason is that their employer provides this insurance.

Q17: Why have you not taken out any disability insurance?

Total Male Female SinglePre-

nesterNester

Nester male

Nester female

Post-nester

Feeling very well insured

Feeling somewhat

insured

Feeling not well insured

n= 183 94* 89 22** 18** 96 51* 45* 46* 75 81* 27**Having disability insurance provided by my company

34% 34% 34% 33% 34% 31% 41% 53% 27%

Too expensive 14% 17% 12% 14% 13% 15% 17% 4% 20%

Never thought about it 12% 16% 8% 11% 12% 10% 4% 7% 20%

Do not need it 5% 1% 10% 4% 0% 8% 11% 9% 4%

Do not know the products 3% 5% 1% 5% 7% 2% 0% 0% 2%

I don't care / it's a waste of money 2% 3% 1% 0% 0% 0% 6% 1% 2%

Do not feel concerned about it yet 2% 1% 4% 3% 3% 4% 3% 2% 4%

Having assets to cover it instead 2% 3% 1% 2% 4% 0% 4% 2% 2%

Too complicated 1% 1% 1% 2% 3% 2% 0% 0% 3%

Covered by the government 1% 1% 1% 1% 1% 0% 3% 1% 1%

No insurance company approached me

1% 0% 2% 1% 0% 2% 1% 0% 1%

Other 20% 17% 23% 21% 21% 21% 14% 16% 25%

Don't know 10% 8% 12% 13% 13% 12% 5% 6% 7%

Significantly inferior to TotalSignificantly superior to Total Too low bases to display results

AXA Equitable Protection Report –December 2007 - 50

Part 4: Theoretical Insurance Gap

In order to allow for international comparison, a common Gap formula was designed to be applicable for all respondents

AXA Equitable Protection Report –December 2007 - 51

Determining the amount of household death coverage needed = "Pure Need "

Number of dependant: for each dependant child: 1for each dependant adults (except spouse/partner): 1

Capital Needs Income Needs

Income Multiple (depending on

personal situation)

Current Annual Gross Household Income x

Uninsured Household Debt

(Mortgage, Student Loans, Consumer

Loans, Other)

+=

Amount of Coverage Needed =

1

1

1

1

Single, No dependants

3 + 2 * Number of dependants361+

4 + 2 * Number of dependants451-60

5 + 2 * Number of dependants541-50

6 + 2 * Number of dependants6Under 40

With Dependants (regardless of marital status)

Married or Partnered, No Dependants

Age

(if married or partnered, use age of younger spouse)

1

1

1

1

Single, No Dependants

3 + 2 * Number of Dependants361+

4 + 2 * Number of Dependants451-60

5 + 2 * Number of Dependants541-50

6 + 2 * Number of Dependants6Under 40

With Dependants (regardless of marital status)

Married or Partnered, No Dependants

Age

(if married or partnered, use age of younger spouse)

+=

AXA Equitable Protection Report –December 2007 - 52

Determining the amount of the gap in death coverage

Existing Household Life Insurance+

Other Household Liquid Assets (obtained from survey responses)

Amount of Household Coverage Needed (“Pure Need”)

as per previous slide

Gap In Household Coverage =

-=

AXA Equitable Protection Report –December 2007 - 53

Based on input from Survey respondents

Personal Situation:•Age (of both spouses)

•Single or Married/Partnered

• Number of Dependants

Current Annual Gross Household Income

Bracket

Uninsured Household Debt Bracket

(Includes Mortgage, Student Loans, Consumer

Loans, Other)

Other Household Liquid Assets Available

(Bracket)

Existing Household Life Insurance Coverage

(Bracket)

AXA Equitable Protection Report –December 2007 - 54

Explanation of Insurance Gap

AMOUNT OF UNINSURED

HOUSEHOLD DEBT / LOAN

CURRENT ANNUAL GROSS INCOME *

(HOUSEHOLD)+ X

NUMBER OF DEPENDANT

MULTIPLIER **=

COVERAGE NEED

-

LIFE INSURANCE,

EXISTING COVERAGE +

= INSURANCE GAP

Which implies that:

A positive insurance gap means that the respondent is “under equipped” in terms of protection products and or in terms of available assets and it is under insuring his or her need.

A negative or zero value means that there is no insurance gap: the respondent has chosen for more than the minimum coverage (as it is always possible in life coverage) or has enough liquid assets, or both.

COVERAGE NEED

( )

LIQUID ASSETS+( )

The insurance is calculated as follows:

* Where people are used to evaluate in net monthly income:For USA: we apply the following formula: net estimation of the respondent * 12 months

** Cf definition from table of page 57

AXA Equitable Protection Report –December 2007 - 55-1 000 000

-500 000

0

500 000

1 000 000

1 500 000

Mean: - 271,928 US$ 81,632 US$ 299,647 US$ 754,740 US$

No Gap 1st tercile = Gap +

2nd tercile = Gap ++

3rd tercile = Gap +++

Calculated Insurance GapThe gap could be calculated for 213 people surveyed, or 59% of interviewees

Have an insurance

gap69%

No insurance gap31%

AXA Equitable Protection Report –December 2007 - 56

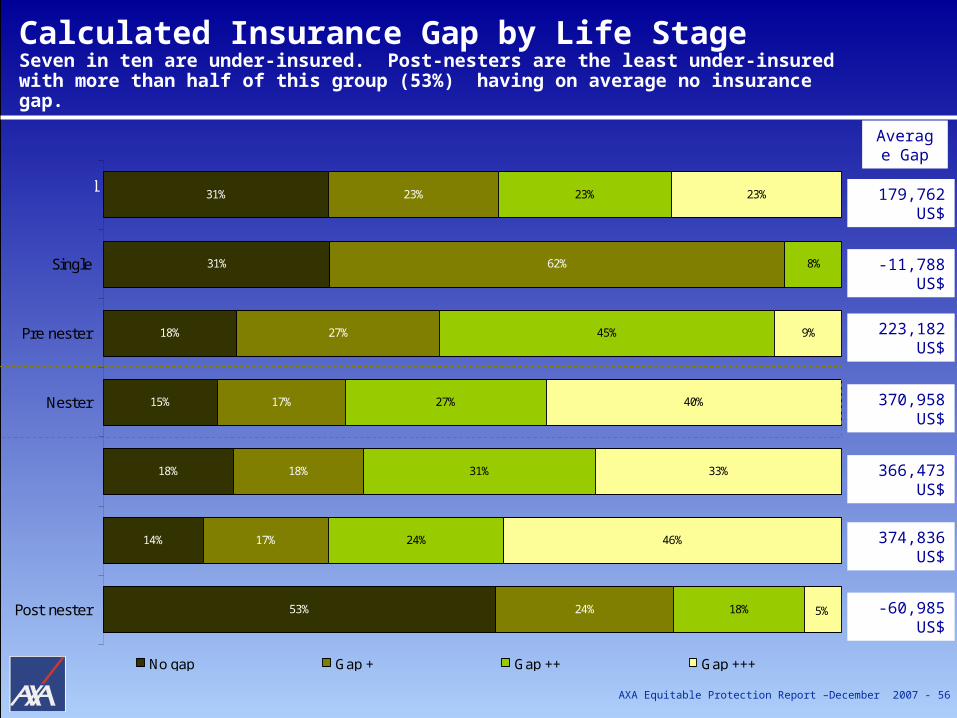

Calculated Insurance Gap by Life StageSeven in ten are under-insured. Post-nesters are the least under-insured with more than half of this group (53%) having on average no insurance gap.

179,762 US$

-11,788 US$

223,182 US$

366,473 US$

374,836 US$

-60,985 US$

370,958 US$

Average Gap

53%

14%

18%

15%

18%

31%

31%

24%

17%

18%

17%

27%

62%

23%

18%

24%

31%

27%

45%

8%

23%

46%

33%

40%

9%

5%

23%

Post nester

Nester

Pre nester

Single

No gap Gap + Gap ++ Gap +++

Total

Nester female

Nester male

AXA Equitable Protection Report –December 2007 - 57

Calculated Insurance Gap by Life Stage

-1 000 000

-500 000

0

500 000

1 000 000

1 500 000

Singlen= 13*

-1 000 000

-500 000

0

500 000

1 000 000

1 500 000

Pre-Nestern= 11*

-1 000 000

-500 000

0

500 000

1 000 000

1 500 000

Nestern= 110

-1 500 000

-1 000 000

-500 000

0

500 000

1 000 000

1 500 000

Post-Nestern= 79

AXA Equitable Protection Report –December 2007 - 58

Composition of Insurance Gap GroupsThe group with no insurance gap is comprised primarily of post-nesters who no longer have dependent children. The group with the widest gap is comprised primarily of nesters, who do have financially dependent children.

-271,928 US$

81,632 US$

299,647 US$

754,740 US$

Average Gap

2%

16%

6%

90%

60%

39%

26%

2%

10%

6%

3%

8%

28%

39%

65%

Gap +++

Gap ++

Gap +

No gap

Single Nester Pre nester Post nester

AXA Equitable Protection Report –December 2007 - 59

Calculated insurance gap vs feeling of being well insured or notPeople who feel they are not well insured have the largest insurance gap, averaging a gap of $214,000…

Average Gap

164,801 US$

181,812 US$

214,416 US$

179,762 US$

12%

33%

36%

31%

34%

21%

21%

23%

38%

23%

18%

23%

16%

23%

25%

23%

Not well + Not at all insured

Somewhat insured

Very well insured

Total

No gap Gap + Gap ++ Gap +++

AXA Equitable Protection Report –December 2007 - 60

Calculated insurance gap vs feeling of being well insured or not… But a lot of people feeling very well insured have an important insurance gap.

-271,928 US$

81,632 US$

299,647 US$

754,740 US$

Average Gap

10%

24%

22%

6%

45%

44%

41%

46%

45%

32%

37%

48%

Gap +++

Gap ++

Gap +

No gap

Not well + Not at all insured Somewhat insured Very well insured

AXA Equitable Protection Report –December 2007 - 61

The Calculated Insurance GapThree countries with quite a large proportion of people showing a gap: Belgium, Hong Kong and Switzerland

15%

15%

20%

23%

25%

28%

29%

29%

31%

36%

24%

86%

85%

85%

80%

77%

75%

72%

71%

71%

69%

64%

76%

14%Belgium (178)

Switzerland (227)

Hong Kong (156)

Germany (191)

Japan (156)

France (227)

Italy (169)

UK (178)

Spain (191)

USA (225)

Australia (225)

Total (2241)

Having no Gap Having a Gap

AXA Equitable Protection Report –December 2007 - 62

Overall analysis for the Gap

On average, Americans 25 to 65 years of age have an insurance gap of $179,762, though the size of that gap varies across life stages.

Nesters, who have dependent children, have on average the highest gap ($370,958) while post-nesters have none on average.

AXA Equitable Protection Report –December 2007 - 63

Part 5: Conclusions

AXA Equitable Protection Report –December 2007 - 64

Key Findings in America

A. There is a serious lack of knowledge regarding financial coverage needs in case of death.

B. There is still an high level of underinsurance on individual’s most precious assets: life. Close to 70 percent of Americans have an insurance gap (which compares favorably to the survey average of 76 percent), and it averages an amount of $180,000 or 127.000 € which is somewhat lower than the survey average of 150,000 €

C. The level of underinsurance is particularly high among the most needing segment, i.e. the nesters with an average gap of $371,000.

D. A dissonance was observed between feeling and being actually very well covered, as still 64 percent of those claiming to feel very well insured do have an insurance gap.

AXA Equitable Protection Report –December 2007 - 65

Appendices

Statistical differences rules

Details about Gap profiles

Details about Gap calculation elements

AXA Equitable Protection Report –December 2007 - 66

Analysis of information

Brackets evaluation: all amounts or percentages will be presented in a range of brackets; in order to determine the values of the brackets we apply the following rules:

for the smallest bracket we took 0.75 of the bracket value (e.g. “Less than 25,000” bracket was evaluated at 18,750)

for the highest bracket we took 1.5 of the bracket value (e.g. “More than 1,000,000” was evaluated at 1,500,000)

for all other brackets we took the average (e.g. “From 25,000 to 50,000” was evaluated at 37,500)

Minimum bases: base between 30 and 59 was analyzed with caution. It is presented as

follows (n= 35*). base under 29 was not analyzed because it was too low. It is presented

as follows (n= 25**).

Significances are calculated with a 10 percent risk level.

AXA Equitable Protection Report –December 2007 - 67

Appendix: Gap descriptionThose with the largest insurance gap have higher gross income than do Americans with lower or no gaps.

In terms of Annual Gross Income

Total NO GAP GAP + GAP ++ GAP +++

n= 225 58* 53* 56* 58*

Under $25,000 10% 13% 25% 5% 0%$25,000 to 50,000 22% 25% 20% 41% 2%$50,000 to 75,000 32% 28% 35% 35% 30%$75,000 to 100,000 16% 14% 15% 11% 23%$100,000 to 150,000 14% 13% 5% 8% 30%$150,000 to 250,000 5% 7% 0% 0% 13%$250,000 to 500,000 1% 1% 0% 0% 2%More than $500,000 0% 0% 0% 0% 0%

In terms of Debts / Loans insured / not insured

Total NO GAP GAP + GAP ++ GAP +++

n= 225 58* 53* 56* 58*

Yes, having loans all insured 37% 42% 38% 38% 32%Yes, having loans not insured 36% 27% 18% 41% 56%No, having no loan 22% 30% 34% 17% 6%

Don't know 5% 1% 10% 4% 6%

Significantly superior to Total Significantly inferior to Total

AXA Equitable Protection Report –December 2007 - 68

Appendix: Gap descriptionSimilarly, that high insurance gap group has higher levels of assets.

In terms of Available assets…

Total NO GAP GAP + GAP ++ GAP +++

n= 218 57* 52* 53* 56*

No assets 2% 0% 3% 3% 3%

Less than $25,000 21% 12% 31% 29% 14%

$25,000 to 50,000 8% 7% 14% 7% 5%

$50,001 to 100,000 15% 6% 13% 29% 14%

$100,001 to 250,000 29% 33% 22% 16% 44%

$250,001 to 500,000 17% 20% 16% 14% 18%

Significantly superior to Total Significantly inferior to Total

AXA Equitable Protection Report –December 2007 - 69

Total NO GAP GAP + GAP ++ GAP +++

n= 225 58* 53* 56* 58*

Frequently 23% 13% 26% 33% 19%

Occasionally 54% 59% 46% 52% 58%

Rarely 17% 25% 20% 11% 12%

Never 6% 3% 8% 5% 10%

n= 211 57* 48* 54* 52*

Your children 97% 96% 98% 97% 99%

Your partner 98% 95% 100% 100% 99%

Yourself 55% 48% 63% 56% 55%

Your previous partner* 31%

Other people 60% 47% 83% 48% 67%

n= 211 57* 48* 54* 52*

Death 85% 80% 93% 80% 87%

Financial hardship 83% 75% 88% 87% 85%

Permanent disability 70% 69% 72% 66% 74%

Temporary disability 66% 68% 64% 62% 68%

Downsizing your standard of

living56% 65% 60% 51% 47%

Appendix: Gap descriptionThose who have the highest gap seem to speak the least to professionals

Total NO GAP GAP + GAP ++ GAP +++

n= 225 58* 53* 56* 58*

Your partner* 86% 88% 76% 93% 88%

Your family 67% 69% 65% 60% 74%

An insurance agent / broker 48% 56% 37% 48% 51%

Your friends 48% 45% 51% 43% 52%

A financial advisor 27% 41% 17% 17% 32%

A notary / solicitor 25% 34% 22% 22% 22%

A tax advisor or accountant 15% 27% 13% 10% 10%

None 17% 15% 22% 20% 11%

With whom do they talk of Life risks…

Base too low to display resultsSignificantly superior to Total Significantly inferior to Total

* only asked to people living as a couple

Q5: Generally speaking, how much have you thought about the consequences of life risks? By “life risks” we mean serious illness, disability, death, long-term unemployment, serious car accidents, etc....Q6: When you think about the consequences of life risks, do you think about their impact on …?Q8: Which of the following consequences of life risks have you already thought about? Have you thought about…Q10: Have you talked about the consequences of life risks with …?

* Only asked to divroced or personv being part of a blended family

AXA Equitable Protection Report –December 2007 - 70

Total NO GAP GAP + GAP ++ GAP +++

n= 225 58* 53* 56* 58*

YES 43% 59% 30% 41% 41%NO 57% 41% 70% 59% 59%

NO, not have yet made one 34% 26% 30% 32% 49%NO, not thought about it 12% 6% 16% 19% 6%NO, not concerning you yet 8% 7% 16% 4% 5%NO, not legally necessary 0% 0% 2% 0% 0%NO, not a very pleasant thought 3% 2% 6% 4% 0%

Total NO GAP GAP + GAP ++ GAP +++