Electronic copy available at: http://ssrn.com/abstract=1557010

1

Bank Diversification, Risk and Profitability in an Emerging Economy with Regulatory

Asset Structure Constraints: Evidence from the Philippines

Céline Meslier, Ruth Tacneng* and Amine Tarazi

Université de Limoges, LAPE, 5 rue Félix Eboué, BP 3127, 87031 Limoges Cedex, France

Abstract

This paper addresses the issue of bank revenue diversification for an emerging country

with a specific regulation to encourage lending to small and medium enterprises, which

constrains the structure of bank assets. Using data with a detailed breakdown for a sample of

Philippine universal and commercial banks, we find that increased involvement in non-

interest activities is associated with higher profitability without affecting the volatility of bank

returns. For a specific type of Philippine banks, universal banks, increased diversification in

non-interest activities tends to lower risk. A closer investigation shows that the positive effect

on profitability is mainly driven by the expansion of trading activities and more specifically

by government securities that banks can purchase instead of directly granting loans to small

and medium enterprises. Moreover, our findings indicate that these activities tend to reduce

risk. Conversely, a higher involvement in underwriting activities in universal banks is

associated with higher risk. Our results are robust to various factors, model specifications, and

alternative diversification measures. Our findings highlight that regulation aiming to promote

lending to small and medium enterprises that banks can circumvent by acquiring specific

government securities, might have lowered their risk exposure.

JEL Classification: G21, G28

Keywords: Emerging economies; Bank Revenue Diversification; Bank Risk and Profitability

* Corresponding author. Tel: +33 555 149214; Fax: +33 555 149211.

Email addresses: [email protected] (C.Meslier), [email protected] (R. Tacneng) and

[email protected] (A. Tarazi)

Electronic copy available at: http://ssrn.com/abstract=1557010

2

1 Introduction

Over the last three decades, the financial industry in developed as well as in

developing countries has experienced major changes. Deregulation and increased competition

has led banks to expand their activities and to develop new lines of businesses beside their

traditional interest activities. Banks have diversified their income sources by performing new

activities, such as underwriting and trading securities, brokerage and investment banking and

other activities, which generate non-interest income. The implications of such changes on

bank performance, i.e. profitability and risk, have been broadly addressed in the literature but

no consensus has been reached at this stage. Most studies find that non-interest activities are

often associated with profitability gains but also higher risk because of their unstable nature.

By investigating the US banking industry, Stiroh (2004a and b), Stiroh (2006) and Stiroh and

Rumble (2006) find that a higher share of noninterest income positively affects the volatility

of bank returns inducing higher risk. Consistent with US studies, Lepetit et al. (2008a) show

that banks that are more reliant on non-interest activities exhibit higher default risk than banks

which mainly supply loans. This positive link mainly holds for small banks and is essentially

driven by commission and fee activities. Specifically, a higher share of trading activities is not

associated in their study with higher risk and for small banks it implies, in some cases, lower

asset and default risks. Mercieca et al. (2007) find that small European banks do not benefit

from diversification. Higher non-interest income shares are associated with lower profitability

and increased risk implying lower risk-adjusted profits. Furthermore, they find trading

activities to be both risky and unprofitable. Conversely, analyzing Italian banks, Chiorazzo et

al. (2008) find that income diversification improves the risk/return trade-off. Such

diversification gains are stronger for large banks.

Whereas the case of developed countries (US and Europe) is well documented in the

empirical literature, very few papers focus on emerging countries. In a cross-country study

conducted for a sample of listed banks from 11 emerging countries, Wolfe and Sanya (2011)

find that diversification between interest and non-interest activities as well as within both

types of activities increases risk-adjusted profitability and reduces bank insolvency risk.

Berger et al. (2010) examine the case of the Chinese banking industry and find evidence of a

diversification discount1, which is stronger for domestic banks than for foreign banks,

suggesting that different ownership structures induce different effects of diversification on

11

Their diversification discount indicators are profit premiums and cost discounts. They are measured as the difference between the

predicted profits (respectively the predicted cost) between the observed diversified bank and a hypothetical quasi-focused bank.

3

bank valuation. Focusing on the Mexican banking system, Maudos and Solis (2009) highlight

the existence of a negative relationship between banks' interest margin and non-interest

income. Their findings are consistent with the results obtained for European banks by Lepetit

et al. (2008b) indicating possible cross-subsidization of non-interest activities with traditional

intermediation activities, banks using loans as a loss leader.

The objective of this paper is to contribute to the scarce literature dedicated to the

impact of diversification on bank profitability and risk in the case of emerging and developing

countries. As financial markets are less mature in such countries than in developed countries,

banks play a crucial role in the financing of the private sector and specifically for small and

medium enterprises (SMEs). As discussed in the Financial Access 2010 Report provided by

the IFC (2010), access to finance by SMEs is one of the main policy issues for developing

countries and specific regulations encouraging banks to lend to priority sectors, including

SMEs, are implemented in some emerging countries like Afghanistan, India, the Philippines

and Pakistan. By imposing constraints on bank lending behavior, such regulations may

influence diversification strategies and could potentially shape the relationship between

diversification and bank performance (risk/profitability). Another important issue for

emerging and developing countries is the role of corporate ownership and governance in

affecting bank behavior. As reported by De Nicolo and Loukoianova (2007), two main trends

in bank ownership structure in emerging countries can be highlighted over the 1993-2004

period. While foreign ownership substantially increased, state-ownership remained stable and

still tends to increase in some group of countries. Several papers have investigated the effect

of a higher foreign presence in local banking markets. Foreign bank entry is generally found

to positively impact competition and, in some cases, improve the efficiency of the local

banking system (Claessens, Demirguc-Kunt, and Huizinga, (2001), Lensink and Hermes

(2003)). However, studies regarding credit availability provide mixed results. While for some

authors, foreign bank entry reduces credit constraints (Clarke et al. (2006)), others such as

Detragiache et al. (2008) and Gormley (2010) find that foreign bank entry does not

necessarily improve access to finance for local firms. Meanwhile, in terms of government

ownership of banks, an abundant theoretical literature stresses its negative effect in terms of

efficiency and risk (Shleifer (1998), Shleifer and Vishny (1998)).

In order to assess the bank diversification/profitability and risk nexus in emerging

countries, we focus on the case of the Philippines. We investigate the effect of diversification

between interest and non-interest activities as well as within non-interest activities using a

detailed breakdown of non-interest income of Philippine banks. Size as well as ownership

4

issues are taken into account as the Philippine banking system has experienced foreign bank

entry and is also characterized by the presence of some state-owned banks. Focusing on a

single country enables us to analyze the effect of diversification within a uniform

environment and to examine the diversification/performance relationship with regards to a

specific aspect of Philippine banking regulation. Indeed, Philippine banks are required to

grant at least six percent and two percent of their total loan portfolio to small and medium

enterprises, respectively. However, banks can comply with this rule by purchasing

government notes, securities and negotiable instruments offered by the Small Business

Guarantee and Finance Corporation (SBGFC)2. Therefore, a bank's decision to hold

government securities is not only driven by concerns for optimal diversification but also to

comply with bank regulation. To our knowledge, this is the first study on an emerging

economy that looks into this regulatory aspect3. This question is of particular interest for

emerging countries where small business lending is a crucial issue. Our study does not aim to

provide a direct assessment of the effect of such regulations for SMEs financing on bank

diversification behavior as data on individual bank loan portfolio disaggregated according to

the size of borrowing firms are not available. Nevertheless, it provides insights on the

potential impact of such regulations on the potential benefits or drawbacks of bank

diversification in terms of profitability and risk.

We conduct our empirical investigation over the 1999-2005 period using a sample of

39 universal and commercial banks in the Philippines with a very detailed breakdown of

annual data on income structure provided by the Central Bank of the Philippines. This allows

us to deeply analyze bank diversification behavior by examining the effect on profitability

and risk not only of the main components of non-interest income (fee-based, trading and other

non-interest income) but also by considering a detailed categorization of such components.

Estimations are conducted over different subsamples of banks categorized according to bank

size, differences in the involvement in non-interest activities, differences in bank asset

structure and ownership types. We also examine the effect of diversification for a specific

category of banks in the Philippines, Universal banks. In addition to the powers of a

commercial bank, Universal banks in the Philippines have investment house functions, which

include engagement in the underwriting of securities of other corporations4. In this regard, we

examine whether there are pronounced differences in the effects of diversification for such

2 Republic Act No. 6977, Section 13. Mandatory Allocation of Credit Resources of Small and Medium Enterprises.

3 Wolfe and Sanya (2011) find that a higher banking freedom and better investor protection are associated with higher profitability.

However, they do not explicitly explore the effect of such regulations on the risk implications of increased bank diversification. 4Republic Act 8791; Presidential Decree No. 129.

5

banks. In addition, we look closely on how income generated from activities that are related

to the additional function of universal banks affect their risk and profitability.

Our findings show that increased reliance on non-interest activities has a positive

influence on the profitability of Philippine banks and that this effect is stronger for banks with

a lower initial level of diversification. Moreover, in contrast with the results obtained in most

US and European studies, diversification does not affect the volatility of bank returns and, in

some cases, implies a reduction in default risk. We also find that diversification benefits more

the smaller banks and foreign banks. The positive effect on profitability is mainly driven by

higher reliance on trading income and more specifically government securities‟ trading.

However, a closer look shows that such a result only holds for banks, which presumably

purchase government securities to comply with the mandatory credit allocation to SMEs

instead of directly lending to them. Finally, the investigation conducted on the sub-sample of

universal banks shows that a higher involvement in investment house activities is associated

with higher risk.

The remainder of the paper is organized as follows. Section 2 discusses the data and

variables used in our study and presents recent trends in the income structure of the Philippine

banking industry. Section 3 describes the hypotheses tested, the method and the econometric

specifications. Section 4 provides the results of our estimations while section 5 reports

robustness checks and discusses further issues. Section 6 summarizes the findings and

concludes the paper.

2. Data and Variables, Descriptive Statistics and Trends in the Philippine Banking

Industry

2.1 Data Collection and Sample Selection

The Philippine banking industry has introduced universal banking in 1980 and has

become increasingly diversified over the last two decades in terms of its revenue-generating

activities. Growing competition over the period in the Philippine banking market has provided

incentives for commercial banks to diversify their activities and to increase the share of non-

interest activities (Gochoco-Bautista (1999)). Banks have been providing a broader array of

financial services, which include not only the extension of loans but also underwriting and

distributing securities, sale of investments, online banking and commission and fee activities5.

5 Over the past twenty years, noninterest income has grown over 700% (200% more than the growth rate in interest income).

6

In the Philippines, banks are classified in six main categories6: universal banks, commercial

banks, thrift and savings banks, rural banks, cooperative banks and Islamic banks. In 2005,

universal and commercial banks alone comprise 89.29%, 89.47% and 90%7 of the total assets,

deposit liabilities and loans and investments outstanding, respectively of the entire Philippine

banking system. Universal banks have the authority to exercise, in addition to the functions

authorized for a commercial bank8, the powers of an investment house

9. These figures show

that universal and commercial banks are the primary lenders to both households and

institutions in the country. Their behavior generally shapes that of the banking system and

impacts the economy. The sample used in this study includes 39 universal and commercial

banks. We construct our sample using two criteria: (1) banks must have at least data for three

years and, (2) the gross income components must be non-negative. The first criterion is set in

order to confine the panel regressions on banks with sufficient number of observations.

Meanwhile, the second criterion ensures that the diversification measures, particularly the

indices and income shares are bounded from 0 to 1. We also apply several measures to check

the presence of outliers and influential observations10

. We also exclude banks that merged

and/or were acquired during the period. We hence end up with an unbalanced panel consisting

of 39 banks and 218 observations.

Our sample of banks represents 86.81%11

of the Philippine banking system and 96.3%

of the universal and commercial banking system in terms of total assets. 12

The whole sample consists of 23 domestic and 16 foreign banks13

, and 16 listed and

23 non-listed entities. In terms of asset size, we identify 8 large banks (Average Asset > 140

billion pesos), 13 medium-sized (30 billion pesos < Average Asset < 120 billion pesos) and

6 The General Banking Law of 2000 (Republic Act No. 8791). 7 Author‟s computations from the Banking Statistics published in the Bangko Sentral ng Pilipinas website. 8 Article II- Operations of Commercial Banks (Republic Act No.8791). A commercial bank shall have, in addition to the general powers

incident to corporations, all such powers as may be necessary to carry on the business of commercial banking, such as accepting drafts and

issuing letters of credit; discounting and negotiating pormissory notes, drafts, bills of exchange, and other evidence of debt; accepting or creating demand deposits; receiving other types of deposits and deposit substitutes; buying and selling foreing exchange and gold or silver

bullion; acquiring marketable bonds and other debt securities; and extending credit, subject to such rules as the Monetary Board may

promulgate. 9 From the Omnibus Rules and Regulations for Investment Houses and Universal banks registered as underwriters of securities, an

investment house is defined as any enterprise which primarily engages, whether regularly or on an isolated basis, in underwriting securities of another person or enterprise, including securities of the Government or its instrumentalities. 10 Aside from graphically looking at box plots and scatter plots to identify outliers, we confirm these outliers by computing the DFBETA and

leverage measures after the estimations. The DFBETA measures the distance that a regression coefficient would shift when an observation is

included or excluded from the regression, scaled by the estimated standard error of the coefficient (Baum, 2006). 11 Mean over the period of the study 12 In 1999, there are a total of 46 universal and commercial banks, and in 2005, 41 universal and commercial banks. 13 Banks are classified as foreign if: 1) they are subsidiaries of foreign banks, or 2) branches of foreign banks. This classification is mainly

drawn from the Monetary Board‟s authorized mode of entry (Sec. 2, Republic Act NO. 7721) of foreign banks to operate in the Philippine

banking system. Sec. 2. Modes of Entry – The Monetary Board may authorize foreign banks to operate in the Philippine banking system

through any of the following modes of entry: (i) by acquiring, purchasing or owning up to sixty percent (60%) of the voting stock of an existing bank; (ii) by investing in up to sixty percent (60%) of the voting stock of a new banking subsidiary incorporated under the laws of

the Philippines; or (iii) by establishing branches with full banking authority: provided, that a foreign bank may avail itself of only one(1)

domestic bank of new banking subsidiary. (Republic Act NO. 7721, An Act Liberalizing the Entry and Scope of Operations of Foreign Banks in the Philippines and for other purposes).

7

18 small ones (Average Asset < 30 billion pesos). Bank classifications in terms of size are

defined from an examination of the distribution of banks both in terms of their average assets

over the period of the study (1999-2005) and bank asset distribution by their yearly amounts.

We note that most of the smaller banks in the sample are foreign-owned, branches or

subsidiaries of foreign banks and that the largest banks are dominantly domestic banks.

Among the 8 large banks, 2 are government banks. Excluding the state banks, our sample of

domestic banks is composed of 12 universal banks and 9 commercial banks. The sample

description is summarized in Table 1.

[Insert Table 1]

Balance sheet and net income information are obtained from the Data Center of the

Bangko Sentral ng Pilipinas and its website on an annual basis14

. Moreover, among this

sample, 20 banks also provide quarterly data. We note that most of them are domestic banks

(18 out of 20); 6 are large, 10 are medium-sized and 4 are small. Meanwhile, 15 are listed and

5 non listed, of which 10 among the listed banks are universal banks. These 20 banks

represent 64% of the total banking system and 71% of the total universal and commercial

banking system in terms of total assets. These data are obtained from the Securities and

Exchange Commission.

For the whole sample of banks, the Central Bank of the Philippines also provides us a

detailed breakdown of operating income and its components. This enables us to carry out an

in depth study on noninterest income, its main components – fee-based, trading and other

noninterest income, and their respective disaggregation. Fee-based and trading activities

include respectively bank commissions, service charges/fees and other commissions and

income from trading government securities, private equity/debt; financial futures, forwards

and swaps; profit from the sale of investments; and profit from foreign exchange.

For the listed banks of our sample, daily market data for stock prices are obtained

from Datastream International.

2.2 Main trends in portfolio structure and income structure in the Philippine banking

system

14 www.bsp.gov.ph

8

Tables 2A and 2B highlight significant differences of income structure according to

bank size (large, medium and small), bank type (universal and commercial banks) and

ownership type (foreign and domestic).

[Insert Tables 2A and 2B]

Over the 1999-2005 sample period, the share of non-interest income in total operating

income is, on average, equal to 35.92%. Most of the non-interest income is drawn from

trading activities (45.30%) compared to fee-based activities (38%). Trading in government

securities and foreign exchange profit are the largest source of trading income (30.60% and

51.50%), while service charges dominate the fee-based income sources (61.40%). We can

observe different profiles of diversification and non-interest income structure according to the

size and ownership structure of the bank. Larger banks present a higher level of non-interest

income in total operating income (38.16 % for large banks and 39% for medium-sized banks)

than small banks (32.22%). However, the difference between large and medium-sized banks

becomes more pronounced when we exclude state banks. On average, the larger is the bank,

the higher is its non-interest income share. On the other hand, the degree of involvement in

non-interest activities is similar in domestic banks and foreign banks which operate in the

Philippines. Trading income represents the main source of non-interest income for large

banks (41.30%), medium-sized banks (47.20%) and small banks (46%). Fee-based activities

have a slightly higher share compared to trading activities when state banks are excluded from

the sample of large banks. Within trading activities, foreign exchange profit and trading of

government securities are the two main sources of income for all types of banks. However,

whereas foreign exchange profit represents the main component for large and small banks

(38.50% and 67.60%), trading of government securities is the main source of trading activities

for medium-sized banks (43.10%). For foreign banks, fee-based activities represent the main

source of non-interest income (47.70%), followed by trading activities (40.80%). For these

banks, foreign exchange profit is the main source of revenue in trading activities (74.70%).

On the contrary, domestic banks are more involved in trading activities (47.80%), of which

government securities trading is the largest component (41.90%). Marked differences are also

observed between universal and commercial banks. Universal banks have higher shares of

non-interest income compared to commercial banks (39.38% and 34.62%). In addition,

commercial banks have higher shares on both fee-based and trading income but universal

banks present a higher involvement in other non-interest activities.

9

Philippine banks exhibit higher levels of involvement in non-interest activities than

those reported in Wolfe and Sanya (2011) for their set of emerging countries and similar

levels of involvement in non-interest income activities in comparison with those reported in

US and European studies. Whereas, differences in accounting standards do not allow us to

compare the different sources of non-interest income among countries, the relatively high

involvement in trading activities for Philippine banks has to be stressed. The existence of a

specific regulatory framework which constrains Philippine banks‟ asset structure raises the

question of the influence of such a regulation on bank diversification behavior and its

consequences on profitability and risk.

2.3 Definition of variables

2.3.1 Diversification measures

In this study, three sets of diversification indicators are computed and alternatively

used to assess the effect of the increased diversification of Philippine banks on their

profitability and risk.

A first set of indicators used in this study consists of ratios which represent the share

of non-interest income in total operating income, as well as the shares of each component of

non-interest income in total operating income. The variable NII is equal to the percentage

share of non-interest income to total operating income, where non-interest income15

is the

sum of fee-based income, trading income and other noninterest income. We use the gross

values because there is no categorical expense attributed to these activities alone in the

income statement provided in our data. In addition, the reported non-interest expense is

independent of the non-interest income. The variable NII is then computed as follows:

NII = Non-interest Income/Total Operating Income (1)

where Non-interest Income = Fee-based Income + Trading Income + Other Non-interest

Income, and Total Operating Income = Non-interest Income + Interest Income – Interest

Expense

15

The definition of the non-interest income accounts are shown in the Appendix 1.

10

We also disaggregate NII into three components – FEE, TRAD and Other. These

variables are computed as follows:

FEE = Fee-based income/Total Operating Income (2)

TRAD = Trading income/Total Operating Income (3)

Other = Other income/Total Operating Income (4)

Where Fee-based income16

= Bank commissions + service charges/fees + other

fees/commissions and Trading income = Trading gains/(losses) (from government securities,

private debt/equity securities, and financial futures, options) + Foreign exchange

profits/(losses)+Gold trading gains/(losses) + Profit/(loss) on sale of redemption of

investments.

For the components of non-interest income, we draw the definition of our variables

from the Bangko Sentral ng Pilipinas‟ glossary of terms (BSP website17

). Our definition of

total operating income is consistent with the studies of Stiroh (2004b), Stiroh and Rumble

(2006) and Chiorazzo et al. (2008).

A second set of indicators used in this paper, FOCUSk, consists of Herfindahl indexes

which indicate the degree of bank focus/specialization in its revenue generating activities. As

in Chiorazzo et al. (2008), Stiroh and Rumble (2006) and Wolfe and Sanya (2011), the indices

measure how focused or specialized a bank is on its income generating activities. We

compute them as follows:

Let j

i,tX be the nominal exposure of bank i at time t to activity j where j = 1,....,n. j

i,tx

denotes the corresponding relative exposure, i.e.

j

i,tj

i,tj

i,t

1

Xx

Xn

j

(5)

16

The definition of the different components of non-interest income are drawn from the Bangko Sentral ng Pilipinas‟ glossary of terms,

which can be found in the BSP website, www.bsp.gov.ph/banking/glossary.asp

11

2

j j

i,t i,t

1

FOCUSk xn

j

(6)

where k = 1,…, 4.

FOCUSk is an index equal to 1 when total income is generated from one source

(specialized) and 1

n when exposures to each income component are equal (well-diversified).

A lower value of the index indicates that a bank is more diversified. The subscript „k‟ denotes

the level of disaggregation of operating income (FOCUS1), or of non-interest income

(FOCUS2) and its components (FOCUS3 and FOCUS4) used to compute the indicator. Our

first index, FOCUS1 is based on the disaggregation of the operating income – net interest

income and non-interest income. The three other indices we use, FOCUS2, FOCUS3 and

FOCUS418

, are based on the disaggregation of non-interest income, fee-based income and

trading income, respectively.

We note, however, that FOCUS1 has an important shortcoming. Because the index

predicts the same degree of focus for banks that are more reliant on interest income, and for

those that are more oriented towards non-interest income. For example, FOCUS1 predicts the

same degree of focus for a bank that holds 70% interest income and a bank that holds 70%

non-interest income. Thus this index does not allow us to differentiate on which activities the

bank is focused into.

To overcome this problem, a third indicator, FOCUSDIV, is computed. We interact

FOCUS1 with a dummy variable, DIV1, which is equal to 1 if the share of non-interest

income is higher than 50% and zero, otherwise. DIV1 is interacted with FOCUS1 to

investigate whether it pays to be more focused on non-interest activities compared to interest

generating ones. We also enter both FOCUS1 and DIV1 simultaneously in the estimations.

18 FOCUS2 = (share of interest income to total operating income)^2+(share of fee-based income to total operating income)^2+(share of

trading income to total operating income)^2+(share of other noninterest income to total operating income)^2

FOCUS3 = (share of interest income to total operating income)^2+(share of bank commissions to total operating income)^2+(share of

service charges to total operating income)^2+(share of other commissions/fees to total operating income)^2+(share of trading income to total

operating income)^2+(share of other noninterest income to total operating income)^2

FOCUS4 = (share of interest income to total operating income)^2+(share of fee-based income to total operating income)^2+(share of trading gain from government securities to total operating income)^2+(share of trading gain from private debt/equity to total operating

income)^2+(share of trading gain from financial futures to total operating income)^2+(share of foreign exchange profit to total operating

income)^2+(share of profit from sale of redemption of investments to total operating income)^2+(share of other non-interest income to total operating income)^2

12

2.3.2 Bank Profitability and Performance Measures

To measure the profitability of a bank, we use bank income statement ratios – the

return on average assets (ROA) and the return on average equity (ROE):

it

NetIncomeAfterTaxROA =

AverageAsset

(7)

it

NetIncomeAfterTaxROE =

AverageEquity

(8)

We also construct two types of risk-adjusted profitability measures according to data

availability. First, from the sample of 20 banks for which quarterly data are available, we

calculate the risk-adjusted return measures as the ratio of the average ROA (respectively

ROE) to its standard deviation by using rolling windows of eight quarters19

:

it

it

it

ROAADJROA =

ζROA (9)

it

it

it

ROEADJROE =

ζROE (10)

Second, following Chiorrazo et al. (2008), we also compute risk-adjusted profitability

measures, defined as the ratio of annual ROA (respectively ROE) to the standard deviation of

each bank over the period of study, 1999-2005.

itit

i

ROASHROA =

ζROA

(11)

itit

i

ROESHROE =

ζROE (12)

2.3.3 Bank Risk Measures

Different types of risk taking and default risk measures are computed according to

data availability.

For the sub-sample of 20 banks for which quarterly data are available, two standard

measures of risk based on quarterly accounting data are used in our study. We consider the

volatility of returns, which is measured by (i) the standard deviation of the return on average

assets (SDROA) and (ii) the standard deviation of the return on average equity (SDROE),

(SDROA and SDROE) as proxies for risk taking.

19

The rolling windows cover for year t, the last two quarters of year t-1, the four quarters of year t and the first two quarters of year t+1.

13

For the 16 listed banks in our sample, we also compute risk and insolvency measures

using market data obtained from DataStream International. There are a total of 16 listed banks

in our sample; however, sufficient data are only available for 15 banks. We compute risk-

taking measures such as i) the market model beta (Beta)20

coefficient estimated through a

GARCH model measuring systematic risk, ii) total risk (TotRisk), which is the standard

deviation of weekly returns21

and iii) specific risk (RiskSpec)22

, which is the standard

deviation of the market model residual. We also compute a default risk measure using a

market-data-based Z-score (MZ)23

. This measure represents the number of standard deviations

below the mean by which profits would have to fall to deplete equity capital (Boyd et al

(1993).

3. Hypotheses Tested and Methodology

The objective of this study is to examine how diversification between interest and

non-interest activities as well as within non-interest activities may affect bank profitability

and risk. We also aim to assess whether a specific banking regulation on Philippine bank

portfolios is likely to shape the diversification behavior of Philippine commercial banks. We

conduct a detailed analysis by examining differences in the effect of diversification according

to bank size, the initial level of diversification and ownership type.

For some authors (Stiroh (2004a), Lepetit et al. (2008) and Mercieca et al. (2007)), the

shift towards non-interest activities for small banks tends to worsen their risk/return trade-off

and/or increase their riskiness. Mercieca et al. (2007) explain this result by a lack of expertise

of small banks in these new lines of businesses. However, according to Chiorrazo et al.

(2008), small banks with very low share of non-interest income may benefit from increased

diversification in such activities. The influence of ownership structure is stressed by Berger et

al. (2010). According to the authors, the diversification discount highlighted for Chinese

banks could be attributed to inefficient incentive schemes and/or to the lack of expertise of

local top managers who are appointed by the government. Moreover, their results indicate that

for banks with foreign presence, the diversification discount is smaller. The mitigating effect

20 We estimate the single index market model over the period [t-100, t] to calculate the value of the beta at date t. 21 Daily stock prices are used to calculate weekly stock returns. The standard deviation of weekly stock returns at date t is computed over the

period [t-100, t]. 22 The single index market model is computed for each trading day over the period [t-100, t]. We use the standard deviation of residuals to

estimate specific risk at date t.

23 R+1

MZ = ζ

where R is the mean of the weekly returns Rt for a given year and ζ is the standard deviation of weekly returns.

14

of foreign ownership is attributed to better managerial expertise and increased monitoring of

bank activities. Focusing on the effect of foreign entry in the Philippine banking industry over

the 1990-1998 period, Unite and Sullivan (2003) show that foreign entry was associated with

an improvement of operating efficiency, a reduction in interest rate spreads and profits,

meaning an increased competition. However, the authors also highlight a deterioration of

bank loan portfolio quality reflected by an increase in loan loss provisions.

The set of regressions we estimate can be summarized by the following general

specification:

it it 1 it 2 it it itY = α + β FOCUSk + β NonInterestIncome + δZ + ε

(13)

where Yit is either a measure of profitability, risk-adjusted profitability or risk ; FOCUSkit is

the measure of diversification ; NonInterestIncomeit is either the share of non-interest income,

its components or their disaggregation; Zit are control variables and αit is a constant.

We use the following control variables – Assets, Growth, Equity, Loans in all our

models.

Assets, is the mean of the natural logarithm of bank assets adjusted to the GDP

deflator. This variable, following Chiorazzo et al. (2008), Behr et al. (2007), Stiroh and

Rumble (2006), and Stiroh (2004a, 2004b) captures the effects of bank size to returns and

risk. Larger-sized banks are able to invest in more advanced technologies and generally, have

better risk management. They are also able to expand into other business lines. We therefore

expect a positive sign on the relationship between assets and profits and negative between

asset and risk.

Growth, is the growth rate of total assets. As in Stiroh (2004b) and Chiorazzo et al.

(2008), we use this variable as a proxy for bank manager‟s preference for risk taking. Banks

with lower risk aversion grow more rapidly and thus, have different operating strategies.

Moreover, it may also be interpreted as control for growth-by-acquisition.

Equity, is the leverage ratio computed as the ratio of total capital to total assets. Banks

that hold a lower level of equity in their asset-liability portfolio tend to be riskier. A higher

level of capital then translates to the bank manager‟s risk aversion. This control variable is

also used by several bank diversification studies (Chiorazzo et al., 2008, Stiroh, 2004b).

15

Loans, is the ratio of total loans to total assets. Consistent with Chiorazzo et al. (2008),

Stiroh and Rumble (2006) and DeYoung and Roland (2001), this variable captures the

performance of bank‟s lending strategies relative to its other earning assets.

We run two-way fixed-effects panel regressions to estimate our models. In performing

these estimations, we check for the appropriateness of our estimation method using the

Hausman test to check whether a fixed effects model is more appropriate than a random

effects model. In addition, we use a Huber/White estimator of variance that is robust to some

types of misspecifications along with the fixed effects model.

Since the alternative dependent variables we use, particularly profitability, show the

tendency to persist in time24

, reflecting impediments to competition, informational

asymmetry, and change in business strategies, we consider that their previous values could

partially determine their current values (Berger et al., 2000). We therefore also estimate our

equations using a dynamic model using the methodology proposed by Arellano and Bover

(1995) and Blundell and Bond (1998). In this approach, the system of equations is estimated

in both first-differences and levels. The two step GMM estimator is used to provide a more

robust inference from the results. However, we also use the one-step estimator25

. Since we are

considering a small sample, the two step standard errors are computed to conform to

Windmeijer‟s (2005) finite-sample correction. We also take into account the possibility that

the explanatory variables might not be strictly exogenous, which is presumably the case of the

non-interest income variables. Following Maudos and Solis (2009), to address this

endogeneity problem, the lagged levels and lagged differences of the explanatory variables

are used as instruments. To determine the consistency of the estimators and verify the validity

of the instruments, we use a Sargan test of over identifying restrictions. Meanwhile, we also

check for the appropriateness of using the Blundell dynamic panel data estimation technique

using the statistic proposed by Arellano and Bond (1991) to test the absence of second-order

serial correlation of the first difference residuals.

Each hypothesis is tested using fixed effects and dynamic panel data estimation on

two alternative specifications, one which includes the variable FOCUSk and another which

does not.

Based on the general specification provided by equation (13), we test the three

following hypotheses: 24 In the banking literature, few studies consider profits to be persistent (Levonian, 1993; Roland, 1997; Eichengreen and Gibson, 2001;

Goddard et al., 2004 ) 25

Results using one-step estimators are not reported but are available from the authors on request.

16

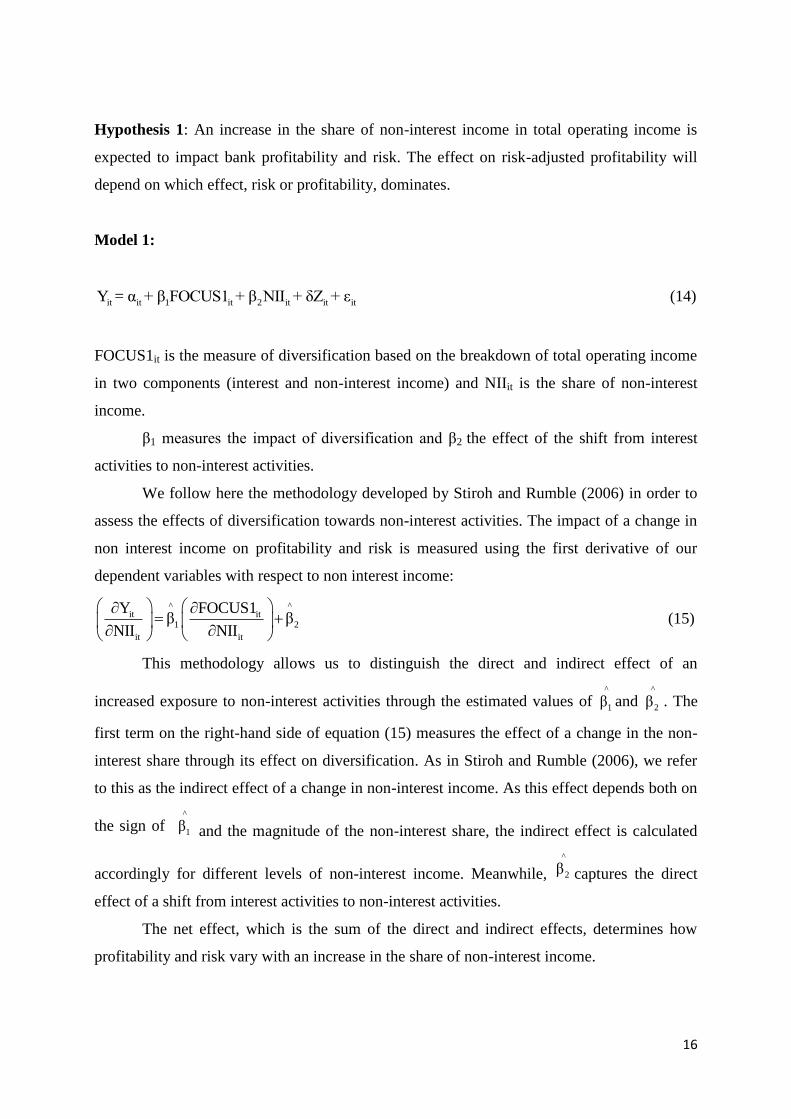

Hypothesis 1: An increase in the share of non-interest income in total operating income is

expected to impact bank profitability and risk. The effect on risk-adjusted profitability will

depend on which effect, risk or profitability, dominates.

Model 1:

it it 1 it 2 it it itY = α + β FOCUS1 + β NII + δZ + ε (14)

FOCUS1it is the measure of diversification based on the breakdown of total operating income

in two components (interest and non-interest income) and NIIit is the share of non-interest

income.

β1 measures the impact of diversification and β2 the effect of the shift from interest

activities to non-interest activities.

We follow here the methodology developed by Stiroh and Rumble (2006) in order to

assess the effects of diversification towards non-interest activities. The impact of a change in

non interest income on profitability and risk is measured using the first derivative of our

dependent variables with respect to non interest income:

^ ^it it

1 2

it it

Y FOCUS1β β

NII NII

(15)

This methodology allows us to distinguish the direct and indirect effect of an

increased exposure to non-interest activities through the estimated values of ^

1β and ^

2β . The

first term on the right-hand side of equation (15) measures the effect of a change in the non-

interest share through its effect on diversification. As in Stiroh and Rumble (2006), we refer

to this as the indirect effect of a change in non-interest income. As this effect depends both on

the sign of ^

1β and the magnitude of the non-interest share, the indirect effect is calculated

accordingly for different levels of non-interest income. Meanwhile,

^

2β captures the direct

effect of a shift from interest activities to non-interest activities.

The net effect, which is the sum of the direct and indirect effects, determines how

profitability and risk vary with an increase in the share of non-interest income.

17

The dependence however between ^

1β and ^

2β raises econometric issues since NII and

FOCUS1 are collinear. Although both estimates may be unbiased, their variance and

covariance are overestimated (Chiorazzo et al. 2008). Wald tests need to be conducted to

check the joint statistical significance of ^

1β and ^

2β in the various estimations. Moreover, we

also estimate the equation by using only NII to check for robustness.

In order to assess the effect of differences in size, the initial level of diversification in

terms of NII and ownership type, three different specifications of Hypothesis 1 are tested:

Hypothesis 1a: Diversification has a stronger/weaker impact on profitability and risk for

small banks compared to larger banks.

In testing Hypothesis 1a, we estimate Model 1 on sub-samples of large, medium and small-

sized banks and alternatively introduce an interaction term NII*ASSET, which is the product

of the diversification variable and the log of total assets.

Hypothesis 1b: Diversification has a stronger/weaker impact on bank profitability and risk

for banks that are already more diversified in terms of non-interest activities.

In order to assess how the direct and indirect effects differ for different levels of our variables,

we estimate Model 1 at different values of the average non-interest income share (10th, 25th,

50th, 75th and 90th percentiles) and bank size. We also separately interact NII with dummy

variables P25 and P75, which indicate the percentile levels of banks relative to the whole

sample. P25 is equal to 1 if a bank is below the 25th percentile in terms of the average value

of NII, and zero otherwise ; P75 is equal to 1 if a bank is above the 75th percentile of average

NII, and zero otherwise.

Hypothesis 1c: Diversification has a stronger/weaker impact on profitability and risk

according to bank ownership type

In testing Hypothesis 1c, we estimate Model 1 on two sub-samples, one which includes

domestic banks and the other on foreign banks.

18

To go further in the analysis of the effect of the shift towards non-interest activities,

we examine the effect of the different components of non-interest income - fee-based, trading

and other income and their respective disaggregation. This enables us to assess whether or not

different product mixes within non-interest activities have similar effects on profitability and

risk. More specifically, we address two main questions.

We first examine whether correlations between interest income growth and the growth

of the different components of non-interest income might affect the impact of diversification

on banks‟ profitability and risk. As pointed by Stiroh (2004b), the existence of a positive

correlation between interest and non-interest income could be due to cross-selling behavior

and might reduce diversification benefits. The absence of a significant correlation between

growth rates would imply that a bank is engaging inefficient diversification. This could

increase profitability. However, it may also increase risk because of the bank‟s lack of

expertise in modern banking activities. Some papers argue that banks benefit from an increase

in diversification as long as income components are imperfectly correlated (Busch and Kick,

2009). Stiroh (2004a) finds that as the growth rates of net interest and net non-interest income

become increasingly correlated the benefits from diversification decrease. Lepetit et al. (2008)

find that higher reliance on non-interest activities is associated with higher risk but that higher

risk is generated by commission and fee activities rather than trading activities.

Second, we address a specific issue related to the Philippine banking regulation. As

stipulated in the RA 697726

, otherwise known as the Magna Carta for Small Enterprises, all

lending institutions, such as banks are mandated to set aside at least six percent (6%) and at

least two percent (2%) of their total loan portfolio to small and medium enterprises (SMEs),

respectively. This requirement could influence bank asset allocation and in effect their

diversification strategies, as banks can comply with this regulation by acquiring instead

government securities offered by the Small Business Guarantee and Finance Corporation27

.

As highlighted in the literature (Berger and Udell, 2006), small business lending tends to rely

more on relationship lending where banks have to gather soft information. Large banks are

then less likely to be involved in relationship lending and tend to lend more to large firms.

Moreover, foreign banks which do not have the specific knowledge of local domestic markets

26 Republic Act No. 6977 (later amended by Republic Act No. 8929)– An act to promote, develop and assist small and medium scale

enterprises through the creation if a Small and Medium Enterprise Development (SMED) Coucil, and the rationalization of government

assistance, programs and agencies concerned with the development of Small and Medium Enterprises, and for other purposes. It was later amended by Republic Act No. 9501 in 2008 to increase the percentage set aside for small enterprises from six percent (6%) to eight percent

(8%). 27 This organization is now known as the Small Business Corporation.

19

could be disadvantaged in collecting soft information. For these reasons, large banks and

foreign banks in the Philippines could have stronger incentives to comply with the

aforementioned regulation by buying government securities instead of directly granting loans

to small firms. As the detailed breakdown of bank loan portfolio according to firm size is

neither available at the individual level nor for the banking industry in the Philippines as a

whole, we base our investigation on the share of government securities held by banks in their

portfolio. We combine the information provided by two ratios28

: the ratio of government

securities to total assets and the ratio of government securities to total loans. As bank

government securities holding could be motivated either by bank diversification strategy or to

comply with regulation, information provided from the ratio of government securities to total

assets cannot be considered as a pure indicator of whether or not banks comply with the

aforementioned regulation by holding government securities. However, we presume that

banks which exhibit a relatively low share of government securities in terms of total assets do

not need to hold government securities for regulatory purposes because they provide

sufficient amounts of loans to small and medium-sized firms. Conversely, a relatively high

share of government securities in total assets could indicate that banks are purchasing

government securities to limit their lending to small and medium-sized firms. Considering the

ratio of government securities to total loans, we conjecture that banks with such a ratio greater

than 8% purchase government securities in lieu of lending to SMEs. As highlighted in Table

3A and 3B, government securities‟ holding strongly differs according to ownership type and

bank size. Foreign banks exhibit a larger share of government securities in total assets than

domestic banks (5.22% for foreign banks in comparison with 1.98% for domestic banks). On

the other hand, large banks present a smaller share of government securities in total assets

(1.55%) compared with smaller banks (3.62% for both medium-sized and small banks).

Majority of the considered small banks, however, are foreign banks. In our investigation, we

consider the lower (25th

) and upper (90th

) percentiles in order to distinguish banks which hold

respectively relatively small and large amounts of government securities in % of total assets.

Banks that belong to the 25th

percentile hold government securities over total loans on the

average, equal to 0.1%, which comprises banks that barely hold government securities. On the

other hand, banks belonging to the 90th

percentile hold on the average, 35.02% of government

securities over total loans, which is way above the 8% required alternative compliance of

combined allocation for both small and medium enterprises. We construct three dummy

28 We use the ratio of government securities to total assets and the ratio of government securities to total loans averaged over the time period

for each bank.

20

variables, two which are based on the ratio of government securities to total assets,

COMP_LEND and COMP_GOVSEC and one which is based on the ratio of government

securities to total loans, COMP_GOVSEC2. COMP_LEND takes the value of 1 if the ratio of

government securities to total assets is lower than the 25th

percentile and the value of 0,

otherwise. This variable corresponds to banks, which do not need to hold government

securities to comply with the obligation of lending to SMEs. COMP_GOVSEC is equal to 1 if

the ratio of government securities to total assets is higher than the 90th

percentile and

otherwise, 0. This variable represents banks that limit their lending to SMEs, hence the need

to purchase government securities. COMP_GOVSEC2 is a dummy variable that is equal to 1

if the ratio of government securities over total loans is greater than 8%, and 0, otherwise. This

variable characterizes banks that do probably not lend enough to SMEs and in lieu, hold

government securities. Banks with a ratio of government securities over total loans less than

8%, on the other hand, are those that lend to SMEs.

Hypothesis 2: Different product mixes within non-interest activities will differently affect

profitability and risk. Specifically the holding of government securities to comply with

regulation on lending to small and medium-sized firms will alter the relationship between

diversification and profitability/risk.

This hypothesis will be first tested by using a three-level breakdown of noninterest

activities (Model 2a and Model 2a‟).

Model 2a:

it it 1 it 2 it 3 it 4 it it itY = α + β FOCUS2 + β FEE + β TRAD + β Other + Z + ε (16)

FOCUS2it is the measure of diversification based on the breakdown of non-interest income in

three components (fee-based, trading and other incomes); FEEit, TRADit and Otherit are the

shares of fee-based income, trading income and other noninterest income, respectively, in

total operating income.

21

Model 2a’:

it it 1 it 2 it 3 it 4 it 2 it 3 it 4 it it itY = α + β FOCUS2 + β FEE + β TRAD + β Other + FEECompliance + TRADCompliance + OtherCompliance + Z + ε

(17)

Where Compliance is either COMP_LEND, COMP_GOVSEC or COMP_GOVSEC2.

FEECompliance, TRADCompliance and OtherCompliance are interaction terms between the

diversification measures and our proxies to distinguish banks that comply with regulation by

holding government securities from those that are purchasing such securities simply to freely

diversify their portfolios. These interaction terms capture the influence of regulation on the

impact of diversification on profitability and risk-adjusted profitability.

Availability of a more detailed breakdown within fee-based and trading activities

allows us to go further and to assess, within each category, whether some sources play an

important role in the link between diversification and bank risk/profitability (Model 2b and

2b‟)29

.

Model 2b:

it it 1 it 21 it 22 it 23 it 3 it 4 it it itY = α + β FOCUS3 + β BC + β SC + β OC + β TRAD + β Other + Z + ε (18)

Model 2b’:

it it 1 2 it 31 it 32 it 33 it 34 it 35 it 4 it it itY α β FOCUS4 β FEE β GS β PD β FF β PI β FP β Other Z εit (19)

FOCUS3it and FOCUS4it are measures of diversification within respectively detailed fee-

based and trading incomes; BCit, SCit and OCit are the three components of fee-based

activities and represent the shares of respectively bank commissions, service charges and

other commissions in total operating income. GSit, PDit, FFit, PIit and FPit are the five

components of trading activities and represent the shares of respectively government

29 We do not estimate model 2a‟ with a more detailed breakdown because it lowers significantly the degrees of freedom of the estimated

model.

22

securities trading gains (losses), private debt trading gains (losses), financial futures gains

(losses), profit from investment and foreign exchange profits in total operating income.

Further differences in the diversification effect of Philippine banks into non-interest

activities are analyzed by examining the specific case of universal banks, which unlike

commercial banks, are allowed to perform the activities of investment houses (RA 879130

, PD

12931

). Following existing studies (Bhargava and Fraser (1998), Akhigbe and Whyte (2004),

Cornett, Ors and Tehranian (2002)) which examine the effects of various regulations that

pertain to bank expansion into investment banking activities, our aim here is to assess the risk

implications of diversifying into such specific non-interest activities. We investigate the

effects of the disaggregated shares of non-interest income (fee-based, trading and other non-

interest income) and their components on the risk of universal banks and focus more

particularly on the effect of increased shares in "other commissions/fees" (a component of

fee-based income), which are commission and fees collected for investment house activities

such as underwriting, securities dealership and equity investments.

The expanded investment opportunity profile of universal banks may result in

enhanced diversification, implying lower risk. On the other hand, risk may actually increase

as banks expand into new activities because the securities business is inherently more risky

than traditional banking activities (Geyfman, 2005).

Hypothesis 3: Increased engagement in security underwriting activities will affect risk for

universal banks.

Model 3

it it 1 it 21 it 22 it 23 it 3 it 4 it it itY = α + β FOCUS3 + β BC + β SC + β OC +β TRAD + β Other + Z + ε (20)

it it 1 it 2 it 31 it 32 it 33 it 34 it 35 it 4 it it itY =α +β FOCUS4 +β FEE +β GS +β PD +β FF +β PI +β FP +β Other + Z + ε (21)

30

Republic Act No. 8791. An Act Providing For the Regulation of the Organization and Operations of Banks, Quasi-Banks, Trust Entities

and for Other Purposes. Artcile 1, Section 23. Powers of a Universal Bank. – A universal bank shall have the authority to exercise, in

addition to the powers authorized for a commercial bank, the powers of an investment hourse as provided in existing laws and the power to invest in non-allied enterprises. 31 Presidential Decree No. 129. The Investment Houses Law. Section 2. Definitions: A) Investment House is any enterprise which primarily

engages, whether regularly or on an isolated basis, in the underwriting of securities of another person or enterprise, including securities of the Government or its instrumentalities.

23

4. Estimation Results

4.1 Non-interest activities affect both bank profitability and risk

The first hypothesis aims to analyze the link between diversification and profitability

and risk. The findings, reported in Table 4A, indicate that increased reliance on non-interest

activities has a positive effect on profitability (columns 1, 5, 9, 11, 13 and 15)32

. Moreover,

we find a negative and significant effect of the variable FOCUS133

using dynamic panel data

estimation (columns 9 to 12), indicating a positive effect of increased diversification on

profitability. On average, increased diversification in non-interest activities improves the

profitability of Philippine banks. We also show that an increase in the share of non-interest

income does not affect the volatility of bank returns (columns 4 and 8). However, results

regarding risk-adjusted profitability are mixed. We obtain a positive and significant effect of

an increased reliance on non-interest activities on risk adjusted return, only when using the

indicator suggested in Chiorazzo et al. (2008), (columns 3, 7, 10, 12, 14, and 16). Estimates of

the direct, indirect and net effect of an increased exposure to non-interest activities evaluated

at the 10th, 25th, 50th, 75th and 90th percentiles show that the net effect on profitability and

risk adjusted return is positive and in most cases significant (Table 4B). Moreover, the size of

the effect decreases with the level of non-interest income; the potential benefits on

profitability are stronger for banks which have a lower level of non-interest income.

We also investigate the effect of diversification on risk over a restricted sample of

listed banks using market-based measures of risk. Our results (Table 5) indicate that

diversification into non-interest activities does not affect risk taking and results in a lower

level of default risk (higher level of the Z-score used as a proxy of the probability of default).

However, when restricting the sub-sample of listed banks to listed universal banks, we find

for all market-based measures that an increased reliance on non interest activities tends to

decrease bank risk taking and default risk.

Overall, our findings suggest that an increased diversification in non-interest activities

increases profitability but does not necessarily lead to more volatile returns. These results are

not in line with those of US banking studies that find a positive relationship between increases

in shares of non-interest income and returns' volatility (Stiroh and Rumble, 2006, Stiroh,

32

Tables provided in the paper present the results obtained using ROA, SHROA, ADJROA and SDROA. Estimations are also conducted

using ROE, as performance variables. As results obtained are in most cases similar, they are not provided here but are available upon

request. 33Estimations conducted with FOCUSDIV variable show similar results than those presented in Table 4. We show that banks which present a

level of diversification greater than 50% have a greater profitability and risk adjusted return. We do not report the table of results but they are

available upon request.

24

2004b and De Young and Roland, 2001). However, as in Chiorazzo et al. (2008) and Wolfe

and Sanya (2011), we find a positive relationship between diversification and risk-adjusted

performance.

When investigating differences in bank size (H1a), we find that increased reliance on

non-interest activities has a positive impact on profitability and risk adjusted return only for

smaller banks (Table 6A)34

. However, the net effect is significant only for small banks which

have an intermediate or high level of diversification (Table 6B). For the group of large banks

which excludes the government banks, diversification positively affects risk-adjusted return.

Moreover, the net effect is significant at low and intermediate level of diversification (below

50th) and its size decreases with the level of diversification in non-interest activities. As

smaller banks have lower average shares of non-interest income (32.22% for small banks in

comparison with 39% for medium-sized banks and 38.12% for large banks), these results are

consistent with those presented in Table 8. Analyzing the impact of differences in the level of

involvement in non-interest activities (H1b), we show that diversification into non-interest

generating activities increases profitability but only for banks which have lower levels of

diversification.

Although some studies highlight a potential negative effect of diversification on small

bank performance (Mercieca et al., 2007), our findings are consistent with other studies

(Chiorazzo et al., 2008, Stiroh, 2004a), which find that there are some opportunities for

smaller banks to diversify. Moreover, the decreasing impact of diversification when bank size

and level of diversification increase is in line with the existing literature which stresses limits

from diversification gains as a bank gets larger. Since larger banks are generally more

diversified, their gains from further diversification are limited as possible saturation occurs

upon reaching an optimum level and size (Demsetz and Strahan, 1997; Stiroh and Rumble,

2006; Chiorazzo et al., 2008).

Some differences according to ownership characteristics can also be highlighted

(H1c). The results are presented in Tables 9A and 9B. They show a positive and significant

effect of the variable NII on profitability and a net positive effect of increased exposure in

non-interest activities on risk adjusted return. In both cases, the effect is stronger for foreign

banks.

34 Using the interaction term, NII*Asset, we find similar results (Table 7A and 7B), which suggest that increased exposure in non-interest income benefits more small banks that have asset sizes which are below the 25th percentile in terms of increased profitability.

25

4.2 The effects of the disaggregated non-interest income components on profitability and

risk

To go further and examine which sources of non-interest income drive the effect of

diversification on profitability and risk, we analyze the impact of the three components of

non-interest income – fee-based, trading and other income and of their disaggregation on our

profitability and risk measures. We first examine the pairwise correlations of the growth rates

of operating income, its components (interest income and non-interest income) and the non-

interest income components (fee-based income, trading income and others non-interest

income). We find that interest income growth is correlated with fee-based income growth at a

5% level of significance possibly due to cross-selling or that fee-based activities complement

the traditional intermediation role of the bank (Table 10). We would have expected

profitability to increase as a consequence of increased engagement in fee-based activities due

to lower costs that are to be incurred when engaging in these activity types. However, we note

that the proportion of loans in total assets has decreased over the period of our study along

with the related revenue streams generated from this asset component that includes fee-based

income. Income from fee-based activities35

relies basically on bank commissions and service

charges that are linked to the amount of loans drafted by the banks. Meanwhile, we do not

find any significant correlation between interest income growth rate and trading income and

other non-interest income growth.

The results of Model 2a are presented in Table 11. We find a negative and significant

influence of an increased share of fee-based income on profitability using dynamic panel data

estimation (columns 9 and 13) and, in most cases, no significant effect on risk adjusted return

and risk. From the results on the pairwise correlations, we thus expect an enhancement of

bank performance attributed to the engagement in trading activities. We find trading income

to have a positive and significant effect in explaining bank profitability (columns 5, 9, 13 and

15) and risk adjusted return (columns 2, 6, 10, 14 and 16). Moreover, we do not find a

significant effect of an increased share of trading income on the volatility of returns.

Estimations conducted on Model 2a‟ show that the positive effect of trading income on

profitability is significant only for banks with a relatively high share of government securities

(Table 12A, 12B) or the banks that hold and purchase government securities non-optimally to

comply with the regulation that mandates banks to lend to SMEs.

35 We note however that other commissions/fees, a component of fee-based come are not necessarily functions of bank loans and of the interest generating activities of the banks.

26

When conducting our investigation on the restricted sub-sample of listed banks (Table

13), we do not find a significant effect when considering the whole sample of listed banks.

However, we show that increased reliance on trading activities reduces risk for universal

listed banks.

These findings are not in line with studies on US banks (i.e. Stiroh, 2004b) which

report higher risk for banks more reliant on trading activities. However, for European banks,

Lepetit et al. (2008) do not find evidence of a positive relationship between trading activities

and risk and, in the case of small banks, they show that a higher share of trading activities is

associated with lower asset and default risk.

Econometric investigations conducted on the detailed breakdown of fee-based and

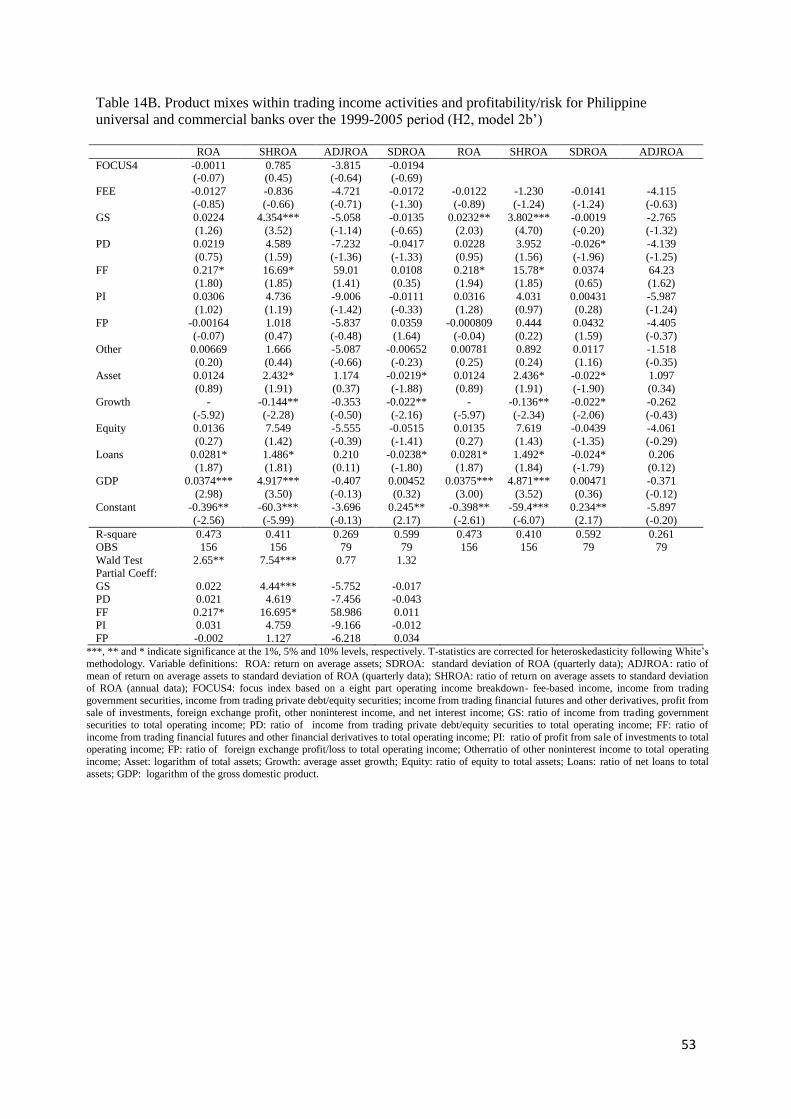

trading activities (Model 2b and 2b‟) provide a clearer insight of how different product mixes

within non-interest activities affect profitability and risk. Two main results are highlighted.

First, in the case of fee-based activities, we find that an increased share of “other commissions

and fees” to total operating income is associated with increased profitability, while increased

reliance on bank commissions negatively affect risk-adjusted returns (Table 14A). The second

result relates to trading activities (Table 14B). We find that the positive effect of an increase

in the share of trading income on profitability is mainly driven by government securities

trading and financial futures activities. The interpretation of diversification must be given

utmost care as the decision to purchase government notes, securities and negotiable securities

can be a means by banks to comply with the requirement on banks to set aside at least six

percent and two percent of their total loan portfolio for small and medium enterprises,

respectively. Thus, if the link between diversification and profitability and risk is driven by

gains from trading government securities, it may purely be attributable to compliance and not

to optimal diversification.

4.3 Does diversification into underwriting activities alter profitability and risk?

Finally, we focus on the diversification behavior of universal banks and more

specifically on the effect of the involvement of universal banks in investment house activities

which cannot be performed by commercial banks (H3). This dimension can be captured by

the component of fees generated by operations such as underwriting, securities dealership and

equity investments. We report the results in Tables 15 and 16. We find that higher shares of

"other commissions and fees," i.e. generated by investment banking operations, are associated

with higher risk, while higher shares of income from trading government securities have the

opposite effect. Risk is also reduced for banks with higher portions of trading gains from

27

private debt and equities securities as well as profit from sale of investments. On the whole,

we find that increased engagement in non-interest activities is associated with lower risk but

this result is essentially driven by trading activities and more specifically, by trading

government securities. Higher involvement of universal banks in underwriting activities and

securities dealership actually increases risk.

5. Robustness Checks36

Several robustness checks are performed to examine whether different definitions of

our variables will leave the main results unchanged. First, we compute alternative measures of

the variable FOCUSDIV. FOCUSDIV is equal to the interaction between FOCUS1 and a

dummy variable, DIV1, which is equal to 1 if the share of non-interest income is higher than

50% and zero, otherwise. We examine different thresholds of DIV1, 30%, 40% and 60% and

find that at a threshold of non-interest income less than 40%, focus does not translate into

increased bank profitability. Moreover, with thresholds greater than 40%, we find that focus

increases bank profitability. Our results are very robust to the 60% and 70% thresholds which

confirm that focusing in activities that generate non-interest income increases the profitability

of Philippine banks.

Second, we use a more limited definition of trading income, which includes only the

gains/losses from trading activities (government securities, private/equity securities, financial

futures options/forwards/swaps). When this definition is used, we find "other non-interest

income" to be positively related to profitability and risk, markedly in medium-sized banks.

This can be explained by the addition of foreign exchange profit, gold trading gain/loss and

the profit on sale or redemption of investments in our definition of "other non-interest

income", which basically drives up bank profitability. The results however regarding trading

income remain unchanged.

Third, we use another definition to categorize large banks, taking the top ten banks

with the largest average assets over the period of our study. We thereby only consider 11

medium-sized banks. The results on the variables of interest remain unchanged. In addition,

we observe that for large banks our non-interest income focus measure (FOCUSDIV) is no

longer significant, which further strengthens our conjecture that deeper focus in non-interest

activities does not improve performance for large banks.

36 For the sake of brevity, we do not report all the results discussed under the section of robustness check. However, the results are available from the authors on request.

28

Lastly, we also examine if there are significant behavioral differences between listed

and non-listed banks. We do not find significant differences over these two subsamples.

6. Conclusion

The aim of this paper is to analyze the impact of revenue diversification on risk and

profitability in the Philippine banking industry and to investigate the influence of a specific

bank regulation which compels bank to allocate a minimum portion of their loans to small and

medium enterprises or hold government securities instead. On the whole, we find that while

increased engagement in noninterest activities tends to be more profitable, there is not much

evidence regarding the volatility of bank returns. Moreover, in some cases, we find a positive

link between diversification and risk-adjusted returns which is not consistent with the results

obtained in the literature for US banks. A closer investigation reveals that fee-based income

growth is significantly correlated with interest income growth, and that trading activities are

generally dominated by trading in government securities, which are inherently less risky than

other income sources. By disaggregating the share of non-interest income, we find trading

income, particularly the gains from trading government securities to be the primary force

behind the positive relationship between profitability and diversification. The positive effect,

however, of trading activities on profitability holds only for banks that have a relatively high

share of government securities in total assets or banks that comply to the mandatory allocation

of credit resources to SMEs by alternatively purchasing government securities.

We also test whether bank size matters in gaining benefits from diversification. Our

findings indicate that small banks gain more from increased diversification as benefits for

large banks tend to be saturated after reaching an optimal size. Furthermore, we find that

diversification into non-interest generating activities increases profitability but only for banks

which have lower levels of diversification as banks with higher levels of diversification have

already exhausted the benefits of further diversification. In addition, our results indicate that

for universal banks a higher involvement in fee-based activities, particularly in commission

activities that generate income related to underwriting and securities dealership, increases

bank risk. Moreover, we find evidence that trading in government securities contributes to

lower risk, driving the negative relationship between risk and the share of non-interest

activities in total activities.

As a whole, we find that isolating the analysis of diversification only on focus indices

and non-interest income shares can mislead result interpretations. The level of income is as

29

important as its sources as some are inherently riskier and are more profitable, and some are

governed by regulations and laws. The implementation of a regulation to promote lending to

small and medium enterprises might have reached an unexpected goal preventing banks from

being more exposed to risk induced by the development of non-interest activities in the

banking sector.

30

APPENDIX 1: Definitions

NONINTEREST INCOME ACCOUNTS

Fee-based Income: sum of bank commissions, service charges/fees and other commissions/fees

Bank Commissions: commissions collected for services rendered as in: (a) opening of letters of

credit, (b) handling of collection items, domestic/export/import bills and telegraphic transfers, and (c)

sale of demand drafts, traveller‟s checks and government securities