CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

LESSON 21-1LESSON 21-1

Accrued Revenue

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

2

LESSON 21-1

ANALYZING AN ADJUSTMENT FOR ANALYZING AN ADJUSTMENT FOR ACCRUED INTEREST INCOMEACCRUED INTEREST INCOME

11

22

page 617

33 1. Debit Interest Receivable.

2. Credit Interest Income.

3. Record the adjusting entry.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

3

LESSON 21-1

2. Post the credit.

POSTING AN ADJUSTING ENTRY FOR POSTING AN ADJUSTING ENTRY FOR ACCRUED INTEREST INCOMEACCRUED INTEREST INCOME page 618

11

22

1. Post the debit.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

4

LESSON 21-1

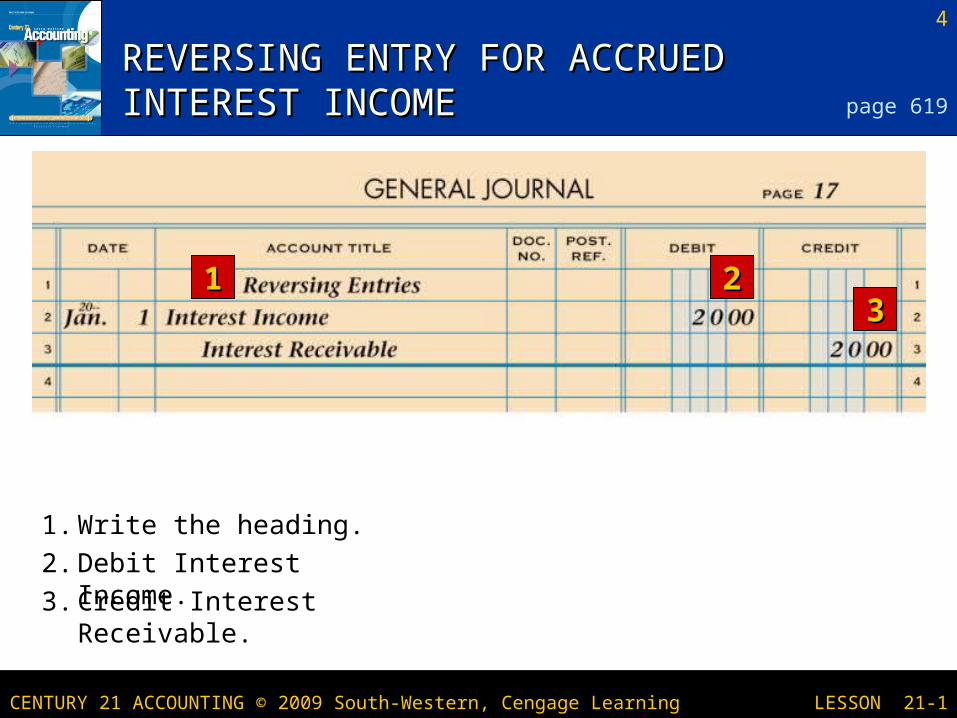

REVERSING ENTRY FOR ACCRUED REVERSING ENTRY FOR ACCRUED INTEREST INCOMEINTEREST INCOME

11 2233

page 619

1. Write the heading.

2. Debit Interest Income.

3. Credit Interest Receivable.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

5

LESSON 21-1

COLLECTING A NOTE RECEIVABLE COLLECTING A NOTE RECEIVABLE ISSUED IN A PREVIOUS FISCAL PERIODISSUED IN A PREVIOUS FISCAL PERIOD

22

page 620

January 30. Received cash for the maturity value of a 90-day, 6% note: principal, $2,000.00, plus interest, $30.00; total, $2,030.00. Receipt No. 9.

3. Debit for the maturity value.

1. Credit for the principal of the note.

2. Credit for the total interest.

4. Post the amounts in the General columns.

11 33

44

44

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

6

LESSON 21-1

TERMS REVIEWTERMS REVIEW

accrued revenue intellectual property accrued interest income reversing entry

page 621

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

LESSON 21-2LESSON 21-2

Accrued Expenses

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

8

LESSON 21-2

ANALYZING AN ADJUSTMENT FOR ANALYZING AN ADJUSTMENT FOR ACCRUED INTEREST EXPENSEACCRUED INTEREST EXPENSE page 622

11

22

33

2. Credit Interest Payable.

1. Debit Interest Expense.

3. Record the adjusting entry.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

9

LESSON 21-2

POSTING AN ADJUSTING ENTRY FOR POSTING AN ADJUSTING ENTRY FOR ACCRUED INTEREST EXPENSEACCRUED INTEREST EXPENSE page 623

1122

2. Post the credit.

1. Post the debit.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

10

LESSON 21-2

REVERSING ENTRY FOR ACCRUED REVERSING ENTRY FOR ACCRUED INTEREST EXPENSEINTEREST EXPENSE

1122

page 624

1. Debit Interest Payable.

2. Credit Interest Expense.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

11

LESSON 21-2

PAYING A NOTE PAYABLE SIGNED IN A PAYING A NOTE PAYABLE SIGNED IN A PREVIOUS FISCAL PERIODPREVIOUS FISCAL PERIOD

11

22

33

44

44

page 625

March 1. Paid cash for maturity value of the September 2 note: principal, $10,000.00, plus interest, $600.00; total, $10,600.00. Check No. 916.

1. Debit for the principal of the note.

2. Debit for the total interest.

3. Credit for the maturity value of the note.

4. Post the amounts in the General columns.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

12

LESSON 21-2

TERMS REVIEWTERMS REVIEW

accrued expenses accrued interest expense

page 627

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

Adjusting, Closing, and Reversing EntriesAdjusting, Closing, and Reversing Entries

Adjusting Entries Last day of fiscal period December 31

Closing Entries Last day of fiscal period December 31

Reversing Entries First day of new fiscal period January 1

13

LESSON 21-1

![Accrued Interest en[1]](https://cdn.vdocuments.net/doc/165x107/577d231d1a28ab4e1e99053c/accrued-interest-en1.jpg)