CFA-DFW/CFA HOUSTON Student Research This report is published for educational purposes only

by students competing in the

Investment Research ChallengeTM

– Texas.

Investment Research Challenge-Texas

CFA-DFW/CFA Houston Important disclosures appear at the back of this report

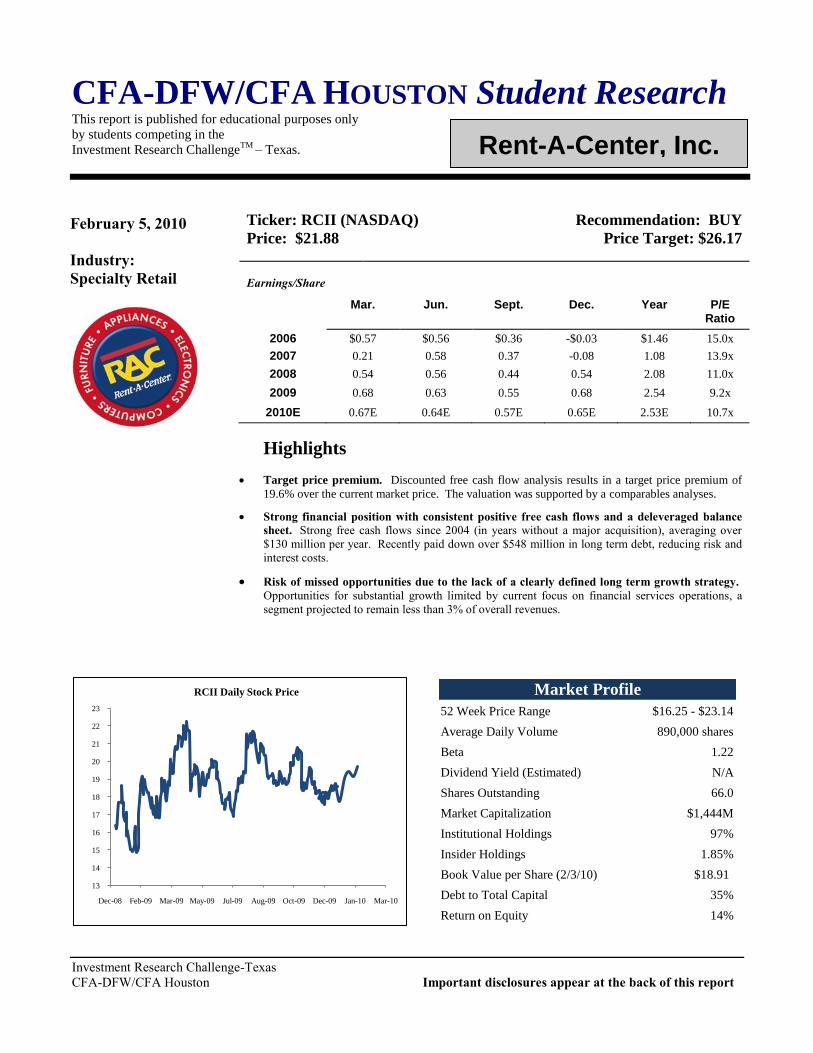

Ticker: RCII (NASDAQ) Recommendation: BUY

Price: $21.88 Price Target: $26.17

Earnings/Share

Mar. Jun. Sept. Dec. Year P/E Ratio

2006 $0.57 $0.56 $0.36 -$0.03 $1.46 15.0x

2007 0.21 0.58 0.37 -0.08 1.08 13.9x

2008 0.54 0.56 0.44 0.54 2.08 11.0x

2009 0.68 0.63 0.55 0.68 2.54 9.2x

2010E 0.67E 0.64E 0.57E 0.65E 2.53E 10.7x

Highlights

Target price premium. Discounted free cash flow analysis results in a target price premium of

19.6% over the current market price. The valuation was supported by a comparables analyses.

Strong financial position with consistent positive free cash flows and a deleveraged balance

sheet. Strong free cash flows since 2004 (in years without a major acquisition), averaging over

$130 million per year. Recently paid down over $548 million in long term debt, reducing risk and

interest costs.

Risk of missed opportunities due to the lack of a clearly defined long term growth strategy.

Opportunities for substantial growth limited by current focus on financial services operations, a

segment projected to remain less than 3% of overall revenues.

13

14

15

16

17

18

19

20

21

22

23

Dec-08 Feb-09 Mar-09 May-09 Jul-09 Aug-09 Oct-09 Dec-09 Jan-10 Mar-10

RCII Daily Stock Price

52 Week Price Range $16.25 - $23.14

Average Daily Volume 890,000 shares

Beta 1.22

Dividend Yield (Estimated) N/A

Shares Outstanding 66.0

Market Capitalization $1,444M

Institutional Holdings 97%

Insider Holdings 1.85%

Book Value per Share (2/3/10) $18.91

Debt to Total Capital 35%

Return on Equity 14%

Market Profile

Rent-A-Center, Inc.

February 5, 2010

Industry:

Specialty Retail

IRC-TX 02/05/2010

Investment Research Challenge- Texas STUDENT RESEARCH 2

Investment Summary Rent-A-Center merits a “BUY” recommendation based on its projected free cash flows and potential for breakout revenue

growth. Our target price of $26.17 represents a premium of 19.6% over the firm’s current market value. The firm is relatively

undervalued as compared to its peers.

Rent-A-Center is expected to generate strong free cash flows into the foreseeable future despite an anticipated decline in long

term growth. The firm will achieve moderate revenue growth in the short to mid-term through the addition of approximately

315 stores, buyouts of about 300 competitor store accounts, improved sales of add-on units, and successful integration of its

financial services operations into its existing stores. However, we are less bullish beyond year five when we believe market

saturation, limited acquisition opportunities, the maturation of existing stores, and the effects of increased competition will

result in growth more in line with the economy as a whole. Even so, we believe Rent-A-Center’s large geographic footprint and

established customer base will provide a consistent, though less rapidly growing revenue source.

The firm is expected to maintain reasonable, albeit diminished, margins despite an increasingly competitive landscape. The

rapid growth of Rent-A-Center’s closest competitor should eventually create downward pricing pressure on the industry as a

whole, negatively impacting margins. Even so, the Rent-A-Center’s more efficient integration of its financial services

operations, reduced inventory costs resulting from the implementation of new inventory management tools, and reduction in

debt related expenses due to its debt reduction efforts, should allow it to maintain sufficient margins into the foreseeable future.

Our target price is based solely upon the results of transactions with Rent-A-Center’s current customer base. However, we

believe Rent-A-Center has barely scratched the surface of its potential customer pool, reaching only one out of seven

individuals that fall within its target demographic. Rent-A-Center has the potential to dramatically increase its customer base

through expansion into large scale retail establishments. The firm is currently testing a strategy whereby it furnishes a sales

force within certain large scale retail stores to provide an additional purchasing option to customers who do not qualify for retail

credit. Should this strategy prove successful, Rent-A-Center would gain access to a customer base even beyond its underserved

target group, providing the potential for both rapid and dramatic revenue growth.

Rent-A-Center’s value could be negatively impacted by the adoption of industry restrictive legislation, the firm’s failure to

integrate its financial services operations, the firm’s failure to identify new markets, continued high unemployment, declining

consumer electronics prices, or the entry of big box retailers into the rent-to-own industry.

Figure 1: Rent-A-Center, Inc. Five Year Stock and News Chart This chart is a timeline of news events with major impact to Rent-A-Center, Inc.’s market price.

Source: Thomson Reuters

0

5

10

15

20

25

30

35

Jan-05 Jul-05 Jan-06 Jul-06 Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10

May 25, 2005

RCII issues FY

guidance below

Analysts’ Estimates

October 24, 2005

RCII issues Q4 2005 and FY 2006

guidance above Analysts'

expectations, comments on same

store sales guidance, and

announces 3.9 million share

repurchase of common stock

July 24, 2006

RCII raises FY 2006 EPS Outlook

and issues FY 2006 revenue

outlook slightly above Analysts'

estimates and issues Q3 2006

outlook above analysts' estimates

August 8, 2006

RCII and Rent-Way, Inc. announce an

agreement to acquire Rent-Way for

$10.65 per share

July 30, 2007

RCII issues Q3 guidance

with EPS forecast below

Analysts' estimates and

lowers FY 2007 guidance

February 4, 2008

RCII issues Q1 2008

guidance and EPS is below

Analysts' estimates, also

issues FY 2008 Revenue

guidance in line with

Analysts' estimate

October 2008

Broad Market selloff

April 27, 2009

RCII lowers end of FY 2009

EPS guidance and issues Q2

2009 revenue guidance

below Analysts' estimates

December 3, 2009

RCII lowers Q4 2009 and

FY 2010 Revenue guidance

February 1, 2010

RCII announces 4Q Results,

issues Q1 2010 guidance that top Analysts’ estimates

IRC-TX 02/05/2010

Investment Research Challenge- Texas STUDENT RESEARCH 3

Business Description Rent-A-Center, Inc. (NASDAQ: RCII) is the largest rent-to-own operator in the industry offering high quality durable goods,

such as consumer electronics, appliances, computers, furniture and accessories under flexible rental purchase agreements. Incorporated in 1986 and headquartered in Plano, TX, Rent-A-Center employs approximately 18,000 people.

Rent-A-Center Operations

RCII’s core business is the offering of rental purchase and sales agreements on major consumer electronics (Sony, Phillips, LG,

Hitachi, Toshiba, Mitsubishi, Panasonic, Magnavox, and JVC), appliances (Whirlpool), computers (Toshiba, Sony, HP, Dell

and Compaq), and furniture and accessories (Ashley, England, Klaussner, Albany, Standard, Welton, Serta, and Corsicana).

These agreements allow the customer to obtain ownership of the merchandise at the end of a specified rental period, providing

consumers with a flexible alternative to incurring debt or spending a significant amount of cash. Other benefits of the rental

purchase transaction include convenient payment options, no long term obligations, right to terminate without penalty, no

requirement of credit history, free set-up and delivery, product maintenance, and flexible ownership options.

Rent-a-Center operates 3,007 company owned stores throughout the United States, as well as in Canada and Puerto Rico,

including 37 stores under the names “Get It Now” and “Home Choice” and 18 stores in Canada under the names “Rent-a-

Centre” and “Better Living.” These stores constitute 35% of the total rent-to-own market. ColorTyme, a wholly owned

subsidiary of Rent-a-Center, is a national franchisor of rent-to-own stores with 213 franchised stores in 33 states, as of third

quarter 2009. Rent-A-Center leases space for all of its stores, service centers and regional offices. The retail stores average

4,700 square feet in size and consist of 75% showroom space and 25% office and storage space.

Customers generally enter rental agreements with weekly, semi-monthly, or monthly payments, which renew automatically

upon receipt of each payment. The company retains title to the merchandise until the customer has completed the agreement, a

period of seven to 30 months, though on average a minimum of 18 months. Although a formal credit investigation is not

conducted, personal information and references are required. The vast majority of renters physically enter the store to make

payments, and 75% of customers are repeat business.

Approximately 25% of the initial rental purchase agreements are taken to the full term (See Figure 2). For the remaining 75%,

the customer returns the merchandise before acquiring

ownership. The average product of this type is rented for

four to five months at a time and is rented four times

before it leaves the system. On average, a product is in

the system for 20 months, generating revenue for 18

months. Each time the product is re-rented, the rental rate

is generally the same, but the term to acquire ownership

and the cash price are reduced. Over 90% of the

merchandise leaves through a rent-to-own transaction,

and 7% are bought upfront. The remaining 3% consists

of losses, including consumer losses (2.5%) and other

(0.5%) to include shrinkage, damage, obsolescence, etc.

Consumer losses have been consistent historically,

ranging from 2.3% to 2.8%, with the latest quarter data at

a low of 2.3%.

Rent-A-Center operates in two broad categories, store and franchise. The store segment, which accounted for 96.7% of

revenues in 2009, includes rentals and fees (85.3%), merchandise sales (9,5%), installment sales (1.9%), and other (2.1%). The

franchise segment consists of franchise merchandise sales (1.0%) and royalty income and fees (0.2%). Store merchandise is

divided into four broad categories, which accounted for revenues in third quarter 2009 as follows: consumer electronics – 36%;

furniture and accessories - 31%; appliances – 17%; and computers - 16%. Margins are generally the same for all product

categories.

In order to further penetrate its markets, Rent-A-Center has implemented an aggressive marketing strategy in recent years to

emphasize a “worry-free” form of ownership, including competitor price matching and a 100% satisfaction guarantee.

Marketing campaigns include celebrity spokespersons Magic Johnson and Troy Aikman.

Rent-A-Center believes its competitive strengths include its geographic distribution, experienced management, strong cash from

operations, effective collections, and integration experience. The company’s strategy includes capitalizing on its competitive

strengths as well as controlling expenses and improving inventory management. The company is in the process of

implementing an inventory management tool, which will allow for a more centralized purchasing approach. The system should

be in place by the end of first quarter 2010. Recent trends include a decrease in rentals per agreement; however store traffic

remains strong.

Figure 2: Rent-A-Center Merchandise Life Cycle

22.5%

67.5%

7.0%

2.5%

0.5%3.0%

How Merchandise Leaves a Rent-A-Center Store

Rent-to-Own Transaction

to Full Term

Rented Repeated Times

Bought Upfront

Consumer Losses

Other

(shrinkage, damage, obsole

scence)

IRC-TX 02/05/2010

Investment Research Challenge- Texas STUDENT RESEARCH 4

Acquisition History

Rent-A-Center has grown rapidly since inception largely from acquisitions. After incorporating in 1986, the company (under

the name Talley Leasing) purchased Vista Rent to Own, a chain of 22 stores, in 1989, then DEF, an 84-store chain, upgrading

merchandise and data systems along the way. After going public in 1995, they acquired Crow Leasing and Pro Rental,

expanding store count to 322. The following year they acquired ColorTyme, adding another 320 stores, most of which were

franchised. The company purchased Central Rents in 1998 (180 stores) and Thorn Americas (1,400 stores). In 2004 the

company acquired Rent Rite (90 stores in 11 states) and Rainbow Rentals (124 stores in 15 states). Rent-A-Center purchased

Rent-Way in 2006 for approximately $600 million (782 stores in 34 states). Overall acquisitions occurred in 240 separate

transactions, including ten transactions in excess of 50 stores. In order to enhance service levels and increase market

penetration, the company strategically opened or acquired stores in existing markets. This strategy resulted in an over

penetration in some markets; therefore, it enacted a store consolidation plan and closed or merged 282 stores in 2007-2008. At

this time, there are few remaining acquisition targets. Excluding Aaron’s, Inc., no current competitor operates more than 87

stores, a mere 1% of the rent-to-own market.

Other Sources of Revenue

In 2005, Rent-A-Center introduced financial service products under the trade names “RAC Financial Services” and “Cash

AdvantEdge” to include short term secured and unsecured loans, debit cards, check cashing, tax preparation, and money transfer

services. As of year-end 2009, the company offered financial services in 353 retail stores in 17 states. After a period of

sustained losses, the segment is projected to become profitable in 2010. The company plans to open 50 more financial services

outlets in 2010. Rent-A-Center has indicated an intent to eventually provide financial services in as many as 1,000 of its rent-

to-own stores within the next four to six years.

Purchasing and Distribution

The general product mix available to the stores is determined by the executive management team based on customer rental

patterns and new product tests. The individual store managers, however, are responsible for selecting the particular product mix

carried in their stores. They, along with the district managers, make purchase orders through an online ordering system. All

merchandise is shipped from the vendors directly to the stores, removing the need for distribution centers. This system allows

for low levels of inventory, tight control, and a low level of product obsolescence.

The largest suppliers of merchandise are Whirlpool, which accounted for 14.8% of merchandise purchased in 2008, and Ashley,

which accounted for 12.6%. No other supplier account for more than 10% of merchandise purchased in 2008, reducing

dependency on any sole supplier.

Growth Strategy

The company plans to grow its store count by an additional 25 to 35 stores in 2010. It also intends to acquire customer accounts

from smaller competitors. As the company has expressed that the existing market will become saturated at a store count of

3,400, (will have reached 90% of this as of YE 2010), additional avenues of revenue growth must be explored. As previously

mentioned, the Financial Services division represents an opportunity for growth; however, unless drastic measures are taken, it

will remain a small percentage of revenues as a whole in the near future (<3%). Other potential growth opportunities mentioned

by management come in the form additional distribution channels including agreements with other retailers, expansion of retail

installment sales, and international market expansion. The most significant of these involves the firm’s current expansion into

large scale retail establishments. Rent-A-Center is presently testing a strategy whereby it establishes a presence in certain large

scale retail stores to provide a purchasing option to customers who do not qualify for store credit. If successful, the firm could

expand rapidly through the acquisition of existing small scale providers such as Flexi Compras, a regional provider of these

services. This strategy could exponentially increase Rent-A-Center’s customer reach and alleviate some of the stigma

associated with the rent to own purchase model. However, unless these efforts are successfully implemented on a large scale,

the bulk of future growth will likely stem from the acquisition of store accounts from smaller competitors and new store

openings.

Insider and Institutional Holders

Mark Speese, the CEO and Chairman of the Board, holds 1.5% of Rent-A-Center’s outstanding shares. Top institutional holders

include Blackrock Institutional Trust Company, N,A., Hotchkis and Wiley Capital Management, L.L.C., The Vanguard Group,

Inc., State Street Global Advisors, and Robeco Investment Management, Inc., which collectively own 27% of RCII. Of Rent-

A-Center’s institutional investors, 29% are value investors, 22% are growth investors, 12% are index funds, and 4% are income

investors. The remaining 33% are a mixture of GARP investors, hedge funds, broker dealers, and specialty funds. See Exhibit

1.

Management

The executive management team has over 100 combined years with the company and extensive experience in the rent-to-own

industry. The CEO and Chairman of the Board, Mark Speese has been with the company since inception. The Executive Vice

President of Finance and CFO, Robert Davis, has been with the company since 1997. Mitchell Fadel, the current President and

COO, served these roles at ColorTyme beginning in 1992, prior to its acquisition by Rent-A-Center in 1996.

IRC-TX 02/05/2010

Investment Research Challenge- Texas STUDENT RESEARCH 5

Industry Overview and Competitive Positioning The rent-to-own concept originated in the 1960s to as a result of a growing need to obtain household products without a

significant cash outlay or the use of credit. In general, no interest is charged, no credit checks are performed, and the customers

can return the merchandise at any time without penalty. The industry consists of dealers who rent furniture, electronics, major

appliances, computers, wheels and tires, and other products with an option to buy. The rent-to-own industry in the United States

and Canada consisted of 8,600 stores as of 2009.

The rent-to-own industry’s expansion has been roughly in line with the rate of U.S. Gross Domestic Product since 1995 with the

exception of a slight contraction from 2004 to 2007. See Exhibit 2-Figure 1. This amounts to a compound annual growth rate of

1.6%. From 2008 to 2009, the rent-to-own industry grew 6.34% while GDP contracted 2.85% (inflation adjusted), the result of

a temporarily increased customer base caused by decreased credit availability. Moving forward, it is anticipated the industry’s

growth will again be in line with the economy as a whole.

Historically, the industry has served a highly specific customer. Every five years dating back to 1994, The Association of

Progressive Rental Organizations (“APRO”) published rent-to-own industry customer statistics regarding income, education,

age, residence, and ethnicity. See Exhibit 3. Based on the latest 2009 APRO data, the average rent-to-own household: has an

income of $15,000 to $49,999 (83% of customers), has a high school diploma and/or some college education (81%), contains

members between the ages of 25 and 54 (81%), owns their residence (69%), and is of Caucasian ethnicity (84%). There have

only been slight deviations from these demographic norms throughout each of the survey periods (1994, 1999, 2004, and 2009),

with the exception of household income. The industry’s average household income tends to rise when credit markets tighten

and vice versa when they relax. The number of rent-to-own customers served has fluctuated greatly since 1995, oscillating

between 2.8 and 4 million due to periodic expansion and contractions in the credit market. See Exhibit 4-Figure 1. The average

rent-to-own customer generates $1,600 in revenues per year. Revenue per customer has steadily declined since 2004. See

Exhibit 4-Figure 2.

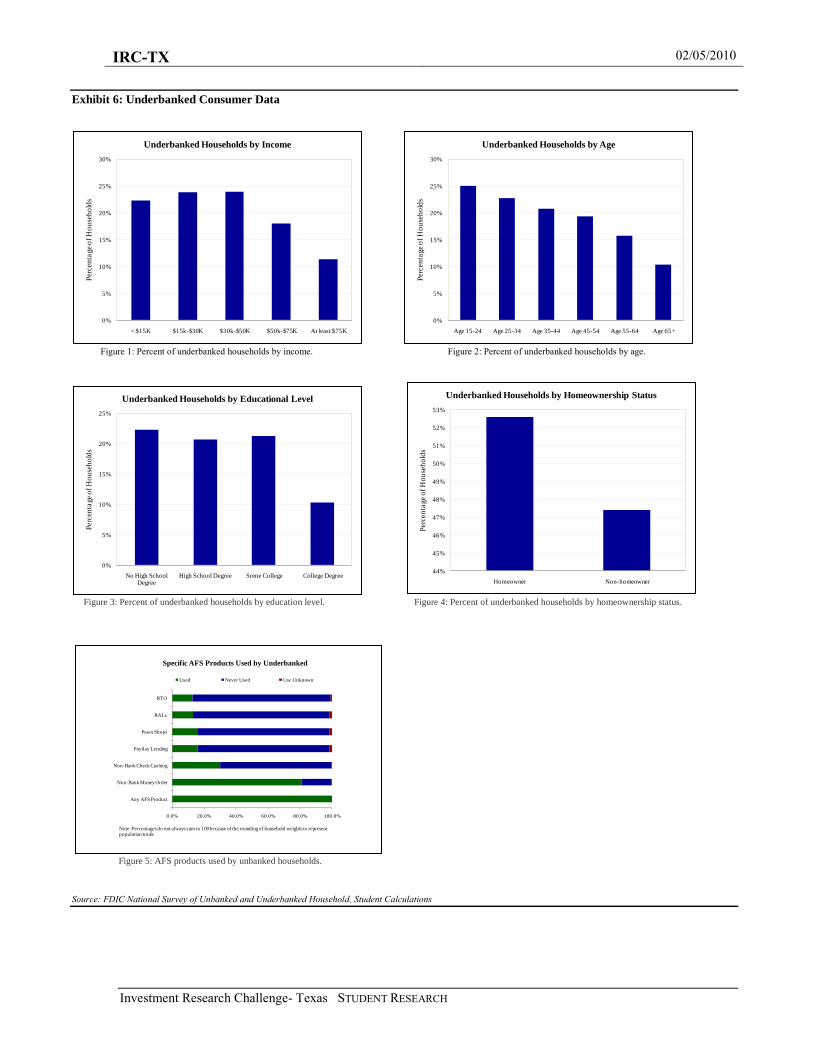

Despite its reach, the rent-to-own industry’s four million

customers represent only a small portion of its potential

customer base. A 2009 study sponsored by the Federal

Depository Insurance Company (“FDIC”) concluded 9

million (7.7%) U.S. households are unbanked and 21

million (17.9%) are underbanked. The unbanked consumer

does not have a checking or savings account. Underbanked

consumers have a checking or savings account but rely on

alternative financial services. Alternative financial services

include non-bank check cashing, non-bank money orders,

payday lending, pawn shops, rent-to-own, and refund

anticipation loans. Refer to Figure 3 to the right. The

FDIC study determined only 11.9% of the unbanked and

13% of the underbanked households have undertaken a

rent-to-own transaction. See Exhibits 5 and 6. Therefore,

it can be inferred the rent-to-own industry serves

approximately one in seven of its potential customers. This

leaves substantial room for growth if the industry can determine an appropriate means to reach these customers.

Competitive Positioning

Rent-A-Center has only one major direct competitor, Aaron’s, Inc. (“Aaron’s”). Aaron’s is the second largest player in the rent-

to-own industry, with an approximate 18.3% market share (1,577 stores) located throughout 47 states and Canada, including

504 franchised stores. Unlike Rent-A-Center, Aaron’s has an active franchise program with approximately half of its projected

2010 store growth expected to be from franchised stores. In addition to the Sales & Lease Ownership division, Aaron’s

manufactures furniture in its MacTavish Furniture Industries segment, which it then sells in its stores. It manufactures

upholstered living room furniture, bedding including mattresses and box springs, and office furniture.

Aaron’s attempts to distinguish itself from Rent-A-Center and “traditional” rent-to-own businesses. Its sales and lease

ownership model encourages customers to obtain ownership of the merchandise. Over 45% of customers obtain ownership

versus the 25% experienced by the industry as a whole. Aaron’s also requires a minimum rental period on some products,

whereas Rent-A-Center customers can return the merchandise at any time. Additionally, the typical Aaron’s plan offers semi-

monthly or monthly payments instead of weekly payments. It also receives more payments through check, credit card, or debit

card (approximately 51% of total dollar volume). These differences are indicative of Aaron’s targeting a slightly higher income

household. The average store is also twice as large as the average Rent-A-Center store at 9,000 square feet.

At this time, Rent-A-Center retains several competitive advantages over Aaron’s, Inc. Rent-A-Center has a significantly larger

geographic footprint, a larger breadth of services, and more direct control over its stores. However, these advantages may erode

Underbanked18%

Unbanked8%

Banked, but underbanked status

unknown*4%

Banked, but not underbanked

70%

Banking Status of U.S. Households

Notes: Percentages based on 118.6 million U.S. households. Percentages do not always sum to 100 because of rounding of household weights to represent population totals.*These households are banked, but there is not enough information to determine if they are underbanked

Figure 3: Banking Status of U.S Households

IRC-TX 02/05/2010

Investment Research Challenge- Texas STUDENT RESEARCH 6

if Aaron’s continues on its current path. Aaron’s recently increased its focus on its core business by disposing of its corporate

furnishings division. Its more nimble structure will allow it to focus on markets already proven successful by Rent-A-Center

(See Exhibit 7).

Porter’s Five Forces – Rent-to-Own Industry Rent-A-Center faces relatively low supplier power, buyer power, and threat of substitutes, while the threat of new entrants is

high. Internal rivalry within the industry is considered rising. The impacts of these forces will ultimately increase pricing

pressures resulting in an industry-wide decrease in margins.

Power of Suppliers – Low Figure 4: Porters Five Forces Model There are several suppliers for electronics, appliances, and

furniture in this industry. These suppliers have little

product differentiation with relatively low margins.

Though Whirlpool and Ashley are Rent-A-Center’s largest

suppliers (14.8% and 12.6% respectively), the

configuration of Rent-A-Center’s distribution system

allows it to change suppliers without major impact to

product availability or distribution.

Threat of Substitutes - Low Consumers in this industry have other options to fund their

product purchases such as credit cards, in store credit, loans and cash. However, the threat of substitution by these products is

low due to the limited availability of these options to the underbanked consumer traditionally pursued by Rent-A-Center.

Decreased credit availability to the consumer and relatively high unemployment rates in the short to medium term make the

rent-to-own transaction an attractive option for its customers. See Exhibit 8.

Power of Buyers - Low

Customers in the rent-to-own industry are individual, decentralized consumers who are underbanked. This consumer has no

bargaining power and behaves as a price taker due to the limited financing options available to them.

Threat of New Entrants - High Industry trends over recent years show Rent-A-Center’s local, regional, and national rent-to-own store markets have been

penetrated by new and established competitors. See Exhibit 7- Figure 5. Over the years, the industry has seen cyclical periods

of store growth and then store consolidation. Current barriers to entry such as capital requirements, switching costs, demand-

side and supply-side economies of scale, distribution, and incumbency barriers are not strong as they have not proven to be

sufficient deterrents. In addition, though not highly probable, the threat of entry by a major competitor with a larger distribution

system and network of low end consumers such as Costco or Wal-Mart could become viable if the rent-to-own industry

becomes attractive enough. Best Buy has already introduced the rent-to-own purchase option on a small scale to its customers

through its relationship with Flexi Compras (currently 18 stores in Texas). Similar to the method being tested by Rent-A-

Center, a representative from the company is placed in a booth in the Best Buy store to provide an alternative method for

purchasing merchandise if the customer cannot provide payment through traditional means. It remains to be seen to whether

Best Buy, or any other big box retailer, will expand such services or begin to provide these services on their own.

Industry Rivalry - Rising Rent-A-Centers margins have decreased over time due to pricing competition from it largest competitor, Aaron’s. Rent-A-

Center’s margins decreased from 19.6% to 13.1% between 2002 and 2009 while Aaron’s increased slightly from 10.1% to

12.4% over the same period. See Exhibit 7- Figure 1. New entrants, as well as Aaron’s plan to grow store count by 8%

annually, will likely intensify internal rivalry and threaten Rent-A-Center’s top line.

Financial Analysis

Revenues

From 2004 through third quarter 2009, revenues have grown at an average rate of 3.9%. A spike in revenue growth in 2007 was

caused by the acquisition of Rent Way, which added 782 stores. Revenues subsequently decreased in 2008 as a result of the

company’s store consolidation plan, which closed 315 stores, partially offset by a 2.3% increase in same store sales. In 2004

and 2005, same store sales growth were negative 3.6% and 2.3%, respectively; however the growth rate increased each year

over the next three years, averaging 2.1%. The 2009 revenues of approximately $2,752 million represent a decline of 4.6%, and

2010 forecasts are essentially flat at 2009 levels. Typical revenue drivers include number of stores, store traffic, units per rental

agreement, as well as method of ownership (buy upfront, rent-to-own full term, or rent-to-own multiple term.)

Bargaining Power of

Suppliers

LOW

Bargaining Power of

Customers

LOW

Threat of Entrants

HIGH

Industry Rivalry

RISING

Threat of Substitutes

LOW

IRC-TX 02/05/2010

Investment Research Challenge- Texas STUDENT RESEARCH 7

Margins

EBITDA margins have gradually decreased since 2004 from 16.8% to 12.5% in 2008, averaging 14.3%. As of year-end 2009,

however, the margin increased to 13.1%. Besides expenses, margins are also driven by method of ownership, as the cost goods

sold remains the same, while revenues double for the same item sold through a rent-to-own transaction as through a buy upfront

transaction. Additionally, if the item is rented an average of four times throughout an average life of 20 months, margins

increase for the same product. The company has employed recent cost cutting measures consisting of staffing models to control

number of employees and overtime, decreasing vehicle capacity from two trucks per store to one truck and one van, and the

implementation of a new inventory management system. These measures are anticipated to be sustainable, and all of the affects

have not yet been realized. The inventory management system had been implemented in less than 10% of Rent-A-Center’s

stores as of the third quarter of 2009. Another important factor is fuel costs, as the company operates 6,000 trucks, spending

roughly $1 million per month on gasoline.

Cash Flow

The firm generated positive free cash flow in 2007, 2008, and 2009 at roughly 4.2%, 5.9%, and 8.1% of revenues, respectively.

In 2006, free cash flow was negative (-15% of revenues) due to the major acquisition of Rent-Way. The prior two years’ free

cash flows were positive at 5.6% and 8% of revenues, respectively. Free cash flow for 2010 is projected at $140 to $160

million, or roughly 5% of revenues. The company spent $102 million in 2007, $62 million in 2008, and $68 million in 2009 on

capital expenditures including maintenance of existing assets as well as the acquisition and construction of new stores.

Management estimates capital expenditures will total approximately $75 million in 2010.

RCII has not paid dividends on its common stock since the time of its initial public offering. Covenants in the company’s senior

credit facility limit its ability to pay cash dividends; however, debt is currently sufficiently low that payment of dividends would

be permitted. Under the current stock repurchase plan, the company is permitted to repurchase up to $500 million of common

stock. As of year-end 2009, Rent-a-Center has repurchased 19,884,850 shares at a total cost of $466.5 million (average price of

$23.46 per share), with $33.5 million remaining. RCII only has one class of equity outstanding.

Balance Sheet & Financing

The debt to equity ratio reached a high of 1.4 in 2006, after averaging 0.9 for the previous three years. Rent-A-Center has used

free cash flow to reduce outstanding debt by $548 million during 2008 and 2009, resulting in current outstanding debt of $711

million, or a D/E of 0.57. Rent-A-Center has restructured their existing credit agreement, extending the final maturity of the

$82.5 million out of the $165 million Term Loan A from June 2011 to September 2013, at an interest rate of LIBOR plus

2.75%. The final maturity of $300 million out of the $484 million Term Loan B was extended from June 2012 to March 2015 at

LIBOR plus 3.0%. Additionally, the revolving credit facility was reduced from $400 million to $350 million, and extended

from July 2011 to September 2013.

Working capital for the company has been negative almost every year, since 1993. Since 2004, it has ranged from -6% to -14%

as a percentage of the previous year’s operating assets. The company has goodwill on its balance sheet valued at $1,269

million, or 54% of total assets, as of third quarter 2009. Rent-A-Center had $101.8 million in cash at year-end 2009.

Valuation Rent-A-Center’s value was assessed through the use of both a discounted cash flow analysis and a comparables analysis. The

application of a discounted free cash flow model resulted in an intrinsic value of $26.17, a premium of 19.6% over its current

market price. The results of a comparables analysis indicated Rent-A-Center is relatively undervalued as compared to its

identified peer group.

Discounted Cash Flow

A discounted free cash flow model with a five year horizon period was utilized to determine Rent-A-Center’s intrinsic value.

This methodology provides the most accurate means of estimating Rent-A-Center’s intrinsic value as the company does not pay

dividends and has only one truly comparable competitor. For the purposes of these calculations, we assumed a risk free rate of

3.75% and an expected market return of 8.75%. We estimated a beta of 1.22 based on the last three years’ weekly correlation

with the S&P 500. See Exhibit 9. Employing this model, we arrived at an intrinsic value of $26.17. See Exhibit 10.

Short to Mid-Term Growth

Rent-A-Center appears poised for moderate revenue growth in the short to mid-term. This growth will be spurred by the

addition of stores, the buyout of store accounts from smaller competitors, increased sales of add-on units, and the continued

integration of Rent-A-Center’s financial services operations into its existing stores.

Rent-A-Center is expected to increase revenues through the addition of roughly 315 stores and the purchase of 300 competitor

store accounts over the next five years. According to Rent-A-Center’s management, its existing markets can support 3,400

stores, roughly 400 more than it currently operates. However, in light of the rapid growth of its closest competitor, we project

more moderate store growth of only 315 new stores over the next five years. Each new store’s revenue is projected based on a

five-year maturation schedule provided by management. Each new store is projected to require $150,000 in startup capex

IRC-TX 02/05/2010

Investment Research Challenge- Texas STUDENT RESEARCH 8

(excluding inventory investment), with an additional $25,000 per year in sustaining capex. These projections were derived from

management guidance and historical capital expenditure data. It is anticipated that Rent-A-Center will place particular emphasis

on store development beginning in 2012 as market conditions improve and credit restrictions loosen, resulting in significantly

higher capital expenditures. We also project a schedule of account buyouts over the next five years. Revenues from account

acquisitions are estimated at 50% of the average rent-to-own store revenues due to high attrition of customer accounts, as

indicated by management. See Exhibit 10. Rent-A-Center’s store growth will allow it to further take advantage of the industry’s

temporarily increased customer base caused by decreased credit availability.

Rent-A-Center is also expected to improve revenues through increased sales of add-on units. Rent-A-Center’s revenues

decreased 4.6% in 2009. This decrease is believed to be the result of a 3.5% reduction in same store sales largely attributed to a

decrease in units per rental agreement as well as a reduction in stores related to Rent-A-Center’s 2007 store restructuring. The

reduction in units per agreement is likely the result of recent negative economic conditions and the effect of these conditions on

consumer spending. Rent-A-Center’s management has indicated its intent to improve the number of units per agreement

through a heightened focus on product offerings and advertising specifically targeting the sale of add-on units. These efforts

will likely result in improved revenues in the short to mid-term as same store sales return to our projected mature growth rate of

1.5%. However, this strategy is not expected to provide a source of significant long term growth.

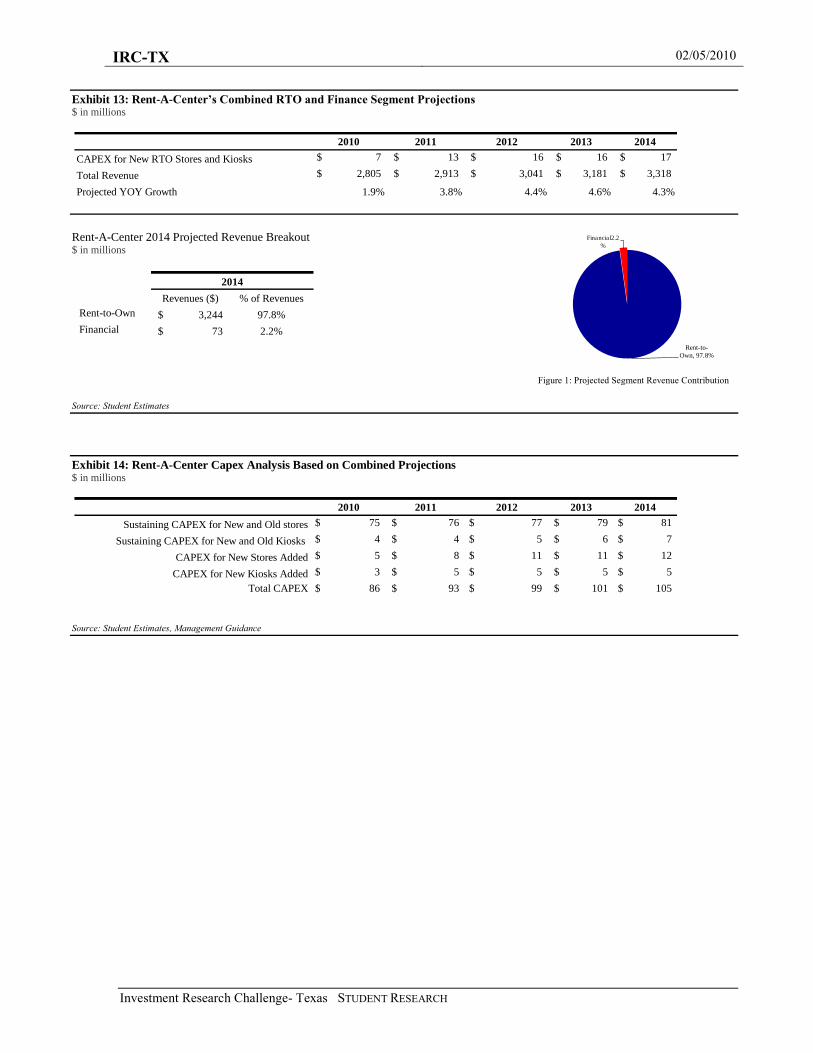

It is further anticipated Rent-A-Center will improve revenues through the continued addition of financial services kiosks to its

existing stores. Rent-A-Center currently operates financial services kiosks at 353 of its 3,007 stores at a start up cost of $50,000

per store and ongoing costs of $120,000 to $144,000 per store per year. Each kiosk generates revenues of approximately

$163,000 per year. Rent-A-Center plans to add 50 additional kiosks in 2010 and hopes to improve its return per kiosk to around

$240,000 per year as its operational efficiency improves. Rent-A-Center intends to continue to add kiosks at a rate of about 100

stores per year for the next four to six years, providing a moderate contribution to revenue growth. Given management’s mature

kiosk revenue estimates, it does not appear likely the firm will improve its return per kiosk beyond $220,000 per year. This

analysis assumes revenue growth for the kiosks on a five-year schedule, similar to that of the rent-to-own stores. See Exhibit 11.

There is no indication Rent-A-Center’s financial services operations will become the focal points of its stores, limiting this

segment’s potential for future growth. See Exhibits 13 and 14 for combined rent-to-own and financial segment projections and

capital expenditure calculations.

Long Term Growth

Rent-A-Center’s long term growth should be less extensive, limited by a reduction in future store growth, the maturation of its

existing stores, increased competition within the industry, and management’s lack of a clearly defined long term growth

strategy. These limitations will likely result in long term growth more in line with that of the economy as a whole.

It is not anticipated Rent-A-Center can continue its historical rate of acquisitions and/or store growth in the long term. Rent-A-

Center and its closest competitor, Aaron’s, Inc., account for almost 60% of existing rent-to-own stores. The remainder of the

market consists of small regional players and independents, leaving little potential for a major acquisition. Rent-A-Center has

indicated its intent to acquire store accounts from smaller competitors, but even this strategy will be restricted somewhat by the

limited room for expansion in Rent-A-Center’s existing markets. Barring entry into international markets, a move for which no

clear plan has yet been articulated, Rent-A-Center’s store growth will most likely be stymied within the next five to seven years.

Despite the addition of acquired accounts, it is unlikely existing stores can contribute sufficient revenues to maintain historical

growth rates. According to Rent-A-Center’s management, the profitability of its existing stores tends to grow at a slower rate

after the first five years with mature growth estimated at 1% to 3% per year. As previously indicated, the contributions of Rent-

A-Center’s financial services operations should be moderate at best. As a result, Rent-A-Center’s same store revenue growth

will likely decrease as its rate of store growth begins to decline and its existing stores mature, relegating long term growth to a

rate more in line with that of the economy as a whole.

Rent-A-Center’s long term revenue growth will be further hindered by management’s lack of any clearly defined strategy

beyond the expansion of its financial services operations. The most likely source of potential future growth would involve the

firm’s expansion into alternative distribution channels. As previously discussed, Rent-A-Center is presently testing a strategy

whereby it establishes a presence in certain large scale retail stores to provide a purchasing option to customers who do not

qualify for store credit. This strategy could exponentially increase Rent-A-Center’s customer reach and alleviate some of the

stigma associated with the rent-to-own purchase model. However, due to the limited implementation of this strategy to date,

this potential revenue source was not included in this analysis.

Margins

Over the next five years, Rent-A-Center’s overall growth will likely be curbed by its increasingly competitive environment. We

anticipate more intense rivalry within the industry as Aaron’s aggressive growth continues. Both Rent-A-Center and Aaron’s

currently provide low price guarantees. As Aaron’s store volume increases and its customer reach grows, these guarantees will

likely begin to more negatively impact Rent-A-Center’s margins. Furthermore, Aaron’s recently increased focus on its core

business model following the disposal of its corporate furnishings division should place each additional store in more direct

IRC-TX 02/05/2010

Investment Research Challenge- Texas STUDENT RESEARCH 9

competition with Rent-A-Center. The combination of Aaron’s growth and more directly targeted stores should create

downward pricing pressure, decreasing both Rent-A-Center’s margins and those of the industry as a whole.

These downward pricing pressures should be partially offset by the positive margin impact of Rent-A-Center’s increased sale of

add-ons and more efficient integration of its financial services operations, buttressed by improvements in the overall economy.

Margins should be further bolstered by cost savings related to the implementation of a new inventory management system,

expected to be in place in all Rent-A-Center stores by the end of the first quarter 2010. This system was implemented in 64% of

the stores during the fourth quarter of 2009. Ultimately, increased competition is anticipated to decrease margins to about

12.5% of revenues.

Conclusion

Despite a reduction in growth and increased competition, Rent-A-Center is expected to continue to produce strong free cash

flow. The firm’s dominant position in the industry will allow it to maintain sufficient revenues and margins to provide positive

returns to investors. Furthermore, the company’s expansion into alternative distribution channels could dramatically improve

future revenues, providing the exponential future growth management has sought from financial services segment.

Sensitivity

The discounted cash flow analysis is particularly sensitive to changes in Rent-A-Center’s beta, future revenue growth, and

EBITDA margins. See Figure 5 to the right and Exhibit 15. The beta was derived from the last three years’ weekly correlation

with the S&P 500 in order to provide a tight confidence

interval while minimizing trading bias. In light of Rent-

A-Center’s current market price, the market appears

overly pessimistic regarding revenue growth and

EBITDA margins. This is likely due to market

uncertainty regarding the economy as a whole, Rent-A-

Center’s reduced margins in recent years, and questions

regarding the firm’s ability to successfully integrate its

financial services operations. It would required a 1.5%

reduction in the revenue growth rate or a 0.8% reduction

in the EBITDA margin each year to reduce our intrinsic

value to the current market price. As Rent-A-Center's

revenues grow and its margins remain at an acceptable

level, as further detailed above, the market price should

increase towards the projected intrinsic value.

Comparables Analysis

A comparables analysis provided further support Rent-A-Center is undervalued at this time. The firm was compared to its

identified peer group index including Aaron’s, Inc., Family Dollar Stores, Inc., 99¢ Only Stores, Dollar Tree Stores, Inc., Dollar

Financial Corp., Advance America, Cash Advance Centers, Inc., EZCORP, Inc., and Cash America International, Inc. Rent-A-

Center appeared relatively undervalued compared to its peers, resulting in an estimated intrinsic value for the firm of $27.81,

27%, higher than its current market price. See Exhibit 16.

DCF Valuation with Terminal Value Multiple In addition to pure DCF and comparable valuations, a value was derived through a combination of the first five years cash flows

and a terminal value determined by a P/E multiple applied to the final 12 months’ earnings. Two multiples were utilized

including the trailing 12 month P/E for Rent-A-Center and the P/E for the company’s identified peer group. This analysis

resulted in values of $23.13 and $ 31.80, respectively; 6% and 45% above its current price. See Exhibit 17.

Investment Risks

Proposed legislation could negatively impact Rent-A-Center’s margins. On December 11, 2009, the United States House of

Representatives passed the Wall Street Reform and Consumer Protection Act of 2009 which, if enacted, would establish a new

federal agency responsible for the regulation of consumer financial products and services. In its current form, this legislation

does not appear applicable to the rent-to-own industry. However, if modified or interpreted to include this industry, the

legislation could subject the rent-to-own transaction to consumer lending restrictions. Similar restrictions are in place in three

states in which Rent-A-Center operates. In these states, Rent-A-Center offers merchandise through installment sales, rather than

through its traditional business model. Any extension of these restrictions to the remaining 47 states could limit assessable

interest rates and require similar changes to the company’s business model. Any limitation on interest rates applicable to the

rent-to-own transaction could severely impact Rent-A-Center’s margins.

Rent-A-Center’s failure to successfully integrate its financial services operations could limit its growth potential. Rent-

A-Center currently operates financial services kiosks at 353 stores at a cost of $120,000 to $144,000 per kiosk per year. Each

Figure 5: Sensitivity Analysis

$16

$20

$24

$28

$32

$36

$40

$44

Revenue

Growth

EBITDA

Margin

Tax Rate Capex Working

Capital

Debt Beta Terminal

Growth

Rate

Sensitivity Variable

IV/S

ha

re

IRC-TX 02/05/2010

Investment Research Challenge- Texas STUDENT RESEARCH 10

kiosk generates revenues of approximately $163,000 per year. Rent-A-Center plans to add 50 additional kiosks in 2010. At its

current rate of return, these additional kiosks would only generate $950,000 in additional profits. Rent-A-Center hopes to

increase its per kiosk revenues to approximately $240,000 per year, or $180,000 in gross profit, but it has yet to demonstrate its

ability to do so. Rent-A-Center must greatly improve its per kiosk return to warrant continued long term investment in this line

of business. A failure to do so would likely result in the discontinuation of Rent-A-Center’s financial services operations,

reducing the company’s overall potential for future growth.

Rent-A-Center’s failure to address market saturation could hamper future growth. Rent-A-Center’s historical growth has

been largely supported by increasing store numbers. At this time, Rent-A-Center estimates its expansion in its existing markets

will be capped at about 3,400 stores, a mere 400 more than it currently operates. This estimate may prove overly optimistic if

Rent-A-Center’s closest competitor, Aaron’s, continues its current rate of store growth, projected at 5% to 9% in 2010. To

achieve continued long term growth, Rent-A-Center must either expand its existing markets or its lines of business within those

markets. At this time, Rent-A-Center has not identified a strategy for international expansion, and has only just begun efforts in

to enter additional distribution channels. A failure to do so before existing stores mature (existing stores experience decreased

growth approximately 5 years after opening), could significantly impact long term revenues.

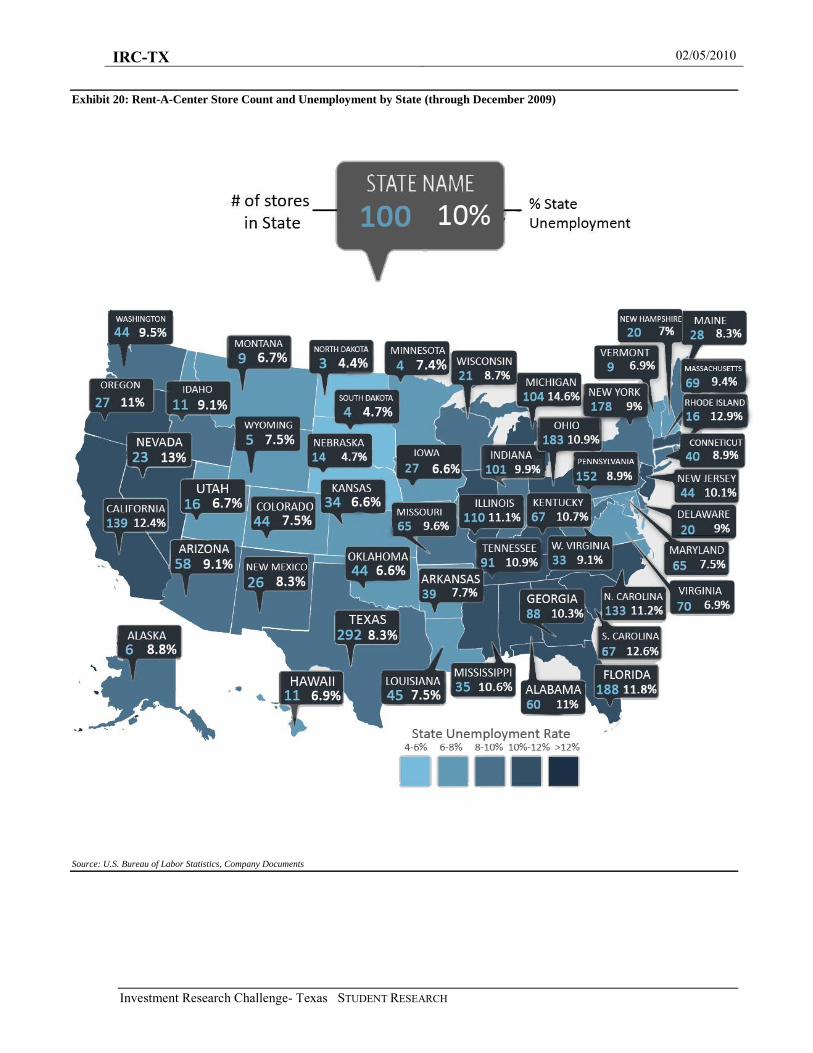

High unemployment rates could limit Rent-A-Center’s customer pool. Rent-A-Center customers must provide proof of

employment to rent or procure financial services from the company. This could prove increasingly difficult as more than 70%

of rent-to-own customers fall into a demographic group that has been disproportionately impacted by the recession. [See

customer profile]. Though it has not negatively impacted the firm to date (See Exhibit 18), continued high unemployment,

currently as high as 15% in certain demographic segments, could substantially reduce Rent-A-Center’s available customer pool.

Currently, states with greater than 9% unemployment account for approximately 56% of Rent-A-Center’s revenues. See Exhibit

20.

Declining consumer electronics prices could decrease the need for the rent-to-own business model. Consumer electronics

currently constitute 36% of Rent-A-Center’s rental revenue. In recent years, consumer electronics prices have fallen due to both

improved technologies and increased competition. In particular, the recent demise of Circuit City has encouraged efforts of

both specialty and more generalized retailers to seek a greater share of the consumer electronics market, sparking price

competition and more aggressive selling techniques. Should these trends continue, Rent-A-Center’s traditional customer base

may no longer require payment plans to obtain the electronic goods they desire.

Entry of big box retailers could substantially impact margins. The rent-to-own industry is currently dominated by two

relatively small competitors, Rent-A-Center and Aaron’s, Inc. As a result, there has been limited price competition, allowing

for higher profit margins. Entry by a substantially larger retailer with greater consistent foot traffic, significantly deeper

pockets, and stronger leverage with suppliers could ignite a protracted price war that could severely impact margins.

IRC-TX 02/05/2010

Investment Research Challenge- Texas STUDENT RESEARCH 11

Exhibit 1: Institutional and Insider Ownership Breakdown

Figure 1: The percent of institutional investors by investment style.

Source: Yahoo Finance, Rent-A-Center.com

Holder Shares % Out Reported

Barclays Global Investors UK Holdings Ltd 6,008,640 9.09 30-Sep-09

HOTCHKIS & WILEY CAPITAL MANAGEMENT, LLC 3,686,085 5.58 30-Sep-09

VANGUARD GROUP, INC. (THE) 2,987,254 4.52 30-Sep-09

STATE STREET CORPORATION 2,829,013 4.28 30-Sep-09

Robeco Investment Management, Inc. 2,633,295 3.98 30-Sep-09

Bank of New York Mellon Corporation 2,125,894 3.22 30-Sep-09

River Road Asset Management, LLC 1,993,354 3.02 31-Dec-09

Brandywine Global Investment Management, LLC 1,682,123 2.54 30-Sep-09

NORTHERN TRUST CORPORATION 1,680,998 2.54 30-Sep-09

ARTISAN PARTNERS LIMITED PARTNERSHIP 1,594,900 2.41 30-Sep-09

Holder Shares % Out Reported

FIDELITY ADVISOR SMALL CAP FUND 1,581,400 2.39 31-Aug-09

HOTCHKIS AND WILEY MID-CAP VALUE FUND 1,434,800 2.17 30-Sep-09

ARTISAN SMALL CAP VALUE FUND 955,785 1.45 30-Sep-09

American Beacon Small Cap Value Fd 926,950 1.4 30-Nov-09

ISHARES RUSSELL 2000 INDEX FD 849,905 1.29 30-Nov-09

VANGUARD SMALL-CAP INDEX FUND 805,353 1.22 30-Jun-09

JNL Variable LLC-JNL/Mellon Cap JNL 5 Fd 623,000 0.94 30-Sep-09

VANGUARD TOTAL STOCK MARKET INDEX FUND 612,075 0.93 30-Jun-09

MIDCAP SPDR TRUST SERIES I 607,072 0.92 30-Sep-09

VANGUARD SMALL CAP VALUE INDEX FUND 522,916 0.79 30-Jun-09

TOP INSTITUTIONAL HOLDERS

TOP MUTUAL FUND HOLDERS

29%

12%

33%

22%

4%

Investment Style of Institutional Holders

Value Index Other Growth Income

IRC-TX 02/05/2010

Investment Research Challenge- Texas STUDENT RESEARCH 12

Exhibit 2: Macro-Industry Analysis

Figure 1: Rent-To-Own industry growth versus US GDP since 1996. Figure 2: Rent-To-Own industry revenue growth since 1995.

Source: The Association of Progressive Rental Organizations, the United States Bureau of Economic Analysis, Student Calculations

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

% C

han

ge

in R

even

ues

/ G

DP

RTO Industry vs. U.S. GDP

RTO Industry

U.S. GDP

0

1

2

3

4

5

6

7

8

Rev

enu

e (B

illi

on

s)

RTO Industry Revenues

Inflation Adjusted 2005

(billions) % change

Inflation Adjusted 2005

(trillions) % change

1995 $5.00 $9.09

1996 $5.10 2.00% $9.43 3.74%

1997 $5.35 4.90% $9.85 4.46%

1998 $5.63 5.23% $10.28 4.36%

1999 $5.86 4.09% $10.78 4.83%

2000 $6.01 2.56% $11.23 4.14%

2001 $6.18 2.83% $11.35 1.08%

2002 $6.51 5.34% $11.55 1.81%

2003 $6.58 1.08% $11.84 2.49%

2004 $6.82 3.65% $12.26 3.57%

2005 $6.70 -1.76% $12.64 3.05%

2006 $6.59 -1.64% $12.98 2.67%

2007 $5.93 -10.02% $13.25 2.14%

2008 $5.99 1.01% $13.31 0.44%

2009 $6.37 6.34% $12.93 -2.85%

IRC-TX 02/05/2010

Investment Research Challenge- Texas STUDENT RESEARCH 13

Exhibit 3: Rent-To-Own Industry Data

Figure 1: Rent-To-Own industry by household income. Figure 2: Rent-To-Own industry by education.

Figure 3: Rent-To-Own industry by education. Figure 4: Rent-To-Own industry by ethnicity.

Source: The Association of Progressive Rental Organizations, Student Calculations

Exhibit 4: Customer Base

Figure 1: Rent-To-Own customers served since 1995. Figure 2: Rent-To-Own industry revenue per customer since 1995.

Source: The Association of Progressive Rental Organizations, Student Calculations

0%

5%

10%

15%

20%

25%

30%

35%

40%

Under $15,000 $15 - $23,999 $24 - $35,999 $36 - $49,999 $50 - $74,999

Income

2009

2004

1999

1994

0%

10%

20%

30%

40%

50%

60%

70%

High School Graduate

Some College College Graduate

Less than High School

Graduate School

Education

2009

2004

1999

1994

0%

5%

10%

15%

20%

25%

30%

35%

40%

Under 25 25-34 35-44 45-54 55-64 65 and over

Age

2009

2004

1999

1994

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Caucasion Black Hispanic Other

Ethnicity

2009

2004

1999

1994

0

1

1

2

2

3

3

4

4

5

Num

ber

of

Cust

om

ers

Ser

ved

(m

illions)

Customers Served

0

500

1,000

1,500

2,000

2,500

3,000

Rev

enue

per

Cust

om

er

Industry Revenue Per Customer

IRC-TX 02/05/2010

Investment Research Challenge- Texas STUDENT RESEARCH 14

Exhibit 5: Unbanked Consumer Data

Figure 1: Percent of unbanked households by income. Figure 2: Percent of unbanked households by age.

Figure 3: Percent of unbanked households by education level. Figure 4: Percent of unbanked households by homeownership status.

Figure 5: AFS products used by unbanked households.

Source: FDIC National Survey of Unbanked and Underbanked Households, Student Calculations

0%

5%

10%

15%

20%

25%

30%

No High School Degree High School Degree Some College College Degree

Perc

en

tage o

f H

ou

seh

old

s

Unbanked Households by Educational Level

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Homeowner Non-homeowner

Perc

en

tage o

f H

ou

seh

old

s

Unbanked Households by Homeownership Status

0.0% 20.0% 40.0% 60.0% 80.0% 100.0%

Any AFS Product

Non-Bank Money Order

Non-Bank Check Cashing

Payday Lending

Pawn Shops

RALs

RTO

Used Never Used Use Unknown

Specific AFS Products Used by Unbanked Households

Note: Percentages do not always sum to 100 because of the rounding of household weights to

represent population totals

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

< $15K $15k-$30K $30k-$50K $50k-$75K At least $75K

Unbanked Households by Income

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Age 15-24 Age 25-34 Age 35-44 Age 45-54 Age 55-64 Age 65+

Perc

en

tage o

f H

ou

seh

old

s

Unbanked Households by Age

IRC-TX 02/05/2010

Investment Research Challenge- Texas STUDENT RESEARCH 15

Exhibit 6: Underbanked Consumer Data

Figure 1: Percent of underbanked households by income. Figure 2: Percent of underbanked households by age.

Figure 3: Percent of underbanked households by education level. Figure 4: Percent of underbanked households by homeownership status.

Figure 5: AFS products used by unbanked households.

Source: FDIC National Survey of Unbanked and Underbanked Household, Student Calculations

0%

5%

10%

15%

20%

25%

30%

< $15K $15k-$30K $30k-$50K $50k-$75K At least $75K

Perc

en

tage o

f H

ou

seh

old

s

Underbanked Households by Income

0%

5%

10%

15%

20%

25%

30%

Age 15-24 Age 25-34 Age 35-44 Age 45-54 Age 55-64 Age 65+

Perc

en

tage o

f H

ou

seh

old

s

Underbanked Households by Age

0%

5%

10%

15%

20%

25%

No High School Degree

High School Degree Some College College Degree

Perc

en

tage o

f H

ou

seh

old

s

Underbanked Households by Educational Level

44%

45%

46%

47%

48%

49%

50%

51%

52%

53%

Homeowner Non-homeowner

Perc

en

tage o

f H

ou

seh

old

s

Underbanked Households by Homeownership Status

0.0% 20.0% 40.0% 60.0% 80.0% 100.0%

Any AFS Product

Non-Bank Money Order

Non-Bank Check Cashing

Payday Lending

Pawn Shops

RALs

RTO

Used Never Used Use Unknown

Specific AFS Products Used by Underbanked

Note: Percentages do not always sum to 100 because of the rounding of household weights to represent population totals

IRC-TX 02/05/2010

Investment Research Challenge- Texas STUDENT RESEARCH 16

Exhibit 7: Rent-A-Center vs. Aarons Comparison Analysis $ in millions

Source: CapitalIQ, Company Documents, The Association of Progressive Rental Organizations

PROFITABILITY COMPARISON - RCII vs. AAN

2009 2008 2007 2006 2005 2004 2003 2002 2001 2000 1999 1998 1997 1996

Rent-A-Center EBITDA Margin % 12.7% 12.5% 13.5% 14.6% 14.0% 16.8% 19.1% 19.6% 16.8% 19.1% 17.5% 16.7% 17.2% 16.6%

Return on Assets % 7.2% 6.7% 7.1% 7.9% 8.2% 10.9% 13.4% 13.5% 9.5% 10.3% 7.9% 7.5% 15.0% 12.1%

Return on Capital % 8.9% 8.1% 8.5% 9.7% 10.5% 13.8% 16.2% 15.9% 10.8% 11.5% 9.3% 9.1% 17.7% 13.8%

Return on Equity % 14.2% 13.8% 8.1% 11.7% 16.8% 19.6% 22.2% 22.4% 10.3% 19.3% 13.3% 8.7% 18.6% 16.2%

Aarons Inc. EBITDA Margin % 12.4% 11.4% 11.2% 11.8% 11.6% 11.5% 10.9% 10.1% 7.6% 12.3% 12.8% 12.6% 13.0% 12.7%

Return on Assets % 8.7% 7.4% 7.0% 7.7% 8.2% 8.4% 7.6% 6.9% 4.2% 8.9% 9.6% 9.5% 9.7% NA

Return on Capital % 11.7% 10.0% 9.2% 10.3% 11.2% 11.8% 10.6% 9.3% 5.3% 10.9% 11.9% 11.7% 11.9% NA

Return on Equity % 13.6% 12.0% 11.5% 13.6% 14.3% 15.1% 12.1% 11.0% 5.8% 13.9% 14.5% 15.1% 16.4% NA

0%

5%

10%

15%

20%

25%

1994 1996 1998 2000 2002 2004 2006 2008 2010

EBITDA Margin %

Rent-A-Center Aarons Inc.

0%

5%

10%

15%

20%

25%

1994 1996 1998 2000 2002 2004 2006 2008 2010

ROE%

Rent-A-Center Aarons Inc.

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

1994 1996 1998 2000 2002 2004 2006 2008 2010

ROIC%

Rent-A-Center Aarons Inc. -20%

0%

20%

40%

60%

80%

100%

120%

140%

160%

Gro

wth

Ra

te

RCII & AAN Revenue Growth

RCII

AAN

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

% o

f R

TO

In

du

stry

Rev

en

ue

RTO Industry Market Share

Others

AAN

RCII

Figure 1: EBITDA comparison

Figure 3: ROIC Comparison

Figure 5: Rent-To-Own Industry Participant Market Share

Figure 2: Return on Equity Comparison

Figure 4: Industry Market Share Comparison

IRC-TX 02/05/2010

Investment Research Challenge- Texas STUDENT RESEARCH 17

Exhibit 8: Available Consumer Credit in the Market

Source: Bloomberg

Exhibit 9: Beta Analysis

Time Span Beta vs S&P 500

1 Year 1.12

3 Year 1.22 Base Case

5 Year 1.19

10 Year 1.05

Source: Yahoo Finance, Student Calculations

-5%

0%

5%

10%

15%

20%

YOY % Change in Available Consumer Credit

IRC-TX 02/05/2010

Investment Research Challenge- Texas STUDENT RESEARCH 18

Exhibit 10: Discounted Cash Flow Model $ in millions

Source: Company Documents, Student Estimates

Model DriversHistoricals

2005 2006 2007 2008 2009 Hist Ave. 2010 2011 2012 2013 2014

Revenue Growth Rate 4.1% 19.4% -0.8% -4.6% 4.5% 1.9% 3.8% 4.4% 4.6% 4.3%

EBITDA Margin 14.0% 14.6% 13.5% 12.5% 13.1% 13.4% 13.0% 13.3% 13.0% 12.75% 12.5%

CAPEX Growth Rate 40.2% 20.9% -39.3% 10.0% 7.9% 25.9% 8.8% 5.8% 2.9% 3.6%

Debt_t / Operating Assets_t 37.2% 47.2% 47.9% 36.6% 29.1% 40.2% 27.5% 25.0% 25.0% 25.0% 25.0%

Working Capital Net_t / Operating Assets_t-1 -16.6% -7.9% -7.0% -9.0% -10.1% -11.5% -10.0% -9.0% -8.1% -6.9%

Tax Rate 35% 35% 37% 34% 37% 35.9% 38% 38% 38% 38% 38%

Required Return on Debt 5.6% 4.5% 7.5% 7.3% 3.6% 5.7% 3.9% 4.9% 5.9% 6.9% 7.9%

Future - Your Projections of Future Performance

Probably need to fill this column in by hand from Reuters or Bloomberg

See also Preferred Stockin cell D70 below. If that cell is empty, iInsert an estimate of market value of preferred stock.

Any historical data items in pink cells that Compustat fails to entermust be entered by hand from Reuters or Bloomberg Hardcode Imported

Data

"q" is the estimate of the portion of total acquisitions that are depreciable. See the

'depreciation' page for an explanation.

(In calculations that use "q" it is constrained to be between 0 and 1.)

Free Cash Flow Forecasts

2005 2006 2007 2008 2009 now 2010 2011 2012 2013 2014 2015

Total Assets (book value) 1,948.66 2,740.96 2,626.94 2,496.70 2,444.00 2,444.00

less: Non-Operating Cash & ST Invest 0.00 0.00 0.00 0.00 0.00 $0.00

less: Non-Cash Non-Operating Assets 0.00 0.00 0.00 0.00 0.00 0.00

Operating Assets (Book Value) 1,948.66 2,740.96 2,626.94 2,496.70 2,444.00 2444.00 2418.55 2506.38 2573.12 2642.15 2706.86

Working Capital (Book Value) -161.22 -323.63 -215.45 -184.83 -224.70 -224.70

Work Cap Net of Ex Cash & ST Invest -161.22 -323.63 -215.45 -184.83 -224.70 -224.70 -281.06 -241.85 -225.57 -208.20 -182.11

Long-Term Debt (Book Value) 724.10 1,293.30 1,259.30 912.80 711.16 711.16 665.10 626.60 643.28 660.54 676.72

Interest Expense 40.70 58.56 94.78 66.24 25.95 25.69 30.47 37.72 45.33 53.21

Depreciation Expense 69.62 55.70 71.30 85.27 68.00 68.00 84.20 87.74 89.42 92.87

Revenue from Operations 2,339.11 2,433.91 2,906.12 2,884.17 2,751.96 2804.79 2912.70 3041.39 3181.30 3317.81

less: Operating Expenses 2,082.18 2,138.67 2,585.18 2,609.80 2,460.50 2510.17 2600.77 2725.01 2859.69 2992.08

plus: Depreciation & Amort. 69.62 61.22 71.30 85.27 68.63 70.00 74.00 79.00 84.00 89.00

EBITDA 326.55 356.46 392.24 359.64 360.09 364.62 385.93 395.38 405.62 414.73

less: Taxes 73.33 61.05 40.02 81.72 102.52 170.00 118.53 120.22 122.21 123.78

less: Cap Ex. 60.20 84.40 102.00 61.90 68.09 85.71 93.21 98.58 101.46 105.08

less: Acquisitions 38.32 657.38 20.11 15.70 7.00 depreciable

non-depr. 13.21 39.62 39.62 39.62 26.41

less: Incr. in working capital -0.52 -162.41 108.18 30.62 -39.87 -56.36 39.20 16.28 17.38 26.09

Minority Interest Percentage 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

FCF from Operations (adj. for min. int.) 155.22 -283.96 121.93 169.70 222.35 152.07 95.37 120.67 124.95 133.37 137.37

PV's = 140.56 81.48 95.29 91.20 89.98

Acctg Operating Earngs (adj. for min. int.) 157.17 196.17 221.39 149.21 167.86 Hist Ave. 166.73 174.51 172.77 171.29 168.96 0.00

Operating Earnings per (current) Share 2.38 2.97 3.36 2.26 2.54 2.53 2.64 2.62 2.60 2.56 0.00

Operating Earnings Growth 24.8% 12.9% -32.6% 12.5% 4.4% -0.7% 0.1%

1-year Projected Earnings Growth 5-year

Rev / Op Assets 1.20 0.89 1.11 1.16 1.13 1.16 1.16 1.18 1.20 1.23

FCF / Op Assets 0.08 -0.10 0.05 0.07 0.09 0.06 0.04 0.05 0.05 0.05

Historicals (million $) Future (million$)

IRC-TX 02/05/2010

Investment Research Challenge- Texas STUDENT RESEARCH 19

Exhibit 11: Rent-A-Center Historical Performance Store Profile $ in millions

Source: CapitalIQ, Company Documents

Rent-A-Center’s Rent-To-Own Segment Projections $ in millions

Source: Student Estimates, Management Guidance

Exhibit 12: Rent-A-Center’s Finance Segment Projections $ in millions

Source: Student Estimates, Management Guidance

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Total Stores 2440 2522 2623 2725 2977 3188 3056 3688 3308 3259 3007

Revenue (millions) $ 1,415 $ 1,599 $ 1,805 $ 2,007 $ 2,225 $ 2,310 $ 2,331 $ 2,418 $ 2,881 $ 2,841 $ 2,694

Rev/Store (thousands) 580$ 634$ 688$ 737$ 747$ 724$ 763$ 656$ 871$ 872$ 896$

YOY Rev/Store Growth 9.30% 8.57% 7.05% 1.46% -3.07% 5.29% -14.04% 32.80% 0.12% 2.77%

5-Year Average Rev/Store (thousands) $ 811

5-Year Rev/Store CAGR 3.27%

2010 2011 2012 2013 2014

Stores at Beginning 3007 3037 3092 3167 3242

New Stores Added 30 55 75 75 80

CAPEX for New Stores 5$ 8$ 11$ 11$ 12$

Revenue from New Stores 13$ 46$ 100$ 163$ 232$

Number of Accounts Bought Out 25 75 75 75 50

Revenue from Account Buyouts 10$ 31$ 31$ 31$ 20$

Account Buyout Cost 13$ 40$ 40$ 40$ 26$

Revenue from Previously Existing Stores 2,721$ 2,772$ 2,844$ 2,918$ 2,992$

Total Revenue 2,744$ 2,849$ 2,975$ 3,111$ 3,244$

YOY RTO Segment Revenue Growth 1.9% 3.8% 4.4% 4.6% 4.3%

Projected Average Rev/Store (thousands) 904$ 921$ 939$ 960$ 977$

Projected 5-Year Rev/Store CAGR: 1.57%

Assumptions (dollar values in thousands):

1) Revenue Growth Schedule for New Stores Added Year 1 Year 2 Year 3 Year 4 Year 5

$430 $760 $860 $890 $910

2) Average CAPEX Required to Open a New Store: $150

3) Average Inventory on the Floor of a Rent-A-Center Store $150

$528

5) Average Store Revenue from Account Buyouts (based on 2009 Industry Average/Store): $814

6) Stores at the Beginning of 2010: 3,007

1.50%7) Projected YOY Growth in Rev/Store, Next 5 yrs (with the exception of 2010, growth rate is 1%):

4) Average Cost of Account Buyout (10X monthly revenue multiplier less inventory):

2010 2011 2012 2013 2014

Kiosks at Beginning 353 403 503 603 703

Kiosks Added 50 100 100 100 100

Revenue from New Kiosks 4$ 14$ 28$ 44$ 64$

CAPEX for New Kiosks 3$ 5$ 5$ 5$ 5$

Total Revenue from Kiosks 60$ 63$ 67$ 70$ 73$

YOY Kiosk Revenue Growth 4.9% 5.0% 5.0% 5.0% 5.0%

Assumptions (dollar values in thousands):

1) Revenue per Kiosk is Currently Approximately $163,000 and Assumed Growth per Existing Kiosk: 5%

2) Average CAPEX to Open a Kiosk: $50,000 163,000

3) Revenue Growth Schedule for New Kiosks: Year 1 Year 2 Year 3 Year 4 Year 5

$80,000 $120,000 $150,000 $180,000 $220,000

IRC-TX 02/05/2010

Investment Research Challenge- Texas STUDENT RESEARCH 20

Exhibit 13: Rent-A-Center’s Combined RTO and Finance Segment Projections $ in millions

Rent-A-Center 2014 Projected Revenue Breakout $ in millions

Source: Student Estimates

Exhibit 14: Rent-A-Center Capex Analysis Based on Combined Projections $ in millions

Source: Student Estimates, Management Guidance

2010 2011 2012 2013 2014

CAPEX for New RTO Stores and Kiosks 7$ 13$ 16$ 16$ 17$

Total Revenue 2,805$ 2,913$ 3,041$ 3,181$ 3,318$

Projected YOY Growth 1.9% 3.8% 4.4% 4.6% 4.3%

Revenues ($) % of Revenues

Rent-to-Own 3,244$ 97.8%

Financial 73$ 2.2%

2014

2010 2011 2012 2013 2014

Sustaining CAPEX for New and Old stores $ 75 $ 76 $ 77 $ 79 $ 81

Sustaining CAPEX for New and Old Kiosks $ 4 $ 4 $ 5 $ 6 $ 7

CAPEX for New Stores Added $ 5 $ 8 $ 11 $ 11 $ 12

CAPEX for New Kiosks Added $ 3 $ 5 $ 5 $ 5 $ 5

Total CAPEX $ 86 $ 93 $ 99 $ 101 $ 105

Figure 1: Projected Segment Revenue Contribution

Rent-to-

Own, 97.8%

Financial2.2

%

IRC-TX 02/05/2010

Investment Research Challenge- Texas STUDENT RESEARCH 21

Exhibit 15: Discounted Cash Flow Sensitivity Analysis

Source: Student Calculations

2010 2011 2012 2013 2014

Intrinsic

Value IV/MV

0.9% 2.8% 3.4% 3.6% 3.3% 23.28$ 1.058

1.4% 3.3% 3.9% 4.1% 3.8% 24.72$ 1.123

base 1.9% 3.8% 4.4% 4.6% 4.3% 26.17$ 1.190

2.4% 4.3% 4.9% 5.1% 4.8% 27.66$ 1.257

2.9% 4.8% 5.4% 5.6% 5.3% 29.17$ 1.326

12.0% 12.3% 12.0% 11.8% 11.5% 20.72$ 0.942

12.5% 12.8% 12.5% 12.3% 12.0% 23.45$ 1.066

base 13.0% 13.3% 13.0% 12.8% 12.5% 26.17$ 1.190

13.5% 13.8% 13.5% 13.3% 13.0% 28.90$ 1.314

14.0% 14.3% 14.0% 13.8% 13.5% 31.63$ 1.438

37.0% 37.0% 37.0% 37.0% 37.0% 26.98$ 1.226

37.5% 37.5% 37.5% 37.5% 37.5% 26.58$ 1.208

base 38.0% 38.0% 38.0% 38.0% 38.0% 26.17$ 1.190

38.5% 38.5% 38.5% 38.5% 38.5% 25.77$ 1.171

39.0% 39.0% 39.0% 39.0% 39.0% 25.37$ 1.153

24.9% 7.8% 4.8% 1.9% 2.6% 26.17$ 1.190

25.4% 8.3% 5.3% 2.4% 3.1% 26.17$ 1.190

base 25.9% 8.8% 5.8% 2.9% 3.6% 26.17$ 1.190

26.4% 9.3% 6.3% 3.4% 4.1% 26.17$ 1.190

26.9% 9.8% 6.8% 3.9% 4.6% 26.17$ 1.190

-12.5% -11.0% -10.0% -9.1% -7.9% 26.69$ 1.213

-12.0% -10.5% -9.5% -8.6% -7.4% 26.44$ 1.202

base -11.5% -10.0% -9.0% -8.1% -6.9% 26.17$ 1.190

-11.0% -9.5% -8.5% -7.6% -6.4% 25.91$ 1.178

-10.5% -9.0% -8.0% -7.1% -5.9% 25.64$ 1.166

26.5% 24.0% 24.0% 24.0% 24.0% 26.17$ 1.189

27.0% 24.5% 24.5% 24.5% 24.5% 26.17$ 1.190

base 27.5% 25.0% 25.0% 25.0% 25.0% 26.17$ 1.190

28.0% 25.5% 25.5% 25.5% 25.5% 26.18$ 1.190

28.5% 26.0% 26.0% 26.0% 26.0% 26.18$ 1.190

Beta IV IV/MV

0.82 39.52$ 1.797

1.02 31.77$ 1.444

base 1.22 26.17$ 1.190

1.42 21.95$ 0.998

1.62 18.64$ 0.847

Terminal Growth Rate

2.50% 23.67$ 1.076

current 3.00% 26.17$ 1.190

3.50% 29.21$ 1.328

CAPEX

Working Capital % Revenues

Debt as % Assets

Revenue Growth

EBITDA margin

Tax Rate

IRC-TX 02/05/2010

Investment Research Challenge- Texas STUDENT RESEARCH 22

Exhibit 16: Comparables Valuation Analysis

Source: CapitalIQ, Student Calculations

Exhibit 17: Rent-A-Center Valuation with Terminal Value Calculated from P/E Multiple

Source: CapitalIQ Student Estimates

Rent-A-Center Identified Peer Group

Company Ticker Exchange Price Shares Market Cap

Trailing

P/E- basic

Trailing

P/E- diluted Forward P/E EV/EBITDA P/BV P/EPS P/Sales

Rent-A-Center RCII NASDAQ 21.88 66.00 1444.08 9.01 9.10 9.81 5.87 1.19 9.01 0.52

Aaron's, Inc. AAN NYSE 28.13 54.24 1525.77 14.02 14.06 12.51 6.91 1.77 14.02 0.89

Family Dollar Stores FDO NYSE 31.13 138.40 4308.39 14.51 14.57 13.57 6.57 2.92 14.51 0.58

99 Cents Only Stores NDN NYSE 15.27 68.90 1052.10 27.33 27.61 23.10 11.25 1.91 27.33 0.79

Dollar Tree, Inc. DLTR NASDAQ 49.09 88.30 4334.65 14.91 15.31 14.21 6.86 3.27 14.91 0.86

Dollar Financial Corp. DLLR NASDAQ 20.81 24.10 501.52 -119.41 -119.41 9.75 6.40 2.28 -119.41 0.97

Advance America, Cash Advance Centers, Inc. AEA NYSE 4.42 61.60 272.27 6.76 6.76 5.74 3.92 1.39 6.76 0.42

EZCORP, Inc. EZPW NASDAQ 17.44 48.70 849.33 12.07 12.25 10.36 7.33 2.04 12.07 1.42

Cash America International, Inc. CSH NYSE 36.74 29.30 1076.48 13.74 14.10 10.47 7.57 1.68 13.74 1.00

Mean (DLLR excluded due to negative earnings) 14.04 14.22 12.47 7.03 2.02 14.04 0.81

Intrinsic Value (Based on Forward P/E) $27.81

Discount Rate (CAPM) 8.18%

2010 2011 2012 2013 2014

FCF 152.07$ 95.37$ 120.67$ 124.95$ 133.37$

PV of FCF 140.57$ 81.49$ 95.31$ 91.22$ 90.00$

Terminal EPS $2.56

P/E for Rent-A-Center 9.0

P/E for Rent-A-Center Identified Peer Group 14.0

Rent-A-Center P/E

PV (FCF Operations 10 yrs) Per share $7.54 33%

PV P/E Multiple Terminal Value $15.58 67%

Total Value Per Share $23.13

Rent-A-Center Identified Peer Group

PV (FCF Operations 10 yrs) Per share $7.54 24%

PV P/E Multiple Terminal Value $24.26 76%

Total Value Per Share $31.80

IRC-TX 02/05/2010

Investment Research Challenge- Texas STUDENT RESEARCH 23

Exhibit 18: Personal Consumption versus Personals Savings

Source: Bloomberg, Student Calculations

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

Personal Consumption Expenditure Rate % Change MOM

Personal Savings Rate % Change MOM

IRC-TX 02/05/2010

Investment Research Challenge- Texas STUDENT RESEARCH 24

Exhibit 20: Rent-A-Center Store Count and Unemployment by State (through December 2009)

Source: U.S. Bureau of Labor Statistics, Company Documents

IRC-TX 02/05/2010

Investment Research Challenge- Texas STUDENT RESEARCH 25

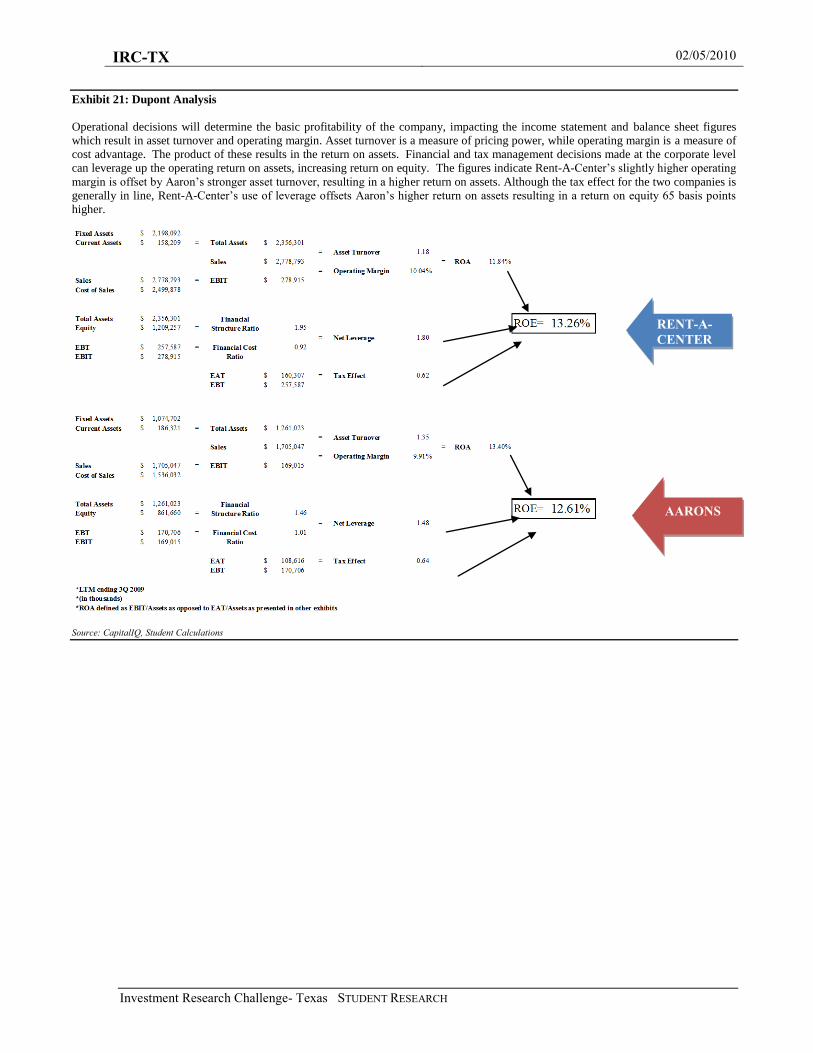

Exhibit 21: Dupont Analysis

Operational decisions will determine the basic profitability of the company, impacting the income statement and balance sheet figures

which result in asset turnover and operating margin. Asset turnover is a measure of pricing power, while operating margin is a measure of

cost advantage. The product of these results in the return on assets. Financial and tax management decisions made at the corporate level

can leverage up the operating return on assets, increasing return on equity. The figures indicate Rent-A-Center’s slightly higher operating

margin is offset by Aaron’s stronger asset turnover, resulting in a higher return on assets. Although the tax effect for the two companies is

generally in line, Rent-A-Center’s use of leverage offsets Aaron’s higher return on assets resulting in a return on equity 65 basis points

higher.

Source: CapitalIQ, Student Calculations

RENT-A-

CENTER

AARONS

IRC-TX 02/05/2010

Investment Research Challenge- Texas STUDENT RESEARCH 26

Exhibit 22: Rent-A-Center Historic Ratios

Source: CapitalIQ,

Exhibit 23: Z-Score Calculations

The Altman Z score has proven to be a reliable tool in predicting bankruptcy. Z score profiles for failing businesses often indicate a

consistent downward trend as they approach bankruptcy.

Source: www.nysscpa.org, CapitalIQ, Student Estimates

HISTORIC RISK

2005 2006 2007 2008 2009

Liquidity

Current Ratio 0.4x 0.4x 0.5x 0.5x 0.4x

Quick Ratio 0.3x 0.3x 0.4x 0.4x 0.3x

Days Inventory 0.3 NA NA NA NA

Days Payable 16.7 NA 16.2 14.4 NA

Cash Conversion Cycle (13.6) NA NA NA NA

HISTORIC PROFITABILITY ANALYSIS

2002 2003 2004 2005 2006 2007 2008 2009

Liquidity