Download - Chamber of Agribusiness Ghana (CAG)

Chamber of Agribusiness Ghana (CAG)

Agribusiness Sector Survey Report, 2020

Effects of COVID-19 on Agribusinesses in Ghana

Authored by

Kojo Ahiakpa1,2, Benjamin Karikari2, Alex Ametowobla1 & Stephen Frimpong2

May, 2020

1 Policy Development & Research (CAG), 2 Research Desk Consulting Ltd, Accra, Ghana

Page 2 of 18

Executive Summary

The flareup of the novel Coronavirus is having a significant toll on the global economy and

food markets, especially in developing countries. Food insecurity levels in Africa are on the

ascendancy. In Ghana, disruption in food supply chains may occasion imminent food

unavailability. The ramifications of COVID-19 pandemic will be severe on agribusinesses and

smallholders who are most vulnerable. Government promise to offer stimulus package to

vulnerable groups, agribusinesses and adjoining industries have been received with greater

anticipation. However, government’s roadmap to implement policies and programmes to

mitigate the associated economic effects of this pandemic is yet to be fully outlined. The

Chamber of Agribusiness Ghana as the apex body for coordinating agricultural sector players

in Ghana conducted a nation-wide survey to assess the economic effects of COVID-19

pandemic on Ghanaian agribusinesses. This is aimed at providing data-driven inputs and

proposals to government to map out immediate interventions to cushion the agribusiness sector

from the dreaded impact of the pandemic. From our study, average monthly revenue of

Ghanaian agribusiness firms reduced by 61.2 % during the COVID-19 restriction periods.

Small scale agribusiness firms suffered the largest revenue shortfalls of about 77.4 %; with

large scale agribusiness firms experiencing the least revenue shortfall over the same period.

Page 3 of 18

Contents

Executive Summary 2

List of Tables 4

List of Figures 5

Background 6

COVID-19 Global and Africa Overview 6

Survey Approach 6

COVID-19 Cases in the World, Africa and Ghana 7

COVID-19 Hotspots, Regional Case Distribution and Agribusiness Actors 8

Economic Effects of COVID-19 on Agribusinesses in Ghana 10

Measures to address the Economic Impacts of COVID-19 on Agribusinesses 13

Coping Strategies by Agribusinesses and Smallholders 14

Employee Management Strategies by Agribusinesses 15

Support for Agribusiness in Ghana 16

Post-COVID-19 Business Continuity by Agribusinesses 16

Policy Recommendations 17

Acknowledgements 18

Page 4 of 18

List of Tables

Table 1: COVID-19 cases in the World, Africa, and Ghana as of 11th May, 2020 8

Table 2: Revenue changes due to COVID-19 restrictions on Ghanaian agribusinesses 13

Page 5 of 18

List of Figures

Figure 1. Agribusiness companies and COVID-19 cases across the country 9

Figure 2. Value chain actors who participated in the survey 10

Figure 3. Agribusiness firms revenue shortfalls due to COVID-19 restriction policies 12

Figure 4. Agribusiness COVID-19 coping strategies 11

Figure 5. Agribusiness post-COVID-19 employee management strategies 12

Figure 6. Agribusiness required external supports 13

Figure 7. Decision to continue business operations without external support by agribusiness 14

Page 6 of 18

Background

COVID-19 Global and Africa overview

Governments across the world have executed diverse measures to contain the spread and lessen

impact of the coronavirus pandemic. Closure of national borders; strict contact tracing and

social distancing, travel restrictions; partial and temporary lockdowns of cities, towns, schools

and businesses, public health education, provision of shelter and food for the homeless are

among these measures across the world. In Ghana, government has closed down schools;

imposed travel bans; banned religious and social gatherings; issued partial lockdown;

suspension of consular services; public health sensitisation on improved hygiene; strict social

distancing, contact tracing and quarantining of all travellers and infected persons. The

shutdown and restrictions are already causing untold misery for informal workers and the poor,

who lead precarious lives facing hunger and malnutrition. The World Health Organisation

(WHO) has indicated that, global health systems are being overwhelmed by the worsening

coronavirus crisis. Ghana recorded the first two COVID-19 cases on 12 March, 2020, and have

since spiralled across almost all regions.

Preliminary analysis of the economic impact of the pandemic indicates a substantial go-slow

in gross domestic product (GDP) growth, petroleum revenues shortfall and import duties;

decline in tax revenues; swelling health expenditure and stringent financing conditions directly

impacting on the 2020 budget. This necessitates some cushioning actions to lessen COVID-19

effects on the Ghanaian economy, particularly the agribusiness sector which constitutes

majority of the smallholders and the vulnerable. These vulnerable groups comprises

agribusinesses including smallholder farmers and low-income earners without public support

and stand to be the most affected by this unfortunate pandemic.

Survey Approach

The survey was conducted to gain insight and knowledge of the specific challenges and effects

of COVID-19 pandemic on agribusinesses operating in the Ghanaian landscape. Semi-

structured questionnaires were administered to managers and owners of small, medium and

large-scale agribusinesses across the country using the Microsoft forms (survey platform).

Information on the current state of development of the industry were sourced from publications

from government and development institutions such as the Ghana Export Promotion Authority

(GEPA), Ministry of Trade and Industry (MoTI), Federation of Association of Ghanaian

Page 7 of 18

Exporters (FAGE) and Ministry of Food and Agriculture (MoFA). We validated the data

collection instruments in-house with key members of the Chamber of Agribusiness (CAG)

among 10 different registered agribusinesses who were subsequently excluded from the main

survey. Export managers, marketing directors, customer service managers, and general

managers directly involved with operations of agribusinesses were equally interviewed using

teleconferencing tools and social media applications such as WhatsApp. A challenge that was

faced in the administering of the questionnaire was the response time from agribusinesses. Two

(2) weeks grace period was initially given to respondents but had to be extended by one week

as some of the respondents took a longer time to respond to the questionnaires. We shared the

survey link with smallholders and agribusinesses on our social media platforms and other

media. Participants were given the privilege to express views on how the COVID-19 pandemic

is impacting their business operations and service delivery and how this is affecting staff

productivity and improvised measures taken to reduce the unexpected ramifications. In all, a

total of 110 responses were employed for the study after cleaning.

Responses from the questionnaire administered and interview from the smallholders and

agribusinesses were content analysed. Analysis was done by grouping responses in the context

of the five (5) sections in the questionnaire. Tables were provided for each section of the

questionnaire and responses gathered were recorded therein.

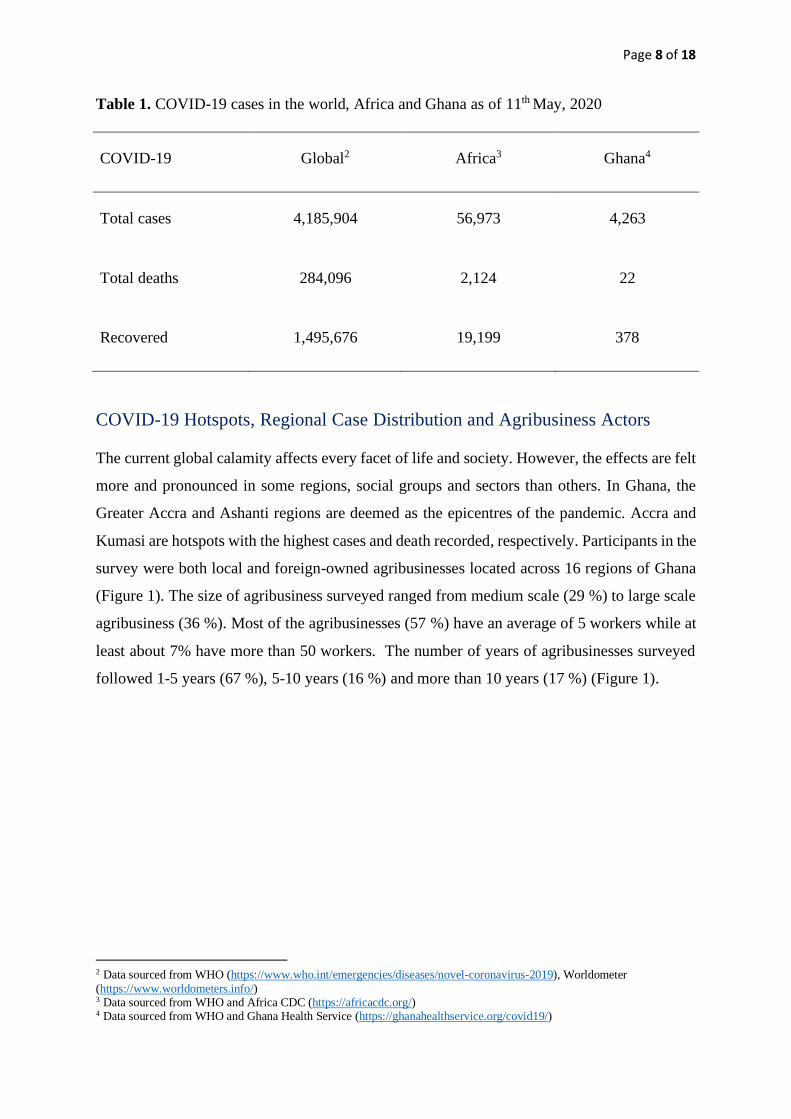

COVID-19 cases in the World, Africa, and Ghana

The COVID-19 pandemic has since spread to over 199 countries globally with estimated

4,185,904 cases recorded. Total of 284,096 deaths have since been reported globally while

1,495,676 have recovered (Table 1). In Africa, 56,973 total case have been recorded with 2,124

deaths and 19,199 recoveries according the Africa CDC. A total of 4,263 cases have been

recorded in Ghana as at 11th May, 2020 with 22 deaths and 378 recoveries (Table 1).

Page 8 of 18

Table 1. COVID-19 cases in the world, Africa and Ghana as of 11th May, 2020

COVID-19 Global2 Africa3 Ghana4

Total cases 4,185,904 56,973 4,263

Total deaths 284,096 2,124 22

Recovered 1,495,676 19,199 378

COVID-19 Hotspots, Regional Case Distribution and Agribusiness Actors

The current global calamity affects every facet of life and society. However, the effects are felt

more and pronounced in some regions, social groups and sectors than others. In Ghana, the

Greater Accra and Ashanti regions are deemed as the epicentres of the pandemic. Accra and

Kumasi are hotspots with the highest cases and death recorded, respectively. Participants in the

survey were both local and foreign-owned agribusinesses located across 16 regions of Ghana

(Figure 1). The size of agribusiness surveyed ranged from medium scale (29 %) to large scale

agribusiness (36 %). Most of the agribusinesses (57 %) have an average of 5 workers while at

least about 7% have more than 50 workers. The number of years of agribusinesses surveyed

followed 1-5 years (67 %), 5-10 years (16 %) and more than 10 years (17 %) (Figure 1).

2 Data sourced from WHO (https://www.who.int/emergencies/diseases/novel-coronavirus-2019), Worldometer

(https://www.worldometers.info/) 3 Data sourced from WHO and Africa CDC (https://africacdc.org/) 4 Data sourced from WHO and Ghana Health Service (https://ghanahealthservice.org/covid19/)

Page 9 of 18

Figure 1. Agribusiness companies and COVID-19 cases across the country (Authors’ data)

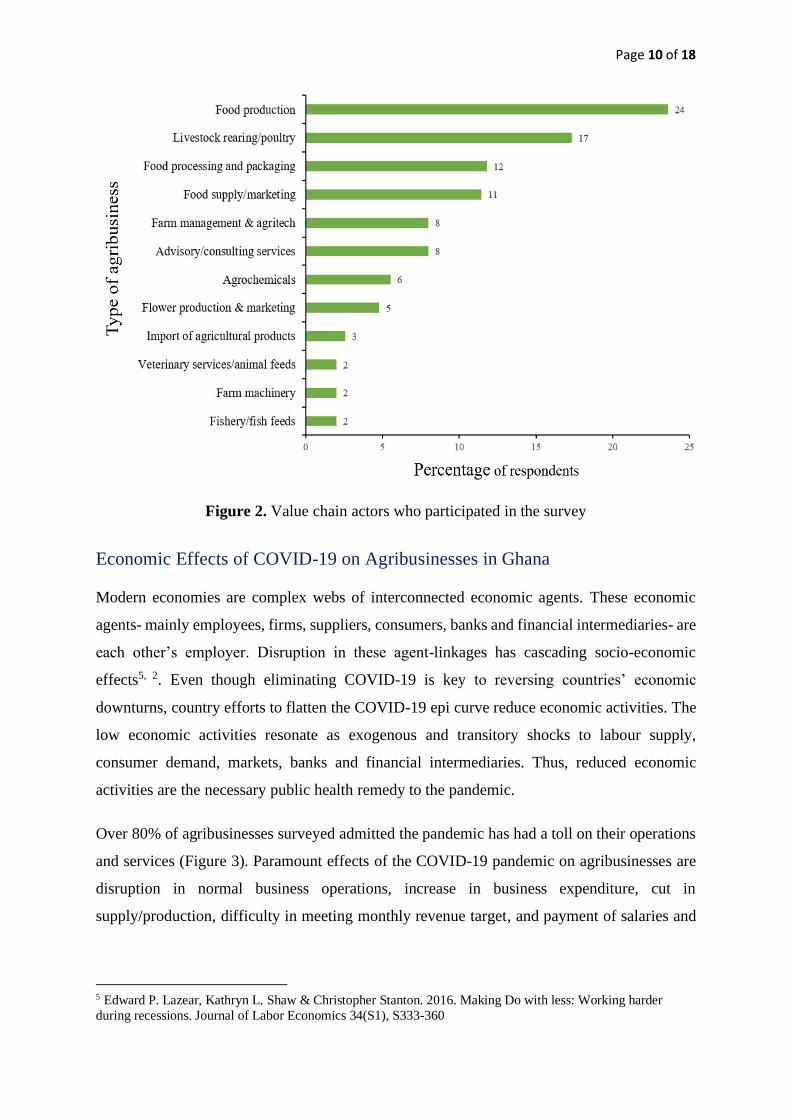

The participants comprised various actors in the agribusiness industry in Ghana (Figure 2).

Most of the participants (24 %) are involved in food production while 6 % are involved in

either veterinary services/animal feeds, farm machinery or fishery/fish feeds (Figure 2).

Page 10 of 18

Figure 2. Value chain actors who participated in the survey

Economic Effects of COVID-19 on Agribusinesses in Ghana

Modern economies are complex webs of interconnected economic agents. These economic

agents- mainly employees, firms, suppliers, consumers, banks and financial intermediaries- are

each other’s employer. Disruption in these agent-linkages has cascading socio-economic

effects5, 2. Even though eliminating COVID-19 is key to reversing countries’ economic

downturns, country efforts to flatten the COVID-19 epi curve reduce economic activities. The

low economic activities resonate as exogenous and transitory shocks to labour supply,

consumer demand, markets, banks and financial intermediaries. Thus, reduced economic

activities are the necessary public health remedy to the pandemic.

Over 80% of agribusinesses surveyed admitted the pandemic has had a toll on their operations

and services (Figure 3). Paramount effects of the COVID-19 pandemic on agribusinesses are

disruption in normal business operations, increase in business expenditure, cut in

supply/production, difficulty in meeting monthly revenue target, and payment of salaries and

5 Edward P. Lazear, Kathryn L. Shaw & Christopher Stanton. 2016. Making Do with less: Working harder

during recessions. Journal of Labor Economics 34(S1), S333-360

Page 11 of 18

wages, difficulty in honouring tax obligation/debt repayment, and threat to employees’ health

and life.

Whiles Ghana’s ‘stay in place orders’ largely exempted food supply, non-food agribusiness

operations were affected by the restrictions. Even for the agrifood supply businesses,

government lockdown and restrictions on some consumer food demand sectors, such as hotels,

educational institutions, social events, and restaurants, raptured the linkages between

agribusinesses and other interactive sectors of the economy. These disruptions interacted with

panic buying, hoarding, and expectation shocks leading to high food prices for consumers, high

food transport and delivery costs for agribusinesses, and thus, rising food inflationary

pressures. However, the low food demand and limited agribusiness operations largely offset

these inflationary pressures6.

Distortions in the agri-food supply chains is also expected to affect employment, labour,

migration, wage rates, revenue or profitability of agribusinesses, and agriculture’s contribution

to gross domestic product (GDP). For instance, agribusiness contribution to Ghana’s GDP

reduced by 19.5 % during the lockdown period7. However, no one knows how much worse the

disease will get as the disease persists. There is also the danger of subsequent waves of

infection, as was the case of the 1918 Spanish Flu. Thus, COVID-19 could push broad societal

shifts in terms of pre-pandemic behaviours and industry-wide disruption, such as restructuring

of agribusiness operations, and lead to a new normal for economic change. For these reasons,

we focus on the short-term micro-level effects of COVID-19 lockdowns and social distancing

policies on agribusiness revenue. The micro-level analysis is important as it provides a

simplified and stylised view of ongoing effects of the pandemic. While the macro-impacts are

equally important, data limitations prevent the incorporation of important economic factors,

especially in the case of agribusiness in Ghana. For instance, gained revenue due to reduced

foreign imports, wage variations, expectation shocks, and the influence of technology, such as

information communication tools, teleworking, and other marketing and distribution tools that

enhance market access are poorly captured in general equilibrium models. Also, the

restructuring of agribusiness activities due to lockdowns and restrictions will have varied

effects for agribusiness operations in Ghana. General equilibrium models may also fail to

6 See Richard Baldwin and Beatrice Weder di Mauro. 2020. Mitigating the COVID Economic Crisis: Act Fast

and Do Whatever It Takes. Centre for Economic Policy Research, CEPR Press 7 Sena Amewu, Seth Asante, Karl Pauw & James Thurlow. Impacts of COVID-19 on Production, Poverty & Food

Systems. International Food Policy Research Institute

Page 12 of 18

capture behavioural response to supply and demand for agribusiness goods and services, such

as whether the individual will feel safe to ease or maintain social distancing during and after

the stay in place orders. Therefore, micro-analysis of the effects of COVID-19 restriction

policies on agribusinesses gives detailed and policy-relevant insights.

Generally, majority of agribusiness firms in Ghana lost revenues due to COVID-19 lockdowns

and social distancing policies (Figure 3). Compared to pre-pandemic periods, Ghanaian

agribusiness firms’ average monthly revenues ranged from zero (0) to hundred (100) percent

(Figure 3).

Figure 3. Agribusiness firms revenue shortfalls due to COVID-19 restriction policies

These revenue losses stem from social distancing policies and disruption in adjacent

agribusiness industry activities. Again, in Ghana, where there is large informal sectors and

employee income is linked to daily wage activities, COVID-19 stay in place restrictions could

have a dire effect on consumer’s disposable income. Even with employees who have regular

income sources, uncertainties associated with COVID-19 lockdowns and easing of social

distancing might have prompted them to save to mitigate any future income disruptions.

Consumers might have limited their expenditure on non-food agribusiness goods and services.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Large Medium Small

Per

cent

of

pre

-pan

dem

ic

reven

ue

Agribusiness firms revenue flows

Covid-19 Revenue Levels Pre-Covid-19 Revenue Levels

Page 13 of 18

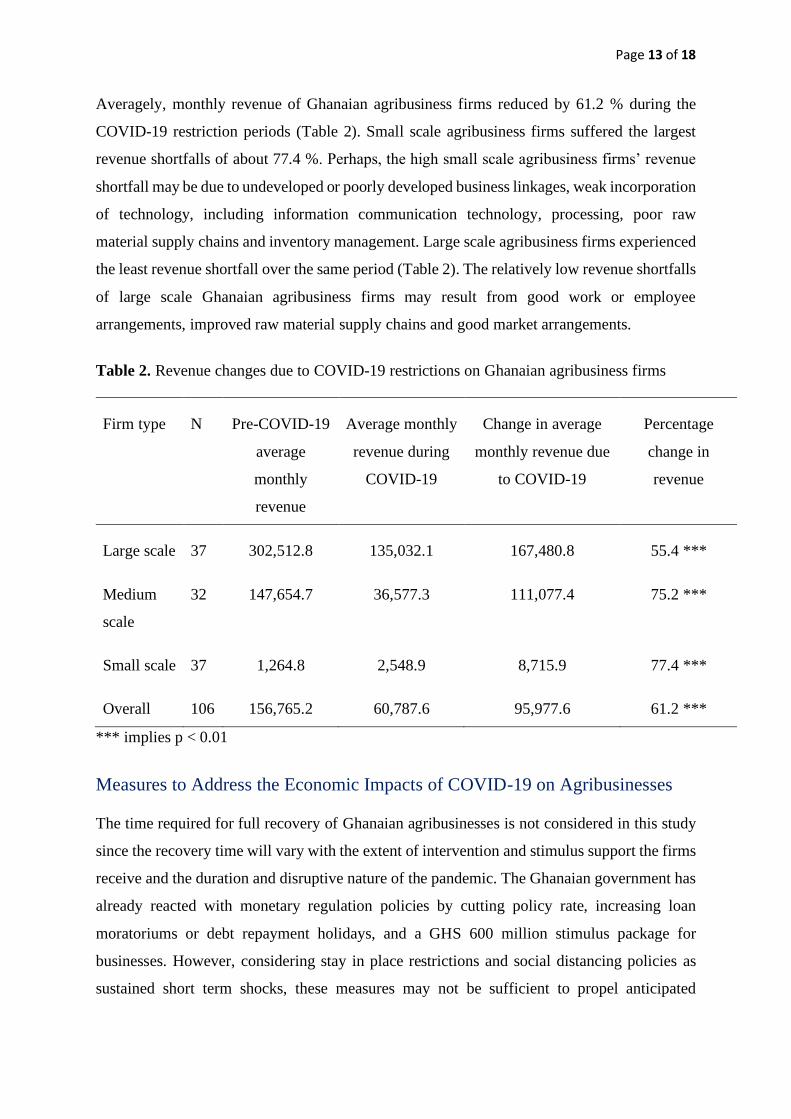

Averagely, monthly revenue of Ghanaian agribusiness firms reduced by 61.2 % during the

COVID-19 restriction periods (Table 2). Small scale agribusiness firms suffered the largest

revenue shortfalls of about 77.4 %. Perhaps, the high small scale agribusiness firms’ revenue

shortfall may be due to undeveloped or poorly developed business linkages, weak incorporation

of technology, including information communication technology, processing, poor raw

material supply chains and inventory management. Large scale agribusiness firms experienced

the least revenue shortfall over the same period (Table 2). The relatively low revenue shortfalls

of large scale Ghanaian agribusiness firms may result from good work or employee

arrangements, improved raw material supply chains and good market arrangements.

Table 2. Revenue changes due to COVID-19 restrictions on Ghanaian agribusiness firms

Firm type N Pre-COVID-19

average

monthly

revenue

Average monthly

revenue during

COVID-19

Change in average

monthly revenue due

to COVID-19

Percentage

change in

revenue

Large scale 37 302,512.8 135,032.1 167,480.8 55.4 ***

Medium

scale

32 147,654.7 36,577.3 111,077.4 75.2 ***

Small scale 37 1,264.8 2,548.9 8,715.9 77.4 ***

Overall 106 156,765.2 60,787.6 95,977.6 61.2 ***

*** implies p < 0.01

Measures to Address the Economic Impacts of COVID-19 on Agribusinesses

The time required for full recovery of Ghanaian agribusinesses is not considered in this study

since the recovery time will vary with the extent of intervention and stimulus support the firms

receive and the duration and disruptive nature of the pandemic. The Ghanaian government has

already reacted with monetary regulation policies by cutting policy rate, increasing loan

moratoriums or debt repayment holidays, and a GHS 600 million stimulus package for

businesses. However, considering stay in place restrictions and social distancing policies as

sustained short term shocks, these measures may not be sufficient to propel anticipated

Page 14 of 18

agribusiness recovery. Government has an array of policy tools, including fiscal and social

insurance policies. For instance, lowering policy rate or granting debt repayment holidays will

have minor effects on liquidity of already crippled agribusinesses. Also, the stimulus amount

may not be enough to support economy-wide enterprises. But some firms may require high

capital injection to restart their grounded business operations. Alternatively, banks and

financial institutions may be unwilling to lend to agribusinesses due to uncertainties of the

COVID-19 pandemic. Government can therefore, offer credit guarantees for agribusiness

companies. Government could also defer taxes to support agribusiness firms’ liquidity.

Coping Strategies by Agribusinesses and Smallholders

In a crisis situation like COVID-19 pandemic, businesses and individual lives are usually the

most affected. This requires some level of cushioning by government, industry stakeholders

and non-governmental organisations (NGOs) to mitigate the impact.

Almost all of the participants reported to have significant reduction (more than 70 %) in total

revenue per month since the outbreak in Ghana. Also, actors have adopted different strategies

to deliver products/services to their customers (Figure 4). Key among them is direct delivery

at business location (41 %), price reduction and discount sale (28 %), door-to-door delivery via

courier services (17 %) and using e-commerce platforms (online sales)(14 %) (Figure 4).

Figure 4. Coping strategies implemented by agribusiness participants

Page 15 of 18

Employee Management Strategies by Agribusinesses

Workers mostly bear the blunt of unexpected crisis such as this COVID-19 pandemic.

Agribusinesses we surveyed admitted to the fact that, apart from disruption of normal business

operation and service delivery, their workforce are the next greatest victims of the fall-out of

this pandemic. However, crisis usually provoke high-level of creativity and innovative way of

doing things by both businesses and individuals. Thus, agribusinesses we surveyed have

adopted a number of innovative approaches to manage their workforce as coping strategies to

keep their businesses running at minimal levels (Figure 5). Thirty-two (32 %) of the

respondents indicated to explore alternative/new markets, offering flexible/remote working

options to workers (20 %), providing emergency support to staff working remotely (20 %),

using dedicated communication channel for staff/clients (13 %), providing leave with pay for

workers to self-isolate (8 %) and subsidising workers health insurance (7 %).

Figure 5. Employee management strategies by agribusiness during the COVID-19 pandemic

period

Page 16 of 18

Support for Agribusiness in Ghana

Different agribusiness value chain actors (respondents) across the country expressed different

support schemes that can help them mitigate the effect of COVID-19 pandemic on their

business operations and services. Notable among them include financial support, market access

and linkage, formalisation of their business as the topmost need to cushion them against the

consequences of the pandemic (Figure 6).

Figure 6. Required supports by agribusinesses surveyed8

Post-COVID-19 Business Continuity by Agribusinesses

There is life after every crisis. Nations, communities, businesses and people plan to rebuild

their lives after every crisis. We asked participants whether they will continue their business

operations after the pandemic is fully contained; varied responses were adduced by the

8 RGD refers to Registrar’s General Department; FDA refers to Food and Drugs Authority; PPRSD refers to Plant Protection and Regulatory Services Division; GSA refers to Ghana Standards Authority

Page 17 of 18

agribusinesses to continue rebuilding their businesses after the pandemic. 35 % of the

participants were somewhat likely to continue working and adjust their business model to stay

afloat; while 25 % of the participating agribusinesses were very likely to stay in business

(Figure 7). Contrary, 24 % of agribusinesses indicated they are not likely to continue

operations without any external support. This decision will severely impact staff and

communities in which these businesses operate and it is expedient such agribusinesses are

supported to stay in business.

Figure 7. Decision to continue business operatons even without external support by

agribusiness

Policy Recommendations

The government has fittingly issued lockdown guidelines that somewhat exempt agribusiness

operations and supply chains; but challenges in implementation with parallel labour shortages

and rising food commodity prices should be remedied. Sustaining supply chains to function

well is critical to food security. Many starving households across marginalised communities

are due to food supply disruptions—not a lack of food availability. Smallholder farm

Page 18 of 18

populations must be protected from the coronavirus to the extent possible by rigorous contact

tracing, testing and practising social distancing. Smallholders must be assisted by government

and stakeholders to have continued access to markets via a mix of private markets and

government procurement schemes. Smallholder crop, poultry and dairy farmers need more

targeted support, as their pandemic-related input supply and market-access challenges are

urgent.

Smallholder farmers and agribusinesses should be included in government’s stimulus package

and social protection programmes addressing the crisis. As restriction measures are gradually

easing, demand has mounted for home delivery of foodstuffs and e-commerce. This trend

should be encouraged and promoted. The government should promote trade by avoiding export

bans and import restrictions. Government agencies like the Registrar’s General Department

should offer mobile-enabled service for smallholder agribusinesses to formalise their

operations and be assisted by the Ghana Revenue Authority (GRA) to plan and honour their

tax obligation post-COVID-19 when the situation is normalised.

Acknowledgements

We would like to acknowledge our partners and sponsors for their support. We gratefully

acknowledge Henson Geodata Technologies for working on the GIS map and Research Desk

Consulting Ltd for allowing some of their staff to assist us in this survey. We also thank

Anthony Morrison, CEO of CAG, Ebenezer Ennibil, Bernard Ayittah of the Policy

Development and Research Bureau of CAG, and Dr. Ralph Nordjo of the Copenhagen

Consensus for their inputs. We acknowledge all our partners for their support over the years.