Download - Chapter Eight Proprietorships, Partnerships, and Corporations © 2015 McGraw-Hill Education

Chapter Eight

Proprietorships, Partnerships,

and Corporations

© 2015 McGraw-Hill Education.

• Corporate AdvantagesSeparate legal EntityLimited liability of stockholdersContinuous lifeManagement StructureEasily transferable ownership rightsAbility to raise capital

• Corporate DisadvantagesGovernmental regulationCorporate double taxation

• Corporate AdvantagesSeparate legal EntityLimited liability of stockholdersContinuous lifeManagement StructureEasily transferable ownership rightsAbility to raise capital

• Corporate DisadvantagesGovernmental regulationCorporate double taxation

Comparing Corporations with Proprietorships and Partnerships

8-2

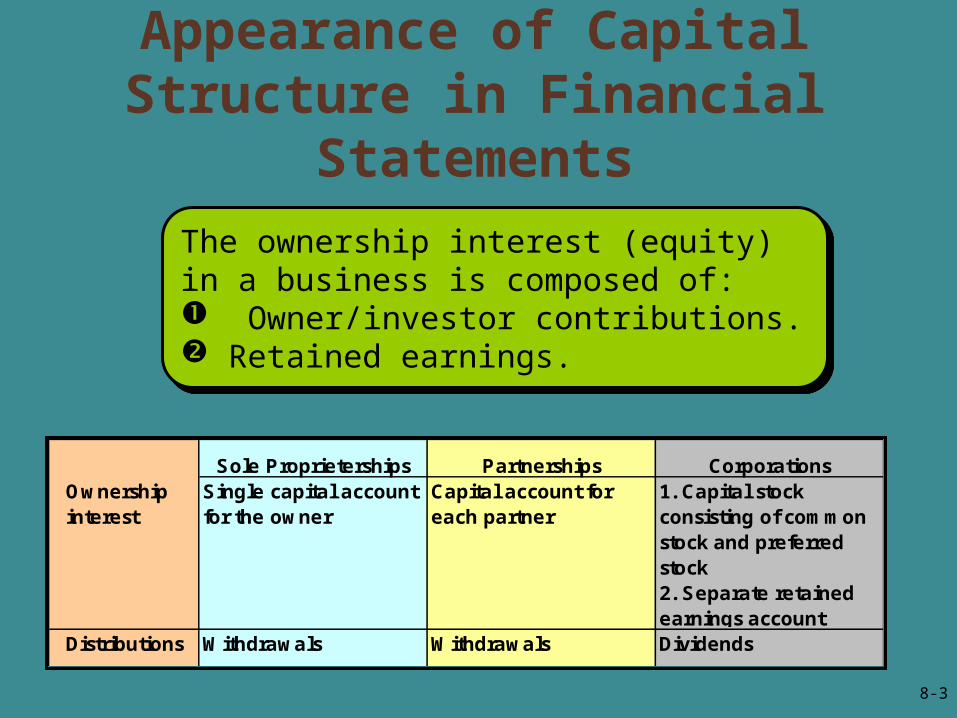

Appearance of Capital Structure in Financial

Statements

Sole Proprieterships Partnerships CorporationsOwnership interest

Single capital account for the owner

Capital account for each partner

1. Capital stock consisting of common stock and preferred stock 2. Separate retained earnings account

Distributions Withdrawals Withdrawals Dividends

The ownership interest (equity)in a business is composed of: Owner/investor

contributions. Retained earnings.

The ownership interest (equity)in a business is composed of: Owner/investor

contributions. Retained earnings.

8-3

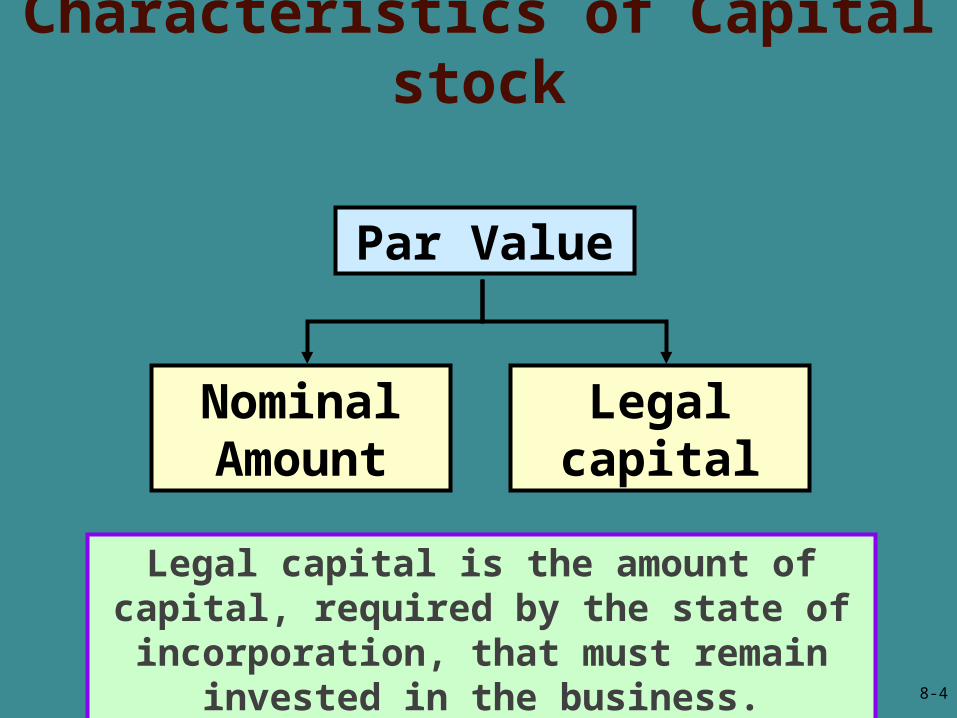

Legal capital is the amount of capital, required by the state of incorporation, that

must remain invested in the business.

Par Value

Nominal Amount

Legal capital

Characteristics of Capital stock

8-4

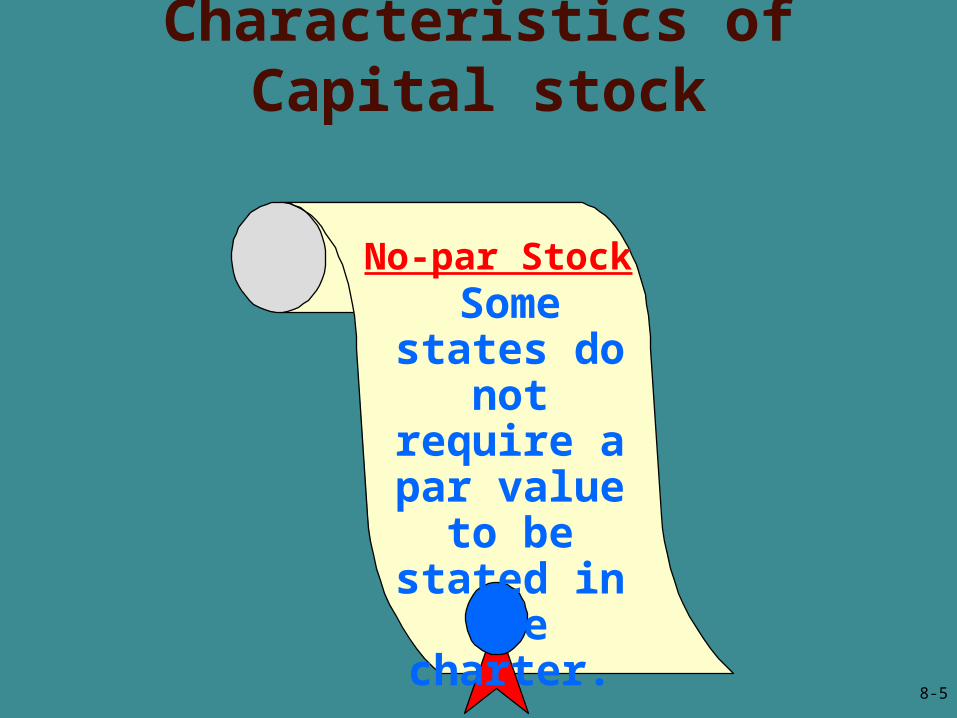

Some states do not

require a par value to be

stated in the charter.

No-par Stock

Characteristics of Capital stock

8-5

Par value is an arbitrary amount assigned to each

share of stock when it is authorized.

Par value is an arbitrary amount assigned to each

share of stock when it is authorized.

Market price is the amount that each share of stock will

sell for in the market.

Market price is the amount that each share of stock will

sell for in the market.

Characteristics of Capital stock

8-6

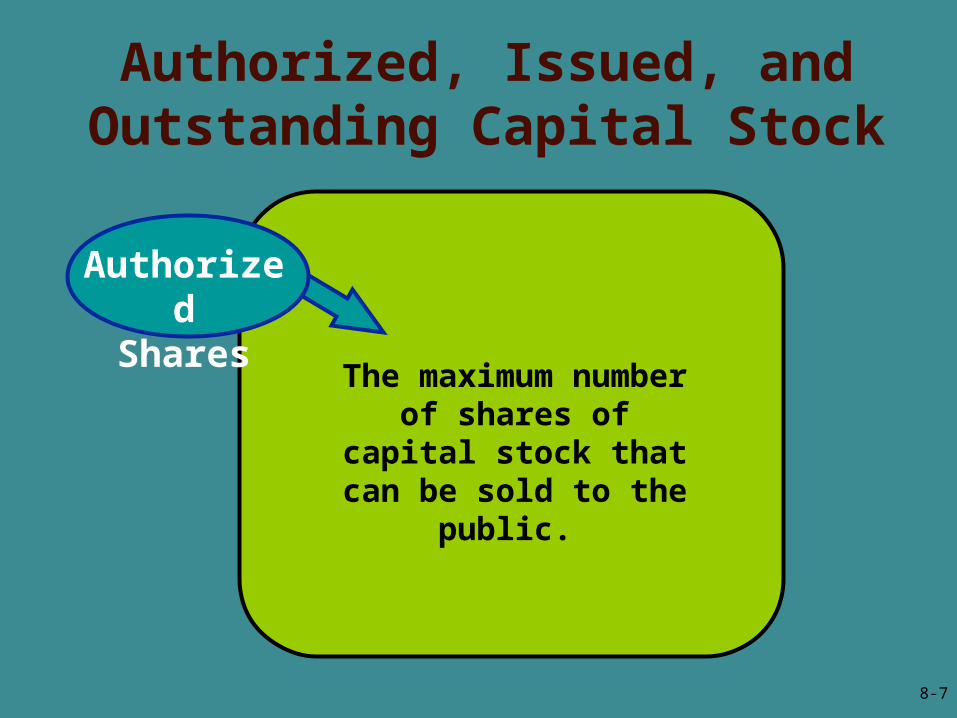

Authorized, Issued, and Outstanding Capital Stock

The maximum number of shares of capital stock

that can be sold to the public.

Authorized

Shares

8-7

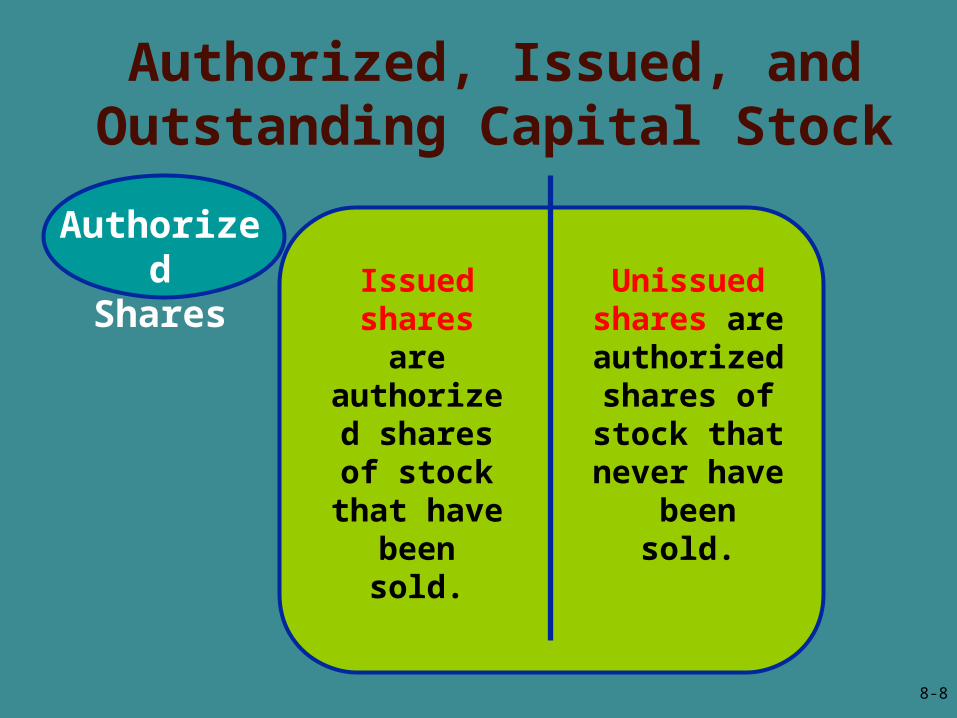

Authorized, Issued, and Outstanding Capital Stock

Issued shares

are authorized shares of stock

that have been sold.

Unissued shares are authorized shares of stock

that never have

been sold.

Authorized

Shares

8-8

Authorized, Issued, and Outstanding Capital Stock

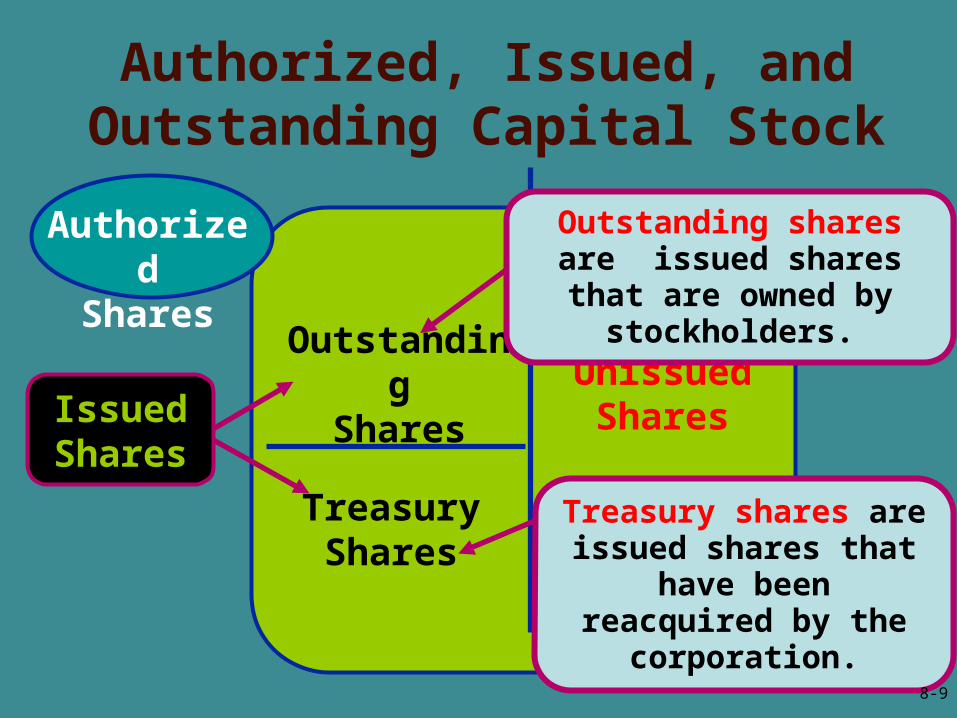

Unissued

SharesTreasuryShares

Outstanding

SharesIssuedShares

Treasury shares are issued shares that

have been reacquired by the

corporation.

Outstanding shares are issued shares that are owned by

stockholders.

Authorized

Shares

8-9

Common stockholders have the rights to: Buy and sell stock. Share in the distribution of profits. Share in the distribution of assets in

the case of liquidation. Vote on significant matters that affect

the corporate charter. Participate in the election of directors.

Common stockholders have the rights to: Buy and sell stock. Share in the distribution of profits. Share in the distribution of assets in

the case of liquidation. Vote on significant matters that affect

the corporate charter. Participate in the election of directors.

Classes of Stock – Common Stock

8-10

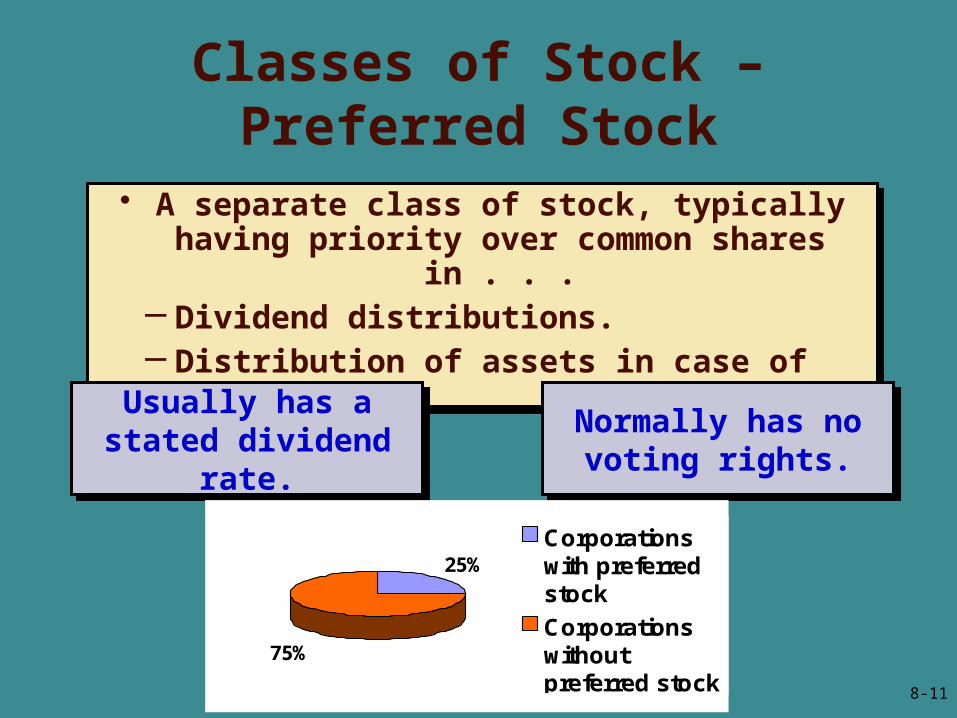

• A separate class of stock, typically having priority over common shares in . . .

– Dividend distributions.– Distribution of assets in case of liquidation.

• A separate class of stock, typically having priority over common shares in . . .

– Dividend distributions.– Distribution of assets in case of liquidation.

Classes of Stock – Preferred Stock

25%

75%

Corporationswith preferredstock

Corporationswithoutpreferred stock

Usually has a stated dividend

rate.

Usually has a stated dividend

rate.

Normally has no voting rights.

Normally has no voting rights.

8-11

NoncumulativeCumulativeDividends in arrears must be paid before

dividends may be paid on common

stock.

Dividends in arrears must be paid before

dividends may be paid on common

stock.

Undeclared dividends from current and

prior years do not have to be paid in future

years.

Undeclared dividends from current and

prior years do not have to be paid in future

years.

Most preferred stock is cumulative.

Most preferred stock is cumulative.

Preferred Stock Dividends

8-12

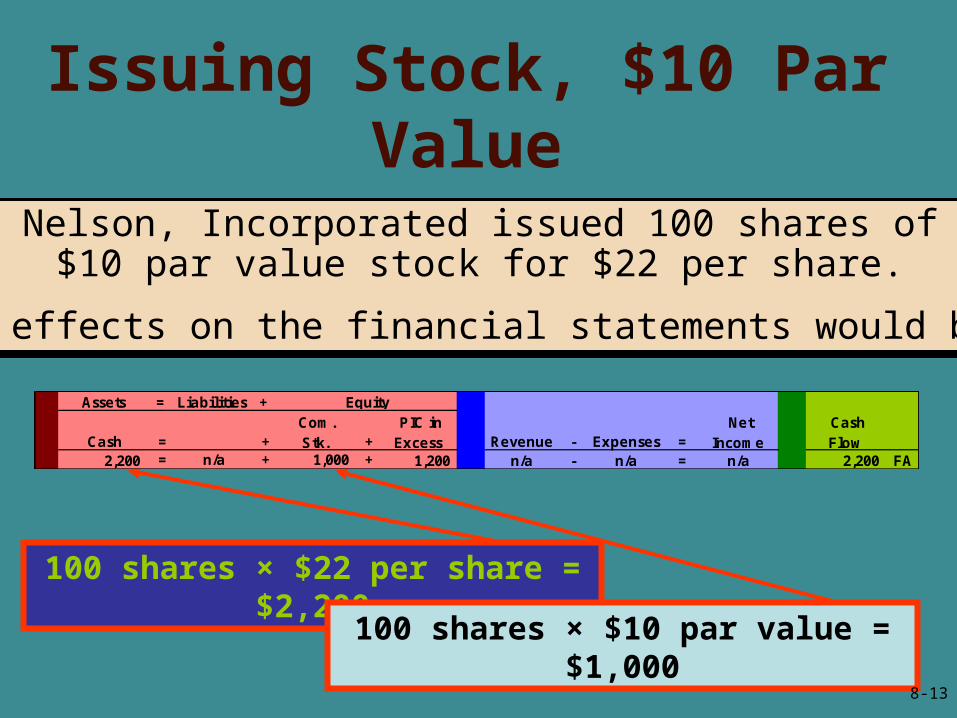

Issuing Stock, $10 Par Value

Nelson, Incorporated issued 100 shares of$10 par value stock for $22 per share.

The effects on the financial statements would be:

Nelson, Incorporated issued 100 shares of$10 par value stock for $22 per share.

The effects on the financial statements would be:

Assets = Liabilities +

Cash = + Com.

Stk. + PIC in Excess Revenue - Expenses =

Net Income

Cash Flow

2,200 = n/a + 1,000 + 1,200 n/a - n/a = n/a 2,200 FA

Equity

100 shares × $22 per share = $2,200

100 shares × $10 par value = $1,000

8-13

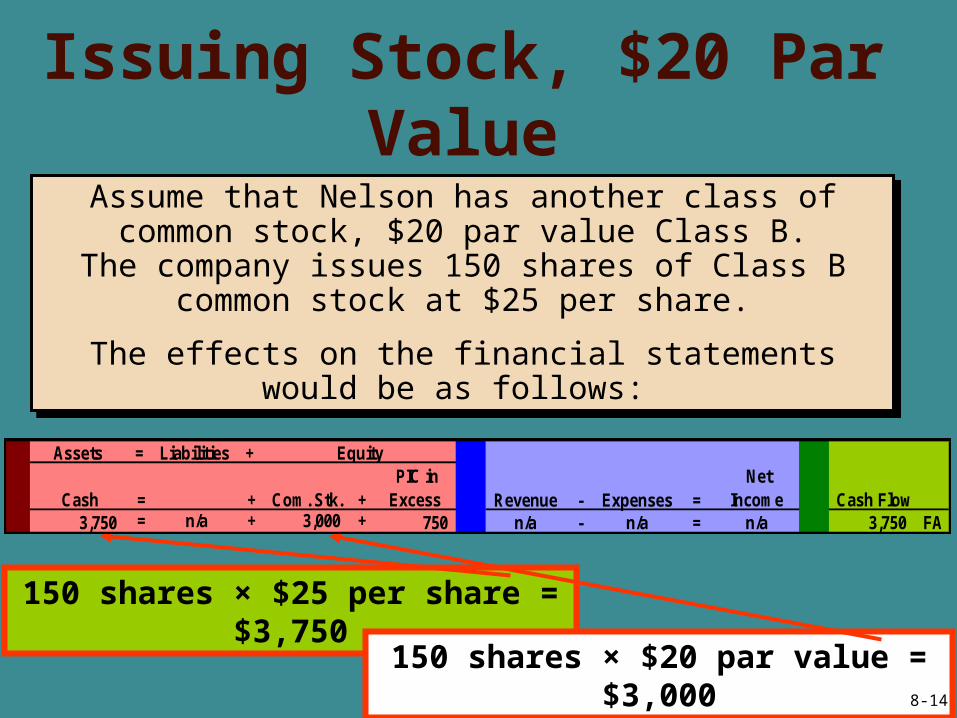

Issuing Stock, $20 Par Value

Assume that Nelson has another class ofcommon stock, $20 par value Class B.

The company issues 150 shares of Class Bcommon stock at $25 per share.

The effects on the financial statements would be as follows:

Assume that Nelson has another class ofcommon stock, $20 par value Class B.

The company issues 150 shares of Class Bcommon stock at $25 per share.

The effects on the financial statements would be as follows:

Assets = Liabilities +

Cash = + Com. Stk. + PIC in Excess Revenue - Expenses =

Net Income Cash Flow

3,750 = n/a + 3,000 + 750 n/a - n/a = n/a 3,750 FA

Equity

150 shares × $25 per share = $3,750

150 shares × $20 par value = $3,000 8-14

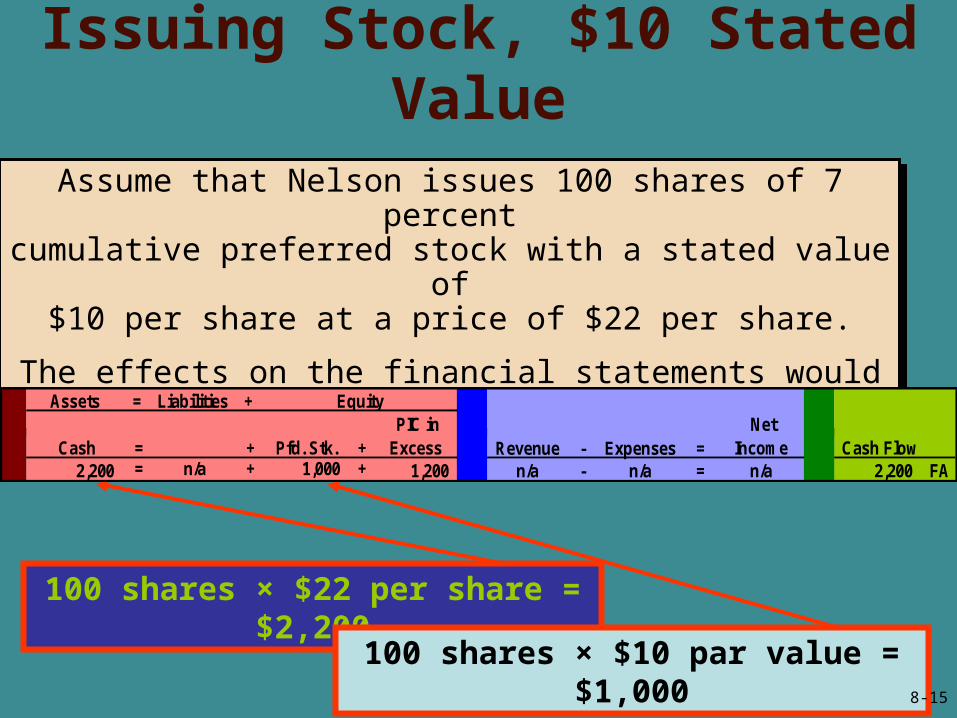

Assume that Nelson issues 100 shares of 7 percentcumulative preferred stock with a stated value of

$10 per share at a price of $22 per share.

The effects on the financial statements would be as follows:

Assume that Nelson issues 100 shares of 7 percentcumulative preferred stock with a stated value of

$10 per share at a price of $22 per share.

The effects on the financial statements would be as follows:

Issuing Stock, $10 Stated Value

Assets = Liabilities +

Cash = + Pfd. Stk. + PIC in Excess Revenue - Expenses =

Net Income Cash Flow

2,200 = n/a + 1,000 + 1,200 n/a - n/a = n/a 2,200 FA

Equity

100 shares × $22 per share = $2,200

100 shares × $10 par value = $1,000 8-15

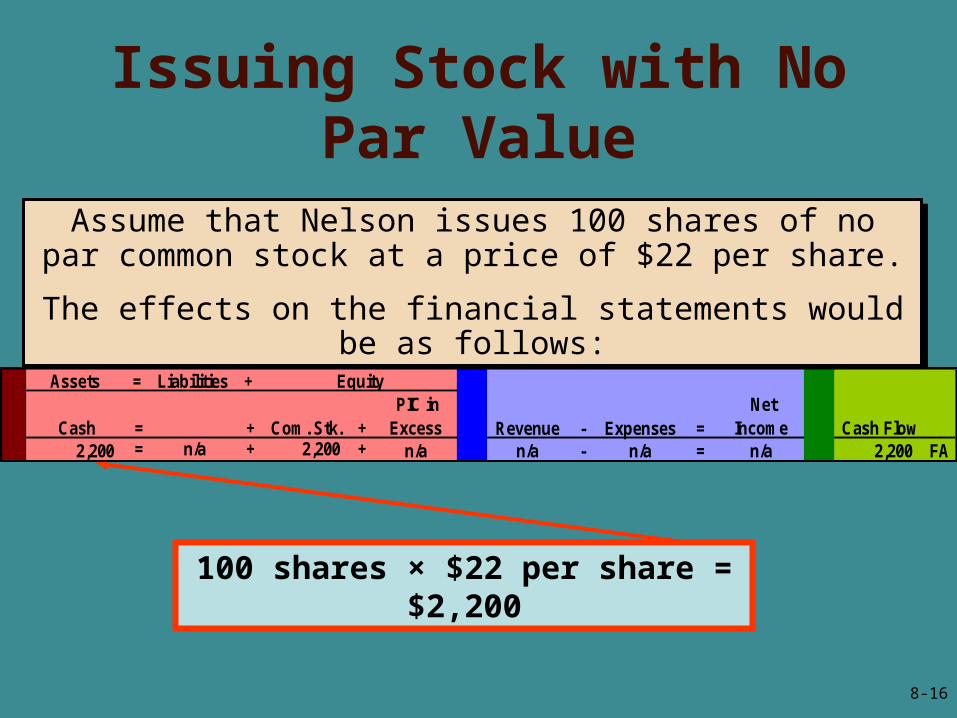

Issuing Stock with No Par Value

Assume that Nelson issues 100 shares of nopar common stock at a price of $22 per share.

The effects on the financial statements would be as follows:

Assume that Nelson issues 100 shares of nopar common stock at a price of $22 per share.

The effects on the financial statements would be as follows:

Assets = Liabilities +

Cash = + Com. Stk. + PIC in Excess Revenue - Expenses =

Net Income Cash Flow

2,200 = n/a + 2,200 + n/a n/a - n/a = n/a 2,200 FA

Equity

100 shares × $22 per share = $2,200

8-16

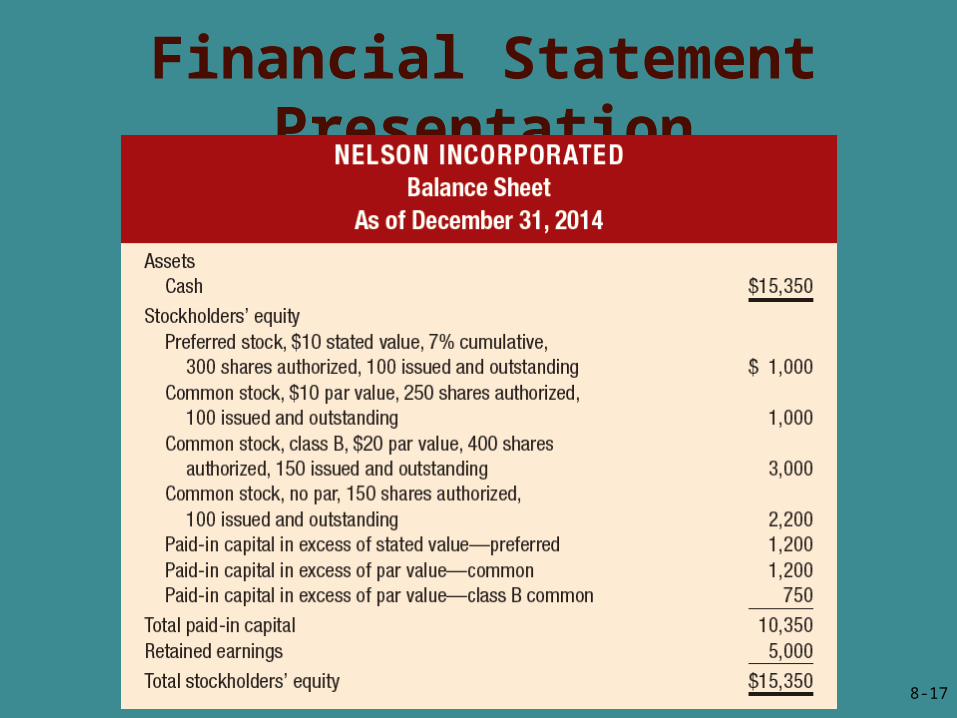

Financial Statement Presentation

8-17

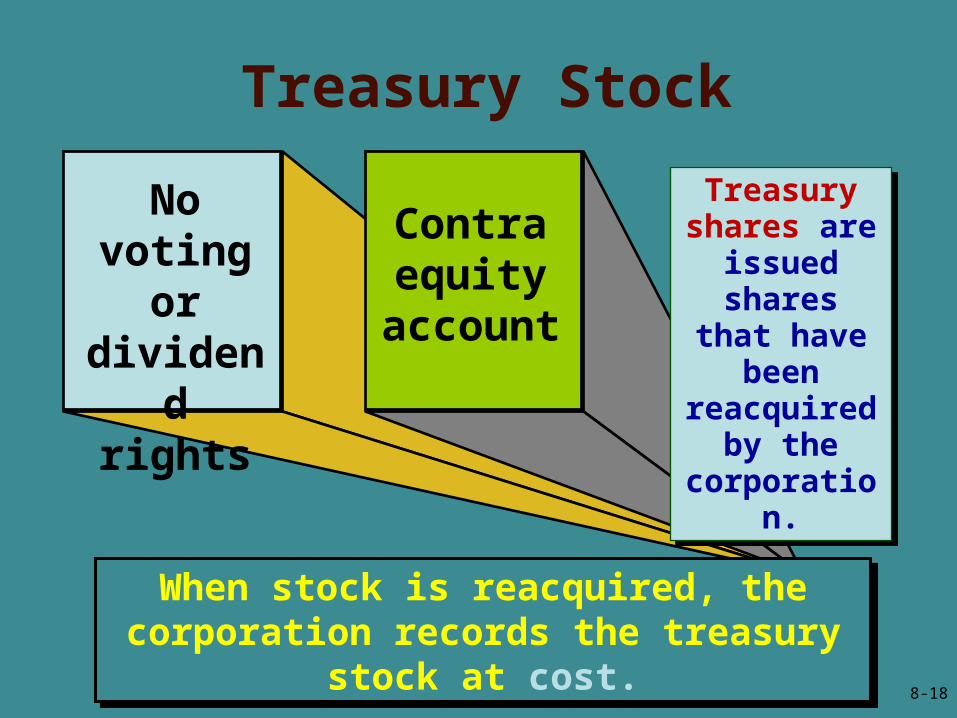

No voting or

dividend rights

Contra equity

account

When stock is reacquired, the corporation records the treasury stock at cost.

When stock is reacquired, the corporation records the treasury stock at cost.

Treasury shares are

issued shares that have been reacquired

by the corporation.

Treasury shares are

issued shares that have been reacquired

by the corporation.

Treasury Stock

8-18

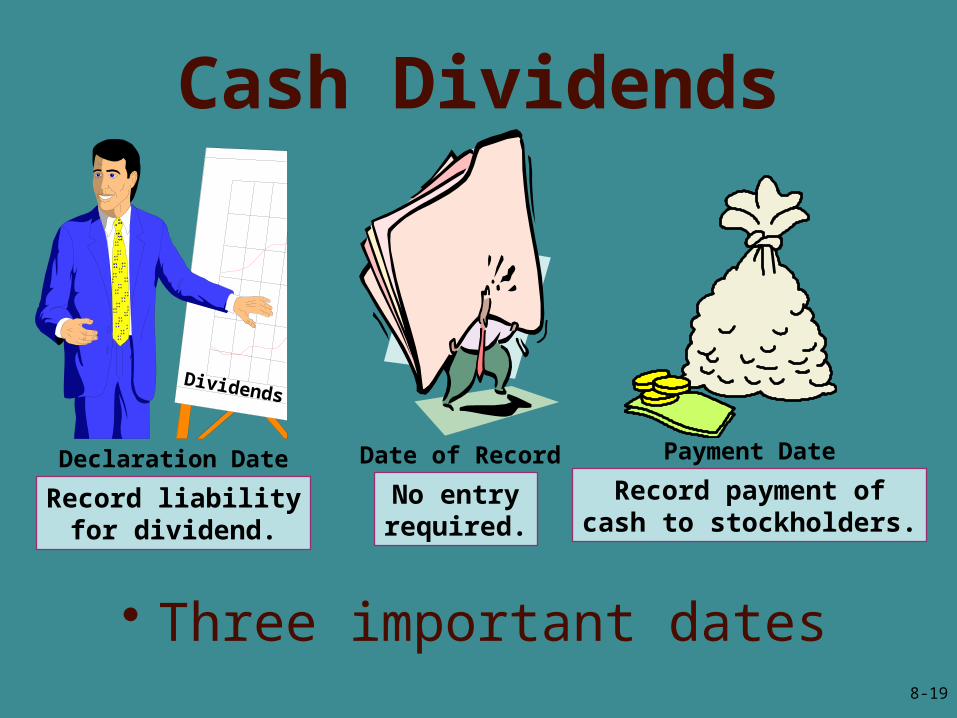

• Three important dates

Cash Dividends

Date of Record

No entryrequired.

Payment DateRecord payment of

cash to stockholders.

Declaration Date

Record liabilityfor dividend.

Dividends

8-19

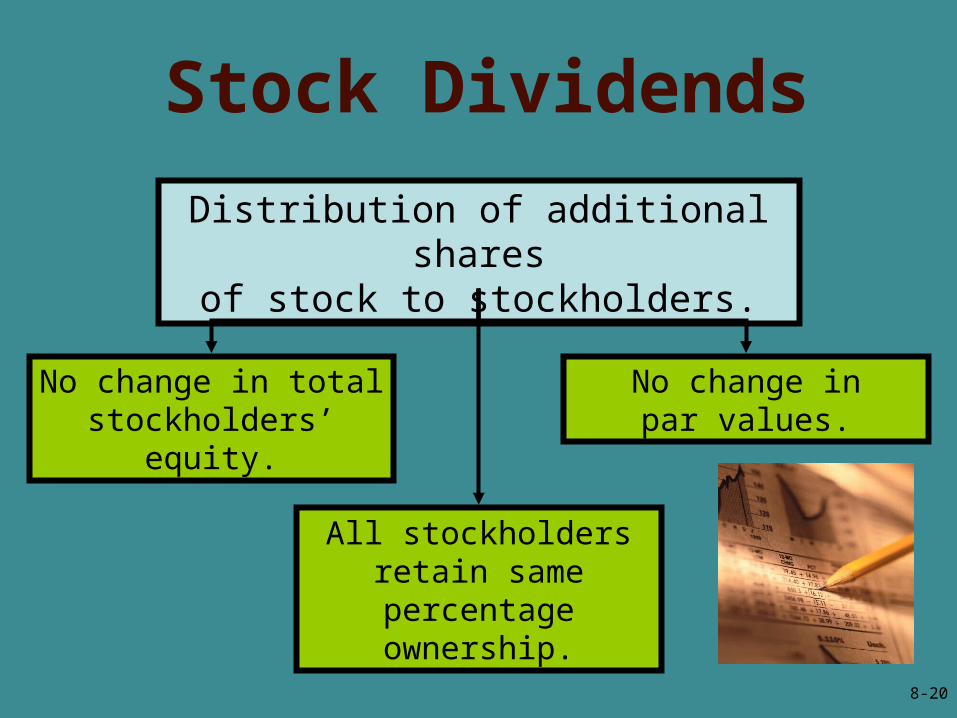

Stock Dividends

Distribution of additional sharesof stock to stockholders.

No change in total stockholders’ equity.

No change inpar values.

All stockholders retain same percentage ownership.

8-20

Stock Splits Stock splits replace existing

shares with a greater number of new shares.

Companies use stock splits to reduce market price per share of their outstanding stock.

The number of outstanding shares increase and par value is decreased proportionately.

Retained earnings is not affected.

Stock splits replace existing shares with a greater number of new shares.

Companies use stock splits to reduce market price per share of their outstanding stock.

The number of outstanding shares increase and par value is decreased proportionately.

Retained earnings is not affected.

8-21

End of Chapter Eight

8-22