© ABB Group May 20, 2013 | Slide 1

Energy Efficiency Cost of Losses

Douglas Getson PE, Global Product Manager, ZA Transformer Day, May 2013

Agenda

Network Impact Transformer losses

Total Ownership Cost

Definition

Net Present Value

Loss Capitalization

A & B factors

Payback method

Case Study

Renewable energy

© ABB Group May 20, 2013 | Slide 2

© ABB Group May 20, 2013 | Slide 3

Distribution Transformers Impacting efficiency of the networks

Losses in Distribution Transformers (DT) represent a considerable part of the total distribution losses

Europe T&D losses represent 7% of the total generated power with DT representing 25% of the total losses

DT average load varies typically from 10-60%. Therefore, no-load losses can be a significant component of DT total losses.

High variability average loads makes it important to evaluate based on total ownership cost when defining the most economical solution

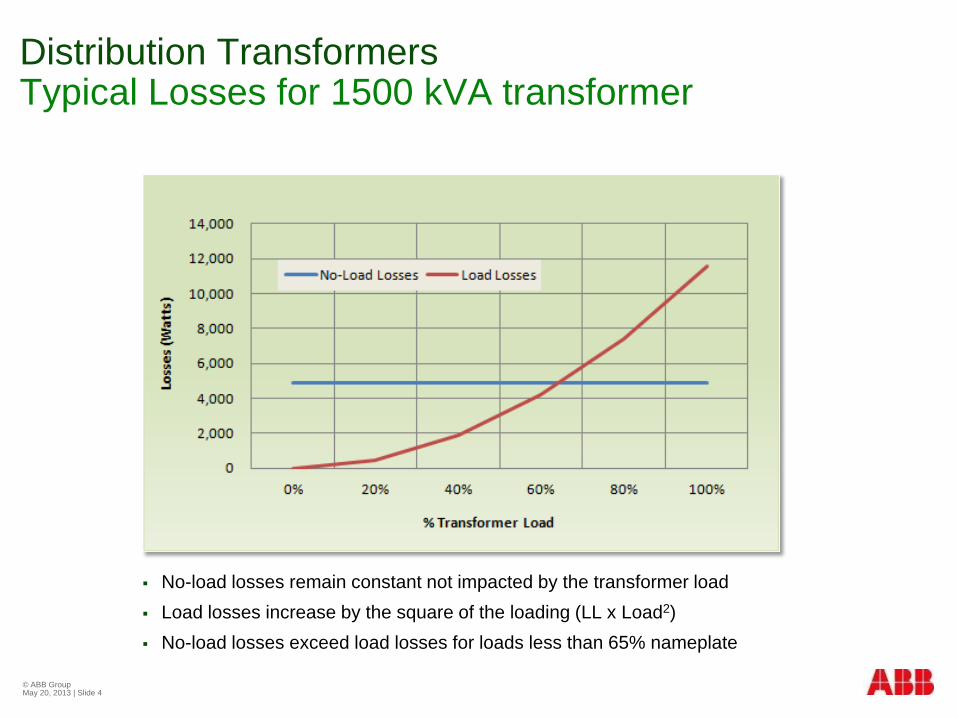

Distribution Transformers Typical Losses for 1500 kVA transformer

No-load losses remain constant not impacted by the transformer load Load losses increase by the square of the loading (LL x Load2) No-load losses exceed load losses for loads less than 65% nameplate

© ABB Group May 20, 2013 | Slide 4

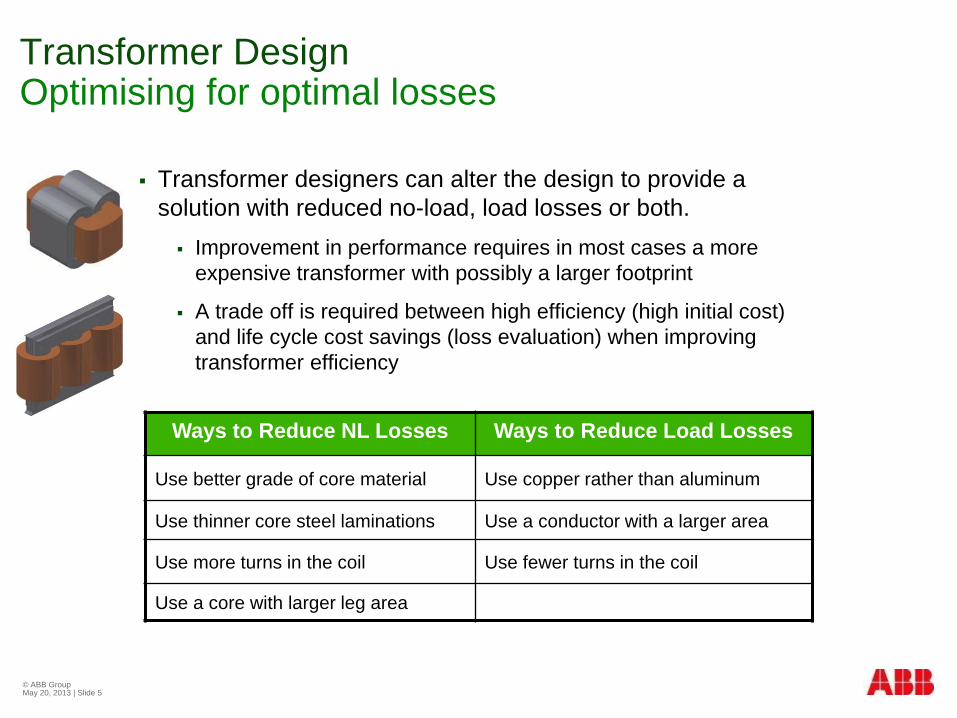

Transformer Design Optimising for optimal losses

Ways to Reduce NL Losses Ways to Reduce Load Losses

Use better grade of core material Use copper rather than aluminum

Use thinner core steel laminations Use a conductor with a larger area

Use more turns in the coil Use fewer turns in the coil

Use a core with larger leg area

© ABB Group May 20, 2013 | Slide 5

Transformer designers can alter the design to provide a solution with reduced no-load, load losses or both. Improvement in performance requires in most cases a more

expensive transformer with possibly a larger footprint

A trade off is required between high efficiency (high initial cost) and life cycle cost savings (loss evaluation) when improving transformer efficiency

© ABB Group May 20, 2013 | Slide 6

Total Ownership Cost Definition

© ABB 22/07/2009 | Slide 7

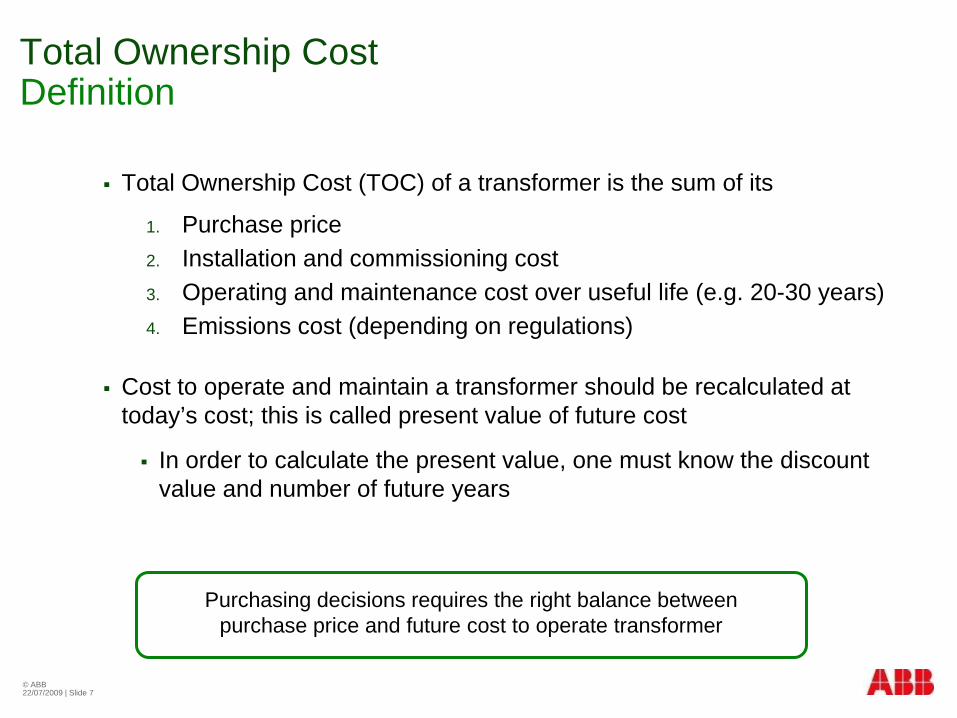

Total Ownership Cost Definition Total Ownership Cost (TOC) of a transformer is the sum of its

1. Purchase price 2. Installation and commissioning cost 3. Operating and maintenance cost over useful life (e.g. 20-30 years) 4. Emissions cost (depending on regulations)

Cost to operate and maintain a transformer should be recalculated at today’s cost; this is called present value of future cost

In order to calculate the present value, one must know the discount value and number of future years

Purchasing decisions requires the right balance between purchase price and future cost to operate transformer

© ABB 22/07/2009 | Slide 8

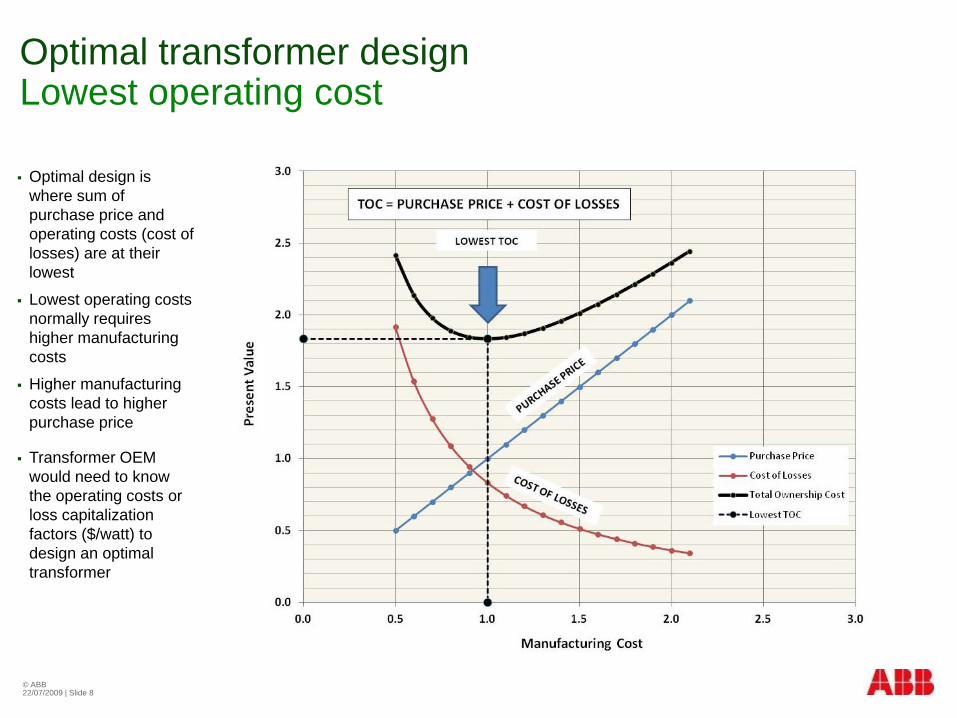

Optimal transformer design Lowest operating cost

Optimal design is where sum of purchase price and operating costs (cost of losses) are at their lowest

Lowest operating costs normally requires higher manufacturing costs

Higher manufacturing costs lead to higher purchase price

Transformer OEM would need to know the operating costs or loss capitalization factors ($/watt) to design an optimal transformer

© ABB Group May 20, 2013 | Slide 9

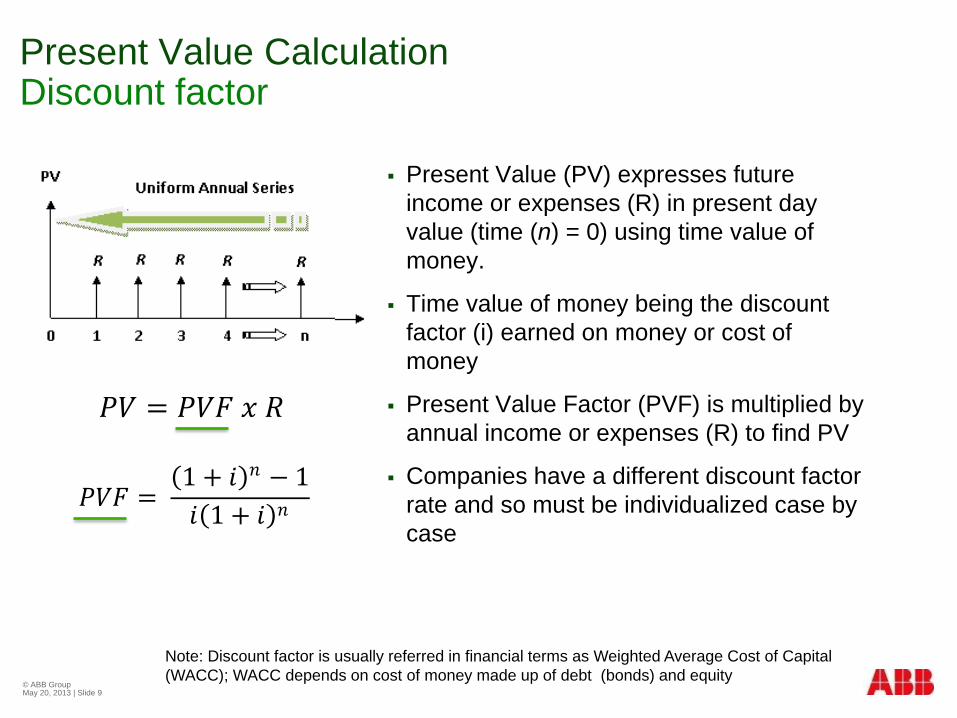

Present Value Calculation Discount factor

Present Value (PV) expresses future income or expenses (R) in present day value (time (n) = 0) using time value of money.

Time value of money being the discount factor (i) earned on money or cost of money

Present Value Factor (PVF) is multiplied by annual income or expenses (R) to find PV

Companies have a different discount factor rate and so must be individualized case by case

𝑃𝑃𝑃𝑃 = 𝑃𝑃𝑃𝑃𝑃𝑃 𝑥𝑥 𝑅𝑅

𝑃𝑃𝑃𝑃𝑃𝑃 = (1 + 𝑖𝑖)𝑛𝑛 − 1𝑖𝑖(1 + 𝑖𝑖)𝑛𝑛

Note: Discount factor is usually referred in financial terms as Weighted Average Cost of Capital (WACC); WACC depends on cost of money made up of debt (bonds) and equity

Present Value Calculation Time value of money

Your money is worth more today than in the future

Inflation reduces the purchasing power of future money relative to current ones

Overall uncertainty increases as one looks out further into the future.

The promise to pay 100 USD in 30 days is worth more than 100 USD in 90 days

Waiting to receive your money carries an opportunity cost associated with it as one is foregoing an opportunity to invest in the next best alternative

© ABB Group May 20, 2013 | Slide 10

Large discount rates reflect higher cost of capital and increased opportunity cost which results in lower present value factor

Present Value Calculation Time value of money

Discount factor (%) and project life (yrs) have an opposite impact on the present value factor

As discount factor increases it decreases the PVF

And as project life decreases it decreases the PVF

© ABB Group May 20, 2013 | Slide 11

Cost to operate transformers from a present value perspective becomes more expensive as useful life increases and as cost of money (% discount factor) becomes less

30 25 20 15 105.0% 15.37 14.09 12.46 10.38 7.726.0% 13.76 12.78 11.47 9.71 7.368.0% 11.26 10.67 9.82 8.56 6.7112.5% 7.77 7.58 7.24 6.63 5.5415.0% 6.57 6.46 6.26 5.85 5.0217.5% 5.67 5.61 5.49 5.21 4.5820.0% 4.98 4.95 4.87 4.68 4.19

PV FACTORS - Discount Factor (%) vs Project Life (yrs)

𝑃𝑃𝑃𝑃𝑃𝑃 = (1 + 𝑖𝑖)𝑛𝑛 − 1𝑖𝑖(1 + 𝑖𝑖)𝑛𝑛

© ABB Group May 20, 2013 | Slide 12

Net Present Value Example

𝑃𝑃𝑃𝑃 =(1 + 9%)8 − 19%(1 + 9%)8 𝑥𝑥 100 𝑈𝑈𝑈𝑈𝑈𝑈

NPV= -180 USD (570-750)

+30% Cost

CASE #1

CASE #2

2x Savings NPV Case #2 > Case #1

NPV= +121 USD (1096-975)

© ABB Group May 20, 2013 | Slide 13

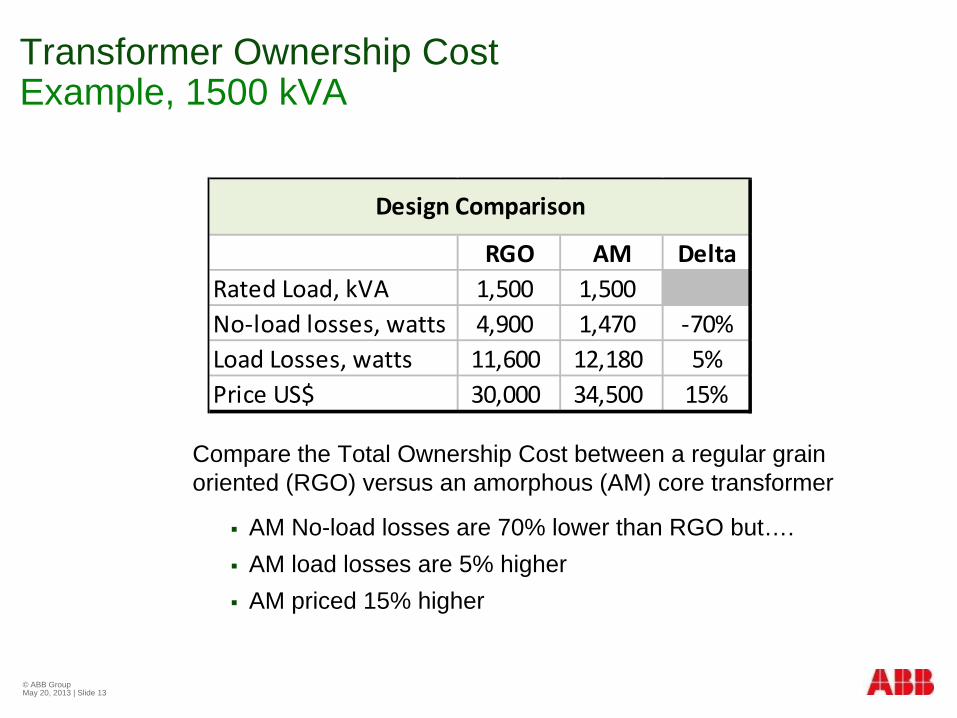

Transformer Ownership Cost Example, 1500 kVA

Compare the Total Ownership Cost between a regular grain oriented (RGO) versus an amorphous (AM) core transformer

AM No-load losses are 70% lower than RGO but…. AM load losses are 5% higher AM priced 15% higher

RGO AM DeltaRated Load, kVA 1,500 1,500No-load losses, watts 4,900 1,470 -70%Load Losses, watts 11,600 12,180 5%Price US$ 30,000 34,500 15%

Design Comparison

© ABB Group May 20, 2013 | Slide 14

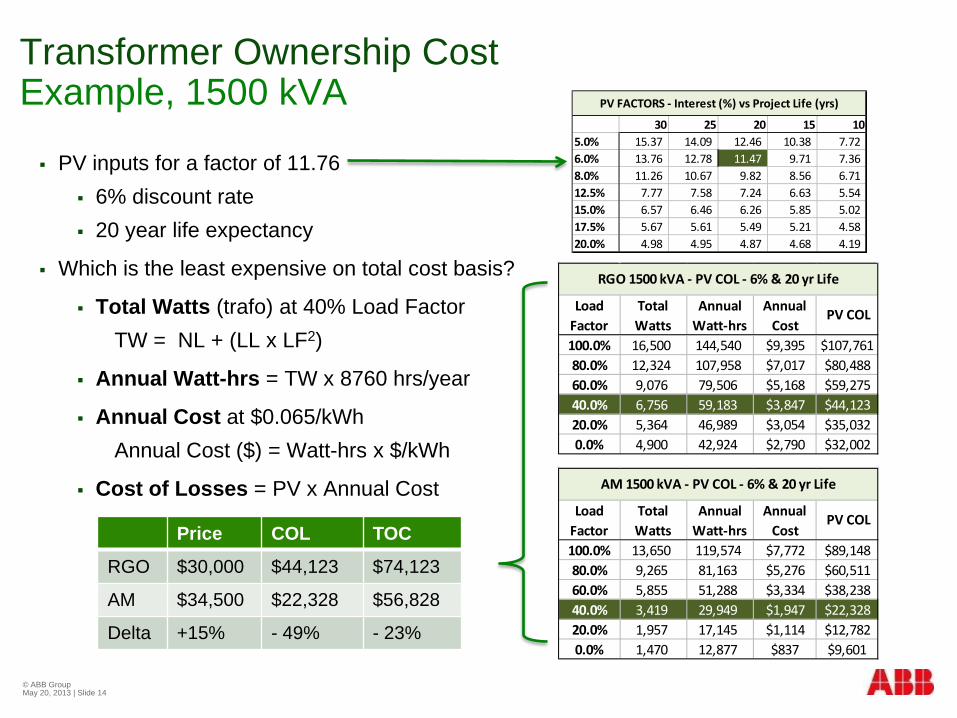

Transformer Ownership Cost Example, 1500 kVA

PV inputs for a factor of 11.76 6% discount rate 20 year life expectancy

Which is the least expensive on total cost basis?

Total Watts (trafo) at 40% Load Factor TW = NL + (LL x LF2)

Annual Watt-hrs = TW x 8760 hrs/year

Annual Cost at $0.065/kWh Annual Cost ($) = Watt-hrs x $/kWh

Cost of Losses = PV x Annual Cost

100.0% 16,500 144,540 $9,395 $107,76180.0% 12,324 107,958 $7,017 $80,48860.0% 9,076 79,506 $5,168 $59,27540.0% 6,756 59,183 $3,847 $44,12320.0% 5,364 46,989 $3,054 $35,0320.0% 4,900 42,924 $2,790 $32,002

RGO 1500 kVA - PV COL - 6% & 20 yr Life

Load Factor

Total Watts

Annual Watt-hrs

Annual Cost

PV COL

100.0% 13,650 119,574 $7,772 $89,14880.0% 9,265 81,163 $5,276 $60,51160.0% 5,855 51,288 $3,334 $38,23840.0% 3,419 29,949 $1,947 $22,32820.0% 1,957 17,145 $1,114 $12,7820.0% 1,470 12,877 $837 $9,601

Load Factor

Total Watts

Annual Watt-hrs

Annual Cost

PV COL

AM 1500 kVA - PV COL - 6% & 20 yr Life

Price COL TOC

RGO $30,000 $44,123 $74,123

AM $34,500 $22,328 $56,828

Delta +15% - 49% - 23%

30 25 20 15 105.0% 15.37 14.09 12.46 10.38 7.726.0% 13.76 12.78 11.47 9.71 7.368.0% 11.26 10.67 9.82 8.56 6.7112.5% 7.77 7.58 7.24 6.63 5.5415.0% 6.57 6.46 6.26 5.85 5.0217.5% 5.67 5.61 5.49 5.21 4.5820.0% 4.98 4.95 4.87 4.68 4.19

PV FACTORS - Interest (%) vs Project Life (yrs)

© ABB Group May 20, 2013 | Slide 15

Loss capitalization A & B factors

© ABB Group May 20, 2013 | Slide 16

Total Ownership Cost Available via www.abb.com/transformers

Transformers Ownership Cost Universal calculator

© ABB Group May 20, 2013 | Slide 17

© ABB Group May 20, 2013 | Slide 18

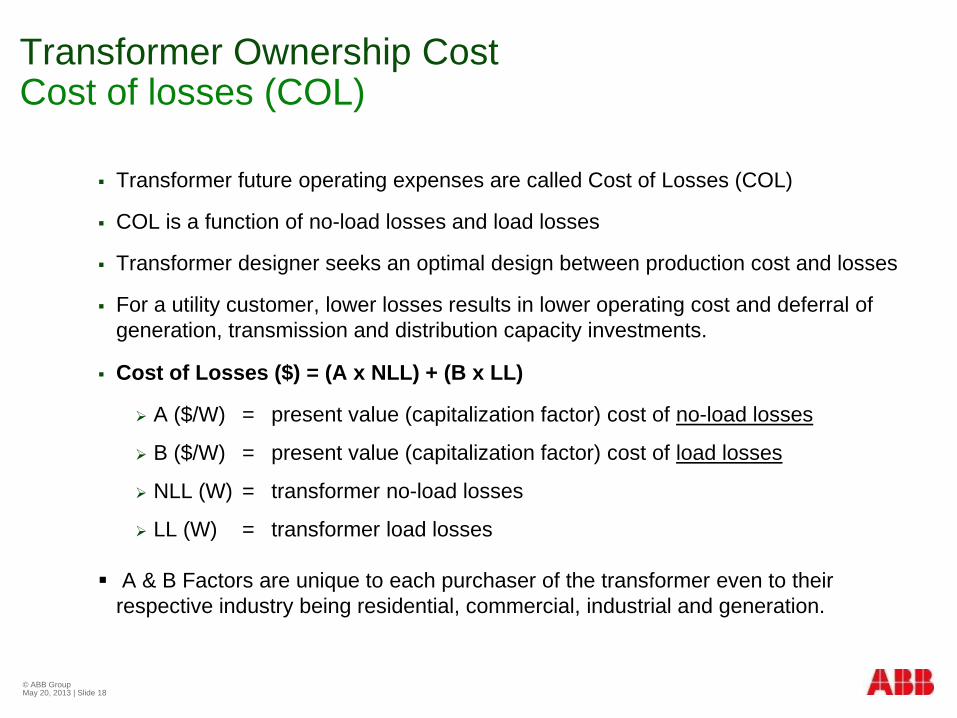

Transformer Ownership Cost Cost of losses (COL)

Transformer future operating expenses are called Cost of Losses (COL)

COL is a function of no-load losses and load losses

Transformer designer seeks an optimal design between production cost and losses

For a utility customer, lower losses results in lower operating cost and deferral of generation, transmission and distribution capacity investments.

Cost of Losses ($) = (A x NLL) + (B x LL)

A ($/W) = present value (capitalization factor) cost of no-load losses

B ($/W) = present value (capitalization factor) cost of load losses

NLL (W) = transformer no-load losses

LL (W) = transformer load losses A & B Factors are unique to each purchaser of the transformer even to their

respective industry being residential, commercial, industrial and generation.

© ABB Group May 20, 2013 | Slide 19

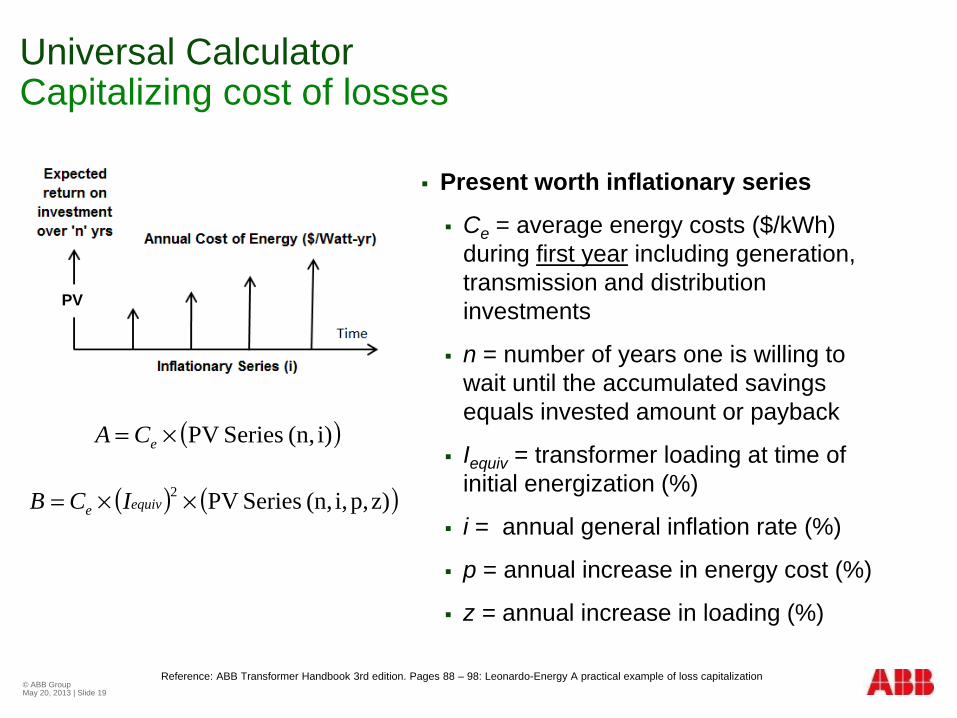

Universal Calculator Capitalizing cost of losses

Reference: ABB Transformer Handbook 3rd edition. Pages 88 – 98: Leonardo-Energy A practical example of loss capitalization

Present worth inflationary series

Ce = average energy costs ($/kWh) during first year including generation, transmission and distribution investments

n = number of years one is willing to wait until the accumulated savings equals invested amount or payback

Iequiv = transformer loading at time of initial energization (%)

i = annual general inflation rate (%)

p = annual increase in energy cost (%)

z = annual increase in loading (%)

PV

( )i)(n, Series PV×= eCA

( ) ( )z)p,i,(n, Series PV2 ××= equive ICB

© ABB Group May 20, 2013 | Slide 20

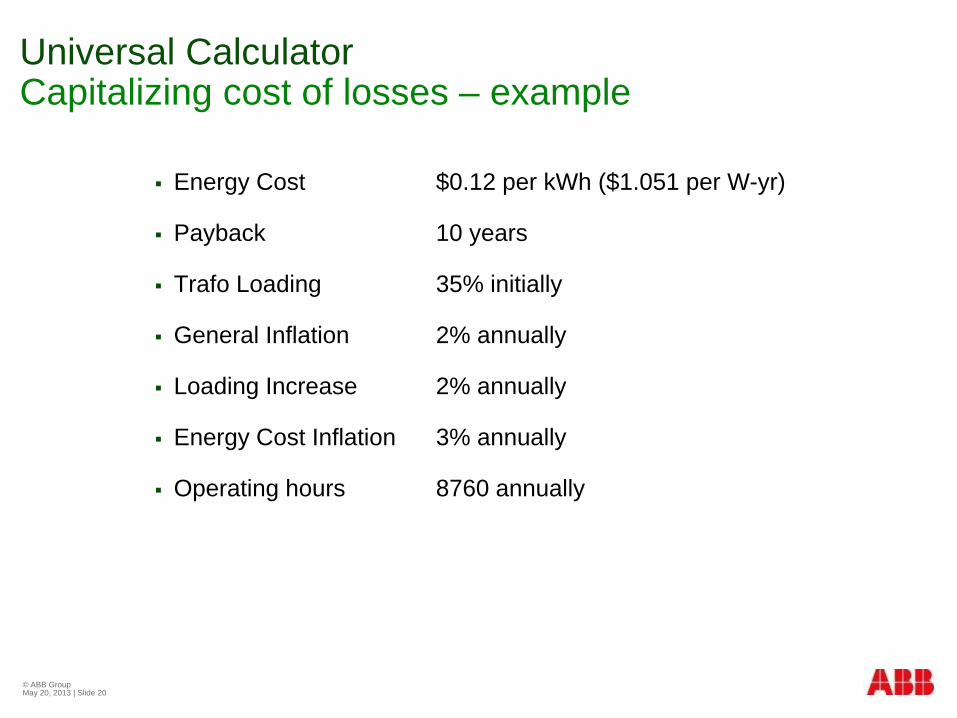

Universal Calculator Capitalizing cost of losses – example

Energy Cost $0.12 per kWh ($1.051 per W-yr)

Payback 10 years

Trafo Loading 35% initially

General Inflation 2% annually

Loading Increase 2% annually

Energy Cost Inflation 3% annually

Operating hours 8760 annually

© ABB Group May 20, 2013 | Slide 21

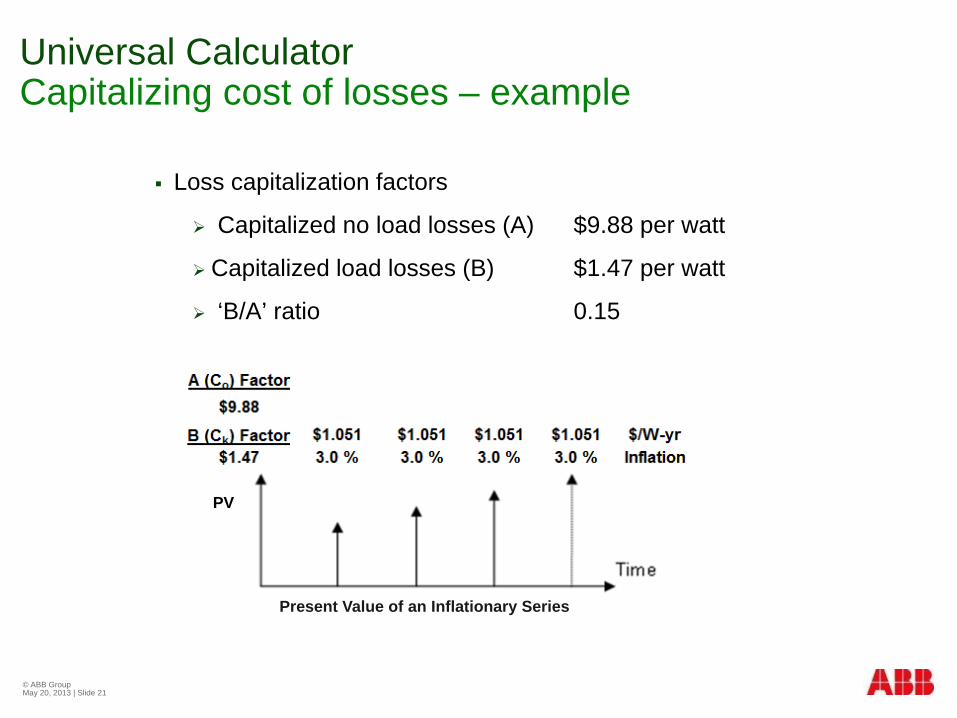

Loss capitalization factors

Capitalized no load losses (A) $9.88 per watt

Capitalized load losses (B) $1.47 per watt

‘B/A’ ratio 0.15

Universal Calculator Capitalizing cost of losses – example

PV

Present Value of an Inflationary Series

© ABB Group May 20, 2013 | Slide 22

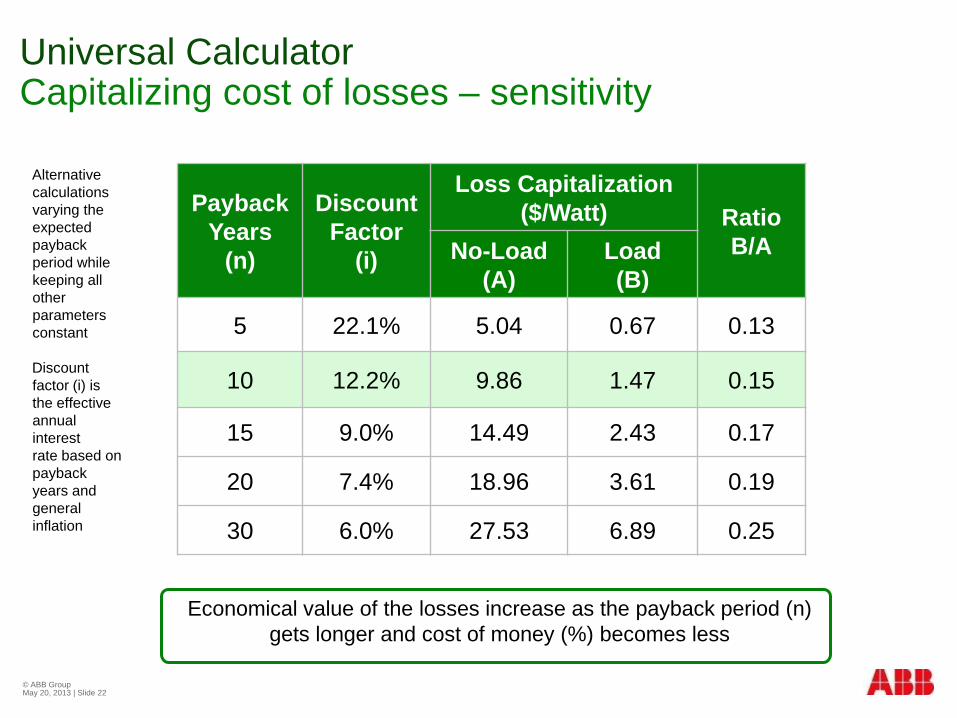

Universal Calculator Capitalizing cost of losses – sensitivity

Economical value of the losses increase as the payback period (n) gets longer and cost of money (%) becomes less

Alternative calculations varying the expected payback period while keeping all other parameters constant Discount factor (i) is the effective annual interest rate based on payback years and general inflation

Payback Years

(n)

Discount Factor

(i)

Loss Capitalization ($/Watt) Ratio

B/A No-Load (A)

Load (B)

5 22.1% 5.04 0.67 0.13

10 12.2% 9.86 1.47 0.15

15 9.0% 14.49 2.43 0.17

20 7.4% 18.96 3.61 0.19

30 6.0% 27.53 6.89 0.25

Cost of Emissions Included within the cost of energy (Ce)

Emissions are also a cost to be considered not only on environmental but also economic impact

Several nations have agreed on a market value for certain pollutants (USD/ton) in a ‘Cap and Trade’ arrangement

One can consider such economic costs within the TOC calculation by adding emissions costs (Cem) to the cost of energy (Ce) for a total cost of energy (CE) which would take the place of Ce in the previous equations.

Emissions cost (Cem) would be calculated by multiplying the emissions per electricity generated Ep (tons/Wh) by the market value of the pollutant Ec (USD/ton)

© ABB Group May 20, 2013 | Slide 23

emeE CCC +=

cpem EEC ×=

© ABB Group May 20, 2013 | Slide 24

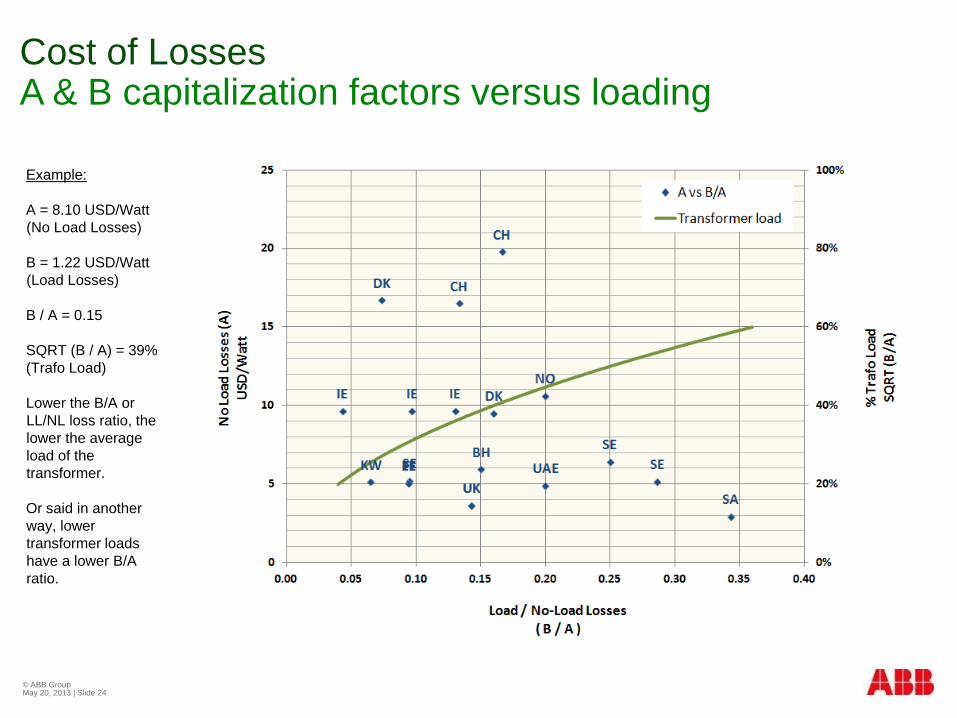

Cost of Losses A & B capitalization factors versus loading

Example: A = 8.10 USD/Watt (No Load Losses) B = 1.22 USD/Watt (Load Losses) B / A = 0.15 SQRT (B / A) = 39% (Trafo Load) Lower the B/A or LL/NL loss ratio, the lower the average load of the transformer. Or said in another way, lower transformer loads have a lower B/A ratio.

© ABB Group May 20, 2013 | Slide 25

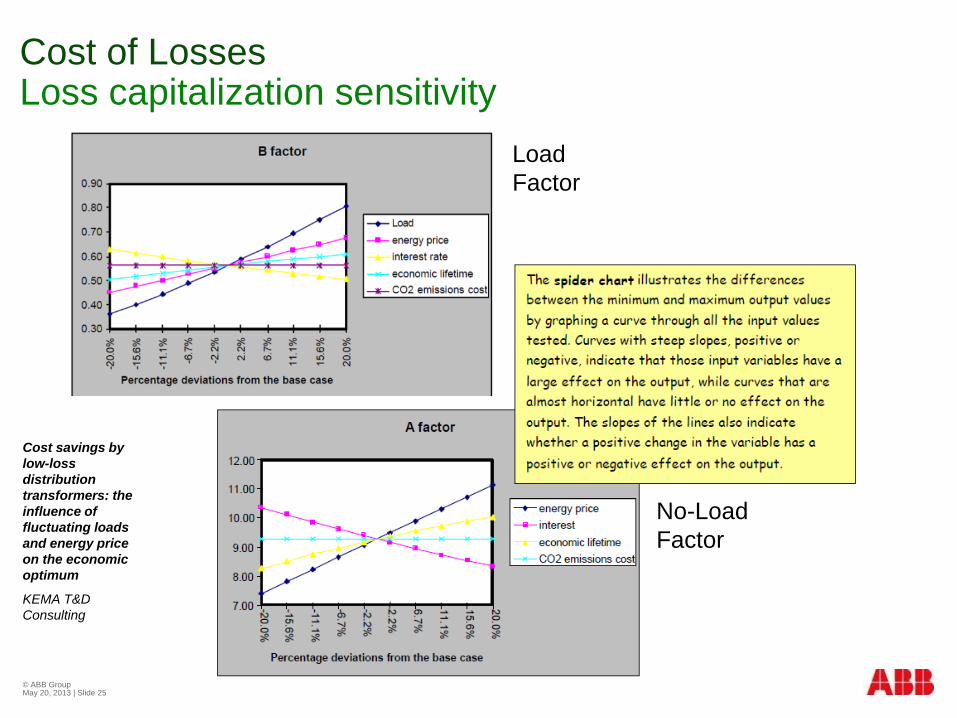

Cost of Losses Loss capitalization sensitivity

Cost savings by low-loss distribution transformers: the influence of fluctuating loads and energy price on the economic optimum

KEMA T&D Consulting

Load Factor

No-Load Factor

© ABB Group May 20, 2013 | Slide 26

Total Ownership Cost Payback period

© ABB Group May 20, 2013 | Slide 27

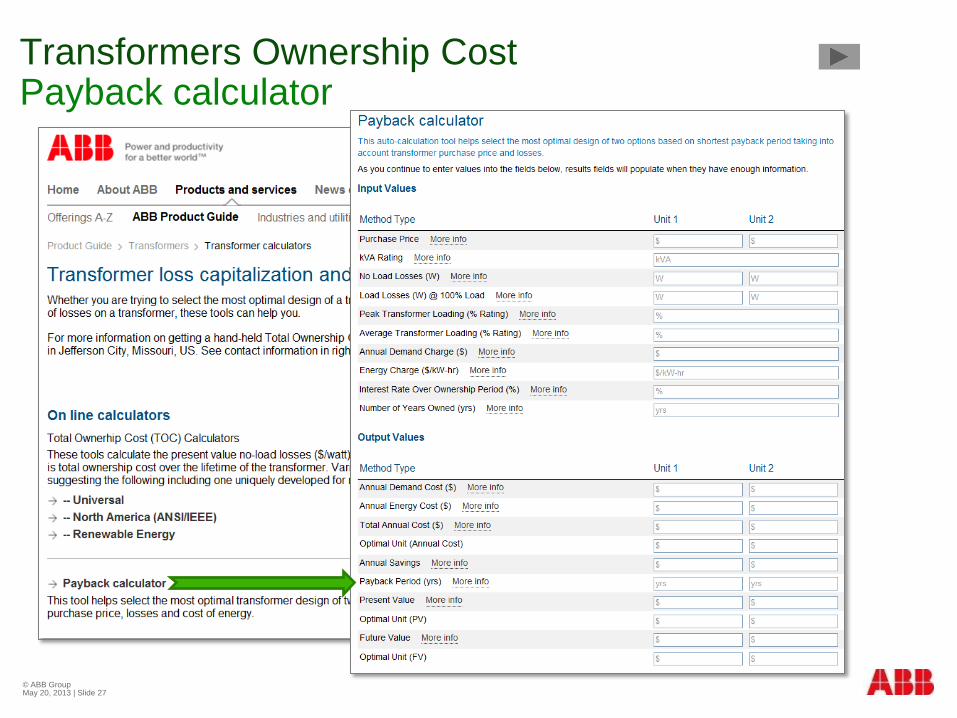

Transformers Ownership Cost Payback calculator

© ABB 22/07/2009 | Slide 28

Payback Period Definition

Payback period refers to the number of years a customers

would need to recover the additional investment (e.g. the

higher purchase price for a more efficient transformer) thanks

to the annual savings generated by having lower transformer

operating cost.

Purchasing decisions requires the right balance between

purchase price and future cost of losses.

© ABB Group May 20, 2013 | Slide 29

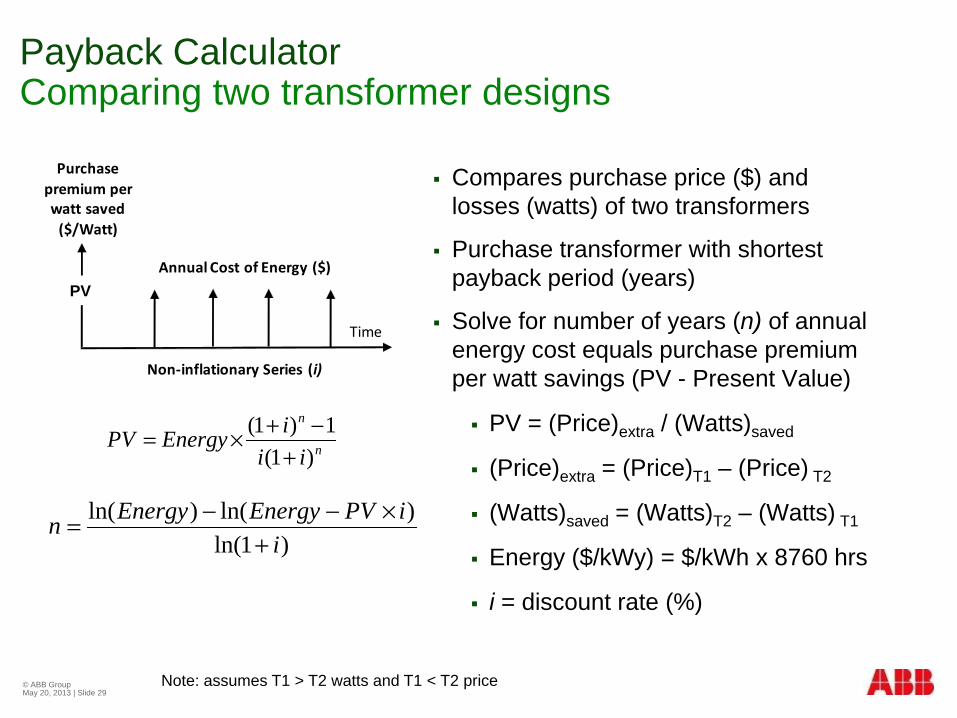

Payback Calculator Comparing two transformer designs

Compares purchase price ($) and losses (watts) of two transformers

Purchase transformer with shortest payback period (years)

Solve for number of years (n) of annual energy cost equals purchase premium per watt savings (PV - Present Value)

PV = (Price)extra / (Watts)saved

(Price)extra = (Price)T1 – (Price) T2

(Watts)saved = (Watts)T2 – (Watts) T1

Energy ($/kWy) = $/kWh x 8760 hrs

i = discount rate (%)

Time

Purchase premium per watt saved

($/Watt)

Annual Cost of Energy ($)

Non-inflationary Series (i)

PW

Note: assumes T1 > T2 watts and T1 < T2 price

n

n

iiiEnergyPV

)1(1)1(

+−+×=

)1ln()ln()ln(

iiPVEnergyEnergyn

+×−−=

PV

© ABB Group May 20, 2013 | Slide 30

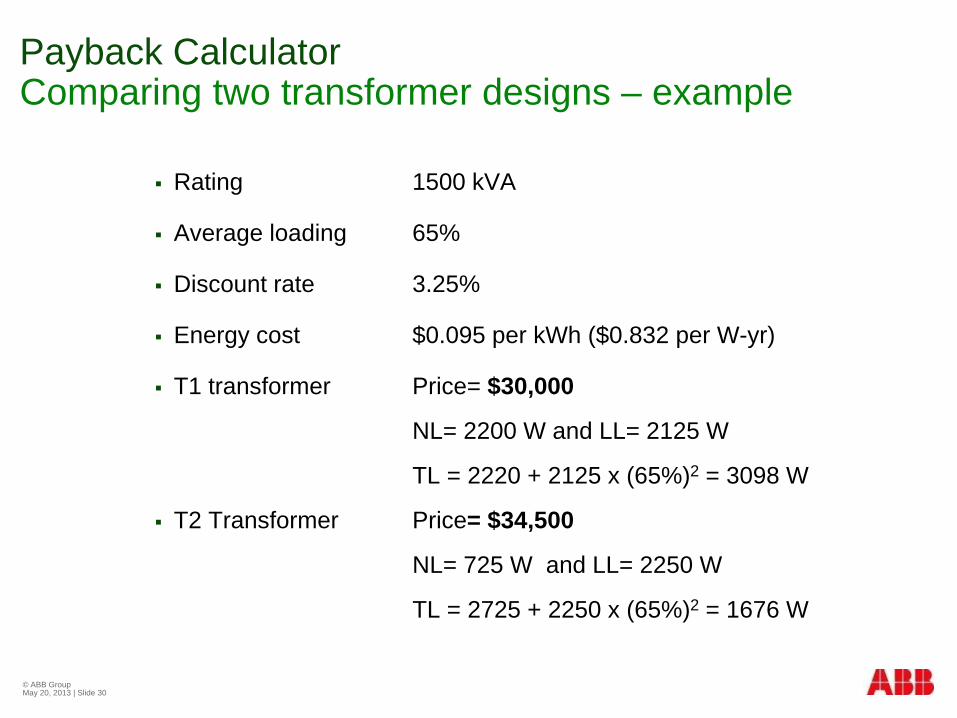

Payback Calculator Comparing two transformer designs – example

Rating 1500 kVA

Average loading 65%

Discount rate 3.25%

Energy cost $0.095 per kWh ($0.832 per W-yr)

T1 transformer Price= $30,000

NL= 2200 W and LL= 2125 W

TL = 2220 + 2125 x (65%)2 = 3098 W

T2 Transformer Price= $34,500

NL= 725 W and LL= 2250 W

TL = 2725 + 2250 x (65%)2 = 1676 W

© ABB Group May 20, 2013 | Slide 31

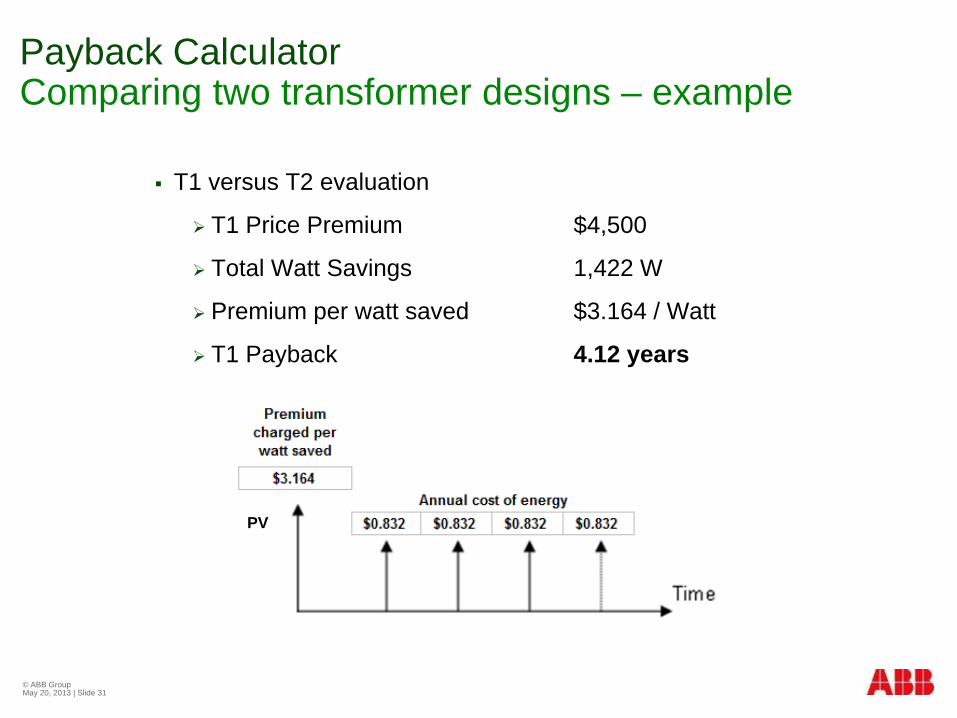

T1 versus T2 evaluation

T1 Price Premium $4,500

Total Watt Savings 1,422 W

Premium per watt saved $3.164 / Watt

T1 Payback 4.12 years

Payback Calculator Comparing two transformer designs – example

PV

© ABB Group May 20, 2013 | Slide 32

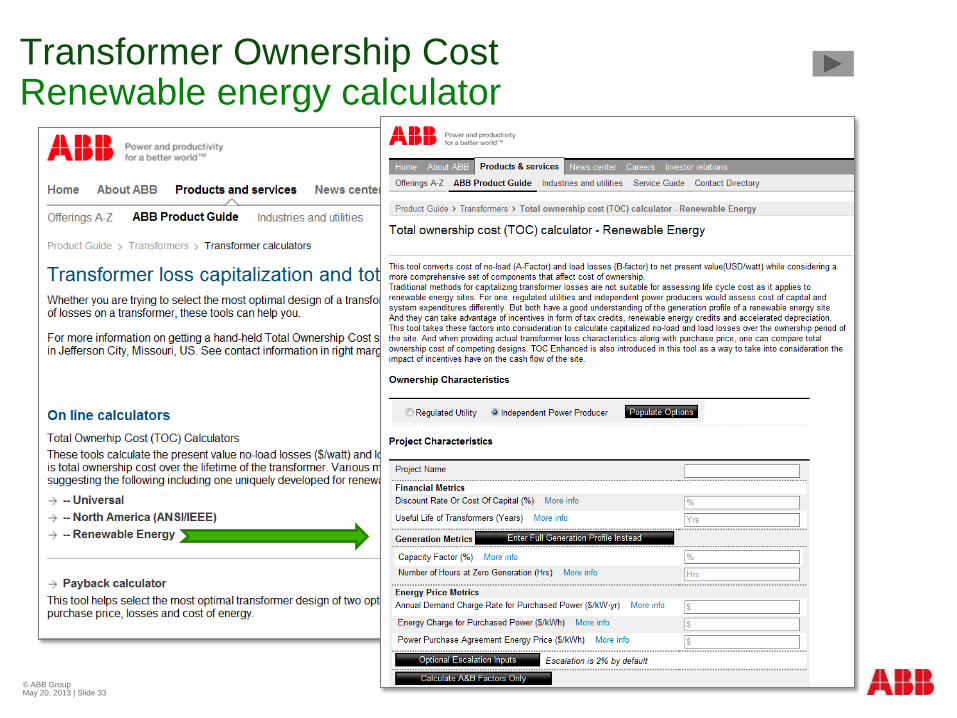

Case Study Renewable energy

Transformer Ownership Cost Renewable energy calculator

© ABB Group May 20, 2013 | Slide 33

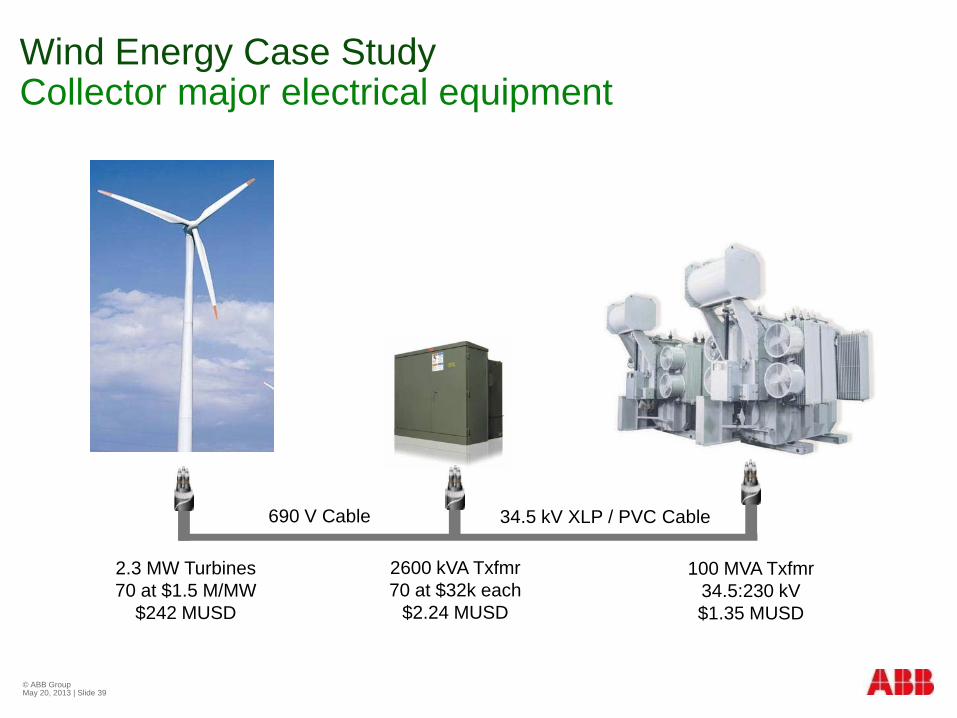

Wind Energy Case Study Collector major electrical equipment

© ABB Group May 20, 2013 | Slide 39

2.3 MW Turbines 70 at $1.5 M/MW

$242 MUSD

2600 kVA Txfmr 70 at $32k each

$2.24 MUSD

690 V Cable 34.5 kV XLP / PVC Cable

100 MVA Txfmr 34.5:230 kV $1.35 MUSD

© ABB Group May 20, 2013 | Slide 40

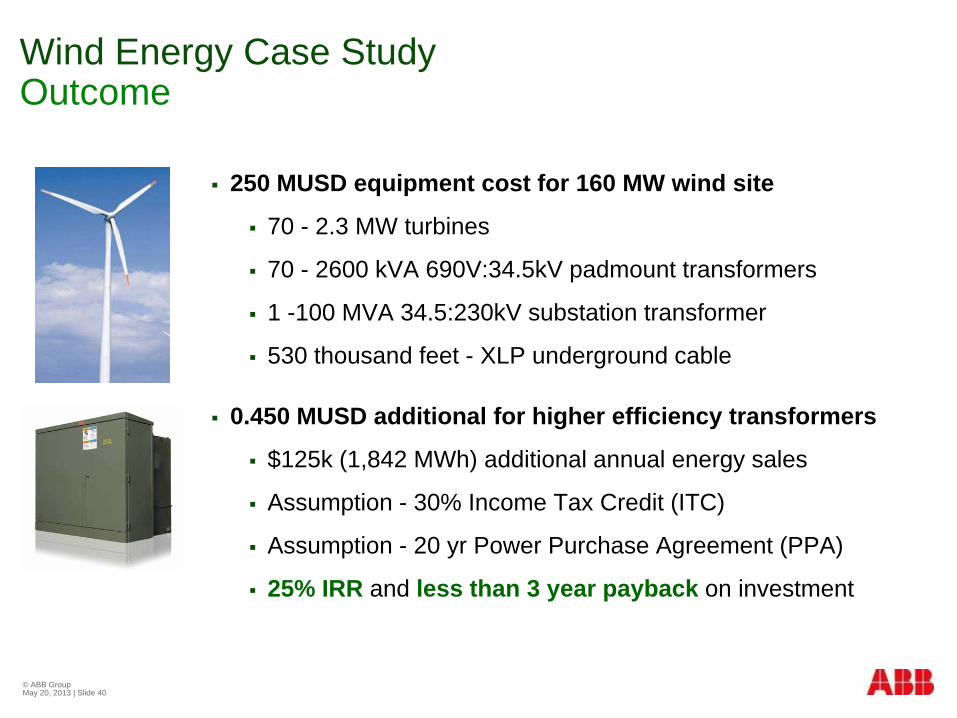

Wind Energy Case Study Outcome

250 MUSD equipment cost for 160 MW wind site

70 - 2.3 MW turbines

70 - 2600 kVA 690V:34.5kV padmount transformers

1 -100 MVA 34.5:230kV substation transformer

530 thousand feet - XLP underground cable

0.450 MUSD additional for higher efficiency transformers

$125k (1,842 MWh) additional annual energy sales

Assumption - 30% Income Tax Credit (ITC)

Assumption - 20 yr Power Purchase Agreement (PPA)

25% IRR and less than 3 year payback on investment

© ABB Group May 20, 2013 | Slide 41

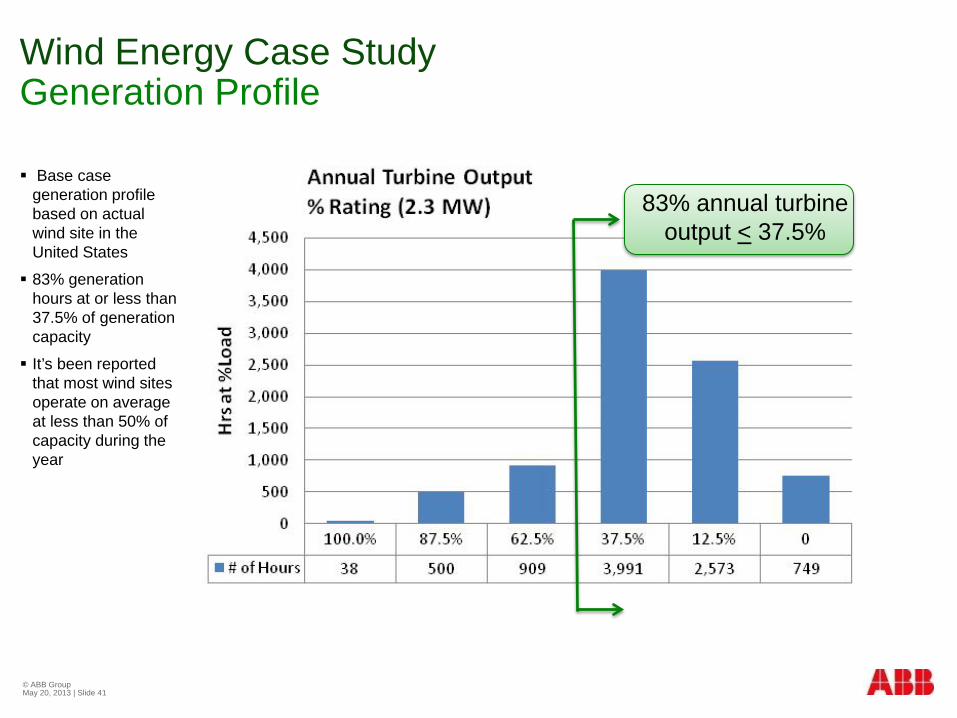

Wind Energy Case Study Generation Profile

Base case generation profile based on actual wind site in the United States

83% generation hours at or less than 37.5% of generation capacity

It’s been reported that most wind sites operate on average at less than 50% of capacity during the year

83% annual turbine output < 37.5%

© ABB Group May 20, 2013 | Slide 42

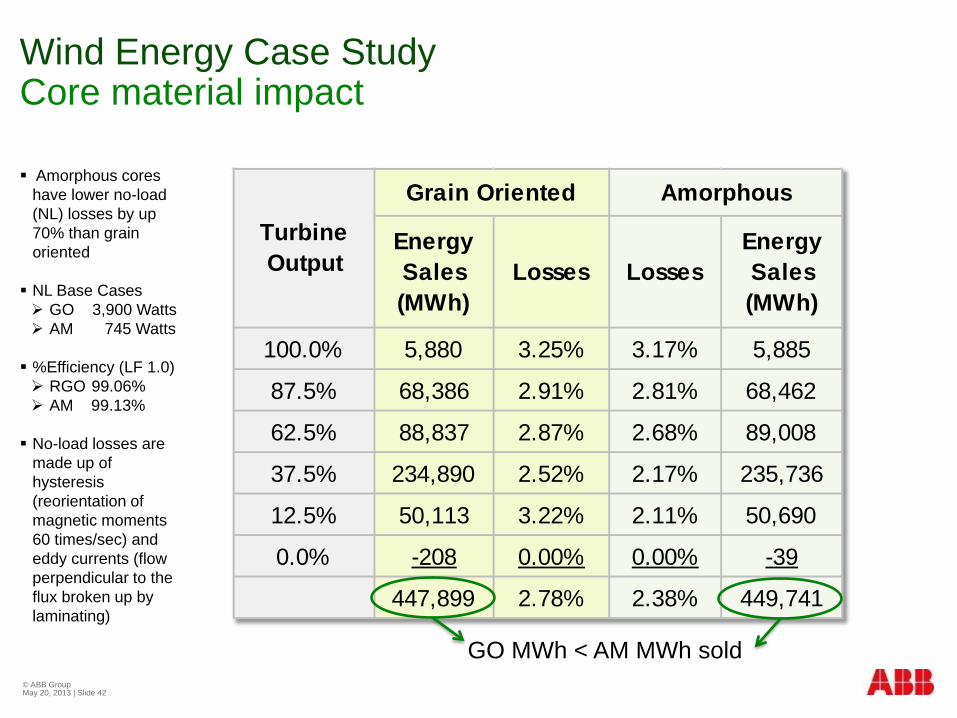

Wind Energy Case Study Core material impact

Amorphous cores have lower no-load (NL) losses by up 70% than grain oriented NL Base Cases GO 3,900 Watts AM 745 Watts %Efficiency (LF 1.0) RGO 99.06% AM 99.13% No-load losses are

made up of hysteresis (reorientation of magnetic moments 60 times/sec) and eddy currents (flow perpendicular to the flux broken up by laminating)

Energy Sales (MWh)

Losses LossesEnergy Sales (MWh)

100.0% 5,880 3.25% 3.17% 5,885

87.5% 68,386 2.91% 2.81% 68,462

62.5% 88,837 2.87% 2.68% 89,008

37.5% 234,890 2.52% 2.17% 235,736

12.5% 50,113 3.22% 2.11% 50,690

0.0% -208 0.00% 0.00% -39

447,899 2.78% 2.38% 449,741

Grain Oriented AmorphousTurbine Output

GO MWh < AM MWh sold

© ABB Group May 20, 2013 | Slide 43

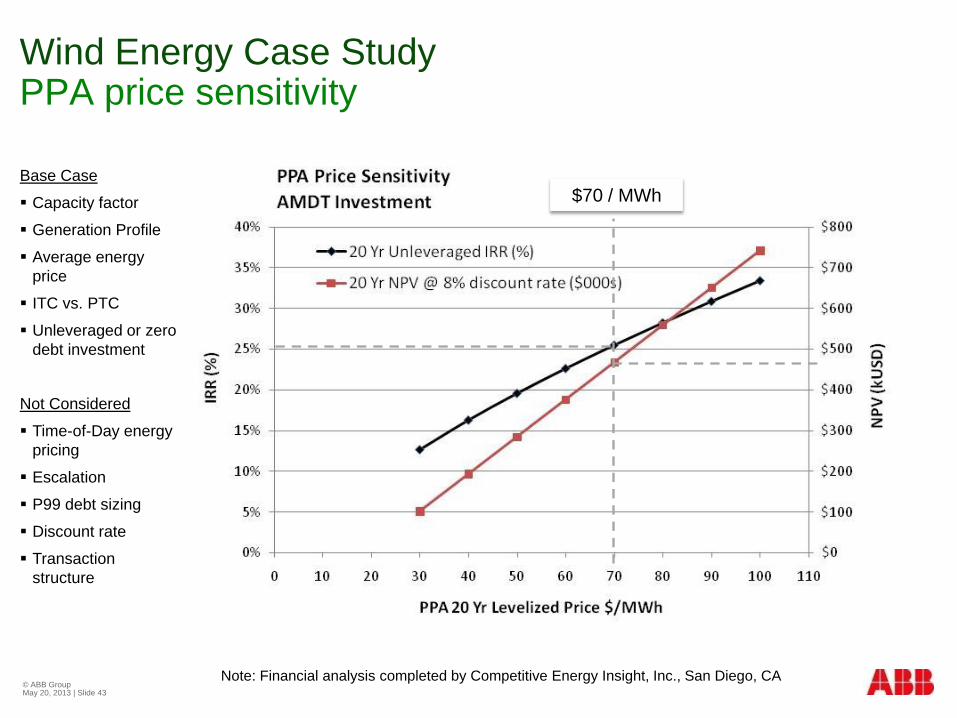

Wind Energy Case Study PPA price sensitivity

Base Case

Capacity factor

Generation Profile

Average energy price

ITC vs. PTC

Unleveraged or zero debt investment

Not Considered

Time-of-Day energy pricing

Escalation

P99 debt sizing

Discount rate

Transaction structure

$70 / MWh

Note: Financial analysis completed by Competitive Energy Insight, Inc., San Diego, CA

© ABB Group May 20, 2013 | Slide 44