Dr Neil J. Bristow

Presentation at WSD Steel Success Strategies XXVI New York, 22nd June 2011

H & W Worldwide Consulting

[email protected]+61240286268

0

100

200

300

400

500

600

700

2005 2010

Bill

ion

US$

Market Cap of top 3 producers

AutomotiveSteelIron Ore

Source: Renault, MB Iron Ore presentation

The market capitalisation of the top iron ore companies has risen from 40% to ~ 60% as value has moved upstream with corresponding declines in steel and the automotive sectors.

1. Consumption and demand drivers

2. Supply response

3. Some impacts of future supply

Strong Chinese steel production

Delays in Supply

Rapid Supply Response

The interplay of the different forces will determine the duration and extent of industry profitability

H & W Worldwide Consulting

Source: BHPBilliton presentation

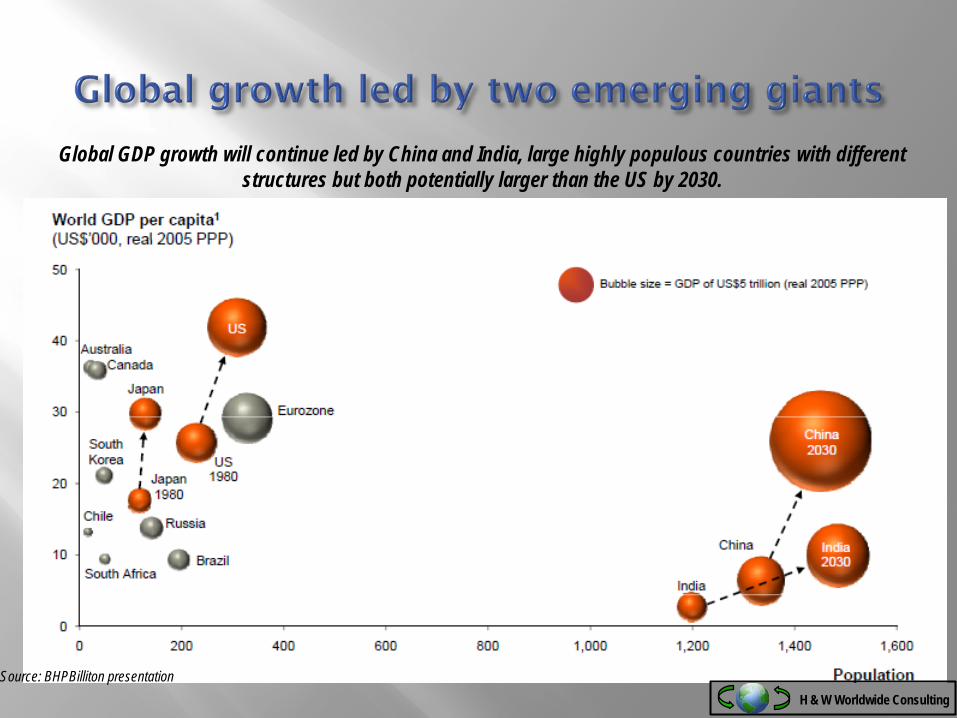

Global GDP growth will continue led by China and India, large highly populous countries with different structures but both potentially larger than the US by 2030.

H & W Worldwide Consulting

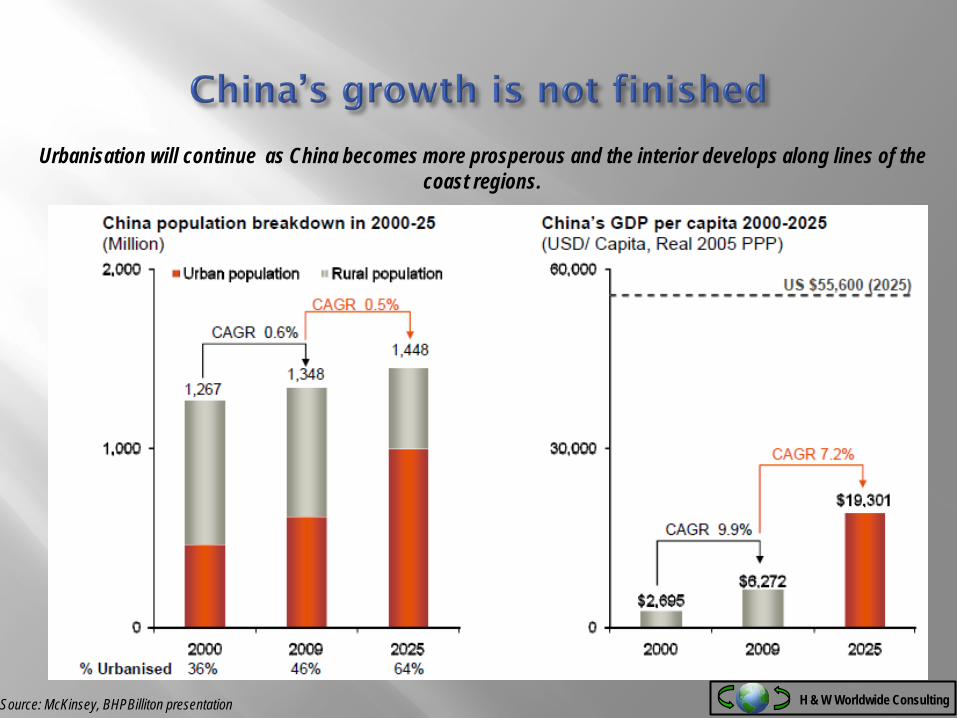

Urbanisation will continue as China becomes more prosperous and the interior develops along lines of the coast regions.

Source: McKinsey, BHPBilliton presentation H & W Worldwide Consulting

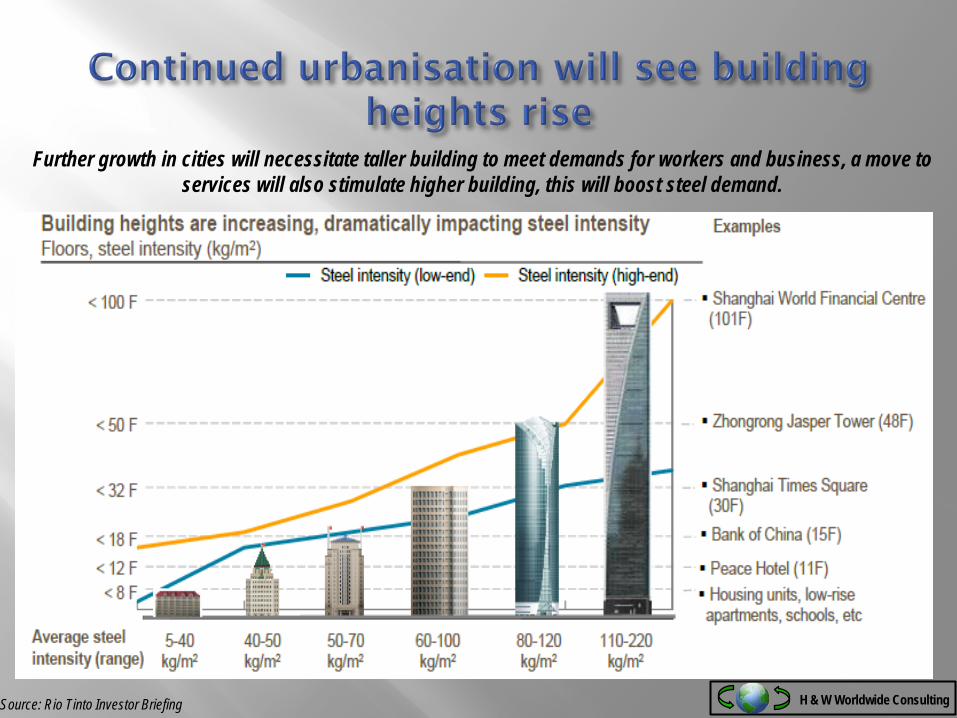

Further growth in cities will necessitate taller building to meet demands for workers and business, a move to services will also stimulate higher building, this will boost steel demand.

Source: Rio Tinto Investor Briefing H & W Worldwide Consulting

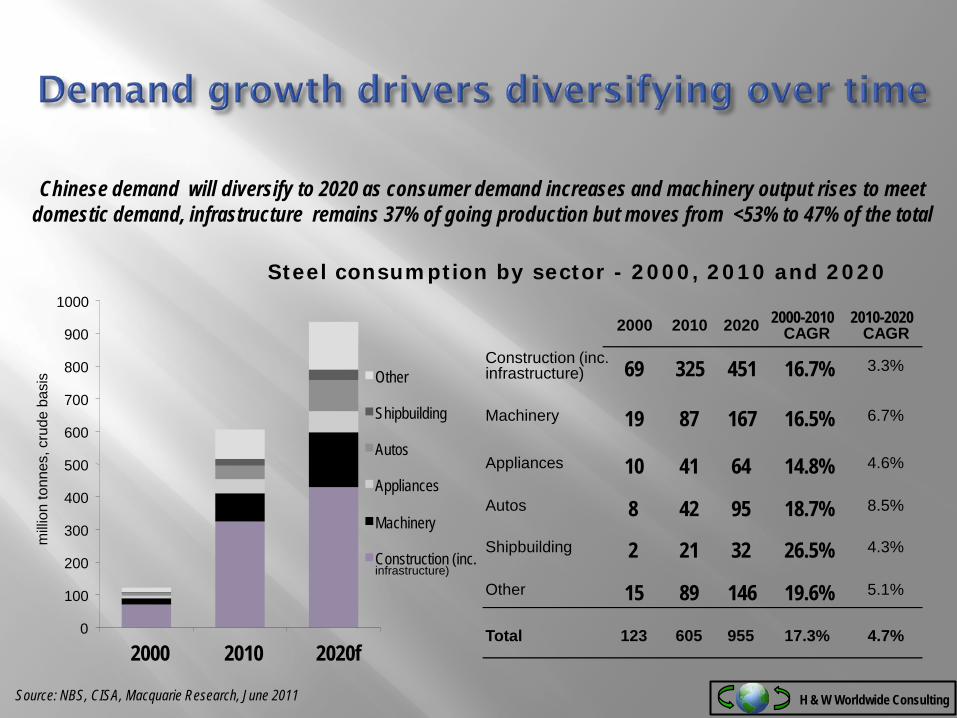

Steel consumption by sector - 2000, 2010 and 2020

Source: NBS, CISA, Macquarie Research, June 2011

2000 2010 2020 2000-2010 CAGR

2010-2020 CAGR

Construction (inc. infrastructure) 69 325 451 16.7% 3.3%

Machinery 19 87 167 16.5% 6.7%

Appliances 10 41 64 14.8% 4.6%

Autos 8 42 95 18.7% 8.5%

Shipbuilding 2 21 32 26.5% 4.3%

Other 15 89 146 19.6% 5.1%

Total 123 605 955 17.3% 4.7%0

100

200

300

400

500

600

700

800

900

1000

2000 2010 2020f

milli

on to

nnes

, cru

de b

asis Other

Shipbuilding

Autos

Appliances

Machinery

Construction (inc.infrastructure)

Chinese demand will diversify to 2020 as consumer demand increases and machinery output rises to meet domestic demand, infrastructure remains 37% of going production but moves from <53% to 47% of the total

H & W Worldwide Consulting

Source: worldsteel, Macquarie Research, June 2011

18.2%

6.5%6.0%

4.5% 4.5% 4.4% 4.0%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

2010 2011e 2012f 2013f 2014f 2015f 2016f

Annual increase in consumption

20 year CAGR

Steel consumption is forecast to sustain a strong growth rate about the long term growth trends over the next 5 years, with continued growth in China and emerging markets. India is expected to pick up growth later

in the period.

H & W Worldwide Consulting

Source: CISA

CISA 10 day production data

612

594

570 571584 587

600610 616

631

654

619 624

652662

698 692710

702 704695

708 711

500

550

600

650

700

21-3

0 Se

p

1-10

Oct

11-2

0 O

ct

21-3

1 O

ct

1-10

Nov

11-2

0 N

ov

21-3

0 N

ov

1-10

Dec

11-2

0 D

ec

21-3

1 D

ec

1-10

Jan

11-2

0 Ja

n

21-3

1 Ja

n

1-10

Feb

11-2

0 Fe

b

21-2

8 Fe

b

1-10

Mar

11-2

0 M

ar

20-2

1 M

ar

1-10

Apr

11-2

0 Ap

r

21-3

0 Ap

r

1-10

May

Cru

de s

teel

pro

duct

ion

(Mtp

a)

Chinese steel production has been far stronger than forecast in late 2010, early 2011 and has been running at record rates ....can it sustain these levels???

H & W Worldwide Consulting

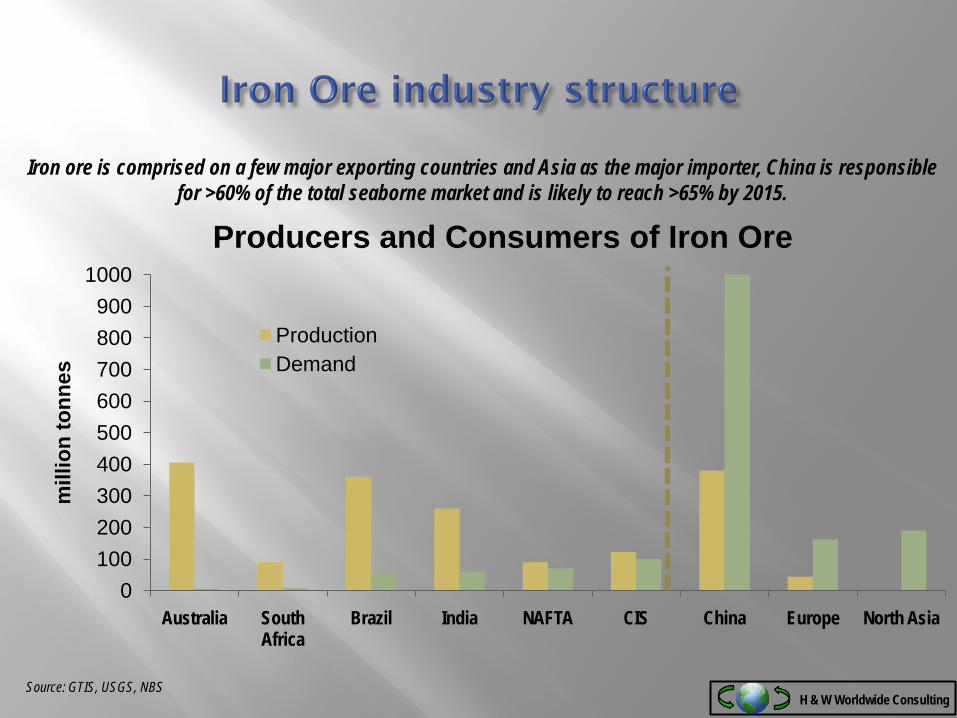

0100200300400500600700800900

1000

Australia South Africa

Brazil India NAFTA CIS China Europe North Asia

mill

ion

tonn

es

Producers and Consumers of Iron Ore

ProductionDemand

Source: GTIS, USGS, NBS

Iron ore is comprised on a few major exporting countries and Asia as the major importer, China is responsible for >60% of the total seaborne market and is likely to reach >65% by 2015.

H & W Worldwide Consulting

• Demand out look seems positive for next few years

• Hence the supply response will determine when the market comes back into “balance”

• But how quickly can new projects enter the market?

• What will the cost be?

H & W Worldwide Consulting

Major seaborne supply basinMajor prospective supply basinMajor domestic supply basin

Mid WestLack of infrastructure, costs mid/high logistics uncertain

Pilbara Large orebodies, quality declining, no low-hanging fruit, costs rising

Northern AreaCarajas large reserves infrastructure - increasing costs

CanadaHigh project and operating costs, due to arctic conditions, rail, barge and port constraints near term, new areas lack of infrastructure

Southern AreaCarajas large reserves infrastructure - increasing costs

SwedenLarge magnetite reserves, high cost UG mining

RussiaLarge magnetite reserves, mid cost largely domestic

UkraineLarge magnetite reserves, low grade, largely domestic

Chinalow grade, costs mid/high land rising

IndiaLarge reserves inc low grade, costs low poor infrastructure

West AfricaLarge reserves high grade, costs mid?? no infrastructure

South AfricaLarge reserves high grade, high costs long rail haul

USALarge madnetitereserves, low grade,

ChileLarge/medium reserves, mixed grade,

South AustraliaLack of infrastructure, costs mid/high potential reserves

NZ Iron sandslow grade, costs mid/high impurities

Large numbers of potential new reserves with significant expansion potential…..how quickly can they be brought into the market?

H & W Worldwide Consulting

• Logistics constraints

• Resources and Reserve Quality

• Rising Environmental and Political Pressures

• Costs – deepening pockets!!!

H & W Worldwide Consulting

100110120130140150160170180190200

Jan-

10

Feb-

10

Mar

-10

Apr

-10

May

-10

Jun-

10

Jul-1

0

Aug

-10

Sep

-10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Feb-

11

Mar

-11

Apr

-11

May

-11

US

$/t,

62%

Fe

CFR

N.C

hina

por

t

China & RoW both growing steel output rapidly –severe deficit

China property tightening, iron ore destocking

Final stages of price ramp-up to bring back Chinese domestic production

Chinese steel production undershoots real demand – scramble for supply

Chinese power-related cutbacks

Cost support floor tested

Strong Chinese restock/ steel production ramp up

Concerns over China tightening - destock

Scramble to replenish inventory

Source: TSI, Macquarie Research, June 2011

Market

loose

tight

The spot price has been a good guide to market conditions, suggesting currently market tight and supply constrained.

H & W Worldwide Consulting

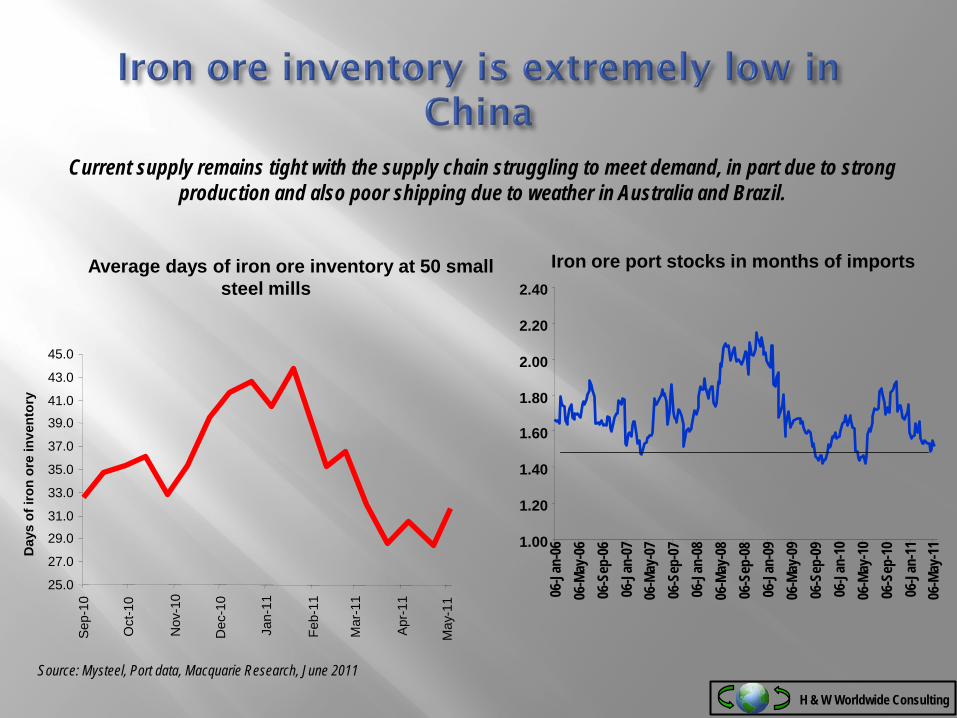

Source: Mysteel, Port data, Macquarie Research, June 2011

Iron ore port stocks in months of imports

1.00

1.20

1.40

1.60

1.80

2.00

2.20

2.40

06-J

an-0

606

-May

-06

06-S

ep-0

606

-Jan

-07

06-M

ay-0

706

-Sep

-07

06-J

an-0

806

-May

-08

06-S

ep-0

806

-Jan

-09

06-M

ay-0

906

-Sep

-09

06-J

an-1

006

-May

-10

06-S

ep-1

006

-Jan

-11

06-M

ay-1

1

Average days of iron ore inventory at 50 small steel mills

25.0

27.0

29.0

31.0

33.0

35.0

37.0

39.0

41.0

43.0

45.0

Sep-

10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Feb-

11

Mar

-11

Apr-

11

May

-11

Day

s of

iron

ore

inve

ntor

y

Current supply remains tight with the supply chain struggling to meet demand, in part due to strong production and also poor shipping due to weather in Australia and Brazil.

H & W Worldwide Consulting

Source: Shipping data, Macquarie Research, June 2011

Cumulative change in export volumes

-15

-10

-5

-

5

10

Jan-

10

Feb-

10

Mar

-10

Apr

-10

May

-10

Jun-

10

Jul-1

0

Aug

-10

Sep

-10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Feb-

11

Mar

-11

Apr

-11

milli

on to

nnes

YoY growth in Indian export volumes

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

140%

Jan-

08

Apr

-08

Jul-0

8

Oct

-08

Jan-

09

Apr

-09

Jul-0

9

Oct

-09

Jan-

10

Apr

-10

Jul-1

0

Oct

-10

Jan-

11

Apr

-11

Bans on Indian exports has see Indian exports sharply down in late 2010 and 2011 compounding the problems with supply from the main exporters.

H & W Worldwide Consulting

0

50

100

150

200

250

2009 2010 2011

mill

ion

tonn

es

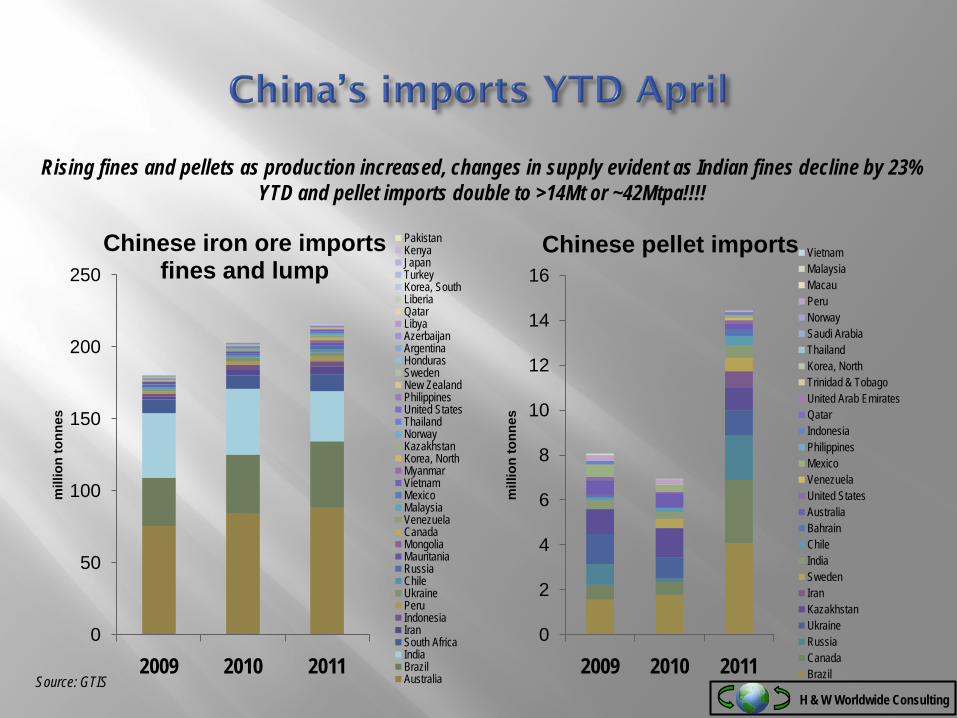

Chinese iron ore imports fines and lump

PakistanKenyaJapanTurkeyKorea, SouthLiberiaQatarLibyaAzerbaijanArgentinaHondurasSwedenNew ZealandPhilippinesUnited StatesThailandNorwayKazakhstanKorea, NorthMyanmarVietnamMexicoMalaysiaVenezuelaCanadaMongoliaMauritaniaRussiaChileUkrainePeruIndonesiaIranSouth AfricaIndiaBrazilAustralia

0

2

4

6

8

10

12

14

16

2009 2010 2011

mill

ion

tonn

es

Chinese pellet imports VietnamMalaysiaMacauPeruNorwaySaudi ArabiaThailandKorea, NorthTrinidad & TobagoUnited Arab EmiratesQatarIndonesiaPhilippinesMexicoVenezuelaUnited StatesAustraliaBahrainChileIndiaSwedenIranKazakhstanUkraineRussiaCanadaBrazilSource: GTIS

Rising fines and pellets as production increased, changes in supply evident as Indian fines decline by 23% YTD and pellet imports double to >14Mt or ~42Mtpa!!!!

H & W Worldwide Consulting

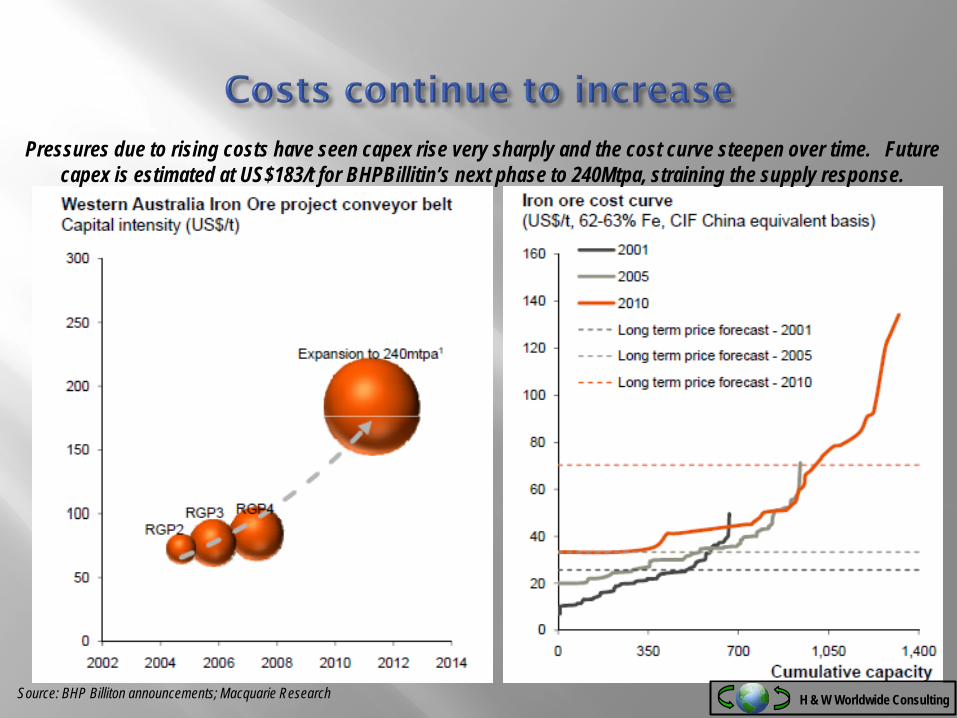

Pressures due to rising costs have seen capex rise very sharply and the cost curve steepen over time. Future capex is estimated at US$183/t for BHPBillitin’s next phase to 240Mtpa, straining the supply response.

Source: BHP Billiton announcements; Macquarie Research H & W Worldwide Consulting

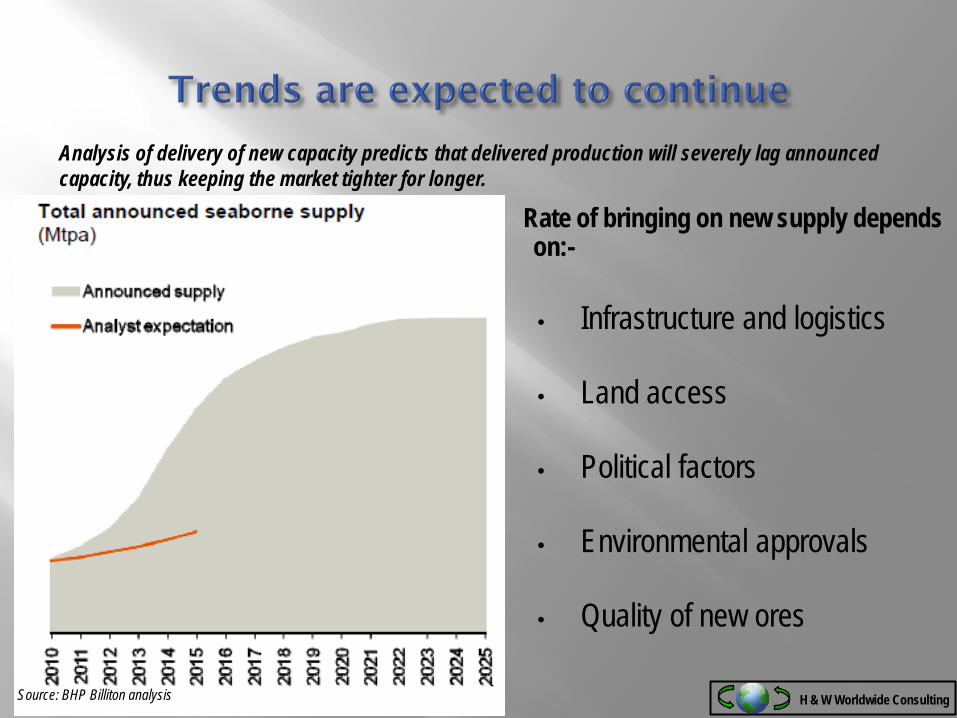

Analysis of delivery of new capacity has shown that ~55% of new capacity announced in 2008 did not materialize., other analysis has supported this view.

Source: BHP Billiton analysisH & W Worldwide Consulting

Source: BHP Billiton analysis

Analysis of delivery of new capacity predicts that delivered production will severely lag announced capacity, thus keeping the market tighter for longer.

Rate of bringing on new supply depends on:-

• Infrastructure and logistics

• Land access

• Political factors

• Environmental approvals

• Quality of new ores

H & W Worldwide Consulting

Assumptions• Driven off seaborne pig iron with adjustments for

domestic production

• 2010 surpasses 1bt seaborne trade

• Overall growth led by China , >65% of seaborne demands

• Indian exports decline as domestic demand rises and political pressures increase – more tariffs

• Chinese domestic production rises then peaks as grade declines and costs rise to 2013 and beyond

• Low cost regions Australia and Brazil grow shareImplications• Market remains undersupplied in near/medium term

• Likely strong prices 2011 to 2014-5

• Market supports new entrants

• Potential for insufficient raw materials for forecast production in 2011 wildcard???

• Space for Australian magnetite?Source: World Steel Association, UNCTAD, Macquarie Research, H&W Worldwide

H & W Worldwide Consulting

Iron Ore Demand 2009 2010 2011e 2012f 2013f 2015fEurope 106 145 155 164 167 173Asia 791 824 917 991 1062 1158

China 622 610 690 755 820 910Japan 109 134 137 140 140 140Korea 43 56 64 68 72 75

Taiwan 13 19 20 21 22 23Other Asia 4 5 6 7 8 10

Other 36 40 46 50 54 60Total 933 1009 1118 1205 1283 1391

Iron Ore Supply 2009 2010 2011e 2012f 2013f 2015f

Australia 378 402 455 525 580 630

Brazil 280 311 350 375 400 450

India 110 105 100 90 80 65

South Africa 35 38 44 46 46 50

Sweden 16 21 23 23 24 27

Canada 26 28 28 30 33 38

Other 80 85 90 95 100 115

Total 921 990 1090 1184 1263 1375

Net balance -12 -19 -28 -21 -20 -16

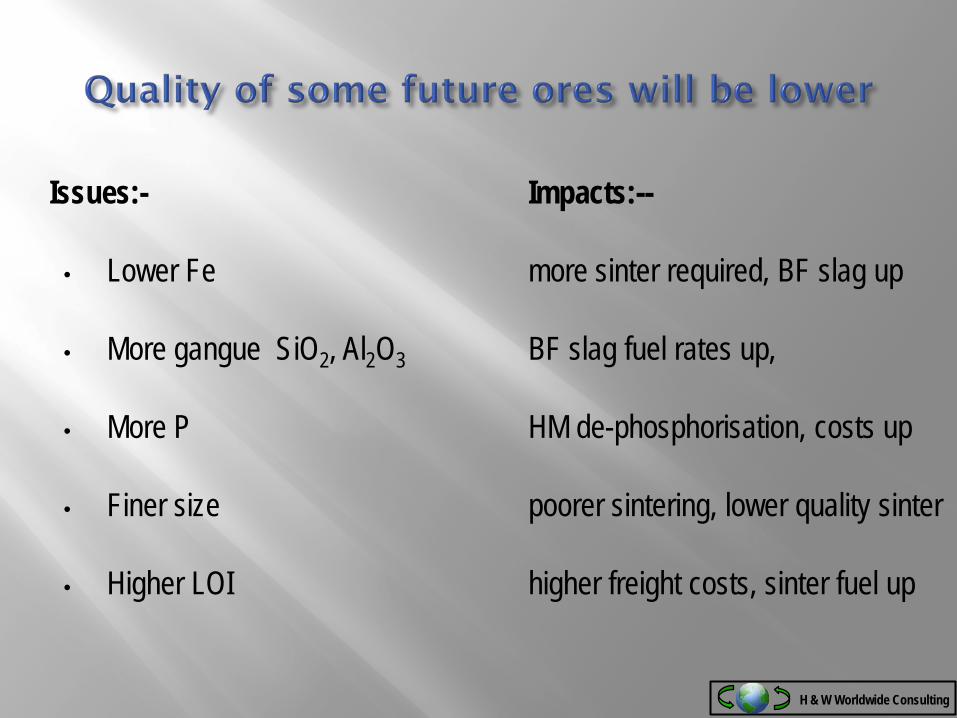

Issues:- Impacts:--

• Lower Fe more sinter required, BF slag up

• More gangue SiO2, Al2O3 BF slag fuel rates up,

• More P HM de-phosphorisation, costs up

• Finer size poorer sintering, lower quality sinter

• Higher LOI higher freight costs, sinter fuel up

H & W Worldwide Consulting

Source: Rio Tinto, Vale June 2011

Divergence of views of pricing between the three majors. Vale seeking quarterly pricing and some VIU adjustments; Rio Tinto looking at range of flexible mechanisms of variable contract length with possible development of lump and pellet indices, BHPBilliton seeking shorter term pricing and increased use of indices –more uncertainty ahead with more opacity??

H & W Worldwide Consulting

0

1000

2000

3000

4000

5000

6000

7000

01/05/09 01/08/09 01/11/09 01/02/10 01/05/10 01/08/10 01/11/10 01/02/11 01/05/11

ICEXNOS ClearingCME GroupLCH.ClearnetSGX

US$ (m)

Iron Ore Financial Contracts – Cumulative Value Cleared

US$6 billion (over 40 million tonnes) of iron ore swaps and options have been cleared since launch (basis TSI)

Source: The Steel IndexH & W Worldwide Consulting

• Overall demand and supply suggests iron ore should remain a “star” for a further 3-4 years

• Although significant new capacity is planned delays are highly likely keeping the market tight

• Declining future quality in grade and size will present challenges to steelmakers in sinter, BF & BOF

• Rising uncertainty in pricing mechanism will continue as the market settles on new processes